Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - G III APPAREL GROUP LTD /DE/ | t1602108_ex99-1.htm |

| 8-K - FORM 8-K - G III APPAREL GROUP LTD /DE/ | t1602108_8k.htm |

Exhibit 99.2

G - III Apparel Group, Ltd. to Acquire Donna Karan International, Inc. August 2 016

63 106 133 240 224 210 234 182 134 216 184 170 140 136 136 232 232 232 115 76 82 Forward Looking Statements Statements concerning G - III's business outlook or future economic performance, anticipated revenues, expenses or other financial items; product introductions and plans and objectives related thereto; and statements concerning assumptions made or expectations as to any future events, conditions, performance or other matters are "forward - looking statements" as that term is defined under the Federal Securities laws. Forward - looking statements are subject to risks, uncertainties and factors which include, but are not limited to, reliance on licensed product, reliance on foreign manufacturers, risks of doing business abroad, the current economic and credit environment, the nature of the apparel industry, including changing customer demand and tastes, customer concentration, seasonality, risks of operating a retail business, customer acceptance of new products, the impact of competitive products and pricing, dependence on existing management, possible disruption from acquisitions and general economic conditions, as well as other risks detailed in G - III's filings with the Securities and Exchange Commission. G - III assumes no obligation to update the information in this presentation. Certain information included in this release is forward looking and is subject to important risks and uncertainties and factors beyond our control or ability to predict, that could cause actual results to differ materially from those anticipated, projected or implied. It only reflects our views as of the date of this presentation. No undue reliance should therefore be based on any such information, it being also agreed that we undertake no commitment to amend or update it after the date hereof. 1

63 106 133 240 224 210 234 182 134 216 184 170 140 136 136 232 232 232 115 76 82 G - III to Acquire Donna Karan and DKNY · G - III is acquiring one of the world’s most iconic and recognizable power brand portfolios · Donna Karan International, Inc. (“DKI”) fits squarely into G - III’s stated strategy to diversify and expand its business to further drive long - term shareholder value · G - III’s goal has been to acquire a brand in order to accelerate operating margin expansion; G - III expects DKI to have the highest operating margin within its stable of brands · Significant opportunity to generate incremental sales across channels and categories in U.S. and key markets worldwide · Financially compelling transaction that is expected to be accretive in the fiscal year ending January 31, 2019 (year 2) 2

63 106 133 240 224 210 234 182 134 216 184 170 140 136 136 232 232 232 115 76 82 Transaction Overview Transaction Summary · Transaction announced on July 25, 2016 · G - III will acquire DKI, parent of the Donna Karan and DKNY brands, from LVMH · Enterprise value of $650 million Sources of Financing Financial Impact · Committed financing from Barclays, JPMorgan Chase Bank, N.A. and others for an initial amount of $650 million in a new ABL credit facility replacing G - III’s existing $450 million ABL credit facility and $350 million in a 6 - year term loan · $75 million 6½ year Seller Note · $75 million of newly issued G - III common stock to LVMH · Post - close, G - III expected to have significant cash flow generation capabilities from existing operations to enable deleveraging · Current valuation based on the potential of the brand, distribution enhancements and product launches planned in the next 12 - 18 months, in addition to turnaround measures taken by previous owners Due Diligence · Conducted significant due diligence over 4 months to ensure that DKI was the best fit for our business Key Conditions & Timing · Expected closing by early 2017 · Subject to certain closing conditions 3

63 106 133 240 224 210 234 182 134 216 184 170 140 136 136 232 232 232 115 76 82 DKI is a Powerful Iconic Global Brand 255 255 255 0 0 0 255 255 255 189 187 187 140 136 136 68 69 71 0 0 0 189 187 187 232 232 232 158 135 140 0 56 107 240 224 210 173 91 99 239 165 84 247 148 30 234 182 134 232 209 195 255 204 204 211 186 89 216 184 170 202 152 82 28 117 188 126 169 207 0 83 158 63 106 133 115 76 82 240 224 210 234 182 134 216 184 170 140 136 136 232 232 232 · Established in 1984, Donna Karan International has a stable of one of the world’s most iconic portfolios of fashion brands, including Donna Karan, DKNY and DKNY Jeans · Designs, sources, markets, retails, and distributes collections of women’s and men’s clothing, sportswear, accessories and shoes under the Donna Karan and DKNY brand names · DKNY will generate ~$300 million in sales in 2016; reduced from over ~$500 million in 2015 · Operates three segments: · Wholesale (53% of 2016E Net Sales): Maintains partnerships with Neiman Marcus, Bloomingdale’s, Nordstrom, Lord & Taylor, Saks Fifth Avenue, Harrods and Harvey Nichols, as well as best in class international distributors · Retail (35% of 2016E Net Sales) : By year end 2016E, will operate approximately 45 stores, primarily outlets · Royalties (12% of 2016E Net Sales) : Strong relationships with category leading license partners, including Estée Lauder, Fossil, Hanes and Luxottica · Business at key inflection point · In 2014, LVMH announced the appointment of Caroline Brown, former President of Carolina Herrera, effective January 2015 · In June 2015, Donna Karan stepped down from her role as Chief Designer and Dao - Yi Chow and Maxwell Osborne of the Public School label were named Donna Karan NY Creative Directors · Over the course of the last year and a half, LVMH took significant steps to reposition and elevate the brand and meaningfully reduce overhead costs including: · Eliminating unprofitable stores · Limiting channels of distribution by significantly reducing sales to off price and club accounts 4

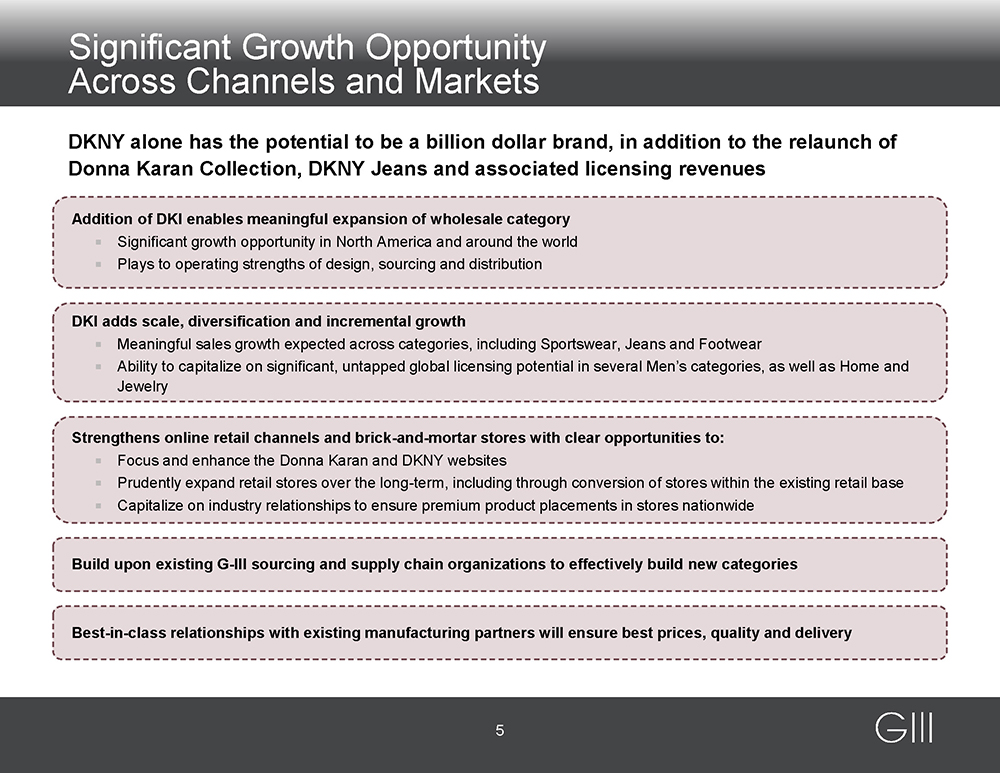

63 106 133 240 224 210 234 182 134 216 184 170 140 136 136 232 232 232 115 76 82 Addition of DKI enables meaningful expansion of wholesale category · Significant growth opportunity in North America and around the world · Plays to operating strengths of design, sourcing and distribution DKNY alone has the potential to be a billion dollar brand, in addition to the relaunch of Donna Karan Collection, DKNY Jeans and associated licensing revenues Significant Growth Opportunity Across Channels and Markets DKI adds scale, diversification and incremental growth · M eaningful sales growth expected across categories, including Sportswear, Jeans and Footwear · Ability to capitalize on significant, untapped global licensing potential in several Men’s categories, as well as Home and Jewelry Strengthens online retail channels and brick - and - mortar stores with clear opportunities to: · Focus and enhance the Donna Karan and DKNY websites · Prudently expand retail stores over the long - term, including through conversion of stores within the existing retail base · Capitalize on industry relationships to ensure premium product placements in stores nationwide Build upon existing G - III sourcing and supply chain organizations to effectively build new categories Best - in - class relationships with existing manufacturing partners will ensure best prices, quality and delivery 5

63 106 133 240 224 210 234 182 134 216 184 170 140 136 136 232 232 232 115 76 82 DKI Enhances and Complements our Global Brand Portfolio · Great fit along - side G - III’s other powerful brands: · Calvin Klein: Modern American minimalist ($1.5 billion annual sales potential ) · Tommy Hilfiger: American classic ($1+ billion annual sales potential) · Karl Lagerfeld: Parisian chic ($500 million annual sales potential ) · Donna Karan: Aspirational luxury · DKNY: City elegant ($1 billion annual sales potential) · Vilebrequin: Status resort ($250 million annual sales potential ) · Brings increased scale, channel diversification, and incremental growth to G - III · Further diversifies G - III’s sales distribution by broadening non - licensed sales G - III is committed to building all of its brands and has a proven track record of doing so 6

63 106 133 240 224 210 234 182 134 216 184 170 140 136 136 232 232 232 115 76 82 Demonstrated Track Record of Acquiring, Managing and Integrating Businesses Adding new categories and brands to diversify G - III’s portfolio is at the heart of its growth strategy G - III has grown from $1.4 billion to $2.5 billion in global sales over the past 5 years and DKI will be a significant driver of future growth Prior actions at DKI have repositioned the brand for future growth , creating stronger foundation from which to grow and expand margins · Poor performing stores closed and distribution to off - price and club channels significantly reduced · LVMH undertook a significant restructuring in 2015 / 2016 and incurred related costs Strong track record of developing new growth opportunities in well - recognized brands · Built Calvin Klein Women’s to a $1 billion business · Successfully launched Karl Lagerfeld and introduced Tommy Hilfiger women’s product in the U.S. · Recently expanded license for Tommy Hilfiger includes women’s sportswear, suit separates, performance and denim in the U.S. and Canada Demonstrated ability to grow and diversify businesses across categories · Wholesale business continues to perform well · Strong infrastructure for apparel, handbags and shoes · Launched ecommerce initiative across multiple brands 7

63 106 133 240 224 210 234 182 134 216 184 170 140 136 136 232 232 232 115 76 82 2005 2008 2007 2015 2012 2014 2016 Joint Venture Eight acquisitions, and one joint venture, over the last eleven years – successful in broadening via product offerings, geographic reach and channel diversification Acquired both brands in May 2007 Acquired in February 2008 Acquired in July 2008 Acquired in August 2012 Acquired in November 2013 Announced acquisition in July 2016 Entered into a joint venture; acquired 49% ownership in the North American JV for consumer products and apparel Expanded partnership through the acquisition of a ~19% minority interest in the parent entity Acquired Licenses: Over a Decade of Successful Brand Integration 8

63 106 133 240 224 210 234 182 134 216 184 170 140 136 136 232 232 232 115 76 82 ($10) $55 $105 2017E 2018E 2019E ($ in millions) (3% ) 10% 14% % Margin Preliminary DKI Financial Targets $325 $550 $750 2017E 2018E 2019E ($ in millions) Total Revenues (1) (2) Operating Income (1) ___________________________ Note: Assumes February 1, 2017 transaction close. 1. Reflects fiscal year ending January 31 of the following year. 2. Includes royalty revenues. G - III has developed financial targets for DKI based on extensive due diligence and a bottoms - up approach to the DKI operating model 8 % 69% 36% % Growth 9

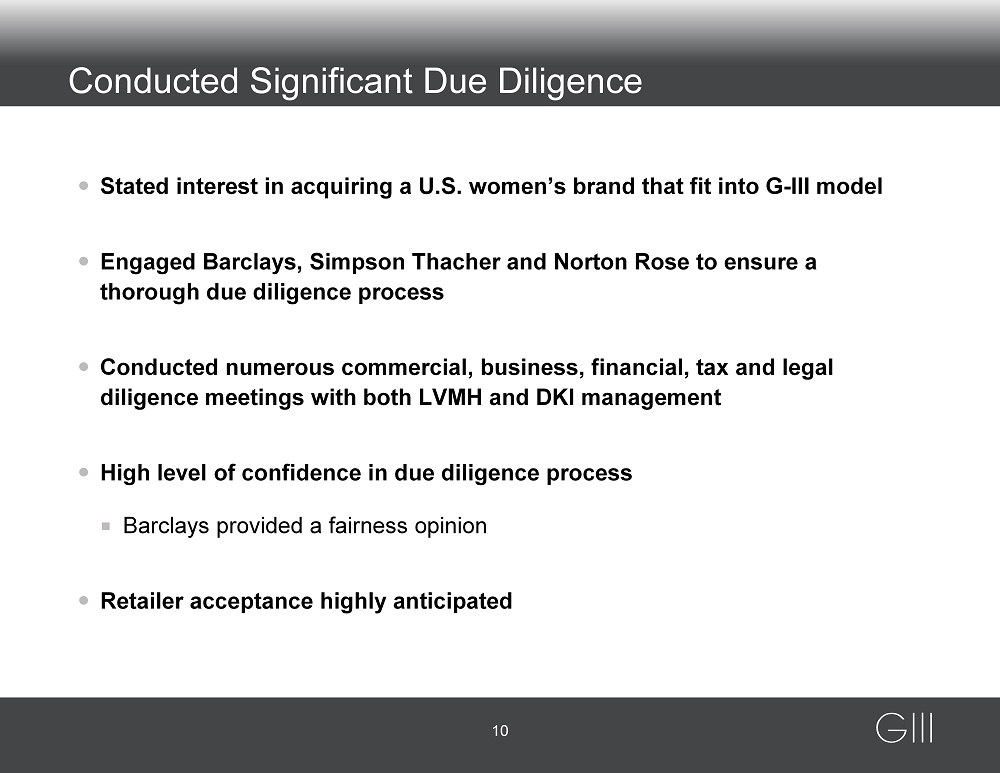

Conducted Significant Due Diligence · Stated interest in acquiring a U.S. women’s brand that fit into G - III model · Engaged Barclays, Simpson Thacher and Norton Rose to ensure a thorough due diligence process · Conducted numerous commercial, business, financial, tax and legal diligence meetings with both LVMH and DKI management · High level of confidence in due diligence process · Barclays provided a fairness opinion · Retailer acceptance highly anticipated 10

63 106 133 240 224 210 234 182 134 216 184 170 140 136 136 232 232 232 115 76 82 Conducted Significant Due Diligence · Stated interest in acquiring a U.S. women’s brand that fit into G - III model · Engaged Barclays, Simpson Thacher, Ernst & Young and Norton Rose to ensure a thorough due diligence process · Conducted numerous commercial, business, financial, tax and legal diligence meetings with both LVMH and DKI management · High level of confidence in due diligence process · Barclays provided a fairness opinion; E&Y provided quality of earnings report · Retailer acceptance highly anticipated 10

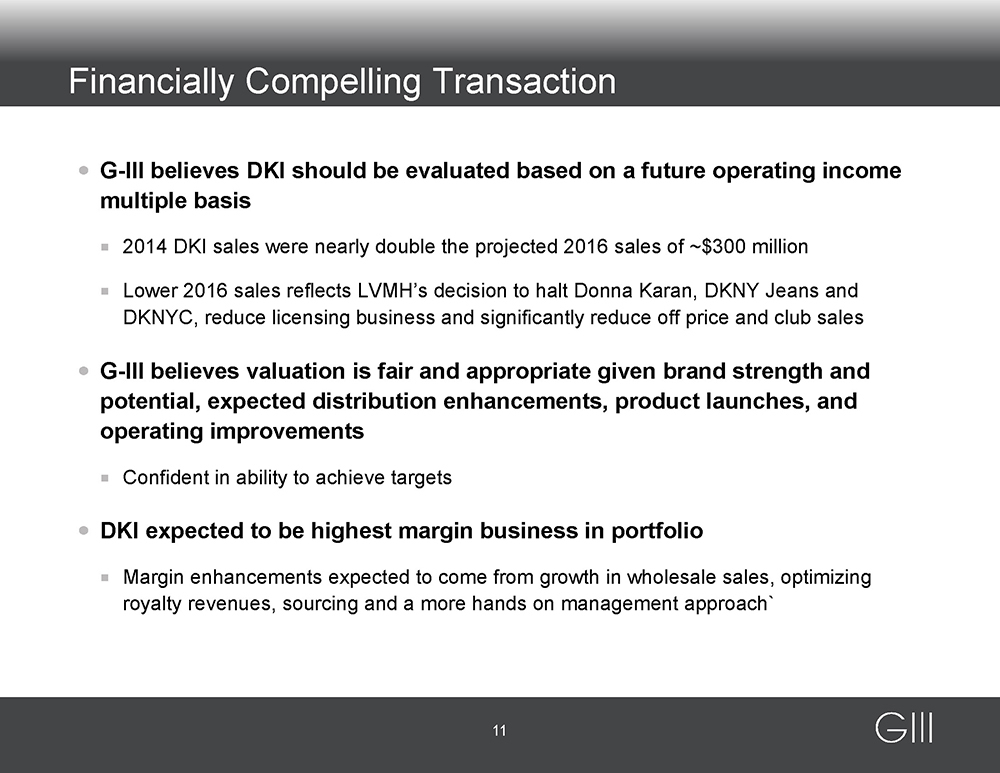

63 106 133 240 224 210 234 182 134 216 184 170 140 136 136 232 232 232 115 76 82 Financially Compelling Transaction · G - III believes DKI should be evaluated based on a future operating income multiple basis · 2014 DKI sales were nearly double the projected 2016 sales of ~$300 million · Lower 2016 sales reflects LVMH’s decision to halt Donna Karan, DKNY Jeans and DKNYC, reduce licensing business and significantly reduce off price and club sales · G - III believes valuation is fair and appropriate given brand strength and potential, expected distribution enhancements, product launches, and operating improvements · Confident in ability to achieve targets · DKI expected to be highest margin business in portfolio · Margin enhancements expected to come from growth in wholesale sales, optimizing royalty revenues, sourcing and a more hands on management approach` 11

63 106 133 240 224 210 234 182 134 216 184 170 140 136 136 232 232 232 115 76 82 Conclusion · Iconic power brand with deep heritage, global recognition · Significant growth potential leveraging G - III’s core competencies, strong track record and industry reputation · Complementary addition to G - III’s portfolio of owned and licensed brands · Demonstrated integration capabilities · Attractive valuation based on intrinsic value of brand / business and forward operating income multiple · LVMH’s investment through $75 million of G - III common stock received as part of the purchase price is a strong indicator of support of G - III 12