Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - AUGUSTA GOLD CORP. | Financial_Report.xls |

| EX-31 - AUGUSTA GOLD CORP. | bfgc20150331_ex31.htm |

| EX-32 - AUGUSTA GOLD CORP. | bfgc20150331_ex32.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________________

FORM 10-Q

(Mark One)

| x | QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For quarterly period ended March 31, 2015

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________ to ___________

Commission File Number 333-164908

BULLFROG GOLD CORP.

(Exact name of registrant as specified in its charter)

| Delaware | 41-2252162 |

| (State or other jurisdiction of | (I.R.S. Employer |

| incorporation or organization) | Identification No.) |

| 897 Quail Run Drive | |

| Grand Junction, Colorado | 81505 |

| (Address of principal executive offices) | (Zip Code) |

(970) 628-1670

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o | ||

| Non-accelerated filer (Do not check if a smaller reporting company) | o | Smaller reporting company | x |

Indicate by check mark whether the registrant is a shell company (as defined in 12b-2 of the Exchange Act.) Yes o No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date: 45,741,045 shares of common stock, par value $0.0001, were outstanding on May 1, 2015.

BULLFROG GOLD CORP.

TABLE OF CONTENTS TO FORM 10-Q

| Part I | Financial Information | Page |

| Item 1. | Consolidated Financial Statements (Unaudited) | 1 |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. | 19 |

| Item 3. | Quantitative and Qualitative Disclosures about Market Risk. | 31 |

| Item 4. | Controls and Procedures. | 31 |

| Part II | OTHER INFORMATION | |

| Item 1. | Legal Proceedings | 32 |

| Item 1A. | Risk Factors | 32 |

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 32 |

| Item 3. | Defaults Upon Senior Securities | 32 |

| Item 4. | Mine Safety Disclosures | 32 |

| Item 5. | Other Information | 32 |

| Item 6. | Exhibits | 32 |

| Signatures | 33 | |

| Exhibit 31 | Section 302 Certification of President, Chief Executive Officer and Chief Financial Officer | EX31 |

| Exhibit 32 | Section 906 Certification of President, Chief Executive Officer and Chief Financial Officer | EX32 |

BULLFROG GOLD CORP.

CONSOLIDATED BALANCE SHEETS

MARCH 31, 2015 AND DECEMBER 31, 2014

(unaudited)

| Assets | 3/31/15 | 12/31/14 | ||||||

| Current assets | ||||||||

| Cash | $ | 821 | $ | 790 | ||||

| Deposits | 10,682 | 10,682 | ||||||

| Total current assets | 11,503 | 11,472 | ||||||

| Other assets | ||||||||

| Mineral properties | 246,300 | 246,300 | ||||||

| Deferred financing fees | 11,916 | 14,666 | ||||||

| Total other assets | 258,216 | 260,966 | ||||||

| Total assets | $ | 269,719 | $ | 272,438 | ||||

| Liabilities and Stockholders' Equity (Deficit) | ||||||||

| Current liabilities | ||||||||

| Accounts payable | $ | 34,850 | $ | 22,856 | ||||

| Related party payable | 286,403 | 209,013 | ||||||

| Note payable | 2,590,752 | 2,544,598 | ||||||

| Other liabilities | — | 84 | ||||||

| Total current liabilities | 2,912,005 | 2,776,551 | ||||||

| Long term liabilities | ||||||||

| Accrued interest | 25,212 | 18,336 | ||||||

| Warrant liability | 112 | 20 | ||||||

| Note payable | 220,000 | 220,000 | ||||||

| Total long term liabilities | 245,324 | 238,356 | ||||||

| Total liabilities | 3,157,329 | 3,014,907 | ||||||

| Stockholders' equity (deficit) | ||||||||

| Preferred stock, 50,000,000 shares authorized, $.0001 par value; Series B 400,000 issued and outstanding as of 3/31/15 and 12/31/14, respectively | 40 | 40 | ||||||

| Common stock, 200,000,000 shares authorized, $ .0001 par value; 45,741,045 shares issued and outstanding as of 3/31/15 and 12/31/14, respectively | 4,574 | 4,574 | ||||||

| Additional paid in capital | 6,336,512 | 6,258,467 | ||||||

| Accumulated deficit | (9,228,736 | ) | (9,005,550 | ) | ||||

| Total stockholders' equity (deficit) | (2,887,610 | ) | (2,742,469 | ) | ||||

| Total liabilities and stockholders' equity (deficit) | $ | 269,719 | $ | 272,438 |

See accompanying notes to consolidated financial statements

| 1 |

BULLFROG GOLD CORP.

CONSOLIDATED STATEMENTS OF OPERATIONS

FOR THE THREE MONTHS ENDED MARCH 31, 2015 AND 2014

(unaudited)

| Three Months Ended | ||||||||

| 3/31/15 | 3/31/14 | |||||||

| Revenue | $ | — | $ | — | ||||

| Operating expenses | ||||||||

| General and administrative | 167,315 | 145,012 | ||||||

| Exploration costs | — | 82,904 | ||||||

| Marketing | — | 2,796 | ||||||

| Total operating expenses | 167,315 | 230,712 | ||||||

| Net operating loss | (167,315 | ) | (230,712 | ) | ||||

| Gain on extinguishment of debt | — | 15,500 | ||||||

| Interest expense | (55,779 | ) | (212,845 | ) | ||||

| Revaluation of warrant liability | (92 | ) | 180,525 | |||||

| Net loss | $ | (223,186 | ) | $ | (247,532 | ) | ||

| Weighted average common shares outstanding – basic and diluted | 45,741,045 | 44,991,045 | ||||||

| Loss per common share – basic and diluted | $ | (0.00 | ) | $ | (0.01 | ) | ||

See accompanying notes to consolidated financial statements

| 2 |

BULLFROG GOLD CORP.

CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE THREE MONTHS ENDED MARCH 31, 2015 AND 2014

(unaudited)

| Three Months Ended | ||||||||

| 3/31/15 | 3/31/14 | |||||||

| Cash flows from operating activities | ||||||||

| Net loss | $ | (223,186 | ) | $ | (247,532 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities | ||||||||

| Gain on extinguishment of debt | — | (15,500 | ) | |||||

| Capitalized interest to note payable | 46,154 | — | ||||||

| Revaluation of warrant liability | 92 | (180,525 | ) | |||||

| Stock-based compensation | 78,045 | — | ||||||

| Amortization of deferred financing fees | 2,750 | 163,449 | ||||||

| Change in operating assets and liabilities: | ||||||||

| Prepaid expenses | — | 7,437 | ||||||

| Accounts payable | 11,994 | (37,540 | ) | |||||

| Related party payable | 77,390 | 634 | ||||||

| Accrued interest | 6,876 | |||||||

| Other liabilities | (84 | ) | — | |||||

| Net cash used in operating activities | 31 | (309,577 | ) | |||||

| Cash flows from financing activity | ||||||||

| Proceeds from notes payable | — | 300,000 | ||||||

| Net cash provided by financing activity | — | 300,000 | ||||||

| Net increase (decrease) in cash | 31 | (9,577 | ) | |||||

| Cash, beginning of period | 790 | 207,332 | ||||||

| Cash, end of period | $ | 821 | $ | 197,755 | ||||

| Supplemental disclosure of cash flow information | ||||||||

| Cash paid during period for interest | $ | — | $ | 49,396 | ||||

See accompanying notes to consolidated financial

statements

| 3 |

BULLFROG GOLD CORP.

Notes to Consolidated Financial Statements

(unaudited)

NOTE 1 – NATURE OF BUSINESS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Nature of Business

Bullfrog Gold Corp. (the “Company”, “we”, “our”) is a junior exploration company engaged in the acquisition and exploration of properties that may contain gold, silver and other metals in the United States. The Company’s target properties are those that have been the subject of historical exploration. The Company owns, controls or has acquired mineral rights on Federal patented and unpatented mining claims in the state of Nevada for the purpose of exploration and potential development of gold, silver and other metals on a total of approximately 4,380 acres. The Company plans to review opportunities and acquire additional mineral properties with current or historic precious and base metal mineralization with meaningful exploration potential.

The Company’s properties do not have any reserves. The Company plans to conduct exploration programs on these properties with the objective of ascertaining whether any of its properties contain economic concentrations of precious and base metals that are prospective for mining.

Basis of Presentation

The consolidated unaudited financial statements included in this Form 10-Q have been prepared in accordance with generally accepted accounting principles in the United States of America for interim financial information and with the instructions to Form 10-Q. Accordingly, these financial statements do not include all of the disclosures required by U.S. generally accepted accounting principles for complete financial statements. These consolidated unaudited interim financial statements should be read in conjunction with the audited financial statements for the fiscal year ended December 31, 2014 in our Annual Report on Form 10-K. The financial information furnished herein reflects all adjustments consisting of normal, recurring adjustments which, in the opinion of management, are necessary for a fair presentation of our financial position, the results of operations and cash flows for the periods presented. Operating results for the three months ended March 31, 2015 are not necessarily indicative of results for future quarters or periods in the fiscal year ending December 31, 2015.

Principles of Consolidation

The consolidated financial statements include the accounts of Bullfrog Gold Corp. and its wholly owned subsidiaries, Standard Gold Corp. (“Standard Gold”) a Nevada corporation and Rocky Mountain Minerals Corp. (“Rocky Mountain Minerals”) a Nevada corporation. All significant inter-entity balances and transactions have been eliminated in consolidation.

Going Concern and Management’s Plans

The Company has incurred losses from operations since inception and has an accumulated deficit of approximately $9,229,000 as of March 31, 2015. Additionally, the Company had negative working capital of approximately $2,901,000 at March 31, 2015. The Company’s financial statements have been prepared on the basis that it is a going concern, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. The Company’s continuation as a going concern is dependent upon attaining profitable operations through achieving revenue growth.

The Company has no revenues and does not expect to have revenues in 2015. Should we be unable to continue as a going concern, we may be unable to realize the carrying value of our assets and to meet our obligations as they become due. To continue as a going concern, we are dependent on continued fund raising. However, we have no commitment from any party to provide additional capital and there is no

| 4 |

assurance that such funding will be available when needed, or if available, that its terms will be favorable or acceptable to us. The Company is currently exploring various financing alternatives to refinance or repay the amount outstanding to RMB Australia Holdings Limited (“RMB”). To do so, the Company will have to raise additional funds from external sources. There can be no assurance that additional financing will be available at all or on acceptable terms. If additional financing is not available, we may have to substantially reduce or cease operations. Further, if the Company fails to restructure or refinance its RMB indebtedness or should any of RMB’s indebtedness be accelerated, the Company will not have adequate liquidity to fund its operations, meet its obligations (including its debt payment obligations) and we may not be able to continue as a going concern, and will likely be forced to surrender our ownership interest in the Bullfrog Project as part of the Facility.

Cash and Cash Equivalents and Concentration

The Company considers all highly liquid investments with a maturity of three months or less when acquired to be cash equivalents. The Company places its cash with a high credit quality financial institution. The Company’s account at this institution is insured by the Federal Deposit Insurance Corporation for losses up to $250,000. At March 31, 2015, the Company’s cash balance was approximately $1,000. To reduce its risk associated with the failure of such financial institution, the Company will evaluate at least annually the rating of the financial institution in which it holds deposits.

Use of Estimates

The preparation of consolidated financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Mineral Property Acquisition and Exploration Costs

Mineral property acquisition and exploration costs are expensed as incurred until such time as economic reserves are quantified. To date, the Company has not established any proven or probable reserves on its mineral properties. Costs of lease, exploration, carrying and retaining unproven mineral lease properties are expensed as incurred. The Company has chosen to expense all mineral exploration costs as incurred given that it is still in the exploration stage. Once the Company has identified proven and probable reserves in its investigation of its properties and upon development of a plan for operating a mine, it would enter the development stage and capitalize future costs until production is established. When a property reaches the production stage, the related capitalized costs will be amortized over the estimated life of the probable-proven reserves. When the Company has capitalized mineral properties, these properties will be periodically assessed for impairment of value and any diminution in value. To date, the Company has not established the commercial feasibility of any exploration prospects; therefore, all costs are being expensed. During the three months ended March 31, 2015 and 2014, the Company incurred exploration costs of approximately $0 and $83,000, respectively. Costs of property acquisitions are being capitalized.

The Company entered an Option to Purchase the Newsboy Gold Project in September 2011, at which time the gold price was near $1,900 per ounce. Since then the Company completed four exploration programs that included 27,201 feet of drilling in 160 holes to test potential expansions to an open pit mine proposed in 1992 and at priority exploration targets within 3 miles of the main deposit. An independent technical report was completed in February 2014 that showed the project was not economic under reasonably foreseeable gold prices. Based on that report and option payments deemed too high under current circumstances, the Company concluded it was in the best interest of its shareholders to terminate the Newsboy Project and apply its resources and expertise on other endeavors. A loss on asset abandonment of $1,500,400 was recorded in 2014 related to the Newsboy Project.

| 5 |

Deferred Financing Fees

RMB Facility

In conjunction with a Facility Agreement evidencing the Facility with RMB, the Company paid financing fees of approximately $1,300,000 in cash and warrants in 2012. These fees were capitalized as deferred financing fees and were amortized over the life of the Facility using the effective interest method through December 31, 2014. Amortization of deferred financing fees included in interest expense during both the three months ended March 31, 2015 and 2014 was approximately $0 and $163,000.

NPX Convertible Note

In conjunction with the NPX Convertible Note (as discussed in Note 4) the Company paid financing fees of approximately $22,000 in cash in April 2014. These fees were capitalized as deferred financing fees and will be amortized over the life of the Note using the effective interest method. Amortization of deferred financing fees included in interest expense during the three months ended March 31, 2015 was approximately $2,750.

Related Party Payable

The Company’s Chief Executive Officer and President, Dave Beling, has advanced the Company funds to pay for current expenses. Advances as of March 31, 2015 and December 31, 2014 of $286,403 and $209,013, respectively, are due on demand and bear no interest.

Fair Value Measurement

Fair value is defined as the exchange price that would be received for an asset or paid to transfer a liability (an exit price) in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. There are three levels of inputs that may be used to measure fair value:

Level 1 – Valuation based on quoted market prices in active markets for identical assets and liabilities.

Level 2 – Valuation based on quoted market prices for similar assets and liabilities in active markets.

Level 3 – Valuation based on unobservable inputs that are supported by little or no market activity, therefore requiring management’s best estimate of what market participants would use as fair value.

The Company does not have any assets or liabilities measured using Level 1 or 2 inputs. The Company’s Level 3 financial liabilities measured at fair value consisted of the warrant liability as of March 31, 2015 and December 31, 2014. See Note 3.

Fair Value of Financial Instruments

The respective carrying value of certain on-balance-sheet financial instruments approximated their fair values due to the short-term nature of these instruments. These financial instruments include cash, accounts payable, and other liabilities. The warrant liability, a long-term liability, is already recorded at fair value. The fair value of the Company’s notes payable are not practicable to calculate due to the unique terms of the notes.

Income Taxes

Income taxes are accounted for under the asset and liability method in accordance with ASC 740, "Income Taxes". Deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the financial carrying amounts of existing assets and liabilities and their respective tax bases as well as operating loss and tax credit carry forwards. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the periods in which those temporary differences are expected to be recovered or settled. The effect on deferred tax

| 6 |

assets and liabilities of a change in tax rates is recognized in income in the period that includes the enactment date. Deferred tax assets are reduced by a valuation allowance to the extent that the recoverability of the asset is unlikely to be recognized.

The Company reports a liability, if any, for unrecognized tax benefits resulting from uncertain tax positions taken, or expected to be taken, in an income tax return. The Company has elected to classify interest and penalties related to unrecognized income tax benefits, if and when required, as part of income tax expense in the statement of operations. No liability has been recorded for uncertain income tax positions, or related interest or penalties as of March 31, 2015 or December 31, 2014. The periods ended December 31, 2014, 2013, 2012 and 2011 are open to examination by taxing authorities.

Long Lived Assets

The Company assesses the impairment of long-lived assets whenever events or changes in circumstances indicate that the carrying value may not be recoverable. When the Company determines that the carrying value of long-lived assets may not be recoverable based upon the existence of one or more indicators of impairment and the carrying value of the asset cannot be recovered from projected undiscounted cash flows, the Company records an impairment charge. The Company measures any impairment based on a projected discounted cash flow method using a discount rate determined by management to be commensurate with the risk inherent in the current business model. Significant management judgment is required in determining whether an indicator of impairment exists and in projecting cash flows.

Preferred Stock

The Company accounts for its preferred stock under the provisions of the ASC on Distinguishing Liabilities from Equity, which sets forth the standards for how an issuer classifies and measures certain financial instruments with characteristics of both liabilities and equity. This standard requires an issuer to classify a financial instrument that is within the scope of the standard as a liability if such financial instrument embodies an unconditional obligation to redeem the instrument at a specified date and/or upon an event certain to occur. The Company has determined that its preferred stock does not meet the criteria requiring liability classification as its obligation to redeem these instruments is not based on an event certain to occur. Future changes in the certainty of the Company’s obligation to redeem these instruments could result in a change in classification.

Derivative Financial Instruments

The Company accounts for derivative instruments in accordance with Financial Accounting Standards Board (“FASB”) ASC 815, Derivatives and Hedging (“ASC 815”), which requires additional disclosures about the Company’s objectives and strategies for using derivative instruments, how the derivative instruments and related hedged items are accounted for, and how the derivative instruments and related hedging items affect the financial statements. The Company does not use derivative instruments to hedge exposures to cash flow, market or foreign currency risk. Terms of convertible debt and equity instruments are reviewed to determine whether or not they contain embedded derivative instruments that are required under ASC 815 to be accounted for separately from the host contract, and recorded on the balance sheet at fair value. The fair value of derivative liabilities, if any, is required to be revalued at each reporting date, with corresponding changes in fair value recorded in current period operating results. Pursuant to ASC 815, an evaluation of specifically identified conditions is made to determine whether the fair value of warrants issued is required to be classified as equity or as a derivative liability.

Stock-Based Compensation

Stock-based compensation is accounted for based on the requirements of the Share-Based Payment Topic of ASC 718 which requires recognition in the consolidated financial statements of the cost of employee and director services received in exchange for an award of equity instruments over the period the employee or director is required to perform the services in exchange for the award (presumptively, the

| 7 |

vesting period). This ASC also requires measurement of the cost of employee and director services received in exchange for an award based on the grant-date fair value of the award.

The estimated fair value of each stock option as of the date of grant was calculated using the Black-Scholes pricing model. The Company estimates the volatility of its common stock at the date of grant based on the volatility of a comparable peer company which is publicly traded. The Company determines the expected life based on historical experience with similar awards, giving consideration to the contractual terms, vesting schedules and post-vesting forfeitures. The Company uses the risk-free interest rate on the implied yield currently available on U.S. Treasury issues with an equivalent remaining term approximately equal to the expected life of the award. The Company has never paid any cash dividends on its common stock and does not anticipate paying any cash dividends in the foreseeable future. The shares of common stock subject to the stock-based compensation plan shall consist of unissued shares, treasury shares or previously issued shares held by any subsidiary of the Company, and such number of shares of common stock are reserved for such purpose.

Net Loss per Common Share

Net losses were reported during the quarterly period ended March 31, 2015 and 2014. As such, the Company excluded the following from computation as their effect would be anti-dilutive:

| 3/31/15 | 3/31/14 | |||

| Stock options | 4,500,000 | 4,460,000 | ||

| Warrants | 17,048,660 | 21,392,285 | ||

| Preferred stock | 400,000 | 400,000 | ||

| Convertible note payable | 880,000 | - |

Risks and Uncertainties

Our limited operating history makes it difficult for potential investors to evaluate our business or prospective operations. Since our formation, we have not generated any revenues. As an early stage company, we are subject to all the risks inherent in the initial organization, financing, expenditures, complications and delays inherent in a new business. Investors should evaluate an investment in us in light of the uncertainties encountered by developing companies in a competitive environment. Our business is dependent upon the implementation of our business plan. There can be no assurance that our efforts will be successful or that we will ultimately be able to attain profitability.

Natural resource exploration, and exploring for gold in particular, is a business that by its nature is very speculative. There is a strong possibility that we will not discover gold or any other resources which can be mined or extracted at a profit. Even if we do discover gold or other deposits, the deposit may not be of the quality or size necessary for us or a potential purchaser of the property to make a profit from actually mining it. Few properties that are explored are ultimately developed into producing mines. Unusual or unexpected geological formations, geological formation pressures, fires, power outages, labor disruptions, flooding, explosions, cave-ins, landslides and the inability to obtain suitable or adequate machinery, equipment or labor are just some of the many risks involved in mineral exploration programs and the subsequent development of gold deposits.

Our business is exploring for gold and other minerals. In the event that we discover commercially exploitable gold or other deposits, we will not be able to make any money from them unless the gold or other minerals are actually mined or we sell all or a part of our interest. Accordingly, we will need to find some other entity to mine our properties on our behalf, mine them ourselves or sell our rights to mine to third parties. Mining operations in the United States are subject to many different federal, state and local laws and regulations, including stringent environmental, health and safety laws. In the event we assume any operational responsibility for mining our properties, it is possible that we will be unable to comply

| 8 |

with current or future laws and regulations, which can change at any time. It is possible that changes to these laws will be adverse to any potential mining operations. Moreover, compliance with such laws may cause substantial delays and require capital outlays in excess of those anticipated, adversely affecting any potential mining operations. Our future mining operations, if any, may also be subject to liability for pollution or other environmental damage. It is possible that we will choose to not be insured against this risk because of high insurance costs or other reasons.

Recent Accounting Pronouncements

There are several new accounting pronouncements issued by the FASB which are not yet effective. Management does not believe any of these accounting pronouncements will be applicable and therefore will not have a material impact on the Company's financial position or operating results.

| 9 |

NOTE 2 - STOCKHOLDER’S EQUITY

Recent Sales of Unregistered Securities

On October 29, 2014, Rocky Mountain Minerals Corp. (“RMM”) the 100% owned subsidiary of Bullfrog Gold Corp. entered into an Option Agreement (“Option”) with Mojave Gold Mining Corporation (“Mojave”). In order to maintain in force the working right and Option granted to it, and to exercise the Option, Rocky Mountain granted Mojave 750,000 common shares of the Company.

Convertible Preferred Stock

In August 2011, the Board of Directors of the Company (the “Board of Directors”) designated 5,000,000 shares of its Preferred Stock as Series A Preferred Stock. Each share of Series A Preferred Stock is convertible into one share of common stock at the option of the preferred holder. The Series A Preferred Stock in not entitled to receive dividends and does not possess redemption rights. The Company is prohibited from effecting the conversion of the Series A Preferred Stock to the extent that, as a result of the conversion, the holder of such shares beneficially owns more than 4.99% (or, if this limitation is waived by the holder upon no less than 61 days prior notice to us, 9.99%) in the aggregate of the issued and outstanding shares of our common stock calculated immediately after giving effect to the issuance of shares of common stock upon conversion of the Series A Preferred Stock. The holders of the Company’s Series A Preferred Stock are also entitled to certain liquidation preferences upon the liquidation, dissolution or winding up of the business of the Company.

As of March 31, 2015 all issued shares of Series A Preferred Stock have been converted into common stock.

In October 2012, the Board of Directors designated 5,000,000 shares of its Preferred Stock as Series B Preferred Stock. Each share of Series B Preferred Stock is convertible into one share of common stock at the option of the preferred holder. The Series B Preferred Stock is not entitled to receive dividends and does not possess redemption rights. The Company is prohibited from effecting the conversion of the Series B Preferred Stock to the extent that, as a result of the conversion, the holder of such shares beneficially owns more than 4.99% (or, if this limitation is waived by the holder upon no less than 61 days prior notice to us, 9.99%) in the aggregate of the issued and outstanding shares of our common stock calculated immediately after giving effect to the issuance of shares of common stock upon conversion of the Series B Preferred Stock. The holders of the Company’s Series B Preferred Stock are also entitled to certain liquidation preferences upon the liquidation, dissolution or winding up of the business of the Company.

As of March 31, 2015 there have been 1,604,600 shares of Series B Preferred Stock converted into common stock, leaving a total of 400,000 shares of Series B Preferred Stock outstanding.

Common Stock Options

On September 30, 2011, the Board of Directors and stockholders adopted the 2011 Stock Incentive Plan (the “2011 Plan”). Under the 2011 Plan, options may be granted which are intended to qualify as Incentive Stock Options under Section 422 of the Internal Revenue Code of 1986 (the "Code") or which are not intended to qualify as Incentive Stock Options thereunder. In addition, direct grants of stock or restricted stock may be awarded. The 2011 Plan has reserved 4,500,000 shares of common stock for issuance.

There were a total of 4,060,000 non-qualified stock options granted in September 2011 (the “September 2011 Options”).

| 10 |

There were a total of 400,000 non-qualified stock options granted in December 2013 (the “December 2013 Options”).

All September 2011 Options and December 2013 Options were fully vested when they were canceled in September 2014.

There were a total of 4,500,000 options granted in March 2015 (the “March 2015 Options”), these options issued are nonqualified stock options and were 100% vested on grant date. All expense related to these stock options has been recognized.

A summary of the March 2015 Options is presented below:

| March 2015 Options | Options | Strike Price | Term | |||||

| Officer | 1,775,000 | $0.025 | 10 years | (1) | ||||

| Consultant | 250,000 | $0.025 | 10 years | |||||

| Consultant | 355,000 | $0.025 | 10 years | |||||

| Consultant | 705,000 | $0.025 | 10 years | |||||

| Director | 1,415,000 | $0.025 | 10 years | (2) | ||||

| TOTAL | 4,500,000 | |||||||

| (1) Issued to David Beling, the Company's Chief Executive Officer and President. | ||||||||

| (2) Issued to Alan Lindsay, the Company's Chairman of the Board of Directors. | ||||||||

The Black Scholes option pricing model was used to estimate the fair value of $78,045 of the March 2015 Options with the following inputs:

| Options | Exercise Price | Term | Volatility | Risk Free Interest Rate | Fair Value |

| 4,500,000 | $0.025 | 6 years | 87.1% | 1.71% | $78,045 |

A summary of the stock options as of March 31, 2015 and changes during the period are presented below:

| Number of Options | Weighted Average Exercise Price | Weighted Average Remaining Contractual Life (Years) |

Aggregate Intrinsic Value | ||||||||||

| Balance at December 31, 2014 | - | - | - | - | |||||||||

| Granted | 4,500,000 | $ | 0.025 | 10 | - | ||||||||

| Exercised | - | - | - | - | |||||||||

| Forfeited | - | - | - | - | |||||||||

| Canceled | - | - | - | - | |||||||||

| Balance at March 31, 2015 | 4,500,000 | $ | 0.025 | 10 | - | ||||||||

| Options exercisable at March 31, 2015 | 4,500,000 | $ | 0.025 | 10 | - | ||||||||

| 11 |

NOTE 3 – DERIVATIVE FINANCIAL INSTRUMENTS

In applying current accounting standards to the financial instruments issued in the historical private placements, the Company first considered the classification of the Series B Preferred Stock under ASC 480 Distinguishing Liabilities from Equity, and the Warrants under ASC 815 Derivatives and Hedging. The Series B Preferred Stock is perpetual preferred stock without redemption or dividend provisions, contingent or otherwise. Further, the Series B Preferred Stock is convertible into a fixed number of shares of Common Stock with adjustments to the conversion price solely associated with equity restructuring events such a stock splits and recapitalization. Generally redemption provisions that provide for the mandatory payment of cash to the Investor to settle the contract or certain provisions that cause the number of linked shares of Common Stock to vary result in liability classification; and, in some instances, classification outside of stockholders’ equity. There being no such provisions associated with the Series B Preferred Stock, it is classified as a component of stockholders’ equity.

The warrants were also evaluated for purposes of classification. The warrants issued contain a feature that is not consistent with the concept of stockholders’ equity. The exercise price of the warrants is subject to adjustment upon the issuance of common stock or common share linked contracts at prices below the contractual exercise prices. The 2012 Private Placement and February 2013 Private Placement warrants price adjustment expires four years after the date of issuance, and the June 2013 Private Placement warrants price adjustment expires three years after the date of issuance. The August 2013 Private Placement and October 2013 Private Placement warrants were amended on December 2, 2013 and allows for a price adjustment that expires three years after the date of original issuance. Current accounting standards provide that such provisions are not consistent with the concept of stockholders’ equity. As a result, all warrants with price adjustment features require classification in liability as derivative warrants. Derivative warrants are carried initially at fair value (up to the value of cash received) and subsequently at fair value with changes in fair value reflected in income.

| Closing date of private placement | ||||||||||||||||||||||||||||

| 11/19/12 | 12/17/12 | 02/04/13 | 06/21/13 | 08/15/13 | 10/09/13 | Total warrant liability | ||||||||||||||||||||||

| Ending balance at December 31, 2014 | $ | 13 | $ | 5 | $ | 2 | $ | 0 | $ | 0 | $ | 0 | $ | 20 | ||||||||||||||

| Issuance of derivative warrants | — | — | — | — | — | — | — | |||||||||||||||||||||

| Exercise or expiration | — | — | — | — | — | — | — | |||||||||||||||||||||

| Change in fair value of warrant liability | 29 | 22 | 41 | 0 | 0 | 0 | 92 | |||||||||||||||||||||

| Ending balance at March 31, 2015 | $ | 42 | $ | 27 | $ | 43 | $ | 0 | $ | 0 | $ | 0 | $ | 112 | ||||||||||||||

| 12 |

The derivative warrants were calculated using Black-Scholes valuation technique. Significant inputs into this technique are as follows:

| 2012 Private Placement | 12/31/2014 | 3/31/2015 |

| Fair market value of common stock | $0.01 | $0.02 |

| Exercise price | $0.35 | $0.35 |

| Term (1) | (4) | (6) |

| Volatility range (2) | (5) | (7) |

| Risk-free rate (3) | 0.67% | 0.56% |

| February 2013 Private Placement | 12/31/2014 | 3/31/2015 |

| Fair market value of common stock | $0.01 | $0.02 |

| Exercise price | $0.35 | $0.35 |

| Term (1) | 2.11 Years | 1.86 Years |

| Volatility range (2) | 64.69% | 68.72% |

| Risk-free rate (3) | 0.67% | 0.56% |

| June 2013 Private Placement | 12/31/2014 | 3/31/2015 |

| Fair market value of common stock | $0.01 | $0.02 |

| Exercise price | $0.35 | $0.35 |

| Term (1) | 1.48 Years | 1.24 Years |

| Volatility range (2) | 71.47% | 64.13% |

| Risk-free rate (3) | 0.67% | 0.56% |

| August 2013 Private Placement | 12/31/2014 | 3/31/2015 |

| Fair market value of common stock | $0.01 | $0.02 |

| Exercise price | $0.35 | $0.35 |

| Term (1) | 1.63 Years | 1.38 Years |

| Volatility range (2) | 71.65% | 65.02% |

| Risk-free rate (3) | 0.67% | 0.56% |

| October 2013 Private Placement | 12/31/2014 | 3/31/2015 |

| Fair market value of common stock | $0.01 | $0.02 |

| Exercise price | $0.35 | $0.35 |

| Term (1) | 1.78 Years | 1.53 Years |

| Volatility range (2) | 73.33% | 66.55% |

| Risk-free rate (3) | 0.67% | 0.56% |

| 13 |

| (1) | The term is the remaining years until expiration of warrants. | |

| (2) | The Company does not have a trading market value upon which to base its forward-looking volatility. Accordingly, the Company selected a peer company that provided a reasonable basis upon which to calculate volatility. | |

| (3) | The risk-free rate used represents the yield on zero coupon US Government Securities with a period to maturity consistent with the interval described in (2), above. | |

| (4) | The remaining term for the 2012 Private Placement with a November 19, 2012 closing date was 2.15 years, and the December 17, 2012 closing date was 2.22 years. | |

| (5) | The volatility for the 2012 Private Placement with a November 19, 2012 closing date was 65.4%, and the December 17, 2012 closing date was 68.75%. | |

| (6) | The remaining term for the 2012 Private Placement with a November 19, 2012 closing date was 1.64 years, and the December 17, 2012 closing date was 1.72 years. | |

| (7) | The volatility for the 2012 Private Placement with a November 19, 2012 closing date was 66.94%, and the December 17, 2012 closing date was 68.48%. |

Warrants contain limitations on exercise, including the limitation that the holders may not convert their warrants to the extent that upon exercise the holder, together with its affiliates, would own in excess of 4.99% of our outstanding shares of common stock (subject to an increase upon at least 61-days’ notice by the subscriber to us, of up to 9.99%).

The second classification-related accounting consideration related to the possibility that the conversion option embedded in the Series B Preferred Stock may require classification outside of stockholders’ equity. Generally, an embedded feature in a hybrid financial instrument (such as the Series B Preferred Stock) that both meets the definition of a derivative financial instrument and is not clearly and closely related to the host contract in term of risks would require bifurcation and accounting under derivative standards. The embedded conversion option is a feature that embodies risks of equity. The Company has concluded that the Series B Preferred Stock is a contract that affords solely equity risks.

| 14 |

NOTE 4 – NOTES PAYABLE

RMB Facility

On December 10, 2012 (the “Closing Date”), the Company entered into the Facility with RMB, as the lender, in the amount of $4.2 million. The loan proceeds from the Facility will be used to fund an agreed work program relating to the Newsboy gold project located in Arizona and for agreed general corporate purposes. Standard Gold the Company’s wholly owned subsidiary is the borrower under the Facility and the Company is the guarantor of Standard Gold’s obligations under the Facility. Standard Gold paid an arrangement fee of 7% of the Facility amount due upon the first draw down of the Facility. The Facility funds were available to drawdown until March 31, 2014 with the final repayment date due 24 months after the Closing Date, which was December 10, 2014. The Facility bears interest at the rate of LIBOR plus 7% with interest payable quarterly in cash. During the quarter ended June 30, 2014 the $500,000 restricted cash account was applied to the quarterly interest payment and the principal balance. This resulted in an RMB note payable balance of approximately $2,453,000. As previously discussed the Newsboy Project was terminated, and therefore the only collateral remaining for the RMB note is the Bullfrog Project with a March 31, 2015 balance of approximately $100,000.

On December 15, 2014, RMB amended the Facility to extend the repayment date to December 15, 2015. All interest accrued but unpaid as of December 15, 2014 is to be capitalized and added to the outstanding principal balance.

In connection with the Facility, the Company issued 7,000,000 warrants to purchase shares of the Company’s Common Stock for $0.35 per share to be exercisable for 36 months after the Closing Date, with the proceeds from the exercise of the warrants to be used to repay the Facility. The Company met all of the conditions precedent to complete the closing for the Facility.

In applying current accounting standards to the warrants issued in the Facility with RMB, the Company considered the warrants under ASC 815 Derivatives and Hedging. Under these standards the warrants would qualify as equity. The fair value of the warrants were calculated to be $1,063,592 and are classified as deferred financing fees that were amortized for 24 months from the Closing Date of the RMB Facility.

NPX Convertible Note

On April 25, 2014 (“NPX Closing Date”), the Company entered into a Securities Purchase Agreement for an unsecured 12.5% convertible promissory note (the “Note”) with NPX Metals, Inc (“NPX”), as the lender, in the amount of $220,000. The Note proceeds were used to fund the Klondike Project and for general corporate purposes. The Company paid an arrangement fee of 10% of the Note and issued 220,000 warrants to purchase one full share at a price of $0.35 within three years from the NPX Closing Date. The Note principal and unpaid accrued interest will be due and payable 24 months from the NPX Closing Date. The president of NPX is Johnathan Lindsay, the son of the chairman of the board of the Company Alan Lindsay.

During the term of the Note, NPX may elect by giving five days to convert their Note and any accrued but unpaid interest thereon, into shares of the Company’s common shares at a conversion price equal to $0.25 per common share. Additionally, for each common share purchased there will be a three year warrant to purchase one hundred percent of the number of shares purchased at a per share exercise price of $0.35.

The ability of NPX to exercise the warrants is not contingent upon the conversion of the Note and, accordingly, we determined that the warrant was “detachable” from the Note. The estimated fair value of the warrant was calculated on the date of issuance using the Black-Scholes pricing model, however we

| 15 |

concluded the estimated fair value of the warrant was not material and does not require separate accounting treatment. The warrant also contains a provision that the warrant will be adjusted under certain conditions in the event future warrants are issued with more favorable terms.

We concluded that the conversion feature of the Note met the criteria of an embedded derivative and should be bifurcated from the Note (host contract) and accounted for as a derivative liability and calculated at fair value. We estimated the fair value of the conversion feature of the Note on the date of issuance using the Black-Scholes pricing model, however we concluded the estimated fair value of the conversion feature was not material and does not require separate accounting treatment. If the Note is converted the warrants that will be issued on the conversion date will be accounted for as a derivative liability.

| 16 |

NOTE 5 - COMMITMENTS

On June 11, 2012, the Company entered into an option agreement with Arden Larson, an unrelated party, to purchase a 100% interest in the Klondike Project (“Klondike”) that currently includes 109 unpatented mining claims. Klondike is located in the Alpha Mining District about 40 miles north of Eureka, Nevada.

The remaining amount due to Mr. Larson of the original price of $575,000 is payable on the following schedule:

| Klondike Project - Payment Date | Payment Amount |

| June 11, 2015 | $40,000 |

| June 11, 2016 | $45,000 |

| June 11, 2017 | $50,000 |

| June 11, 2018 | $55,000 |

| June 11, 2019 | $60,000 |

| June 11, 2020 | $65,000 |

| June 11, 2021 | $70,000 |

| June 11, 2022 | $75,000 |

The Company has the option to buy-down the royalty component by making payments of $500,000 per 0.25% of base net smelter return royalties for gold, silver and other products to Mr. Larson based on the following schedule:

| Product | Base net smelter return royalty | Average market price | Maximum buy-down net smelter return royalty |

| GOLD | 1.00 | Less than $1,200/troy oz. | 0.50 |

| 1.50 | $1,201 to $1,600/troy oz. | 0.75 | |

| 2.00 | $1,601 to $2,000/troy oz. | 1.00 | |

| 2.50 | $2,001 to $2,400/troy oz. | 1.25 | |

| 3.00 | $2,401 to $2,800/troy oz. | 1.50 | |

| 3.50 | $2,801 to $3,200/troy oz. | 1.75 | |

| 4.00 | Greater than $3,200/troy oz. | 2.00 | |

| SILVER | 1.00 | Less than $15/troy oz. | 0.50 |

| 1.50 | $15.01 to $30/troy oz. | 0.75 | |

| 2.00 | $30.01 to $45/troy oz. | 1.00 | |

| 2.50 | $45.01 to $60/troy oz. | 1.25 | |

| 3.00 | $60.01 to $75/troy oz. | 1.50 | |

| 3.50 | $75.01 to $90/troy oz. | 1.75 | |

| 4.00 | Greater than $90/troy oz. | 2.00 | |

| OTHER | 2.00 | As determined by products | 1.00 |

| 17 |

In addition, the Company is committed to spend no less than $850,000 for the benefit of the Klondike Project on the following schedule:

| 1. | $100,000 prior to June 11, 2013 | |

| 2. | An additional $150,000 prior to June 11, 2014 | |

| 3. | An additional $200,000 prior to June 11, 2015 | |

| 4. | An additional $200,000 prior to June 11, 2016 | |

| 5. | An additional $200,000 prior to June 11, 2017 |

Should the Company choose not to maintain the work commitment and option to the property the Company can forego future payments to Mr. Larson without penalty. As of June 11, 2013 the Company spent approximately $86,000 on the Klondike Project, therefore in accordance with the option agreement the Company paid Mr. Larson half of the work commitment shortage. The 2014 work commitment was met therefore no additional payment was due to Mr. Larson.

On March 23, 2015 (“Effective Date”), Rocky Mountain Minerals Corp. (“RMM”) the 100% owned subsidiary of Bullfrog Gold Corp. (the “Company”) entered into a Mineral Lease and Option to Purchase Agreement (“Agreement”) with Barrick Bullfrog Inc. (“Barrick Bullfrog”) involving patented mining claims, unpatented mining claims, and mill site claims (“Properties”) located three miles west of Beatty, Nevada. These Properties are strategically located adjacent to the Company’s Bullfrog Gold Project and include two patents that cover the SW half of the Montgomery-Shoshone (M-S) open pit gold mine. In October 2014 the Company optioned the NE half of the M-S pit and now controls the entire pit.

RMM shall expend as minimum work commitments for the benefit of the Properties prior to the 5th anniversary of the Effective Date per the schedule below:

| Anniversary of Effective Date | Minimum Project Work Commitment ($) |

| First | 100,000 |

| Second | 200,000 |

| Third | 300,000 |

| Fourth | 400,000 |

| Fifth | 500,000 |

| 18 |

ITEM 2 – MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Forward Looking Statements

The following discussion and analysis is provided to increase the understanding of, and should be read in conjunction with, our unaudited condensed consolidated financial statements and related notes included elsewhere in this Quarterly Report. Historical results and percentage relationships among any amounts in these financial statements are not necessarily indicative of trends in operating results for any future period. This Report contains “forward-looking statements”. The statements, which are not historical facts contained in this Report, including this Management’s discussion and analysis of financial condition and results of operation, and notes to our unaudited condensed consolidated financial statements, particularly those that utilize terminology such as “may” “will,” “should,” “expects,” “anticipates,” “estimates,” “believes,” or “plans” or comparable terminology are forward-looking statements. Such statements are based on currently available operating, financial and competitive information, and are subject to various risks and uncertainties. Future events and our actual results may differ materially from the results reflected in these forward-looking statements. Factors that might cause such a difference include, but are not limited to, limited ability to establish new strategic relationships, ability to sustain and manage growth, variability of operating results, our expansion and development of new projects, general economic conditions, dependence on key personnel, the ability to attract, hire and retain personnel who possess the technical skills and experience necessary to maintain and develop new projects, the potential liability with respect to actions taken by our existing and past employees, and other risks described herein and in our other filings with the Securities and Exchange Commission.

The safe harbor for forward-looking statements provided by Section 21E of the Securities Exchange Act of 1934 excludes issuers of “penny stock” (as defined under Rule 3a51-1 of the Securities Exchange Act of 1934). Our Common Stock currently falls within that definition.

All forward-looking statements in this document are based on information currently available to us as of the date of this report, and we assume no obligation to update any forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the actual results to differ materially from any future results, performance or achievements expressed or implied by such forward-looking statements.

Company History and Recent Events

Bullfrog Gold Corp., (“Bullfrog Gold” or, the “Company") was incorporated under the laws of the State of Delaware on July 23, 2007 as Kopr Resources Corp. On July 19, 2011, Bullfrog Gold's Board of Directors approved an Amended and Restated Certificate of Incorporation of the Company to authorize (i) the change of the name of the Company to "Bullfrog Gold Corp." from "Kopr Resources Corp." (ii) the increase in the authorized capital stock to 250,000,000 shares and (iii) the change in par value of the capital stock to $0.0001 per share. The Company is in the exploration stage of its resource business.

There were a total of 4,500,000 options granted in March 2015 (the “March 2015 Options”), these options issued are nonqualified stock options and were 100% vested on grant date. All expense related to these stock options has been recognized.

On March 23, 2015 (“Effective Date”), Rocky Mountain Minerals Corp. (“RMM”) the 100% owned subsidiary of Bullfrog Gold Corp. (the “Company”) entered into a Mineral Lease and Option to Purchase Agreement (“Agreement”) with Barrick Bullfrog Inc. (“Barrick Bullfrog”) involving patented mining claims, unpatented mining claims, and mill site claims (“Properties”) located three miles west of Beatty, Nevada. These Properties are strategically located adjacent to the Company’s Bullfrog Gold Project and

| 19 |

include two patents that cover the SW half of the Montgomery-Shoshone (M-S) open pit gold mine. In October 2014 the Company optioned the NE half of the M-S pit and now controls the entire pit.

On December 15, 2014, RMB amended the Facility to extend the repayment date to December 15, 2015. All interest accrued but unpaid as of December 15, 2014 was capitalized and added to the outstanding principal balance.

On October 29, 2014, Rocky Mountain Minerals Corp. (“RMM”) the 100% owned subsidiary of Bullfrog Gold Corp. entered into an Option Agreement with Mojave Gold Mining Corporation (“Mojave”). RMM granted Mojave 750,000 common shares and paid $16,000. RMM must pay to Mojave a total of $190,000 over the next 10 years.

As of September 11, 2014 the Board of Directors canceled the remaining granted options in the aggregate amount of 3,810,000.

As of September 5, 2014 the 650,000 stock options issued to Consultants (“Consultants”) were terminated due to non-renewal of their consulting agreements.

On May 30, 2014, we sent a notice of termination (“Termination Notice”) to Southwest Exploration Inc. (“SWI”) for the Option to Purchase and Royalty Agreement (“Agreement”) dated September 28, 2011 for the Newsboy Project in Arizona. Per the Agreement, this Termination Notice gave 30 day notice to SWI and was effective on June 30, 2014.

On April 25, 2014, we entered into a Securities Purchase Agreement (“SPA”) for an unsecured 12.5% convertible promissory note (the “Note”) with NPX Metals, Inc (“NPX”), as the lender, in the amount of $220,000.

On March 31, 2014, we created a new wholly-owned subsidiary of the Company with the name of Rocky Mountain Minerals Corp. (“RMM”). RMM will be used to account for the exploration costs of Klondike.

Company Overview

We are an exploration stage company engaged in the acquisition and exploration of properties that may contain gold and other mineralization primarily in the United States. Our target properties are those that have been the subject of historical exploration. We have acquired exploration permits on state lands and Federal patented and unpatented mining claims in the Nevada for the purpose of exploration and potential development of gold and silver on a total of approximately 6,240 acres. We plan to review opportunities and acquire additional mineral properties with current or historic precious and base metal mineralization with meaningful exploration potential.

Bullfrog Project

The Bullfrog Gold Project lies approximately 3 miles northwest of the town of Beatty and 116 miles northwest of Las Vegas, Nevada. In September 2011 Standard Gold acquired a 100% right, title and interest in and to79 mining claims and two patents that contain approximately 1,650 acres subject to a 3% net smelter royalty.

On October 29, 2014, Rocky Mountain Minerals Corp. (“RMM”) the 100% owned subsidiary of Bullfrog Gold Corp. entered into an Option Agreement (“Option”) with Mojave Gold Mining Corporation (“Mojave”). Mojave holds and possesses the purchase rights to 100% of 12 patented mining claims located in Nye County, Nevada. This Property is contiguous to the Company’s Bullfrog Gold Project and covers approximately 156 acres, including the northeast half of the Montgomery-Shoshone pit mined by Barrick Gold in the mid 1990’s.

| 20 |

Mojave granted to RMM the sole and immediate working right and option with respect to the Property until the 10th anniversary of the Closing Date, to earn a One Hundred Percent (100%) interest in and to the Property free and clear of all charges encumbrances and claims, save and except a sliding scale NSR Royalty.

In order to maintain in force the working right and Option granted to it, and to exercise the Option, Rocky Mountain granted Mojave 750,000 common shares and paid $16,000. RMM must pay to Mojave a total of $190,000 over the next 10 years. The Company proposes to drill 22 holes during 2015 to test for potential mineralization under the Montgomery-Shoshone pit and that may extend onto the Company’s adjacent property. For reference, Barrick Bullfrog Inc. (“Barrick Bullfrog”) terminated a lease on these patents after they ceased operations in late 1999.

On March 23, 2015, Rocky Mountain Minerals Corp. entered into a Mineral Lease and Option to Purchase Agreement (“Agreement”) with Barrick Bullfrog involving 6 patented mining claims, 20 unpatented mining claims, and 8 mill site claims (“Properties”) located three miles west of Beatty, Nevada. These Properties are strategically located adjacent to the Company’s Bullfrog Gold Project and include two patents that cover the SW half of the Montgomery-Shoshone (M-S) open pit from which Barrick produced approximately 220,000 ounces of gold by the late 1990’s. Underground mining in the early 1900’s produced approximately 70,000 ounces of gold from the M-S deposit. Also included in the Agreement is the northern one third of the main Bullfrog deposit where Barrick mined approximately 2.1 million additional ounces by open pit and underground methods. In addition to prospective adjacent lands, these acquisitions provide the potential to expand the M-S deposit along strike and at depth and in the northern part of the main Bullfrog deposit.

The Company also has access to Barrick’s substantial data base within a 1.5 mile radius of the leased lands to further advance its exploration and development programs. To maintain the lease and option, the Company must spend $1.5 million dollars within five years on the Barrick properties and then pay Barrick 3.25 million shares of Bullfrog stock while providing a 2% gross royalty on production from the Barrick properties. Overriding royalties of 5% net smelter returns and 5% gross proceeds are respectively limited to three claims and two patents in the main Bullfrog pit area. Barrick has retained a back-in right to reacquire a 51% interest in the Barrick properties, subject to definition of a mineral resource on the Barrick properties meeting certain criteria, and reimbursing the Company in an amount equal to two and one half times Company expenditures on the Barrick properties.

Company management has estimated that 41,000 ounces of gold in 1.44 million tons of material averaging 0.97 gram per ton remains within a cutoff depth up to 75 meters under the existing M-S pit. This manual estimate was based on cross sections typically spaced 15 meters apart, a cutoff grade of 0.3 gram gold per ton at the top and bottom of mineral intervals, and drill data and pit surveys completed by Barrick. Notwithstanding, Barrick makes no representation concerning the accuracy or completeness of the data used by the Company. Additional drilling is required to confirm some of the Company’s mineral projections and to test for extensions at greater depths and along strike beyond the existing pit limits. Half of this M-S mineralization is on two Barrick patents within the pit and half is on two of the 12 Mojave patents. The direct ratio of waste to mineral tons within a cross-sectional preliminary pit outline is 0.97:1, but this does not include waste removal for ramps and other considerations that would otherwise be included in a future pit plan based on computerized block modelling and 3-D mine planning and design programs. It is cautioned that the Company’s current and expanded properties contain no reserves or resources and that the estimates and additional potential mineralization discussed herein may never become viable, feasible or economic. These estimates were mainly prepared to assess the available M-S information and plan additional drilling.

| 21 |

Significant drilling is required to test projections of mineralized trends and structures that extend for considerable distances to the north and east of the M-S pit on the original lands acquired by the Company in 2011. Located east of the M-S pit is an area 700 meters by 1,300 meters in which there is only one shallow hole from which there is no data available. Only a portion of this area may be prospective, but it certainly warrants additional study and exploration drilling.

There is only one drill hole located about 150 meters NE of the M-S pit limit and another hole 1,000 meters NE of the pit along strike of a major geologic structure. In this regard, the Company’s lands extend nearly 5,000 meters NNE of the pit and there has been very little drilling in this area, even though several structures have been mapped by Barrick and others.

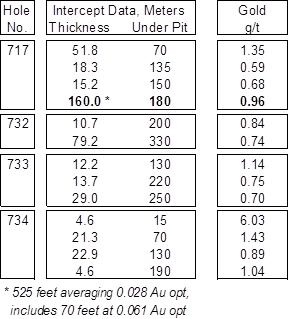

Barrick drilled twelve deep holes in the M-S area ranging from 318 meters to 549 meters. Notable mineral intercepts from four holes below the central part of the pit are summarized below:

These results demonstrate that substantial amounts of gold occur in an exceptionally large epithermal system that has good potential for expansion and possibly higher grades at depth. Three of these intercepts are less than 75 meters below the existing pit. Two holes located 40 meters and 90 meters east of the 160 meter interval in hole #717 contained no significant mineralization at this depth, whereas the 29 meters of mineral in hole #733 is 60 meters west and the mineral zone is open to the north, south and west.

For reference, Barrick terminated all mining and milling operations in the autumn of 1999 when their cash production costs exceeded gold prices that averaged less than $300 per ounce for the year and reached a low of $258/oz in August 1999. The economic margins for heap leaching lower grades at current gold prices near $1200/oz are deemed much better than in 1999, and the Company is positioned to explore such opportunities. Furthermore, Barrick never controlled or had access to a patented claim on the immediate east and north limits of the M-S pit, but this patent is owned by the Company.

| 22 |

Klondike Project

The Company acquired the option to purchase the Klondike Project in Nevada in June 2012. The Klondike Project is located in the Alpha Mining District about 40 miles north of Eureka, Nevada. The initial property included 64 unpatented mining claims, to which Bullfrog staked an additional 168 claims but dropped 123 claims in 2015. The current land position is now 109 claims that cover approximately 2,180 acres.

The Klondike Project covers mineralized structures 5 miles long and 1.5 miles wide along the west flank of the Sulfur Springs mountain range. The rocks within this corridor are intensely broken by numerous periods of faulting, thereby providing a favorable environment for several sequences of hydrothermal solutions to form mineral deposits. These host rocks are mostly Devonian age sediments typical of most Carlin gold deposits.

At least two styles of mineral deposits exist on the Company’s property:

| | The oldest is a silver-rich, lead-zinc event that appears to be related to a molybdenum porphyry system that is not exposed but indicated by geochemistry and alteration. In this regard, the Klondike claims lie 10 miles north of the Mt. Hope molybdenum mine which is currently under development as one of the world’s largest molybdenum deposits. The Mt. Hope deposit has a halo of silver-zinc mineralization that is typically more than a thousand feet thick and above several thousand feet of molybdenum mineralization. A silver-rich copper event may also be related to this style of mineralization. |

| | A later stage Carlin-style gold-arsenic-barite mineralizing event over-printed the earlier silver-zinc-molybdenum system. This event has wide-spread anomalous gold values with arsenic and associated calcite veining. Barite may be related to all events. A new gold discovery is currently being drilled by other companies 10 miles west of the Klondike and may be the continuation of the massive Cortez gold trend. |

The Company completed a phase 1 drill program on the Klondike Project in May 2014. The following are the results:

Copper Hill Drilling and Results:

Hole #24 was angled toward the west and collared about 100 feet east of several shallow historic shafts sunk in the heart of the north-south mineralized outcrops on Copper Hill. This hole included 30 feet that averaged 1.8 ounces of silver per ton, 0.23% copper, 800 ppm antimony and 257 ppm arsenic. However, this hole only penetrated what we now know as the eastern edge of the significant mineralized zone. Highly prospective drill sites on the top, north, south and west side of Copperhill as well as some other areas could not be drilled during phase 1 (see the General section for details).

Vertical hole #25 was collared at the same drill site as #24 and contained significant anomalous but peripheral mineralization that was about 100 feet east and a similar depth of the prime intercept in #24. Vertical holes #26 and #27 were approximately 200 feet east of holes #24 and #25 but are now known to be too far east of the main mineral trend. Notwithstanding Hole #26 intersected 5 feet of 14 ppm (0.4 opt) silver. Mineralization at Copper Hill may extend 2,000 feet south to Cougar Hill, which also could not be drilled in phase 1 but remains a priority target.

| 23 |

| Copper Hill Assay Results | ||||||||||

| Hole | Intervals, Feet | Silver | Copper | Lead | Zinc | Antimony | Arsenic | |||

| No. | From | To | Thick. | ppm | ppm | ppm | ppm | ppm | ppm | |

| 24 | 15 | 20 | 5 | <1 | 71 | 87 | 589 | 40 | 172 | |

| 70 | 95 | 25 | 2 | 116 | 94 | 102 | 73 | 38 | ||

| 125 | 155 | 30 | 61 | 2,335 | 694 | 239 | 803 | 257 | ||

| incl. | 130 | 135 | 5 | 115 | 4,570 | 1,130 | 381 | 1,600 | 417 | |

| 25 | 95 | 125 | 30 | <1 | 64 | 70 | 151 | 55 | 116 | |

| 220 | 240 | 20 | 3 | 142 | 38 | 123 | 125 | 32 | ||

| 290 | 300 | 10 | 4 | 54 | 445 | 17 | 56 | 48 | ||

| 320 | 330 | 10 | 2 | 157 | 78 | 69 | 238 | 63 | ||

| 26 | 170 | 175 | 5 | 14 | 644 | 18 | 59 | 181 | 51 | |

| 200 | 205 | 5 | 2 | 45 | 60 | 82 | 155 | 18 | ||

| 27 | 100 | 115 | 15 | <1 | 24 | 43 | 261 | 37 | 163 | |

Glory Hole Drilling and Results:

Holes #19 and #20 were collared approximately 100 feet due west and hole #21 about 70 feet SSW of the Glory Hole area. These three holes were angled -50º in a due east direction. Vertical hole #22 was approximately 140 feet west of the Glory Hole area. After analyzing data now available along with field observations, it has been concluded that the host rocks exposed in the Glory hole pit dip about -15º to the east and were mineralized as a manto-style deposit rather than a near vertical zone that was thought to have been mineralized via a near vertical fault. As a result the angled holes went under the prime target area and the only intercept of significance was five feet of 6 ppm silver at a depth of 45 feet. Due to the constraints described in the General section herein, it was not deemed practical to build a drill access road to the north and east sides of the Glory Hole pit during this phase 1 program.

The south side of the Glory Hole is adjacent to a dry creek that is topographically and stratigraphically below the near flat lying dolomite host beds. It is therefore planned in phase 2 to drill north and east of the Glory Hole and at higher elevations south and east of the dry creek where the dolomite host rocks outcrop and continue dipping toward the east.

| 24 |

| Glory Hole Assay Results |

| Hole | Intervals, Feet | Silver | Copper | Barium | Lead | Zinc | Antimony | Arsenic | Titanium | Moly | |||

| No. | From | To | Thick. | ppm | ppm | ppm | ppm | ppm | ppm | ppm | ppm | ppm | |

| 19 | 75 | 85 | 10 | 1 | 16 | 2,188 | 155 | 132 | 20 | <10 | 585 | <2 | |

| 145 | 150 | 5 | 1 | <15 | 36,805 | 534 | 87 | 25 | 13 | 16,093 | <2 | ||

| 21 | 45 | 50* | 5 | 6 | 126 | 14,350 | 1,460 | 9,680 | 95 | 15 | 4,018 | 3 | |

| * Duplicate sample | |||||||||||||

Black Lizard Drilling and Results:

Twelve holes were drilled in the Black Lizard area with the best three holes summarized below. Although some holes proposed could not be drilled, the Black Lizard area is a lower priority target.

| Black Lizard Assay Results | ||||||||||

| Hole | Intervals, Feet | Silver | Copper | Lead | Zinc | Molybdenum | Antimony | |||

| No. | From | To | Thick. | ppm | ppm | ppm | ppm | ppm | ppm | |

| 2 | 10 | 25 | 15 | 4 | 76 | 63 | 4550 | <2 | 41 | |

| 3 | 35 | 45 | <10 | 1 | 22 | 115 | 300 | 2 | 28 | |

| 10 | 75 | 109 | 34 | <1 | 15 | 193 | 297 | 3.6 | 18 | |

| incl | 105 | 109 * | 4 | 2 | 38 | 183 | 437 | 5 | 49 | |

| * Bottom of hole | ||||||||||

General

Much of the proposed phase 1 drill program was constrained with respect to:

- Archeological sites that were all related to historic mining but could not be cleared during the program.

- A 5 acre disturbance limitation required by the Notice of Intent to Drill procedures of the US Bureau of Land Management.

- International migratory bird nesting treaties that had requirements in effect during the time drilling was performed.

- Budgetary constraints.

| 25 |

Notwithstanding, the next program will include advance archeological clearances and approvals of all phase 2 holes to be drilled. The concurrent completion of phase 1 reclamation requirements should also allow up to nearly 5 acres of new disturbances during the phase 2 drill program.

Two of the known styles of mineralization were the copper-silver-antimony in the Copper Hill area and the barite-lead-silver-zinc mineralization in the Glory Hole and Old Whalen Mine areas. Three new styles of mineralization were recognized from phase 1 assay results:

| 1. | Anomalous molybdenum and associated metals within a de-calcified brecciated dolomite, particularly in Hole #10 in the Black Lizard target area. |

| 2. | Numerous zones that contain strong iron staining with associated arsenic in decalcified, brecciated, and altered dolomite that is similar to alteration and mineralization in Carlin-style gold deposits. |

| 3. | More than 2,000 ppm of antimony in the bottom 10 feet of Hole #18. |

All drilling was performed in the oxide zone but potential remains below the water table where primary sulfides may occur in other deeper dolomitic formations that may host manto-style mineralization. Feeder veins and zones that mineralized these beds could also possibly provide high grade vein-style mineralization in the oxide and sulfide zones.

Drilling, Sampling and Assaying Procedures and Results:

Drilling the first 16 holes was performed with a blast hole drill using percussion drilling methods. Holes 17 through 27 were drilled with a reverse circulation rig. Drill cuttings were sampled at intervals of 5 feet and split to typically produce 15-pound representative samples for further sample preparation by the assay lab. All field activities, including the collection, logging, bagging and tagging of sample splits were under the direct supervision and custody of Clive Bailey, CPG, Qualified Person and Lead Project Consultant. Sample splits were loaded on trucks operated by American Assay Laboratories (AAL), transported to their facilities for sample preparation and assayed using x-ray fluorescence (XRF) procedures for base metals, silver, barium and other select elements. XRF was selected since it is the best procedure for analyzing barite contents. Eight samples containing more than 10 ppm silver as determined by XRF were fire assayed, which was 5.8% higher than the XRF silver assays. Fire assay gold contents for the eight samples averaged less than 0.015 ppm gold.

In compliance with US and other international QA/QC procedures, separate blank, duplicate and standard samples were randomly submitted and assayed with the drill sample splits. AAL also performed numerous assays using duplicates, blanks and standards for their own internal QA/QC policies.

Immediate Plans:

The Company intends to raise additional funds and drill the targets that have been further defined from the first phase program. Additional assays have been ordered to further quantify where contents of gold and other elements may be helpful in understanding the geology of the main exploration targets and for guiding future work.

| 26 |

Results of Operations

Three Months Ended March 31, 2015 Compared to March 31, 2014

| Three Months Ended | ||||||||

| 3/31/15 | 3/31/14 | |||||||

| Revenue | $ | — | $ | — | ||||

| Operating expenses | ||||||||

| General and administrative | 167,315 | 145,012 | ||||||

| Exploration costs | — | 82,904 | ||||||

| Marketing | — | 2,796 | ||||||

| Total operating expenses | 167,315 | 230,712 | ||||||

| Net operating loss | (167,315 | ) | (230,712 | ) | ||||

| Gain on extinguishment of debt | — | 15,500 | ||||||

| Interest expense | (55,779 | ) | (212,845 | ) | ||||

| Revaluation of warrant liability | (92 | ) | 180,525 | |||||

| Net loss | $ | (223,186 | ) | $ | (247,532 | ) | ||

We are still in the exploration stage and have no revenues to date.

During the three months ended March 31, 2015 we had a net loss of $223,186 compared to a net loss of $247,532 for the three months ended March 31, 2014. The decrease of $24,346 is due primarily to:

| 1. | The increase of approximately $22,000 in the general and administrative expenses is due to approximately $78,000 stock option compensation that was expensed in 2015 versus zero in 2014. See Note 2 in the Notes to the Consolidated Financial Statements for a complete discussion of the stock options issued. | |

| 2. | The exploration cost in 2014 was approximately $83,000 for the final phase at the Newsboy Project in Arizona. An independent technical report was completed in February 2014 that showed the project was not economic under reasonably foreseeable gold prices. Based on that report and option payments deemed too high under current circumstances, the Company concluded it was in the best interest of its shareholders to terminate the Newsboy Project and apply its resources and expertise on other endeavors. | |

| 3. | Interest expense was greater in 2014 versus 2015 due to the amortization of arrangement fee and warrants associated with the RMB loan. See Note 4 in the Notes to the Consolidated Financial Statements for a complete discussion of the RMB debt facility. | |

| 4. | The revaluation of warrant liability change of approximately $180,000 for the three months ended March 31, 2015 for the same period in 2014 was primarily due to an increase in stock price. See Note 3 in the Notes to the Consolidated Financial Statements for a complete discussion and valuation of the warrant liability. |

| 27 |

Liquidity and Capital Resources

Losses from operations have been incurred since inception and there is an accumulated deficit of $9,228,736 as of March 31, 2015. Continuation as a going concern is dependent upon raising additional funds and attaining profitable operations.