Attached files

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended September 30, 2016

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-33977

VISA INC.

(Exact name of Registrant as specified in its charter)

Delaware | 26-0267673 | |

(State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | |

P.O. Box 8999 San Francisco, California | 94128-8999 | |

(Address of principal executive offices) | (Zip Code) | |

(650) 432-3200

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Class A common stock, par value $0.0001 per share | New York Stock Exchange | |

(Title of each Class) | (Name of each exchange on which registered) | |

Securities registered pursuant to Section 12(g) of the Act:

Class B common stock, par value $0.0001 per share

Class C common stock, par value $0.0001 per share

(Title of each Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See the definitions of “large accelerated filer” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer þ | Accelerated filer o | |

Non-accelerated filer o | Smaller reporting company o | |

(Do not check if a smaller reporting company) | ||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of the registrant’s class A common stock, par value $0.0001 per share, held by non-affiliates (using the New York Stock Exchange closing price as of March 31, 2016, the last business day of the registrant’s most recently completed second fiscal quarter) was approximately $145.5 billion. There is currently no established public trading market for the registrant’s class B common stock, par value $0.0001 per share, or the registrant’s class C common stock, par value $0.0001 per share.

As of November 9, 2016, there were 1,867,580,597 shares outstanding of the registrant’s class A common stock, par value $0.0001 per share, 245,513,385 shares outstanding of the registrant’s class B common stock, par value $0.0001 per share, and 16,814,896 shares outstanding of the registrant’s class C common stock, par value $0.0001 per share.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Proxy Statement for the 2016 Annual Meeting of Stockholders are incorporated herein by reference in Part III of this Annual Report on Form 10-K to the extent stated herein. Such Proxy Statement will be filed with the Securities and Exchange Commission within 120 days of the Registrant’s fiscal year ended September 30, 2016.

TABLE OF CONTENTS

Page | ||

Item 1 | ||

Item 1A | ||

Item 1B | ||

Item 2 | ||

Item 3 | ||

Item 4 | ||

Item 5 | ||

Item 6 | ||

Item 7 | ||

Item 7A | ||

Item 8 | ||

Item 9 | ||

Item 9A | ||

Item 9B | ||

Item 10 | ||

Item 11 | ||

Item 12 | ||

Item 13 | ||

Item 14 | ||

Item 15 | ||

Unless the context indicates otherwise, reference to "Visa," "Company," "we," "us" or "our" refers to Visa Inc. and its subsidiaries.

"Visa" and our other trademarks referenced in this report are Visa's property. This report may contain additional trade names and trademarks of other companies. The use or display of other companies' trade names or trademarks does not imply our endorsement or sponsorship of, or a relationship with these companies.

2

Forward-Looking Statements:

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 that relate to, among other things, our future operations, prospects, developments, strategies, growth of our business, integration of Visa Europe, anticipated expansion of our products in certain countries, plans to issue additional debt, industry developments, expectations regarding litigation, timing and amount of stock repurchases, sufficiency of sources of liquidity and funding, effectiveness of our risk management programs and expectations regarding the impact of recent accounting pronouncements on our consolidated financial statements. Forward-looking statements generally are identified by words such as "believes," "estimates," "expects," "intends," "may," "projects," “could," "should," "will," "continue" and other similar expressions. All statements other than statements of historical fact could be forward-looking statements, which speak only as of the date they are made, are not guarantees of future performance and are subject to certain risks, uncertainties and other factors, many of which are beyond our control and are difficult to predict. We describe risks and uncertainties that could cause actual results to differ materially from those expressed in, or implied by, any of these forward-looking statements in Item 1—Business, Item 1A—Risk Factors, Item 7—Management's Discussion and Analysis of Financial Condition and Results of Operations and elsewhere in this report. Except as required by law, we do not intend to update or revise any forward-looking statements as a result of new information, future events or otherwise.

3

PART I

ITEM 1. Business

OVERVIEW

Visa is a global payments technology company that connects consumers, merchants, financial institutions, businesses, strategic partners and government entities in more than 200 countries and territories to fast, secure and reliable electronic payments. We enable global commerce through the transfer of value and information among these participants. Our advanced transaction processing network facilitates authorization, clearing and settlement of payment transactions and enables us to provide our financial institution and merchant clients a wide range of products, platforms and value-added services.

Our vision is to be the best way to pay and be paid for everyone, everywhere. To deliver on this vision, we focus on six strategic goals:

• | Evolve our client interactions to build deeper partnerships with financial institutions, merchants and new industry partners; |

• | Transform Visa’s technology assets to drive efficiency and enable innovation; |

• | Achieve success as a leading partner for digital payments comparable to what we have achieved in the physical world; |

• | Expand access to Visa products and services globally; |

• | Champion payment system security for the industry; and |

• | Be the employer of choice for top talent. |

Visa is one of the world’s largest retail electronic payments network based on payments volume, number of transactions and number of cards in circulation.

Visa Network

* Total volume includes Europe for the fourth quarter.

Visa operates in a four party model, which includes card issuing financial institutions, acquirers and merchants. We are not a bank and do not issue cards, extend credit or set rates and fees for account holders on Visa products. In most cases, our financial institution clients are responsible for and manage account holder and merchant relationships.

We do not earn revenues from, or bear credit risk with respect to, interest or fees paid by account holders on Visa products. Interchange reimbursement fees represent a transfer of value between the financial institutions participating in our open-loop payments network. We administer the collection and remittance of interchange reimbursement fees through the settlement process, but we generally do not receive any revenue related to interchange reimbursement fees. In addition, we do not receive as revenue any of the fees that merchants are charged directly for acceptance by the acquirers.

4

Visa Brand

The Visa brand is one of the most well-known and valuable brands in the world. Anchored on the notion that Visa is 'everywhere you want to be,' the brand stands for acceptance, security, convenience and universality. In recognition of its strength among clients and consumers, the Visa brand is ranked highly in a number of widely recognized brand studies, including the 2016 BrandZ Top 100 Most Valuable Global Brands Study (#6), Interbrand’s 2016 Best Global Brands (#61) and Forbes 2016 World’s Most Valuable Brands (#30). We leverage our brand strength to deliver added value to financial institutions, merchants and other clients through compelling brand expressions, expanded products and services, and innovative marketing efforts.

Payment Security

Security is critical to maintaining trust and confidence in electronic payments. To ensure that Visa remains one of the safest ways to pay and be paid, we deploy a multi-layered security approach focused on eliminating vulnerable data from the payments environment, securing the data that remains, preventing fraud and empowering system participants to protect themselves. This approach has historically kept fraud rates low as payment volumes have grown. With commerce moving to digital channels, we are investing in new technologies and solutions in order to maintain the trust that consumers, clients and merchants place in Visa. This requires innovation, leadership and cross-industry collaboration.

5

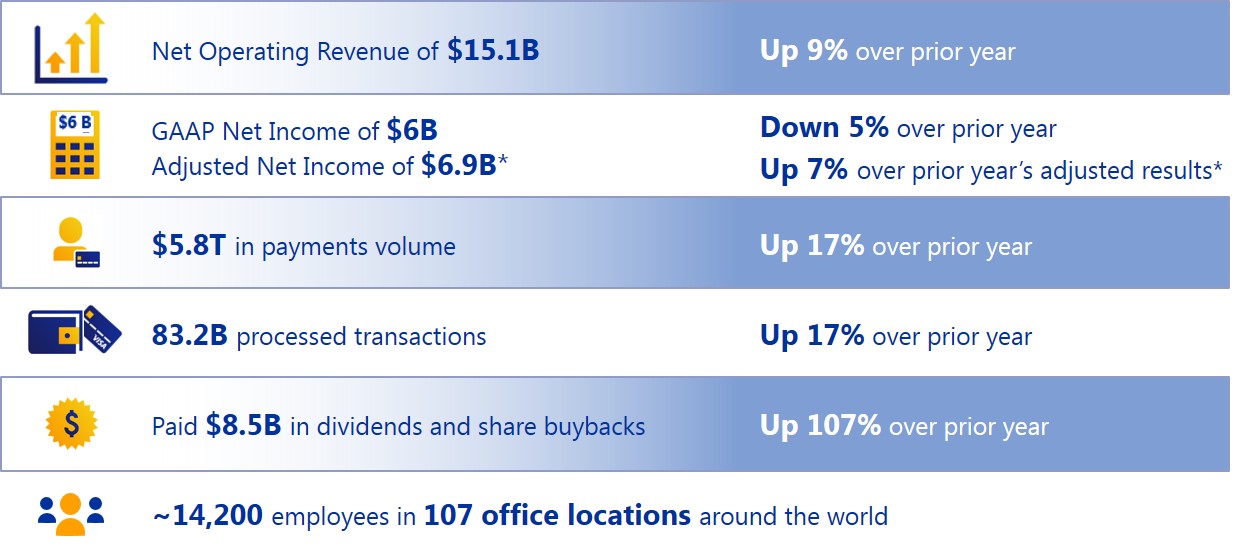

Fiscal 2016 Key Statistics

*Please see Item 7—Management's Discussion and Analysis of Financial Condition and Results of Operations for a reconciliation of our adjusted financial results.

KEY INITIATIVES

Visa Europe Acquisition. Prior to our 2007 reorganization, Visa operated as a collection of member-owned associations, with each region serving its member financial institutions and administering Visa programs within a global framework. In 2007, Visa reorganized, with all of the regions except Visa Europe coming together to form Visa Inc., a Delaware corporation. Visa Europe remained owned by its European member financial institutions.

On June 21, 2016, we acquired Visa Europe. We believe the acquisition positions our Company to create additional value through increased scale, efficiencies realized by integration of the businesses, and benefits related to Visa Europe's transition from a member-owned association to a for-profit enterprise. We plan to bring Visa's global capabilities to our European clients, deliver a more seamless experience operating as one single global company and grow our business in that region. As part of the acquisition, we acquired 100% of the share capital of Visa Europe for €12.2 billion ($13.9 billion) and €5.3 billion ($6.1 billion) in preferred stock, with an additional €1.0 billion, plus 4% compound annual interest, to be paid on June 21, 2019.

Capital Structure. In December 2015, we issued $16 billion of senior notes with maturities ranging between two and 30 years, and in June 2016, we issued two new series of preferred stock to Visa Europe's member financial institutions that are convertible into approximately 79 million shares of class A common stock as part of the Visa Europe transaction. We also have plans to raise an additional $2 billion in debt by the end of calendar year 2016, subject to market conditions.

Technology Transformation. At its heart, Visa is a technology company. With the intensifying digital economy and the ubiquity of mobile technology, data and enhanced security driving the future of payments, we embarked on a multi-year journey in 2015 to transform technology at Visa with the main areas of focus on opening our network and creating a digital platform for innovation while at the same time adding layers of security and operational resilience. We have executed on our workforce plan by hiring a total of 1,700 technology employees globally over the past two years, including nearly 750 new college graduates, replacing a significant percentage of our contractor and vendor spend. We are making steady progress on our technology strategic roadmap, resulting in enhanced services for our ecosystem stakeholders and positive impacts to our infrastructure. Since the launch of Visa’s Developer Platform (VDP) in 2015, more than 180 of Visa’s product or service functions are available in API or application program interface format to our clients and partners. We added new services to enable clients to develop support for tokenized transactions and create new and innovative solutions in mobile, ecommerce and digital face-to-face transactions. Cybersecurity remains a top focus and in fiscal 2016 we launched our new Threat Intelligence Fusion Platform, a cyber command and control center that provides integrated cybersecurity operations to further help protect our data and assets. At the same time, new open technologies have been added

6

systematically to our infrastructure and platform components and we continue to bolster the resiliency of our infrastructure and application services to provide high availability of our services for our clients.

How We Work with Partners - Innovation Centers, VDP & API Suite. To drive new technologies in the payments space and accelerate the proliferation of safe and fast digital payments, we opened new innovation centers in Dubai, Miami and Singapore in fiscal 2016. Along with the San Francisco innovation center and European innovation hubs in London, Tel Aviv and Berlin, these centers foster collaboration with our financial institution clients, partners and developers across the regions to spur creation of the next generation of payments and commerce applications and solutions. In 2016, VDP became generally available, offered application developers around the globe access to Visa technology, services and tools, and provided safe testing environments for the development of new digital payments and commerce solutions. By exposing new and modified APIs through a variety of channels, Visa has made digital payment solutions available to support hundreds of financial institutions and technology partners such as Google, Microsoft and Samsung.

PRODUCTS & SERVICES

Core Products

Debit: Debit cards are issued by banks to allow consumers to access funds held in their demand deposit accounts (DDAs). Debit cards allow consumers to transact without needing cash or checks and without accessing a line of credit. Visa provides the network infrastructure, product support and industry knowledge to help issuers optimize their debit offerings and help consumers and merchants efficiently transact for the purchase of goods and services, whether in person or through online or mobile channels. Across all Visa’s core products, Visa offers security protections that help prevent, detect and resolve fraud. Where applicable, Visa's zero-liability policy protects consumer cardholders from any unauthorized charges.

Credit: Credit cards are issued by banks to allow consumers to access credit to pay for goods and services. Visa does not extend credit; however, we provide combinations of card benefits and brand support, that financial institutions use to support and enable their credit products. We also partner with our clients on product design, customer segmentation and customer experience design to help financial institutions better deliver products and services that match their consumers’ needs. In fiscal 2016, we saw significant volume growth from the conversion of the USAA portfolio to Visa and opening of credit acceptance at Costco membership warehouses in the U.S.

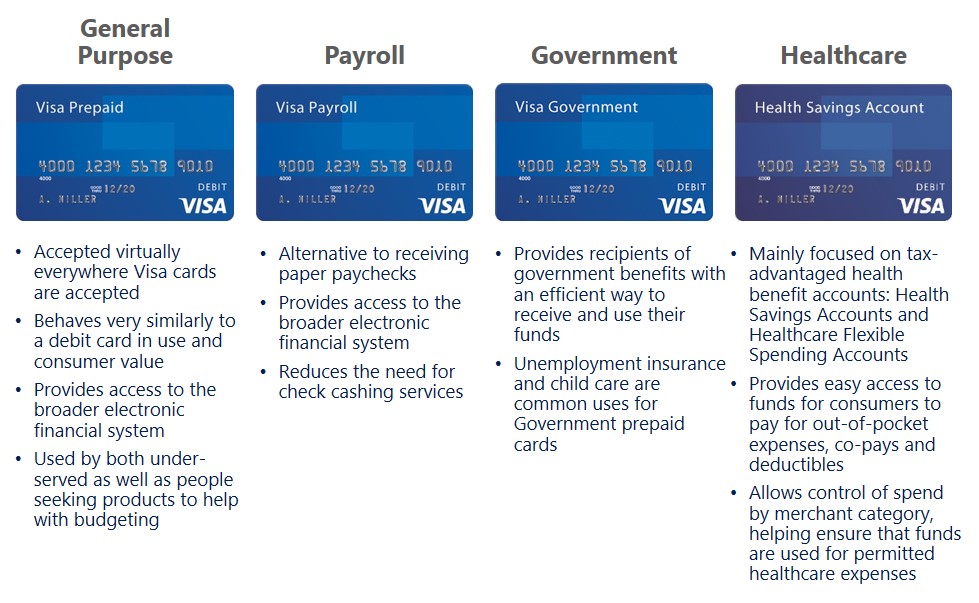

Prepaid: Prepaid products draw funds from a designated pool of funds. Prepaid cards can be funded by individuals, corporations or governments. Prepaid cards address many consumer use cases and needs:

7

Commercial: We offer a portfolio of corporate (travel) cards and purchasing card (P-card) products covering all major segments. The Commercial category is not one single product but a portfolio of products designed to bring efficiency, controls and automation to corporate and government travel and procurement processes ranging from employee travel to fully integrated, invoice-based payables. We support financial institutions, accounts payable platforms, like Bottomline and MineralTree, and technology companies as they build and expand their business-to-business platforms.

Processing Infrastructure

VisaNet authorizes, clears and settles transactions processed by Visa, excluding European domestic transactions, which are routed through the European processing platform. VisaNet consists of multiple synchronized processing centers that are linked by a global telecommunications network and engineered for minimal downtime and uninterrupted connectivity. While Visa Europe's systems are being integrated with our systems, we will continue to maintain mostly separate authorization, clearing and settlement systems from Visa Europe while ensuring interoperability with their processing centers in the United Kingdom (U.K.).

VisaNet is capable of handling more than 65,000 transactions per second reliably, conveniently and securely. In fiscal 2016, Visa processed over 83 billion payment and cash disbursement authorization transactions, which included Europe during the fourth quarter. VisaNet is built on a centralized architecture, enabling us to analyze each authorization we process in real time and provide value-added processing services, such as risk scoring and tokenization. It provides the infrastructure for delivering innovation and other payment system enhancements for domestic payment systems and cross border international transactions globally.

A typical Visa transaction begins when the account holder presents his or her Visa product to a merchant as payment for goods or services. The transaction is then sent to the acquirer and routed over VisaNet or Visa Europe's processing platform to an issuer for an authorization decision. The transaction is either approved or declined and routed back to the acquirer and merchant usually in a matter of seconds.

Transaction Processing Services

Our core transaction processing services involve the routing of payment information and related data to facilitate the authorization, clearing and settlement of transactions between our issuers and acquirers. Our processing services also address the varied needs of other participants in the evolving payments ecosystem, through such offerings as our merchant gateway and Visa DPS issuer processing. Merchant gateway services, provided through CyberSource, enable merchants to accept, process and reconcile payments, manage fraud and safeguard payment security online and in-store. CyberSource additionally enables acquirers and other partners to offer these services to their merchants. DPS provides comprehensive issuer processing services for participating issuers of Visa debit, prepaid and ATM products. Value-added offerings by DPS to issuer clients include: fraud and risk services, data analytics, marketing campaign management, mobile and digital solutions, back office tools and services, card fulfillment and management, network gateway services, call centers and web hosting solutions. These and other services support our issuers and acquirers and their use of our products, and promote the growth and security of our payments network by expanding the payment value chain and increasing network utilization.

Digital Products

Visa Checkout: Visa Checkout offers consumers an expedited and secure payment experience for online transactions wherever Visa Checkout is enabled. Visa Checkout helps merchants convert higher numbers of consumers to sale, a particularly important issue as digital commerce shifts from desktop devices to mobile devices which have lower conversion rates. At the end of fiscal 2016, Visa Checkout had over 15 million consumer accounts in 21 countries, seven languages and over 1,400 financial institution partners across the globe participating. More than 300,000 merchants, including some of the largest global retailers accept Visa Checkout. In October 2016, we rolled out a redesigned Visa Checkout experience, making it easier for consumers to enroll and complete purchases on mobile devices. We recently announced that we are opening the Visa Checkout platform to clients and partners, allowing them to integrate their digital wallets into Visa Checkout for streamlined authentication and checkout.

Visa Direct: Visa Direct is a push payment product platform that facilitates payer-initiated transactions that are sent directly to the Visa account of the recipient. It supports faster payments use cases like person-to-person (P2P) payments, and disbursements. We are working with key partners, including processors like Fiserv, FIS and Jack Henry & Associates, and originators like Early Warning (EWS), Ingo Money, Hyperwallet, Wells Fargo and QIWI, along with merchants to expand the distribution and usage of push payments.

8

We are also enabling push payments in developing economies to electronify payments. We recently launched a new service called mVisa in Kenya. First launched in Rwanda in 2014 and India in 2015, mVisa allows consumers to transfer money to merchants in real time using their mobile phones and merchants are able to accept Visa transactions without the need to install card acceptance hardware.

Visa Token Service: The Visa Token Service replaces the card account numbers from the transaction with a token. Tokenization helps to protect consumer financial information and lessen the risk of stolen card credentials. In fiscal 2017, we announced new specifications that allow certified third party service providers such as Gemalto, Giesecke & Devrient and Inside Secure to connect directly to our Token Service and become Token Service Providers (TSP). These TSPs will be able to provide a range of services to support Visa tokens for issuers and token requestors participating in the Visa Token Service, including new account provisioning and life cycle management. By expanding access to the Visa Token Service to new partners, we expect Visa issuers will be able to more quickly and easily offer secure digital payment services across a wide range of solutions.

Merchant Products

Visa has a suite of products and services to help merchants reduce their payment fraud and improve their customer engagement. Visa Advertising Solutions, Visa Commerce Network and CyberSource’s product offerings are examples of Visa’s continued investment to deliver industry-leading products and capabilities to our merchant partners.

Visa launched Visa Advertising Solutions, a service that allows merchants to better target and track the efficacy of their digital campaigns. Visa has partnered with strategic advertising technology leaders to help deliver targeting and measurement capabilities using aggregated and anonymous spend insights. The Visa Commerce Network (VCN) uses Visa’s global payment network to enable merchants to promote relevant offers to acquire new customers, drive loyalty and increase sales. For example, Uber uses the platform to provide its customers with card-linked offers from local restaurants and retailers. Qualifying purchases are recognized at the point of sale and rewards are applied to the riders' Uber accounts - eliminating the need for coupons.

CyberSource offers a suite of products and services for merchants to manage online, mobile and in-store payments. CyberSource gateway services enable global payment acceptance of cards and other digital payment types. CyberSource Decision Manager is a comprehensive solution for fraud management including a merchant risk model, rules engine, managed services and solutions for specific categories such as airline fraud. Decision Manager Replay is an analytical tool that allows merchants to compare fraud strategies in real-time using their historical data to test and quantify the expected impact of various risk management strategies. CyberSource additionally offers payment security services including tokenization and payer authentication, commerce services such as tax calculation and recurring billing, and merchant reporting and analytics. CyberSource also offers products and services tailored to the needs of small and mid-sized merchants under the Authorize.Net brand. CyberSource and Authorize.Net capabilities are offered through Visa and our partners.

Risk Products & Payment Security Initiatives

Visa continues to develop our suite of risk products and services to help clients minimize risk and enable secure commerce. Visa Risk Manager is a decision making solution that helps issuers improve loss prevention and profitability through effective, enhanced risk evaluation capabilities. Products like Visa Advanced Authorization evaluate the risk associated with every participating VisaNet transaction. Our case studies have shown that an issuer employing Visa Advanced Authorization can significantly improve fraud detection. In addition to reducing fraud, approval rates can be increased by accepting transactions that were once deemed too risky. For example, in fiscal 2016 we introduced Mobile Location Confirmation, a service that enhances Visa Advanced Authorization by adding geolocation intelligence in real time. Mobile Location Confirmation informs issuers if their participating account holder’s mobile phone is near a purchase location. This new data improves the issuer’s ability to make more informed approve or decline decisions.

We have also extended our fraud prediction capabilities to merchants via Visa Transaction Advisor. Our first implementation of this product is at fuel pumps, whereby we provide a risk indicator to the merchant for each Visa card transaction so the merchant can decide if they would like to require incremental authentication for risky transactions. Fuel merchants using our Visa Transaction Advisor product have seen a significant decline in counterfeit fraud rates and in lost and stolen fraud chargebacks.

Verified by Visa is a solution designed to make online transactions safer by authenticating an account holder’s identity at the time of purchase. It is designed to improve account holder and merchant confidence in online

9

purchases and to reduce disputes and fraud related to the use of Visa payment products. Visa Consumer Authentication Service is a hosted solution for issuers on Verified by Visa transactions delivering protection against online fraud through risk-based authentication. Issuers have full control of when and how they decide to authenticate based on their transaction risk threshold, existing fraud-detection tools, operational requirements and user demands.

We also launched Visa Consumer Transaction Controls in fiscal 2016, which allow account holders to place restrictions on their enrolled cards that define when, where and how those cards can be used to better manage account spending and security. Issuers can utilize this solution across their entire card portfolio.

EMV Migration in the United States: To enhance payment security and mitigate counterfeit fraud, we have been working with U.S. merchants and financial institutions to encourage the adoption of EMV chip payment technology. EMV, which stands for Europay, MasterCard and Visa, is a global standard for chip cards and chip terminals. Chip technology generates a one-time use code for every transaction that is used to authenticate that the transaction is originating from a valid (i.e., not fraudulent) card. Under policies announced by Visa in 2011, effective October 2015, the party that has not adopted the more secure chip technology is responsible for any resulting counterfeit fraud. Over the last year, there has been steady growth in chip card issuance and in the activation of chip-enabled terminals. As of September 30, 2016, more than 373 million Visa chip cards have been issued, making the United States the largest chip card market in the world. Nearly 1.6 million merchant locations in the United States are now chip-enabled, or roughly 30% of all U.S. merchants that accept Visa cards at the physical point of sale. Over 30% of U.S. in-store payment volume is now being processed as chip transactions. We continue to work to help improve the merchant and account holder experience, with the roll out of Quick Chip, a solution designed to reduce the time it takes to complete a chip transaction. We are also working with merchants and acquirers to simplify the terminal certification process, and have taken steps to limit merchants’ exposure to counterfeit fraud liability for those that have had challenges getting terminals certified and activated.

SIGNIFICANT BUSINESS DEVELOPMENTS

CEO Succession. On October 17, 2016, we announced that Alfred Kelly, Jr. will become CEO, effective December 1, 2016, replacing Charles Scharf. Mr. Scharf will serve as an advisor to Mr. Kelly for a period of several months to assist with the transition.

Interchange Multidistrict Litigation. Visa, MasterCard and various U.S. financial institutions are defendants in class and individual actions challenging, among other things, Visa’s and MasterCard’s purported setting of interchange reimbursement fees and certain network rules. In 2012, Visa, MasterCard, various U.S. financial institution defendants, and class plaintiffs signed a settlement agreement to resolve the class plaintiffs’ claims. On January 14, 2014, the U.S. District Court for the Eastern District of New York entered a final judgment order approving the settlement, from which a number of objectors appealed. On June 30, 2016, the U.S. Court of Appeals for the Second Circuit vacated the lower court's certification of the merchant class and reversed the approval of the settlement. The Second Circuit determined that the class plaintiffs were inadequately represented and remanded the case to the lower court for further proceedings not inconsistent with its decision. Prior to November 23, 2016, class plaintiffs may file a petition for writ of certiorari with the U.S. Supreme Court seeking review of the Second Circuit’s decision. Until the appeals process is complete, it is uncertain whether the Company will be able to resolve the class plaintiffs' claims as contemplated by the settlement agreement. See Item 1A—Risk Factors—We may be adversely affected by the outcome of litigation or investigations, despite certain protections that are in place and Item 8—Financial Statements and Supplementary Data—Note 20—Legal Matters of this report for more information.

INTELLECTUAL PROPERTY

We own and manage the Visa brand, which stands for acceptance, security, convenience and universality. Our portfolio of trademarks, in particular our family of Visa marks, our PLUS mark and our Dove design mark, are important to our business. We give our clients access to these assets through agreements with our issuers and acquirers, which authorize the use of our trademarks in connection with their participation in our payments network. We also own a number of patents, patent applications and other intellectual property relating to payment solutions, transaction processing, security systems and other matters. We rely on a combination of patent, trademark, copyright and trade secret laws in the U.S. and other jurisdictions, as well as confidentiality procedures and contractual provisions, to protect our proprietary technology.

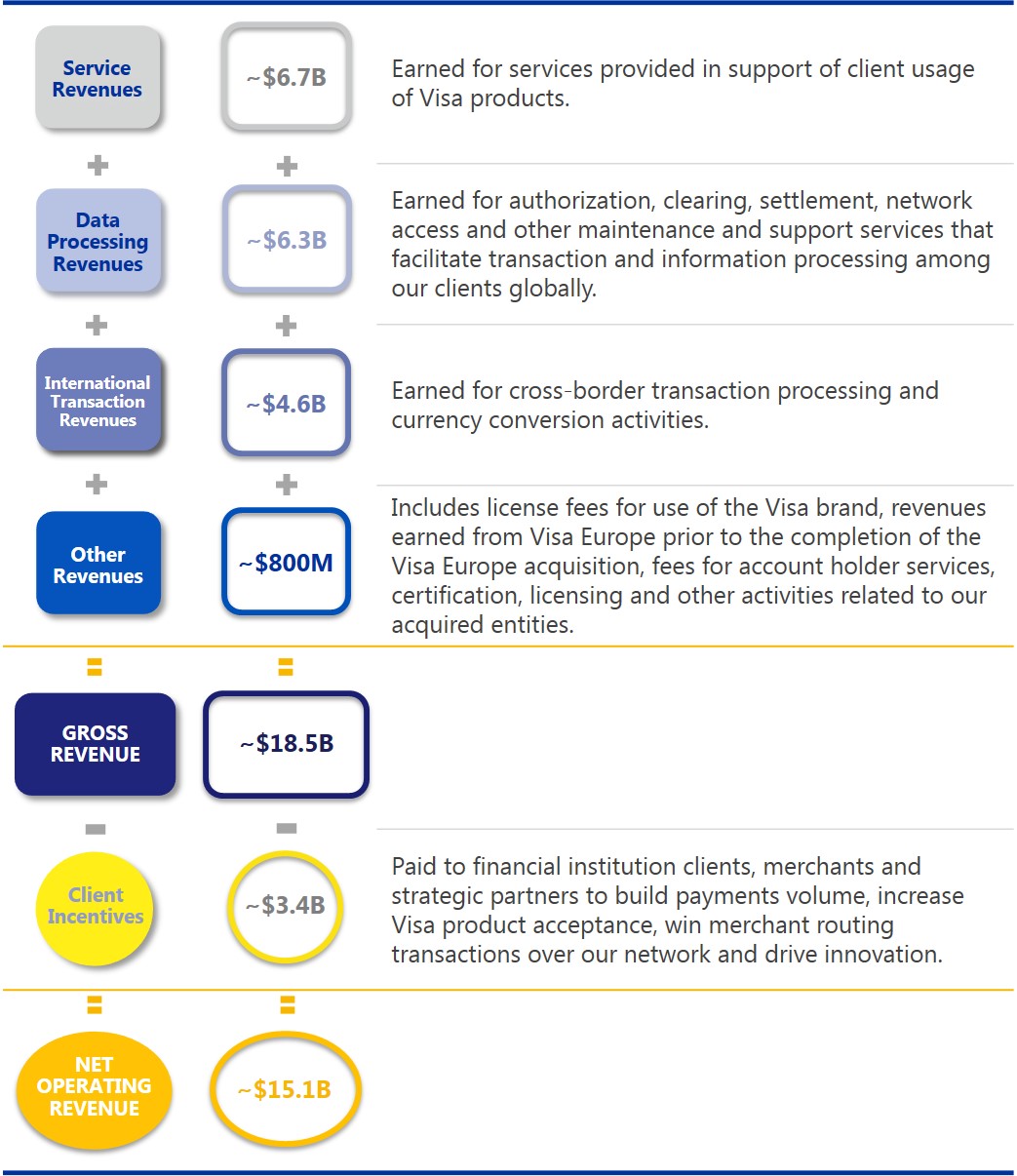

NET OPERATING REVENUES

10

Our gross revenues are principally comprised of service revenues, data processing revenues, international transaction revenues and other revenues. Net operating revenues are gross revenues reduced by costs incurred under client incentive arrangements. We have one reportable segment, Payment Services.

Revenue Details

COMPETITION

The global payments industry continues to undergo dynamic change. Existing and emerging competitors compete with Visa for consumers, financial institution clients and merchant participation in our network and payment solutions. Technology and innovation is shifting consumer habits and driving growth opportunities in ecommerce, mobile payments, block chain technology and digital currencies. These advances are enabling new entrants, many of which depart from traditional network payment models. In certain countries, the evolving regulatory landscape is changing how we compete, creating local networks or enabling processing competition.

We compete against all forms of payment. This includes paper-based payments, primarily cash and checks, and all forms of electronic payments. Our electronic payment competitors principally include:

11

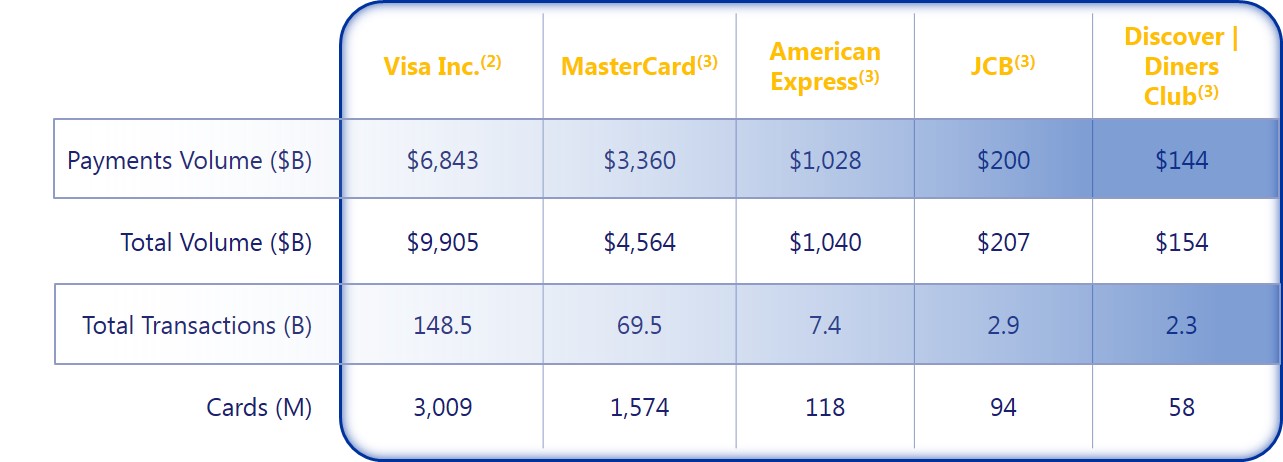

Global or Multi-Regional Networks, which typically offer a range of branded, general purpose card payment products that can be used at millions of merchant locations around the world. Examples include MasterCard, American Express, Discover and JCB. These competitors may be more concentrated in specific geographic regions, such as JCB in Japan and Discover in the U.S., or have a leading position in certain countries. For example, UnionPay operates the sole domestic acceptance mark in China. Based on available data, Visa is one of the largest retail electronic funds transfer networks used throughout the world. The following chart compares our network with these network competitors for calendar year 2015(1):

(1) | UnionPay, which operates primarily within the Chinese domestic market, is not included in this table as Visa currently does not compete in that market under local law. Although we are uncertain how UnionPay reports certain volumes, reportedly its numbers could approach or exceed some of those listed in this chart. |

(2) | The data presented are provided by our financial institution clients. Previously submitted information may be updated and all data are subject to review by Visa. Visa Europe data are included. |

(3) | MasterCard, American Express, JCB and Discover/Diners Club data sourced from The Nilson Report issue 1085 (April 2016). Includes all consumer and commercial credit, debit and prepaid cards. Some figures are estimates and currency figures are in U.S. dollars. MasterCard excludes Maestro and Cirrus figures. American Express includes figures for third-party issuers. Discover figures consist of U.S. data only and include third-party issuers. JCB figures include third-party issuers and other payment-related products. |

Local and regional networks, that operate in many countries, often with the support of government influence or mandate. In some cases, they are owned by financial intuitions. These networks typically focus on debit payment products, have functionality or their brand marks present with the Visa brand on the card or payment device, and may have strong local acceptance and recognizable brands. Examples include STAR, NYCE, and Pulse in the United States, Interac in Canada, and EFTPOS in Australia.

Alternate Payment Providers, which often have a primary focus of enabling payments through ecommerce and mobile channels. These companies may process payments using in-house account transfers between parties, electronic funds transfer networks like the Automated Clearing House (ACH), or global or local networks like Visa. In some cases, these entities are both a partner and a competitor to Visa. Examples include PayPal and Alipay.

Other Electronic Payment Networks like the ACH in the U.S. are often created and governed by local governments. Historically focused on interbank transfers, many are adding capabilities that may make them more competitive for retail payments. We also compete with closed-loop payment systems, wire transfers and electronic benefit transfers.

Payment Processors, where we face competition for the processing of Visa transactions or are not permitted to do so under local regulation. For example, as a result of regulation in Europe under the Second Payment Services Directive (PSD2), we may face competition from other networks, processors and other third-parties who could process Visa transactions directly with issuers and acquirers.

We also face increasingly intense competitive pressure on the prices we charge our financial institution clients. We believe our fundamental value proposition of acceptance, security, convenience and universality offers us a key competitive advantage. We succeed in part because we understand the needs of the individual markets in which we operate. We do so by partnering with local financial institutions, merchants, governments, non-governmental

12

organizations and business organizations to provide tailored solutions to meet their varied needs. We believe Visa is well-positioned competitively, due to our global brand, our broad set of Visa-branded payment products and our proven track record of processing payment transactions securely and reliably through VisaNet.

SEASONALITY

We generally do not experience any pronounced seasonality in our business. No individual quarter of fiscal 2016 or fiscal 2015 accounted for more than 30% of our operating revenues in those years.

WORKING CAPITAL

Payments settlement due to and from our financial institution clients can represent a substantial daily working capital requirement. Most U.S. dollar settlements are settled within the same day and do not result in a receivable or payable balance, while settlement in currencies other than the U.S. dollar generally remain outstanding for one to two business days, which is consistent with industry practice for such transactions.

FINANCIAL INFORMATION ABOUT GEOGRAPHIC AREAS

For more information on the concentration of our operating revenues and other financial information, see Item 8—Financial Statements and Supplementary Data—Note 13—Enterprise-wide Disclosures and Concentration of Business included elsewhere in this report.

GOVERNMENT REGULATION

As a global payments technology company, we are subject to complex and evolving global regulations in the various jurisdictions in which our products and services are used. The most significant government regulations that impact our business are discussed below. For further discussion of how global regulations may impact our business, see Item 1A—Risk Factors—Regulatory Risks.

Supervisory Oversight of the Payments Industry. Visa is subject to financial sector oversight and regulation in substantially all of the jurisdictions in which we operate. In the U.S., the Federal Financial Institutions Examination Council (FFIEC) has supervisory oversight over Visa under applicable federal banking laws and policies. The federal banking agencies comprising the FFIEC are the Federal Reserve Board, the Comptroller of the Currency, the Federal Deposit Insurance Corporation and the National Credit Union Administration. Visa also may be examined by the Consumer Financial Protection Bureau (CFPB) as a service provider to the banks that issue Visa-branded consumer credit and debit card products. Central banks in other countries, including Russia, Ukraine, Hong Kong and Europe (as discussed below), have recognized or designated Visa for purposes of various degrees of financial stability regulation as a retail payment system. Visa is also subject to oversight by banking and financial sector authorities in other jurisdictions, such as Brazil, Mexico and Colombia.

Government-imposed Market Participation and Restrictions. Certain governments, including China, Russia and India, have taken actions to advantage domestic payments systems and/or certain issuers, payments networks or processors, including by imposing regulations that favor domestic providers or that mandate domestic processing be done entirely in that country.

Interchange Rates and Fees. An increasing number of jurisdictions around the world regulate or influence debit and credit interchange reimbursement rates in their regions. For example, the Dodd-Frank Act in the U.S. limits interchange reimbursement rates for certain debit card transactions, the E.U.’s Interchange Fee Regulation (IFR) limits interchange rates in Europe (as discussed below) and the Reserve Bank of Australia has regulated average permissible levels of interchange for over a decade.

Network Exclusivity and Routing. In the U.S., the Dodd-Frank Act limits network exclusivity and preferred routing for the debit and prepaid market segments. Other jurisdictions impose similar limitations, such as the IFR’s prohibition on restrictions that prevent multiple payment brands or functionality on the same card.

No-surcharge Rules. We have historically enforced rules that prohibit merchants from charging higher prices to consumers who pay using Visa products instead of other means. However, merchants’ ability to surcharge varies by geographic market as well as Visa product type, and continues to be impacted by litigation, regulation and legislation.

Privacy and Data Protection. Aspects of our operations or business are subject to privacy, data use and data security regulations, which impact the way we use and handle data, operate our products and services, and even

13

impact our ability to offer a product or service. In addition, regulators are proposing new laws or regulations which could require Visa to adopt certain cybersecurity practices. In many jurisdictions consumers must be notified in the event of a data breach, and such notification requirements continue to increase in scope and cost. The European Union’s General Data Protection Regulation, which will become effective in May 2018, will create new individual privacy rights and impose worldwide obligations on companies handling personal data.

Anti-corruption, Anti-money Laundering, Anti-terrorism and Sanctions. We are subject to anti-corruption laws and regulations, including the U.S. Foreign Corrupt Practices Act (FCPA), the U.K. Bribery Act and other laws, that generally prohibit the making or offering of improper payments to foreign government officials and political figures for the purpose of obtaining or retaining business or to gain an unfair business advantage. We are also subject to anti-money laundering and anti-terrorist financing laws and regulations, including the U.S. Bank Secrecy Act and the USA PATRIOT Act. In addition, we are subject to economic and trade sanctions programs administered by the Office of Foreign Assets Control (OFAC) in the U.S.

Internet Transactions. Many jurisdictions have adopted regulations that require payments system participants to monitor, identify, filter, restrict or take other actions with regard to certain types of payment transactions on the Internet, such as gambling and the purchase of cigarettes or alcohol.

Additional Regulatory Developments. Various regulatory agencies also continue to examine a wide variety of other issues, including mobile payment transactions, tokenization, money transfer, identity theft, account management guidelines, disclosure rules, security and marketing that could affect our financial institution clients and us.

European Regulations and Supervisory Oversight. In addition, following the Visa Europe acquisition in June 2016, we are subject to complex and evolving regulation of our business in the European Union. Visa Europe has been designated as a Recognized Payment System, bringing it within the scope of the Bank of England’s oversight to ensure the financial stability of the U.K. Visa Europe is also subject to the Eurosystem’s oversight, including the security of payment instruments and ecommerce security policies and scheme rules. Furthermore, Visa Europe is regulated by the U.K.’s Payment Systems Regulator (PSR), which has wide ranging powers and authority to review our business practices, systems, rules and fees with respect to promoting competition and innovation in the U.K., and ensuring payments meet account holder needs. It also is the regulator responsible for monitoring and enforcing the IFR in the U.K. Outside the U.K., in relation to IFR, Visa is also subject to compliance monitoring by national competent authorities in all markets. The IFR regulates interchange rates within Europe, requires Visa Europe to separate its payment card scheme activities from processing activities for accounting, organization and decision making purposes within the E.U. and imposes limitations on network exclusivity and routing.

There are other regulations in the E.U. that impact our business, as discussed above, including, privacy and data protection, anti-bribery, anti-money laundering, anti-terrorism and sanctions. Other recent regulatory changes in Europe such as the PSD2 could reduce perceived barriers to entry for emerging, non-card payments.

AVAILABLE INFORMATION

We are subject to the reporting requirements of the Securities Exchange Act of 1934, as amended (Exchange Act) and its rules and regulations. The Exchange Act requires us to file periodic reports, proxy statements and other information with the U.S. Securities and Exchange Commission (SEC). Copies of these reports, proxy statements and other information can be viewed at http://www.sec.gov. Our corporate website is accessible at http://corporate.visa.com. We make available, free of charge, on our investor relations website at http://investor.visa.com our annual reports on Form 10-K, our quarterly reports on Form 10-Q, our current reports on Form 8-K and any amendments to those reports as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC. We also may include supplemental financial information on our investor relations website at http://investor.visa.com and may use this website as a means of disclosing material, non-public information and for complying with our disclosure obligations under Regulation FD. Accordingly, investors should monitor such portions of our investor relations website, in addition to following SEC filings and publicly available conference calls. The information contained on, or accessible through, our corporate website, including the information contained on our investor relations website, is not incorporated by reference into this report or any other report filed with, or furnished to, the SEC.

ITEM 1A. Risk Factors

Regulatory Risks

14

Increased regulation of the global payments industry, including with respect to interchange reimbursement fees, operating rules and related practices, could harm our business.

Regulators around the world have been establishing or increasing their authority to regulate certain aspects of the payments industry. See Item 1. Business —Government Regulation for more information. In the U.S. and many other jurisdictions, we have historically set default interchange reimbursement fees. Even though we generally do not receive any revenue related to interchange reimbursement fees in a purchase transaction (those fees are paid by the acquirers to the issuers), interchange reimbursement fees are a factor on which we compete with other payments providers and are therefore an important determinant of the volume of transactions we process. Consequently, changes to these fees, whether voluntarily or by mandate, can substantially affect our overall payments volumes and revenues.

Interchange reimbursement fees, certain operating rules and related practices continue to be subject to increased government regulation globally, and regulatory authorities and central banks in a number of jurisdictions have reviewed or are reviewing these fees, rules and practices. For example, in 2011, in accordance with the U.S. Dodd-Frank Act, the U.S. Federal Reserve capped the maximum U.S. debit interchange reimbursement rate received by large financial institutions at 21 cents plus 5 basis points, plus a possible fraud adjustment of 1 cent. This amounted to a significant reduction in the average system-wide interchange reimbursement fees received by large issuers. The Dodd-Frank Act also limited issuers' and our ability to adopt network exclusivity and preferred routing in the debit and prepaid area, which also impacted our business. In 2015, the E.U.’s IFR placed an effective cap on consumer credit and consumer debit interchange fees for both domestic and cross border transactions (30 basis points and 20 basis points, respectively), significantly reducing the fees received by E.U. issuers. E.U. Member States have the ability to further restrict these interchange levels within their territories. More recently, in September 2016, Argentina's Senate approved a bill to reduce existing caps on the merchant discount rate charged by acquirers to 1.5% for credit transactions and zero for debit transactions.

In addition to the regulation of interchange reimbursement fees, a number of regulators impose restrictions on other aspects of our payments business. For example, government regulations or pressure may require or allow other networks to be supported by Visa products or services or to have the other network's functionality or brand marks on our products. As innovations in payment technology have enabled us to expand into new products and services, they have also expanded the potential scope of regulatory influence. In addition, the E.U.’s requirement to separate scheme and processing adds costs and could impact the efficient integration of Visa Europe; the execution of our commercial, innovation and product strategies; our ability to provide effective customer service; and the amount of data available for use in fraud and risk systems and loyalty services.

We are also subject to central bank oversight in the U.K. and the E.U. This oversight could result in new governance, reporting, licensing, cybersecurity, processing infrastructure, capital or credit risk management requirements. We could also be required to adopt policies and practices designed to mitigate settlement and liquidity risks, including increased requirements to maintain sufficient levels of capital and financial resources locally. Increased central bank oversight could also lead to new or different criteria for financial institution participation in, and access to our payments system. Additionally, regulators in other jurisdictions are considering or adopting approaches based on similar regulatory principles.

Regulators around the world increasingly take note of each other’s approaches to regulating the payments industry. Consequently, a development in one jurisdiction may influence regulatory approaches in another. The risks created by a new law or regulation in one jurisdiction have the potential to be replicated and to negatively affect our business in another jurisdiction or in other product offerings. The U.S. Dodd-Frank Act and the E.U. IFR are developments with such potential, as are approaches taken by regulators in Australia, Canada and other countries. See Note 20—Legal Matters of this report. Similarly, new regulations involving one product offering may prompt regulators to extend the regulations to other product offerings. For example, credit payments could become subject to the same regulation as debit payments. Additionally, regulation in an individual country could continue and expand. For example, in Australia the Reserve Bank of Australia (RBA) initially capped credit interchange, but subsequently capped debit interchange as well.

When we cannot set default interchange reimbursement rates at optimal levels, issuers and acquirers may find our payments system less attractive. This may increase the attractiveness of other payments systems, such as our competitors' closed-loop payments systems with direct connections to both merchants and consumers. We believe some issuers may react to such regulations by charging new or higher fees to consumers, making our products less appealing to consumers. Some acquirers may elect to charge higher merchant discount rates regardless of the Visa interchange reimbursement rate, causing merchants not to accept our products or to steer customers to alternate

15

payments systems or forms of payment. In addition, in an effort to reduce the expense of their card programs, some issuers and acquirers have obtained, and may continue to obtain, incentives from us and reductions in the fees that we charge, which may directly impact our revenues. For these reasons, increased global regulation of the payments industry may make our products less desirable, diminish our ability to compete, reduce our transaction volumes and harm our business.

Government-imposed restrictions on payment systems may prevent us from competing against providers in certain countries.

Governments in various jurisdictions, such as in Asia and the Gulf Cooperation Countries in the Middle East, protect certain domestic payment card networks, brands and processors. These governments may impose regulatory requirements that favor domestic providers or that mandate domestic payments processing be done entirely in that country, which would prevent us from overseeing the end-to-end processing of certain transactions. In China, for example, UnionPay continues to enjoy advantages over other international networks, remains the sole processor of domestic payment card transactions and operates the sole domestic acceptance mark. Though the Chinese State Council has announced that international schemes, such as Visa would be able to participate in the domestic market and be eligible to apply for a license to operate a Bank Card Clearing Institution (BCCI) in China, the full implementation guidelines for BCCI’s have yet to be finalized. In Russia, legislation has effectively prevented us from processing in the domestic market and mandated that we migrate our domestic processing business to the state-owned NSPK (or national payment card system), which is the only entity allowed to process domestically.

Due to our inability to oversee the end-to-end processing of transactions for cards carrying our brands in these countries, we depend on our close working relationships with our clients or third party processors in these regions to ensure transactions involving our products are processed effectively. National laws that protect domestic processing may increase our costs, decrease the number of Visa products issued or processed, impede us from utilizing our global processing capabilities and control the quality of the services supporting our brands, restrict our activities, force us to leave countries or prevent us from entering new markets, all of which could harm our ability to operate our business, maintain or increase our revenues globally and extend our global brands.

We are subject to complex and evolving global regulations that could harm our business and financial results.

As a global payments technology company, we are subject to complex and evolving regulations that govern our operations. See Item 1—Business—Government Regulation for more information on the most significant areas of regulation that affect our business. The impact of these regulations on us (and on our clients and other third parties) could limit our ability to enforce our payments system rules or require us to adopt new rules or change existing rules, and it may increase our compliance costs and reduce our revenue opportunities. We may face differing rules and regulations in matters like interchange reimbursement rates, preferred routing, domestic processing requirements, currency conversion, point-of-sale transaction rules and practices, privacy, data use or protection and associated product technology. As a result, the Visa Rules and our other contractual commitments may differ from country to country or by product offering. Complying with these and other regulations increases our costs and can reduce our revenue opportunities. Further, as regulations change, they may affect our existing contractual arrangements.

If widely varying regulations come into existence worldwide, we may have difficulty rapidly adjusting our product offerings, services and fees, and other important aspects of our business in the various regions where we operate. Our compliance programs and policies are designed to support our compliance with a wide array of regulations and laws, and we continually enhance our compliance programs as regulations evolve. However, we cannot guarantee that our practices will be deemed compliant by all applicable regulatory authorities. In the event our controls should fail or we are found to be out of compliance for other reasons, we could be subject to monetary damages, civil and criminal penalties, litigation and damage to our global brands and reputation. Furthermore, the evolving and increased regulatory focus on the payments industry could reduce the number of Visa products our clients issue, the volume of payments we process and our revenue; negatively impact our brands and our competitive positioning; and limit the types of products and services that we offer, the countries in which our products are used and the types of customers and merchants who can obtain or accept our products, all of which could harm our business.

We may be subject to tax examinations or disputes, or changes in the tax laws.

16

We exercise significant judgment in calculating our worldwide provision for income taxes and other tax liabilities. Although we believe our tax estimates are reasonable, many factors may limit their accuracy. We are currently under examination by, or in disputes with, the U.S. Internal Revenue Service, the U.K.’s HM Revenue & Customs as well as tax authorities in other jurisdictions, and we may be subject to additional examinations or disputes in the future. Relevant tax authorities may disagree with our tax treatment of certain material items and thereby increase our tax liability. Failure to sustain our position in these matters could harm our cash flow and financial position. In addition, changes in existing laws, such as recent proposals for fundamental U.S. and international tax reform or those resulting from the Base Erosion and Profit Shifting (BEPS) project being conducted by the Organization for Economic Cooperation and Development, may also increase our effective tax rate. A substantial increase in our tax payments could have a material, adverse effect on our financial results. See also Note 19—Income Taxes to our consolidated financial statements included in Item 8 of this report.

Litigation Risks

We may be adversely affected by the outcome of litigation or investigations, despite certain protections that are in place.

We are involved in numerous civil actions and government investigations alleging violations of competition and antitrust law, consumer protection law and intellectual property law, among others. Details of the claims and the status of those proceedings are described more fully in Note 20—Legal Matters. Legal and regulatory proceedings and investigations are inherently uncertain, expensive and disruptive to our operations. In the event we are found liable in any material litigation, proceedings or investigations, particularly in a large class action lawsuit or an antitrust claim entitling the plaintiff to treble damages, we may be required to pay significant awards or settlements. In addition, settlement terms, judgments or pressures resulting from legal proceedings or investigations may require us, to modify the default interchange reimbursement rates we set, revise the Visa Rules or the way in which we enforce our rules, modify our fees or pricing, or modify the way we do business, which may harm our business. Finally, we are required by some of our commercial agreements to indemnify other entities for litigation asserted against them, even if Visa is not a defendant.

For certain litigation matters like the U.S. covered litigation and the VE territory covered litigation, which are described in Note 3—U.S. and Europe Retrospective Responsibility Plans and Note 20—Legal Matters, we have certain protections provided for in the respective retrospective responsibility plans. The two retrospective responsibility plans are different in the protections they provide and the mechanisms by which we are able to either fund the settlements and judgments in the case of the U.S. covered litigation or recoup covered losses in the case of the VE territory covered litigation. The failure of one or both of the retrospective responsibility plans to adequately insulate us from the impact of such settlements, judgments, losses or liabilities could materially harm our financial condition or cash flows, or even cause us to become insolvent.

Business Risks

We face intense competition in our industry.

The global payments space is intensely competitive. As technology evolves, new competitors emerge and existing clients and competitors assume different roles. Our products compete with cash, checks, electronic funds, virtual currency payments, global or multi-regional networks, other closed-loop payments systems, and alternative payment providers primarily focused on enabling payments through ecommerce and mobile channels. As the global payments space becomes more complex, we face increasing competition from our clients, emerging payment providers and other digital and technology companies. Many of these providers have developed payments systems enabled through online activity in ecommerce and mobile channels, and are seeking to expand into other channels that compete with or replace our products and services.

Additionally, some of our competitors may develop substantially better technology, more widely adopted delivery channels or have greater financial resources. They may offer a wider range of programs, products and services, including some that are more innovative. They may use advertising and marketing strategies that are more effective than ours, achieving broader brand recognition, and greater issuance and merchant acceptance. They may also develop better security solutions or more favorable pricing arrangements.

Certain of our competitors operate with different business models, have different cost structures or participate in different market segments. Those business models may ultimately prove more successful or more adaptable to

17

regulatory, technological and other developments. In some cases, these competitors have the support of government mandates that prohibit, limit or otherwise hinder our ability to compete for transactions within certain countries and regions.

Some of our competitors, including American Express, Discover, private-label card networks, virtual currency providers, technology companies that enable the exchange of digital assets and certain alternate payments systems, operate closed-loop payments systems, with direct connections to both merchants and consumers. Government actions or initiatives such as the U.S. Dodd-Frank Act or the U.S. Federal Reserve’s Faster Payments initiatives may provide them with increased opportunities to derive competitive advantages from these business models. Similarly, regulation in Europe under PSD2 and in the U.K. through the PSR may require us to open up access to, and allow participation in, our network to additional participants, and reduce the infrastructure investment and regulatory burden on potential competitors. We also run the risk of disintermediation due to factors such as emerging technologies, including mobile payments, alternate payment credentials, other ledger technologies or payment forms, and by virtue of increasing bilateral agreements between entities that prefer not to use our payments network for processing payments. For example, merchants could process transactions directly with issuers, or processors could process transactions directly with issuers and acquirers.

We expect the competitive landscape to continue to shift and evolve. For example:

• | competitors, clients and others are developing alternative payment networks or products that could disintermediate us from the transaction processing or the value-added services we provide to support such processing. Examples include initiatives like The Clearing House, an ACH-based payment system comprised of large financial institutions, and EWS, an alternative to an ACH payment system that provides faster funds or real-time payments across P2P, corporate and government disbursement, bill pay and deposit check transactions; |

• | similarly, multiple countries are developing or promoting ACH-based real-time payment systems or mandating local networks with clients that also present a risk of disintermediation to our business; |

• | parties that process our transactions may try to minimize or eliminate our position in the payments value chain; |

• | parties that access our payment credentials, tokens and technologies, including clients, technology solution providers or others might be able to migrate account holders and other clients to alternate payment methods or utilize our payment credentials, tokens and technologies to establish or help bolster alternate payment methods and platforms; |

• | competitors, clients and others may develop methods to use our payment credentials, tokens and technologies to compete with, impair or replace digital payment products that use and support our network and processing over our network; |

• | we may need to adjust our local rules and practices to remain competitive amidst evolving regulatory landscapes and competitors’ practices; |

• | we may be asked to develop or customize certain aspects of our payment services for use by our customers, processors or other third parties, thereby increasing operational costs; |

• | we may need to agree to business arrangements with terms less protective of Visa’s proprietary technology and interests in order to compete with others, including those with issuers and with competing networks; |

• | participants in the payments industry may merge, form joint ventures or enable or enter into other business combinations that strengthen their existing business propositions or create new, competing payment services; |

• | competition may increase from alternate types of payment services, such as mobile payment services, ecommerce payment services, P2P payment services, faster payment initiatives and payment services that permit ACH payments or direct debit of consumer checking accounts; |

18

• | new players and intermediaries in the payments value chain may redirect transactions or steer participants away from our network; |

• | we may face increasing risk of others asserting their intellectual property rights and potential litigation, as market entrants include technology companies and companies from industries where patent rights are actively asserted; |

• | as this landscape is quickly evolving, we may not be able to foresee or respond sufficiently to emerging risks associated with new business, products, services and practices; or |

• | new or revised industry standards related to EMV-chip payment technology, cloud-based payments, tokenization or other technologies set by organizations such as the International Organization for Standardization, American National Standards Institute and EMVCo may result in additional costs and expenses for Visa and its clients, or otherwise negatively impact the functionality and competitiveness of our products and services. |

Our failure to compete effectively in light of any such developments could harm our business and prospects for future growth.

Our revenues and profits are dependent on our client and merchant base, which may be costly to win, retain and maintain.

Our financial institution clients and merchants can reassess their commitments to us at any time or develop their own competitive services. While we have certain contractual protections, our clients, including some of our largest clients, generally have flexibility to issue non-Visa products. Further, in certain circumstances, our financial institution clients may decide to terminate our contractual relationship on relatively short notice without paying significant early termination fees. Because a significant portion of our operating revenues is concentrated among our largest clients, the loss of business from any one of these larger clients could harm our business, results of operations and financial condition.

In order to stay competitive, we offer incentives to our clients to increase payments volume, enter new market segments and expand their use and acceptance of Visa products and services. These include up-front cash payments, fee discounts and rebates, credits, performance-based incentives, marketing and other support payments that impact our revenues and profitability. In addition, we offer incentives to certain merchants or acquirers to win routing preference in situations where other network functionality is enabled on our products and there is a choice of network routing options. Market pressures on providing incentives, fee discounts and rebates could moderate our growth. If we are not able to implement cost containment and productivity initiatives in other areas of our business or increase our volumes in other ways to offset the financial impact of these incentives, fee discounts and rebates, it may harm our net revenues and profits.

In addition, it may be difficult or costly for us to acquire or conduct business with financial institutions or merchants that have longstanding exclusive, or nearly exclusive, relationships with our competitors. These financial institutions or merchants may be more successful and may grow more quickly than our existing clients or merchants. In addition, if there is a consolidation or acquisition of one or more of our largest clients or co-brand partners by a financial institution client or merchant with a strong relationship with one of our competitors, it could result in our business shifting to a competitor, which could put us at a competitive disadvantage and harm our business.

Merchants' and processors' continued push to lower acceptance costs and challenge industry practices could harm our business.

We rely in part on merchants and their relationships with our clients to maintain and expand the acceptance of Visa products. Certain large retail merchants have been exercising their influence in the global payments system to attempt to lower their acceptance costs by lobbying for new legislation, seeking regulatory enforcement, filing lawsuits and in some cases, refusing to accept Visa products. If they are successful in their efforts, we may face increased compliance and litigation expenses and issuers may decrease their issuance of our products. In the U.S., the cost of payment card acceptance has emerged in the context of payment security. A number of merchant trade associations claim that EMV cards without PIN cardholder verification are not worth the investment. The October 2015 liability shift and ongoing transition to EMV resulted in calls for a PIN verification mandate. More recently, U.S. merchant-affiliated groups and processors have expressed concerns regarding the EMV certification process. Some

19

policymakers have called upon U.S. competition authorities to consider potential concerns arising from the roles of industry bodies such as EMVCo and the Payment Card Industry Security Standards Council. Additionally, some merchants and processors have pushed for changes to industry practices and our requirements for Visa acceptance at the point of sale, including the ability for merchants to accept only certain types of Visa products, to mandate only PIN authenticated transaction, to differentiate or steer among Visa product types issued by different financial institutions, and to impose surcharges on customers presenting Visa products as their form of payment. If successful, these efforts could adversely impact consumers' usage of our products, lead to regulatory enforcement and/or litigation, increase our compliance and litigation expenses, and harm our business.

We depend on relationships with our financial institution clients, acquirers, merchants and other third parties.

We depend significantly on relationships with our financial institution clients and on their relationships with customers and merchants to support our programs and services and thereby compete effectively in the marketplace. Our relationships with industry participants are complex and require us to balance the interests of multiple third parties. For example, in the U.S., the EMV migration has been resisted by certain merchants, leading to conflicts and litigation concerning the timing and scope of the liability shift, chargebacks and debit routing, among others.

We engage in discussions with merchants, acquirers and processors to provide incentives to promote routing preference and acceptance growth. We engage in many payment card co-branding efforts with merchants, who receive incentives from us. As these and other relationships become more prevalent and take on a greater importance to our business, our success will increasingly depend on our ability to continue to engage in these discussions in order to sustain and grow these relationships.

In addition, we depend on third parties, including suppliers, and our financial institution clients to provide various services associated with our payments network, on our behalf. To the extent that such parties fail to perform or deliver adequate services, our business and reputation could be harmed.

If we are not able to maintain and enhance our brands, if events occur that damage our reputation or brands or we experience brand disintermediation, it could harm our business.

Our brands are globally recognized and are key assets of our business. We believe that our clients and customers associate our brands with acceptance, security, convenience and universality. Our success depends in large part on our ability to maintain the value of our brands and reputation of our products and services in the payments ecosystem, elevate the brand through new and existing products, services and partnerships, and uphold our corporate reputation. The increased use or popularity of products that we have developed in partnership with large technology and financial institution companies could result in consumer confusion or brand disintermediation and decrease the value of our brand. In addition, our brands and reputation may be negatively impacted by a number of factors, including data security breaches, compliance failures, negative perception of our industry or the industries of our clients, actions by clients or other third parties, such as sponsorship partners, that do not reflect our views or are inconsistent with our own business practices, and fraudulent or other illegal activity using our payment products. If we are unable to maintain our reputation, or if events occur that damage our reputation, the value of our brands may be impaired, which could harm our relationships with clients, customers and the public, as well as impact our business.

Global economic, political, market and social events or conditions may harm our business.

Our revenues are dependent on the volume and number of payment transactions made by customers, governments and businesses, whose spending patterns may be affected by prevailing economic conditions. In addition, almost half of our operating revenues are earned outside the U.S. International transaction revenues represent a significant part of our revenue and are an important part of our growth strategy. Therefore, adverse macroeconomic conditions, including recessions, inflation, high unemployment, currency fluctuations, actual or anticipated large-scale defaults or failures, or slowdown of global trade, could decrease consumer and corporate confidence and reduce consumer, government and corporate spending, which have a direct impact on our revenues. In addition, outbreaks of illnesses, pandemics or other local or global health issues like the Zika virus, political uncertainties like Brexit, international hostilities, armed conflict, or unrest, and natural disasters could impact our operations, our clients and our activities in a particular location. These events could also reduce cross-border travel and spend, which impacts our international transaction revenues, which are generated by processing cross-border payments and cash volume transactions, as well as from foreign currency exchange transactions. Any

20

such decline in cross-border activity could impact the number of cross-border transactions we process and our foreign currency exchange activities, and in turn reduce our revenues.

A decline in economic conditions could impact our clients as well, and their decisions to reduce the number of cards, accounts and credit lines of their account holders, which ultimately impact our revenues. They may also implement cost-reduction initiatives that reduce or eliminate marketing budgets, and decrease spending on optional or enhanced, value-added services from us.