Attached files

| file | filename |

|---|---|

| EX-99.2 - EX-99.2 - CVR PARTNERS, LP | d203893dex992.htm |

| 8-K - 8-K - CVR PARTNERS, LP | d203893d8k.htm |

Exhibit 99.1

Unless the context otherwise requires, references to the “Issuers” refer to CVR Partners, LP and CVR Nitrogen Finance Corporation and references to “we,” “our,” “us,” and the “Partnership” refer to CVR Partners and its subsidiaries, except as specifically noted otherwise.

Our Company

Overview

We are a master limited partnership formed by CVR Energy (NYSE: CVI) to own, operate and grow our nitrogen fertilizer business. Our common units are listed on the New York Stock Exchange (NYSE: UAN) and we had an equity market capitalization of $1,039 million as of May 27, 2016. We are structured as a variable distribution master limited partnership and as such we do not have a targeted minimum quarterly cash distribution. Instead, the amount of our quarterly cash distributions vary both quarterly and annually based upon the performance of our business. We principally produce ammonia and urea ammonium nitrate (UAN), an aqueous solution of urea and ammonium nitrate. Our products are used by farmers to improve the yield and quality of their crops, primarily corn and wheat.

We produce our nitrogen fertilizer products at two manufacturing facilities located in Coffeyville, Kansas and East Dubuque, Illinois. We acquired the East Dubuque, Illinois facility in April 2016 through our acquisition of Rentech Nitrogen Partners, L.P. The acquisition has substantially increased our scale, reduced single facility risk and geographically diversified our operations and marketing footprint to include the Mid Corn Belt, the largest market in the United States for direct application of nitrogen fertilizer products. On a pro forma basis, after giving effect to the acquisition of our East Dubuque Facility, for the twelve months ended March 31, 2016, we would have generated net sales, net income, Adjusted EBITDA and Adjusted EBITDA minus capital expenditures of $468.7 million, $49.4 million, $195.9 million and $147.7 million. Adjusted EBITDA including the impacts of the anticipated $12.0 million of synergies from the Merger would have been $207.9 million. For a reconciliation of Adjusted EBITDA to net income, see “—Summary Historical and Pro Forma Consolidated Financial Data—CVR Partners.”

We are a leading North American producer and distributor of nitrogen fertilizers, with a presence extending from the Southern Plains to the Mid Corn Belt regions of the United States. These farming regions have some of the best growing conditions in the world for corn and wheat and the proximity of our manufacturing facilities to these regions provides us with a cost advantage compared to certain of our competitors. Our products are delivered to customers primarily by rail or truck, which allows us to maximize our geographic footprint and provides flexibility to sell product at the highest available netback pricing. In 2015, our facilities delivered a combined total of approximately 1.5 million tons of nitrogen fertilizer, primarily to retailers and distributors.

Our presence in the Southern Plains region will be enhanced through the recent agreement with LSB Industries that will allow us to market UAN from its Pryor, Oklahoma facility, commencing on June 1, 2016. The ability to offer product from three production facilities to a broad geographic area will allow us to create value for our customers, particularly large retailers and distributors that prefer to buy in scale for delivery throughout their network.

Coffeyville Facility

Our Coffeyville Facility is the only fertilizer facility in North America that utilizes a gasification process to convert petroleum coke, or pet coke, to hydrogen for subsequent conversion to ammonia and UAN. The pet coke used is a byproduct of the crude oil refining process. We currently purchase most of our pet coke from CVR Refining (NYSE: CVRR), which owns the Coffeyville refinery adjacent to our fertilizer plant. During the past five years, over 70% of the pet coke consumed by our plant was produced and supplied by CVR Refining pursuant to a long-term agreement. We believe our relationship with CVR Refining provides us with the benefit of a stable and secure raw material supply and there are other Midwestern refineries and pet coke brokers with ample supply available in proximity to the Coffeyville Facility. The Coffeyville Facility includes a 1,300 ton-per-day ammonia unit, a 3,000 ton-per-day UAN unit and a gasifier complex having a capacity of 89 million standard cubic feet per day of hydrogen.

1

In February 2013 we completed a significant two-year expansion at the Coffeyville Facility that increased our annual UAN production capacity by 400,000 tons, or approximately 50%. Subsequent to this expansion, we upgrade substantially all of the ammonia we produce at our Coffeyville Facility to UAN fertilizer, which has historically commanded a premium price over ammonia on a nutrient ton basis. In 2015, our Coffeyville Facility produced 385,400 tons of ammonia, of which approximately 96% was upgraded to produce 928,600 tons of UAN. Typically, approximately 0.41 tons of ammonia is required to produce one ton of UAN.

The largest raw material expense used in the production of ammonia at the Coffeyville Facility is pet coke. For the year ended December 31, 2015, we incurred approximately $11.9 million for pet coke, which represented 6.9% of the operating costs and expenses of our Coffeyville Facility. Major fixed costs include electrical energy, employee labor, maintenance (including contract labor) and outside services. Consistent, safe and reliable operations are critical to our financial performance. Over the past five years, the average on-stream factors of the gasification, ammonia and UAN plants at our Coffeyville Facility have been greater than 90%. The plant requires a scheduled maintenance turnaround approximately every two to three years, which generally lasts 14 to 21 days. The plant underwent a full facility turnaround in the third quarter of 2015 and the next scheduled turnaround is in the second half of 2017.

The primary geographic markets for our Coffeyville Facility fertilizer products are Kansas, Missouri, Nebraska, Iowa and Illinois in the Mid Corn Belt and Texas in the Southern Plains. The close proximity of our Coffeyville Facility to the Union Pacific mainline provides a cost advantage over certain of our competitors by reducing the costs of distributing our products to customers. The majority of the products we manufacture at our Coffeyville Facility (approximately 80% in 2015) are delivered by rail to destinations located principally on the Union Pacific railroad.

East Dubuque Facility

Our recently acquired East Dubuque Facility uses low-cost, North American natural gas to produce nitrogen fertilizer, primarily ammonia and UAN. The plant includes a 1,025 ton-per-day ammonia unit and a 1,100 ton-per-day UAN unit. The facility is located on a 210-acre, 140-foot bluff above the Mississippi River, with access to the river for loading certain products. We are able to purchase natural gas at competitive prices due to the plant’s connection to the Northern Natural Gas interstate pipeline system, which is within one mile of the facility, and the ANR Pipeline Company pipeline. Over the last five years, U.S. natural gas reserves have increased significantly due to, among other factors, advances in extracting shale gas, which have reduced and stabilized natural gas prices, significantly lowering our production costs.

The East Dubuque Facility has the flexibility to significantly vary its product mix. This enables us to upgrade our ammonia production into varying amounts of UAN, nitric acid and liquid and granulated urea each season, depending on market demand, pricing and storage availability. Product sales are heavily weighted toward sales of ammonia and UAN, which together made up 80% or more of the plant’s total revenues for the years ended December 31, 2015, 2014 and 2013. In 2015, the plant produced 340,300 tons of ammonia, of which approximately 34% was upgraded to produce 279,000 tons of UAN.

The principal raw material utilized by our East Dubuque Facility is natural gas. For the year ended December 31, 2015, the East Dubuque Facility incurred expenses of approximately $43.5 million for natural gas, which represented approximately 47% of the operating costs and expenses (excluding depreciation and amortization) of our East Dubuque Facility. Historically, the plant has required a planned maintenance turnaround every two to three years. Turnarounds generally last between 15 and 30 days. We began the 2016 turnaround on May 21, 2016. The turnaround coincides with the completion of the ammonia converter project, which is expected to add approximately 50 tons per day of ammonia production capacity, and is expected to be completed before the end of the second quarter of 2016.

The East Dubuque Facility is located in northwest Illinois, in the Mid Corn Belt. The plant primarily sells its product to customers located within 200 miles of the facility, as Illinois and Iowa have been the two largest corn producing and nitrogen fertilizer consuming states for the last 20 years, according to the USDA. In most instances, customers take delivery of nitrogen products at the plant and arrange and pay to transport them to their final destinations by truck. Our East Dubuque Facility has

2

on-site storage capacity of 60,000 tons of ammonia and 80,000 tons of UAN. The combination of the plant’s proximity to customers and storage capacity allows for better timing of the pick-up and application of products, as shipments from more distant locations have a greater risk of missing the short periods of favorable weather conditions during which the application of nitrogen fertilizer may occur. The plant also benefits from its location on the Mississippi River, with direct access to a barge dock as well as a nearby rail spur serviced by the Canadian National Railway Company.

Our Competitive Strengths

Strategically Located Assets. Our nitrogen fertilizer plants, located in Coffeyville, Kansas and East Dubuque, Illinois, provide geographical advantages in that we are located in the Mid Corn Belt and close to the Southern Plains. According to the USDA, Iowa, Illinois, Kansas and Nebraska accounted for approximately 50% of total U.S. corn production in 2015. Together these states represented 75% of total delivered tons from the Coffeyville and East Dubuque plants for 2015. Both regions consume more nitrogen fertilizer than they produce, requiring product to be imported from the U.S. Gulf Coast and international producers. The plants’ markets are highly attractive because of their strong and growing demand for nitrogen fertilizer. Nitrogen fertilizer prices in these regions factor in the transportation costs of out-of-region producers. As a result of our close proximity to these agricultural markets, our transportation cost advantage allows us to cost-effectively sell substantially all of our products at a high margin. In addition, our on-site storage facilities allow for better timing of product pickup and application by customers across both regions.

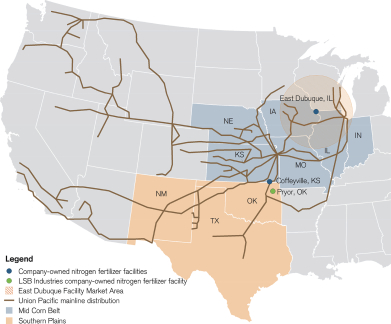

The following map shows the location of our two production facilities and LSB Industries’ Pryor, OK facility where we have a UAN marketing arrangement. It also shows the broad distribution footprint of these facilities, accessible either by rail or truck. The ability to offer product from three production facilities to this broad geographic area will allow us to create additional value for our customers going forward, particularly large retailers and distributors that prefer to buy in scale for delivery throughout their network.

Map of Operations

3

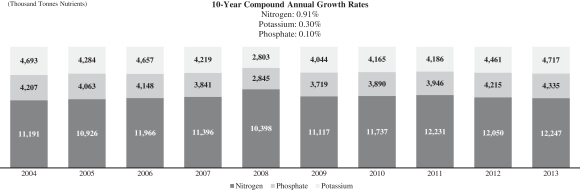

Leading North American producer and distributor of nitrogen fertilizer products. We are a leading North American producer and distributor of nitrogen fertilizers. We derive substantially all of our revenue from the production and sale of nitrogen fertilizers, primarily in the agricultural market, whereas many of our competitors are meaningfully diversified into other crop nutrients, such as phosphate and potassium, and make significant sales into the lower-margin industrial market. Nitrogen is an essential element for plant growth as it is the primary determinant of crop yield. Nitrogen fertilizer production is a higher margin, growing business with more stable demand compared to the production of the two other essential crop nutrients, potassium and phosphate, because nitrogen must be reapplied annually. From 2004 to 2013, US nitrogen fertilizer consumption grew at a Compound Annual Growth Rate of 0.91%, compared to 0.30% and 0.10% for potassium and phosphate, respectively.

Historical U.S. Fertilizer Consumption by Product

Source: International Fertilizer Industry Association database. Product categories include both straight and compound products.

Asset Diversification Enhances Flexibility and Reduces Operational Risk. We produce nitrogen fertilizer products out of strategically located assets located in Coffeyville, Kansas and East Dubuque, Illinois. We believe that the acquisition of the East Dubuque facility significantly enhances our business profile through:

| • | substantially increased scale with the addition of a second manufacturing facility that approximately doubles our production capacity and eliminates single facility risk, |

| • | greater geographic diversification with access to the attractive Mid Corn Belt market that typically experiences a pricing premium compared to other regions and, |

| • | feedstock diversification through the addition of a natural gas feedstock plant to our existing pet coke feedstock facility, |

History of High Average Net Sales Prices in the Mid Corn Belt and Southern Plains Regions. The locations of our East Dubuque and Coffeyville facilities generally enable us to realize higher average net sales prices per ton of UAN and ammonia than plants in other regions, because the prevailing prices in our markets reflect the cost to transport product into our market.

4

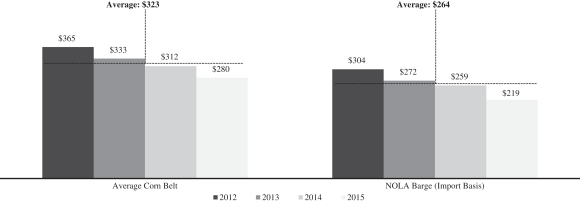

The chart below represents historical UAN prices (spot, UAN 32 equivalent basis) in the Corn Belt and Gulf Coast Region (NOLA Barge), according to data compiled by Blue Johnson.

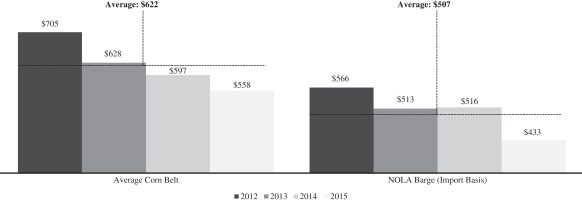

The chart below represents historical ammonia spot prices in the Corn Belt and the Gulf Coast Region market (NOLA barge), according to data compiled by Blue Johnson.

According to Blue Johnson, during the four years ended December 31, 2015, ammonia sold for a premium in the Corn Belt compared to the Gulf Coast Region. Over the four years ended December 31, 2015, the average Corn Belt spot price for ammonia was $622 per ton fob compared to $507 per ton fob in the Gulf Coast Region (NOLA Barge) market. UAN prices in the Corn Belt have also experienced a pricing premium compared to the Gulf Coast Region (NOLA Barge). For example, over the four years ended December 31, 2015, the average Corn Belt price for UAN was $323 per ton compared to $264 per ton in the Gulf Coast Region (NOLA Barge). Given the location of our Coffeyville and East Dubuque facilities, we typically realize pricing premiums for UAN and ammonia similar to the premiums in the Corn Belt and Southern Plains regions.

Favorable Long Term Industry Trends. According to a study funded by the FAO, global fertilizer demand is projected to increase by 45% between 2005 and 2030, primarily driven by population growth, decrease in farmland per capita, increased bio-fuel consumption and the continued evolution to more protein-based diets in developing countries. We believe that these trends are positive for nitrogen fertilizer products as nitrogen represents approximately 61% of total global fertilizer consumption. Nitrogen, along with phosphate and potash, are the primary crop nutrients utilized by producers to enhance the quality and yield of crops. Nutrients are depleted in soil over time and therefore must be replenished through fertilizer use. Nitrogen is the most quickly depleted nutrient and as a result must be replenished every year, whereas phosphate and potassium can be retained in

5

soil for up to three years. Given that nitrogen fertilizers must be applied annually and are generally the most important determinant of plant growth and crop yield, we believe demand for nitrogen fertilizers are more stable in nature. The United States has generally been a net importer of nitrogen products in order to meet fertilizer, industrial and other demand requirements. Although new capacity will continue to come online over the next several years, we believe that the additional capacity will be insufficient to fully displace imports, which will still be needed to meet domestic demand.

Experienced Management Team. We are managed by a highly experienced management team. Mark Pytosh, our President and Chief Executive Officer, has extensive industry experience having served in senior management roles in the energy, renewable energy and waste industries. Susan Ball, our Treasurer and Chief Financial Officer, has over 30 years of experience in finance and accounting and also serves the same roles at CVR Energy, Inc. and CVR Refining, LP. William White, Executive Vice President of Marketing and Operations, has nearly 40 years of experience in the chemical industry, including over 10 years with CVR Partners. John Lipinski, our Executive Chairman, has over 40 years of experience in the refining and chemicals industries and also serves as Chief Executive Officer, President and a Director of the general partner of CVR Refining, LP and Chief Executive Officer, President and a Director of CVR Energy, Inc. In addition, both our Coffeyville and East Dubuque facilities have very experienced senior operations and marketing teams which collectively have an average of over 35 years of experience in the fertilizer industry.

Our Business Strategy

Be a Low-Cost Producer. Our customers make their purchasing decisions principally on the basis of delivered price and availability of product. In order to deliver product in the most cost effective way for our customers, in an environment where price and raw material costs are largely market driven, we are focused on keeping our operating costs low. The critical focus area to minimize costs is to maximize on-stream rates. In recent years we have focused on preventative maintenance and critical spare parts to allow us to achieve high levels of online production.

Provide a High Level of Customer Service. We focus on providing our customers with the highest level of service. In addition to price, our customers value reliable on time deliveries. The recent acquisition of the East Dubuque Facility and our UAN marketing agreement with LSB Industries allow us to provide product in an expanded geographic area, which is important to our customers. Substantially all of our product shipments are targeted to freight advantaged destinations located in the Southern Plains and Mid Corn Belt, allowing us to quickly and reliably service customer demand. Furthermore, we maintain our own fleet of railcars, capable of safely transporting UAN and ammonia, which helps us ensure prompt delivery. We believe a continued focus on customer service will allow us to maintain relationships with existing customers and grow our business with new customers.

Continue to Focus on Safety and Training. We intend to continue our focus on safety and training in order to minimize accidents and injuries to our employees to improve the reliability and high on-stream availability of our plants. We have developed a series of comprehensive safety programs, involving active participation of employees at all levels of the organization, that are aimed at preventing recordable incidents.

Pursue Growth Opportunities. We intend to continue to expand our existing asset base and utilize the experience of our and CVR Energy’s management teams to expand production at existing facilities and acquire and build additional infrastructure and production assets.

| • | Organic Growth. Our facilities have undergone various expansion projects that have increased production and product upgrade capabilities. Our Coffeyville Facility completed a significant two-year plant expansion in 2013, designed to increase its UAN production capacity by 400,000 tons, or approximately 50% per year. Total capital expenditures associated with the UAN expansion were approximately $130 million. In December 2013, our East Dubuque Facility completed an ammonia production and storage capacity expansion project that increased the facility’s ammonia production capacity by 23%, or 190 tons per day and is in the process of installing a new ammonia converter that is expected to add approximately 50 tons per day of ammonia production capacity. Total capital expenditure associated |

6

| with these expansions is approximately $125 million. We intend to continue to evaluate additional opportunities to increase our profitability by expanding our production capabilities and product offerings. We expect to further increase our ammonia production in the second half of 2016 once the new hydrogen plant at CVR Refining’s adjacent refinery comes online. At that point, we expect to take enough hydrogen to allow for additional ammonia production of 50 to 75 tons per day. We expect the incremental ammonia will be sold into the fertilizer market and not upgraded to UAN because the plant is operating at or near its rated UAN capacity. |

| • | Selectively Pursue Accretive Acquisitions. The nitrogen fertilizer industry has undergone significant consolidation over the last decade as a result of mergers and acquisitions. We expect industry consolidation to continue, and intend to evaluate strategic acquisitions within the nitrogen fertilizer industry and to focus on disciplined and accretive investments that leverage our core strengths. |

Maintain a Conservative Financial Position. We intend to maintain a conservative total debt level. We are targeting a leverage multiple of 2.0x Adjusted EBITDA (mid-cycle) and believe that level is appropriate as a steady-state target debt level. We expect to reduce leverage from the level at closing of the notes offering through organic growth driven by improved operating efficiency and a recovery in nitrogen fertilizer prices. We plan to retain significant financial flexibility through our business cycles by maintaining liquidity through cash on hand and our anticipated ABL Credit Facility. Our policy is to distribute to our unitholders all of the cash available for distribution that we generate each quarter after debt service and maintenance capital needs, however as a variable distribution master limited partnership, we do not have a minimum quarterly distribution. Cash available for distribution is determined by the board of directors of our general partner and excludes reserves for future operating or capital needs, allowing us to maintain sufficient liquidity. Our conservative financial policy was demonstrated in the 2015 third quarter, when we did not pay a cash distribution as a result of unplanned plant downtime.

Recent Developments

The Merger

On April 1, 2016, we completed the merger whereby we acquired Rentech Nitrogen Partners, L.P. (“Rentech Nitrogen”) for total consideration of approximately $802 million exclusive of the fair value of noncontrolling interest (the “Merger”). Pursuant to the Merger we acquired our East Dubuque, Illinois nitrogen fertilizer facility. Rentech Nitrogen was required to sell or spin off its facility located in Pasadena, Texas (the “Pasadena Facility”) as a condition to closing of the Merger. On March 14, 2016, Rentech Nitrogen completed the sale of its subsidiary that owned the Pasadena Facility to a third party. The primary reasons for the Merger were to expand our geographic footprint, diversify our raw material feedstocks, widen our customer reach and increase our potential for cash-flow generation. We believe we can achieve annual run-rate synergies of at least $12 million, through reduced corporate overhead costs which includes associated public company costs and with expected improved production and overall enhanced efficiencies of marketing and related logistics efforts through the integration of the two standalone facilities and management teams.

Coffeyville Credit Facility

On April 1, 2016, in connection with the closing of the Merger, CVR Partners entered into the Coffeyville Credit Facility with Coffeyville, as the lender, which was used (i) to fund the repayment of amounts outstanding under the GE Credit Facility, (ii) to pay the cash consideration and fees and expenses in connection with the Merger and related transactions and (iii) to repay all of the loans outstanding under the previous CVR Partners credit agreement.

As of May 30, 2016, we had $300.0 million in outstanding borrowings under the Coffeyville Credit Facility. We intend to use a portion of the net proceeds from this offering of notes to repay in full and terminate the Coffeyville Credit Facility.

7

The 2021 Notes Tender Offer and Change of Control Offer

On April 29, 2016, we announced that our subsidiary, CVR Nitrogen, commenced a cash tender offer (the “Tender Offer”) to purchase any and all of the outstanding 2021 Notes. In connection with the Tender Offer, CVR Nitrogen is soliciting the consents (“Consents”) of holders of the 2021 Notes to certain proposed amendments (the “Consent Solicitation”) to the indenture governing the 2021 Notes (the “2021 Notes Indenture”) to eliminate or modify substantially all of the restrictive covenants relating to CVR Nitrogen and its subsidiaries, eliminate all events of default other than the failure to pay principal, premium or interest on the 2021 Notes, eliminate all conditions to satisfaction and discharge, and release the liens on the collateral securing the 2021 Notes (the “Proposed Amendments”). Concurrently with, but separate from the Tender Offer, CVR Nitrogen has commenced an offer to purchase for cash any and all of the 2021 Notes at a purchase price of 101% of the aggregate principal amount of the 2021 Notes (the “Change of Control Offer” and, together with the Tender Offer, the “Offers”).

According to information provided by Ipreo LLC, the Information and Tender Agent for the Tender Offer, as of 5:00 p.m., New York City time, on May 26, 2016, CVR Nitrogen had received tenders and Consents from holders of $315,245,000 in aggregate principal amount of the 2021 Notes, representing approximately 98.5% of the total outstanding principal amount of the 2021 Notes. CVR Nitrogen received the requisite consents in respect of the 2021 Notes in connection with the Consent Solicitation to the Proposed Amendments. As a result, CVR Nitrogen intends to execute a supplemental indenture relating to the 2021 Notes (the “Supplemental Indenture”) setting forth the Proposed Amendments. The Proposed Amendments will become operative upon payment for the tendered 2021 Notes pursuant to the terms of the Tender Offer and Consent Solicitation.

Any 2021 Notes that remain outstanding following the consummation of the Offers will continue to be obligations of CVR Nitrogen under the 2021 Notes Indenture. The 2021 Notes that remain outstanding will no longer have the benefit of restrictive covenants, reporting obligations and certain of the events of default and other provisions presently contained in the 2021 Notes Indenture and the liens on the collateral securing the 2021 Notes will be released. The Tender Offer will expire at 5:00 p.m., New York City time on June 8, 2016, unless extended or earlier terminated.

8

SUMMARY HISTORICAL AND PRO FORMA CONSOLIDATED FINANCIAL DATA—CVR PARTNERS

The following summary historical consolidated financial data as of and for each of the years ended December 31, 2013, 2014 and 2015 are derived from CVR Partners’ audited consolidated financial statements and the summary historical consolidated financial data as of and for the three months ended March 31, 2015 and 2016 are derived from CVR Partners’ unaudited condensed consolidated interim financial statements. You should read the following data in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and the related notes thereto set forth in CVR Partners’ Annual Report on Form 10-K for the year ended December 31, 2015 and its Quarterly Report on Form 10-Q for the quarter ended March 31, 2016. You should not assume the results of operations for any past period indicate results for any future period.

The summary pro forma condensed combined balance sheet data as of March 31, 2016 has been prepared to give effect to the Merger as if it occurred on March 31, 2016. The summary unaudited pro forma condensed combined statements of operations data for the three months ended March 31, 2016, the year ended December 31, 2015 and the last twelve months ended March 31, 2016, has been prepared to give effect to the Merger as if it occurred on January 1, 2015. You should read the following pro forma data in conjunction with CVR Partners, LP unaudited pro forma financial statements included herein. The summary pro forma financial information was prepared using the acquisition method of accounting with the Partnership as the acquirer. Therefore, the historical basis of the Partnership’s assets and liabilities was not affected by the Merger. This pro forma financial information also gives effect to this offering and the intended use of proceeds therefrom (collectively with the Merger, the “transactions”).

For purposes of preparing the unaudited pro forma condensed combined balance sheet data as of March 31, 2016, CVR Nitrogen’s assets and liabilities have been recorded at their estimated fair values. The fair values assigned in these unaudited pro forma financial statements are preliminary and represent management’s estimate of fair value and are subject to revision. Pro forma adjustments are included only to the extent they are (i) directly attributable to the transactions, (ii) factually supportable, and (iii) with respect to the statement of operations, expected to have a continuing impact on the combined results. The accompanying summary pro forma financial information is presented for illustrative purposes only and is based on available information and assumptions the Partnership believes is reasonable. It does not purport to represent what the actual combined results of operations or the combined financial position of the Partnership would have been had the Merger occurred on the dates indicated, nor is it necessarily indicative of future combined results of operations or combined financial position. The actual financial position and results of operations will differ, perhaps significantly, from the pro forma amounts reflected herein due to a variety of factors, including access to additional information, final valuations and changes in operating results following the date of the pro forma financial statements.

9

| Historical | Pro Forma | |||||||||||||||||||||||||||||||||

| In millions, except as otherwise indicated | As of and for the Years Ended December 31, |

As of and for the Three Months Ended March 31, |

Year Ended December 31, |

Three Months Ended March 31, |

Last Twelve Months Ended March 31, |

|||||||||||||||||||||||||||||

| 2013 | 2014 | 2015 | 2015 | 2016 | 2015 | 2016 | 2016 | |||||||||||||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||||||||||||||||

| Net sales |

$ | 323.7 | $ | 298.7 | $ | 289.2 | $ | 93.1 | $ | 73.1 | $ | 490.5 | $ | 107.9 | $ | 468.7 | ||||||||||||||||||

| Cost of product sold |

58.1 | 72.0 | 65.2 | 25.8 | 16.3 | 95.3 | 19.1 | 86.3 | ||||||||||||||||||||||||||

| Direct operating expenses |

94.1 | 98.9 | 106.1 | 24.4 | 23.7 | 159.6 | 37.7 | 159.0 | ||||||||||||||||||||||||||

| Selling, general and administrative expenses |

21.0 | 17.7 | 20.8 | 4.6 | 6.4 | 35.4 | 8.2 | 35.4 | ||||||||||||||||||||||||||

| Depreciation and amortization |

25.6 | 27.3 | 28.4 | 6.8 | 7.0 | 78.5 | 19.0 | 84.5 | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Operating income |

124.9 | 82.8 | 68.7 | 31.5 | 19.7 | 121.7 | 23.9 | 103.5 | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Interest expense and other financing costs |

(6.3 | ) | (6.7 | ) | (7.0 | ) | (1.7 | ) | (1.7 | ) | (54.2 | ) | (13.4 | ) | (54.2 | ) | ||||||||||||||||||

| Other income (expense), net |

0.1 | — | 0.3 | — | — | 0.1 | 0.1 | 0.1 | ||||||||||||||||||||||||||

| Total other income (expense) |

(6.2 | ) | (6.7 | ) | (6.7 | ) | (1.7 | ) | (1.7 | ) | (54.1 | ) | (13.3 | ) | (54.1 | ) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Income before income tax expense |

118.7 | 76.1 | 62.0 | 29.8 | 18.0 | 67.6 | 10.6 | 49.4 | ||||||||||||||||||||||||||

| Income tax expense (benefit) |

0.1 | — | — | — | — | — | — | — | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Net Income |

$ | 118.6 | $ | 76.1 | $ | 62.0 | $ | 29.8 | $ | 18.0 | $ | 67.6 | $ | 10.6 | $ | 49.4 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Balance Sheet Data: |

||||||||||||||||||||||||||||||||||

| Cash and cash equivalents |

$ | 85.1 | $ | 79.9 | $ | 50.0 | $ | 72.6 | $ | 52.0 | $ | 98.8 | ||||||||||||||||||||||

| Working capital |

107.6 | 89.1 | 72.7 | 93.7 | 76.5 | 129.6 | ||||||||||||||||||||||||||||

| Total assets |

591.7 | 577.8 | 536.3 | 567.3 | 529.2 | 1,411.2 | ||||||||||||||||||||||||||||

| Total debt, net of unamortized debt issuance costs |

123.2 | 124.0 | 124.8 | 124.2 | 125.0 | 623.1 | ||||||||||||||||||||||||||||

| Statement of Cash Flows Data: |

||||||||||||||||||||||||||||||||||

| Net cash flow provided by (used in): |

||||||||||||||||||||||||||||||||||

| Operating activities |

$ | 129.0 | $ | 118.9 | $ | 78.4 | $ | 25.4 | $ | 23.6 | ||||||||||||||||||||||||

| Investing activities |

(43.7 | ) | (21.0 | ) | (16.9 | ) | (2.7 | ) | (1.7 | ) | ||||||||||||||||||||||||

| Financing activities |

(128.0 | ) | (103.1 | ) | (91.4 | ) | (30.0 | ) | (19.9 | ) | ||||||||||||||||||||||||

| Net increase (decrease) in cash and cash equivalents |

$ | (42.7 | ) | $ | (5.2 | ) | $ | (29.9 | ) | $ | (7.3 | ) | $ | 2.0 | ||||||||||||||||||||

| Other Data (unaudited): |

||||||||||||||||||||||||||||||||||

| EBITDA(1) |

$ | 150.6 | $ | 110.1 | $ | 97.4 | $ | 38.3 | $ | 26.7 | $ | 200.3 | $ | 43.0 | $ | 188.1 | ||||||||||||||||||

| Adjusted EBITDA(1)(2) |

$ | 152.8 | $ | 110.3 | $ | 106.8 | $ | 38.4 | $ | 27.9 | $ | 208.3 | $ | 43.2 | $ | 195.9 | ||||||||||||||||||

| Maintenance capital expenditures |

$ | 3.5 | $ | 4.7 | $ | 9.6 | $ | 1.3 | $ | 0.9 | $ | 20.3 | $ | 3.0 | $ | 20.2 | ||||||||||||||||||

| Growth capital expenditures |

$ | 40.3 | $ | 16.4 | $ | 7.4 | $ | 1.4 | $ | 0.8 | $ | 25.0 | $ | 7.1 | $ | 28.0 | ||||||||||||||||||

| Available cash for distribution(3) |

$ | 145.2 | $ | 102.0 | $ | 81.0 | $ | 32.6 | $ | 30.6 | ||||||||||||||||||||||||

| Key Operating Data (unaudited): |

||||||||||||||||||||||||||||||||||

| Production volume (thousand tons): |

||||||||||||||||||||||||||||||||||

| Ammonia (gross produced)(4) |

402.0 | 388.9 | 385.4 | 96.0 | 113.7 | |||||||||||||||||||||||||||||

| Ammonia (net available for sale)(4)(5) |

37.9 | 28.3 | 37.3 | 14.6 | 15.1 | |||||||||||||||||||||||||||||

| UAN |

930.6 | 963.7 | 928.6 | 252.1 | 248.2 | |||||||||||||||||||||||||||||

| Pet coke consumed (thousand tons) |

487.0 | 489.7 | 469.9 | 124.9 | 126.9 | |||||||||||||||||||||||||||||

| Pet coke consumed (cost per ton)(6) |

$ | 30 | $ | 28 | $ | 25 | $ | 29 | $ | 17 | ||||||||||||||||||||||||

| Sales (thousand tons): |

||||||||||||||||||||||||||||||||||

| Ammonia |

40.5 | 24.4 | 32.3 | 12.8 | 24.4 | |||||||||||||||||||||||||||||

| UAN |

904.6 | 951.0 | 939.5 | 274.5 | 267.0 | |||||||||||||||||||||||||||||

| Product pricing at gate (dollars per ton)(7): |

||||||||||||||||||||||||||||||||||

| Ammonia |

$ | 643 | $ | 518 | $ | 521 | $ | 553 | $ | 367 | ||||||||||||||||||||||||

| UAN |

$ | 282 | $ | 259 | $ | 247 | $ | 263 | $ | 209 | ||||||||||||||||||||||||

| On-stream factors(8): |

||||||||||||||||||||||||||||||||||

| Gasification |

95.6 | % | 96.8 | % | 90.2 | % | 99.4 | % | 97.7 | % | ||||||||||||||||||||||||

| Ammonia |

94.4 | % | 92.6 | % | 87.5 | % | 94.4 | % | 97.2 | % | ||||||||||||||||||||||||

| UAN |

91.9 | % | 92.0 | % | 87.3 | % | 97.8 | % | 91.4 | % | ||||||||||||||||||||||||

| Selected Data and Ratios (as adjusted for the offering): |

|

|||||||||||||||||||||||||||||||||

| Total debt(9) |

$ | 629.8 | ||||||||||||||||||||||||||||||||

| Net total debt(10) |

531.0 | |||||||||||||||||||||||||||||||||

| Cash interest expense(11) |

53.4 | |||||||||||||||||||||||||||||||||

| Ratio of total debt to Adjusted EBITDA |

3.21 | |||||||||||||||||||||||||||||||||

| Ratio of net total debt to Adjusted EBITDA |

2.71 | |||||||||||||||||||||||||||||||||

| Ratio of Adjusted EBITDA to cash interest costs |

3.67 | |||||||||||||||||||||||||||||||||

10

| (1) | EBITDA is defined as net income before (i) interest (income) expense, (ii) income tax expense and (iii) depreciation and amortization expense. Adjusted EBITDA is defined as EBITDA further adjusted for the impact of non-cash share-based compensation, and, when applicable, major scheduled turnaround expense, loss on extinguishment of debt, loss on disposition of assets and expenses associated with the Merger. |

We present EBITDA because we believe it allows users of our financial statements, such as investors and analysts, to assess our financial performance without regard to financing methods, capital structure or historical cost basis. We present Adjusted EBITDA because we have found it helpful to consider an operating measure that excludes expenses, such as major scheduled turnaround expenses, loss on extinguishment of debt, loss on disposition of assets and expenses associated with the Merger, relating to transactions not reflective of our core operations. When applicable, each of these expenses is discussed herein, so that investors have complete information about expenses. In addition, we believe that it is useful to exclude from Adjusted EBITDA non-cash share-based compensation, although it is a recurring cost incurred in the ordinary course of business. In our view, non-cash share-based compensation, which also is presented in our financial statements, reflects a non-cash cost which may obscure, for a given period, trends in the underlying business, due to the timing and nature of the equity awards. We also present Adjusted EBITDA because it is the starting point used by the board of directors of our general partner when calculating our available cash for distribution.

EBITDA and Adjusted EBITDA are not recognized terms under GAAP and should not be substituted for net income or cash flows from operations. Management believes that EBITDA and Adjusted EBITDA enable investors and analysts to better understand our ability to make distributions to common unitholders, help investors and analysts evaluate our ongoing operating results and allow for greater transparency in reviewing our overall financial, operational and economic performance by allowing investors to evaluate the same information used by management. EBITDA and Adjusted EBITDA presented by other companies may not be comparable to our presentation, since each company may define these terms differently.

A reconciliation of our Net Income to EBITDA and Adjusted EBITDA is as follows:

| Historical | Pro Forma | |||||||||||||||||||||||||||||||||

| Years Ended December 31, |

Three Months Ended March 31, |

Year Ended December 31, |

Three Months Ended March 31, |

Last Twelve Months Ended March 31, |

||||||||||||||||||||||||||||||

| 2013 | 2014 | 2015 | 2015 | 2016 | 2015 | 2016 | 2016 | |||||||||||||||||||||||||||

| (unaudited, in millions) | ||||||||||||||||||||||||||||||||||

| Net income |

$ | 118.6 | $ | 76.1 | $ | 62.0 | $ | 29.8 | $ | 18.0 | $ | 67.6 | $ | 10.6 | $ | 49.4 | ||||||||||||||||||

| Add: |

||||||||||||||||||||||||||||||||||

| Interest expense and other financing costs, net |

6.3 | 6.7 | 7.0 | 1.7 | 1.7 | 54.2 | 13.4 | 54.2 | ||||||||||||||||||||||||||

| Income tax expense (benefit) |

0.1 | — | — | — | — | — | — | — | ||||||||||||||||||||||||||

| Depreciation and amortization |

25.6 | 27.3 | 28.4 | 6.8 | 7.0 | 78.5 | 19.0 | 84.5 | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| EBITDA |

$ | 150.6 | $ | 110.1 | $ | 97.4 | $ | 38.3 | $ | 26.7 | $ | 200.3 | $ | 43.0 | $ | 188.1 | ||||||||||||||||||

| Add: |

||||||||||||||||||||||||||||||||||

| Major scheduled turnaround expenses |

— | — | 7.0 | — | — | 7.0 | — | 7.0 | ||||||||||||||||||||||||||

| Share-based compensation, non-cash |

2.2 | 0.2 | 0.1 | 0.1 | — | 1.0 | 0.2 | 0.8 | ||||||||||||||||||||||||||

| Expenses associated with the Merger |

— | — | 2.3 | — | 1.2 | — | — | — | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Adjusted EBITDA |

$ | 152.8 | $ | 110.3 | $ | 106.8 | $ | 38.4 | $ | 27.9 | $ | 208.3 | $ | 43.2 | $ | 195.9 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| (2) | Adjusted EBITDA on a pro forma basis and including the impact of the anticipated $12.0 million of synergies would have been $207.9 million for the last twelve months ended March 31, 2016. |

| (3) | The board of directors of our general partner has a policy to calculate available cash for distribution starting with Adjusted EBITDA. Available cash for distribution is defined as our Adjusted EBITDA reduced for cash needed for (i) net cash interest expense (excluding capitalized interest) and debt service and other contractual obligations; (ii) maintenance capital expenditures; and (iii) to the extent applicable, major scheduled turnaround expenses, reserves for future operating or capital needs that the board of directors of the general partner deemed necessary or appropriate, and transaction expenses associated with the Merger, if any. Available cash for distribution may be increased by the release of previously established cash reserves, if any, at the discretion of the board of directors of our general partner. Actual distributions are set by the board of directors of our general partner. The board of directors of our general partner may modify our cash distribution policy at any time, and our partnership agreement does not require us to make distributions at all. |

Available cash for distribution is not a recognized term under GAAP. Available cash for distribution should not be considered in isolation or as an alternative to net income or operating income, or any other measure of financial performance or operating performance. In addition, available cash for distribution is not presented as, and should not be considered, an alternative to cash flows from operations or as a measure of liquidity. Available cash for distribution as reported by the Partnership may not be comparable to similarly titled measures of other entities, thereby limiting its usefulness as a comparative measure.

11

A reconciliation of the available cash for distribution is as follows:

| Years Ended December 31, | Three Months Ended March 31, |

|||||||||||||||||||

| 2013 | 2014 | 2015 | 2015 | 2016 | ||||||||||||||||

| (unaudited) | ||||||||||||||||||||

| (in millions, except units and per unit data) | ||||||||||||||||||||

| Adjusted EBITDA |

$ | 152.8 | $ | 110.3 | $ | 106.8 | $ | 38.4 | $ | 27.9 | ||||||||||

| Adjustments: |

||||||||||||||||||||

| Less: |

||||||||||||||||||||

| Net cash interest expense (excluding capitalized interest) and debt service |

(5.4 | ) | (5.8 | ) | (6.0 | ) | (1.5 | ) | (1.5 | ) | ||||||||||

| Maintenance capital expenditures |

(3.5 | ) | (4.7 | ) | (9.6 | ) | (1.3 | ) | (0.9 | ) | ||||||||||

| Major scheduled turnaround expenses |

— | — | (7.0 | ) | — | — | ||||||||||||||

| Cash reserves for future turnaround expenses |

— | — | (7.9 | ) | (3.0 | ) | — | |||||||||||||

| Cash reserves for future operating needs |

(2.2 | ) | — | — | — | — | ||||||||||||||

| Expenses associated with the Merger |

— | — | (2.3 | ) | — | (1.2 | ) | |||||||||||||

| Plus: |

||||||||||||||||||||

| Release of cash reserves established for turnaround expenses |

— | — | 7.0 | — | — | |||||||||||||||

| Release of previously established cash reserves |

2.5 | 2.2 | — | — | — | |||||||||||||||

| Available cash associated with CVR Nitrogen 2016 first quarter |

— | — | — | — | 6.3 | |||||||||||||||

| Other non-cash adjustments |

1.0 | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Available cash for distribution |

$ | 145.2 | $ | 102.0 | $ | 81.0 | $ | 32.6 | $ | 30.6 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (4) | Gross tons produced for ammonia represent total ammonia produced, including ammonia produced that was upgraded to UAN. Net tons available for sale represent ammonia available for sale that was not upgraded into UAN. |

| (5) | Includes purchased ammonia. |

| (6) | Our pet coke cost per ton purchased from CVR Refining averaged $19, $24, and $27 for the years ended December 31, 2015, 2014 and 2013, respectively. Third-Party per coke prices averaged $40, $41 and $40 for the year ended December 31, 2015, 2014 and 2013, respectively. Our pet coke cost per ton purchased from CVR Refining averaged $9 and $21 for the three months ended March 31, 2016 and 2015, respectively. Third-Party pet coke prices averaged $33 and $44 for the three months ended March 31, 2016 and 2015, respectively. |

| (7) | Product pricing at gate represents net sales less freight revenue divided by product sales volume in tons, and is shown in order to provide a pricing measure that is comparable across the fertilizer industry. |

| (8) | On-stream factor is the total number of hours operated divided by the total number of hours in the reporting period and is included as a measure of operating efficiency. |

| (9) | Total debt was $629.8 million, or $623.1 million net of $6.7 million unamortized debt issue costs. |

| (10) | Net total debt is defined as total debt less cash. |

| (11) | Cash interest expense relates to estimated cash interest expense on the notes issued in this offering and the remaining $4.8 million untendered 2021 Notes. |

12

SUMMARY CONSOLIDATED HISTORICAL FINANCIAL DATA—CVR NITROGEN

The following tables include CVR Nitrogen’s selected summary financial data as of and for the years ended December 31, 2013, 2014 and 2015, which are derived from the audited income statements and cash flow financial statements of CVR Nitrogen for the corresponding periods, the audited balance sheets of CVR Nitrogen for the corresponding periods in 2015 and 2014, the unaudited balance sheets of CVR Nitrogen as of December 31, 2013 and the unaudited financial statements of CVR Nitrogen for the three months ended March 31, 2015 and 2016, which are derived from the unaudited financial statements of CVR Nitrogen for the corresponding periods. You should read the following data in conjunction with CVR Nitrogen’s audited and unaudited financial statements included in CVR Partners’ Current Report on Form 8-K filed on May 25, 2016. You should not assume results of operations for any past period indicates results for any future period. The selected balance sheet data as of March 31, 2015 and December 31, 2013 is derived from the unaudited financial statements of CVR Nitrogen, which are not included herein.

On March 14, 2016, CVR Nitrogen completed the sale of Rentech Nitrogen Pasadena Holdings, LLC and its subsidiaries, which owned and operated the Pasadena Facility. As a result of the sale, CVR Nitrogen classified its consolidated balance sheets and consolidated statements of operations for all periods presented in the table below to reflect the Pasadena Facility as discontinued operations. All discussions and amounts in the tables below for all periods presented, exclude the financial results attributable to the Pasadena Facility, unless otherwise noted.

| In millions, or as otherwise indicated | Years Ended December 31, | Three Months Ended March 31, |

||||||||||||||||||

| 2013 | 2014 | 2015 | 2015 | 2016 | ||||||||||||||||

| (unaudited) | ||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||

| Revenues |

$ | 177.7 | $ | 196.4 | $ | 201.3 | $ | 36.8 | $ | 34.8 | ||||||||||

| Cost of sales |

96.8 | 121.6 | 105.2 | 19.4 | 20.3 | |||||||||||||||

| Gross profit |

80.9 | 74.8 | 96.1 | 17.4 | 14.5 | |||||||||||||||

| Total operating expenses |

13.5 | 13.6 | 16.4 | 3.6 | 3.7 | |||||||||||||||

| Operating income (loss) |

67.4 | 61.2 | 79.8 | 13.8 | 10.8 | |||||||||||||||

| Total other income (expense), net |

(20.1 | ) | (19.9 | ) | (21.8 | ) | (5.0 | ) | (5.6 | ) | ||||||||||

| Income from continuing operations before income taxes |

47.3 | 41.3 | 58.0 | 8.8 | 5.2 | |||||||||||||||

| Income tax expense (benefit) |

0.3 | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income from continuing operations |

47.6 | 41.3 | 58.0 | 8.8 | 5.2 | |||||||||||||||

| Income (loss) from discontinued operations, net of tax |

(43.5 | ) | (42.4 | ) | (159.5 | ) | 0.2 | (2.5 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

$ | 4.1 | $ | (1.1 | ) | $ | (101.5 | ) | $ | 9.0 | $ | 2.7 | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Balance Sheet Data: |

||||||||||||||||||||

| Cash |

$ | 31.2 | $ | 24.5 | $ | 7.2 | $ | 31.1 | $ | 33.8 | ||||||||||

| Working capital |

$ | 16.8 | $ | 3.1 | $ | (2.8 | ) | $ | 0.1 | $ | 15.6 | |||||||||

| Total assets |

$ | 209.1 | $ | 212.3 | $ | 201.9 | $ | 227.1 | $ | 240.1 | ||||||||||

| Total debt, net of unamortized debt issuance costs |

$ | 311.6 | $ | 326.7 | $ | 347.6 | $ | 331.0 | $ | 362.5 | ||||||||||

| Statement of Cash Flows Data: |

||||||||||||||||||||

| Net cash flow provided by (used in): |

||||||||||||||||||||

| Operating activities(1) |

$ | 44.5 | $ | 64.9 | $ | 79.5 | $ | 22.5 | $ | 20.9 | ||||||||||

| Investing activities(2) |

(90.5 | ) | (72.6 | ) | (36.4 | ) | (10.4 | ) | (9.3 | ) | ||||||||||

| Financing activities(3) |

24.3 | 1.6 | (55.2 | ) | (7.7 | ) | 6.4 | |||||||||||||

| Net increase (decrease) in cash and cash equivalents |

(21.7 | ) | (6.0 | ) | (12.2 | ) | 4.4 | 17.9 | ||||||||||||

13

| In millions, or as otherwise indicated | Years Ended December 31, | Three Months Ended March 31, |

||||||||||||||||||

| 2013 | 2014 | 2015 | 2015 | 2016 | ||||||||||||||||

| (unaudited) | ||||||||||||||||||||

| Net cash provided by (used in) operating activities from discontinued operations |

28.8 | 47.4 | 13.9 | 1.2 | (4.2 | ) | ||||||||||||||

| Net cash provided by (used in) investing activities from discontinued operations |

(32.3 | ) | (46.8 | ) | (8.8 | ) | (3.4 | ) | (4.4 | ) | ||||||||||

| Net cash provided by (used in) discontinued operations |

(3.4 | ) | 0.6 | 5.1 | (2.2 | ) | (8.6 | ) | ||||||||||||

| Other Data: |

||||||||||||||||||||

| Adjusted EBITDA (unaudited)(4) |

$ | 83.0 | $ | 78.1 | $ | 102.6 | $ | 17.4 | $ | 15.7 | ||||||||||

| Maintenance capital expenditures (unaudited)(5) |

9.3 | 9.4 | 10.7 | 1.8 | 2.1 | |||||||||||||||

| Growth capital expenditures (unaudited)(5) |

50.5 | 14.4 | 17.6 | 2.7 | 6.3 | |||||||||||||||

| Key Operating Data (unaudited and excluding the Pasadena Facility): |

||||||||||||||||||||

| Production (tons, in thousands): |

||||||||||||||||||||

| Ammonia |

244.4 | 324.1 | 340.3 | 83.8 | 87.0 | |||||||||||||||

| UAN |

262.1 | 269.2 | 279.0 | 69.9 | 84.8 | |||||||||||||||

| Natural gas used in production: |

||||||||||||||||||||

| Volume (in thousands of MMBtu) |

8,942 | 11,487 | 12,301 | 3,021 | 3,207 | |||||||||||||||

| Pricing ($ per MMBtu) |

$ | 4.18 | $ | 4.98 | $ | 3.53 | $ | 4.68 | $ | 3.19 | ||||||||||

| Products sold (tons, in thousands): |

||||||||||||||||||||

| Ammonia |

102.7 | 152.7 | 186.3 | 30.6 | 43.8 | |||||||||||||||

| UAN |

268.9 | 266.9 | 275.7 | 48.1 | 49.0 | |||||||||||||||

| Products pricing (dollars per ton) |

||||||||||||||||||||

| Ammonia |

$ | 650 | $ | 549 | $ | 538 | $ | 520 | $ | 404 | ||||||||||

| UAN |

$ | 295 | $ | 280 | $ | 255 | $ | 267 | $ | 228 | ||||||||||

| Natural gas in cost of sales, excluding gas derivatives: |

||||||||||||||||||||

| Volume (MMBtu) |

10,085 | 11,335 | 12,348 | 2,186 | 2,657 | |||||||||||||||

| Pricing ($ per MMBtu) |

$ | 4.16 | $ | 5.00 | $ | 3.74 | $ | 3.59 | $ | 3.18 | ||||||||||

| On-stream factors(6): |

||||||||||||||||||||

| Ammonia |

83.6 | % | 95.6 | % | 98.4 | % | 100 | % | 100 | % | ||||||||||

| UAN |

84.1 | % | 95.3 | % | 97.0 | % | 100 | % | 100 | % | ||||||||||

| (1) | Includes Operating activities at the Pasadena Facility. |

| (2) | Includes Investing activities at the Pasadena Facility. |

| (3) | Includes Financing activities at the Pasadena Facility. |

| (4) | Excludes Adjusted EBITDA at the Pasadena Facility. EBITDA is defined as net income before (i) interest (income) expense, (ii) income tax expense and (iii) depreciation and amortization expense. Adjusted EBITDA is defined as EBITDA further adjusted for the impact of non-cash share-based compensation, and, when applicable, major scheduled turnaround expense, loss on extinguishment of debt, loss on disposition of assets and expenses associated with the Merger. |

We present EBITDA because we believe it allows users of our financial statements, such as investors and analysts, to assess our financial performance without regard to financing methods, capital structure or historical cost basis. We present Adjusted EBITDA because we have found it helpful to consider an operating measure that excludes expenses, such as major scheduled turnaround expenses, loss on extinguishment of debt, loss on disposition of assets and expenses associated with the Merger, relating to transactions not reflective of our core operations. When applicable, each of these expenses is discussed

14

herein, so that investors have complete information about expenses. In addition, we believe that it is useful to exclude from Adjusted EBITDA non-cash share-based compensation, although it is a recurring cost incurred in the ordinary course of business. In our view, non-cash share-based compensation, which also is presented in our financial statements, reflects a non-cash cost which may obscure, for a given period, trends in the underlying business, due to the timing and nature of the equity awards. We also present Adjusted EBITDA because it is the starting point used by the board of directors of our general partner when calculating our available cash for distribution.

EBITDA and Adjusted EBITDA are not recognized terms under GAAP and should not be substituted for net income or cash flows from operations. Management believes that EBITDA and Adjusted EBITDA enable investors and analysts to better understand our ability to make distributions to common unitholders, help investors and analysts evaluate our ongoing operating results and allow for greater transparency in reviewing our overall financial, operational and economic performance by allowing investors to evaluate the same information used by management. EBITDA and Adjusted EBITDA presented by other companies may not be comparable to our presentation, since each company may define these terms differently.

A reconciliation of our Net Income to EBITDA and Adjusted EBITDA, exclusive of amounts attributable to the Pasadena Facility is as follows:

| Years Ended December 31, | Three Months Ended March 31, |

|||||||||||||||||||

| 2013 | 2014 | 2015 | 2015 | 2016 | ||||||||||||||||

| (unaudited, in millions) | ||||||||||||||||||||

| Net income from continuing operations |

$ | 47.6 | $ | 41.3 | $ | 58.0 | $ | 8.8 | $ | 5.2 | ||||||||||

| Add: |

||||||||||||||||||||

| Interest expense and other financing costs, net |

14.1 | 19.1 | 21.7 | 5.0 | 5.6 | |||||||||||||||

| Income tax expense (benefit) |

(0.2 | ) | — | — | — | — | ||||||||||||||

| Depreciation and amortization |

9.2 | 15.9 | 18.3 | 3.3 | 4.0 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| EBITDA |

$ | 70.7 | $ | 76.3 | $ | 98.0 | $ | 17.1 | $ | 14.8 | ||||||||||

| Add: |

||||||||||||||||||||

| Major scheduled turnaround expenses |

4.9 | — | — | — | — | |||||||||||||||

| Share-based compensation, non-cash |

1.4 | 1.2 | 0.9 | 0.3 | 0.2 | |||||||||||||||

| Loss on debt extinguishment |

6.0 | 0.6 | — | — | — | |||||||||||||||

| Expenses associated with the Merger |

— | — | 3.7 | — | 0.7 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted EBITDA |

$ | 83.0 | $ | 78.1 | $ | 102.6 | $ | 17.4 | $ | 15.7 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (5) | Excludes expenditures at the Pasadena Facility. |

| (6) | The respective on-stream factors for the ammonia and UAN plant equal the total days the applicable plant operated in any given period, divided by the total days in that period. |

15

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

CVR Partners – Coffeyville Facility

Major Influences on Results of Operations

Our earnings and cash flows from operations are primarily affected by the relationship between nitrogen fertilizer product prices, on-stream factors and direct operating expenses. Natural gas is the most significant raw material required in our competitors’ production of nitrogen fertilizer. Our Coffeyville Facility does not use natural gas as a feedstock and uses a minimal amount of natural gas as an energy source in our operations. Instead, CVR Refining’s adjacent refinery supplies us with most of the pet coke feedstock we need pursuant to a 20-year pet coke supply agreement entered into in October 2007. The price at which our products are ultimately sold depends on numerous factors, including the global supply and demand for nitrogen fertilizer products which, in turn, depends on, among other factors, world grain demand and production levels, changes in world population, the cost and availability of fertilizer transportation infrastructure, weather conditions, the availability of imports and the extent of government intervention in agriculture markets.

Nitrogen fertilizer prices are also affected by local factors, including local market conditions and the operating levels of competing facilities. An expansion or upgrade of competitors’ facilities, political and economic developments and other factors are likely to continue to play an important role in nitrogen fertilizer industry economics. These factors can impact, among other things, the level of inventories in the market, resulting in price volatility and a reduction in product margins. Moreover, the industry typically experiences seasonal fluctuations in demand for nitrogen fertilizer products.

As a result of a favorable global demand environment for grains, nitrogen fertilizer prices rose to near historic levels beginning in 2011. In addition, North American producers began to benefit from lower natural gas prices due to the significant increase in shale basin and other non-conventional production in the region. The combination of higher nitrogen fertilizer prices globally and a feedstock cost advantage led to high margins for North American nitrogen fertilizer producers. This resulted in numerous announcements for expansion plans for existing plants as well as new facility development in the corn belt and the gulf coast. The majority of the additional supply from this expansion phase in North America is expected to come online in 2016. We expect product pricing may experience volatility as the new supply displaces imports into the gulf coast and corn belt. However, over the longer-term the U.S. is expected to remain a net importer of nitrogen fertilizer with domestic prices influenced by the higher cost of imported tons into the United States.

Since mid-2013, global nitrogen fertilizer prices have trended down as global grain supply increased and growth in grain demand slowed due to more challenging worldwide economic considerations. During 2015, there were announced transactions for further

16

consolidation in the North American nitrogen fertilizer market, including our definitive merger agreement under which we acquired all outstanding units of CVR Nitrogen.

While there is risk of short-term volatility given the inherent nature of the commodity cycle, the longer-term fundamentals for the U.S. nitrogen fertilizer industry remain intact. We view the anticipated combination of (i) increasing global population, (ii) decreasing arable land per capita, (iii) continued evolution to more protein-based diets in developing countries, (iv) sustained use of corn as feedstock for the domestic production of ethanol and (v) positioning at the lower end of the global cost curve will continue to provide a solid foundation for nitrogen fertilizer producers in the U.S.

In order to assess our operating performance, we calculate the product pricing at gate as an input to determine our operating margin. Product pricing at gate represents net sales less freight revenue divided by product sales volume in tons. We believe product pricing at gate is a meaningful measure because we sell products at our plant gate and terminal locations’ gates (“sold gate”) and delivered to the customer’s designated delivery site (“sold delivered”). The relative percentage of sold gate versus sold delivered can change period to period. The product pricing at gate provides a measure that is consistently comparable period to period.

We and other competitors in the U.S. farm belt share a significant transportation cost advantage when compared to our out-of-region competitors in serving the U.S. farm belt agricultural market; therefore we are able to cost-effectively sell substantially all of our products in the higher margin agricultural market. Further, we believe a significant portion of our competitors’ revenues are derived from the lower margin industrial market. Our products leave our Coffeyville Facility either in railcars for destinations located principally on the Union Pacific Railroad or in trucks for direct shipment to customers. We do not currently incur significant intermediate transfer, storage, barge freight or pipeline freight charges; however, we do incur costs to maintain and repair our railcar fleet. Selling products to customers within economic rail transportation limits of the Coffeyville Facility and keeping transportation costs low are keys to maintaining profitability.

As a result of the UAN expansion project completed in 2013, we will continue to upgrade substantially all of our ammonia production into UAN for as long as it makes economic sense to do so. The value of nitrogen fertilizer products is also an important consideration in understanding our results. For the years ended December 31, 2015 and 2014, we upgraded approximately 96% and 97%, respectively, of our ammonia production into UAN, a product that presently generates greater profit than ammonia.

The high fixed cost of our direct operating expense structure also directly affects our profitability. Our Coffeyville Facility’s pet coke gasification process results in a significantly higher percentage of fixed costs than a natural gas-based fertilizer plant. Major fixed operating expenses of our Coffeyville Facility include a large portion of electrical energy, employee labor, maintenance, including contract labor and outside services. We estimate these fixed costs averaged approximately 80% of direct operating expenses over the 24 months ended March 31, 2016.

Our largest raw material expense used in the production of ammonia at our Coffeyville Facility is pet coke, which we purchase from CVR Refining and third parties. For the three months ended March 31, 2016 and 2015, we incurred approximately $2.1 million and $3.6 million, respectively, for the cost of pet coke, which equaled an average cost per ton of $17 and $29, respectively.

Agreements with CVR Energy and CVR Refining

We are party to several agreements with CVR Energy and its affiliates that govern the business relations among us, CVR Energy and its subsidiaries (including CVR Refining), and our general partner. These include the pet coke supply agreement under which we buy the pet coke we use in our Coffeyville Facility; a services agreement, under which CVR Energy and its subsidiaries provide us with management services including the services of its senior management team; a feedstock and shared services agreement, which governs the provision of feedstocks for our Coffeyville Facility, including, but not limited to, hydrogen, high-pressure steam, nitrogen, instrument air, oxygen and natural gas; a raw water and facilities sharing agreement, which allocates raw water resources between the two businesses; an easement agreement; an environmental agreement which, among other matters, allocates liability and responsibility for remediating contamination at the Coffeyville Facility; a lease agreement pursuant to which we lease office space and laboratory space; and certain financing agreements that we entered into in connection with the Merger. These agreements were not the result of arm’s-length negotiations and the terms of these agreements are not necessarily as favorable to the parties to these agreements as terms which could have been obtained from unaffiliated third parties.

Factors Affecting Comparability

Our historical results of operations for the periods presented may not be comparable with prior periods or to our results of operations in the future for the reasons discussed below.

17

2015 Turnaround

During the third quarter of 2015, the Coffeyville Facility completed a major scheduled turnaround and the gasification, ammonia and UAN units were down for between 17 to 20 days each. Overall results were negatively impacted due to the lost production during the downtime that resulted in reduced sales and certain reduced variable expenses included in cost of product sold (exclusive of depreciation and amortization) and direct operating expenses (exclusive of depreciation and amortization). Costs of approximately $7.0 million associated with the 2015 turnaround are included in direct operating expenses (exclusive of depreciation and amortization) in the Consolidated Statements of Operations for the year ended December 31, 2015.

Linde Air Separation Unit Related Downtime

Linde owns, operates, and maintains the air separation plant that provides contract volumes of oxygen, nitrogen, and compressed dry air to our Coffeyville Facility. During the third quarter of 2015, the Linde air separation unit experienced downtime, in excess of the downtime associated with the major scheduled turnaround discussed above, that resulted in the gasification, ammonia and UAN units being down for between 16 to 19 days each. Overall results were negatively impacted due to the lost production during the downtime that resulted in reduced sales and certain reduced variable expenses included in cost of product sold (exclusive of depreciation and amortization) and direct operating expenses (exclusive of depreciation and amortization) for the year ended December 31, 2015.

The Merger

On April 1, 2016, we completed the Merger, which is not reflected in our results of operations.

Results of Operations

The period to period comparisons of CVR Partners’ results of operations have been prepared using the historical periods included in CVR Partners’ consolidated financial statements. In order to effectively review and assess our historical financial information, we have also included supplemental operating measures and industry measures that we believe are material to understanding our business.

Three Months Ended March 31, 2016 Compared to the Three Months Ended March 31, 2015

Net Sales. Net sales were $73.1 million for the three months ended March 31, 2016 compared to $93.1 million for the three months ended March 31, 2015. The decrease of $20.0 million was primarily the result of lower UAN sales prices ($14.2 million), lower hydrogen sales volumes ($4.8 million), lower ammonia sales prices ($4.6 million) and lower UAN sales volumes ($2.1 million), partially offset by higher ammonia sales volumes ($6.5 million). For the three months ended March 31, 2016, UAN and ammonia made up $62.6 million and $9.1 million of our net sales, respectively. This compared to UAN and ammonia net sales of $78.9 million and $7.2 million, respectively, for the three months ended March 31, 2015. The following table demonstrates the impact of changes in sales volumes and pricing for UAN, ammonia and hydrogen for the three months ended March 31, 2016 as compared to the three months ended March 31, 2015:

| Three Months Ended March 31, 2016 |

Three Months Ended March 31, 2015 |

Total Variance | Price Variance |

Volume Variance |

||||||||||||||||||||||||||||||||||||

| Volume(1) | $ per ton(2) | Sales $(3) | Volume(1) | $ per ton(2) | Sales $(3) | Volume(1) | Sales $(3) | |||||||||||||||||||||||||||||||||

| UAN |

267,049 | $ | 234 | $ | 62.6 | 274,540 | $ | 288 | $ | 78.9 | (7,491 | ) | $ | (16.3 | ) | $ | (14.2 | ) | $ | (2.1 | ) | |||||||||||||||||||

| Ammonia |

24,397 | $ | 373 | $ | 9.1 | 12,821 | $ | 562 | $ | 7.2 | 11,576 | $ | 1.9 | $ | (4.6 | ) | $ | 6.5 | ||||||||||||||||||||||

| Hydrogen |

160,408 | $ | 7 | $ | 1.1 | 600,278 | $ | 11 | $ | 6.5 | (439,870 | ) | $ | (5.4 | ) | $ | (0.6 | ) | $ | (4.8 | ) | |||||||||||||||||||

| (1) | UAN and ammonia sales volumes are in tons. Hydrogen sales volumes are in MSCF. |

| (2) | Includes freight charges. Hydrogen is based on $ per MSCF. |

| (3) | Sales dollars in millions. |

The decrease in UAN and ammonia sales prices for the three months ended March 31, 2016 compared to the three months ended March 31, 2015 was primarily attributable to pricing fluctuation in the market. The increase of ammonia sales volume for the three months ended March 31, 2016 compared to the three months ended March 31, 2015 was primarily attributable to the timing of customer demand. On-stream factors (total number of hours operated divided by total hours in the reporting period) for the gasification, ammonia and UAN units were 97.7%, 97.2% and 91.4%, respectively, for the three months ended March 31, 2016. Product pricing at gate for the three months ended March 31, 2016 compared to the three months ended March 31, 2015 decreased 20.5% for UAN and decreased 33.6% for ammonia.

18

Cost of Product Sold (Exclusive of Depreciation and Amortization). Cost of product sold (exclusive of depreciation and amortization) consists primarily of freight and distribution expenses, pet coke expense, purchased ammonia and purchased hydrogen. Cost of product sold (exclusive of depreciation and amortization) for the three months ended March 31, 2016 was $16.3 million, compared to $25.8 million for the three months ended March 31, 2015. The $9.5 million decrease resulted from lower costs from transactions with third parties of $8.5 million and affiliates of $1.0 million. The lower third-party costs incurred during the three months ended March 31, 2016 was primarily the result of less purchased ammonia and third-party coke costs. The lower affiliate costs incurred during the three months ended March 31, 2016 were primarily the result of lower expense of CVR Refining pet coke. The decrease in affiliate and third-party coke expense was primarily related to decreased market prices of petroleum coke.

Direct Operating Expenses (Exclusive of Depreciation and Amortization). Direct operating expenses (exclusive of depreciation and amortization) consist primarily of energy and utility costs, direct costs of labor, property taxes, plant-related maintenance services and environmental and safety compliance costs as well as catalyst and chemical costs. Direct operating expenses (exclusive of depreciation and amortization) for the three months ended March 31, 2016 were $23.7 million as compared to $24.4 million for the three months ended March 31, 2015. The $0.7 million decrease resulted primarily from lower utilities, net ($1.7 million), partially offset by higher outside services ($1.0 million). The lower utilities, net is primarily the result of lower electrical rates.

Selling, General and Administrative Expenses (Exclusive of Depreciation and Amortization). Selling, general and administrative expenses include the direct selling, general and administrative expenses of our business as well as certain expenses incurred by our affiliates, CVR Energy and Coffeyville Resources, on our behalf and billed or allocated to us in accordance with the applicable agreements. We also reimburse our general partner in accordance with the partnership agreement for expenses it incurs on our behalf. Reimbursed expenses to our general partner are included as selling, general and administrative expenses from affiliates. Selling, general and administrative expenses (exclusive of depreciation and amortization) were $6.4 million for the three months ended March 31, 2016 and $4.6 million for the three months ended March 31, 2015. The $1.8 million increase resulted primarily from a $1.6 million increase in costs of transactions with third parties and a $0.2 million increase in costs of transactions with affiliates. The overall variance was primarily the result of expenses associated with the Merger ($1.2 million), higher labor ($0.4 million) and higher bad debt reserves ($0.2 million) during the three months ended March 31, 2016.

Operating Income. Operating income was $19.7 million for the three months ended March 31, 2016, as compared to operating income of $31.5 million for the three months ended March 31, 2015. The decrease of $11.8 million for the three months ended March 31, 2016 as compared to the three months ended March 31, 2015 was the result of the decrease in net sales ($20.0 million) and increases in selling general and administrative expenses ($1.8 million) and depreciation and amortization ($0.2 million), partially offset by decreases in cost of product sold ($9.5 million) and in direct operating expenses ($0.7 million).

Year Ended December 31, 2015 Compared to the Year Ended December 31, 2014

Net Sales. Net sales were $289.2 million for the year ended December 31, 2015, compared to $298.7 million for the year ended December 31, 2014. The net sales decrease of $9.5 million for the year ended December 31, 2015 as compared to the year ended December 31, 2014 was primarily the result of lower UAN sales prices ($11.6 million), lower UAN sales volumes ($3.3 million), and lower hydrogen sales prices ($0.3 million), partially offset by higher ammonia sales volumes ($4.2 million) and higher hydrogen sales volumes ($2.0 million). For the year ended December 31, 2015, UAN, ammonia and hydrogen made up $258.8 million, $17.2 million, and $11.8 million of our net sales, respectively. This compared to UAN, ammonia and hydrogen net sales of $273.7 million, $13.1 million and $10.1 million, respectively, for the year ended December 31, 2014. The following table demonstrates the impact of changes in sales volumes and sales price for UAN, ammonia and hydrogen for the year ended December 31, 2015 compared to the year ended December 31, 2014.

| Year Ended December 31, 2015 | Year Ended December 31, 2014 | Total Variance | Price Variance |

Volume Variance |

||||||||||||||||||||||||||||||||||||