Attached files

| file | filename |

|---|---|

| EX-32.2 - CERTIFICATION - Edge Data Solutions, Inc. | safelane_10k-ex3202.htm |

| EX-32.1 - CERTIFICATION - Edge Data Solutions, Inc. | safelane_10k-ex3201.htm |

| EX-31.2 - CERTIFICATION - Edge Data Solutions, Inc. | safelane_10k-ex3102.htm |

| EX-31.1 - CERTIFICATION - Edge Data Solutions, Inc. | safelane_10k-ex3101.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_____________

FORM 10-K

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2015

| [_] | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

COMMISSION FILE NO. 333-198435

SAFE LANE SYSTEMS, INC.

(EXACT NAME OF REGISTRANT SPECIFIED IN ITS CHARTER)

| COLORADO | 46-3892319 | |

| (STATE OR OTHER JURISDICTION | (I.R.S. EMPLOYER | |

| OF INCORPORATION OR ORGANIZATION) | IDENTIFICATION NUMBER) | |

| 1624 MARKET STREET, SUITE 202 | ||

| DENVER, CO | 80202 | |

| (ADDRESS OF PRINCIPAL EXECUTIVE OFFICES) | (ZIP CODE) |

(949) 825-6512

(REGISTRANT'S TELEPHONE NUMBER, INCLUDING AREA CODE)

Securities registered pursuant to Section 12(b) of the Act: NONE

Securities to be registered pursuant to Section 12(g) of the Act: COMMON STOCK, $0.0001 PAR VALUE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| Yes | [_] | No | [x] |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

| Yes | [_] | No | [x] |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| Yes | [x] | No | [_] |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check One).

| Large accelerated filer | [_] | Accelerated filer | [_] | |

|

Non-accelerated filer (Do not check if a smaller reporting company) |

[_] | Smaller reporting company | [x] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| Yes | [_] | No | [x] |

As of April 14, 2016 there were 25,118,273 shares outstanding of the issuer’s common stock, par value $0.0001 per share of which 23,118,273 shares were held by non-affiliates. There were 10,000,000 shares of the Issuer’s Class “A” preferred stock outstanding, par value $0.0001 per share.

TABLE OF CONTENTS

| ITEM | DESCRIPTION | PAGE |

| Part I | ||

| Item 1. | Business | 3 |

| Item 1A. | Risk Factors | 16 |

| Item 1B. | Unresolved Staff Comments | 25 |

| Item 2. | Description of Properties | 25 |

| Item 3. | Legal Proceedings | 25 |

| Item 4. | Mine Safety Disclosures | 25 |

| Part II | ||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters, and Issuer Purchases of Equity Securities | 26 |

| Item 6. | Selected Financial Data | 26 |

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 26 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 32 |

| Item 8. | Financial Statements and Supplementary Data | 32 |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 43 |

| Item 9A. | Controls and Procedures | 43 |

| Item 9B. | Other Information | 44 |

| Part III | ||

| Item 10. | Directors, Executive Officers and Corporate Governance | 45 |

| Item 11. | Executive Compensation | 47 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 49 |

| Item 13. | Certain Relationships and Related Transactions and Director Independence | 50 |

| Item 14. | Principal Accountant Fees and Services | 51 |

| Part IV | ||

| Item 15. | Exhibits and Financial Statement Schedules | 52 |

| Signatures | 53 |

| 1 |

FORWARD-LOOKING STATEMENTS

In addition to historical information, some of the information presented in this Annual Report on Form 10-K contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 (the “Reform Act”). Although Safe Lane Systems, Inc. (“Safe Lane” or the “Company”, which may also be referred to as “we”, “us” or “our”) believes that its expectations are based on reasonable assumptions within the bounds of its knowledge of its business and operations: there can be no assurance that actual results will not differ materially from our expectations. Such forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those anticipated. Cautionary statements regarding the risks, uncertainties and other factors associated with these forward-looking statements are discussed under "Risk Factors" in this Form 10-K. You are urged to carefully consider these factors, as well as other information contained in this Form 10-K and in our other periodic reports and documents filed with the SEC.

| 2 |

PART I

ITEM 1. BUSINESS

Company History and Overview

History of Safe Lane Systems, Inc., a Colorado corporation

Safe Lane Systems, Inc. (“Safe Lane Systems”, “Safe Lane Systems,” “We,” “Us,” “Our,” or “Company” hereafter), was incorporated in the State of Colorado on September 10, 2013. We were formed to engage in the sale of traffic safety equipment. We may also engage in any other business permitted by law, as designated by the Board of Directors of our Company.

We have licensed and sub-licensed I.P. for a spring traffic cone dispenser designed to protect highway workers, first responders to vehicle collisions and highway incidents, law enforcement personnel, towing operators, private and public utility workers, as well as pedestrians and motorists. Our flagship product, The Kone General Automatic Safety Cone Deployment System, is the world’s first and only portable safety cone dispensing system. Safe D-Ploy Spring Cones are patented MUTCD (Manual on Uniform Traffic Control Devices) compliant highway safety cones. We must commence manufacture and sales by January 1, 2016.

We have begun initial minimal operations and currently have only had one revenue transaction for $1,725. We had three contract employees at December 31, 2015, our CEO, marketing director and sales manager. Since that time the marketing director and sales manager have resigned. Upon formation, the founder, our CEO and Chairman, Paul D. Dickman, purchased 2,000,000 shares of the Company’s common stock as a price of $0.0005, per share for a total price of $1,000 and in addition he was granted 10,000,000 ($0.0001 par value) shares of Class “A” Super Majority Voting stock for organizational services.

We engaged a marketing consultant to develop a marketing and sales plan for both the spring traffic cone and our automatic traffic cone dispenser. The consultant’s final marketing plan was received and approved in 2015 We have engaged and are currently under agreement with a globally recognized manufacturer’s representation firm, The Johander Company of Minneapolis, to help guide us into retail markets, build a manufacturer’s representative network, and drive retail sales of our Spring Cone and Safe-D-ploy product accessories. Johander was founded in 1987 by Bill Johander and remains a family business operated by his daughter Jennifer who joined the company after a successful career at Target Stores. We will pursue under a ‘pay for success’ commission structure the following existing Johander retail relationships including; Target and Target.com, Bluestem Brands (Fingerhut), Meijer, Menard’s, Home Depot, Lowe’s, Advance Auto, Sam’s Club and Gander Mountain, Walmart, Costco, Dick's Sporting Goods, Sports Authority, Academy Amazon, NAPA, Auto Zone, O'Reillys, Pep Boys, AC Delco, ULine, Grainger, Gempler's, Toys R Us, and Streicher's. Through this relationship we expect to have a new manufacture in place by the end of the year at no additional costs until such time as manufacturing begins.

We began marketing our products in early 2015 based upon the recommendation of our marketing consultants. We expect we will need to raise an additional $1,250,000 in equity financing prior to implementing our full marketing and sales plan. We owe a note payable of $395,000 that was due December 31, 2015. As we are currently unable to pay this note the Company is in the process or refinancing the note.

We are in the developmental stage of our business. Since our incorporation September 2013, we have been engaged in securing both exclusive and non-exclusive license agreements for our key products, designing a marketing plan, and lining up suppliers and manufacturers for production.

During the 2015 fiscal year, we focused our efforts on our product launch and marketing of the Kone General Automatic Safety Cone Deployment System. We must commence manufacture and sales by January 1, 2016 or our licenses will be in default. Since we sold one unit in 2015 this requirement has been met.

Our Auditors have issued a going concern opinion and the reasons noted for issuing the opinion are our lack of revenues or business and very modest capital.

As of December 31, 2015, we had approximately $15,000 in cash on hand. Our current monthly cash burn rate is approximately $12,500, and it is expected that burn rate will continue until significant additional capital is raised and our marketing plan is executed. Once additional capital is raised to support our marketing efforts, we expect to increase our monthly general and administrative cash burn rate to approximately $25,000 per month until revenue is generated to offset this expense. Based upon our current burn rate, we will use all current cash by the end of January 2016. We will need to raise an additional approximately $1,250,000 to execute our plan of operations.

| 3 |

Implications of Being an Emerging Growth Company

We qualify as an emerging growth company as that term is used in the JOBS Act. An emerging growth company may take advantage of specified reduced reporting and other burdens that are otherwise applicable generally to public companies. These provisions include:

· A requirement to have only two years of audited financial statements and only two years of related MD&A;

· Exemption from the auditor attestation requirement in the assessment of the emerging growth company’s internal control over financial reporting under Section 404 of the Sarbanes-Oxley Act of 2002;

· Reduced disclosure about the emerging growth company’s executive compensation arrangements; and

· No non-binding advisory votes on executive compensation or golden parachute arrangements.

We have already taken advantage of these reduced reporting burdens in this prospectus, which are also available to us as a smaller reporting company as defined under Rule 12b-2 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)2(B) of the Securities Act of 1933, as amended (the “Securities Act”) for complying with new or revised accounting standards. We have elected to use the extended transition period provided above and therefore our financial statements may not be comparable to companies that comply with public company effective dates.

We could remain an emerging growth company for up to five years, or until the earliest of (i) the last day of the first fiscal year in which our annual gross revenues exceed $1 billion, (ii) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act, which would occur if the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, or (iii) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three year period.

For more details regarding this exemption, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Critical Accounting Policies.”

COMPANY BUSINESS OVERVIEW

Our Company, Safe Lane Systems, Inc., was formed to develop the marketing and contract the manufacturing of certain products resulting from development of IP in design and manufacturing by Superior Traffic Controls, Inc. We licensed certain IP under a Master License and a Sub License to capitalize the marketing and contract manufacturing of certain products.

Safe Lane System's line-up features proprietary products, all of which have been made available via exclusive and non-exclusive licensing agreements with Superior Traffic Controls, Inc.

Safe Lane System's product offerings include both a commercial and consumer safety cone product line, as well as an automatic safety cone dispenser, The Kone General. These products represent the culmination of a research project begun several years ago to address the critical need for safer roads, highways, and city streets.

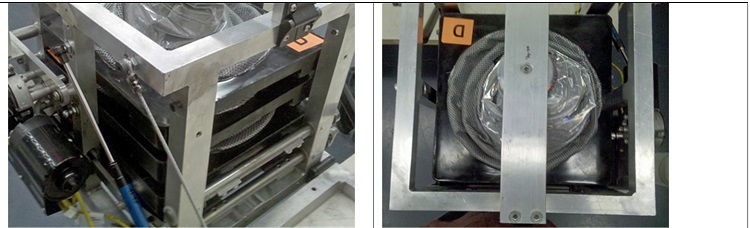

The Kone General Automatic Safety Cone Dispenser

The Kone General is our flagship product and is a patent pending device that can be installed on a wide range of vehicles ranging, but not limited to, fire engines, police cars, tow trucks, telecom vans, construction vehicles, federal, state, and local transit vehicles, that automatically deploys traffic cones by the operator of the attending vehicle. Management believes, the Kone General Dispensing System is the world’s first, and only portable, plug-and-play safety cone dispenser. As the attending vehicle approaches an emergency, construction area, job site, or auto accident, patented spring loaded safety cones are automatically deployed at the touch of a button.

We licensed the IP for this “incident management” automatic cone dispenser (The Kone General), which we intend to launch into markets. The Kone General currently holds up to five, 18” or 28” MUTCD compliant cones. Design is currently in progress to develop a magazine capable of increasing its capacity by an additional 5-10 cones. The Kone General provides for a safer, highly efficient, and more effective solution, addressing numerous issues in all areas of incident management and highway worker safety.

| 4 |

The Kone General is currently designed in two models. Our first model has been engineered specifically for the wired or wireless installation directly onto service vehicles. This has come as a result of extensive research that identified specific design parameters, exclusive to certain types of specialty vehicles such as Fire Trucks.

The dimensional footprint of the unit provides for tremendous flexibility relative to physical installation locations onto new vehicles, as well as for retro-install applications onto existing fleet vehicles. Couple this with simple electronics and seamless integration is easily accomplished.

The second model can be universally installed onto almost any vehicle via a universal mounting apparatus tied to existing vehicle trailer hitch configurations, and controlled via a wireless RF transmitter. Power to the unit is provided using a standard trailer “pig-tail,” eliminating the need for professional installation, providing Kone General end users with 100% “PLUG-AND-PLAY” functionality.

Availability

The Kone General product launch is intended for the second quarter of 2015. Both models are scheduled undergoing beta and field testing that is necessary prior to distribution and full product launch. Prior to our Kone General product launch, several reliability tests will continue to be performed, as well as environmental simulations that will help to identify any potential issues that changes in climate may have on the reliable and consistent operation of the unit. We intend to engage the field testing of the unit on fire engine and emergency services vehicle applications in the second quarter 2015.

Safe Lane System's Traffic Safety Spring Cones and ("tote") Systems

The basic safety cone design has not changed in over 65 years, until now. It is only now with today’s technology in spring manufacturing and with new reflective materials that a retractable cone can be manufactured with the quality that can meet both governmental regulations and industry demands.

The spring cone on which we have a non-exclusive distributorship (as a private label) is designed to better serve U.S. workers that regularly use cones in performing their daily work routines. We intend to attempt to introduce the practicality of their use to millions of new customers in the consumer markets, who traditionally have not considered using traffic cones before because of storage and handling problems and relative inconvenience tied to cargo space limitations. We do not have an exclusive right on this product and others may manufacture, market and private label this product.

| 5 |

For example, four Safe Lane System cones can be stored in the same space needed by a single standard PVC cone.

Now, over 250 million plus vehicle owners can consider easily carrying full sized 28” safety cones for their protection while on the road, by utilizing our consumer cone systems which can store a minimum of two cones in a space of just 16”x14”x4”.

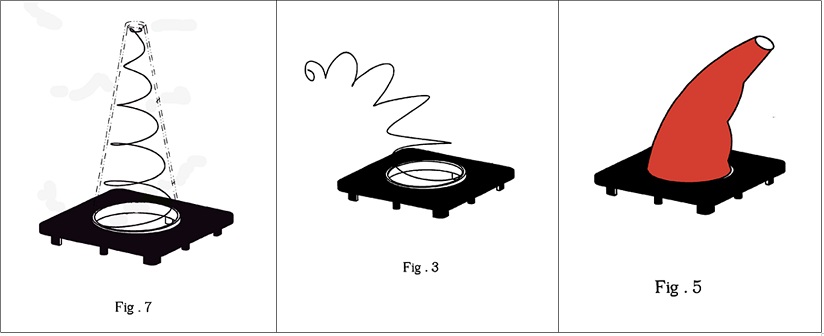

Our safety spring cone has the same form factor as a standard traffic cone, 28” in height with a standard 14” x 14” square base (See Fig. 7).

The uniqueness of our cone’s design lies in its ability for “perturbation,” or flexing from side to side, and up and down (See Fig. 3 and 5). These unique features come as a result of the licensed product design, which incorporate spring technology, a mesh material covering, state of the art reflective materials, and a heavier base.

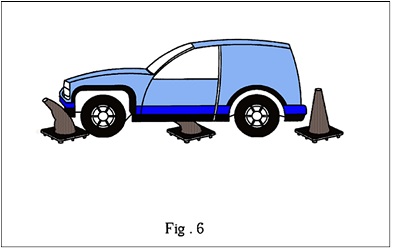

When combined, these factors result in the prevention of the cones being knocked over by passing vehicles (See Fig. 6), as well as from being blown over by gusting winds. In addition, by utilizing spring technology, the cones are neatly and efficiently stored in a compressed state, creating the desirable benefits of space maximization, and ease of transport. We believe design puts our traffic safety cone in the very fortunate position to cross over into several other vertical target markets as well as in the consumer market segments.

| 6 |

Recent changes in legislation require specific physical characteristics in traffic cone use in the United States. The legislation is called The Manual on Uniform Traffic Control Devices, or MUTCD defines the standards used by road managers nationwide to install and maintain traffic control devices on all streets and highways. The MUTCD is published by the Federal Highway Administration (FHWA) under 23 Code of Federal Regulations (CFR), Part 655, Subpart F (http://mutcd.fhwa.dot.gov/ ). States and localities have left this area to the Federal Highway Administration.

Description of MUTCD compliant spring cones bundled in the Kone General

With regard to our Kone General Systems, the use of MUTCD compliant spring cones come standard as included components of the device. This will ensure the Kone General’s compliance with all current legislation related to the use of traffic safety cones on Federal highways. In a compressed condition, the cone measures only 12” x 12” x 3 ¼” and weighs 5.5 pounds, compared to 8 up to 25 pounds for traditional cones. The cone’s reflective qualities are provided by applying Reflexite’s GP 800 reflective material, which is a patented product by Reflexite, one of the world leaders in highway safety reflective materials. The material generates a 500 Ra (candlepower) versus 250-300 candlepower for similar types of applications. The GP 800’s reflective sheeting material is ideal for construction zones. Our cone is environmentally friendly, and can handle high-speed impacts and heavy gusts of wind without displacing the cone. The 5-year total cost of ownership of our cone we believe is significantly less than that of a standard traffic cone, is more functional, takes up a fraction of the space of a standard cone, and is less than half the weight. Our cones which we intend to sell are designed as MUTCD compliant.

Consumer Products

We intend to develop a line of consumer cones in various sizes and configurations for the retail sector. The 2-10 cone safety systems are ideally suited for personal transportation safety since they take up very little room in a personal vehicle. A cone system with wheels and a capacity of 25-40 cones is in development. These will be targeted at schools for their crossing areas, parking lots, play grounds and sport fields.

We have identified a unique niche for the marketing and sale of its safety cones and tote systems by crossing over into the marketing and promotional industries. Our management believes that significant profits can be generated by doubling its safety cones and systems as marketing, advertising, and promotional tools. This can be easily accomplished by placing branded logos, custom embroidery, and/or silk-screening onto our safety cones. This integration of signage, logos, or promotional messages, instantly transforms the our safety cone into a powerful branding tool for companies, municipalities, hotels, restaurants, theme parks, outdoor arenas, stadiums, and any number of entities wishing to get their message across. To date, there hasn’t been any use of traffic cones as advertising mediums or for any other form of product placement or branding.

The parking industry would be a direct line into these market segments. Many restaurants, hotels, commercial buildings, and public parking areas source traffic control and parking responsibilities to third party lot management and valet parking companies.

Our Proposed Products:

(1) Consumer Cone Systems (bundles or "totes"): This product will be manufactured and marketed immediately at retail and discount construction supply, hardware and automotive outlets. Big box retailers, for example, Lowes, Ace Hardware, Home Depot and Sears in the U.S. total over 8,000 outlets. Smaller outlets easily exceed 60,000 in the U.S. As stated in the Market Analysis Summary, above, according to the U.S. Department of Labor, Bureau of Statistics there are over 10 million employees in occupations that regularly use safety cones in their workday activities, all of which are targeted customers for this product.

| 7 |

Further, our Safe D-Ploy cone systems are designed to be marketed to both auto manufacturers, and motorists to be carried in all types of vehicles as part of the spare tire assembly.

(2) Kone General System: Our Kone General system has been designed to dispense five to seven safety cones. The dispenser systems offer an important business tool to private/ public providers of “incident management” services such police, fire/medical, tow and repair activities. These service providers need to set up temporary secure areas on streets, roads, sidewalks or highways to handle traffic control incidents. Additionally, public utilities, telephone and telecommunications companies like Verizon and AT&T need to establish similar safe areas for their road-site workers when providing essential services, such as telephone line repair. Collectively, the potential market for private/public vehicles needing a cone dispensing system exceeds 12 million. Our other potential markets for the Kone General are road painting, striping and asphalt contractors. Usually, these contractors use 18” cones, and therefore would require a redesign of the existing Kone General to provide the capability of handling smaller sized 18” cones. This product will be pursued next year. Presently, only 28” cones are available. 18” and 36” cones can be ordered, but delivery will take longer because there are no immediate plans to maintain an existing inventory of these cones.

(3) Stand-alone Perturbation Safety Cone: The safety cone will be initially sold as a component to the cone dispensing system (an extra 5 pack of safety spring cones will be offered and marketed as an “up sell” to purchasers of the Kone General for the purposes of having spare cones on hand), and other systems as an alternative and space saving vehicle safety solution.

However, before doing so for on-highway use several issues must be resolved. First, a magazine system capable of increasing the Kone General’s capacity to 10-20 cones needs to be perfected. Design work is in progress, and proof of concept has been resolved. Additional funding to complete prototypes is required. Second, regulatory analysis needs to be completed to identify state regulations and standards requiring additional state and local government testing and approval. Presently, the cone meets federal standards as a Category I directional device. The Company is able to self certify the cone’s compliance with federal regulations, but in many states we must still comply with additional requirements before the product can be marketed for federal highway usage. States requiring additional testing must be identified and the approval process researched. The Company needs to prioritize the states needing additional testing based upon market potential, user interest, the time needed, and difficulty of meeting compliance standards.

At this time we are not addressing to international markets.

We have aligned our intended manufacturing and production per-engineering criteria with international suppliers but focused today on the Domestic markets. Specifically, the Safe D-Ploy Cone product and Kone General are being bid through international manufacturers who supply global companies including mass market retailers under private label. Foreign laws and regulations do vary and we acknowledge this as a business reality and potential barrier to entry. The market opportunity and cost associated with modifying our MUTD United States compliant cone to meet the foreign markets among many factors in consideration. It’s a future plan based on expected demand after successful United Stated market penetration. Sales, Marketing, Manufacturing and Distribution, as will as operational costs and ongoing finance, will be fully assessed before determining if each foreign market is worth the investment of time, capital and other resources.

Potential future commercial products utilizing the safety cone:

| · | barricade |

| · | barrel |

| · | cone w/ sign |

| · | Kone General (large capacity) |

| · | Kone General magazine |

| · | cone collector system (large capacity) |

Buyers/Users:

| · | Law Enforcement |

| · | Fire/medical emergency response |

| · | Government Road Maintenance |

| · | Construction |

| · | Building/Ground Maintenance |

| · | Consumers |

| · | Utilities |

| · | OEM |

| · | School/ Athletics |

| 8 |

Any one or all products may be used at some time by the above-mentioned buyers/users. For example, all buyers/users may need in varying quantities safety cones for their business, for recreation uses and for their business and/or personal vehicles.

Sales and Marketing Plan

Sales Planning is a critical element to any business. Having a proper plan in place will accomplish several objectives but the most critical in our opinion are: drive profitable sales, avoid conflict between sales channels, and promote the activity with volume incentives. We believe we have structured a revenue model for our sales channel (wholesale, value added resale, and retail (on-line and brick & mortar). In the highway safety products industry, stocking distributors are key because when a contractor or agency needs cone products it is on an instant need basis and shipment needs to be immediate. We have explored the need to develop a relationship with a leading warehouse distributor, a global leader who supplies many channels including Amazon.com to facilitate order delivery.

Marketing, brand/product awareness, and clear value proposition are areas of great importance at this stage of the business. We intend to implement a plan around the core externally facing elements: Brand identity (logos, color palette, design elements, tag lines, etc.), Digital (Website, Social media like Linkedin/Facebook Pages, Twitter, Google, You Tube Channels), and Print Literature (Corporate collateral, Product collateral, Channel Support literature, Direct Mail, etc.)

We are also working on license agreements of complimentary products that can be “add on” sales to existing customer and open new markets as well.

Facts and Statistics Related to Our Product Designs

The National Highway Traffic Safety Administration confirmed Nov. 14 that U.S. highway deaths rose by 4 percent in 2012 from the previous year, as the agency released the 2012 Fatality Analysis Reporting System (FARS) data. The increase to 33,561 deaths in 2012 -- 1,082 more fatalities than in 2011 -- and most of them involved motorcyclists and pedestrians. Deaths for both of those categories increased for the third consecutive year in 2012.

Key 2012 statistics include:

| · | Fatalities among pedestrians increased 6.4 percent from 2011. The data showed the large majority of pedestrian deaths occurred in urban areas, at non-intersections, at night, and many involved alcohol. |

| · | Motorcyclist fatalities increased 7.1 percent year over year. NHTSA reported 10 times as many riders died not wearing a helmet in states without a universal helmet law than in states with those laws. |

| · | Large-truck occupant fatalities also rose for the third consecutive year, by 8.9 percent from 2011. |

| · | Deaths in crashes involving drunk drivers rose 4.6 percent to 10,322 in 2012, and most of those crashes involved drivers with a blood alcohol concentration of .15 or higher. |

A preliminary total of 4,405 fatal work injuries were recorded in the United States in 2013, lower than the revised count of 4,628 fatal work injuries in 2012, according to results from the Census of Fatal Occupational Injuries (CFOI) conducted by the U.S. Bureau of Labor Statistics. The rate of fatal work injury for U.S. workers in 2013 was 3.2 per 100,000 full-time equivalent (FTE) workers, compared to a final rate of 3.4 per 100,000 in 2012.

Since 2011, CFOI has identified whether fatally-injured workers were working as contractors at the time of the fatal incident. In 2013, 734 decedents were identified as contractors, above the 715 reported in 2012. Workers who were working as contractors at the time of their fatal injury accounted for 17 percent of all cases in 2013.

The number of fatal work injuries among firefighters was considerably higher in 2013, rising from 18 in 2012 to 53 in 2013. The large increase resulted from a few major incidents in which multiple fatalities were recorded, including the Yarnell Hill wildfires in Arizona which claimed the lives of 19 firefighters.

Fatal transportation incidents were lower by 10 percent in 2013, but still accounted for about 2 out of every 5 fatal work injuries in 2013. (See chart 1.) Of the 1,740 transportation-related fatal injuries in 2013, nearly 3 out of every 5 (991 cases) were roadway incidents involving motorized land vehicles. Non-roadway incidents, such as a tractor overturn in a farm field, accounted for another 13 percent of the transportation-related fatal injuries. About 16 percent of fatal transportation incidents (284 cases) in 2013 involved pedestrians who were struck by vehicles. Forty-eight of these occurred in work zones.

| 9 |

Fatal occupational injuries by event or exposure, 2012-2013

| 2012 | 2013 | |||||||

| Transportation incidents | 1,923 | 1,740 | ||||||

| Roadway incidents involving motorized land vehicle | 1,153 | 991 | ||||||

| Roadway collision with other vehicle | 565 | 517 | ||||||

| Roadway collision - moving in same direction | 124 | 127 | ||||||

| Roadway collision - moving in opposite directions, oncoming | 204 | 178 | ||||||

| Roadway collision - moving perpendicularly | 134 | 124 | ||||||

| Roadway collision with object other than vehicle | 338 | 288 | ||||||

| Vehicle struck object or animal on side of roadway | 318 | 270 | ||||||

| Roadway non-collision incident | 247 | 182 | ||||||

| Jack-knifed or overturned, roadway | 202 | 157 | ||||||

| Non-roadway incidents involving motorized land vehicles | 233 | 223 | ||||||

| Non-roadway non-collision incident | 175 | 178 | ||||||

| Jack-knifed or overturned, non-roadway | 115 | 116 | ||||||

| Pedestrian vehicular incident | 293 | 284 | ||||||

| Pedestrian struck by vehicle in work zone | 65 | 48 | ||||||

| Rail vehicle incidents | 41 | 41 | ||||||

| Water vehicle incidents | 38 | 60 | ||||||

| Aircraft incidents | 127 | 133 |

Market Analysis Summary

In addition to the consumer cone described above, we have also specifically targeted a niche market consisting of “incident management” type vehicles, such as police, fire/medical and tow service vehicles as ideal users of its cone dispensing system. According to the National Highway Traffic Safety Administration, it is estimated that this market, together with repair and utility vehicles, exceeds 12 million in the US market.

Today, not only in the United States, but globally, road accidents and traffic related deaths are increasing. Our highways are becoming more dangerous despite government and industry efforts to make vehicles safer and stronger. The fact is, more vehicles, both large and small are taking up shrinking lane space on our highways. With increased demand for additional travel lanes, state and federal governments have encroached into road shoulder right of way area to solve the need for more traffic lanes. Government efforts to expand right of way areas are regularly the subject of litigation by special interest groups, which, in turn, drives road construction costs beyond capabilities and can result in years of delay and snarled roads. In many urban areas, roadways have been widened to expand across the entire breath of right of way leaving no safe shoulder area for disabled vehicles or road police action. Furthermore, any necessary repair or construction work on a roadway can create hazardous risks for workers, long traffic delays for motorists and increased opportunities for serious traffic accidents.

A large portion of the safety cones we hope to market pursuant to this business plan result from the anticipated acceptance and sale of our consumer cone line. According to the United States Department of Labor, Bureau of Statistics, Occupational Data, in 2001 there were over 10 million individuals employed in industries where the use of traffic safety cones is a standard workday practice. Although safety cones are used for multiple purposes by many different types of business and industries, we believe there has never been a safety cone that has been more user friendly in terms of ease of handling, storage, performance, weight, and convenience.

We believe there has never been a similar product that is durable, flexible, rugged and functional. We hope that our cone will generate new consumer base. For example, the very user-friendly cone could be a safety device for family personal vehicles, which rarely have carried cones in the past.

Safety cones on highways weigh between 8 to 25 pounds, and stand from 18” to 36” high. Placing these cones on the highway is almost always done by hand putting workers in danger of being struck by passing cars. According to the California Department of Transportation (CalTrans), 166 CalTrans employees have been killed in the line of duty with many deaths coming as a remit of errant vehicles entering highway work zones.

The majority of these accidents were the result of speeding and inattentive drivers. In 2002, there were over 1,000 work zone fatalities nationwide, as well as 8,374 work zone injuries. Further, according to the Federal Highway Administration, three worker fatalities occur nationally in all cone zones every five days. Many accidents occurred as a result of drivers running over a cone and losing control of their automobiles.

| 10 |

The public works employee is also at risk while placing these cones on the highway and during the retrieval process. Another added hazard is when safety cones are struck by a car and thrown into traffic, resulting in a public works employee or highway patrol officer having to cross traffic to retrieve them. Traffic cones are often stored on trucks making them difficult to load and unload. Many repetitive motion injuries have occurred as a result of the constant gripping and the awkward cone placement postures, especially to the shoulder area (flexion of 127-138 degrees).

An evaluation of U.S. Census Bureau Statistics for employment indicates over 10 million individuals are employed in professions, which regularly use safety cones in their daily work. Even a casual observer on any day will notice hundreds of safety cones riding in the trunk bed of pickup trucks and utility vehicles. Safety cones are universally used by all sorts of people for all sorts of purposes, despite the fact that they take up too much space, often stick together and are difficult and heavy to handle.

We believe traffic safety is a growing business. Our Safe D-ploy Spring Cone and Kone General System are unique in the marketplace, and are more than specifically designed for traffic safety, but adaptive enough so that we hope to qualify them as the industry standard in numerous alternate applications.

Our interviews with consumers indicated that there is a potential consumer market which is ready for our cone models. We believe there are many inherent advantages of using our safety cone instead of a standard PVC cone, such as; it will not blow over, weighs less, will not stick together, ships and handles easier, and if hit by a vehicle and projected into the roadway or work zone, will do less physical damage to people and personal property, as is currently the case with standard rubber safety cones.

The construction industry in general and road construction, in particular, uses and replaces several million cones each year. Government regulations require the use of safety cones at work sites throughout the country. For these companies, our products may offer important advantages over standard PVC cones in the fact that our cones can be repaired with interchangeable parts at a fraction of the cost of a new cone.

New government regulations, both in the U.S. and internationally, require different colored cones to indicate various conditions or situations, such as hazardous materials and school areas. We intend to offer its cones in various colors to meet industry needs.

Sales Strategy

We intend to sell its Safe D-Ploy product line to customers generated by the Company both internally, as well as through reputable, established distributor networks. We intend to actively seek distributor networks, with existing clientele consistent with our target market of particular buyers/users.

We will also sell through independent manufacturer’s representatives on a case- by-case or market-by-market basis. Outside of our expansive internal plans to launch that have been previously mentioned, our main strategy is to communicate the unique and desired attributes of our cone, Kone General and consumer systems to a broad segment of the North American Market during the first year and to expand it internationally in our second and third year.

We believe we have a unique and innovative product line. The basic traffic safety cone has not been changed in over 60 years. As a result of technology and the reduction in material cost and labor, we intend to market our products to a growing market segment with a well-defined list of cost and functional benefits. We intend to communicate our high value proposition to the distribution network as well as end users through personal selling, targeted print advertising and improved communications capabilities via a sophisticated website.

We plan to be active in traffic control and other industry trade associations, and attend trade shows and exhibitions. Our trade show presence is a big part of our deployment strategy, beginning with the goal to feature our product line at the FDIC trade show which is held annually in Indianapolis, IN.

Furthermore, foreign markets need to be considered a high priority and distributors will be sought to market not only the Kone General but also all our products internationally. We will consider offering Distributors exclusive selling rights in their markets for various segments of the trade for one to three years. In return our Distributors will pay a license fee for said exclusivity. Our sales agreement will call for the Distributor to clearly identify its markets, and time frame as to when those markets will have product. If after an agreed upon time period those accounts are not being stocked with our product or products, then we will have the right to seek another Distributor to service the specific market(s).

| 11 |

Milestones Reached To Date

We have completed these milestones in our business plan progression:

| · | Obtained the exclusive rights (via exclusive licensing agreements entered into between our Company and the I.P. holder) to both manufacture and distribute our primary product(s). |

| · | Secured non-exclusive licensing rights to related ancillary products that we intend to market in both the consumer and commercial market segments. |

| · | Secured USPTO trademark protection of the branded product name of our flagship product and related components, Safe D-ploy Spring ConeTM and The Kone GeneralTM |

| · | Developed our website (www.safelanesystems.com), marketing materials, brochures, sales aids, and product demonstration videos to be used to market the Company’s products. |

| · | Acquired all intellectual property related to technical and CAD, 2D, and 3D drawings in preparation for mass manufacture of the Kone General Automatic Safety Cone Dispenser. |

| · | Acquired value engineering of the Kone General to significantly reduce the unit CGS. |

| · | Completed marketing plan and hires sales staff to pursue direct sales efforts. |

Our Goals for the next year are as follows:

FUTURE MILESTONES

| · | Generate additional capital to allow us to fund customer field trials. |

| · | Fully implement direct and online sales marketing strategy. |

1st Quarter 2016

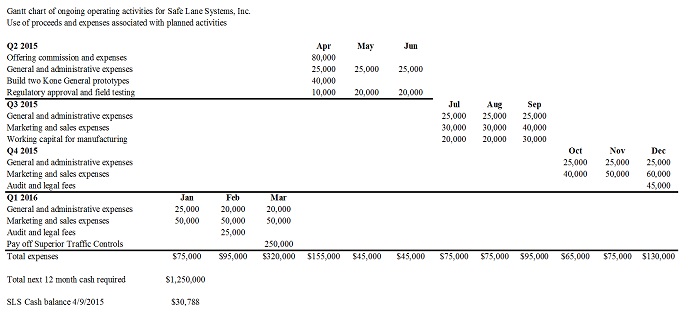

As of April 9, 2015, the Company had a cash balance of approximately $15,000. At a current monthly cash burn rate of $12,500, it is estimated that we will run out of cash before the end of January 2015.

Our milestones in this time period will be to receive additional financing through a private placement, have a design for two Kone General prototypes, refinance or pay off the note payable to Superior Traffic Controls, Inc., and enter into a manufacturing agreement to build the two prototypes. We will need to raise additional debt or equity capital for funding of operations beyond the second quarter. If no additional capital is obtained and the Company is not able to refinance or pay off the note to Superior Traffic Controls, Inc., it is highly probable that Safe Lane Systems, Inc. will cease operations.

Company's operations during this quarter entirely depend on successfully obtaining additional capital. We intend to complete production of two Kone General prototypes before the end of April 2016. It will take approximately $40,000 to build these prototypes. Once the two prototypes are built, we intend to spend approximately $50,000 on field testing and necessary procedures to obtain regulatory approval. The Company will incur approximately $75,000 on general and administrative expenses during this quarter, which may be partially used to compensate for expenses associated with field testing and regulatory approval. We will identify the most promising sales channels to utilize after the product receives regulatory approval.

During this quarter, primary milestones will be to build and obtain regulatory approval for two Kone General prototypes.

| 12 |

3rd Quarter 2016

Company's operations, during this time period, rely on successfully obtaining sufficient financing as well as completing production and obtaining regulatory approval for two Kone General prototypes. The primary focus during this quarter will be on marketing and sales assuming that the manufacturing relationship has been proven and we achieved desired results with the product. It will be important to achieve limited manufacturing with a firm delivery date. The Company plans to allocate $80,000 to cover marketing and sales expenses. The budget for sales and marketing will be partially utilized to hire at least two sales representatives, who will be responsible to establish a sales channel through a network of manufacturer's representatives and/or approach DOTs (Department of Transportation) in various states.

The milestones during this quarter will be to achieve market acceptance for the Kone General and to sell sample units. If we are unable to achieve either or both of such milestones, we will have to extend into the following quarter. If we have orders, we will try to partially finance manufacturing production with some type of accounts receivable financing or issue additional stock, which is not yet arranged and of which there can be no assurance.

4th Quarter 2016

Assuming any success in the prior quarter with sales and deliveries, our emphasis in this quarter will again be to increase sales and manufacturing output. We estimate using approximately $250,000 on marketing and general and administrative expenses. We will increase sales staff in an expanded nationwide marketing efforts, with resulting expense increases. However, we may have to allocate marketing funds to support manufacturing of ordered units. The Company will have to secure either accounts receivable financing or obtain additional capital to support the sales cycle.

1st Quarter 2017

Assuming success in the prior quarter with sales and deliveries, our emphasis in this quarter will again be to increase sales and manufacturing output. We estimate we will continue to invest approximately $250,000 on marketing and general and administrative expenses. We will increase sales staff in expanded nationwide marketing efforts, with resulting expense increases. As in previous quarter, the Company will have to secure either accounts receivable financing or obtain additional capital to support the sales cycle.

COMPETITION, MARKETS, AND REGULATION

Competition

Our dispenser is the world’s first portable safety cone dispenser design known to exist, and we have yet to identify any competitors as of the writing of this summary. Note: Other automatic safety cone dispensing systems currently exist. However, systems currently sold in the marketplace are designed for mass cone deployment (i.e. road striping applications), are not portable, require the purchase of heavy equipment, dedicated specialty vehicles, and are very expensive. Safety cones are manufactured by many PVC and injection molding companies, and they are all price competitive for basic expandable units and constitute significant price/per unit competition for our cones.

Markets

Primary target market segments include highway departments, private/public utilities, fire/ems, law enforcement, trucking/transportation, telecomm, vehicle parking industry, construction, and the military. Calculation of market size is difficult to determine due to the uniqueness of the product, as well as being first to market over several vertical market segments.

Applicable Regulations in the Industry

The leading cause of highway construction worker injuries and fatalities is contact with construction vehicles, objects, and equipment. These injuries and deaths are preventable through a number of good practices. (Source: http://ops.fhwa.dot.gov/wz/workersafety/)

As our highway infrastructure ages, many transportation agencies are focusing on rebuilding and improving existing roadways. This means more roadwork is being performed on roadways that are open to traffic. At the same time, traffic continues to grow and create more congestion, particularly in urban areas. To avoid major queues during peak travel periods, urban areas are seeing more night work. The combination of more work done alongside increasingly heavier traffic and greater use of night work can result in increased safety considerations for highway workers. However, there are regulations and available resources on good practices that can help workers perform their jobs safely.

| 13 |

Work zones are a necessary part of maintaining and upgrading our highway system. The combination of more work zones and heavier traffic volumes means work zones are having a greater effect on roadway systems. The American public has cited work zones as second only to poor traffic flow in causing dissatisfaction with the roadway system.

Note: The following are significant statements on Regulations and Rules in the highway safety industry.

The FHWA Work Zone Mobility and Safety Program is working to "make work zones work better" by providing transportation practitioners with high-quality products, tools, and information that can be of value in planning, designing, and implementing safer, more efficient, and less congested work zones. The Work Zone Mobility and Safety Web site serves as a central location for work zone-related resources and is updated with new information and resources on a frequent basis. These resources include:

| · | Comprehensive information and guidance for implementing the Work Zone Safety and Mobility Rule (23 CFR 630 Subpart J). |

| · | Peer-to-Peer Program that provides State and Local transportation agencies easy access to knowledgeable peers across a range of work zone issues, at no cost to these agencies. |

| · | Best Practices Guidebook, which includes recommended "state of the practice" approaches, procedures, and technologies for work zone mobility and safety management, collected from State and Local transportation agencies. |

| · | Work Zone Self Assessment, used by each FHWA Division Office and partner State on an annual basis to measure their current state-of-practice and identify future work zone quality improvement efforts. |

| · | Work zone training courses, to help practitioners plan, design, and implement safe and effective work zones. |

| · | Current news related to work zones, from both national and international sources. |

| · | Publications and studies on a variety of work zone topics, including work zone ITS, traffic analysis tools for work zones, contracting methods, construction strategies, public information and outreach for work zones, and others. |

Worker Safety for Highway Construction Standard

ANSI/ASSE A10.47-2009: Work Zone Safety for Highway Construction became effective on February 24, 2010 and applies to workers engaged in construction, utility work, maintenance, or repair activities on any area of a highway. It covers practices including Flagger Safety, Runover/Backover Prevention, Equipment Operator Safety, Illumination, Personal Protective Equipment, and more.

Work Zone Traffic Management

Managing traffic during construction is necessary to minimize traffic delays, maintain motorist and worker safety, complete roadwork in a timely manner, and maintain access for businesses and residents. Effective work zone traffic management includes assessing work zone impacts and documenting strategies for mitigating the impacts in a transportation management plan (TMP). The Work Zone Safety and Mobility Rule requires TMPs for all Federal-aid highway projects.

(Source: http://ops.fhwa.dot.gov/wz/traffic_mgmt/index.htm)

Work Zone Safety and Mobility Rule

The Work Zone Safety and Mobility Rule (Rule) was published on September 9, 2004 in the Federal Register. All state and local governments that receive federal-aid funding were required to comply with the provisions of the rule no later than October 12, 2007. The Rule updated and broadened the former regulation at 23 CFR 630 Subpart J to address more of the current issues affecting work zone safety and mobility. The changes to the regulation encouraged the broader consideration of the safety and mobility impacts of work zones across project development and the implementation of strategies that help manage these impacts during project delivery.

(Source: http://ops.fhwa.dot.gov/wz/resources/final_rule.htm)

| 14 |

Temporary Traffic Control

FHWA has published several documents and studies regarding temporary traffic control in highway maintenance.

| · | Field Guide on Installation and Removal of Temporary Traffic Control (TTC) for Safe Maintenance and Work Zone Operations (PDF 845) - Provides field personnel with introductory guidance on proper setup and operation of TTC zones, which improves the safety of those working near traffic. |

| · | Work Zone Safety: Temporary Traffic Control for Maintenance Operations (PDF 283KB) - Provides seven fundamental principles for setting up TTC Zones to protect workers and incident responders and allow for the safe and efficient movement of road users. |

| · | Work Zone Positive Protection Toolbox (PDF 961KB) - Describes various types of positive protection devices and provides guidance on where and how each is typically used. These devices may be used to help protect road users from entering hazardous areas in work zones and to shield workers and pedestrians. |

(Source: http://ops.fhwa.dot.gov/wz/workersafety/index.htm)

The Temporary Traffic Control Devised Rule (Subpart K of 23 CFR 630) provides guidance for devices, and we believe our products meet the requirements of the Rule.

Selected Federal Regulations

§ 630.1102 Purpose.

To decrease the likelihood of highway work zone fatalities and injuries to workers and road users by establishing minimum requirements and providing guidance for the use of positive protection devices between the work space and motorized traffic, installation and maintenance of temporary traffic control devices, and use of uniformed law enforcement officers during construction, utility, and maintenance operations, and by requiring contract pay items to ensure the availability of funds for these provisions. This subpart is applicable to all Federal-aid highway projects, and its application is encouraged on other highway projects as well.

§ 630.1110 Maintenance of temporary traffic control devices.

To provide for the continued effectiveness of temporary traffic control devices, each agency shall develop and implement quality guidelines to help maintain the quality and adequacy of the temporary traffic control devices for the duration of the project. Agencies may choose to adopt existing quality guidelines such as those developed by the American Traffic Safety Services Association (ATSSA) or other state highway agencies. A level of inspection necessary to provide ongoing compliance with the quality guidelines shall be provided.

Title to Properties

None.

We have an exclusive License and a non-exclusive Sub-License for certain Intellectual Property associated with the Kone dispenser and the Kone design, respectively.

Backlog of Orders

We currently have no orders for sales at this time.

Government Contracts

We have no government contracts.

Company Sponsored Research and Development

We are not conducting any research, although our products and future products may be in development.

Number of Persons Employed

As of April 14, 2016, we have no employees and 1 independent consultant. Our officers are spending part-time in this business – up to 10 hours per week.

| 15 |

PLAN OF OPERATIONS

Our Budget for operations in next fiscal year, 2016, is as follows:

| APPLICATION OF FUNDS (1) | ||||

| Working Capital | $ | 250,000 | ||

| General & Administrative | $ | 250,000 | ||

| Marketing & PR | $ | 500,000 | ||

| Total | $ | 1,000,000 | ||

(1) These items are variable and no commitment has been obtained from any source.

We may change any or all of the budget categories in the execution of its business model. None of the line items are to be considered

fixed or unchangeable. We may need substantial additional capital to support its budget. We have recognized minimal revenues from

our existing operational activities.

We may need to raise additional funds to support not only our expected budget, but our continued operations. We cannot make any assurances that we will be able to raise such funds or whether we would be able to raise such funds with terms that are favorable to us. We may seek to borrow monies from lenders at commercial rates, but such lenders will probably be at higher than bank rates, which higher rates could, depending on the amount borrowed, make the net operating income insufficient to cover the interest.

If we are unable to begin to generate enough revenue to cover our operational costs, we will need to seek additional sources of funds. Currently, we have no committed source for any funds as of date hereof. No representation is made that any funds will be available when needed. In the event funds cannot be raised if and when needed, we may not be able to carry out our business plan and could fail in business as a result of these uncertainties.

We intend to conduct research and development, market research, product formulation, and will investigate regionally compounding licensed pharmacies for potential acquisition.

ITEM 1A. RISK FACTORS

An investment in our Company's securities involves a high degree of risk. You should carefully consider the following risk factors and all the other information contained in this document before you decide to buy our Company's shares. If any of the following risks related to our Company's business actually occurs, its business, financial condition and operating results would be adversely affected.

RISK FACTORS RELATED TO OUR COMPANY

Our securities are highly speculative and should be purchased only by persons who can afford to lose their entire investment in us. Each prospective investor should carefully consider the following risk factors, as well as all other information set forth elsewhere in this prospectus, before purchasing any of the shares of our common stock.

We have a lack of revenue history and investors cannot view our past performance since we are a start-up company.

We were formed on September 10, 2013 for the purpose of engaging in any lawful business and adopted a plan to engage in the traffic safety business. We have had one sales transaction since inception through Amazon.com for $1,725. We are not profitable and the business effort is considered to be in an early development stage. We must be regarded as a new or development venture with all of the unforeseen costs, expenses, problems, risks and difficulties to which such ventures are subject. We should be considered highly speculative.

We have limited working capital and limited cash funds.

Our capital needs are projected to be $1,250,000 during the next 12 months of operations. Such funds are not committed, at this time in any amount. Within the next six months additional financing requirements are projected to be $90,000. We have a note payable agreement in place with our current lender that will provide this funding need.

We have limited funds, and such funds may not be adequate to carry out the business plan. We have limited funds (as of December 31, 2015, we had $15,282 in cash on hand), and such funds may not be adequate to carry out the business plan. The ultimate success of our Company may depend upon our ability to raise additional capital. We have investigated the availability, source, or terms that might govern the acquisition of additional capital. If additional capital is needed, there is no assurance that funds will be available from any source or, if available, that they can be obtained on terms acceptable to us. If not available, our operations will be limited to those that can be financed with our modest capital.

| 16 |

The ultimate success of our Company may depend upon our ability to raise additional capital. Safe Lane Systems has investigated the availability, source, or terms that might govern the acquisition of additional capital. If additional capital is needed, there is no assurance that funds will be available from any source or, if available, that they can be obtained on terms acceptable to Safe Lane Systems. If not available, Safe Lane System’s operations will be limited to those that can be financed with its modest capital.

Our officers and directors may have conflicts of interest which may not be resolved favorably to us.

Certain conflicts of interest may exist between us and our officers and directors. Our Officers and Directors have other business interests to which they devote their attention and may be expected to continue to do so although management time should be devoted to our business. As a result, conflicts of interest may arise that can be resolved only through exercise of such judgment as is consistent with fiduciary duties to us. Our officer is spending part-time in this business – up to 10 hours per week.

We may in the future issue more shares which could dilute current stockholders.

We may issue further shares as consideration for the cash or assets or services out of our authorized but unissued common stock that would, upon issuance, represent more equity of our Company. The result of such an issuance would be those new stockholders and management would control our Company, and persons unknown could replace our management at this time. Such an occurrence could result in a greatly reduced percentage of ownership of our Company by our current shareholders and distributes and their purchasers in the event of resale, which could present significant risks to investors.

We will incur significant costs to be a public company to ensure compliance with U.S.. corporate governance and accounting requirements and we may not be able to absorb such costs.

We may incur significant costs associated with our public company reporting requirements, costs associated with newly applicable corporate governance requirements, including requirements under the Sarbanes-Oxley Act of 2002 and other rules implemented by the Securities and Exchange Commission. We expect these costs to be approximately $50,000-$75,000 per year. We expect all of these applicable rules and regulations to significantly increase our legal and financial compliance costs and to make some activities more time consuming and costly. We also expect that these applicable rules and regulations may make it more difficult and more expensive for us to obtain director and officer liability insurance and we may be required to accept reduced policy limits and coverage or incur substantially higher costs to obtain the same or similar coverage. As a result, it may be more difficult for us to attract and retain qualified individuals to serve on our board of directors or as executive officers. We are currently evaluating and monitoring developments with respect to these newly applicable rules, and we cannot predict or estimate the amount of additional costs we may incur or the timing of such costs. In addition, we may not be able to absorb these costs of being a public company which will negatively affect our business operations.

We are an “emerging growth company,” and any decision on our part to comply only with certain reduced disclosure requirements applicable to “emerging growth companies” could make our common stock less attractive to investors.

We are an “emerging growth company,” as defined in the JOBS Act, and, for as long as we continue to be an “emerging growth company,” we expect and fully intend to take advantage of exemptions from various reporting requirements applicable to other public companies but not to “emerging growth companies,” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We could be an “emerging growth company” for up to five years, or until the earliest of (i) the last day of the first fiscal year in which our annual gross revenues exceed $1 billion, (ii) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act, which would occur if the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, or (iii) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three year period.

In addition, Section 107 of the JOBS Act also provides that an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)2(B) of the Securities Act for complying with new or revised accounting standards. In other words, an “emerging growth company” can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have elected to opt in to the extended transition period for complying with the revised accounting standards. We have elected to rely on these exemptions and reduced disclosure requirements applicable to “emerging growth companies” and expect to continue to do so.

| 17 |

We may not be able to meet the filing and internal control reporting requirements imposed by the SEC which may result in a decline in the price of our common shares and an inability to obtain future financing.

As directed by Section 404 of the Sarbanes-Oxley Act, as amended by SEC Release No. 33-8934 on June 26, 2008, the SEC adopted rules requiring each public company to include a report of management on the company’s internal controls over financial reporting in its annual reports. In addition, the independent registered public accounting firm auditing a company’s financial statements may have to also attest to and report on management’s assessment of the effectiveness of the company’s internal controls over financial reporting. We may be required to include a report of management on its internal control over financial reporting. The internal control report must include a statement

| · | Of management’s responsibility for establishing and maintaining adequate internal control over its financial reporting; |

| · | Of management’s assessment of the effectiveness of its internal control over financial reporting as of year end; and |

| · | Of the framework used by management to evaluate the effectiveness of our internal control over financial reporting. |

Furthermore, our independent registered public accounting firm may be required to file its attestation on whether it believes that we have maintained, in all material respects, effective internal control over financial reporting.

While we expect to expend significant resources in developing the necessary documentation and testing procedures required by Section 404 of the Sarbanes-Oxley Act, there is a risk that we may not be able to comply timely with all of the requirements imposed by this rule. In the event that we are unable to receive a positive attestation from our independent registered public accounting firm with respect to our internal controls, investors and others may lose confidence in the reliability of our financial statements and our stock price and ability to obtain equity or debt financing as needed could suffer.

In addition, in the event that our independent registered public accounting firm is unable to rely on our internal controls in connection with its audit of our financial statements, and in the further event that it is unable to devise alternative procedures in order to satisfy itself as to the material accuracy of our financial statements and related disclosures, it is possible that we would be unable to file our Annual Report on Form 10-K with the SEC, which could also adversely affect the market price of our Common Stock and our ability to secure additional financing as needed.

The JOBS Act allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies.

Since, we have elected to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(1) of the JOBS Act, this election allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. As a result of this election, our financial statements may not be comparable to companies that comply with public company effective dates.

Our common shares will not initially be registered under the exchange act and as a result we will have limited reporting duties which could make our common stock less attractive to investors.

Our common shares are not registered under the Exchange Act. As a result, we will not be subject to the federal proxy rules and our directors, executive officers and 10% beneficial holders will not be subject to Section 16 of the Exchange Act. In additional our reporting obligations under Section 15(d) of the Exchange Act may be suspended automatically if we have fewer than 300 shareholders of record on the first day of our fiscal year. Our common shares are not registered under the Securities Exchange Act of 1934, as amended, and we do not intend to register our common shares under the Exchange Act for the foreseeable future, provided that, we will register our common shares under the Exchange Act if we have, after the last day of our fiscal year, more than either (i) 2000 persons; or (ii) 500 shareholders of record who are not accredited investors, in accordance with Section 12(g) of the Exchange Act. As a result, although, upon the effectiveness of the registration statement of which this prospectus forms a part, we will be required to file annual, quarterly, and current reports pursuant to Section 15(d) of the Exchange Act, as long as our common shares are not registered under the Exchange Act, we will not be subject to Section 14 of the Exchange Act, which, among other things, prohibits companies that have securities registered under the Exchange Act from soliciting proxies or consents from shareholders without furnishing to shareholders and filing with the Securities and Exchange Commission a proxy statement and form of proxy complying with the proxy rules. In addition, so long as our common shares are not registered under the Exchange Act, our directors and executive officers and beneficial holders of 10% or more of our outstanding common shares will not be subject to Section 16 of the Exchange Act. Section 16(a) of the Exchange Act requires executive officers and directs, and persons who beneficially own more than 10% of a registered class of equity securities to file with the SEC initial statements of beneficial ownership, reports of changes in ownership and annual reports concerning their ownership of common shares and other equity securities, on Forms 3, 4 and 5, respectively. Such information about our directors, executive officers, and beneficial holders will only be available through this (and any subsequent) registration statement, and periodic reports we file thereunder. Furthermore, so long as our common shares are not registered under the Exchange Act, our obligation to file reports under Section 15(d) of the Exchange Act will be automatically suspended if, on the first day of any fiscal year (other than a fiscal year in which a registration statement under the Securities Act has gone effective), we have fewer than 300 shareholders of record. This suspension is automatic and does not require any filing with the SEC. In such an event, we may cease providing periodic reports and current or periodic information, including operational and financial information, may not be available with respect to our results of operations.

| 18 |

Because our common stock is not registered under the Securities Exchange Act of 1934, as amended, our reporting obligations under section 15(d) of the Securities Exchange Act of 1934, as amended, may be suspended automatically if we have fewer than 300 shareholders of record on the first day of our fiscal year.

Our common stock is not registered under the Exchange Act, and we do not intend to register our common stock under the Exchange Act for the foreseeable future (provided that, we will register our common stock under the Exchange Act if we have, after the last day of our fiscal year, $10,000,000 in total assets and either more than 2,000 shareholders of record or 500 shareholders of record who are not accredited investors (as such term is defined by the Securities and Exchange Commission), in accordance with Section 12(g) of the Exchange Act). As long as our common stock is not registered under the Exchange Act, our obligation to file reports under Section 15(d) of the Exchange Act will be automatically suspended if, on the first day of any fiscal year (other than a fiscal year in which a registration statement under the Securities Act has gone effective), we have fewer than 300 shareholders of record. This suspension is automatic and does not require any filing with the SEC. In such an event, we may cease providing periodic reports and current or periodic information, including operational and financial information, may not be available with respect to our results of operations.

Our articles of incorporation provide for indemnification of officers and directors at our expense and limit their liability which may result in a major cost to us and hurt the interests of our shareholders because corporate resources may be expended for the benefit of officers and/or directors.

Our By-Laws include provisions that eliminate the personal liability of the directors of the Company for monetary damages to the fullest extent possible under the laws of the State of Colorado or other applicable law. These provisions eliminate the liability of directors to the Company and its stockholders for monetary damages arising out of any violation of a director of his fiduciary duty of due care. Under Colorado law, however, such provisions do not eliminate the personal liability of a director for (i) breach of the director’s duty of loyalty, (ii) acts or omissions not in good faith or involving intentional misconduct or knowing violation of law, (iii) payment of dividends or repurchases of stock other than from lawfully available funds, or (iv) any transaction from which the director derived an improper benefit. These provisions do not affect a director’s liabilities under the federal securities laws or the recovery of damages by third parties.

Reporting requirements under the Exchange Act and compliance with the Sarbanes-Oxley Act of 2002, including establishing and maintaining acceptable internal controls over financial reporting, are costly and may increase substantially.

The rules and regulations of the SEC require a public company to prepare and file periodic reports under the Exchange Act, which will require that the Company engage legal, accounting, auditing and other professional services. The engagement of such services is costly. Additionally, the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”) requires, among other things, that we design, implement and maintain adequate internal controls and procedures over financial reporting. The costs of complying with the Sarbanes-Oxley Act and the limited technically qualified personnel we have may make it difficult for us to design, implement and maintain adequate internal controls over financial reporting. In the event that we fail to maintain an effective system of internal controls or discover material weaknesses in our internal controls, we may not be able to produce reliable financial reports or report fraud, which may harm our overall financial condition and result in loss of investor confidence and a decline in our share price.

As a public company, we will be subject to the reporting requirements of the Exchange Act, the Sarbanes-Oxley Act, the Dodd-Frank Act of 2010 and other applicable securities rules and regulations. Despite recent reforms made possible by the JOBS Act, compliance with these rules and regulations will nonetheless increase our legal and financial compliance costs, make some activities more difficult, time-consuming or costly and increase demand on our systems and resources, particularly after we are no longer an “emerging growth company.” The Exchange Act requires, among other things, that we file annual, quarterly, and current reports with respect to our business and operating results.

We are not diversified and we will be dependent on only one business.