Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - MEDALLION FINANCIAL CORP | d128183dex322.htm |

| EX-32.1 - EX-32.1 - MEDALLION FINANCIAL CORP | d128183dex321.htm |

| EX-31.2 - EX-31.2 - MEDALLION FINANCIAL CORP | d128183dex312.htm |

| EX-99.1 - EX-99.1 - MEDALLION FINANCIAL CORP | d128183dex991.htm |

| EX-12.1 - EX-12.1 - MEDALLION FINANCIAL CORP | d128183dex121.htm |

| EX-21.1 - EX-21.1 - MEDALLION FINANCIAL CORP | d128183dex211.htm |

| EX-23.1 - EX-23.1 - MEDALLION FINANCIAL CORP | d128183dex231.htm |

| EX-31.1 - EX-31.1 - MEDALLION FINANCIAL CORP | d128183dex311.htm |

| EX-10.8 - EX-10.8 - MEDALLION FINANCIAL CORP | d128183dex108.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2015

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 814-00188

MEDALLION FINANCIAL CORP.

(Exact name of registrant as specified in its charter)

| DELAWARE | 04-3291176 | |

| (State of Incorporation) |

(IRS Employer Identification No.) |

437 MADISON AVENUE, 38th Floor, NEW YORK, NEW YORK 10022

(Address of principal executive offices) (Zip Code)

(212) 328-2100

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act

Common Stock, par value $0.01 per share

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ¨ NO x

Indicated by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act: YES ¨ NO x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or such shorter period that the Registrant was required to submit and post such files). YES ¨ NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K x

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (check one):

| Large Accelerated Filer ¨ | Accelerated Filer x | Non Accelerated Filer ¨ | Smaller Reporting Company ¨ |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) YES ¨ NO x

The aggregate market value of the voting common equity held by non-affiliates of the registrant, computed by reference to the last reported price at which the stock was sold on June 30, 2015 was $176,474,929.

The number of outstanding shares of registrant’s Common Stock, par value $0.01, as of March 7, 2016 was 24,346,479.

Table of Contents

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Definitive Proxy Statement for its 2016 Annual Meeting of Shareholders, which Definitive Proxy Statement will be filed with the Securities and Exchange Commission not later than 120 days after the registrant’s fiscal year-end of December 31, 2015, are incorporated by reference into Part III of this form 10-K

MEDALLION FINANCIAL CORP.

2015 FORM 10-K ANNUAL REPORT

2

Table of Contents

The following discussion should be read in conjunction with our financial statements and the notes to those statements and other financial information appearing elsewhere in this report.

This report contains forward-looking statements relating to future events and future performance applicable to us within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, including, without limitation, statements regarding our expectations, beliefs, intentions, or future strategies that are signified by the words expects, anticipates, intends, believes, or similar language. Actual results could differ materially from those anticipated in such forward-looking statements. All forward-looking statements included in this document are based on information available to us on the date hereof, and we assume no obligation to update any forward-looking statements. We caution investors that our business and financial performance are subject to substantial risks and uncertainties.

| ITEM 1. | OUR BUSINESS |

We, Medallion Financial Corp. or the Company, are a specialty finance company that has a leading position in originating, acquiring, and servicing loans that finance taxicab medallions and various types of commercial businesses. A wholly-owned portfolio company of ours, Medallion Bank, also originates consumer loans for the purchase of recreational vehicles, boats, motorcycles, trailers, and to finance small scale home improvements. Our core philosophy has been “In niches there are riches.” We try to identify markets that are profitable and where we can become an industry leader. Our investment objectives are to provide high level of distributable income, consistent with the preservation of capital, as well as long-term growth of net asset value and our stock price. These investment objectives may be changed without shareholder approval. We also provide other debt, mezzanine, and equity investment capital to companies in a variety of industries, consistent with our investment objectives. For additional information about our business and operations, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Since 1996, the year in which we became a public company, we have increased our taxicab medallion loan portfolio at a compound annual growth rate of 4%, and our commercial loan portfolio at a compound annual growth rate of 4% (9% and 6% on a managed basis when combined with Medallion Bank). Since Medallion Bank acquired a consumer loan portfolio and began originating consumer loans in 2004, it has increased its consumer loan portfolio at a compound annual growth rate of 18%. Total assets under our management and the management of our unconsolidated wholly-owned subsidiaries, which includes our managed net investment portfolio, as well as assets serviced for third party investors, were $1,655,000,000 as of December 31, 2015 and $1,497,000,000 as of December 31, 2014, and have grown at a compound annual growth rate of 11% from $215,000,000 at the end of 1996. Since our initial public offering in 1996, we have paid/declared distributions in excess of $254,000,000 or $14.31 per share.

We conduct our business through various wholly-owned investment company subsidiaries including:

| • | Medallion Funding LLC, or Medallion Funding, a Small Business Investment Company, or SBIC, our primary taxicab medallion lending company; |

| • | Medallion Capital, Inc., or Medallion Capital, an SBIC and a regulated investment company, or RIC, which conducts a mezzanine financing business; and |

| • | Freshstart Venture Capital Corp., or Freshstart, an SBIC and a RIC, which originates and services taxicab medallion and commercial loans. |

We formed a wholly-owned portfolio company, Medallion Servicing Corporation, or MSC, to provide loan services to Medallion Bank, also a portfolio company wholly-owned by us. We have assigned all of our loan servicing rights for Medallion Bank, which consists of servicing taxi medallion and commercial loans originated by Medallion Bank, to MSC, which bills and collects the related service fee income from Medallion Bank, and is allocated and charged by us for MSC’s share of these servicing costs.

We also conduct business through our asset-based lending division, Medallion Business Credit, an originator of loans to small businesses for the purpose of financing inventory and receivables.

3

Table of Contents

In addition, we conduct business through a wholly-owned portfolio company, Medallion Bank, a bank regulated by the FDIC and the Utah Department of Financial Institutions which originates taxicab medallion, commercial, and consumer loans, raises deposits, and conducts other banking activities. Medallion Bank generally provides us with our lowest cost of funds which it raises through bank certificates of deposit issued to its customers. To take advantage of this low cost of funds, we refer a portion of our taxicab medallion and commercial loans to Medallion Bank, which then originates these loans, which are then serviced by MSC. However, the FDIC restricts the amount of taxicab medallion loans that Medallion Bank may finance to three times Tier 1 capital, or $485,814,000 as of December 31, 2015. MSC earns referral and servicing fees for these activities. As a non-investment company, Medallion Bank is not consolidated with the Company, which is an investment company under the Investment Company Act of 1940, or the 1940 Act.

We are a closed-end, non-diversified management investment company, organized as a Delaware corporation, under the 1940 Act. We have elected to be treated as a business development company, or BDC, under the 1940 Act. We have also elected to be treated for federal income tax purposes as a RIC under Subchapter M of the Internal Revenue Code, or the Code. As a RIC, we generally do not have to pay corporate-level federal income taxes on any net ordinary income or capital gains that we distribute to our shareholders as dividends, if we meet certain source-of-income and asset diversification requirements. Medallion Bank is not a RIC and must pay corporate-level US federal and state income taxes.

We are managed by our executive officers under the supervision of our Board of Directors. As a result, we do not pay investment advisory fees, but instead we incur the operating costs associated with employing investment and portfolio management professionals. Alvin Murstein, our chairman and chief executive officer, has over 50 years of experience in the ownership, management, and financing of taxicab medallions and other commercial businesses. Andrew M. Murstein, our president, has over 25 years of experience and is the third generation in his family to participate in the business.

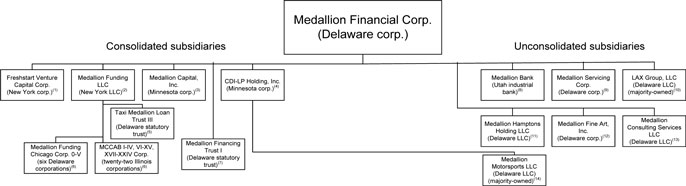

Below is our organizational structure reflecting our consolidated and unconsolidated subsidiaries.

| (1) | An SBIC and a RIC which originates and services taxicab medallion and commercial loans. |

| (2) | An SBIC which is our primary taxicab medallion lending company. |

| (3) | An SBIC and a RIC which conducts a mezzanine financing business. |

| (4) | Formed for the purpose of holding and managing equity investments in a racing team, an equipment manufacturing business, and an airport and food retail business. |

| (5) | Formed for the purpose of owning medallion loans originated by Medallion Funding. |

| (6) | Formed for purpose of owning and leasing repossessed Chicago taxicab medallions. |

| (7) | Formed for the purpose of issuing unsecured preferred securities to investors. |

| (8) | A Utah industrial bank regulated by the FDIC and the Utah Department of Financial Institutions which originates taxicab medallion, commercial, and consumer loans, raises deposits, and conducts other banking activities. |

| (9) | Formed for the purpose of conducting loan servicing activities. |

| (10) | Formed for the purpose of holding an equity investment in a professional lacrosse team. |

| (11) | Formed for the purpose of holding and managing a hotel investment and such investment was sold in March 2015. |

| (12) | Formed for the purpose of engaging in art dealing. |

| (13) | Formed for the purpose of engaging in general consulting services. |

| (14) | Formed for the purpose of holding an equity investment in a racing team. |

4

Table of Contents

Our Market

We provide loans to individuals and small to mid-size businesses, both directly through our investment company subsidiaries and also through Medallion Bank, in three primary markets:

| • | loans that finance taxicab medallions; |

| • | loans that finance commercial businesses; and |

| • | loans that finance consumer purchases of recreational vehicles, boats, motorcycles, and trailers, and to finance small scale home improvements. |

The following chart shows the components of our $1,501,555,000 managed net investment portfolio as of December 31, 2015.

| (Dollars in thousands) |

On-Balance Sheet | Off-Balance Sheet (1) | Total Managed Investments | |||||||||

| Medallion loans |

$ | 308,408 | $ | 332,496 | $ | 640,904 | ||||||

| Commercial loans |

81,895 | 43,987 | 125,882 | |||||||||

| Consumer loans |

— | 619,887 | 619,887 | |||||||||

| Investments in Medallion Bank and other controlled subsidiaries |

159,913 | (137,298 | ) | 22,615 | ||||||||

| Investment securities |

49,884 | 35,524 | 85,408 | |||||||||

| Equity investments |

6,859 | — | 6,859 | |||||||||

|

|

|

|

|

|

|

|||||||

| Net investment portfolio |

$ | 606,959 | $ | 894,596 | $ | 1,501,555 | ||||||

|

|

|

|

|

|

|

|||||||

| (1) | Off-balance sheet investments are those owned by our wholly-owned unconsolidated portfolio companies, primarily Medallion Bank. |

Medallion Loans

Taxi medallion loans of $308,408,000 comprised 51% of our $606,959,000 net investment portfolio as of December 31, 2015, compared to $311,894,000 or 59% of our $527,601,000 net investment portfolio as of December 31, 2014. Managed taxi medallion loans of $640,904,000 comprised 43% of our $1,501,555,000 managed net investment portfolio as of December 31, 2015, compared to $677,155,000 or 52% of our $1,310,685,000 managed net investment portfolio as of December 31, 2014. Including loans to unaffiliated investors, the total amount of medallion loans under our management was $667,863,000 as of December 31, 2015, compared to $704,813,000 as of December 31, 2014. Since 1979, we and Medallion Bank have originated, on a combined basis, approximately $3,539,000,000 in medallion loans in New York City, Chicago, Boston, Newark, Cambridge, and other cities within the United States. In addition, our management has a long history of owning, managing, and financing taxicab fleets, taxicab medallions, and corporate car services, dating back to 1956.

Medallion loans collateralized by New York City taxicab medallions and related assets comprised 69% and 68% of the value of the medallion loan portfolio as of December 31, 2015 and 2014, and were 74% on a managed basis. Based on taxi medallion values published by the New York City Taxi and Limousine Commission, or TLC, we estimate that the total value of all of New York City taxicab medallions and related assets such as the vehicle, taximeter, and roof lights exceeded $10.7 billion as of December 31, 2015. We estimate that the total value of all taxicab medallions and related assets in our major US markets exceeded $13.5 billion as of December 31, 2015.

Although some of the medallion loans have from time to time been in arrears or in default, our loss experience on medallion loans has been negligible to date. We believe that our medallion loan portfolio is of good credit quality as all of our medallion loans are secured by the medallion and enhanced with personal guarantees of the shareholders and owners. When a borrower defaults on a loan, we can repossess the medallion collateralizing that loan. If the loan is not brought current, the medallion is sold in the traditionally active market and personal guarantees are pursued.

The following table displays information on managed medallion loans outstanding (other than those managed for third party investors) in each of our major markets at December 31, 2015. For a presentation of only the consolidated on-balance sheet medallion loans, see the Consolidated Summary Schedule of Investments in the consolidated financial statements on page F-32.

| (Dollars in thousands) |

# of Loans | % of Medallion Loan Portfolio (1) |

Average Interest Rate (2) |

Principal Balance |

||||||||||||

| Managed medallion loans |

||||||||||||||||

| New York |

774 | 74 | % | 3.61 | % | $ | 479,588 | |||||||||

| Chicago |

266 | 14 | 4.92 | 92,704 | ||||||||||||

| Newark |

146 | 5 | 5.23 | 31,659 | ||||||||||||

| Boston |

66 | 4 | 4.58 | 29,660 | ||||||||||||

5

Table of Contents

| Cambridge |

22 | 2 | 4.40 | 12,302 | ||||||||||||

| Other |

44 | 1 | 7.80 | 3,805 | ||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total managed medallion loans |

1,318 | 100 | % | 3.96 | 649,718 | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Deferred loan acquisition costs |

760 | |||||||||||||||

| Unrealized depreciation on loans |

(9,574 | ) | ||||||||||||||

|

|

|

|||||||||||||||

| Net managed medallion loans |

$ | 640,904 | ||||||||||||||

|

|

|

| (1) | Based on principal balance outstanding at December 31, 2015. |

| (2) | Based on the contractual rates of the portfolios at December 31, 2015. |

The New York City Market. A New York City taxicab medallion is the only permitted license to operate a taxicab and accept street hails in New York City, except as discussed below. As reported by the TLC, individual (owner-driver) medallions sold for approximately $715,000 and corporate medallions sold for approximately $793,000 as of December 31, 2015. Individual medallions are issued to an owner-driver who must drive the taxicab for a minimum number of hours in each calendar year whereas corporate medallions are medallions that can be aggregated by businesses, leased to drivers, and operated for more than one shift. The number of taxicab medallions is limited by law, and as a result of the limited supply of medallions, an active market for medallions has developed. The law limiting the number of medallions also stipulates that the ownership for the 13,630 medallions outstanding as of December 31, 2015 shall remain divided into 5,733 individual medallions and 7,897 fleet or corporate medallions. Corporate medallions are more valuable because they can be aggregated by businesses, leased to drivers, and operated for more than one shift. New York City auctioned 600 additional medallions during 2004, 308 during 2006, 89 during 2008, 200 in 2013, and 206 in 2014. The medallions auctioned in 2006 were restricted to hybrid fuel vehicles and wheelchair accessible vehicles. In addition, New York City auctioned an additional 63 medallions for wheelchair accessible vehicles in 2007. There was a 25% fare increase which took effect in May 2004 and a 17% fare increase that took effect in September 2012. The New York State legislature enacted a law on December 21, 2011 which was amended on February 17, 2012 to permit cars for hire to pick up street hails in the boroughs outside Manhattan. Pursuant to the law, the TLC began issuing Street Hail Livery licenses in June 2013.

A prospective medallion owner must qualify under the medallion ownership standards set and enforced by the TLC. These standards prohibit individuals with criminal records from owning medallions, require that the funds used to purchase medallions be derived from legitimate sources, and mandate that taxicab vehicles and meters meet TLC specifications. In addition, before the TLC will approve a medallion transfer, the TLC requires a letter from the seller’s insurer stating that there are no outstanding claims for personal injuries in excess of insurance coverage. After the transfer is approved, the owner’s taxicab is subject to quarterly TLC inspections.

Most New York City medallion transfers are handled through approximately 24 medallion brokers licensed by the TLC. In addition to brokering medallions, these brokers also arrange for TLC documentation insurance, vehicles, meters, and financing. We have excellent relations with many of the most active brokers, and regularly receive referrals from them. Brokers generated 24% of the loans originated during 2015, and 28% for 2014. However, we receive most of our referrals from a small number of brokers.

The Chicago Market. We estimate that Chicago medallions sold for approximately $239,000 as of December 31, 2015. Pursuant to a municipal ordinance, the number of outstanding medallions is capped at 6,995 as of December 31, 2015. We estimate that the total value of all Chicago medallions and related assets is over $1,741,755,000 as of December 31, 2015.

The Boston Market. We estimate that Boston medallions sold for approximately $389,000 as of December 31, 2015. The number of Boston medallions is capped at 1,825 as of December 31, 2015. We estimate that the total value of all Boston medallions and related assets is over $732,409,000 as of December 31, 2015.

The Newark Market. We estimate that Newark medallions sold for approximately $321,000 as of December 31, 2015. The number of Newark medallions has been limited to 600 since 1950 by local law. We estimate that the total value of all Newark medallions and related assets is over $196,350,000 as of December 31, 2015.

The Cambridge Market. We estimate that Cambridge medallions sold for approximately $301,000 as of December 31, 2015. The number of Cambridge medallions is 257 as of December 31, 2015. We estimate that the total value of all Cambridge medallions and related assets is over $80,055,000 as of December 31, 2015.

6

Table of Contents

Commercial Loans

Commercial loans finance either the purchase of the equipment and related assets necessary to open a new business or the purchase or improvement of an existing business. From the inception of the commercial loan business in 1987 through December 31, 2015, we and Medallion Bank have originated more than $908,067,000 of commercial loans. Commercial loans of $81,895,000 comprised 14% of our $606,959,000 net investment portfolio as of December 31, 2015, compared to $71,149,000 or 14% of our $527,601,000 net investment portfolio as of December 31, 2014. Managed commercial loans of $125,882,000 comprised 8% of our $1,501,555,000 net investment portfolio as of December 31, 2015, compared to $114,404,000 or 9% of our $1,310,685,000 managed net investment portfolio as of December 31, 2014. We have worked to increase our commercial loan activity in recent years, primarily because of the attractive higher yielding, floating rate nature of most of this business. The outstanding balances of managed commercial loans have grown at a compound annual rate of 6% since 1996. The increase since 1996 has been primarily driven by internal growth through the origination of additional commercial loans. We focus our marketing efforts on the manufacturing, retail trade, professional, scientific, and technical services and other services. The majority of our commercial borrowers are located in the New York metropolitan area and the Midwest. We plan to continue expanding our commercial loan activities by developing a more diverse borrower base, a wider geographic area of coverage, and by expanding targeted industries.

Commercial loans are generally secured by equipment, accounts receivable, real estate, or other assets, and have interest rates averaging 668 basis points over the prevailing prime rate at year end, up from 595 basis points over prime at the end of 2014. As with medallion loans, the vast majority of the principals of borrowers personally guarantee commercial loans. The aggregate realized loss of principal on managed commercial loans has averaged 2.5% per annum for the last five years.

The following table displays information on managed commercial loans outstanding (other than those managed for third party investors) in each of our major markets at December 31, 2015. For a presentation of only the consolidated on-balance sheet commercial loans, see the Consolidated Summary Schedule of Investments in the consolidated financial statements on F-30.

| (Dollars in thousands) |

# of Loans | % of Commercial Loan Portfolio (1) |

Average Interest Rate (2) |

Principal Balance |

||||||||||||

| Managed commercial loans |

||||||||||||||||

| Secured mezzanine |

33 | 53 | % | 13.59 | % | $ | 67,849 | |||||||||

| Asset-based |

49 | 34 | 5.31 | 44,620 | ||||||||||||

| Other secured commercial |

89 | 13 | 9.34 | 16,386 | ||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total managed commercial loans |

171 | 100 | % | 10.18 | 128,855 | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| Deferred loan acquisition income |

(116 | ) | ||||||||||||||

| Unrealized depreciation on loans |

(2,857 | ) | ||||||||||||||

|

|

|

|||||||||||||||

| Net managed commercial loans |

$ | 125,882 | ||||||||||||||

|

|

|

|||||||||||||||

| (1) | Based on principal balance outstanding at December 31, 2015. |

| (2) | Based on the contractual rates of the portfolios at December 31, 2015. |

Secured Mezzanine Loans. Through our subsidiary Medallion Capital, we originate both senior and subordinated loans nationwide to businesses in a variety of industries, including manufacturing and various service providers, more than 70% of which are located in the Midwest and Northeast regions, with the rest scattered across the country. These mezzanine loans are primarily secured by a second position on all assets of the businesses and generally range in amount from $1,000,000 to $5,000,000, and represent approximately 53% of our managed commercial loan portfolio as of December 31, 2015, and were 47% as of December 31, 2014. Frequently, we also receive warrants to purchase an equity interest in the borrowers of secured mezzanine loans.

Asset Based Loans. Through our Medallion Business Credit division, we source, originate, manage, and service asset-based loans to small businesses which require working capital credit facilities ranging from $500,000 to $9,300,000. Medallion Business Credit refers most of its potential commercial loans to Medallion Bank to originate, so that we can benefit from Medallion Bank’s lower cost of funds. Additionally, from time to time, Medallion Business Credit also sells and purchases loan participations to and from independent third party lenders. Together, these loans represent approximately 34% of the managed commercial loan portfolio as of December 31, 2015, and were 37% as of December 31, 2014. These commercial loans are generally secured principally by the borrower’s accounts receivable, but may also be secured by inventory, machinery, equipment, and/or real estate, and are generally personally guaranteed by the principals. Currently, our clients are mostly located in the New York metropolitan area, and include wholesale and retail trade, transportation and warehousing, professional, scientific, and technical services, and other industrial and services businesses. We had successfully originated 49 commercial loans as of December 31, 2015.

Other Secured Commercial Loans. We originate, primarily through our subsidiary Freshstart, other commercial loans that are focused on retail trade businesses, which are typically located within 200 miles of New York City. These commercial loans are generally secured by all of the assets of the businesses and are generally personally guaranteed by the principals. Frequently, we

7

Table of Contents

receive assignments of lease from our borrowers. The loans generally range in size from under $100,000 to approximately $8,300,000. These loans represented approximately 13% of the managed commercial loan portfolio as of December 31, 2015, and were 16% as of December 31, 2014. Historically, most of the portfolio has consisted of fixed-rate loans.

Consumer Loans. Consumer loans are originated by Medallion Bank, a wholly-owned, unconsolidated portfolio company. Consumer loans of $619,887,000 comprised 41% of our $1,501,555,000 managed net investment portfolio as of December 31, 2015, compared to $472,547,000 or 36% of our $1,310,685,000 managed net investment portfolio as of December 31, 2014. The loans are collateralized by recreational vehicles, boats, motorcycles, trailers, and home improvements, located in all 50 states. The portfolio is serviced by a large third party servicer. We believe that Medallion Bank’s consumer loan portfolio is of acceptable credit quality given the high interest rates earned on the loans, which compensate for the higher degree of credit risk in the portfolio.

Other. As a business development company, we also provide debt, mezzanine, and equity investment capital to companies in a variety of industries. These investments may be venture capital style investments which may not be fully collateralized. This is a small, but growing portion of our business.

Our Strategy

Our core philosophy has been “In niches there are riches.” We try to identify markets that are profitable and where we can be an industry leader. Key elements of our strategy include:

Capitalize on our relationships with brokers and dealers. We are committed to establishing, building, and maintaining our relationships with our brokers and dealers. Our marketing efforts are focused on building relationships with brokers in the medallion market and dealers in the consumer market. We believe that our relationships with brokers and dealers provide us with, in addition to potential investment opportunities, other significant benefits, including an additional layer of due diligence and additional monitoring capabilities. We have assembled a management team that has developed an extensive network of broker and dealer relationships in our target markets over the last 50 years. We believe that our management team’s relationships with these brokers and dealers have and will continue to provide us with significant investment opportunities. In 2015, 20% of our managed originated medallion and commercial loans and 100% of our consumer loans were generated by brokers and dealers.

Employ disciplined underwriting policies and maintain rigorous portfolio monitoring. We have an extensive investment underwriting and monitoring process. We conduct a thorough analysis of each potential investment and its prospects, competitive position, financial performance, and industry dynamics. We stress the importance of credit and risk analysis in our underwriting process. We believe that our continued adherence to this disciplined process will permit us to continue to generate a stable, diversified and increasing revenue stream of current income from our debt investments to enable us to make distributions to our shareholders.

Leverage the skills of our experienced management team. Our management team is led by our Chief Executive Officer, Mr. Alvin Murstein, and our President, Mr. Andrew M. Murstein. Alvin Murstein has over 60 years of experience in the ownership, management, and financing of taxicab medallions and other commercial businesses, and Andrew M. Murstein is the third generation in his family to participate in the business and has over 25 years of experience in the ownership, management, and financing of taxicab medallions and other commercial businesses. The other members of our management team have broad investment backgrounds, with prior experience at specialty finance companies, middle market commercial banks, and other financial services companies. We believe that the experience and contacts of our management team will continue to allow us to effectively implement the key aspects of our business strategy.

Perform Strategic Acquisitions. In addition to increasing market share in existing lending markets and identifying new niches, we seek to acquire medallion financing businesses and related portfolios and specialty finance companies that make secured loans to small businesses which have experienced historically low loan losses similar to our own. Since our initial public offering in May 1996, eight specialty finance companies, five loan portfolios, and three taxicab rooftop advertising companies have been acquired.

Investment Activity

The following table sets forth the components of investment activity in the managed investment portfolio for the years indicated.

| Year ended December 31, | ||||||||||||

| (Dollars in thousands) |

2015 | 2014 | 2013 | |||||||||

| Net investments at beginning of year |

$ | 1,310,685 | $ | 1,144,596 | $ | 1,048,635 | ||||||

| Investments originated (1) |

492,127 | 469,816 | 649,776 | |||||||||

| Repayments of investments (1) |

(288,783 | ) | (288,649 | ) | (532,220 | ) | ||||||

| Net realized losses on investments |

(3,902 | ) | (12,290 | ) | (5,163 | ) | ||||||

| Net increase in unrealized appreciation (depreciation) (2) |

3,286 | 8,661 | (3,841 | ) | ||||||||

| Transfers to other assets/liabilities, net |

(8,553 | ) | (8,413 | ) | (9,519 | ) | ||||||

| Amortization of origination costs |

(3,305 | ) | (3,036 | ) | (3,072 | ) | ||||||

|

|

|

|

|

|

|

|||||||

| Net increase in investments |

190,870 | 166,089 | 95,961 | |||||||||

|

|

|

|

|

|

|

|||||||

| Net investments at end of year |

$ | 1,501,555 | $ | 1,310,685 | $ | 1,144,596 | ||||||

|

|

|

|

|

|

|

|||||||

| (1) | Includes refinancings. |

| (2) | Excludes net unrealized appreciation (depreciation) of ($10,839), ($1,759), and $6,647 for the years ended December 31, 2015, 2014, and 2013 related to investments other than securities and other assets. |

8

Table of Contents

Investment Characteristics

Medallion Loans. Our medallion loan portfolio consists of mostly fixed-rate loans, collateralized by first security interests in taxicab medallions and related assets (vehicles, meters, and the like). We estimate that the weighted average loan-to-value ratio of all of the medallion loans was 76% as of December 31, 2015. In addition, we have recourse against a vast majority of the owners of the taxicab medallions and related assets through personal guarantees.

Medallion loans generally require equal monthly payments covering accrued interest and amortization of principal over a five to twenty-five year schedule, subject to a balloon payment of all outstanding principal at maturity. Historically, we have originated loans with one-to-five year maturities where interest rates are adjusted and a new maturity period set. In most cases, borrowers may prepay medallion loans upon payment of a fee of approximately 1% to 2%.

We generally retain the medallion loans we originate; however, from time to time, we participate or sell shares of some loans or portfolios to interested third party financial institutions. In these cases, we retain the borrower relationships and service the sold loans.

Commercial Loans. We have typically originated commercial loans in principal amounts generally ranging from under $100,000 to $9,300,000, and occasionally, have originated loans in excess of that amount. These loans are generally retained and typically have maturities ranging from three to ten years and require monthly payments ranging from full amortization over the loan term to fully deferred interest and principal at maturity, with multiple payment options in between. Substantially all loans may be prepaid with a fee ranging from 30 to 120 days’ interest. The term of, and interest rate charged on, certain of our outstanding loans are subject to SBA regulations. Under SBA regulations, the maximum rate of interest permitted on loans originated by us is 19%. Unlike medallion loans, for which competition precludes us from charging the maximum rate of interest permitted under SBA regulations, we are able to charge the maximum rate on certain commercial loans. We believe that the increased yield on commercial loans compensates for their higher risk relative to medallion loans and further illustrates the benefits of diversification.

Commercial loans are generally originated at an average loan-to-value ratio of 60% to 75%. Substantially all of the commercial loans are collateralized by security interests in the assets being financed by the borrower. In addition, we have recourse against the vast majority of the principals of borrowers who personally guarantee the loans. Although personal guarantees increase the commitment of borrowers to repay their loans, we cannot assure you that the assets available under personal guarantees would, if required, be sufficient to satisfy the obligations secured by such guarantees.

Consumer Loans. Consumer loans generally require equal monthly payments covering accrued interest and amortization of principal over a negotiated term, generally around ten years. Interest rates offered are fixed. Borrowers may prepay consumer loans without any prepayment penalty. In general, Medallion Bank has established relationships with dealers in the industry, who are the sources for most of the customers of Medallion Bank.

Marketing, Origination, and Loan Approval Process

We employ 36 loan originators to originate medallion, commercial, and consumer loans. Each loan application is individually reviewed through analysis of a number of factors, including loan-to-value ratios, a review of the borrower’s credit history, public records, personal interviews, trade references, personal inspection of the premises, and approval from the TLC, SBA, or other regulatory body, if applicable. Each medallion and commercial loan applicant is required to provide personal or corporate tax returns, premises leases, and/or property deeds. Senior management establishes loan origination criteria. Loans that conform to such criteria may be processed by a loan officer with the proper credit authority, and non-conforming loans must be approved by the chief executive officer and/or the chief credit officer. Both medallion and commercial loans are sourced from brokers with extensive networks of applicants, and commercial loans are also referred by contacts with banks, attorneys, and accounting firms. Consumer loans are primarily sourced through relationships which have been established with recreational vehicle and boat dealers, and home improvement contractors throughout our market area.

9

Table of Contents

Sources of Funds

We have historically funded our lending operations primarily through credit facilities with bank syndicates and, to a lesser degree, through equity or debt offerings or private placements, and fixed-rate, senior secured notes and long-term subordinated debentures issued to or guaranteed by the SBA. Since the inception of Medallion Bank, substantially all of Medallion Bank’s funding has been provided by FDIC insured brokered certificates of deposit. The determination of funding sources is established by our management, based upon an analysis of the respective financial and other costs and burdens associated with funding sources. Our funding strategy and interest rate risk management strategy is to have the proper structuring of debt to minimize both rate and maturity risk, while maximizing returns with the lowest cost of funding over an intermediate period of time.

The table below summarizes our sources of available funds and amounts outstanding under credit facilities and their respective end of period weighted average interest rates at December 31, 2015. See Note 4 to the consolidated financial statements for additional information about each credit facility.

| Consolidated sources of funds (Dollars in thousands) |

Total | |||

| Cash |

$ | 30,912 | ||

| Bank loans |

$ | 133,997 | ||

| Amounts undisbursed |

11,568 | |||

| Amounts outstanding |

122,429 | |||

| Average interest rate |

2.60 | % | ||

| Maturity |

2/16-12/20 | |||

| Preferred securities |

$ | 33,000 | ||

| Average interest rate |

2.58 | % | ||

| Maturity |

9/37 | |||

| Lines of credit |

$ | 135,000 | ||

| Amounts undisbursed |

5,482 | |||

| Amounts outstanding |

129,518 | |||

| Average interest rate |

2.05 | % | ||

| Maturity |

12/16 | |||

| Margin loans |

$ | 45,108 | ||

| Average interest rate |

1.48 | % | ||

| Maturity |

N/A | |||

| SBA debentures |

$ | 77,485 | ||

| Amounts undisbursed |

3,000 | |||

| Amounts outstanding |

74,485 | |||

| Average interest rate |

3.52 | % | ||

| Maturity |

3/19-3/26 | |||

|

|

|

|||

| Total cash and amounts remaining undisbursed under credit facilities |

$ | 50,962 | ||

|

|

|

|||

| Total debt outstanding |

$ | 404,540 | ||

|

|

|

|||

| Medallion Bank sources of funds |

||||

| Cash |

$ | 23,094 | ||

| Deposits and other borrowings |

908,896 | |||

| Average interest rate |

1.04 | % | ||

| Maturity |

1/16-12/20 | |||

|

|

|

|||

| Total cash and amounts remaining undisbursed under credit facilities, including Medallion Bank |

$ | 74,056 | ||

|

|

|

|||

| Total debt outstanding, including Medallion Bank |

$ | 1,313,436 | ||

|

|

|

|||

We fund our fixed-rate loans with variable-rate credit lines and bank debt, and with fixed-rate SBA debentures. The mismatch between maturities and interest-rate sensitivities of these balance sheet items results in interest rate risk. We seek to manage our exposure to increases in market rates of interest to an acceptable level by:

| • | Originating adjustable rate loans; |

| • | Incurring fixed-rate debt; and |

| • | Purchasing interest rate caps to hedge a portion of variable-rate debt against increases in interest rates. |

10

Table of Contents

Nevertheless, we accept varying degrees of interest rate risk depending on market conditions. For additional discussion of our funding sources and asset liability management strategy, see Asset/Liability Management on page 54.

Competition

Banks, credit unions, and finance companies, some of which are SBICs, compete with us in originating medallion, commercial, and consumer loans. In addition, finance subsidiaries of equipment manufacturers also compete with us in originating commercial loans. Many of these competitors have greater resources than we do and certain competitors are subject to less restrictive regulations than us. As a result, we cannot assure you that we will be able to identify and complete the financing transactions that will permit us to compete successfully.

Employees

As of December 31, 2015 we employed 143 persons, including 58 at our Medallion Bank subsidiary. We believe that relations with all of our employees are good.

MATERIAL US FEDERAL INCOME TAX CONSIDERATIONS

The following discussion is a general summary of the material US federal income tax considerations applicable to us and to an investment in shares of our common stock. This summary does not purport to be a complete description of the income tax considerations applicable to such an investment. For example, we have not described tax consequences that we assume to be generally known by investors or certain considerations that may be relevant to certain types of holders subject to special treatment under US federal income tax laws, including shareholders subject to the alternative minimum tax, tax-exempt organizations, insurance companies, dealers in securities, pension plans and trusts, and financial institutions. This summary assumes that investors hold our common stock as capital assets (within the meaning of the Code). The discussion is based upon the Code, Treasury regulations, and administrative and judicial interpretations, each as of the date of this annual report and all of which are subject to change, possibly retroactively, which could affect the continuing validity of this discussion. We have not sought and will not seek any ruling from the Internal Revenue Service, or the IRS, regarding an investment in our common stock. This summary does not discuss any aspects of the Medicare Contribution tax, US estate or gift tax, or foreign, state, or local tax. It does not discuss the special treatment under US federal income tax laws that could result if we invested in tax-exempt securities or certain other investment assets.

As used herein, a “US person” is a person that is for US federal income tax purposes:

| • | a citizen or individual resident of the United States; |

| • | a corporation, or other entity treated as a corporation for US federal income tax purposes, created or organized in or under the laws of the US or any state thereof or the District of Columbia; or |

| • | a trust or an estate, the income of which is subject to US federal income taxation regardless of its source. |

A “US shareholder” is a beneficial owner of shares of our common stock that is a US person.

A “non-US shareholder” is a beneficial owner of shares of our common stock that is not a US shareholder and is not a partnership for US federal income tax purposes.

11

Table of Contents

If a partnership (including an entity treated as a partnership for US federal income tax purposes) holds shares of our common stock, the tax treatment of a partner in the partnership will generally depend upon the status of the partner and the activities of the partnership. A prospective shareholder that is a partner of a partnership holding shares of our common stock should consult its tax advisors with respect to the purchase, ownership, and disposition of shares of our common stock.

Tax matters are very complicated and the tax consequences to an investor of an investment in our shares will depend on the facts of his, her, or its particular situation. We encourage investors to consult their own tax advisors regarding the specific consequences of such an investment, including tax reporting requirements, the applicability of federal, state, local, and foreign tax laws, eligibility for the benefits of any applicable tax treaty and the effect of any possible changes in the tax laws.

Election to Be Taxed as a RIC

As a business development company, we have elected to be treated as a RIC under Subchapter M of the Code. As a RIC, we generally will not have to pay corporate-level US federal income taxes on any ordinary income or capital gains that we distribute to our shareholders as dividends. To qualify as a RIC, we must, among other things, meet certain source-of-income and asset diversification requirements (as described below). In addition, to obtain RIC tax treatment we must distribute to our shareholders, for each taxable year, at least 90% of our “investment company taxable income,” which is generally our ordinary income plus the excess of realized net short-term capital gains over realized net long-term capital losses. We refer to this distribution requirement as the Annual Distribution Requirement.

Taxation as a RIC

If we:

| • | qualify as a RIC; and |

| • | satisfy the Annual Distribution Requirement; |

then we will not be subject to US federal income tax on the portion of our investment company taxable income and net capital gain (i.e., net long-term capital gains in excess of net short-term capital losses) we distribute to shareholders. We will be subject to US federal income tax at the regular corporate rates on any income or capital gain not distributed (or deemed distributed) to our shareholders.

We will be subject to a 4% nondeductible US federal excise tax on certain undistributed income of RICs unless we distribute in a timely manner an amount at least equal to the sum of (1) 98% of our ordinary income for each calendar year, (2) 98.2% of our capital gain net income for the one-year period ending October 31 in that calendar year, and (3) any income realized, but not distributed, in preceding years. We refer to this distribution requirement as the Excise Tax Avoidance Requirement. We currently intend to make sufficient distributions each taxable year to satisfy the Excise Tax Avoidance Requirement.

In order to qualify as a RIC for US federal income tax purposes, we must, among other things:

| • | qualify to be treated as a business development company under the 1940 Act at all times during each taxable year; |

| • | derive in each taxable year at least 90% of our gross income from dividends, interest, payments with respect to certain securities loans, gains from the sale of stock or other securities, or foreign currencies, or other income derived with respect to our business of investing in such stock or securities or currencies, and net income derived from interests in “qualified publicly traded partnerships” (i.e., partnerships that are traded on an established securities market or tradable on a secondary market, other than partnerships that derive 90% of their income from interest, dividends, capital gains, and other traditionally permitted mutual fund income described in this paragraph) or the 90% Income Test; and |

| • | diversify our holdings so that at the end of each quarter of the taxable year: |

| • | at least 50% of the value of our assets consists of cash, cash equivalents, US Government securities, securities of other RICs, and other securities if such other securities of any one issuer do not represent more than 5% of the value of our assets or more than 10% of the outstanding voting securities of the issuer; and |

| • | no more than 25% of the value of our assets is invested in the securities, other than US Government securities or securities of other RICs, of one issuer or of two or more issuers that are controlled, as determined under applicable tax rules, by us and that are engaged in the same or similar or related trades or businesses or in the securities of one or more qualified publicly traded partnerships. We refer to these two requirements as the Diversification Tests. |

12

Table of Contents

We may be required to recognize taxable income in circumstances in which we do not receive cash. For example, if we hold debt obligations that are treated under applicable tax rules as having original issue discount (such as debt instruments with payment-in-kind interest or, in certain cases, increasing interest rates or issued with warrants), we must include in income each year a portion of the original issue discount that accrues over the life of the obligation, regardless of whether cash representing such income is received by us in the same taxable year. Because any original issue discount accrued will be included in our investment company taxable income for the year of accrual, we may be required to make a distribution to our shareholders in order to satisfy the Annual Distribution Requirement, even though we will not have received any corresponding cash amount.

Gain or loss realized by us from warrants acquired by us as well as any loss attributable to the lapse of such warrants generally will be treated as capital gain or loss. Such gain or loss generally will be long-term or short-term, depending on how long we held a particular warrant.

We are authorized to borrow funds and to sell assets in order to satisfy distribution requirements. However, under the 1940 Act, we are not permitted to make distributions to our shareholders while our debt obligations and other senior securities are outstanding unless certain “asset coverage” tests are met. See “Regulation—Senior Securities.” Moreover, our ability to dispose of assets to meet our distribution requirements may be limited by (1) the illiquid nature of our portfolio and/or (2) other requirements relating to our status as a RIC, including the Diversification Tests. If we dispose of assets in order to meet the Annual Distribution Requirement or the Excise Tax Avoidance Requirement, we may make such dispositions at times that, from an investment standpoint, are not advantageous.

If we fail to satisfy the Annual Distribution Requirement or otherwise fail to qualify as a RIC in any taxable year, we will be subject to tax in that year on all of our taxable income, regardless of whether we make any distributions to our shareholders. In that case, all of our income will be subject to corporate-level US federal income tax, reducing the amount available to be distributed to our shareholders. In contrast, assuming we qualify as a RIC, our corporate-level federal US income tax should be substantially reduced or eliminated. See “Election to be Taxed as a RIC” above.

The remainder of this discussion assumes that we qualify as a RIC and have satisfied the Annual Distribution Requirement.

Taxation of US Shareholders

Distributions by us generally are taxable to US shareholders as ordinary income or capital gains. Distributions of our “investment company taxable income” (which is, generally, our ordinary income plus realized net short-term capital gains in excess of realized net long-term capital losses) will be taxable as ordinary income to US shareholders to the extent of our current or accumulated earnings and profits, whether paid in cash or reinvested in additional common stock. To the extent such distributions paid by us to non-corporate shareholders (including individuals) are attributable to dividends from US corporations and certain qualified foreign corporations, such distributions generally will be eligible for a maximum tax rate of 20%. In this regard, it is anticipated that distributions paid by us will generally not be attributable to dividends and, therefore, generally will not qualify for the 20% maximum rate. Distributions of our net capital gains (which is generally our realized net long-term capital gains in excess of realized net short-term capital losses) properly reported by us as “capital gain dividends” will be taxable to a US shareholder as long-term capital gains (currently at a maximum rate of 20% in the case of individuals, trusts, or estates), regardless of the US shareholder’s holding period for his, her, or its common stock, and regardless of whether paid in cash or reinvested in additional common stock. Distributions in excess of our earnings and profits first will reduce a US shareholder’s adjusted tax basis in such shareholder’s common stock and, after the adjusted basis is reduced to zero, will constitute capital gains to such US shareholder.

Although we currently intend to distribute any long-term capital gains at least annually, we may in the future decide to retain some or all of our long-term capital gains but designate the retained amount as a “deemed distribution.” In that case, among other consequences, we will pay tax on the retained amount, each US shareholder will be required to include his, her, or its share of the deemed distribution in income as if it had been actually distributed to the US shareholder, and the US shareholder will be entitled to claim a credit equal to his, her, or its allocable share of the tax paid thereon by us. The amount of the deemed distribution net of such tax will be added to the US shareholder’s tax basis for his, her, or its common stock. Since we expect to pay tax on any retained capital gains at our regular corporate tax rate, and since that rate is in excess of the maximum rate currently payable by individuals on long-term capital gains, the amount of tax that individual shareholders will be treated as having paid and for which they will receive a credit will exceed the tax they owe on the retained net capital gain. Such excess generally may be claimed as a credit against the US shareholder’s other US federal income tax obligations or may be refunded to the extent it exceeds a shareholder’s liability for US

13

Table of Contents

federal income tax. A shareholder that is not subject to federal income tax or otherwise required to file a US federal income tax return would be required to file a US federal income tax return on the appropriate form in order to claim a refund for the taxes we paid. In order to utilize the deemed distribution approach, we must provide written notice to our shareholders prior to the expiration of 60 days after the close of the relevant taxable year. We cannot treat any of our investment company taxable income as a “deemed distribution.”

For purposes of determining (1) whether the Annual Distribution Requirement is satisfied for any year and (2) the amount of capital gain dividends paid for that year, we may, under certain circumstances, elect to treat a dividend that is paid during the following taxable year as if it had been paid during the taxable year in question. If we make such an election, the US shareholder will still be treated as receiving the dividend in the taxable year in which the distribution is made. However, any dividend declared by us in October, November, or December of any calendar year, payable to shareholders of record on a specified date in such a month and actually paid during January of the following year, will be treated as if it had been received by our US shareholders on December 31 of the year in which the dividend was declared.

If an investor purchases shares of our common stock shortly before the record date of a distribution, the price of the shares will include the value of the distribution and the investor will be subject to tax on the distribution even though it represents a return of his, her, or its investment.

A shareholder generally will recognize taxable gain or loss if the shareholder sells or otherwise disposes of his, her, or its shares of our common stock. Any gain arising from such sale or disposition generally will be treated as capital gain or loss if the shareholder has held his, her or its shares for more than one year. Otherwise, it would be classified as short-term capital gain or loss. However, any capital loss arising from the sale or disposition of shares of our common stock held for six months or less will be treated as long-term capital loss to the extent of the amount of capital gain dividends received, or undistributed capital gain deemed received, with respect to such shares. In addition, all or a portion of any loss recognized upon a disposition of shares of our common stock may be disallowed if other shares of our common stock are purchased (whether through reinvestment of distributions or otherwise) within 30 days before or after the disposition.

In general, individual and other non-corporate US shareholders currently are subject to a maximum US federal income tax rate of 20% on their net capital gain, i.e., the excess of realized net long-term capital gain over realized net short-term capital loss for a taxable year, including a long-term capital gain derived from an investment in our shares. Such rate is lower than the maximum rate on ordinary income currently payable by individuals. Corporate US shareholders currently are subject to US federal income tax on net capital gain at the maximum 35% rate also applied to ordinary income. Non-corporate shareholders with net capital losses for a year (i.e., capital losses in excess of capital gains) generally may deduct up to $3,000 of such losses against their ordinary income each year; any net capital losses of a non-corporate shareholder in excess of $3,000 generally may be carried forward and used in subsequent years as provided in the Code. Corporate shareholders generally may not deduct any net capital losses against ordinary income for a year, but may carryback such losses for three years or carry forward such losses for five years.

We will send to each of our US shareholders, as promptly as possible after the end of each calendar year, a notice detailing, on a per share basis, the amounts includible in such US shareholder’s taxable income for such year as ordinary income and as long-term capital gain. In addition, the US federal tax status of each year’s distributions generally will be reported to the IRS (including the amount of dividends, if any, eligible for the 20% maximum rate applicable to qualifying dividends). Distributions may also be subject to additional state, local, and foreign taxes depending on a US shareholder’s particular situation. Dividends distributed by us generally will not be eligible for the dividends-received deduction or the 20% maximum rate applicable to qualifying dividends.

We may be required to withhold US federal income tax (“backup withholding”) currently at a rate of 28% from all taxable distributions to any non-corporate US shareholder (1) who fails to furnish us with a correct taxpayer identification number or a certificate that such shareholder is exempt from backup withholding, or (2) with respect to whom the IRS notifies us that such shareholder has failed to properly report certain interest and dividend income to the IRS and to respond to notices to that effect. An individual’s taxpayer identification number is his or her social security number. Any amount withheld under backup withholding is allowed as a credit against the US shareholder’s federal income tax liability and may entitle such shareholder to a refund, provided that proper information is timely provided to the IRS.

The exercise of a warrant to purchase common stock generally will not constitute a taxable event. Accordingly, a holder of a warrant that is a US person generally will not recognize gain or loss upon the exercise of a warrant. Rather, a holder of a warrant that is a US person will recognize taxable gain or loss if and when such holder disposes of the common stock received pursuant to the exercise of the warrant in a taxable transaction. The aggregate tax basis of a US person that is a holder of a warrant in the common stock received pursuant to the exercise of the warrant equals the amount paid upon the exercise of the warrant plus the holder’s basis in the warrant. The holding period of the common stock received pursuant to the exercise of the warrant would begin on the day that the warrant is exercised.

14

Table of Contents

Generally, for United States federal income tax purposes, a holder of a warrant that is a US person will recognize taxable gain or loss upon the sale or other disposition of the warrants in an amount equal to the difference between the amounts realized for the warrants and the holder’s tax basis in the warrants. Such gain or loss will generally be treated as capital gain or loss.

If a warrant is allowed to lapse unexercised, a holder of a warrant that is a US person will recognize a capital loss equal to such holder’s basis in the warrant. Such loss will be long-term if the warrant has been held for more than one year.

The exercise price of the warrants will be adjusted in certain circumstances. Under Section 305(c) of the Code, adjustments (or failures to make adjustments) that have the effect of increasing a holder’s proportionate interest in our assets or earnings may in some circumstances result in a deemed distribution to such holder. Adjustments to the exercise price made pursuant to a bona fide reasonable adjustment formula that has the effect of preventing the dilution of the interest of the holders of the warrants, however, will generally not be considered to result in a deemed distribution to holders. Certain of the possible exercise price adjustments provided in the warrants (including, without limitation, adjustments in respect of taxable dividends to holders of our common stock) may not qualify as being pursuant to a bona fide reasonable adjustment formula. If such adjustments are made, a warrant holder will be deemed to have received a distribution even though such holder has not received any cash or property as a result of such adjustments. Any deemed distributions will be taxable as a dividend, return of capital, or capital gain in accordance with the earnings and profits rules under the Code. US shareholders should consult their own tax advisors regarding the possible application of Section 305(c) of the Code.

Taxation of Non-US Shareholders

Whether an investment in our common stock is appropriate for a non-US shareholder will depend upon that person’s particular circumstances. An investment in our common stock by a non-US shareholder may have adverse tax consequences. Non-US shareholders should consult their tax advisers before investing in our common stock.

Dividends paid by us to non-US shareholders are generally subject to withholding at a 30% rate or a reduced rate specified by an applicable income tax treaty to the extent derived from net investment company income. In order to obtain a reduced rate of withholding, a non-US shareholder will be required to provide an IRS Form W-8BEN or IRS Form W-8BEN-E certifying its entitlement to benefits under a treaty. The withholding tax does not apply to regular dividends paid to a non-US shareholder who provides a Form W-8ECI, certifying that the dividends are effectively connected with the non-US shareholder’s conduct of a trade or business within the United States. Instead, the effectively connected dividends will be subject to regular US income tax as if the non-US shareholder were a US shareholder. A non-US corporation receiving effectively connected dividends may also be subject to additional “branch profits tax” imposed at a rate of 30% (or lower treaty rate). A non-US shareholder who fails to provide an IRS Form W-8BEN or IRS Form W-8BEN-E or other applicable form may be subject to backup withholding at the appropriate rate.

In general, US federal withholding tax will not apply to any gain or income realized by a non-US shareholder in respect of any distributions of net long-term capital gains over net short-term capital losses, exempt-interest dividends, or upon the sale or other disposition of shares of our common stock.

Properly reported dividends are generally exempt from US federal withholding tax where they (i) are paid in respect of our “qualified net interest income” (generally, our US source interest income, other than certain contingent interest and interest from obligations of a corporation or partnership in which we are at least a 10% shareholder, reduced by expenses that are allocable to such income) or (ii) are paid in respect of our “qualified short-term capital gains” (generally, the excess of our net short-term capital gain over our long-term capital loss for such taxable year). However, depending on certain circumstances, we may report all, some, or none of our potentially eligible dividends as such qualified net interest income or as qualified short-term capital gains and/or treat such dividends, in whole or in part, as ineligible for this exemption from withholding. In order to qualify for this exemption from withholding, a non-US shareholder would need to comply with applicable certification requirements relating to its non-US status (including, in general, furnishing an IRS Form W-8BEN or substitute Form). In the case of shares held through an intermediary, the intermediary could withhold even if we designate the payment as qualified net interest income or qualified short-term capital gain. Non-US shareholders should contact their intermediaries with respect to the application of these rules to their accounts.

A 30% withholding tax is currently imposed on dividends, and will be imposed on certain redemption proceeds paid after December 31, 2018, to foreign financial institutions including non-US investment funds and certain other non-financial foreign entities unless they comply with certain information reporting requirements. Non-US persons holding our common shares and warrants should consult with their tax advisors as to the effect of any such withholding tax on their investments.

15

Table of Contents

Non-US persons should consult their own tax advisors with respect to the US federal income tax and withholding tax, and state, local, and foreign tax consequences of an investment in the shares.

Failure to Qualify as a RIC

If we were unable to qualify for treatment as a RIC, we would be subject to tax on all of our taxable income at regular corporate rates. We would not be able to deduct distributions to shareholders, nor would they be required to be made. Distributions would generally be taxable to our shareholders as ordinary dividend income eligible for the 20% maximum rate to the extent of our current and accumulated earnings and profits for US federal tax purposes. Subject to certain limitations under the Code, corporate distributees would be eligible for the dividends received deduction. Distributions in excess of our current and accumulated earnings and profits would be treated first as a return of capital to the extent of the shareholder’s tax basis, and any remaining distributions would be treated as a capital gain.

GOVERNMENT REGULATION

Regulation by the SEC and under the 1940 Act

We are a closed-end, management investment company that has elected to be treated as a business development company (BDC) under the 1940 Act. We conduct our business through various wholly-owned investment company subsidiaries including Medallion Funding LLC, a closed end investment company, Medallion Capital, Inc., a BDC, and Freshstart Venture Capital Corp., a BDC. Pursuant to various exemptive orders, we operate and are regulated as a single BDC. The 1940 Act contains prohibitions and restrictions relating to transactions between BDCs and their affiliates (including any investment advisers or sub-advisers), principal underwriters and affiliates of those affiliates or underwriters, and requires that a majority of the directors be persons other than “interested persons,” as that term is defined in the 1940 Act. In addition, the 1940 Act provides that we may not change the nature of our business so as to cease to be, or to withdraw our election as, a BDC unless approved by a majority of our outstanding voting securities voting as a class.

We may invest up to 100% of our assets in securities acquired directly from issuers in privately negotiated transactions. With respect to such securities, we may, for the purpose of public resale, be deemed an “underwriter” as that term is defined in the Securities Act of 1933. Similarly, in connection with an acquisition, we may acquire rights to require the issuers of acquired securities or their affiliates to repurchase them under certain circumstances. We also do not intend to acquire securities issued by any investment company that exceed the limits imposed by the 1940 Act. Under these limits, we generally cannot acquire more than 3% of the voting stock of any registered investment company, invest more than 5% of the value of our total assets in the securities of one investment company or invest more than 10% of the value of our total assets in the securities of more than one investment company. Certain of these limits are not applicable to our investments in our wholly-owned SBIC subsidiaries. With regard to that portion of our portfolio invested in securities issued by investment companies, it should be noted that such investments might subject our stockholders to additional expenses. None of our policies are fundamental, and each may be changed without stockholder approval.

Qualifying Assets

Under the 1940 Act, a BDC may not acquire any asset other than assets of the type listed in Section 55(a) of the 1940 Act, which are referred to as qualifying assets, unless, at the time the acquisition is made, qualifying assets represent at least 70% of the company’s total assets. The principal categories of qualifying assets relevant to our business are the following:

| (1) | Securities purchased in transactions not involving any public offering from the issuer of such securities, which issuer (subject to certain limited exceptions) is an eligible portfolio company, or from any person who is, or has been during the preceding 13 months, an affiliated person of an eligible portfolio company, or from any other person, subject to such rules as may be prescribed by the SEC. An eligible portfolio company is generally defined in the 1940 Act as any issuer which: |

| (a) | is organized under the laws of, and has its principal place of business in, any state in the US; |

| (b) | is not an investment company (other than a small business investment company wholly owned by the BDC) or a company that would be an investment company but for certain exclusions under the 1940 Act; and |

| (c) | satisfies any of the following: |

| • | does not have any class of securities listed on a national securities exchange, or has a class of securities listed on a national securities exchange, but has an aggregate market value of outstanding voting and non-voting common equity of less than $250 million; |

16

Table of Contents

| • | is controlled by a BDC or a group of companies including a BDC, and the BDC in fact exercises a controlling influence on the management or policies of such eligible portfolio company and, as a result of such control, has an affiliated person who is a director of the eligible portfolio company; or |

| • | is a small and solvent company having total assets of not more than $4 million and capital and surplus of not less than $2 million. |

| (2) | Securities of any eligible portfolio company which we control. |

| (3) | Securities purchased in transactions not involving any public offering from a US issuer that is not an investment company or from an affiliated person of the issuer, or in transactions incident thereto, if the issuer is in bankruptcy and subject to reorganization or if the issuer, immediately prior to the purchase of its securities was unable to meet its obligations as they came due without material assistance other than conventional lending or financing arrangements. |

| (4) | Securities of an eligible portfolio company purchased from any person in a private transaction if there is no ready market for such securities and we already own at least 60% of the outstanding equity of the eligible portfolio company. |

| (5) | Securities received in exchange for or distributed on or with respect to securities described in (1) through (4) above, or pursuant to the exercise of warrants or rights relating to such securities. |

| (6) | Cash, cash equivalents, US Government securities or high-quality debt securities maturing in one year or less from the time of investment. |

| (7) | Subject to certain conditions, securities issued by a company that met the definition of eligible portfolio company at the time of our initial investment but subsequently does not meet the definition because the company no longer meets the definition set forth above. |

Managerial Assistance to Portfolio Companies

In addition, a BDC must have been organized and have its principal place of business in the US and must be operated for the purpose of making investments in the types of securities described in (1), (2), or (3) above. However, in order to count portfolio securities as qualifying assets for the purpose of the 70% test, the BDC must either control the issuer of the securities or must offer to make available to the issuer of the securities (other than small and solvent companies described above) significant managerial assistance; except that, where the BDC purchases such securities in conjunction with one or more other persons acting together, one of the other persons in the group may make available such managerial assistance. Making available managerial assistance means, among other things, any arrangement whereby the BDC, through its directors, officers, or employees, offers to provide, and, if accepted, does so provide, significant guidance and counsel concerning the management, operations, or business objectives and policies of a portfolio company.

Temporary Investments

Pending investment in other types of “qualifying assets,” as described above, our investments may consist of cash equivalents, US government securities, or high-quality debt securities maturing in one year or less from the time of investment, which we refer to, collectively, as temporary investments, so that 70% of our assets are qualifying assets. Typically, we will invest in US Treasury bills or in repurchase agreements, provided that such agreements are fully collateralized by cash or securities issued by the US government or its agencies. A repurchase agreement involves the purchase by an investor, such as us, of a specified security and the simultaneous agreement by the seller to repurchase it at an agreed-upon future date and at a price which is greater than the purchase price by an amount that reflects an agreed-upon interest rate. There is no percentage restriction on the proportion of our assets that may be invested in such repurchase agreements.

Senior Securities