Attached files

| file | filename |

|---|---|

| EX-23.2 - EXHIBIT 23.2 - Vaxart, Inc. | ex23-2.htm |

| EX-23.1 - EXHIBIT 23.1 - Vaxart, Inc. | ex23-1.htm |

| EX-32.2 - EXHIBIT 32.2 - Vaxart, Inc. | ex32-2.htm |

| EX-21.1 - EXHIBIT 21.1 - Vaxart, Inc. | ex21-1.htm |

| EX-23.1A - EXHIBIT 23.1A - Vaxart, Inc. | ex23-1a.htm |

| EX-31.1 - EXHIBIT 31.1 - Vaxart, Inc. | ex31-1.htm |

| EX-31.2 - EXHIBIT 31.2 - Vaxart, Inc. | ex31-2.htm |

| EX-32.1 - EXHIBIT 32.1 - Vaxart, Inc. | ex32-1.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES |

|

|

EXCHANGE ACT OF 1934 |

||

|

For the fiscal year ended June 30, 2015 |

||

|

OR |

||

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES |

|

|

EXCHANGE ACT OF 1934 |

For the transition period from ____________ to ____________

Commission file number: 001-35285

Biota Pharmaceuticals Inc.

(Exact name of Registrant as specified in its charter)

|

Delaware |

|

59-1212264 |

|

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification Number) |

|

2500 Northwinds Parkway, Suite 100, Alpharetta, GA |

30009 | |

|

(Address of Principal Executive Offices) |

(Zip Code) |

(678) 221 3343

(Registrant’s telephone number, including area code)

Securities registered pursuant to section 12(b) of the Act:

|

Title of each class |

Name of each exchange on which registered | |

|

Common Stock, par value $.10 per share |

The Nasdaq Stock Market LLC NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer”, ”accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ Accelerated filer ☑ Non-accelerated filer ☐ Smaller reporting company ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

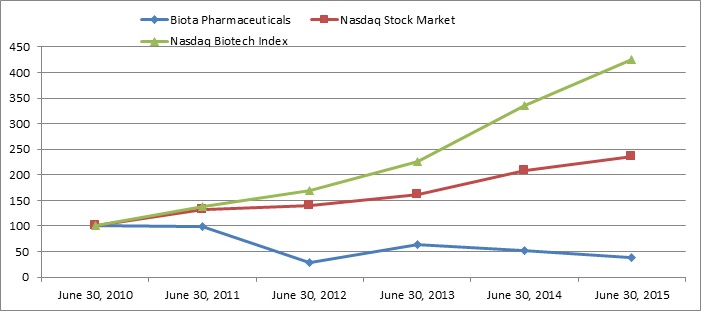

The aggregate market value of the common stock held by non-affiliates of the registrant, based on the closing price on December 31, 2014 was approximately $78.1 million.

Number of shares of Common Stock outstanding as of September 9, 2015: 38,609,086. The common stock is listed on the NASDAQ Global Select Market (trading symbol “BOTA”)

Documents incorporated by reference:

Portions of the definitive Proxy Statement with respect to the 2015 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission within 120 days after the close of the fiscal year are incorporated by reference into Part III of this report.

TABLE OF CONTENTS

|

Page | |||

|

Item1 |

Business |

4 | |

|

Item1A |

Risk Factors |

23 | |

|

Item 1B |

Unresolved Staff Comments |

40 | |

|

Item2 |

Properties |

40 | |

|

Item3 |

Legal Proceedings |

41 | |

|

Item4 |

Mine Safety Disclosures |

41 | |

|

Item5 |

Market for the Registrant’s Common Equity, Related Stockholders’ Matters, and Issuer Purchases of Equity Securities |

42 | |

|

Item6 |

Select Financial Data |

44 | |

|

Item7 |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

45 | |

|

Item7A |

Quantitative and Qualitative Disclosures about Market Risk |

54 | |

|

Item8 |

Financial Statements and Supplementary Data |

55 | |

|

Item9 |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

55 | |

|

Item9A |

Controls and Procedures |

56 | |

|

Item9B |

Other Information |

56 | |

|

Item10 |

Directors, Executives Officers and Corporate Governance |

57 | |

|

Item11 |

Executive Compensation |

57 | |

|

Item12 |

Security Ownership of Certain Beneficial Owners; and Management; and Related Stockholder Matters |

57 | |

|

Item13 |

Certain Relationships, Related Transactions, and Director Independence |

57 | |

|

Item14 |

Principal Accounting Fees and Services |

57 | |

|

Item15 |

Exhibits; Financial Statement Schedules |

58 | |

|

Signatures |

59 | ||

|

ITEM 1. |

BUSINESS |

PART I

SPECIAL NOTE ON FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the Securities Exchange Act of 1934, as amended. These forward-looking statements are principally contained in the sections entitled “Item 1-Business”, “Item 2-Properties” and “Item 7-Management’s Discussion and Analysis of Financial Condition and Results of Operations”, but may appear elsewhere. All statements other than those of historical facts contained herein are forward looking statements, which reflect our current expectations and assumptions about the future. Forward looking statements involve known and unknown risks and uncertainties that may cause actual future results, performance, achievements or events to be materially different from any results, performance, achievements or events expressed or implied by the forward-looking statements. In general, you can identify forward-looking statements by terms such as, but not limited to, “may,” “will,” “should,” “could,” “would,” “expect,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “project,” “predict,” “forecast,” “potential,” “continue,” “target,” “likely” or “possible,” as well as the negative of such expressions, and similar expressions intended to identify forward-looking statements. These forward-looking statements include, but are not limited to, statements relating to:

|

● |

our anticipated timing to fully enroll and report top line-data from our Phase2b SPIRITUS clinical trial; |

|

● |

our anticipated timing to complete the Phase 1 single ascending dose clinical trial for BTA585 and report top-line data; |

|

● |

our planned timing of the initiation of the Phase 1 multiple ascending dose clinical trial for BTA585 and report top-line data; |

|

● |

our planned timing of the initiation of the Phase 2a challenge study for BTA585; |

|

● |

our planned timing of the initiation of the Phase 2 clinical trial for BTA074 and reporting top line-data; |

|

● |

our preclinical respiratory syncytial virus (“RSV”) non-fusion inhibitor that may complement BTA585; |

|

● |

our plans to select a lead candidate from our RSV non-fusion inhibitor program; |

|

● |

our plans to out-license the rights to laninamivir octanoate (“LANI”) outside of Japan in concert with Daiichi Sankyo Company Ltd. (“Daiichi Sankyo”); |

|

● |

our anticipation that royalty revenue from the net sales of Relenza® may decrease in fiscal 2016 due to the expiration of the composition of matter patents for Relenza® in multiple countries and the outcome of the pending patent application in the U.S.; |

|

● |

our anticipation that we will generally incur net losses from operations in the future due to our intention to continue to support the preclinical and clinical development of our product candidates; |

|

● |

our future financing requirements, the factors that may influence the timing and amount of those requirements and our ability to fund them; |

|

● |

the number of months that our current cash, cash equivalents and anticipated future proceeds from existing royalty-bearing licenses and other existing license and collaboration agreements will allow us to operate; and |

|

● |

our plan to continue to finance our operations with our existing cash, cash equivalents and proceeds from existing or potential future royalty-bearing licenses, government contracts, or collaborative research and development arrangements, or through future equity and/or forms of asset or debt financings or other financing vehicles. |

These forward looking statements are subject to key risks and uncertainties including, without limitation: the U.S. Food and Drug Administration (“FDA”) or similar foreign regulatory agency, a data safety monitoring board, an institutional review board delaying, or we limiting, suspending or terminating the clinical development of any of our clinical development programs at any time for a lack of safety, tolerability, biologic activity, commercial viability, regulatory or manufacturing issues, or any other reason whatsoever; the safety or efficacy data from ongoing or future preclinical studies of any of our product candidates not supporting the clinical development of that product candidate; our capacity to successfully enroll, manage and conduct several simultaneous clinical trials on a worldwide timely basis; our ability to comply with applicable government regulations in various countries and regions in which we are conducting, or expect to conduct, clinical trials; our ability to manufacture and maintain sufficient quantities of preclinical and clinical trial material on hand to conduct and complete our preclinical studies or clinical trials on a timely basis; our ability, or that of our clinical research organizations or clinical investigators, to enroll a sufficient number of patients in our clinical trials on a timely basis; our ability to retain and recruit sufficient staff, including key executive management and employees, to manage our business; our ability to secure, manage and retain qualified third-party clinical research, preclinical research, data management, contract manufacturing and other similar vendors who we outsource many of our activities to and rely on to assist us in the design, development and implementation of the development of our product candidates; our third-party contract research, data management and manufacturing organizations fulfilling their contractual obligations on a timely basis or otherwise performing satisfactorily in the future; GlaxoSmithKline (“GSK”) or Daiichi Sankyo continuing to generate net sales from Relenza® and Inavir®, respectively, and otherwise continuing to fulfill their obligations under our royalty-bearing license agreements with them in the future; our ability to maintain, protect or defend our proprietary intellectual property rights from unauthorized use by others, or not infringe on the intellectual property rights of others; our ability to successfully manage our expenses, operating results and financial position in line with our plans and expectations; the condition of the financial equity and debt markets and our ability to raise sufficient funding in such markets; changes in general economic business or competitive conditions related to our industry or product candidates; and other statements contained elsewhere in this Annual Report on Form 10-K and the risk factors described in or referred to in greater detail in the “Risk Factors” section of this Form 10-K. There may be events in the future that we are unable to predict accurately, or over which we have no control. You should read this Form 10-K, as well as the documents that we reference herein and that have been filed or incorporated by reference as exhibits, completely and with the understanding that our actual future results may be materially different from our expectations. Our business, financial condition, results of operations, and prospects may change. We undertake no obligation to update these forward-looking statements, unless we are required by law. We qualify all of the information presented in this Form 10-K, and particularly our forward-looking statements, by these cautionary statements.

Biota is a registered trademark of Biota Pharmaceuticals, Inc., Relenza® is a registered trademark of GlaxoSmithKline plc, Inavir® is a registered trademark of Daiichi Sankyo Company, Ltd, and TwinCaps® is a registered trademark of Hovione FarmaCiencia SA.

References to “we,” “us,” and “our” refer to Biota Pharmaceuticals, Inc. and its subsidiaries.

Our Business

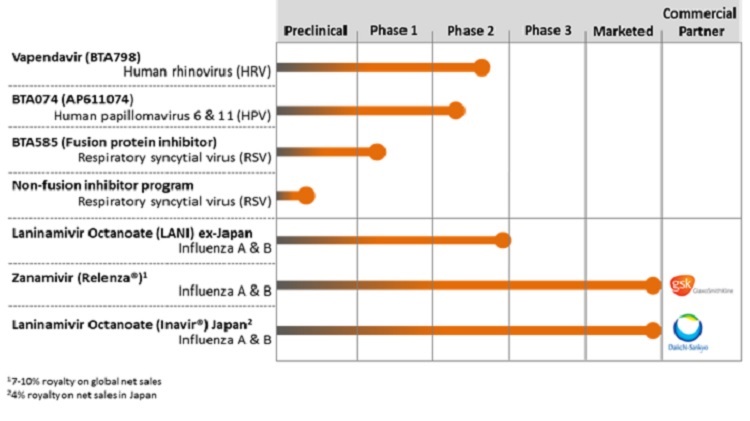

We are focused on the discovery and development of direct-acting antivirals to treat infections that affect a significant number of patients globally. We have four product candidates in clinical development that address viral infections that have limited therapeutic options. vapendavir, an oral treatment for human rhinovirus (“HRV”) infections in moderate-to-severe asthmatics, currently being evaluated in our ongoing Phase 2b SPIRITUS trial; BTA074, a Phase 2 topical antiviral treatment for genital warts caused by human papillomavirus (“HPV”) types 6 & 11; BTA585, an oral fusion (“F”) protein inhibitor in Phase 1 development for the treatment of RSV-A and RSV-B infections; and laninamivir octanoate, a one-time, inhaled treatment in Phase 2 development for influenza A and B infections. We also have preclinical RSV non-fusion inhibitor program that we believe complements our F-protein inhibitor BTA585.

Background

We have historically focused our research and drug development capabilities on discovering and developing small molecule compounds that can prevent or treat infectious diseases. Infectious diseases are caused by pathogens that are present in the environment, such as viruses and bacteria, which enter the body through various means and overwhelm its natural defenses and cause an infection. The severity of an infectious disease varies depending on the nature of the infectious pathogen, as well as the degree to which the body’s immune system or available therapies can prevent or fight the infection. The market for anti-infective drugs generally can be divided into three general categories: antiviral, antibacterial and antifungal. We are currently focused on developing antiviral compounds.

The use of antiviral drugs has led to a significant reduction in the morbidity and mortality associated with infectious diseases. However, for many infectious diseases, current treatment options, to the extent any such treatment options are currently available, are associated with suboptimal treatment outcomes, significant toxicities, tolerability issues or adverse side effects, the emergence of drug resistant pathogens, complex dosing schedules, and inconvenient methods of administration. These sub-optimal characteristics of many existing treatment options often lead to patients prematurely discontinuing treatment or not fully complying with treatment dosing schedules, resulting in a treatment failure. A patient’s failure to comply fully with a recommended dosing schedule can also both accelerate and exacerbate the emergence of drug-resistant strains. In recent years, the increasing prevalence of drug-resistant pathogens has created ongoing treatment challenges with respect to many infectious diseases. The ability of viruses to adapt rapidly to existing or new treatments through genetic mutations allows new strains to develop that may be resistant to currently available drugs. In recent years, the increasing prevalence of drug-resistant pathogens has created ongoing treatment challenges with respect to many infectious diseases.

Our Pipeline

The following chart summarizes key information regarding our antiviral product candidates:

|

|

Human Rhinovirus (“HRV”), Asthma and Chronic Obstructive Pulmonary Disease (“COPD”) |

HRV is a non-enveloped, single-stranded viruses that belong to the Picornaviridiae family. Currently more than 100 distinct serotypes of HRV are classified into three species, HRV-A, HRV-B, and HRV-C. Primary market research conducted by the IMS Consulting Group on our behalf with pulmonologists, internists and general practitioners indicated that adult asthma and chronic obstructive pulmonary disease (“COPD”) patients experience four to six colds per year. Asthma is a common disease with underlying inflammation of the airways that affects an estimated 300 million people worldwide and 26 million people in the United States. A 2015 study commissioned by us with the IMS Consulting Group indicated that there were 10.5 million people in the U.S. categorized as having moderate to severe asthma based on its research of primary and secondary market sources dating between 2008 and 2015.1 Acute asthma exacerbations are a major healthcare burden, accounting for almost half of the total healthcare costs associated with asthma, and also have a major impact on the quality of life and in some cases can cause death. Recent studies in adults with asthma have documented an association between respiratory tract infection and worsening asthma symptoms, decline in lung function (disease progression), and exacerbations. Respiratory viruses, and in particular HRV, are a significant cause of exacerbations. In a 2014 study of asthma patients with cold-like symptoms, 63% of the patients had respiratory viruses that were detected by qPCR (quantitative PCR) and the majority of those samples (68%) contained HRV.

Exacerbations are important sequelae of HRV infection in asthma patients and their prevention has historically been the focus of asthma drug development. Poor asthma control and use of asthma reliever bronchodilator medications have been linked with an increased risk of death and asthma exacerbations can be fatal. In recent years asthma treatment guidelines have also focused on asthma control as an important goal. Asthma control is defined by a global assessment of symptoms, use of rescue medications, lung function, and patient-reported functioning and activity limitations. The Asthma Control Questionnaire (“ACQ-6”) is a patient reported outcome (“PRO”) tool often used to measure a drug’s therapeutic impact on the worsening of asthma symptoms. In general, a well-controlled asthma patient has an ACQ score of ≤ 0.75 – 1.0 and a patient with uncontrolled asthma has an ACQ score of ≥ 1.50. An improvement in ACQ score of ≥ 0.5 is generally considered indicative of a clinically meaningful change. Although there are several FDA approved drugs for the treatment of asthma, none are directed at respiratory viruses, including HRV.

COPD is the most common chronic respiratory condition in adults whose prevalence is expected to continue to increase in the future. Currently, the World Health Organization (“WHO”) estimates that 64 million people have moderate to severe COPD worldwide. In the U.S. there are an estimated 28 million individuals over the age of 40 with COPD, with an annual average growth rate of 1.9%. Further, of the estimated 28 million COPD patients in the U.S., approximately 13 million are classified as having moderate to severe/very severe COPD.

Similar to asthma, HRV is the most common virus detected during exacerbations of COPD. In COPD patients, colds often precede exacerbation symptoms. In a published experimental challenge study, COPD patients with an HRV infection showed more severe and prolonged lower respiratory symptoms, airway obstruction, and neutrophilic airway inflammation than subjects without COPD. In addition, a recent natural exposure study in COPD patients demonstrated that HRV prevalence and viral load at exacerbation presentation were significantly higher compared to a period when the patient was not experiencing an exacerbation. Further, the HRV viral load was elevated in COPD patients that presented to the clinic, consistent with the experimental challenge study, suggesting that viral replication may be ongoing, and antiviral therapy may be an effective treatment modality to prevent or reduce the severity of exacerbations.

There are currently no direct antiviral drugs approved for the treatment of HRV. As such, there remains a significant unmet medical need to identify treatments that can reduce the impact that HRV infection has on the frequency of exacerbations and loss of control, prevent viral transmission, lessen the severity and duration of cold-like HRV symptoms and minimize secondary bacterial infections in asthma and COPD patients.

|

|

Vapendavir (BTA798) |

We are developing vapendavir (BTA798), a potent antiviral capsid binder that is designed to bind to a highly conserved pocket in the HRV capsid and interfere with receptor binding and/or related early steps in the infectious cycle. Vapendavir is a potent inhibitor of picornaviruses and has been shown to inhibit the replication of a wide range of HRV serotypes and the replication of a majority of recent HRV clinical isolates in tissue culture assays. The median EC50 value for vapendavir against the 100 HRV serotypes is 5.8 ng/mL (15.2 nM). Vapendavir has also demonstrated antiviral activity against other clinically relevant enteroviruses (“EV”) including EV- 71 and poliovirus types 1, 2 and 3.

Vapendavir (BTA798) Clinical Trials

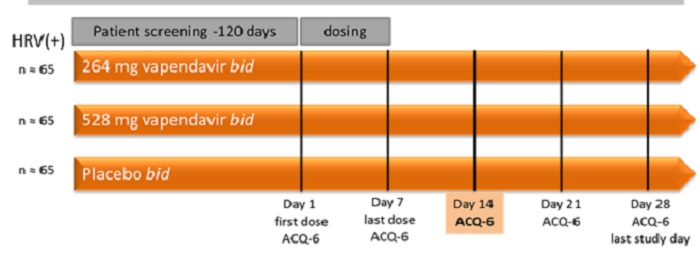

Phase 2b SPIRITUS Trial. The ongoing Phase 2b SPIRITUS clinical trial of vapendavir is being conducted at approximately 65 sites in North America and Central Europe with a goal of enrolling approximately 190 laboratory-confirmed HRV-infected patients for the intent to treat-infected (“ITT-I”) population. Patients aged 18-70 years of age that have an established history of moderate-to-severe asthma and a history of losing asthma control as a result of an upper respiratory tract infection will be eligible to be enrolled in the trial.

The following diagram summarizes the design of the multi-center, 1:1:1 randomized, double-blind, placebo-controlled dose-ranging SPIRITUS Trial:

The primary endpoint of SPIRITUS is the least square mean change from baseline (day 1) to study day 14 in ACQ-6 total score.

The secondary endpoints of this study are focused on safety and tolerability, lung function assessments such as forced expiratory volume in one second (“FEV1”), incidence of asthma exacerbations, assessments of the severity and duration of cold symptoms as measured by the Wisconsin Upper Respiratory Symptom Survey-21 (“WURSS-21”), and virology assessments such as changes in viral load. The primary efficacy analysis population will be the ITT-I population defined as all subjects with confirmed HRV infection (by either the eSensor® Respiratory Viral Panel (GenMark) or RT-PCR on any of Study Days 1, 3, 5, or 7).

Phase 1 Bioavailability Trial. In 2014, we completed enrollment in a Phase 1 study entitled ‘A Randomized, Single-Center, Open-Label, Two-Period, Two-Sequence, Crossover, Comparative Study to Compare the Oral Bioavailability of Single Doses of Two Vapendavir Drug Product Formulations in Healthy Volunteers’ designed to establish the systemic exposure profile of a single dose of a vapendavir free-base tablet formulation compared to the exposure profile following a single dose of two vapendavir phosphate salt capsules, which was the formulation used in prior clinical trials. Thirty-six subjects received a single dose of the capsule formulation or the tablet formulation in Period 1 and, after a washout, crossed over to receive a single dose of the other formulation in Period 2 of the study, according to their sequence treatment assignment. No serious adverse events occurred during the study. The pharmacokinetics (“PK”) results demonstrated that the free-base tablet formulation achieved approximately 60% of the mean bioavailability as the phosphate salt capsule formulation. The half-life and time to peak concentration (“Tmax”) were comparable between the two formulations. Based on these PK findings additional formulation activities with the free-base tablet were initiated to improve its bioavailability and the phosphate salt form of vapendavir was selected for use in the Phase 2b SPIRITUS trial.

Phase 1 Drug-Drug Interaction Trial. In 2014, we also completed a drug-drug interaction study entitled ‘A Phase 1, Randomized, Open-Label Study to Evaluate the Effect of Vapendavir (BTA798) on the Pharmacokinetics of Orally Administered Midazolam, a CYP3A4 Substrate, in Healthy Male and Female Volunteers’. This study was designed to assess the effect of vapendavir on the PK profile of midazolam, a CYP3A4 substrate. Additionally, the effect of midazolam on the PK profile of vapendavir, the PK profile differences of vapendavir in males and females, and the safety profile of vapendavir were assessed. Twelve (12) male and 12 female subjects aged 18 to 55 years were randomized to receive one of two oral doses of vapendavir and midazolam. Of the 24 subjects randomized, 22 completed all study visits. No serious adverse events (“SAEs”) occurred during the study. The results of the study confirmed vapendavir’s pharmacokinetic profile as established in prior clinical trials and established that vapendavir is a weak to moderate inducer of CYP3A4, which suggests that vapendavir may be used to treat asthma and COPD patients receiving multiple background medications.

Phase 2. In 2012, we completed a 300-patient, multicenter, randomized, double-blind, placebo-controlled study of vapendavir in adults with mild to moderate asthma that had a symptomatic HRV infection. The primary objective of the study was to determine the efficacy of vapendavir on symptoms of presumptive HRV infection in asthmatic adults, as measured by the WURSS-21 severity scores. Vapendavir was dosed twice daily for six days., The study was conducted over two HRV seasons (18 months), with an estimated 1200 individuals screened in order to randomize 300 subjects, 155 in the vapendavir arm and 145 in the placebo group. The trial successfully met its primary endpoint, which was a reduction of cold symptoms based on the WURSS-21 severity score averaged over days two through day four. The mean daily reduction in WURSS-21 severity score averaged over days two to four was significantly greater in the vapendavir treated group compared to the placebo group (least square mean difference: -4.01, p = 0.020). Vapendavir was generally tolerated and most treatment-related adverse events were of mild intensity, with moderate treatment-related events reported in 2.3% of subjects. No SAE’s occurred during the study.

Phase 2 HRV39 Challenge Study. In 2009, we completed a Phase 2a placebo-controlled, double-blind, randomized, parallel group trial to determine the potential of 25 mg, 100 mg and 400 mg of vapendavir, when dosed twice daily for 10 days, to prevent experimental HRV39 infection (challenge design) in 41 healthy volunteers. Subjects that received 400 mg of vapendavir achieved a statistically significant reduction compared to placebo in mean viral load on days two to five inclusive. Vapendavir was generally well tolerated, and the overall incidence of adverse events was low, not dose dependent, and was similar to placebo. There was one SAE of neutropenic sepsis in a subject in the 100 mg arm of the trial.

Phase 1 Single Ascending and Multiple Ascending Trials. In 2006, we completed Phase 1, placebo-controlled, single and multiple ascending oral dose, safety, tolerability and pharmacokinetic studies in 56 healthy volunteers. Single oral doses of 25 mg, 50 mg, 100 mg, 200 mg, 400 mg, 800 mg or 1600 mg of vapendavir were evaluated. Vapendavir was generally well tolerated and there were no dose limiting toxicities or trends in adverse events or laboratory parameters observed, with the incidence and nature of adverse events similar between placebo recipients and all dosing groups of vapendavir. In a subsequent multiple ascending dose trial evaluating 200 and 400 mg of vapendavir, administered either once a day (“QD”) or twice a day (“BID”) for seven or eight consecutive days, vapendavir was well tolerated. There were no SAE’s and there were no dose limiting toxicities or clinically relevant changes in vital signs, ECG or laboratory parameters observed.

Human Papillomavirus (“HPV”)

HPVs are small non-enveloped, double stranded DNA viruses that infect mucosal or cutaneous squamous epithelia, where they may cause benign or malignant hyperproliferation of the skin and mucosa. HPV is the most common cause of sexually transmitted infections and the disease burden includes skin warts, genital warts, cervical and other anogenital dysplasias and carcinomas, oropharyngeal cancer and recurrent respiratory papillomatosis (“RRP”). HPV is the most common sexually transmitted infection. Over 40 distinct types can infect the genital tract. Approximately 90% of infections caused by HPV’s are asymptomatic and resolve spontaneously within two years. However, persistent infection with some HPV types can cause cancer and other benign diseases. Of the 13 HPV types designated as human carcinogens, types 16 and 18 account for 70% of cervical cancers worldwide. Among non-carcinogenic types, types, HPV 6 and 11 are responsible for 90% of anogenital warts.

Genital warts also referred to as anogenital warts or condyloma is the most commonly identified pathology caused by genital HPVs. Genital warts are sexually transmitted, with a high rate of transmission and significant psychosocial morbidity. Genital warts are one of the most common viral sexually transmitted disease (“STD”) worldwide. It is one of the most frequent STDs diagnosed among genitourinary medicine (“GUM”) clinics and accounts for more frequent visits to general practitioners or GUM clinics than those for genital herpes. In 2013, the Centers for Disease Control and Prevention estimated that in the U.S. there were >400,000 visits to physicians’ offices related to genital warts.

HPV types 6 and 11 are also associated with RRP, a condition of tumors or wart-like lesions of the upper respiratory tract, particularly the larynx. In the U.S., the incidence of RRP is two per 100,000 adults and four per 100,000 children. Juvenile-onset RRP (“JORRP”) is usually diagnosed between the ages of one and four years, is equally prevalent in both sexes, and is believed to be acquired by newborns from their mothers during labor. Adult-onset RRP (“AORRP”) has a broad peak of occurrence between ages 20 and 40 years, and is most frequent in males. Afflicted infants and children with JORRP present with difficulty breathing or swallowing and therefore the lesions can become life-threatening, while adults usually present with hoarseness, chronic coughing or breathing problems. A small percentage of afflicted patients go on to have systemic disseminated disease which can invade the lungs and become potentially lethal. Typically, RRP lesions have to be removed surgically. On average, in the U. S., children undergo 19.7 surgical procedures over their lifetime, with a mean frequency of 4.4 procedures per year. In 20 percent of JORRP and AORRP patients the disease will be more aggressive and can require more than 40 surgical procedures during a lifetime. It is estimated that 15,000 surgical procedures due to RRP are performed per year in the U. S., at a total cost of $150 million, and lifetime costs per individual patient can reach up to $470,000.

Currently, no approved HPV-specific direct acting anti-viral drugs exist to treat genital warts or RRP. Existing treatments for genital warts can be divided broadly into two categories: provider-administered ablative/cytodestructive therapies (including cryotherapy, laser ablation, and trichloroacetic acid) and patient-administered topical therapies, such as podophyllotoxin, sinecatechins, and imiquimod. Imiquimod directly activates innate immune cells through Toll-like receptor 7, resulting in production of cytokines. Treatment choice depends on the morphology, number, and distribution of warts and patient preference. Significant failure and relapse rates, often as much as 20-30% or more have been reported for all of these existing treatments. Further, all existing therapies are associated with local skin reactions including itching, burning, erosions and pain. There are no cures for RRP, however current maintenance treatments include CO2 laser surgery, pulse dye laser surgery, endoscopic microdebriders, and intralesional injection with cidofovir. The high reoccurrence rates make the current therapies less than optimal for patients suffering with RRP. Therefore, despite the existence of marketed prophylactic vaccines, effective therapies against pathologies caused by HPV6 and HPV11 are still needed.

|

BTA074 (AP611074) |

BTA074 is in development for the treatment of genital warts, as well as the orphan indication of RRP. BTA074 is a potent and selective inhibitor of the interaction between two viral proteins from HPV6 and HPV11, E1 and E2, an interaction that is an essential step for HPV DNA replication and thus, viral production and pathogenesis. This inhibition results from the binding of BTA074 to the E2 protein (Kd=168 nM). BTA074 is a first-in-class directing acting antiviral specific to HPV and possesses new mechanism of action that can be exploited to treat infections caused by HPV types 6 & 11. BTA074 was selected for clinical development among more than 1200 unique compounds tested. BTA074 was developed by combining chemo-informatics modeling and in cellulo screening of E1/E2 protein-protein interactions. These studies showed that BTA074 inhibits the HPV6 and HPV11 E1/E2 interaction or HPV DNA replication in cellulo with an IC50 of 0.5-1 “M. Moreover, BTA074 is highly selective for low-risk types HPV 6 and HPV 11, since it does not inhibit replication of HPV 18 or E1/E2 protein interactions of other HPVs.

BTA074 (AP611074) Clinical Trials

Phase 2. We plan to initiate a Phase 2 trial in late 2015 to further validate BTA074 favorable local skin tolerability profile and antiviral activity. The trial is designed as a double-blind placebo controlled, randomized, Phase 2 study the primarily objective of which is to assess the safety, tolerability, pharmacokinetics and efficacy of twice daily topical treatments of BTA074 5% gel for up to 16 weeks in approximately 210 genital warts patients. The primary objective of the trial is to evaluate the safety and tolerability in genital warts patients with special focus on local skin reactions. A primary efficacy endpoint is to determine the complete clearance rate for baseline genital warts lesions after twice daily application of BTA074 5% gel or placebo from baseline week 0 visit to the completion of the treatment.

Phase 2a. In 2013, a Phase 2a clinical trial of BTA074 5% gel was completed. The six-week, Phase 2a study in 24 subjects (sixteen active; eight placebo) demonstrated that twice daily application of 100 mg BTA074 5% gel had an excellent local skin tolerability profile and resulted in high patient compliance and no patient drop-outs or treatment interruptions. Further, treatment with BTA074 produced a 56% overall response rate and a -38% change in mean baseline wart area.

Phase 1b. In 2013, a Phase 1b multicenter, double-blind, randomized, placebo-controlled study in eight genital warts subjects (six active; two placebo) was completed. 100 mg BTA074 5% gel was applied topically twice daily for seven days to the infected area. No adverse events were reported during this study and no clinically relevant findings were observed in clinical examination, laboratory parameters, vital signs or electrocardiogram (“ECG”) parameters.

Phase 1. In 2011, a Phase 1 single center, double-blind, randomized, placebo-controlled study in eight healthy male volunteers (six active; two placebo) was completed. The study drug dose was 250 mg BTA074 5% gel applied on 25 cm² skin, corresponding to 12.5 mg BTA074/application. BTA074 5% gel was applied twice daily for seven days. Repeated topical applications of BTA074 on the back of healthy volunteers were well tolerated. One subject receiving BTA074 5% gel and one subject receiving placebo experienced mild isolated erythema on pre-dose day five.

|

|

Respiratory Syncytial Virus (“RSV”) |

RSV, a member of the Paramyxoviridae family of viruses, is a major cause of acute upper and lower respiratory tract infections in infants, young children, and adults. Datamonitor estimates that approximately 18 million people are infected annually with RSV in the seven major markets worldwide, including over nine million children under the age of four, five and half million elderly, and three million adults with underlying disease. About 900,000 of these individuals are hospitalized for their RSV infection. These infections are particularly problematic in infants, as approximately 91,000 are hospitalized with RSV infection in the U.S. in any given year. RSV infections are also responsible for 40 to 50% of hospitalizations for pediatric bronchiolitis and 25% of hospitalizations for pediatric pneumonia. In addition to pediatric patients, elderly patients with cardiac or pulmonary conditions and adults that have received a bone marrow transplant are at an increased risk for severe RSV infection. The overall magnitude of hospitalizations makes RSV a costly disease, although mortality is low.

To date, only three drugs have been approved to either prevent or treat RSV infections. Ribavirin is used to treat serious RSV infections in infants with severe bronchiolitis and in immunocompromised patients. However, its use is restricted due to highly variable efficacy and toxicity risks. In fact, current American Academy of Pediatrics guidelines for the treatment of bronchiolitis in children do not recommend the routine use of ribavirin to treat RSV infection due to lack of clinical evidence supporting its use. Antibody-based products RespiGam® (no longer available) and Synagis® (palivizumab) were designed, developed and approved to prevent, not treat, RSV infections in high risk premature infants. Due to the high cost of treatment with Synagis®, its use is limited in many hospitals. There remains a significant unmet need for a safe and effective treatment for RSV in all at-risk populations.

|

|

BTA585 |

Our lead compound, BTA585, is a potent, non-cytotoxic and selective inhibitor of the RSV F protein. Data from studies investigating the mechanism of BTA585 anti-viral activity, including analysis of RSV resistance mutants, support the conclusion that BTA585 inhibits the function of the RSV protein. Therefore, BTA585 exerts its antiviral activity by interfering with the earliest stage of infection by inhibiting the attachment and/or fusion of the virus to the host cell. BTA585 is equally active against both RSV A and B subtypes but has no known activity against other pathogenic viruses. When tested against a panel of RSV clinical isolates, BTA585 was found to be highly potent with an average EC50 =95.6nM.

In September 2015, we presented at the 54th Interscience Conference on Antimicrobial Agents and Chemotherapy Meeting in Washington, D.C. from a number of in vivo studies designed to assess the antiviral activity of BTA585 prior to and during experimental RSV infection in a cotton rat model. These studies demonstrated a dose-dependent decrease in virus titers in lung tissue. Similarly, a highly significant dose-dependent decrease in RSV mRNA in lung tissue was also observed in the cotton rat model.

BTA585 Clinical Trials

Phase 1 Single Ascending Dose (“SAD”) Clinical Trial

In August 2015, we commenced dosing in a 50-subject, randomized, placebo-controlled, Phase 1 single ascending dose (“SAD”) clinical trial to evaluate the safety and PK of BTA585 in healthy volunteers. The Phase 1 SAD trial has five dose level cohorts ranging from 50 mg to 500 mg and includes an evaluation of the effect of food on the PK of BTA585.

Non-Fusion RSV Inhibitors

In addition to BTA585, we have identified a series of potent RSV non-fusion inhibitors that we intend to further develop and believe could be useful as a stand-alone treatment or potentially in combination therapy with BTA585 for the treatment of patients infected with RSV. Our goal is to select a lead candidate from this program by mid-year 2016.

|

|

Influenza |

Influenza, or the flu, is an acute viral infection caused by an influenza virus. There are three types of influenza – A, B and C. Influenza A viruses are further typed into subtypes according to the different kinds and combinations of virus surface proteins. Among the many subtypes of influenza A viruses, currently influenza A(H1N1)pmd09 and influenza A(H3N2) are the most common subtypes circulating among humans. Type C influenza cases occur much less frequently than types A and B.

Influenza is characterized by a sudden onset of high fever, headache, muscle and joint pain, severe malaise (feeling unwell), cough (usually dry), sore throat and a runny nose. Most people generally recover from fever and most of the other symptoms within a week without requiring medical attention. However, influenza can cause severe illness, hospitalization or death in people at high risk, which include the very young, the elderly and the chronically ill. The time from infection to illness, known as the incubation period, is generally about two days. Influenza epidemics generally occur annually during the autumn and winter in temperate regions. According to the WHO, annual epidemics result in about three to five million cases of severe illness and about 250,000 to 500,000 deaths worldwide. Most deaths associated with influenza in industrialized countries occur among people ages 65 or older.

Controlling influenza virus infections continues to be a major public health challenge. Despite increasingly widespread vaccination, influenza remains a significant burden that can give rise to a potential crisis, even in communities with advanced health care. Data from the CDC suggest that each year 5-20% of the U.S. population (16-63 million according to 2012 U.S. population estimates) suffer from influenza, and approximately 200,000 people in the U.S. are hospitalized each year for respiratory and heart conditions associated with influenza infections. In pandemic influenza outbreaks, vaccines can only be developed following identification of the pandemic strain, which results in vaccines not being available immediately. These limitations of vaccination emphasize the importance of and need for antiviral drugs to treat and prevent influenza.

The market opportunity for antivirals to prevent or treat influenza, and their utilization in the seasonal influenza market, is often difficult to project given the year-to-year variability in the circulating strain of influenza, the severity of influenza illness, and the length of the influenza season. Further, if there is a year in which a pandemic occurs, the variability in the market potential is magnified. In addition to this seasonal influenza market, government stockpiling of antivirals to prevent or treat influenza have historically contributed significantly to the overall market opportunity.

|

|

Laninamivir Octanoate (“LANI”) |

In 2003, we cross-licensed intellectual property related to a new class of inhaled long acting neuraminidase inhibitors (“NI’s”) with Daiichi Sankyo. The lead product from this collaboration is LANI, also known as CS-8958, a second-generation octanoyl ester pro-drug of laninamivir. LANI has been shown to have in vitro neuraminidase-inhibitory activity against various influenza A and B viruses, including subtypes N1 to N9 and oseltamivir-resistant viruses, and it has also been found to be effective against a swine origin H1N1 strain. Moreover, LANI has long-lasting antiviral activity. Preclinical studies in mice have demonstrated that after intranasal administration, it was rapidly converted to its active metabolite, laninamivir, which was retained in the lungs where it had a long half-life of approximately 40 hours. Further, a single intranasal dose of LANI exhibited efficacy similar to that of repeated doses of zanamivir or oseltamivir phosphate.

LANI was successfully developed by Daiichi Sankyo in Japan and since 2010 has been marketed there as Inavir® for the treatment of influenza A and B infections. In December 2013, Inavir® was approved for use in the post-exposure prevention of influenza. Since 2009, we have been developing LANI under an IND in the U.S. for the treatment of influenza A and B.

|

|

LANI Clinical Trials |

Phase 2. In June 2013, we commenced enrollment in a multi-national, randomized, double blind, placebo controlled, parallel arm Phase 2 clinical trial that compared the safety and efficacy of 40 mg and 80 mg of LANI with placebo, all delivered by a TwinCaps® inhaler in adults with symptomatic influenza A or B infection. The trial, which we refer to as “IGLOO”, was designed to enroll 636 subjects, randomized equally across the three treatment arms. The primary endpoint of the IGLOO trial was the reduction in the median time to alleviation (reported to be mild or absent for greater than 24 hours) of seven influenza symptoms (headache, feeling feverish, body aches and pains, fatigue, cough, sore throat and nasal congestion) plus fever (<38oC), compared to placebo. Symptom data were collected through the Flu-iiQTM patient-recorded outcomes (“PRO”) questionnaire. Secondary end points included quantitative changes in virus shedding, evaluating whether the use of LANI reduces the incidence of secondary bacterial infections compared to placebo, the development of resistance by phenotypic and genotypic analyses, and the impact of treatment with LANI on the quality of life.

On August 1, 2014, we announced top-line data from the IGLOO trial. We enrolled a total of 639 patients across 12 countries in the northern and southern hemispheres from June 2013 to April 2014. Of the 639 patients enrolled, 248, or 39%, had PCR confirmed influenza A or B virus and were included in the intent-to-treat efficacy analyses. Approximately 75% and 19% of the influenza-confirmed patients were infected with influenza A H1N1 2009 and H3N2, respectively, while 6% were infected with influenza B. As compared to placebo, neither the 40 mg nor the 80 mg cohort achieved a statistically significant reduction in the median time to alleviation of the seven influenza symptoms, which was the primary efficacy endpoint. The median time to alleviation of the seven influenza symptoms was 102.3 hours for the 40 mg cohort and 103.2 hours for the 80 mg cohort, as compared to 104.1 hours for the placebo cohort.

Although neither the 40 mg nor the 80 mg LANI cohorts achieved a statistically significant difference compared to placebo for the entire seven symptom primary endpoint, notable effects were seen in individual symptoms, the subset of systemic symptoms (headache, feeling feverish, body aches and pains and fatigue) and a number of key secondary endpoints. Subjects in the 40 mg cohort reported alleviation of the subset of systemic symptoms significantly earlier as compared to placebo (median time 59 hours and 79 hours, respectively, p=0.029). Patients in the 40 mg cohort also reported a significant reduction in the number of days in which all seven symptoms were severe (p=0.02) and in secondary bacterial infections as compared to placebo (0% compared to 7.8% of placebo recipients; p=0.013). Patients in the 40 mg (p<0.001) cohort demonstrated a statistically significant reduction in viral shedding on day 3 of the study compared to placebo as quantified by qRT-PCR. In addition, a statistically significant proportion of patients in both the 40 mg (p=0.002) and 80 mg (p=0.02) cohorts were culture negative on day 3 of the study as compared to placebo. The nature and extent of adverse events were similar in the three cohorts, with diarrhea (3.1% vs. 0.9%), headache (1.4% vs. 0.5%), gastritis (1.4% vs. 0%), urinary tract infection (1.4% vs. 0%), and sinusitis (1.2% vs. 0.9%) being the most common adverse events that occurred more frequently in the treatment cohorts as compared to placebo. The incidence of serious adverse events was low and balanced across the three cohorts.

We and Daiichi Sankyo intend to collectively pursue a license agreement, or other similar transaction, with regional or global third-party pharmaceutical or biopharmaceutical companies that have greater clinical development, manufacturing and commercialization capabilities than we do that we believe could advance the development and/or commercialization of LANI regionally or globally.

Phase 1 Clinical Trials. In 2014, we completed two Phase 1 clinical trials of LANI; one to evaluate its safety and pharmacokinetics in patients with chronic asthma and the other being a QT/QTc study to evaluate the effect of therapeutic (40 mg) and supra-therapeutic (240 mg) doses of laninamivir octanoate on the QT-interval.

The safety profile of 40 mg and 80 mg doses of LANI by inhalation via the TwinCaps® DPI in adults with mild or moderate chronic asthma demonstrated that inhaled LANI was well tolerated. Treatment with inhaled LANI at therapeutic antiviral doses did not result in significant changes in lung function as measured by spirometry. These results suggest that inhaled LANI can be safely administered to asthma patients. Top-line results of the QT/QTc study indicate LANI was not associated with any clinically significant ECG changes, no serious adverse events (“SAEs”) occurred, no subjects terminated the study or the study treatment due to an adverse event and a low proportion of subjects experienced adverse events during the study treatments. Between these two recent Phase 1safety studies, a total of 211 subjects participated and, of these, 118 received inhaled LANI at doses ranging from 40 mg to 240 mg.

Prior to initiating the Phase 2 IGLOO trial in June 2013, we completed three other Phase 1 trials of inhaled LANI. These trials provided safety and pharmacokinetic data at single doses of LANI ranging from five mg to 40 mg in healthy volunteers aged 18 to 77 years, and at multiple doses up to 40 mg (twice daily for three days or twice weekly for six weeks) in healthy volunteers aged 20 to 47 years. A total of 94 subjects were enrolled in these studies, with 70 of those receiving LANI. In healthy adult volunteers, LANI was generally well tolerated at single doses up to 120 mg and at multiple doses up to 40 mg administered twice daily for three days or twice weekly for six weeks.

Our Strategy

We are focused on the discovery and development of direct-acting antivirals to treat infections that affect a significant number of patients globally for which there are limited therapeutic options. In the near-term we intend to employ the following strategy:

|

● |

Focus Our Resources on the Development of our Clinical Stage Antiviral Product Candidates. We plan to focus our resources on vapendavir, an oral treatment for HRV infections in moderate-to-severe asthmatics; BTA074, a novel topical treatment for genital warts caused by HPV types 6 & 11; and BTA585, an oral fusion inhibitor in development for the treatment of RSV infections. |

More specifically, over the next 12 months we intend to:

|

■ |

Initiate a Phase 2 clinical trial for BTA074 in patients with genital warts late 2015; |

|

■ |

Complete and report top-line data from a Phase 1 single ascending dose clinical trial for BTA585 in healthy volunteers in the fourth quarter of 2015; |

|

■ |

Complete and report top-line data from a Phase 1 multiple ascending dose clinical trial for BTA585 in healthy volunteers in the first quarter of 2016; |

|

■ |

Complete the Phase 2b SPIRITUS trial of vapendavir in patients with moderate-to-severe asthma and report top-line data in mid-2016; |

|

■ |

Initiate a Phase 2a RSV challenge study in healthy volunteers for BTA585 in the second quarter of 2016; and |

|

■ |

Continue process development and formulation activities (adult and pediatric) for BTA585 and BTA074. | |

|

● |

Evaluate our RSV preclinical candidates and select a lead candidate for IND-enabling studies. We intend to develop a series of potent RSV non-fusion inhibitors that we believe could be used as a stand-alone treatment or potentially in combination therapy. Our goal is to select a lead candidate from this series by mid-year 2016. |

|

● |

Seek to out-license LANI. We, in concert with Daiichi Sankyo, intend to pursue a license agreement, or other similar transaction, with larger third-party regional or global pharmaceutical or biopharmaceutical companies that have greater clinical development, manufacturing and commercialization capabilities than we do that we believe could advance the development and/or commercialization of LANI. |

Research and Development

Our research and development expense in fiscal 2015, 2014 and 2013 was $19.8 million, $17.5 million and $19.2 million, respectively. In fiscal 2016, we plan to focus our research and development resources primarily on (i) the clinical development of vapendavir, BTA074, and BTA585, (ii) continue process development and formulation activities for vapendavir, BTA074, and BTA585, and (iii) conduct screening, lead-optimization, and preclinical studies on several series of RSV non-fusion inhibitors.

Our basic research and discovery activities, including medicinal chemistry, virology, and cell culture assays have historically been conducted internally by our research staff. In March 2015, we closed our laboratory facilities in Melbourne, Australian. We now use third party research firms and consultants more extensively to conduct these activities under our management. We do not have any future plans to build laboratory facilities or hire significant staff to conduct research, discovery and certain development activities. To the extent we continue these activities in the near-future, we anticipate that we will outsource them and rely on third-party research firms and consultants to a greater extent than we did in the past.

Sales and Marketing

We currently do not have any commercialization or sales and marketing capabilities, and we have no near term plans to invest in or build such capabilities internally. At this time, we anticipate partnering, collaborating with or licensing certain rights to our development programs to other larger pharmaceutical or biopharmaceutical companies in the future to support the late stage development and commercialization of our product candidates.

Manufacturing

We currently do not own or operate any facilities in which we can formulate, manufacture, fill or package our product candidates. We currently rely on single group of contract manufacturers to produce our drug substance and to fill and package the materials required to conduct clinical trials under current good manufacturing practices, (“cGMP”). If an existing contract manufacture fails to deliver on schedule, or at all, or fails to manufacture our material is accordance with their or our specifications and/or FDA regulations, it could significantly delay or interrupt the development or commercialization of our product candidates and affect our operating results and estimated development timelines. We have used contract manufacturers to produce all of the clinical trial material used in the preclinical studies and clinical trials we have conducted to-date.

Competition

The pharmaceutical and biotechnology industries are intensely competitive. Many companies, including biotechnology, chemical and pharmaceutical companies, are actively engaged in activities similar to ours, including research and the development of product candidates for the treatment of infectious diseases. Many of these companies have substantially greater financial and other resources, larger research and development staffs, and more extensive marketing and manufacturing capabilities than we do. In addition, some of them have considerably more experience in preclinical testing, conducting clinical trials and other regulatory approval procedures. There are also academic institutions, governmental agencies and other research organizations that are conducting research in areas in of infectious disease which we are working. We expect to encounter significant direct competition for any of the product candidates we plan to develop. Companies that complete clinical trials obtain required regulatory approvals and commence commercial sales of their products before their competitors may achieve a significant competitive advantage.

Currently, there are no approved direct-acting antiviral drugs to treat HRV infections. However, our vapendavir product candidate, if successfully developed, would indirectly compete with drugs approved to reduce the incidence of exacerbations or improve lung function in patients with asthma and COPD, such as fluticasone propionate (Advair®), tiotoprium bromide (Spiriva®), fluticasone furoate/vilanterol (Breo Ellipta®), and roflumilast (Daliresp®). In addition to these approved drugs, there are compounds in the clinical development stage, such as inhaled ß-interferon, that if successfully developed for the treatment of HRV infections could compete with vapendavir.

Currently there no approved HPV-specific directing acting anti-viral drugs to treat genital warts or RRP. Treatments for genital warts can be divided broadly into two categories: provider-administered ablative/cytodestructive therapies (including cryotherapy, laser ablation, and trichloroacetic acid) and patient-administered topical therapies such as podophyllotoxin (Condylox; Wartec), sinecatechins (Veregen®), and imiquimod (Zyclara®, Aldara®). There are no cures for RRP, however current maintenance treatments include CO2 laser surgery, pulse dye laser surgery, endoscopic microdebriders, and intralesional injection with cidofovir. We anticipate that BTA074, if successfully developed, would directly compete with the patient-applied topical treatments for genital warts and could become first-line therapy for RRP. We believe key differentiating features of BTA074 could be its mechanism of action, favorable local skin tolerability, efficacy, and lower reoccurrence rate. Three prophylactic vaccines, primarily designed to prevent cervical, vulvar, vaginal, and anal cancers, are currently marketed: a bivalent HPV16/18 vaccine (Cervarix®; GSK), quadrivalent HPV16/18/6/11 (Gardasil®, Merck) and the 9-valent HPV 6/11/16/18/33/52/58 (Gardasil®9; Merck). Gardasil® 9 is indicated for females aged 9 through 26 and males aged 9 through 15, to prevent various HPV related cancers and genital warts in both sexes. Gardasil®, Gardasil® 9, and Cervarix® are not known to exhibit a therapeutic effect on existing HPV lesions.

Effective treatments of RSV infections in pediatrics, the elderly, and the immunocompromised are very limited. Currently, only Virazole® (ribavirin) is indicated for the treatment of hospitalized infants and young children with severe lower respiratory tract infections due to RSV. We are aware that the following compounds are under development: Gilead’s GS-5806, Johnson and Johnson’s JJ-53718678 (ALS-8176), Ark Biosciences’ AK0529 and Teva Pharmaceutical’s MDT-637. The only approved drug for the prevention of RSV infections in high risk infants is MedImmune’s palivizumab (Synagis®), a monoclonal antibody.There are several vaccines and antibody products designed to prevent RSV infections in clinical development. Among the clinical stage product candidates in development are Novavax’s RSV F vaccine, GSK’s GSK3003898A vaccine, GSK’s GSK3003898A vaccine, Bavarian Nordic’s BN® RSV vaccine, MedImmune’s MEDI ÄM2-2 vaccine, MedImmune’s monoclonal antibody MEDI8897, and Regeneron’s monoclonal antibody REGN2222C.

The pharmaceutical market for products that prevent or treat influenza is competitive. Key competitive advantages for LANI may include its single administration treatment regimen, its resistance profile, and to-date, its reported safety profile. A number of NIs are currently available in the U.S. and/or other counties, including Japan, for the prevention and/or treatment of influenza. These include oseltamivir phosphate from Hoffmann-La Roche Ltd. (“Roche”), which is marketed as Tamiflu®, zanamivir from GSK, which is marketed as Relenza®, laninamivir octanoate from Daiichi Sankyo, which is marketed as Inavir®, and peramivir marketed as Rapivab® or Rapiacta® by CSL Limited and Shionogi & Co. Ltd., respectively. We anticipate that LANI, if ever successfully developed and approved, would compete directly or indirectly with drugs that will be “generic” by the time LANI may be approved for sale. Generic drugs are drugs whose patent protection has expired, which generally have an average selling price substantially lower than drugs protected by patents and intellectual property rights. Unless a patented drug can sufficiently differentiate itself from a competing generic drug in a meaningful manner, the existence of generic competition in any indication will generally impose significant pricing pressure on competing patented drugs.

Intellectual Property Rights and Patents

Patents and other proprietary intellectual rights are crucial in our business and industry, and establishing and maintaining these rights are essential to justify the cost to develop and commercialize any of our product candidates and products. We have sought, and intend to continue to seek, viable and strategic intellectual property rights, including, but not limited to, patent protection for our inventions, and intend to rely upon patents, trade secrets, confidential information, know-how, trademarks, improvements in our technological innovations and licensing opportunities to develop and maintain a competitive advantage for our products and product candidates. In order to protect our intellectual property rights, we typically require employees, consultants, collaborators, advisors, potential partners, service providers and contractors to enter into confidentiality agreements with us, generally stating that they will not disclose our confidential information to third parties for a certain period of time, and will otherwise not use our confidential information for anyone’s benefit but ours.

The patent positions of biotechnology and pharmaceutical companies are highly uncertain and involve complex legal and factual questions. Therefore, the patentability of subject matter we claim in our patent applications, the breadth of the claims ultimately granted, or their enforceability cannot be predicted. For this reason, we may not have or be able to obtain or maintain worldwide patent protection for any or all of our products and product candidates, and our intellectual property rights may not be protected or legally enforceable in all countries throughout the world. In some cases we may rely upon data exclusivity or similar exclusivities, although there is no guarantee that such exclusivity will be available or obtained in any jurisdiction. Further, as the publication of discoveries in the scientific and/or patent literature often lags behind the actual discoveries, we cannot be certain that we or our licensors were the first to make the inventions described in our patent applications or that we or our licensors were the first to file patent applications for such inventions.

Pursuant to the terms of the Uruguay Round Agreements Act, patents filed on or after June 8, 1995 in the U. S. have a term of 20 years from the date of filing, regardless of the period of time it may take for the patent to ultimately issue. This may shorten the period of patent protection afforded to our products as patent applications in the biopharmaceutical sector often take considerable time to issue. Under the Drug Price Competition and Patent Term Restoration Act of 1984, a sponsor may obtain marketing exclusivity for a period of time following FDA approval of certain drug applications, regardless of patent status, if the drug is a new chemical entity or if new clinical studies were used to support the marketing application for the drug.

Zanamivir, a neuraminidase inhibitor approved for the treatment and prevention of influenza A and B, is marketed worldwide as Relenza® by GSK. Most of our Relenza® patents have expired and the only substantial remaining intellectual property related to the Relenza® patent portfolio is scheduled to expire in July 2019 in Japan. On May 12, 2015, we filed a request for rehearing with the U.S. Patent and Trademark Office, Patent Trial and Appeal Board (“PTAB”) in relation to the pending patent application No. 08/737,141 related to Relenza IP in the U.S. On June 23, 2015 the PTAB denied our request for a rehearing. We reported on September 11, 2015, that we have filed an another appeal in relation to the pending patent application No. 08/737,141 related to Relenza® to the United States Court of Appeals for the Federal Circuit. While we cannot determine the duration or the outcome of this appeal process, or how long this patent application will remain pending, however we do believe that if this most recent appeal is unsuccessful, it is unlikely that the patent claims will be ever issued and we will receive no further royalties. If the patent claims are ultimately issued, we would be eligible to receive royalties from net sales of Relenza® in the U.S. for an additional 17 years from the date of allowance.

LANI, a long acting NI for the treatment and prevention of influenza A and B, is currently marketed as Inavir® in Japan by Daiichi-Sankyo. The patent relating to the structure of LANI expires in 2017 in the U.S., the EU and Japan. The patent relating to hydrates and the crystalline form of LANI actually used in the product expires in 2021 (not including extensions) in the U.S. and EU and in 2024 in Japan. In February 2015, a patent containing claims relevant to the manufacture of Inavir® was issued in Japan and expires in December 2029. The dry-powder inhaler device patent portfolio, which includes TwinCaps®, is owned by Hovione International Limited (“Hovione”) and is exclusively licensed to us and Daiichi Sankyo worldwide for the prevention and treatment of influenza and other influenza-like viral infections. These patents will expire in 2029 in the U.S., and in 2027 in the EU and Japan.

Vapendavir is an oral antiviral capsid binder we are developing to treat HRV infections. We exclusively own the vapendavir patent portfolio, and issued claims under this portfolio will begin to expire in some countries in December 2021, not including extensions. Claims filed in recent patent applications related to a free-base form of vapendavir, if allowed, would extend coverage until 2034, without extensions, however we cannot make any assurance that these claims will be allowed.

BTA074 is a direct-acting antiviral we are developing as a treatment for genital warts and RRP caused by HPV 6 and 11. The patent containing composition of matter claims expires in the U.S. in 2029 without extensions. Pending U.S. patent applications related to pharmaceutical compositions and methods of synthesis of BTA074 if allowed, would extend coverage until 2033, without extensions, however we cannot make any assurance that these claims will be allowed.

We also own a patent portfolio focused on developing several series of oral antivirals for RSV. Our RSV patent portfolio is comprised of a number of patent filings directed to several compound series, with the earliest projected expiries of such patents ranging from late-2024 to late-2031. Issued patent claims covering the BTA585 composition of matter will begin to expire in 2031 without extensions.

Patent Term Restoration/Extension and Marketing Exclusivity

Depending upon the timing, duration and specifics of FDA approval for the intended use of our product candidates, some of our U.S. patents may be eligible for limited patent term extension under the Drug Price Competition and Patent Term Restoration Act of 1984, commonly referred to as the Hatch-Waxman Act. The Hatch-Waxman Act permits a patent restoration term, or extension, of up to five years as compensation for patent term lost during product development and the FDA regulatory review process. However, patent term restoration cannot extend the remaining term of a patent beyond a total of 14 years from the product’s approval date. Subject to certain limitations, the patent term restoration period is generally one-half the time between the effective date of an investigational new drug (“IND”) and the submission date of a new drug application (“NDA”) plus the time between the submission date of an NDA and the approval of that application, up to a total of five years. Only one patent applicable to an approved drug is eligible for the extension. The application for such extension must be submitted prior to the expiration of the patent and within 60 days of the drug’s approval. The United States Patent and Trademark Office (“USPTO”), in consultation with the FDA, reviews and approves the application for any patent term extension or restoration. Similar provisions are available in Europe and other foreign jurisdictions to extend the term of a patent that covers an approved drug. In the future, we may apply for restoration of patent term for one or more of our currently owned or licensed patents to add patent life beyond its current expiration date, depending on the expected length of the clinical trials and other factors involved in the filing of the relevant NDA.

Market exclusivity provisions under the Federal Drug, Food and Cosmetic Act (“FDCA”) can also delay the submission or the approval of certain applications of other companies seeking to reference another company’s NDA. The FDCA provides a five-year period of non-patent data exclusivity within the U.S. to the first applicant to obtain approval of an NDA for a new chemical entity. A drug is a new chemical entity if the FDA has not previously approved any other new drug containing the same active moiety, which is the molecule responsible for the action of the drug substance. During the exclusivity period, the FDA may not accept for review an Abbreviated New Drug Application (“ANDA”), or a 505(b)(2) NDA submitted by another company for another version of such drug where the applicant does not own or have a legal right of reference to all the data required for approval. However, an application may be submitted after four years if it contains a certification of patent invalidity or non-infringement to one of the patents listed with the FDA by the innovator NDA holder. The FDCA also provides three years of marketing exclusivity for an NDA, 505(b)(2) NDA or supplement to an existing NDA if new clinical investigations, other than bioavailability studies, that were conducted or sponsored by the applicant are deemed by the FDA to be essential to the approval of the application, for example new indications, dosages or strengths of an existing drug. This three-year exclusivity covers only the conditions associated with the new clinical investigations and does not prohibit the FDA from approving ANDAs for drugs containing the original active agent. Five-year and three-year exclusivity will not delay the submission or approval of a full NDA. However, an applicant submitting a full NDA would be required to conduct or obtain a right of reference to all of the pre-clinical studies and adequate and well-controlled clinical trials necessary to demonstrate safety and effectiveness. We cannot assure you that we will be able to take advantage of either the patent term extension or marketing exclusivity provisions of this law.

Pediatric exclusivity is another type of exclusivity available in the U.S. Pediatric exclusivity, if granted, provides an additional six months to existing exclusivity periods and patent terms. This six-month exclusivity, which runs from the end of other exclusivity protection or the patent term, may be granted based on the voluntary completion of a pediatric study in accordance with a FDA request for such a study. The current pediatric exclusivity provision was reauthorized in September 2007 as part of the Food and Drug Administration Amendments Act.

Licenses and Agreements

|

|

GSK |

In 1990, we entered into a royalty-bearing research and license agreement with GSK for the development and commercialization of zanamivir, a NI marketed by GSK as Relenza® to prevent and treat influenza. Under the terms of the agreement, we licensed zanamivir to GSK on an exclusive, worldwide basis and are entitled to receive royalty payments of 7% of GSK's annual net sales of Relenza® in the U.S., Europe, Japan and certain other countries and 10% in Australia, New Zealand, South Africa and Indonesia to the extent that the underlying patents in those respective countries do not expire. Most of our Relenza® patents have expired and the only substantial remaining intellectual property related to the Relenza® patent portfolio is scheduled to expire in July 2019 in Japan. GSK has recently verified that we will continue to receive royalties on the net sales of Relenza® in the U.S. beyond December 2014 to the extent that U.S. Patent Application No. 08/737,141 remains pending.

|

|

Daiichi Sankyo |

In 2003, we entered into collaboration and license agreement with Daiichi Sankyo related to the development of second generation long acting NIs, including LANI. Under the collaboration and license agreement, we and Daiichi Sankyo cross-licensed the right to develop, make, use, sell or offer for sale, or import products based on our respective intellectual property related to our long acting NIs. A primary focus of the agreement was for the parties to collectively seek third-party licensees that could develop and commercialize the related long-acting NIs on a worldwide basis. In the event that the related intellectual property was out-licensed to a third party, we would share equally with Daiichi Sankyo in any future royalties, license fees, milestones or other payments received from such a licensee. Further, although it was the intention of the parties to seek a third-party licensee or licensees worldwide, the parties retained the right to market or co-market related products in the U.S. and other markets outside of Japan, and any sales made by either party in the U.S. would result in the selling party paying the other party a royalty rate that was half of the royalty rate paid by any other third-party licensee. To date, there have been no third-party licenses granted pursuant to this agreement; therefore a royalty rate on net sales outside of Japan has not been established.

In March 2009, we entered into a commercialization agreement with Daiichi Sankyo, pursuant to which Daiichi Sankyo obtained exclusive marketing rights in Japan for long acting NI’s, including LANI, covered by the 2003 collaboration and license agreement between the parties. In consideration for these rights, Daiichi Sankyo agreed to pay us a royalty rate equal to 4% on net sales in Japan. In September 2010, LANI (Inavir®) was approved for sale by the Japanese Ministry of Health and Welfare for the treatment of influenza in adults and children. Accordingly, under this agreement, we currently receive a 4% royalty on net sales of Inavir® in Japan and are eligible to earn sales milestone payments.

|

|

Hovione |

On January 25, 2007, we and Daiichi Sankyo collectively entered into an exclusive license agreement with Hovione for the use of its proprietary dry-powder inhaler technology for prevention and treatment of influenza and other influenza-like viral infections with LANI or any other long-acting NI selected by us or Daiichi Sankyo during the term of the agreement. Under the terms of the agreement, in the event we sublicense LANI administered by the dry-powder inhaler to a third-party, we will owe Hovione a sublicense fee and a royalty on net sales. In the event we or Daiichi Sankyo commercialize LANI administered by the dry-powder inhaler outside of Japan, the terms, conditions, and any royalty rate due to Hovione have not yet been determined. The license agreement terminates with expiration of the last patent claim covering the dry-powder inhaler intellectual property used. These claims are currently scheduled to expire in 2029 in the U.S., and in 2027 in the EU and Japan.

Regulatory Matters

|

|

Overview |

The preclinical and clinical testing, manufacture, labeling, storage, distribution, promotion, sale, export, reporting and record-keeping of drug products and product candidates is subject to extensive regulation by numerous governmental authorities in the U.S., principally the FDA and corresponding state agencies, and similar regulatory authorities in other countries.

Non-compliance with applicable regulatory requirements can result in, among other things, total or partial suspension of the clinical development, manufacturing and marketing of a product or product candidate, the refusal of the FDA or similar regulatory authorities in other countries to grant marketing approval, the withdrawal of marketing approvals, fines, injunctions, seizure of products and criminal prosecution.

|

|

U.S. Regulatory Approval |

Pursuant to FDA regulations, we are required to successfully undertake a long and rigorous development process before any of our product candidates can be approved and marketed or sold in the U.S. This regulatory process typically includes the following steps:

|

● |