Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - PUBLIX SUPER MARKETS INC | Financial_Report.xls |

| EX-23 - EXHIBIT 23 - PUBLIX SUPER MARKETS INC | publix-fy14q4xex23.htm |

| EX-21 - EXHIBIT 21 - PUBLIX SUPER MARKETS INC | publix-fy14q4xex21.htm |

| EX-31.2 - EXHIBIT 31.2 - PUBLIX SUPER MARKETS INC | publix-fy14q4xex312.htm |

| EX-31.1 - EXHIBIT 31.1 - PUBLIX SUPER MARKETS INC | publix-fy14q4xex311.htm |

| EX-32.2 - EXHIBIT 32.2 - PUBLIX SUPER MARKETS INC | publix-fy14q4xex322.htm |

| EX-32.1 - EXHIBIT 32.1 - PUBLIX SUPER MARKETS INC | publix-fy14q4xex321.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 27, 2014

Commission File Number 0-00981

PUBLIX SUPER MARKETS, INC.

(Exact name of Registrant as specified in its charter)

Florida | 59-0324412 | |

(State of Incorporation) | (I.R.S. Employer Identification No.) | |

3300 Publix Corporate Parkway | ||

Lakeland, Florida | 33811 | |

(Address of principal executive offices) | (Zip code) | |

Registrant’s telephone number, including area code: (863) 688-1188

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Common Stock $1.00 Par Value

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes No X

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes No X

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months and (2) has been subject to such filing requirements for the past 90 days. Yes X No

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months.

Yes X No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. (X)

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | Accelerated filer | Non-accelerated filer X | Smaller reporting company | |||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes No X

The aggregate market value of the voting stock held by non-affiliates of the Registrant was approximately $12,701,577,000 as of June 27, 2014, the last trading day of the Registrant’s most recently completed second fiscal quarter.

The number of shares of the Registrant’s common stock outstanding as of February 3, 2015 was 773,305,000.

Documents Incorporated By Reference

The information required by Part III of this report, to the extent not set forth herein, is incorporated by reference from the Proxy Statement solicited for the 2015 Annual Meeting of Stockholders to be held on April 14, 2015.

TABLE OF CONTENTS

Page | |||

Item 1. | |||

Item 1A. | |||

Item 1B. | |||

Item 2. | |||

Item 3. | |||

Item 4. | |||

Item 5. | |||

Item 6. | |||

Item 7. | |||

Item 7A. | |||

Item 8. | |||

Item 9. | |||

Item 9A. | |||

Item 9B. | |||

Item 10. | |||

Item 11. | |||

Item 12. | |||

Item 13. | |||

Item 14. | |||

Item 15. | |||

PART I

Item 1. Business

Publix Super Markets, Inc. and its wholly owned subsidiaries (the Company) are in the primary business of operating retail food supermarkets in Florida, Georgia, Alabama, South Carolina, Tennessee and North Carolina. The Company was founded in 1930 and later merged into another corporation that was originally incorporated in 1921. The Company has no other significant lines of business or industry segments.

Merchandising and manufacturing

The Company sells grocery (including dairy, produce, deli, bakery, meat and seafood), health and beauty care, general merchandise, pharmacy, floral and other products and services. The percentage of consolidated sales by merchandise category for 2014, 2013 and 2012 was as follows:

2014 | 2013 | 2012 | |||||||

Grocery | 85 | % | 85 | % | 85 | % | |||

Other | 15 | % | 15 | % | 15 | % | |||

100 | % | 100 | % | 100 | % | ||||

The Company’s lines of merchandise include a variety of nationally advertised and private label brands as well as unbranded merchandise such as produce, meat and seafood. The Company receives the food and nonfood products it distributes from many sources. These products are delivered to the supermarkets through Company distribution centers or directly from the suppliers and are generally available in sufficient quantities to enable the Company to adequately satisfy its customers. Approximately 75% of the total cost of products purchased is delivered to the supermarkets through the Company’s distribution centers. The Company believes that its sources of supply of these products and raw materials used in manufacturing are adequate for its needs and that it is not dependent upon a single supplier or relatively few suppliers. Private label items are produced in the Company’s dairy, bakery and deli manufacturing facilities or are manufactured for the Company by suppliers.

The Company has experienced no significant changes in the kinds of products sold or in its methods of distribution since the beginning of the fiscal year.

Store operations

The Company operated 1,095 supermarkets at the end of 2014, compared with 1,079 at the beginning of the year. In 2014, 32 supermarkets were opened (including 14 replacement supermarkets) and 138 supermarkets were remodeled. Sixteen supermarkets were closed during the period. Replacement supermarkets opened in 2014 replaced 10 of the supermarkets closed during the same period, six of which were replaced on site, and four supermarkets closed in 2013 that were replaced on site. Four of the remaining supermarkets closed in 2014 will be replaced on site in subsequent periods and two supermarkets will not be replaced. New supermarkets added 0.9 million square feet in 2014, an increase of 1.7%. At the end of 2014, the Company had 760 supermarkets located in Florida, 182 in Georgia, 58 in Alabama, 51 in South Carolina, 38 in Tennessee and six in North Carolina. Also, as of year end, the Company had five supermarkets under construction in Florida, four in North Carolina and two in South Carolina.

Competition

The Company is engaged in the highly competitive retail food industry. The Company’s competitors include national and regional supermarket chains, independent supermarkets, supercenters, membership warehouse clubs, mass merchandisers, dollar stores, drug stores, specialty food stores, restaurants and convenience stores. The Company’s ability to attract and retain customers is based primarily on quality of goods and service, price, convenience, product mix and store location.

Working capital

The Company’s working capital at the end of 2014 consisted of $3,733.5 million in current assets and $2,697.8 million in current liabilities. Normal operating fluctuations in these balances can result in changes to cash flows from operating activities presented in the consolidated statements of cash flows that are not necessarily indicative of long-term operating trends. There are no unusual industry practices or requirements relating to working capital items.

Seasonality

The historical influx of winter residents to Florida and increased purchases of products during the traditional Thanksgiving, Christmas and Easter holidays typically result in seasonal sales increases between November and April of each year.

1

Employees

The Company had 175,000 employees at the end of 2014. The Company considers its employee relations to be good.

Intellectual property

The Company’s trademarks, trade names, copyrights and similar intellectual property are important to the success of the Company’s business. Numerous trademarks, including “Publix” and “Where Shopping is a Pleasure,” have been registered with the U.S. Patent and Trademark Office. Due to the importance of its intellectual property to its business, the Company actively defends and enforces its rights to such property.

Environmental matters

Compliance by the Company with federal, state and local environmental protection laws and regulations during 2014 had no material effect on capital expenditures, results of operations or the competitive position of the Company.

Company information

This Annual Report on Form 10-K and the 2015 Proxy Statement will be mailed on or about March 12, 2015 to stockholders of record as of the close of business on February 3, 2015. These reports as well as Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports may also be obtained electronically, free of charge, through the Company’s website at www.publix.com/stock.

Item 1A. Risk Factors

In addition to the other information contained in this Form 10-K, the following risk factors should be considered carefully in evaluating the Company’s business. The Company’s financial condition and results of operations could be materially adversely affected by any of these risks.

Increased competition and low profit margins could adversely affect the Company.

The retail food industry in which the Company operates is highly competitive with low profit margins. The Company’s competitors include national and regional supermarket chains, independent supermarkets, supercenters, membership warehouse clubs, mass merchandisers, dollar stores, drug stores, specialty food stores, restaurants and convenience stores. The Company’s ability to attract and retain customers is based primarily on quality of goods and service, price, convenience, product mix and store location. The Company believes it will face increased competition in the future from existing, and potentially new, competitors and its financial condition and results of operations could be impacted by the pricing, purchasing, advertising or promotional decisions made by its competitors as well as competitor format innovation and location additions.

General economic and other conditions that impact consumer spending could adversely affect the Company.

The Company’s results of operations are sensitive to changes in general economic conditions that impact consumer spending. Adverse economic conditions, including high unemployment, home foreclosures and weakness in the housing market, declines in the stock market and the instability of the credit markets, could cause a reduction in consumer spending. Other conditions that could also affect disposable consumer income include increases in tax, interest and inflation rates, increases in fuel and energy costs, increases in health care costs, the impact of natural disasters or acts of terrorism, and other factors. This reduction in the level of consumer spending could cause customers to purchase lower-margin items or to shift spending to lower-priced competitors, which could adversely affect the Company’s financial condition and results of operations.

Increased operating costs could adversely affect the Company.

The Company’s operations tend to be more labor intensive than some of its competitors due to the additional customer service offered in its supermarkets. Consequently, uncertain labor markets, government mandated increases in the minimum wage or other benefits, an increased proportion of full-time employees, increased costs of health care due to health insurance reform or other factors could result in an increase in labor costs. In addition, the inability to improve or manage operating costs, such as payroll, facilities or other non-product related costs, could adversely affect the Company’s financial condition and results of operations.

Failure to execute on the Company’s core strategies could adversely affect the Company.

The Company’s core strategies focus on customer service, product quality, shopping environment, competitive pricing and convenient locations. The Company has implemented several strategic business and technology initiatives as part of the execution of these core strategies. The Company believes these core strategies and related strategic initiatives differentiate it from its competition and present opportunities for sustained market share and financial growth. Failure to execute on these core strategies, or failure to execute the core strategies on a cost effective basis, could adversely affect the Company’s financial condition and results of operations.

2

Failure to identify and obtain or retain suitable supermarket sites could adversely affect the Company.

The Company’s ability to obtain sites for new supermarkets and, to a lesser extent, acquire existing supermarket locations is dependent on identifying and entering into lease or purchase agreements on commercially reasonable terms for properties that are suitable for its needs. If the Company fails to identify suitable sites and enter into lease or purchase agreements on a timely basis for any reason, including competition from other companies seeking similar sites, the Company’s growth could be adversely affected because it may be unable to open new supermarkets as anticipated. Similarly, its business could be adversely affected if it is unable to renew the leases on its supermarkets on commercially reasonable terms.

Failure to maintain the privacy and security of confidential customer and business information and the resulting unfavorable publicity could adversely affect the Company.

The Company receives, retains and transmits certain confidential information about its customers, employees and suppliers and entrusts that information to third party service providers. The Company depends upon the secure transmission of confidential information over external networks, including customer payments. Additionally, the use of individually identifiable data by the Company and its third party service providers is regulated at the national and local or state level. A compromise of the Company’s information technology systems or those of its third party service providers that results in customer, employee or supplier information being obtained by unauthorized persons could adversely affect the Company’s reputation with existing and potential customers, employees and others. A security breach could require expending significant additional resources related to remediation, lead to legal proceedings and regulatory actions, result in a disruption of operations and adversely affect the Company’s financial condition and results of operations.

Disruptions in information technology systems could adversely affect the Company.

The Company is dependent on complex information technology systems to operate its business, enhance customer service, improve the efficiency of its supply chain and increase employee efficiency. The Company’s information technology systems are subject to damage or interruption from power outages, computer and telecommunications failures, computer viruses, malicious service disruptions, catastrophic events and user errors. Any disruptions in information technology systems could have an adverse effect on the Company’s financial condition and results of operations.

Unexpected changes in the insurance market or factors affecting self-insurance reserve estimates could adversely affect the Company.

The Company uses a combination of insurance coverage and self-insurance to provide for potential liability for workers’ compensation, general liability, fleet liability, employee benefits and directors and officers liability. The Company is self-insured for property, plant and equipment losses. There is no assurance that the Company will be able to continue to maintain its insurance coverage or obtain comparable insurance coverage at a reasonable cost. Self-insurance reserves are determined based on actual claims experience and an estimate of claims incurred but not reported including, where necessary, actuarial studies. Actuarial projections of losses are subject to variability caused by, but not limited to, such factors as future interest and inflation rates, future economic conditions, litigation trends and benefit level changes. The Company’s financial condition and results of operations could be adversely affected by an increase in the frequency or costs of claims, changes in actuarial assumptions or catastrophic events involving property, plant and equipment losses.

Product liability claims, product recalls and the resulting unfavorable publicity could adversely affect the Company.

The packaging, marketing, distribution and sale of grocery, drug and other products purchased from suppliers or manufactured by the Company entails an inherent risk of product liability claims, product recall and the resulting adverse publicity. Such products may contain contaminants that may be inadvertently distributed by the Company. These contaminants may, in certain cases, result in illness, injury or death if processing at the consumer level, if applicable, does not eliminate the contaminants. Even an inadvertent shipment of adulterated products is a violation of law and may lead to a product recall and/or an increased risk of exposure to product liability claims. There can be no assurance that such claims will not be asserted against the Company or that the Company will not be obligated to perform product recalls in the future. If a product liability claim is successful, the Company’s insurance coverage may not be adequate to pay all liabilities and it may not be able to continue to maintain such insurance coverage or obtain comparable insurance coverage at a reasonable cost. If the Company does not have adequate insurance coverage or contractual indemnification available, product liability claims relating to defective products could have an adverse effect on the Company’s ability to successfully market its products and on the Company’s financial condition and results of operations. In addition, even if a product liability claim is not successful or is not fully pursued, the adverse publicity surrounding any assertion that the Company’s products caused illness or injury could have an adverse effect on the Company’s reputation with existing and potential customers and on the Company’s financial condition and results of operations.

Unfavorable changes in, failure to comply with or increased costs to comply with environmental laws and regulations could adversely affect the Company.

The Company is subject to federal, state and local laws and regulations that govern activities that may have adverse environmental effects and impose liabilities for the costs of contamination cleanup and damages arising from sites of past spills, disposals or other releases of hazardous materials. Under current environmental laws, the Company may be held responsible for the remediation

3

of environmental conditions regardless of whether the Company leases, subleases or owns the supermarkets or other facilities and regardless of whether such environmental conditions were created by the Company or a prior owner or tenant. The costs of investigation, remediation or removal of environmental conditions may be substantial. In addition, the increased focus on climate change, waste management and other environmental issues may result in new environmental laws or regulations that could negatively affect the Company directly or indirectly through increased costs on its suppliers. There can be no assurance that environmental conditions relating to prior, existing or future sites or other environmental changes will not adversely affect the Company’s financial condition and results of operations through, for instance, business interruption, cost of remediation or adverse publicity.

Unfavorable changes in, failure to comply with or increased costs to comply with laws and regulations could adversely affect the Company.

In addition to environmental laws and regulations, the Company is subject to federal, state and local laws and regulations relating to, among other things, product labeling and safety, zoning, land use, workplace safety, public health, accessibility and restrictions on the sale of various products, including alcoholic beverages, tobacco and drugs. The Company is also subject to laws governing its relationship with employees, including minimum wage requirements, overtime, labor, working conditions, disabled access and work permit requirements. Compliance with, or changes in, these laws, the passage of new laws and the inability to deal with increased government regulation could adversely affect the Company’s financial condition and results of operations.

Unfavorable results of legal proceedings could adversely affect the Company.

The Company is subject from time to time to various lawsuits, claims and charges arising in the normal course of business, including employment, personal injury, commercial and other matters. Some lawsuits also contain class action allegations. The Company estimates its exposure to these legal proceedings and establishes reserves for the estimated liabilities. Assessing and predicting the outcome of these matters involves substantial uncertainties. Although not currently anticipated by the Company, material differences in actual outcomes or changes in the Company’s evaluation could arise that could have a material adverse effect on the Company’s financial condition or results of operations.

Item 1B. Unresolved Staff Comments

None

Item 2. Properties

At year end, the Company operated 51.2 million square feet of supermarket space. The Company’s supermarkets vary in size. Current supermarket prototypes range from 28,000 to 61,000 square feet. Supermarkets are often located in strip shopping centers where the Company is the anchor tenant. The majority of the Company’s supermarkets are leased. Substantially all of these leases will expire during the next 20 years. However, in the normal course of business, it is expected that the leases will be renewed or replaced by new leases. Both the building and land are owned at 196 locations. The building is owned while the land is leased at 55 other locations.

The Company supplies its supermarkets from eight primary distribution centers located in Lakeland, Miami, Jacksonville, Sarasota, Orlando, Deerfield Beach and Boynton Beach, Florida and Lawrenceville, Georgia. The Company operates six manufacturing facilities, including three dairy plants located in Lakeland and Deerfield Beach, Florida and Lawrenceville, Georgia, two bakery plants located in Lakeland, Florida and Atlanta, Georgia and a deli plant located in Lakeland, Florida.

The Company’s corporate offices, primary distribution centers and manufacturing facilities are owned with no outstanding debt. The Company’s properties are well maintained, in good operating condition and suitable and adequate for operating its business.

Item 3. Legal Proceedings

The Company is subject from time to time to various lawsuits, claims and charges arising in the normal course of business. The Company believes its recorded reserves are adequate in light of the probable and estimable liabilities. The estimated amount of reasonably possible losses for lawsuits, claims and charges, individually and in the aggregate, is considered to be immaterial. In the opinion of management, the ultimate resolution of these legal proceedings will not have a material adverse effect on the Company’s financial condition, results of operations or cash flows.

Item 4. Mine Safety Disclosures

Not applicable

4

Name | Age | Business Experience During Last Five Years | Served as Officer of Company Since | |||

Executive Officers of the Company | ||||||

John A. Attaway, Jr. | 56 | Senior Vice President, General Counsel and Secretary of the Company. | 2000 | |||

Hoyt R. Barnett | 71 | Vice Chairman of the Company and Trustee of the Employee Stock Ownership Plan. | 1977 | |||

David E. Bornmann | 57 | Vice President of the Company to March 2013, Senior Vice President thereafter. | 1998 | |||

William E. Crenshaw | 64 | Chief Executive Officer of the Company. | 1990 | |||

Laurie Z. Douglas | 51 | Senior Vice President and Chief Information Officer of the Company. | 2006 | |||

John T. Hrabusa | 59 | Senior Vice President of the Company. | 2004 | |||

Randall T. Jones, Sr. | 52 | President of the Company. | 2003 | |||

David P. Phillips | 55 | Chief Financial Officer and Treasurer of the Company. | 1990 | |||

Michael R. Smith | 55 | Vice President of the Company to March 2013, Senior Vice President thereafter. | 2005 | |||

Officers of the Company | ||||||

David E. Bridges | 65 | Vice President of the Company. | 2000 | |||

Scott E. Brubaker | 56 | Vice President of the Company. | 2005 | |||

Jeffrey G. Chamberlain | 58 | Director of Real Estate Strategy of the Company to January 2011, Vice President thereafter. | 2011 | |||

Joseph DiBenedetto, Jr. | 55 | Regional Director of Retail Operations of the Company to January 2011, Vice President thereafter. | 2011 | |||

G. Gino DiGrazia | 52 | Vice President of the Company. | 2002 | |||

David S. Duncan | 61 | Vice President of the Company. | 1999 | |||

Sandra J. Estep | 55 | Vice President of the Company. | 2002 | |||

Linda S. Hall | 55 | Vice President of the Company. | 2002 | |||

Mark R. Irby | 59 | Vice President of the Company. | 1989 | |||

Linda S. Kane | 49 | Vice President and Assistant Secretary of the Company. | 2000 | |||

Erik J. Katenkamp | 43 | Director of Information Systems of the Company to January 2013, Vice President thereafter. | 2013 | |||

L. Renee Kelly | 53 | Director of Information Systems of the Company to January 2013, Vice President thereafter. | 2013 | |||

Thomas M. McLaughlin | 64 | Vice President of the Company. | 1994 | |||

Peter M. Mowitt | 55 | Business Development Director of Grocery Retail Support of the Company to March 2013, Vice President thereafter. | 2013 | |||

Kevin S. Murphy | 44 | Regional Director of Retail Operations of the Company to March 2014, Vice President thereafter. | 2014 | |||

Dale S. Myers | 62 | Vice President of the Company. | 2001 | |||

Alfred J. Ottolino | 49 | Vice President of the Company. | 2004 | |||

Charles B. Roskovich, Jr. | 53 | Vice President of the Company to January 2011, Senior Vice President to January 2013, Vice President thereafter. | 2008 | |||

Marc H. Salm | 54 | Vice President of the Company. | 2008 | |||

Alison Midili Smith | 44 | Director of Human Resources of the Company to January 2013, Vice President thereafter. | 2013 | |||

Jeffrey D. Stephens | 59 | Director of Fresh Product Manufacturing of the Company to September 2010, Director of Manufacturing Operations to March 2013, Vice President thereafter. | 2013 | |||

Casey D. Suarez, Sr. | 55 | District Manager of the Company to October 2010, Director of Warehousing to May 2014, Vice President thereafter. | 2014 | |||

Steven B. Wellslager | 48 | Director of Information Systems of the Company to January 2013, Vice President thereafter. | 2013 | |||

The terms of all officers expire in May 2015 or upon the election of their successors.

5

PART II

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity

Securities

(a) | Market Information |

The Company’s common stock is not traded on an established securities market. Therefore, substantially all transactions of the Company’s common stock have been among the Company, its employees, former employees, their families and the benefit plans established for the Company’s employees. The Company’s common stock is made available for sale only to the Company’s current employees and members of the Company’s Board of Directors through the Company’s Employee Stock Purchase Plan (ESPP) and Non-Employee Directors Stock Purchase Plan (Directors Plan) and to participants of the Company’s 401(k) Plan. In addition, common stock is provided to employees through the Employee Stock Ownership Plan (ESOP). The Company currently repurchases common stock subject to certain terms and conditions. The ESPP, Directors Plan, 401(k) Plan and ESOP each contain provisions prohibiting any transfer for value without the owner first offering the common stock to the Company. The Company serves as the registrar and stock transfer agent for its common stock.

Because there is no trading of the Company’s common stock on an established securities market, the market price of the Company’s common stock is determined by its Board of Directors. As part of the process to determine the stock value, an independent valuation is obtained. The process includes comparing the Company’s financial results to those of comparable companies that are publicly traded (comparable publicly traded companies). The purpose of the process is to determine a value for the Company’s common stock that is comparable to the stock value of comparable publicly traded companies by considering both the results of the stock market and the relative financial results of comparable publicly traded companies. The market prices for the Company’s common stock for 2014 and 2013 were as follows:

2014 | 2013 | ||||||

January - February | $ | 30.00 | 22.50 | ||||

March - April | 30.15 | 23.20 | |||||

May - July | 32.50 | 26.90 | |||||

August - October | 33.85 | 27.55 | |||||

November - December | 33.80 | 30.00 | |||||

(b) | Approximate Number of Equity Security Holders |

As of February 3, 2015, the approximate number of holders of the Company’s common stock was 166,000.

(c) | Dividends |

On June 2, 2014 and December 1, 2014, the Company paid semiannual dividends on its common stock of $0.37 per share totaling $577.2 million for the year to stockholders of record as of the close of business April 30, 2014 and October 31, 2014, respectively. On June 3, 2013 and December 2, 2013, the Company paid semiannual dividends on its common stock of $0.35 per share or $547.3 million for the year. Payment of dividends is within the discretion of the Company’s Board of Directors and depends on, among other factors, net earnings, capital requirements and the financial condition of the Company. It is believed that comparable dividends will be paid in the future.

6

(d) | Purchases of Equity Securities by the Issuer |

Issuer Purchases of Equity Securities

Shares of common stock repurchased by the Company during the three months ended December 27, 2014 were as follows (amounts are in thousands, except per share amounts):

Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs (1) | Approximate Dollar Value of Shares That May Yet Be Purchased Under the Plans or Programs (1) | ||||||||||||

September 28, 2014 through November 1, 2014 | 362 | $ | 33.85 | N/A | N/A | |||||||||||

November 2, 2014 through November 29, 2014 | 2,392 | 33.80 | N/A | N/A | ||||||||||||

November 30, 2014 through December 27, 2014 | 1,274 | 33.80 | N/A | N/A | ||||||||||||

Total | 4,028 | $ | 33.80 | N/A | N/A | |||||||||||

____________________________

(1) | Common stock is made available for sale only to the Company’s current employees and members of the Company’s Board of Directors through the Company’s ESPP and Directors Plan and to participants of the Company’s 401(k) Plan. In addition, common stock is provided to employees through the ESOP. The Company currently repurchases common stock subject to certain terms and conditions. The ESPP, Directors Plan, 401(k) Plan and ESOP each contain provisions prohibiting any transfer for value without the owner first offering the common stock to the Company. |

The Company’s common stock is not traded on an established securities market. The amount of common stock offered to the Company for repurchase is not within the control of the Company, but is at the discretion of the stockholders. The Company does not believe that these repurchases of its common stock are within the scope of a publicly announced plan or program (although the terms of the plans discussed above have been communicated to the participants). Thus, the Company does not believe that it has made any repurchases during the three months ended December 27, 2014 required to be disclosed in the last two columns of the table.

7

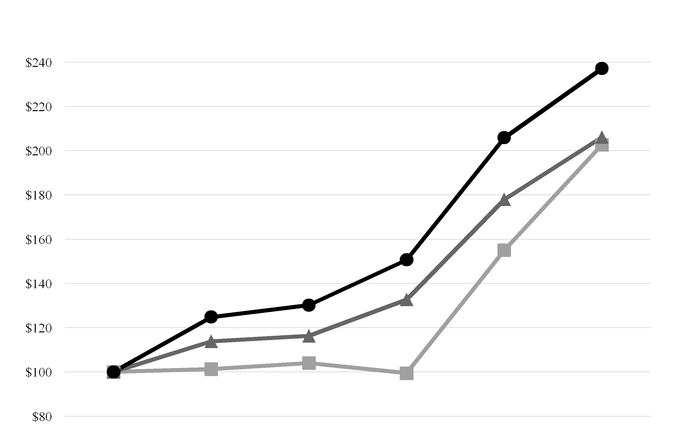

(e) | Performance Graph |

The following performance graph sets forth the Company’s cumulative total stockholder return during the five years ended December 27, 2014, compared to the cumulative total return on the S&P 500 Index and a custom Peer Group Index including retail food supermarket companies.(1) The Peer Group Index is weighted based on the various companies’ market capitalization. The comparison assumes $100 was invested at the end of 2009 in the Company’s common stock and in each of the related indices and assumes reinvestment of dividends.

The Company’s common stock is valued as of the end of each fiscal quarter. After the end of a quarter, however, shares continue to be traded at the prior valuation until the new valuation is received. The cumulative total return for the companies represented in the S&P 500 Index and the custom Peer Group Index is based on those companies’ calendar year end trading price. The following performance graph is based on the Company’s trading price at fiscal year end based on its market price as of the prior fiscal quarter. Due to the timing of the filing of this document with the Securities and Exchange Commission (SEC), a performance graph based on the fiscal year end valuation (market price as of March 1, 2015) is not presented below. Rather, for comparative purposes, a performance graph based on the fiscal year end valuation is provided in the 2015 Proxy Statement.

Comparison of Five-Year Cumulative Return Based Upon Year End Trading Price

2009 | 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||

l | Publix | $100.00 | 124.81 | 130.12 | 150.63 | 205.80 | 237.04 | ||||||||

p | S&P 500 | 100.00 | 113.82 | 116.31 | 132.68 | 177.94 | 206.01 | ||||||||

n | Peer Group (1) | 100.00 | 101.29 | 104.03 | 99.46 | 155.04 | 202.64 | ||||||||

___________________________

(1)Companies included in the Peer Group are Ahold, Delhaize Group, Kroger, Safeway, Supervalu and Weis Markets.

8

Item 6. Selected Financial Data

2014 | 2013 | 2012 | 2011(1) | 2010 | ||||||||||||||||||||||||||

(Amounts are in thousands, except per share amounts and number of supermarkets) | ||||||||||||||||||||||||||||||

Sales: | ||||||||||||||||||||||||||||||

Sales | $ | 30,559,505 | 28,917,439 | 27,484,766 | 26,967,389 | 25,134,054 | ||||||||||||||||||||||||

Percent change | 5.7 | % | 5.2 | % | 1.9 | % | 7.3 | % | 3.3 | % | ||||||||||||||||||||

Comparable store sales percent change | 5.4 | % | 3.6 | % | 2.2 | % | 4.1 | % | 2.3 | % | ||||||||||||||||||||

Earnings: | ||||||||||||||||||||||||||||||

Gross profit (2) | $ | 8,326,855 | 7,980,120 | 7,573,782 | 7,447,019 | 7,022,611 | ||||||||||||||||||||||||

Earnings before income tax expense | $ | 2,570,121 | 2,465,689 | 2,302,594 | 2,261,773 | 2,039,418 | ||||||||||||||||||||||||

Net earnings | $ | 1,735,308 | 1,653,954 | 1,552,255 | 1,491,966 | 1,338,147 | ||||||||||||||||||||||||

Net earnings as a percent of sales | 5.7 | % | 5.7 | % | 5.6 | % | 5.5 | % | 5.3 | % | ||||||||||||||||||||

Common stock: | ||||||||||||||||||||||||||||||

Weighted average shares outstanding | 778,708 | 780,188 | 782,553 | 784,815 | 786,378 | |||||||||||||||||||||||||

Basic and diluted earnings per share | $ | 2.23 | 2.12 | 1.98 | 1.90 | 1.70 | ||||||||||||||||||||||||

Dividends per share | $ | 0.74 | 0.70 | 0.89 (3) | 0.53 | 0.46 | ||||||||||||||||||||||||

Financial data: | ||||||||||||||||||||||||||||||

Capital expenditures | $ | 1,374,124 | 668,485 | 697,112 | 602,952 | 468,530 | ||||||||||||||||||||||||

Working capital | $ | 1,035,758 | 881,222 | 928,138 | 752,464 | 771,918 | ||||||||||||||||||||||||

Current ratio | 1.38 | 1.37 | 1.42 | 1.37 | 1.37 | |||||||||||||||||||||||||

Total assets | $ | 15,083,480 | 13,546,641 | 12,278,320 | 11,268,232 | 10,159,087 | ||||||||||||||||||||||||

Long-term debt (including current portion) | $ | 217,638 | 162,154 | 158,472 | 134,584 | 149,361 | ||||||||||||||||||||||||

Common stock related to ESOP | $ | 2,680,528 | 2,322,903 | 2,272,963 | 2,137,217 | 2,016,696 | ||||||||||||||||||||||||

Total equity | $ | 11,345,223 | 10,267,796 | 9,128,818 | 8,341,457 | 7,305,592 | ||||||||||||||||||||||||

Supermarkets | 1,095 | 1,079 | 1,069 | 1,046 | 1,034 | |||||||||||||||||||||||||

____________________________

(1) | Fiscal year 2011 includes 53 weeks. All other years include 52 weeks. |

(2) | Gross profit represents sales less cost of merchandise sold as reported in the consolidated statements of earnings. |

(3) | The Company paid dividends on its common stock of $0.89 per share in 2012, which included an annual dividend of $0.59 per share paid in June 2012 and a semiannual dividend of $0.30 per share paid in December 2012. |

9

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Overview

The Company is primarily engaged in the retail food industry, operating supermarkets in Florida, Georgia, Alabama, South Carolina, Tennessee and North Carolina. The Company has no other significant lines of business or industry segments. As of December 27, 2014, the Company operated 1,095 supermarkets including 760 located in Florida, 182 in Georgia, 58 in Alabama, 51 in South Carolina, 38 in Tennessee and six in North Carolina. In 2014, 32 supermarkets were opened (including 14 replacement supermarkets) and 138 supermarkets were remodeled. Sixteen supermarkets were closed during the period. During 2014, the Company opened 16 supermarkets in Florida, six in North Carolina, four in South Carolina, three in Alabama, two in Tennessee and one in Georgia. Replacement supermarkets opened in 2014 replaced 10 of the supermarkets closed during the same period. Four of the remaining supermarkets closed in 2014 will be replaced on site in subsequent periods and two supermarkets will not be replaced.

The Company’s revenues are earned and cash is generated as merchandise is sold to customers. Income is earned by selling merchandise at price levels that produce sales revenues in excess of the cost of merchandise sold and operating and administrative expenses. The Company has generally been able to increase revenues and net earnings from year to year. Further, the Company has been able to meet its cash requirements from internally generated funds without the need to generate cash through debt financing. The Company’s year end cash balances are impacted by capital expenditures, investment transactions, stock repurchases and dividend payments.

The Company sells a variety of merchandise to generate revenues. This merchandise includes grocery (including dairy, produce, deli, bakery, meat and seafood), health and beauty care, general merchandise and other products and services. Most of the Company’s supermarkets also have pharmacy and floral departments. Merchandise includes a mix of nationally advertised and private label brands as well as unbranded merchandise such as produce, meat and seafood. The Company’s private label brands play an important role in its merchandising strategy.

Operating Environment

The Company is engaged in the highly competitive retail food industry. The Company’s competitors include traditional supermarkets, such as national and regional supermarket chains and independent supermarkets, as well as nontraditional competitors, such as supercenters, membership warehouse clubs, mass merchandisers, dollar stores, drug stores, specialty food stores, restaurants and convenience stores. The Company’s ability to attract and retain customers is based primarily on quality of goods and service, price, convenience, product mix and store location. In addition, the Company competes with other companies for additional retail site locations. The Company also competes with retailers as well as other labor market competitors in attracting and retaining quality employees. As a result of the highly competitive environment, traditional supermarkets, including the Company, face business challenges. There has been a trend in recent years for traditional supermarkets to lose market share to nontraditional competitors. The success of the Company, in particular its ability to retain its customers, depends on its ability to meet the business challenges created by this highly competitive environment.

In order to meet the competitive challenges facing the Company, management continues to focus on the Company’s core strategies, including customer service, product quality, shopping environment, competitive pricing and convenient locations. The Company has implemented several strategic business and technology initiatives as part of the execution of these core strategies. The Company believes these core strategies and related strategic initiatives differentiate it from its competition and present opportunities for sustained market share and financial growth.

Results of Operations

The Company’s fiscal year ends on the last Saturday in December. Fiscal years 2014, 2013 and 2012 include 52 weeks.

Sales

Sales for 2014 were $30.6 billion as compared with $28.9 billion in 2013, an increase of $1,642.1 million or 5.7%. The increase in sales for 2014 as compared to 2013 was primarily due to a 5.4% increase in comparable store sales (supermarkets open for the same weeks in both periods, including replacement supermarkets). Sales for supermarkets that are replaced on site are classified as new supermarket sales since the replacement period for the supermarket is generally 9 to 12 months. Comparable store sales for 2014 increased primarily due to product cost inflation and increased customer counts resulting from a better economic climate.

Sales for 2013 were $28.9 billion as compared with $27.5 billion in 2012, an increase of $1,432.7 million or 5.2%. The increase in sales for 2013 as compared to 2012 was primarily due to a 3.6% increase in comparable store sales. Comparable store sales for 2013 increased primarily due to product cost inflation and increased customer counts resulting from a better economic climate.

10

Sales for 2012 were $27.5 billion as compared with $27.0 billion in 2011, an increase of $517.4 million or 1.9%. After excluding sales of $485.2 million for the extra week in 2011, the Company estimates that its sales increased $1,002.6 million or 3.8%. This increase is primarily due to a 2.2% increase in comparable store sales. Comparable store sales for 2012 increased primarily due to product cost inflation and increased customer counts resulting from a better, but still difficult, economic climate.

Gross profit

Gross profit (sales less cost of merchandise sold) as a percentage of sales was 27.2%, 27.6% and 27.6% in 2014, 2013 and 2012, respectively. Excluding the last-in, first-out (LIFO) reserve effect of $30.7 million, $14.8 million and $28.4 million in 2014, 2013 and 2012, respectively, gross profit as a percentage of sales would have been 27.3%, 27.6% and 27.7% in 2014, 2013 and 2012, respectively. After excluding the LIFO reserve effect, the decrease in gross profit as a percentage of sales for 2014 as compared with 2013 and for 2013 as compared with 2012 was primarily due to increases in promotional activity and product cost increases, some of which were not passed on to customers.

Operating and administrative expenses

Operating and administrative expenses as a percentage of sales were 20.2%, 20.4% and 20.5% in 2014, 2013 and 2012, respectively. The decrease in operating and administrative expenses as a percentage of sales for 2014 as compared with 2013 was primarily due to the adoption of the Accounting Standards Update (ASU) discussed in Recently Issued Accounting Standards below and decreases in rent as a percentage of sales due to the acquisition of shopping centers with the Company as the anchor tenant. The decrease in operating and administrative expenses as a percentage of sales for 2013 as compared with 2012 was primarily due to decreases in rent and utilities as a percentage of sales.

Investment income

Investment income was $143.9 million, $127.3 million and $88.4 million in 2014, 2013 and 2012, respectively. The increase in investment income for 2014 as compared with 2013 was primarily due to an increase in dividend income and realized gains on the sale of equity securities. The increase in investment income for 2013 as compared with 2012 was primarily due to an increase in realized gains on the sale of equity securities.

Income tax expense

The effective income tax rate was 32.5%, 32.9% and 32.6% in 2014, 2013 and 2012, respectively. The decrease in the effective income tax rate for 2014 as compared with 2013 was primarily due to an increase in qualified inventory donations and investment related tax credits partially offset by an increase in income tax expense due to the adoption of the ASU discussed in Recently Issued Accounting Standards below. The increase in the effective income tax rate for 2013 as compared with 2012 was primarily due to a decrease in dividends paid to ESOP participants due to the payment of the first semiannual dividend in 2012, as noted in Dividends below, partially offset by an increase in tax exempt investment income and investment related tax credits.

Net earnings

Net earnings were $1,735.3 million or $2.23 per share, $1,654.0 million or $2.12 per share and $1,552.3 million or $1.98 per share for 2014, 2013 and 2012, respectively. Net earnings as a percentage of sales were 5.7%, 5.7% and 5.6% for 2014, 2013 and 2012, respectively. Net earnings as a percentage of sales for 2014 as compared with 2013 remained unchanged. The increase in net earnings as a percentage of sales for 2013 as compared with 2012 was primarily due to the decrease in operating and administrative expenses, as noted above.

11

Liquidity and Capital Resources

Cash and cash equivalents, short-term investments and long-term investments totaled $6,638.2 million as of December 27, 2014, as compared with $6,293.4 million as of December 28, 2013. This increase is primarily due to the Company generating cash in excess of the amount needed for current operations.

Net cash provided by operating activities

Net cash provided by operating activities was $2,777.2 million for 2014, as compared with $2,567.3 million and $2,604.2 million for 2013 and 2012, respectively. The increase in net cash provided by operating activities for 2014 as compared with 2013 was primarily due to the increase in net earnings and the timing of payments for merchandise, partially offset by the timing of payments for income taxes. Net cash provided by operating activities for 2013 as compared with 2012 remained relatively unchanged. Any net cash in excess of the amount needed for current operations is invested in short-term and long-term investments.

Net cash used in investing activities

Net cash used in investing activities was $1,641.7 million for 2014, as compared with $1,721.5 million and $1,563.6 million for 2013 and 2012, respectively. The primary use of net cash in investing activities for 2014 was funding capital expenditures and net increases in investment securities. Capital expenditures for 2014 totaled $1,374.1 million. These expenditures were incurred in connection with the opening of 32 new supermarkets (including 14 replacement supermarkets) and remodeling 138 supermarkets. Expenditures were also incurred for new supermarkets and remodels in progress, the construction of new warehouses, new or enhanced information technology hardware and applications and the acquisition of shopping centers with the Company as the anchor tenant. In 2014, the payment for investments, net of the proceeds from the sale and maturity of such investments, was $307.8 million.

The primary use of net cash in investing activities for 2013 was funding capital expenditures and net increases in investment securities. Capital expenditures for 2013 totaled $668.5 million. These expenditures were incurred in connection with the opening of 22 new supermarkets (including seven replacement supermarkets) and remodeling 109 supermarkets. Expenditures were also incurred for new supermarkets and remodels in progress, the construction of new warehouses, new or enhanced information technology hardware and applications and the acquisition of shopping centers with the Company as the anchor tenant. In 2013, the payment for investments, net of the proceeds from the sale and maturity of such investments, was $1,074.4 million.

The primary use of net cash in investing activities for 2012 was funding capital expenditures and net increases in investment securities. Capital expenditures for 2012 totaled $697.1 million. These expenditures were incurred in connection with the opening of 31 new supermarkets (including 12 replacement supermarkets) and remodeling 113 supermarkets. Expenditures were also incurred for the expansion of warehouses, new or enhanced information technology hardware and applications and the acquisition of shopping centers with the Company as the anchor tenant. In 2012, the payment for investments, net of the proceeds from the sale and maturity of such investments, was $871.9 million.

Capital expenditure projection

Capital expenditures expected to use cash in 2015 are approximately $1,300 million, primarily consisting of new supermarkets, remodeling existing supermarkets, new or enhanced information technology hardware and applications and the acquisition of shopping centers with the Company as the anchor tenant. The shopping center acquisitions are financed with internally generated funds and assumed debt, if prepayment penalties for the debt are determined to be significant. This capital program is subject to continuing change and review. In the normal course of operations, the Company replaces supermarkets and closes supermarkets that are not meeting performance expectations. The impact of future supermarket closings is not expected to be material.

12

Net cash used in financing activities

Net cash used in financing activities was $1,029.9 million in 2014, as compared with $881.3 million and $1,070.1 million in 2013 and 2012, respectively. The increase in net cash used in financing activities for 2014 as compared with 2013 was primarily due to an increase in net common stock repurchases. Net common stock repurchases totaled $404.2 million in 2014, as compared with $321.3 million in 2013. The decrease in net cash used in financing activities for 2013 as compared with 2012 was primarily due to the Company paying dividends of $0.70 per share or $547.3 million in 2013 as compared with dividends of $0.89 per share or $698.7 million in 2012, as noted in Dividends below. Net common stock repurchases totaled $321.3 million in 2013, as compared with $354.4 million in 2012. The Company currently repurchases common stock at the stockholders’ request in accordance with the terms of the Company’s ESPP, Directors Plan, 401(k) Plan and ESOP. The amount of common stock offered to the Company for repurchase is not within the control of the Company, but is at the discretion of the stockholders. The Company expects to continue to repurchase its common stock, as offered by its stockholders from time to time, at its then current value for amounts similar to those in prior years. However, with the exception of certain shares distributed from the ESOP, such purchases are not required and the Company retains the right to discontinue them at any time.

Dividends

The Company paid dividends on its common stock of $0.74 per share or $577.2 million, $0.70 per share or $547.3 million and $0.89 per share or $698.7 million in 2014, 2013 and 2012, respectively. Due to the growth of the Company’s dividend over the last several years, the Company decided in 2012 to begin paying a semiannual dividend rather than an annual dividend. To not delay any dividend payments to the Company’s stockholders, the first semiannual dividend of $0.30 per share or $234.1 million was paid on December 3, 2012. As a result, dividends paid in 2014 and 2013 were less than in 2012.

Cash requirements

In 2015, the cash requirements for current operations, capital expenditures, common stock repurchases and dividend payments are expected to be financed by internally generated funds or liquid assets. Based on the Company’s financial position, it is expected that short-term and long-term borrowings would be available to support the Company’s liquidity requirements, if needed.

13

Contractual Obligations

Following is a summary of contractual obligations as of December 27, 2014:

Payments Due by Period | ||||||||||||||||

Total | 2015 | 2016- 2017 | 2018- 2019 | There- after | ||||||||||||

(Amounts are in thousands) | ||||||||||||||||

Contractual obligations: | ||||||||||||||||

Operating leases (1) | $ | 3,902,354 | 421,634 | 780,335 | 668,687 | 2,031,698 | ||||||||||

Purchase obligations (2)(3)(4) | 1,906,378 | 983,246 | 281,277 | 183,285 | 458,570 | |||||||||||

Other long-term liabilities: | ||||||||||||||||

Self-insurance reserves (5) | 364,366 | 151,153 | 95,570 | 40,873 | 76,770 | |||||||||||

Accrued postretirement benefit cost (6) | 110,808 | 4,238 | 9,005 | 9,669 | 87,896 | |||||||||||

Long-term debt (7) | 217,638 | 24,936 | 106,241 | 40,129 | 46,332 | |||||||||||

Other | 83,702 | 39,761 | 24,606 | 1,430 | 17,905 | |||||||||||

Total | $ | 6,585,246 | 1,624,968 | 1,297,034 | 944,073 | 2,719,171 | ||||||||||

Off-Balance Sheet Arrangements

The Company is not a party to any off-balance sheet arrangements that have, or are reasonably likely to have, a current or future effect on the Company’s financial condition, results of operations or cash flows.

____________________________

(1) | For a more detailed description of the operating lease obligations, refer to Note 9(a) Commitments and Contingencies - Operating Leases in the Notes to Consolidated Financial Statements. |

(2) | Purchase obligations include agreements to purchase goods or services that are enforceable and legally binding on the Company and that specify all significant terms, including fixed or minimum quantities to be purchased, fixed, minimum or variable price provisions and the approximate timing of the transaction. Purchase obligations exclude agreements that are cancelable within 30 days without penalty. |

(3) | As of December 27, 2014, the Company had $6.5 million outstanding in trade letters of credit and $5.0 million in standby letters of credit to support certain of these purchase obligations. |

(4) | Purchase obligations include $948.2 million in real estate taxes, insurance and maintenance commitments related to operating leases. The actual amounts to be paid are variable and have been estimated based on current costs. |

(5) | As of December 27, 2014, the Company had a restricted trust account in the amount of $169.2 million for the benefit of the Company’s insurance carrier related to self-insurance reserves. |

(6) | For a more detailed description of the postretirement benefit obligations, refer to Note 5 Postretirement Benefits in the Notes to Consolidated Financial Statements. |

(7) | For a more detailed description of the long-term debt obligations, refer to Note 4 Consolidation of Joint Ventures and Long-Term Debt in the Notes to Consolidated Financial Statements. |

14

Recently Issued Accounting Standards

In January 2014, the Financial Accounting Standards Board (FASB) issued an ASU permitting companies to make an accounting policy election to account for qualified affordable housing investments using the proportional amortization method if certain criteria are met. Under this method, the investment is amortized in proportion to the tax credits received and the net investment performance is recognized in the statements of earnings as a component of income tax expense. This ASU is effective for reporting periods beginning after December 15, 2014 with early adoption permitted. The Company elected to adopt the ASU early. The cumulative effect of the change from adopting the ASU was recorded during the quarter ended March 29, 2014 as the effect on the quarter and prior periods was not material to the Company’s financial condition or results of operations.

In May 2014, the FASB issued an ASU on the recognition of revenue from contracts with customers. The ASU requires additional disclosures about the nature, amount, timing and uncertainty of revenue and cash flows arising from customer contracts. This ASU is effective for reporting periods beginning after December 15, 2016 and early adoption is not permitted. The adoption of this ASU will not have an effect on the Company’s financial condition, results of operations or cash flows.

Critical Accounting Policies

The Company’s discussion and analysis of its financial condition and results of operations are based upon the Company’s consolidated financial statements, which have been prepared in accordance with U.S. generally accepted accounting principles. The preparation of these financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. The Company’s significant accounting policies are described in Note 1 in the Notes to Consolidated Financial Statements. The Company believes the following critical accounting policies reflect its more significant judgments and estimates used in the preparation of its consolidated financial statements.

Inventories

Inventories are valued at the lower of cost or market. The cost for 84% of inventories was determined using the dollar value LIFO method as of December 27, 2014 and December 28, 2013. Under this method, inventory is stated at cost, which is determined by applying a cost-to-retail ratio to each similar merchandise category’s ending retail value. The cost of the remaining inventories was determined using the first-in, first-out (FIFO) method. The FIFO cost of inventory approximates replacement or current cost. The FIFO method is used to value manufactured, seasonal, certain perishable and other miscellaneous inventory items because of fluctuating costs and inconsistent product availability. The Company also reduces inventory for estimated losses related to shrink.

Investments

All of the Company’s debt and equity securities are classified as available-for-sale (AFS) and carried at fair value. The Company evaluates whether AFS securities are other-than-temporarily impaired (OTTI) based on criteria that include the extent to which cost exceeds market value, the duration of the market decline, the credit rating of the issuer or security, the failure of the issuer to make scheduled principal or interest payments and the financial health and prospects of the issuer or security. Declines in the value of AFS securities determined to be OTTI are recognized in earnings and reported as OTTI losses, while declines in the value of AFS securities determined to be temporary are reported, net of tax, as other comprehensive losses and included as a component of stockholders’ equity. If market or issuer conditions decline, the Company may incur future impairments.

Debt securities with unrealized losses are considered OTTI if the Company intends to sell the debt security or if the Company will be required to sell the debt security prior to any anticipated recovery. If the Company determines that a debt security is OTTI under these circumstances, the impairment recognized in earnings is measured as the difference between the amortized cost and the current fair value. A debt security is also determined to be OTTI if the Company does not expect to recover the amortized cost of the debt security. However, in this circumstance, if the Company does not intend to sell the debt security and will not be required to sell the debt security, the impairment recognized in earnings equals the estimated credit loss as measured by the difference between the present value of expected cash flows and the amortized cost of the debt security. Expected cash flows are discounted using the debt security’s effective interest rate. Debt securities held by the Company at year end primarily consisted of corporate, state and municipality issued bonds with high credit ratings; therefore, the Company believes the credit risk is low. The Company believes a 50 basis point increase in long-term interest rates would result in an immaterial unrealized loss on its debt securities. Since the Company does not intend to sell its debt securities or will likely not be required to sell its debt securities prior to any anticipated recovery, such a hypothetical temporary unrealized loss would impact comprehensive earnings, but not net earnings or cash flows.

15

Equity securities held by the Company are subject to equity price risk that results from fluctuations in quoted market prices as of the balance sheet date. Market price fluctuations may result from perceived changes in the underlying economic characteristics of the issuer, the relative price of alternative investments and general market conditions. An equity security is determined to be OTTI if the Company does not expect to recover the cost of the equity security. A hypothetical decrease of 5% in the value of the Company’s equity securities would result in an immaterial decrease in the value of long-term investments.

Long-Lived Assets

The Company reviews its long-lived assets for impairment whenever events or changes in circumstances indicate that the net book value of an asset may not be recoverable. Recoverability of assets to be held and used is measured by a comparison of the net book value of an asset to the future net undiscounted cash flows expected to be generated by the asset. An impairment loss is recorded for the excess of the net book value over the fair value of the asset impaired. The fair value is estimated based on expected discounted future cash flows. Assets to be disposed of are reported at the lower of the carrying amount or fair value less cost to sell and are no longer depreciated. Long-lived assets, including buildings and improvements, leasehold improvements, and furniture, fixtures and equipment, are evaluated for impairment at the supermarket level.

The Company’s judgment regarding the existence of circumstances that indicate the potential impairment of an asset’s net book value is based on several factors, including the decision to close a supermarket or a decline in operating cash flows. The variability of these factors depends on a number of conditions, including uncertainty about future events and general economic conditions; therefore, the Company’s accounting estimates may change from period to period. These factors could cause the Company to conclude that a potential impairment exists, and the applicable impairment tests could result in a determination that the value of long-lived assets is impaired, resulting in a write-down of the long-lived assets. The Company attempts to select supermarket sites that will achieve the forecasted operating results. To the extent the Company’s assets are maintained in good condition and the forecasted operating results of the supermarkets are achieved, it is relatively unlikely that future assessments of recoverability would result in impairment charges that would have a material effect on the Company’s financial condition and results of operations. There were no material changes in the estimates or assumptions related to the impairment of long-lived assets in 2014.

Cost of Merchandise Sold

Cost of merchandise sold includes costs of inventory and costs related to in-store production. Cost of merchandise sold also includes inbound freight charges, purchasing and receiving costs, warehousing costs and other costs of the Company’s distribution network.

Vendor allowances and credits, including cooperative advertising fees, received from a vendor in connection with the purchase or promotion of the vendor’s products are recognized as a reduction of cost of merchandise sold as earned. These allowances and credits are recognized as earned in accordance with the underlying agreement with the vendor and completion of the earnings process. Short-term vendor agreements with advance payment provisions are recorded as a current liability and recognized over the appropriate period as earned according to the underlying agreements. Long-term vendor agreements with advance payment provisions are recorded as a noncurrent liability and recognized over the appropriate period as earned according to the underlying agreements.

Self-Insurance

The Company is self-insured for health care claims and property, plant and equipment losses. The Company has insurance coverage for losses in excess of self-insurance limits for fleet liability, general liability and workers’ compensation claims. Historically, it has been infrequent for incurred claims to exceed these self-insurance limits.

Self-insurance reserves are established for health care, fleet liability, general liability and workers’ compensation claims. These reserves are determined based on actual claims experience and an estimate of claims incurred but not reported including, where necessary, actuarial studies. The Company believes that the use of actuarial studies to determine self-insurance reserves represents a consistent method of measuring these subjective estimates. Actuarial projections of losses for general liability and workers’ compensation claims are discounted and subject to variability. The causes of variability include, but are not limited to, such factors as future interest and inflation rates, future economic conditions, claims experience, litigation trends and benefit level changes. The Company believes a 100 basis point change in the discount rate would result in an immaterial change in the Company’s self-insurance reserves.

16

Forward-Looking Statements

From time to time, certain information provided by the Company, including written or oral statements made by its representatives, may contain forward-looking information as defined in Section 21E of the Securities Exchange Act of 1934. Forward-looking information includes statements about the future performance of the Company, which is based on management’s assumptions and beliefs in light of the information currently available to them. When used, the words “plan,” “estimate,” “project,” “intend,” “believe” and other similar expressions, as they relate to the Company, are intended to identify such forward-looking statements. These forward-looking statements are subject to uncertainties and other factors that could cause actual results to differ materially from those statements including, but not limited to, the following: competitive practices and pricing in the food and drug industries generally and particularly in the Company’s principal markets; results of programs to increase sales, including private label sales; results of programs to control or reduce costs; changes in buying, pricing and promotional practices; changes in shrink management; changes in the general economy; changes in consumer spending; changes in population, employment and job growth in the Company’s principal markets; and other factors affecting the Company’s business within or beyond the Company’s control. These factors include changes in the rate of inflation, changes in state and federal legislation or regulation, adverse determinations with respect to litigation or other claims, ability to recruit and retain employees, increases in operating costs including, but not limited to, labor costs, credit card fees and utility costs, particularly electric rates, ability to construct new supermarkets or complete remodels as rapidly as planned and stability of product costs. Other factors and assumptions not identified above could also cause the actual results to differ materially from those set forth in the forward-looking statements. The Company assumes no obligation to publicly update these forward-looking statements.

17

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

The Company does not utilize financial instruments for trading or other speculative purposes, nor does it utilize leveraged financial instruments.

The Company’s cash equivalents and short-term investments are subject to three market risks, namely interest rate risk, credit risk and secondary market risk. Most of the cash equivalents and short-term investments are held in money market investments and debt securities that mature in less than one year. Due to the quality of the short-term investments held, the Company does not expect the valuation of these investments to be significantly impacted by future market conditions.

The Company’s long-term investments consist of debt and equity securities that are classified as AFS and carried at fair value. The Company evaluates whether AFS securities are OTTI based on criteria that include the extent to which cost exceeds market value, the duration of the market decline, the credit rating of the issuer or security, the failure of the issuer to make scheduled principal or interest payments and the financial health and prospects of the issuer or security. Declines in the value of AFS securities determined to be OTTI are recognized in earnings and reported as OTTI, while declines in the value of AFS securities determined to be temporary are reported, net of tax, as other comprehensive losses and included as a component of stockholders’ equity. If market or issuer conditions decline, the Company may incur future impairments.

Debt securities are subject to both interest rate risk and credit risk. Debt securities with unrealized losses are considered OTTI if the Company intends to sell the debt security or if the Company will be required to sell the debt security prior to any anticipated recovery. If the Company determines that a debt security is OTTI under these circumstances, the impairment recognized in earnings is measured as the difference between the amortized cost and the current fair value. A debt security is also determined to be OTTI if the Company does not expect to recover the amortized cost of the debt security. However, in this circumstance, if the Company does not intend to sell the debt security and will not be required to sell the debt security, the impairment recognized in earnings equals the estimated credit loss as measured by the difference between the present value of expected cash flows and the amortized cost of the debt security. Expected cash flows are discounted using the debt security’s effective interest rate. Debt securities held by the Company at year end primarily consisted of corporate, state and municipality issued bonds with high credit ratings; therefore, the Company believes the credit risk is low. The Company believes a 50 basis point increase in long-term interest rates would result in an immaterial unrealized loss on its debt securities. Since the Company does not intend to sell its debt securities or will likely not be required to sell its debt securities prior to any anticipated recovery, such a hypothetical temporary unrealized loss would impact comprehensive earnings, but not net earnings or cash flows.

Equity securities held by the Company are subject to equity price risk that results from fluctuations in quoted market prices as of the balance sheet date. Market price fluctuations may result from perceived changes in the underlying economic characteristics of the issuer, the relative price of alternative investments and general market conditions. An equity security is determined to be OTTI if the Company does not expect to recover the cost of the equity security. A hypothetical decrease of 5% in the value of the Company’s equity securities would result in an immaterial decrease in the value of long-term investments.

18

Management’s Report on Internal Control over Financial Reporting

Management of the Company is responsible for establishing and maintaining adequate internal control over financial reporting (as defined in Rule 13a-15(f) and Rule 15d-15(f) under the Securities Exchange Act of 1934). The Company’s internal control over financial reporting is designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with U.S. generally accepted accounting principles. Because of inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions or that the degree of compliance with the policies or procedures may deteriorate.

Management assessed the effectiveness of the Company’s internal control over financial reporting as of December 27, 2014. In making this assessment, management used the criteria set forth by the Committee of Sponsoring Organizations of the Treadway Commission in Internal Control – Integrated Framework (2013). Based on this assessment and these criteria, management believes that the Company’s internal control over financial reporting was effective as of December 27, 2014.

19

Item 8. Financial Statements and Supplementary Data

Index to Consolidated Financial Statements and Schedule | ||

Page | ||

Report of Independent Registered Public Accounting Firm | ||

Consolidated Financial Statements: | ||

Consolidated Balance Sheets – December 27, 2014 and December 28, 2013 | ||

Consolidated Statements of Earnings – Years ended December 27, 2014, December 28, 2013 and December 29, 2012 | ||

Consolidated Statements of Comprehensive Earnings – Years ended December 27, 2014, December 28, 2013 and December 29, 2012 | ||

Consolidated Statements of Cash Flows – Years ended December 27, 2014, December 28, 2013 and December 29, 2012 | ||

Consolidated Statements of Stockholders’ Equity – Years ended December 27, 2014, December 28, 2013 and December 29, 2012 | ||

Notes to Consolidated Financial Statements | ||

The following consolidated financial statement schedule of the Company for the years ended December 27, 2014, December 28, 2013 and December 29, 2012 is submitted herewith: | ||

Schedule II – Valuation and Qualifying Accounts | ||

All other schedules are omitted as the required information is inapplicable or the information is presented in the financial statements or related notes. | ||

20

Report of Independent Registered Public Accounting Firm

The Board of Directors and Stockholders

Publix Super Markets, Inc.:

We have audited the accompanying consolidated balance sheets of Publix Super Markets, Inc. and subsidiaries as of December 27, 2014 and December 28, 2013, and the related consolidated statements of earnings, comprehensive earnings, cash flows and stockholders’ equity for each of the years in the three-year period ended December 27, 2014. In connection with our audits of the consolidated financial statements, we also have audited the financial statement schedule listed in the accompanying index. These consolidated financial statements and financial statement schedule are the responsibility of the Company’s management. Our responsibility is to express an opinion on these consolidated financial statements and financial statement schedule based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Publix Super Markets, Inc. and subsidiaries as of December 27, 2014 and December 28, 2013, and the results of their operations and their cash flows for each of the years in the three-year period ended December 27, 2014, in conformity with U.S. generally accepted accounting principles. Also in our opinion, the related financial statement schedule, when considered in relation to the basic consolidated financial statements taken as a whole, presents fairly, in all material respects, the information set forth therein.

/s/ KPMG LLP

Tampa, Florida

March 2, 2015

Certified Public Accountants

21

PUBLIX SUPER MARKETS, INC.

Consolidated Balance Sheets

December 27, 2014 and

December 28, 2013

Assets | 2014 | 2013 | ||||||

(Amounts are in thousands) | ||||||||

Current assets: | ||||||||