Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CIVISTA BANCSHARES, INC. | d32298d8k.htm |

Shareholder Update

Second Quarter 2015

James O. Miller - Chairman, President & Chief Executive Officer Dennis G. Shaffer - Executive Vice President & President of Civista Bank Richard J. Dutton - Senior Vice President, Chief Operating Officer 1 Exhibit 99.1 |

Forward-Looking Statements

Comments made in this presentation include “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are subject to numerous assumptions, risks and uncertainties. Although management believes that the expectations reflected in the forward-looking statements are reasonable, actual results or future events could differ, possibly materially, from those anticipated in these forward-looking statements. For factors that could cause actual results to differ from our forward-looking statements, please refer to “Risk Factors” in the Company’s Form 10-K filed with the SEC on March 13, 2015. The forward-looking statements speak only as of the date of this presentation, and Civista Bancshares, Inc. assumes no duty to update any forward-looking statements to reflect events or circumstances after the date of this presentation, except to the extent required by law. 2 |

3 Participants in the Solicitation The directors and executive officers of Civista Bancshares, Inc. and other persons may be deemed to be participants in the solicitation of proxies in respect of the planned special meeting of shareholders to consider the governance matters referenced in this letter. Information regarding Civista Bancshares, Inc.’s directors and executive officers is available in its Annual Report on Form 10-K filed with the SEC on March 13, 2015 and its Proxy Statement on Schedule 14A filed with the SEC on March 13, 2015. Other information regarding the participants in the proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, will be contained in the proxy statement and other relevant materials to be filed with the SEC when they become available. Investors should read the proxy statement carefully when it becomes available before making any voting or investment decisions. You may read and copy the proxy statement after we file it at the SEC’s public reference room at 100 F. Street, N.E., Room 1580, Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the public reference room. Our SEC filings are also available for free to the public from the SEC’s web site at www.sec.gov or on our website at www.civb.com. Written requests for copies of the proxy statement we file with the SEC should be directed to Civista Bancshares, Inc., 100 East Water Street, Sandusky, Ohio 44870, Attention: James E. McGookey, telephone: (419) 625-4121. |

Contact Information

Civista Bancshares, Inc.’s common shares are traded on the NASDAQ Capital

Market under the symbol “CIVB.” The Company’s

depository shares, each representing

1/40 ownership interest in a Series B Preferred Share, are traded on the NASDAQ Capital Market under the symbol “CIVBP.” Additional information can be found at: www.civb.com James O. Miller Chairman, President & Chief Executive Officer jomiller@civb.com Telephone: 888.645.4121 4 th |

Corporate Overview

9 th Largest Publicly Traded Commercial Bank in Ohio Community Banking Focused Operations in 12 Ohio Counties – 27 Branches & 1 Loan Production Office Operations in Stable Ohio Markets Acquisitive Franchise Poised for Future Growth Corporate Overview Full-Service Banking Organization with Diversified Revenue Streams – Commercial Banking – Retail Banking – Wealth Management – Mortgage Banking Key Facts 5 Corporate Rebranding NASDAQ: CIVB ¹ Market data as of September 10, 2015. As of June 30, 2015, $s millions Assets $1,317.3 Gross Loans $1,002.9 Deposits $1,075.8 Market Cap. ¹ $78.8 |

6 Financial Highlights - Tangible book value excludes Goodwill and other intangible assets from the book value calculation

- ROATCE equals annualized net income, adjusted for amortization of intangibles, divided by average common equity minus average intangible assets Financial Highlights ($s in thousands, except per share data) June 30, 2015 June 30, 2014 % Change Balance Sheet Assets $1,317,272 $1,185,130 11.15% Gross Loans 1,002,917 867,978 15.55% Deposits 1,075,806 979,136 9.87% Performance Analysis Net Income Available to Common $5,497 $3,890 41.31% ROAA 0.93% 0.78% 19.40% ROAE 10.74% 8.84% 21.55% ROATCE 16.66% 13.83% 20.48% Market Data Market Capitalization $84,527 $69,538 Price / Tangible Book Value 124.0% 123.9% Dividend Yield 1.85% 2.22% |

7 Investment Highlights Experienced management team with strong track record Leading Ohio community bank franchise focused on rural and targeted urban markets

Demonstrated organic growth and proven acquirer

– Opened Loan Production Office on east side of Cleveland (Mayfield Heights) in Q1 2015

– Completed acquisition of TCNB Financial Corp. in Q1 2015 Successful unification into Civista brand in Q2 2015 Continued focus on credit quality Demonstrated earnings growth – Y-o-Y net income available to common shareholders growth of ~41%

– ROATCE of 16.66% through Q2 2015 Improving operating leverage – Closed four branches in 2014 – Continued focus on opportunities Capital – $50 million shelf offering went effective with SEC in August 2015 |

8 Experienced Management Team Chairman, President & CEO 41 years of banking experience Joined in 1986 James O. Miller SVP & Chief Operating Officer 29 years of banking experience Joined in 2007 Richard J. Dutton EVP, Chief Lending Officer & President of Civista Bank 30 years of banking

experience

Joined in 2009 Dennis G. Shaffer SVP & General Counsel 14 years of banking experience Joined in 2003 James E. McGookey SVP and Controller 27 years of banking experience Joined in 1988 Todd A. Michel SVP & Chief Risk Officer 20 years of banking experience Joined in 2013 John A. Betts SVP & Chief Credit Officer 31 years of banking experience Joined in 2011 Paul J. Stark |

9 Branch Footprint Note: Branch information as of June 30, 2015. Sandusky / Akron / Cleveland, Ohio $567 million in loans $614 million in deposits 11 branch locations #1 deposit market share in Sandusky, Ohio with ~ 43% market share North Central Ohio $93 million in loans $179 million in deposits 7 branch locations ~40% deposit market share $263 million in loans $199 million in deposits 7 branch locations 23% deposit market share in the rural markets West Central Ohio Greater Dayton, Ohio $80 million in loans $84 million in deposits 3 branch locations ~1.47% deposit market share |

10 Proven Acquirer & Attractive Organic Growth Acquired six banks from 1998 – 2015, serving to increase assets by over $800 million Expanded commercial loan growth in Columbus, Cleveland, Akron and Dayton markets

– Since year-end 2010, loan portfolios in these markets have increased from $117

million to $385

million through Q2 2015

Maintain a low cost, locally generated deposit base

Expanded residential mortgage lending with Q3 2013 hiring of experienced

lending team in the Columbus / Dublin, Ohio market

Positioned to capitalize on loan opportunities in greater Cleveland,

Akron, Columbus, Dayton

Total Assets $s in millions Total Gross Loans $s in millions Total Deposits $s in millions |

11 Successful Rebranding Brand Differentiation 316 “Citizens” Banks in the United States 16 “Citizens” Banks in Ohio Alone Citizens / Champaign Bank Branding Confusing for Existing Customers Avoid Customer Identity Confusion on the Internet Why Rebrand? NASDAQ: CIVB |

12 Peer Leading Net Interest Margin Source: SNL Financial. Comparable peers represents banks located in Ohio, Indiana, and Kentucky with total assets between $1.0 billion

and $5.0 billion; excludes merger targets. 3.94%

4.00% 3.98% 3.79% 3.79% 3.81% 3.88% 3.83% 3.71% 3.57% 3.59% 3.66% 2010Y 2011Y 2012Y 2013Y 2014 YTD 2015 CIVB Peer Median |

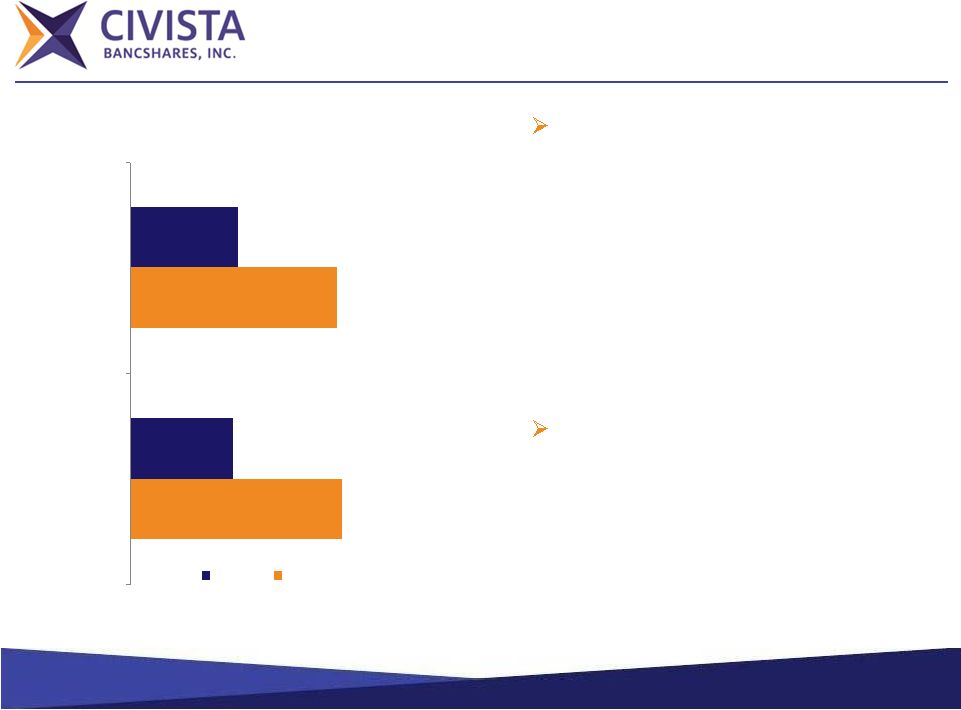

13 Effectively Managing Duration Asset duration of less than two years – Sell fixed rate mortgages – Encourage variable rate commercial lending or swap into variable, if appropriate – Limit fixed rate terms to five years Liability duration greater than three years – Focus on low-cost “sticky” demand deposits – Don’t overprice or overextend time deposits 3.38 3.31 1.64 1.72 Q2 2015 Q2 2014 Assets Liabilities |

14 Non-Interest Metrics & Initiatives ¹ From American Banker Magazine, September 2015 © 2015 SourceMedia, Inc. All rights reserved. Used by permission

and protected by the Copyright Laws of the United States.

The printing, copying, redistribution, or retransmission of this Content without expressed written permission is prohibited. Efficiency Ratio Non-Interest Income / Average Assets Growing fee income platform – Service charges on deposit accounts were $877 thousand and $722 thousand through Q2 2015 and 2014, respectively Wealth management – ~$419 million in Assets Under Management as of June 30, 2015 Income tax refund processing program – Evaluated/refined over five tax seasons – Specialized payment processing earned $2.0 and $2.3 million through Q2 2015 and 2014 Continuing focus on improving efficiency and operating leverage Investment in people ¹ Continuing evaluation of branch network and opportunities 0.85% 0.89% 0.98% 1.00% 1.11% 1.18% 2010 2011 2012 2013 2014 YTD 2015 65.94% 67.34% 70.57% 80.44% 71.77% 67.23% 2010 2011 2012 2013 2014 YTD 2015 |

15 Profitability & Returns Analysis ¹ LTM basis. Diluted Earnings per Share ROATCE ROAA Net Income Available to Common Shareholders |

16 Increasing Shareholder Value Source: SNL Financial. Market Data as of June 30, 2015. ¹ Comparable peers represents banks located in Ohio, Indiana, and Kentucky with total assets between $1.0 billion and $5.0 billion;

excludes merger targets. Stock Price

Dividend yield of 1.85%

Dividend payout ratio YTD 2015 is

approximately 12.3% Price / Tangible Book Value of

124% as compared to peer average of

153% ¹ Price / LTM EPS of 10.8x as

compared to peer average of 14.3x ¹ 61.15% Total Return in

2014 6.03% Total Return through June

30, 2015 |

17 Commitment to Shareholders Long-term Shareholder Value through Growth and Profitability |

18 Strategic Focus & Growth Strategy Organic growth – Capitalize on commercial and consumer lending opportunities – Grow core deposit base in rural and targeted urban markets – Identify and evaluate loan production opportunities in select metro markets

Acquisition opportunities

– Rural – Urban Asset quality Efficiency and operating leverage Capital |

19 The Civista Story Strong and Seasoned Management Team Leading Ohio Community Banking Franchise Proven and Disciplined Acquirer Platform to Support Future Growth Attractively Valued Versus Peers |

20 Special Shareholders’ Meeting Why a Special Shareholders’ Meeting? |

21 Special Shareholders’ Meeting We have had great recovery from the recession We are positioned to continue to grow the company Growth will add to the value of the company For continued growth we will need, at some point, additional capital – probably through the issuance of common shares While we have no current plans to issue additional common shares, before we consider the issuance of additional shares, we need to address cumulative voting and preemptive rights |

22 Special Shareholders’ Meeting Cumulative voting and preemptive rights are relics of the 19 th Century, when they were created. They were more appropriate for smaller privately held companies or companies with concentrated ownership (as we were in 1987). These are uncommon provisions for a company like us today. The Board of Directors and Management strongly believe that cumulative voting and preemptive rights should be eliminated in order to have a successful equity offering. |

23 Special Shareholders’ Meeting What is Cumulative Voting? If you own 1,000 shares of common stock and there are 8 director nominees on the ballot, you may cast 8,000 votes for one director, 4,000 for two directors, or 1,000 for each of the eight. |

24 Special Shareholders’ Meeting The Impact of Cumulative Voting If we were to issue 4,000,000 new common shares – existing shareholders purchase about 25%, or 1,000,000 shares, and the balance is sold to institutional investors. Would you want a block of 3,000,000 new shares to new owners enjoying cumulative voting? |

25 Special Shareholders’ Meeting What are Preemptive Rights? If we issue common stock, you have the right to purchase a proportional amount relative to your current ownership. This is done through a process called a rights offering. |

26 Special Shareholders’ Meeting The Challenge of Preemptive Rights Existing shareholders seldom purchase their proportional amount of shares. Therefore a company must have a backup purchaser – typically an institutional investor. For the backup institutional investor to make a commitment and wait (sometimes 60 days or more) for the completion of a rights offering – they will want a discount on the pricing. This affects you! |

27 Special Shareholders’ Meeting Preemptive Rights Proposal The Board and Management want existing shareholders to purchase as much of a common stock offering as they would desire. But – we would like to do this in one step instead of two. By issuing in one step, the argument for discounted shares is diminished. |

28 April 2015 Voting Results Shares Voting (non broker) 4,509,000 Shares Required for Passage 3,875,000 Votes to Remove Cumulative Voting 3,376,000 Percent of Total Votes 75% Votes to Remove Preemptive Rights 3,603,000 Percent of Shares Voting 80% |

29 Thank You |