Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - AutoWeb, Inc. | abtl8k_feb262015.htm |

| EX-99.1 - PRESS RELEASE DATED FEBRUARY 26, 2015 - AutoWeb, Inc. | ex99-1.htm |

Exhibit 99.2

AUTOBYTEL INC.

Moderator: Jeff Coats

February 26, 2015

5:00 p.m. ET

|

Operator:

|

This is conference number 82791859.

|

Good afternoon everyone, and thank you for participating in today's conference call to discuss Autobytel's financial results for the fourth quarter and full year ended December 31, 2014.

Joining us today are Autobytel's President and CEO, Jeff Coats, the company's CFO, Curt DeWalt, the company's Senior Vice President of Business Analysis and Websites, Kim Boren, and the Company's outside investor relations adviser, Cody Slach with Liolios Group.

Following their remarks, we'll open the call for your questions.

As a reminder, today's call is being recorded. I’d now like to turn the call over to Mr. Slach for some introductory comments.

|

Cody Slach:

|

Thank you, Ben.

|

Before I introduce Jeff, I’ll remind you that during today's call, including the question-and-answer session, any projections and forward looking statements made regarding future events or Autobytel's future financial performance are covered by the safe harbor statements contained in today's press release, the slides accompanying this presentation, and the Company's public filings with the SEC. Actual events may differ materially from those forward looking statements.

Specifically, please refer to the Company's Form 10-K for the year ended December 31, 2014, which was filed prior to this call, as well as other filings made by Autobytel with the SEC from time to time. These filings identify factors that could cause results to differ materially from those forward looking statements.

There are slides included with today's presentation to help illustrate some of the points being made and discussed during the call. The slides can be accessed by clicking on the link in today's press release or by visiting Autobytel's website at autobytel.com. When there, go to “Investor Relations” and then click on “Events & Presentations.”

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 2

Please also note that during this call and/or in the accompanying slides, management will be disclosing EBITDA, adjusted EBITDA, adjusted EBITDA per diluted share, non-GAAP income and non-GAAP EPS, which are non-GAAP financial measures as defined by SEC Regulation G. Reconciliations of these non-GAAP financial measures to the most directly comparable GAAP measures are included in today's press release and/or in the slides which are posted in the Company's website.

And with that, I will now turn the call over to Jeff. Jeff?

|

Jeff Coats:

|

Thank you, Cody. Good afternoon, everyone. Thank you for joining us today to discuss our fourth quarter and full year 2014 results. We are pleased to note that we either achieved or exceeded our Q4 guidance on all metrics.

|

2014 was a pivotal year as we generated increases in nearly every metric of our business, most notably record revenues, an 84% increase in non-GAAP income, and a 30% increase in lead volume. This performance reflected the significant expansion of our dealer footprint as well as improvement in the quality of our leads.

Strategically, we made great strides in 2014 with the successful acquisition and integration of AutoUSA, as well as the advancement of several new product offerings that continue to gain market traction. We are also beginning to experience meaningful contributions from our commercial relationship with AutoWeb, which is driving growth in our advertising business.

As announced over a month ago, we promoted Kim Boren to Chief Financial Officer to succeed Curt effective April 1, 2015.

Curt has served as an exceptional finance executive for Autobytel and was instrumental to our progress and growth over the last 7.5 years. We thank him for his service and appreciate his assistance during this transition and wish him all the best in his future endeavors.

As many of you know, Kim was a member of Autobytel's financial analysis and planning group from July 2007 to June 2009 and rejoined the Company in April 2010 as our Senior Director of Financial Planning and Analytics. After a series of promotions, Kim was most recently the Company's Senior Vice President of Business Analysis and Websites, a position she has held since February 2014.

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 3

Kim has the full confidence of the senior management and board of directors, and we all look forward to working with her in this new role.

Now I'd like to turn the call over to Curt as he introduces Kim on her well-deserved appointment. Curt?

|

Curt DeWalt:

|

Thanks, Jeff.

|

I’ve thoroughly enjoyed my 7 ½ years at Autobytel, 6 as CFO, and I'm appreciative of the opportunity to contribute to the Autobytel team in its turnaround. While entering the next chapter of my life, I'm happy to serve the Company in a consultative capacity to assist in its continued success. Nevertheless, with Kim and the financial team in place, I'm confident that I leave the Company in very capable hands.

Now I'd like to introduce Kim and have her take us through the important details of our financial results for the fourth quarter. Kim?

|

Kim Boren:

|

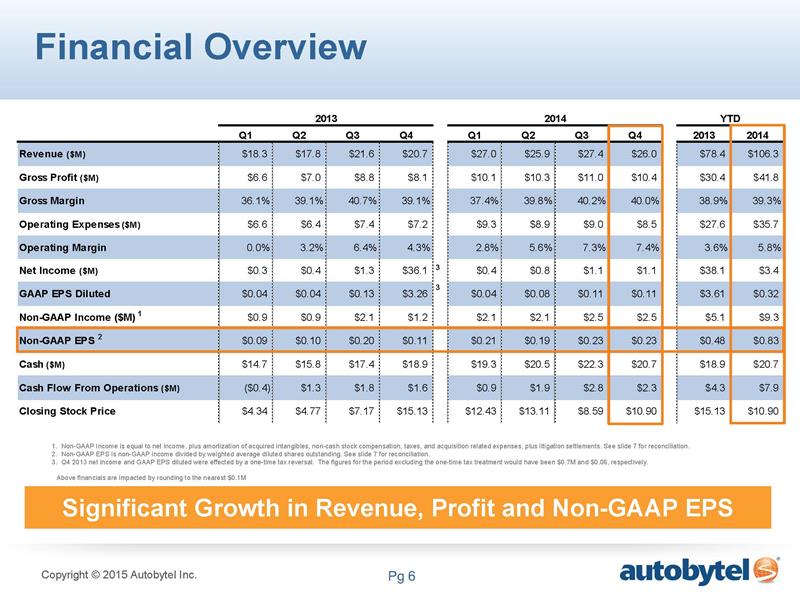

Thanks Curt, and good afternoon everyone. For those of you following along with our earnings presentation, on Slide 4 you can see our fourth quarter revenues increased 26% to $26.0 million compared to the prior year.

|

This was largely driven by 23% growth in automotive leads and services. The increase reflects the ongoing demand from automotive dealers, our retail channel, which rose 52% to $11.3 million. This channel continues to benefit from our AutoUSA acquisition, strong internally-generated lead supply and increases in our average selling price. Revenues from auto manufacturers, our wholesale channel, grew 3% to $11.5 million during the fourth quarter.

Advertising revenues were $1.6 million, up 50% on a sequential basis and 127% compared with last year, as we continue to optimize our relationship with Jumpstart and generated a higher volume of page views. Our increase in advertising revenue was also driven by growth in our commercial relationship with AutoWeb, which is beginning to meaningfully contribute to our results.

Page views more than doubled versus the fourth quarter of 2013. The reason for the increase is twofold. First, we generated an increase in traffic, a primary driver of which was Google's Panda release in May which was designed to help boost quality content sites like Autobytel.com. Second, page views per visit increased as a result of our continued optimization of content to provide users with a more engaging experience on our site, demonstrating the effectiveness of our ongoing content and video investments.

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 4

Moving now to Slide 5, you’ll see that we delivered approximately 1.6 million automotive leads during the fourth quarter, a 17% increase over last year. Retail new leads increased 43%, while used leads increased 87%. 67% of the leads were delivered to the wholesale channel with the remaining 33% to the retail channel.

We delivered nearly 92,000 specialty finance leads during the 2014 fourth quarter, up from 77,000 in the corresponding year-ago period, reflecting our continued efforts to ease supply constraints. Specialty finance lead revenue grew to $1.6 million for the fourth quarter, an increase of 14% from the same quarter last year.

On Slide 6, I'd like to point you to an approximate 29% improvement in gross profit, which grew to $10.4 million from the 2014 fourth quarter. Gross margin was 40.0%, a year-over-year improvement of 90 basis points.

The improvement continues to reflect the delivery of a higher percentage of internally-generated leads to former AutoUSA dealers and leveraged purchasing power from our outside suppliers for those dealers. It's also worth noting that our advertising revenue through Jumpstart currently flows through to our P&L at approximately 99% margins, while advertising revenue from our AutoWeb relationship flows through at 100% margins. As this segment of our business continues to grow, we anticipate seeing the incremental benefit contribute to our bottom line.

Total operating expenses were $8.5 million or 32.5% of total revenues, compared with $7.2 million, or 34.8%, for the same quarter last year. While the majority of the dollar increase is related to sales and marketing expenses associated with the acquisition of AutoUSA and activities in the SaleMove program, our 230 basis point improvement in operating margins reflects our internal operating efficiencies and prudent cost management of AutoUSA.

On a GAAP, basis net income was $1.1 million or $0.11 per diluted share compared to $36.1 million or $3.26 per diluted share from last year's fourth quarter.

As you may recall, net income in the fourth quarter of 2013 included a one-time benefit of $35.5 million, or approximately $3.20 per diluted share, for the release of a valuation allowance against our deferred tax assets. Excluding this benefit, year-over-year net income increased a healthy 69%.

Due to the valuation allowance release, we now have a higher effective tax rate provision for book purposes than we've had in the past. However, this increase will not impact cash due to the utilization of NOL tax credits.

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 5

We are including non-GAAP financial information to help investors better understand Autobytel's financial performance given this higher tax rate provision. As such, on Slide 7 you’ll see that non-GAAP income, which adds back amortization on acquired intangibles, non-cash stock-based compensation, acquisition costs, litigation settlements and income taxes, increased 107% to $2.5 million or $0.23 per diluted share.

Our cash and cash equivalents balance grew to $20.7 million at year end 2014, up from $18.9 million at the end of 2013. Cash provided by operations for the 2014 fourth quarter increased 43% to $2.3 million compared to $1.6 million in the prior year quarter. For 2014, cash flow from operations increased 82% to $7.9 million versus $4.3 million in 2013.

During the fourth quarter, we repurchased 164,028 shares at an average price of $10.85 per share under our stock repurchase plan. Approximately $1.2 million remains available for repurchase under our repurchase program. The timing and the actual number of repurchases of additional shares, if any, under our repurchase program is in the sole discretion of the Company and is dependent upon a variety of factors including regulatory compliance and corporate considerations. A significant factor that we consider in evaluating repurchases is the impact under our Tax Benefit Preservation Plan and on the use of our net operating loss carryovers and other tax attributes under Section 382 of the Internal Revenue Code.

Now, I'll turn the call back over to Jeff. Jeff?

|

Jeff Coats:

|

Thank you, Kim.

|

As I mentioned earlier, we are very pleased with our 2014 results, particularly our record revenue, 39% annual gross margin and 84% growth in non-GAAP income. As indicated on Slide 8, our total lead volume in 2014 improved to a record $6.6 million, up 30% from $5.1 million in 2013. Based on our IHS data, as you can see on Slide 10, we estimate that consumers submitting leads that we delivered to our customers accounted for over 4% of all light vehicle sales in the United States in 2014.

Referenced in Slide 11, our total active dealer count at December 31st was 4,154, up 15% from last year's fourth quarter, but down from 4,522 at the end of the third quarter as a result of AutoUSA's higher than average dealer churn, combined with the usual seasonal fourth quarter reduction in dealer marketing budgets. Our current dealer franchise footprint only represents 13% of the 31,609 franchises in the United States at the end of 2014, as reported by Urban Science, leaving a significant growth opportunity for our business.

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 6

As I've mentioned in past calls, our business plan expected the dealer churn from AutoUSA, along with a commensurate decline in retail revenue from AutoUSA dealers. By expanding our dealer retention staff and improving our retention processes, we are seeing positive results, and churn is continuing to stabilize. We expect churn to bottom out this year and to once again see growth in dealer count. With that said, retail new leads per dealer was up 22% year-over-year in the fourth quarter of 2014, and retail used leads per dealer was up 59% in the same period, illustrating our shift to focus on larger, more profitable dealer relationships as opposed to focusing purely on dealer count. This is reflective, in part, of the larger relationships we have retained with many of the 900 or so overlap dealers from the AutoUSA acquisition. In addition, we have successfully expanded AutoUSA's gross margin from 25% when we acquired it to 39% today, falling in line with our expectations and the rest of our business.

On Slide 12, you’ll note that for several of our OEM customers, we estimate that consumers submitting leads that we delivered to these OEMs and their dealers accounted for over 6% of their respective total retail sales in 2014.

You can also see that we experienced healthy organic growth last year as most of our existing OEM relationships significantly expanded their leads programs with us. Overall, OEMs increased their lead purchases by 30% from Autobytel in 2014, and in fact, after one major OEM reviewed its business rules it increased the monthly volume of leads purchased from Autobytel by over 300%.

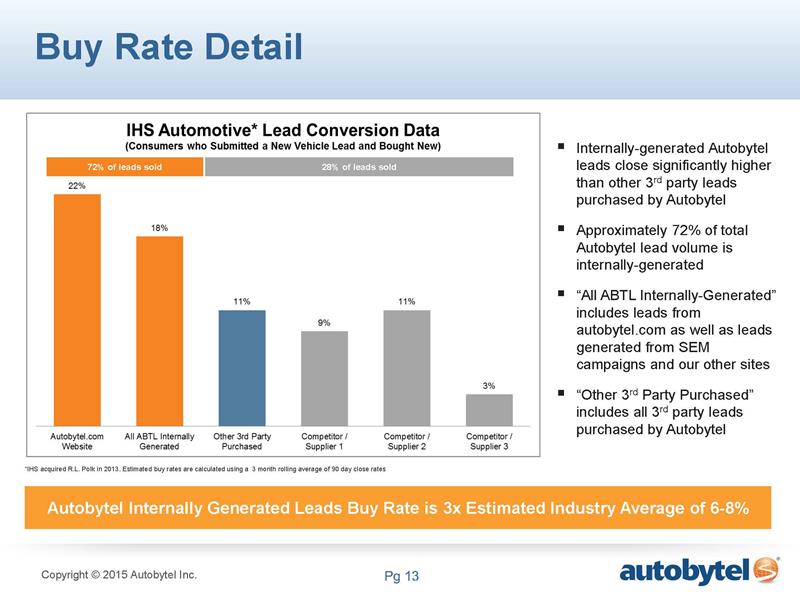

The ramp within our existing client base demonstrates that what we believe is the pent up demand for our high quality leads, especially as OEMs and dealers are becoming increasingly cognizant of the ROI they provide. This realization is largely due to our unique relationship with IHS Automotive, formerly R.L. Polk. As indicated on Slide 13, our estimated average buy rate for Autobytel internally-generated leads in the fourth quarter was 18%.

We believe this high buy rate from our new car leads is actually conservative. Not all sales can be matched given that many consumers buy outside the 90-day measurement window, buy a used car instead, or register a vehicle under a different name than the original lead submission. So the 18% buy rate may very well be higher.

Autobytel's high quality leads were the gold standard in the early years of the automotive internet, and we believe our leads are once again being acknowledged as the gold standard today.

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 7

I'd like to provide a little more color on our relationship with IHS and why it's so important to not just Autobytel but to all third party lead providers and customers.

We believe third party leads have been the standard in our industry for many years. However, from time to time, new products and services are introduced that take the focus away from third party lead generation as a profitable way to sell cars to in-market buyers. Dealers and OEMs may decide to temporarily pull back on their third party programs to test these new approaches.

However, it's important to note that dealers and OEMs acknowledge that a significant percentage of consumers will do research on third party sites like Autobytel, and accordingly, relationships with high quality lead sources typically are maintained. Anecdotally, we know that a significant number of dealers and OEMs tend to return to purchasing increased volumes of high quality leads after comparing the ROI they receive from other forms of marketing.

Until recently, credible validation of the value of third party leads was not possible because there was no established way to independently track this information. However, through our relationship with IHS we can now derive a buy rate for our leads through actual registration data from all 50 state DMVs. We can even let dealers know when they lose a customer to another competitor in the market. This information is not only pertinent to our services, but dealers can now gain a better understanding of the performance of their own sales teams.

While our core new car leads continue to drive growth, there is a significant opportunity to expand our used car leads business, which will be a major focal point for 2015. We believe it's much easier to finance a used car today than ever before, especially given current interest rates. Used car sales in the U.S. are also roughly two to three times that of new car sales, providing us with a large opportunity. It's worth noting that used car leads only represent about 15% of our total leads business today. We plan to tackle this vast opportunity similar to how we've grown our new car leads business by enhancing the technology of our used car lead generation activities, particularly through our SEM operations. This will allow us to generate an increasing volume of high quality used car leads at very attractive margins similar to our new car lead generation.

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 8

Another significant growth opportunity in 2015 is the advancement of our mobile offerings. On Slide 14, you'll see our various mobile products currently being offered. TextShield, the centerpiece of our mobile suite, continues to gain market traction. In March, we plan to launch our newest enhancement to our cutting edge TextShield product, which will enable dealers to receive mobile text messages from in-market consumers on their existing dealership landlines, a significant innovation. Needless to say, the consumer car shopping experience continues to evolve, and it's becoming all the more important for dealers to accommodate consumers through mobile and text based applications. We've already received strong initial interest from dealers regarding this new lead management system for text. We plan to continue to advance our mobile products and expect this part of our business to meaningfully contribute in 2015.

Another key focus of this year will be dealer facing marketing as well as education and training. As I noted earlier, both new and used car leads per dealer increased significantly year-over-year in Q4, which reinforces that the better we can educate our dealer customers, the better they will understand our true value proposition and the high return on investment we believe our high quality leads can provide, especially relative to our competitors, and typically increased. I'm sure many of you may be familiar with the version of the pay per sale model currently being pursued in the market by one of our competitors and the $299 cost to dealers per new car sold and $399 per car sold under this model. In addition to these high fees, this model gets between the dealer and the consumer on actual vehicle price, which also takes additional profit out of the dealers' pockets. We continue to hear anecdotally from many of our dealer customers that they maintain higher gross profit per sale from Autobytel leads than they do from this version of the pay per sale model. Our dealer marketing and education activities this year will be designed to highlight these differences and ensure our dealers understand the higher ROI they should achieve from Autobytel leads.

On Slide 15, you'll see how our pay per lead model compares with pay per sale. At our estimated average current buy rate of 18% for leads we deliver to our dealer customers, the hypothetical pay per sale in our model is about $120 assuming a $22 price per lead. Even at an 8% average dealer close rate, which is significantly less than our high quality leads, but more in line with other lead providers, the equivalent pay per sale is only $275. It's also worth noting that the cost of our used car leads is currently only about $1 to $2 more than our new car leads. This creates a significant margin opportunity for used car dealers given the lower pay per sale economics from our leads and the higher profit generally made on used cars compared to new cars.

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 9

We continue to be excited about our strategic investment in and commercial relationship with AutoWeb, a company whose platform enables specialized targeting to high intent online car shoppers while allowing advertisers to optimize their campaigns efficiently. The company's website, which is still in beta mode, allows shoppers to use search criteria, including preferred monthly payment, vehicle type, make, model and MSRP. Over the last twelve months, they've been averaging 1.5 million searches per month, a number that has been growing significantly and is expected to continue to grow.

Given this momentum, AutoWeb is now beginning to meaningfully contribute to our advertising results. AutoWeb has announced that it expects to generate more than $10 million in revenue this year from $0 in 2013, implying a very high growth rate. While our current ownership is approximately 16%, we also have an option through mid-September 2015 to purchase additional shares at the price of our initial investment, which would increase our ownership to approximately 22%.

In recent news, many of you may have noticed that we made a small strategic investment in a company called GoMoto, which is a provider of hardware and SaaS services that enables consumer to interact with car shopping kiosks, or hubs, inside of a dealership. These hubs allow car buyers to independently explore vehicles and promotions while at the dealership without having to engage with a salesperson if they're not quite yet ready. The large screen in-store displays powered by GoMoto turns up the volume on the iPad shopping experience that exists today. In addition to browsing inventory and building vehicles, consumers can value their trade-in, research sales and specials, and even look into financing and warranty information. When a consumer is ready or has incremental questions, they can then utilize a salesperson that is just footsteps away at their convenience. We will be providing GoMoto with access to our content and video libraries to further enhance this in-store experience. This investment is just another avenue for growth and an incremental step to enhance the overall car buying and selling experience by connecting dealers and consumers in real time as often as possible.

As you can see on Slide 16, both retail and total light vehicle sales are expected to be 14 million and 17 million, respectively, in 2015. The February retail seasonally adjusted annual run rate, or SAAR, is expected to be 13.5 million units, which is down 300 units from January 2015, but up 1.1 million units stronger than February 2014.

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 10

Although the bar chart on Slide 16 shows the deceleration in U.S. retail light vehicle sales, as I have stated before, we do consider our business somewhat insulated to market downturns, so if sales do slow in 2015 dealers would likely turn to the highest ROI activities available to sell more cars, which we believe includes Autobytel leads.

Now moving on to our outlook for 2015… we are constantly looking for more effective ways for our shareholders to think about the Company. The leads business can be characterized by seasonal and/or intermittent fluctuations that can occur not only on a quarterly basis but also monthly or even weekly. In order to smooth these often times episodic fluctuations we are moving forward with full year guidance. With that being said, we expect fiscal year 2015 revenue to range between $114 million and $120 million, representing an increase of approximately 7% to 13% from 2014. These conservative expectations take into consideration last week's J.D. Power LMC study, which as I just discussed, expects industry sales growth to decelerate to 3%, as well as December and January SAAR coming in below industry expectations. We also expect non-GAAP diluted EPS in the fiscal year 2015 to range between $0.97 and $1.16 as compared to $0.83 in 2014, representing an increase of approximately 17% to 40%. This healthy non-GAAP EPS growth is a function of some of the very high margin revenues from advertising, AutoWeb, as well as our other dealer products.

Using our annual outlook for 2015 as context, we encourage our investors to keep in mind that the first quarter of 2015 is the first quarter that we compare against the acquisition of AutoUSA. As most of you are aware by now, Q1 of 2014 (the first quarter of our ownership) reflected revenue that we expected to diminish due to higher than average dealer churn and intercompany eliminations, since we were already supplying leads to AutoUSA before the acquisition. Today, AutoUSA's current annual revenue run rate is approximately $16 million and contributing gross margin that continues to improve and stabilize falling closer in line with our core leads business. So we'd like our investors to be appropriately sensitive to these year-over-year revenue comparisons in Q1 and Q2. At the same time, we remain bullish about the full year.

Our primary focus for 2015, as always, is to provide value to all of our customers, which we believe will ultimately translate to enhanced value for our stockholders. Through the continued growth of our dealer footprint, high quality leads and value added products, we expect to carry our momentum through 2015 and capitalize on the evolving consumer and automotive marketplace.

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 11

At this time we'd like to open the call to questions.

|

Operator:

|

Thank you, sir.

|

Ladies and gentlemen on the phone lines, if you would like to ask a question, please press star and then one now. If your question has been answered, or you would like to remove yourself from the queue for any reason, you may press the pound key. Again, for a question, please press star and then one now.

And our first question will come from Eric Martinuzzi of Lake Street Capital. Your line is open. Please proceed.

|

Eric Martinuzzi:

|

Thanks for taking the questions. Congratulations on the new position Kim, and Curt I enjoyed working with you. The 2015 outlook here, I appreciate the full year color. That's helpful. I think that's what we were kind of expecting. I am kind of feeling around in the dark though, given the year-on-year compare with AutoUSA there.

|

I know the comps get a little bit easier in the back half of the year, but can you get more granular, even to the point of does the business grow Q1 2015 versus Q1 2014? Can you speak-- if you can't give us that level of insight, just some kind of seasonality, just because I know Q1's probably the toughest one for me to model.

|

Jeff Coats:

|

Q1 will be the toughest comparison, Eric, as we had a full quarter of the largest number of the AutoUSA dealers, some of which churned off during Q1 and then continued to churn off during Q2, as well as we had a full quarter--probably a full quarter and a half of the revenue from that OEM customer that ended up pulling back in Q2 that we've since recovered some from. So it'll be a pretty straightforward comparison.

|

There will not be a lot of growth in Q1. In fact it will be flat in Q1 to possibly down a little bit, but strong on the bottom line and good margins.

|

Eric Martinuzzi:

|

Okay. That's helpful. And then as I look to, I guess, AutoWeb, you've used the word meaningful in characterizing the success of that business and your participation in it. I know there's a difference between meaningful and material, at least from an accounting perspective. At the midpoint of what you've talked about for 2015, you hope to do $117 million.

|

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 12

In my mind, a material contribution would be somewhere around 10%. I don't know, maybe 5%, but when you talk about breaking that out later on in the year, what's your yardstick for breaking it out? Is it the 5% of revenue? Is it the 10% of revenue? Is it a gross profit percentage?

|

Jeff Coats:

|

It would probably be more at the 5% level. We would not expect to hit the 5% level in 2015 based on what we understand about their current growth plans. However, they're an early stage company. They could end up growing faster than expected, and if so, that would translate into additional revenue for us. We do expect to see some nice low 7-digit numbers coming from AutoWeb this year.

|

|

Eric Martinuzzi:

|

Okay. And the last question for me. What is the timing of the investment there? I think your option is $2.5 million. When do you pull the trigger on that investment given that you've got between now and September?

|

|

Jeff Coats:

|

We'll probably pull that trigger sometime in the summer, I would think, perhaps second quarter. There's no real rush in doing it. It is $2.5 million. It's the same valuation as our initial investment, and I think we have until September 18th to pull that trigger.

|

|

Eric Martinuzzi:

|

Okay. Congrats on the quarter.

|

|

Jeff Coats:

|

Thank you.

|

|

Operator:

|

Thank you. Our next question comes from the line of Sameet Sinha of B. Riley. Your line is open. Please proceed.

|

|

Austin Drake:

|

Good afternoon. This is Austin on for Sameet. Just a couple questions here. On the Q3 call you had indicated that one small OEM relationship could be ramping and could become a major source of growth. Can you update us on that? And then secondly, where do your NOLs stand at the end of the year? Thanks.

|

|

Jeff Coats:

|

I'll answer the OEM question. We have seen a significant increase with one of the major OEMs. It did begin ramping in Q4, and we are seeing continued nice growth as we roll into Q1. So we are seeing that. Curt, you want to answer the--.

|

|

Curt DeWalt:

|

On the NOLs, we have $94 million of federal NOLs and $59 million of state NOLs.

|

|

Austin Drake:

|

Okay. Thank you. Congrats on the quarter.

|

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 13

|

Jeff Coats:

|

Thank you.

|

|

Operator:

|

Thank you. Our next question comes from the line of Ed Woo of Ascendiant Capital. Your line is open. Please go ahead.

|

|

Ed Woo:

|

Yes, I’d also would like to send my congrats to Kim, and also Curt, wish you good luck in your new endeavors. I think it was a very good quarter. I just want to have a little bit more color on your relationship with AutoWeb. Do they--what exactly is your relationship, and also can you provide any comments on any changes in your valuation since you guys made your investment?

|

|

Jeff Coats:

|

We have not made any adjustments to the value of the investment. We did make an incremental investment in AutoWeb in the fourth quarter. It's detailed in the K that we just filed before we did the call today.

|

So, we did take essentially our pro rata piece in the round that they raised during the fourth quarter, which is how we've maintained our approximately 16% ownership level. And I'm sorry, what was the first part of your question, Ed?

|

Ed Woo:

|

Yes, so exactly – for AutoWeb, they are also a lead generation website as well. So how do you guys -- I guess I wanted to just get a little better understanding of how do you guys work with them, the lead generation?

|

|

Kim Boren:

|

Sure. So we worked very closely with them as they put their site up and enabled that lead generation, and to my knowledge, we are the primary beneficiary, if not the only beneficiary, of the lead flow coming off of their site. So it's a very close partnership from that perspective.

|

|

Curt DeWalt:

|

So there's both the lead revenue and advertising revenue.

|

|

Kim Boren:

|

Correct.

|

|

Ed Woo:

|

Okay. Thank you. That clears things up. And then the other question I had is we've seen low oil prices seem to be persisting -- well, maybe not in California recently, but generally low crude prices, low oil prices across the board. How has that impacted your forecast for auto sales in 2015?

|

|

Jeff Coats:

|

You know, Ed, we have expected to see the major analysts like J.D. Power increase their expectations for 2015. Their initial estimates, I think, were for something between 1% and 2% growth in 2015.

|

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 14

It was ultimately increased to 3%, but that's about half of the growth rate for 2014. I think it has a lot to do with coming up to the magic 17 million units sold per year, which is a combination of retail and fleet, that gets you the overall sales number.

I think also there's just some concern with regard to -- financing is fully available in the market today, but as many people will have noticed, the CFPB is going after the commercial banks that actually either provide automotive financing or buy automotive loans from dealers who make those loans, and there's just a lot of, I'd say, concern and kind of a lack of knowledge as to where all of that is ultimately going, especially since to my knowledge the CFPB in its charter is not supposed to be involved in auto financing.

So I think it's just a variety of things. I would say the drop in oil prices, one would have thought would have increased the sales numbers for 2015, but we've not seen that. What we have seen is an increase in large SUV sales and pickup truck sales pretty strongly in the fourth quarter and rolling into 2015, which of course are where a lot of the manufacturers and dealers make most of their profits because those are very high margin vehicles.

|

Ed Woo:

|

Great. Do you have any differentiations in terms of price per leads based on the model of the cars, or is it just an average price for cars?

|

|

Jeff Coats:

|

The way the leads industry has developed in the automotive sector is that it's pretty much a flat price per vehicle. It doesn't matter whether or not it's for a Mercedes 550 or a Volkswagen Beetle.

|

|

Ed Woo:

|

Great. Well, thanks for clarifying that also, and good luck.

|

|

Jeff Coats:

|

Thank you, Ed.

|

|

Operator:

|

Thank you.

|

And once again, ladies and gentlemen, if you would like to ask a question, please press star and then one.

Our next question comes from the line of Patrick Lin of Primarius Capital. Your line is open. Please go ahead.

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 15

|

Patrick Lin:

|

Hi there. I just wanted to echo the others and congrats on the quarter. Jeff and Cody, I think this is probably the best put together conference call that I've heard in a long, long time, so keep the good work going. And good luck to Curt, and congrats to Kim. My question is Jeff, you guys have done a great job over the last several years also investing and acquiring in either third party companies to bring in-house or partnering like AutoWeb., and I'm wondering if you have things in the pipeline to do more of these accretive deals, and also what does the pipeline look like for this type of activity? Thank you.

|

|

Jeff Coats:

|

Thank you, Patrick. Yes, we constantly have our eyes open. We are constantly looking for interesting opportunities, but probably even more favorable than that, given some of the investments we've made, particularly AutoWeb and doing AutoUSA last year and some of the other investments, we've developed a bit of a reputation as being a forward-looking technology player, and so we are fortunate that we get to see a lot of investment opportunities these days, which helps keep our technology on the cutting edge and our ability to look at some of the newest business models that are out there. So we are constantly looking for that as well as for just outright acquisitions.

|

As you know, I can't really comment on anything in detail, but we have found this a very good way to help us in terms of being able to help connect dealers and consumers more often with some of the investments we've made, so we do continue to look for those opportunities.

|

Patrick Lin:

|

Thank you. I was just curious in terms of the environment though, whether with the economy having improved the valuations out there and the number of opportunities out there, maybe just give a little color in terms of the trend.

|

|

Jeff Coats:

|

I'd say there's probably more opportunities. The valuations -- some of the -- it depends on kind of the part of the automotive industry somebody is looking at as to how high or not the valuations are. I would say we've been pretty fortunate so far because as a truly strategic investor who has a dealer-facing sales force and relationships with all of the manufacturers and essentially all of the major dealer groups, we can open a lot of doors. We can really help some of these companies promulgate their technology and/or increase their footprint, and so we're able to generally drive pretty good terms on our investments.

|

Autobytel Inc.

Moderator: Jeff Coats

02-26-15/5:00 p.m. ET

Confirmation # 82791859

Page 16

So, I think we'll probably continue to see valuations continue to rise. Certainly we see that across most markets these days, but we've got a little bit of a benefit in terms of our strategic nature, so it helps us to balance that and occasionally get better deals than we would have otherwise.

|

Patrick Lin:

|

Thank you very much, and as a final thought, I just wanted to say thanks for continuing to buy back shares and would encourage the board to continue to do the buyback once this is done.

|

|

Jeff Coats:

|

Thank you. Well, as we noted in the remarks, one of the considerations that we always have to take into account when looking at buying back shares at the corporate level are the impact it will have on pushing our shareholders that are close to 4.9% either to or beyond that threshold. If we inadvertently do that and push them to 5% we will unfortunately add negatively to our 382 calculations which could cause us to lose the ability to utilize large chunks of our NOLs. So we're very careful about that.

|

We have -- based on the way the calculations are done by one of the outside large accounting firms for us, we do see availability to do things periodically, and as that occurs, I'm sure the board will continue to take that into account as we look at the opportunity to buy more shares in the future.

|

Patrick Lin:

|

Perfect. Thank you.

|

|

Jeff Coats:

|

Thank you.

|

|

Operator:

|

Thank you, and this does conclude our Q and A session.

|

I’d now like to turn the call back over to Mr. Coats for closing remarks.

|

Jeff Coats:

|

Thank you. Thanks everybody for joining us today on the call.

|

I want to thank our really great team of employees scattered across the country for a great 2014 also. We look forward to speaking with all of our investors and analysts as we move forward during the months ahead.

Thank you very much. Goodbye.

|

Operator:

|

Ladies and gentlemen, thank you for your participation in today's conference. This does conclude the program, and you may all disconnect. Have a great rest of your day.

|

END