Attached files

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

___________________________________

FORM 10-K

___________________________________

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2014

Commission File Number 001-35761

United Insurance Holdings Corp.

Delaware | 75-3241967 | |||

(State of Incorporation) | (IRS Employer Identification Number) | |||

360 Central Avenue, Suite 900

St. Petersburg, Florida 33701

727-895-7737

Securities registered pursuant to Section 12(b) of the Act: | ||||

COMMON STOCK, $0.0001 PAR VALUE PER SHARE | NASDAQ Stock Market LLC | |||

Securities registered pursuant to Section 12(g) of the Act: | ||||

PREFERRED SHARE PURCHASE RIGHTS | ||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes £ No R

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes £ No R

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes R No £

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes R No £

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | £ | Accelerated filer | þ | |

Non-accelerated filer | £ | Smaller reporting company | £ | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes £ No R

Non-affiliates held common stock issued by the registrant with an aggregate market value of $286,999,712 as of June 30, 2014, calculated using the closing sales price reported for such date on the NASDAQ Stock Market. For purposes of this disclosure, shares of common stock held by persons who hold more than 10% of the outstanding shares of common stock and shares held by executive officers and directors of the registrant have been excluded because such persons may be deemed to be affiliates. This determination of executive officer or affiliate status is not necessarily a conclusive determination for other purposes.

As of February 25, 2015, 21,473,534 shares of common stock, par value $0.0001 per share, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Form 10-K incorporates by reference certain information from the Proxy Statement for the 2015 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission within 120 days after the end of our fiscal year ended December 31, 2014.

UNITED INSURANCE HOLDINGS CORP.

Forward-Looking Statements | ||

Item 1. Business | ||

Item 1A. Risk Factors | ||

Item 1B. Unresolved Staff Comments | ||

Item 2. Properties | ||

Item 3. Legal Proceedings | ||

Item 4. Mine Safety Disclosures | ||

Part II. | ||

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | ||

Item 6. Selected Financial Data | ||

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations | ||

Item 7A. Quantitative and Qualitative Disclosures about Market Risk | ||

Item 8. Financial Statements and Supplementary Data | ||

Auditor's Report | ||

Consolidated Balance Sheets | ||

Consolidated Statements of Comprehensive Income | ||

Consolidated Statements of Stockholders' Equity | ||

Consolidated Statements of Cash Flows | ||

Notes to Consolidated Financial Statements | ||

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | ||

Item 9A. Controls and Procedures | ||

Item 9B. Other Information | ||

Part III. | ||

Item 10. Directors, Executive Officers and Corporate Governance | ||

Item 11. Executive Compensation | ||

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | ||

Item 13. Certain Relationships and Related Transactions, and Director Independence | ||

Item 14. Principal Accounting Fees and Services | ||

Part IV. | ||

Item 15. Exhibits, Financial Statement Schedules | ||

Exhibit Index | ||

Signatures | ||

Throughout this Annual Report on Form 10-K (Annual Report), we present amounts in all tables in thousands, except for share amounts, per share amounts, policy counts or where more specific language or context indicates a different presentation. In the narrative sections of this Annual Report, we show full values rounded to the nearest thousand.

2

UNITED INSURANCE HOLDINGS CORP.

FORWARD-LOOKING STATEMENTS

Statements in this Form 10-K for the year ended December 31, 2014 or in documents incorporated by reference that are not historical fact are “forward-looking statements” within the meaning of the Private Securities Reform Litigation Act of 1995. These forward-looking statements include statements about anticipated growth in revenues, earnings per share, estimated unpaid losses on insurance policies, investment returns and expectations about our liquidity. These statements are based on current expectations, estimates and projections about the industry and market in which we operate, and management’s beliefs and assumptions. Without limiting the generality of the foregoing, words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “could,” “would,” “estimate,” or “continue” or the negative variations thereof or comparable terminology are intended to identify forward-looking statements. Forward-looking statements are not guarantees of future performance and involve certain known and unknown risks and uncertainties that could cause actual results to differ materially from those expressed or implied by such statements. The risks and uncertainties include, without limitation:

• | the regulatory, economic and weather conditions present in the states in which we operate; |

• | the impact of new federal or state regulations that affect the property and casualty insurance market; |

• | the cost of reinsurance; |

• | assessments charged by various governmental agencies; |

• | pricing competition and other initiatives by competitors; |

• | our ability to attract and retain the services of senior management; |

• | the outcome of litigation pending against us, including the terms of any settlements; |

• | dependence on investment income and the composition of our investment portfolio and related market risks; |

• | our exposure to catastrophic events and severe weather conditions; |

• | downgrades in our financial strength ratings; and |

• | other risks and uncertainties described under "Risk Factors" below. |

We caution you to not place reliance on these forward-looking statements, which are valid only as of the date they were made. We undertake no obligation to update or revise any forward-looking statements to reflect new information or the occurrence of unanticipated events or otherwise. In addition, we prepare our financial statements in accordance with U.S. generally accepted accounting principles (GAAP), which prescribes when we may reserve for particular risks, including litigation exposures. Accordingly, our results for a given reporting period could be significantly affected if and when we establish a reserve for a major contingency. Therefore, the results we report in certain accounting periods may appear to be volatile.

These forward-looking statements are subject to numerous risks, uncertainties and assumptions about us described in our filings with the SEC. The forward-looking events that we discuss in this Form 10-K are valid only as of the date of this Form 10-K and may not occur in light of the risks, uncertainties and assumptions that we describe in our filings with the SEC. A detailed discussion of these and other risks and uncertainties that could cause actual results and events to differ materially from our forward-looking statements is included in the section entitled “RISK FACTORS” in Part I, Item 1A of this Form 10-K. Except as required by applicable law, we undertake no obligation and disclaim any obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

3

UNITED INSURANCE HOLDINGS CORP.

PART I

Item 1. Business

INTRODUCTION

Company Overview

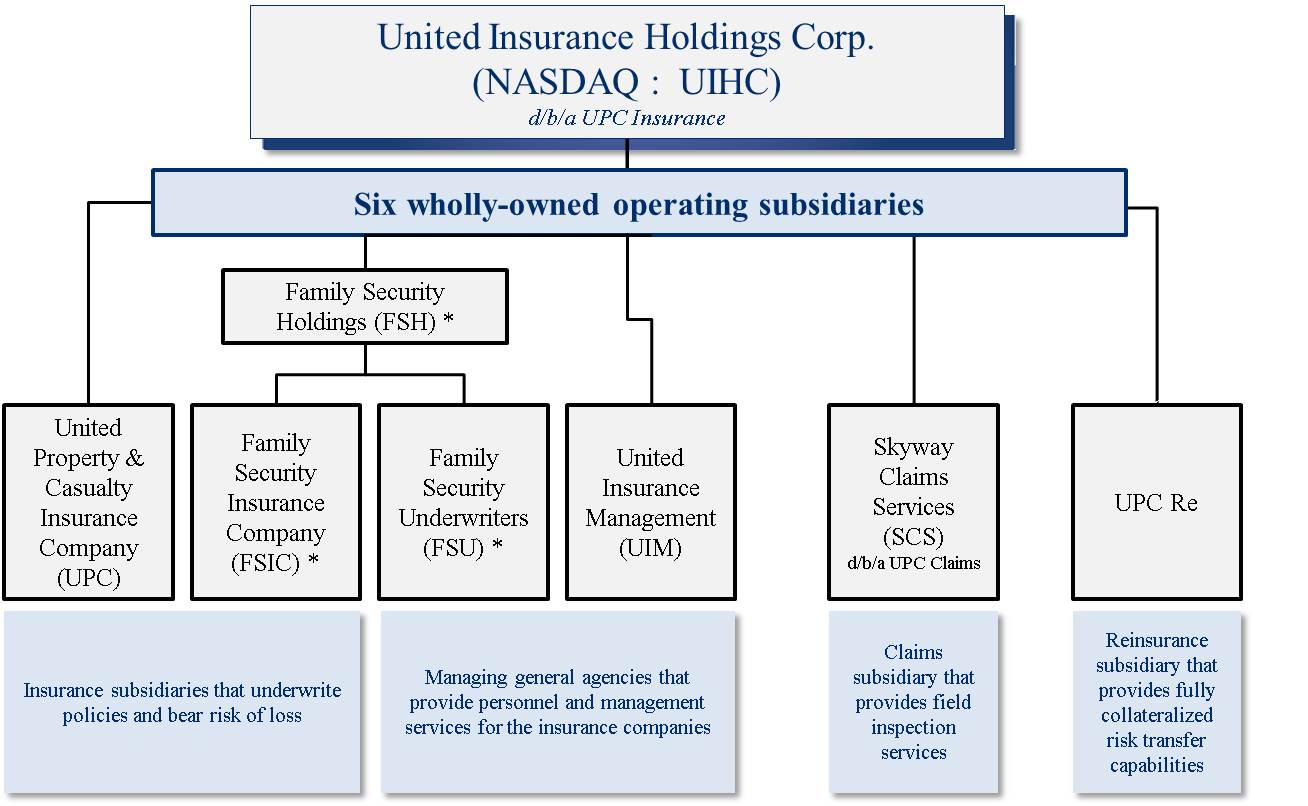

United Insurance Holdings Corp. serves as the holding company for United Property & Casualty Insurance Company and its affiliated companies (referred to in this document as we, our, us, the Company and UPC Insurance). We conduct our business principally through the six wholly-owned operating subsidiaries shown below. Collectively, including United Insurance Holdings Corp., we refer to these entities as “UPC Insurance,” which is the preferred brand identification we are establishing for our Company.

* FSH, FSIC and FSU were not part of our corporate structure as of December 31, 2014.

UPC Insurance is primarily engaged in the residential property and casualty insurance business in the United States. We currently write in Florida, Louisiana, Massachusetts, New Jersey, North Carolina, Rhode Island, South Carolina, and Texas, and we are licensed to write in Alabama, Connecticut, Delaware, Georgia, Hawaii, Maryland, Mississippi, New Hampshire, New York and Virginia. Our target market currently consists of areas where the perceived threat of natural catastrophe has caused large national insurance carriers to reduce their concentration of policies. In such areas we believe an opportunity exists for UPC Insurance to write profitable business. We manage our risk of catastrophic loss primarily through sophisticated pricing algorithms, avoidance of policy concentration, and the use of a comprehensive catastrophe reinsurance program. UPC Insurance has been operating continuously in Florida since 1999, and has successfully managed its business through various hurricanes, tropical storms, and other weather related events. We believe our record of successful risk management and experience in writing business in catastrophe-exposed areas provides us a competitive advantage as we grow our business in other states facing similar perceived threats.

We conduct our operations under one business segment.

4

UNITED INSURANCE HOLDINGS CORP.

To achieve our goals in 2015, UPC Insurance seeks to:

• | Grow premium base in existing states; |

• | Begin writing policies in several new states in support of our growth and diversification strategy; |

• | Expand our product offerings in states outside Florida; |

• | Grow commercial residential property writings in Florida; |

• | Utilize and add strategic partnerships to expand distribution and service capabilities in all states; |

• | Improve the efficiency of our catastrophe reinsurance program; and |

• | Leverage investments in technology and analytics to drive profitability. |

Corporate Information

In 1999, we formed our original holding company, United Insurance Holdings, L.C., a Florida limited liability company, our original insurance affiliate - United Property & Casualty Insurance Company, and our original management affiliate - United Insurance Management, and conducted operations under that structure until 2004. In 2004, we added our claims adjusting affiliate - Skyway Claims Services, and continued operations under the new structure until we completed a merger with Fund Management Group (FMG) Acquisition Corp.

In May 2007, FMG Acquisition Corp, a blank-check company, was incorporated under the laws of Delaware. In September 2008, in a cash and stock transaction, we completed a reverse merger whereby United Subsidiary Corp., a wholly-owned subsidiary of FMG Acquisition Corp., merged with and into United Insurance Holdings, L.C., a Florida limited liability company, with United Insurance Holdings, L.C. remaining as the surviving entity. In connection with that merger, FMG Acquisition Corp. changed its name to United Insurance Holdings Corp. and became a public operating company trading in the over-the-counter market under the ticker symbol "UIHC". In April 2011, we founded our reinsurance affiliate - UPC Re. In December 2012, in connection with an underwritten public offering of 5,000,000 shares of our common stock, we applied to list our common stock on The Nasdaq Capital Market (NASDAQ). Our application was approved, and our common stock began trading on NASDAQ on December 11, 2012.

Our principal executive offices are located at 360 Central Avenue, Suite 900, St. Petersburg, FL 33701 and our telephone number at that location is (727) 895-7737.

Recent Events

On February 5, 2015, our Board of Directors declared a $0.05 per share quarterly cash dividend payable on March 6, 2015, to stockholders of record on February 27, 2015.

On February 3, 2015, we acquired Family Security Holdings, LLC (FSH), and its two wholly-owned subsidiaries via merger. In connection with the closing of the merger, the holders of FSH membership interests were issued 503,883 shares of our common stock. In addition to the foregoing, FSH members will receive three percent (3%) of all gross premiums written during the twelve-month period following the closing on the renewal of FSIC policies in-force as of the closing date. Such contingent consideration, if any, will be paid to FSH members approximately 30 days following the anniversary of the closing date in the form of additional shares of our common stock. The number of shares to be issued will be based on the average closing price of our common stock over the 180-day period preceding the payment date.

On January 9, 2015, we assumed more than 30 commercial residential policies from Citizens Property Insurance Corporation (Citizens), representing approximately $1,200,000 of annualized premiums. The total amount of assumed premium may be reduced by additional opt outs and cancellations by policyholders.

On January 9, 2015, we filed a shelf registration statement on Form S-3 (Reg. No. 333-201425), which enables us to offer, issue and sell up to an aggregate of $75,000,000 of our common stock, preferred stock, debt securities, warrants, stock purchase contracts and/or units.

On December 9, 2014, we assumed more than 50 commercial residential policies from Citizens, representing approximately $1,350,000 of annualized premiums. The total amount of assumed premium may be reduced by additional opt outs and cancellations by policyholders.

5

UNITED INSURANCE HOLDINGS CORP.

On November 18, 2014, we assumed more than 25,000 homeowners and fire policies from Citizens, representing approximately $45,851,000 of annualized premiums. The total amount of assumed premium may be reduced by additional opt outs and cancellations by policyholders.

On November 5, 2014, we assumed more than 50 commercial residential policies from Citizens, representing approximately $2,375,000 of annualized premiums. The total amount of assumed premium may be reduced by additional opt outs and cancellations by policyholders.

PRODUCTS AND DISTRIBUTION

Homeowners policies and related coverage account for the vast majority of the business that we write. In 2014, homeowners policies (by which we mean both standard homeowners and dwelling fire policies) produced written premium of $418,071,000 and accounted for 96% of our total written premium. In addition to homeowners policies, we write flood policies, which accounted for 3%, and commercial residential policies, which accounted for the remaining 1% of our 2014 written premium. In 2013, homeowners policies accounted for 96% of our total written premium, while flood policies accounted for the majority of the remaining 4%. In 2012, homeowners policies accounted for 95% and flood accounted for 5% of our total written premium. On our flood policies, we earn a commission while retaining no risk of loss, since all such risk is ceded to the federal government via the National Flood Insurance Program. Policies we issue under our homeowners programs in the various states where we do business provide structure, content and liability coverage. We offer standardized policies for a broad range of exposures, and our policies include coverage options for standard single-family homeowners, tenants (renters), and condominium unit owners.

We have developed a unique and proprietary homeowners product we refer to as "UPC 1.0". This new product uses a granular approach to pricing for catastrophe perils. Our objective is to create specific geographic areas such that within each territory or "catastrophe band" the expected losses are within a specified range of error or approximation from a central estimate. These areas may have millions of data points that help us create distance-to-coast factors that provide a sophisticated market segmentation that is highly correlated to our risk exposure and reinsurance costs. UPC 1.0 has been filed and approved for use in South Carolina and we plan to file it for use in all our states.

We currently market and distribute our policies to consumers through over 4,000 independent agencies. United Property & Casualty Insurance Company has been focused on the independent agency distribution channel since its inception, and we believe we have built significant credibility and loyalty with the independent agent community in the states in which we operate. In 2011, we became a Trusted Choice partner company. Trusted Choice is a group of unaffiliated independent agents around the country that seek to maintain the highest levels of service quality and product offerings to consumers. United Property & Casualty Insurance Company is one of 70 insurance companies nationwide that have qualified to be Trusted Choice partner companies. We recruit, train and appoint the full-service insurance agencies that distribute our products. Typically, a full service agency is small to medium in size and represents several insurance companies for both personal and commercial product lines. We depend heavily upon our independent agents to produce new business for us. We compensate our independent agents primarily with fixed-rate commissions that are consistent with market practices. In addition to our relationships with individual agencies, we have important relationships with aggregators of underlying agency demand. The two most significant of these relationships are with Allstate in Florida, which, through its Ivantage program, refers homeowners to United Property & Casualty Insurance Company and other partner companies, and with the Florida Association of Insurance Agents (FAIA), which serves as a conduit between United Property & Casualty Insurance Company and many smaller agencies in Florida with whom we do not have direct appointments.

Our sales representatives monitor and support our agents and also have the principal responsibility for recruiting and training our new agents. We manage our independent agents through periodic business reviews using established benchmarks/goals for premium volume and profitability.

6

UNITED INSURANCE HOLDINGS CORP.

COMPETITION

The market for personal and commercial residential property insurance is highly competitive. In our primary market, Florida, there are over 165 licensed insurance companies that write homeowners' policies. The table below shows year-to-date in-force premium volume and market share for the top 20 companies in Florida as of September 30, 2014, which is the most recent date that the information is publicly available. We compete to varying degrees with all of these companies and others, including large national carriers, Citizens Property Insurance Corporation, the Florida state-sponsored homeowners insurance entity, and single state or regional carriers. Similar competitive groups exist in our other geographic markets.

Florida Property Insurance Market - Personal and Commercial Residential - Ranked by DWP* | ||||||||||||||

Company Name | Policies in-Force | Exposure | Direct Written Premium in-Force | Percentage Distribution | ||||||||||

Citizens Property Insurance Corporation | 910,154 | $ | 269,927,439 | $ | 2,046,715 | 19.1 | % | |||||||

Universal Property & Casualty Insurance Company | 500,503 | 109,414,644 | 747,956 | 7.0 | % | |||||||||

Homeowners Choice Property & Casualty Insurance Company, Inc. | 147,737 | 39,960,506 | 349,465 | 3.3 | % | |||||||||

Florida Peninsula Insurance Company | 134,584 | 47,385,408 | 316,874 | 3.0 | % | |||||||||

American Coastal Insurance Company | 4,294 | 45,922,226 | 311,891 | 2.9 | % | |||||||||

Federated National Insurance Company | 167,597 | 69,950,824 | 311,667 | 2.9 | % | |||||||||

Heritage Property & Casualty Insurance Company | 173,512 | 51,067,683 | 302,065 | 2.8 | % | |||||||||

United Property & Casualty Insurance Company | 156,696 | 62,622,700 | 301,014 | 2.8 | % | |||||||||

United Services Automobile Association | 124,834 | 50,696,614 | 296,723 | 2.8 | % | |||||||||

St. Johns Insurance Company, Inc. | 173,166 | 64,898,779 | 284,299 | 2.7 | % | |||||||||

People's Trust Insurance Company | 132,790 | 37,356,380 | 266,234 | 2.5 | % | |||||||||

American Integrity Insurance Company of Florida | 192,131 | 58,339,677 | 236,957 | 2.2 | % | |||||||||

Security First Insurance Company | 192,058 | 51,891,500 | 236,901 | 2.2 | % | |||||||||

Tower Hill Prime Insurance Company | 139,242 | 53,691,890 | 228,924 | 2.1 | % | |||||||||

First Community Insurance Company | 33,800 | 6,958,296 | 212,328 | 2.0 | % | |||||||||

Federal Insurance Company | 31,977 | 48,968,272 | 176,966 | 1.6 | % | |||||||||

Tower Hill Signature Insurance Company | 98,566 | 30,301,767 | 168,709 | 1.6 | % | |||||||||

USAA Casualty Insurance Company | 53,942 | 19,188,617 | 147,942 | 1.4 | % | |||||||||

Tower Hill Preferred Insurance Company | 67,530 | 26,514,589 | 139,070 | 1.3 | % | |||||||||

AIG Property Casualty Company | 13,764 | 40,097,514 | 139,027 | 1.3 | % | |||||||||

Total - Top 20 Insurers | 3,448,877 | 1,185,155,325 | 7,221,727 | 67.5 | % | |||||||||

Total - All Insurers | 5,797,120 | $ | 1,892,065,499 | $ | 10,714,561 | 100.0 | % | |||||||

*The information displayed in the table above is compiled and published by the Florida Office of Insurance Regulation as of September 30, 2014 based on information filings submitted quarterly by all Florida licensed insurance companies. The information above is presented for each individual company and is not consolidated or aggregated.

We compete primarily on the basis of product features, the strength of our distribution network, high-quality service to our agents and policyholders, and our reputation for long-term financial stability and commitment. Our long and successful track record writing homeowners insurance in catastrophe-exposed areas has enabled us to develop sophisticated pricing techniques that endeavor to accurately reflect the risk of loss while allowing us to be competitive in our target markets. This pricing segmentation approach allows us to offer products in areas that have a high demand for property insurance yet are underserved by the national carriers.

We price our product at levels that we project will generate an acceptable underwriting profit. We try to be extremely granular in our approach, so that our price can accurately reflect the risk and profitability of each potential customer. In our pricing algorithm, we consider credit scores (where allowable) and historical attritional loss costs for the rating territory in which the customer resides, as well as projected reinsurance costs based on the specific geographic and structural characteristics of the home. In addition to the specific characteristics of the policy being priced, we also evaluate the reinsurance cost of each incremental policy on our portfolio as a whole. In this regard, we seek to optimize our portfolio by diversifying our geographic exposure in order to limit our probable maximum loss, total insured value and average annual loss.

7

UNITED INSURANCE HOLDINGS CORP.

We use the output from third-party modeling software to analyze our risk exposures, including wind exposures, by zip code or street address as part of the optimization process.

We establish underwriting guidelines to provide a uniform approach to our risk selection and to achieve underwriting profitability. Our underwriters review the property inspection report during their risk evaluation and if the policy does not meet our underwriting criteria, we have the right to cancel the policy within 90 days in Florida and within 60 days in other states.

We strive to provide excellent service to our independent agents and our policyholders. We continue to enhance our web-based systems which allow our agents to prepare and process new policies and policy changes online and deliver policy declarations quickly. We work with a select group of third party vendors to develop, manage and maintain our information technology systems. This allows us to obtain up-to-date technology at a reasonable cost and to achieve economies of scale without incurring significant fixed-overhead expenses. As agent and consumer behaviors evolve we continue to enhance our technology platforms to offer solutions that meet their needs.

GEOGRAPHIC MARKETS

United Property & Casualty Insurance Company began operations in Florida in 1999, and has operated continuously there since that time. In 2010, we began to expand to other states, beginning with South Carolina in 2010, Massachusetts in 2011 and Rhode Island in 2012. In 2013, we began writing business in North Carolina, New Jersey and Texas, and in 2014 we wrote our first policies in Louisiana. Our insurance affiliates are also licensed to write, but have not commenced writing business in Alabama, Connecticut, Delaware, Georgia, Hawaii, Maryland, Mississippi, New Hampshire, New York and Virginia. It is a fundamental part of our strategy to diversify our operations outside of Florida and to write in multiple states where the perceived threat of natural catastrophes has caused large national insurance companies to reduce their concentration.

The table below shows the geographic distribution of our 252,104 policies in-force as of December 31, 2014, and 202,454 policies in-force as of December 31, 2013.

Policies In-Force By State | 2014 Policies | % | 2013 Policies | % | ||||||||

Florida | 173,630 | 69.0 | % | 163,314 | 80.6 | % | ||||||

Massachusetts | 20,463 | 8.1 | % | 10,900 | 5.4 | % | ||||||

South Carolina | 19,492 | 7.7 | % | 15,186 | 7.5 | % | ||||||

Rhode Island | 14,387 | 5.7 | % | 9,990 | 4.9 | % | ||||||

North Carolina | 11,314 | 4.5 | % | 2,533 | 1.3 | % | ||||||

Texas | 8,927 | 3.5 | % | 102 | 0.1 | % | ||||||

New Jersey | 3,881 | 1.5 | % | 429 | 0.2 | % | ||||||

Louisiana | 10 | — | % | — | — | % | ||||||

Total | 252,104 | 100.0 | % | 202,454 | 100.0 | % | ||||||

8

UNITED INSURANCE HOLDINGS CORP.

As of December 31, 2014, our total insured value of all polices in-force was approximately $115,244,742,000, an increase of $24,382,381,000, or 26.8%, from the same date in 2013. We have approximately 60.9% of our total insured value in Florida compared to roughly 74.3% as of December 31, 2013. The following table provides evidence of our improving geographic diversification by illustrating the breakdown of total insured value:

Total Insured Value By State | 2014 TIV | % | 2013 TIV | % | ||||||||

Florida | 70,200,560 | 60.9 | % | 67,499,187 | 74.3 | % | ||||||

Massachusetts | 14,830,428 | 12.9 | 7,604,145 | 8.4 | ||||||||

South Carolina | 10,096,269 | 8.8 | 8,018,613 | 8.8 | ||||||||

Rhode Island | 8,920,721 | 7.7 | 6,300,783 | 6.9 | ||||||||

North Carolina | 4,952,372 | 4.3 | 1,138,785 | 1.3 | ||||||||

Texas | 4,085,220 | 3.5 | 42,243 | — | ||||||||

New Jersey | 2,154,756 | 1.9 | 258,605 | 0.3 | ||||||||

Louisiana | 4,416 | — | — | — | ||||||||

Total | 115,244,742 | 100.0 | % | 90,862,361 | 100.0 | % | ||||||

9

UNITED INSURANCE HOLDINGS CORP.

RESERVE FOR UNPAID LOSSES

We generally use the term loss(es) to collectively refer to both loss and loss adjusting expenses. We establish reserves for both reported and unreported unpaid losses that have occurred at or before the balance sheet date for amounts we estimate we will be required to pay in the future. Our policy is to establish these loss reserves after considering all information known to us at each reporting period. At any given point in time, our loss reserve represents our best estimate of the ultimate settlement and administration cost of our insured claims incurred and unpaid. Since the process of estimating loss reserves requires significant judgment due to a number of variables, such as fluctuations in inflation, judicial decisions, legislative changes and changes in claims handling procedures, our ultimate liability will likely differ from these estimates. We revise our reserve for unpaid losses as additional information becomes available, and reflect adjustments, if any, in our earnings in the periods in which we determine the adjustments are necessary.

Reserves for unpaid losses fall into two categories: case reserves and reserves for claims incurred but not reported. See our APPLICATION OF CRITICAL ACCOUNTING ESTIMATES section under Item 7 of this Annual Report for a discussion of these two categories of reserves for unpaid losses and for a discussion of the methods we use to estimate those reserves.

On an annual basis, our consulting actuary issues a statement of actuarial opinion that documents the actuary’s evaluation of the adequacy of our unpaid loss obligations under the terms of our policies. We review the analysis underlying the actuary's opinion and compare the projected ultimate losses per the actuary's analysis to our own projection of ultimate losses to ensure that our reserve for unpaid losses recorded at each annual balance sheet date is based upon our analysis of all internal and external factors related to known and unknown claims against us and to ensure our reserve is within guidelines promulgated by the National Association of Insurance Commissioners (NAIC).

We maintain an in-house claims staff that monitors and directs all aspects of our claims process. We assign the fieldwork to our wholly-owned claims subsidiary, or to third-party claims adjusting companies, none of whom have the authority to settle or pay any claims on our behalf. The claims adjusting companies conduct inspections of the damaged property and prepare initial estimates. We review the inspection reports and initial estimates to determine the amounts to be paid to the policyholder in accordance with the terms and conditions of the policy in effect at the time that the policyholder incurs the loss. We maintain strategic relationships with multiple claims adjusting companies that we can engage should we need additional non-catastrophe claims servicing capacity. We believe the combination of our internal resources and relationships with external claims servicing providers provide an adequate level of claims servicing in the event catastrophes affect our policyholders.

10

UNITED INSURANCE HOLDINGS CORP.

The table below shows the analysis of our reserve for unpaid losses for each of our last three fiscal years on a GAAP basis:

2014 | 2013 | 2012 | |||||||||

Balance at January 1 | $ | 47,451 | $ | 35,692 | $ | 33,600 | |||||

Less: reinsurance recoverable on unpaid losses | 1,957 | 1,935 | 3,318 | ||||||||

Net balance at January 1 | $ | 45,494 | $ | 33,757 | $ | 30,282 | |||||

Incurred related to: | |||||||||||

Current year | 122,114 | 94,752 | 57,739 | ||||||||

Prior years | (4,037 | ) | 4,078 | 670 | |||||||

Total incurred | $ | 118,077 | $ | 98,830 | $ | 58,409 | |||||

Paid related to: | |||||||||||

Current year | 83,967 | 62,494 | 37,906 | ||||||||

Prior years | 26,420 | 24,599 | 17,028 | ||||||||

Total paid | $ | 110,387 | $ | 87,093 | $ | 54,934 | |||||

Net balance at December 31 | $ | 53,184 | $ | 45,494 | $ | 33,757 | |||||

Plus: reinsurance recoverable on unpaid losses | 1,252 | 1,957 | 1,935 | ||||||||

Balance at December 31 | $ | 54,436 | $ | 47,451 | $ | 35,692 | |||||

Composition of reserve for unpaid losses and LAE: | |||||||||||

Case reserves | 29,726 | 28,054 | 20,438 | ||||||||

IBNR reserves | 24,710 | 19,397 | 15,254 | ||||||||

Balance at December 31 | $ | 54,436 | $ | 47,451 | $ | 35,692 | |||||

11

UNITED INSURANCE HOLDINGS CORP.

LOSS RESERVE DEVELOPMENT

The table on the next page displays UPC Insurance's loss reserve development, on a GAAP basis, for business written in each year from 2004 through 2014; it does not distinguish between catastrophe and attritional losses. The following explanations of the main sections of the table should provide a better understanding of the information displayed:

Original net liability. The original net liability represents the original estimated amount of reserves for unpaid losses recorded at the balance sheet date for each of the years indicated in the column headings, net of reinsured losses. We record reserves related to claims arising in the current year and in all prior years that remained unpaid at the balance sheet date for each of the years indicated, including estimated losses that had been incurred but not reported.

Net cumulative paid as of. This section displays the net cumulative payments we have made for losses, as of the balance sheet date of each succeeding year, related to claims incurred prior to the balance sheet date of the year indicated in the column heading.

Net liability re-estimated as of. This section displays the re-estimated amount of the previously recorded liability based on experience as of the end of each succeeding year. An increase or decrease from the original reserve estimate is caused by a combination of factors, including (i) claims being settled for amounts different than originally estimated, (ii) reserves being increased or decreased for claims remaining open as more information becomes available on those individual claims and (iii) more or fewer claims being reported after the year end than estimated.

Cumulative redundancy (deficiency) at December 31, 2014. The cumulative redundancy or deficiency results from the comparison of the net liability re-estimated as of the current balance sheet date to the original net liability, and it indicates an overestimation of the original net liability (a redundancy) or an underestimation of the original net liability (a deficiency).

It is important to note that the table presents a run-off of balance sheet liability for the periods indicated rather than accident or policy loss development for those periods. Therefore, each amount in the table includes the cumulative effects of changes in liability for all prior periods. Conditions and trends that have affected liabilities in the past may not necessarily occur in the future.

12

UNITED INSURANCE HOLDINGS CORP.

2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2005 | 2004 | ||||||||||||||||||||||||||||||||||

Original net liability | $ | 53,184 | $ | 45,494 | $ | 33,757 | $ | 30,282 | $ | 23,600 | $ | 20,665 | $ | 19,192 | $ | 21,559 | $ | 23,735 | $ | 20,447 | $ | 8,449 | ||||||||||||||||||||||

Net cumulative paid as of: | ||||||||||||||||||||||||||||||||||||||||||||

One year later | 26,240 | 24,599 | 17,028 | 3,322 | 12,533 | 8,984 | 9,707 | 9,047 | 12,872 | 10,962 | ||||||||||||||||||||||||||||||||||

Two years later | 32,622 | 26,889 | 10,562 | 7,409 | 13,148 | 12,127 | 13,083 | 14,363 | 13,871 | |||||||||||||||||||||||||||||||||||

Three years later | 30,929 | 16,776 | 12,444 | 6,030 | 14,310 | 14,115 | 15,582 | 14,868 | ||||||||||||||||||||||||||||||||||||

Four years later | 18,382 | 16,369 | 10,145 | 6,113 | 15,395 | 16,312 | 15,021 | |||||||||||||||||||||||||||||||||||||

Five years later | 17,556 | 13,441 | 9,552 | 7,032 | 17,356 | 15,214 | ||||||||||||||||||||||||||||||||||||||

Six years later | 14,403 | 11,649 | 10,264 | 8,722 | 15,291 | |||||||||||||||||||||||||||||||||||||||

Seven years later | 12,543 | 12,219 | 11,787 | 15,322 | ||||||||||||||||||||||||||||||||||||||||

Eight years later | 13,067 | 13,605 | 15,353 | |||||||||||||||||||||||||||||||||||||||||

Nine years later | 14,426 | 15,361 | ||||||||||||||||||||||||||||||||||||||||||

Ten years later | 15,361 | |||||||||||||||||||||||||||||||||||||||||||

Net liability re-estimated as of: | ||||||||||||||||||||||||||||||||||||||||||||

End of year | $ | 53,184 | $ | 45,494 | $ | 33,757 | $ | 30,282 | $ | 23,600 | $ | 20,665 | $ | 19,192 | $ | 21,559 | $ | 23,735 | $ | 20,447 | $ | 8,449 | ||||||||||||||||||||||

One year later | 41,464 | 37,835 | 30,949 | 19,444 | 21,674 | 16,556 | 16,864 | 17,652 | 18,802 | 12,989 | ||||||||||||||||||||||||||||||||||

Two years later | 39,328 | 33,960 | 18,382 | 18,184 | 17,472 | 15,759 | 16,707 | 17,675 | 15,260 | |||||||||||||||||||||||||||||||||||

Three years later | 34,469 | 20,395 | 17,123 | 14,400 | 16,505 | 16,337 | 17,355 | 15,586 | ||||||||||||||||||||||||||||||||||||

Four years later | 20,385 | 18,395 | 13,590 | 13,688 | 16,781 | 16,781 | 17,814 | 15,582 | ||||||||||||||||||||||||||||||||||||

Five years later | 18,520 | 14,838 | 12,568 | 14,140 | 18,052 | 15,672 | ||||||||||||||||||||||||||||||||||||||

Six years later | 15,111 | 12,854 | 12,943 | 15,604 | 15,409 | |||||||||||||||||||||||||||||||||||||||

Seven years later | 13,060 | 13,171 | 14,303 | 15,376 | ||||||||||||||||||||||||||||||||||||||||

Eight years later | 13,387 | 14,525 | 15,420 | |||||||||||||||||||||||||||||||||||||||||

Nine years later | 14,746 | 15,364 | ||||||||||||||||||||||||||||||||||||||||||

Ten years later | 15,361 | |||||||||||||||||||||||||||||||||||||||||||

Cumulative redundancy (deficiency) at December 31, 2014 | 4,030 | (5,571 | ) | (4,187 | ) | 3,215 | 2,145 | 4,081 | 8,499 | 10,348 | 5,701 | (6,912 | ) | |||||||||||||||||||||||||||||||

Cumulative redundancy (deficiency) as a % of reserves originally established | 8.9 | % | (16.5 | )% | (13.8 | )% | 13.6 | % | 10.4 | % | 21.3 | % | 39.4 | % | 43.6 | % | 27.9 | % | (81.8 | )% | ||||||||||||||||||||||||

Net reserves | $ | 53,184 | $ | 45,494 | $ | 33,757 | $ | 30,282 | $ | 23,600 | $ | 20,665 | $ | 19,192 | $ | 21,559 | $ | 23,735 | $ | 20,447 | $ | 8,449 | ||||||||||||||||||||||

Ceded reserves | 1,252 | 1,957 | 1,935 | 3,318 | 23,814 | 23,447 | 20,907 | 14,445 | 33,440 | 153,768 | 4,100 | |||||||||||||||||||||||||||||||||

Gross reserves | $ | 54,436 | $ | 47,451 | $ | 35,692 | $ | 33,600 | $ | 47,414 | $ | 44,112 | $ | 40,099 | $ | 36,004 | $ | 57,175 | $ | 174,215 | $ | 12,549 | ||||||||||||||||||||||

Net re-estimated | $ | 41,464 | $ | 39,328 | $ | 34,469 | $ | 20,385 | $ | 18,520 | $ | 15,111 | $ | 13,060 | $ | 13,387 | $ | 14,746 | $ | 15,361 | ||||||||||||||||||||||||

Ceded re-estimated | 1,784 | 2,254 | 3,777 | 20,570 | 21,012 | 16,461 | 8,750 | 18,861 | 110,895 | 7,454 | ||||||||||||||||||||||||||||||||||

Gross re-estimated | $ | 43,248 | $ | 41,582 | $ | 38,246 | $ | 40,955 | $ | 39,532 | $ | 31,572 | $ | 21,810 | $ | 32,248 | $ | 125,641 | $ | 22,815 | ||||||||||||||||||||||||

Note: The cash we received in relation to the commutation of our 2005 contract with the Florida Hurricane Catastrophe Fund caused the decrease in the net cumulative paid amounts beginning in the 2005 column in the table above.

13

UNITED INSURANCE HOLDINGS CORP.

The NAIC requires all property and casualty insurers to present current and historical loss information in an alternative format known as Schedule P, Part 2. This summary schedule in United Property & Casualty Insurance Company's statutory filings is designed to measure reserve adequacy by evaluating the inception-to-date loss and defense and cost containment (DCC) expenses incurred by calendar year and accident year and calculating the one and two year development on those expenses reported in prior periods.

The following table includes United Property & Casualty Insurance Company's Schedule P, Part 2 information, but was modified to also include all remaining loss adjustment expenses incurred, known as adjusting and other, as well as backing out loss payments from United Property & Casualty Insurance Company to Skyway Claims Services, LLC that are included in Schedule P, Part 2, but are eliminated in our consolidated GAAP results:

CALENDAR YEAR | |||||||||||||||||||||||||||||||||||||||||||||||||||||

2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 1 YR Development | 2 YR Development | |||||||||||||||||||||||||||||||||||||||||

2004 AY* | $ | 39,636 | $ | 43,633 | $ | 45,211 | $ | 46,036 | $ | 45,864 | $ | 45,891 | $ | 45,742 | $ | 45,721 | $ | 45,766 | $ | 45,710 | $ | 45,707 | $ | 3 | $ | 59 | |||||||||||||||||||||||||||

2005 AY | 58,205 | 53,998 | 52,824 | 52,509 | 52,901 | 53,378 | 50,963 | 49,618 | 49,894 | 50,120 | (226 | ) | (502 | ) | |||||||||||||||||||||||||||||||||||||||

2006 AY | 36,386 | 31,195 | 30,570 | 29,728 | 29,946 | 29,753 | 29,857 | 29,864 | 29,858 | 6 | (1 | ) | |||||||||||||||||||||||||||||||||||||||||

2007 AY | 31,465 | 27,432 | 26,696 | 27,000 | 26,824 | 26,901 | 26,958 | 26,949 | 9 | (48 | ) | ||||||||||||||||||||||||||||||||||||||||||

2008 AY | 33,039 | 31,157 | 31,338 | 31,083 | 31,394 | 32,356 | 32,422 | (66 | ) | (1,028 | ) | ||||||||||||||||||||||||||||||||||||||||||

2009 AY | 43,732 | 43,826 | 43,406 | 43,155 | 43,179 | 43,179 | 43,031 | 43,031 | 148 | 124 | |||||||||||||||||||||||||||||||||||||||||||

2010 AY | 41,525 | 40,862 | 40,858 | 41,596 | 41,464 | 132 | (606 | ) | |||||||||||||||||||||||||||||||||||||||||||||

2011 AY | 43,018 | 44,746 | 45,744 | 46,265 | (521 | ) | (1,519 | ) | |||||||||||||||||||||||||||||||||||||||||||||

2012 AY | 57,746 | 58,818 | 59,793 | (975 | ) | (2,047 | ) | ||||||||||||||||||||||||||||||||||||||||||||||

2013 AY | 94,750 | 89,223 | 5,527 | — | |||||||||||||||||||||||||||||||||||||||||||||||||

2014 AY | 122,109 | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||

(unfavorable) favorable | $ | 4,037 | $ | (5,568 | ) | ||||||||||||||||||||||||||||||||||||||||||||||||

* Accident Year

As indicated above, the one-year development was $4,037,000 favorable for 2014, and a reconciliation of these components is as follows:

2014 | |||

Insurance affiliate schedule P, part 2 (loss and DCC) as filed | $ | 944 | |

Adjusting and other added to table above | 423 | ||

One year development total including adjusting and other | 1,367 | ||

Internal payment eliminations for consolidation | 2,670 | ||

Consolidated one year development | $ | 4,037 | |

REGULATION

We are subject to extensive regulation in the markets we serve, primarily at the state level. In general, these regulations are designed to protect the interests of insurance policyholders. These rules have a substantial effect on our business and relate to a wide variety of matters, including insurer solvency, reserve adequacy, insurance company licensing and examination, agent and adjuster licensing, policy forms, rate setting, the nature and amount of investments, claims practices, participation in shared markets and guaranty funds, transactions with affiliates, the payment of dividends, underwriting standards, statutory accounting methods, trade practices, and corporate governance. Some of these matters are discussed in more detail below. From time to time, individual states and/or the NAIC propose new regulations and/or legislation that affect us. We can neither predict whether any of these proposals in the various jurisdictions might be adopted, nor what effect, if any, their adoption may have on our results of operations or financial condition. For a discussion of statutory financial information and regulatory

14

UNITED INSURANCE HOLDINGS CORP.

contingencies, see Note 12 to our Notes to Consolidated Financial Statements which is incorporated in this Part I, Item 1 by reference.

Our insurance affiliates provide audited statutory financial statements to the various insurance regulatory authorities. With regard to periodic examinations of an insurance company's affairs, insurance regulatory authorities, in general, defer to the insurance regulatory authority in the state in which an insurer is domiciled; however, insurance regulatory authorities from any state in which we operate may conduct examinations at their discretion. United Property & Casualty Insurance Company is domiciled in Florida and Family Security Insurance Company is domiciled in Hawaii.

Florida's insurance regulatory authority completed a limited-scope financial examination pertaining to our December 31, 2011 Annual Statement in November 2012. We received the results in September 2012, and there were no material adverse findings reported.

Florida state law requires our insurance affiliate to maintain adequate surplus as to policyholders such that 90% of written premiums divided by surplus does not exceed the ratio of 10:1 for gross written premiums or 4.5:1 for net written premiums. The ratio of gross and net written premium to surplus as of December 31, 2014, was 3.2:1 and 1.9:1, respectively, and United Property & Casualty Insurance Company’s surplus as regards policyholders of $126,249,000 exceeded the minimum capital of $5,000,000 required by state laws.

We are subject to various assessments imposed by governmental agencies or certain quasi-governmental entities. While we may be able to recover from policyholders some of the assessments imposed upon us, our payment of the assessments and our recoveries through policy surcharges may not offset each other in the same fiscal period in our financial statements. See Note 2(j) and Note 12 in our Notes to Consolidated Financial Statements for additional information regarding the assessments that we are currently collecting.

Limitations on Dividends by Insurance Subsidiaries

As a holding company with no significant business operations of our own, we rely on payments from our insurance affiliates as one of the principal sources of cash to pay dividends and meet our obligations. Our insurance affiliates are regulated as property and casualty insurance companies and their ability to pay dividends is restricted by Florida and Hawaii law. For additional information regarding those restrictions, see Part II, Item 5 of this report.

15

UNITED INSURANCE HOLDINGS CORP.

Risk-Based Capital Requirements

To enhance the regulation of insurer solvency, the NAIC published risk-based capital (RBC) guidelines for insurance companies designed to assess capital adequacy and to raise the level of protection statutory surplus provides for policyholders. The guidelines measure three major areas of risk facing property and casualty insurers: (i) underwriting risks, which encompass the risk of adverse loss developments and inadequate pricing; (ii) declines in asset values arising from credit risk; and (iii) other business risks. Most states, including Florida and Hawaii, have enacted the NAIC guidelines as statutory requirements, and insurers having less statutory surplus than required will be subject to varying degrees of regulatory action, depending on the level of capital inadequacy. Insurance regulatory authorities could require our insurance subsidiaries to cease operations in the event it fails to maintain the required statutory capital.

The level of required risk-based capital is calculated and reported annually. There are five outcomes to the RBC calculation set forth by the NAIC which are as follows:

1. | No Action Level - If RBC is greater than 200%, no further action is required. |

2. | Company Action Level - If RBC is between 150% -200%, the insurer must prepare a report to the regulator outlining a comprehensive financial plan that identifies conditions that contributed to the insurer's financial condition and proposes corrective actions. |

3. | Regulatory Action Level - If RBC is between 100% -150%, the state insurance commissioner is required to perform any examinations or analyses to the insurer's business and operations that he or she deems necessary as well as issuing appropriate corrective orders. |

4. | Authorized Control Level - If RBC is between 70% - 100%, this is the first point that the regulator may take control of the insurer even if the insurer is still technically solvent and is in addition to all the remedies available at the higher action levels. |

5. | Mandatory Control Level - If RBC is less than 70%, the regulator is required to take steps to place the insurer under its control regardless of the level of capital and surplus. |

At December 31, 2014, the RBC ratio for United Property & Casualty Insurance Company and Family Security Insurance Company was 597% and 269%, respectively.

Insurance Holding Company Regulation

As a holding company of insurance subsidiaries, we are subject to laws governing insurance holding companies in Florida and Hawaii. These laws, among other things, (i) require us to file periodic information with the insurance regulatory authority, including information concerning our capital structure, ownership, financial condition and general business operations, (ii) regulate certain transactions between our affiliates and us, including the amount of dividends and other distributions and the terms of surplus notes and (iii) restrict the ability of any one person to acquire certain levels of our voting securities without prior regulatory approval. Any purchaser of 5% or more of the outstanding shares of our common stock could be presumed to have acquired control of us unless the insurance regulatory authority, upon application, determines otherwise.

Insurance holding company regulations also govern the amount any affiliate of the holding company may charge our insurance affiliates for services (e.g., management fees and commissions). We have a long-term management agreement between United Property & Casualty Insurance Company and United Insurance Management, L.C., which presently provides for monthly management fees. The Florida insurance regulatory authority must approve any changes to this agreement.

We also have a management agreement between Family Security Insurance Company and Family Security Underwriters, LLC, which presently provides for monthly management fees. The Hawaii regulatory authority must approve any changes to this agreement.

16

UNITED INSURANCE HOLDINGS CORP.

Underwriting and Marketing Restrictions

During the past several years, various regulatory and legislative bodies have adopted or proposed new laws or regulations to address the cyclical nature of the insurance industry, catastrophic events and insurance capacity and pricing. These regulations (i) created “market assistance plans” under which insurers are induced to provide certain coverage; (ii) restrict the ability of insurers to reject insurance coverage applications, to rescind or otherwise cancel certain policies in mid-term, and to terminate agents; (iii) restrict certain policy non-renewals and require advance notice on certain policy non-renewals; and (iv) limit rate increases or decrease rates permitted to be charged.

Most states also have insurance laws requiring that rate schedules and other information be filed with the insurance regulatory authority, either directly or through a rating organization with which the insurer is affiliated. The insurance regulatory authority may disapprove a rate filing if it finds that the rates are inadequate, excessive or unfairly discriminatory.

Most states require licensure or insurance regulatory authority approval prior to the marketing of new insurance products. Typically, licensure review is comprehensive and includes a review of a company’s business plan, solvency, reinsurance, character of its officers and directors, rates, forms and other financial and non-financial aspects of a company. The insurance regulatory authorities may prohibit entry into a new market by not granting a license or by withholding approval.

FINANCIAL STABILITY RATING

Financial stability ratings are important to insurance companies in establishing their competitive position and such ratings may impact an insurance company’s ability to write policies. Demotech maintains a letter-scale financial stability rating system ranging from A** (A double prime) to L (licensed by insurance regulatory authorities); they have assigned our insurance subsidiaries a financial stability rating of A, which is the third highest of six rating levels. According to Demotech, "Regardless of the severity of a general economic downturn or deterioration in the insurance cycle, insurers earning a Financial Stability Rating of A possess Exceptional financial stability related to maintaining surplus as regards policyholders at an acceptable level.” With a financial stability rating of A, we expect our property insurance policies will be acceptable to the secondary mortgage marketplace and mortgage lenders. This rating is intended to provide an independent opinion of an insurer’s financial strength and is not an evaluation directed at our investors. At least annually, based on year-to-date results as of the third quarter, Demotech reviews our rating and may revise it upward or downward or revoke it at their sole discretion.

EMPLOYEES

As of February 2015, we have two part time employees, and 118 full time employees, which includes our executive officers. We are neither party to any collective bargaining agreements nor have we experienced any work stoppages or strikes as a result of labor disputes. We believe we have good working relationships with our employees.

AVAILABLE INFORMATION

We make available, free of charge through our website, www.upcinsurance.com, our Annual Report, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after we electronically file such materials with, or furnish them to, the SEC.

These reports may also be obtained at the SEC’s Public Reference Room at 100 F Street NE, Washington, D.C. 20549. Information on the operation of the Public Reference Room is available by calling the SEC at 1-800-SEC-0330. You may also access this information at the SEC’s website (www.sec.gov). This site contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC.

17

UNITED INSURANCE HOLDINGS CORP.

Item 1A. Risk Factors

Many factors affect our business and results of operations, some of which are beyond our control. Additional risks and uncertainties we are unaware of, or we currently deem immaterial, also may become important factors that affect us. If any of the following risks occur, our business, financial conditions or results of operations may be materially and adversely affected. In that event, the trading price of our securities could decline, and our stockholders could lose all or part of their investment in our securities. This discussion contains forward-looking statements. See the section entitled FORWARD-LOOKING STATEMENTS for a discussion of uncertainties, risks and assumptions associated with these statements.

RISKS RELATED TO OUR BUSINESS

As a property and casualty insurer, we may experience significant losses and our financial results may vary from period to period due to our exposure to catastrophic events and severe weather conditions, the incidence and severity of which could be affected by climate change.

Our property and casualty insurance operations expose us to claims arising from catastrophes. Catastrophes can be caused by various natural events, including hurricanes, windstorms, earthquakes, hail, severe winter weather and fires; they can also be man-made, such as terrorist attacks (including those involving nuclear, biological, chemical or radiological events) or consequences of war or political instability. We may incur catastrophe losses that exceed the amount of:

• | catastrophe losses that we experienced in prior years; |

• | catastrophe losses that, using third-party catastrophe modeling software, we projected could be incurred; |

• | catastrophe losses that we used to develop prices for our products; or |

• | our current reinsurance coverage (which would cause us to have to pay such excess losses). |

The incidence and severity of weather conditions are largely unpredictable, but the frequency and severity of property claims generally increase when severe weather conditions occur. A body of scientific evidence seems to indicate that climate change may be occurring. Climate change, to the extent that it may affect weather patterns, may cause an increase in the frequency and/or the severity of catastrophic events or severe weather conditions which, in addition to the attendant increase in claims-related costs, may also cause an increase in our reinsurance costs and/or negatively impact our ability to provide homeowners insurance to our policyholders in the future. Governmental entities may also respond to climate change by enacting laws and regulations that may adversely affect our cost of providing homeowners insurance in the future.

Catastrophes may cause a material adverse effect on our results of operations during any reporting period; they may also materially harm our financial condition, which in turn may materially harm our liquidity and impair our ability to raise capital on acceptable terms or at all. In addition to catastrophes, the accumulation of losses from smaller weather-related events in any reporting period may cause a material adverse effect on our results of operations and liquidity in that period.

Because we conduct the majority of our business in Florida, our financial results substantially depend on the regulatory, economic and weather conditions present in that state.

Although we began writing policies outside of Florida in 2010, we still write approximately 74% of our premium in Florida; therefore, prevailing regulatory, legal, economic, political, demographic, competitive, weather and other conditions in Florida affect our revenues and profitability. Changes in conditions could make doing business in Florida less attractive for us and would have a more pronounced effect on us than it would on other insurance companies that are more geographically diversified.

We are subject to increased exposure to certain catastrophic events such as hurricanes, as well as an increased risk of losses. The occurrence of one or more catastrophic events or other conditions affecting losses in Florida may cause a material adverse effect on our results of operations and financial condition.

18

UNITED INSURANCE HOLDINGS CORP.

We may enter new markets and there can be no assurance that our diversification strategy will be effective.

Although we intend to continue focusing on Florida as a key market for our insurance products, we also may seek to take advantage of prudent opportunities to expand our core business into other states where we believe the independent agent distribution channel is strong. As a result of a number of factors, including the difficulties of finding appropriate expansion opportunities and the challenges of operating in an unfamiliar market, we may not be successful in this diversification. Additionally, in order to carry out any such strategy, we would need to obtain the appropriate licenses from the insurance regulatory authority of any such state.

Because we rely on insurance agents, the loss of these agent relationships or our ability to attract new agents could have an adverse impact on our business.

We currently market our policies to a broad range of prospective policyholders through over 4,000 independent agencies. Many of these agents are independent insurance agents that own their customer relationships, and our agency contracts with them limit our ability to directly solicit business from our existing policyholders. Independent agents most commonly represent other insurance companies and we do not control their activities. Historically, we have used marketing relationships with two well-known national insurance companies that do not write new homeowners insurance policies in Florida and two associations of independent insurance agents in Florida to attract and retain agents and agency groups. The loss of these marketing relationships could adversely impact our ability to attract new agents or retain our agency network.

Actual claims incurred may exceed our loss reserves for claims, which could adversely affect our results of operations and financial condition.

Loss reserves represent our estimate of ultimate unpaid losses for claims that have been reported and claims that have been incurred but not yet reported. Loss reserves do not represent an exact calculation of liability, but instead represent our best estimate, generally utilizing actuarial expertise, historical information and projection techniques at a given reporting date.

The process of estimating our loss reserves involves a high degree of judgment and is subject to a number of variables. These variables can be affected by both internal and external events, such as changes in claims handling procedures, economic inflation, legal trends, legislative changes, and varying judgments and viewpoints of the individuals involved in the estimation process, among others.

Because of the inherent uncertainty in estimating loss reserves, including reserves for catastrophes, additional liabilities resulting from one insured event, or an accumulation of insured events, may exceed our existing loss reserves and cause a material adverse effect on our results of operations and our financial condition.

Our financial results may vary from period to period based on the timing of our collection of government-levied assessments from our policyholders.

Our insurance affiliates are subject to assessments levied by various governmental and quasi-governmental entities in the states in which we operate. While we may have the ability to recover these assessments from policyholders through policy surcharges in some states in which we operate, our payment of the assessments and our recoveries may not offset each other in the same reporting period in our financial statements and may cause a material adverse effect on our results of operations in a particular reporting period.

Violation(s) of certain debt covenants related to our note payable to the Florida State Board of Administration could allow the Florida SBA to call the note, which could cause a material adverse effect on our financial condition.

United Property & Casualty Insurance Company is subject to certain debt covenants related to our note payable with the Florida SBA. As a remedy for covenant violations related to the note payable, the Florida SBA may make the note due and payable upon demand. Any demand by the Florida SBA for payment related to the note, whether immediate payment of the full balance or some other amount, is subject to approval by the insurance regulatory authority in Florida. Should the insurance regulatory authority grant approval of a demand for immediate full payment, such payment could cause a material adverse effect on our cash flows and financial condition. We were in compliance with the covenants under the note payable during the years ended December 31, 2014 and 2013.

19

UNITED INSURANCE HOLDINGS CORP.

Our failure to implement and maintain adequate internal controls over financial reporting in our business could have a material adverse effect on our business, financial condition, results of operations and stock price.

We have complied with the provisions regarding annual management assessments of the effectiveness of our internal controls over financial reporting as required by Section 404 of the Sarbanes-Oxley Act of 2002 during 2014 and 2013.

If we fail to achieve and maintain the adequacy of our internal controls in accordance with applicable standards as then in effect, and as supplemented or amended from time to time, we may be unable to conclude on an ongoing basis that we have effective internal controls over financial reporting in accordance with Section 404. Moreover, effective internal controls are necessary for us to produce reliable financial reports. If we cannot produce reliable financial reports or otherwise maintain appropriate internal controls, our business, financial condition and results of operations could be harmed, investors could lose confidence in our reported financial information, and the market price for our stock could decline.

If we experience difficulties with technology, data security and/or outsourcing relationships, our ability to conduct our business could be negatively impacted.

While technology can streamline many business processes and ultimately reduce the cost of operations, technology initiatives present certain risks. Our business is highly dependent upon our information technology systems and upon our contractors' and third-party administrators' ability to perform, in an efficient and uninterrupted fashion, necessary business functions such as the processing of policies and the adjusting of claims. Because our information technology and telecommunications systems interface with and often depend on these third-party systems, we could experience service denials if demand for such service exceeds capacity or a third-party system fails or experiences an interruption. If sustained or repeated, such a business interruption, system failure or service denial could result in a deterioration of our ability to write and process new and renewal business, provide customer service, pay claims in a timely manner or perform other necessary business functions.

Despite our implementation of security measures, our information technology systems are vulnerable to computer viruses, natural disasters, unauthorized access, cyber-attacks, system failures and similar disruptions. A material breach in the security of our information technology systems and data could include the theft of our confidential or proprietary information, including trade secrets and the personal information of our customers, claimants and employees. From time to time, we have experienced threats to our data and information technology systems, including malware and computer virus attacks, unauthorized access, system failures and disruptions. To the extent that any disruptions or security breaches result in a loss or damage to our data or inappropriate disclosure of proprietary or confidential information, it could cause significant damage to our reputation, adversely affect our relationships with our customers, result in litigation, increased costs and/or regulatory penalties, and ultimately harm our business. Third parties to whom we outsource certain of our functions are also subject to the risks outlined above, any one of which may result in our incurring substantial costs and other negative consequences, including a material adverse effect on our business, financial condition, results of operations and liquidity.

Loss of key vendor relationships or failure of a vendor to protect personal information of our customers, claimants or employees could affect our operations.

We rely on services and products provided by many vendors. These include, for example, vendors of computer hardware and software and vendors of services such as claim adjustment services and human resource benefits management services. In the event that one or more of our vendors suffers a bankruptcy or otherwise becomes unable to continue to provide products or services, or fails to protect personal information of our customers, claimants or employees, we may suffer operational impairments and financial losses.

Our success has been and will continue to be greatly influenced by our ability to attract and retain the services of senior management.

Our senior executive officers play an integral role in the development and management of our business. We do not maintain any key person life insurance policies on any of our officers or employees. The loss of the services of any of our senior executive officers could have an adverse effect on our business, financial condition, results of operations, cash flows and/or future prospects.

20

UNITED INSURANCE HOLDINGS CORP.

RISKS RELATED TO THE INSURANCE INDUSTRY

Because we are smaller than some of our competitors, we may lack the resources to increase or maintain our market share.

The property and casualty insurance industry is highly competitive, and we believe it will remain highly competitive for the foreseeable future. The principal competitive factors in our industry are price, service, commission structure and financial condition. We compete with other property and casualty insurers that write coverage in the same territories in which we write coverage; some of those insurers have greater financial resources and have a longer operating history than we do. In addition, our competitors may offer products for alternative forms of risk protection. Competition could limit our ability to retain existing business or to write new business at adequate rates, and such limitation may cause a material adverse effect on our results of operations and financial position.

State regulations limiting rate increases and requiring us to underwrite business in certain areas are beyond our control and may adversely affect our results of operation and financial condition.

States have from time to time passed legislation, and regulators have taken action, that has the effect of limiting the ability of insurers to manage catastrophe risk, such as legislation prohibiting insurers from reducing exposures or withdrawing from catastrophe-prone areas, or mandating that insurers participate in residual markets. In addition, following catastrophes, there are sometimes legislative initiatives and court decisions which seek to expand insurance coverage for catastrophe claims beyond the original intent of the policies. Further, our ability to increase pricing to the extent necessary to offset rising costs of catastrophes requires approval of insurance regulatory authorities.

One example of such legislation occurred following the 2004 and 2005 hurricane seasons, when the Florida legislature required all insurers issuing replacement cost policies to pay the full replacement cost of damaged properties without depreciation whether or not the insureds repaired or replaced the damaged property. Under prior law, insurers would have paid the depreciated amount of the property until insureds commenced repairs or replacement. This law has led to an increase in disagreements regarding the scope of damage. Despite our efforts to adjust claims and promptly pay meritorious amounts, our operating results have been affected by a claims environment in Florida that produces opportunities for fraudulent or overstated claims.

Our ability or willingness to manage our catastrophe exposure by raising prices, modifying underwriting terms or reducing exposure to certain geographies may be limited due to considerations of public policy, the evolving political environment and our ability to penetrate other geographic markets, which may cause a material adverse effect on our results of operations, financial condition and cash flows. We cannot predict whether and to what extent new legislation and regulations that would affect our ability to manage our exposure to catastrophic events will be adopted, the timing of adoption or the effects, if any, they would have on our ability to manage our exposure to catastrophic events.

The insurance industry is heavily regulated and further restrictive regulation may reduce our profitability and limit our growth.

The insurance industry is extensively regulated and supervised. Insurance regulatory authorities generally design insurance rules and regulations to protect the interests of policyholders, and not necessarily the interests of insurers, their stockholders and other investors. Regulatory systems also address authorization for lines of business, capital and surplus requirements, limitations on the types and amounts of certain investments, underwriting limitations, licensing, transactions with affiliates, dividend limitations, changes in control, premium rates and a variety of other financial and non-financial components of an insurer’s business.

In recent years, the state insurance regulatory framework has come under increased federal scrutiny. Although the United States federal government does not directly regulate the insurance business, changes in federal legislation, regulation and/or administrative policies in several areas, including changes in financial services regulation and federal taxation, could negatively affect the insurance industry and us. In addition, Congress and some federal agencies from time to time investigate the current condition of insurance regulation in the United States to determine whether to impose federal or national regulation or to allow an optional federal charter, similar to the option available to most banks. Further, the NAIC and state insurance regulators continually reexamine existing laws and regulations, specifically focusing on modifications to holding company regulations,

21

UNITED INSURANCE HOLDINGS CORP.

interpretations of existing laws and the development of new laws and regulations. We cannot predict what effect, if any, proposed or future legislation or NAIC initiatives may have on the manner in which we conduct our business.

As part of ongoing, industry-wide investigations, we may from time to time receive subpoenas and written requests for information from government agencies and authorities at the state or federal level. If we are subpoenaed for information by government agencies and authorities, potential outcomes could include enforcement proceedings or settlements resulting in fines, penalties and/or changes in business practices that could cause a material adverse effect on our results of operations. In addition, these investigations may result in changes to laws and regulations affecting the industry.

Changes to insurance laws or regulations, or new insurance laws and regulations, may be more restrictive than current laws or regulations and could cause material adverse effects on our results of operations and our prospects for future growth. Additionally, our failure to comply with certain provisions of applicable insurance laws and regulations may cause a material adverse effect on our results of operations or financial condition.

Our inability to obtain reinsurance on acceptable terms would increase our loss exposure or limit our ability to underwrite policies.

We use, and we expect to continue to use, reinsurance to help manage our exposure to property and casualty risks. The availability and cost of reinsurance are each subject to prevailing market conditions beyond our control which can affect business volume and profitability. We may be unable to maintain our current reinsurance coverage, to obtain additional reinsurance coverage in the event our current reinsurance coverage is exhausted by a catastrophic event, or to obtain other reinsurance coverage in adequate amounts or at acceptable rates. Similar risks exist whether we are seeking to replace coverage terminated during the applicable coverage period or to renew or replace coverage upon its expiration. We provide no assurance that we can obtain sufficient reinsurance to cover losses resulting from one or more storms in the future, or that we can obtain such reinsurance in a timely or cost-effective manner. If we are unable to renew our expiring coverage or to obtain new reinsurance coverage, either our net exposure to risk would increase or, if we are unwilling to accept an increase in net risk exposures, we would have to reduce the amount of risk we underwrite. Either increasing our net exposure to risk or reducing the amount of risk we underwrite may cause a material adverse effect on our results of operations and our financial condition.

In each of the past ten years, a portion of our reinsurance protection has been provided by the Florida Hurricane Catastrophe Fund (FHCF), a government sponsored entity that provides a layer of reinsurance protection at a price that is lower than otherwise available in the commercial market. The purpose of the FHCF is to protect and advance the state's interest in maintaining insurance capacity in Florida by providing reimbursements to insurers for a portion of their catastrophe hurricane losses. There is no assurance that FHCF will continue to make such reinsurance available on terms consistent with historical practice. The loss of reinsurance provided by FHCF would have an adverse impact on our results of operations and financial condition.