Attached files

| file | filename |

|---|---|

| 8-K - 8-K - CU Bancorp | d924101d8k.htm |

| Exhibit 99.1

|

CU Bancorp

Investor Presentation

as of March 31, 2015

… a better banking experience

|

|

Forward-Looking Statements

This press release contains certain forward-looking information about CU Bancorp (the “Company”), 1st Enterprise Bank and the combined company after the close of the transaction that is intended to be covered by the safe harbor for “forward looking statements” provided by the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact are forward-looking statements. Such statements involve inherent risks and uncertainties, many of which are difficult to predict and are generally beyond the control of the Company. Forward-looking statements speak only as of the date they are made and we assume no duty to update such statements. We caution readers that a number of important factors could cause actual results to differ materially from those expressed in, implied or projected by, such forward-looking statements. Risks and uncertainties include, but are not limited to: lower than expected revenues; credit quality deterioration or a reduction in real estate values could cause an increase in the allowance for credit losses and a reduction in net earnings; increased competitive pressure among depository institutions; the Company’s ability to complete future acquisitions, successfully integrate such acquired entities, or achieve expected beneficial synergies and/or operating efficiencies within expected time-frames or at all; the possibility that personnel changes will not proceed as planned; the cost of additional capital is more than expected; a change in the interest rate environment reduces net interest margins; asset/liability repricing risks and liquidity risks; legal matters could be filed against the Company and could take longer or cost more than expected to resolve or may be resolved adversely to the Company; general economic conditions, either nationally or in the market areas in which the Company does or anticipates doing business, are less favorable than expected; environmental conditions, including natural disasters and drought, may disrupt our business, impede our operations, negatively impact the values of collateral securing the Company’s loans and leases or impair the ability of our borrowers to support their debt obligations; the economic and regulatory effects of the continuing war on terrorism and other events of war, including the conflicts in the Middle East; legislative or regulatory requirements or changes adversely affecting the Company’s business; changes in the securities markets; regulatory approvals for any capital activities cannot be obtained on the terms expected or on the anticipated schedule; and, other risks that are described in CU Bancorp’s public filings with the U.S. Securities and Exchange Commission (the “SEC”). If any of these risks or uncertainties materializes or if any of the assumptions underlying such forward-looking statements proves to be incorrect, CU Bancorp’s results could differ materially from those expressed in, implied or projected by such forward-looking statements. CU Bancorp assumes no obligation to update such forward-looking statements. For a more complete discussion of risks and uncertainties, investors and security holders are urged to read CU Bancorp’s annual report on Form 10-K, quarterly reports on Form 10-Q and other reports filed by CU Bancorp with the SEC. The documents filed by CU Bancorp with the SEC may be obtained at CU Bancorp’s website at www.cubancorp.com or at the SEC’s website at www.sec.gov. These documents may also be obtained free of charge from CU Bancorp by directing a request to: CU Bancorp c/o California United Bank, 15821 Ventura Boulevard, Suite 100, Encino, CA 91436. Attention: Investor Relations. Telephone 818-257-7700.

2

|

|

Investment Highlights

Premier community-based, business banking franchise serving attractive Southern California market Strong organic loan growth Attractive low-cost core deposit base Exceptional credit quality Growing visibility in the investment community

Scarcity value of $2.4 billion “pure play” business bank in large and diverse greater Los Angeles market Opportunistic acquirer with successful history of transactions

3

|

|

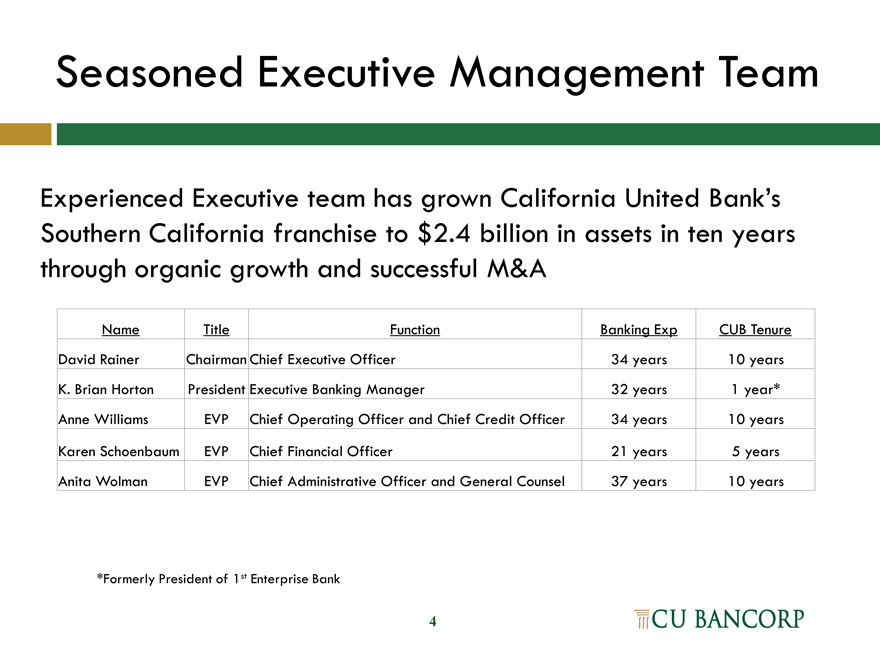

Seasoned Executive Management Team

Experienced Executive team has grown California United Bank’s

Southern California franchise to $2.4 billion in assets in ten years through organic growth and successful M&A

Name Title Function Banking Exp CUB Tenure

David Rainer Chairman Chief Executive Officer 34 years 10 years

K. Brian Horton President Executive Banking Manager 32 years 1 year*

Anne Williams EVP Chief Operating Officer and Chief Credit Officer 34 years 10 years

Karen Schoenbaum EVP Chief Financial Officer 21 years 5 years

Anita Wolman EVP Chief Administrative Officer and General Counsel 37 years 10 years

*Formerly President of 1st Enterprise Bank

4

|

|

Relationship Banking Strategy Creates Competitive Advantage

High-touch relationship management team offers what we consider

“a better banking experience” for small- and medium-sized businesses

Personalized and responsive service – no “800” number, customer service delivered by dedicated relationship managers

Majority of new customers come from larger banks, unhappy with service

Most new business results from “warm leads” provided by referrals

Expertise in, and focus on, business banking

C&I and owner-occupied commercial real estate are 52% of loan portfolio ? Non-interest bearing deposits are 53% of total deposits

Strong credit culture maintains solid asset quality

NPAs to total assets of 0.24% at March 31, 2015

Positioned in extraordinary market

Current 10-branch footprint covers one of the largest and most attractive metropolitan areas in the U.S.

5

|

|

Southern California is an Exceptional Environment for Middle-Market Commercial Banking

The L.A. Basin (Los Angeles, Orange, Riverside, San Bernardino and Ventura counties) is the 16th largest economy in the world1, behind Spain and Mexico and ahead of the Netherlands, Indonesia and Turkey

Los Angeles County is the largest manufacturing center in the U.S. and would be 9th largest state in U.S. by population

Los Angeles County expected to add more than 150,000 jobs over the next two years; March 2015 unemployment rate of 7.2% projected to fall to 7.0% by end of 20152

Orange County would be 31st largest state in U.S. by population

Orange County unemployment rate is 4.4% as of March 20152

Four-county area is home to more than 606,298 small- and middle-market businesses3 (defined as employing 1 to 499 workers)

Our typical customer has between $10 and $60 million in annual sales ? Typical loan commitment ranges from $1 million to $5 million (excluding SBA) ? Significant percentage of customers in the manufacturing, distribution and services industries

1) Source: IMF World Economic Outlook (WEO), Oct. 7, 2014

2) Source: Forecast by Los Angeles County Economic Development Corp,; actual unemployment rates from Bureau of Labor and Statistics (BLS)

3) Source: County data from Los Angeles Economic Development Corp. and California EDD, as of 9/30/13

6

|

|

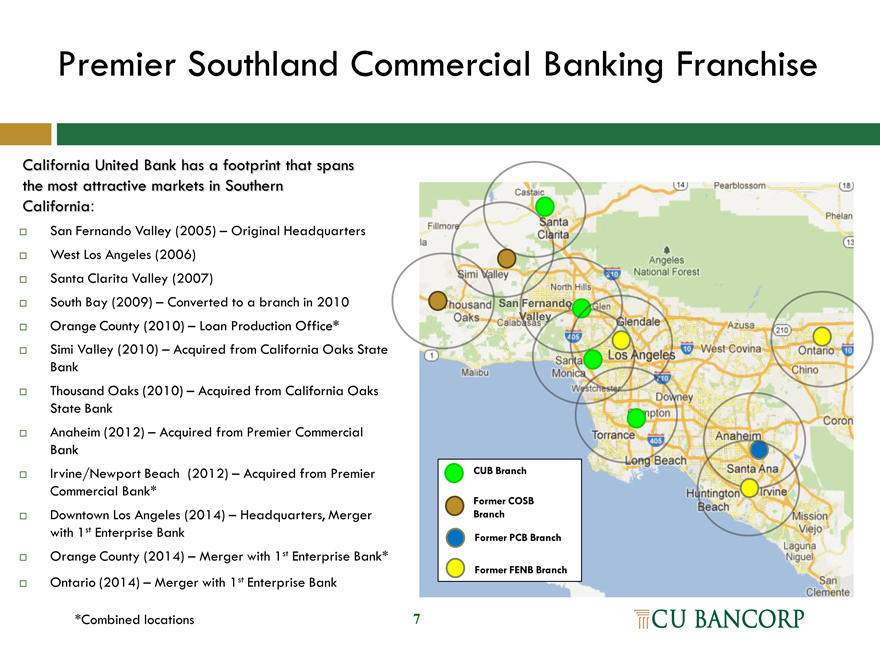

Premier Southland Commercial Banking Franchise

California United Bank has a footprint that spans the most attractive markets in Southern California:

San Fernando Valley (2005) – Original Headquarters West Los Angeles (2006) Santa Clarita Valley (2007) South Bay (2009) – Converted to a branch in 2010 Orange County (2010) – Loan Production Office* Simi Valley (2010) – Acquired from California Oaks State Bank Thousand Oaks (2010) – Acquired from California Oaks State Bank Anaheim (2012) – Acquired from Premier Commercial Bank Irvine/Newport Beach (2012) – Acquired from Premier Commercial Bank* Downtown Los Angeles (2014) – Headquarters, Merger with 1st Enterprise Bank Orange County (2014) – Merger with 1st Enterprise Bank* Ontario (2014) – Merger with 1st Enterprise Bank

*Combined locations

San Fernando Valley

CUB Branch

Former COSB Branch

Former PCB Branch

Former FENB Branch

7

|

|

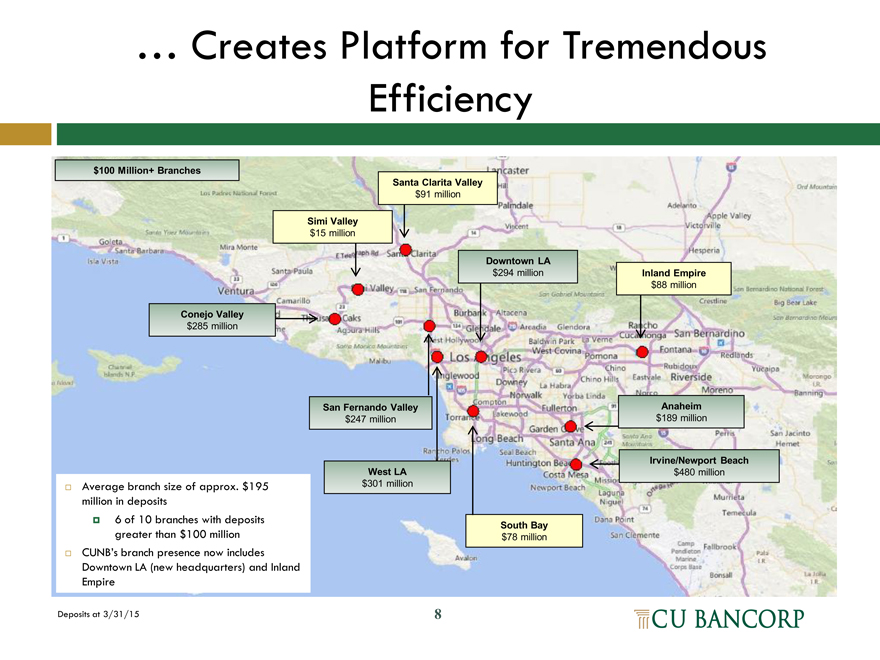

… Creates Platform for Tremendous

Efficiency

$100 Million+ Branches

Santa Clarita Valley $91 million

Simi Valley $15 million

Downtown LA $294 million Inland Empire $88 million

Conejo Valley $285 million

San Fernando Valley Anaheim $247 million $189 million

Irvine/Newport Beach

West LA $480 million

size of approx. $195 $301 million Average branch million in deposits 6 of 10 branches with deposits

South Bay

greater than $100 million $78 million

CUNB’s branch presence now includes

Downtown LA (new headquarters) and Inland Empire

Deposits at 3/31/15

8

|

|

Strategy for High Quality Growth

Strong and Ongoing Organic Growth

Establish a highly desirable footprint in region with tremendous opportunities for growth ? Leverage relationship-based banking approach and superior service

Recruit experienced and connected “in market” talent

Build on products and expertise acquired in strategic acquisitions, such as the SBA lending platform obtained with Premier Commercial Bank ? Strong capital management ? Result: Asset CAGR of 41% from inception in 2005 through 2014

Growth by Opportunistic Merger/Acquisition

Strong management team experienced with strategic, successful acquisitions ? Focus on in-market and adjacent market acquisitions and mergers ? Immediately accretive to earnings ? Tangible book value payback under four years ? Result: Successfully completed three transactions since 2010

9

|

|

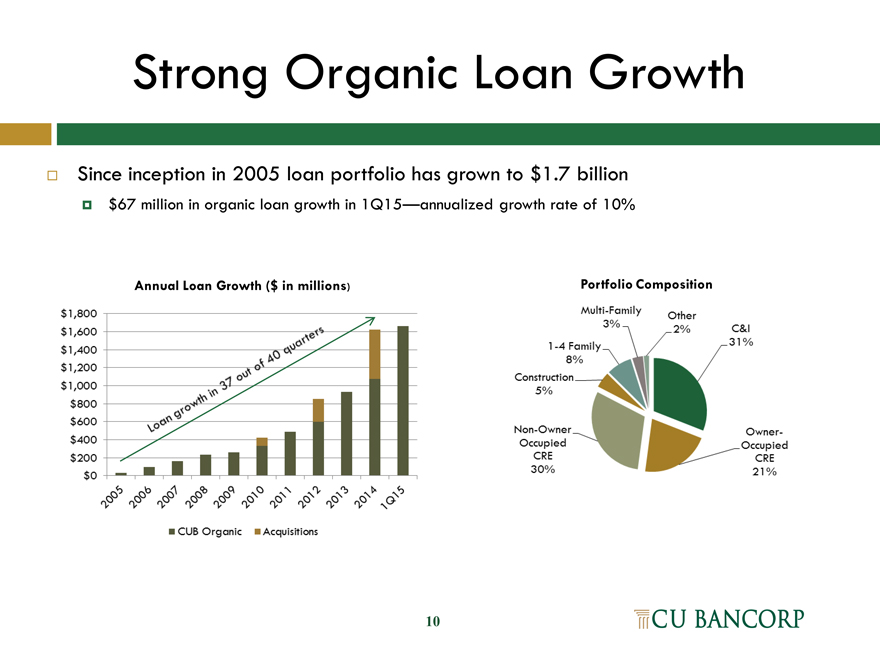

Strong Organic Loan Growth

Since inception in 2005 loan portfolio has grown to $1.7 billion

? $67 million in organic loan growth in 1Q15—annualized growth rate of 10%

Annual Loan Growth ($ in millions)

Portfolio Composition

10

|

|

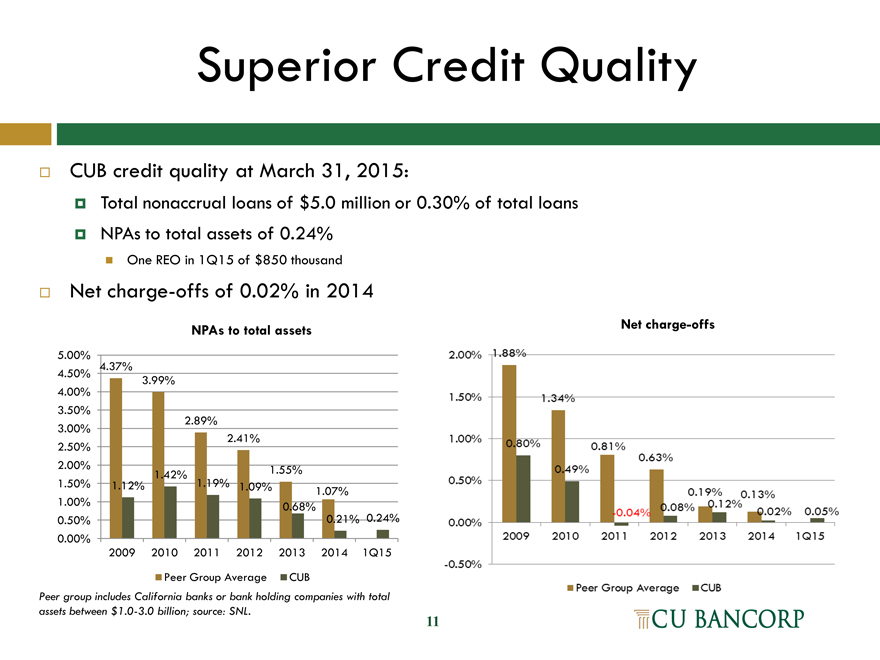

Superior Credit Quality

CUB credit quality at March 31, 2015:

Total nonaccrual loans of $5.0 million or 0.30% of total loans ? NPAs to total assets of 0.24%

One REO in 1Q15 of $850 thousand

Net charge-offs of 0.02% in 2014

NPAs to total assets

NPAs to total assets

5.00%

4.37% 4.50%

3.99% 4.00%

3.50% 2.89% 3.00%

2.41% 2.50%

2.00% 1.55% 1.42% 1.50% 1.12% 1.19% 1.09%

1.00% 1.07% 0.68%

0.50% 0.21% 0.24% 0.00% 2009 2010 2011 2012 2013 2014 1Q15

Net charge-offs

Peer group includes California banks or bank holding companies with total assets between $1.0-3.0 billion; source: SNL.

11

|

|

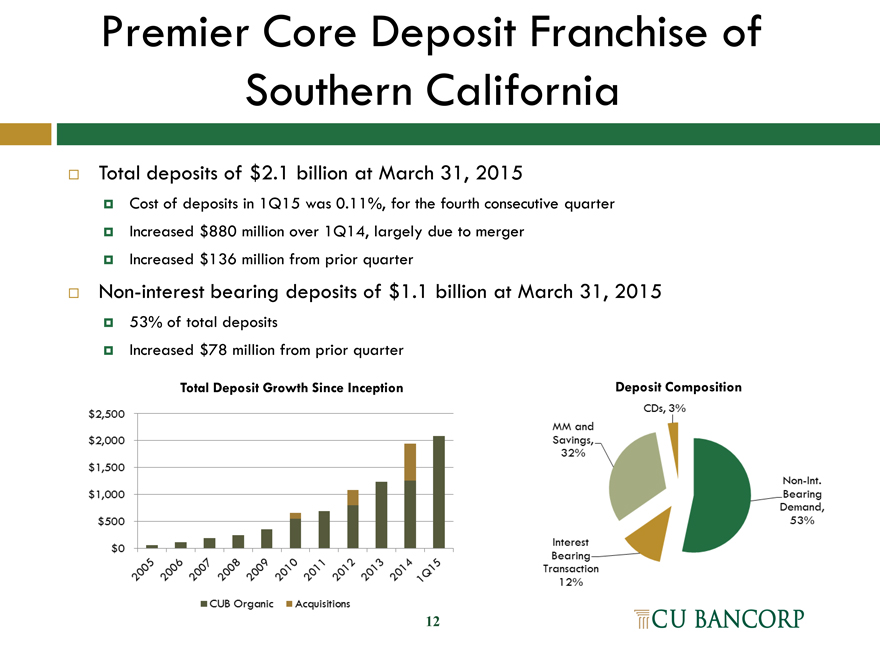

Premier Core Deposit Franchise of Southern California

Total deposits of $2.1 billion at March 31, 2015

Cost of deposits in 1Q15 was 0.11%, for the fourth consecutive quarter ? Increased $880 million over 1Q14, largely due to merger ? Increased $136 million from prior quarter

Non-interest bearing deposits of $1.1 billion at March 31, 2015

53% of total deposits

Increased $78 million from prior quarter

Total Deposit Growth Since Inception

Deposit Composition

12

|

|

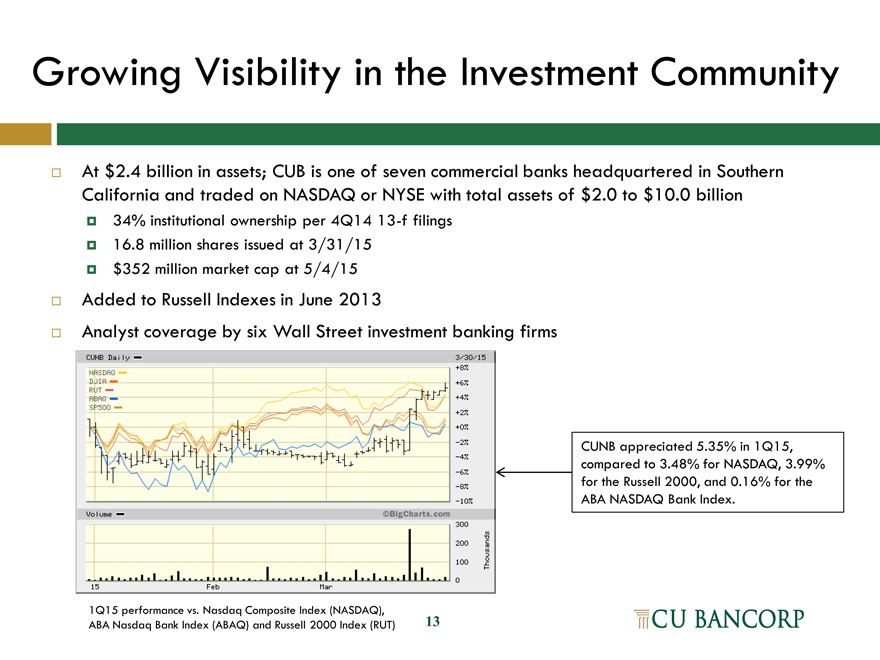

Growing Visibility in the Investment Community

At $2.4 billion in assets; CUB is one of seven commercial banks headquartered in Southern California and traded on NASDAQ or NYSE with total assets of $2.0 to $10.0 billion

? 34% institutional ownership per 4Q14 13-f filings ? 16.8 million shares issued at 3/31/15 ? $352 million market cap at 5/4/15

Added to Russell Indexes in June 2013

Analyst coverage by six Wall Street investment banking firms

1Q15 performance vs. Nasdaq Composite Index (NASDAQ), ABA Nasdaq Bank Index (ABAQ) and Russell 2000 Index (RUT)

CUNB appreciated 5.35% in 1Q15, compared to 3.48% for NASDAQ, 3.99% for the Russell 2000, and 0.16% for the ABA NASDAQ Bank Index.

13

|

|

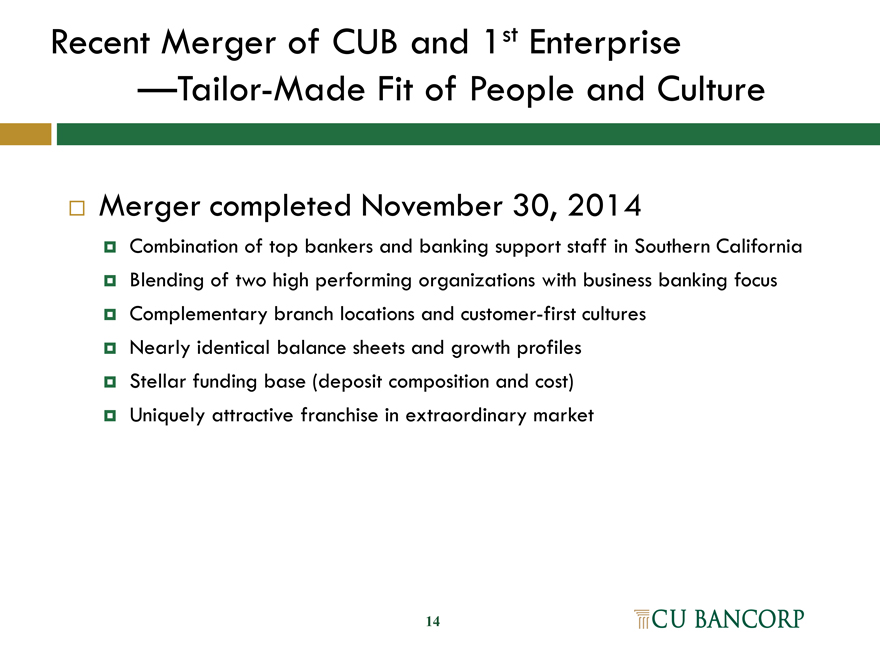

Recent Merger of CUB and 1st Enterprise —Tailor-Made Fit of People and Culture

Merger completed November 30, 2014

? Combination of top bankers and banking support staff in Southern California ? Blending of two high performing organizations with business banking focus ? Complementary branch locations and customer-first cultures ? Nearly identical balance sheets and growth profiles ? Stellar funding base (deposit composition and cost) ? Uniquely attractive franchise in extraordinary market

14

|

|

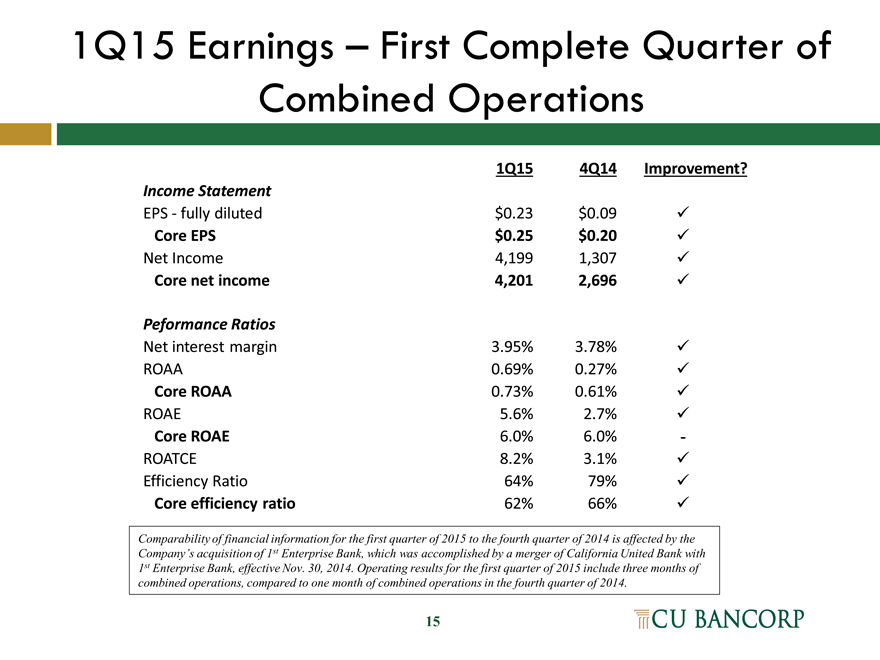

1Q15 Earnings – First Complete Quarter of Combined Operations

1Q15 4Q14 Improvement?

Income Statement

EPS—fully diluted $0.23 $0.09 ?

Core EPS $0.25 $0.20 ?

Net Income 4,199 1,307 ?

Core net income 4,201 2,696 ?

Peformance Ratios

Net interest margin 3.95% 3.78% ?

ROAA 0.69% 0.27% ?

Core ROAA 0.73% 0.61% ?

ROAE 5.6% 2.7% ?

Core ROAE 6.0% 6.0% -

ROATCE 8.2% 3.1% ?

Efficiency Ratio 64% 79% ?

Core efficiency ratio 62% 66% ?

Comparability of financial information for the first quarter of 2015 to the fourth quarter of 2014 is affected by the Company’s acquisition of 1st Enterprise Bank, which was accomplished by a merger of California United Bank with 1st Enterprise Bank, effective Nov. 30, 2014. Operating results for the first quarter of 2015 include three months of combined operations, compared to one month of combined operations in the fourth quarter of 2014.

15

|

|

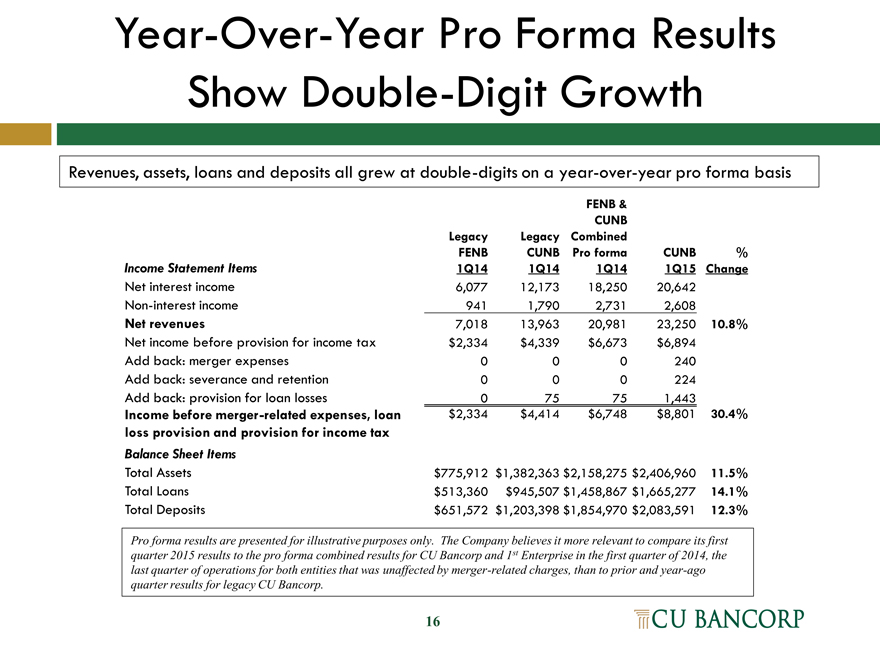

Year-Over-Year Pro Forma Results Show Double-Digit Growth

Revenues, assets, loans and deposits all grew at double-digits on a year-over-year pro forma basis

FENB &

CUNB

Legacy Legacy Combined

FENB CUNB Pro forma CUNB %

Income Statement Items 1Q14 1Q14 1Q14 1Q15 Change

Net interest income 6,077 12,173 18,250 20,642

Non-interest income 941 1,790 2,731 2,608

Net revenues 7,018 13,963 20,981 23,250 10.8%

Net income before provision for income tax $2,334 $4,339 $6,673 $6,894

Add back: merger expenses 0 0 0 240

Add back: severance and retention 0 0 0 224

Add back: provision for loan losses 0 75 75 1,443

Income before merger -related expenses, loan $2,334 $4,414 $6,748 $8,801 30.4%

loss provision and provision for income tax

Balance Sheet Items

Total Assets $775,912 $1,382,363 $2,158,275 $2,406,960 11.5%

Total Loans $513,360 $945,507 $1,458,867 $1,665,277 14.1%

Total Deposits $651,572 $1,203,398 $1,854,970 $2,083,591 12.3%

Pro forma results are presented for illustrative purposes only. The Company believes it more relevant to compare its first quarter 2015 results to the pro forma combined results for CU Bancorp and 1st Enterprise in the first quarter of 2014, the last quarter of operations for both entities that was unaffected by merger-related charges, than to prior and year-ago quarter results for legacy CU Bancorp.

16

|

|

Appendix

17

|

|

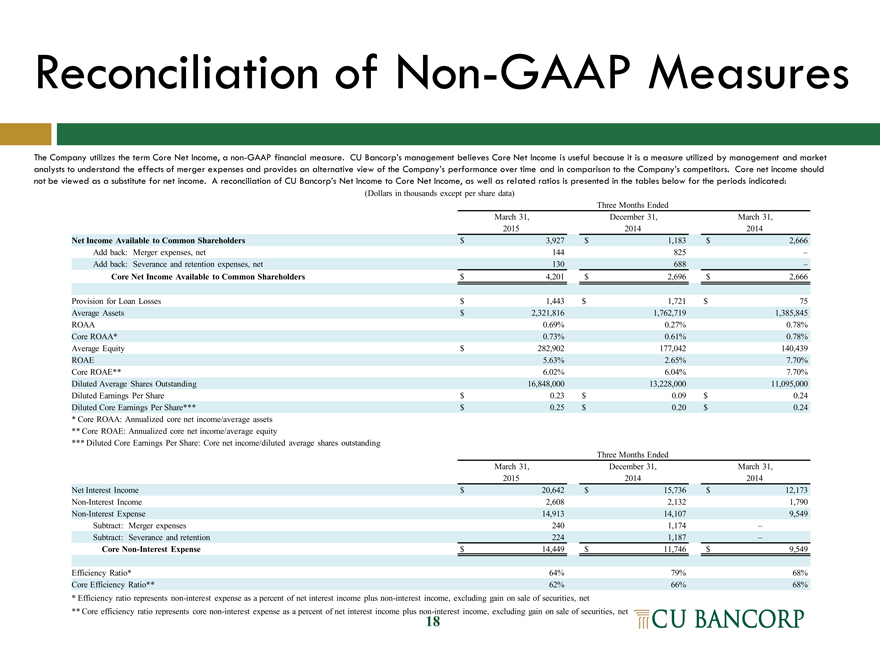

Reconciliation of Non-GAAP Measures

The Company utilizes the term Core Net Income, a non-GAAP financial measure. CU Bancorp’s management believes Core Net Income is useful because it is a measure utilized by management and market

analysts to understand the effects of merger expenses and provides an alternative view of the Company’s performance over time and in comparison to the Company’s competitors. Core net income should

not be viewed as a substitute for net income. A reconciliation of CU Bancorp’s Net Income to Core Net Income, as well as related ratios is presented in the tables below for the periods indicated:

(Dollars in thousands except per share data)

Three Months Ended

March 31, December 31, March 31,

2015 2014 2014

Net Income Available to Common Shareholders $ 3,927 $ 1,183 $ 2,666

Add back: Merger expenses, net 144 825 –

Add back: Severance and retention expenses, net 130 688 –

Core Net Income Available to Common Shareholders $ 4,201 $ 2,696 $ 2,666

Provision for Loan Losses $ 1,443 $ 1,721 $ 75

Average Assets $ 2,321,816 1,762,719 1,385,845

ROAA 0.69% 0.27% 0.78%

Core ROAA* 0.73% 0.61% 0.78%

Average Equity $ 282,902 177,042 140,439

ROAE 5.63% 2.65% 7.70%

Core ROAE** 6.02% 6.04% 7.70%

Diluted Average Shares Outstanding 16,848,000 13,228,000 11,095,000

Diluted Earnings Per Share $ 0.23 $ 0.09 $ 0.24

Diluted Core Earnings Per Share*** $ 0.25 $ 0.20 $ 0.24

* Core ROAA: Annualized core net income/average assets

** Core ROAE: Annualized core net income/average equity

*** Diluted Core Earnings Per Share: Core net income/diluted average shares outstanding Three Months Ended

March 31, December 31, March 31,

2015 2014 2014

Net Interest Income $ 20,642 $ 15,736 $ 12,173

Non-Interest Income 2,608 2,132 1,790

Non-Interest Expense 14,913 14,107 9,549

Subtract: Merger expenses 240 1,174 –

Subtract: Severance and retention 224 1,187 –

Core Non-Interest Expense $ 14,449 $ 11,746 $ 9,549

Efficiency Ratio* 64% 79% 68%

Core Efficiency Ratio** 62% 66% 68%

* Efficiency ratio represents non-interest expense as a percent of net interest income plus non-interest income, excluding gain on sale of securities, net

** Core efficiency ratio represents core non-interest expense as a percent of net interest income plus non-interest income, excluding gain on sale of securities, net

18

|

|

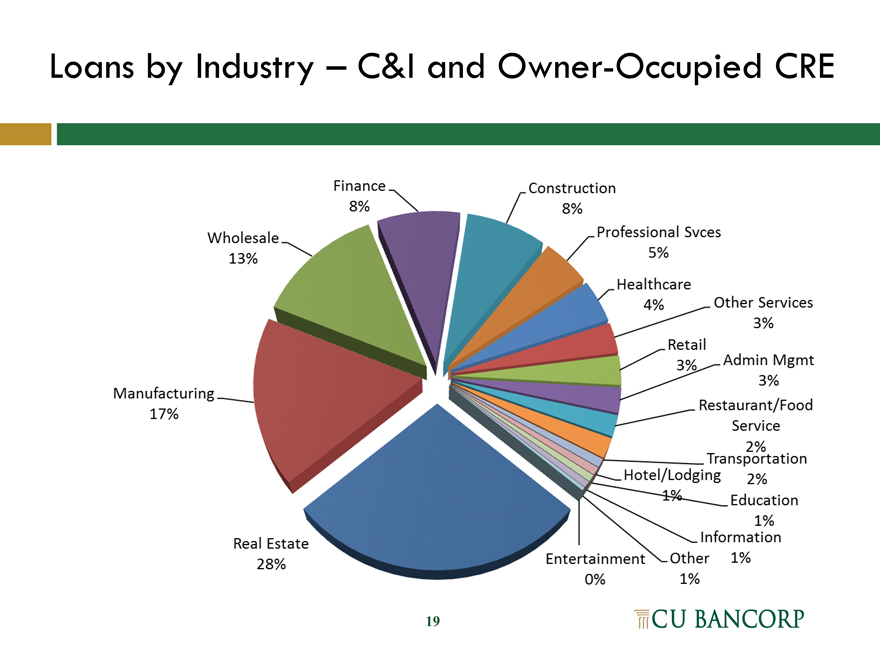

Loans by Industry – C&I and Owner-Occupied CRE

Finance 8% Construction 8% Professional Svces 5% Health care 4% Other Services 3% Retail 3% Admin Mgmt 3% Restaurant/Food Service 2% Transportation 2% Hotel/Lodging 1% Education 1% Information 1% Other 1% Entertainment 0% Real Estate 28% Manufacturing 17% Wholesale 13%

19

|

|

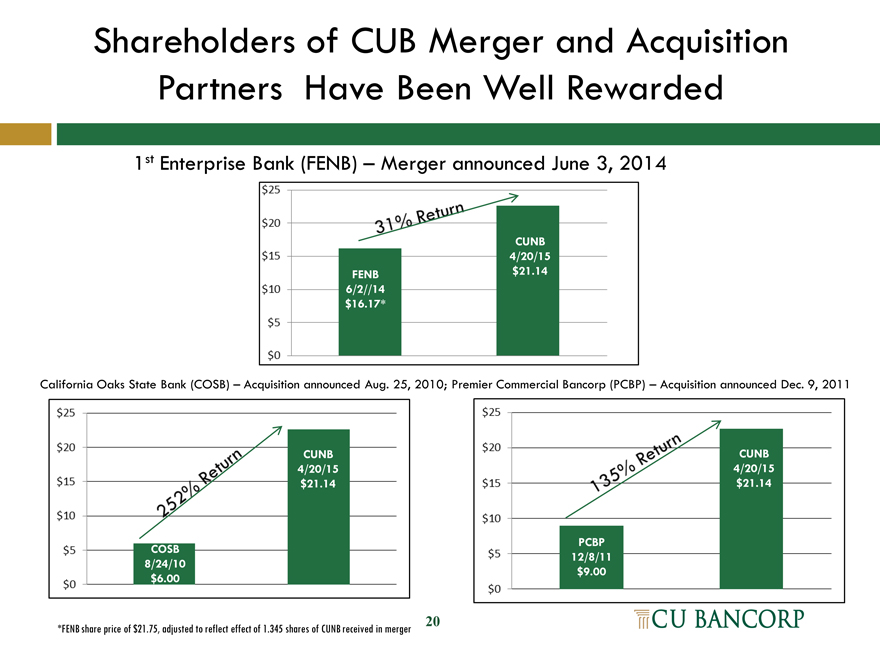

Shareholders of CUB Merger and Acquisition Partners Have Been Well Rewarded

1st Enterprise Bank (FENB) – Merger announced June 3, 2014

$25 20 $15 $10 $5 $0

31% Return

CUNB 4/20/15 FENB $21.14 6/2//14 $16.17*

California Oaks State Bank (COSB) – Acquisition announced Aug. 25, 2010; Premier Commercial Bancorp (PCBP) – Acquisition announced Dec. 9, 2011

$25 20 $15 $10 $5 $0

252% Return

CUNB

4/20/15

$21.14

COSB

8/24/10

$6.00

$25 20 $15 $10 $5 $0

135% Return

CUNB

4/20/15

$21.14

PCBP

12/8/11

$9.00

*FENB share price of $21.75, adjusted to reflect effect of 1.345 shares of CUNB received in merger

20