Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - QTS Realty Trust, Inc. | v444967_ex99-1.htm |

| 8-K - FORM 8-K - QTS Realty Trust, Inc. | v444967_8k.htm |

Exhibit 99.2

| Table of Contents |

| Overview | |

| Company Profile | 3 |

| Financial Statements | |

| Combined Consolidated Balance Sheets | 4 |

| Combined Consolidated Statements of Operations and Comprehensive Income (Loss) | 5 |

| Summary of Financial Data | 7 |

| Reconciliations of Return on Invested Capital (ROIC) | 9 |

| Implied Enterprise Value and Weighted Average Shares | 10 |

| Operating Portfolio | |

| Data Center Properties | 11 |

| Redevelopment Costs Summary | 12 |

| Redevelopment Summary | 13 |

| NOI by Facility and Capital Expenditure Summary | 14 |

| Leasing Statistics – Signed Leases | 15 |

| Leasing Statistics – Renewed Leases and Rental Churn | 17 |

| Leasing Statistics – Commenced Leases | 18 |

| Lease Expirations | 19 |

| Largest Customers | 20 |

| Industry Segmentation | 21 |

| Product Diversification | 22 |

| Capital Structure | |

| Debt Summary and Debt Maturities | 23 |

| Interest Summary | 24 |

| Appendix | 25 |

| 1 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

Forward Looking Statements

Some of the statements contained in this document constitute forward-looking statements within the meaning of the federal securities laws. Forward-looking statements relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. In particular, statements pertaining to the Company’s capital resources, portfolio performance and results of operations contain forward-looking statements. Likewise, all of the statements regarding anticipated growth in funds from operations and anticipated market conditions are forward-looking statements. In some cases, you can identify forward-looking statements by the use of forward-looking terminology such as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” or “potential” or the negative of these words and phrases or similar words or phrases which are predictions of or indicate future events or trends and which do not relate solely to historical matters. You can also identify forward-looking statements by discussions of strategy, plans or intentions.

The forward-looking statements contained in this document reflect the Company’s current views about future events and are subject to numerous known and unknown risks, uncertainties, assumptions and changes in circumstances that may cause actual results to differ significantly from those expressed in any forward-looking statement. The Company does not guarantee that the transactions and events described will happen as described (or that they will happen at all). The following factors, among others, could cause actual results and future events to differ materially from those set forth or contemplated in the forward-looking statements: adverse economic or real estate developments in the Company’s markets or the technology industry; global, national and local economic conditions; risks related to our international operations; difficulties in identifying properties to acquire and completing acquisitions; the Company’s failure to successfully develop, redevelop and operate acquired properties or lines of business, including data centers acquired in the Company’s acquisition of Carpathia Hosting, Inc.; significant increases in construction and development costs; the increasingly competitive environment in which the Company operates; defaults on, or termination or non-renewal of, leases by customers; increased interest rates and operating costs, including increased energy costs; financing risks, including the Company’s failure to obtain necessary outside financing; decreased rental rates or increased vacancy rates; dependence on third parties to provide Internet, telecommunications and network connectivity to the Company’s data centers; the Company’s failure to qualify and maintain its qualification as a real estate investment trust; environmental uncertainties and risks related to natural disasters; financial market fluctuations; and changes in real estate and zoning laws, revaluations for tax purposes and increases in real property tax rates.

While forward-looking statements reflect the Company’s good faith beliefs, they are not guarantees of future performance. The Company disclaims any obligation to publicly update or revise any forward-looking statement to reflect changes in underlying assumptions or factors, of new information, data or methods, future events or other changes. For a further discussion of these and other factors that could cause the Company’s future results to differ materially from any forward-looking statements, see the section entitled “Risk Factors” in the Company’s Annual Report on Form 10-K for the year ended December 31, 2015 and other periodic reports the Company files with the Securities and Exchange Commission.

| 2 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Company Profile |

| 3 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Combined Consolidated Balance Sheets |

(in thousands)

| June 30, | December 31, | |||||||

| 2016 | 2015 | |||||||

| (unaudited) | ||||||||

| ASSETS | ||||||||

| Real Estate Assets | ||||||||

| Land | $ | 64,568 | $ | 57,112 | ||||

| Buildings, improvements and equipment | 1,393,920 | 1,180,386 | ||||||

| Less: Accumulated depreciation | (274,145 | ) | (239,936 | ) | ||||

| 1,184,343 | 997,562 | |||||||

| Construction in progress | 316,797 | 345,655 | ||||||

| Real Estate Assets, net | 1,501,140 | 1,343,217 | ||||||

| Cash and cash equivalents | 12,776 | 8,804 | ||||||

| Rents and other receivables, net | 35,226 | 28,233 | ||||||

| Acquired intangibles, net (1) | 142,848 | 115,702 | ||||||

| Deferred costs, net (2) (3) | 34,921 | 30,042 | ||||||

| Prepaid expenses | 8,947 | 6,502 | ||||||

| Goodwill (1) | 173,843 | 181,738 | ||||||

| Other assets, net (4) | 36,984 | 33,101 | ||||||

| TOTAL ASSETS | $ | 1,946,685 | $ | 1,747,339 | ||||

| LIABILITIES | ||||||||

| Unsecured credit facility, net (3) | $ | 493,255 | $ | 520,956 | ||||

| Senior notes, net of discount and debt issuance costs (3) | 291,521 | 290,852 | ||||||

| Capital lease and lease financing obligations | 43,440 | 49,761 | ||||||

| Accounts payable and accrued liabilities | 63,963 | 95,924 | ||||||

| Dividends and distributions payable | 19,692 | 15,378 | ||||||

| Advance rents, security deposits and other liabilities | 20,923 | 18,798 | ||||||

| Deferred income taxes (1) | 19,742 | 18,813 | ||||||

| Deferred income | 18,306 | 16,991 | ||||||

| TOTAL LIABILITIES | 970,842 | 1,027,473 | ||||||

| EQUITY | ||||||||

| Common stock, $0.01 par value, 450,133,000 shares authorized, 47,864,968 and 41,225,784 shares issued and outstanding as of June 30, 2016 and December 31, 2015, respectively | 478 | 412 | ||||||

| Additional paid-in capital | 928,313 | 670,275 | ||||||

| Accumulated dividends in excess of earnings | (73,883 | ) | (52,732 | ) | ||||

| Total stockholders’ equity | 854,908 | 617,955 | ||||||

| Noncontrolling interests | 120,935 | 101,911 | ||||||

| TOTAL EQUITY | 975,843 | 719,866 | ||||||

| TOTAL LIABILITIES AND EQUITY | $ | 1,946,685 | $ | 1,747,339 | ||||

| (1) | During the second quarter of 2016, the purchase price allocation associated with the acquisition of Carpathia Hosting, Inc. (“Carpathia”) was finalized. The primary adjustments to the purchase price allocation made during the first and second quarters of 2016 consisted of a $14.7 million increase in intangible assets, a $6.0 million increase in deferred tax liability and a reduction in goodwill of $7.9 million. |

| (2) | As of June 30, 2016 and December 31, 2015, deferred costs, net, included $5.5 million and $6.3 million of deferred financing costs net of amortization, respectively, $26.8 million and $21.0 million of deferred leasing costs net of amortization, respectively, and $2.6 million and $2.8 million, net of amortization, related to a leasing arrangement at the Company’s Princeton facility, respectively. |

| (3) | Debt issuance costs, net, related to the Senior Notes and term loan portion of the Company’s unsecured credit facility aggregating $9.3 million and $10.2 million at June 30, 2016 and December 31, 2015, respectively, have been netted against the related debt liability line items for both periods presented, as required by recently issued accounting guidance. |

| (4) | As of June 30, 2016 and December 31, 2015, other assets, net, primarily included $29.2 million and $25.9 million of corporate fixed assets, respectively, primarily relating to construction of corporate offices, leasehold improvements and product related assets. |

| 4 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Combined Consolidated Statements of Operations and Comprehensive Income |

| (unaudited and in thousands except share and per share data) |

The following financial data for the three and six months ended June 30, 2016 includes the operating results of the Piscataway, New Jersey facility (the “Piscataway facility”) for the period June 6, 2016 (the date the Company acquired the facility) through June 30, 2016.

| Three Months Ended | Six Months Ended | |||||||||||||||||||

| June 30, | March 31, | June 30, | June 30, | |||||||||||||||||

| 2016 | 2016 | 2015 | 2016 | 2015 | ||||||||||||||||

| Revenues: | ||||||||||||||||||||

| Rental | $ | 71,670 | $ | 68,426 | $ | 52,193 | $ | 140,096 | $ | 101,526 | ||||||||||

| Recoveries from customers | 6,168 | 5,435 | 5,582 | 11,603 | 11,246 | |||||||||||||||

| Cloud and managed services | 17,015 | 18,890 | 8,220 | 35,905 | 14,015 | |||||||||||||||

| Other (1) | 3,834 | 2,017 | 2,122 | 5,851 | 2,716 | |||||||||||||||

| Total revenues | 98,687 | 94,768 | 68,117 | 193,455 | 129,503 | |||||||||||||||

| Operating expenses: | ||||||||||||||||||||

| Property operating costs | 32,646 | 31,781 | 22,031 | 64,427 | 41,367 | |||||||||||||||

| Real estate taxes and insurance | 2,020 | 1,740 | 1,474 | 3,760 | 2,959 | |||||||||||||||

| Depreciation and amortization | 30,355 | 28,639 | 18,062 | 58,994 | 34,305 | |||||||||||||||

| General and administrative (2) | 21,608 | 20,286 | 14,615 | 41,894 | 28,453 | |||||||||||||||

| Transaction and integration costs (3) | 3,833 | 2,087 | 4,669 | 5,920 | 4,774 | |||||||||||||||

| Total operating expenses | 90,462 | 84,533 | 60,851 | 174,995 | 111,858 | |||||||||||||||

| Operating income | 8,225 | 10,235 | 7,266 | 18,460 | 17,645 | |||||||||||||||

| Other income and expense: | ||||||||||||||||||||

| Interest income | 2 | - | 1 | 2 | 1 | |||||||||||||||

| Interest expense | (4,874 | ) | (5,981 | ) | (4,799 | ) | (10,855 | ) | (10,141 | ) | ||||||||||

| Other expense, net (4) | - | - | (83 | ) | - | (83 | ) | |||||||||||||

| Income before taxes | 3,353 | 4,254 | 2,385 | 7,607 | 7,422 | |||||||||||||||

| Tax benefit of taxable REIT subsidiaries (5) | 2,454 | 2,605 | 3,135 | 5,059 | 3,135 | |||||||||||||||

| Net income | 5,807 | 6,859 | 5,520 | 12,666 | 10,557 | |||||||||||||||

| Net income attributable to noncontrolling interests (6) | (707 | ) | (970 | ) | (888 | ) | (1,677 | ) | (1,843 | ) | ||||||||||

| Net income attributable to QTS Realty Trust, Inc. | $ | 5,100 | $ | 5,889 | $ | 4,632 | $ | 10,989 | $ | 8,714 | ||||||||||

| Net income per share attributable to common shares: | ||||||||||||||||||||

| Basic | $ | 0.11 | $ | 0.14 | $ | 0.13 | $ | 0.25 | $ | 0.26 | ||||||||||

| Diluted | 0.10 | 0.14 | 0.12 | 0.24 | 0.25 | |||||||||||||||

| Weighted average common shares outstanding: | ||||||||||||||||||||

| Basic | 47,783,093 | 41,292,445 | 36,668,755 | 44,537,769 | 33,996,467 | |||||||||||||||

| Diluted | 55,574,545 | 48,973,851 | 44,444,104 | 52,274,198 | 41,867,944 | |||||||||||||||

| 5 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| (1) | Other revenue - Includes straight line rent, sales of scrap metals and other unused materials and various other income items. Straight line rent was $3.5 million, $1.9 million and $1.4 million for the three months ended June 30, 2016, March 31, 2016 and June 30, 2015, respectively. Straight line rent was $5.4 million and $1.8 million for the six months ended June 30, 2016 and 2015, respectively. |

| (2) | General and administrative expenses - Includes personnel costs, sales and marketing costs, professional fees, travel costs, product investment costs and other corporate general and administrative expenses. General and administrative expenses were 21.9%, 21.4%, and 21.5% of total revenues for the three month periods ended June 30, 2016, March 31, 2016 and June 30, 2015, respectively. General and administrative expenses were 21.7% and 22.0% of total revenues for the six month periods ended June 30, 2016 and 2015, respectively. |

| (3) | Transaction and integration costs - For the three month periods ended June 30, 2016 and June 30, 2015, the Company recognized $0.8 million, and $4.3 million, respectively, related to the examination of actual and potential acquisitions. Transaction costs were $0.8 million and $4.4 million for the six months ended June 30, 2016 and 2015, respectively. The Company also recognized $3.0 million, $2.1 million and $0.4 million in integration costs for the three month periods ended June 30, 2016, March 31, 2016 and June 30, 2015. These costs include various costs to integrate QTS and Carpathia, including consulting fees, costs to consolidate office space and costs which are currently duplicated, but will be eliminated in the near future. Integration costs were $5.1 million and $0.4 million for the six months ended June 30, 2016 and 2015, respectively. |

| (4) | Other expense, net - Generally includes write offs of unamortized deferred financing costs associated with the early extinguishment of certain debt instruments. |

| (5) | Tax benefit of taxable REIT subsidiaries – For the three months ended June 30, 2016, March 31, 2016 and June 30, 2015, the Company recorded an approximate $2.5 million, $2.6 million and $3.1 million deferred tax benefit, respectively. The current year amounts related to recorded operating losses which include certain transaction and integration costs. The prior year amount related to the reversal of valuation allowances of deferred tax assets which was a result of the purchase of Carpathia. The Company recorded $5.1 million and $3.1 million in deferred tax benefits for the six months ended June 30, 2016 and 2015, respectively. |

| (6) | Noncontrolling interest – The noncontrolling ownership interest of QualityTech, LP was 12.4% and 14.6% as of June 30, 2016 and 2015, respectively, with the decrease primarily attributable to the equity issuance in April 2016. |

| 6 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Summary of Financial Data |

(in thousands, except operating portfolio statistics data and per share data)

This summary includes certain non-GAAP financial measures that management believes are helpful in understanding the Company’s business, as further described in the Appendix.

| Three Months Ended | Six Months Ended | |||||||||||||||||||

| June 30, | March 31, | June 30, | June 30, | |||||||||||||||||

| 2016 | 2016 | 2015 | 2016 | 2015 | ||||||||||||||||

| Summary of Results | ||||||||||||||||||||

| Total revenue | $ | 98,687 | $ | 94,768 | $ | 68,117 | $ | 193,455 | $ | 129,503 | ||||||||||

| Net income | $ | 5,807 | $ | 6,859 | $ | 5,520 | 12,666 | 10,557 | ||||||||||||

| Fully diluted weighted average shares | 55,575 | 48,974 | 44,444 | $ | 52,274 | $ | 41,868 | |||||||||||||

| Net income per basic share | $ | 0.11 | $ | 0.14 | $ | 0.13 | $ | 0.25 | $ | 0.26 | ||||||||||

| Net income per diluted share | $ | 0.10 | $ | 0.14 | $ | 0.12 | $ | 0.24 | $ | 0.25 | ||||||||||

| Other Data | ||||||||||||||||||||

| FFO | $ | 32,216 | $ | 31,728 | $ | 21,845 | $ | 63,944 | $ | 41,184 | ||||||||||

| Operating FFO | $ | 34,866 | $ | 33,067 | $ | 23,422 | $ | 67,933 | $ | 42,866 | ||||||||||

| Operating FFO per share | $ | 0.63 | $ | 0.68 | $ | 0.53 | $ | 1.30 | $ | 1.02 | ||||||||||

| Recognized MRR in the period | $ | 84,506 | $ | 83,162 | $ | 57,953 | $ | 167,668 | $ | 110,417 | ||||||||||

| MRR (at period end) | $ | 28,872 | $ | 27,480 | $ | 25,473 | $ | 28,872 | $ | 25,473 | ||||||||||

| EBITDA | $ | 38,580 | $ | 38,874 | $ | 25,245 | $ | 77,454 | $ | 51,867 | ||||||||||

| Adjusted EBITDA | $ | 45,613 | $ | 43,011 | $ | 31,828 | $ | 88,624 | $ | 59,862 | ||||||||||

| NOI | $ | 64,021 | $ | 61,247 | $ | 44,612 | $ | 125,268 | $ | 85,177 | ||||||||||

| NOI as a % of revenue | 64.9 | % | 64.6 | % | 65.5 | % | 64.8 | % | 65.8 | % | ||||||||||

| Adjusted EBITDA as a % of revenue | 46.2 | % | 45.4 | % | 46.7 | % | 45.8 | % | 46.2 | % | ||||||||||

| General and administrative expenses as a % of revenue | 21.9 | % | 21.4 | % | 21.5 | % | 21.7 | % | 22.0 | % | ||||||||||

| Annualized ROIC | 15.1 | % | 15.6 | % | 15.8 | % | 15.3 | % | 15.3 | % | ||||||||||

| June 30, | December 31, | |||||||

| Balance Sheet Data | 2016 | 2015 | ||||||

| Real estate at cost | $ | 1,775,285 | $ | 1,583,153 | ||||

| Net investment in real estate | 1,501,140 | 1,343,217 | ||||||

| Total assets | 1,946,685 | 1,747,339 | ||||||

| Total debt | 839,440 | (1) | 873,763 | (1) | ||||

| Debt to last quarter annualized Adjusted EBITDA | 4.6 | x | 5.3 | x | ||||

| Debt to undepreciated real estate assets | 47.3 | %(1) | 55.2 | %(1) | ||||

| Debt to Implied Enterprise Value | 21.2 | %(1) | 28.4 | %(1) | ||||

| (1) | In accordance with recent accounting changes, as noted on page 4, certain debt issuance costs have been reclassified from assets to liabilities in the prior period presented above. In addition, the Company has excluded the Senior Note discount and associated debt issuance costs from the Total Debt line item for both periods presented. As a result, the amounts referenced above represent the full amount of debt that will be repaid. |

| 7 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| June 30, | December 31, | |||||||

| 2016 | 2015 | |||||||

| Operating Portfolio Statistics | ||||||||

| Built out square footage: | ||||||||

| Raised floor | 1,283,941 | 1,118,506 | ||||||

| Leasable raised floor (1) | 1,012,203 | 839,356 | ||||||

| Leased raised floor | 890,477 | 761,166 | ||||||

| Total Raw Shell: | ||||||||

| Total | 5,250,927 | 4,878,342 | ||||||

| Basis-of-design raised floor space (1) | 2,360,605 | 2,184,631 | ||||||

| Data center properties | 25 | 24 | ||||||

| Basis of design raised floor % developed | 54.4 | % | 51.2 | % | ||||

| Data center % occupied | 88.0 | % | 90.7 | % | ||||

| Data center raised floor % wholly-owned | 87.4 | %(2) | 85.5 | %(2) | ||||

| (1) | See definition in Appendix. |

| (2) | Amounts assume the Santa Clara facility is not wholly-owned, as it is subject to a long-term ground lease. Had the Santa Clara facility been included as wholly-owned, the percentage of data center raised floor that is wholly-owned by the Company would be 91.8% and 90.5% at June 30, 2016 and December 31, 2015, respectively. |

| 8 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Reconciliations of Return on Invested Capital (ROIC) |

(unaudited and in thousands)

Return on Invested Capital (“ROIC”) is a non-GAAP measure that provides additional information to users of the financial statements. Management believes ROIC is a helpful metric for users of the financial statements to gauge the Company's performance against the capital it has invested.

| Return on Invested Capital (ROIC) | Three Months Ended | Six Months Ended | ||||||||||||||||||

| June 30, | March 31, | June 30, | June 30, | |||||||||||||||||

| 2016 | 2016 | 2015 | 2016 | 2015 | ||||||||||||||||

| NOI (1) | $ | 64,021 | $ | 61,247 | $ | 49,112 | $ | 125,268 | $ | 89,677 | ||||||||||

| Annualized NOI | 256,084 | 244,988 | 196,448 | 250,536 | 179,354 | |||||||||||||||

| Average undepreciated real estate assets and other net fixed assets placed in service (2) | 1,692,551 | 1,568,645 | 1,243,782 | 1,640,984 | 1,170,135 | |||||||||||||||

| Annualized ROIC | 15.1 | % | 15.6 | % | 15.8 | % | 15.3 | % | 15.3 | % | ||||||||||

| (1) | Includes facility level G&A allocation charges of 4% of cash revenue for all facilities, with the exception of the leased facilities acquired in 2015, which include G&A expense allocation charges of 10% of cash revenue. These allocated charges aggregated to $5.1 million, $5.0 million and $2.7 million for the three month periods ended June 30, 2016, March 31, 2016 and June 30, 2015, respectively. |

| (2) | Calculated by using average quarterly balance of each account. |

| Calculation of Average Undepreciated Real Estate Assets and other Net Fixed Assets Placed in Service | As of | As of | ||||||||||||||||||

| Undepreciated Real Estate Assets and other | June 30, | March 31, | June 30, | June 30, | June 30, | |||||||||||||||

| Net Fixed Assets Placed in Service | 2016 | 2016 | 2015 | 2016 | 2015 | |||||||||||||||

| Real Estate Assets, net | $ | 1,501,140 | $ | 1,384,180 | $ | 1,241,151 | $ | 1,501,140 | $ | 1,241,151 | ||||||||||

| Less: Construction in progress | (316,797 | ) | (340,511 | ) | (320,885 | ) | (316,797 | ) | (320,885 | ) | ||||||||||

| Plus: Accumulated depreciation | 274,145 | 255,344 | 205,284 | 274,145 | 205,284 | |||||||||||||||

| Plus: Goodwill | 173,843 | 171,679 | 173,237 | 173,843 | 173,237 | |||||||||||||||

| Plus: Other fixed assets, net | 15,698 | 13,185 | 11,400 | 15,698 | 11,400 | |||||||||||||||

| Plus: Acquired intangibles, net (1) | 108,194 | 90,070 | 90,173 | 108,194 | 90,173 | |||||||||||||||

| Plus: Leasing Commissions, net | 29,438 | 25,494 | 22,735 | 29,438 | 22,735 | |||||||||||||||

| Total as of period end | $ | 1,785,661 | $ | 1,599,441 | $ | 1,423,095 | $ | 1,785,661 | $ | 1,423,095 | ||||||||||

| Average undepreciated real estate assets and other net fixed assets as of reporting period (2) | $ | 1,692,551 | $ | 1,568,645 | $ | 1,243,782 | $ | 1,640,984 | $ | 1,170,135 | ||||||||||

| (1) | Net of acquired intangible liabilities and deferred tax liabilities. In addition, for the period ended March 31, 2016, there was a reclassification between goodwill and acquired intangibles. |

| (2) | Calculated by using average quarterly balance of each account. |

| 9 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Implied Enterprise Value and Weighted Average Shares |

| Implied Enterprise Value as of June 30, 2016: | ||||

| Total Shares Outstanding: | ||||

| Class A Common Stock | 47,731,968 | |||

| Class B Common Stock | 133,000 | |||

| Total Shares Outstanding | 47,864,968 | |||

| Units of Limited Partnership (1) | 7,423,473 | |||

| Options to purchase Class A Common Stock (2) | 454,082 | |||

| Fully Diluted Total Shares and Units of Limited Partnership outstanding as of June 30, 2016 | 55,742,523 | |||

| Share price as of June 30, 2016 | $ | 55.98 | ||

| Market equity capitalization (in thousands) | $ | 3,120,466 | ||

| Debt (in thousands) | 839,440 | (3) | ||

| Implied Enterprise Value (in thousands) | $ | 3,959,906 |

| (1) | Includes 652,529 of operating partnership units representing the “in the money” value of Class O LTIP units on an “as if” converted basis as of June 30, 2016. |

| (2) | Represents options to purchase 454,082 shares of Class A Common Stock of QTS Realty Trust, Inc. representing the “in the money” value of options on an “as if” converted basis as of June 30, 2016. |

| (3) | Excludes the Senior Note discount and all debt issuance costs reflected as liabilities at June 30, 2016. |

The following table presents the weighted average fully diluted shares for the three and six months ended June 30, 2016:

| Three Months Ended | Six Months Ended | |||||||

| June 30, 2016 | June 30, 2016 | |||||||

| Weighted average shares outstanding - basic | 47,783,093 | 44,537,769 | ||||||

| Effect of Class A and Class RS partnership units (1) | 6,794,021 | 6,797,482 | ||||||

| Effect of Class O units on as "as if" converted basis (1) | 598,342 | 579,900 | ||||||

| Effect of options to purchase Class A common stock on an "as if" converted basis (2) | 399,089 | 359,047 | ||||||

| Weighted average shares outstanding - diluted | 55,574,545 | 52,274,198 | ||||||

| (1) | The Class A units, Class RS units and Class O units represent limited partnership interests in the Operating Partnership. |

| (2) | The weighted average share price for the three and six months ended June 30, 2016 was $51.24 and $47.89, respectively. |

| 10 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Data Center Properties |

(in thousands, except NRSF data)

The following table presents an overview of the portfolio of data center properties that the Company owns or leases, referred to herein as our data center properties, based on information as of June 30, 2016:

| Operating Net Rentable Square Feet (Operating NRSF) (3) | ||||||||||||||||||||||||||||||||||||||||||

| Property | Year Acquired (1) | Gross Square | Raised Floor (4) | Office & Other (5) | Supporting Infrastructure (6) | Total | % Occupied (7) | Annualized Rent (8) | Available Utility Power (MW) (9) | Basis of Design ("BOD") NRSF | Current Raised Floor as a % of BOD | |||||||||||||||||||||||||||||||

| Richmond, VA | 2010 | 1,318,353 | 167,309 | 51,093 | 178,854 | 397,256 | 88.1 | % | $ | 35,510,868 | 110 | 557,309 | 30.0 | % | ||||||||||||||||||||||||||||

| Atlanta, GA (Metro) | 2006 | 968,695 | 452,986 | 36,953 | 331,426 | 821,365 | 94.1 | % | $ | 90,118,528 | 72 | 527,186 | 85.9 | % | ||||||||||||||||||||||||||||

| Dallas-Fort Worth, TX | 2013 | 698,000 | 95,614 | 6,981 | 77,425 | 180,020 | 95.3 | % | $ | 19,956,036 | 140 | 292,000 | 32.7 | % | ||||||||||||||||||||||||||||

| Princeton, NJ | 2014 | 553,930 | 58,157 | 2,229 | 111,405 | 171,791 | 100.0 | % | $ | 9,702,840 | 22 | 158,157 | 36.8 | % | ||||||||||||||||||||||||||||

| Suwanee, GA | 2005 | 369,822 | 185,422 | 8,697 | 107,128 | 301,247 | 81.3 | % | $ | 56,471,954 | 36 | 208,008 | 89.1 | % | ||||||||||||||||||||||||||||

| Chicago, IL | 2014 | 317,000 | - | - | - | - | - | % | $ | - | 8 | 133,000 | - | % | ||||||||||||||||||||||||||||

| Santa Clara, CA* | 2007 | 135,322 | 55,905 | 944 | 45,094 | 101,943 | 77.9 | % | $ | 22,072,713 | 11 | 80,940 | 69.1 | % | ||||||||||||||||||||||||||||

| Jersey City, NJ** | 2006 | 122,448 | 31,503 | 14,208 | 41,901 | 87,612 | 97.1 | % | $ | 11,680,023 | 7 | 52,744 | 59.7 | % | ||||||||||||||||||||||||||||

| Sacramento, CA | 2012 | 92,644 | 54,595 | 2,794 | 23,916 | 81,305 | 46.1 | % | $ | 11,998,463 | 8 | 57,906 | 94.3 | % | ||||||||||||||||||||||||||||

| Piscataway | 2016 | 360,000 | 88,820 | 14,311 | 91,851 | 194,982 | 76.2 | % | $ | 8,914,718 | 111 | 176,000 | 50.5 | % | ||||||||||||||||||||||||||||

| Miami, FL | 2008 | 30,029 | 19,887 | - | 6,592 | 26,479 | 67.2 | % | $ | 5,295,855 | 4 | 19,887 | 100.0 | % | ||||||||||||||||||||||||||||

| Leased facilities acquired in 2015 *** | 2015 | 167,278 | 71,250 | 5,418 | 32,992 | 109,660 | 86.6 | % | $ | 73,887,964 | 20 | 94,975 | 75.0 | % | ||||||||||||||||||||||||||||

| Other | Misc | 117,406 | 2,493 | 49,337 | 23,482 | 75,312 | 60.7 | % | $ | 857,268 | 1 | 2,493 | 100.0 | % | ||||||||||||||||||||||||||||

| Total | 5,250,927 | 1,283,941 | 192,965 | 1,072,066 | 2,548,972 | 88.0 | % | $ | 346,467,230 | 550 | 2,360,605 | 54.4 | % | |||||||||||||||||||||||||||||

| (1) | Represents the year a property was acquired or, in the case of a property under lease, the year the Company’s initial lease commenced for the property. |

| (2) | With respect to the Company’s owned properties, gross square feet represents the entire building area. With respect to leased properties, gross square feet represents that portion of the gross square feet subject to our lease. This includes 292,086 square feet of QTS office and support space, which is not included in operating NRSF. |

| (3) | Represents the total square feet of a building that is currently leased or available for lease plus developed supporting infrastructure, based on engineering drawings and estimates, but does not include space held for redevelopment or space used for the Company’s own office space. |

| (4) | Represents management’s estimate of the portion of NRSF of the facility with available power and cooling capacity that is currently leased or readily available to be leased to customers as data center space based on engineering drawings. |

| (5) | Represents the operating NRSF of the facility other than data center space (typically office and storage space) that is currently leased or available to be leased. |

| (6) | Represents required data center support space, including mechanical, telecommunications and utility rooms, as well as building common areas. |

| (7) | Calculated as data center raised floor that is subject to a signed lease for which space is occupied (890,477 square feet as of June 30, 2016), divided by leasable raised floor based on the current configuration of the properties (1,012,203 square feet as of June 30, 2016), expressed as a percentage. |

| (8) | The Company defines annualized rent as MRR multiplied by 12. The Company calculates MRR as monthly contractual revenue under executed contracts as of a particular date, which includes revenue from the Company’s C1, C2 and C3 rental and cloud and managed services activities, but excludes customer recoveries, deferred set up fees, variable related revenues, non-cash revenues and other one-time revenues. MRR does not include the impact from booked-not-billed contracts as of a particular date, unless otherwise specifically noted. This amount reflects the annualized cash rental payments. It does not reflect the accounting associated with any free rent, rent abatements or future scheduled rent increases and also excludes operating expense and power reimbursements. |

| (9) | Represents installed utility power and transformation capacity that is available for use by the facility as of June 30, 2016. |

| * | Subject to long-term ground lease. |

| ** | Represents facilities that we lease. |

| *** | Includes 13 facilities. All facilities are leased, including those subject to capital leases. |

| 11 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Redevelopment Costs Summary |

(in millions, except NRSF data)

During the second quarter of 2016, the Company brought online approximately 10.8 megawatts of gross power and approximately 43,000 NRSF of raised floor and customer specific capital at its Richmond, Atlanta-Metro and Dallas-Fort Worth data centers at an aggregate cost of approximately $68 million, which excludes the recently acquired Piscataway facility. The under construction table below summarizes the Company’s outlook for development projects which it expects to complete by December 31, 2016 (in millions).

| Under Construction Costs (1) | ||||||||||||||

| Property | Actual (2) | Estimated Cost to Completion (3) | Total | Expected Completion date | ||||||||||

| Atlanta-Metro | $ | 8 | $ | 7 | $ | 15 | Q4 2016 | |||||||

| Atlanta-Suwanee | 13 | 2 | 15 | Q3 2016 | ||||||||||

| Chicago | 25 | 20 | 45 | Q3 2016 | ||||||||||

| Dallas-Fort Worth | 9 | 19 | 28 | Q4 2016 | ||||||||||

| Totals | $ | 55 | $ | 48 | $ | 103 | ||||||||

| (1) | In addition to projects currently under construction, the Company’s near-term redevelopment projects are expected to be delivered in a modular manner, and the Company currently expects to invest additional capital to complete these near term projects. The ultimate timing and completion of, and the commitment of capital to, the Company’s future redevelopment projects are within the Company’s discretion and will depend upon a variety of factors, including the actual contracts executed, availability of financing and the Company’s estimation of the future market for data center space in each particular market. |

| (2) | Actual costs under construction through June 30, 2016. In addition to the $55 million of construction costs incurred through June 30, 2016 for redevelopment expected to be completed by December 31, 2016, as of June 30, 2016 the Company had incurred $262 million of additional costs (including acquisition costs and other capitalized costs) for other redevelopment projects that are expected to be completed after December 31, 2016. |

| (3) | Represents management’s estimate of the additional costs required to complete the current NRSF under development. There may be an increase in costs if customers’ requirements exceed the Company’s current basis of design. |

| 12 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Redevelopment Summary |

(in millions, except NRSF data)

The following redevelopment table presents an overview of the Company’s redevelopment pipeline, based on information as of June 30, 2016. This table shows the Company’s ability to increase its raised floor of 1,283,941 square feet as of June 30, 2016 by approximately 1.8 times to 2.4 million square feet.

| Raised Floor NRSF | ||||||||||||||||||||

| Overview as of June 30, 2016 | ||||||||||||||||||||

| Property | Current NRSF in Service | Under Construction (1) | Future Available (2) | Basis of Design NRSF | Approximate Adjacent Acreage of Land (3) | |||||||||||||||

| Richmond | 167,309 | - | 390,000 | 557,309 | 111.1 | |||||||||||||||

| Atlanta-Metro | 452,986 | - | 74,200 | 527,186 | 6.0 | |||||||||||||||

| Dallas-Fort Worth | 95,614 | 12,500 | 183,886 | 292,000 | 29.4 | |||||||||||||||

| Princeton | 58,157 | - | 100,000 | 158,157 | 65.0 | |||||||||||||||

| Atlanta-Suwanee | 185,422 | 19,000 | 3,586 | 208,008 | 15.4 | |||||||||||||||

| Santa Clara | 55,905 | - | 25,035 | 80,940 | - | |||||||||||||||

| Sacramento | 54,595 | - | 3,311 | 57,906 | - | |||||||||||||||

| Jersey City | 31,503 | - | 21,241 | 52,744 | - | |||||||||||||||

| Chicago | - | 14,000 | 119,000 | 133,000 | 23.0 | |||||||||||||||

| Miami | 19,887 | - | - | 19,887 | - | |||||||||||||||

| Leased facilities acquired in 2015 | 71,250 | - | 23,725 | 94,975 | - | |||||||||||||||

| Piscataway | 88,820 | - | 87,180 | 176,000 | - | |||||||||||||||

| Other | 2,493 | - | - | 2,493 | - | |||||||||||||||

| Totals as of June 30, 2016 | 1,283,941 | 45,500 | 1,031,164 | 2,360,605 | 249.9 | |||||||||||||||

| (1) | Reflects NRSF at a facility for which the initiation of substantial activities has begun to prepare the property for its intended use on or before December 31, 2016. |

| (2) | Reflects NRSF at a facility for which the initiation of substantial activities has begun to prepare the property for its intended use after December 31, 2016. |

| (3) | The total cost basis of adjacent land, which is land available for the future development, is approximately $20 million. This is included in land on the Combined Consolidated Balance Sheets. The Basis of Design NRSF does not include any build-out on the adjacent land. |

| 13 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| NOI by Facility and Capital Expenditure Summary |

(unaudited and in thousands)

The Company calculates net operating income, or NOI, as net income (loss), excluding: interest expense, interest income, depreciation and amortization, write-off of unamortized deferred financing costs, tax expense (benefit) of taxable REIT subsidiaries, gain (loss) on extinguishment of debt, transaction and integration costs, gain (loss) on sale of real estate, restructuring costs and general and administrative expenses. The Company believes that NOI is another metric that is often utilized to evaluate returns on operating real estate from period to period and also, in part, to assess the value of the operating real estate. The breakdown of NOI by facility is shown below:

| Three Months Ended | Six Months Ended | |||||||||||||||||||

| June 30, | March 31, | June 30, | June 30, | |||||||||||||||||

| 2016 | 2016 | 2015 | 2016 | 2015 | ||||||||||||||||

| Breakdown of NOI by facility: | ||||||||||||||||||||

| Atlanta-Metro data center | $ | 20,885 | $ | 19,972 | $ | 16,875 | $ | 40,857 | $ | 33,641 | ||||||||||

| Atlanta-Suwanee data center | 11,272 | 11,500 | 10,094 | 22,772 | 20,224 | |||||||||||||||

| Santa Clara data center | 3,653 | 3,764 | 3,574 | 7,417 | 6,951 | |||||||||||||||

| Richmond data center | 7,976 | 6,602 | 4,933 | 14,578 | 9,188 | |||||||||||||||

| Sacramento data center | 2,140 | 1,922 | 1,900 | 4,062 | 3,771 | |||||||||||||||

| Princeton data center | 2,356 | 2,356 | 2,310 | 4,712 | 4,659 | |||||||||||||||

| Dallas-Fort Worth data center | 3,914 | 2,624 | 1,462 | 6,538 | 2,211 | |||||||||||||||

| Leased data centers acquired in 2015 | 10,035 | 11,415 | 2,250 | 21,450 | 2,250 | |||||||||||||||

| Piscataway data center (2) | 670 | - | - | 670 | - | |||||||||||||||

| Other facilities | 1,120 | 1,092 | 1,214 | 2,212 | 2,282 | |||||||||||||||

| NOI (1) | $ | 64,021 | $ | 61,247 | $ | 44,612 | $ | 125,268 | $ | 85,177 | ||||||||||

| (1) | Includes facility level G&A allocation charges of 4% of cash revenue for all facilities, with the exception of the leased facilities acquired in 2015, which include G&A expense allocation charges of 10% of cash revenue. These allocated charges aggregated to $5.1 million, $5.0 million and $2.7 million for the three month periods ended June 30, 2016, March 31, 2016 and June 30, 2015, respectively. |

| (2) | Includes results of the Piscataway facility for the period June 6, 2016 through June 30, 2016. |

Capital expenditures incurred are summarized as follows:

| Capital Expenditures (1) | ||||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||

| 2016 | 2015 | 2016 | 2015 | |||||||||||||

| Redevelopment | $ | 29,026 | $ | 78,416 | $ | 82,508 | $ | 164,483 | ||||||||

| Acquisitions (2) | 125,000 | 335,150 | 125,000 | 335,150 | ||||||||||||

| Maintenance capital expenditures | 380 | 609 | 715 | 626 | ||||||||||||

| Other capitalized costs | 9,135 | 5,786 | 15,831 | 11,845 | ||||||||||||

| Total capital expenditures | $ | 163,541 | $ | 419,961 | $ | 224,054 | $ | 512,104 | ||||||||

| (1) | Does not include capitalized leasing commissions included in deferred costs or other management-related fixed assets included in other assets. |

| (2) | The three and six months ended June 30, 2016 reflects the total consideration transferred for the purchase of the Piscataway facility on June 6, 2016. The three and six months ended June 30, 2015 reflects the total consideration transferred for the Carpathia acquisition on June 16, 2015 (excluding the assumption of $19.8 million in deferred tax liabilities assumed). |

| 14 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Leasing Statistics – Signed Leases |

The mix of leasing activity has a significant impact on quarterly rates, both within major product segments and for overall blended leasing rates. The Company’s rate performance will vary quarter to quarter based on the mix of deals leased – C1 Custom Data Center, C2 Colocation (Cabinet, Cage and Suite), and C3 Cloud and Managed Services categories all vary on a rate per square foot basis. The amounts below include renewals when there was a change in square footage rented, and renewals where C3 dedicated server cloud customers had shifts in their MRR related to their use of fully depreciated equipment. The amounts below exclude renewals where square footage remained consistent before and after renewal. (See renewal table on page 17 for such renewals).

During the second quarter of 2016, the Company signed 410 new and modified leases aggregating to $25.8 million of annualized rent which includes new leased revenue plus revenue from modified renewals. Removing annualized modified renewal MRR and deducting period downgrades results in $13.3 million in incremental annualized rent for the quarter, which is a 54% increase over the prior four quarter average. This growth was driven by both the C1 and C2/C3 aspects of the QTS platform. Pricing of the C1 deals signed during the quarter was down slightly over the prior four quarter average primarily due to contracting additional space with existing C1 customers whereby the scale allows QTS to provide lower pricing. Pricing of the Company’s C2/C3 deals exceeded the prior four quarter average primarily attributable to customers contracting additional services with those leases.

Annualized Rent of New and Modified Leases represents total MRR associated with all new and modified leases for the respective periods for the purposes of computing annualized rent rates per square foot during the period. Incremental Annualized Rent, Net of Downgrades reflects net incremental MRR signed during the period for purposes of tracking incremental revenue contribution.

| Period | Number of Leases | Total Leased sq ft | Annualized Rent per Leased sq ft | Annualized Rent of New and Modified Leases | Incremental Rent, Net of | |||||||||||||||

| New/modified leases signed - Total | Q2 2016 | 410 | 41,251 | $ | 625 | $ | 25,787,118 | $ | 13,310,055 | |||||||||||

| P4QA* | 384 | 22,611 | 745 | 16,844,647 | 8,646,107 | |||||||||||||||

| Q1 2016 | 367 | 47,262 | 434 | 20,503,532 | 8,566,303 | |||||||||||||||

| Q4 2015 | 357 | 21,801 | 801 | 17,471,080 | 9,849,694 | |||||||||||||||

| Q3 2015 | 448 | 7,513 | 1,686 | 12,669,407 | 5,582,511 | |||||||||||||||

| Q2 2015 | 365 | 13,867 | 1,207 | 16,734,571 | 10,585,921 | |||||||||||||||

| New/modified leases signed - C1 | Q2 2016 | 23 | 28,018 | $ | 265 | $ | 7,429,308 | |||||||||||||

| P4QA* | 20 | 12,552 | 285 | 3,579,439 | ||||||||||||||||

| Q1 2016 | 16 | 38,960 | 240 | 9,361,740 | ||||||||||||||||

| Q4 2015 | 20 | 10,476 | 373 | 3,910,932 | ||||||||||||||||

| Q3 2015 | 20 | 128 | 3,983 | 509,776 | ||||||||||||||||

| Q2 2015 | 22 | 644 | 831 | 535,306 | ||||||||||||||||

| New/modified leases signed - C2/C3 | Q2 2016 | 387 | 13,233 | $ | 1,387 | $ | 18,357,810 | |||||||||||||

| P4QA* | 365 | 10,059 | 1,319 | 13,265,209 | ||||||||||||||||

| Q1 2016 | 351 | 8,302 | 1,342 | 11,141,792 | ||||||||||||||||

| Q4 2015 | 337 | 11,325 | 1,197 | 13,560,148 | ||||||||||||||||

| Q3 2015 | 428 | 7,385 | 1,647 | 12,159,631 | ||||||||||||||||

| Q2 2015 | 343 | 13,223 | 1,225 | 16,199,265 | ||||||||||||||||

| * | Average of prior 4 quarters NOTE: Figures above do not include cost recoveries. In general, C1 customers reimburse the Company for certain operating costs whereas C2/C3 customers are on a gross lease basis. As a result, pricing and resulting per square foot rates for C2/C3 customers includes the recovery of such operating costs. |

| 15 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

The following table outlines the booked-not-billed (“BNB”) balance as of June 30, 2016 and how that will affect revenue in 2016 and subsequent years:

| Booked-not-billed ("BNB") | 2016 | 2017 | Thereafter | Total | ||||||||||||

| MRR | $ | 1,597,343 | $ | 1,330,716 | $ | 1,162,655 | $ | 4,090,714 | ||||||||

| Incremental revenue (1) | 8,223,055 | 9,304,366 | 13,951,854 | |||||||||||||

| Annualized revenue (2) | 19,168,121 | 15,968,589 | 13,951,854 | 49,088,564 | ||||||||||||

| (1) | Incremental revenue represents the expected amount of recognized MRR in the period based on when the booked-not-billed leases commence throughout the period. |

| (2) | Annualized revenue represents the booked-not-billed MRR multiplied by 12, demonstrating how much recognized MRR might have been recognized if the booked-not-billed leases commencing in the period were in place for an entire year. |

The Company estimates the remaining cost to provide the space, power, connectivity and other services to the customer contracts which had not billed as of June 30, 2016 to be approximately $50 million. This estimate generally includes C1 customers with newly contracted space of more than 3,300 square feet. The space, power, connectivity and other services provided to customers that contract for smaller amounts of space is generally provided by existing space which was previously developed.

| 16 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Leasing Statistics – Renewed Leases and Rental Churn |

The mix of leasing activity has a significant impact on quarterly rates, both within major product segments and for overall blended renewal rates. The Company’s rate performance will vary quarter to quarter based on the mix of deals leased – C1 Custom Data Center, C2 Colocation, and C3 Cloud and Managed Services categories all vary on a rate per square foot basis.

Consistent with the Company’s 3C strategy and business model, the renewal rates below reflect total MRR per square foot including all subscribed services. For comparability, the Company includes only those customers that have maintained consistent space footprints in the computations below. All customers with space changes are incorporated into new/modified leasing statistics and rates.

The overall blended rate for renewals signed in the second quarter of 2016 was 2.0% higher than the rates for those customers immediately prior to renewal. The Company believes that renewal rates will generally increase in the low to mid-single digits.

Rental Churn (which the Company defines as MRR lost to a customer intending to fully exit the platform compared to total MRR at the beginning of the period) was 1.3% for the second quarter of 2016 and 3.6% for the six months ended June 30, 2016.

| Period | Number of renewed leases | Total Leased sq ft | Annualized rent per leased sq ft | Annualized Rent | Rent Change (1) | |||||||||||||||

| Renewed Leases - Total | Q2 2016 | 82 | 9,719 | $ | 739 | $ | 7,183,415 | 2.0 | % | |||||||||||

| P4QA* | 74 | 11,972 | 874 | 10,462,725 | 0.1 | % | ||||||||||||||

| Q1 2016 | 59 | 16,705 | 950 | 15,871,969 | -3.7 | %** | ||||||||||||||

| Q4 2015 | 71 | 9,306 | 1,002 | 9,329,194 | 2.3 | % | ||||||||||||||

| Q3 2015 | 89 | 12,338 | 742 | 9,157,450 | 0.9 | % | ||||||||||||||

| Q2 2015 | 76 | 9,540 | 785 | 7,492,287 | 5.1 | % | ||||||||||||||

| Renewed Leases - C1 | Q2 2016 | - | - | $ | - | $ | - | 0.0 | % | |||||||||||

| P4QA* | 1 | 1,850 | 266 | 491,258 | 9.7 | % | ||||||||||||||

| Q1 2016 | - | - | - | - | 0.0 | % | ||||||||||||||

| Q4 2015 | 1 | 4,200 | 241 | 1,013,852 | 3.0 | % | ||||||||||||||

| Q3 2015 | 3 | 3,200 | 297 | 951,180 | 17.9 | % | ||||||||||||||

| Q2 2015 | - | - | - | - | 0.0 | % | ||||||||||||||

| Renewed Leases - C2/C3 | Q2 2016 | 82 | 9,719 | $ | 739 | $ | 7,183,415 | 2.0 | % | |||||||||||

| P4QA* | 73 | 10,122 | 985 | 9,971,467 | -0.3 | % | ||||||||||||||

| Q1 2016 | 59 | 16,705 | 950 | 15,871,969 | -3.7 | %** | ||||||||||||||

| Q4 2015 | 70 | 5,106 | 1,629 | 8,315,343 | 2.2 | % | ||||||||||||||

| Q3 2015 | 86 | 9,138 | 898 | 8,206,270 | -0.7 | % | ||||||||||||||

| Q2 2015 | 76 | 9,540 | 785 | 7,492,287 | 5.1 | % | ||||||||||||||

| * | Average of prior 4 quarters |

| ** | The decline in the renewal rate of 3.7% was due to changes in product mix by two customers that renewed. If the renewals related to those customers were excluded from the renewal base, rates would have been consistent with pre-renewal rates. |

| (1) | Calculated as the percentage change of the rent per square foot immediately before renewal when compared to the rent per square foot immediately after renewal. |

| 17 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Leasing Statistics – Commenced Leases |

The mix of leasing activity across C1, C2 and C3 has significant impact on quarterly rates, both within major product segments and for overall blended commencement rates. The Company’s rate performance will vary quarter to quarter based on the mix of deals leased. C1 Custom Data Center, C2 Colocation, and C3 Cloud and Managed Services categories all vary on a rate per square foot basis.

During the second quarter of 2016, the Company commenced customer leases (which includes both new customers and existing customers that modified their lease terms) representing approximately $27.4 million of annualized rent. This compares to customer leases representing an aggregate trailing four quarter average of approximately $35.5 million of annualized rent. Average pricing on QTS commenced leases during the second quarter of 2016 decreased compared to the prior four quarter average due to the change in C1 versus C2/C3 mix.

The C1 average commencement rate of $232 per square foot represents an increase of 16% over the prior four quarter average of $200 per square foot, which was due to customers commencing with additional redundancy in the current period. The C2/C3 average commencement rate of $1,255 per square foot represents an increase of 8% over the prior four quarter average of $1,157 per square foot, which was due to additional services being attached to C2/C3 customer commencements.

| Period | Number of leases | Total Leased sq ft | Annualized rent per leased sq ft | Annualized Rent | ||||||||||||

| Leases commenced - Total | Q2 2016 | 409 | 53,503 | $ | 513 | $ | 27,449,191 | |||||||||

| P4QA* | 492 | 57,791 | 615 | 35,527,044 | ||||||||||||

| Q1 2016 | 411 | 49,858 | 776 | 38,666,890 | ||||||||||||

| Q4 2015 | 446 | 52,783 | 733 | 38,669,556 | ||||||||||||

| Q3 2015 | 651 | 77,273 | 490 | 37,887,304 | ||||||||||||

| Q2 2015 | 459 | 51,248 | 525 | 26,884,427 | ||||||||||||

| Leases commenced - C1 | Q2 2016 | 21 | 38,818 | $ | 232 | $ | 9,020,640 | |||||||||

| P4QA* | 28 | 32,745 | 200 | 6,545,714 | ||||||||||||

| Q1 2016 | 21 | 17,540 | 225 | 3,941,117 | ||||||||||||

| Q4 2015 | 21 | 40,618 | 233 | 9,457,608 | ||||||||||||

| Q3 2015 | 33 | 43,199 | 181 | 7,822,312 | ||||||||||||

| Q2 2015 | 37 | 29,622 | 168 | 4,961,821 | ||||||||||||

| Leases commenced - C2/C3 | Q2 2016 | 388 | 14,685 | $ | 1,255 | $ | 18,428,551 | |||||||||

| P4QA* | 464 | 25,046 | 1,157 | 28,981,330 | ||||||||||||

| Q1 2016 | 390 | 32,318 | 1,075 | 34,725,773 | ||||||||||||

| Q4 2015 | 425 | 12,165 | 2,401 | 29,211,948 | ||||||||||||

| Q3 2015 | 618 | 34,074 | 882 | 30,064,992 | ||||||||||||

| Q2 2015 | 422 | 21,626 | 1,014 | 21,922,606 | ||||||||||||

| * | Average of prior 4 quarters |

| 18 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Lease Expirations |

C1 leases are typically 5-10 years with the majority of C1 lease expirations occurring in 2017 and beyond. C2/C3 leases are typically 3 years in duration, with the majority of C2/C3 lease expirations occurring in 2017 and 2018. The following table sets forth a summary schedule of the lease expirations as of June 30, 2016 at the properties in the Company’s portfolio. Unless otherwise stated in the footnotes, the information set forth in the table assumes that customers exercise no renewal options and all early termination rights are exercised:

| Year

of Lease Expiration | Number

of Leases Expiring (1) | Total

Raised Floor of Expiring Leases | %

of Portfolio Leased Raised Floor | Annualized

Rent (2) | %

of Portfolio Annualized Rent | C1

as % of Portfolio Annualized Rent | C2

as % of Portfolio Annualized Rent | C3

as % of Portfolio Annualized Rent | ||||||||||||||||||||||||

| Month-to-Month (3) | 383 | 13,999 | 2 | % | $ | 17,111,657 | 5 | % | 0 | % | 3 | % | 2 | % | ||||||||||||||||||

| 2016 | 1,024 | 43,395 | 5 | % | 47,504,525 | 14 | % | 2 | % | 6 | % | 6 | % | |||||||||||||||||||

| 2017 | 1,224 | 144,038 | 16 | % | 87,916,834 | 25 | % | 6 | % | 16 | % | 3 | % | |||||||||||||||||||

| 2018 | 933 | 270,976 | 31 | % | 89,875,217 | 26 | % | 11 | % | 9 | % | 6 | % | |||||||||||||||||||

| 2019 | 312 | 34,186 | 4 | % | 24,130,898 | 7 | % | 1 | % | 5 | % | 1 | % | |||||||||||||||||||

| 2020 | 123 | 44,564 | 5 | % | 18,622,507 | 5 | % | 2 | % | 3 | % | 0 | % | |||||||||||||||||||

| After 2020 | 89 | 318,819 | 37 | % | 61,305,592 | 18 | % | 17 | % | 1 | % | 0 | % | |||||||||||||||||||

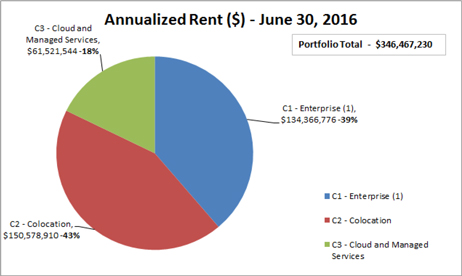

| Portfolio Total | 4,088 | 869,977 | 100 | % | $ | 346,467,230 | 100 | % | 39 | % | 43 | % | 18 | % | ||||||||||||||||||

| (1) | Represents each agreement with a customer signed as of June 30, 2016 for which billing has commenced; a lease agreement could include multiple spaces and a customer could have multiple leases. |

| (2) | Annualized rent is presented for leases commenced as of June 30, 2016. The Company defines annualized rent as MRR multiplied by 12. The Company calculates MRR as monthly contractual revenue under signed leases as of a particular date, which includes revenue from our C1, C2 and C3 rental and cloud and managed services activities, but excludes customer recoveries, deferred set-up fees, variable related revenues, non-cash revenues and other one-time revenues. MRR does not include the impact from booked-not-billed leases as of a particular date, unless otherwise specifically noted. This amount reflects the annualized cash rental payments. It does not reflect the accounting associated with any free rent, rent abatements or future scheduled rent increases and also excludes operating expense and power reimbursements. |

| (3) | Consists of customers whose leases expired prior to June 30, 2016 and have continued on a month-to-month basis. |

| 19 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Largest Customers |

As of June 30, 2016, the Company’s portfolio was leased to over 1,000 customers comprised of companies of all sizes representing an array of industries, each with unique and varied business models and needs. The following table sets forth information regarding the ten largest customers in the portfolio based on annualized rent as of June 30, 2016 (does not include rents or maturities associated with booked-not-billed customers or ramps for existing customers which have not yet commenced billing):

| Principal Customer Industry | Product | Number of Locations | Annualized Rent (1) | % of Portfolio Annualized Rent | Weighted Average Remaining Lease Term (Months) (2) | |||||||||

| Internet | C1 | 2 | $ | 40,057,416 | 11.6 | % | 53 | |||||||

| Information Technology | C1 | 2 | 12,131,594 | 3.5 | % | 95 | ||||||||

| Information Technology | C1, C3 | 3 | 11,328,674 | 3.3 | % | 95 | ||||||||

| Technology | C2, C3 | 4 | 9,654,378 | 2.8 | % | 11 | ||||||||

| Internet | C1 | 1 | 9,644,400 | 2.8 | % | 28 | ||||||||

| Government | C2 | 2 | 9,405,960 | 2.7 | % | 7 | ||||||||

| Technology | C2, C3 | 5 | 7,286,112 | 2.1 | % | 9 | ||||||||

| Retail | C3 | 2 | 6,409,400 | 1.8 | % | 23 | ||||||||

| Information Technology | C2, C3 | 6 | 5,991,937 | 1.7 | % | 11 | ||||||||

| Information Technology | C1 | 1 | 5,935,800 | 1.7 | % | 69 | ||||||||

| Total / Weighted Average | $ | 117,845,671 | 34.0 | % | 46 | |||||||||

| (1) | Annualized rent is presented for leases commenced as of June 30, 2016. We define annualized rent as MRR multiplied by 12. We calculate MRR as monthly contractual revenue under signed leases as of a particular date, which includes revenue from our C1, C2 and C3 rental and cloud and managed services activities, but excludes customer recoveries, deferred set-up fees, variable related revenues, non-cash revenues and other one-time revenues. MRR does not include the impact from booked-not-billed leases as of a particular date. This amount reflects the annualized cash rental payments. It does not reflect any free rent, rent abatements or future scheduled rent increases and also excludes operating expense and power reimbursements. |

| (2) | Weighted average based on customer’s percentage of total annualized rent expiring and is as of June 30, 2016. |

| 20 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

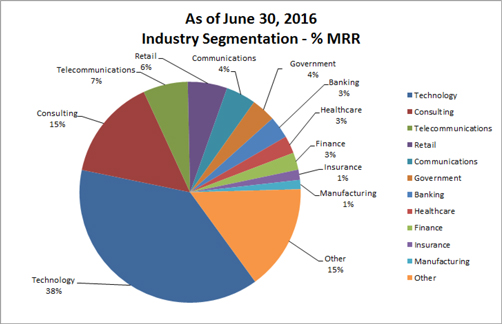

| Industry Segmentation |

The following table sets forth information relating to the industry segmentation as of June 30, 2016:

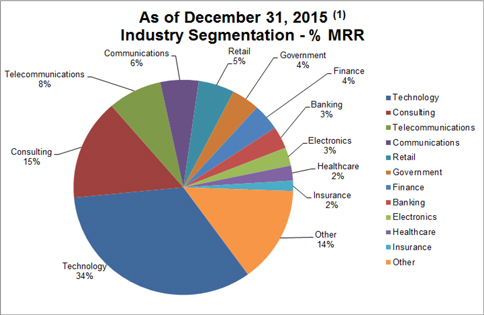

The following table sets forth information relating to the industry segmentation as of December 31, 2015:

| (1) | Subsequent to December 31, 2015, industries of certain customers have been refined and reclassified. As such, the industry segmentation table as of December 31, 2015 has been conformed to these new classifications. |

| 21 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Product Diversification |

The following table sets forth information relating to the distribution of leases at the properties, by type of product offering, as of June 30, 2016:

| (1) | As of June 30, 2016, C1 customers renting at least 6,600 square feet represented $89.8 million of annualized C1 MRR, C1 customers renting 3,300 square feet to 6,599 square feet represented $22.7 million of annualized C1 MRR, and C1 customers renting below 3,300 square feet represented $22.0 million of annualized C1 MRR. As of June 30, 2016, C1 customers’ median used square footage was 3,892 square feet. |

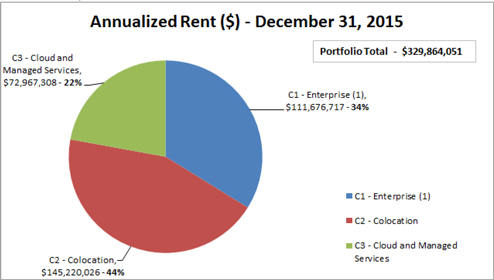

The following table sets forth information relating to the distribution of leases at the properties, by type of product offering, as of December 31, 2015:

| (1) | As of December 31, 2015, C1 customers renting at least 6,600 square feet represented $72.5 million of annualized C1 MRR, C1 customers renting between 3,300 and 6,599 square feet represented $17.8 million of annualized C1 MRR, and C1 customers renting below 3,300 square feet represented $21.4 million of annualized C1 MRR. As of December 31, 2015, C1 customers’ median used square footage was 3,876 square feet. |

| 22 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Debt Summary and Debt Maturities |

(in thousands)

| Weighted Average | ||||||||||||||

| Coupon Interest Rate at | June 30, | December 31, | ||||||||||||

| June 30, 2016 | Maturities | 2016 | 2015 | |||||||||||

| Unsecured Credit Facility | ||||||||||||||

| Revolving Credit Facility | 2.01 | % | December 17, 2019 | $ | 196,000 | $ | 224,002 | |||||||

| Term Loan I | 1.95 | % | December 17, 2020 | 150,000 | 150,000 | |||||||||

| Term Loan II | 1.95 | % | April 27, 2021 | 150,000 | 150,000 | |||||||||

| Senior Notes (1) | 5.88 | % | August 1, 2022 | 300,000 | 300,000 | |||||||||

| Capital Lease and Lease Financing Obligations | 3.45 | % | 2016 - 2025 | 43,440 | 49,761 | |||||||||

| Total | 3.44 | % | $ | 839,440 | $ | 873,763 | ||||||||

| (1) | Excludes the Senior Note discount and debt issuance costs reflected as liabilities at June 30, 2016. |

As of June 30, 2016:

| Debt instruments | 2016 | 2017 | 2018 | 2019 | 2020 | Thereafter | Total | |||||||||||||||||||||

| Unsecured Credit Facility | $ | - | $ | - | $ | - | $ | 196,000 | $ | 150,000 | $ | 150,000 | $ | 496,000 | ||||||||||||||

| Senior Notes (1) | - | - | - | - | - | 300,000 | 300,000 | |||||||||||||||||||||

| Capital Lease and Lease Financing Obligations | 6,237 | 12,388 | 8,804 | 2,461 | 2,190 | 11,360 | 43,440 | |||||||||||||||||||||

| Total | $ | 6,237 | $ | 12,388 | $ | 8,804 | $ | 198,461 | $ | 152,190 | $ | 461,360 | $ | 839,440 | ||||||||||||||

| (1) | Excludes the Senior Note discount and all debt issuance costs reflected as liabilities at June 30, 2016. |

| 23 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Interest Summary |

(unaudited and in thousands)

| Three Months Ended | Six Months Ended | |||||||||||||||||||

| June 30, | March 31, | June 30, | June 30, | June 30, | ||||||||||||||||

| 2016 | 2015 | 2015 | 2016 | 2015 | ||||||||||||||||

| Interest expense and fees | $ | 7,153 | $ | 7,885 | $ | 6,367 | $ | 15,038 | $ | 12,838 | ||||||||||

| Amortization of deferred financing costs and bond discount | 877 | 877 | 854 | 1,754 | 1,703 | |||||||||||||||

| Capitalized interest (1) | (3,156 | ) | (2,781 | ) | (2,422 | ) | (5,937 | ) | (4,400 | ) | ||||||||||

| Total interest expense | $ | 4,874 | $ | 5,981 | $ | 4,799 | $ | 10,855 | $ | 10,141 | ||||||||||

| (1) | The weighted average interest rate for the three months ended June 30, 2016, March 31, 2016, and June 30, 2015 was 4.27%, 3.77%, and 4.60%, respectively. As of June 30, 2016 and December 31, 2015 our weighted average coupon interest rate was 3.44% and 3.31%, respectively. |

| 24 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Appendix |

Non-GAAP Financial Measures

This document includes certain non-GAAP financial measures that management believes are helpful in understanding the Company’s business, as further described below.

The Company considers the following non-GAAP financial measures to be useful to investors as key supplemental measures of the Company’s performance: (1) FFO; (2) Operating FFO; (3) Adjusted Operating FFO; (4) MRR; (5) NOI; (6) EBITDA; and (7) Adjusted EBITDA. These non-GAAP financial measures should be considered along with, but not as alternatives to, net income or loss and cash flows from operating activities as a measure of the Company’s operating performance. FFO, Operating FFO, Adjusted Operating FFO, MRR, NOI, EBITDA and Adjusted EBITDA, as calculated by us, may not be comparable to FFO, Operating FFO, Adjusted Operating FFO, MRR, NOI, EBITDA and Adjusted EBITDA as reported by other companies that do not use the same definition or implementation guidelines or interpret the standards differently from us.

Definitions

C1 – Custom Data Center. Power costs are passed on to customers (metered power); generally 3,000 square feet or more of raised floor; lease term of 5 to 10 years; customers are large corporations, government agencies, and global Internet businesses.

C2 – Colocation. Power overages charged separately; specified kW included in lease; up to 3,000 square feet of raised floor; lease term of up to 3 years; customers are large corporations, small and medium businesses and government agencies.

C3 – Cloud and Managed Services. Power bundled with service; small amounts of space; customers rent managed virtual servers; lease term up to 3 years; customers are large corporations, small and medium businesses and government agencies.

Booked-not-billed (“BNB”). The Company defines booked-not-billed as customer leases that have been signed, but for which lease payments have not yet commenced.

Leasable raised floor. The Company defines leasable raised floor as the amount of raised floor square footage that the Company has leased plus the available capacity of raised floor square footage that is in a leasable format as of a particular date and according to a particular product configuration. The amount of leasable raised floor may change even without completion of new redevelopment projects due to changes in the Company’s configuration of C1, C2 and C3 product space.

Basis-of-design floor space. The Company defines basis-of-design floor space as the total data center raised floor potential of its existing data center facilities.

Operating NRSF. Represents the total square feet of a building that is currently leased or available for lease plus developed supporting infrastructure, based on engineering drawings and estimates, but does not include space held for redevelopment or space used for the Company’s own office space.

The Company. Refers to QTS Realty Trust, Inc., a Maryland corporation, together with its consolidated subsidiaries, including QualityTech, LP.

| 25 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

FFO, Operating FFO and Adjusted Operating FFO

The Company considers funds from operations (“FFO”), to be a supplemental measure of its performance which should be considered along with, but not as an alternative to, net income (loss) and cash provided by operating activities as a measure of operating performance. The Company calculates FFO in accordance with the standards established by the National Association of Real Estate Investment Trusts (“NAREIT”). FFO represents net income (loss) (computed in accordance with GAAP), adjusted to exclude gains (or losses) from sales of property, real estate-related depreciation and amortization and similar adjustments for unconsolidated partnerships and joint ventures. The Company’s management uses FFO as a supplemental performance measure because, in excluding real estate related depreciation and amortization and gains and losses from property dispositions, it provides a performance measure that, when compared year over year, captures trends in occupancy rates, rental rates and operating costs.

Due to the volatility and nature of certain significant charges and gains recorded in the Company’s operating results that management believes are not reflective of its core operating performance, management computes an adjusted measure of FFO, which the Company refers to as Operating FFO. The Company generally calculates Operating FFO as FFO excluding certain non-routine charges and gains and losses that management believes are not indicative of the results of the Company’s operating real estate portfolio. The Company believes that Operating FFO provides investors with another financial measure that may facilitate comparisons of operating performance between periods and, to the extent they calculate Operating FFO on a comparable basis, between REITs.

Adjusted Operating Funds From Operations (“Adjusted Operating FFO”) is a non-GAAP measure that is used as a supplemental performance measure and to provide additional information to users of the financial statements. The Company calculates Adjusted Operating FFO by adding or subtracting from Operating FFO items such as: maintenance capital investment, paid leasing commissions, amortization of deferred financing costs and bond discount, non-real estate depreciation, straight line rent adjustments, deferred taxes and non-cash compensation.

The Company offers these measures because it recognizes that FFO, Operating FFO and Adjusted Operating FFO will be used by investors as a basis to compare its operating performance with that of other REITs. However, because FFO, Operating FFO and Adjusted Operating FFO exclude real estate depreciation and amortization and capture neither the changes in the value of the Company’s properties that result from use or market conditions, nor the level of capital expenditures and capitalized leasing commissions necessary to maintain the operating performance of its properties, all of which have real economic effect and could materially impact its financial condition, cash flows and results of operations, the utility of FFO, Operating FFO and Adjusted Operating FFO as measures of its operating performance is limited. The Company’s calculation of FFO may not be comparable to measures calculated by other companies that do not use the NAREIT definition of FFO or do not calculate FFO in accordance with NAREIT guidance. In addition, the Company’s calculations of FFO, Operating FFO and Adjusted Operating FFO are not necessarily comparable to FFO, Operating FFO and Adjusted Operating FFO as calculated by other REITs that do not use the same definition or implementation guidelines or interpret the standards differently from us. FFO, Operating FFO and Adjusted Operating FFO are non-GAAP measures and should not be considered a measure of the Company’s results of operations or liquidity or as a substitute for, or an alternative to, net income (loss), cash provided by operating activities or any other performance measure determined in accordance with GAAP, nor is it indicative of funds available to fund its cash needs, including its ability to make distributions to its stockholders.

| 26 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Three Months Ended | Six Months Ended | |||||||||||||||||||

| June 30, | March 31, | June 30, | June 30, | |||||||||||||||||

| 2016 | 2016 | 2015 | 2016 | 2015 | ||||||||||||||||

| FFO | ||||||||||||||||||||

| Net income | $ | 5,807 | $ | 6,859 | $ | 5,520 | $ | 12,666 | $ | 10,557 | ||||||||||

| Real estate depreciation and amortization | 26,409 | 24,869 | 16,325 | 51,278 | 30,627 | |||||||||||||||

| FFO | 32,216 | 31,728 | 21,845 | 63,944 | 41,184 | |||||||||||||||

| Write off of unamortized deferred finance costs | - | - | 83 | - | 83 | |||||||||||||||

| Integration costs | 3,026 | 2,053 | 422 | 5,079 | 422 | |||||||||||||||

| Transaction costs | 807 | 34 | 4,247 | 841 | 4,352 | |||||||||||||||

| Deferred tax benefit associated with transaction and integration costs | (1,183 | ) | (748 | ) | - | (1,931 | ) | - | ||||||||||||

| Non-cash reversal of deferred tax asset valuation allowance | - | - | (3,175 | ) | - | (3,175 | ) | |||||||||||||

| Operating FFO * | 34,866 | 33,067 | 23,422 | 67,933 | 42,866 | |||||||||||||||

| Maintenance Capex | (380 | ) | (335 | ) | (609 | ) | (715 | ) | (626 | ) | ||||||||||

| Leasing commissions paid | (3,388 | ) | (5,807 | ) | (3,782 | ) | (9,195 | ) | (6,866 | ) | ||||||||||

| Amortization of deferred financing costs and bond discount | 877 | 877 | 854 | 1,754 | 1,703 | |||||||||||||||

| Non real estate depreciation and amortization | 3,946 | 3,770 | 1,682 | 7,716 | 3,623 | |||||||||||||||

| Straight line rent revenue and expense and other | (3,243 | ) | (1,610 | ) | (1,160 | ) | (4,853 | ) | (1,525 | ) | ||||||||||

| Deferred tax benefit from operating results | (1,271 | ) | (1,857 | ) | - | (3,128 | ) | - | ||||||||||||

| Equity-based compensation expense | 3,200 | 2,050 | 1,831 | 5,250 | 3,138 | |||||||||||||||

| Adjusted Operating FFO * | $ | 34,607 | $ | 30,155 | $ | 22,238 | $ | 64,762 | $ | 42,313 | ||||||||||

| * | The Company’s calculations of Operating FFO and Adjusted Operating FFO may not be comparable to Operating FFO and Adjusted Operating FFO as calculated by other REITs that do not use the same definition. |

Monthly Recurring Revenue (MRR)

The Company calculates MRR as monthly contractual revenue under signed leases as of a particular date, which includes revenue from its C1, C2 and C3 rental and cloud and managed services activities, but excludes customer recoveries, deferred set-up fees, variable related revenues, non-cash revenues and other one-time revenues. MRR does not include the impact from booked-not-billed leases as of a particular date, unless otherwise specifically noted.

Separately, the Company calculates recognized MRR as the recurring revenue recognized during a given period, which includes revenue from its C1, C2 and C3 rental and cloud and managed services activities, but excludes customer recoveries, deferred set-up fees, variable related revenues, non-cash revenues and other one-time revenues.

Management uses MRR and recognized MRR as supplemental performance measures because they provide useful measures of increases in contractual revenue from the Company’s customer leases. MRR and recognized MRR should not be viewed by investors as alternatives to actual monthly revenue, as determined in accordance with GAAP. Other companies may not calculate MRR or recognized MRR in the same manner. Accordingly, the Company’s MRR and recognized MRR may not be comparable to other companies’ MRR and recognized MRR. MRR and recognized MRR should be considered only as supplements to total revenues as a measure of its performance. MRR and recognized MRR should not be used as measures of the Company’s results of operations or liquidity, nor is it indicative of funds available to meet its cash needs, including its ability to make distributions to its stockholders.

| 27 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Three Months Ended | Six Months Ended | |||||||||||||||||||

| June 30, | March 31, | June 30, | June 30, | |||||||||||||||||

| 2016 | 2016 | 2015 | 2016 | 2015 | ||||||||||||||||

| Recognized MRR in the period | ||||||||||||||||||||

| Total period revenues (GAAP basis) | $ | 98,687 | $ | 94,768 | $ | 68,117 | $ | 193,455 | $ | 129,503 | ||||||||||

| Less: Total period recoveries | (6,168 | ) | (5,435 | ) | (5,582 | ) | (11,603 | ) | (11,246 | ) | ||||||||||

| Total period deferred setup fees | (2,256 | ) | (1,903 | ) | (1,412 | ) | (4,159 | ) | (2,658 | ) | ||||||||||

| Total period straight line rent and other | (5,757 | ) | (4,268 | ) | (3,170 | ) | (10,025 | ) | (5,182 | ) | ||||||||||

| Recognized MRR in the period | 84,506 | 83,162 | 57,953 | 167,668 | 110,417 | |||||||||||||||

| MRR at period end | ||||||||||||||||||||

| Total period revenues (GAAP basis) | $ | 98,687 | $ | 94,768 | $ | 68,117 | $ | 193,455 | $ | 129,503 | ||||||||||

| Less: Total revenues excluding last month | (64,520 | ) | (63,020 | ) | (41,871 | ) | (159,288 | ) | (103,257 | ) | ||||||||||

| Total revenues for last month of period | 34,167 | 31,748 | 26,246 | 34,167 | 26,246 | |||||||||||||||

| Less: Last month recoveries | (2,805 | ) | (1,876 | ) | (2,185 | ) | (2,805 | ) | (2,185 | ) | ||||||||||

| Last month deferred setup fees | (756 | ) | (676 | ) | (513 | ) | (756 | ) | (513 | ) | ||||||||||

| Last month straight line rent and other | (1,734 | ) | (1,716 | ) | 1,925 | (1,734 | ) | 1,925 | ||||||||||||

| MRR at period end | $ | 28,872 | $ | 27,480 | $ | 25,473 | $ | 28,872 | $ | 25,473 | ||||||||||

Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA) and Adjusted EBITDA

The Company calculates EBITDA as net income (loss) adjusted to exclude interest expense and interest income, provision (benefit) for income taxes (including income taxes applicable to sale of assets) and depreciation and amortization. Management believes that EBITDA is useful to investors in evaluating and facilitating comparisons of the Company’s operating performance between periods and between REITs by removing the impact of its capital structure (primarily interest expense) and asset base charges (primarily depreciation and amortization) from its operating results.

In addition to EBITDA, the Company calculates an adjusted measure of EBITDA, which it refers to as Adjusted EBITDA, as EBITDA excluding write off of unamortized deferred financing costs, gains (losses) on extinguishment of debt, transaction and integration costs, equity-based compensation expense, restructuring costs, gain (loss) on legal settlement and gain (loss) on sale of real estate. The Company believes that Adjusted EBITDA provides investors with another financial measure that can facilitate comparisons of operating performance between periods and between REITs.

Management uses EBITDA and Adjusted EBITDA as supplemental performance measures as they provide useful measures of assessing the Company’s operating results. Other companies may not calculate EBITDA or Adjusted EBITDA in the same manner. Accordingly, the Company’s EBITDA and Adjusted EBITDA may not be comparable to others. EBITDA and Adjusted EBITDA should be considered only as supplements to net income (loss) as measures of the Company’s performance and should not be used as substitutes for net income (loss), as measures of its results of operations or liquidity or as an indications of funds available to meet its cash needs, including its ability to make distributions to its stockholders.

| 28 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

| Three Months Ended | Six Months Ended | |||||||||||||||||||

| June 30, | March 31, | June 30, | June 30, | |||||||||||||||||

| 2016 | 2016 | 2015 | 2016 | 2015 | ||||||||||||||||

| EBITDA and Adjusted EBITDA | ||||||||||||||||||||

| Net income | $ | 5,807 | $ | 6,859 | $ | 5,520 | $ | 12,666 | $ | 10,557 | ||||||||||

| Interest expense | 4,874 | 5,981 | 4,799 | 10,855 | 10,141 | |||||||||||||||

| Interest income | (2 | ) | - | (1 | ) | (2 | ) | (1 | ) | |||||||||||

| Tax benefit of taxable REIT subsidiaries | (2,454 | ) | (2,605 | ) | (3,135 | ) | (5,059 | ) | (3,135 | ) | ||||||||||

| Depreciation and amortization | 30,355 | 28,639 | 18,062 | 58,994 | 34,305 | |||||||||||||||

| EBITDA | 38,580 | 38,874 | 25,245 | 77,454 | 51,867 | |||||||||||||||

| Write off of unamortized deferred finance costs | - | - | 83 | - | 83 | |||||||||||||||

| Equity-based compensation expense | 3,200 | 2,050 | 1,831 | 5,250 | 3,138 | |||||||||||||||

| Integration costs | 3,026 | 2,053 | 422 | 5,079 | 422 | |||||||||||||||

| Transaction costs | 807 | 34 | 4,247 | 841 | 4,352 | |||||||||||||||

| Adjusted EBITDA | $ | 45,613 | $ | 43,011 | $ | 31,828 | $ | 88,624 | $ | 59,862 | ||||||||||

| 29 QTS Q2 Earnings 2016 | Contact: IR@qtsdatacenters.com |

Net Operating Income (NOI)