Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Easterly Government Properties, Inc. | d152290d8k.htm |

| EX-99.1 - EX-99.1 - Easterly Government Properties, Inc. | d152290dex991.htm |

| Exhibit 99.2

|

Supplemental Information Package

Fourth Quarter and Year Ended December 31, 2015

|

|

Disclaimers

Forward-looking Statement

We make statements in this Supplemental Information Package that are considered “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, which are usually identified by the use of words such as “anticipates,” “believes,” “estimates,” “expects,” “intends,” “may,” “plans,” “projects,” “seeks,” “should,” “will,” and variations of such words or similar expressions. We intend these forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995 and are including this statement in this Supplemental Information Package for purposes of complying with those safe harbor provisions. These forward-looking statements reflect our current views about our plans, intentions, expectations, strategies and prospects, which are based on the information currently available to us and on assumptions we have made. Although we believe that our plans, intentions, expectations, strategies and prospects as reflected in or suggested by those forward-looking statements are reasonable, we can give no assurance that the plans, intentions, expectations or strategies will be attained or achieved. Furthermore, actual results may differ materially from those described in the forward-looking statements and will be affected by a variety of risks and factors that are beyond our control including, without limitation: risks associated with our dependence on the U.S. Government and its agencies for substantially all of our revenues; risks associated with ownership and development of real estate; decreased rental rates or increased vacancy rates; loss of key personnel; general volatility of the capital and credit markets and the market price of our common stock; the risk that the market price of our common stock may be negatively impacted by increased selling activity following the liquidation of certain private investment funds that contributed assets in our initial public offering; the risk we may lose one or more major tenants; failure of acquisitions or development projects to occur at anticipated levelsorto yield anticipated results; risks associated with actual or threatened terrorist attacks; intense competition in the real estate market that may limit our ability to attract or retain tenants or re-lease space; insufficient amounts of insurance or exposure to events that are either uninsured or underinsured; uncertainties and risks related to adverse weather conditions, natural disasters and climate change; exposure to liability relating to environmental and health and safety matters; limited ability to dispose of assets because of the relative illiquidity of real estate investments and the nature of our assets; exposure to litigation or other claims; risks associated with breaches of our data security; risks associated with our indebtedness; and other risks and uncertainties detailed in the “Risk Factors” section of our Form 10-K for the year ended December 31, 2015, to be filed with the Securities and Exchange Commission on or about March 2, 2016. In addition, our anticipated qualification as a real estate investment trust involves the application of highly technical and complex provisions of the Internal Revenue Code of 1986, or the Code, and depends on our ability to meet the various requirements imposed by the Code through actual operating results, distribution levels and diversity of stock ownership. We assume no obligation to update publicly any forward looking statements, whether as a result of new information, future events or otherwise.

Ratings

Ratings are not recommendations to buy, sell or hold the Company’s securities.

The following discussion related to the consolidated financial statements of the Company should be read in conjunction with the financial statements for the year ended December 31, 2015 that will be released on Form 10-K to be filed on or about March 2, 2016.

| 2 |

|

|

|

Supplemental Definitions

Annualized lease income is defined as the annualized contractual base rent for the last month in a specified period, plus the annualized straight line rent adjustments for the last month in such period and the annualized expense reimbursements earned by us for the last month in such period.

Cash Available for Distribution (CAD), is a non-GAAP financial measure that is not intended to represent cash flow for the period and is not indicative of cash flow provided by operating activities as determined under GAAP. CAD is calculated in accordance with the current NAREIT definition as FFO minus normalized recurring real estate-related expenditures and other non-cash items and nonrecurring expenditures. CAD is presented solely as a supplemental disclosure with respect to liquidity because the Company believes it provides useful information regarding the Company’s ability to fund its dividends. Because all companies do not calculate CAD the same way, the presentation of CAD may not be comparable to similarly titled measures of other companies.

EBITDA is calculated as the sum of net income (loss) before interest expense, income taxes, depreciation and amortization. EBITDA is not intended to represent cash flow for the period, is not presented as an alternative to operating income as an indicator of operating performance, should not be considered in isolation or as a substitute for measures of performance prepared in accordance with GAAP and is not indicative of operating income or cash provided by operating activities as determined under GAAP. EBITDA is presented solely as a supplemental disclosure with respect to liquidity because the Company believes it provides useful information regarding the Company’s ability to service or incur debt. Because all companies do not calculate EBITDA the same way, the presentation of EBITDA may not be comparable to similarly titled measures of other companies.

Fully diluted basis assumes the exchange of all outstanding common units representing limited partnership interests in the Company’s operating partnership, or common units, the full vesting of all restricted stock units, and the exchange of all earned and outstanding LTIP units in the Company’s operating partnership for shares of common stock on a one-for-one basis, which is not the same as the meaning of “fully diluted” under GAAP. Fully diluted basis does not include outstanding LTIP units in the Company’s operating partnership that are subject to performance criteria that have not yet been met.

Funds From Operations (FFO) is generally defined by NAREIT as net income (loss), calculated in accordance with GAAP, excluding gains or losses from sales of property and impairment losses on depreciable real estate, plus real estate depreciation and amortization, and after adjustments for unconsolidated partnerships and joint ventures. FFO is a widely recognized measure of REIT performance. Although FFO is a non-GAAP financial measure, the Company believes that information regarding FFO is helpful to shareholders and potential investors.

Funds From Operations, as Adjusted (FFO, as Adjusted) adjusts Funds From Operations (FFO) to present an alternative measure of our operating performance that we believe is useful to shareholders and potential investors, which, when applicable, excludes the impact of acquisition costs, straight-line rent, above-/below-market leases, non-cash interest and non-cash compensation. In the Future, we may also exclude other items from FFO, as Adjusted that we believe may help investors compare our results. Because all companies do not calculate FFO, as Adjusted in the same way, the presentation of FFO, as Adjusted may not be comparable to similarly titled measures of other companies.

Net Operating Income (NOI) is calculated as total property revenues (rental income, tenant reimbursements and other income) less property operating expenses and real estate taxes from the properties owned by the Company. Cash NOI excludes from NOI straight-line rent and amortization of above-/below-market leases. NOI presented by the Company may not be comparable to NOI reported by other REITs that define NOI differently. NOI should not be considered an alternative to net incomeasan indication of our performance or to cash flows as a measure of the Company’s liquidity or its ability to make distributions.

Pro forma year ended December 31, 2015 (1) removes from the Company’s financial results for the period from February 11, 2015 (the date of the closing of the Company’s initial public offering) to December 31, 2015 the impact of one-time, non-recurring expenses related to its initial public offering, including legal and accounting fees and new entity formation costs and (2) reflects a full quarter of operations for the period from January 1, 2015 to March 31, 2015 on a pro forma basis basedonthe financial results of the 49 days of operations between February 11, 2015 and March 31, 2015.

| 3 |

|

|

|

Table of Contents

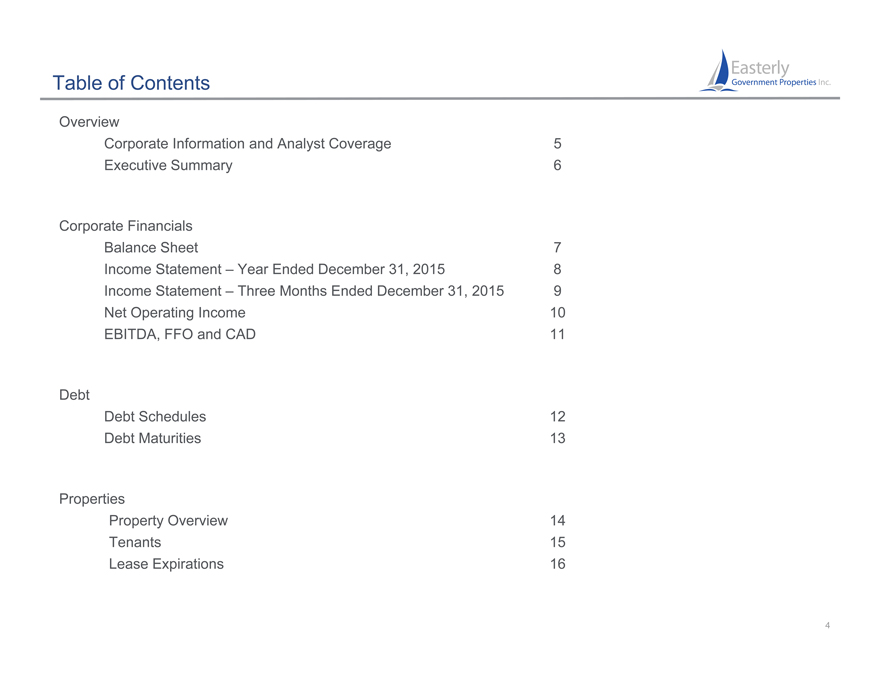

Overview

Corporate Information and Analyst Coverage 5

Executive Summary 6

Corporate Financials

Balance Sheet 7

Income Statement – Year Ended December 31, 2015 8

Income Statement – Three Months Ended December 31, 2015 9

Net Operating Income 10

EBITDA, FFO and CAD 11

Debt

Debt Schedules 12

Debt Maturities 13

Properties

Property Overview 14

Tenants 15

Lease Expirations 16

| 4 |

|

|

|

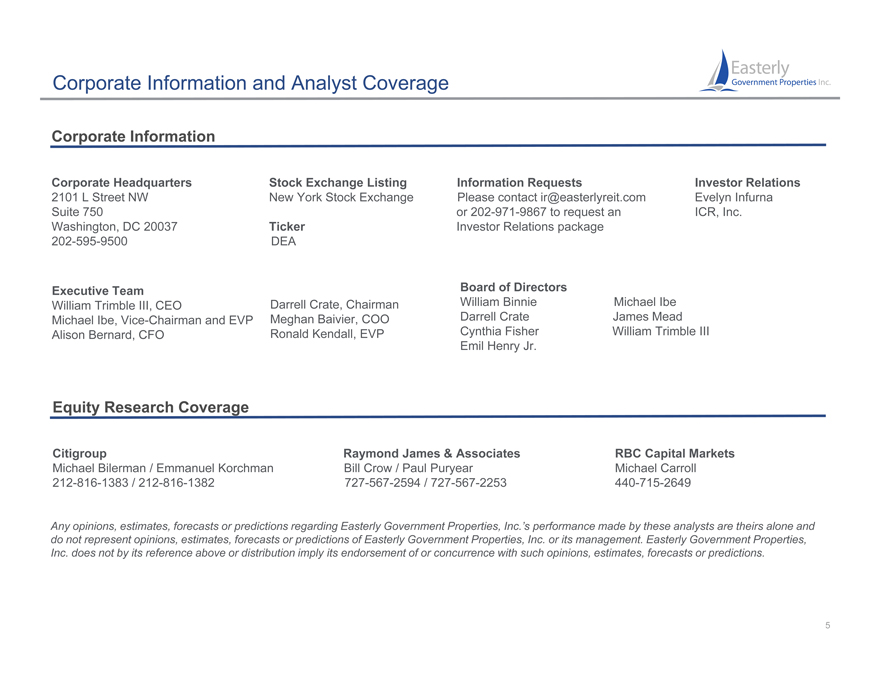

Corporate Information and Analyst Coverage

Corporate Information

Corporate Headquarters Stock Exchange Listing Information Requests Investor Relations

2101 L Street NW New York Stock Exchange Please contact ir@easterlyreit.com Evelyn Infurna

Suite 750 or 202-971-9867 to request an ICR, Inc.

Washington, DC 20037 Ticker Investor Relations package

202-595-9500 DEA

Executive Team Board of Directors

William Trimble III, CEO Darrell Crate, Chairman William Binnie Michael Ibe

Michael Ibe, Vice-Chairman and EVP Meghan Baivier, COO Darrell Crate James Mead

Alison Bernard, CFO Ronald Kendall, EVP Cynthia Fisher William Trimble III

Emil Henry Jr.

Equity Research Coverage

Citigroup Raymond James & Associates RBC Capital Markets

Michael Bilerman / Emmanuel Korchman Bill Crow / Paul Puryear Michael Carroll

212-816-1383 / 212-816-1382 727-567-2594 / 727-567-2253 440-715-2649

Any opinions, estimates, forecasts or predictions regarding Easterly Government Properties, Inc.’s performance made by these analysts are theirs alone and

do not represent opinions, estimates, forecasts or predictions of Easterly Government Properties, Inc. or its management. Easterly Government Properties,

Inc. does not by its reference above or distribution imply its endorsement of or concurrence with such opinions, estimates, forecasts or predictions.

| 5 |

|

|

|

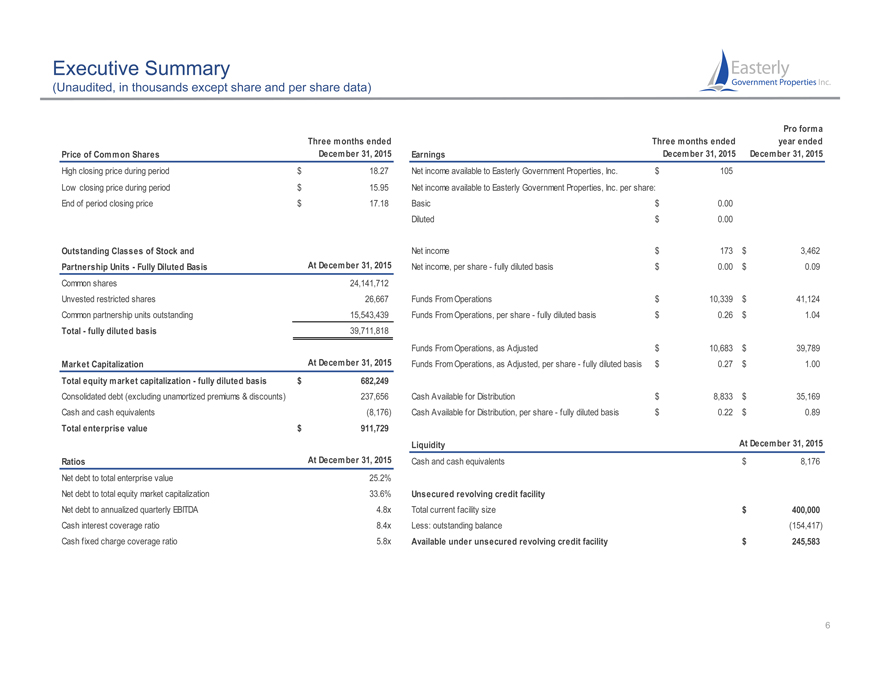

Executive Summary

(Unaudited, in thousands except share and per share data)

Pro forma

Three months ended Three months ended year ended

Price of Common Shares December 31, 2015 Earnings December 31, 2015 December 31, 2015

High closing price during period $ 18.27 Net income available to Easterly Government Properties, Inc. $ 105

Low closing price during period $ 15.95 Net income available to Easterly Government Properties, Inc. per share:

End of period closing price $ 17.18 Basic $ 0.00

Diluted $ 0.00

Outstanding Classes of Stock and Net income $ 173 $ 3,462

Partnership Units—Fully Diluted Basis At December 31, 2015 Net income, per share—fully diluted basis $ 0.00 $ 0.09

Common shares 24,141,712

Unvested restricted shares 26,667 Funds From Operations $ 10,339 $ 41,124

Common partnership units outstanding 15,543,439 Funds From Operations, per share—fully diluted basis $ 0.26 $ 1.04

Total—fully diluted basis 39,711,818

Funds From Operations, as Adjusted $ 10,683 $ 39,789

Market Capitalization At December 31, 2015 Funds From Operations, as Adjusted, per share—fully diluted basis $ 0.27 $ 1.00

Total equity market capitalization—fully diluted basis $ 682,249

Consolidated debt (excluding unamortized premiums & discounts) 237,656 Cash Available for Distribution $ 8,833 $ 35,169

Cash and cash equivalents(8,176) Cash Available for Distribution, per share—fully diluted basis $ 0.22 $ 0.89

Total enterprise value $ 911,729

Liquidity At December 31, 2015

Ratios At December 31, 2015 Cash and cash equivalents $ 8,176

Net debt to total enterprise value 25.2%

Net debt to total equity market capitalization 33.6% Unsecured revolving credit facility

Net debt to annualized quarterly EBITDA 4.8x Total current facility size $ 400,000

Cash interest coverage ratio 8.4x Less: outstanding balance(154,417)

Cash fixed charge coverage ratio 5.8x Available under unsecured revolving credit facility $ 245,583

| 6 |

|

|

|

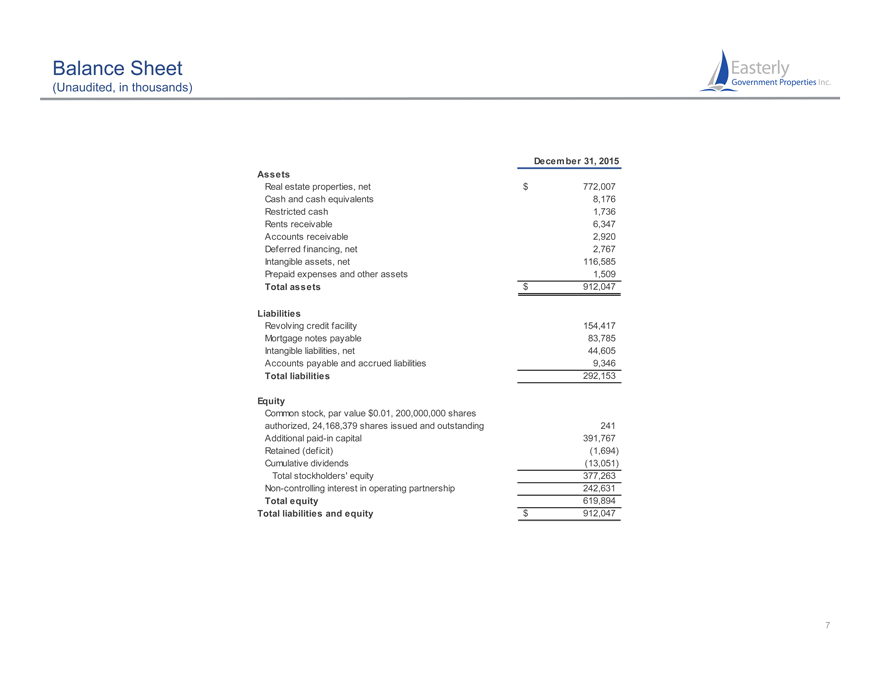

Balance Sheet

(Unaudited, in thousands)

December 31, 2015

Assets

Real estate properties, net $ 772,007

Cash and cash equivalents 8,176

Restricted cash 1,736

Rents receivable 6,347

Accounts receivable 2,920

Deferred financing, net 2,767

Intangible assets, net 116,585

Prepaid expenses and other assets 1,509

Total assets $ 912,047

Liabilities

Revolving credit facility 154,417

Mortgage notes payable 83,785

Intangible liabilities, net 44,605

Accounts payable and accrued liabilities 9,346

Total liabilities 292,153

Equity

Common stock, par value $0.01, 200,000,000 shares

authorized, 24,168,379 shares issued and outstanding 241

Additional paid-in capital 391,767

Retained (deficit)(1,694)

Cumulative dividends(13,051)

Total stockholders’ equity 377,263

Non-controlling interest in operating partnership 242,631

Total equity 619,894

Total liabilities and equity $ 912,047

| 7 |

|

|

|

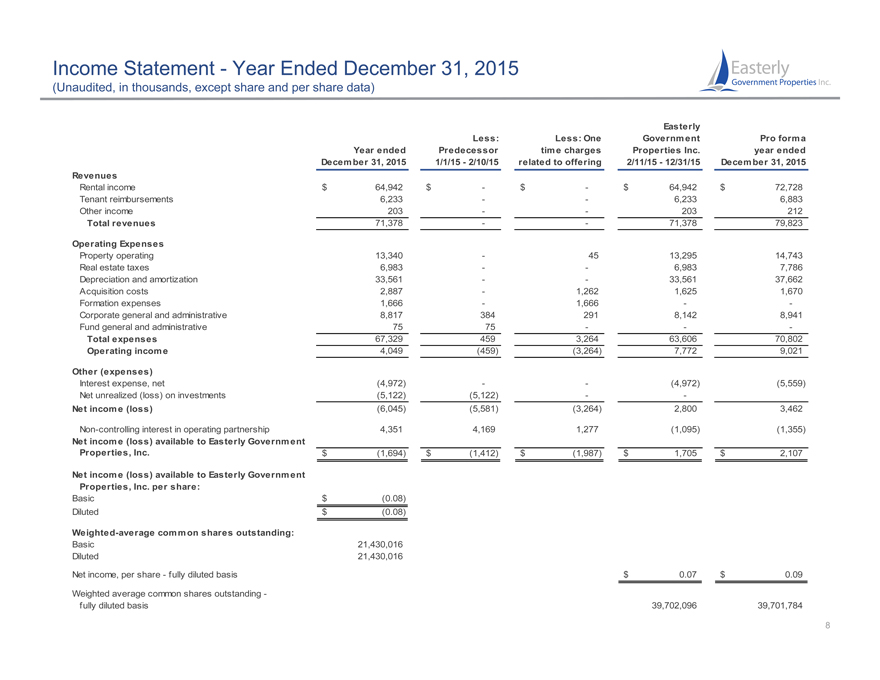

Income Statement—Year Ended December 31, 2015

(Unaudited, in thousands, except share and per share data)

Easterly

Less: Less: One Government Pro forma

Year ended Predecessor time charges Properties Inc. year ended

December 31, 2015 1/1/15—2/10/15 related to offering 2/11/15—12/31/15 December 31, 2015

Revenues

Rental income $ 64,942 $—$—$ 64,942 $ 72,728

Tenant reimbursements 6,233 — 6,233 6,883

Other income 203 — 203 212

Total revenues 71,378 — 71,378 79,823

Operating Expenses

Property operating 13,340—45 13,295 14,743

Real estate taxes 6,983 — 6,983 7,786

Depreciation and amortization 33,561 — 33,561 37,662

Acquisition costs 2,887—1,262 1,625 1,670

Formation expenses 1,666—1,666 —

Corporate general and administrative 8,817 384 291 8,142 8,941

Fund general and administrative 75 75 — -

Total expenses 67,329 459 3,264 63,606 70,802

Operating income 4,049(459)(3,264) 7,772 9,021

Other (expenses)

Interest expense, net(4,972) —(4,972)(5,559)

Net unrealized (loss) on investments(5,122)(5,122) —

Net income (loss)(6,045)(5,581)(3,264) 2,800 3,462

Non-controlling interest in operating partnership 4,351 4,169 1,277(1,095)(1,355)

Net income (loss) available to Easterly Government

Properties, Inc. $(1,694) $(1,412) $(1,987) $ 1,705 $ 2,107

Net income (loss) available to Easterly Government

Properties, Inc. per share:

Basic $(0.08)

Diluted $(0.08)

Weighted-average common shares outstanding:

Basic 21,430,016

Diluted 21,430,016

Net income, per share—fully diluted basis $ 0.07 $ 0.09

Weighted average common shares outstanding -

fully diluted basis 39,702,096 39,701,784

| 8 |

|

|

|

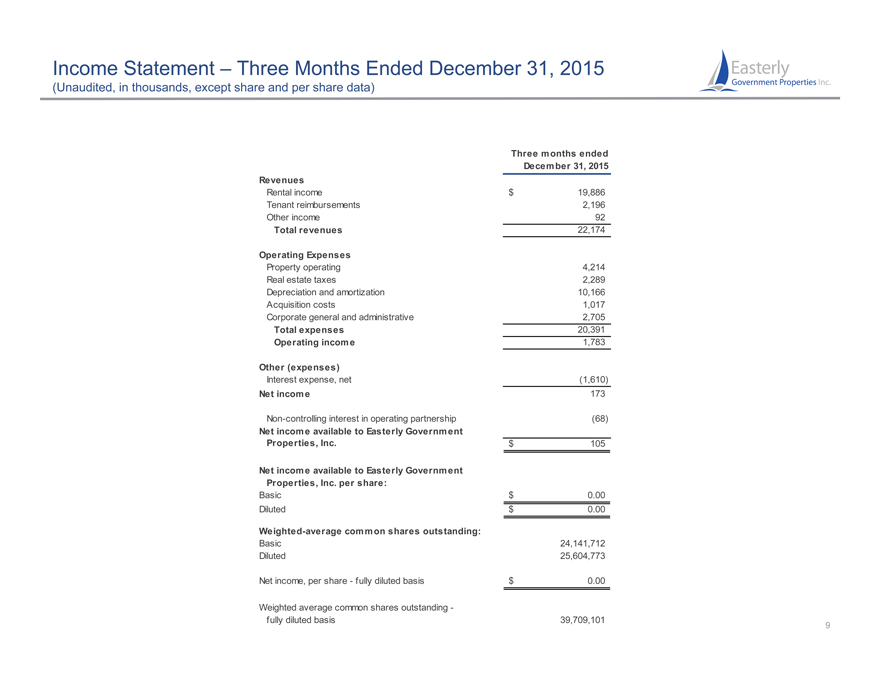

Income Statement – Three Months Ended December 31, 2015

(Unaudited, in thousands, except share and per share data)

Three months ended

December 31, 2015

Revenues

Rental income $ 19,886

Tenant reimbursements 2,196

Other income 92

Total revenues 22,174

Operating Expenses

Property operating 4,214

Real estate taxes 2,289

Depreciation and amortization 10,166

Acquisition costs 1,017

Corporate general and administrative 2,705

Total expenses 20,391

Operating income 1,783

Other (expenses)

Interest expense, net(1,610)

Net income 173

Non-controlling interest in operating partnership(68)

Net income available to Easterly Government

Properties, Inc. $ 105

Net income available to Easterly Government

Properties, Inc. per share:

Basic $ 0.00

Diluted $ 0.00

Weighted-average common shares outstanding:

Basic 24,141,712

Diluted 25,604,773

Net income, per share—fully diluted basis $ 0.00

Weighted average common shares outstanding -

fully diluted basis 39,709,101 9

|

|

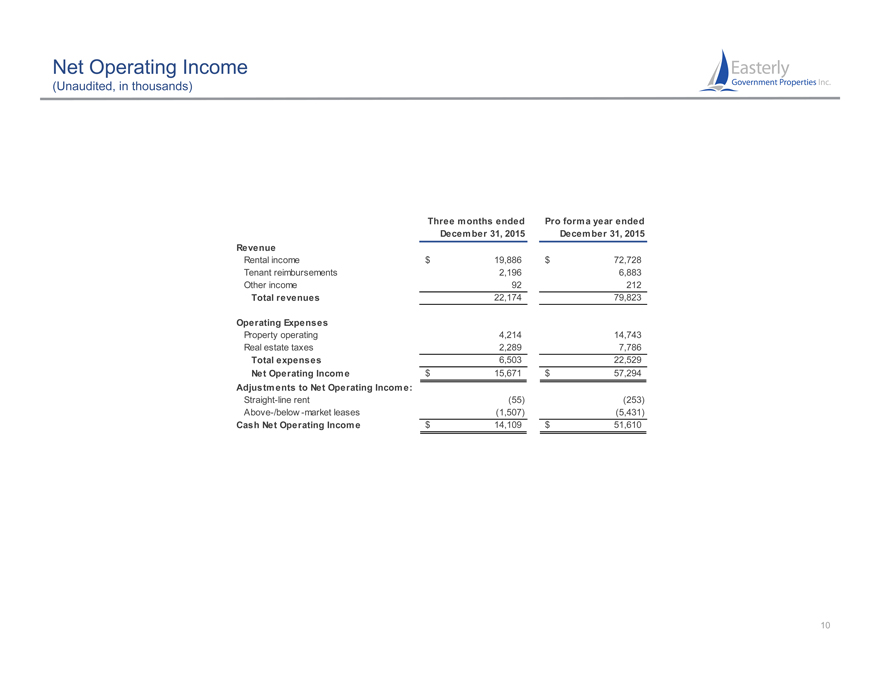

Net Operating Income

(Unaudited, in thousands)

Three months ended Pro forma year ended

December 31, 2015 December 31, 2015

Revenue

Rental income $ 19,886 $ 72,728

Tenant reimbursements 2,196 6,883

Other income 92 212

Total revenues 22,174 79,823

Operating Expenses

Property operating 4,214 14,743

Real estate taxes 2,289 7,786

Total expenses 6,503 22,529

Net Operating Income $ 15,671 $ 57,294

Adjustments to Net Operating Income:

Straight-line rent(55)(253)

Above-/below -market leases(1,507)(5,431)

Cash Net Operating Income $ 14,109 $ 51,610

| 10 |

|

|

|

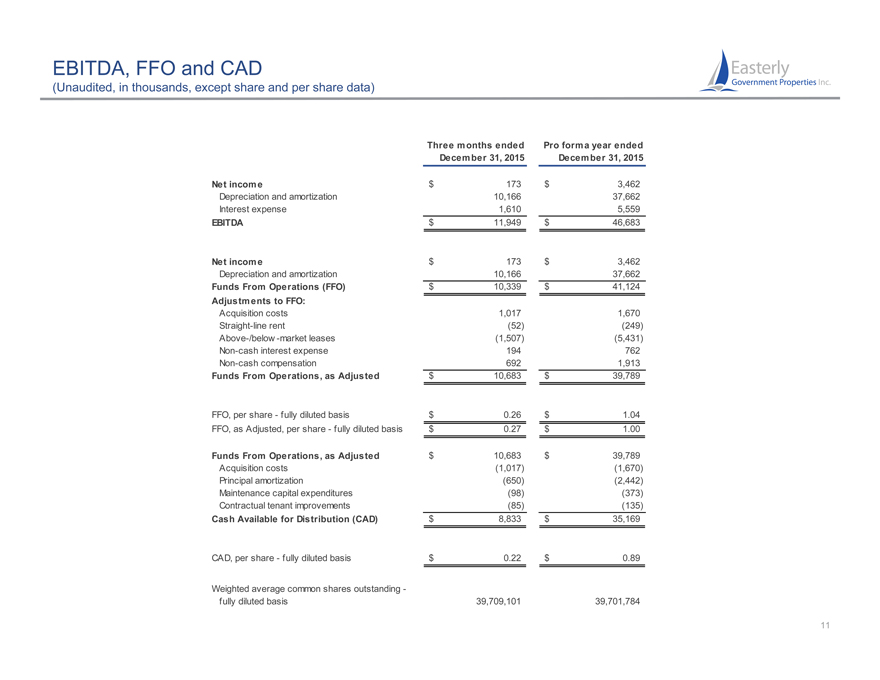

EBITDA, FFO and CAD

(Unaudited, in thousands, except share and per share data)

Three months ended Pro forma year ended

December 31, 2015 December 31, 2015

Net income $ 173 $ 3,462

Depreciation and amortization 10,166 37,662

Interest expense 1,610 5,559

EBITDA $ 11,949 $ 46,683

Net income $ 173 $ 3,462

Depreciation and amortization 10,166 37,662

Funds From Operations (FFO) $ 10,339 $ 41,124

Adjustments to FFO:

Acquisition costs 1,017 1,670

Straight-line rent(52)(249)

Above-/below -market leases(1,507)(5,431)

Non-cash interest expense 194 762

Non-cash compensation 692 1,913

Funds From Operations, as Adjusted $ 10,683 $ 39,789

FFO, per share—fully diluted basis $ 0.26 $ 1.04

FFO, as Adjusted, per share—fully diluted basis $ 0.27 $ 1.00

Funds From Operations, as Adjusted $ 10,683 $ 39,789

Acquisition costs(1,017)(1,670)

Principal amortization(650)(2,442)

Maintenance capital expenditures(98)(373)

Contractual tenant improvements(85)(135)

Cash Available for Distribution (CAD) $ 8,833 $ 35,169

CAD, per share—fully diluted basis $ 0.22 $ 0.89

Weighted average common shares outstanding -

fully diluted basis 39,709,101 39,701,784

| 11 |

|

|

|

Debt Schedules

(Unaudited, in thousands)

December 31, 2015

December 31, 2015 Percent of

Debt Instrument Maturity Date Stated Rate (2) Balance Total Indebtedness

Unsecured revolving credit facility

Unsecured revolving credit facility(1) 11-Feb-19(3) LIBOR + 140bps $ 154,417 65.0%

| 3.1 |

|

years 1.75% |

Total unsecured revolving credit facility $ 154,417 65.0%

(wtd-avg maturity)(wtd-avg rate)

Secured mortgage debt

ICE—Charleston 15-Jan-27 4.21% $ 21,993 9.3%

USFS II—Albuquerque 14-Jul-26 4.46% 17,477 7.4%

DEA—Pleasanton 18-Oct-23 LIBOR + 150bps 15,700 6.6%

CBP—Savannah 10-Jul-33 3.40% 15,580 6.4%

MEPCOM—Jacksonville 14-Oct-25 4.41% 12,489 5.3%

| 11.4 |

|

years 3.68% |

Total secured mortgage debt $ 83,239 35.0%

(wtd-avg maturity)(wtd-avg rate)

Debt Statistics December 31, 2015

Variable rate debt—unhedged $ 170,117

Fixed rate debt 67,539

Total debt (excluding unamortized premiums & discounts) $ 237,656

% Variable rate debt—unhedged 71.6%

% Fixed rate debt 28.4%

Weighted average maturity 6 years

Weighted average interest rate 2.4%

(1)Credit facility has available capacity of $245,583 as of December 31, 2015.

(2)Average stated rates represent the weighted average interest rate at December 31, 2015.

(3)Credit facility has two six-month as-of-right extension options subject to certain conditions and the payment of an extension fee. 12

|

|

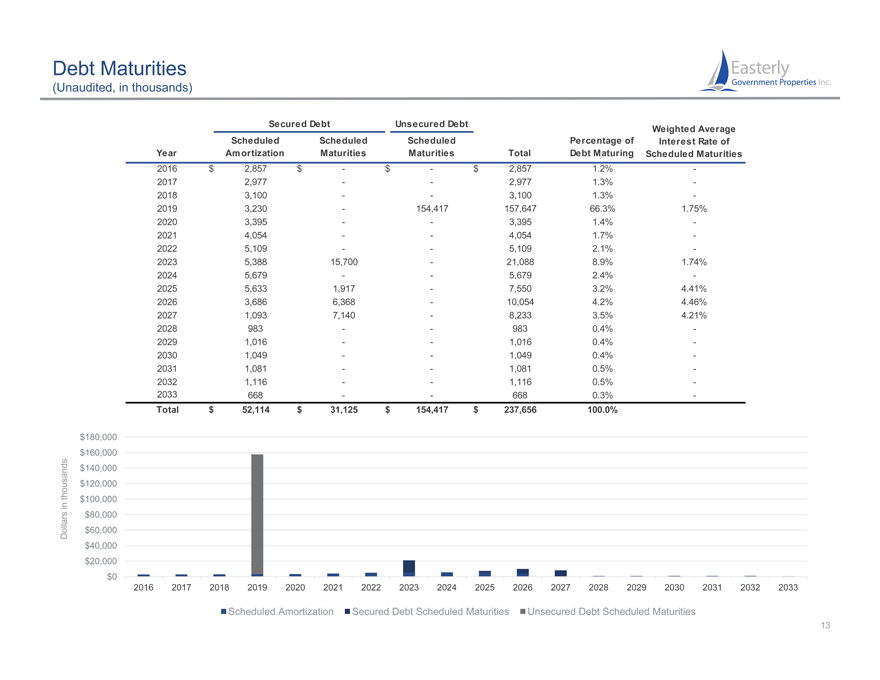

Debt Maturities

(Unaudited, in thousands)

Secured Debt Unsecured Debt Weighted Average

Scheduled Scheduled Scheduled Percentage of Interest Rate of

Year Amortization Maturities Maturities Total Debt Maturing Scheduled Maturities

2016 $ 2,857 $—$—$ 2,857 1.2% -

2017 2,977 — 2,977 1.3% -

2018 3,100 — 3,100 1.3% -

2019 3,230—154,417 157,647 66.3% 1.75%

2020 3,395 — 3,395 1.4% -

2021 4,054 — 4,054 1.7% -

2022 5,109 — 5,109 2.1% -

2023 5,388 15,700—21,088 8.9% 1.74%

2024 5,679 — 5,679 2.4% -

2025 5,633 1,917—7,550 3.2% 4.41%

2026 3,686 6,368—10,054 4.2% 4.46%

2027 1,093 7,140—8,233 3.5% 4.21%

2028 983 — 983 0.4% -

2029 1,016 — 1,016 0.4% -

2030 1,049 — 1,049 0.4% -

2031 1,081 — 1,081 0.5% -

2032 1,116 — 1116, 05%. -

2033 668 — 668 0.3% -

Total $ 52,114 $ 31,125 $ 154,417 $ 237,656 100.0%

$180,000

$160,000

ds $140,000

thousan $120,000

$100,000

in

$80,000

Dollars $60,000

$40,000

$20,000

$0

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033

Scheduled Amortization Secured Debt Scheduled Maturities Unsecured Debt Scheduled Maturities

| 13 |

|

|

|

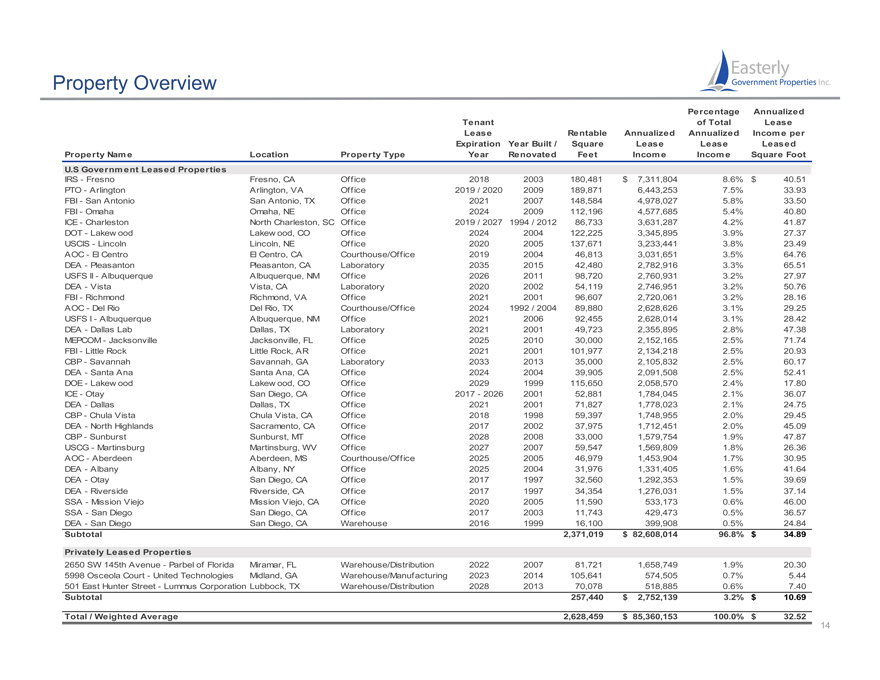

Property Overview

Percentage Annualized

Tenant of Total Lease

Lease Rentable Annualized Annualized Income per

Expiration Year Built / Square Lease Lease Leased

Property Name Location Property Type Year Renovated Feet Income Income Square Foot

U.S Government Leased Properties

IRS—Fresno Fresno, CA Office 2018 2003 180,481 $ 7,311,804 8.6% $ 40.51

PTO—Arlington Arlington, VA Office 2019 / 2020 2009 189,871 6,443,253 7.5% 33.93

FBI—San Antonio San Antonio, TX Office 2021 2007 148,584 4,978,027 5.8% 33.50

FBI—Omaha Omaha, NE Office 2024 2009 112,196 4,577,685 5.4% 40.80

ICE—Charleston North Charleston, SC Office 2019 / 2027 1994 / 2012 86,733 3,631,287 4.2% 41.87

DOT—Lakew ood Lakew ood, CO Office 2024 2004 122,225 3,345,895 3.9% 27.37

USCIS—Lincoln Lincoln, NE Office 2020 2005 137,671 3,233,441 3.8% 23.49

AOC—El Centro El Centro, CA Courthouse/Office 2019 2004 46,813 3,031,651 3.5% 64.76

DEA—Pleasanton Pleasanton, CA Laboratory 2035 2015 42,480 2,782,916 3.3% 65.51

USFS II—Albuquerque Albuquerque, NM Office 2026 2011 98,720 2,760,931 3.2% 27.97

DEA—Vista Vista, CA Laboratory 2020 2002 54,119 2,746,951 3.2% 50.76

FBI—Richmond Richmond, VA Office 2021 2001 96,607 2,720,061 3.2% 28.16

AOC—Del Rio Del Rio, TX Courthouse/Office 2024 1992 / 2004 89,880 2,628,626 3.1% 29.25

USFS I—Albuquerque Albuquerque, NM Office 2021 2006 92,455 2,628,014 3.1% 28.42

DEA—Dallas Lab Dallas, TX Laboratory 2021 2001 49,723 2,355,895 2.8% 47.38

MEPCOM—Jacksonville Jacksonville, FL Office 2025 2010 30,000 2,152,165 2.5% 71.74

FBI—Little Rock Little Rock, AR Office 2021 2001 101,977 2,134,218 2.5% 20.93

CBP—Savannah Savannah, GA Laboratory 2033 2013 35,000 2,105,832 2.5% 60.17

DEA—Santa Ana Santa Ana, CA Office 2024 2004 39,905 2,091,508 2.5% 52.41

DOE—Lakew ood Lakew ood, CO Office 2029 1999 115,650 2,058,570 2.4% 17.80

ICE—Otay San Diego, CA Office 2017—2026 2001 52,881 1,784,045 2.1% 36.07

DEA—Dallas Dallas, TX Office 2021 2001 71,827 1,778,023 2.1% 24.75

CBP—Chula Vista Chula Vista, CA Office 2018 1998 59,397 1,748,955 2.0% 29.45

DEA—North Highlands Sacramento, CA Office 2017 2002 37,975 1,712,451 2.0% 45.09

CBP—Sunburst Sunburst, MT Office 2028 2008 33,000 1,579,754 1.9% 47.87

USCG—Martinsburg Martinsburg, WV Office 2027 2007 59,547 1,569,809 1.8% 26.36

AOC—Aberdeen Aberdeen, MS Courthouse/Office 2025 2005 46,979 1,453,904 1.7% 30.95

DEA—Albany Albany, NY Office 2025 2004 31,976 1,331,405 1.6% 41.64

DEA—Otay San Diego, CA Office 2017 1997 32,560 1,292,353 1.5% 39.69

DEA—Riverside Riverside, CA Office 2017 1997 34,354 1,276,031 1.5% 37.14

SSA—Mission Viejo Mission Viejo, CA Office 2020 2005 11,590 533,173 0.6% 46.00

SSA—San Diego San Diego, CA Office 2017 2003 11,743 429,473 0.5% 36.57

DEA—San Diego San Diego, CA Warehouse 2016 1999 16,100 399,908 0.5% 24.84

Subtotal 2,371,019 $ 82,608,014 96.8% $ 34.89

Privately Leased Properties

2650 SW 145th Avenue—Parbel of Florida Miramar, FL Warehouse/Distribution 2022 2007 81,721 1,658,749 1.9% 20.30

5998 Osceola Court—United Technologies Midland, GA Warehouse/Manufacturing 2023 2014 105,641 574,505 0.7% 5.44

501 East Hunter Street—Lummus Corporation Lubbock, TX Warehouse/Distribution 2028 2013 70,078 518,885 0.6% 7.40

Subtotal 257,440 $ 2,752,139 3.2% $ 10.69

Total / Weighted Average 2,628,459 $ 85,360,153 100.0% $ 32.52

| 14 |

|

|

|

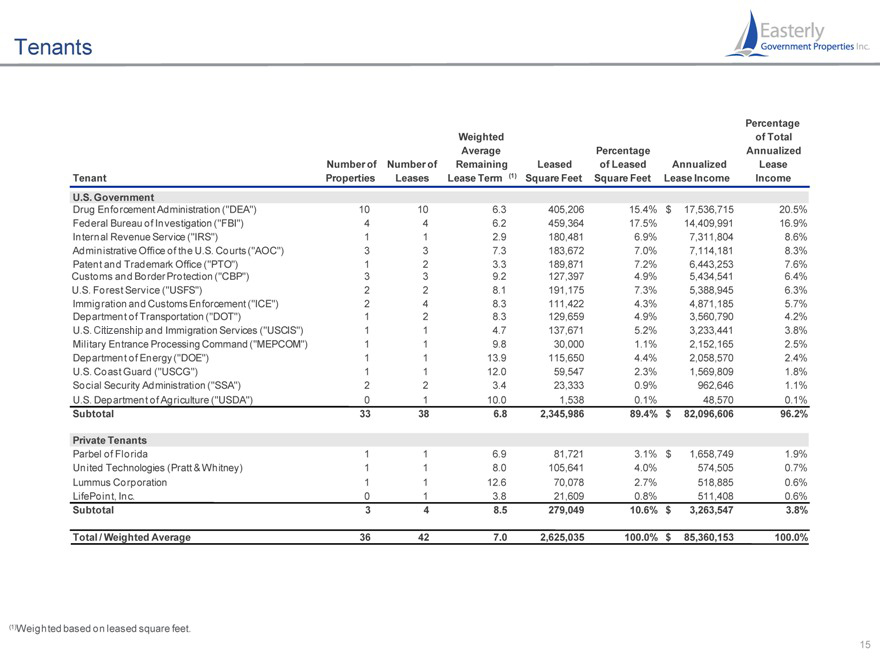

Tenants

Percentage

Weighted of Total

Average Percentage Annualized

Number of Number of Remaining Leased of Leased Annualized Lease

Tenant Properties Leases Lease Term (1) Square Feet Square Feet Lease Income Income

U.S. Government

Drug Enforcement Administration (“DEA”) 10 10 6.3 405,206 15.4% $ 17,536,715 20.5%

Federal Bureau of Investigation (“FBI”) 4 4 6.2 459,364 17.5% 14,409,991 16.9%

Internal Revenue Service (“IRS”) 1 1 2.9 180,481 6.9% 7,311,804 8.6%

Administrative Office of the U.S. Courts (“AOC”) 3 3 7.3 183,672 7.0% 7,114,181 8.3%

Patent and Trademark Office (“PTO”) 1 2 3.3 189,871 7.2% 6,443,253 7.6%

Customs and Border Protection (“CBP”) 3 3 9.2 127,397 4.9% 5,434,541 6.4%

U.S. Forest Service (“USFS”) 2 2 8.1 191,175 7.3% 5,388,945 6.3%

Immigration and Customs Enforcement (“ICE”) 2 4 8.3 111,422 4.3% 4,871,185 5.7%

Department of Transportation (“DOT”) 1 2 8.3 129,659 4.9% 3,560,790 4.2%

U.S. Citizenship and Immigration Services (“USCIS”) 1 1 4.7 137,671 5.2% 3,233,441 3.8%

Military Entrance Processing Command (“MEPCOM”) 1 1 9.8 30,000 1.1% 2,152,165 2.5%

Department of Energy (“DOE”) 1 1 13.9 115,650 4.4% 2,058,570 2.4%

U.S. Coast Guard (“USCG”) 1 1 12.0 59,547 2.3% 1,569,809 1.8%

Social Security Administration (“SSA”) 2 2 3.4 23,333 0.9% 962,646 1.1%

U.S. Department of Agriculture (“USDA”) 0 1 10.0 1,538 0.1% 48,570 0.1%

Subtotal 33 38 6.8 2,345,986 89.4% $ 82,096,606 96.2%

Private Tenants

Parbel of Florida 1 1 6.9 81,721 3.1% $ 1,658,749 1.9%

United Technologies (Pratt & Whitney) 1 1 8.0 105,641 4.0% 574,505 0.7%

Lummus Corporation 1 1 12.6 70,078 2.7% 518,885 0.6%

LifePoint, Inc. 0 1 3.8 21,609 0.8% 511,408 0.6%

Subtotal 3 4 8.5 279,049 10.6% $ 3,263,547 3.8%

Total / Weighted Average 36 42 7.0 2,625,035 100.0% $ 85,360,153 100.0%

(1)Weighted based on leased square feet.

| 15 |

|

|

|

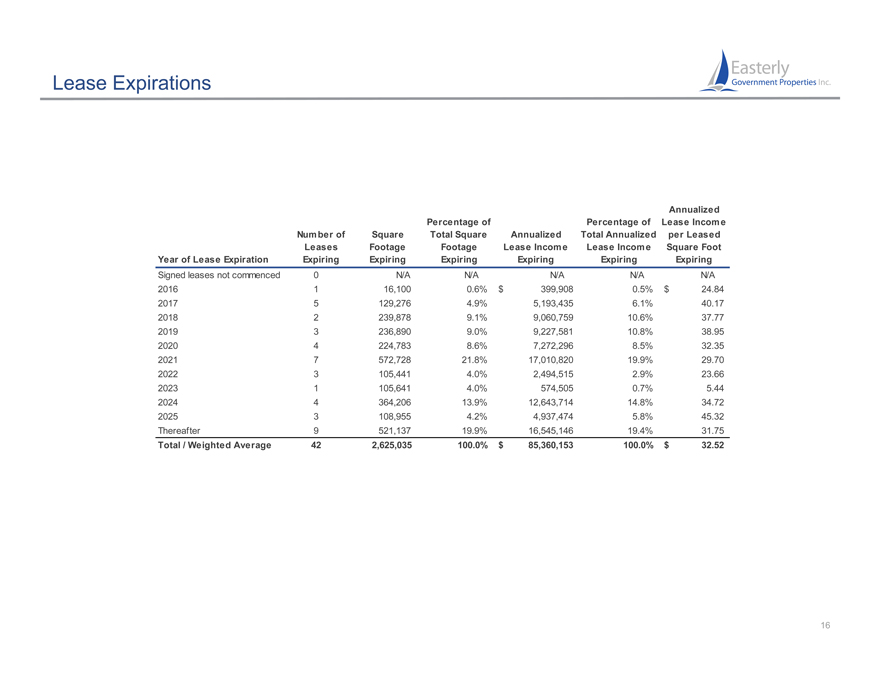

Lease Expirations

Annualized

Percentage of Percentage of Lease Income

Number of Square Total Square Annualized Total Annualized per Leased

Leases Footage Footage Lease Income Lease Income Square Foot

Year of Lease Expiration Expiring Expiring Expiring Expiring Expiring Expiring

Signed leases not commenced 0 N/A N/A N/A N/A N/A

2016 1 16,100 0.6% $ 399,908 0.5% $ 24.84

2017 5 129,276 4.9% 5,193,435 6.1% 40.17

2018 2 239,878 9.1% 9,060,759 10.6% 37.77

2019 3 236,890 9.0% 9,227,581 10.8% 38.95

2020 4 224,783 8.6% 7,272,296 8.5% 32.35

2021 7 572,728 21.8% 17,010,820 19.9% 29.70

2022 3 105,441 4.0% 2,494,515 2.9% 23.66

2023 1 105,641 4.0% 574,505 0.7% 5.44

2024 4 364,206 13.9% 12,643,714 14.8% 34.72

2025 3 108,955 4.2% 4,937,474 5.8% 45.32

Thereafter 9 521,137 19.9% 16,545,146 19.4% 31.75

Total / Weighted Average 42 2,625,035 100.0% $ 85,360,153 100.0% $ 32.52

| 16 |

|