Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - BANC OF CALIFORNIA, INC. | d885911d8k.htm |

| EX-99.1 - EX-99.1 - BANC OF CALIFORNIA, INC. | d885911dex991.htm |

2014 Fourth

Quarter Earnings March 6, 2015

Investor Presentation

Exhibit 99.2 |

| 1

1

Forward-looking Statements

When used in this presentation and in documents filed with or furnished to the Securities and

Exchange Commission (the “SEC”), or other public shareholder communications,

or in oral statements made with the approval of an authorized executive officer, the words or phrases “believe,” “will,” “should,” “will likely

result,” “are expected to,” “will continue,” “is

anticipated,” “estimate,” “project,” “plans,” or similar expressions are intended to identify “forward-looking

statements” within the meaning of the Private Securities Litigation Reform Act of 1995.

You are cautioned not to place undue reliance on any forward-looking statements,

which speak only as of the date made. These statements may relate to future financial performance, strategic plans or objectives, revenue,

expense or earnings projections, or other financial items of Banc of California Inc. and its

affiliates (“BANC,” the “Company,” “we,” “us” or “our”). By their

nature, these statements are subject to numerous uncertainties that could cause actual results

to differ materially from those anticipated in the statements. Factors that could cause actual results to differ materially from the results anticipated or

projected include, but are not limited to, the following: (i) risks that the

Company’s recently completed acquisitions, including the acquisitions of branches from Banco Popular, The Private Bank of California, CS Financial, Inc.,

and The Palisades Group, may disrupt current plans and operations, the potential difficulties

in customer and employee retention as a result of those transactions and the amount of

the costs, fees, expenses and charges related to those transactions; (ii) the credit risks of lending activities, which may be

affected by further deterioration in real estate markets and the financial condition of

borrowers, may lead to increased loan and lease delinquencies, losses and nonperforming

assets in our loan portfolio, and may result in our allowance for loan and lease losses not being adequate to cover actual losses and

require us to materially increase our loan and lease loss reserves; (iii) the quality and

composition of our securities and loan portfolios; (iv) changes in general economic

conditions, either nationally or in our market areas; (v) continuation of the historically low short-term interest rate environment, changes in the

levels of general interest rates, and the relative differences between short- and

long-term interest rates, deposit interest rates, our net interest margin and

funding sources; (vi) fluctuations in the demand for loans and leases, the number of unsold

homes and other properties and fluctuations in commercial and residential real estate

values in our market area; (vii) results of examinations of us by regulatory authorities and the possibility that any such regulatory

authority may, among other things, require us to increase our allowance for loan and lease

losses, write-down asset values, increase our capital levels, or affect our ability

to borrow funds or maintain or increase deposits, which could adversely affect our liquidity and earnings; (viii) legislative or regulatory

changes that adversely affect our business, including changes in regulatory capital or other

rules; (ix) our ability to control operating costs and expenses; (x) staffing

fluctuations in response to product demand or the implementation of corporate strategies that affect our work force and potential associated charges;

(xi) errors in our estimates in determining fair value of certain of our assets, which may

result in significant declines in valuation; (xii) the network and computer systems on

which we depend could fail or experience a security breach; (xiii) our ability to attract and retain key members of our senior

management team; (xiv) costs and effects of litigation, including settlements and judgments;

(xv) increased competitive pressures among financial services companies; (xvi) changes

in consumer spending, borrowing and saving habits; (xvii) adverse changes in the securities markets; (xviii) earthquake, fire or other

natural disasters affecting the condition of real estate collateral; (xix) the availability of

resources to address changes in laws, rules or regulations or to respond to regulatory

actions; (xx) inability of key third-party providers to perform their obligations to us; (xxi) changes in accounting policies and practices, as

may be adopted by the financial institution regulatory agencies or the Financial Accounting

Standards Board or their application to our business or final audit adjustments,

including additional guidance and interpretation on accounting issues and details of the implementation of new accounting methods; (xxii) war

or terrorist activities; and (xxiii) other economic, competitive, governmental, regulatory,

and technological factors affecting our operations, pricing, products and services and

the other risks described in this report and from time to time in other documents that we file with or furnish to the SEC. You should not place

undue reliance on forward-looking statements, and we undertake no obligation to update any

such statements to reflect circumstances or events that occur after the date on which

the forward-looking statement is made. |

2

2

Net Income

Net income available to common shareholders of $9.3 million, or $0.25 per diluted share

Return on average assets of 0.8% and return on average tangible common equity of 11.2%

2014 Fourth Quarter Accomplishments

Banco

Popular

Transaction

Completed the acquisition and conversion of the California footprint of Banco Popular with

$1.1 billion of loans and $1.1 billion of deposits

Transaction is immediately accretive to earnings

Approximately 97% of deposit balances retained as year-end 2014

Originations

& Loans

Originated

over

$1.3

billion

of

loans

during

the

fourth

quarter,

totaling

over

$5

billion

in

originations for the full year

Total assets of $6 billion as of year-end 2014 with loans over $5 billion

Dramatically

diversified

the

held

for

investment

loan

mix

to

66%

commercial

loans,

compared to 43% commercial loans as of year-end 2013

Capital

Raised $50 million of common stock through the direct private placement with Oaktree

and Patriot to support the Banco Popular transaction |

3

3

Income Statement –

Quarterly

4Q 2014

3Q 2014

4Q 2013

Net Interest Income

$46.3

$38.2

$33.3

Noninterest Income

40.9

44.1

34.5

Total Revenue

87.2

82.3

67.8

Expenses

(78.4)

(67.6)

(57.2)

Pre-Tax, Pre-Provision Income

8.8

14.7

10.6

Provision

(4.2)

(2.8)

(1.8)

Pre-Tax Income

4.6

11.9

8.8

Tax Benefit (Expense)

5.5

(0.7)

(5.5)

Net Income

10.2

11.2

3.3

Preferred Dividends

(0.9)

(0.9)

(1.0)

Net Income Available to Common

$9.3

$10.3

$2.4

Diluted Earnings Per Share

$0.25

$0.30

$0.12

ROAA

0.8%

1.0%

0.4%

ROATCE

11.2%

13.2%

5.9%

Average shares outstanding for diluted EPS

calculation

(1)

35.4

32.7

19.6

($ in millions except per share data)

*

Figures may not foot due to rounding.

1 Average shares outstanding include potential TEU conversions to common shares (in

millions). |

4

4

Income Statement –

Full Year

FY 2014

FY 2013

Net Interest Income

$155.3

$97.2

Noninterest Income

145.6

96.7

Total Revenue

300.9

194.0

Expenses

(264.2)

(178.7)

Pre-Tax, Pre-Provision Income

36.7

15.3

Provision

(11.0)

(8.0)

Pre-Tax Income

25.8

7.3

Tax Benefit (Expense)

4.5

(7.3)

Net Income

30.3

0.1

Preferred Dividends

(3.6)

(2.2)

Net Income Available to Common

$26.7

$(2.1)

Diluted Earnings Per Share

$0.91

$(0.14)

ROAA

0.7%

n/m

ROATCE

10.1%

n/m

($ in millions except per share data) |

5

5

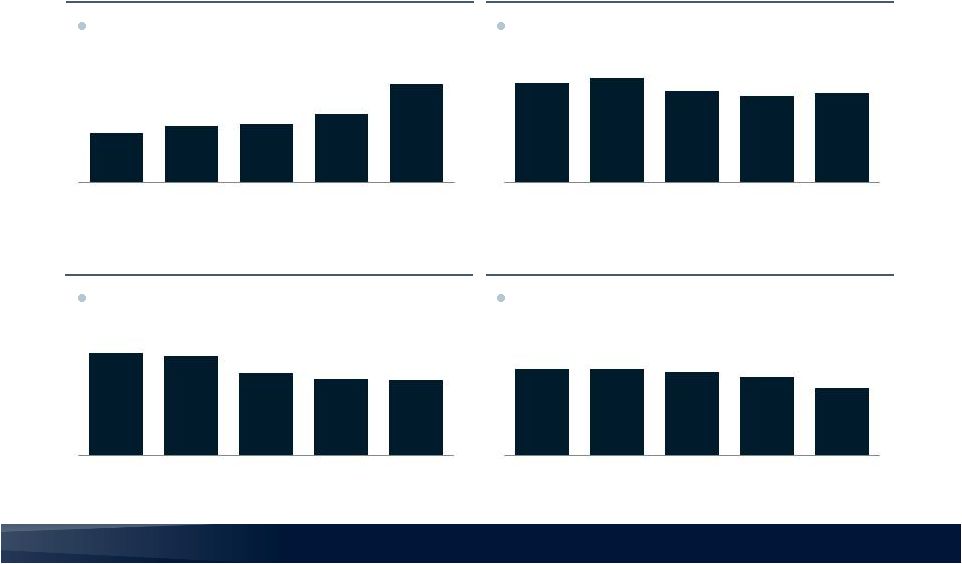

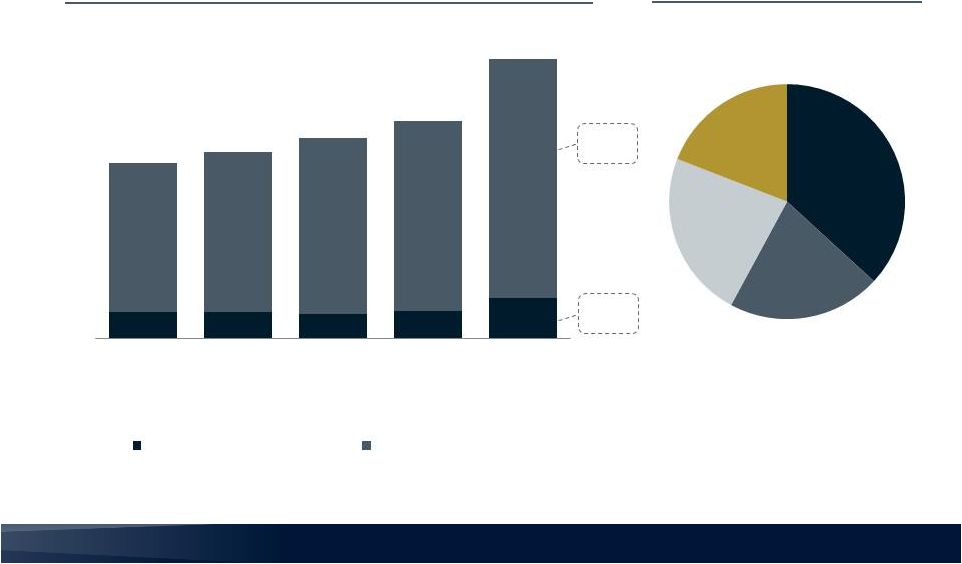

Net Interest Income and Net Interest Margin

Net

Interest

Income

($

in

millions)

Cost of Deposits

Loan Yields

Net Interest Margin

Popular acquisition contributed approximately $7

million to Q4 net interest income

Downward pressure on loan yields persists, partially

offset by acquired Popular assets

Consolidated net interest margin expanded due to

both Popular acquisition and deposit repricing

Both the addition of Popular and repricing of existing

deposits contributed to the favorable drop

0.77%

0.77%

0.74%

0.70%

0.60%

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

5.18%

5.12%

4.75%

4.62%

4.60%

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

3.90%

4.00%

3.70%

3.58%

3.65%

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

$33.3

$35.2

$35.6

$38.2

$46.3

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014 |

6

6

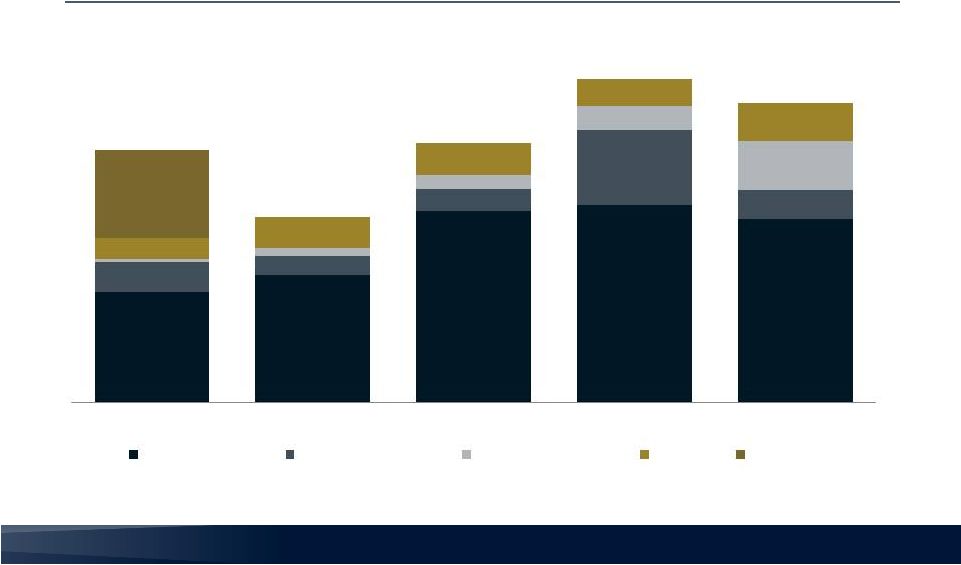

Noninterest Income

Noninterest Income

($ in millions)

$15.0

$17.3

$26.1

$26.9

$25.0

$4.2

$2.6

$3.0

$10.3

$3.9

$0.4

$1.1

$1.8

$3.3

$6.7

$2.8

$4.2

$4.4

$3.6

$5.2

$12.1

$34.5

$25.3

$35.4

$44.1

$40.9

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

Mortgage Banking

Gain on Sale of Loans

Advisory Service Fees

All Other

Branch Sale |

7

7

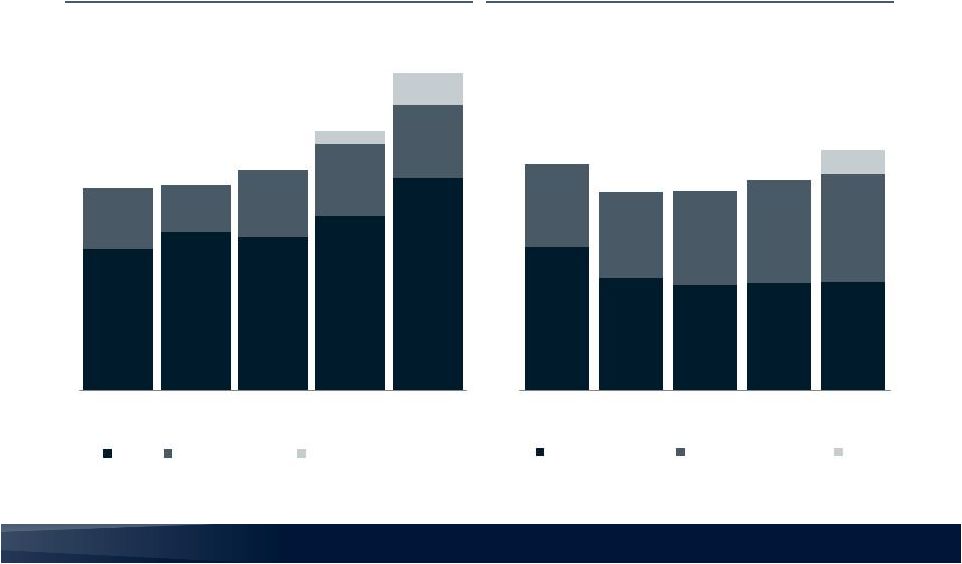

Noninterest Expense

($ in millions)

Number of Employees

(Headcount)

Noninterest Expenses

$57.8

$60.5

$57.2

1

$67.6

1 Includes mortgage-related commissions, bonus and loan-related

expenses. 2 Acquired employees from BPOP; retail branches,

business banking, commercial real estate, and operations. $78.4

2

$46.0

$49.1

$48.2

$52.0

$59.0

$11.3

$8.7

$12.3

$13.2

$13.5

$2.4

$5.9

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

Base

Volume-Related

Acquisition/Non-core

878

690

647

658

662

506

527

573

634

664

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

Banc Home Loans

Bank / TPG / HoldCo

BPOP

149

1,384

1,217

1,220

1,292

1,475 |

8

8

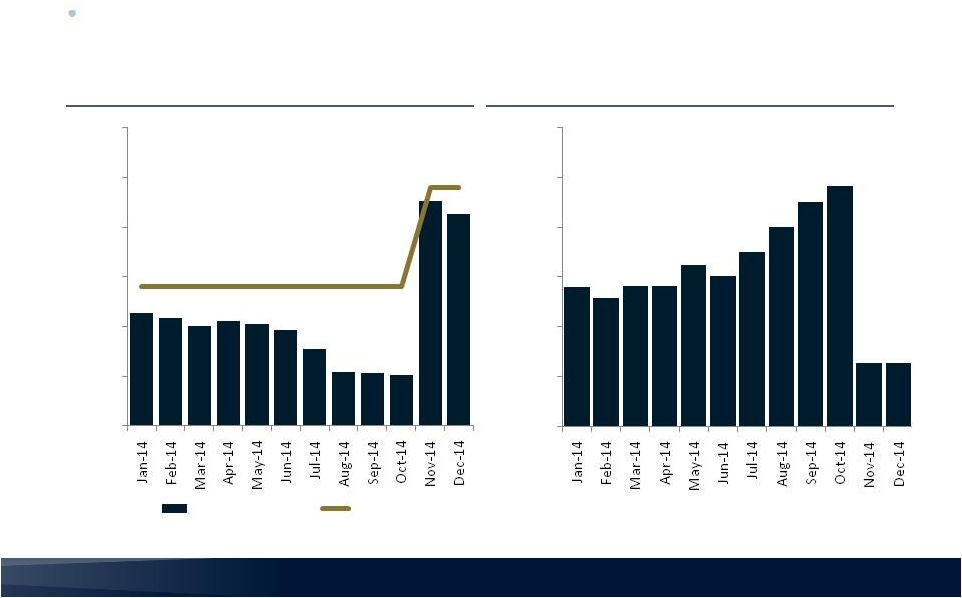

Efficiencies in Deposit Operations

FY 2014 All in Productivity

Annualized Salary Cost per Account

Popular

acquisition

added

scale

and

enhanced

productivity

within

deposit

operations

group

-

250

500

750

1,000

1,250

1,500

All In Productivity

Target

$

$50

$100

$150

$200

$250

$300

- |

9

9

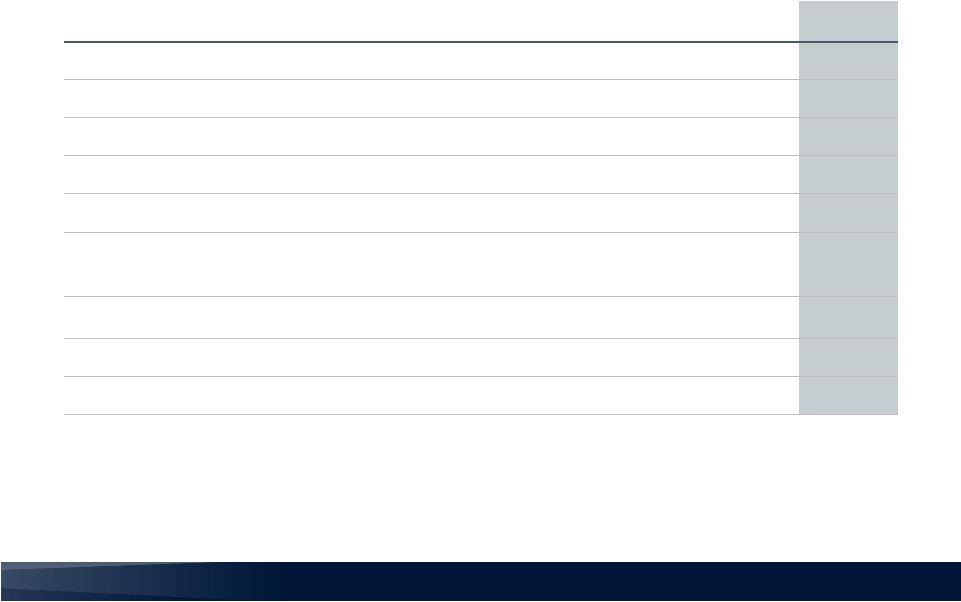

Balance Sheet

4Q 2014

3Q 2014

4Q 2013

Cash and All Deposits in Financial Institutions

$233

$187

$112

Securities

346

310

170

Loans Held for Sale

1,187

1,127

717

Loans Held for Investment

3,949

2,712

2,446

ALLL

(29)

(25)

(19)

All Other Assets

286

227

202

Total Assets

$5,972

$4,538

$3,628

Deposits

$4,672

$3,632

$2,919

FHLB Advances / Fed Funds Purchased

633

305

250

Notes Payable

94

96

82

All Other Liabilities

70

59

52

Total Liabilities

5,468

4,091

3,303

Equity

504

447

325

Total Liabilities and Equity

$5,972

$4,538

$3,628

($ in millions, period ending balances)

* Figures may not foot due to rounding. |

10

10

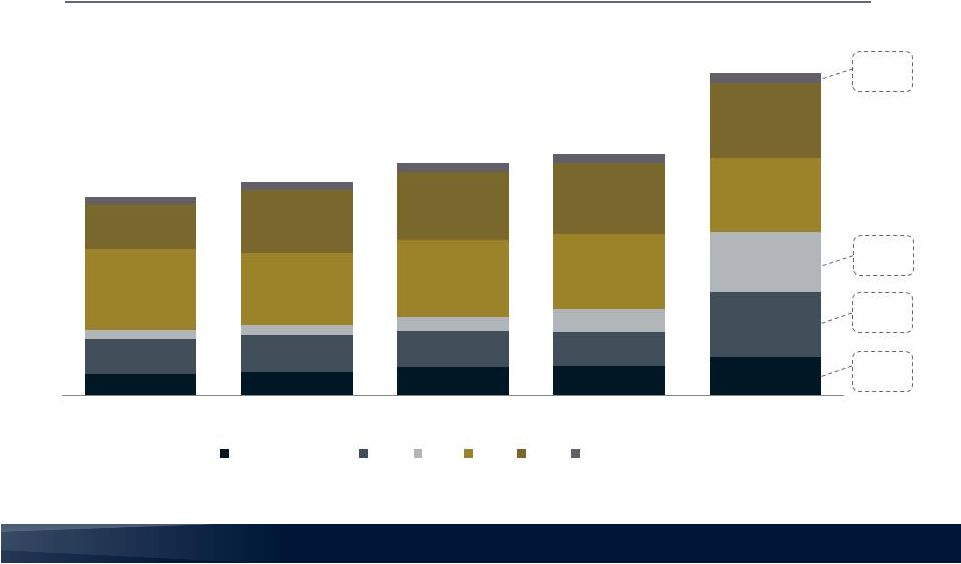

Loan Portfolio

* All Balances Period-End.

Total Loans (HFS/HFI)

($ in millions)

$480

BPOP

$497

BPOP

$54

BPOP

$23

BPOP

$347

$374

$455

$464

$613

$555

$586

$567

$548

$1,042

$142

$155

$234

$367

$956

$1,287

$1,159

$1,213

$1,191

$1,172

$717

$1,000

$1,096

$1,127

$1,187

$116

$123

$134

$142

$167

$3,163

$3,397

$3,698

$3,839

$5,136

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

C&I/SBA/Leasing

CRE

MF

SFR

HFS

Other Consumer |

11

11

Deposit Portfolio

$2.9

$3.1

$3.3

$3.6

* All Balances December 31, 2014 Period-End.

$4.7

Total Deposits

($ in billions)

Deposit Mix

(12/31/14 period end balance)

0.60%

0.70%

0.74%

0.77%

0.77%

Cost of

Deposits:

$.15

BPOP

$.9

BPOP

DDA /

NOW

37%

Savings

21%

MMDA

23%

CDs

19%

$0.43

$0.43

$0.41

$0.46

$0.66

$2.49

$2.68

$2.94

$3.17

$4.01

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

Noninterest-bearing Deposits

Interest-bearing Deposits |

12

12

Capital Position

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

Banc of California, Inc.

Tangible common equity to tangible assets

5.7%

5.1%

7.3%

7.2%

6.2%

Tier 1 leverage ratio

8.0%

7.6%

9.9%

9.3%

8.6%

Tangible book value per share

$10.06

$9.94

$11.45

$11.34

$10.54

Tangible book value per share, adjusted

1

$10.06

$9.94

$9.66

$9.89

$9.65

Banc of California, N.A.

Tier 1 leverage ratio

9.6%

9.4%

9.7%

9.8%

9.2%

Tier 1 risk based capital ratio

13.6%

13.5%

13.8%

14.8%

11.3%

Total risk based capital ratio

14.7%

14.5%

14.9%

15.8%

12.0%

1

Tangible equity per common stock and shares issuable under purchase contracts. Represents the

effect on TBV/share including conversion of TEUs to common shares

|

13

13

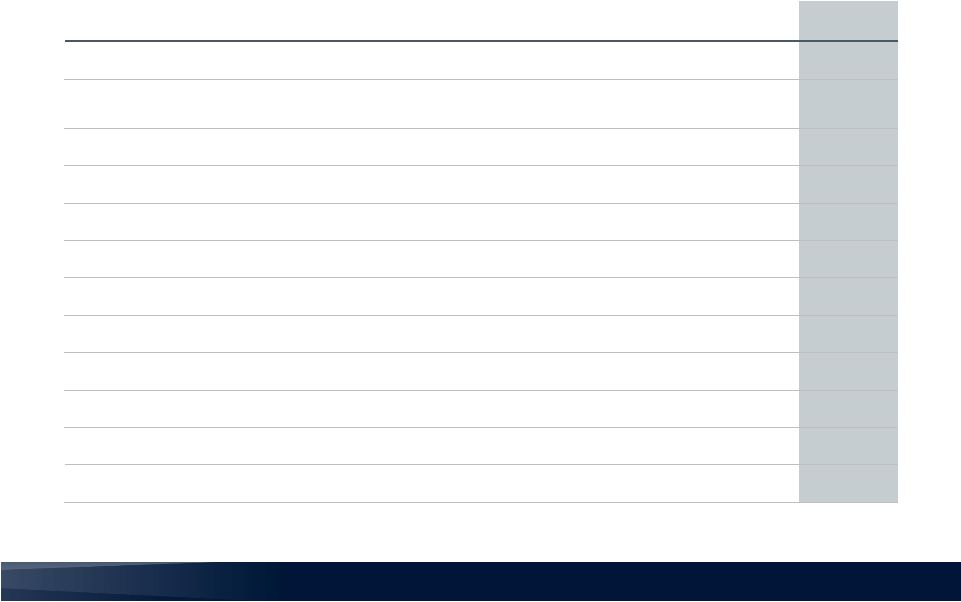

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

Total Loans (HFI + HFS)

$3.2 bln

$3.4 bln

$3.7 bln

$3.8 bln

$5.1 bln

Delinquent non-PCI loans to total non-PCI loans

2.43%

2.21%

2.69%

2.08%

1.55%

Non-performing Loans, excluding PCI loans

$31.6

$32.4

$41.6

$38.3

$38.4

NPLs / Loans (HFI)

1.29%

1.35%

1.60%

1.41%

0.97%

NPAs / Assets

0.87%

0.81%

0.96%

0.86%

0.65%

NPAs / Equity

9.7%

10.0%

9.6%

8.7%

7.7%

Net Charge Offs (recoveries)

$0.7

$(0.2)

$(0.3)

$0.2

n/m

Provision for Loan Losses

$1.8

$1.9

$2.1

$2.8

$4.2

ALLL ($)

$18.8

$20.0

$22.6

$25.3

$29.5

ALLL to Originated Loans

1.45%

1.43%

1.34%

1.33%

1.38%

ALLL & Discount / Loans

6.99%

6.32%

5.65%

4.45%

3.34%

ALLL / NPLs

59%

62%

54%

66%

77%

Asset Quality

($ in millions unless otherwise noted) |

14

14

1%

3.75 –

4.00%

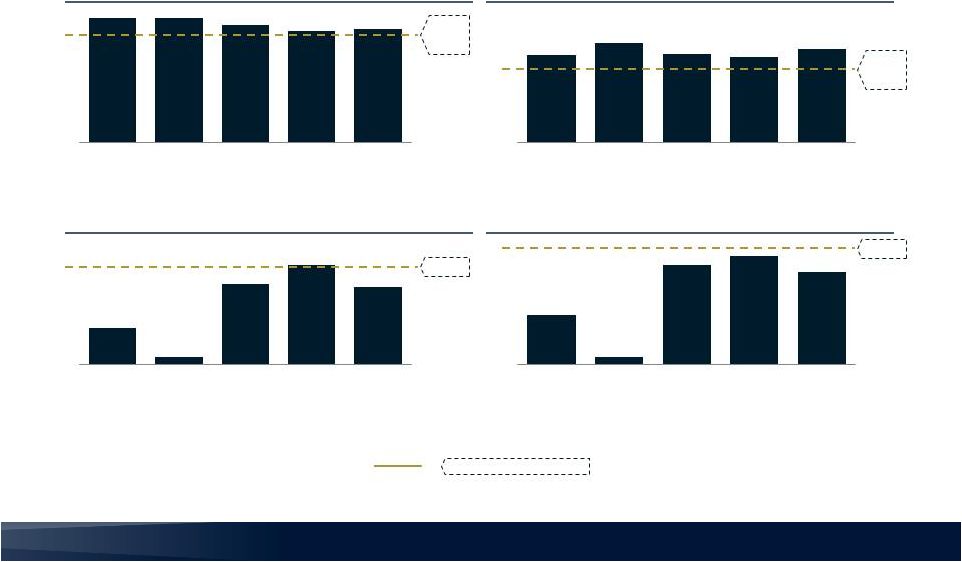

Financial Performance

15%

70 –

75%

1 Net Interest Margin shown for Banc of California, N.A. subsidiary. Excludes Holding Company

debt interest expense. Stated YE 2015 Targets

ROAA

ROATCE

Net Interest Margin

1

Efficiency Ratio

0.4%

0.1%

0.8%

1.0%

0.8%

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

6.0%

0.9%

12.0%

13.2%

11.2%

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

84%

96%

85%

82%

90%

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014

4.05%

4.19%

3.88%

3.78%

3.82%

4Q 2013

1Q 2014

2Q 2014

3Q 2014

4Q 2014 |