Attached files

| file | filename |

|---|---|

| EX-31.2 - EX-31.2 - EVERTEC, Inc. | d827106dex312.htm |

| EX-23.1 - EX-23.1 - EVERTEC, Inc. | d827106dex231.htm |

| EX-31.1 - EX-31.1 - EVERTEC, Inc. | d827106dex311.htm |

| EX-21.1 - EX-21.1 - EVERTEC, Inc. | d827106dex211.htm |

| EX-32.2 - EX-32.2 - EVERTEC, Inc. | d827106dex322.htm |

| EX-10.36 - EX-10.36 - EVERTEC, Inc. | d827106dex1036.htm |

| EX-10.37 - EX-10.37 - EVERTEC, Inc. | d827106dex1037.htm |

| EX-10.40 - EX-10.40 - EVERTEC, Inc. | d827106dex1040.htm |

| EX-10.38 - EX-10.38 - EVERTEC, Inc. | d827106dex1038.htm |

| EX-10.39 - EX-10.39 - EVERTEC, Inc. | d827106dex1039.htm |

| EXCEL - IDEA: XBRL DOCUMENT - EVERTEC, Inc. | Financial_Report.xls |

| EX-32.1 - EX-32.1 - EVERTEC, Inc. | d827106dex321.htm |

Table of Contents

Index to Financial Statements

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 001-35872

EVERTEC, Inc.

(Exact name of registrant as specified in its charter)

| Puerto Rico | 66-0783622 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. employer identification number) | |

| Cupey Center Building, Road 176, Kilometer 1.3, San Juan, Puerto Rico |

00926 | |

| (Address of principal executive offices) | (Zip Code) | |

(787) 759-9999

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, $0.01 par value | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.:

| Large accelerated filer | x | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the common stock held by non-affiliates of EVERTEC, Inc. was approximately $1,577,414,218 based on the closing price of $24.03 as of the close of business on June 30, 2014.

As of February 20, 2015, there were 77,893,144 outstanding shares of common stock of EVERTEC, Inc.

Documents Incorporated by Reference:

Part III incorporates certain information by reference to the Proxy Statement for the 2015 Annual Meeting of Shareholders

Table of Contents

Index to Financial Statements

EVERTEC, Inc.

2014 Annual Report on Form 10-K

| Page | ||||

| 1 | ||||

| Part I |

||||

| 3 | ||||

| 17 | ||||

| 36 | ||||

| 36 | ||||

| 36 | ||||

| 36 | ||||

| Part II |

||||

| 37 | ||||

| 40 | ||||

| Item 7—Management’s Discussion and Analysis of Financial Condition and Results of Operations |

42 | |||

| Item 7A—Quantitative and Qualitative Disclosures About Market Risks |

62 | |||

| 62 | ||||

| Item 9—Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

63 | |||

| 63 | ||||

| 65 | ||||

| Part III |

||||

| Item 10—Directors, Executive Officers and Corporate Governance |

66 | |||

| 66 | ||||

| 66 | ||||

| Item 13—Certain Relationships and Related Transactions and Director Independence |

66 | |||

| 66 | ||||

| Part IV |

||||

| 66 | ||||

| 73 | ||||

Table of Contents

Index to Financial Statements

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of, and subject to the protection of, the Private Securities Litigation Reform Act of 1995. Such statements can be identified by the use of forward-looking terminology such as “believes,” “expects,” “may,” “estimates,” “will,” “should,” “plans” or “anticipates” or the negative thereof or other variations thereon or comparable terminology, or by discussions of strategy. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and may involve significant risks and uncertainties, and that actual results may vary materially from those in the forward-looking statements as a result of various factors. Among the factors that significantly impact our business and could impact our business in the future are:

| • | our reliance on our relationship with Popular, Inc. (“Popular”) for a significant portion of our revenues and with Banco Popular de Puerto Rico (“Banco Popular”), Popular’s principal banking subsidiary, to grow our merchant acquiring business; |

| • | our ability to renew our client contracts on terms favorable to us; |

| • | our dependence on our processing systems, technology infrastructure, security systems and fraudulent payment detection systems, as well as on our personnel and certain third parties with whom we do business, and the risks to our business if our systems are hacked or otherwise compromised; |

| • | our ability to develop, install and adopt new software, technology and computing systems; |

| • | a decreased client base due to consolidations and failures in the financial services industry; |

| • | the credit risk of our merchant clients, for which we may also be liable; |

| • | the continuing market position of the ATH network; |

| • | a reduction in consumer confidence, whether as a result of a global economic downturn or otherwise, which leads to a decrease in consumer spending; |

| • | our dependence on credit card associations, including any adverse changes in credit card association or network rules or fees; |

| • | changes in the regulatory environment and changes in international, legal, political, administrative or economic conditions; |

| • | the geographical concentration of our business in Puerto Rico; |

| • | operating an international business in multiple regions with potential political and economic instability, including Latin America; |

| • | increased legal compliance risks associated with operating in countries outside the United States; |

| • | our ability to execute our geographic expansion and acquisition strategies; |

| • | our ability to protect our intellectual property rights against infringement and to defend ourselves against claims of infringement brought by third parties; |

| • | our ability to recruit and retain the qualified personnel necessary to operate our business; |

| • | our ability to comply with U.S. federal, state, local and foreign, regulatory requirements; |

| • | evolving industry standards and adverse changes in global economic, political and other conditions; |

| • | our high level of indebtedness and restrictions contained in our debt agreements, including our senior secured credit facilities, as well as debt that could be incurred in the future; |

| • | our ability to generate sufficient cash to service our indebtedness and to generate future profits; and |

| • | other risks and uncertainties detailed in Part I, Item IA “Risk Factors” in this Annual Report on Form 10-K (“Report”). |

1

Table of Contents

Index to Financial Statements

These forward-looking statements involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by the forward-looking statements. Forward-looking statements should, therefore, be considered in light of various factors, including those set forth under “Item 1A. Risk Factors,” in “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in this Report. These forward-looking statements speak only as of the date of this Report, and we do not undertake any obligation to publicly release any revisions to these forward-looking statements to reflect events or circumstances after the date of this Report or to reflect the occurrence of unanticipated events.

INDUSTRY AND MARKET DATA

This Form 10-K includes industry data that we obtained from periodic industry publications, including the January 2013 and July 2014 Nilson Reports, the October 2013 Gartner Dataquest Market Statistics and the 2014 World Payments Report. Industry publications generally state that the information contained therein has been obtained from sources believed to be reliable. This Form 10-K also includes market share and industry data that were prepared primarily based on management’s knowledge of the industry and industry data. Unless otherwise noted, statements as to our market share and market position relative to our competitors are approximated and based on management estimates using the above-mentioned latest-available third-party data and our internal analyses and estimates. While we are not aware of any misstatements regarding any industry data presented herein, our estimates, in particular as they relate to market share and our general expectations, involve risks and uncertainties and are subject to change based on various factors, including those discussed under “Risk Factors,” “Forward-Looking Statements” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this Form 10-K.

The Gartner report, “Forecast: Enterprise IT Spending by Vertical Industry Market, Worldwide, 2011-2017, 3Q13 Update,” October 2013, described herein (the “Gartner Report”), represents data, research opinion or viewpoints published as part of a syndicated subscription service by Gartner, Inc. and are not representations of fact. The Gartner Report speaks as of its original publication date (and not as of the date of this Form 10-K) and the opinions expressed in the Gartner Report are subject to change without notice.

2

Table of Contents

Index to Financial Statements

Part I

Except as otherwise indicated or unless the context otherwise requires, (a) the terms “EVERTEC,” “we,” “us,” “our,” “our Company” and “the Company” refer to EVERTEC, Inc. and its subsidiaries on a consolidated basis, (b) the term “Holdings” refers to EVERTEC Intermediate Holdings, LLC, but not any of its subsidiaries and (c) the term “EVERTEC Group” refers to EVERTEC Group, LLC and its predecessor entities and their subsidiaries on a consolidated basis, including the operations of its predecessor entities prior to the Merger (as defined below). EVERTEC Inc.’s subsidiaries include Holdings, EVERTEC Group, EVERTEC Dominicana, SAS, EVERTEC Panamá, S.A., EVERTEC Costa Rica, S.A. (“EVERTEC CR”), EVERTEC Guatemala, S.A. and EVERTEC México Servicios de Procesamiento, S.A. de C.V. Neither EVERTEC nor Holdings conducts any operations other than with respect to its indirect or direct ownership of EVERTEC Group.

Company Overview

EVERTEC is the leading full-service transaction processing business in Latin America, providing a broad range of merchant acquiring, payment processing and business process management services. According to the July 2014 Nilson Report, we are the largest merchant acquirer in the Caribbean and Central America and one of the largest in Latin America, based on total number of transactions. We serve 19 countries in the region from our base in Puerto Rico. We manage a system of electronic payment networks that process more than two billion transactions annually, and offer a comprehensive suite of services for core bank processing, cash processing and technology outsourcing. In addition, we own and operate the ATH network, one of the leading personal identification number (“PIN”) debit networks in Latin America. We serve a diversified customer base of leading financial institutions, merchants, corporations and government agencies with “mission-critical” technology solutions that enable them to issue, process and accept transactions securely. We believe our business is well-positioned to continue to expand across the fast-growing Latin American region.

We are differentiated, in part, by our diversified business model, which enables us to provide our varied customer base with a broad range of transaction-processing services from a single source across numerous channels and geographic markets. We believe this single-source capability provides several competitive advantages that will enable us to continue to penetrate our existing customer base with complementary new services, win new customers, develop new sales channels and enter new markets. We believe these competitive advantages include:

| • | Our ability to provide best in class individual products across all verticals; |

| • | Our ability to provide in one package a range of services that traditionally had to be sourced from different vendors; |

| • | Our ability to serve customers with disparate operations in several geographies with a single integrated technology solution that enables them to manage their business as one enterprise; and |

| • | Our ability to capture and analyze data across the transaction processing value chain and use that data to provide value-added services that are differentiated from those offered by pure-play vendors that serve only one portion of the transaction processing value chain (such as only merchant acquiring or payment processing). |

Our broad suite of services spans the entire transaction processing value chain and includes a range of front-end customer-facing solutions such as the electronic capture and authorization of transactions at the point-of-sale, as well as back-end support services such as the clearing and settlement of transactions and account reconciliation for card issuers. These include: (i) merchant acquiring services, which enable point of sales (“POS”) and e-commerce merchants to accept and process electronic methods of payment such as debit, credit, prepaid and electronic benefit transfer (“EBT”) cards; (ii) payment processing services, which enable financial institutions

3

Table of Contents

Index to Financial Statements

and other issuers to manage, support and facilitate the processing for credit, debit, prepaid, automated teller machines (“ATM”) and EBT card programs; and (iii) business process management solutions, which provide “mission-critical” technology solutions such as core bank processing, as well as IT outsourcing and cash management services to financial institutions, corporations and governments. We provide these services through a highly scalable, end-to-end technology platform that we manage and operate in-house and that generates significant operating efficiencies that enable us to maximize profitability.

We sell and distribute our services mainly through a proprietary direct sales force with strong customer relationships. We are also building a variety of indirect sales channels that enable us to leverage the distribution capabilities of partners in adjacent markets, including value-added resellers. Also, we continue to pursue joint ventures and merchant acquiring alliances.

We benefit from an attractive business model, the hallmarks of which are recurring revenue, scalability, significant operating margins and low capital expenditure requirements. Our revenue is recurring in nature because of the “mission-critical” and embedded nature of the services we provide, the high switching costs associated with these services and the multi-year contracts we negotiate with our customers. Our business model enables us to continue to grow our business organically without significant additional capital expenditures.

We generate revenues based primarily on transaction or discount fees paid by our merchants and financial institutions in our merchant acquiring and payment processing segments and on transaction fees or fees based on number of accounts on file in our business solutions segment. Our total revenues increased from $276.3 million for the year ended December 31, 2009 to $361.1 million for the year ended December 31, 2014, representing a compound annual growth rate (“CAGR”) of 5%. Our Adjusted EBITDA (as defined in “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Net Income Reconciliation to EBITDA, Adjusted EBITDA, Adjusted Net Income and Adjusted Net Income per common share”) increased from $117.6 million for the year ended December 31, 2009 to $182.8 million for the year ended December 31, 2014, representing a CAGR of 9%. Our Adjusted Net Income (as defined in “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Net Income Reconciliation to EBITDA, Adjusted EBITDA, Adjusted Net Income and Adjusted Net Income per common share”) increased from $58.2 million for the year ended December 31, 2009 to $130.0 million for the year ended December 31, 2014, representing a CAGR of 17%.

Corporate Background

EVERTEC, Inc. (formerly known as Carib Latam Holdings, Inc.) is a Puerto Rico corporation organized in April 2012. Our main operating subsidiary, EVERTEC Group, LLC (formerly known as EVERTEC, LLC and EVERTEC, Inc., hereinafter “EVERTEC Group”), was organized in Puerto Rico in 1988. EVERTEC Group was formerly a wholly-owned subsidiary of Popular. On September 30, 2010, pursuant to an Agreement and Plan of Merger (as amended, the “Merger Agreement”), AP Carib Holdings, Ltd. (“Apollo”) acquired a 51% indirect ownership interest in EVERTEC Group as part of a merger (the “Merger”) and EVERTEC Group became a wholly-owned subsidiary of Holdings.

On April 17, 2012, EVERTEC Group was converted from a Puerto Rico corporation to a Puerto Rico limited liability company (the “Conversion”) for the purpose of improving its consolidated tax efficiency by taking advantage of changes to the Puerto Rico Internal Revenue Code, as amended (the “PR Code”), that permit limited liability companies to be treated as partnerships that are pass-through entities for Puerto Rico tax purposes. Concurrent with the Conversion, Holdings, which is our direct subsidiary, was also converted from a Puerto Rico corporation to a Puerto Rico limited liability company. Prior to these conversions, EVERTEC, Inc. was formed in order to act as the new parent company of Holdings and its subsidiaries, including EVERTEC Group. The transactions described above in this paragraph are collectively referred to as the “Reorganization.”

4

Table of Contents

Index to Financial Statements

History and Separation from Popular

We have a 25 year operating history in the transaction processing industry. Prior to the Merger, EVERTEC Group was 100% owned by Popular, the largest financial institution in the Caribbean, and operated substantially as an independent entity within Popular. As mentioned above, following the Merger, Apollo which is an affiliate of the leading private equity investor Apollo Global Management, LLC, owned a 51% interest in us and shortly thereafter, we began the transition to a separate, stand-alone entity. As a stand-alone company, we have made substantial investments in our technology and infrastructure, recruited various senior executives with significant transaction processing experience in Latin America, enhanced our profitability through targeted productivity and cost savings actions and broadened our footprint beyond the markets historically served.

We continue to benefit from our relationship with Popular. Popular is our largest customer, acts as one of our largest merchant referral partners and sponsors us with the card associations (such as Visa or MasterCard), enabling merchants to accept these card associations’ credit card transactions. Popular also provides merchant sponsorship as one of the participants of the ATH network, enabling merchants to connect to the ATH network and accept ATH debit card transactions. We provide a number of critical products and services to Popular, which are governed by a 15-year Amended and Restated Master Services Agreement (the “Master Services Agreement”) that runs through 2025.

Initial Public Offering and Secondary Offerings

On April 17, 2013, we completed our initial public offering of 28,789,943 shares of common stock at a price to the public of $20.00 per share. EVERTEC offered a total of 6,250,000 shares and selling stockholders offered a total of 22,539,943 shares, of which 13,739,284 shares were sold by Apollo, and 8,800,659 shares were sold by Popular. We used the net proceeds of approximately $117.4 million, after deducting underwriting discounts and commissions, from our sale of shares in the initial public offering and proceeds from borrowings under the 2013 Credit Agreement (as defined below), together with available cash on hand, to redeem our 11.0% senior notes due 2018 (the “senior notes”) and to refinance our previous senior secured credit facilities.

On September 18, 2013, we completed a public offering of 23,000,000 shares of our common stock by Apollo, Popular, and current and former employees at a price to the public of $22.50 per share. We did not receive any proceeds from this offering. After the completion of the offering, Apollo owned approximately 9.2 million shares, or 11.2%, of our common stock, and Popular owned approximately 17.5 million shares or 21.3% of our common stock.

On December 13, 2013, we completed a public offering of 15,233,273 shares of our common stock by Apollo, Popular, and current and former employees at a price to the public of $20.60 per share. We did not receive any proceeds from this offering. After the completion of the offering, Popular owns approximately 11.7 million shares, or 14.9% of our common stock, and Apollo no longer owns any shares of our common stock.

Principal Stockholder

Popular, Inc. (NASDAQ: BPOP), whose principal banking subsidiary’s history dates back to 1893, is the No. 1 bank holding company by both assets and deposits based in Puerto Rico, and, as of September 30, 2014, ranks 49 by assets among U.S. bank holding companies. As of December 31, 2014, Popular owned approximately 15% of our common stock.

5

Table of Contents

Index to Financial Statements

Industry Trends

Shift to Electronic Payments

The ongoing migration from cash, check and other paper methods of payment to electronic payments continues to benefit the transaction processing industry globally. This migration is driven by factors including customer convenience, marketing efforts by financial institutions, card issuer rewards and the development of new forms of payment. We believe that the penetration of electronic payments in the markets where we principally operate is significantly lower relative to more mature U.S. and European markets and that this ongoing shift will continue to generate substantial growth opportunities for our business.

Fast Growing Latin American and Caribbean Financial Services and Payments Markets

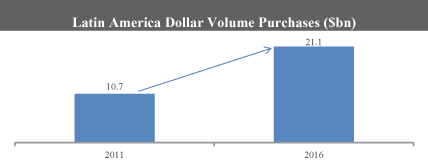

Currently, the adoption of banking products, including electronic payments, in the Latin American and Caribbean region is lower relative to the mature U.S. and European markets. As these markets continue to evolve and grow, the emergence of a larger and more sophisticated consumer base will influence and drive an increase in card (like debit, credit, prepayment, and EBT) and electronic payments usage. According to the January 2013 Nilson Report, Latin American purchase transactions are projected to continue to grow at a CAGR of 15% through 2016 (as illustrated in the chart below), which represents the third fastest growing market in the world.

We believe that the attractive characteristics of our markets and our leadership positions across multiple services and sectors will continue to drive growth and profitability in our businesses.

Ongoing Technology Outsourcing Trends

Financial institutions globally are facing significant challenges including the entrance of non-traditional competitors, the compression of margins on traditional products, significant channel proliferation and increasing regulation that could potentially curb profitability. Many of these institutions have traditionally fulfilled their IT needs through legacy computer systems, operated by the institution itself. Legacy systems are generally highly proprietary, inflexible and costly to operate and maintain and we believe the trend to outsource in-house technology systems and processes by financial institutions will continue. According to the Gartner Report, the banking and securities sector in Latin America is forecasted to have $33 billion of annual IT expenditures by 2017. We believe our ability to provide integrated, open, flexible, customer-centric and efficient IT products and services cater to the evolving needs of our customers, particularly for small- and mid-sized financial institutions in the Latin American markets in which we operate.

Industry Innovation

The electronic payments industry experiences ongoing technology innovation. Emerging payment technologies such as prepaid cards, contactless payments, payroll cards, mobile commerce, online “wallets” and innovative POS devices facilitate the continued shift away from cash, check and other paper methods of payment.

6

Table of Contents

Index to Financial Statements

According to the 2014 World Payments Report, mobile payments transactions are expected to grow by 60.8% annually through to 2015. E-payments growth will decelerate to 15.9% growth during the same period. The increasing demand for new and flexible payment options catering to a wider range of consumer segments is driving growth in the electronic payment processing sector.

Our Competitive Strengths

Market Leadership in Latin America and the Caribbean

We believe we have an inherent competitive advantage relative to U.S. competitors based on our ability to locally leverage our infrastructure, as well as our first-hand knowledge of the Latin American and Caribbean markets, language and culture. We have built leadership positions across the transaction processing value chain in the geographic markets that we serve, which we believe will enable us to continue to penetrate our core markets and provide advantages to enter new markets. According to the July 2014 Nilson Report, we are one of the largest merchant acquirers in Latin America and the largest in the Caribbean and Central America based on total number of transactions. We own and operate the ATH network, one of the leading ATM and PIN debit networks in Latin America. The ATH network and processing businesses processed over two billion transactions in 2014, which according to management estimates, makes ATH branded products the most frequently used electronic method of payment in Puerto Rico, exceeding the total transaction volume of Visa, MasterCard, American Express and Discover, combined. Given our scale and customer base of top tier financial institutions and government entities, we believe we are the leading card issuer and core bank processor in the Caribbean and the only non-bank provider of cash processing services to the U.S. Federal Reserve in the Caribbean. We believe our competitive position and strong brand recognition increases card acceptance, driving usage of our proprietary network, and presents opportunities for future strategic relationships.

Diversified Business Model Across the Transaction Processing Value Chain

Our leadership position in the region is driven in part by our diversified business model which provides the full range of merchant acquiring, payment processing and business solutions services to financial institutions, merchants, corporations and government agencies across different geographies. We offer end-to-end technology solutions through a single provider and we have the ability to tailor and customize the features and functionality of all our products and services to the specific requirements of our customers in various industries and across geographic markets. We believe the breadth of our offerings enables us to penetrate our customer base from a variety of perspectives and positions us favorably to cross-sell our other offerings over time. For example, we may host a client’s electronic cash register software (part of the business solutions segment), acquire transactions that originate at that electronic cash register (part of the merchant acquiring segment), route the transaction through the ATH network (part of the payment processing segment), and finally settle the transaction between the client and the issuer bank (part of the payment processing segment). In addition, we can serve customers with disparate operations in several geographies with a single integrated technology solution that enables them to access one processing platform and manage their business as one enterprise. We believe these services are becoming increasingly complementary and integrated as our customers seek to capture, analyze and monetize the vast amounts of data that they process across their enterprises. As a result, we are able to capture significant value across the transaction processing value chain and believe that this combination of attributes represents a differentiated value proposition vis-à-vis our competitors who have a limited product and service offering.

Broad and Deep Customer Relationships and Recurring Revenue Business Model

We have built a strong and long-standing portfolio of top tier financial institution, merchant, corporate and government customers across Latin America and the Caribbean, which provides us with a reliable, recurring revenue base and powerful references that have helped us expand into new channels and geographic markets. Customers representing approximately 99% of our 2013 revenue continued to be customers in 2014, due to the “mission-critical” and embedded nature of the services provided and the high switching costs associated with

7

Table of Contents

Index to Financial Statements

these services. Our Payment Processing and Merchant Acquiring segments, as well as certain business lines representing the majority of our business solutions segment, generate recurring revenues that collectively accounted for approximately 89% of our total revenues in 2014. We receive recurring revenues from services based on our customers’ on-going daily commercial activity such as processing loans, hosting accounts and information on our servers, and processing everyday payments at grocery stores, gas stations and similar establishments. We generally provide these services under one to five year contracts, often with automatic renewals. We also provide a few project-based services that generate non-recurring revenues in our business solutions segment such as IT consulting for a specific project or integration. Additionally, we entered into a 15-year Master Services Agreement with Popular on September 30, 2010. We provide a number of critical payment processing and business solutions products and services to Popular and benefit from the bank’s distribution network and continued support. Through our long-standing and diverse customer relationships, we are able to gain valuable insight into trends in the marketplace that allows us to identify new market opportunities. In addition, we believe the recurring nature of our business model provides us with significant revenue and earnings stability.

Highly Scalable, End-to-End Technology Platform

Our diversified business model is supported by our highly scalable, end-to-end technology platform which allows us to provide a full range of transaction processing services and develop and deploy a broad suite of technology solutions to our customers at low incremental costs and increasing operating efficiencies. We have spent over $140 million over the last five years on technology investments to continue to build the capacity and functionality of our platform and we have been able to achieve attractive economies of scale with flexible product development capabilities. We have a proven ability to seamlessly leverage our existing platforms to develop new products and services and expand in new markets. We believe that our platform will increasingly allow us to provide differentiated services to our customers and facilitate further expansion into new sales channels and geographic markets.

Experienced Management Team with a Strong Track Record of Execution

We have grown our revenue organically by introducing new products and services and expanding our geographic footprint throughout Latin America. We have a proven track record of creating value from operational and technology improvements and capitalizing on cross-selling opportunities. We have combined new leadership at EVERTEC, bringing many years of industry experience, with long-standing leadership at the operating business level. In April 2015, Morgan M. Schuessler, Jr., former President of International for Global Payments, Inc., will join our management team as President and Chief Executive Officer. In 2013, Eduardo Camargo, former Chief Information Officer and Chief Technology Officer for Bank of America Merrill Lynch Brazil, joined our management team as Chief Information Officer. In 2012, Philip Steurer, former Senior Vice President of Latin America for First Data Corporation, joined our management team as our Chief Operating Officer. Mr. Schuessler and Mr. Steurer both have extensive experience managing and growing transaction processing businesses in Latin America as well as North America, Asia and Europe. In addition, we successfully executed our separation from Popular, transitioning EVERTEC from a division of a larger company to a stand-alone entity with public company best practices. Instrumental to this transition was our Chief Financial Officer Juan J. Román, former CFO of Triple-S Management, a publicly listed insurance company. Collectively our management team benefits from an average of over 20 years of industry experience and we believe they are well positioned to continue to drive growth across business lines and regions.

8

Table of Contents

Index to Financial Statements

Our Growth Strategy

We intend to grow our business by continuing to execute on the following business strategies:

Continue Cross-Sales to Existing Customers

We seek to grow revenue by continuing to sell additional products and services to our existing merchant, financial institution, corporate and government customers. We intend to broaden and deepen our customer relationships by leveraging our full suite of end-to-end technology solutions. For example, we believe that there is significant opportunity to cross-sell our network services, ATM point-of-sale processing and card issuer processing services to our over 180 existing financial institution customers, particularly in markets outside of Puerto Rico. We will also seek to continue to cross-sell value added services into our existing merchant base of over 27,500 locations.

Leverage Our Franchise to Attract New Customers in the Markets We Currently Serve

We intend to attract new customers by leveraging our comprehensive product and services offering, the strength of our brand and our leading end-to-end technology platform. Furthermore, we believe we are uniquely positioned to develop new products and services to take advantage of our access to and position in markets we currently serve. For example, in markets we serve outside of Puerto Rico, we believe there is a significant opportunity to penetrate small to medium financial institutions with our products and services, as well as to penetrate governments with offerings such as EBT.

Expand in the Latin American Region

We believe there is substantial opportunity to expand our businesses in the Latin American region. We believe that we have a competitive advantage relative to U.S. competitors based on our ability to locally leverage our infrastructure, breadth of products and services as well as our first-hand knowledge of Latin American markets, language and culture. Significant growth opportunities exist in a number of large markets such as Colombia, México, and Chile, among others. We also believe that there is an opportunity to provide our services to existing financial institution customers in other regions where they operate. Additionally, we continually evaluate our strategic plans for geographic expansion, which can be achieved through joint ventures, partnerships, alliances or strategic acquisitions.

Develop New Products and Services

Our experience with our customers provides us with insight into their needs and enables us to continuously develop new transaction processing services. We plan to continue growing our merchant, financial institution, corporate and government customer base by developing and offering additional value-added products and services to cross-sell along with our core offerings. We intend to continue to focus on these and other new product opportunities in order to take advantage of our leadership position in the transaction processing industry in the Latin American and Caribbean region.

Our Business

We offer our customers end-to-end products and solutions across the transaction processing value chain from a single source across numerous channels and geographic markets, as further described below.

Merchant Acquiring

According to the July 2014 Nilson Report, we are the largest merchant acquirer in the Caribbean and Central America and one of the largest in Latin America based on total number of transactions. Our merchant acquiring business provides services to merchants at over 27,500 locations that allow them to accept electronic methods of

9

Table of Contents

Index to Financial Statements

payment such as debit, credit, prepaid and EBT cards carrying the ATH, Visa, MasterCard, Discover and American Express brands. Our full suite of merchant acquiring services includes, but is not limited to, the underwriting of each merchant’s contract, the deployment and rental of POS devices and other equipment necessary to capture merchant transactions, the processing of transactions at the point-of-sale, the settlement of funds with the participating financial institution, detailed sales reports and customer support. In 2014, our merchant acquiring business processed over 320 million transactions.

Our Merchant Acquiring business generated $79.1 million, or 21.9%, of total revenues and $34.3 million, or 24.2%, of total segment income from operations for the year ended December 31, 2014.

Payment Processing

We are the largest card processor and network services provider in the Caribbean. We provide an innovative and diversified suite of payment processing products and services to blue chip regional and global corporate customers, government agencies, and financial institutions across Latin American and the Caribbean. These services provide the infrastructure technology necessary to facilitate the processing and routing of payments across the transaction processing value chain.

At the point-of-sale, we sell transaction processing technology solutions, similar to the services in our merchant acquiring business, to other merchant acquirers to enable them to service their own merchant customers. We also offer terminal driving solutions to merchants, merchant acquirers (including our merchant acquiring business) and financial institutions, which provide the technology to securely operate, manage and monitor POS terminals and ATMs. We also rent POS devices to financial institution customers who seek to deploy them across their own businesses.

To connect the POS terminals to card issuers, we own and operate the ATH network, one of the leading ATM and PIN debit networks in Latin America. The ATH network connects the merchant or merchant acquirer to the card issuer and enables transactions to be routed or “switched” across the transaction processing value chain. The ATH network offers the technology, communications standards, rules and procedures, security and encryption, funds settlement and common branding that allow consumers, merchants, merchant acquirers, ATMs, card issuer processors and card issuers to conduct commerce seamlessly, across a variety of channels, similar to the services provided by Visa and MasterCard. The ATH network and processing businesses processed over two billion transactions in 2014. Management believes that over 70% of all ATM transactions and over 80% of all debit transactions in Puerto Rico are processed through the ATH network.

To enable financial institutions, governments and other businesses to issue and operate a range of payment products and services, we offer an array of card processing and other payment technology services, such as internet and mobile banking software services, bill payment systems and EBT solutions. Financial institutions and certain retailers outsource to us certain card processing services such as card issuance, processing card applications, cardholder account maintenance, transaction authorization and posting, fraud and risk management services, and settlement. Our payment products include electronic check processing, automated clearing house (“ACH”), lockbox, online, interactive voice response and web-based payments through personalized websites, among others.

We have been the only provider of EBT services to the Puerto Rican government since 1998. Our EBT application allows certain agencies to deliver government benefits to participants through a magnetic card system and serves over 775,000 active participants.

Our Payment Processing business accounted for $105.4 million, or 29.2%, of total revenues and $66 million, or 42.0%, of total segment income from operations for the year ended December 31, 2014.

10

Table of Contents

Index to Financial Statements

Business Solutions

We provide our financial institution, corporate and government customers with a full suite of business process management solutions including specifically core bank processing, network hosting and management, IT consulting services, business process outsourcing, item and cash processing, and fulfillment. In addition, we believe we are the only non-bank provider of cash processing services to the U.S. Federal Reserve in the Caribbean.

Our Business Solutions business accounted for $176.6 million, or 48.9%, of total revenues and $47.6 million, or 33.9%, of total segment income from operations for the year ended December 31, 2014.

For additional information regarding the Company’s segments refer to Note 21 of the Notes to Audited Consolidated Financial Statements included elsewhere in this Annual Report on Form 10-K.

Competition

Competitive factors impacting the success of our services include the quality of the technology-based application or service, application features and functions, ease of delivery and integration, ability of the provider to maintain, enhance, and support the applications or services, and price. We believe that we compete favorably in each of these categories. In addition, we believe that our relationship with Banco Popular, large market share and financial institution industry expertise, combined with our ability to offer multiple applications, services and integrated solutions to individual customers, enhances our competitiveness against companies with more limited offerings.

In merchant acquiring, we compete with several other service providers and financial institutions, including Vantiv, Inc., First Data Corporation, Global Payments Inc., Elavon, Inc., Sage Payment Solutions and some local banks. Also, the card associations and payment networks are increasingly offering products and services that compete with ours. The main competitive factors are price, brand awareness, strength of the relationship with financial institutions, system functionality, service capabilities and innovation. Our business is also impacted by the expansion of new payments methods and devices, card association business model expansion, and bank consolidation.

In payment processing, we compete with several other third party card processors and debit networks, including First Data Corporation, Fidelity National Information Services, Inc., Fiserv, Inc., Total System Services, Inc., Vantiv, Inc. and Global Payments Inc. Also, card associations and payment networks are increasingly offering products and services that compete with our products and services. The main competitive factors are price, system performance and reliability, system functionality, security, service capabilities and disaster recovery and business continuity capabilities.

In business solutions, our main competition includes internal technology departments within financial institutions, retailers, data processing or software development departments of large companies and/or large technology and consulting companies. Main competitive factors are price, system performance and reliability, system functionality, security, service capabilities, and disaster recovery and business continuity capabilities.

Intellectual Property

We own numerous registrations for several trademarks in different jurisdictions and own or have licenses to use certain software and technology, which are critical to our business and future success. For example, we own the ATH and EVERTEC trademarks, which are associated by the public, financial institutions and merchants with high quality and reliable electronic commerce, payments, and debit network solutions and services. Such goodwill allows us to be competitive, retain our customers, and expand our business. Further, we also use a combination of (i) proprietary software, and (ii) duly licensed third party software to operate our business and

11

Table of Contents

Index to Financial Statements

deliver secure and reliable products and services to our customers. The licensed software is subject to terms and conditions that we considered within the industry standards. Most are perpetual licenses and the rest are term licenses with renewable terms. In addition, we monitor these license agreements and maintain close contact with our suppliers to ensure their continuity of service.

We seek to protect our intellectual property rights by securing appropriate statutory intellectual property protection in the relevant jurisdictions, including patents. We also protect proprietary know-how and trade secrets through company confidentiality policies, licenses, programs, and contractual agreements.

Employees

As of December 31, 2014, we employed 1,700 persons across 6 countries in Latin America and the Caribbean. None of our employees are subject to collective bargaining agreements, and we consider our relationships with our employees to be good. We have not experienced any work stoppages.

Government Regulation and Payment Network Rules

Oversight by the Federal Reserve

Popular is a bank holding company that has elected to be treated as a financial holding company under the provisions of the Gramm-Leach-Bliley Act of 1999. So long as we are deemed to be a “subsidiary” of Popular for purposes of the BHC Act, we will be subject to regulation and oversight by the Board of Governors of the Federal Reserve System (the “Federal Reserve Board”) and our activities will be subject to several related significant restrictions, the more significant of which are discussed below.

Transactions with Affiliates

So long as we are deemed to be an affiliate of Popular for purpose of the affiliate transaction rules found in Section 23A and 23B of the Federal Reserve Act and Regulation W of the Federal Reserve Board, we will be subject to various restrictions on our ability to borrow from, and engage in certain other transactions with Popular’s bank subsidiaries, Banco Popular and Banco Popular North America (“BPNA”). In general these rules require that any “covered transaction” that we enter into with Banco Popular or BPNA (or any of their respective operating subsidiaries), as the case may be, must be secured by designated amounts of specified collateral and must be limited to 10% of Banco Popular’s or BPNA’s, as the case may be, capital stock and surplus. In addition, all “covered transactions” between Banco Popular or BPNA, on the one hand, and Popular and all of its subsidiaries and affiliates on the other hand, must be limited to 20% of Banco Popular’s or BPNA’s, as the case may be, capital stock and surplus. “Covered transactions” are defined by statute to include a loan or extension of credit, as well as a purchase of securities issued by an affiliate, a purchase of assets (unless otherwise exempted by the Federal Reserve Board) from the affiliate, the acceptance of securities issued by the affiliate as collateral for a loan, and the issuance of a guarantee, acceptance or letter of credit on behalf of an affiliate.

In addition, Section 23B and Regulation W require that as long as we are deemed an affiliate of Banco Popular or BPNA, all transactions between us and either Banco Popular or BPNA be on terms and conditions, including credit standards, that are substantially the same or at least as favorable to Banco Popular or BPNA, as the case may be, as those prevailing at the time for comparable transactions involving other non-affiliated companies or, in the absence of comparable transactions, on terms and conditions, including credit standards, that in good faith would be offered by Banco Popular or BPNA to, or would apply to, non-affiliated companies.

Permissible Activities

As long as we are deemed to be controlled by Popular for bank regulatory purposes, we may conduct only those activities that are authorized for a bank holding company or a financial holding company under the BHC Act, the Federal Reserve Board’s Regulation K and other relevant U.S. federal banking laws. These activities generally

12

Table of Contents

Index to Financial Statements

include activities that are related to banking, financial in nature or incidental to financial activities. In addition, restrictions placed on Popular as a result of supervisory or enforcement actions may restrict us or our activities in certain circumstances, even if these actions are unrelated to our conduct or business. For so long as we are deemed to be a foreign subsidiary of a bank holding company under the Federal Reserve Board’s regulations, we will rely on the authority granted under the Federal Reserve Board’s Regulation K to conduct our data processing, management consulting and related activities outside the United States. The Federal Reserve Board’s Regulation K generally limits activities of a bank holding company outside the Unites States that are not banking or financial in nature, specifically permitted under Regulation K to foreign subsidiaries or necessary to carry on such activities that are not otherwise permissible for a foreign subsidiary under the banking regulations. We continue to engage in certain activities outside the scope of such permissible activities pursuant to authority under the Federal Reserve Board’s Regulation K, which allows a bank holding company to retain, in the context of an acquisition of a going concern, such otherwise impermissible activities if they account for not more than 5% of either the consolidated assets or consolidated revenues of the acquired organization.

New lines of business, other new activities, divestitures or acquisitions that we may wish to commence in the future may not be permissible for us under the BHC Act, Regulation K or other relevant U.S. federal banking laws. Further, as a result of being subject to regulation and supervision by the Federal Reserve Board, we may be required to obtain the approval of the Federal Reserve Board before engaging in certain new activities or businesses, whether organically or by acquisition, unless such activities are considered financial in nature. More generally, the Federal Reserve Board has broad power to approve, deny or refuse to act upon applications or notices for us to conduct new activities, acquire or divest businesses or assets, or reconfigure existing operations.

Examinations

As a technology service provider to financial institutions, we are also subject to regulatory oversight and examination by the Federal Financial Institutions Examination Council (the “FFIEC”), an interagency body of federal financial regulators that includes the Federal Reserve Board. The office of the Commissioner of Financial Institutions of Puerto Rico also participates in such examinations by the FFIEC. In addition, independent auditors annually review several of our operations to provide reports on internal controls for our clients’ auditors and regulators.

Regulatory Reform and Other Legislative Initiatives

The payment card industry has come under increased scrutiny from lawmakers and regulators. In July 2010, the Dodd-Frank Act was signed into law in the United States. The Dodd-Frank Act sets forth significant structural and other changes to the regulation of the financial services industry and establishes a new agency, the Consumer Financial Protection Bureau, to regulate consumer financial products and services (including many offered by us and by our customers). In addition, Section 1075 of the Dodd-Frank Act (commonly referred to as the “Durbin Amendment”) imposes new restrictions on card networks and debit card issuers. More specifically, the Durbin Amendment provides that interchange transaction fees that a card issuer may receive or charge for an electronic debit transaction must be “reasonable and proportional” to the cost incurred by the card issuer in processing the transaction.

The Federal Reserve Board adopted the final regulations on June 29, 2011 and added a fraud-prevention adjustment on July 27, 2012. The regulations (a) set a cap on debit transaction interchange fees to $.21 +(5 bps times the value of the transactions) + $.01 (as a fraud adjustment for issuers that have in place policies and measures to address fraud); (b) require that issuers must enable at least two unaffiliated payment card networks on their debit cards without regard to authentication method; and (c) prohibit card issuers and payment card networks from entering into exclusivity arrangements for debit card processing and restrict card issuers and payment networks from inhibiting the ability of merchants to direct the routing of debit card transactions over

13

Table of Contents

Index to Financial Statements

networks of their choice. The Dodd-Frank Act also allows merchants to set minimum dollar amounts (currently, not to exceed $10) for the use of a credit card and provide discounts to consumers who pay with various payment methods, such as cash (which two practices previously violated applicable payment card network rules).

To date, the Durbin Amendment has had mixed implications for our business, but the overall net impact has been positive due to lower interchange costs improving the overall margins of the business. However, we cannot be certain that this trend will continue, and we believe that any future impact (positive or negative) resulting from the Durbin Amendment is uncertain due to the competitive landscape in which we operate. In addition to the Dodd-Frank Act, from time to time, various legislative and regulatory initiatives are introduced in Congress and state legislatures, as well as by regulatory agencies. Such initiatives may include proposals to diminish the powers of bank holding companies and their affiliates. Such legislation could change banking statutes and our operating environment in substantial and unpredictable ways. If enacted, such legislation could increase the cost of doing business or limit permissible activities. We cannot predict whether any such legislation will be enacted, and, if enacted, the effect that it, or any implementing regulations, would have on our financial condition or results of operations.

Other Government Regulations

In addition to oversight by the Federal Reserve Board, our services are subject to a broad range of complex federal, state, Puerto Rico and foreign regulation, including privacy laws, international trade regulations, the Bank Secrecy Act, anti-money laundering laws, the U.S. Internal Revenue Code, the PR Code, the Employee Retirement Income Security Act, the Health Insurance Portability and Accountability Act and other Puerto Rico laws and regulations. Failure of our services to comply with applicable laws and regulations could result in restrictions on our ability to provide such services, as well as the imposition of civil fines and/or criminal penalties. The principal areas of regulation (in addition to oversight by the Federal Reserve Board) that impact our business are described below.

Privacy

We and our financial institution clients are required to comply with various U.S. state, federal and foreign privacy laws and regulations, including those imposed under the Gramm-Leach-Bliley Act and the Health Insurance Portability and Accountability Act. These regulations place restrictions on the use of certain personal information. All financial institutions must disclose detailed privacy policies to their customers and offer them the opportunity to direct the financial institution not to share information with third parties. The regulations, however, permit financial institutions to share information with non-affiliated parties who perform services for the financial institutions. These laws also impose requirements for safeguarding personal information through the issuance of data security standards or guidelines. Certain state laws impose similar privacy obligations, as well as, in certain circumstances, obligations to provide notification to affected individuals, states officers and consumer reporting agencies, as well as businesses and governmental agencies that own data, of security breaches of computer databases that contain personal information. In addition, U.S. state and federal government agencies have been contemplating or developing new initiatives to safeguard privacy and enhance data security. Some foreign privacy laws are stricter than those applicable under U.S. federal, state or Puerto Rican law. As a provider of services to financial institutions, we are required to comply with the privacy regulations and are bound by the same limitations on disclosure of the information received from our customers as apply to the financial institutions themselves. See “Item 1A. Risk Factors—Risks Related to Our Business—Security breaches or our own failure to comply with privacy regulations and industry security requirements imposed on providers of services to financial institutions and card processing services could harm our business by disrupting our delivery of services and damaging our reputation.”

14

Table of Contents

Index to Financial Statements

Anti-Money Laundering and Office of Foreign Assets Control Regulation

Since we provide data processing services to both foreign and domestic financial institutions, we are required to comply with certain anti-money laundering and terrorist financing laws and economic sanctions imposed on designated foreign countries, nationals and others. Specifically, we must adhere to the requirements of the Bank Secrecy Act regarding processing and facilitation of financial transactions. Furthermore, as a data processing company that provides services to foreign parties and facilitates financial transactions between foreign parties, we are obligated to screen transactions for compliance with the sanctions programs administered by the U.S. Department of the Treasury’s Office of Foreign Assets Control (“OFAC”). These regulations prohibit us from entering into or facilitating a transaction that involves persons, governments, or countries designated by the U.S. Government under one or more sanctions regimes.

A major focus of governmental policy in recent years has been aimed at combating money laundering and terrorist financing. Preventing and detecting money laundering, and other related suspicious activities at their earliest stages warrants careful monitoring. The Bank Secrecy Act, along with a number of other anti-money laundering laws, imposes various reporting and record-keeping requirements concerning currency and other types of monetary instruments. Actions, such as structuring transactions to avoid Bank Secrecy Act and anti-money laundering law reporting requirements, failing to prepare or file required reports, preparing inaccurate reports, money laundering, attempted money laundering, and advising customers in any of these activities are violations or potential violations of law. These laws and regulations impose obligations to maintain appropriate policies, procedures and controls to detect, prevent and report money laundering and terrorist financing and to verify the identity of their customers. Failure to maintain and implement adequate programs to combat money laundering and terrorist financing, or to comply with all of the relevant laws or regulations, could have serious legal and reputational consequences for us.

The United States has imposed economic sanctions that affect transactions with designated foreign countries, nationals and others. The OFAC-administered sanctions targeting countries take many different forms. Generally, however, they contain one or more of the following elements: (1) restrictions on trade with or investment in a sanctioned country, including prohibitions against direct or indirect imports of goods or services from and exports to a sanctioned country and prohibitions on “U.S. persons” engaging in financial transactions relating to making investments in, or providing investment-related advice or assistance to, a sanctioned country; and (2) a blocking of assets in which the government or specially designated nationals of the sanctioned country have an interest, by prohibiting transfers of property subject to U.S. jurisdiction (including property in the possession or control of U.S. persons). Blocked assets (e.g., property and bank deposits) cannot be paid out, withdrawn, set off or transferred in any manner without a license from OFAC. Failure to comply with these sanctions could have serious legal and reputational consequences.

Foreign Corrupt Practices Act (“FCPA”) and Other

As a data processing company that services both foreign and domestic clients, our business activities in foreign countries, and in particular our transactions with foreign governmental entities, subject us to the anti-bribery provisions of the FCPA, as well as the laws and regulations of the foreign jurisdiction where we operate. Pursuant to applicable anti-bribery laws, our transactions with foreign government officials and political candidates are subject to certain limitations. Finally, in the course of business with foreign clients and subsidiaries, we export certain software and hardware that is regulated by the Export Administration Regulations from the United States to the foreign parties. Together, these regulations place restrictions on who we can transact with, what transactions may be facilitated, how we may operate in foreign jurisdictions, and what we may export to foreign countries.

15

Table of Contents

Index to Financial Statements

Association and Network Rules

Several of our subsidiaries are registered with or certified by card associations and payment networks, including the ATH network, MasterCard, Visa, American Express, Discover and numerous debit and EBT networks as members or as service providers for member institutions in connection with the services we provide to our customers. As such, we are subject to applicable card association and network rules, which could subject us to a variety of fines or penalties that may be levied by the card associations or networks for certain acts and/or omissions by us, our acquirer customers, processing customers and/or merchants. For example, “EMV” is a credit and debit card authentication methodology that the card associations are mandating to processors, issuers and acquirers in the payment industry. Compliance deadlines for EMV mandates vary by country and by payment network. We have invested significant resources and man-hours to develop and implement this methodology in all our payment related platforms. However, we are not certain if or when our financial institution customers will use or accept the methodology and the time it will take for this technology to be rolled-out to all customer ATM and POS devices connected to our platforms or adopted by our card issuing clients. Non-compliance with EMV mandates could result in lost business or financial losses from fraud or fines from network operators. We are also subject to network operating rules promulgated by the National Automated Clearing House Association relating to payment transactions processed by us using the Automated Clearing House Network and to various government laws regarding such operations, including laws pertaining to EBT.

Geographic Concentration

Our revenue composition by geographical area is based in Latin America and Caribbean. Latin America includes, among others, Costa Rica, México, Guatemala and Panamá. The Caribbean includes Puerto Rico, the Dominican Republic and Virgin Islands, among others. See Note 21 of the Notes to Audited Consolidated Financial Statements included elsewhere in this Annual Report on Form 10-K for additional information related to geographic areas.

Seasonality

Our payment businesses generally experiences increased activity during the traditional holiday shopping periods and around other nationally recognized holidays.

Available Information

EVERTEC’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K and amendments to such reports (if applicable) filed or furnished pursuant to Sections 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) are available free of charge , through our website, http://www.evertecinc.com, as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. In addition, we makes available on our website under the heading of “Corporate Information” our: (i) Code of Ethics; (ii) Code of Ethics for Service Providers; (iii) Corporate Governance Guidelines; (iv) the charters of the Audit, Compensation and Nominating and Corporate Governance committees, and also we intend to disclose any amendments to the Code of Ethics. The aforementioned reports and materials can also be obtained free of charge upon written request or telephoning to the following address or telephone number:

EVERTEC, Inc.

Cupey Center Building

Road, 176, Kilometer 1.3

San Juan, Puerto Rico 00926

(787) 759-9999

16

Table of Contents

Index to Financial Statements

The public may read and copy any materials EVERTEC files with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. In addition, the public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Our filings with the SEC are also available to the public from commercial document retrieval services and at the web site maintained by the SEC at http://www.sec.gov.

Readers should carefully consider, in connection with other information disclosed in this Annual Report on Form 10-K, the risks and uncertainties described below. The following discussion sets forth some of the more important risk factors that could affect our business, financial condition, operating results or cash flow. However, other factors, besides those discussed below or elsewhere in this Report or other of our reports filed with or furnished to the Securities and Exchange Commission (“SEC”), also could adversely affect our business, financial condition, operating results or cash flow. We cannot assure you that the risk factors described below or elsewhere in this document are a complete set of all potential risks we may face; additional risks and uncertainties not presently known to us or not believed by us to be material may also negatively impact us. These risk factors also serve to describe factors which may cause our results to differ materially from those discussed in forward looking statements included herein or in other documents or statements that make reference to this Annual Report on Form 10-K. Please also refer to the section titled “Forward Looking Statements” in this Annual Report on Form 10-K.

Risks Related to Our Business

We expect to continue to derive a significant portion of our revenue from Popular.

Our services to Popular account for a significant portion of our revenues, and we expect that our services to Popular will continue to represent a significant portion of our revenues for the foreseeable future. In 2014, products and services billed through Popular accounted for approximately 45% of our total revenues, of which approximately 83% (or approximately 37% of total revenues) are derived from core bank processing and related services for Popular and approximately 17% (or approximately 8% of total revenues) are transaction processing activities driven by third parties. If Popular were to terminate, or fail to perform under, the Master Services Agreement or our other material agreements with Popular, our revenues could be significantly reduced.

We depend, in part, on our merchant relationships and our alliance with Banco Popular, a wholly-owned subsidiary of Popular, to grow our merchant acquiring business. If we are unable to maintain these relationships and this alliance, our business may be adversely affected.

Growth in our merchant acquiring business is derived primarily from acquiring new merchant relationships, new and enhanced product and service offerings, cross selling products and services into existing relationships, the shift of consumer spending to increased usage of electronic forms of payment, and the strength of our relationship with Banco Popular. A substantial portion of our business is generated from our ISO Agreement with Banco Popular.

Banco Popular acts as a merchant referral source and provides sponsorship into the ATH, Visa, Discover and MasterCard networks for merchants, as well as card association sponsorship, clearing and settlement services. We provide transaction processing and related functions. Both alliance partners may provide management, sales, marketing, and other administrative services. We rely on the continuing growth of our merchant relationships, our alliance with Banco Popular and other distribution channels. There can be no guarantee that this growth will continue and the loss or deterioration of these relationships could negatively impact our business and result in a reduction of our revenue and profit.

17

Table of Contents

Index to Financial Statements

If we are unable to renew client contracts at favorable terms, we could lose clients and our results of operations and financial condition may be adversely affected.

Failure to achieve favorable renewals of client contracts could negatively impact our business. Our contracts with private clients generally run for a period of one to five years, except for the Master Services Agreement with Popular, which has a term of 15 years, and provide for termination fees upon early termination. Our government contracts generally run for one year without automatic renewal periods due to requirements of the government procurement rules. Our standard merchant contract has an initial term of one or three years, with automatic one-year renewal periods. At the end of the contract term, clients have the opportunity to renegotiate their contracts with us and to consider whether to engage one of our competitors to provide products and services. If we are not successful in achieving high renewal rates and contract terms that are favorable to us, our results of operations and financial condition may be adversely affected.

Our substantial leverage could adversely affect our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or our industry, expose us to interest rate risk to the extent of our variable rate debt and prevent us from meeting our obligations under our notes and senior secured credit facilities.

We are highly leveraged. As of December 31, 2014, the total principal amount of our indebtedness was approximately $700 million. Our high degree of leverage could have important consequences for you, including:

| • | increasing our vulnerability to adverse economic, industry or competitive developments; |

| • | requiring a substantial portion of cash flow from operations to be dedicated to the payment of principal and interest on our indebtedness, therefore reducing our ability to use our cash flow for other purposes, including for our operations, capital expenditures and future business opportunities; |

| • | exposing us to the risk of increased interest rates because our borrowings are at variable rates of interest; |

| • | making it more difficult for us to satisfy our obligations with respect to our indebtedness, and any failure to comply with the obligations of any of our other debt instruments, including restrictive covenants and borrowing conditions, could result in an event of default under the agreements governing such other indebtedness; |

| • | restricting us from making strategic acquisitions or causing us to make non-strategic divestitures; |

| • | limiting our ability to obtain additional debt or equity financing for working capital, capital expenditures, business development, debt service requirements, acquisitions and general corporate or other purposes; and |

| • | limiting our flexibility in planning for, or reacting to, changes in our business or market conditions and placing us at a competitive disadvantage compared to our competitors who are less highly leveraged and who therefore, may be able to take advantage of opportunities that our leverage prevents us from exploiting. |

For the year ended December 31, 2014, our cash interest expense on the senior secured credit facilities amounted to $22.4 million. Our interest expense could increase if interest rates increase because the entire amount of the indebtedness under the senior secured credit facilities bears interest at a variable rate. At December 31, 2014, we had approximately $695 million aggregate principal amount of variable rate indebtedness under the senior secured credit facilities. A 100 basis point increase in interest rates over our floor(s) on our debt balances outstanding as of December 31, 2014 under the senior secured credit facilities would increase our annual interest expense by approximately $6.9 million.

18

Table of Contents

Index to Financial Statements

We rely on our systems, employees and certain counterparties, and certain failures could materially adversely affect our operations.

Our businesses are dependent on our ability to process, record and monitor a large number of transactions. If any of our financial, accounting, or other data processing systems or applications fail or have other significant shortcomings or limitations, we could be materially adversely affected. We are similarly dependent on our employees. We could be materially adversely affected if one of our employees causes a significant operational breakdown or failure, either as a result of human error or where an individual purposefully sabotages or fraudulently manipulates our operations or systems. Third parties with which we do business could also be sources of operational risk to us, including relating to breakdowns or failures of such parties’ own systems or employees. Any of these occurrences could diminish our ability to operate one or more of our businesses, or result in potential liability to clients, reputational damage and regulatory intervention, any of which could materially adversely affect us.

We may be subject to disruptions of our operating systems arising from events that are wholly or partially beyond our control, which may include, for example, computer viruses or electrical or telecommunications outages, natural disasters, disease pandemics or other unanticipated damage to property or physical assets. Such disruptions may give rise to losses in service to customers and loss or liability to us. In addition, there is the risk that our controls and procedures as well as business continuity and data security systems prove to be inadequate. Any such failure could affect our operations and could materially adversely affect our results of operations by requiring us to expend significant resources to correct the defect, as well as by exposing us to litigation, regulatory fines or penalties or losses not covered by insurance.