Attached files

| file | filename |

|---|---|

| EX-32.2 - EX 32.2 - VERDE RESOURCES, INC. | vrdr_ex322.htm |

| EX-32.1 - EX 32.1 - VERDE RESOURCES, INC. | vrdr_ex321.htm |

| EX-31.2 - EX 31.2 - VERDE RESOURCES, INC. | vrdr_ex312.htm |

| EX-31.1 - EX 31.1 - VERDE RESOURCES, INC. | vrdr_ex311.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 30, 2016

or

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from [______] to [______]

Commission file number: 000-55276

VERDE RESOURCES, INC. |

(Exact name of registrant as specified in its charter) |

Nevada |

| 32-0457838 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

| ||

Unit 701, 7/F, The Phoenix, 21-25 Luard Rd, Wanchai, Hong Kong |

| N/A |

(Address of principal executive offices) |

| (Zip Code) |

Registrant's telephone number, including area code: (852) 2152-1223

Securities registered pursuant to Section 12(b) of the Act:

Securities registered pursuant to Section 12(b) |

| Name of Each Exchange |

|

|

|

N/A |

| N/A |

Securities registered pursuant to Section 12(g) of the Act: Common Stock, $0.001 par value.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes x No o

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the last 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registration statement was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ¨ | Accelerated filer | ¨ |

Non-accelerated filer | ¨ | Smaller reporting company | x |

(Do not check if a smaller reporting company) |

|

|

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold of $0.05 (or the average bid and asked price of such common equity) as of the last business day of the registrant’s most recently completed second fiscal quarter, being December 31, 2015, was $3,740,308.

Indicate the number of shares outstanding of each of the registrant's classes of common stock as of the latest practicable date.

91,288,909 as of September 26, 2016

DOCUMENTS INCORPORATED BY REFERENCE

None.

| 2 |

Cautionary Note Regarding Forward-Looking Statements

Except for historical information, this report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward-looking statements involve risks and uncertainties, including, among other things, statements regarding our business strategy, future revenues and anticipated costs and expenses. Such forward-looking statements include, among others, those statements including the words "expects," "anticipates," "intends," "believes" and similar language. Our actual results may differ significantly from those projected in the forward-looking statements. Factors that might cause or contribute to such differences include, but are not limited to, those discussed in the sections "Business," "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations." You should carefully review the risks described in this Annual Report on Form 10-K and in other documents we file from time to time with the Securities and Exchange Commission. You are cautioned not to place undue reliance on the forward-looking statements, which speak only as of the date of this report. We undertake no obligation to publicly release any revisions to the forward-looking statements or reflect events or circumstances after the date of this document.

Although we believe that the expectations reflected in these forward-looking statements are based on reasonable assumptions, there are a number of risks and uncertainties that could cause actual results to differ materially from such forward-looking statements.

All references in this Form 10-K to the "Company," "Verde," "we," "us" or "our" are to Verde Resources, Inc.

Overview

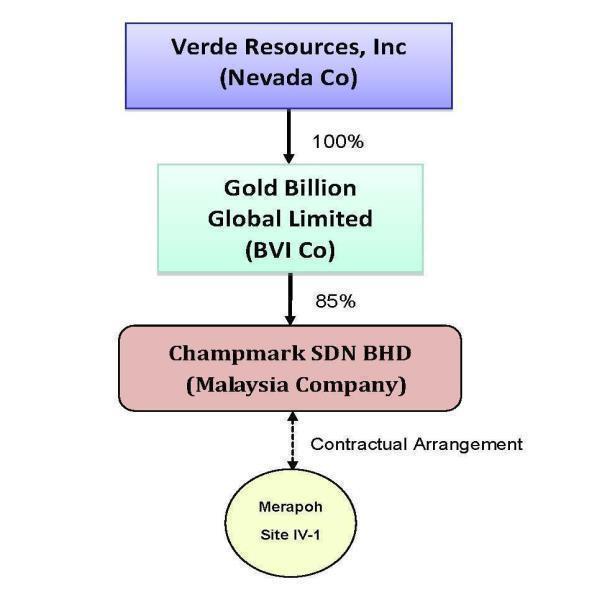

Verde Resources, Inc. (the "Company" or "VRDR") was incorporated in the State of Nevada on April 22, 2010. The Company conducts business operations in Pahang Malaysia through Champmark Sdn Bhd ("CSB"), a privately limited liability company incorporated in Malaysia, which is a deemed subsidiary under the management control of our 100% subsidiary Gold Billion Global Limited ("GBL"), a company incorporated under the laws of the British Virgin Islands.

On October 25, 2013, we entered into an Assignment Agreement For the Assignment of Management Right in Merapoh Gold Mines in Malaysia ("Assignment Agreement") with Federal Mining Resources Limited ("FMR"), a company incorporated under the laws of the British Virgin Islands.

FMR owns 85% equity interest in CSB, a privately limited liability company incorporated in Malaysia. CSB is the Mining Contractor of the Mining Lease for Site IV-1 at the Merapoh Gold Mine under the Contract for Work with MMC Corporation Berhad, the Permit Holder of the Mining Lease.

Under the terms of the Assignment Agreement, FMR has assigned its management rights of CSB's mining operation in the Mining Lease to the Company, through its wholly-owned subsidiary Gold Billion Global Limited ("GBL"), in exchange for 80,000,000 shares of the Company's common stock, which constituted 95.26% of our issued and outstanding capital stock as of and immediately after the consummation of the acquisition.

GBL was formed on February 7, 2013, by the Board of Directors of FMR to monitor the CSB operation. The acquisition of 100% of the issued and outstanding capital stock of GBL was agreed upon on October 18, 2013, and completed on October 25, 2013, subject to the approval of the Board of Directors and the audit of GBL.

On February 17, 2014, we entered into a Supplementary Agreement to the Assignment Agreement and completed a reverse acquisition of GBL pursuant to the Supplementary Agreement. As a result of the acquisition, the Company holds 100% equity interest in GBL and 85% variable interest in CSB. Our consolidated subsidiaries include GBL being our wholly-owned subsidiary and 85% of CSB being a variable interest entity (VIE) and deemed subsidiary of GBL. On April 1, 2014, GBL purchased 85% equity interest of CSB, and CSB became indirect subsidiary of the Company.

| 3 |

| Table of Contents |

Corporate History and Structure

Verde Resources, Inc. was incorporated on April 22, 2010, in the State of Nevada, U.S.A. On October 17, 2013, Stephen Spalding and Michael Stiege resigned from all of their positions as officers and directors of the Company that complies with the requirements of Section 14f-1 of the Exchange Act. The following persons were appointed to serve as directors and to assume the responsibilities of officers on October 17, 2013. Mr. Wu Ming Ding, as President and Director; Mr. Balakrishnan B S Muthu as Treasurer Chief Financial Officer, General Manager and Director; and Mr. Liang Wai Keen as Secretary. Mr. Wu and Mr. Muthu were added to the Board of Directors.

On October 17, 2013, the Company provided written notice to Gold Explorations, LLC, that the Purchase Agreement dated May 17, 2010, amended February 8, 2012, and further amended May 17, 2013 (the "Purchase Agreement"), has been cancelled according to the terms of the Purchase Agreement. By providing this notification, the Company has no further obligations under the Purchase Agreement and has released any interest in the mineral claims located in Esmeralda County, Nevada.

On April 1, 2014, the Board of Directors of Gold Billion Global Limited ("GBL") notified Federal Mining Resources Limited ("FMR") upon the decision to exercise the right of option to purchase 85% equity interest of Champmark Sdn Bhd ("CSB") under Management Agreement Section 3.2.4 dated July 1, 2013, between GBL and FMR. This acquisition was completed on April 1, 2014, with consideration of US$1, and GBL then became 85% shareholder of CSB.

Effective August 27, 2014, the Company's Articles of Incorporation were amended to increase the authorized shares of the Company from 100,000,000 shares of common stock to 250,000,000 shares of common stock.

Effective February 20, 2016, Mr. Wu Ming Ding resigned all of his positions as President and Director of the Company with Mr. Balakrishnan B S Muthu being appointed President to fill the vacancy created. Effective February 20, 2016, Mr. Chen Ching was appointed Director of the Company and the entire Board of Directors now consists of Mr. Balakrishnan B S Muthu and Mr. Chen Ching.

The following diagram illustrates our current corporate structure:

According to ASC 810-05-08 A, CSB is a deemed subsidiary of GBL where GBL controls the Board of Directors of CSB, rights to receive future benefits and residual value, and obligation to absorb loss and finance for CSB. GBL has the power to direct the activities of CSB that most significantly impact CSB's economic performance and the obligation to absorb losses of CSB that could potentially be significant to the CSB or the right to receive benefits from CSB that could potentially be significant to CSB. GBL is the primary beneficiary of CSB because GBL can direct the activities of CSB through the common directors and 85% shareholder FMR. Under 810-23-42, 43, it is determined that CSB is de-facto agent of the principal GBL and so GBL will consolidate CSB from July 1, 2013. On April 1, 2014, GBL purchased 85% equity interest of CSB, and CSB became indirect subsidiary of the Company.

| 4 |

| Table of Contents |

Contractual Arrangements

Our exploration and mining business is currently provided through contractual arrangements with CSB through our wholly-owned subsidiary GBL.

CSB, the VIE of GBL, sells gold minerals directly to the registered gold trading company in Malaysia. We have been and are expected to continue to be dependent on our VIE to operate our exploration and mining business. GBL has entered into contractual arrangements with its VIE, which enable us to exercise effective control over the VIE, receive substantially all of the economic benefits from the VIE, and have the option to purchase equity interests in the VIE.

On July 1, 2013, the Company's subsidiary GBL entered into a series of agreements ("VIE agreements") with FMR and details of the VIE agreements are as follows :

| 1. | Management Agreement, FMR entrusted the management rights of its subsidiary CSB to GBL that include: | |

| i.) | management and administrative rights over the day-to-day business affairs of CSB and the mining operation at Site IV-1 of the Merapoh Gold Mine; | |

| ii.) | final right for the appointment of members to the Board of Directors and the management team of CSB; | |

| iii.) | act as principal of CSB; | |

| iv.) | obligation to provide financial support to CSB; | |

| v.) | option to purchase an equity interest in CSB; | |

| vi.) | entitlement to future benefits and residual value of CSB; | |

| vii.) | right to impose no dividend policy; | |

| viii.) | human resources management. | |

|

|

| |

2. | Debt Assignment, FMR assigned to GBL the sum of money in the amount of three hundred nine thousand three hundred thirty one dollars and ninety-two cents (US$ 309,331.92), now due to GBL from CSB under the financing obligation from the FMR to CSB. | ||

With the above agreements, GBL demonstrates its ability to control CSB as the primary beneficiary and the operating results of the VIE was included in the condensed consolidated financial statements for the year ended June 30, 2014.

CSB holds the operating right to Merapoh Gold Mine (the "Mine") with all regulatory and government operating licenses in Malaysia.

On April 1, 2014, GBL purchased 85% equity interest of CSB, and CSB became indirect subsidiary of the Company.

Stage Of Operation

The Company does not own any title and/or concession right in any mines. The Company is undertaking natural mineral resource extraction management services. The Company expects to hire a mine management team to supervise the mineral resource extraction activities to ensure that the operations can be carried out without significant problems.

According to the United States Industry Guide 7 (a) (4) on mining operations, the Merapoh Gold Mine is currently in the production stage because the mine has produced approximately 30 kilograms of gold from July 2015 to June 2016. According to the ASC 930-330-20 Glossary, the production phase is defined as "when saleable minerals are extracted (produced) from an ore body, regardless of the level of production". However, the production is limited to a small part of the site, and extraction is alluvial gold only. The objective of the Company is preparing to improve the productivity of the mines to ensure that the operation will be carried out effectively and efficiently at minimum cost.

| 5 |

| Table of Contents |

Table of Contents

Current Mining Property and Location

Merapoh Gold Mine (the "Mine")

The Merapoh Gold Mine is located in northern Pahang, with convenient road access through Kelantan directly to the mine site and is about 400 kilometers away from Kuala Lumpur. The Mine is located in the middle of Malaysia's gold metallogenic belt. The central gold belt is the source of the majority of the gold deposits in the peninsula. It lies between the western and eastern tin belts and extends from Kelantan (Sungai Pergau, Sungai Galas) to Pahang (Merapoh, Kuala Lipis, Raub), Terengganu (Lubuk Mandi), Negri Sembilan and Johor (Gunung Ledang).

Mine Area:

Site IV-1 of the Merapoh Gold Mine consists of a mining area of 400 acres with mining lease.

Location and Access:

The Merapoh Gold Mine is about 280km from Kuala Lumpur, and 50km from Kuala Lipis, the former state capital of Pahang, accessible via secondary paved highways with a new major highway under construction expected to be complete d in 2018. The geological coordinates of the mine are 101 ° 58 ′ , 4 ° 35 ′ ,

| 6 |

| Table of Contents |

Type of Claim:

Champmark Sdn Bhd, the subsidiary of Gold Billion Global Limited, is the Mining Contractor of the Mining Lease for Site IV-1 of the Merapoh Gold Mine under the Contract for Work with MMC Corporation Berhad, the Permit Holder of the Mining Lease.

Identifying Information of the Merapoh Gold Mine:

Mining Right:

Mining Lease No.: ML 08/2008

Operational Mining Scheme No.: JMG.PHG.(M)24/2014/11(Au)

Concession Period: From April 4, 2014 to April 3, 2015

Regional Geology:

The Malaysia Central Gold Belt runs along the entire backbone of Peninsular Malaysia, extending further to the north. It was formed between the Sibumasu block in the west and Manabor block in the east that runs along major mineral deposits in Thailand, Myanmar and China. The regional gold deposits were made of Epithermal deposits that formed in a series of volcanic environment, where the tensional fractures along the subduction zone allows the intrusion of mineral rich acidic magma within deep faults.

Rock Formations and Mineralization:

Site IV-1 of the Merapoh Gold Mine covers an area of 400 acres with mineralization structure being Permian limestone dominating the South-East portion, felsic volcanic tuff in the Western portion of the area and intrusive dacite rock to the north-west of the area. Tectonic contact within the sheer zone of creates epithermal mineralization, forming mineral rich vein along the contact zone. The mineralized zone is made of highly altered tuffacaous rock with abundant pyrite dissemination and moderately spaced quartz vein.

Work Completed and Present Condition:

Lode gold exploration on Site IV-1 has commenced since 2011 and still in progress with both in-house drilling team and third party drilling services running in parallel to expedite data collection to generate a comprehensive JORC compliant gold reserve report.

Equipment, Infrastructure and Other Facilities of the Merapoh Gold Mine:

Parlongs

These are basic production plants and the processing method employed five high powered manual water guns, angled water buffering control and 5-lane carpeted sluice with lateral barriers. The processing capacity is between 40 - 45 tons per hour.

OPS 1

This is a modified production plant and the processing method employed four high powered manual water guns, tapered rotating screen scrubber, angled water flow buffering and 3-lane carpeted sluice with lateral barriers. The processing capacity is between 30 - 35 tons per hour.

GS 150

This is a non-self-propelled mobile production plant and the processing method employed fixed spray guns, 6m x 2m rotating screen scrubber, 6-lane carpeted sluice with lateral barriers and conveyer belt pebble dispenser. The processing capacity is between 25 - 30 tons per hour.

GS 120

This is a self-propelled mobile plant with concentrator and the processing method employed fixed spray guns, 4m x 3m rotating screen scrubber, fixed screen, conveyer belt pebble dispenser and triple concentrator processor. The processing capacity is between 15 - 20 tons per hour.

| 7 |

| Table of Contents |

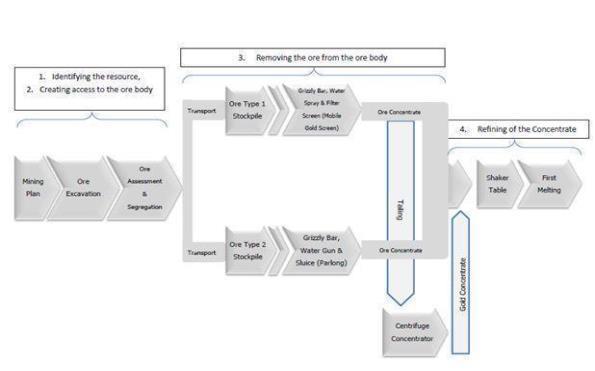

Description of Processing Facilities:

Process for removing ore concentrates from the ore body

1. | The ore body is transported to the treatment plants in vehicles capable of hauling huge, heavy loads. |

2. | The ore body is separated into Ore Type 1 Stockpile and Ore Type 2 Stockpile. |

3. | The monitor washes finer gold bearing material off larger rocks which is screened on an inclined coarse wire screen. |

4. | An excavator is used to turn over the rocks so wash is removed from all sides of the coarse material. |

5. | A monitor pushes the rock down the inclined coarse screen where the course is removed and stockpiled at the bottom. |

6. | Finer material passes through the mesh screen into the sluice system and runs over the sluice. |

7. | The carpets are removed and taken to refining facility for gold recovery. |

8. | A suction pipe recovers water of the fine tailings pond for use in the system. |

Refining of the concentrate

1. | The carpets holding concentrate from the sluice are brought to a shed in the camp site where the gold is refined. |

2. | The first stage of the refining is to wash the gold containing concentrate into large bins. This is pumped to a jig and shaking table. |

3. | Nuggets are handpicked from the coarse fraction and the fine fraction is amalgamated to remove the gold. After distillation, gold from the amalgam and the coarse are melted with flux and the gold is poured into small bars. |

Current State of Exploration:

As of the date of this report, the Merapoh Gold Mine property is without known reserves.

The Merapoh Gold Mine commenced exploratory operation in alluvia mining and achieved its first gold pour in July 2011. Through the years of operation, the Company has performed ongoing exercises to improve upon the matching of processing method with the types of ore in order to optimize cost to recovery ratio. In July 2013, production was outsourced to a reputable subcontractor, and developed a resource management system to match ore against processes to achieve the most cost efficient and highest recovery production procedure.

| 8 |

| Table of Contents |

Table of Contents

Gold ore extraction of the Merapoh Gold Mine for the twelve months ended June 30, 2016, was approximately 285,745 tons of gold ore or a monthly average of 23,812 tons (using a 12-month average), with an average gold grade of 0.106 g/t. Gold concentrate sold for the twelve months ended June 30, 2016, was approximately 27.47 kg. The production level, in units of daily tonnage of raw mineral rocks extracted, averaged 783 tons/day (12-month average) during the fiscal year 2016.

The Merapoh Gold Mine is currently at the production stage. In the effort to expand production capacity, the Company intends to purchase more vehicles, machineries and equipment as well as to conduct feasibility studies for exploration of alluvial and lode gold resources.

Subcontractors

In an effort to enhance the efficiency of mine operations at the Merapoh Gold Mine, Champmark Sdn Bhd ("CSB") entered into an Operation Term Sheet ("OTS") agreement in July 2013 to outsource the exploitation works of alluvial gold resources at Site IV-1 of the Merapoh Gold Mine to a third party subcontractor Borneo Oil & Gas Corporation Sdn Bhd ("BOG"). However, BOG became the Company's shareholder in January 29, 2014 and was no longer a third party subcontractor.

BOG has the experience and local knowledge in managing the exploitation of alluvial gold at the Merapoh Gold Mine. The Company currently intends to continue to outsource the exploitation of alluvial gold at our mine site to BOG as our third party subcontractor. The Company will provide necessary disclosure when any significant agreements have been made with the sub-contractor in the future.

Number of Employees

The Company had 3 employees during the year from July 1, 2015 to June 30, 2016.

Reports to Security Holders

The public may read and copy any materials filed with the SEC at the SEC's Public Reference Room at 100 F Street NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The Company files its reports electronically with the SEC. The SEC maintains an Internet site that contains reports, proxy and information statements, and other electronic information regarding New Media and filed with the SEC at http://www.sec.gov.

Change of Control

On October 25, 2013, the Company entered into an Assignment Agreement for the Assignment of Management Right ("AAMA") in Merapoh Gold Mines in Malaysia with Federal Mining Resources Limited ("FMR"). Under the terms of the Agreement and relevant subsequent Supplemental Agreement, FMR assigned its management rights to the Company Board of Directors of FMR agreed to transfer 1 share common stock of Gold Billion Global Limited ("GBL") which represented all shares of common stock of GBL owned by the Investor, and the Company's Board of Directors agreed to issue 80,000,000 million shares of common stock in full value as consideration. At the time of closing under the AAMA, the Investor transferred 100% ownership of GBL shares to the Company, and the Company issued 80,000,000 million shares of common stock to the shareholders of FMR in exchange for the GBL Shares. The effect of the transaction was to make GBL and its deemed subsidiaries become wholly-owned and 85.00% owned subsidiaries of the Company, and to cause a change of control of GBL. Following the closing, there was a change of control in the Company.

The Transaction was accounted for as a "reverse merger," since FMR owned a majority of the outstanding shares of VRDR's common stock immediately following the execution of the transaction. The Company was deemed to be the accounting acquirer in the reverse merger. Consequently, the assets and liabilities and the historical operations that were reflected in the financial statements for periods prior to the transaction were those of the Company and its deemed subsidiaries, and were recorded at the historical cost basis of the Company. After completion of the transaction, the Company's consolidated financial statements were include the assets and liabilities of the Company and its subsidiaries, the historical operations of the Company and its subsidiaries, and the operations of the Company and its subsidiaries from the closing date of the transaction.

| 9 |

| Table of Contents |

Risks Associated With Verde Resources, Inc.

We are dependent on certain key personnel and loss of these key personnel could have a material adverse effect on our business, financial condition and results of operations.

Messrs. Balakrishnan Muthu, our current principal executive officer and financial officer, has extensive contacts and experience in the gold exploration and natural resource industry in Malaysia, and we are dependent upon his abilities and services to develop and market our business. He is responsible for overseeing all of our day-to-day business operations of our operating company, CSB, and its subsidiaries and VIEs, including the mining operations and negotiations for the sales of any gold concentrates extracted. We may not be able to retain the executive officers/managers for any given period of time. The loss of their services could have a material adverse effect upon our business operations, financial condition and results of operations. In addition, we must attract, recruit and retain a sizeable workforce of technically competent employees in Malaysia to run our mining operations. Our ability to effectively implement our proposed business strategies and expand our operations will depend upon the successful recruitment and retention of additional highly skilled and experienced management and other key personnel in Malaysia. If we cannot maintain highly experienced and skilled management teams, our business could fail and you could lose any investment you make in our shares.

Since our business consists of managing gold mining projects, the drop in the price of gold would negatively impact our asset values, cash flows, potential revenues and profits.

We plan to pursue opportunities in properties with gold mineralized material or reserves with exploration potential. Our potential future revenues are expected to be derived from the production and sale of gold from these properties, or from the sale of some of these properties. The value of any gold reserves or other mineralized materials, and the value of any potential mineral production will vary in direct proportion to changes in those mineral prices. The price of gold has fluctuated widely as a result of numerous factors beyond our control. The effect of these factors on the price of gold and other minerals, and therefore the economic viability of any of our projects, cannot accurately be predicted. Any drop in the price of gold and other minerals we may produce would negatively affect our asset values, cash flows and potential revenues and profits.

We may not be able to find commercially viable reserves.

Mineral exploration and development involve a high degree of risk and few properties that are explored are ultimately developed into producing mines. The reserve estimates, if any, are based only on prefeasibility studies that are inherited with the following drawbacks:

| - | Limited amount of drilling completed to date; |

| - | The process testing is limited to small pilot plants and bench scale testing; |

| - | Difficulty in obtaining expected metallurgical recoveries when scaling up to production scale from pilot plant scale; |

| - | Preliminary nature of the mine plans and processing concepts; |

| - | Preliminary nature of operating and capital cost estimates |

| - | Metallurgical flow sheets and recoveries still in development; |

| - | Limited history of prefeasibility studies that might be underestimating capital and operating costs. |

We cannot assure that any future mineral exploration and development activities will result in any discoveries of proven or probable reserves as defined by the SEC. Further, we cannot provide any assurance that, even if we discover commercial quantities of mineralization, a mineral property will be brought into commercial production. Development of our mineral property will follow only upon obtaining sufficient funding and satisfactory exploration results.

| 10 |

| Table of Contents |

Estimates of mineral reserves and of mineralized material are inherently forward-looking statements, subject to error, which could force us to curtail or cease our business operations.

Estimates of mineral reserves and of mineralized materials are inherently forward-looking statements subject to error. Unforeseen events and uncontrollable factors can have significant adverse impacts on the estimates. Actual conditions inherently differ from estimates. The unforeseen adverse events and uncontrollable factors may include: geologic uncertainties including inherent sample variability, metal price fluctuations, fuel price increases, variations in mining and processing parameters, and adverse changes in environmental or mining laws and regulations. The timing and effects of variances from estimated values cannot be predicted.

| - | Geologic Uncertainty and Inherent Variability: Estimated reserves and additional mineralized materials are generally derived from appropriately spaced drilling to provide a high degree of assurance in the continuity of the mineralization; however, there is generally variability between duplicate samples taken adjacent to each other and between sampling points that cannot be reasonably eliminated. There are also unknown geologic details that are not always identified or correctly appreciated at the current level of delineation. This results in uncertainties that cannot be reasonably eliminated from the estimation process. Some of the resulting variances can have a positive effect, and others can have a negative effect on mining operations. Acceptance of these uncertainties is part of any mining operation. |

| - | Gold Price Variability: The prices for gold fluctuate in response to many factors beyond any ability to predict. The prices used in making the reserve estimates are disclosed and differ from daily prices quoted in the news media. The percentage change in the price of a metal cannot be directly related to the estimated reserve quantities, which are affected by a number of additional factors. For example, a ten percent (10%) change in price may have little impact on the estimated reserve quantities and affect only the resultant positive cash flow, or it may result in a significant change in the amount of reserves. Because mining occurs over a number of years, it may be prudent to continue mining for some period during which cash flows are temporarily negative for a variety of reasons, including a belief that the low price is temporary and/or the greater expense would be incurred in closing a property permanently. |

| - | Fuel Price Variability: The cost of fuel can be a major variable in the cost of mining; one that is not necessarily included in the contract mining prices obtained from mining contractors, but is passed on to the overall cost of operation. Future fuel prices and their impact are difficult to predict, but an increase in prices could force us to curtail or cease our business operations. |

| - | Variations in Mining and Processing Parameters: The parameters used in estimating mining and processing efficiency are based on testing and experience with previous operations at the properties or on operations at similar properties. Various unforeseen conditions can occur that may materially affect the estimates. In particular, past operations indicate that care must be taken to ensure that proper ore grade control is employed and that proper steps are taken to ensure that the leaching operations are executed as planned. Unforeseen difficulties may occur in our current or future operations which would force us to curtail or cease our business operations. |

| - | Changes in Environmental and Mining Laws and Regulations: Our reserve estimates contain cost estimates based on compliance with current laws and regulations in Malaysia. While there are no currently known proposed changes in these laws or regulations, significant changes have affected past operations of mining companies in Malaysia, and if additional changes do occur in the future, we may or may not be able to comply with them and continue our operations. |

We may not be able to successfully compete with other mineral exploration and mining companies.

We compete with other mineral exploration and mining companies or individuals, including large, well established mining companies with substantial capabilities and financial resources in Malaysia, to research and acquire rights to mineral properties containing gold and other minerals. There is a limited supply of desirable mineral lands available for claim staking, lease or other acquisition in Malaysia. We do not know if we will be able to successfully acquire any prospective mineral properties against competitors with substantially greater financial resources than we have. If we cannot successfully acquire other mining properties to manage and explore and generally expand our business operations, our results of operations, financial condition and future revenues could be reduced and you could suffer a loss of any investment made in our shares.

| 11 |

| Table of Contents |

We are subject to the many risks of doing business internationally, including but not limited to the difficulty of enforcing liabilities in foreign jurisdictions.

We are a Nevada corporation and, as such, are subject to the jurisdiction of the State of Nevada and the United States courts for purposes of any lawsuit, action or proceeding by investors. An investor would have the ability to effect service of process in any action against the Company within the United States. In addition, we are registered as a foreign corporation doing business in Malaysia, and as such, are subject to the local laws of Malaysia governing an investors' ability to bring actions in foreign courts and enforce liabilities against a foreign private issuer, or any person, based on U.S. federal securities laws. Generally, a final and conclusive judgment obtained by investors in U.S. courts would be recognized and enforceable against us in the Malaysia courts having jurisdiction without re-examination of the merits of the case.

Investors may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing original actions in Malaysia based upon U.S. laws, including the federal securities laws or other foreign laws against us or our management.

All of our current operations are conducted in Malaysia, and all of our directors and officers are nationals and residents of Malaysia and other foreign countries. All or substantially all of the assets of these persons are located outside the United States and in other foreign countries. As a result, it may not be possible to effect service of process within the United States or elsewhere outside Malaysia upon these persons. In addition, uncertainty exists as to whether the courts of Malaysia would recognize or enforce judgments of U.S. courts obtained against us or such officers and/or directors predicated upon the civil liability provisions of the securities laws of the United States or any state thereof, or be competent to hear original actions brought in Malaysia against us or such persons predicated upon the securities laws of the United States or any state thereof.

Failure to comply with the United States Foreign Corrupt Practices Act could subject us to penalties and other adverse consequences.

We are subject to the United States Foreign Corrupt Practices Act, which generally prohibits U.S. companies from engaging in bribery or other prohibited payments to foreign officials for the purpose of obtaining or retaining business. In addition, we are required to maintain records that accurately and fairly represent our transactions and have an adequate system of internal accounting controls. Foreign companies, including some that may compete with us, are not subject to these prohibitions, and therefore may have a competitive advantage over us. Our executive officers and employees have not been subject to the United States Foreign Corrupt Practices Act prior to 2010. If our employees or other agents are found to have engaged in such practices, we could suffer severe penalties and other consequences that may have a material adverse effect on our business, financial condition and results of operations.

Mining risks and insurance could negatively effect on our profitability.

The business of mining for gold is generally subject to a number of risks and hazards including environmental hazards, industrial accidents, labor disputes, unusual or unexpected geological conditions, pressures, cave-ins, changes in the regulatory environment, and natural phenomena such as inclement weather conditions, floods, blizzards and earthquakes. At the present time, we have in effect statutory required social insurance for all employees and mine workers. There is currently no other insurance in place for the mining site and management, and even if we were to purchase additional insurance, we cannot be sure that such insurance would be available to us, or that we could afford the premiums. Insurance coverage may not continue to be available or may not be adequate to cover any resulting liability. In addition, insurance against risks such as environmental pollution or other hazards as a result of exploration and production is not generally available to companies in the mining industry on acceptable terms. We might also become subject to liability for pollution or other hazards which we may not be insured against, or which we may elect not to insure against, because of premium costs or other reasons. Any losses from any of these events may cause us to incur significant costs that could have a material adverse effect upon our financial performance and results of operations, which could negatively impact any investment you make in our shares.

| 12 |

| Table of Contents |

If we fail to maintain effective internal controls over financial reporting, the price of our common stock may be adversely affected.

Malaysian companies may not always adopt a Western style of management and financial reporting concepts and practices, which includes strong corporate governance, internal controls and computer, financial and other control systems. In addition, we may have difficulty in hiring and retaining a sufficient number of qualified employees to work in Malaysia. As a result of these factors, we may experience difficulty in establishing management, legal and financial controls, collecting financial data and preparing financial statements, books of account and corporate records and instituting business practices that meet Western standards for foreign subsidiaries. As a result, we may experience difficulties in implementing and maintaining adequate internal controls as required under Section 404 of the Sarbanes-Oxley Act of 2002. This could result in significant deficiencies or material weaknesses in our internal controls, which could impact the reliability of our financial statements and prevent us from complying with SEC rules and regulations and the requirements of the Sarbanes-Oxley Act of 2002. Any actual or perceived weaknesses and conditions that need to be addressed in our internal control over financial reporting, disclosure of management's assessment of our internal controls over financial reporting or disclosure of our public accounting firm's attestation to or report on management's assessment of our internal controls over financial reporting may have an adverse impact on the price of our common stock.

Changes in interest rates could negatively impact our results of operations, stockholders' equity (deficit) and fair value of net assets.

Our investment activities and credit guarantee activities expose us to interest rate and other market risks. Changes in interest rates, up or down, could adversely affect our net interest yield. Although the yield we earn on our assets and our funding costs tend to move in the same direction in response to changes in interest rates, either can rise or fall faster than the other, causing our net interest yield to expand or compress. For example, due to the timing of maturities or rate reset dates on variable-rate instruments, when interest rates rise, our funding costs may rise faster than the yield we earn on our assets. This rate change could cause our net interest yield to compress until the effect of the increase is fully reflected in asset yields. Changes in the slope of the yield curve could also reduce our net interest yield.

Interest rates can fluctuate for a number of reasons, including changes in the fiscal and monetary policies of the federal government and its agencies, such as the Federal Reserve. Federal Reserve policies directly and indirectly influence the yield on our interest-earning assets and the cost of our interest-bearing liabilities. The availability of derivative financial instruments (such as options and interest rate and foreign currency swaps) from acceptable counterparties of the types and in the quantities needed could also affect our ability to effectively manage the risks related to our investment funding. Our strategies and efforts to manage our exposures to these risks may not be effective in the future, which could negatively impact our results of operations and the price of our common stock.

The audit report included in our Annual Report was prepared by auditors who are not inspected by the Public Accounting Oversight Board (“PCAOB”) and as a result, our shareholders are deprived of the benefit of having PCAOB inspections.

The independent registered public accounting firm that issues the audit reports included in our annual reports filed with the SEC, as auditors of companies that are traded publicly in the United States and a firm registered with the Public Company Accounting Oversight Board (United States), or the “PCAOB”, is required by the laws of the United States to undergo regular inspections by the PCAOB to assess its compliance with the laws of the United States and professional standards. Because our auditors are located in Hong Kong SAR, a jurisdiction where the PCAOB is currently unable to conduct inspections without the approval of the Hong Kong authorities, our auditors are not currently inspected by the PCAOB.

Inspections of other firms that the PCAOB has conducted outside Hong Kong SAR have identified deficiencies in those firms' audit procedures and quality control procedures, which may be addressed as part of the inspection process to improve future audit quality. The inability of the PCAOB to conduct inspections in Hong Kong SAR prevents the PCAOB from regularly evaluating our auditor's statements, audits and quality control procedures. As a result, investors may be deprived of the benefits of PCAOB inspections.

The inability of the PCAOB to conduct inspections of auditors in Hong Kong SAR makes it more difficult to evaluate the effectiveness of our auditor's quality control and audit procedures as compared to auditors outside of Hong Kong SAR that are subject to PCAOB inspections. Investors may lose confidence in our reported financial information and procedures and the quality of our financial statements.

We may be exposed to risks relating to management’s conclusion that our disclosure controls and procedures and internal controls over financial reporting are ineffective.

We do not have an independent audit committee and our Board of Directors may be unable to fulfill the functions of such a committee, which may compromise the management of our business. Our Board of Directors functions as our audit committee and is comprised of two directors, none of whom are considered to be "independent" in accordance with the requirements of Rule 10A-3 under the Securities Exchange Act of 1934. An independent audit committee plays a crucial role in the corporate governance process, assessment of the Company's processes relating to its risks and control environment, oversight of financial reporting, and evaluation of internal and independent audit processes. The lack of an independent audit committee may prevent the Board of Directors from being independent in its judgments and decisions and its ability to pursue the committee's responsibilities, which could compromise the management of our business.

| 13 |

| Table of Contents |

Risks Associated with Our Common Stock

Our shares are defined as "penny stock." The rules imposed on the sale of the shares may affect your ability to resell any shares you may purchase, if at all.

Our shares are defined as a "penny stock" under the Securities and Exchange Act of 1934, and rules of the Commission. The Exchange Act and such penny stock rules generally impose additional sales practice and disclosure requirements on broker-dealers who sell our securities to persons other than certain accredited investors who are, generally, institutions with assets in excess of $5,000,000 or individuals with net worth in excess of $1,000,000 or annual income exceeding $200,000, or $300,000 jointly with spouse, or in transactions not recommended by the broker-dealer. For transactions covered by the penny stock rules, a broker-dealer must make a suitability determination for each purchaser and receive the purchaser's written agreement prior to the sale. In addition, the broker-dealer must make certain mandated disclosures in penny stock transactions, including the actual sale or purchase price and actual bid and offer quotations, the compensation to be received by the broker-dealer and certain associated persons, and deliver certain disclosures required by the Commission. Consequently, the penny stock rules may affect the ability of broker-dealers to make a market in or trade our common stock, and may also affect your ability to resell any shares you may purchase.

Market for penny stock has suffered in recent years from patterns of fraud and abuse

Stockholders should be aware that, according to SEC Release No. 34-29093, the market for penny stocks has suffered in recent years from patterns of fraud and abuse. Such patterns include:

| · | Control of the market for the security by one or a few broker-dealers that are often related to the promoter or issuer; |

| · | Manipulation of prices through prearranged matching of purchases and sales and false and misleading press releases; |

| · | Boiler room practices involving high-pressure sales tactics and unrealistic price projections by inexperienced salespersons; |

| · | Excessive and undisclosed bid-ask differential and markups by selling broker-dealers; and, |

| · | The wholesale dumping of the same securities by promoters and broker-dealers after prices have been manipulated to a desired level, along with the resulting inevitable collapse of those prices and with consequential investor losses. |

Our management is aware of the abuses that have occurred historically in the penny stock market. Although we do not expect to be in a position to dictate the behavior of the market or of broker-dealers who participate in the market, management will strive within the confines of practical limitations to prevent the described patterns from being established with respect to our securities. The occurrence of these patterns or practices could increase the volatility of our share price.

Inability and unlikelihood to pay dividends

To date, we have not paid, nor do we intend to pay in the foreseeable future, dividends on our common stock, even if we become profitable. Earnings, if any, are expected to be used to advance our activities and for general corporate purposes, rather than to make distributions to stockholders. Prospective investors will likely need to rely on an increase in the price of Company stock to profit from his or her investment. There are no guarantees that any market for our common stock will ever develop or that the price of our stock will ever increase.

Since we are not in a financial position to pay dividends on our common stock and future dividends are not presently being contemplated, investors are advised that return on investment in our common stock is restricted to an appreciation in the share price. The potential or likelihood of an increase in share price is questionable at best.

Item 1B. Unresolved Staff Comments.

None.

| 14 |

| Table of Contents |

We do not currently own any properties.

On October 25, 2013, we entered into an Assignment Agreement For the Assignment of Management Right in Merapoh Gold Mines in Malaysia ("Assignment Agreement") with Federal Mining Resources Limited ("FMR"), a company incorporated under the laws of the British Virgin Islands.

FMR owns 85% equity interest in Champmark Sdn Bhd ("CSB"), a privately limited liability company incorporated in Malaysia. CSB is the Mining Contractor of the Mining Lease for Site IV-1 at the Merapoh Gold Mine under the Contract for Work with MMC Corporation Berhad, the Permit Holder of the Mining Lease.

Under the terms of the Assignment Agreement, FMR assigned its management rights of CSB's mining operation in the Mining Lease to the Company, through its wholly-owned subsidiary Gold Billion Global Limited ("GBL"), in exchange for 80,000,000 shares of the Company's common stock, which constituted 95.26% of our issued and outstanding capital stock as of and immediately after the consummation of the acquisition.

On April 1, 2014, the Board of Director of Gold Billion Global Limited ("GBL") notified Federal Mining Resources Limited ("FMR") upon the decision to exercise the right of option to purchase 85% equity interest of Champmark Sdn Bhd ("CSB") under Management Agreement Section 3.2.4 dated July 1, 2013, between GBL and FMR. The original agreement was filed with SEC as ex10-2.htm of Form 8K on February 20, 2014. This acquisition was completed on April 1, 2014, with consideration of US$1. GBL then became 85% shareholder of CSB.

As at June 30, 2016, the property and equipment owned by CSB are summarized, at net book values as follows:

Land and Building |

| $ | 33,120 |

|

Plant and Machinery |

| $ | 15,760 |

|

Office equipment |

| $ | 921 |

|

Project equipment |

| $ | 76,347 |

|

Computer |

| $ | 403 |

|

Motor Vehicle |

| $ | 25,074 |

|

|

| $ | 151,625 |

|

None

Item 4. Mine Safety Disclosures.

Pursuant to Section 1503(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (" Dodd-Frank Act "), issuers that are operators, or that have a subsidiary that is an operator, of a coal or other mine in the United States are required to disclose in their periodic and annual reports filed with the SEC information regarding specified health and safety violations, orders and citations, related assessments and legal actions, and mining-related fatalities under the regulation of the Federal Mine Safety and Health Act of 1977. The Company did not have any mines in the United States during the year ended June 30, 2016.

| 15 |

| Table of Contents |

Market Information

Our common stock is now quoted on the OTCQB, under the symbol "VRDR". Our stock was approved for quotation on the OTCBB on September 26, 2012. However, the Company's common stock did not begin active trading until October, 2013.

The following table sets forth the high and low bid prices for our common stock per quarter as reported by the OTCBB since trading began October 7, 2013, based on our fiscal year end June 30, 2016. These prices represent quotations between dealers without adjustment for retail mark-up, markdown or commission, and may not represent actual transactions.

Fiscal Quarter Ended |

| High |

|

| Low |

| ||

|

|

|

|

|

|

| ||

December 31, 2015 |

| $ | 0.068 |

|

| $ | 0.05 |

|

March 31, 2016 |

| $ | 0.075 |

|

| $ | 0.05 |

|

June 30, 2016 |

| $ | 0.05 |

|

| $ | 0.041 |

|

As of September 26, 2016, we had 26 shareholders of record of our common stock and 91,288,909 shares issued and outstanding.

Dividend Policy

We have not paid any cash dividends on our common stock and have no present intention of paying any dividends on the shares of our common stock. Our current policy is to retain earnings, if any, for use in our operations and in the development of our business. Our future dividend policy will be determined from time to time by our board of directors.

Equity Compensation Plan Information

None.

Recent Sales of Unregistered Securities; Use of Proceeds from Registered Securities

We did not sell any equity securities which were not registered under the Securities Act during the year ended June 30, 2016, that were not otherwise disclosed on our quarterly reports on Form 10-Q or our current reports on Form 8-K filed during the year ended June 30, 2016.

On October 25, 2013, the Company issued 80,000,000 common shares at par value under the terms of the Assignment Agreement whereby FMR will assign its management rights of CSB's mining operation in the Mining Lease to VRDR, through its wholly-owned subsidiary GBL, in exchange for 80,000,000 shares of the Company's common stock.

On November 11, 2013, the Company issued 75,000 common shares at US$1.75 per share to Marketing Management International, LLC ("MMI"), a Florida Limited Liability Company, under the terms of the Consulting Agreement for the engagement of its consulting services.

| 16 |

| Table of Contents |

On January 29, 2014, the Company issued a total of 643,229 common shares for $665,238, of which 288,288 common shares at US$1.25 per share, 183,661 common shares at US$0.83 per share and 171,280 common shares at US$0.89 per share, to Borneo Oil & Gas Corporation Sdn Bhd ("BOG"), a Malaysia Limited Liability Company, under the terms of the Sub-Contractor Agreement for the engagement of its sub-contractor services.

On March 10, 2014, the Company issued a total of 693,180 common shares for $609,756, of which 179,340 common shares at US$0.85 per share and 513,840 common shares at US$0.89 per share, to Borneo Oil & Gas Corporation Sdn Bhd ("BOG"), a Malaysia Limited Liability Company, under the terms of the Sub-Contractor Agreement for the engagement of its sub-contractor services.

On January 21, 2015, the Company issued 5,900,000 common shares at US$0.05 per share to Borneo Oil & Gas Corporation Sdn Bhd ("BOG"), a Malaysia Limited Liability Company, under the terms of the Consultant Agreement for the additional services of its sub-contractor.

Purchase of Equity Securities by the Issuer and Affiliated Purchasers

We did not purchase any of our shares of common stock or other securities during our fourth quarter of our fiscal year ended June 30, 2016.

Item 6. Selected Financial Data.

As a "smaller reporting company," we are not required to provide the information required by this Item.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion should be read in conjunction with our audited financial statements and the related notes that appear elsewhere in this annual report. The following discussion contains forward-looking statements that reflect our plans, estimates and beliefs. Our actual results could differ materially from those discussed in the forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to those discussed below and elsewhere in this annual report, particularly in the section entitled "Risk Factors" of this annual report.

Our audited financial statements are stated in United States Dollars and are prepared in accordance with United States Generally Accepted Accounting Principles.

| 17 |

| Table of Contents |

Results of Operations

We have generated $929,655 and $831,339 revenues for the year ended June 30, 2016 and 2015, respectively, and have recorded a gross loss of $205,153 and $731,989 for the year ended June 30, 2016 and 2015. We have incurred $498,411 and $803,741in operating expenses through June 30, 2016 and June 30, 2015. We have other income $77,093 and $38,014 for the year ended June 30, 2016 and 2015.

The following table provides selected financial data about our company for the year ended June 30, 2016 and June 30, 2015.

Statement of Operation |

| June 30, 2016 |

|

| June 30, 2015 |

|

| Change |

| |||

| Amount |

|

| Amount |

|

| % |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenue |

| $ | 929,655 |

|

| $ | 831,339 |

|

|

| 12 |

|

Cost of revenue |

| $ | 1,134,808 |

|

| $ | 1,563,328 |

|

|

| (27 | ) |

Gross Loss |

| $ | 205,153 |

|

| $ | 731,989 |

|

|

| (72 | ) |

Operating Expenses |

| $ | 498,411 |

|

| $ | 803,741 |

|

|

| (38 | ) |

Other Income |

| $ | 77,093 |

|

| $ | 38,014 |

|

|

| 103 |

|

The revenue derived from the sales of gold mineral to customers in Malaysia. The increase of revenue for the period ended June 30, 2016 was mainly due to an increase in gold production and gold sales during the period. The decrease of cost of revenue was mainly due to a decrease of salaries and depreciation and increased of closing stock as at period ended and weakness of average rate for MYR:USD compared with last year. (2016: 0.2422 2015: 0.2883). Operating expenses comprised mainly of salaries, office costs, legal and professional fees and travelling expenses. The decrease in operating expenses for the period was mainly due to the due to the weakness of average rate for MYR:USD as mentioned above, and a reduction in the provision for professional and consultancy fees payable to related companies.

Plan of Operation

Our Industry and Principal Markets

Based on the forecast of Business Monitor International, a leading independent proprietary data provider, Malaysia's mining industry is anticipated to reach US$38.7bn by 2017, growing at an annual average rate of 2.5% from 2011 levels. The bulk of this growth will be led by the country's nascent gold mining sector, which has attracted a number of foreign investors in recent years. Our mineral exploration activities are subject to extensive national and local government regulations in Malaysia, which regulations may be revised or expanded at any time. Generally, compliance with these regulations requires the company to obtain the permits issued by government regulatory agencies. Certain permits require periodic renewal or review of their conditions. Malaysia provides an attractive mining legislative environment for foreign investors, but there is the risk that these laws will change once the country is able to attract enough foreign money.

| 18 |

| Table of Contents |

Subcontractor

In an effort to enhance the efficiency of mine operations at the Merapoh Gold Mine, Champmark Sdn Bhd ("CSB") entered into an Operation Term Sheet ("OTS") agreement in July 2013, to outsource the exploitation works of alluvial gold resources at Site IV-1 of the Merapoh Gold Mine to a third party subcontractor Borneo Oil & Gas Corporation Sdn Bhd ("BOG").

BOG has the experience and local knowledge in managing the exploitation of alluvial gold at the Merapoh Gold Mine. The Company currently intends to continue to outsource the exploitation of alluvial gold at our mine site to BOG as our third party subcontractor. The Company will provide necessary disclosure when any significant agreements have been made with the sub-contractor in the future.

BOG became the Company's shareholder in January 29, 2014 and was no longer a third party subcontractor.

Expansion Plans

At present, we are well positioned working with our third party subcontractor, who has the experience and local knowledge, in managing our exploitation of alluvial gold at the Merapoh Gold Mine. The Company believes that there are excellent growth opportunities for its business outside of Malaysia. We are constantly exploring for potential acquisition of mining projects in other parts of the world.

The Company is currently operating the gold mining operation at a small scale and is still in its initial stages to expand the production capacity of the gold mining operation. The Company has purchased a number of units of vehicles such as excavators, wheel loader, mobile mining equipment, motor vehicles and trucks for the mining of alluvial gold at the Mining Area. In the effort to expand production capacity, the Company intends to purchase more vehicles, machineries and equipment as well as to conduct feasibility studies for exploration of alluvial and lode gold resources.

As our business is affected by the fluctuations of gold prices, the Company intends to diversify its product line by acquiring mining projects with potential for different mineral resources other than gold. We are holding discussions with other mining companies for potential collaboration to carry out exploration and exploitation works on other mineral resources in Southeast Asia regions.

Limited Operating History; Need for Additional Capital

There is limited historical financial information about us upon which to base an evaluation of our performance. We cannot guarantee we will be successful in our business operations. Our business is subject to risks inherent in the establishment of a new business enterprise, including limited capital resources, possible delays in the exploration of our properties, and possible cost overruns due to price and cost increases in services.

We have no assurance that future financing will be available to us on acceptable terms. If financing is not available on satisfactory terms, we may be unable to continue, develop or expand our operations. Equity financing could result in additional dilution to existing shareholders.

| 19 |

| Table of Contents |

Liquidity and Capital Resources

The following table provides selected cash flow data about our company for the year ended June 30, 2016 and 2015.

Cash Flow Date |

| June 30, 2016 |

|

| June 30, 2015 |

| ||

|

|

|

|

|

|

| ||

Net Loss from operation |

| $ | 626,471 |

|

| $ | 1,497,716 |

|

Net Cash Generated/(Used) from operating activities |

| $ | (32,387 | ) |

| $ | (322,244 | ) |

Net Cash Generated/(Used) from investing activities |

| $ | - |

|

| $ | 76,456 |

|

Net Cash Generated/(Used) from financing activities |

| $ | (39,866 | ) |

| $ | 39,642 |

|

For the year ended June 30, 2016, the Company had incurred net loss from operation of $626,471 which posted a negative impact to the company's cash flow. The reconciliation on non-cash items such as depreciation provides negative impact on cash.

In the operation analysis, the net cash used in operating activities decreased from $322,244 to $32,387 for the years ended June 30, 2015 and 2016, respectively. The operation loss of $626,471 was partially offset by the noncash expenses such as $290,774 in depreciation. In the operating assets and liabilities, the net decrease in current assets, such as accounts receivable, inventory and deposits was $46,973 whereas the net increase in current liabilities, such as accounts payable, accrued liabilities, advanced from sub-contractor & related parties and taxation payable was $256,337, which provided $303,310 positive cash flow effect but not enough to offset the $626,471 loss in operation and loss from non-cash loss in the reorganization. The final result of the cash flow from operating activities was $32,387 negative cash flow effect.

In the investing and financing analysis, the repayments of bank loans end up with a negative cash flow of $39,866. The negative factors contribute to increase the negative operating cash flow. In addition, the net decrease in exchange rate effect of $51,439 also provided positive cash flow effect. The cash and cash equivalents at the end of June 30, 2016, was decreased by $20,814 with $16,113 as balance.

The cash flow situation will not allow for operations in the coming next 12 months by self-generated cash provided from operating activities. The Company needs to increase cash flow supplies with a long term plan until the Company makes sustainable profits and has a positive cash flow. Otherwise, loans from related parties may be a temporary solution, although we have no written loan agreements. There is no guarantee that we will be able to secure adequate financing. If we fail to secure sufficient funds, our business activities may be curtailed, or we may cease to operate.

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures, or capital resources that is material to investors.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk.

As a "smaller reporting company", we are not required to provide the information required by this Item.

| 20 |

| Table of Contents |

Item 8. Financial Statements and Supplementary Data

INDEX TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2016

| Page | ||

| |||

F-1 | |||

| |||

F-2 | |||

| |||

F-3 |

| ||

|

| ||

Consolidated Statements of Changes in Shareholders' Equity (Deficit) | F-4 | ||

|

| ||

F-5 |

| ||

|

| ||

F-6 |

| 21 |

CERTIFIED PUBLIC ACCOUNTANTS

7th Floor, Nan Dao Commercial Building

359-361 Queen's Road Central

Hong Kong

Tel : 2851 7954

Fax: 2545 4086

| To: | The board of directors and stockholders of |

| Verde Resources, Inc. ("the Company") |

Report of Independent Registered Public Accounting Firm

We have audited the accompanying consolidated balance sheet of Verde Resources, Inc. and its subsidiaries as of June 30, 2016 and 2015, and the related consolidated statements of loss, stockholders' equity and cash flows for the year ended June 30, 2016 and 2015. These consolidated financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

We were not engaged to examine management's assertion about the effectiveness of the Company's internal control over financial reporting as of June 30, 2016 included in the Company's Item 9A "Controls and Procedures" in the Annual Report on Form 10-K and, accordingly, we do not express an opinion thereon.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the consolidated financial position of Verde Resources, Inc. as of June 30, 2016 and 2015, and the results of its operations and its cash flows for the year ended June 30, 2016 and 2015 in conformity with accounting principles generally accepted in the United States of America.

The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 14 to the consolidated financial statements, the Company has suffered recurring losses from operations and has a significant accumulated deficit. In addition, the Company continues to experience negative cash flows from operations. These factors raise substantial doubt about the Company's ability to continue as a going concern. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Hong Kong, China | DCAW (CPA) Limited |

September 26, 2016 | Certified Public Accountants |

| F-1 |

| Table of Contents |

Verde Resources, Inc

|

| As at June 30, |

|

| As at June 30, |

| ||

|

| 2016 |

|

| 2015 |

| ||

ASSETS |

|

|

|

|

|

| ||

Current Assets |

|

|

|

|

|

| ||

Cash and cash equivalents |

| $ | 16,113 |

|

| $ | 36,927 |

|

Amount due from related parties |

|

| 3,619 |

|

|

| 3,017 |

|

Inventories |

|

| 123,238 |

|

|

| 11,865 |

|

Other deposit & prepayment |

|

| 1,546 |

|

|

| 161,431 |

|

Total Current Assets |

| $ | 144,516 |

|

| $ | 213,240 |

|

Long Term Assets |

|

|

|

|

|

|

|

|

Property, plant and equipment |

| $ | 151,625 |

|

| $ | 478,225 |

|

Total Long Term Assets |

| $ | 151,625 |

|

| $ | 478,225 |

|

|

|

|

|

|

|

|

|

|

TOTAL ASSETS |

| $ | 296,141 |

|

| $ | 691,465 |

|

|

|

|

|

|

|

|

|

|

LIABILITIES AND STOCKHOLDERS' DEFICIT |

|

|

|

|

|

|

|

|

Current Liabilities |

|

|

|

|

|

|

|

|

Accounts payable |

| $ | 1,626,524 |

|

| $ | 1,729,304 |

|

Advanced from related parties |

|

| 781,333 |

|

|

| 524,522 |

|

Accrual |

|

| 147,310 |

|

|

| 157,026 |

|

Taxation payable |

|

| 2,473 |

|

|

| 1,495 |

|

Loans from banks |

|

| 27,319 |

|

|

| 39,585 |

|

Total Current Liabilities |

| $ | 2,584,959 |

|

| $ | 2,451,932 |

|

Long term Liabilities |

|

|

|

|

|

|

|

|

Loans from banks (non-current) |

| $ | 7,777 |

|

| $ | 37,207 |

|

Total Long Term Liabilities |

| $ | 7,777 |

|

| $ | 37,207 |

|

|

|

|

|

|

|

|

|

|

TOTAL LIABILITIES |

| $ | 2,592,736 |

|

| $ | 2,489,139 |

|

|

|

|

|

|

|

|

|

|

STOCKHOLDERS' DEFICIT |

|

|

|

|

|

|

|

|

Preferred stock, par value $0.001, 50,000,000 shares authorized, none issued and outstanding |

|

| - |

|

|

| - |

|

Common stock, par value $0.001, 250,000,000 shares authorized, 91,288,909 shares issued and outstanding as of June 30, 2016 & June 30, 2015 |

| $ | 91,289 |

|

| $ | 91,289 |

|

Additional paid-in capital |

|

| 1,869,993 |

|

|

| 1,869,993 |

|

Accumulated deficit |

|

| (4,235,777 | ) |

|

| (3,653,699 | ) |

Accumulated other comprehensive income(loss) |

|

| 531,571 |

|

|

| 404,021 |

|

Non-controlled interest |

|

| (553,671 | ) |

|

| (509,278 | ) |

Total Stockholders' Deficit |

| $ | (2,296,595 | ) |

| $ | (1,797,674 | ) |

|

|

|

|

|

|

|

|

|

TOTAL LIABILITIES AND STOCKHOLDERS' DEFICIT |

| $ | 296,141 |

|

| $ | 691,465 |

|

The accompanying notes are an integral part of these consolidated financial statements.

| F-2 |

| Table of Contents |

Verde Resources, Inc.

Consolidated Statements of Operations

|

| For the year |

|

| For the year |

| ||

|

| ended |

|

| Ended |

| ||

|

| June 30, |

|

| June 30, |

| ||

|

|

|

|

|

|

| ||

REVENUES |

|

|

|

|

|

| ||

Revenue |

| $ | 929,655 |

|

| $ | 831,339 |

|

Cost of revenue |

|

| (1,134,808 | ) |

|

| (1,563,328 | ) |

Gross loss |

|

| (205,153 | ) |

|

| (731,989 | ) |

|

|

|

|

|

|

|

|

|

OPERATING EXPENSES: |

|

|

|

|

|

|

|

|

Selling, general & administrative expenses |

|

| (498,411 | ) |

|

| (803,741 | ) |

LOSS FROM OPERATIONS |

| $ | (703,564 | ) |

| $ | (1,535,730 | ) |

|

|

|

|

|

|

|

|

|

OTHER INCOME (EXPENSE) |

|

| 77,093 |

|

|

| 38,014 |

|

|

|

|

|

|

|

|

|

|

NET LOSS BEFORE INCOME TAX |

| $ | (626,471 | ) |

| $ | (1,497,716 | ) |

|

|

|

|

|

|

|

|

|

Provision of Income Tax |

|

| - |

|

|

| - |

|

NET LOSS |

| $ | (626,471 | ) |

| $ | (1,497,716 | ) |

|

|

|

|

|

|

|

|

|

Non-controlled interest |

|

| 44,393 |

|

|

| 125,928 |

|

Net loss contributed to the group |

|

| (582,078 | ) |

|

| (1,371,788 | ) |

Other comprehensive income(loss) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign currency translation gain(loss) |

| $ | 127,550 |

|

| $ | 404,432 |

|

|

|

|

|

|

|

|

|

|

Comprehensive loss |

| $ | (454,528 | ) |

| $ | (967,356 | ) |

|

|

|

|

|

|

|

|

|

Basic and Diluted Loss per Common Share |

| $ | (0.01 | ) |

| $ | (0.02 | ) |

|

|

|

|

|

|

|

|

|

Weighted Average Number of Common Shares Outstanding |

|

| 91,288,909 |

|

|

| 87,991,375 |

|

The accompanying notes are an integral part of these consolidated financial statements.

| F-3 |

| Table of Contents |

Verde Resources, Inc.

Statement of Changes in Stockholders' Equity (Deficit)

|

| Common Shares |

|

| Additional Paid-In |

|

| Accumulated |

|

| Non-Controlling |

|

| Accumulated Other |

|

|

| |||||||||||

|

| Shares |

|

| Amount |

|

| Capital |

|

| Deficit |

|

| Interest |

|

| Income (Loss) |

|

| Total |

| |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Balance - June 30, 2014 |

|

| 85,388,909 |

|

| $ | 85,389 |

|

| $ | 1,580,893 |

|

| $ | (2,281,911 | ) |

| $ | (383,350 | ) |

| $ | (411 | ) |

| $ | (999,390 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares issued |

|

| 5,900,000 |

|

|

| 5,900 |

|

|

| 289,100 |

|

|

| - |

|

|

| - |

|

|

| - |

|

|