Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - TUBEMOGUL INC | Financial_Report.xls |

| EX-31.2 - EX-31.2 - TUBEMOGUL INC | tube-ex312_201412319.htm |

| EX-31.1 - EX-31.1 - TUBEMOGUL INC | tube-ex311_201412318.htm |

| EX-32.2 - EX-32.2 - TUBEMOGUL INC | tube-ex322_2014123111.htm |

| EX-32.1 - EX-32.1 - TUBEMOGUL INC | tube-ex321_2014123110.htm |

| EX-10.7 - EX-10.7 - TUBEMOGUL INC | tube-ex107_20141231174.htm |

| EX-23.1 - EX-23.1 - TUBEMOGUL INC | tube-ex231_20141231237.htm |

| EX-21.1 - EX-21.1 - TUBEMOGUL INC | tube-ex211_20141231116.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

OR

|

¨ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 001-36543

TubeMogul, Inc.

(Exact name of Registrant as specified in its Charter)

|

Delaware |

|

51-0633881 |

|

( State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer |

|

1250 53rd Street, Suite 2 Emeryville, California |

|

94608 |

|

(Address of principal executive offices) |

|

(Zip Code) |

(510) 653-0126

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

|

|

Name of each exchange on which registered |

|

Common Stock, $0.001 par value |

|

|

The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ¨ NO x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. YES ¨ NO x

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). YES x NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Report or any amendment to this Report. x

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of “large accelerated filer”, “accelerated filer”, and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer |

|

¨ |

|

Accelerated filer |

|

¨ |

|

|

|

|

|

|||

|

Non-accelerated filer |

|

x (Do not check if a smaller reporting company) |

|

Smaller reporting company |

|

¨ |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ¨ NO x

The aggregate market value of voting stock held by non-affiliates of the Registrant on July 23, 2014, based on the closing price of $9.74 for shares of the Registrant’s common stock, was approximately $82.5 million. The Registrant has elected to use July 23, 2014 (the closing date of the Registrant’s initial public offering of its common stock on The NASDAQ Global Select Market) as the calculation date because on June 30, 2014 (the last business day of the Registrant’s second fiscal quarter), the Registrant was a privately-held company. Shares of common stock held by each executive officer, director and by each person who owns 5% or more of the outstanding common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of shares of Registrant’s common stock outstanding as of March 23, 2015 was 30,268,482.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Definitive Proxy Statement relating to the Annual Meeting of Stockholders are incorporated by reference into Part III of this Annual Report on Form 10-K. Such Definitive Proxy Statement will be filed with the Securities and Exchange Commission within 120 days after the end of the Registrant’s fiscal year ended December 31, 2014.

Report Table of Contents

TABLE OF CONTENTS

|

|

|

|

|

Page |

|

|

5 |

|||

|

Item 1. |

|

|

5 |

|

|

Item 1A. |

|

|

17 |

|

|

Item 1B. |

|

|

34 |

|

|

Item 2. |

|

|

34 |

|

|

Item 3. |

|

|

34 |

|

|

Item 4. |

|

|

35 |

|

|

|

36 |

|||

|

Item 5. |

|

|

36 |

|

|

Item 6. |

|

|

38 |

|

|

Item 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

41 |

|

Item 7A. |

|

|

57 |

|

|

Item 8. |

|

|

58 |

|

|

Item 9. |

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosures |

|

82 |

|

Item 9A. |

|

|

82 |

|

|

Item 9B. |

|

|

82 |

|

|

|

83 |

|||

|

Item 10. |

|

|

83 |

|

|

Item 11. |

|

|

83 |

|

|

Item 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

83 |

|

Item 13. |

|

Certain Relationships and Related Transactions, and Director Independence |

|

83 |

|

Item 14. |

|

|

83 |

|

|

|

83 |

|||

|

Item 15. |

|

|

83 |

|

|

|

86 |

|||

2

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K, or the Report, contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends affecting our business. Forward-looking statements should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of the times at, or by, which such performance or results will be achieved. Forward-looking statements are based on information available to our management at the date of this Report and our management’s good faith belief as of such date with respect to future events, and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Important factors that could cause such differences include, but are not limited to:

|

· |

our financial performance, including our revenue, costs, expenditures, growth rates and operating expenses, and our ability to become profitable; |

|

· |

our ability to maintain our rate of revenue growth; |

|

· |

our ability to expand our customer base; |

|

· |

our ability to convince our customers to maintain or increase their advertising spend through our platform; |

|

· |

the expansion of the digital video advertising market; |

|

· |

our ability to adapt to changing market conditions; |

|

· |

our ability to effectively manage our growth; |

|

· |

the effects of increased competition in our markets and our ability to compete effectively; |

|

· |

our ability to effectively grow and train our sales team; |

|

· |

our ability to maintain, protect and enhance our intellectual property; |

|

· |

costs associated with defending intellectual property infringement and other claims; |

|

· |

our ability to grow our market share in and penetrate emerging video advertising channels; |

|

· |

our ability to successfully enter new geographic markets; |

|

· |

our ability to develop and introduce enhancements and new features and functionality of our platform that achieve market acceptance; |

|

· |

our expectations concerning relationships with third parties; |

|

· |

our ability to retain our founders and attract and retain qualified employees and key personnel; and |

|

· |

other factors discussed in this Report under Item 1A “Risk Factors” and Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” |

In addition, in this Report, the words “anticipate,” “believe,” “continue,” “could,” “seek,” “might,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “approximately,” “project,” “should,” “will,” “would” or the negative or plural of these words or similar expressions, as they relate to our company, business and management, are intended to identify forward-looking statements. In light of these risks and uncertainties, the future events and circumstances discussed in this Report may not occur, and actual results could differ materially from those anticipated or implied in the forward-looking statements.

Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. We discuss these risks in greater detail in Item 1A “Risk Factors” and elsewhere in this Report. We derive many of our forward-looking statements from our operating budgets and forecasts, which we base on many assumptions. While we believe that our assumptions are reasonable, we caution that it is difficult to predict the impact of known factors, and it is impossible for us to anticipate all factors that could affect our actual results. Given these uncertainties, you should not place undue reliance on these forward-looking statements. You should read this Report and the documents that we reference in this Report and have filed with the Securities Exchange Commission, or SEC, as exhibits thereto, completely and with the understanding that our actual future results may be materially different from what we expect.

3

Forward-looking statements speak only as of the date of this Report. We caution you that the foregoing list of important factors may not contain all of the material factors that are important to you. Except as required by law, we assume no obligation to publicly update or revise any forward-looking statement to reflect actual results, changes in assumptions based on new information, future events or otherwise. If we update one or more forward-looking statements, no inference should be drawn that we will make additional updates with respect to those or other forward-looking statements.

Unless the context otherwise requires, the terms “TubeMogul,” “the Company,” “we,” “us,” and “our” in this Report refer to TubeMogul, Inc., a Delaware corporation and our predecessor, TubeMogul, Inc., a California corporation, and where appropriate, their respective consolidated subsidiaries.

4

Overview

TubeMogul is an enterprise software company for digital branding. By reducing complexity, improving transparency and leveraging real-time data, our platform enables brands to gain greater control of their digital video advertising spend and achieve their brand advertising objectives.

Our customers plan, buy, measure and optimize their global digital video advertising spend from our self-serve platform. By integrating programmatic technologies and disparate sources of inventory within a single platform, we enable our customers to launch sophisticated, scalable digital video advertising campaigns — onto any digital device — within minutes. This is in contrast to the still prevailing and inefficient approach to media buying that occurs through a manual campaign-by-campaign request for proposal, or RFP, process, which often involves multiple digital advertising service providers.

Our customers primarily include brands, which generally refer to companies, or product lines within companies, that control advertising budgets for a single marketing brand or a group of marketing brands, and the advertising agencies that serve them. Agency trading desks, ad networks and publishers also use our platform. We refer to our customers and other businesses that are engaged in purchasing digital marketing as advertisers.

Our platform is integrated with many public digital video ad inventory sources, where individual ad impressions can be purchased dynamically utilizing real-time bidding technology, or RTB. Our platform automates the real-time purchase of ad impressions based upon campaign objectives. Additionally, our customers can easily integrate the ad inventory they source directly from publishers and private exchanges. As a result, our platform enables holistic campaign management across public and private inventory using a single interface.

As consumers are increasingly watching video content on digital devices, advertisers are shifting more of their video advertising spend from traditional TV to digital video. As a result, advertisers want to plan, buy and measure TV and digital video on an equivalent basis. Our platform enables advertisers to plan and buy digital video advertising using industry-standard metrics such as gross rating points, or GRPs, which are a measure of reach and frequency among a target audience, and verify the audience they reach using Nielsen reporting, thereby unifying the planning and measurement of TV and digital video campaigns.

Brand advertisers seek to optimize their media buys across all channels, with TV the most important, as it is typically their largest advertising medium. In December 2014, we introduced a solution to plan and buy television advertising using our software platform. More recently, in February 2015, we introduced a solution to buy display advertising using our platform. As we enhance the capabilities of our platform to address these new formats, advertisers will be able to plan and measure across television and digital media to better optimize their spend to the formats that are most effective for them.

Our platform measures key brand advertising metrics including brand lift, as measured by integrated brand surveys, as well as GRPs and engagement. As a result, advertisers can verify the success and impact of their digital video advertising campaigns by measuring the audience reached by the campaign, how the audience interacted with their advertisements and the impact the campaign had on the consumer’s perception of the brand. Using these real-time insights, our platform dynamically optimizes spend based upon brand advertising objectives set by the advertiser.

We offer advertisers unique visibility into the inventory they purchase, including enabling them to see video ad performance and viewability at any dimension of a campaign. Our platform also includes a suite of brand safety technologies designed to prevent unacceptable ad placements and to detect and block sites with inappropriate content, auto-play ad placements or fraudulent bot-driven traffic.

5

We make our platform available through two offerings: Platform Direct, which allows advertisers to continuously run campaigns through a self-serve model, and Platform Services, which allows advertisers to specify campaign objectives and have our team execute on their behalf using our platform. We believe our customers value both of our offerings. For 2014, campaigns were executed through our platform for over 4,000 brands, usually through an agency but in some cases directly. For the years ended December 31, 2012, 2013 and 2014, our total revenue was $34.2 million, $57.2 million and $114.2 million respectively, representing a compound annual growth rate, or CAGR, of 83%, and Total Spend through our platform was $53.8 million, $111.9 million, and $254.3 million, respectively, representing a CAGR of 117%. We define Total Spend as the aggregate gross dollar volume that our Platform Direct customers and Platform Services customers spend through our platform, which includes cost of media purchases and our fees. Please see Item 6 “Selected Financial Data” for information regarding the limitations of using Total Spend as a financial measure and for reconciliations of Total Spend to revenue, the most directly comparable financial measure calculated in accordance with GAAP. For the years ended December 31, 2012, 2013 and 2014, our gross margin was 52%, 66%, and 70%, respectively. For the years ended December 31, 2012, 2013 and 2014, our net loss was $3.6 million, $7.4 million, and $4.4 million, respectively, with our net loss for the year ended December 31, 2014 representing a 40% decrease compared to the year ended December 31, 2013.

Market Overview

Given the importance of branding to maintain and improve differentiation, market share and pricing power, a significant portion of global advertising dollars are spent on brand advertising. Brands rely on the sight, sound and motion of video advertising to establish an emotional connection with consumers that is critical to branding. Brands have primarily utilized traditional TV advertising to deliver video messages to the large audiences they require.

While TV advertising represents the largest single portion of today’s advertising spend, consumers are shifting their consumption of media content from analog mediums, such as TV, print and radio, to digital mediums such as websites and mobile applications. Consumers expect to be able to view digital media content seamlessly across multiple digital devices, including computers, tablets, smartphones and connected TVs.

Recognizing this trend, brands are increasingly shifting their advertising spend to digital mediums. The majority of digital advertising spend to date has been directed to search and display advertising to achieve direct response objectives. Direct response advertising is designed to optimize the delivery of ads to increase ‘conversions’ or the action the viewer takes after seeing the ad, such as visiting a website, filling out a form or making an online purchase. However, direct response advertising does not serve the needs of brand advertisers who want to reach and persuade their target audiences and track the impact on consumer perceptions of their brand. As a result, brands are increasingly seeking to use digital video advertising channels for their brand advertising campaigns. This form of advertising allows brands to establish emotional connections with viewers by presenting powerful messages to consumers on whatever digital device they choose to view content. Further, as consumers watch video content on websites and within mobile applications, they create a record of their demographic, behavioral and socioeconomic data. By leveraging this data, brands are able to more effectively target the right audience, with the right message, on the right screen at the right time.

As brands shift advertising spend to digital mediums, they encounter increasing complexity in executing their digital video advertising campaigns. Brands, their agencies and other entities, which we refer to as advertisers, generally need to use dozens of digital advertising service providers to execute a campaign. These service providers include the many sources of inventory available to advertisers, such as public ad exchanges, supply-side platforms, private marketplaces, ad networks and direct premium publishers, as well as providers of specific technologies, including ad serving, ad verification, data management, brand safety, rich media, audience data and analytics. Brands have traditionally relied on media agencies to allocate their spend to these service providers on a campaign-by-campaign basis through individual requests for proposal, or RFPs. This has resulted in a complex, fragmented and inefficient system.

Software’s Impact on Brand Advertising

Over the last two decades, enterprise software solutions, such as enterprise resource planning, customer relationship management and human capital management, have transformed many business processes. More recently, cloud-based solutions have reduced operating costs, increased scalability, and provided better data for decision making. Largely because software solutions that address the complexities of digital video advertising are in the early stages of development, brand marketers within large corporations have not yet realized the benefits that enterprise software solutions can offer.

While adoption of comprehensive enterprise software solutions for digital video advertising is in its early stages, there has been rapid growth in the use of technology to buy and sell digital video advertising inventory. This technology, which is generally referred to as programmatic, includes RTB where advertisers bid in real-time in hundredths of a second for the right to serve an ad to a particular consumer. The adoption of programmatic technology has been driven by the opportunity to apply the massive amounts of data, or big data, collected by brands and third parties to improve the performance of digital marketing campaigns.

6

To date, programmatic technology has been primarily applied to display advertising campaigns with direct response objectives. More recently, brands and their agencies have begun to adopt programmatic tools for video advertising campaigns with branding objectives.

Challenges of Video Advertising for Brands

As the digital video advertising market continues to develop and grow, advertisers are seeking alternatives to the highly manual, repetitive and uncoordinated processes that they have historically used to plan, execute and measure their digital video advertising campaigns. However, they continue to face several specific challenges including:

|

· |

Fragmented and Manual System for Buying Digital Media. Compared to the number of national broadcast networks and cable networks on traditional TV, tens of thousands of digital publishers sell digital video advertising inventory. Digital publishers typically offer their premium inventory directly to advertisers, then make remaining inventory available through many service providers, including ad exchanges, supply-side platforms, and ad networks. Advertisers need to reach audiences on many websites to achieve campaign goals, and must do so across many types of digital devices. Advertisers also typically engage in repetitive manual RFP processes with multiple sources of inventory to select the video advertising inventory suitable to reach their target audience, resulting in significant inefficiencies. |

|

· |

Challenging to Integrate and Leverage Multiple Technology Providers. Advertisers need multiple technologies to execute digital video advertising campaigns, such as ad serving, ad verification, data management, brand safety, rich media, audience data and analytics technologies. However, these technologies are generally offered by different providers and it is difficult for advertisers to make these technologies work well together. This impedes campaign performance, increases costs and lowers efficiency. |

|

· |

Limited Options for Advertisers to Manage and Control Entire Buying Process. Current service providers do not allow advertisers to manage, control and optimize digital video campaigns using a self-serve model. Instead, to reach audiences across thousands of websites, advertisers are often forced to purchase inventory through media aggregators, which generally do not allow advertisers to choose the websites on which their ads run, make adjustments during the course of a given campaign, or obtain the performance data necessary to evaluate and improve ongoing campaign decision making. |

|

· |

TV Advertising and Digital Video Advertising are Purchased and Measured Differently. Traditional TV remains an important medium to reach consumers with brand messages. To date, TV and digital advertising campaigns have been executed separately and measured by different metrics, leading to inefficiencies. The separate processes and metrics make it difficult to effectively plan and measure video campaigns focused on reaching targeted audiences across TV and digital channels. |

|

· |

Advertising Service Providers Have Conflicting Interests and Offer Limited Inventory and Economic Transparency. Many digital video advertising service providers offer services to both advertisers and publishers. These service providers typically purchase advertising inventory directly from publishers and resell it to advertisers seeking to purchase the same inventory. This model can create conflicting interests. In particular, when fulfilling campaigns, such service providers may have an economic incentive to favor their own inventory, over equally effective or superior inventory that is otherwise available. Further, it may be in the interests of these service providers to not disclose to the advertiser the sites on which their video advertising campaigns are shown or their cost to purchase that inventory. |

|

· |

Difficult to Measure Return on Investment. As consumers increasingly view content through a broader range of devices and channels, it is difficult for brands to verify a number of objectives important to brand advertising, such as reach and frequency among a target audience, engagement and brand lift. |

|

· |

Challenging to Deploy and Manage Global Campaigns. Advertisers often seek to reach and impact a global consumer base by launching targeted video advertising campaigns across multiple countries simultaneously. Managing video advertising campaigns globally is currently a costly and inefficient process requiring brands to contract with multiple agencies, ad exchanges, ad networks, supply-side platforms, publishers and technology providers. |

|

· |

Difficult to Identify and Eliminate Undesired Ad Placements and Fraudulent Traffic. Given the emerging nature of the digital video advertising market, there are few standards and tools to categorize various types of digital video ad placements. For example, a video ad that requires a consumer to initiate a video is more valuable than a video ad that plays automatically in a display, or banner, space, but some providers do not make a distinction between the two placements. Advertisers also have limited control over the content alongside which their ad is placed, which is critical to brands, and whether each ad placement is viewable by the consumer. Finally, advertisers are also concerned with the increasing proportion of fraudulent web traffic that is generated by computers, or bots, resulting in advertisers paying for impressions that are not viewed by consumers. |

7

Our Solution

We enable advertisers to plan, buy, measure and optimize global video advertising spend from a single platform. Our platform incorporates our proprietary programmatic technologies, including RTB, automated optimization and advanced audience targeting capabilities, and integrates key third-party technologies. Through an intuitive user interface, our customers are able to control and automate advertising spend across the various sources of inventory, including inventory acquired directly from individual publishers, to reach targeted audiences across digital devices at any time. In addition, by using a single platform, our customers benefit from comprehensive, real-time reporting that is comparable across sources of inventory, geographies, digital devices and ad formats. We make our cloud-based platform available through two offerings: Platform Direct, which allows advertisers to continuously run campaigns through a self-serve model, and Platform Services, which allows advertisers to specify campaign objectives and have our team execute on their behalf using our platform.

|

· |

Integrated Software Platform. Our platform integrates with over 30 third-party technology providers who offer specific technologies for digital video campaigns. For example, we integrate with data management platforms to enhance audience targeting and reporting, with video rich media providers to enhance ad formats, and with contextual data providers to enhance brand safety. By using our platform, advertisers can utilize a single control interface that integrates with best-of-breed third-party technology suppliers for campaign execution. |

|

· |

Designed for Self-Serve Model. Through our Platform Direct offering, our platform is accessible using a cloud-based, self-serve model. Our Platform Direct customers have full control and transparency over their digital video advertising spend. Our intuitive user interface enables advertisers to manage an unlimited number of campaigns simultaneously on a single platform, thereby reducing cost, complexity and inefficiencies caused by intermediaries. |

|

· |

Enable TV Advertisers to Buy Digital Video. Our platform enables TV advertisers to buy digital video advertising using industry standard metrics such as GRPs, and verify the audience they reach using integrated Nielsen reporting, thereby unifying the planning and measurement of TV and digital video advertising campaigns and improving efficiencies. |

|

· |

Independent and Transparent Buy-Side Positioning. We have built our business to serve only buyers of digital video advertising. We generally do not take an economic interest in the inventory that customers can access through our platform and as a result, we do not have an incentive to favor specific inventory when fulfilling campaigns. We show our customers the specific sites where ads are displayed and our Platform Direct customers can see the price they pay for the media. We charge our Platform Direct customers a fee as a percentage of their spend, providing them with greater economic transparency. |

|

· |

Verifies and Measures Campaign Performance and Brand Lift. Our platform enables advertisers to verify audience reach and engagement and measure the impact of a video ad campaign on consumers through our integrated brand survey module. Our reporting is made available for multiple dimensions of a campaign, including by video ad, ad format, website and mobile application. |

|

· |

Purpose-Built for Global Video Advertising. Our platform has been designed for brands to manage and execute global digital video campaigns using a single integrated workflow. Although substantially all of our revenue to date has been generated from English language countries, we currently enable campaigns in over 70 countries and our platform is currently available in four languages and supports 18 currencies. By providing access to inventory and targeting data across many countries, we enable brands to launch global campaigns without the need for additional service providers. |

|

· |

Integrated Brand Safety Tools. Our platform includes a suite of technologies designed to prevent unacceptable ad placements. Our platform detects, categorizes and blocks sites with inappropriate content, fraudulent bot-driven traffic and auto-play ad placements. We integrate technology that scans the content of individual web pages prior to an ad being served to ensure the content is appropriate for the brand. |

Our Strengths

We believe the following attributes and capabilities provide us with long-term competitive advantages:

|

· |

Focused on Software-Based Solutions for Brands. Our platform offers advertisers a robust and comprehensive solution for digital branding, which we believe differentiates our offerings from those of our competitors. We work to continuously improve our platform to provide our customers with the necessary capabilities to meet their evolving brand advertising objectives. |

|

· |

Empower Customers Through Our Self-Serve Model. Our Platform Direct customers have direct access to our platform which enables them to execute their own strategies for their digital video advertising spend. As a result of the performance and functionality of our platform, we believe many of our customers rely on our platform for a significant and growing portion of their digital video advertising spend. These self-serve customers are highly engaged. For example, they attend and provide input at our various weekly webinars, TubeMogul University customer conferences, and quarterly business and roadmap updates to provide ongoing feedback to our product teams and management. |

8

|

· |

Product Built for Global Opportunity. Our platform is built for managing and executing global advertising campaigns. In addition, our intuitive user interface enables geographically dispersed personnel within a global organization to work together seamlessly with an auditable workflow. We have operations in many large advertising markets. For 2014, 31% of our revenue was generated from customers with billing addresses outside of the U.S. |

|

· |

Industry Pioneer. We believe we were the first to deliver a programmatic digital video advertising platform designed exclusively for advertisers, and as a result, we believe we have developed a deep expertise and a strong reputation in our market. Additionally, we demonstrate thought leadership through industry initiatives such as founding the OpenVideoViewability consortium and creating the first education and certification program for programmatic video. |

|

· |

Attractive and Scalable Financial Model. We are able to scale our operations in a highly efficient manner with our Platform Direct offering. Because our Platform Direct offering allows advertisers to continuously run campaigns on a self-serve basis, we require fewer sales resources following initial sales and, therefore, our sales expense tends to represent a lesser portion of follow-on Platform Direct Spend. |

|

· |

Experienced Team. We are a founder-led software company that has been focused on developing innovative software solutions for digital video since we were founded in 2007. The extensive industry and technology experience of our management team has allowed us to create and maintain a culture of innovation at every level of the company. |

Our Strategy

We believe that the digital video advertising market is in the early stages of a significant shift toward enterprise software solutions that address the complexities of digital brand advertising. We intend to capitalize on this opportunity by pursuing the following key growth strategies.

|

· |

Expand Our Customer Base. Our global sales force is focused on growing the number of our customers, particularly our Platform Direct customers. To increase our global market share, we continue to invest in training and other initiatives to increase the productivity of our sales personnel. |

|

· |

Increase Our Share of Our Customers’ Video Advertising Spend. We continue to add features and functionality to our platform that encourage customers to consolidate, and ultimately increase, their digital video advertising spend on our platform. Our customers support team trains and educates our Platform Direct customers on these new features and identifies opportunities to capture an increased share of advertising spend from our existing customers. |

|

· |

Migrate Platform Services Customers to Platform Direct. We plan to continue to focus on educating our Platform Services customers about the benefits of our Platform Direct solution. Using our Platform Direct solution, customers are frequently able to save fifty percent of the fees exclusive of media costs that they would typically pay using our Platform Services solution. Using the self-service features of our Platform Direct solution, customers gain increased control over the execution of their campaigns and increased transparency into impression-level economics as compared to traditional insertion order based purchasing. We believe that an increased migration to our Platform Direct solution will ultimately increase the number of recurring campaigns and size of advertising spend on our platform and as a result, increase our gross profit. |

|

· |

Expand Into Cross-Screen Advertising. We are expanding into television advertising and adding other digital advertising formats, including display and social, to our platform. The expansion into TV expands our addressable market and the addition of other digital formats makes our platform more compelling to brand advertisers that desire a single platform to manage all of their media buying. |

|

· |

Continue to Innovate. We intend to continue to make substantial investments in our platform by introducing enhancements and new features and functionality that position us to capture a larger share of new market opportunities. In addition to improving our algorithms and underlying software, we also intend to continue to invest in ways of extracting greater value from the data we collect for the benefit of our customers. We believe these investments will enhance our value proposition for both existing and prospective customers. |

|

· |

Extend Global Footprint. To best support our global advertisers, we plan to utilize our cloud-based architecture to expand our international presence in a cost-effective manner. |

9

Our Customers

Our customers include many of the world’s leading advertisers. For example, during 2014, advertising for 83 advertisers listed on the 2013 AdAge Top 100 U.S. Brands was placed through our platform. Our Platform Direct customers primarily consist of brands, agencies, agency trading desks, ad networks and publishers. Our Platform Services customers are primarily composed of media agencies working on behalf of brand advertisers. For 2014, we had 333 Platform Direct Clients and we had 228 Platform Services customers that had Total Spend of at least $10,000 through our platform. For this purpose, all branches of a single entity are considered a single Platform Services customer. Platform Direct customers that had Total Spend (excluding revenue, which equals spend, from our video syndication software offering) with us of less than $10,000 through our platform had spend of $263,000, $389,000 and $679,000 in the years ended December 31, 2012, 2013 and 2014.

There were no customers that accounted for more than 10% of our revenue during the year ended December 31, 2014. For this purpose, we define a Platform Direct customer as one which operates under a distinct contract with us for our Platform Direct offering and we define a Platform Services customer as one which has provided an insertion order and has a distinct billing address. Branches or divisions of an advertiser that operate under distinct contracts are generally considered as separate customers. In particular, we treat as separate customers different groups within global advertising agencies if they are based in different jurisdictions or with respect to which we have negotiated and manage separate contractual relationships. If all branches and divisions within each global advertising agency were considered to be a single customer, WPP plc and Publicis Groupe SA would have represented 17% and 12% of our 2014 total revenue, respectively.

Information about Segment and Geographic Revenue

Information about segment and geographic revenue is set forth in Note 11 of the Notes to Consolidated Financial Statements under Item 8 “Financial Statements and Supplementary Data” of this Report.

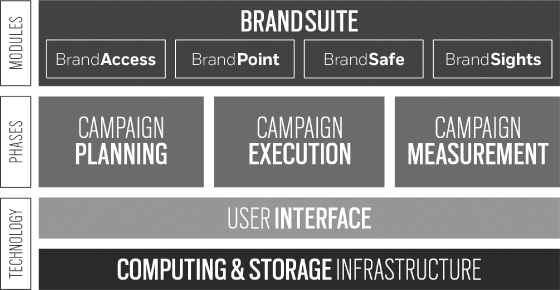

Our Platform

Our platform integrates the various technology components and digital video ad inventory sources required to enable advertisers to manage and execute digital video advertising globally. Our platform is cloud-based and accessed using a simple and intuitive user interface. The components are organized into the three phases of managing a campaign: campaign planning, campaign execution and campaign measurement. In addition, we offer specific modules as part of our BrandSuite that integrate various platform components to create distinct solutions for our customers. The following graphic illustrates these components of our platform:

User Interface

Our user interface simplifies the video ad buying process and enables advertisers to launch sophisticated video campaigns in minutes. Each feature of the interface has been designed with the user in mind and offers an intuitive approach to planning campaigns, buying impressions, optimizing spend and measuring campaign effectiveness. Users can easily view trends in key campaign statistics over any time period, view sites, pacing, spend and key statistics for each placement and manage campaigns, creative assets, inventory sources and brand surveys from one interface.

10

Campaign Planning

Customers access the information critical for campaign planning and then select the campaign parameters they require. Our interface dynamically predicts available inventory levels based on the targeting options and video ad formats selected by the customers.

Global Inventory

Using our platform, customers can access inventory across both public and private sources of inventory, on desktop, mobile and connected TV devices, in over 70 countries. We display inventory availability by publisher and ad format, enabling our customers to plan campaigns more effectively.

|

· |

Public Inventory Sources. We connect with a large number of video ad exchanges, including all major exchanges. In addition, our TubeMogul Select offering allows access to inventory from super premium publishers that only make their inventory available to limited high quality advertisers. |

|

· |

Private Inventory Sources. Many publishers seek to control their premium inventory and offer it directly to advertisers. Using our BrandAccess module, advertisers can establish an automated connection to inventory they buy directly from premium publishers using our platform. By consolidating private inventory onto our platform, customers benefit from integrated planning, buying and reporting for their entire video buy. This provides customers with a more streamlined workflow, consistent application of targeting data and optimization across sources of inventory. |

Audience Targeting

Our platform offers advertisers control over multiple targeting parameters to enable them to deliver video campaigns to their desired audiences. Targeting options that can be selected include first- and third-party audience data, site-level contextual targeting, keyword topic targeting, global geo targeting, device, operating system, day of week and time of day.

Ad Formats and Rich Media

There are many different ways to present video advertising on digital devices and we enable access to inventory across video ad formats including: pre-roll, in-banner (user-initiated), social, mobile, tablet and connected TV. An ad configurator within our platform allows simple and rapid creation of interactive creative elements, such as call-to-action animations, banner overlays or social network sharing buttons.

Campaign Execution

Our powerful, real-time optimization and decisioning engine helps enhance brand advertising performance while at the same time focusing on brand safety.

Media Buying

Our platform automates impression buying and ad serving for campaigns. Based on budget and targeting parameters set in the planning module, our platform continually evaluates impressions across sources of inventory and dynamically bids for each impression. When an auction is won, the platform serves the ad to the publisher site to be displayed to the user. The entire process typically takes less than 0.25 seconds.

Decisioning and Optimizing

Our platform enables customers to purchase the “best” impression each time according to the audience targeting criteria established in the campaign planning phase. Each second, our platform evaluates as many as 150,000 ad impressions, determines which impressions would be desirable for our customers, based on their targeting criteria, and bids accordingly.

In addition to the decisions made on each bid for an ad impression, our platform continually evaluates which of the criteria are delivering the best performance and then automatically makes adjustments to the bidding strategy to help maximize overall campaign performance.

11

Fraudulent Placements and Brand Safety

Using site, page and player safety technology, our platform is designed to screen and block sites with objectionable content, in-banner auto-play ad placements and fraudulent bot-driven traffic, with the goal of ensuring that ad placements are consistent with campaign objectives. Our multi-layered approach for protecting brand equity includes manual site screening and categorizing of websites according to content quality, combined with technology that assesses page and placement level content.

Campaign Measurement

We reduce the complexity typically associated with video ad buys by offering a unified view of advertising performance across the campaign for all sources of inventory. Comprehensive and granular site, audience and video level analytics are delivered in real-time across all sources of inventory accessed through our platform.

Audience Verification

We enable advertisers to compare the reach and frequency of their digital and TV campaigns with a common GRP metric through our integration with Nielsen reporting. In addition, our audience analytics help brands gain valuable insights into the types of consumers they reach with information about age, gender and other relevant demographic traits that are important to advertisers. Using our platform, advertisers are able to dynamically review gender distribution, verify the audience reached by a campaign and cost per point and review the age breakdown for each campaign.

Brand Metrics

We offer our proprietary integrated brand survey module that enables advertisers to understand the impact of a campaign with survey-based measurement of brand awareness, favorability, purchase intent and other metrics. We also support major third-party brand survey providers.

Video Analytics

We provide transparent, site-by-site video analytics that enable advertisers to measure the effectiveness of their campaigns. Detailed information on how viewers are consuming videos includes real-time tracking and analysis for metrics such as viewed minutes, completion rates, playtime per view, social shares and geo tracking down to the city level.

Viewability Measurement

We offer viewability reporting that enables advertisers to determine whether their ads were viewed based upon 11 metrics including viewable impressions, viewability rate, viewable completions and player size. Our viewability reporting is based on OpenVideoView, an open source software technology originally developed by us. We founded the OpenVideoView consortium, which is currently supported by over 30 industry members.

BrandSuite

To supplement the various phases of our campaign management platform, we offer our BrandSuite collection of software modules. These modules include:

BrandAccess

BrandAccess enables advertisers to automate direct buys of inventory from premium publishers and other sources of inventory, including ad networks. With BrandAccess, our customers benefit from improved on-target audience delivery and viewability reporting across all the sources of video inventory they utilize.

BrandPoint

BrandPoint provides a simple solution for advertisers that want to plan, buy and measure digital video based on GRPs. By mirroring broadcast buying practices — such as the ability to target by demographic criteria and desired GRPs — advertisers can execute digital video campaigns in a comparable way to TV. BrandPoint is built on proprietary audience modeling technology that is designed to continually learn and adjust automatically over time and includes integrated Nielsen-verified reporting.

BrandSafe

BrandSafe is our multi-layered approach to protect brand equity that is part of our core platform and includes:

12

SiteSafe. Every site that is available on our platform has been manually screened and categorized into a 3-Tier structure by site quality. Advertisers have complete control over which tiers they are comfortable running on and are able to select sites before, and even during, a campaign.

PageSafe. PageSafe examines the content of individual web pages and determines if they contain objectionable content. This technology is integrated into our real-time buying process, so we can block ads before they are served on pages with offensive content. Pages are categorized into safety ratings (G, PG-13, PG, R) and topics that may be objectionable to the advertiser, such as alcohol, tobacco or adult content, and advertisers can select the safety rating and topics on which they want to avoid running ads.

PlaySafe. PlaySafe prevents in-banner auto-play video ads from running within display banners on low quality sites. We manually identify and categorize these placements on the platform and run PlaySafe technology to detect ad unit and video player size.

BrandSights

BrandSights is an integrated survey module that enables advertisers to gather insights in real-time. In the same way video campaigns are set up and managed on our platform, BrandSights enables customers to easily create, target and launch customized surveys to measure brand awareness, favorability and purchase intent.

Programmatic Television (PTV)

TubeMogul PTV provides advertisers with an automated solution to plan, buy and measure TV ads. PTV enables brands to access linear TV inventory and use richer audience attributes to target their TV buys, all through the same software they use to execute their digital video ad buys.

Customer Service, Support and Training

We offer a full-service campaign management solution that runs on our platform for those advertisers seeking to transact on a campaign-by-campaign basis using our Platform Services team. This team utilizes our platform to execute campaigns according to customer specifications. Our sales and support teams respond to RFPs, execute campaigns and provide periodic reporting.

As part of our Platform Direct offering, we provide a dedicated customer support team to our customers. This team assists customers with advanced campaign setup and execution as needed. This team also educates customers on the benefits of our platform and provides training to customers to enable them to extract the most value from our platform. We also have a dedicated training team that designs the training curriculum, manages our extensive “Help Wiki” that customers can access via our platform, and runs the certification program we offer our customers to verify their skill level in using our platform.

Technology and Infrastructure

Our platform is the result of a significant and sustained financial investment over seven years of research and engineering efforts. Our product and research and development organizations are responsible for the design, development and testing of our platform. We are committed to continuous innovation and rapid introduction of new technologies, features and functionality that bring value to our customers.

Core elements of the platform include:

|

· |

Scalable Big Data Architecture. Our platform is composed of scalable and flexible services built from proprietary and open-source technologies. On a daily basis, the platform reviews billions of ad opportunities and runs over 10 terabytes of queries on this data. Our platform infrastructure is a hybrid of cloud services and collocated facilities in six global data centers across three continents. |

|

· |

Real-Time Bidding. On average, our real-time bidding technology evaluates more than 30 billion ad opportunities per day, with each ad opportunity evaluated in less than approximately 50 milliseconds. Our core bidding technology utilizes adapters that allow it to communicate in the format required by different sources of inventory. This allows our platform to easily adapt to a variety of inventory formats, including across channels such as mobile and connected TV. |

|

· |

User Demographics Predictive Models. Our machine learning team leverages the massive data sets captured by our platform to build predictive models around user demographic attributes to maximize alignment with Nielsen Online Campaign Ratings and/or Comscore Validated Campaign Essentials, the primary third-party verification services for the digital video advertising industry. Data from our platform is continually fed back into these models, which are reconstructed daily, and improve with engagement with consumers. |

13

|

· |

Optimization. During campaign execution, the optimization engine continually scores a variety of attributes of each impression, such as website, industry vertical or geography, for their likelihood to achieve campaign performance goals. Our real-time bidding engine then shifts budget in real-time to those delivering the most optimal performance. Our platform enables customers to set multiple, simultaneous optimization goals. |

|

· |

Video Ad Serving. Our platform includes a robust, globally-distributed video ad server capable of low-latency delivery of digital video ads onto digital devices. The ad server supports uploading video files, transcoding files into the required format and rendering custom interactive components. |

|

· |

Real-Time Analytics. Data is collected regarding inventory available for ad opportunities for continuous assessment of the availability of advertising inventory and the associated costs of that inventory. In addition, real-time campaign delivery and spend totals are used to manage campaign budgets and goal caps, as well as for campaign reporting. All collected data is fed back into the optimization engine to improve campaign performance, and into machine-learning models for user demographic predictive modeling. |

|

· |

World-Class User Interface. A self-serve user interface provides a robust and intuitive set of campaign workflow management, data reporting and visualization tools, ensuring video advertising campaigns can be easily managed by our broad customer set. User experience and interface design have been paramount in designing an interface that is as simple as most consumer products. |

|

· |

Partner Integrations. Our platform is integrated with over 300 sources of inventory and dozens of data management platforms and data exchanges, making thousands of targeting segments available for reaching a desired audience through our platform. Our platform incorporates numerous third-party ad servers, ad verification services, survey vendors and other third-party campaign tools to streamline various campaign execution processes. |

The technical infrastructure for our platform is currently primarily managed through third-party web hosting services providers, or third-party service providers, and to a limited extent our own servers which are located at a third-party data center facility. We do not have long term agreements with these service providers and the operator of the data center facility.

Our research and development expenses were $7.4 million, $11.8 million and $22.1 million for the years ended December 31, 2012, 2013 and 2014, respectively.

Sales and Marketing

Sales

Our global sales force is focused on growing the number of our customers, particularly our Platform Direct customers. We plan to selectively add to our sales force. Our Platform Direct sales team sells our enterprise software solution to customers who want to directly manage and execute their digital video advertising initiatives. These customers include brands, agencies, agency trading desks, ad networks, and publishers seeking to augment their own inventory to satisfy their campaign commitments. Platform Direct sales are complex and difficult to complete. Prospective customers generally consider a number of factors at a senior level and over an extended period of time. Our Platform Direct sales team seeks to build relationships with senior-level decision makers, usually vice president and above at these organizations, and focuses their efforts on informing prospective customers about the value our platform offers. Our Platform Services team primarily addresses media agencies working on behalf of brand advertisers who prefer a fully managed service solution and typically purchase through an RFP and insertion order process. Our Platform Services team includes salespeople and the account managers who execute and optimize campaigns on our customers’ behalf.

Marketing

Our marketing activities are focused on increasing awareness of our brand, executing thought-leadership initiatives, supporting our direct sales team and generating new advertiser leads. We seek to accomplish these objectives by presenting at industry conferences, hosting customer conferences, publishing white papers and research, public relations, social media, and executing integrated advertising campaigns that include direct e-mail, digital advertising, webinars and blog posts.

We host three annual customer conferences, known as TubeMogul University, in North America, Europe and Asia-Pacific. We offer 2-3 days of education, training and other activities at these conferences. We believe these events have increased our profile in each region, developed our reputation as a thought-leader in the industry and helped to solidify relationships with customers.

Employees and Culture

As of December 31, 2014 we had 416 worldwide employees, 77 of which are located outside of the United States, or U.S. Our engineering and product teams reside primarily within our Emeryville, California headquarters. None of our employees are covered by collective bargaining agreements. We believe our employee relations are good and we have never experienced any work stoppages.

14

We have a strong, founder-led culture that is cultivated and sustained through highly coordinated training and performance management. We have received many industry awards, including the 2013 ASPY Award for Best Customer Service and in 2015 were named 5th Best Place to Work by Glassdoor for Small and Medium Businesses in the U.S.

Competition

The market to provide programmatic solutions for digital video brand advertising is at an early stage of development. As such, this market is rapidly evolving and highly competitive, subject to changing technology, branding objectives and customer demands. We compete primarily with companies developing solutions to automate the purchase of video advertising impressions across multiple sources of inventory. We also compete with other companies that address certain aspects of the digital video advertising market, including demand-side platforms and video-focused ad networks, and in-house tools and custom solutions currently used by brand advertisers and their agencies and by publishers to manage advertising activities. In addition, we compete for advertising spend with large entities that offer digital video advertising services as part of a larger solution for digital media buying. In the future, we may compete with companies developing comprehensive marketing platforms. Other companies that offer analytics, mediation, exchange or other third-party specific technologies may also compete with us. As our platform evolves and we introduce new technologies, features and functionality of our platform, we may become subject to additional competition. Some of our current and prospective competitors in the broader digital advertising market have substantially greater resources and longer histories than us in the digital advertising space, may actively seek to serve our market and have the power to significantly change the nature of the marketplace to their advantage. These companies could develop and offer new solutions that directly compete with ours or leverage their position to make changes to their existing platforms that could be disadvantageous to our competitive position.

We believe the principal competitive factors in our industry include the availability of brand-focused tools and an easy to use user interface, the capability to enable advertisers to effectively reach target audiences, multi-device campaign execution capability, buy-side positioning, proven and scalable technologies, relationships with leading brand advertisers and their respective agencies and brand awareness and reputation. We believe that we compete favorably with respect to all of these factors and are well-positioned as a provider of a digital video brand advertising software platform.

Intellectual Property

The protection of our technology and intellectual property is an important component of our success. We rely on intellectual property laws, including trade secret, copyright, trademark and patent laws in the U.S. and abroad, and use contracts, confidentiality procedures, non-disclosure agreements, employee disclosure and invention assignment agreements and other contractual rights to protect our intellectual property.

As of December 31, 2014, we held one issued U.S. patent, which expires in 2028 and had filed 11 non-provisional patent applications and four provisional patent applications in the U.S. In addition, we maintain a trademark portfolio including common law trademarks, trademark applications pending in the U.S., Canada and the European Union, or EU, and a trademark registration with the World Intellectual Property Organization.

Circumstances outside of our control could pose a threat to our intellectual property rights. Effective intellectual property protection may not be available in the U.S. or other countries in which we provide our solution. In addition, the efforts we have taken to protect our intellectual property rights may not be sufficient or effective. Any impairment of our intellectual property rights could harm our business, our ability to compete and harm our operating results. In addition, as the number of competitors grows and solutions of competitors overlap, we may in the future face claims by third parties that we infringe upon or misappropriate their intellectual property rights, and we may be found to be infringing upon or to have misappropriated such rights. In the future, we, or our customers, may be the subject of legal proceedings alleging that our solutions or underlying technology infringe or violate the intellectual property rights of others.

15

Privacy and Government Regulation

We and our customers use data about Internet users collected through our platform to manage and execute ad campaigns in a variety of ways, including delivering advertisements to Internet users in particular geographic locations and using particular devices, and to enhance the accuracy of our demographic categorization of websites and Internet users. In addition, our customers may elect to use their own data about Internet users and data segments provided by third-party data companies on our platform to target advertisements to particular audiences. We do not use data that can be used to identify specific people, and we take steps to avoid collecting such personally identifiable information from any source. The definition of personally identifiable information, or personal data, however, varies by country and is evolving, and therefore we have to continually assess our technology platform against an evolving legal landscape. Future regulation affecting our ability to collect and use this data could harm our business. The collection and use of data about Internet users has come under scrutiny by consumer advocacy organizations and regulatory agencies in the U.S. and abroad that focus on online privacy. More specifically, these groups have voiced concern about the use of cookies and other online tools to record an Internet user’s browsing history, and the use of that information to deliver advertisements online based on inferred interests of the Internet user. If future regulation, industry standards or consumer preferences make the collection or use of such data more difficult or impracticable, the value of online advertising could be adversely affected which, in turn, could impact the demand for our products. The costs of compliance with privacy and other laws and regulations are high and are likely to increase in the future and any failure on our part to comply with laws and regulations may expose us to significant liabilities.

We participate in several industry self-regulatory organizations, including the Network Advertising Initiative, or NAI, the Digital Advertising Alliance, or DAA, and the Internet Advertising Bureau. The self-regulatory principles for “interest based” or “online behavioral” advertising upheld by the NAI, the DAA and other organizations require us to provide consumers with notice and choice, including the ability to opt out of interest-based advertising. Our privacy policy offers consumers an easy, one-click opt-out mechanism, which we highlight for consumer users by using an icon with a link to our privacy policy in or around advertisements we handle that are targeted based on consumer interests. In addition to industry self-regulation, our compliance with our privacy policy is also subject to regulation by the U.S. Federal Trade Commission which may bring enforcement actions under Section 5 of the Federal Trade Commission Act against unfair and deceptive trade practices, including the violation of privacy policies.

Corporate Information

TubeMogul was incorporated in California in March 2007 and reincorporated in Delaware in March 2014. Our principal executive offices are located at 1250 53rd Street, Suite 2, Emeryville, California 94608, and our telephone number is (510) 653-0126. Our corporate website address is www.tubemogul.com. Information contained on, or that can be accessed through, our website does not constitute part of this Report and inclusions of our website address in this Report are inactive textual references only.

Available Information

We file Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, proxy and information statements and amendments to reports filed or furnished pursuant to Sections 13(a), 14 and 15(d) of the Securities Exchange Act of 1934, as amended, or the Exchange Act. The public may obtain these filings at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549 or by calling the SEC at 1-800-SEC-0330. The SEC also maintains a website at http://www.sec.gov that contains reports, proxy and information statements and other information regarding TubeMogul and other companies that file materials with the SEC electronically. Copies of our reports on Form 10-K, Form 10-Q and Form 8-K, may be obtained, free of charge, electronically through our internet website, http://investor.tubemogul.com/sec.cfm.

16

You should carefully consider the risks described below together with the other information set forth in this Report, which could materially affect our business, financial condition and future results. The risks described below are not the only risks facing our company. Risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially adversely affect our business, financial condition and operating results. If any of the following risks is realized, our business, financial condition, results of operations and prospects could be materially and adversely affected. In that event, the trading price of our common stock could decline.

Risks Related to Our Business

We have a history of losses and we may not achieve or sustain profitability in the future.

We have incurred losses in each fiscal year since our incorporation in 2007 and had an accumulated deficit of $23.3 million as of December 31, 2014. We may not be profitable in the future as we anticipate that our operating expenses will increase significantly in the foreseeable future as we continue to invest in research and development to enhance our platform and in sales and marketing to acquire new customers. These efforts may prove more expensive than we currently anticipate, and we may not succeed in increasing our revenue sufficiently to offset these higher expenses. Even if we are successful in increasing our customer base, we may not become profitable in the future or may be unable to maintain any profitability achieved if we fail to increase our revenue and manage our operating expenses or if we incur unanticipated liabilities. Although our revenue has increased substantially in recent periods, we may not be able to sustain this rate of revenue growth. Revenue growth may slow or revenue may decline for a number of reasons, including slowing demand for our offering, increasing competition, lengthening sales cycles, decelerating growth of, or declines in, our overall market, or our failure to capitalize on growth opportunities or to introduce new offerings. We could also incur increased losses as we continue to focus on growing our Platform Direct offering because the sales cycle with those customers tends to be protracted, resulting in the majority of costs associated with sales of our Platform Direct offering being generally incurred up front, while customers are billed over time through our usage-based pricing model. Any failure by us to achieve and maintain profitability could cause the price of our common stock to decline significantly.

Our limited operating history makes it difficult to evaluate our current business and future prospects.

Although we began our operations in March 2007, we did not launch our platform or begin generating substantial revenue until the second half of 2011. While we have experienced significant growth in recent periods, our short operating history and developing business model make it difficult to evaluate our current business and our future prospects. We have encountered and will continue to encounter risks and difficulties frequently experienced by growing companies in rapidly developing and changing industries, including challenges in forecasting accuracy, determining appropriate investments of our limited resources, market acceptance of our platform and future features and functionality, competition from new and established companies, including those with greater financial and technical resources, acquiring and retaining customers and increasing revenue from existing customers, enhancing our platform and developing new technologies, features and functionality. You should consider our business and prospects in light of the risks and difficulties that we will encounter as we continue to develop our business model. We may not be able to address these risks and difficulties successfully, which would materially harm our business and operating results and cause the market price of our common stock to decline.

We may not maintain our recent revenue growth.

Our revenue growth will depend, in part, on our ability to acquire new customers, gain a larger amount of our existing customers’ advertising spend, continue to innovate and develop new technologies, features and functionality, extend our global footprint and increase our share of and compete successfully in new, growing digital video advertising markets, and we may fail to do so. A variety of factors outside of our control could affect our revenue growth, including changes in spend budgets of advertisers and the timing and size of their spend. Decisions by advertisers to delay or reduce their advertising spending or divert spending away from video advertising could slow our revenue growth or reduce our revenue. Our success in implementing our strategy of migrating customers from our Platform Services offering to our Platform Direct offering could also slow our revenue growth as we recognize a higher amount of revenue from the same amount of spend associated with our Platform Services offering than with our Platform Direct offering. You should not consider our recent growth rate in revenue as indicative of our future growth.

We may experience quarterly fluctuations in our operating results due to a number of factors which make our future results difficult to predict and could cause our operating results to fall below expectations.

Our quarterly operating results may fluctuate due to a variety of factors, many of which are outside of our control. As a result, comparing our operating results on a period-to-period basis may not be meaningful. You should not consider our past results, including our recent growth rates in terms of advertising spend and revenue, as indicative of our future performance.

17

In addition to other risk factors listed in this section, factors that may affect our quarterly operating results include the following:

|

· |

fluctuations in demand for our platform, including seasonal variations in our customers’ advertising spend; |

|

· |

the level of advertising spend managed through our platform for a particular quarter and the mix between spend managed through our Platform Direct offering and Platform Services offering; |

|

· |

budgeting cycles and changes in video advertising budgets of and spending by our customers; |

|

· |

the length and associated unpredictability of our sales cycle; |

|

· |

the timing and amount of operating expenses related to the maintenance and expansion of our business, operations and infrastructure; |

|

· |

the timing and amount of investment in the development of new technologies, and features and functionality of our platform; |

|

· |

changes in the availability or price of advertising inventory; |

|

· |

the timing and success of changes in our offerings or those of our competitors; |

|

· |

changes in our pricing or pricing of our competitors’ solutions and changes in the pricing of digital video advertising generally; |

|

· |

network outages or security breaches or the perception that our platform or customer or consumer data is not secure and any associated expenses; |

|

· |

delay between our payments for advertising inventory purchased through our platform and our subsequent collection of fees from our customers related to that inventory; |

|

· |

changes in the competitive dynamics of our industry, including consolidation among competitors or customers; |

|

· |

changes in government regulation applicable to our industry; |

|

· |

foreign currency exchange rate fluctuations; and |

|

· |

general economic and political conditions in our domestic and international markets. |

Based upon all of the factors described above, we have a limited ability to forecast our future revenue, costs and expenses, and as a result, our operating results may from time to time fall below our estimates.

If our customers do not maintain and increase their advertising spend through our platform, our revenue growth and results of operations will be adversely affected.

Our contracts and relationships with advertisers generally do not include long-term or exclusive obligations requiring them to use our platform or maintain or increase their advertising spend on our platform. Furthermore, advertisers generally use multiple providers in managing advertising spend. Accordingly, we must convince our customers to use our platform, increase their usage and spend a larger share of their advertising budgets with us, and do so on an on-going basis. We may not be successful at educating and training customers, particularly our newer customers, on the benefits of our platform to increase usage and generate higher levels of advertising spend. If these efforts are unsuccessful or advertisers decide not to continue to maintain or increase their advertising spend through our platform for any other reason, then we may not attract new advertisers or our existing customers may reduce their video advertising spend through or cease using our platform. Therefore, we cannot assure you that advertisers that have generated advertising spend through our platform in the past will continue to generate similar levels of advertising spend in the future or that they will continue to use our platform at all. We may not be able to replace customers who decrease or cease their usage of our platform with new customers that spend similarly on our platform. If our existing customers do not continue to use and increase their use of our platform, or if we are unable to attract sufficient advertising spend on our platform from new customers, our revenue could decline, which would materially and adversely harm our business and results of operations.

18