Attached files

| file | filename |

|---|---|

| 8-K - 8-K - CITIZENS FINANCIAL GROUP INC/RI | d913224d8k.htm |

| EX-99.1 - EX-99.1 - CITIZENS FINANCIAL GROUP INC/RI | d913224dex991.htm |

| EX-99.3 - EX-99.3 - CITIZENS FINANCIAL GROUP INC/RI | d913224dex993.htm |

1Q15 Financial

Results April 22, 2015

Exhibit 99.2 |

Forward-looking statements

1

This document contains forward-looking statements within the Private Securities Litigation

Reform Act of 1995. Any statement that does not describe historical or current facts is a

forward-looking statement. These statements often include the words “believes,”

“expects,” “anticipates,” “estimates,” “intends,” “plans,” “goals,” “targets,” “initiatives,” “potentially,”

“probably,” “projects,” “outlook” or similar expressions or

future conditional verbs such as “may,” “will,” “should,” “would,” and “could.”

Forward-looking statements are based upon the current beliefs and expectations of

management, and on information currently available to management. Our statements speak as of the

date hereof, and we do not assume any obligation to update these statements or to update the

reasons why actual results could differ from those contained in such statements in light

of new information or future events. We caution you, therefore, against relying on any of

these forward-looking statements. They are neither statements of historical fact nor guarantees

or assurances of future performance. While there is no assurance that any list of risks and

uncertainties or risk factors is complete, important factors that could cause actual results to

differ materially from those in the forward-looking statements include the following,

without limitation: negative economic conditions that adversely affect the general economy, housing prices, the

job market, consumer confidence and spending habits which may affect, among other

things, the level of nonperforming assets, charge-offs and provision expense;

the rate of growth in the economy and employment levels, as well as general business and

economic conditions;

our ability to implement our strategic plan, including the cost savings and efficiency

components, and achieve our indicative performance targets;

our ability to remedy regulatory deficiencies and meet supervisory requirements and

expectations; liabilities resulting from litigation and regulatory investigations; our capital and liquidity requirements (including under regulatory capital standards, such as

the Basel III capital standards) and our ability to generate capital internally or

raise capital on favorable terms;

the effect of the current low interest rate environment or changes in interest rates on our

net interest income, net interest margin and our mortgage originations, mortgage

servicing rights and mortgages held for sale;

changes in interest rates and market liquidity, as well as the magnitude of such changes,

which may reduce interest margins, impact funding sources and affect the ability

to originate and distribute financial products in the primary and secondary markets;

the effect of changes in the level of checking or savings account deposits on our funding

costs and net interest margin;

financial services reform and other current, pending or future legislation or regulation that

could have a negative effect on our revenue and businesses, including the

Dodd-Frank Act and other legislation and regulation relating to bank products and

services; a failure in or breach of our operational or security systems or infrastructure, or those of

our third party vendors or other service providers, including as a result of cyber

attacks;

management’s ability to identify and manage these and other risks; and any failure by us to successfully replicate or replace certain functions, systems and

infrastructure provided by The Royal Bank of Scotland Group plc (RBS).

In addition to the above factors, we also caution that the amount and timing of any future

common stock dividends or share repurchases will depend on our financial condition,

earnings, cash needs, regulatory constraints, capital requirements (including requirements of

our subsidiaries), and any other factors that our board of directors deems relevant in

making such a determination. Therefore, there can be no assurance that we will pay any dividends to holders of our common stock, or as to the amount of any such dividends.

In addition, the timing and manner of the sale of RBS’s remaining ownership of our common

stock remains uncertain, and we have no control over the manner in which RBS may seek

to divest such remaining shares. Any such sale would impact the price of our shares of common stock.

More information about factors that could cause actual results to differ materially from those

described in the forward-looking statements can be found under “Risk Factors” in

Part I, Item 1A in our Annual Report on Form 10-K for the year ended December 31, 2014,

filed with the United States Securities and Exchange Commission on March 3, 2015.

Note: Percentage changes, per share amounts, and ratios presented in this document are

calculated using whole dollars. |

1Q15

highlights 2

Improving

profitability and

returns

GAAP diluted EPS of $0.38; Adjusted diluted EPS

1

of $0.39, up 30% from 1Q14

Adjusted ROTCE

1

of 6.7% vs. 5.2% in 1Q14

Adjusted operating leverage

1

of nearly 3% vs 1Q14

Strong capital,

liquidity, and

funding

Excellent credit

quality and

progress on risk

management

Continued progress

on strategic growth

and efficiency

initiatives

Robust capital levels with a Common Equity Tier 1 Ratio of 12.2%

with 2% growth from 4Q14 in tangible

book value/share

1

to $23.96

Average deposits grew $9.3 billion, or 7% vs 1Q14; Loan-to-deposit ratio of 96% (99%

on an average basis)

Received non-objection on 2015 CCAR submission

Supported successful $3.7 billion secondary offering, and in early April executed $250

million preferred stock offering and share repurchase

Continued strong credit quality with net charge-off ratio of 0.23%, down 12 bps from 4Q14

and 18 bps from 1Q14

Allowance for loan and lease losses of 1.27% of total loans and leases stable with 4Q14

NPLs as a % of total loans and leases of 1.20% stable with 4Q14

YoY average loan growth of 9% with strength in Commercial, Auto,

Mortgage

YoY average loan growth of $7.8 billion broadly on target with $3.8 billion in commercial,

$3.5 billion in auto, and a net $518 million across other portfolios

Progress in recruiting mortgage loan officers: 442 at quarter end, up 29 in 1Q15

YoY Adjusted noninterest expense

1

down modestly

–

initiatives on track; have achieved 32% of

targeted $200 million goal by end of 2016

1

Adjusted results are non-GAAP items and exclude the effect of net restructuring charges

and special items associated with Chicago Divestiture, efficiency and effectiveness programs

and separation from RBS. See important information on use of Non-GAAP items in the

Appendix. “Chicago Divestiture“ refers to the June 23, 2014 sale of the Chicago-area Charter

One branches, small business and select middle market relationships. |

Financial summary

– GAAP

3

1

Non-GAAP item. See important information on use of Non-GAAP items in the Appendix.

2

Includes held for sale.

3

Return on average tangible common equity.

4

Return on average total tangible assets.

5

Full-time equivalent employees.

Linked quarter:

Net income up 6%, reflecting positive

operating leverage and lower provision

expense

NII down modestly on fewer days in the

quarter

Continued earning asset growth

Noninterest income up $8 million on

strong mortgage banking income

Noninterest expense down $14 million

driven by $23 million decrease in

restructuring charges and special items

Investments to drive future growth

continue

Prior year quarter:

Net income up 26%

NII up 3% despite an estimated $13

million decrease tied to Chicago

Divestiture

8% average earning asset growth

Runoff of pay-fixed swap book

helped mitigate continued impact of

the low-rate environment

Noninterest income down 3% driven by

an estimated $12 million impact of the

Chicago Divestiture and $17 million

lower securities gains, partially offset by

underlying growth

Noninterest expense held flat

Provision decreased $63 million driven

by lower charge-offs/strong recoveries

Highlights

1Q15 change from

$s in millions

1Q15

4Q14

1Q14

4Q14

1Q14

$

%

$

%

Net interest income

836

$

840

$

808

$

(4)

$

—

%

28

$

3 %

Noninterest income

347

339

358

8

2 %

(11)

(3) %

Total revenue

1,183

1,179

1,166

4

—

%

17

1 %

Noninterest expense

810

824

810

(14)

(2) %

—

—

%

Pre-provision profit

373

355

356

18

5 %

17

5 %

Provision for credit losses

58

72

121

(14)

(19) %

(63)

(52) %

Income before income tax expense

315

283

235

32

11 %

80

34 %

Income tax expense

106

86

69

20

23 %

37

54 %

Net income

209

$

197

$

166

$

12

$

6 %

43

$

26 %

$s in billions

Average interest earning assets

121.3

$

118.7

$

112.5

$

2.6

$

2 %

8.8

$

8 %

Average deposits

2

95.6

$

94.8

$

91.6

$

0.8

$

1 %

4.0

$

4 %

Key metrics

Net interest margin

2.77

%

2.80

%

2.89

%

(3)

bps

(12)

bps

Loan-to-deposit ratio (period-end)

2

95.8

%

97.9

%

95.5

%

(205)

bps

36

bps

ROTCE

1,3

6.5

%

6.1

%

5.2

%

41

bps

129

bps

ROTA

1,4

0.7

%

0.6

%

0.6

%

4

bps

10

bps

Efficiency ratio

1

68

%

70

%

69

%

(139)

bps

(94)

bps

FTEs

5

17,792

17,677

18,856

115

1 %

(1,064)

(6) %

Per common share

Diluted earnings

0.38

$

0.36

$

0.30

$

0.02

$

6 %

0.08

$

27 %

Tangible book value

1

23.96

$

23.46

$

23.08

$

0.50

$

2 %

0.88

$

4 %

Average diluted shares outstanding

(in millions)

549.8

550.7

560.0

(0.9)

—

%

(10.2)

(2) % |

Restructuring

charges and special items 4

GAAP results included restructuring charges and special items related to enhancing

efficiencies and improving processes across the organization and separation from The

Royal Bank of Scotland Group plc (“RBS”). Expect

to

utilize

the

balance

of

the

Chicago

Divestiture

gain

to

continue

to

reinvest

to

drive

future

growth,

and

to

fund an additional $35-40 million of further restructuring charges and special expense

items in 2Q15. 1

See page 27 for additional details.

Restructuring

charges

and

special

items

1

1Q15 change from

($s in millions, except per share data)

1Q15

4Q14

1Q14

4Q14

1Q14

Pre-tax restructuring charges and special items

10

$

33

$

—

$

(23)

$

(70) %

10

$

NM

After-tax restructuring charges and special items

6

$

20

$

—

$

(14)

$

(70) %

6

$

NM

Diluted EPS impact

(0.01)

$

(0.03)

$

—

$

0.02

$

(67) %

(0.01)

$

NM |

1Q15 change

from $s in millions

1Q15

4Q14

1Q14

4Q14

1Q14

$

%

$

%

184

Net interest income

836

$

840

$

808

$

(4)

$

—

%

28

$

3 %

185

Noninterest income

347

339

358

8

2 %

(11)

(3) %

186

Total revenue

1,183

1,179

1,166

4

—

%

17

1 %

187

1

800

791

810

9

1 %

(10)

(1) %

188

Adjusted

pre-provision

profit

1

383

388

356

(5)

(1) %

27

8 %

189

Provision for credit losses

58

72

121

(14)

(19) %

(63)

(52) %

190

Adjusted

pretax

income¹

325

316

235

9

3 %

90

38 %

191

Adjusted

income

tax

expense

1

110

99

69

11

11 %

41

59 %

192

Adjusted

net

income

1

215

$

217

$

166

$

(2)

$

(1) %

49

$

30 %

s in billions

193

Average interest earning assets

121.3

$

118.7

$

112.5

$

2.6

$

2 %

8.8

$

8 %

194

Average

deposits

2

95.6

$

94.8

$

91.6

$

0.8

$

1 %

4.0

$

4 %

Key metrics

195

Net interest margin

2.77

%

2.80

%

2.89

%

(3)

bps

(12)

bps

109

Loan-to-deposit

ratio

(period-end)

2

95.8

%

97.9

%

95.5

%

(205)

bps

36

bps

197

Adjusted

ROTCE

1,3

6.7

%

6.8

%

5.2

%

(3)

bps

149

bps

198

Adjusted

ROTA

1,4

0.7

%

0.7

%

0.6

%

—

bps

12

bps

199

Adjusted

efficiency

ratio

1

68

%

67

%

69

%

54

bps

(178)

bps

200

FTEs

5

17,792

17,677

18,856

115

1 %

(1,064)

(6) %

Per common share

156

Adjusted

diluted

EPS

1

0.39

$

0.39

$

0.30

$

—

$

—

%

0.09

$

30 %

157

Tangible

book

value

1

23.96

$

23.46

$

23.08

$

0.50

$

2 %

0.88

$

4 %

158

Average diluted shares outstanding

(in millions)

549.8

550.7

560.0

(0.9)

—

%

(10.2)

(2) %

Adjusted

1Q15

financial

summary

-

excluding

restructuring

charges

and

special

items

5

1

Non-GAAP

item.

Adjusted

results

exclude

the

effect

of

net

restructuring

charges

and

special

items

associated

with

Chicago

Divestiture,

efficiency

and

effectiveness

programs

and

separation

from

RBS.

See

important

information

on

use of

Non-GAAP

items

in

the

Appendix.

2

Includes held for sale.

3

Return on average tangible common equity.

4

Return on average total tangible assets.

5

Full-time equivalent employees.

Linked quarter:

Adjusted net income broadly stable in seasonally

weaker quarter

Total revenue up $4 million

–

NII down $4 million driven by fewer days in the

quarter ($12 million impact)

–

NIM broadly stable with underlying 4Q14 results

–

Noninterest income up $8 million on mortgage

banking gain of $10 million, partially offset by

seasonal impacts

Adjusted noninterest expense increased 1%

–

Seasonally higher employee benefits and

continued investments to drive growth,

somewhat offset by the impact of efficiency

initiatives

Adjusted efficiency ratio up slightly

Provision expense down 19%

Prior year quarter:

Adjusted net income up 30% reflecting positive

operating leverage and a $63 million reduction in

provision expense

Total revenue up $17 million despite an estimated

$25 million impact of Chicago Divestiture

Adjusted efficiency ratio improved by 178 bps

Highlights

–

NII up 3% with 8% earning asset growth, and

NIM contraction of 12 bps

–

Noninterest income down 3%

–

Adjusted noninterest expense down 1%

driven by Chicago Divestiture impact

1

Adjusted noninterest expense

$ |

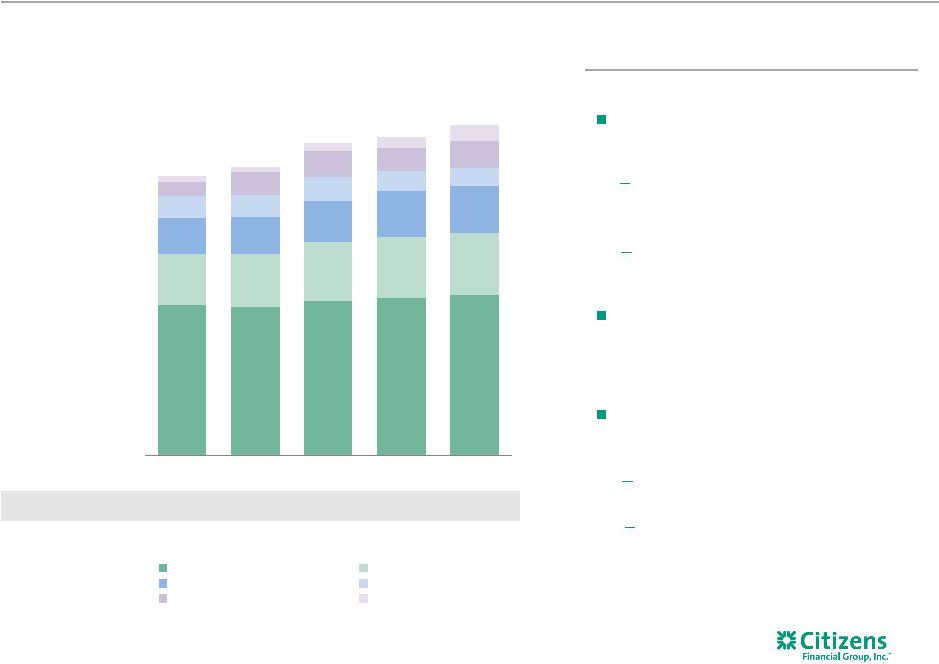

$s in

billions 1Q14

2Q14

3Q14

4Q14

1Q15

Retail loans

$46.4

$47.5

$48.5

$49.8

$50.4

Commercial loans

39.7

40.5

41.2

42.3

43.5

Investments and cash²

25.2

26.8

27.3

26.5

27.1

Loans held for sale¹

1.2

1.2

0.2

0.2

0.3

Total interest-earning assets

$112.5

$116.0

$117.2

$118.7

$121.3

Loan Yields

3.41%

3.40%

3.33%

3.34%

3.34%

Cost of funds

0.45%

0.43%

0.45%

0.49%

0.50%

$113B

$116B

$117B

$119B

$121B

$808

$833

$820

$840

$836

1Q14

2Q14

3Q14

4Q14

1Q15

2.89%

2.87%

2.77%

2.80%

2.77%

Net interest income

Linked quarter:

NII down modestly

Impact of two fewer days in the quarter

($12 million) and slightly higher borrowing and

deposit costs

Benefit of continued loan growth and a reduction

in pay-fixed swap costs

NIM remained relatively stable; down 3 bps to 2.77%

4Q14 included an estimated 2 bps non-recurring

benefit related to a securities portfolio duration

extension trade and reduction in excess cash

position

Benefit of loan growth and initiatives to improve

loan mix and lower swap costs broadly offset by

higher deposits

Prior year quarter:

NII up $28 million, or 3% despite an estimated $13

million impact from Chicago Divestiture, driven by

increased investment portfolio income and 9%

average loan growth

NIM declined 12 bps to 2.77% driven by the

continued impact of the low-rate environment

6

Highlights

Net interest income

$s in millions,

except earning

assets

Average interest-earning assets

Average interest earning assets

Net interest income

Net interest margin

$820

3

$795

3

1

2

3

1Q14 and 2Q14 include other loans held for sale associated with Chicago Divestiture. Includes

Interest-bearing cash and due from banks and deposits in banks

Represents estimated underlying net interest income adjusted for the effect of Chicago

Divestiture. |

Linked

quarter: Noninterest income up $8 million as gains

related to repositioning the mortgage and

securities portfolio offset seasonally lower

results in other categories

Mortgage banking fees up $17 million

driven by a $10 million gain on the sale of

conforming mortgages as well as higher

origination volumes

Other income reflects change in

accounting on low-income housing

investment portfolio

7

Highlights

1

Other income includes interest rate product fees, leasing income, bank owned life insurance,

and other income. $s in millions

$347

$339

$358

1Q15

4Q14

1Q14

Service charges and fees

Card fees

Trust and inv services

FX & trade finance fees

Mortgage banking fees

Capital markets fee income

Securities gains (losses)

Other income

Prior year quarter:

Noninterest income down $11 million

•

$17 million decrease in securities gains

•

$12 million estimated decrease tied to

Chicago Divestiture

•

Underlying fee growth estimated at 5%

Noninterest income

Strength in capital markets fees and

higher FX & trade finance fees and

underlying momentum in other core

fees more than offset by

1Q14 change from

$s in millions

1Q15

4Q14

1Q14

4Q14

1Q14

$

%

$

%

215

Service charges and fees

135

$

144

$

139

$

(9)

$

(6) %

(4)

$

(3) %

216

Card fees

52

58

56

(6)

(10) %

(4)

(7) %

217

Trust & investment services fees

36

38

39

(2)

(5) %

(3)

(8) %

218

FX & trade finance fees

23

25

22

(2)

(8) %

1

5 %

219

Mortgage banking fees

33

16

20

17

106 %

13

65 %

220

Capital markets fees

22

25

18

(3)

(12) %

4

22 %

221

Securities gains, net

8

1

25

7

700 %

(17)

(68) %

222

Other income

1

38

32

39

6

19 %

(1)

(3) %

225

Noninterest income

347

$

339

$

358

$

8

$

2 %

(11)

$

(3) % |

$800

$791

$810

68%

67%

69%

1Q15

4Q14

1Q14

Adjusted salary and benefits

Adjusted occupancy & equip

Adjusted all other

Adjusted efficiency ratio

Adjusted noninterest expense –

excluding restructuring charges and special items

1

Linked quarter:

Adjusted noninterest expense up

$9 million driven by seasonal impacts

Adjusted salaries and benefits up

$24 million driven by the impact of

seasonally higher payroll taxes and

incentives expense

•

FTEs up 115 reflecting continued

investments to drive growth and

effectiveness

Virtually all other expense categories

reflect strong cost control

Efficiency initiatives drove incremental cost

savings of $9 million vs. 4Q14

8

Highlights

1

Non-GAAP item. Adjusted results exclude the effect of net restructuring charges and

special items associated with Chicago Divestiture, efficiency and effectiveness

programs and separation from RBS. See important information on use of Non-GAAP items in the Appendix. Additional details on

restructuring charges and special items provided on page 27.

2

Excludes restructuring charges and special items.

.

2

2

change from

$s in millions

1Q15

4Q14

1Q14

4Q14

1Q14

Adjusted

salaries

and

benefits

1

420

$

396

$

405

$

24

$

6 %

15

$

4 %

Adjusted

occupancy

1

78

76

81

2

3 %

(3)

(4) %

Adjusted equipment expense

62

62

64

—

—

%

(2)

(3) %

Adjusted

outside

services

1

71

88

83

(17)

(19) %

(12)

(14) %

Adjusted

amortization

of

software

36

37

31

(1)

(3) %

5

16 %

Adjusted

other

expense

1

133

132

146

1

1 %

(13)

(9) %

Adjusted noninterest expense

800

$

791

$

810

$

9

$

1 %

(10)

$

(1) %

Restructuring charges and special items

10

33

—

(23)

(70) %

10

NM

Total noninterest expense

810

$

824

$

810

$

(14)

$

(2) %

—

$

—

%

Prior year quarter:

Adjusted noninterest expense decreased $10

million as an estimated $21 million decrease

related to the Chicago Divestiture was more

than offset by net investments to drive growth

and effectiveness as well as regulatory

improvements

FTEs down 1,064 reflecting the impact of the

Chicago Divestiture and various efficiency

initiatives, partially offset by investments in

growth initiatives

1

1

1 |

1Q15 change

from $s in billions

1Q15

4Q14

1Q14

4Q14

1Q14

$

%

$

%

265

Investments and interest bearing

deposits

27.1

$

26.5

$

25.2

$

0.6

$

2 %

1.9

$

8 %

266

Total commercial loans

43.5

42.3

39.7

1.2

3 %

3.8

10 %

267

Total retail loans

50.4

49.8

46.4

0.7

1 %

4.0

9 %

268

Total loans and leases

94.0

92.0

86.1

1.9

2 %

7.8

9 %

269

Loans held for sale

0.3

0.2

1.2

0.1

43 %

(0.9)

(73) %

270

Total interest-earning assets

121.3

118.7

112.5

2.6

2 %

8.8

8 %

271

Total noninterest-earning assets

12.0

11.9

11.4

—

— %

0.6

5 %

272

Total assets

133.3

$

130.7

$

123.9

$

2.6

$

2 %

9.4

$

8 %

273

Low-cost core deposits¹

49.8

49.7

45.8

0.1

— %

4.1

9 %

274

Money market deposits

33.6

33.2

31.3

0.5

1 %

2.4

8 %

275

Term deposits

12.2

11.9

9.3

0.3

2 %

2.9

31 %

Held for sale

—

—

5.2

—

— %

(5.2)

(100) %

276

Total deposits

95.6

$

94.8

$

91.6

$

0.8

$

1 %

4.0

$

4 %

277

Total borrowed funds

15.5

14.0

10.7

1.5

11 %

4.8

44 %

278

Total liabilities

113.9

$

111.5

$

104.5

$

2.4

$

2 %

9.4

$

9 %

279

Total stockholders' equity

19.4

19.2

19.4

0.2

1 %

—

— %

280

Total liabilities and equity

133.3

$

130.7

$

123.9

$

2.6

$

2 %

9.4

$

8 %

Consolidated 1Q15 average balance sheet

Linked quarter:

Total earning assets up 2%

Commercial loans up $1.2 billion, given

strength in Industry Verticals, Middle

Market, Mid-Corporate and Commercial

Real Estate

Retail loans up $664 million driven by

growth in auto, mortgage, and student

Total deposits increased 1%

Growth focused on commercial

relationships and consumer term deposits

Total earning assets up 8%

Retail loans up 9% driven by growth in auto,

mortgage and student

Commercial loans up 10% due to growth in

Mid-Corporate, Commercial Real Estate,

Franchise Finance and Industry Verticals

Total deposits up $4.0 billion reflecting

strength in low-cost core deposits and term

deposits

Borrowed funds up $4.8 billion reflecting

sub-debt issuance tied to our capital

exchange transactions, as well as senior

debt issuance and FHLB borrowings to fund

balance sheet growth

9

Highlights

$121.3 billion

Interest-earning assets

$111.2 billion

Deposits/borrowed funds

Total

Retail

42%

Total

Commercial

36%

1

Low-cost core deposits include demand, checking with interest, and regular savings.

2

Total deposits includes deposits held for sale.

CRE

Other

Commercial

Residential

mortgage

Total home

equity

Automobile

Other

Retail

Investments

and

interest-bearing

deposits

Retail /

Personal

Commercial/

Municipal/

Wholesale

Borrowed

funds

17%

6%

30%

10%

17%

11%

4%

22%

50%

37%

13%

Prior year quarter: |

$8.7

$9.2

$9.9

$10.6

$10.9

$19.9

$19.7

$19.1

$18.8

$18.4

$9.3

$10.5

$11.4

$12.4

$12.9

$1.9

$1.8

$1.6

$1.8

$2.3

$3.3

$3.2

$3.0

$3.0

$3.1

$2.9

$2.8

$2.7

$2.6

$2.5

$46.0B

$47.2B

$47.7B

$49.2B

$50.1B

1Q14

2Q14

3Q14

4Q14

1Q15

Mortgage

Home Equity

Auto

Student

Business Banking

Other

Consumer Banking average loans and leases

Linked quarter:

Average loans increased $890 million, or 2%

Net average impact of loan purchases and sales of

$382 million; average impact of purchases was an

increase of $269 million in auto, $191 in student

and a decrease of $79 million in mortgages

Consumer loan yields up 4 basis points reflecting

some variability in auto and student

Prior year quarter:

Average loans up $3.8 billion largely as growth in

auto of $3.3 billion, mortgage of $2.2 billion and

student of $0.4 billion was partially offset by lower

home equity outstandings ($1.5 billion)

Average yields up modestly as improvement in

auto and student was partially offset by the

continued effect of the low-rate environment

10

Highlights

1

Excludes held for sale.

2

Other includes Credit Card, RV, Marine, Other.

Average

loans

$s in billions

Yields

3.71 %

3.70 %

3.67 %

3.68 %

3.72 %

1

2

1 |

$5.4

$5.6

$5.9

$6.0

$6.3

$2.1

$2.2

$2.1

$2.5

$2.9

$2.3

$2.5

$2.7

$2.8

$2.9

$12.4

$12.4

$11.8

$11.7

$12.0

$5.8

$5.8

$6.1

$6.3

$6.1

$6.6

$6.7

$7.0

$7.2

$7.4

$2.0

$2.2

$2.2

$2.5

$2.6

$36.6B

$37.4B

$37.8B

$38.9B

$40.2B

1Q14

2Q14

3Q14

4Q14

1Q15

Mid-Corporate

Industry Verticals

Franchise Finance

Middle Market

Asset Finance

Commercial Real Estate

Other

Commercial Banking average loans and leases

Linked quarter:

Average loans up $1.3 billion, or 3% on

strength in Industry Verticals, Middle Market,

Mid-Corporate and Commercial Real Estate

Loan yields decreased 5 bps, reflecting 4Q14

impacts that included higher loan fees and

interest recoveries, as well as the continued

effect of the low-rate environment

Prior year quarter:

Average loans up $3.7 billion on strength in

Commercial Real Estate, Industry Verticals,

Mid-Corporate and Franchise Finance

Loan yields down 13 bps largely reflecting

continued impact of low-rate environment

11

Highlights

1

Other includes Business Capital, Govt & Professional Banking, Corporate Finance &

Global Markets, Treasury Solutions, Corporate and Commercial Banking Admin. $s in

billions Average loans

Yields

2.71 %

2.67 %

2.61 %

2.63 %

2.58 %

1 |

$72.3B

$74.8B

$80.8B

$82.5B

$85.4B

$1.4

$1.4

$2.0

$2.8

$3.9

$3.6

$6.0

$6.7

$6.1

$7.0

$5.7

$5.7

$6.3

$5.1

$4.6

$9.3

$9.4

$10.6

$11.9

$12.2

$13.3

$13.8

$15.2

$15.7

$16.0

$38.9

$38.4

$40.1

$40.9

$41.7

1Q14

2Q14

3Q14

4Q14

1Q15

Money market & savings

Checking with interest

Term & time deposits

Total fed funds & repo

Short-term borrowed funds

Total long-term borrowings

Average funding and cost of funds

Linked quarter:

Average interest-bearing deposits increased

$1.4 billion, or 2%, with growth in nearly

every category

Term deposits up $292 million, money

market & savings up $810 million,

interest checking up $321 million

Total deposit costs increased 2 bps to

0.22%, reflecting shift in mix to longer

duration deposits

Continued progress in repositioning

liabilities structure to better align with peers

12

Highlights

Average interest-bearing liabilities

$s in billions

1

Interest-bearing liabilities costs excluding deposits held for sale.

Prior year quarter:

Average interest-bearing deposits

increased $8.3 billion, or 14%, on strength

across all categories

Cost of funds (excluding HFS) increased

4 bps

Interest-bearing deposits including HFS

were up $4.1 billion, or 6%, as the

Chicago Divestiture impact of $5.2

billion was offset by strong overall

growth

Total cost of funds

1

0.46%

0.44%

0.45%

0.49%

0.50%

1 |

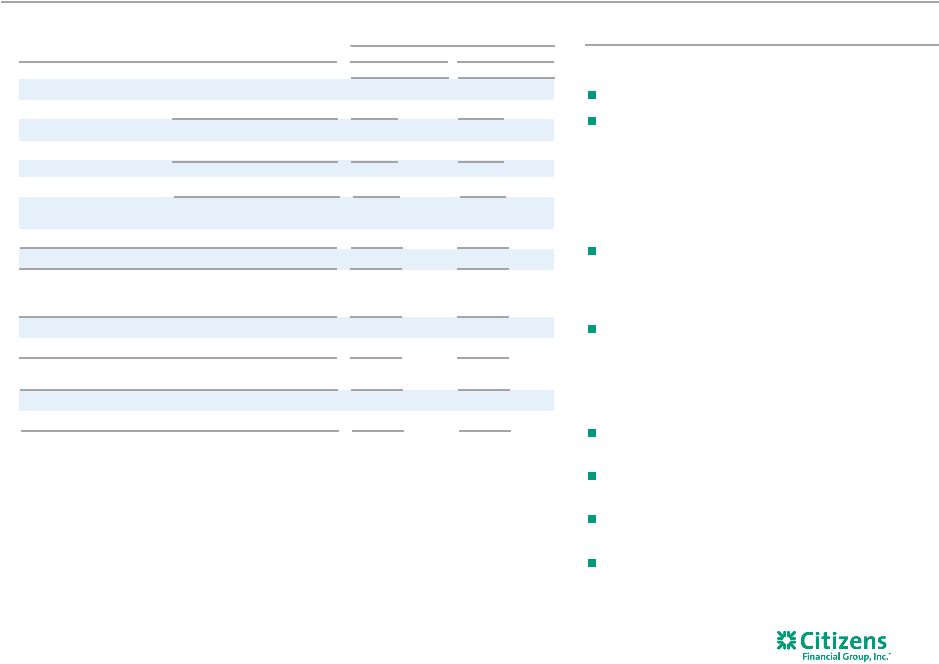

Strong credit

quality trends continue Overall credit quality remains strong

Net charge-offs were $54 million, or 0.23% of average loans and leases

Commercial net recoveries were $22 million in 1Q15, including a large

recovery of $15 million (previously expected to occur in 2Q15)

Provision for credit losses of $58 million decreased $14 million

vs. 4Q14

driven by a single large commercial real estate recovery

Results reflect reserve build of $4 million vs. $8 million release in 4Q14

Allowance as a % of total loans and leases stable, 1.27% vs. 1.28% in 4Q14

NPLs to total loans stable, 1.20% vs. 1.18% in 4Q14

Allowance coverage for NPLs 106% vs. 109% in 4Q14

13

Highlights

Net charge-offs (recoveries)

Provision for credit losses, charge-offs, NPLs

Allowance for loan and lease losses

$s in millions

1

Allowance for loan and lease losses to nonperforming loans and leases.

|

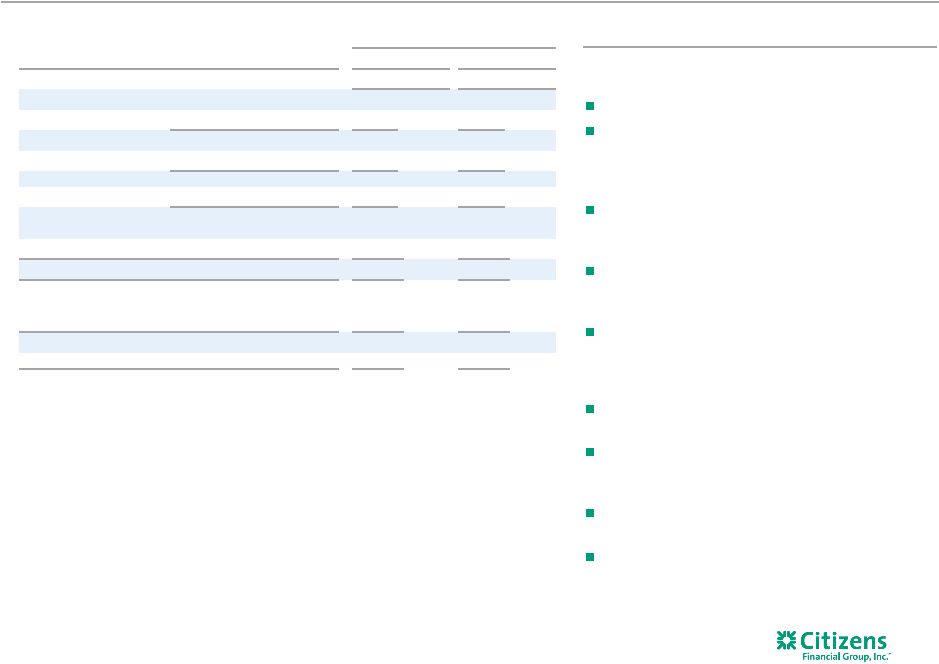

as of

$s in billions (period-end)

1Q14

2Q14

3Q14

4Q14

1Q15

Basel I/III transitional basis

1,2

Basel I

Basel III

Common equity tier 1 capital

13.5

$

13.4

$

13.3

$

13.2

$

13.4

$

Risk-weighted assets

100.4

$

101.4

$

103.2

$

106.0

$

109.8

$

Common equity tier 1 risk-based

capital ratio

13.4 %

13.3 %

12.9 %

12.4 %

12.2 %

Total risk-based capital ratio

16.0 %

16.2 %

16.1 %

15.8 %

15.5 %

Basel III fully phased-in

1,2,3

Common equity tier 1 risk-based

capital ratio

13.1%

13.0%

12.5%

12.1%

12.1%

Basel III minimum for CET1 ratio

2015

2016

2017

2018

2019

Basel III minimum plus

Phased-in capital conservation buffer

4.5 %

5.1 %

5.8 %

6.4 %

7.0 %

Capital and liquidity remain strong

14

Highlights

Loan-to-deposit ratio

5

Capital ratio trend

Capital levels remain well above regional peers

1Q15 Basel III common equity tier 1 ratio

(transitional basis) down approximately 26

basis points from 4Q14

Net income: 19 bps increase

RWA growth: 44 bps decrease

Dividends/other: 1 bp decrease

As part of plan to adjust capital mix, in early

April we completed a $250 million preferred

stock offering and repurchased 10.5 million

common shares at a price of $23.87 per share

Reduced pro forma 3/31/15 CET1 risk-

based capital ratio by 23 bps

LDR remained relatively stable at 96% (99% on

average basis)

Already meet initial LCR requirement

4

1

2

3

4

5

Current reporting period regulatory capital ratios are preliminary. Periods prior to 1Q15

reported on a Basel I basis. Basel III ratios assume that certain definitions impacting qualifying Basel III capital will phase in

through 2018. Ratios also reflect the required US Standardized methodology for calculating

RWAs, effective January 1, 2015.

Non-GAAP item. See important information on use of Non-GAAP items in the Appendix. Based on the September

2014 release of the U.S. version of the Liquidity Coverage Ratio (LCR). Note that as a modified LCR company, CFG’s formal

compliance requirement of 90% does not begin until January 2016. Period-end Includes

held for sale. |

Delivered for all

stakeholders in Q1 15

Customers

2014 Greenwich Middle Market Banking Excellence Awards in the Northeast for overall/Client

satisfaction Citizens’

mobile

apps

recognized

for

two

years

in

a

row

as

among

the

best

in

the

industry

by

Javelin

Strategy & Research, with average customer ratings of 4.2 out of

5 stars

Consumer Banking continues to make progress in customer experience as measured internally and

through JD Power assessments

Colleagues

Announced Eric Aboaf as new CFO and Don McCree as Vice-Chair, Head of Commercial

Developed ambitious agenda around leadership standards, employee

training and cultural initiatives

Continue to attract high quality talent in areas of focus

Community

Received prestigious Consumer Bankers Association’s Award in recognition of our

“Citizens Helping Citizens Manage Money”

initiative

Partnered in Cleveland to launch and support citywide initiative

to improve the economic security of

residents

Shareowners

Tracking well overall on key turnaround initiatives

Financial performance broadly in line with expectations

Continue work on further revenue and expenses initiatives

Supported RBS successful sell down of 155 million shares ($3.7 billion)

Regulators

Successful CCAR effort, already working on next year

Making steady progress on broader regulatory remediation effort

Focused on resolving older enforcement matters

Objective is to become a top-performing regional bank |

Summary of

progress on strategic initiatives 16

INITIATIVE

1Q15

Status

2015

Outlook

Commentary

Reenergize household growth

1Q15 YoY checking households up 2%; new customer cross-sell rate

improved to 3.3 vs. 2.9 in 1Q14

Expand mortgage sales force

LOs up 84, or 23%, from 1Q14; Origination volume up 87% over 1Q14

given strong refinance activity

Grow Auto

Continued level of robust loan growth with portfolio up $3.2B, or 32%,

from 1Q14; balanced mix of organic and purchased loan growth

Grow Student

Strong new refinance product originations of $293 million in 1Q15; new

Parent loan product launched in mid-April

Expand Business Banking

Origination volume of $152mm in 1Q15 up 67% vs. 1Q14

Expand Wealth sales force

Added 28 wealth managers and 198 licensed bankers over the past year

(overall growth 38%); Competitive hiring environment continues

Build out Mid-Corp & verticals

Mid-Corp and specialty verticals grew YoY outstanding balances by 15%

and 41%, respectively

Continue development of Capital

Markets

Overall Middle Market League Table ranking rose to number 5 in 1Q15,

compared to number 9 in 4Q14 and 12 in 1Q14

Build out Treasury Solutions

Beginning to see ramp up in benefits from recent people and technology

investments driven by core cash management product

Grow Franchise Finance

Strong client acquisition efforts with a 16% increase in customers in 1Q15

vs. 1Q14 driving origination growth of 19% over the same period

Core: Middle Market

Originations

up

6%

in

1Q15

vs.

1Q14,

with

commitment

pipeline

up

over

20% YoY; continue to see competitive pricing environment

Core: CRE

CRE loans up 14% YoY to $7.9 billion at 1Q15

Core: Asset Finance

New business initiatives progressing with origination activity in 1Q15 up

9% compared to 1Q14

1

Thomson Reuters LPC, 1Q15 data based on number of deals for Overall Middle Market (defined as

Borrower Revenues < $500MM and Deal Size < $500MM). 1

2

3

4

5

6

7

8

9

10

11a

11b

11c

1 |

Steady progress

against key financial targets 17

Key Indicators

1Q14

1Q15

End 2016

targets

Adjusted return on average tangible common

equity

5.2%

6.7%

10%+

Adjusted return on average total tangible

assets

0.6%

0.7%

1.0%+

Adjusted efficiency ratio

69%

68%

~60%

CET 1 risk-based capital ratio

13.4%

12.2%

~11%

Delivering on our plan to improve returns

1

Note: Financial targets assume that interest rates will evolve consistent with the market

implied forward rates based on the yield curve as of February 28 2014, and that

macroeconomic and competitive conditions are consistent with those used in our planning

assumptions. 1

1

1

2

3

2

3

Non-GAAP item. Adjusted results exclude the effect of net restructuring charges and

special items associated with Chicago Divestiture, efficiency and effectiveness

programs and separation from RBS. See important information on use of Non-GAAP items in the Appendix.

Current reporting period regulatory capital ratio is preliminary and based on Basel III

transitional rules. Periods prior to 1Q15 reported on a Basel I basis. Basel III ratios

assume that certain definitions impacting qualifying Basel III capital will phase in through 2018. Ratios also reflect the required US

Standardized methodology for calculating RWAs, effective January 1, 2015. Target represents fully

phased in Basel III. |

2Q15 outlook

18

2Q15 expectations vs. 1Q15

Net interest

income, net

interest margin

Operating

leverage, efficiency

ratio

Credit trends

and costs

Average loan growth rate 1.5 -2% vs. prior quarter

Net interest margin broadly stable/down slightly, as pressure from low-rate environment

continues Positive day count benefit of $6 million expected

Expect return to positive operating leverage and improvement in the efficiency ratio

Expect stable asset quality trends but with lower commercial recoveries

Provision

expense

expected

to

revert

towards

25%

of

low

end

of

full-year

guidance

range

of

$350

-

$400 million

Restructuring

costs

Restructuring costs of ~$35-$40 million in 2Q15

Capital, liquidity

and funding

Quarter-end Basel III common equity Tier 1 ratio ~12%

Loan-to-deposit ratio 98-99%

Continue to diversify funding sources |

Key

messages 19

Continuing to execute well against broad market stakeholder agenda

Financial performance has been led by balance sheet growth, expense

discipline, and favorable credit

Keeping NIM stable is near-term priority pending higher rates

Currently making the necessary investments to get key fee-based

activities to scale, will take some time to realize the benefit

Asset quality and capital ratios remain strong |

Appendix

20 |

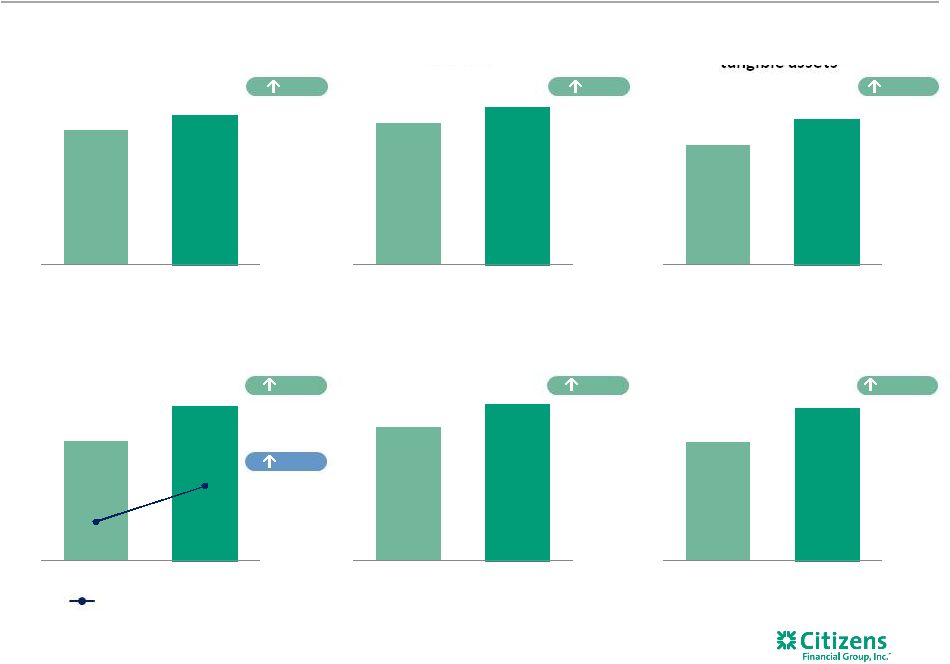

$356

$383

1Q14

1Q15

$166

$215

$0.30

$0.39

1Q14

1Q15

$87.1

$94.5

1Q14

1Q15

$87.5

$99.0

1Q14

1Q15

0.6%

0.7%

1Q14

1Q15

5.2%

6.7%

1Q14

1Q15

Quarter over quarter results

21

Adjusted pre-provision profit

1

$s in millions

Adjusted return on average

tangible assets

1

Adjusted net income

1

$s in millions

1

Adjusted results are non-GAAP items and exclude the effect of net restructuring charges

and special items associated with Chicago Divestiture, efficiency and effectiveness

programs and separation from RBS. See important information on use of Non-GAAP items in the Appendix.

2

Excludes loans and deposits held for sale.

tangible common equity

1

149 bps

12 bps

30%

8%

Period-end loans

2

$s in billions

Period-end deposits

2

$s in billions

13%

9%

30%

Adjusted Diluted EPS

Adjusted return on average

1 |

$388

$383

4Q14

1Q15

12.4%

12.2%

4Q14

1Q15

0.7%

0.7%

4Q14

1Q15

10.6%

10.5%

4Q14

1Q15

6.8%

6.7%

4Q14

1Q15

$217

$215

$0.39

$0.39

4Q14

1Q15

Linked quarter results

22

Adjusted

pre-provision

profit

1

$s in millions

Adjusted return on average

tangible

assets

1

Adjusted

net

income

1

$s in millions

Adjusted return on average

tangible

common

equity

1

Tier

1

leverage

ratio

2

3 bps

unchanged

~10 bps

1%

1%

1

effectiveness programs and separation from RBS. See important information on use of

Non-GAAP items in the Appendix. 2

Current reporting period regulatory capital ratios are preliminary.

3

Basel I tier 1 common equity ratio.

unchanged

Adjusted

Diluted

EPS

1

3

Basel III common equity

tier

1

risk-based

capital

ratio

2

~20 bps

Adjusted results are non-GAAP items and exclude the effect of net restructuring charges

and special items associated with Chicago Divestiture, efficiency and |

Net interest

margin NIM% walk 1Q14 to 1Q15

NIM% walk 4Q14 to 1Q15

23

2.89%

2.77%

0.05%

(0.05%)

(0.05%)

(0.04%)

(0.02%)

(0.01%)

1Q14 NIM%

Pay-fixed

swap costs

Sub-debt/Term

issuance

Loan yields,

mix, & fees

Deposit costs

Chicago

Divestiture

Other short-

term borrowed

funds

1Q15 NIM%

2.80%

2.77%

0.02%

(0.02%)

(0.01%)

(0.01%)

(0.01%)

4Q14 NIM%

Pay-fixed

swap costs

Investment

yields

Deposit costs

Loan yields,

mix, & fees

Term-debt

issuance

1Q15 NIM% |

Consumer Banking

segment 24

1

Non-GAAP item. Adjusted results exclude the effect of net restructuring charges and

special items associated with Chicago Divestiture, efficiency and effectiveness

programs and separation from RBS. See important information on use of Non-GAAP

items in the Appendix. 2

Includes held for sale.

3

Operating segments are allocated capital on a risk-adjusted basis considering economic and

regulatory capital requirements. We approximate that regulatory capital is equivalent

to a sustainable target level for Tier 1 common equity and then allocate that

approximation to the segments based on economic capital. Highlights

1Q15 change from

$s in millions

1Q15

4Q14

1Q14

4Q14

1Q14

$

%

$

%

310

Net interest income

533

$

536

$

537

$

(3)

$

(1) %

(4)

$

(1) %

311

Noninterest income

219

218

219

1

—

%

—

—

%

312

Total revenue

752

754

756

(2)

—

%

(4)

(1) %

313

Noninterest expense

596

611

638

(15)

(2) %

(42)

(7) %

314

Pre-provision profit

156

143

118

13

9 %

38

32 %

315

Provision for credit losses

63

64

70

(1)

(2) %

(7)

(10) %

316

Income before income tax

expense

93

79

48

14

18 %

45

94 %

317

Income tax expense

32

27

16

5

19 %

16

100 %

318

Net income

61

$

52

$

32

$

9

$

17 %

29

$

91 %

Average balances

$s in billions

319

50.3

$

49.4

$

46.2

$

0.9

$

2 %

4.1

$

9 %

320

67.5

$

66.4

$

70.8

$

1.1

$

2 %

(3.3)

$

(5) %

Mortgage Banking metrics

Originations

1,211

$

1,101

$

648

$

110

$

10 %

563

$

87 %

Origination Pipeline

1,609

1,110

828

499

45 %

781

94 %

Gain on sale of secondary

originations

2.65%

1.98%

1.98%

67

bps

67

bps

Performance metrics

321

ROTCE

1,3

5.3%

4.3%

2.8%

100

bps

249

bps

322

Efficiency

ratio

1

79%

81%

84%

(184)

bps

(514)

bps

Linked quarter:

Net income up $9 million

Net interest income decreased $3 million driven by two

fewer days in the quarter

–

loan growth and improved

yields, partially offset by higher deposit costs

–

Average loans and deposit growth of 2%

Noninterest income relatively stable driven by a

$17 million increase in mortgage banking, including

a $10 million gain on the sale of conforming

mortgages

–

Mortgage originations up 10%

–

Service charges and card fees lower, primarily due

to seasonality

Noninterest expense decreased $15 million driven by a

reduction in outside services, equipment, advertising

and employee benefits

Prior year quarter:

Net income up $29 million

Revenue down $4 million driven by an estimated $31

million decrease related to Chicago Divestiture;

underlying up $25 million on strong loan growth and

momentum in household growth and mortgage

–

Loans up $4.1 billion; total deposits down $3.3

billion reflecting Chicago Divestiture

Noninterest expense down $42 million, including

$20 million related to Chicago Divestiture

Total loans and

leases²

Total

deposits² |

Commercial

Banking segment 25

1

Non-GAAP item. Adjusted results exclude the effect of net restructuring charges and

special items associated with Chicago Divestiture, efficiency and effectiveness

programs and separation from RBS. See important information on use of Non-GAAP items in the Appendix.

2

Includes held for sale.

3

Operating segments are allocated capital on a risk-adjusted basis considering economic and

regulatory capital requirements. We approximate that regulatory capital is equivalent

to a sustainable target level for Tier 1 common equity and then allocate that

approximation to the segments based on economic capital.

1Q15 change from

$s in millions

1Q15

4Q14

1Q14

4Q14

1Q14

$

%

$

%

323

Net interest income

276

$

283

$

256

$

(7)

$

(2) %

20

$

8 %

324

Noninterest income

100

111

107

(11)

(10) %

(7)

(7) %

325

Total revenue

376

394

363

(18)

(5) %

13

4 %

326

Noninterest expense

173

180

153

(7)

(4) %

20

13 %

327

Pre-provision profit

203

214

210

(11)

(5) %

(7)

(3) %

328

Provision for credit losses

(21)

1

(5)

(22)

NM

(16)

(320) %

329

Income before income tax

expense

224

213

215

11

5 %

9

4 %

330

Income tax expense

77

73

74

4

5 %

3

4 %

331

Net income

147

$

140

$

141

$

7

$

5 %

6

$

4 %

Average balances

$s in billions

332

Total loans and leases²

40.2

$

38.9

$

36.6

$

1.3

$

3 %

3.7

$

10 %

333

Total deposits²

21.9

$

22.5

$

17.4

$

(0.6)

$

(3) %

4.5

$

26 %

Performance metrics

334

ROTCE

1,3

13.2%

12.8%

14.2%

39

bps

(102)

bps

335

Efficiency

ratio

1

46%

45%

42%

53

bps

388

bps

Linked quarter:

Commercial Banking net income increased $7 million

Total revenue down $18 million, net interest income

down $7 million on a 3% increase in loans and 3%

decrease in deposits

–

Strength in Industry Verticals, Middle Market, Mid-

Corporate, and Commercial Real Estate,

–

Deposits down $568 million, or 3%

Noninterest income down $11 million reflecting

seasonal weakness in interest rate products, capital

markets, leasing and foreign exchange and trade

finance

Noninterest expense decreased $7 million driven by

lower regulatory costs, depreciation on leased

equipment, and outside services partially offset by

higher insurance and tax costs and salaries and benefits

Prior year quarter:

Net income up $6 million reflecting higher revenue and

expenses and lower provision expense

NII up $20 million on $3.7 billion increase in loans and

$4.5 billion increase in deposits

Noninterest income down $7 million from 1Q14 which

included unusually high leasing income

Noninterest expense up $20 million reflecting higher

salaries and benefits and insurance and taxes

Highlights |

Other

Linked quarter:

Net income decreased $4 million from 4Q14

Net interest income increased $6 million, as lower

swap expense was partially offset by increased

wholesale funding and lower investment portfolio

income

Noninterest income increased $18 million driven by

securities gains and a change in low-income housing

investment portfolio accounting (offset in taxes)

Noninterest expense increased $8 million reflecting

increased incentive expense and higher insurance and

tax expense

Provision for credit losses up $9 million which included

a $4 million reserve build

Prior year quarter:

Net income up $8 million from a loss of $7 million in

1Q14

Net interest income up $12 million given a reduction in

hedging costs and the benefit of growth in investment

portfolio income

Noninterest income down $4 million reflecting a

decrease in securities gains

Provision for credit losses down $40 million from 1Q14

which included a $34 million reserve build

26

1

Includes held for sale.

Highlights

1Q15 change from

$s in millions

1Q15

4Q14

1Q14

4Q14

1Q14

$

%

$

%

336

Net interest income

27

$

21

$

15

$

6

$

29 %

12

$

80 %

337

Noninterest income

28

10

32

18

180 %

(4)

(13) %

338

Total revenue

55

31

47

24

77 %

8

17 %

339

Noninterest expense

41

33

19

8

24 %

22

116 %

340

Pre-provision profit (loss)

14

(2)

28

16

800 %

(14)

(50) %

341

Provision for credit losses

16

7

56

9

129 %

(40)

(71) %

342

Income (loss) before income

tax expense (benefit)

(2)

(9)

(28)

7

78 %

26

93 %

343

Income tax expense (benefit)

(3)

(14)

(21)

11

79 %

18

86 %

344

Net income (loss)

1

$

5

$

(7)

$

(4)

$

(80) %

8

$

114 %

Average balances

$s in billions

345

Total loans and leases

1

3.8

$

4.0

$

4.6

$

(0.2)

$

(5) %

(0.8)

$

(18) %

346

Total deposits

6.2

$

5.9

$

3.4

$

0.3

$

5 %

2.8

$

83 % |

Restructuring

charges and special items 27

GAAP results included restructuring charges and special items related to enhancing

efficiencies and improving processes across the organization and separation from the

Royal Bank of Scotland Group plc (“RBS”). Expect

to

utilize

the

balance

of

the

Chicago

Divestiture

gain

to

continue

to

reinvest

to

drive

future

growth,

and

to

fund an additional $35-40 million of further restructuring charges and special expense

items in 2Q15. as of and for the three months ended

Restructuring charges and special items

($s in millions, except per share data)

pre-tax

after-tax

pretax

after tax

pre-tax

after-tax

Noninterest expense restructuring charges

and special items:

Salaries and employee benefits

(1)

—

1

—

(2)

—

Outside services

8

5

18

12

(10)

(7)

Occupancy

2

1

5

3

(3)

(2)

Equipment expense

1

—

1

—

—

—

Software expense

—

—

6

4

(6)

(4)

Other operating expense

—

—

2

1

(2)

(1)

Total noninterest expense restructuring

charges and special items

10

$

6

$

33

$

20

$

(23)

$

(14)

$

Net restructuring charges and special items

(10)

$

(6)

$

(33)

$

(20)

$

23

$

14

$

Diluted EPS impact

(0.01)

$

(0.03)

$

0.02

$

March 31, 2015

December 31, 2014

increase/decrease |

Loan

Reconciliation 28

Average balances

$s in millions

Consumer Banking Segment

46,154

$

47,368

$

47,848

$

49,351

$

50,260

$

Add:

Non-core loans

3,199

3,066

2,932

2,801

2,667

Retail loans in Commercial Banking

(1)

117

135

134

145

143

Other

798

776

736

681

629

Less:

Commercial loans in Consumer Banking

(2)

3,265

3,221

3,022

3,017

3,056

Chicago Divestiture loans reclassed to LHFS

477

438

LHFS

123

138

170

179

197

Total Retail loans

46,403

$

47,547

$

48,459

$

49,782

$

50,446

$

Commercial Banking Segment

36,577

$

37,389

$

37,787

$

38,926

$

40,241

$

Add:

Commercial loans in Consumer Banking

(2)

3,265

3,221

3,022

3,017

3,056

Non-core loans

463

405

353

309

266

CRA

139

165

171

182

198

Other

22

21

25

28

25

Less:

Retail loans in Commercial Banking

(1)

117

135

134

145

143

Chicago Divestiture loans reclassed to LHFS

587

489

LHFS

32

106

33

54

136

Total Commercial loans

39,729

$

40,472

$

41,191

$

42,263

$

43,506

$

(1)

Primarily Treasury Solutions (Credit cards)

(2)

Primarily Business Banking

1Q14

2Q14

3Q14

4Q14

1Q15 |

$3.6B

$3.4B

$3.2B

$3.0B

$2.9B

1Q14

2Q14

3Q14

4Q14

1Q15

Retail

Commercial

SBO

Non-core home equity portfolio serviced by others (SBO)

SBO balances by FICO

SBO balances by LTV

SBO balances and charge-offs

Top 5 SBO balances by state

Non-core period-end loans

SBO balances by product

SBO Lien Position

1st Lien

2nd Lien

< 70

70-79

80-89

90-99

100-119

120+

< 620

620-679

680-719

720-759

760+

HE Loan

HELOC

29

$s in millions

1

A portion of the serviced by others portfolio is serviced by CFG.

2

SBO distribution gross period-end balances as of March 31, 2015.

3

FICO scores updated quarterly.

25%

20%

24%

16%

12%

3

14%

17%

18%

20%

31%

$1.2B

69%

$0.5B

31%

5%

95%

$307

$111

$105

$102

$91

$548

$489

2

2

2

2

2,3

1 |

Non-GAAP

Financial Measures 30

This document contains non-GAAP financial measures. The table below presents

reconciliations of certain non-GAAP measures. These reconciliations exclude restructuring

charges and/or special items, which are usually included, where applicable, in the financial

results presented in accordance with GAAP. Restructuring charges and special items

include expenses related to our efforts to improve processes and enhance efficiencies, as well

as rebranding, separation from RBS and regulatory expenses.

The non-GAAP measures set forth below include “total revenue”, “noninterest

income”, “ noninterest expense”, “pre-provision profit”, “income before income tax expense

(benefit)”, “income tax expense (benefit)”, “net income (loss)”,

“salaries and employee benefits”, “outside services”, “occupancy”, “equipment expense”, “amortization of

software”, “other operating expense”, “net income (loss) per average

common share”, “return of average common equity” and “return on average total assets”. In addition,

we present computations for "tangible book value per common share", “return on

average tangible common equity”, “return on average total tangible assets” and “efficiency

ratio” as part of our non-GAAP measures. Additionally, "pro forma Basel III fully

phased-in common equity tier 1 capital" computations for periods prior to 1Q15 are presented

as part of our non-GAAP measures.

We believe these non-GAAP measures provide useful information to investors because these

are among the measures used by our management team to evaluate our operating

performance and make day-to-day operating decisions. In addition, we believe restructuring charges and special items in any period do not reflect the operational

performance of the business in that period and, accordingly, it is useful to consider these

line items with and without restructuring charges and special items. We believe this

presentation also increases comparability of period-to-period results.

Prior to first quarter 2015, we also consider pro forma capital ratios defined by banking

regulators but not effective at each period end to be non-GAAP financial measures.

Since analysts and banking regulators may assess our capital adequacy using these pro forma

ratios, we believe they are useful to provide investors the ability to assess our

capital adequacy on the same basis.

Other companies may use similarly titled non-GAAP financial measures that are calculated

differently from the way we calculate such measures. Accordingly, our non-GAAP

financial measures may not be comparable to similar measures used by other companies. We

caution investors not to place undue reliance on such non-GAAP measures, but

instead to consider them with the most directly comparable GAAP measure. Non-GAAP

financial measures have limitations as analytical tools, and should not be considered in

isolation, or as a substitute for our results as reported under GAAP.

|

Non-GAAP

Reconciliation Table 31

(Excluding restructuring charges and special items)

$s in millions, except per share data

1Q15

4Q14

3Q14

2Q14

1Q14

Noninterest income, excluding special items:

Noninterest income (GAAP)

A

$347

$339

$341

$640

$358

—

—

—

288

—

Noninterest income, excluding special items (non-GAAP)

B

$347

$339

$341

$352

$358

Total revenue, excluding special items:

Total revenue (GAAP)

C

$1,183

$1,179

$1,161

$1,473

$1,166

—

—

—

288

—

Total revenue, excluding special items (non-GAAP)

D

$1,183

$1,179

$1,161

$1,185

$1,166

Noninterest expense (GAAP)

E

$810

$824

$810

$948

$810

Less: Restructuring charges and special items

LL

10

33

21

115

—

F

$800

$791

$789

$833

$810

Net income, excluding restructuring charges and special items:

Net income (GAAP)

G

$209

$197

$189

$313

$166

Add: Restructuring charges and special items, net of income tax expense (benefit)

6

20

13

(108)

—

Net income, excluding restructuring charges and special items (non-GAAP)

H

$215

$217

$202

$205

$166

Average common equity (GAAP)

I

$19,407

$19,209

$19,411

$19,607

$19,370

items (non-GAAP)

H/I

4.49 %

4.48 %

4.14 %

4.19 %

3.48 %

Return on average tangible common equity and return on average tangible

common equity, excluding restructuring charges and special items:

Average common equity (GAAP)

I

$19,407

$19,209

$19,411

$19,607

$19,370

Less: Average goodwill (GAAP)

6,876

6,876

6,876

6,876

6,876

Less: Average other intangibles (GAAP)

5

6

6

7

7

Add: Average deferred tax liabilities related to goodwill (GAAP)

422

403

384

369

351

Average tangible common equity (non-GAAP)

J

$12,948

$12,730

$12,913

$13,093

$12,838

Return on average tangible common equity (non-GAAP)

G/J

6.53 %

6.12 %

5.81 %

9.59 %

5.24 %

Return on average tangible common equity, excluding restructuring charges and

special items (non-GAAP)

H/J

6.73 %

6.76 %

6.22 %

6.28 %

5.24 %

Return on average total assets, excluding restructuring charges and special items:

Average total assets (GAAP)

K

$133,325

$130,671

$128,691

$127,148

$123,904

Return on average total assets, excluding restructuring charges and special items

(non-GAAP)

H/K

0.65 %

0.66 %

0.62 %

0.65 %

0.54 %

Return on average total tangible assets and return on average total tangible

assets, excluding restructuring charges and special items:

Average total assets (GAAP)

K

$133,325

$130,671

$128,691

$127,148

$123,904

Less: Average goodwill (GAAP)

6,876

6,876

6,876

6,876

6,876

Less: Average other intangibles (GAAP)

5

6

6

7

7

Add: Average deferred tax liabilities related to goodwill (GAAP)

422

403

384

369

351

Average tangible assets (non-GAAP)

L

$126,866

$124,192

$122,193

$120,634

$117,372

Return on average total tangible assets (non-GAAP)

G/L

0.67 %

0.63 %

0.61 %

1.04 %

0.57 %

special items (non-GAAP)

H/L

0.69 %

0.69 %

0.66 %

0.68 %

0.57 %

QUARTERLY TRENDS

Noninterest expense, excluding restructuring charges and special items:

Noninterest expense, excluding restructuring charges and special items (non-GAAP)

Return on average common equity, excluding restructuring charges and special items:

Return on average common equity, excluding restructuring charges and special

Return on average total tangible assets, excluding restructuring charges and

Less: Special items - Chicago gain

Less: Special items - Chicago gain

|

1Q15

4Q14

3Q14

2Q14

1Q14

Efficiency ratio and efficiency ratio, excluding restructuring charges and special items:

Net interest income (GAAP)

$836

$840

$820

$833

$808

Add: Noninterest income (GAAP)

347

339

341

640

358

Total revenue (GAAP)

C

$1,183

$1,179

$1,161

$1,473

$1,166

Efficiency ratio (non-GAAP)

E/C

68.49 %

69.88 %

69.84 %

64.33 %

69.43 %

Efficiency ratio, excluding restructuring charges and special items (non-GAAP)

F/D

67.65 %

67.11 %

68.02 %

70.23 %

69.43 %

Tangible book value per common share:

Common shares - at end of period (GAAP)

M

547,490,812

545,884,519

559,998,324

559,998,324

559,998,324

Stockholders' equity (GAAP)

$19,564

$19,268

$19,383

$19,597

$19,442

Less: Goodwill (GAAP)

6,876

6,876

6,876

6,876

6,876

Less: Other intangible assets (GAAP)

5

6

6

7

7

Add: Deferred tax liabilities related to goodwill (GAAP)

434

420

399

384

366

Tangible common equity (non-GAAP)

N

$13,117

$12,806

$12,900

$13,098

$12,925

Tangible book value per common share (non-GAAP)

N/M

23.96

23.46

23.04

23.39

23.08 Net income per average common share - basic and diluted, excluding

restructuring charges and special items:

Average common shares outstanding - basic (GAAP)

O

546,291,363

546,810,009

559,998,324

559,998,324

559,998,324

Average common shares outstanding - diluted (GAAP)

P

549,798,717

550,676,298

560,243,747

559,998,324

559,998,324

Net income applicable to common stockholders (GAAP)

Q

$209

$197

$189

$313

$166

Net income per average common share - basic (GAAP)

Q/O

0.38

0.36

0.34

0.56

0.30

Net income per average common share - diluted (GAAP)

Q/P

0.38

0.36

0.34

0.56

0.30

Net income applicable to common stockholders, excluding restructuring charges

and special items (non-GAAP)

R

215

217

202

205

166

Net income per average common share - basic, excluding restructuring charges

and special items (non-GAAP)

R/O

0.39

0.40

0.36

0.37

0.30

Net income per average common share - diluted, excluding restructuring charges

and special items (non-GAAP)

R/P

0.39

0.39

0.36

0.37

0.30

Pro forma Basel III fully phased-in common equity tier 1 capital

ratio¹: Common equity tier 1 (regulatory)

$13,360

$13,173

$13,330

$13,448

$13,460

Less: Change in DTA and other threshold deductions (GAAP)

(3)

(6)

(5)

(7)

(7)

Pro forma Basel III fully phased-in common equity tier 1 (non-GAAP)

S

$13,357

$13,179

$13,335

$13,455

$13,467

Risk-weighted assets (regulatory general risk weight approach)

$109,786

$105,964

$103,207

$101,397

$100,368

Add: Net change in credit and other risk-weighted assets (regulatory)

242

2,882

3,207

2,383

2,450

Basel III standardized approach risk-weighted assets (non-GAAP)

T

$110,028

$108,846

$106,414

$103,780

$102,818

Pro forma Basel III fully phased-in common equity tier 1 capital ratio (non-GAAP)¹ S/T

12.1%

12.1%

12.5%

13.0%

13.1%

Salaries and employee benefits, excluding restructuring charges and special items:

Salaries and employee benefits (GAAP)

U

$419

$397

$409

$467

$405

Less: Restructuring charges and special items

(1)

1

—

43