Attached files

| file | filename |

|---|---|

| EX-31.2 - EX-31.2 - CU Bancorp | d916313dex312.htm |

| EX-31.1 - EX-31.1 - CU Bancorp | d916313dex311.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

Amendment Number 1

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

CU BANCORP

(Exact name of registrant as specified in its charter)

Commission File Number 001-35683

| California | 90-0779788 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 818 W. 7th Street, Suite 220 Los Angeles, California |

90017 | |

| (Address of principal executive offices) | (Zip Code) | |

(818) 257-7700

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(g) of the Act:

None

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, no par value, The NASDAQ Stock Market, LLC

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark whether the registrant is not required to file reports pursuant Section 13 or 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, if definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes ¨ No x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated Filer | x | |||

| Non Accelerated Filer | ¨ | Smaller Reporting Company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of June 30, 2014, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the voting and non-voting common equity held by non-affiliates was approximately $190.5 million based upon the closing price of shares of the registrant’s Common Stock, no par value, as reported by The NASDAQ Stock Market, LLC.

The number of shares outstanding of the registrant’s common stock (no par value) at the close of business on March 9, 2015 was 16,732,061

DOCUMENTS INCORPORATED BY REFERENCE

None

Table of Contents

EXPLANATORY NOTE

This amendment on the Annual Report on Form 10-K/A (the “Form 10-K/A”) amends CU Bancorp’s Annual Report on Form 10-K for the fiscal year ended December 31, 2014, as filed with the Securities and Exchange Commission (“SEC”) on March 13, 2015. This Form 10-K/A includes the previously incorporated by reference material from the Proxy Statement which was not filed within 120 days of year end. Except for Items 10, 11, 12, 13 and 14 of Part III no other information in this Form 10-K/A is being amended.

Table of Contents

| 13 | ||

| 38 | ||

| ITEM 13. CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS AND DIRECTOR INDEPENDENCE |

41 | |

| 41 | ||

| 43 |

Table of Contents

Forward Looking Statements

In addition to the historical information, this Annual Report on Form 10-K includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, (the “1933 Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “1934 Act”). Those sections of the 1933 Act and 1934 Act provide a “safe harbor” for forward-looking statements to encourage companies to provide prospective information about their financial performance so long as they provide meaningful, cautionary statements identifying important factors that could cause actual results to differ significantly from projected results.

The Company’s forward-looking statements include descriptions of plans or objectives of management for future operations, products or services, and forecasts of its revenues, earnings or other measures of economic performance. Forward-looking statements can be identified by the fact that they do not relate strictly to historical or current facts. They often include the words “believe,” “expect,” “intend,” “estimate” “anticipates,” “project”, “assume”, “plan”, “predict” or words of similar meaning, or future or conditional verbs such as “will,” “would,” “should,” “could” or “may.”

We make forward-looking statements as set forth above and regarding projected sources of funds, availability of acquisition and growth opportunities, dividends, adequacy of our allowance for loan and lease losses and provision for loan and lease losses, our loan portfolio and subsequent charge-offs. Forward-looking statements involve substantial risks and uncertainties, many of which are difficult to predict and are generally beyond our control. There are many factors that could cause actual results to differ materially from those contemplated by these forward-looking statements. Risks and uncertainties that could cause our financial performance to differ materially from our goals, plans, expectations and projections expressed in forward-looking statements include those set forth in our filings with the SEC, Item 1A of this Annual Report on Form 10-K, and the following:

| • | Current and future economic and market conditions in the United States generally or in the communities we serve, including the effects of declines in property values, high unemployment rates and overall slowdowns in economic growth. |

| • | Loss of customer checking and money-market account deposits as customers pursue other, higher-yield investments. |

| • | Possible changes in consumer and business spending and saving habits and the related effect on our ability to increase assets and to attract deposits. |

| • | Competitive market pricing factors. |

| • | Deterioration in economic conditions that could result in increased loan losses. |

| • | Risks associated with concentrations in real estate related loans. |

| • | Risks associated with concentrations in deposits. |

| • | Market interest rate volatility. |

| • | Possible changes in the creditworthiness of customers and the possible impairment of the collectability of loans. |

| • | Changes in the speed of loan prepayments, loan origination and sale volumes, loan loss provisions, charge offs or actual loan losses. |

| • | Compression of our net interest margin. |

| • | Stability of funding sources and continued availability of borrowings. |

| • | Changes in legal or regulatory requirements or the results of regulatory examinations that could restrict growth. |

| • | The inability of our internal disclosure controls and procedures to prevent or detect all errors or fraudulent acts. |

| • | Inability of our framework to manage risks associated with our business, including operational risk and credit risk, to mitigate all risk or loss to us. |

1

Table of Contents

| • | Our ability to keep pace with technological changes, including our ability to identify and address cyber-security risks such as data security breaches, “denial of service” attacks, “hacking” and identity theft. |

| • | The effects of man-made and natural disasters, including earthquakes, floods, droughts, brush fires, tornadoes and hurricanes. |

| • | Our ability to recruit and retain key management and staff. |

| • | Availability of, and competition for acquisition opportunities. |

| • | Risks associated with merger and acquisition integration. |

| • | Significant decline in the market value of the Company that could result in an impairment of goodwill. |

| • | Regulatory limits on the Bank’s ability to pay dividends to the Company. |

| • | New accounting pronouncements. |

| • | The impact of the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank Act”) and related rules and regulations on the Company’s business operations and competitiveness. |

| • | Our ability to comply with applicable capital and liquidity requirements (including the finalized Basel III capital standards), including our ability to generate capital internally or raise capital on favorable terms. |

| • | The effects of any damage to our reputation resulting from developments related to any of the items identified above. |

For a more detailed discussion of some of the risk factors, see the section entitled “Risk Factors” in the Company’s Form 10-K for the year ended December 31, 2014.

Forward-looking statements speak only as of the date they are made. The Company does not undertake to update forward-looking statements to reflect circumstances or events that occur after the date the forward-looking statements are made or to reflect the occurrence of unanticipated events. You should consider any forward looking statements in light of this explanation, and we caution you about relying on forward-looking statements.

2

Table of Contents

| ITEM 10. | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE |

Directors

The Bylaws of the CU Bancorp (the “Company” or “CUB”) provide that the number of directors shall not be less than nine or more than seventeen until changed by an amendment to the Articles of Incorporation or the Bylaws, leaving the Board of Directors with the authority to fix the exact number of directors within that range. The Board of Directors last fixed the exact number of directors at twelve.

Directors are elected annually for a term ending on the next annual shareholders’ meeting date.

The Board of Directors has determined that all of the current directors on the Board, except for Mr. Rainer, Mr. Horton and Mr. Cosgrove, are “independent,” as that term is defined by the rules and regulations of The NASDAQ Stock Market. These nine independent directors comprise a majority of the Board of Directors.

The following table lists the names and certain information as of April 15, 2015 regarding CUB’s directors. All the named individuals serve as directors of CU Bancorp and its subsidiary California United Bank.

| Name |

Age | Position with CUB |

Year First Appointed or Elected | |||

| Roberto E. Barragan |

54 | Director | 2004 | |||

| Charles Beauregard** |

67 | Director | 2014 | |||

| Kenneth J. Cosgrove |

67 | Vice Chairman California United Bank | 2012 | |||

| David Holman** |

66 | Director (Lead) | 2014 | |||

| K. Brian Horton** |

55 | Director and President | 2014 | |||

| Eric S. Kentor* |

56 | Director | 2014 | |||

| Jeffrey Leitzinger, Ph.D.** |

60 | Director | 2014 | |||

| David I. Rainer |

58 | Chairman, President and Chief Executive Officer | 2004 | |||

| Roy A. Salter |

58 | Director | 2004 | |||

| Daniel F. Selleck |

58 | Director | 2004 | |||

| Lester M. Sussman |

60 | Director | 2011 | |||

| Charles H. Sweetman |

72 | Director | 2004 |

| * | Appointed by the Board for a term commencing April 1, 2014 |

| ** | Appointed November 30, 2014 following acquisition of 1st Enterprise Bank |

CUB’s directors serve one-year terms. None of the directors or executive officers was selected pursuant to any arrangement or understanding, other than with the directors and executive officers of CUB acting within their capacities as such. There are no family relationships between the directors and executive officers of CUB. None of the directors or executive officers of CUB serve as directors of any company which has a class of securities registered under, or which are subject to the periodic reporting requirements of, the Securities Exchange Act of 1934, as amended, or any investment company registered under the Investment Company Act of 1940. None of the directors or executive officers of CUB have been involved in any legal proceedings during the past ten years that are material to an evaluation of the ability or integrity of any director or executive officer of CUB.

The following is the business experience of the members of CUB’s current board of directors:

Roberto E. Barragan. Mr. Barragan currently is President of the Valley Economic Development Center, Inc. (“VEDC”). He has served in various capacities with the VEDC since 1995. The VEDC is a 501(c)3 community based private non-profit corporation which offers training, consulting, technical assistance and financing to small- and medium-sized businesses. He was a founder of the Pacoima Development Federal Credit Union. Mr. Barragan is an expert on the needs of small businesses within CUB’s communities and assists significantly in the Community Reinvestment Act efforts of CUB. Mr. Barragan serves as the Community Reinvestment Act “CRA” Board Liaison, between the Bank’s CRA committee and the Board of Directors. Mr. Barragan is an expert on the needs of small businesses within the Company’s communities as well as lending, community development and government programs designed to assist in small business lending. His experience and community contacts provide him with the knowledge to assist significantly in the Community Reinvestment Act and small business lending efforts of California United Bank.

3

Table of Contents

Charles P. Beauregard. Mr. Beauregard has served as a director of the Company since November 30, 2014, following the merger of 1st Enterprise Bank with and into California United Bank. He was a director of 1st Enterprise Bank since its incorporation in 2006 and served as Chairman of the Director’s Loan Committee at 1st Enterprise as well as a member of the Compensation Committee, the Strategic and Capital Planning Committee, and the Governance Committee. Mr. Beauregard is a retired bank executive with over 30 years of commercial banking experience. Mr. Beauregard was formerly chief credit officer for Wells Fargo Bank’s Trust and Private Bank Group. Mr. Beauregard provides the benefit of his lengthy experience in the financial services industry and a bank director to the Company.

Kenneth J. Cosgrove. Mr. Cosgrove was previously the Chairman and Chief Executive Officer of Premier Commercial Bancorp and Premier Commercial Bank, N.A. and had served in that position since the formation. He has over 40 years of banking experience. He is currently also a member of the Board of Directors of the holding company for Pacific Coast Bankers Bank as well as Pacific Coast Bankers Bank, a bankers’ bank in San Francisco, CA and serves as the Chairman of the Board. Mr. Cosgrove as a former independent banker has extensive knowledge of the community banking industry and the Southern California banking market as well as SBA lending.

David C. Holman. Mr. Holman was previously the Chairman of the board of directors of 1st Enterprise Bank, serving since incorporation of 1st Enterprise since in February 2006 and was also a private investor throughout that period. He was Chairman of both the Strategic and Capital Planning Committee and the Nominating and Governance Committee, and a member of the Compliance and Compensation Committees of 1st Enterprise. Mr. Holman was formerly a senior executive at First Interstate Bank in Los Angeles and has been actively involved in the commercial banking industry for 40 years in California as a banker or investor. As a former banker and chairman of the board of a community bank, Mr. Holman brings experience in banking and corporate governance to the Company.

K. Brian Horton is President and a director of CU Bancorp and California United Bank. He previously served as the President and a director of 1st Enterprise since February 2006. Previously, he served as Division President of Mellon 1st Business Bank, from September 2004 to June 2005, and in various management positions at Mellon 1st Business Bank (and its predecessor, 1st Business Bank) from 1988 through June 2005, including Executive Vice President from 2003 to 2004, and Regional Vice President for the Orange County Regional Office from 1997 to 2003. Mr. Horton provides the Board with his banking and market expertise as well as additional insight into the Company’s loan and other business production activities.

Eric S. Kentor. Mr. Kentor is an attorney, independent business consultant and private investor working primarily with companies in the medical technology and clean tech, or “green” sectors. From 1995, until its purchase by Medtronic in 2001, Kentor served as Senior Vice President, General Counsel, and Corporate Secretary and as a permanent member of the Executive Management Committee at MiniMed Inc. The company was a world leader in the design, development, manufacture and marketing of advanced systems for the treatment of diabetes. Prior to MiniMed, Kentor served as Vice President of Legal Services for Health Net, California’s second-largest health maintenance organization, as well as Executive Counsel for its parent corporation. Previously, Kentor was a partner at the law firm of McDermott, Will & Emery. Kentor has also served as a director of both private and public companies, including Endocare, Inc., a publicly traded medical device company where he served as a director until the company was acquired in 2009. As an attorney experienced in corporate governance, Mr. Kentor provides legal and corporate governance expertise as well as experience as an executive officer and director of public companies.

Jeffrey J. Leitzinger, Ph.D. previously served as a director of 1st Enterprise since its incorporation in 2006. He was a member of the ALCO Committee, the Nominating and Governance Committee, and the Strategic and Capital Planning Committee. Dr. Leitzinger has been President and Chief Executive Officer of Econ One Research, Inc. in Los Angeles since 1997, and has been an economic consultant for over 30 years. Dr. Leitzinger is an economic expert and assists the Company in this area, including expertise in asset-liability management as well as community banking.

David I. Rainer. Mr. Rainer is Chairman of the board of directors and the Chief Executive Officer of CU Bancorp and California United Bank. He was previously California State President for US Bank and Executive Vice President of Commercial Banking for US Bank, in which capacity he led the commercial banking operations for US Bank in the Western United States, from Colorado to California. In February 1999, Mr. Rainer became President and Chief Executive Officer of Santa Monica Bank which was acquired by US Bank in November 1999. From 1992 to 1999, Mr. Rainer was an executive officer of California United Bank (not related to the current California United Bank), and its successor Pacific Century Bank, N.A., and served as Executive Vice President and then director, President and Chief Executive Officer. Mr. Rainer is a member of the Board of Directors of the Federal Reserve Bank of San Francisco, Los Angeles Branch. As the Company’s Chief Executive, Mr. Rainer provides the Board with essential information about the Company and management activities as well as leading initiatives intended to promote and enhance shareholder value.

4

Table of Contents

Roy A. Salter. Mr. Salter is a Senior Managing Director of FTI, LLC. Previously he was a Founding Principal of The Salter Group based in the Los Angeles Office where he co-managed the firm’s overall practice and project management efforts. The Salter Group was a leading independent financial and strategic advisory firm specializing in providing business and intangible asset valuations, financial opinions, financial and strategic analysis, forecasting, and transaction support covering a broad spectrum of industries and situations to both middle market and Fortune 500 companies and capital market constituents. The Salter Group combined with FTI in 2012. Mr. Salter brings financial analysis and valuation expertise to the Board as well as a background in bank marketing.

Daniel F. Selleck. Mr. Selleck is President of the Westlake Village-based Selleck Development Group, Inc. which specializes in the development and acquisition of commercial properties. That company has completed the development of more than 3.5 million square feet of property, with a value approximating $1 billion, including the development of the former General Motors Assembly Plant in Van Nuys, California. As a real estate expert, Mr. Selleck provides his expertise to CUB’s Directors’ Loan Committee and provides expertise in real estate lending and structure.

Lester M. Sussman. Mr. Sussman since 2005 has been a Senior Practice Director at Resources Global Professionals, a consulting firm that provides services to businesses throughout the world, where he specializes in providing corporate governance, risk management and compliance services and is the Western region practice leader for financial services. Prior to joining Resources Global Professionals, he was the Senior Vice President, Finance of Gemstar TV Guide International. Mr. Sussman is a Retired Partner of Deloitte & Touche, LLP, where he served as Partner in Charge, Financial Services Group – Los Angeles and Pacific Southwest Region. Mr. Sussman is a Certified Public Accountant. Mr. Sussman’s financial institution accounting expertise and corporate governance expertise provides support to CUB in these areas. Mr. Sussman is the Audit and Risk Committee designated financial expert and is Chairman of the Audit and Risk Committee.

Charles H. Sweetman. Mr. Sweetman is a managing partner of Sweetman Properties, LLC, a commercial income property company located in Palm Desert, California and also is the President and Chief Executive Officer of Sweetman Group, Inc. a property management and consulting firm. Mr. Sweetman provides strong entrepreneurial experience to the Board as well as significant business development skills. He is the Chairman of the Compensation, Nominating and Corporate Governance Committee. Mr. Sweetman provides leadership experience and entrepreneurial experience in founding and managing small-to-medium size businesses which is one of the Company’s target market.

Executive Officers

The following sets forth the names and certain information as of April 15, 2015 with respect to CUB’s executive officers (except for Mr. Rainer and Mr. Horton whose information is included above):

| Name |

Age | Position with CUB |

Year First Appointed | |||

| Anne A. Williams |

57 | Director – California United Bank, Executive Vice President, Chief Operating Officer / Chief Credit Officer | 2005 | |||

| Karen A. Schoenbaum |

52 | Executive Vice President and Chief Financial Officer | 2009 | |||

| Anita Y. Wolman |

63 | Executive Vice President, Chief Administrative Officer, General Counsel & Corporate Secretary1 | 2009 |

| 1 | Ms. Wolman was previously Senior Vice President Legal/Compliance and had served in that capacity since 2005. |

Anne A. Williams. Ms. Williams is a Director of California United Bank and Executive Vice President of CUB and has served in this capacity since January 2009 and October 2004, respectively. She is also Chief Operating Officer and Chief Credit Officer of CUB and has served in these capacities since April 2008 and October 2004, respectively. Prior to joining us, Ms. Williams served as Senior Vice President and Credit Risk Manager for US Bank’s Commercial Banking Market for the State of California.

5

Table of Contents

Ms. Williams was previously the Executive Vice President and Chief Credit Officer of Santa Monica Bank, which was acquired by US Bank in November 1999. Prior to joining Santa Monica Bank, Ms. Williams was the Executive Vice President and Chief Credit Officer at California United Bank (and its successor, Pacific Century Bank, N.A.) from 1992 to 1999.

Karen A. Schoenbaum, Executive Vice President and Chief Financial Officer has served as CUB’s Executive Vice President and Chief Financial Officer since October 2009. Prior to joining CUB, Ms. Schoenbaum was Executive Vice President and Interim Chief Financial Officer of Premier Business Bank in Los Angeles. She previously served as Executive Vice President and Chief Financial Officer of California National Bank from 2001 to 2008, where she was responsible for the financial and regulatory reporting, accounting, treasury, asset and liability management, general services and corporate real estate departments. From 1997, Ms. Schoenbaum was Executive Vice President, Chief Financial Officer and Chief Information Officer of Pacific Century Bank, N.A. a subsidiary of Bank of Hawaii Corporation.

Anita Y. Wolman, Executive Vice President, Chief Administrative Officer, General Counsel & Corporate Secretary was appointed Chief Administrative Officer in 2013 and Executive Vice President & General Counsel in January 2009. She previously was Senior Vice President Legal/Compliance beginning in 2005. Prior to joining CUB, Ms. Wolman was Senior Vice President, General Counsel & Corporate Secretary of California Commerce Bank (Citibank/Banamex USA). Earlier Ms. Wolman was Executive Vice President, General Counsel & Corporate Secretary of Pacific Century Bank, N.A. a subsidiary of Bank of Hawaii Corporation and its predecessor California United Bank.

There are no family relationships between any Director and an Executive Officer or among any Directors.

SECTION 16(a) BENEFICIAL OWNERSHIP REPORTING COMPLIANCE

Section 16(a) of the Securities Exchange Act of 1934, as amended, (the “Exchange Act”) requires the Company’s directors and executive officers, and persons who own more than 10% of a registered class of the Company’s equity securities, to file reports of ownership of, and transactions in, the Company’s equity securities with the SEC. Such directors, executive officers and 10% stockholders are also required to furnish the Company with copies of all Section 16(a) reports that they file. Based solely on a review of the copies of such reports received by the Company, and on written representations from certain reporting persons, the Company believes that except for a Form 4 filed late for K. Brian Horton due to an administrative error, all Section 16(a) filing requirements applicable to its directors, executive officers and 10% stockholders were complied with during 2014.

6

Table of Contents

CORPORATE GOVERNANCE PRINCIPLES AND CODE OF ETHICS

The Board of Directors is committed to good business practices, transparency in financial reporting and the highest level of corporate governance. In response to this, the Board has adopted formally the following Corporate Governance Guidelines:

Corporate Governance Guidelines

Our corporate governance guidelines provide for, among other things:

| • | A Board consisting of a majority of independent directors; |

| • | Periodic executive sessions of non-management directors; |

| • | An Audit and Risk Committee and a Compensation, Nominating and Corporate Governance Committee consisting entirely of independent directors; |

| • | Annual Performance Evaluation of the Board; |

| • | Director education and orientation; and |

| • | Ethical conduct of directors and adherence to a duty of loyalty to the Bank. |

In connection with our ongoing review of corporate governance and best practices, in March 2015, the Board appointed David Holman to the newly created position of Lead Independent Director. Mr. Holman was previously the Chairman of the Board of 1st Enterprise Bank and additionally brings many years of banking experience to this position. As Lead Director he will call and chair meetings of the independent and non-management directors, act as a liaison between the independent

The Board has adopted a Code of Ethics that applies to the Bank’s principal executive officer, principal financial officer, controller and principal accounting officer, or persons performing similar functions, as well as Principles of Business Conduct & Ethics that apply to its directors, officers and employees. A copy is available on the Company’s website at www.cunb.com or by contacting Anita Wolman, Corporate Secretary, at 15821 Ventura Boulevard, Suite 100, Encino, CA 91436. A copy will be provided without charge.

We also have an Insider Trading Policy which prohibits Directors and Senior Officers from the purchase or sale of puts, calls, options or other derivative securities based on the Company’s securities.

Director Resignation Policy

As part of its Corporate Governance Guidelines, the CU Bancorp board of directors has adopted a “Director Resignation Policy.” This policy provides that at any shareholder meeting at which directors are subject to an uncontested election, any nominee for director who receives a greater number of votes “withheld” from his or her election than votes “for” such election will then be required to tender a letter of resignation to the Chairman of the Board for consideration by the board’s Compensation, Nominating and Corporate Governance Committee which will thereafter recommend to the CU Bancorp board of directors the action to be taken with respect to such offer of resignation. The CU Bancorp board of directors will act no later than 90 days following the date of the shareholder meeting with respect to each such letter of resignation and will notify the director concerned of its decision and promptly publicly disclose such decision. Any director who tenders his or her resignation pursuant to this provision will not participate in any board or committee action regarding whether to accept his or her resignation offer.

7

Table of Contents

THE BOARD OF DIRECTORS AND COMMITTEES OF THE COMPANY

The Board of Directors of the Company oversees its business and monitors the performance of management. In accordance with corporate governance principles, our Board of Directors does not involve itself in day-to-day operations. The directors keep themselves informed through, among other things, discussions with the Chief Executive Officer, other key executives and our principal outside advisors (legal counsel, outside auditors, and other consultants), by reading reports and other materials that the Company sends them and by participating in Board and committee meetings.

During 2014, the board of directors of CU Bancorp held eleven meetings. During 2014, no director of the Company attended less than 75% of all Board meetings and the meetings of any committee of the Boards on which he or she served.

In 2014, the Board of Directors had the following committees: Audit and Risk Committee; Compensation, Nominating and Corporate Governance Committee, and Executive Committee. In addition California United Bank maintained a Board of Directors Loan Committee. The Audit and Risk Committee and the Compensation, Nominating and Corporate Governance Committee both consisted solely of independent directors.

Executive Sessions

Executive sessions of non-management directors are held by the Board on an “as needed” basis and at least annually. The executive sessions of non-management directors are chaired by the Vice Chairman of the Board, when there is one, or in his or her absence, a director chosen by the non-management directors. In March 2015 the Board appointed David Holman as the Lead Independent Director. In that role he will chair meetings of the independent directors at least twice annually.

Attendance at Annual Meetings

It is the policy of the Board to encourage directors to attend each Annual Meeting of Shareholders. Such attendance allows for direct interaction with shareholders. All of the Company’s directors attended the Company’s 2014 Meeting of Shareholders.

Reporting of Complaints/Concerns Regarding Accounting or Auditing Matters

The Company’s Board of Directors has adopted procedures for receiving and responding to complaints or concerns regarding accounting and auditing matters. These procedures were designed to provide a channel of communication for employees and others who have complaints or concerns regarding accounting or auditing matters involving the Company. Employee concerns may be communicated in a confidential or anonymous manner to the Audit and Risk Committee of the Board. The Audit and Risk Committee Chairman will make a determination on the level of inquiry, investigation or disposal of the complaint. All complaints are discussed with the Company’s senior management, as appropriate, and monitored by the Audit and Risk Committee for handling, investigation and final disposition. The Chairman of the Audit and Risk Committee will report the status and disposition of all complaints to the Board of Directors. No complaints were received during 2014.

Shareholder Communications With The Board

Shareholders wishing to communicate with the Board of Directors as a whole, or with an individual director, may do so by e-mail from the Bank’s or the Company’s website, www.cunb.com, or by writing to the following address:

CU Bancorp

15821 Ventura Boulevard, Suite 110

Encino, California 91436

Attention: Corporate Secretary

8

Table of Contents

Any communications directed to the Corporate Secretary will be forwarded to the entire Board of Directors, unless the Chairman of the Board reasonably believes communication with the entire Board of Directors is not appropriate or necessary or unless the communication is addressed solely to a specific committee or to an individual director.

Audit and Risk Committee and Board of Directors Risk Management

Board Authority for Risk Oversight

The Board has active involvement and responsibility for overseeing risk management of the Company arising out of its operations and business strategy. The Board monitors, reviews and reacts to material enterprise risks identified by management. The Board receives specific oral and written reports from officers with oversight responsibility for particular risks within the Company. Executive management reports include reporting on financial, credit, liquidity, interest rate, capital, operational, legal and regulatory compliance and reputation risks and the Company’s degree of exposure to those risks. The Board helps ensure that management is properly focused on risk by, among other things, reviewing and discussing the performance of senior management and business line leaders. Board committees also have responsibility for risk oversight in specific areas.

Audit and Risk Management Committee Oversight

The Company has a separately designated standing Audit and Risk Committee established in accordance with applicable regulatory and NASDAQ requirements. The Audit and Risk Committee also serves as the Audit and Risk Committee of California United Bank. The Audit and Risk Committee Charter adopted by the Board sets out the responsibilities, authority and specific duties of the Audit and Risk Committee. The Audit and Risk Committee must consist of at least three members, each of whom are non-management (independent) directors and each of whom must meet the independence and expertise requirements of the NASDAQ, the Sarbanes-Oxley Act of 2002 and rules promulgated thereunder, and other applicable rules and regulations. At least one member must have accounting or related financial management expertise and qualify as a “financial expert”, as defined under the regulations of the SEC. Pursuant to the Audit and Risk Committee Charter, the Audit and Risk Committee has the following primary duties and responsibilities:

| • | oversight of the quality and integrity of regulatory and financial accounting, financial statements, financial reporting processes and systems of internal accounting and financial controls; |

| • | oversight of the quality of compliance risk management and enterprise risk management; |

| • | oversight of the Company’s compliance with legal and regulatory requirements; |

| • | oversight of the annual independent audit of the Company’s financial statements and internal controls over financial reporting; engagement of the independent registered public accounting firm and evaluation of the qualifications, independence and performance of the independent registered public accounting firm; |

| • | approval of all audit and non-audit services permitted to be provided by the independent registered public accountants (other than those services that meet the requirements of any de minimus exception established by law or regulation); |

| • | oversight and retention of internal audit and/or outsourced internal audit services, as well as review of the performance of the internal auditors and review of all internal audit reports and follow up on citations, comments and recommendations; and |

| • | Preparation of an annual report substantially in compliance with the rules of the SEC with regard to companies subject to the Sarbanes-Oxley Act, to be included in the Company’s annual proxy statement, if applicable. |

9

Table of Contents

The Audit and Risk Committee is primarily responsible for overseeing the risk management function at the Company, on behalf of the Board. The Company’s Enterprise Risk Manager reports directly to the Audit and Risk Committee. Both the Bank’s Bank Secrecy Act and Compliance Officers also have direct reporting lines to the Audit and Risk Committee. The Audit and Risk Committee directs and employs third parties to conduct periodic reviews and monitoring of compliance efforts with a special focus on those areas that expose the Company to compliance risk. Among the purposes of the periodic monitoring is to ensure adherence to established policy and procedures. All reviews are reported to the Audit and Risk Committee, which regularly reports to the board of directors. The Audit and Risk Committee regularly meets with various members of management and receives reports on risk management and the processes in place to monitor and control such risk.

The Audit and Risk Committee has the authority to conduct any investigation appropriate to fulfilling its responsibilities and has direct access to the independent auditors, as well as to anyone in our organization. The Audit and Risk Committee has the ability to retain special legal or accounting experts, or such other consultants, advisors or experts it deems necessary in the performance of its duties and shall receive appropriate funding from the Company for payment of compensation to any such persons. The Audit and Risk Committee works closely with management and the Company’s independent registered public accounting firm. At December 31, 2014, the Audit and Risk Committee consisted of Messrs. Sussman (Chairman), Beauregard, Kentor, Leitzinger and Salter, each of whom was “independent” as defined by the rules and regulations of the NASDAQ Stock Market.

The board of directors has also determined that Mr. Sussman, who serves as the Chairman of the Audit and Risk Committee, is qualified as an “audit committee financial expert” and is “independent” as those terms are defined by the applicable rules and regulations of the Securities and Exchange Commission and the NASDAQ Stock Market. The designation of a person as an audit committee financial expert does not result in the person being deemed an expert for any purpose, including under Section 11 of the Securities Act of 1933. The designation does not impose on the person any duties, obligations or liability greater than those imposed on any other audit committee member or any other director and does not affect the duties, obligations or liability of any other member of the Audit Committee or Board of Directors.

The Audit and Risk Committee held 9 meetings during 2014. The Audit Committee regularly meets without members of management present.

Compensation, Nominating and Corporate Governance Committee and Bank Loan Committee Oversight

In addition to the Audit and Risk Committee, other committees of the board of directors of the Company and California United Bank consider the risks within their area of responsibility. For example, the Compensation, Nominating and Corporate Governance Committee reviews the risks that may be implicated by the Company’s executive and other compensation programs. For a discussion of that Committee’s review of executive officer compensation plans and employee incentive plans and the risks associated with these plans. See “Executive Compensation – Risk of Compensation Programs,” herein. The Bank’s Loan Committee reviews credit risk, portfolio quality and trends, as well as the results of and external credit review. The Compensation, Nominating and Corporate Governance Committee recommends director candidates with appropriate experience and skills who will set the proper tone for the Company’s risk profile and provide competent oversight over our material risks.

Audit and Risk Committee Report

The following report of the Audit and Risk Committee does not constitute soliciting material and should not be deemed filed or incorporated by reference into any of CU Bancorp’s other filings under the Securities Act or under the Exchange Act, except to the extent CU Bancorp specifically incorporates this report by reference.

The Audit and Risk Committee oversees CU Bancorp’s financial reporting process on behalf of the board of directors. The Audit and Risk Committee consists of five (5) members of the Board of Directors, each of whom is independent under the NASDAQ listing standards, SEC Rules and other regulations applicable to audit

10

Table of Contents

committees. In fulfilling its oversight responsibilities, the Audit and Risk Committee approved the engagement and retention of McGladrey LLP as CU Bancorp’s independent registered public accountants, reviewed and discussed with management and the external auditors the audited financial statements included in CU Bancorp’s Annual Report on Form 10-K filed with the Securities and Exchange Commission and the unaudited financial statements included in CU Bancorp’s Quarterly Reports on Form 10-Q filed with the Securities and Exchange Commission. The Audit and Risk Committee operates pursuant to a written charter that was most recently ratified in October 2014. A copy of the Audit and Risk Committee’s Charter may be obtained on CU Bancorp’s website at www.cubancorp.com under the section entitled “Corporate Governance.” The Audit and Risk Committee also oversees the performance of CU Bancorp’s internal audit function, including outsourcing of that function and review of reports.

Management is responsible for CU Bancorp’s financial reporting process including its system of internal controls, and for the preparation of financial statements in accordance with generally accepted accounting principles. CU Bancorp’s independent registered public accountants are responsible for auditing those financial statements.

The Audit and Risk Committee’s responsibility is to monitor and review these processes and procedures. The members of the Audit and Risk Committee are not professionally engaged in the practice of accounting or auditing. The Audit and Risk Committee has relied on the information provided and on the representations made by management regarding the effectiveness of internal controls over financial reporting, that the financial statements have been prepared with integrity and objectivity and that these financial statements have been prepared in conformity with generally accepted accounting principles. The Audit and Risk Committee also relies on the opinions of the independent registered public accountants on the financial statements and the effectiveness of internal controls over financial reporting. The Audit and Risk Committee’s oversight does not provide it with an independent basis to determine that management has maintained appropriate accounting and financial reporting principles or policies, or appropriate internal controls and procedures designed to assure compliance with accounting standards and applicable laws and regulations. Furthermore, its consultations and discussions with management and the independent public accountants do not assure that CU Bancorp’s financial statements are presented in accordance with generally accepted accounting principles, that the audit of CU Bancorp’s financial statements has been carried out in accordance with generally accepted auditing standards or that CU Bancorp’s independent registered public accountants are in fact “independent.”

In addition to approving the engagement and retention of the independent registered public accountants, the Audit and Risk Committee reviewed, met and discussed with the independent registered public accountants the matters required to be discussed by the statements on Auditing Standards (SAS) No. 16, as amended (Communication with Audit Committees) as adopted by the Public Company Accounting Oversight Board in Rule 3200T. These discussions included the clarity of the disclosures made therein, the underlying estimates and assumptions used in the financial reporting, and the reasonableness of the significant judgments and management decisions made in developing the financial statements. In addition, the Audit and Risk Committee received the written disclosures and the letter from the independent registered public accountants required by applicable requirements of the Public Company Accounting Oversight Board regarding the independent registered public accountants’ communications with the Audit and Risk Committee concerning independence, and has discussed with the independent registered public accountants their independence.

The Audit and Risk Committee has reviewed management’s report on its assessment of the effectiveness of internal control over financial reporting as of December 31, 2014 and the independent registered public accounting firm’s opinion on the effectiveness of CU Bancorp’s internal control over financial reporting and discussed these reports and opinions with management and the independent registered public accounting firm prior to CU Bancorp’s filing of its Annual Report on Form 10-K for the year ended December 31, 2014.

The Audit and Risk Committee also met and discussed with the independent registered public accountants issues related to the overall scope and objectives of the audit, CU Bancorp’s internal controls and critical accounting policies, and the specific results of the audit. Management was present at all or some part of each of these meetings. The Audit and Risk Committee also met with the independent registered public accountants without management. Lastly, the Audit and Risk Committee met with management and discussed the engagement of McGladrey LLP as CU Bancorp’s independent registered public accountants.

11

Table of Contents

During 2014, the Audit and Risk Committee met in open session and executive session with appropriate internal auditors or entities providing similar services, and McGladrey LLP to discuss the results of their examinations, observations and recommendations regarding financial reporting practices, the effectiveness of CU Bancorp’s internal controls and significant risks affecting CU Bancorp.

The Audit and Risk Committee also monitors and retains the Company’s outsourced internal audit program which is intended to objectively review and evaluate the adequacy, effectiveness and quality of the Company’s system of internal controls related to the reliability and integrity of its financial information and the safeguarding of its assets. The Risk Manager reports directly to the Audit and Risk Committee with regard to the internal audit function.

Pursuant to the reports and discussions described above, and subject to the limitations on the role and responsibility of the Audit and Risk Committee referred to above and in the Audit and Risk Committee’s charter, the Audit and Risk Committee recommended to the board of directors that the audited consolidated financial statements of CU Bancorp for 2014 be included in the Annual Report on Form 10-K for the fiscal year 2014 for filing with the SEC.

Respectfully submitted by the members of the Audit and Risk Committee:

| Lester M. Sussman, Chairman | ||||

| Charles Beauregard Eric Kentor Jeffrey Leitzinger, Ph.D. |

||||

| Roy Salter | ||||

| April 15, 2015 | ||||

The Audit and Risk Committee report shall not be deemed incorporated by reference by any general statement incorporating by reference this joint proxy statement/prospectus into any filing under the Securities Act or the Exchange Act, and shall not otherwise be deemed filed under these Acts.

Compensation, Nominating and Corporate Governance Committee

The Company has a separately designated Compensation, Nominating and Corporate Governance Committee (the “CNCG Committee”), which consists entirely of independent directors as defined by the rules and regulations of the SEC and the NASDAQ Stock Market. The CNCG Committee acts for both CU Bancorp and California United Bank. The members of the Compensation, Nominating and Corporate Governance Committee as of December 31, 2014 were Directors Sweetman (Chairman), Barragan, Kentor, Holman, and Selleck. Each member of the CNCG Committee is an independent director as defined by the requirements of the SEC and NASDAQ Stock Market.

The CNCG Committee has three areas of responsibility. The CNCG Committee is responsible for: (i) ensuring that compensation and benefits policies and programs for executive management and the board of directors of the Company comply with applicable law and stock exchange listing requirements, and are devised and maintained to provide and retain for the Company a high executive level of management and corporate governance competence; (ii) determining the nominees to the board of directors and their qualifications and reviewing performance of directors and committees of the board of directors annually; and (iii) ensuring compliance with the Sarbanes Oxley Act of 2002 relative to corporate governance and such other laws and regulations as may be applicable with regard thereto.

12

Table of Contents

Specifically with regard to compensation, the CNCG Committee is charged with overview of the Company’s compensation matters. The CNCG Committee reviews and approves our compensation philosophy and evaluates and determines CEO and executive officer compensation. It also reviews and approves compensation programs, plans and awards, and is responsible for administration of short-term and long-term incentive plans and other stock or stock based plans. The CNCG Committee is responsible for oversight of regulatory compliance with respect to compensation matters. In order to carry out its duties, the CNCG Committee has the ability to retain advisors to be used to assist the CNCG Committee in its duties.

With regard to nomination and governance functions the CNCG Committee recommends director nominees and appropriate policies and procedures for governance matters. The CNCG Committee has the following specific responsibilities: (i) to make recommendations as to size of the board of directors or any committee; (ii) identify potential board members; (ii) review the performance of the board and its members and committees at least annually; (iii) review the Corporate Governance Guidelines at least annually; (iv) review compliance with corporate governance requirements under applicable law and regulations of stock exchanges; (v) review the Code of Ethical Conduct and Business Practices annually and (vi) review all related party transactions, other than those which are directly reviewed by the Board of Directors.

Shareholders can obtain the CNCG Committee Charter upon request to: CU Bancorp, Corporate Secretary, 15821 Ventura Boulevard, Suite 100, Encino CA 91436. The CNCG Committee met nine (9) times during 2014.

ITEM 11. EXECUTIVE COMPENSATION

Compensation, Nominating and Corporate Governance Committee Interlocks and Insider Participation

None of the Company’s executive officers served on the CNCG Committee, or equivalent, of another entity, one of whose executive officers or board members served on our board of directors, and none of the members of the CNCG Committee serves or has served as an officer or employee of the Company.

COMPENSATION DISCUSSION AND ANALYSIS

EXECUTIVE COMPENSATION

This Compensation Discussion & Analysis (“CD&A”) describes our compensation practices and the executive compensation policies, decisions and actions of our Compensation, Nominating and Corporate Governance Committee (the “CNCG Committee”). We explain how the CNCG Committee determines compensation for our senior executives and its rationale for specific 2014 decisions. We also discuss numerous changes the CNCG Committee has made to our program in early 2015 to further advance its fundamental objective of aligning our executive compensation with the long-term interests of CU Bancorp shareholders. The CD&A focuses specifically on compensation for our named executive officers (“NEOs”) which included the following executives:

2014 Named Executive Officers

| Name |

Position | |

| David I. Rainer |

Chairman, Chief Executive Officer | |

| Brian Horton* |

President | |

| Anne Williams |

Executive Vice President, Chief Credit Officer, Chief Operating Officer | |

| Karen Schoenbaum |

Executive Vice President, Chief Financial Officer | |

| Anita Wolman |

Executive Vice President, Chief Administrative Officer, General Counsel |

| * | Mr. Horton became an NEO of the Company on December 1, 2014 following the Company’s acquisition of 1st Enterprise Bank. |

13

Table of Contents

EXECUTIVE SUMMARY

Summary and Corporate Governance

The CNCG Committee is composed entirely of independent directors and is responsible for reviewing and approving CU Bancorp’s overall compensation programs, plans and awards, including approving salaries, awarding bonuses and granting stock based compensation to the CU Bancorp NEOs and for formulating, implementing and administering CU Bancorp’s short-term and long-term incentive plans and other stock or stock-based plans. The CNCG Committee establishes the factors and criteria upon which the CU Bancorp NEOs’ compensation is based and how such compensation relates to CU Bancorp’s performance, general compensation policies, competitive realities and regulatory requirements. The CNCG Committee also provides recommendations regarding director compensation programs. The CNCG Committee also reviews CU Bancorp’s compensation plans for risk.

2014 Business Highlights

Following record quarterly and annual earnings for the fourth quarter and full year of 2013, resulting in California United Bank being designated as a “Super Premier” performing bank by The Findley Reports, 2014 was most notable for continued growth in core net income, loans and deposits as well as the acquisition of 1st Enterprise Bank (“1st Enterprise”) through the merger of 1st1st Enterprise with and into California United Bank on November 30, 2014. The execution by the management team of this strategic initiative in less than six months from announcement resulted in a bank with 11 full-service branches in four Southern California counties, $2.3 billion in assets, $1.6 billion in loans, and $1.9 billion in deposits at year end 2014. At December 31, 2014, we were one of only eleven (11) Southern California based community commercial banking institutions between $2 billion and $10 billion in total assets.

Following the acquisition of 1st Enterprise, K. Brian Horton, former President of 1st Enterprise, joined CU Bancorp as a director and as President of CU Bancorp and California United Bank. Four former members of the 1st Enterprise Board of Directors, David Holman, Brian Horton, Charles Beauregard, and Jeffrey Leitzinger, Ph.D., joined the CU Bancorp and California United Bank Boards of Directors, replacing retiring CU Bancorp Directors, Kenneth Bernstein and Robert Matranga. In addition, Eric Kentor, who has served as a director on the boards of privately and publicly held companies, was elected to the Boards of Directors of CU Bancorp and California United Bank effective April 1, 2014.

For the year ended December 31, 2014, core net income (net income available to common shareholders adding back net merger expenses and net severance and retention expenses) was $11.4 million, representing an increase of $1.6 million or 16.3% from 2013. The net interest margin increased for the fourth quarter of 2014 to 3.78% from 3.70% for the prior quarter. The provision for loan losses decreased $613,000 year over year, with the ratio of non-performing assets to total assets decreasing to 0.21% at December 31, 2014 from 0.68% at December 31, 2013. The Company’s 2014 efficiency ratio was 71% with core operating efficiency ratio (core non-interest expense as a percent of net interest income plus non-interest income) of 65% down from 68% for 2013. Non-interest bearing demand deposits were 53% of total deposits once again representing over one-half of all deposits and resulting in a cost of funds of 0.13% in the 4th Quarter of 2014, down from 0.16% in the 4th Quarter of 2013. Total Loans were $1.6 billion. Excluding the effect of the acquisition of 1st Enterprise, total loans increased $144.1 million or 15.4% from December 31, 2013, to December 31, 2014. Moreover, at year end 2014 the Company maintained its status as being well-capitalized, the highest regulatory category available.

It should be noted that the comparability of financial information for the fourth quarter and full year of 2014 to 2013, is affected by the Company’s acquisition of 1st Enterprise effective November 30, 2014. Operating results for fourth quarter and full year 2014 include the combined operations from December 1, 2014.

In 2014, CUNB stock price per share appreciated from $17.48 at January 1 to $21.69 at December 31, representing a 24% annualized increase in price per share. An initial investment in CUNB stock of $100 on December 31, 2009 would have been worth $199.91 at December 31, 2014.

14

Table of Contents

2014 Compensation Program Highlights

During 2014 the CNCG Committee, in addition to more routine matters, worked with its independent consultants (discussed below) to improve the Company’s ability to grant performance-based cash and equity incentives to executives and to more formally align NEO compensation to performance and shareholder value. Shareholders were presented and approved amendments to the 2007 Equity and Incentive Plan to (i) permit the grant of performance-based awards that are not subject to the deduction limitations of Section 162(m) of the Internal Revenue Code, including both equity compensation awards and cash bonus payments, (ii) prohibit the repricing of previously granted options; (iii) eliminate a provision in the plan that provides for an automatic annual increase in the shares of common stock available for awards under the plan; and (iv) extend the term of the plan to July 31, 2024.

Benchmarking studies were conducted and reviewed with regard to executive compensation and non-employee director compensation.

Following the acquisition of 1st Enterprise, the Committee approved a special grant of 20,000 shares of restricted stock to Mr. Horton, the new President of the Company (and the former President of 1st Enterprise) to provide him with incentive to continue in that position and to align his interests with shareholders by his participation in increases in shareholder value through those shares of restricted stock. In December of 2014, the CNCG Committee also made annual grants to CEO Rainer and Mses. Williams, Schoenbaum and Wolman in amounts of 13,300, 5,800, 3,700 and 3,700 shares of restricted stock, respectively. For 2014 these grants were based on a formula which established an annual value of the grant based upon a percentage of base salary ranging from 60% for CEO Rainer to 39%, 30% and 30% for each of Mses. Williams, Schoenbaum and Wolman, respectively. Also following the 1st Enterprise transaction, the CNCG Committee approved Mr. Horton’s participation in the Company’s 2012 Change in Control Plan at a multiple of two (2) times compensation (as defined in the 2012 Change in Control Plan).

No changes were made to base salaries of the executives during 2014, with the exception of Mr. Horton whose base salary was increased immediately following the 1st Enterprise acquisition to $340,000 from $282,000.

In addition the CNCG Committee reviewed the performance of executive management, determining that the members of executive management are critical to provide leadership to the Company and to lead the Company in the foreseeable future. The CNCG Committee believes it is of particular concern to retain and incentivize the members of the senior management most responsible for the success of the Company. Therefore the CNCG Committee began a study of appropriate methodologies to retain these executives and incent them to provide continued service while aligning their interests with shareholders

Looking Ahead to 2015

We are committed to continuously evaluating and improving the design of our executive compensation program with a view toward further aligning compensation with performance. In the first quarter of 2015, the CNCG Committee made fundamental modifications to the compensation structure for our NEOs with the following primary objectives:

| • | Strengthen the alignment of executive pay with our business and leadership strategies |

| • | Retain the key executive talent necessary to build on our past success and execute on our strategic objectives for the future |

| • | Emphasize accountability through prospective, measurable performance goals |

| • | Balance the need to encourage short-term profitability with the imperative to deliver long-term, sustainable results |

| • | Remain appropriately competitive as the Company continues to increase shareholder value through organic growth and execution of other selective growth opportunities |

Revised Compensation Peer Group: In light of the scale and complexity of the Company following the 1st Enterprise acquisition and recent organic growth, and to better inform the CNCG Committee’s deliberations and decisions regarding our executive compensation program for 2015, the CNCG Committee worked with its independent consultant to develop a new compensation peer group.

15

Table of Contents

Adoption of Management Incentive Plan: As previously noted, in July 2014 the Company amended its 2007 Equity and Incentive Plan to, among other items, provide for both performance-based cash and equity incentives which are intended to qualify for exceptions to the tax deductibility limitations of Internal Revenue Code Section 162(m). These amendments were approved by the Company’s shareholders in October 2014. The Committee anticipates that the 2007 Equity and Incentive Plan, as amended and restated July 31, 2014 (the “Equity and Incentive Plan”) will be the principal vehicle for providing performance-based cash and equity incentives to NEO’s going forward. In March 2015 the CNCG Committee adopted an annual management incentive plan (the “MIP”) under and pursuant to the Equity and Incentive Plan, as the centerpiece of our performance-based executive compensation program for 2015. The MIP is designed to deliver both cash and equity based incentives contingent on the achievement of pre-established performance goals which the CNCG Committee believes will drive superior long-term performance for the Company and improve the alignment of executive pay with performance. Under the MIP, more than 50% of Mr. Rainer’s target total direct compensation for 2015 is performance based, as compared to 24% in 2014. For the other NEOs, more than 40% of target total direct compensation will be directly tied to the achievement of pre-established goals, compared to roughly 23% in 2014.

Special One-Time Restricted Stock Awards: The CNCG Committee believes that retention of the current NEOs is critical to the future success of the Company. In order to better assure their retention, the CNCG Committee granted one-time special awards of restricted stock to Mr. Rainer, Ms. Williams, Ms. Schoenbaum, and Ms. Wolman in March 2015, similar in nature to the grant of restricted stock awarded to Mr. Horton upon his hire upon the close of the 1st Enterprise acquisition. These awards were structured with a vesting schedule designed to encourage retention over a particularly critical period for the Company following the 1st Enterprise acquisition and during which the Committee expects the Company may be well-positioned for continued growth.

Further discussion about each of the above changes to the NEO compensation program in 2015 is set out in the section below titled “Our Executive Compensation Program in Detail.”

Our Compensation Governance Practices & Policies

Our pay practices emphasize good governance and market practice.

| We do |

We do not | |||||||

| ü | Place an emphasis on variable compensation, which includes annual cash incentive awards dependent on the achievement of short-term financial goals | × | Offer compensation-related tax gross ups | |||||

| ü | Grant performance contingent equity awards | × | Provide significant perquisites | |||||

| ü | Have stock ownership requirements for directors; all NEOs are expected and do hold a significant position in Company common stock (not including vested stock options or unvested restricted stock) | × | Allow hedging, and trading in derivatives of Company securities | |||||

| ü | Have an executive compensation clawback policy to ensure accountability | × | Guarantee bonuses | |||||

| ü | Have an independent compensation consultant advising the CNCG Committee | × | Offer employment agreements | |||||

WHAT GUIDES OUR EXECUTIVE COMPENSATION PROGRAM

Our Compensation Philosophy

CU Bancorp’s compensation programs are designed, among other things, to emphasize the link between compensation and performance, taking into account competitive compensation levels in similar banks and in the markets where CU Bancorp competes for talent, as well as performance by the executive, their particular skills, background and expertise. The policies and underlying philosophy governing CU Bancorp’s compensation programs include the following:

16

Table of Contents

| • | Aligning pay with performance. CU Bancorp provides a competitive salary combined with incentive opportunities that create “leveraged” compensation, providing the opportunity for market to above-market total compensation for outstanding company and individual performance. A meaningful portion of annual executive compensation is related to factors that can affect the financial performance of CU Bancorp, and is designed to incentivize and reward performance that is expected to drive shareholder value. |

| • | Creating shareholder value through incentive opportunities. The CNCG Committee believes that the long-term success of CU Bancorp and its ability to consistently increase shareholder value is dependent on its ability to attract and retain skilled executives, particularly retaining and incentivizing those currently in place who have proved their value. CU Bancorp’s compensation strategy encourages equity-based compensation to align the interests of our shareholders and our executives, as well as performance incentive awards that are designed to reward performance that we expect will result in increased shareholder value. |

| • | Attracting and retaining highly-experienced executives. We strive to employ exceptional performers with experience not typically found in peer community banks. Executives are generally expected to have backgrounds and experience in larger regional or national banks or other similar levels of experience for their particular area of emphasis. We expect our executives to be responsible for the development and success of the organization, client development and shareholder relationships. CU Bancorp executives may also hold multiple positions and responsibilities, which increases their value to the Company and may make comparisons to peers less meaningful. |

| • | Mitigating risk. CU Bancorp uses a combination of short-term and long-term compensation. The latter is impacted by CU Bancorp’s performance and mitigates the benefit to executives from exposing CU Bancorp to short-term risks, as the value of the long-term compensation, particularly equity grants, is substantially impacted by CU Bancorp’s long-term performance. |

Our philosophy is supported by the following principle elements of pay in our executive compensation program:

| Pay Element |

Form |

Purpose | ||

| Base Salary |

Cash (Fixed) |

Provide a competitive level of pay that reflects the executive’s experience, role and responsibilities | ||

| Annual Incentives |

Cash (Variable) |

Reward achievement of individual and corporate performance goals for the most recently-completed fiscal year | ||

| Long-Term Incentives |

Equity (Variable) |

Drive financial performance that links to shareholder value creation and longer-term business strategies. | ||

NEOs are also eligible for other benefits, including salary continuation benefits and a qualified 401(k) Plan that provides participants with the opportunity to defer a portion of their compensation, up to tax code limitations, and may entitle NEOs to receive a company matching contribution. Modest ancillary benefits are also provided to executives by the Company. See below for more information.

Pay Mix

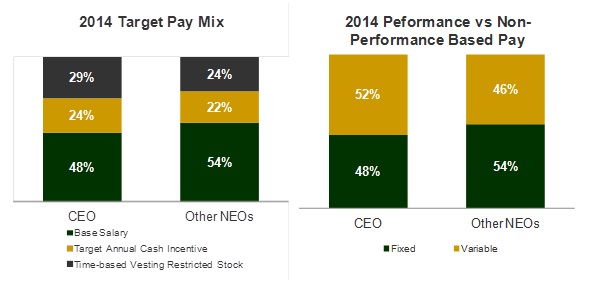

While the Summary Compensation Table sets forth annual compensation data in accordance with SEC requirements, the CNCG Committee considers additional perspectives beyond this format when evaluating our compensation program. This allows us to better understand how our annual pay opportunities and mix of pay elements compare to our competitors, as well as how compensation actually earned (rather than theoretically achievable) aligns with our performance.

The charts below show that most of our NEOs’ target total direct compensation for 2014 is variable (52% for our CEO and an average of 46% for our other NEOs). These charts exclude one-time sign-on awards, as well as the value of other benefits and perquisites.

17

Table of Contents

The Role of the Compensation, Nominating and Corporate Governance Committee

The CNCG Committee is composed entirely of independent directors and is responsible for reviewing and approving CU Bancorp’s overall compensation programs, plans and awards, including approving salaries, awarding bonuses and granting stock based compensation to the CU Bancorp NEOs. The CNCG Committee is also responsible for formulating, implementing and administering CU Bancorp’s short-term and long-term incentive plans and other stock or stock-based plans. The CNCG Committee establishes the factors and criteria upon which the CU Bancorp NEOs’ compensation is based and how such compensation relates to CU Bancorp’s performance, general compensation policies, competitive considerations and regulatory requirements. The CNCG Committee also provides recommendations to the Board regarding director compensation programs. The CNCG Committee also reviews CU Bancorp’s compensation plans for risk.

The Role of the CEO and Management

The CEO does not participate in the CNCG Committee’s determination of his own compensation. However, he makes recommendations to the CNCG Committee for each of the other NEOs. The CEO bases his recommendation on his assessment of each executive’s performance, as well as achievement of overall Company goals for the year. The CNCG Committee reviews the CEO’s recommendations, makes adjustments as it determines appropriate, and approves compensation at its sole discretion.

The Role of Consultants

In 2014, the CNCG Committee retained Pearl Meyer and Partners (“PM&P”) as its executive compensation consultant. In this role, PM&P provided advice regarding:

| • | Amendment to the 2007 Equity and Incentive Plan (approved by shareholders in October 2014) |

| • | The selection of the revised peer group used to assess the executive compensation program; |

| • | The compensation of the CEO and other NEOs; |

| • | General compensation program design; |

| • | The design of a special, one-time equity grant for long-term NEOs designed to help assure retention of key executives; |

| • | The impact of regulatory, tax, and legislative changes on CU Bancorp’s executive compensation program; |

| • | Executive compensation trends and best practices; and |

| • | The compensation practices of competitors. |

18

Table of Contents

During its engagement, PM&P met regularly with the CNCG Committee in executive session without management and has provided no other services to CU Bancorp. PM&P may work directly with management on behalf of the CNCG Committee, but this work is always under the control and supervision of the CNCG Committee. After the CNCG Committee’s review of applicable rules for independence, the CNCG Committee concluded that the advice it receives from PM&P is objective and does not raise any conflict of interest.

The Role of Benchmarking

When reviewing compensation components for the CU Bancorp NEOs and directors, the CNCG Committee considers as one element of analysis, the compensation practices of specific peer companies whose asset size, business type and geography are comparable to CU Bancorp and California United Bank. In April 2013, the CNCG Committee engaged EW Partners, Inc. (“EW”), an independent compensation consulting firm, to conduct a formal review of CU Bancorp’s executive and director compensation. In connection therewith, EW prepared a review of peer bank compensation and benefits of executive officers, assisting the CNCG Committee in determining appropriate peers, benchmarking and compensation ranges for executives. In selecting the peer group, the CNCG Committee considered other public banks and bank holding companies with assets from $1 billion to $3 billion located in California, Oregon and Washington. These companies were primarily chosen due to asset size and geography rather than similar business type. The CNCG Committee approved the following peer group of 20 publicly-traded financial institutions for purposes of benchmarking NEO compensation and informing compensation decisions that were made for 2014:

| Bank of Marin Bancorp | Home Street, Inc. | |

| BofI Holding Inc. | Pacific Continental Corp. | |

| Bridge Capital Holdings | Pacific Mercantile Bancorp | |

| Cascade Bancorp | Pacific Premier Bancorp, Inc. | |

| Farmers & Merchants Bancorp | Preferred Bank | |

| First California Financial Group | Provident Financial Holdings | |

| Hanmi Financial Group | Sierra Bancorp | |

| Heritage Commerce Corp | TriCo Bancshares | |

| Heritage Financial Corporation | Washington Banking Company | |

| Heritage Oaks Bancorp | Wilshire Bancorp, Inc. |

In September 2014, PM&P assisted the CNCG Committee in revising the peer group to more accurately reflect the size of the Company following the acquisition of 1st1st Enterprise and the growth trajectory of the Company. In selecting the peer group, the CNCG Committee considered public banking organizations with total assets from $1.4 billion to $5 billion headquartered in the western U.S. The CNCG Committee approved the following peer group of 17 publicly-traded financial institutions for purposes of benchmarking NEO compensation and informing compensation decisions for 2015:

| Banc of California, Inc. | Heritage Commerce Corp | |

| Bank of Marin Bancorp | Heritage Financial Corporation | |

| Banner Corporation | HomeStreet, Inc. | |

| Bridge Capital Holdings | National Bank Holdings Corporation | |

| Cascade Bancorp | Pacific Continental Corporation | |

| Central Pacific Financial Corp. | Pacific Premier Bancorp, Inc. | |

| CoBiz Financial Inc. | TriCo Bancshares | |

| Farmers & Merchants Bancorp | Westamerica Bancorporation | |

| Guaranty Bancorp |

OUR EXECUTIVE COMPENSATION PROGRAM IN DETAIL

2014 Base Salary

Base salary is the fixed annual compensation we pay to each NEO for performing specific job responsibilities and is based on their experience and requisite skills. Base salaries are determined for each NEO based on the executive’s position and responsibility. We review the base salaries for each NEO annually, as well

19

Table of Contents

as at the time of any promotion or significant change in job responsibilities, and in connection with each review, we consider individual and Company performance over the course of that year. The CNCG Committee did not adjust base salaries in 2014.

2014 Annual and Long-Term Incentives