Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - CSS INDUSTRIES INC | css-3312015xex311.htm |

| EX-32.2 - EXHIBIT 32.2 - CSS INDUSTRIES INC | css-3312015xex322.htm |

| EX-31.2 - EXHIBIT 31.2 - CSS INDUSTRIES INC | css-3312015xex312.htm |

| EX-10.28 - EXHIBIT 10.28 - CSS INDUSTRIES INC | css-3312015xex1028.htm |

| EXCEL - IDEA: XBRL DOCUMENT - CSS INDUSTRIES INC | Financial_Report.xls |

| EX-23 - EXHIBIT 23 - CSS INDUSTRIES INC | css-3312015xex23.htm |

| EX-32.1 - EXHIBIT 32.1 - CSS INDUSTRIES INC | css-3312015xex321.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K |

(Mark one)

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended March 31, 2015

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-2661

CSS INDUSTRIES, INC. (Exact name of registrant as specified in its charter) |

Delaware | 13-1920657 | |

(State or other jurisdiction of | (I.R.S. Employer | |

incorporation or organization) | Identification No.) | |

1845 Walnut Street, Philadelphia, PA | 19103 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (215) 569-9900

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common Stock, $.10 par value | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer | ¨ | Accelerated filer | ý | |||

Non-accelerated filer | ¨ | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

The aggregate market value of the voting stock held by non-affiliates of the registrant is $211,880,956. Such aggregate market value was computed by reference to the closing price of the common stock of the registrant on the New York Stock Exchange on September 30, 2014, being the last trading day of the registrant’s most recently completed second fiscal quarter. Such calculation excludes the shares of common stock beneficially owned at such date by certain directors and officers of the registrant, as described under the section entitled “Ownership of CSS Common Stock” in the proxy statement to be filed by the registrant for its 2015 Annual Meeting of Stockholders. In making such calculation, registrant does not determine the affiliate or non-affiliate status of any holders of the shares of common stock for any other purpose.

At May 18, 2015, there were outstanding 9,343,750 shares of common stock.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for its 2015 Annual Meeting of Stockholders are incorporated by reference into Part III of this Form 10-K.

CSS INDUSTRIES, INC.

FORM 10-K

FOR THE FISCAL YEAR ENDED MARCH 31, 2015

INDEX

Page | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

Item 15. | ||

PART I

Item 1. Business.

General

CSS Industries, Inc. (“CSS” or the “Company”) is a consumer products company primarily engaged in the design, manufacture, procurement, distribution and sale of all occasion and seasonal social expression products, principally to mass market retailers. These all occasion and seasonal products include decorative ribbons and bows, boxed greeting cards, gift tags, gift wrap, gift bags, gift boxes, gift card holders, decorations, classroom exchange Valentines, floral accessories, Easter egg dyes and novelties, craft and educational products, stickers, memory books, stationery, journals, notecards, infant and wedding photo albums, scrapbooks, and other items that commemorate life’s celebrations. CSS’ product breadth provides its retail customers the opportunity to use a single vendor for much of their seasonal product requirements. A substantial portion of CSS’ products are manufactured, packaged and/or warehoused in ten facilities located in the United States, with the remainder sourced from foreign suppliers, primarily in Asia. The Company’s products are sold to its customers by national and regional account sales managers, sales representatives, product specialists and by a network of independent manufacturers’ representatives. CSS maintains a showroom in Hong Kong as well as a purchasing office to administer Asian sourcing opportunities. The Company’s principal operating subsidiaries include Berwick Offray LLC (“Berwick Offray”), Paper Magic Group, Inc. (“Paper Magic”) and C.R. Gibson, LLC (“C.R. Gibson”).

The Company’s fiscal year ends on March 31. References to a particular year refer to the fiscal year ending in March of that year. For example, fiscal 2015 refers to the fiscal year ended March 31, 2015.

The Company’s goal is to expand by developing new or complementary products, by entering new markets and by acquiring companies that are complementary with its existing operating businesses.

On February 19, 2015, a subsidiary of the Company completed the acquisition of substantially all of the business and assets of Hollywood Ribbon Industries, Inc. ("Hollywood Ribbon") for approximately $12,903,000 in cash, including transaction costs of approximately $121,000. The Company also incurred one-time transition costs of approximately $760,000 in fiscal 2015, primarily related to services performed under a transition service agreement and costs related to the relocation of inventory and equipment. Hollywood Ribbon was a manufacturer, distributor and supplier of ribbon, bows and similar products to mass market retailers and national grocery, drug store, party and craft, and discount chains. As of March 31, 2015, a portion of the purchase price is being held in escrow for certain post-closing adjustments and indemnification obligations. The acquisition was accounted for as a purchase, and $745,000, which is the excess of cost over preliminary fair value of the net tangible and identifiable intangible assets acquired, was recorded as goodwill in the accompanying consolidated balance sheet. For tax purposes, goodwill resulting from this acquisition is deductible.

On May 19, 2014, a subsidiary of the Company completed the acquisition of substantially all of the business and assets of Carson & Gebel Ribbon Co., LLC ("Carson & Gebel") for approximately $5,173,000 in cash, including transaction costs of $31,000. Carson & Gebel was a manufacturer, distributor and supplier of decorative ribbon and similar products to wholesale florists, packaging distributors and bow manufacturers. Key product categories include cut edge acetate ribbon and velvet ribbon used in everyday and holiday floral arrangements. As of March 31, 2015, a portion of the purchase price is being held in escrow for certain post-closing adjustments and indemnification obligations. The acquisition was accounted for as a purchase, and $553,000, which is the excess of cost over preliminary fair value of the net tangible and identifiable intangible assets acquired, was recorded as goodwill in the accompanying consolidated balance sheet. For tax purposes, goodwill resulting from this acquisition is deductible.

On December 3, 2013, the Company combined the operations of its C.R. Gibson business with the operations of its Berwick Offray and Paper Magic businesses, which were previously combined on March 27, 2012. These businesses were combined in order to provide stronger management oversight by reallocating sourcing, sales and marketing resources in a more strategic manner.

On September 5, 2012, the Company and its Paper Magic subsidiary sold the Halloween portion of Paper Magic’s business and certain Paper Magic assets relating to such business, including certain tangible and intangible assets associated with Paper Magic’s Halloween business, to Gemmy Industries (HK) Limited (“Gemmy”). Paper Magic’s remaining Halloween assets, including accounts receivable and inventory, were excluded from the sale. Paper Magic retained the right and obligation to fulfill all customer orders for Paper Magic Halloween products (such as Halloween masks, costumes, make-up and novelties) for the Halloween 2012 season. The sale price of $2,281,000 was paid to Paper Magic at closing. The Company incurred $523,000 of transaction costs (included within disposition of product line further discussed in Note 4 to the consolidated financial statements), yielding net proceeds of $1,758,000.

1

On September 9, 2011, the Company and its Cleo Inc (“Cleo”) subsidiary sold the Christmas gift wrap portion of Cleo’s business and certain of its assets relating to such business, including certain equipment, contract rights, customer lists, intellectual property and other intangible assets to Impact Innovations, Inc. (“Impact”). Cleo’s remaining assets, including accounts receivable and inventory, were excluded from the sale. The purchase price was $7,500,000, of which $2,000,000 was paid in cash at closing. The remainder of the purchase price was paid through the issuance by Impact of an unsecured subordinated promissory note, which provided for quarterly payments of interest at 7% and principal payments as follows: $500,000 on March 1, 2012; $2,500,000 on March 1, 2013; and all remaining principal and interest on March 1, 2014. In the fourth quarter of fiscal 2013, the Company received a $2,000,000 principal payment in advance of the March 1, 2014 due date. All interest payments were paid timely and the final principal payment of $500,000 was received in March 2014. The results of operations for the years ended March 31, 2015, 2014 and 2013 reflect the historical operations of the Christmas gift wrap business as discontinued operations and the discussion herein is presented on the basis of continuing operations, unless otherwise stated.

Principal Products CSS designs and markets decorative ribbons and bows, all occasion boxed greeting cards, gift wrap, gift bags, gift boxes, gift card holders, decorative and waxed tissue paper, decorative films and foils, stickers, memory books, stationery, journals, notecards, infant and wedding photo albums, scrapbooks, floral accessories and other gift and craft items to its mass market, craft, specialty and floral retail and wholesale distribution customers, and teachers’ aids and other learning oriented products to the education market through mass market retailers, school supply distributors and teachers’ stores. CSS also designs, manufactures, procures, distributes and sells a broad range of seasonal consumer products primarily through the mass market distribution channel. Christmas products include decorative ribbons and bows, boxed greeting cards, gift tags, gift bags, gift boxes, gift card holders, tissue paper and decorations. CSS’ Valentine product offerings include classroom exchange Valentine cards and other related Valentine products, while its Easter product offerings include Dudley’s® brand of Easter egg dyes and related Easter seasonal products.

Key brands include Paper Magic®, Berwick®, Offray®, C.R. Gibson®, Markings®, Stepping Stones®, Tapestry®, Seastone®, Dudley’s®, Eureka®and Stickerfitti®.

CSS operates ten manufacturing and/or distribution facilities located in Pennsylvania, Maryland, New Hampshire, South Carolina, Alabama and Texas. A description of the Company’s product lines and related manufacturing and/or distribution facilities is as follows:

• | Ribbons and bows are primarily manufactured and warehoused in seven facilities located in Pennsylvania, Maryland, South Carolina and Texas. The manufacturing process is vertically integrated. Non-woven ribbon and bow products are primarily made from polypropylene resin, a petroleum-based product, which is mixed with color pigment, melted and pressed through an extruder. Large rolls of extruded film go through various combinations of manufacturing processes before being made into bows or packaged on ribbon spools or reels as required by various markets and customers. Woven fabric ribbons are manufactured domestically or imported from Mexico and Asia. Imported woven products are either narrow woven or converted from bulk rolls of wide width textiles. Domestic woven products are narrow woven. |

• | Boxed greeting cards are produced by Asian manufacturers to our specifications. Domestically distributed products are warehoused in a distribution facility in Pennsylvania. |

• | Easter egg dye products are manufactured in Asia to specific formulae by contract manufacturers who meet regulatory requirements for the formularization and packaging of such products. Domestically distributed products are warehoused in a distribution facility in Pennsylvania. |

• | Memory books, stationery, journals and notecards, infant and wedding photo albums, scrapbooks, educational products, and other gift items are imported from Asian manufacturers and warehoused and distributed from a distribution facility in Florence, Alabama. |

• | Floral accessories, including pot covers, foil, waxed tissue, shred, aisle runners, corsage bags and other paper and film products, are manufactured in facilities located in New Hampshire or imported from Mexico. Manufacturing includes gravure and flexo printing, waxing and converting. Products are warehoused and distributed from a distribution facility in Pennsylvania. |

Other products including, but not limited to, decorative tissue paper, all occasion gift wrap, gift tags, gift bags, gift boxes, gift card holders, classroom exchange Valentine products, Easter products, educational products, and decorations are designed to the specifications of CSS and are imported primarily from Asian manufacturers.

During our 2015 fiscal year, CSS experienced no material difficulties in obtaining raw materials or finished goods from suppliers.

2

Intellectual Property Rights CSS has a number of copyrights, patents, tradenames, trademarks and intellectual property licenses which are used in connection with its products. Substantially all of its designs and artwork are protected by copyright. Intellectual property license rights which CSS has obtained are viewed as especially important to the success of its classroom exchange Valentines and stickers. It is CSS’ view that its operations are not dependent upon any individual patent, tradename, trademark, copyright or intellectual property license. The collective value of CSS’ intellectual property is viewed as substantial, and CSS seeks to protect its rights in all patents, copyrights, tradenames, trademarks and intellectual property licenses.

Sales and Marketing Most of CSS’ products are sold in the United States and Canada by national and regional account sales managers, sales representatives, product specialists and by a network of independent manufacturers’ representatives. CSS maintains permanent showrooms in Moosic, PA; Dallas, TX; Atlanta, GA and Hong Kong where buyers for major retail customers will typically visit for a presentation and review of the new lines. Products are also displayed and presented in showrooms maintained by various independent manufacturers’ representatives in major cities in the United States and Canada. Relationships are developed with key retail customers by CSS sales personnel and independent manufacturers’ representatives. Customers are generally mass market retailers, discount department stores, specialty chains, warehouse clubs, drug and food chains, dollar stores, office supply stores, independent card, gift and floral shops and retail teachers’ stores. Net sales to Walmart Stores, Inc. and its affiliates and Target Corporation accounted for approximately 28% and 12% of total net sales, respectively, during fiscal 2015. No other customer accounted for 10% or more of the Company’s net sales in fiscal 2015. Our ten largest customers, which include mass market retailers, warehouse clubs and national drug store chains, accounted for approximately 59% of our sales in our 2015 fiscal year. Approximately 62% of the Company’s sales are attributable to all occasion products with the remainder attributable to seasonal (Christmas, Valentine’s Day and Easter) products. Approximately 30% of CSS’ sales relate to the Christmas season. Seasonal products are generally designed and marketed beginning up to 18 to 20 months before the holiday event and manufactured during an eight to ten month production cycle. Due to these long lead time requirements, timely communication with third party factories, licensors, customers and independent manufacturers’ representatives is critical to the timely production of seasonal products. Sales terms for our seasonal products do not generally require payment until just before or just after the holiday, in accordance with industry practice. C.R. Gibson’s social stationery products are sold by a national organization of sales representatives that specialize in the gift and specialty channel, as well as by C.R. Gibson’s key account representatives. The Company also sells custom products to private label customers, to other social expression companies, and to converters of the Company’s ribbon products. Custom products are sold by both independent manufacturers’ representatives and CSS sales managers. CSS products, with some customer specific exceptions, are not sold under guaranteed or return privilege terms. All occasion ribbon and bow products are also sold through sales representatives or independent manufacturers’ representatives to wholesale distributors and independent small retailers who serve the floral, craft and retail packaging trades.

Competition among retailers in the sale of the Company’s products to end users is intense. CSS seeks to assist retailers in developing merchandising programs designed to enable the retailers to meet their revenue objectives while appealing to their consumers’ tastes. These objectives are met through the development and manufacture of custom configured and designed products and merchandising programs. CSS’ years of experience in merchandising program development and product quality are key competitive advantages in helping retailers meet their objectives.

Competition CSS competes with various domestic and foreign companies in each of its product offerings. Some of our competitors, such as American Greetings Corporation, LLC ("American Greetings") and Hallmark Cards, Incorporated (“Hallmark”), are larger and have greater resources than the Company. CSS believes its products are competitively positioned in their primary markets. Since competition is based primarily on category knowledge, timely delivery, creative design, price and, with respect to seasonal products, the ability to serve major retail customers with single, combined product shipments for each holiday event, CSS believes that its focus on products, combined with consistent service levels, allows it to compete effectively in its core markets.

Employees

At May 18, 2015, approximately 1,250 persons were employed by CSS (increasing to approximately 1,450 as seasonal employees are added). The Company believes that relationships with its employees are satisfactory.

With the exception of the bargaining unit at the ribbon manufacturing facility in Hagerstown, Maryland, which totaled approximately 90 employees as of May 18, 2015, CSS employees are not represented by labor unions. Because of the seasonal nature of certain of its businesses, the number of production employees fluctuates during the year. The collective bargaining agreement with the labor union representing the Hagerstown-based production and maintenance employees remains in effect until December 31, 2017. Historically, we have been successful in renegotiating expiring agreements without any disruption of operating activities.

3

SEC Filings

The Company’s Internet address is www.cssindustries.com. Through its website, the following filings are made available free of charge as soon as reasonably practicable after they are electronically filed with or furnished to the Securities and Exchange Commission: its annual report on Form 10-K, its quarterly reports on Form 10-Q, its current reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934.

Item 1A. Risk Factors.

You should carefully consider each of the risk factors we describe below, as well as other factors described in this annual report on Form 10-K and elsewhere in our SEC filings.

Our results of operations fluctuate on a seasonal basis, and quarter to quarter comparisons may not be a good indicator of our performance. Seasonal demand fluctuations may adversely affect our cash flow and our ability to sell our products.

Approximately 62% of our sales are all occasion with the remainder attributable to seasonal (Christmas, Valentine’s Day and Easter) products. Approximately 30% of our sales relate to the Christmas season. The seasonal nature of our business has historically resulted in lower sales levels and operating losses in our first and fourth quarters, and higher sales levels and operating profits in our second and third quarters. As a result, our quarterly results of operations fluctuate during our fiscal year, and a quarter to quarter comparison is not a good indication of our performance or how we will perform in the future. For example, our overall results of operations in the future may fluctuate substantially based on seasonal demand for our products. Such variations in demand could have a material adverse effect on the timing of cash flow and therefore our ability to meet our obligations with respect to our debt and other financial commitments. Seasonal fluctuations also affect our inventory levels. We must carry significant amounts of inventory, especially before the Christmas retail selling period. If we are not successful in selling the inventory during the relevant period, we may have to sell the inventory at significantly reduced prices, or we may not be able to sell the inventory at all.

We rely on a few mass market retailers, warehouse clubs and national drug store chains for a significant portion of our sales. The loss of sales, or a significant reduction of sales, to one or more of our large customers may adversely affect our business, results of operations and financial condition. Past and future consolidation within the retail sector also may lead to reduced profit margins, which may adversely affect our business, results of operations and financial condition.

A few of our customers are material to our business and operations. Our sales to Walmart Stores, Inc. and its affiliates and Target Corporation accounted for approximately 28% and 12% of our sales, respectively, during our 2015 fiscal year. No other single customer accounted for 10% or more of our sales in fiscal 2015. Our ten largest customers, which include mass market retailers, warehouse clubs and national drug store chains, accounted for approximately 59% of our sales in our 2015 fiscal year. Our business depends, in part, on our ability to identify and define product and market trends, and to anticipate, understand and react to changing consumer demands in a timely manner. There can be no assurance that our large customers will continue to purchase our products in the same quantities that they have in the past. The loss of sales, or a significant reduction of sales, with one or more of our large customers, including without limitation a loss or significant reduction in sales resulting from our failure or inability to comply with one or more of any of our customers’ sourcing requirements, may adversely affect our business, results of operations and financial condition. Further, in recent years there has been consolidation among our retail customer base. As the retail sector consolidates, our customers become larger, and command increased leverage in negotiating prices and other terms of sale of our products, including credits, discounts, allowances and other incentive considerations to these customers. Past and future consolidation may lead to reduced profit margins, which may adversely affect our business, results of operations and financial condition.

Increases in raw material and energy costs, resulting from general economic conditions, acts of nature, such as hurricanes, earthquakes or pandemics, acts of war, threats of war, terrorism, civil unrest, or other factors, may raise our cost of goods sold and adversely affect our business, results of operations and financial condition.

Paper and petroleum-based materials are essential in the manufacture of our products, and the cost of such materials is significant to our cost of goods sold. Energy costs, especially fuel costs, also are significant expenses in the production and delivery of our products. Increased costs of raw materials or energy resulting from general economic conditions, acts of nature, such as hurricanes, earthquakes or pandemics, acts of war, threats of war, terrorism, civil unrest, or other factors, may result in declining margins and operating results if market conditions prevent us from passing these increased costs on to our customers through timely price increases on our products.

4

Risks associated with our use of foreign suppliers may adversely affect our business, results of operations and financial condition.

For a large portion of our product lines, with the exception of our decorative ribbon and bow product lines, we use foreign suppliers to manufacture a significant portion of our products. Approximately 58% of our sales in fiscal 2015 were related to products sourced from foreign suppliers. Our use of foreign suppliers exposes us to risks inherent in doing business outside of the United States, including risks associated with foreign currency fluctuations, transportation costs and delays or disruptions, difficulties in maintaining and monitoring quality control (including without limitation risks associated with defective products), enforceability of agreed upon contract terms, compliance with existing and new United States and foreign laws and regulations, such as the United States Foreign Corrupt Practices Act and legislation and regulations relating to imported products, costs relating to the imposition or retrospective application of antidumping and countervailing duties or other trade-related sanctions on imported products, economic, civil or political instability, acts of war, threats of war, terrorism, civil unrest, labor-related issues, such as labor shortages or wage disputes or increases, international public health issues, and restrictions on the repatriation of profits and assets.

Increased overseas sourcing by our competitors and our customers may reduce our market share and profit margins, adversely affecting our business, results of operations and financial condition.

We have relatively high market share in many of our seasonal product categories. Most of our product markets have shown little or no growth, and some of our product markets have declined, in recent years, and we continue to confront significant cost pressure as our competitors source certain products from overseas and certain customers increase direct sourcing from overseas factories. Increased overseas sourcing by our competitors and certain customers may result in a reduction of our market share and profit margins, adversely affecting our business, results of operations and financial condition.

Difficulties encountered by our key customers may cause them to reduce their purchases from us and/or increase our exposure to losses from bad debts, and adversely affect our business, results of operations and financial condition.

Many of our largest customers are national and regional retail chains. The retail channel in the United States has experienced significant shifts in market share among competitors in recent years, including as a result of the emergence of e-commerce retailers. Any current or future economic slowdown, slow economic recovery, or uncertain economic outlook could further adversely affect our key customers. Our business, results of operations and financial condition may be adversely affected if our customers file for bankruptcy protection and/or cease doing business, significantly reduce the number of stores they operate, significantly reduce their purchases from us, do not pay us for their purchases, or if their payments to us are delayed because of bankruptcy or other factors beyond our control.

Our business, results of operations and financial condition may be adversely affected by volatility in the demand for our products.

Our success depends on the sustained demand for our products. Many factors affect the level of consumer spending on our products, including, among other things, general business conditions, interest rates, the availability of consumer credit, taxation, the effects of war, terrorism or threats of war, civil unrest, fuel prices, consumer demand for our products based upon, among other things, consumer trends and the availability of alternative products, and consumer confidence in future economic conditions. A decline in economic activity in the United States or other regions of the world, a slow economic recovery, or an uncertain outlook, in addition to adversely affecting our customers, could adversely affect our business, results of operations and financial condition because of, among other things, reduced consumer spending on discretionary items, including our products. We also routinely utilize new artwork, designs or licensed intellectual property in connection with our products, and our inability to design, select, procure, maintain or sell consumer-desired artwork, designs or licensed intellectual property could adversely affect the demand for our products, which could adversely affect our business, results of operations and financial condition.

Our business, results of operations and financial condition may be adversely affected if we are unable to compete successfully against our competitors.

Our success depends in part on our ability to compete against our competitors in our highly competitive markets. Our competitors, including domestic businesses, such as Hallmark and American Greetings, foreign manufacturers who market directly to our customer base, and importers of products produced overseas, may be able to offer similar products with more favorable pricing, servicing and/or terms of sale or may be able to provide products that more readily meet customer requirements or consumer preferences. Our inability to successfully compete against our competitors could adversely affect our business, results of operations and financial condition.

5

Our business, results of operations and financial condition may be adversely affected if we are unable to hire and retain sufficient qualified personnel.

Our success depends, to a substantial extent, on the ability, experience and performance of our senior management. In order to hire and retain qualified personnel, including our senior management team, we seek to provide competitive compensation programs. Our inability to retain our senior management team, or our inability to attract and retain qualified replacement personnel, may adversely affect us. We also regularly hire a large number of seasonal employees. Any difficulty we may encounter in hiring seasonal employees may result in significant increases in labor costs, which may have an adverse effect on our business, results of operations and financial condition.

Our business, results of operations and financial condition may be adversely affected if we fail to extend or renegotiate our collective bargaining contract with our labor union, if disputes with our union arise, or if our unionized employees were to engage in a strike, or other work stoppage.

Approximately 90 of our employees at our ribbon manufacturing facility in Hagerstown, Maryland are represented by a labor union. The collective bargaining agreement with the labor union representing the Hagerstown-based production and maintenance employees will expire on December 31, 2017. Although we believe our relations with our employees are satisfactory, no assurance can be given that we will be able to successfully extend or renegotiate our collective bargaining agreement. If we fail to extend or renegotiate our collective bargaining agreement, if disputes with our union arise, or if our unionized workers engage in a strike or other work stoppage, we could incur higher ongoing labor costs or experience a significant disruption of operations, which could have an adverse effect on our business, results of operations and financial condition.

Employee benefit costs may adversely affect our business, results of operations and financial condition.

We seek to provide competitive employee benefit programs to our employees. Employee benefit costs, such as healthcare costs for our eligible and participating employees, may increase significantly at a rate that is difficult to forecast, in part because of the current and/or future impact of federal healthcare legislation on our employer-sponsored medical plans. Higher employee benefit costs could have an adverse effect on our business, results of operations and financial condition.

Our acquisition strategy involves risks, and difficulties in integrating potential acquisitions may adversely affect our business, results of operations and financial condition.

We regularly evaluate potential acquisition opportunities to support, strengthen and grow our business. In fiscal 2015, we completed the acquisitions of substantially all of the business and assets of Carson & Gebel and of Hollywood Ribbon. We cannot be sure that we will be able to locate suitable acquisition candidates, acquire possible acquisition candidates, acquire such candidates on commercially reasonable terms, or integrate acquired businesses successfully. Future acquisitions may require us to incur additional debt and contingent liabilities, which may adversely affect our business, results of operations and financial condition. The process of integrating acquired businesses into our existing operations may result in operating, contract and supply chain difficulties, such as the failure to retain customers or management personnel. Also, prior to our completion of any acquisition, we could fail to discover liabilities of the acquired business for which we may be responsible as a successor owner or operator in spite of any investigation we may make prior to the acquisition. Such difficulties may divert significant financial, operational and managerial resources from our existing operations, and make it more difficult to achieve our operating and strategic objectives. The diversion of management attention, particularly in a difficult operating environment, may adversely affect our business, results of operations and financial condition.

Our strategy to continuously review the efficiency, productivity and competitiveness of our business may result in our decision to divest or close selected operations. Any divesture or closure involves risks, and decisions to divest or close selected operations may adversely affect our business, results of operations and financial condition.

We regularly evaluate the efficiency, productivity and competitiveness of our business, including our competitiveness within our product categories. As part of such review, we also regularly evaluate the efficiency and productivity of our production and distribution facilities. In fiscal 2013, we sold the Halloween portion of our Paper Magic business. In fiscal 2012, we sold the Christmas gift wrap portion of our Cleo business and closed our former gift wrap manufacturing facility that was located in Memphis, Tennessee. If we decide to divest a portion of our business, we cannot be sure that we will be able to locate suitable buyers or that we will be able to complete such divestiture successfully, timely or on commercially reasonable terms. If we decide to close a portion of our business, we cannot be sure of the effect such closure would have on the productivity or effectiveness of the remaining portions of our business, including our ongoing relationships with suppliers and customers, or of the expected success, timing or costs relating to such closure. Activities associated with any divestiture or closure may divert significant financial, operational and managerial resources from our existing operations,

6

and make it more difficult to achieve our operating and strategic objectives. Accordingly, future decisions to divest or close any portion of our business may adversely affect our business, results of operations and financial condition.

Our inability to protect our intellectual property rights, or infringement claims asserted against us by others, may adversely affect our business, results of operations and financial condition.

We have a number of copyrights, patents, tradenames, trademarks and intellectual property licenses which are used in connection with our products. While our operations are not dependent upon any individual copyright, patent, tradename, trademark or intellectual property license, we believe that the collective value of our intellectual property is substantial. We rely upon copyright, patent, tradename and trademark laws in the United States and other jurisdictions and on confidentiality agreements with some of our employees and others to protect our proprietary rights. If our proprietary rights were infringed, our business could be adversely affected. In addition, our activities could infringe upon the proprietary rights of others, who could assert infringement claims against us. We could face costly litigation to defend these claims. If we are unsuccessful in defending such claims, our business, results of operations and financial condition could be adversely affected.

We seek to register certain of our copyrights, patents, tradenames and trademarks in the United States and elsewhere. These registrations could be challenged by others or invalidated through administrative process or litigation. In addition, our confidentiality agreements with some employees or others may not provide adequate protection in the event of unauthorized use or disclosure of our proprietary information, or if our proprietary information otherwise becomes known, or is independently developed by competitors.

Various laws and governmental regulations applicable to a manufacturer or distributor of consumer products may adversely affect our business, results of operations and financial condition.

Our business is subject to numerous federal, state, provincial, local and foreign laws and regulations, including laws and regulations with respect to labor and employment, product safety, including regulations enforced by the United States Consumer Products Safety Commission, import and export activities, the Internet and e-commerce, antitrust issues, taxes, chemical usage, air emissions, wastewater and storm water discharges and the generation, handling, storage, transportation, treatment and disposal of waste materials, including hazardous materials. Although we believe that we are in substantial compliance with all applicable laws and regulations, because legal requirements frequently change and are subject to interpretation, we are unable to predict the ultimate cost of compliance or the consequences of non-compliance with these requirements, or the affect on our operations, any of which may be significant. If we fail to comply with applicable laws and regulations, we may be subject to criminal sanctions or civil remedies, including fines, injunctions, or prohibitions on importing or exporting. A failure to comply with applicable laws and regulations, or concerns about product safety, also may lead to a recall or post-manufacture repair of selected products, resulting in the rejection of our products by our customers and consumers, lost sales, increased customer service and support costs, and costly litigation. There is risk that any claims or liabilities, including product liability claims, relating to such noncompliance may exceed, or fall outside the scope of, our insurance coverage. Further, a failure to comply with applicable laws and regulations with respect to the Internet and e-commerce activities, which cover issues relating to user privacy, data protection, copyrights and consumer protection, may subject us to significant liabilities. We cannot be certain that existing laws or regulations, as currently interpreted or reinterpreted in the future, or future laws or regulations, will not have an adverse effect on our business, results of operations and financial condition.

Our business, results of operations and financial condition may be adversely affected by national or global changes in economic or political conditions.

Our business, results of operations and financial condition may be adversely affected by national or global changes in economic or political conditions, including foreign currency fluctuations and fluctuations in inflation and interest rates, a national or international economic downturn, any future terrorist attacks, acts of war, threats of war, civil unrest, and the national and global military, diplomatic and financial exposure to such attacks or other threats.

Our business, results of operations and financial condition may be adversely affected by our ability to successfully manage our information technology (“IT”) infrastructure.

We rely upon our IT infrastructure to operate our business. If we suffer damage, interruption, or impairment of our IT infrastructure resulting from human error, theft, vandalism, fire, flood, power loss, telecommunications failure, terrorist attacks, a computer virus, hacker attack or a malfunction of an IT application, we could experience substantial operational issues, including loss of data or information, misuse of data or information by a third party, increases in costs, disruption of operations or business interruption. Our inability to successfully manage our IT infrastructure could adversely affect our business, results of operations and financial condition.

7

We are subject to a number of restrictive covenants under our borrowing arrangement, including customary operating restrictions and customary financial covenants. Our business, results of operations and financial condition may be adversely affected if we are unable to maintain compliance with such covenants.

Our borrowing arrangement contains a number of restrictive covenants, including customary operating restrictions that limit our ability to engage in activities such as incurring additional debt, making investments, granting liens on our assets, making capital expenditures, paying dividends and making other distributions on our capital stock, and engaging in mergers, acquisitions, asset sales and repurchases of our capital stock. Under such arrangements, we are also subject to customary financial covenants, including covenants requiring us to maintain our capital expenditures below a maximum permitted amount each year and to keep our tangible net worth and our interest coverage ratio at or above certain minimum levels. Compliance with the financial covenants contained in our borrowing arrangements is based on financial measures derived from our operating results.

If our business, results of operations or financial condition is adversely affected by one or more of the risk factors described above, or other factors described in this annual report on Form 10-K or elsewhere in our filings with the SEC, we may be unable to maintain compliance with these covenants. If we fail to comply with such covenants, our lenders under our borrowing arrangements could stop advancing funds to us under these arrangements and/or demand immediate payment of amounts outstanding under such arrangements. Under such circumstances, we may need to seek alternate financing sources to fund our ongoing operations and to repay amounts outstanding and satisfy our other obligations under our existing borrowing arrangements. Such financing may not be available on favorable terms, if at all. Consequently, we may be restricted in how we fund ongoing operations and strategic initiatives and deploy capital, and in our ability to make acquisitions and to pay dividends. As a result, our business, results of operations and financial condition may be further adversely affected if we are unable to maintain compliance with the covenants under our borrowing arrangements.

If our business, results of operations or financial condition is adversely affected as a result of any of the risk factors described above or elsewhere in this annual report on Form 10-K or our other SEC filings, we may be required to incur financial statement charges, such as asset or goodwill impairment charges, which may, in turn, have a further adverse affect on our results of operations and financial condition.

If our business, results of operations or financial condition are adversely affected by one or more circumstances, such as any one or more of the risk factors above or other factors described in this annual report on Form 10-K and elsewhere in our SEC filings, we then may be required under applicable accounting rules to incur additional charges associated with reducing the carrying value on our financial statements of certain assets, such as goodwill, intangible assets or tangible assets.

Goodwill is subject to an assessment for impairment which must be performed at least annually, or more frequently if events or circumstances indicate that goodwill might be impaired. We perform our required annual assessment as of our fiscal year end. Authoritative guidance provides entities with the option of first assessing qualitative factors to determine whether it is more likely than not that the fair value of a reporting unit is less than its carrying amount. If it is determined, on the qualitative factors, that the fair value of the reporting unit is more likely than not less than the carrying amount, the two step impairment test would be required. The first step of the test compares the fair value of a reporting unit to its carrying amount, including goodwill, as of the date of the test. We use both a market approach and an income approach to determine the fair value of our reporting units because we believe that the use of multiple valuation techniques results in a more accurate indicator of the fair value of each of our reporting units. If the carrying amount of the reporting unit exceeds its fair value, the second step is performed. The second step compares the carrying amount of the goodwill to the implied fair value of the goodwill. If the implied fair value of the goodwill is less than the carrying amount of the goodwill, an impairment loss will be reported.

Other indefinite lived intangible assets, such as our tradenames, also are required to be tested annually for impairment. Authoritative guidance gives an entity the option to first assess qualitative factors to determine whether it is more likely than not that an indefinite-lived intangible asset is impaired. To perform a qualitative assessment, an entity must identify and evaluate changes in economic, industry and entity-specific events and circumstances that could affect the significant inputs used to determine the fair value of an indefinite-lived intangible asset. If the result of the qualitative analysis indicates it is more likely than not that an indefinite-lived intangible asset is impaired, a more detailed fair value calculation will need to be performed which is used to identify potential impairments and to measure the amount of impairment losses to be recognized, if any. We calculate the fair value of our tradenames using a “relief from royalty payments” methodology. We also review long-lived assets, except for goodwill and indefinite lived intangible assets, for impairment when circumstances indicate the carrying value of an asset may not be recoverable. If such assets are considered to be impaired, we will recognize, for impairment purposes, an amount by which the carrying amount of the assets exceeds the fair value of the assets.

If we are required to incur any of the foregoing financial charges, our results of operations and financial condition may be further adversely affected.

8

Item 1B. Unresolved Staff Comments.

None.

9

Item 2. Properties.

The following table sets forth the location and approximate square footage of the Company’s manufacturing and distribution facilities:

Use | Approximate Square Feet | ||||||

Location | Owned | Leased | |||||

Danville, PA | Distribution | 133,000 | — | ||||

Berwick, PA | Manufacturing and distribution | 213,000 | — | ||||

Berwick, PA | Manufacturing and distribution | 220,000 | — | ||||

Berwick, PA | Distribution | 226,000 | — | ||||

Berwick, PA | Distribution | — | 451,000 | ||||

Hagerstown, MD | Manufacturing and distribution | 284,000 | — | ||||

Batesburg, SC | Manufacturing | 229,000 | — | ||||

El Paso, TX | Distribution | — | 100,000 | ||||

Florence, AL | Distribution | — | 180,000 | ||||

Milford, NH | Manufacturing | — | 58,000 | ||||

Total | 1,305,000 | 789,000 | |||||

The Company also owns a former manufacturing facility aggregating approximately 253,000 square feet which it is in the process of selling, and utilizes owned and leased space aggregating approximately 160,000 square feet for various marketing and administrative purposes, including approximately 9,000 square feet utilized as an office and showroom in Hong Kong. The headquarters and principal executive office of the Company are located in Philadelphia, Pennsylvania.

Item 3. Legal Proceedings.

CSS and its subsidiaries are involved in ordinary, routine legal proceedings that are not considered by management to be material. In the opinion of Company counsel and management, the ultimate liabilities resulting from such legal proceedings will not materially affect the consolidated financial position of the Company or its results of operations or cash flows.

Item 4. Mine Safety Disclosures.

Not applicable.

10

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

The common stock of the Company is listed for trading on the New York Stock Exchange. The following table sets forth the high and low sales prices per share of that stock, and the dividends declared per share, for each of the quarters during fiscal 2015 and fiscal 2014.

Fiscal 2015 | Dividends Declared | ||||||||||

High | Low | ||||||||||

First Quarter | $ | 27.28 | $ | 23.05 | $ | 0.15 | |||||

Second Quarter | 27.95 | 23.97 | 0.15 | ||||||||

Third Quarter | 32.62 | 23.92 | 0.15 | ||||||||

Fourth Quarter | 30.50 | 26.87 | 0.18 | ||||||||

Fiscal 2014 | Dividends Declared | ||||||||||

High | Low | ||||||||||

First Quarter | $ | 30.97 | $ | 24.57 | $ | 0.15 | |||||

Second Quarter | 27.91 | 21.82 | 0.15 | ||||||||

Third Quarter | 31.14 | 22.85 | 0.15 | ||||||||

Fourth Quarter | 28.53 | 24.60 | 0.15 | ||||||||

At May 18, 2015, there were approximately 4,960 holders of the Company’s common stock and there were no shares of preferred stock outstanding.

The ability of the Company to pay any cash dividends on its common stock is dependent on the Company’s earnings and cash requirements and is further limited by maintaining compliance with financial covenants contained in the Company’s credit facilities. The Company anticipates that quarterly cash dividends will continue to be paid in the future.

11

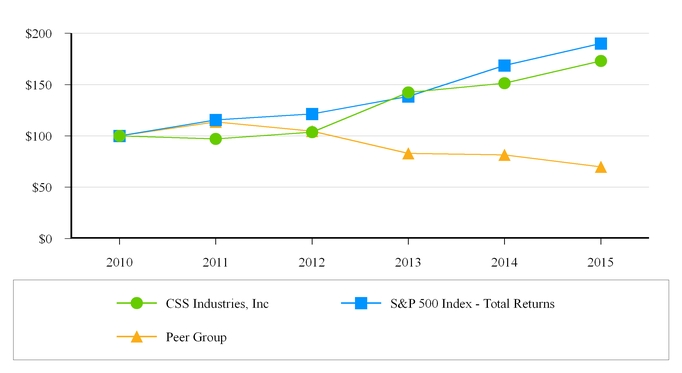

Performance Graph

The graph below compares the cumulative total stockholders’ return on the Company’s common stock for the period from April 1, 2010 through March 31, 2015, with (i) the cumulative total return on the Standard and Poors 500 (“S&P 500”) Index and (ii) a peer group, as described below (assuming the investment of $100 in our common stock, the S&P 500 Index, and the peer group on April 1, 2010 and reinvestment of all dividends).

The peer group utilized consists of Blyth, Inc., Checkpoint Systems, Inc., Ennis, Inc., JAKKS Pacific, Inc. and Lifetime Brands, Inc. (the “Peer Group”). The Company selected this group as its Peer Group because they are engaged in businesses that are sometimes categorized with the Company’s business. However, management believes that a comparison of the Company’s performance to this Peer Group will be flawed, because the businesses of the Peer Group companies are in large part different from the Company’s business. In this regard, Blyth is principally focused on fragranced candle products and related candle accessories, competing only with some of the Company’s products; Lifetime Brands is principally focused on food preparation, tabletop and home décor, competing only with some of the Company’s products; and the other companies principally engage in retail security solutions, printing services or sell juvenile products.

12

Item 6. Selected Financial Data.

Years Ended March 31, | |||||||||||||||||||

2015 | 2014 | 2013 | 2012 | 2011(a)(b) | |||||||||||||||

(in thousands, except per share amounts) | |||||||||||||||||||

Statement of Operations Data: | |||||||||||||||||||

Net sales | $ | 313,044 | $ | 320,459 | $ | 364,193 | $ | 384,663 | $ | 383,660 | |||||||||

Income from continuing operations before income taxes | 26,641 | 27,700 | 22,637 | 25,245 | 26,841 | ||||||||||||||

Income from continuing operations | 16,954 | 18,564 | 15,588 | 16,229 | 17,194 | ||||||||||||||

Income (loss) from discontinued operations, net of tax | — | 205 | (361 | ) | (559 | ) | (11,583 | ) | |||||||||||

Net income | 16,954 | 18,769 | 15,227 | 15,670 | 5,611 | ||||||||||||||

Net income (loss) per common share: | |||||||||||||||||||

Basic: | |||||||||||||||||||

Continuing operations | $ | 1.82 | $ | 1.98 | $ | 1.63 | $ | 1.67 | $ | 1.77 | |||||||||

Discontinued operations | $ | — | $ | 0.02 | $ | (0.04 | ) | $ | (0.06 | ) | $ | (1.19 | ) | ||||||

Total | $ | 1.82 | $ | 2.00 | $ | 1.59 | $ | 1.61 | $ | 0.58 | |||||||||

Diluted: | |||||||||||||||||||

Continuing operations | $ | 1.80 | $ | 1.97 | $ | 1.63 | $ | 1.67 | $ | 1.77 | |||||||||

Discontinued operations | $ | — | $ | 0.02 | $ | (0.04 | ) | $ | (0.06 | ) | $ | (1.19 | ) | ||||||

Total | $ | 1.80 | $ | 1.99 | $ | 1.59 | $ | 1.61 | $ | 0.58 | |||||||||

Balance Sheet Data: | |||||||||||||||||||

Working capital | $ | 194,422 | $ | 187,809 | $ | 175,057 | $ | 163,294 | $ | 145,814 | |||||||||

Total assets | 309,473 | 293,535 | 289,180 | 286,564 | 286,923 | ||||||||||||||

Current portion of long-term debt | — | — | — | — | 66 | ||||||||||||||

Stockholders’ equity | 270,255 | 257,216 | 248,978 | 243,203 | 235,659 | ||||||||||||||

Cash dividends declared per common share | $ | 0.63 | $ | 0.60 | $ | 0.60 | $ | 0.60 | $ | 0.60 | |||||||||

(a) | Statement of Operations and Balance Sheet data for 2011 has been adjusted to reclassify the results of operations of the Christmas gift wrap business to discontinued operations. |

(b) | In the fourth quarter of fiscal 2011, the Company recorded a non-cash pre-tax impairment charge of $11,051,000 primarily due to a full impairment of tangible assets in its former Cleo manufacturing facility that was located in Memphis, Tennessee (of which $10,738,000 is recorded in discontinued operations and $313,000 is recorded in continuing operations). The foregoing impairment charge was partially offset by a $3,965,000 tax benefit (of which $3,853,000 is recorded in discontinued operations and $112,000 is recorded in continuing operations). |

13

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Overview

On September 9, 2011, the Company sold the Christmas gift wrap portion of Cleo’s business and certain of its assets relating to such business, including certain equipment, contract rights, customer lists, intellectual property and other intangible assets to Impact. Cleo’s remaining assets, including accounts receivable and inventory, were excluded from the sale. The purchase price was $7,500,000, of which $2,000,000 was paid in cash at closing. The remainder of the purchase price was paid through the issuance by Impact of an unsecured subordinated promissory note, which provided for quarterly payments of interest at 7% and principal payments as follows: $500,000 on March 1, 2012; $2,500,000 on March 1, 2013; and all remaining principal and interest on March 1, 2014. In the fourth quarter of fiscal 2013, the Company received a $2,000,000 principal payment in advance of the March 1, 2014 due date. All interest payments were paid timely and the final principal payment of $500,000 was received in March 2014. The results of operations for the years ended March 31, 2015, 2014 and 2013 reflect the historical operations of the Christmas gift wrap business as discontinued operations. The discussion in this Management’s Discussion and Analysis of Financial Condition and Results of Operations is presented on the basis of continuing operations, unless otherwise stated.

Approximately 62% of the Company’s sales are attributable to all occasion products with the remainder attributable to seasonal (Christmas, Valentine’s Day and Easter) products. Seasonal products are sold primarily to mass market retailers, and the Company has relatively high market share in many of these categories. Most of these markets have shown little growth and in some cases have declined in recent years. The Company continues to confront significant price pressure as its competitors source certain products from overseas and its customers increase direct sourcing from overseas factories. Increasing customer concentration has augmented their bargaining power, which has also contributed to price pressure. In recent fiscal years, the Company experienced lower sales in its boxed greeting card, gift tissue and gift bag lines.

The Company has taken several measures to respond to sales volume, cost and price pressures. The Company believes it continues to have strong core Christmas product offerings which has allowed it to compete effectively in this competitive market. In addition, the Company is pursuing new product initiatives related to seasonal, craft and all occasion products, including new licensed and non-licensed product offerings. CSS continually invests in product and packaging design and product knowledge to assure that it can continue to provide unique added value to its customers. In addition, CSS maintains a purchasing office in Hong Kong to be able to provide alternatively foreign-sourced products at competitive prices. CSS continually evaluates the efficiency and productivity of its North American production and distribution facilities and of its back office operations to maintain its competitiveness.

The seasonal nature of CSS’ business has historically resulted in lower sales levels and operating losses in the first and fourth quarters and comparatively higher sales levels and operating profits in the second and third quarters of the Company’s fiscal year, which ends March 31, thereby causing significant fluctuations in the quarterly results of operations of the Company.

Historically, significant revenue growth at CSS has come through acquisitions. Management anticipates that it will continue to consider acquisitions as a strategy to stimulate growth.

On February 19, 2015, a subsidiary of the Company completed the acquisition of substantially all of the business and assets of Hollywood Ribbon for approximately $12,903,000 in cash, including transaction costs of approximately $121,000. The Company also incurred one time transition costs of approximately $760,000 in fiscal 2015 primarily related to services performed under a transition service agreement and costs related to the relocation of inventory and equipment. Hollywood Ribbon was a manufacturer, distributor and supplier of ribbon, bows and similar products to mass market retailers and national grocery, drug store, party and craft, and discount chains. As of March 31, 2015, a portion of the purchase price is being held in escrow for certain post-closing adjustments and indemnification obligations. The acquisition was accounted for as a purchase, and the excess of cost over preliminary fair value of the net tangible and identifiable intangible assets acquired of $745,000 was recorded as goodwill in the accompanying consolidated balance sheet. For tax purposes, goodwill resulting from this acquisition is deductible.

On May 19, 2014, a subsidiary of the Company completed the acquisition of substantially all of the business and assets of Carson & Gebel Ribbon for approximately $5,173,000 in cash, including transaction costs of approximately $31,000. Carson & Gebel was a manufacturer, distributor and supplier of decorative ribbon and similar products to wholesale florists, packaging distributors and bow manufacturers. Key product categories include cut edge acetate ribbon and velvet ribbon used in everyday and holiday floral arrangements. As of March 31, 2015, a portion of the purchase price is being held in escrow for certain post-closing adjustments and indemnification obligations. The acquisition was accounted for as a purchase, and the excess of cost over preliminary fair value of the net tangible and identifiable intangible assets acquired of $553,000 was

14

recorded as goodwill in the accompanying consolidated balance sheet. For tax purposes, goodwill resulting from this acquisition is deductible.

On September 5, 2012, the Company and its Paper Magic subsidiary sold the Halloween portion of Paper Magic’s business and certain Paper Magic assets relating to such business, including certain tangible and intangible assets associated with Paper Magic’s Halloween business, to Gemmy. Paper Magic’s remaining Halloween assets, including accounts receivable and inventory, were excluded from the sale. Paper Magic retained the right and obligation to fulfill all customer orders for Paper Magic Halloween products (such as Halloween masks, costumes, make-up and novelties) for the Halloween 2012 season. The sale price of $2,281,000 was paid to Paper Magic at closing. The Company incurred $523,000 of transaction costs (included within disposition of product line further discussed in Note 4 to the consolidated financial statements), yielding net proceeds of $1,758,000.

Litigation

CSS and its subsidiaries are involved in ordinary, routine legal proceedings that are not considered by management to be material. In the opinion of Company counsel and management, the ultimate liabilities resulting from such legal proceedings will not materially affect the consolidated financial position of the Company or its results of operations or cash flows.

Results of Operations

Fiscal 2015 Compared to Fiscal 2014

Consolidated net sales for fiscal 2015 decreased to $313,044,000 from $320,459,000 in fiscal 2014. The decrease in net sales was primarily due to lower sales of Christmas cards, gift bags and decorations of $7,628,000, all occasion stationery products of $5,718,000, and all occasion cards of $2,157,000. These sales declines were partially offset by higher sales of floral products of $5,549,000 (largely due to the acquisition of substantially all of the business and assets of Carson & Gebel on May 19, 2014) and gift card holders of $2,161,000.

Cost of sales, as a percentage of net sales, was 68% in fiscal 2015 and 2014.

Selling, general and administrative (“SG&A”) expenses, as a percentage of net sales, was 24% in fiscal 2015 and 23% in fiscal 2014. The increase in SG&A expenses, as a percentage of net sales, was primarily related to costs of approximately $1,111,000 related to a mergers and acquisitions project that was terminated, partially offset by lower commissions.

Interest expense, net was $7,000 in fiscal 2015 compared to $191,000 in fiscal 2014. The decrease in interest expense was primarily due to higher average balances of funds invested in short-term investments, as well as higher rates of return on invested balances, compared to the prior year.

Income from continuing operations before income taxes was $26,641,000, or 9% of net sales, in fiscal 2015 compared to $27,700,000, or 9% of net sales, in fiscal 2014. The decrease was primarily due to the impact of lower sales volume and higher SG&A expenses, as described above.

Income taxes, as a percentage of income from continuing operations before income taxes, were 36% in fiscal 2015 and 33% in 2014. The increase in income taxes, as a percentage of income from continuing operations before income taxes, was primarily attributable to a tax benefit related to the reduction to the property, plant and equipment deferred tax liability recorded in the prior year which did not recur in the current fiscal year.

There was no income from discontinued operations in the fiscal year ended March 31, 2015. Income from discontinued operations, net of tax of $205,000 for the fiscal year ended March 31, 2014 reflects pre-tax income of $117,000 related to the Christmas gift wrap business which was sold on September 9, 2011 and an income tax benefit of $88,000. See further discussion in Notes 1 and 2 to the consolidated financial statements.

Fiscal 2014 Compared to Fiscal 2013

Consolidated net sales for fiscal 2014 decreased to $320,459,000 from $364,193,000 in fiscal 2013. The decrease in net sales was primarily due to lower sales of Halloween products of $29,548,000 as a result of our sale of the Halloween portion of Paper Magic's business on September 5, 2012, and lower sales of all occasion products of $8,521,000 and Christmas products of $4,933,000 compared to fiscal 2013.

15

Cost of sales, as a percentage of net sales, was 68% in fiscal 2014 and 70% in 2013. This favorable decrease was primarily due to sourcing efficiencies and the absence of a write-down of inventory to net realizable value of $1,266,000 related to the sale of the Halloween portion of Paper Magic's business which was recorded in fiscal 2013.

SG&A expenses, as a percentage of net sales, was 23% in fiscal 2014 and 22% in fiscal 2013.

Disposition of product line, net of $5,798,000 recorded in fiscal 2013 primarily relates to costs associated with the sale of the Halloween portion of Paper Magic’s business, including severance of $1,282,000, facility closure costs of $1,375,000, professional fees of $1,341,000, a write-down of assets of $1,370,000 and a reduction of goodwill of $2,711,000. These costs were offset by proceeds received from the sale of $2,281,000. The Company incurred $523,000 of transaction costs, which is included in the aforementioned professional fees, yielding net proceeds of $1,758,000. A portion of the goodwill associated with the Paper Magic reporting unit was allocated to the business being sold. Such allocation was made on the basis of the fair value of the assets being sold relative to the overall fair value of the Paper Magic reporting unit. See Note 4 to the consolidated financial statements for further discussion.

Interest expense, net was $191,000 in fiscal 2014 compared to interest income, net of $51,000 in fiscal 2013. This change was primarily due to interest income received in fiscal 2013 on the note receivable from Impact (issued by Impact as part of its purchase of the Christmas wrap business on September 9, 2011). The outstanding principal balance of such note receivable was reduced to $500,000 during fiscal 2013 and collected in March 2014.

Income from continuing operations before income taxes was $27,700,000, or 9% of net sales, in fiscal 2014 compared to $22,637,000, or 6% of net sales, in fiscal 2013. The increase was primarily due to the reduction in costs associated with the disposition of product line discussed above and favorable margins, partially offset by the impact of lower sales volume.

Income taxes, as a percentage of income from continuing operations before income taxes, were 33% in fiscal 2014 and 31% in 2013. The increase in income taxes in fiscal 2014 was primarily attributable to a lower benefit related to the changes in tax reserves and valuation allowance of approximately 5%, partially offset by the absence of the unfavorable impact of approximately 3% related to the portion of the goodwill reduction being non-deductible for tax purposes in fiscal 2013.

Income from discontinued operations, net of tax for the fiscal year ended March 31, 2014 was $205,000 compared to a loss from discontinued operations, net of tax of $361,000 for the fiscal year ended March 31, 2013. Income from discontinued operations, net of tax of $205,000 for the fiscal year ended March 31, 2014 reflects pre-tax income of $117,000 related to the Christmas gift wrap business which was sold on September 9, 2011 and an income tax benefit of $88,000. The loss from discontinued operations, net of tax, of $361,000 for the fiscal year ended March 31, 2013 reflects pre-tax income of $89,000 related to this business offset by income tax expense of $450,000. See further discussion in Notes 1 and 2 to the consolidated financial statements.

Liquidity and Capital Resources

At March 31, 2015 and 2014, the Company had working capital of $194,422,000 and $187,809,000, respectively, and stockholders’ equity of $270,255,000 and $257,216,000, respectively. Operating activities of continuing operations provided net cash of $33,223,000 in fiscal 2015 compared to $28,240,000 in fiscal 2014 and $31,428,000 in fiscal 2013. Net cash provided by operating activities from continuing operations in fiscal 2015 reflects our working capital requirements which resulted in a decrease in accounts receivable of $1,593,000, a decrease in other assets of $1,248,000 and an increase in accounts payable of $2,253,000, offset by an increase in inventory of $2,903,000. Included in fiscal 2015 net income were non-cash charges for depreciation and amortization of $7,878,000 and share-based compensation of $2,038,000. Net cash provided by operating activities from continuing operations in fiscal 2014 reflects our working capital requirements which resulted in a decrease in inventory of $3,346,000, offset by an increase in accounts receivable of $3,972,000 and a decrease in accounts payable of $2,536,000. Included in fiscal 2014 net income were non-cash charges for depreciation and amortization of $7,543,000 and share-based compensation of $1,843,000. Net cash provided by operating activities from continuing operations in fiscal 2013 reflects our working capital requirements which resulted in a decrease in inventory of $8,106,000, an increase in accrued expenses and long-term obligations of $1,802,000 and an increase in accrued income taxes of $1,290,000, offset by a decrease in accounts payable of $4,073,000 and an increase in accounts receivable of $2,952,000. Included in fiscal 2013 net income were non-cash charges for depreciation and amortization of $7,594,000, a reduction in goodwill of $2,711,000 related to the sale of the Halloween portion of Paper Magic’s business, and share-based compensation of $1,783,000.

Our investing activities of continuing operations used net cash of $58,793,000 in fiscal 2015, consisting primarily of the purchase of held-to-maturity investment securities of $69,749,000, purchase of businesses of $15,146,000 and capital expenditures of $3,924,000, partially offset by maturities of investment securities of $30,000,000. In fiscal 2014, our investing activities consisted primarily of the purchase of held-to-maturity investment securities of $29,862,000 and capital expenditures

16

of $5,024,000. In fiscal 2013, our investing activities consisted primarily of capital expenditures of $4,494,000, partially offset by net proceeds of $1,758,000 from the sale of the Halloween portion of Paper Magic’s business.

Our financing activities used net cash of $5,969,000 in fiscal 2015, consisting primarily of payments of cash dividends of $5,878,000. In fiscal 2014, financing activities used net cash of $12,360,000, consisting primarily of payments of cash dividends of $5,637,000 and purchases of treasury stock of $6,634,000. In fiscal 2013, financing activities used net cash of $10,671,000, consisting primarily of payments of cash dividends of $5,731,000 and purchases of treasury stock of $4,864,000.

On December 11, 2012, the Company purchased, under the Company’s stock repurchase program, an aggregate of 80,000 shares of its common stock from a trust established by a director of the Company. The terms of the purchase were negotiated on behalf of the Company by a Special Committee of the Board of Directors consisting of four independent, disinterested directors. The price of $20.00 per share was less than the fair market value of a share of the Company’s common stock on the date of the transaction. The Special Committee unanimously authorized the purchase. The total amount of this transaction was $1,600,000.

Under a stock repurchase program authorized by the Company’s Board of Directors, the Company repurchased 272,655 shares of the Company’s common stock for $6,634,000 in fiscal 2014. There were repurchases of 251,180 shares (inclusive of the 80,000 shares described above) of the Company’s common stock for $4,864,000 (inclusive of the $1,600,000 described above) in fiscal 2013. There were no repurchases of the Company's common stock by the Company in fiscal 2015. As of March 31, 2015, the Company had 200,955 shares remaining available for repurchase under the Board’s authorization.

The Company relies primarily on cash generated from its operations and, if needed, seasonal borrowings are available under its revolving credit facility to meet its liquidity requirements throughout the year. Historically, a significant portion of the Company’s revenues have been seasonal, primarily Christmas related, with approximately 67% of sales recognized in the second and third quarters. As payment for sales of Christmas related products is usually not received until just before or just after the holiday selling season in accordance with general industry practice, working capital has historically increased in the second and third quarters, peaking prior to Christmas and dropping thereafter. The sale of the Christmas gift wrap portion of Cleo’s business and the sale of the Halloween portion of Paper Magic’s business has reduced the Company’s seasonal working capital requirements. Seasonal financing requirements are available under a revolving credit facility with two banks. Reflecting the seasonality of the Company’s business, the maximum credit available at any one time under the credit facility (“Commitment Level”) adjusts to $50,000,000 from February to June (“Low Commitment Period”), $100,000,000 from July to October (“Medium Commitment Period”) and $150,000,000 from November to January (“High Commitment Period”) in each respective year over the term of the facility. The Company has the option to increase the Commitment Level during part of any Low Commitment Period from $50,000,000 to an amount not less than $62,500,000 and not in excess of $125,000,000; provided, however, that the Commitment Level must remain at $50,000,000 for at least three consecutive months during each Low Commitment Period. The Company has the option to increase the Commitment Level during all or part of any Medium Commitment Period from $100,000,000 to an amount not in excess $125,000,000. Fifteen days prior written notice is required for the Company to exercise an option to increase the Commitment Level with respect to a particular Low Commitment Period or Medium Commitment Period. The Company may exercise an option to increase the Commitment Level no more than three times each calendar year. This financing facility is available to fund the Company’s seasonal borrowing needs and to provide the Company with sources of capital for general corporate purposes, including acquisitions as permitted under the revolving credit facility. On March 24, 2015, the Company entered into an amendment to extend the expiration date of its revolving credit facility from March 17, 2016 to March 16, 2020. For information concerning this credit facility, see Note 10 to the consolidated financial statements. At March 31, 2015, there were no borrowings outstanding under the Company’s revolving credit facility.