Attached files

| file | filename |

|---|---|

| 10-K - FORM 10-K - VERIZON COMMUNICATIONS INC | d820819d10k.htm |

| EXCEL - IDEA: XBRL DOCUMENT - VERIZON COMMUNICATIONS INC | Financial_Report.xls |

| EX-31.1 - EXHIBIT 31.1 - VERIZON COMMUNICATIONS INC | d820819dex311.htm |

| EX-12 - EXHIBIT 12 - VERIZON COMMUNICATIONS INC | d820819dex12.htm |

| EX-21 - EXHIBIT 21 - VERIZON COMMUNICATIONS INC | d820819dex21.htm |

| EX-10.Q - EXHIBIT 10Q - VERIZON COMMUNICATIONS INC | d820819dex10q.htm |

| EX-32.2 - EXHIBIT 32.2 - VERIZON COMMUNICATIONS INC | d820819dex322.htm |

| EX-31.2 - EXHIBIT 31.2 - VERIZON COMMUNICATIONS INC | d820819dex312.htm |

| EX-32.1 - EXHIBIT 32.1 - VERIZON COMMUNICATIONS INC | d820819dex321.htm |

| EX-23 - EXHIBIT 23 - VERIZON COMMUNICATIONS INC | d820819dex23.htm |

EXHIBIT 13

| Selected Financial Data Verizon Communications Inc. and Subsidiaries | ||

| (dollars in millions, except per share amounts) | ||||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | 2010 | ||||||||||||||||

| Results of Operations |

||||||||||||||||||||

| Operating revenues |

$ | 127,079 | $ | 120,550 | $ | 115,846 | $ | 110,875 | $ | 106,565 | ||||||||||

| Operating income |

19,599 | 31,968 | 13,160 | 12,880 | 14,645 | |||||||||||||||

| Net income attributable to Verizon |

9,625 | 11,497 | 875 | 2,404 | 2,549 | |||||||||||||||

| Per common share – basic |

2.42 | 4.01 | .31 | .85 | .90 | |||||||||||||||

| Per common share – diluted |

2.42 | 4.00 | .31 | .85 | .90 | |||||||||||||||

| Cash dividends declared per common share |

2.160 | 2.090 | 2.030 | 1.975 | 1.925 | |||||||||||||||

| Net income attributable to noncontrolling interests |

2,331 | 12,050 | 9,682 | 7,794 | 7,668 | |||||||||||||||

| Financial Position |

||||||||||||||||||||

| Total assets |

$ | 232,708 | $ | 274,098 | $ | 225,222 | $ | 230,461 | $ | 220,005 | ||||||||||

| Debt maturing within one year |

2,735 | 3,933 | 4,369 | 4,849 | 7,542 | |||||||||||||||

| Long-term debt |

110,536 | 89,658 | 47,618 | 50,303 | 45,252 | |||||||||||||||

| Employee benefit obligations |

33,280 | 27,682 | 34,346 | 32,957 | 28,164 | |||||||||||||||

| Noncontrolling interests |

1,378 | 56,580 | 52,376 | 49,938 | 48,343 | |||||||||||||||

| Equity attributable to Verizon |

12,298 | 38,836 | 33,157 | 35,970 | 38,569 | |||||||||||||||

| • | Significant events affecting our historical earnings trends in 2012 through 2014 are described in “Other Items” in the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section. |

| • | 2011 data includes severance, pension and benefit charges and early debt redemption costs. 2010 data includes severance, pension and benefit charges, merger integration charges, dispositions, Medicare Part D Subsidy charges and other items. |

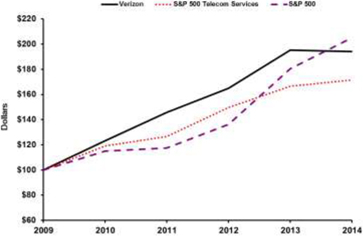

| Stock Performance Graph |

Comparison of Five-Year Total Return Among Verizon,

S&P 500 Telecommunications Services Index and S&P 500 Stock Index

| At December 31, | ||||||||||||||||||||||||

| Data Points in Dollars | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||||||||||

|

Verizon |

100.0 | 123.1 | 145.7 | 164.8 | 195.3 | 194.2 | ||||||||||||||||||

|

S&P 500 Telecom Services |

100.0 | 119.0 | 126.5 | 149.6 | 166.6 | 171.5 | ||||||||||||||||||

|

S&P 500 |

100.0 | 115.1 | 117.5 | 136.2 | 180.3 | 205.0 | ||||||||||||||||||

The graph compares the cumulative total returns of Verizon, the S&P 500 Telecommunications Services Index, and the S&P 500 Stock Index over a five-year period. It assumes $100 was invested on December 31, 2009 with dividends (including the value of the telephone access line spin-off that occurred in 2010) being reinvested.

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| Overview |

Verizon Communications Inc. (Verizon or the Company) is a holding company that, acting through its subsidiaries, is one of the world’s leading providers of communications, information and entertainment products and services to consumers, businesses and governmental agencies. With a presence around the world, we offer voice, data and video services and solutions on our wireless and wireline networks that are designed to meet customers’ demand for mobility, reliable network connectivity, security and control. We have two reportable segments, Wireless and Wireline. Our wireless business, operating as Verizon Wireless, provides voice and data services and equipment sales across the United States using one of the most extensive and reliable wireless networks. Our wireline business provides consumer, business and government customers with communications products and enhanced services, including broadband data and video, corporate networking solutions, data center and cloud services, security and managed network services and local and long distance voice services, and also owns and operates one of the most expansive end-to-end global Internet Protocol (IP) networks. We have a highly skilled, diverse and dedicated workforce of approximately 177,300 employees as of December 31, 2014.

As advances in technology have changed the ways that our customers interact in their personal and professional lives and that businesses operate, we have continued to focus our efforts around higher margin and growing areas of our business: wireless and wireline data and Strategic services, including cloud computing services. Our strategy requires significant capital investments primarily to acquire wireless spectrum, put the spectrum into service, provide additional capacity for growth in our wireless and wireline networks, invest in the fiber optic network that supports our wireless and wireline businesses, maintain our wireless and wireline networks and develop and maintain significant advanced information technology systems and data system capabilities. We believe that steady and consistent investments in networks and platforms will drive innovative products and services and fuel our growth. Our wireless and wireline networks will continue to be the hallmark of our brand, and provide the fundamental strength upon which we build our competitive advantage.

Strategic Transactions

Wireless Transaction

On February 21, 2014, we set the stage for the next phase of our company’s growth when we completed the acquisition of Vodafone Group Plc’s (Vodafone) indirect 45% interest in Cellco Partnership d/b/a Verizon Wireless for aggregate consideration of approximately $130 billion (the Wireless Transaction). The consideration paid was primarily comprised of cash of approximately $58.89 billion and Verizon common stock with a value of approximately $61.3 billion. With full control of Verizon Wireless enhancing our operational efficiency, we believe we are well-positioned to meet the challenges of an increasingly competitive industry. See Note 2 to the consolidated financial statements for additional information.

Spectrum Auction

On January 29, 2015, the Federal Communications Commission (FCC) completed an auction of 65 MHz of spectrum, which it identified as the Advanced Wireless Services (AWS)-3 band. Verizon participated in that auction, and was the high bidder on 181 spectrum licenses, for which we will pay approximately $10.4 billion. During the fourth quarter of 2014, we made a deposit of $0.9 billion related to our participation in this auction. On February 13, 2015, we made a down payment of $1.2 billion for these spectrum licenses. Verizon has submitted an application for these licenses and must complete payment for them in the first quarter of 2015.

Access Line Sale

On February 5, 2015, we announced that we have entered into a definitive agreement with Frontier Communications Corporation (Frontier) pursuant to which Verizon will sell its local exchange business and related landline activities in California, Florida, and Texas, including FiOS Internet and Video customers, switched and special access lines and high-speed Internet service and long distance voice accounts in these three states for approximately $10.5 billion. The transaction, which includes the acquisition by Frontier of the equity interests of Verizon’s incumbent local exchange carriers (ILECs) in California, Florida and Texas, does not involve any assets or liabilities of Verizon Wireless. The assets and liabilities that will be sold are currently included in Verizon’s continuing operations. As part of the transaction, Frontier will assume $0.6 billion of indebtedness from Verizon. The transaction is subject to the satisfaction of certain closing conditions including, among others, receipt of state and federal telecommunications regulatory approvals, and we expect this transaction to close during the first half of 2016.

The transaction will result in Frontier acquiring approximately 1.5 million FiOS Internet subscribers, 1.2 million FiOS Video subscribers and the related ILEC businesses from Verizon. This business generated revenues of approximately $5.4 billion, excluding revenue with affiliates, for Verizon in 2013, which is the most recent year for which audited stand-alone financial statements are currently available.

Tower Monetization Transaction

On February 5, 2015, we announced an agreement with American Tower Corporation (American Tower) pursuant to which American Tower will have the exclusive rights to lease and operate over 11,300 of our wireless towers for an upfront payment of $5.0 billion. Under the terms of the leases, American Tower will have exclusive rights to lease and operate the towers over an average term of approximately 28 years. As part of this transaction, we will also sell 165 towers for $0.1 billion. We will sublease capacity on the towers from American Tower for a minimum of 10 years

at current market rates, with options to renew. As the leases expire, American Tower will have fixed-price purchase options to acquire these towers based on their anticipated fair market values at the end of the lease terms. We plan to account for the upfront payment primarily as prepaid rent and a portion as a financing obligation. This transaction, which is subject to customary closing conditions, is expected to close during the first half of 2015.

Business Overview

Wireless

Demand for our fourth generation (4G) Long Term Evolution (LTE) smartphones and tablets continues to drive growth in our Wireless business. During 2014, Wireless revenue increased $6.6 billion, or 8.2%, compared to 2013 driven by service revenue growth of $3.6 billion, or 5.2%, which does not include recurring equipment installment billings related to Verizon Edge. Also contributing to the increase in Wireless revenue was equipment revenue growth of $2.8 billion, or 35.1%, driven by higher sales of equipment under both the traditional subsidy model and Verizon Edge, a program that enables qualified customers to purchase their devices on an installment payment plan. During 2014, retail postpaid connections increased 5.5% compared to 2013, with smartphones representing 79% of our retail postpaid phone base at December 31, 2014 compared to 70% at December 31, 2013. Also, during 2014, postpaid smartphone activations represented 92% of phones activated compared to 86% in 2013.

We are focusing the capital spending in our Wireless business on adding capacity and density to our 4G LTE network, which is available to over 98% of the U.S. population in more than 500 markets covering approximately 309 million people, including those in areas served by our LTE in Rural America partners. Our 4G LTE network provides higher data throughput performance for data services at a lower cost compared to that provided via third-generation (3G) networks. Approximately 84% of our total data traffic in December 2014 was carried on our 4G LTE network. In May 2014, we announced the deployment of AWS spectrum in our 4G LTE network. This additional bandwidth, which we refer to and brand as XLTE, provides additional network capacity and is currently available in more than 400 markets. Nearly all of the 4G LTE devices Verizon Wireless currently sells can operate on XLTE.

In February 2014, we introduced our More Everything® plans which replaced our Share Everything® plans. These plans feature domestic unlimited voice minutes, unlimited domestic and international text, video and picture messaging, cloud storage and a single data allowance that can be shared among multiple devices connected to the Verizon Wireless network. As of December 31, 2014, More Everything accounts represented approximately 61% of our retail postpaid accounts compared to Share Everything plans representing approximately 46% of our retail postpaid accounts as of December 31, 2013. Verizon Wireless also offers shared data plans for business, with More Everything plans for Small business and Nationwide Business Data Packages and Plans.

Wireline

In our Wireline business, revenues decreased 0.5% during 2014 compared to 2013, primarily due to declines in Global Enterprise Core and Global Wholesale revenues resulting from lower voice services and data networking revenues as well as the contraction of market rates due to competition. To compensate for the shrinking market for traditional voice service, we continue to build our Wireline segment around data, video and advanced business services – areas where demand for reliable high-speed connections is growing. Wireline’s revenues during 2014 included a 2.3% increase in Strategic services revenues, which represented 61% of total Global Enterprise revenues, as compared to 57% of total Global Enterprise revenues during 2013.

Wireline revenues during 2014 also included increases in Consumer retail revenue driven by FiOS services. FiOS represented approximately 76% of Consumer retail revenue during 2014, compared to approximately 71% during 2013. As the penetration of FiOS products increases, we continue to seek ways to increase revenue and further realize operating and capital efficiencies as well as maximize profitability. As more applications are developed for this high-speed service, we expect that FiOS will become a hub for managing multiple home services that will eventually be part of the digital grid, including not just entertainment and communications, but also machine-to-machine communications, such as home monitoring, health monitoring, energy management and utilities management.

We continue to enrich the customer value proposition by creating new and innovative services on our FiOS platform. During 2014, Verizon announced the introduction of FiOS Quantum TV, which provides FiOS video subscribers with new features, including the ability to record up to 12 shows at once and control live TV from any room in their home. This new service is now available everywhere that FiOS TV is offered. With our FiOS Quantum broadband service and certain other data services, our residential and small business customers can achieve symmetrical upload and download speeds of up to 500 megabytes per second, which we refer to as SpeedMatchsm.

Capital Expenditures and Investments

We are investing in wireless networks, high-speed fiber and cloud services to position ourselves at the center of growth trends for the future. During 2014, these investments included capital expenditures of $17.2 billion and acquisitions of wireless licenses of $0.4 billion. See “Cash Flows Used in Investing Activities” and Note 2 to the consolidated financial statements for additional information.

By investing to expand our own capabilities, we are also providing the communities we serve with an efficient, reliable infrastructure for competing in the information economy. We are committed to putting our customers first and being a responsible member of our communities. Guided by this commitment and by our core values of integrity, respect, performance excellence and accountability, we believe we are well-positioned to produce a long-term return for our shareowners, create meaningful work for ourselves and provide lasting value for society.

Trends

In the sections that follow, we provide information about the important aspects of our operations and investments, both at the consolidated and segment levels, and discuss our results of operations, financial position and sources and uses of cash. In addition, we highlight key trends and uncertainties to the extent practicable.

The industries that we operate in are highly competitive, which we expect to continue particularly as traditional, non-traditional and emerging service providers seek increased market share. We believe that our high-quality customer base and superior networks differentiate us from our competitors and enable us to provide enhanced communications experiences to our customers. We believe our focus on the fundamentals of running a good business, including operating excellence and financial discipline, gives us the ability to plan and manage through changing economic and competitive conditions. We will continue to invest for growth, which we believe is the key to creating value for our shareowners.

Connection and Operating Trends

In our Wireless segment, we expect to continue to attract and maintain the loyalty of high-quality retail postpaid customers, capitalizing on demand for data services and bringing our customers new ways of using wireless services in their daily lives. We expect that future connection growth will continue as we introduce new 4G LTE devices, including new smartphones and tablets. We believe these devices will attract and retain higher value retail postpaid connections, contribute to continued increases in the penetration of data services and help us remain competitive with other wireless carriers. However, as a result of the increasing competition within our industry, we expect our churn to increase in 2015. We expect future growth opportunities will be dependent on expanding the penetration of our network services, offering innovative wireless devices for both consumer and business customers and increasing the number of ways that our customers can connect with our network and services.

Service and equipment pricing play an important role in the wireless competitive landscape. As the demand for wireless services continues to grow, wireless service providers are offering service plans that include unlimited voice minutes and text messages and a specific amount of data access in varying megabyte or gigabyte sizes or, in some cases, unlimited data usage at competitive prices. Some wireless service providers also allow customers to rollover unused data allowances to the next billing period and are also offering installment plans that decouple service pricing from equipment pricing and blur the traditional boundary between prepaid and postpaid plans. In 2015, we expect that customers will continue to adopt these installment plans, which also offer discounts on the cost of wireless service. Furthermore, some wireless providers are offering new customers price plans that undercut pricing under the customer’s service plan with its current wireless provider and provide a credit to reimburse early termination fees paid to their former wireless service provider, subject to certain limitations, in addition to promotions targeted specifically to customers of Verizon Wireless. We seek to compete in this area by offering our customers services and equipment that they will regard as the best available value for the price, as well as service plans that meet their wireless service needs.

In our Wireline segment, we have experienced continuing access line losses as customers have disconnected both primary and secondary lines and switched to alternative technologies such as wireless, voice over Internet protocol (VoIP) and cable for voice and data services. We expect to continue to experience access line losses as customers continue to switch to alternate technologies. We also expect Consumer retail revenues to increase, primarily driven by our FiOS services, as we seek to increase our penetration rates within our FiOS service areas.

Despite this challenging environment, we expect that we will be able to grow key aspects of our Wireline segment by providing network reliability, offering product bundles that include broadband Internet access, digital television and local and long distance voice services, offering more robust IP products and service, and accelerating our cloud computing and machine-to-machine strategies. We will also continue to focus on cost efficiencies to attempt to offset adverse impacts from unfavorable economic conditions and competitive pressures.

Operating Revenue

We expect to experience revenue growth in our Wireless segment in 2015, primarily as a result of continued growth in postpaid connections driven by sales of smartphones and tablets, partially offset by declining prices in response to increasing competitive pressure from other wireless carriers. We also expect the activation of devices on Verizon Edge to contribute positively to our Wireless segment revenue and operating income. In 2015, we expect the rate at which customers activate devices on Verizon Edge to increase. As more customers adopt Verizon Edge, we expect equipment and other revenue to be positively impacted, while we expect retail postpaid average revenue per account (ARPA) and service revenue, in each case when considered as a percentage of total revenue, to continue to be negatively impacted. We expect that our future service revenue growth will be substantially derived from an increase in the usage of innovative mobile services in addition to our pricing structure that will encourage customers to continue adding data-enabled devices onto existing accounts. We expect that continued emphasis on increasing smartphone penetration, including continuing to migrate customers from basic phones to smartphones and from 3G devices to 4G LTE devices, in addition to increasing our tablet penetration will positively impact our revenue.

We expect FiOS broadband and video penetration to positively impact our Mass Markets revenue and subscriber base. Although we have recently experienced decelerating revenue growth within our Strategic services business, we expect our Strategic services business to be positively impacted by additional enterprise revenues from application services, such as our cloud, security and other solutions-based services and from continued customer migration of their services to Private IP and other strategic networking services. We believe the trend in these growth areas as well as our offerings in telematics and video streaming will help offset the continuing decline in revenues in our Wireline segment related to retail voice connection losses as a result of technology substitution, as well as the continued decline in our legacy wholesale and enterprise markets. Upon the closing of the sale of our local exchange business and related landline activities in California, Florida and Texas, we expect that our Wireline segment EBITDA margin and operating income margin will decline. Prior to closing this transaction, we expect to undertake initiatives to address our cost structure to mitigate this impact to our margins.

Operating Costs and Expenses

We anticipate our overall wireless operating costs will increase as a result of the expected increase in the volume of smartphone sales, which will result in higher equipment costs. In addition, we expect content costs for our FiOS video service to continue to increase. However, we expect to achieve certain cost efficiencies in 2015 and beyond as data traffic continues to migrate to our lower-cost 4G LTE network and as we continue to streamline our business processes with a focus on improving productivity and increasing profitability.

Capital Expenditures

Our 2015 capital program includes capital to fund advanced networks and services, including 4G LTE and FiOS, the continued expansion of our core networks, including our IP and data center enhancements, and support for our copper-based legacy voice networks and other expenditures to drive operating efficiencies. The level and the timing of the Company’s capital expenditures within these broad categories can vary significantly as a result of a variety of factors outside our control, including, for example, material weather events. We are replacing copper wire with fiber-optic cable which will not alter our capital program but should result in lower maintenance costs in the future. Capital expenditures were $17.2 billion in 2014 and $16.6 billion in 2013. We believe that we have significant discretion over the amount and timing of our capital expenditures on a Company-wide basis as we are not subject to any agreement that would require significant capital expenditures on a designated schedule or upon the occurrence of designated events. We expect capital expenditures in 2015, which will be primarily focused on adding capacity to our 4G LTE network in order to stay ahead of our customers’ increasing data demands, to be in the range of approximately $17.5 billion to $18.0 billion. We also expect our capital expenditures as a percentage of revenue to decline in 2015 from 2014 levels.

Cash Flow from Operations

We create value for our shareowners by investing the cash flows generated by our business in opportunities and transactions that support continued profitable growth, thereby increasing customer satisfaction and usage of our products and services. In addition, we have used our cash flows to maintain and grow our dividend payout to shareowners. Verizon’s Board of Directors increased the Company’s quarterly dividend by 3.8% during 2014, making this the eighth consecutive year in which we have raised our dividend.

Our goal is to use our cash to create long-term value for our shareholders. We will continue to look for investment opportunities that will help us to grow the business. We expect to use our cash to reduce our debt levels in order to return to our pre-Wireless Transaction credit metrics by 2019, invest in the business, including spectrum licenses (see “Cash Flows from Investing Activities”), pay dividends to our shareholders and, when appropriate, buy back shares of our outstanding common stock (see “Cash Flows from Financing Activities”).

| Consolidated Results of Operations |

In this section, we discuss our overall results of operations and highlight items of a non-operational nature that are not included in our segment results. We have two reportable segments, Wireless and Wireline, which we operate and manage as strategic business units and organize by products and services. In “Segment Results of Operations,” we review the performance of our two reportable segments.

On February 21, 2014, we completed the acquisition of Vodafone’s indirect 45% interest in Verizon Wireless. As a result, our results reflect our 55% ownership of Verizon Wireless through the closing of the Wireless Transaction and reflect our full ownership of Verizon Wireless from the closing of the Wireless Transaction through December 31, 2014.

Corporate, eliminations and other includes unallocated corporate expenses such as certain pension and other employee benefit related costs, intersegment eliminations recorded in consolidation, the results of other businesses, such as our investments in unconsolidated businesses, lease financing as well as the historical results of divested operations, other adjustments and gains and losses that are not allocated in assessing segment performance due to their non-operational nature. Although such transactions are excluded from the business segment results, they are included in reported consolidated earnings. Gains and losses that are not individually significant are included in all segment results as these items are included in the chief operating decision maker’s assessment of segment performance. We believe that this presentation assists users of our financial statements in better understanding our results of operations and trends from period to period. Effective January 1, 2014, we have also reclassified the results of certain businesses, such as development stage businesses that support our strategic initiatives, from our Wireline segment to Corporate, eliminations and other. The impact of this reclassification was not material to our consolidated financial statements or our segment results of operations.

On July 1, 2014, our Wireline segment sold a non-strategic business (see “Acquisitions and Divestitures”). Accordingly, the historical Wireline results for these operations, which were not material to our consolidated financial statements or our segment results of operations, have been reclassified to Corporate, eliminations and other to reflect comparable segment operating results. The results of operations related to this divestiture included within Corporate, eliminations and other are as follows:

| (dollars in millions) | ||||||||||||

| Years Ended December 31, | 2014 | 2013 | 2012 | |||||||||

| Impact of Divested Operations |

||||||||||||

| Operating revenues |

$ | 256 | $ | 599 | $ | 835 | ||||||

| Cost of services and sales |

239 | 531 | 756 | |||||||||

| Selling, general and administrative expense |

5 | 25 | 23 | |||||||||

| Consolidated Revenues | ||||||||||||||

| (dollars in millions) | ||||||||||||||||||||||||||||

| Increase/(Decrease) | ||||||||||||||||||||||||||||

| Years Ended December 31, | 2014 | 2013 | 2012 | 2014 vs. 2013 | 2013 vs. 2012 | |||||||||||||||||||||||

| Wireless |

||||||||||||||||||||||||||||

| Service revenue |

$ | 72,630 | $ | 69,033 | $ | 63,733 | $ | 3,597 | 5.2 | % | $ | 5,300 | 8.3 | % | ||||||||||||||

| Equipment and other |

15,016 | 11,990 | 12,135 | 3,026 | 25.2 | (145 | ) | (1.2 | ) | |||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Total |

87,646 | 81,023 | 75,868 | 6,623 | 8.2 | 5,155 | 6.8 | |||||||||||||||||||||

| Wireline |

||||||||||||||||||||||||||||

| Mass Markets |

18,047 | 17,383 | 16,746 | 664 | 3.8 | 637 | 3.8 | |||||||||||||||||||||

| Global Enterprise |

13,684 | 14,182 | 14,577 | (498 | ) | (3.5 | ) | (395 | ) | (2.7 | ) | |||||||||||||||||

| Global Wholesale |

6,222 | 6,594 | 7,094 | (372 | ) | (5.6 | ) | (500 | ) | (7.0 | ) | |||||||||||||||||

| Other |

476 | 465 | 528 | 11 | 2.4 | (63 | ) | (11.9 | ) | |||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Total |

38,429 | 38,624 | 38,945 | (195 | ) | (0.5 | ) | (321 | ) | (0.8 | ) | |||||||||||||||||

| Corporate, eliminations and other |

1,004 | 903 | 1,033 | 101 | 11.2 | (130 | ) | (12.6 | ) | |||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Consolidated Revenues |

$ | 127,079 | $ | 120,550 | $ | 115,846 | $ | 6,529 | 5.4 | $ | 4,704 | 4.1 | ||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

2014 Compared to 2013

The increase in consolidated revenues during 2014 compared to 2013 was primarily due to higher revenues at Wireless, as well as higher Mass Markets revenues driven by FiOS services at our Wireline segment. Partially offsetting these increases were lower Global Enterprise Core and Global Wholesale revenues at our Wireline segment.

Wireless’ revenues increased $6.6 billion, or 8.2%, during 2014 compared to 2013 primarily as a result of growth in service revenue and equipment revenue. The increase in service revenue, which does not include recurring equipment installment billings related to Verizon Edge, during 2014 compared to 2013 was primarily driven by higher retail postpaid service revenue, which increased largely as a result of an increase in retail postpaid connections as well as the continued increase in penetration of 4G LTE smartphones and tablets through our More Everything plans. Equipment and other revenue increased during 2014 compared to 2013 primarily due to an increase in equipment sales under both the traditional subsidy model and Verizon Edge. Retail postpaid connection net additions increased during 2014 compared to 2013 primarily due to an increase in retail postpaid connection gross additions partially offset by an increase in our retail postpaid connection churn rate. Retail postpaid connections per account increased as of December 31, 2014 compared to December 31, 2013 primarily due to the increased penetration of tablets.

Wireline’s revenues decreased $0.2 billion, or 0.5%, during 2014 compared to 2013 primarily as a result of declines in Global Enterprise Core and Global Wholesale, partially offset by higher Mass Markets revenues driven by FiOS services and increased Strategic services revenues within Global Enterprise.

Mass Markets revenues increased $0.7 billion, or 3.8%, during 2014 compared to 2013 primarily due to the expansion of FiOS services (Voice, Internet and Video), including our FiOS Quantum offerings, as well as changes in our pricing strategies, partially offset by the continued decline of local exchange revenues.

Global Enterprise revenues decreased $0.5 billion, or 3.5%, during 2014 compared to 2013 primarily due to lower voice services and data networking revenues, the contraction of market rates due to competition and a decline in Core customer premise equipment revenues. This decrease was partially offset by an increase in Strategic services revenues, primarily due to growth in our application services, such as our cloud and data center offerings and contact center solutions.

Global Wholesale revenues decreased $0.4 billion, or 5.6%, during 2014 compared to 2013 primarily due to a decline in data revenues driven by the continuing demand for high-speed digital data services from fiber-to-the-cell customers upgrading their core data circuits to Ethernet facilities, as well as a decline in traditional voice revenues. During 2014, we also experienced a decline in domestic wholesale connections.

2013 Compared to 2012

The increase in consolidated revenues during 2013 compared to 2012 was primarily due to higher revenues at Wireless, as well as higher Mass Markets revenues driven by FiOS services and increased Strategic services revenues within Global Enterprise at our Wireline segment. Partially offsetting these increases were lower Global Enterprise Core and Global Wholesale revenues at our Wireline segment.

Wireless’ revenues increased $5.2 billion, or 6.8%, during 2013 compared to 2012 due to growth in service revenue. Service revenue increased during 2013 compared to 2012 primarily driven by higher retail postpaid service revenue, which increased largely as a result of an increase in retail postpaid connections as well as the continued increase in penetration of smartphones, tablets and other Internet devices through our Share Everything plans. Retail postpaid connection net additions decreased during 2013 compared to 2012 primarily due to an increase in our retail postpaid connection churn rate, partially offset by an increase in retail postpaid connection gross additions. Retail postpaid connections per account increased as of December 31, 2013 compared to December 31, 2012 primarily due to the increased penetration of tablets and other Internet devices.

Wireline’s revenues decreased $0.3 billion, or 0.8%, during 2013 compared to 2012 primarily driven by declines in Global Enterprise Core and Global Wholesale, partially offset by higher Mass Markets revenues driven by FiOS services and increased Strategic services revenues within Global Enterprise.

Mass Markets revenues increased $0.6 billion, or 3.8%, during 2013 compared to 2012 due to the expansion of FiOS services (Voice, Internet and Video) as well as changes in our pricing strategies, partially offset by the continued decline of local exchange revenues.

Global Enterprise revenues decreased $0.4 billion, or 2.7%, during 2013 compared to 2012 primarily due to a decline in Core customer premise equipment revenues and lower voice services and data networking revenues. This decrease was partially offset by growth in Strategic services revenues, primarily due to an increase in advanced services, such as contact center solutions, IP communications, and our cloud and data center offerings as well as revenue from a telematics services business that we acquired in the third quarter of 2012.

Global Wholesale revenues decreased $0.5 billion, or 7.0%, during 2013 compared to 2012 primarily due to a decline in traditional voice revenues as a result of decreased minutes of use (MOUs) and a decline in domestic wholesale connections, partially offset by continuing demand for high-speed digital data services from fiber-to-the-cell customers upgrading their core data circuits to Ethernet facilities as well as Ethernet migrations from other core customers.

Other revenues decreased during 2013 compared to 2012 primarily due to reduced volumes outside of our network footprint.

| Consolidated Operating Expenses |

|

|

(dollars in millions) |

| ||||||||||||||||||||||||||

| Increase/(Decrease) | ||||||||||||||||||||||||||||

| Years Ended December 31, | 2014 | 2013 | 2012 | 2014 vs. 2013 | 2013 vs. 2012 | |||||||||||||||||||||||

| Cost of services and sales |

$ | 49,931 | $ | 44,887 | $ | 46,275 | $ | 5,044 | 11.2 | % | $ (1,388) | (3.0 | )% | |||||||||||||||

| Selling, general and administrative expense |

41,016 | 27,089 | 39,951 | 13,927 | 51.4 | (12,862) | (32.2 | ) | ||||||||||||||||||||

| Depreciation and amortization expense |

16,533 | 16,606 | 16,460 | (73 | ) | (0.4 | ) | 146 | 0.9 | |||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Consolidated Operating Expenses |

$ | 107,480 | $ | 88,582 | $ | 102,686 | $ | 18,898 | 21.3 | $ (14,104) | (13.7 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

Consolidated operating expenses increased during 2014 primarily due to non-operational charges recorded in 2014 as compared to non-operational credits recorded in 2013 (see “Other Items”) as well as increased operating expenses at Wireless. Consolidated operating expenses decreased during 2013 primarily due to non-operational credits recorded in 2013 as compared to non-operational charges recorded in 2012 (see “Other Items”).

2014 Compared to 2013

Cost of Services and Sales

Cost of services and sales includes the following costs directly attributable to a service or product: salaries and wages, benefits, materials and supplies, content costs, contracted services, network access and transport costs, wireless equipment costs, customer provisioning costs, computer systems support, costs to support our outsourcing contracts and technical facilities and contributions to the Universal Service Fund. Aggregate customer care costs, which include billing and service provisioning, are allocated between Cost of services and sales and Selling, general and administrative expense.

Cost of services and sales increased during 2014 compared to 2013 primarily due to an increase in cost of equipment sales of $5.3 billion at our Wireless segment as a result of an increase in the number of devices sold as well as an increase in the cost per unit.

Selling, General and Administrative Expense

Selling, general and administrative expense includes: salaries and wages and benefits not directly attributable to a service or product, bad debt charges, taxes other than income taxes, advertising and sales commission costs, customer billing, call center and information technology costs, regulatory fees, professional service fees, and rent and utilities for administrative space. Also included are a portion of the aggregate customer care costs as discussed in “Cost of Services and Sales” above.

Selling, general and administrative expense increased during 2014 compared to 2013 primarily due to non-operational charges, primarily severance, pension and benefit charges, recorded in 2014 as compared to non-operational credits, primarily severance, pension and benefit credits, recorded in 2013 (see “Other Items”).

Depreciation and Amortization Expense

Depreciation and amortization expense decreased during 2014 compared to 2013 primarily due to a decrease in net depreciable assets at our Wireline segment, partially offset by an increase in depreciable assets at our Wireless segment.

2013 Compared to 2012

Cost of Services and Sales

Cost of services and sales decreased during 2013 compared to 2012 primarily due to a decrease in cost of equipment sales, decreased data roaming, a decline in cost of data services and a decrease in network connection costs at our Wireless segment, as well as a decrease in costs related to customer premise equipment, a decline in access costs and the net effect of storm-related insurance recoveries at our Wireline segment. Partially offsetting these decreases were higher content costs associated with continued FiOS subscriber growth and programming license fee increases at our Wireline segment, as well as increases in cost of network services at our Wireless segment.

Selling, General and Administrative Expense

Selling, general and administrative expense decreased during 2013 compared to 2012 primarily due to the non-operational credits recorded in 2013 and declines in employee costs at our Wireline segment as well as the non-operational charges recorded in 2012 (see “Other Items”). This decrease was partially offset by higher sales commission expense at our Wireless segment.

Depreciation and Amortization Expense

Depreciation and amortization expense increased during 2013 compared to 2012 primarily due to an increase in net depreciable assets at our Wireless segment and an increase in amortization expense at our Wireline segment. These increases were partially offset by a decline in net depreciable assets at our Wireline segment.

Non-operational (Credits) Charges

Non-operational (credits) charges included in operating expenses (see “Other Items”) were as follows:

| (dollars in millions) | ||||||||||||

| Years Ended December 31, | 2014 | 2013 | 2012 | |||||||||

| Severance, Pension and Benefit (Credits) Charges |

||||||||||||

| Selling, general and administrative expense |

$ | 7,507 | $ | (6,232) | $ | 7,186 | ||||||

| Gain on Spectrum License Transactions |

||||||||||||

| Selling, general and administrative expense |

(707 | ) | (278) | – | ||||||||

| Litigation Settlements |

||||||||||||

| Selling, general and administrative expense |

– | – | 384 | |||||||||

| Other Costs |

||||||||||||

| Cost of services and sales |

27 | – | 40 | |||||||||

| Selling, general and administrative expense |

307 | – | 236 | |||||||||

|

|

|

|||||||||||

| 334 | – | 276 | ||||||||||

|

|

|

|||||||||||

| Total non-operating (credits) charges included in operating expenses |

$ | 7,134 | $ | (6,510) | $ | 7,846 | ||||||

|

|

|

|||||||||||

See “Other Items” for a description of these and other non-operational items.

Consolidated Operating Income and EBITDA

Consolidated earnings before interest, taxes, depreciation and amortization expenses (Consolidated EBITDA) and Consolidated Adjusted EBITDA, which are presented below, are non-GAAP measures and do not purport to be alternatives to operating income as a measure of operating performance. Management believes that these measures are useful to investors and other users of our financial information in evaluating operating profitability on a more variable cost basis as they exclude the depreciation and amortization expense related primarily to capital expenditures and acquisitions that occurred in prior years, as well as in evaluating operating performance in relation to our competitors. Consolidated EBITDA is calculated by adding back interest, taxes, depreciation and amortization expense, equity in earnings of unconsolidated businesses and other income and (expense), net to net income.

Consolidated Adjusted EBITDA is calculated by excluding the effect of non-operational items and the impact of divested operations from the calculation of Consolidated EBITDA. Management believes that this measure provides additional relevant and useful information to investors and other users of our financial data in evaluating the effectiveness of our operations and underlying business trends in a manner that is consistent with management’s evaluation of business performance. See “Other Items” for additional details regarding these non-operational items.

Operating expenses include pension and benefit related credits and/or charges based on actuarial assumptions, including projected discount rates and an estimated return on plan assets. These estimates are updated in the fourth quarter to reflect actual return on plan assets and updated actuarial assumptions. The adjustment has been recognized in the income statement during the fourth quarter or upon a remeasurement event pursuant to our accounting policy for the recognition of actuarial gains/losses.

It is management’s intent to provide non-GAAP financial information to enhance the understanding of Verizon’s GAAP financial information, and it should be considered by the reader in addition to, but not instead of, the financial statements prepared in accordance with GAAP. Each non-GAAP financial measure is presented along with the corresponding GAAP measure so as not to imply that more emphasis should be placed on the non-GAAP measure. The non-GAAP financial information presented may be determined or calculated differently by other companies.

| (dollars in millions) | ||||||||||||

| Years Ended December 31, | 2014 | 2013 | 2012 | |||||||||

| Consolidated Operating Income |

$ | 19,599 | $ | 31,968 | $ | 13,160 | ||||||

| Add Depreciation and amortization expense |

16,533 | 16,606 | 16,460 | |||||||||

|

|

|

|||||||||||

| Consolidated EBITDA |

36,132 | 48,574 | 29,620 | |||||||||

| Add (Less) Non-operating (credits) charges included in operating expenses |

7,134 | (6,510 | ) | 7,846 | ||||||||

| Less Impact of divested operations |

(12 | ) | (43 | ) | (56 | ) | ||||||

|

|

|

|||||||||||

| Consolidated Adjusted EBITDA |

$ | 43,254 | $ | 42,021 | $ | 37,410 | ||||||

|

|

|

|||||||||||

The changes in Consolidated Operating Income, Consolidated EBITDA and Consolidated Adjusted EBITDA in the table above were primarily a result of the factors described in connection with operating revenues and operating expenses.

| Other Consolidated Results |

Equity in Earnings of Unconsolidated Businesses

Equity in earnings of unconsolidated businesses increased $1.6 billion during 2014 compared to the similar period in 2013 primarily due to the gain of $1.9 billion recorded on the sale of our interest in Vodafone Omnitel N.V. (Vodafone Omnitel) during the first quarter of 2014, which was part of the consideration for the Wireless Transaction.

Equity in earnings of unconsolidated businesses decreased $0.2 billion, or 56.2%, in 2013 compared to 2012 primarily due to lower earnings from operations at Vodafone Omnitel. The decrease during 2013 was partially offset by an immaterial gain recorded by Verizon Wireless upon obtaining control of previously unconsolidated wireless partnerships, which were previously accounted for under the equity method and are now consolidated.

Other Income and (Expense), Net

Additional information relating to Other income and (expense), net is as follows:

| (dollars in millions) | ||||||||||||||||||||||||||||

| Increase/(Decrease) | ||||||||||||||||||||||||||||

| Years Ended December 31, | 2014 | 2013 | 2012 | 2014 vs. 2013 | 2013 vs. 2012 | |||||||||||||||||||||||

| Interest income |

$ | 108 | $ | 64 | $ | 57 | $ | 44 | 68.8 | % | $ | 7 | 12.3 | % | ||||||||||||||

| Other, net |

(1,302 | ) | (230 | ) | (1,073 | ) | (1,072 | ) | nm | 843 | (78.6 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Total |

$ | (1,194 | ) | $ | (166 | ) | $ | (1,016 | ) | $ | (1,028 | ) | nm | $ | 850 | (83.7 | ) | |||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

nm – not meaningful

Other income and (expense), net changed unfavorably during 2014 compared to the similar period in 2013 primarily due to early debt redemption costs of $1.4 billion incurred in 2014 (see “Other Items”).

Other income and (expense), net changed favorably during 2013 compared to 2012 primarily due to fees of $1.1 billion incurred in 2012 related to the early redemption of debt, partially offset by $0.2 billion of fees incurred during the fourth quarter of 2013 as a result of the termination of a bridge credit agreement upon the effectiveness of a term loan agreement (see “Other Items”).

Interest Expense

| (dollars in millions) | ||||||||||||||||||||||||||||

| Increase/(Decrease) | ||||||||||||||||||||||||||||

| Years Ended December 31, | 2014 | 2013 | 2012 | 2014 vs. 2013 | 2013 vs. 2012 | |||||||||||||||||||||||

| Total interest costs on debt balances |

$ | 5,291 | $ | 3,421 | $ | 2,977 | $ | 1,870 | 54.7 | % | $ | 444 | 14.9 | % | ||||||||||||||

| Less Capitalized interest costs |

376 | 754 | 406 | (378 | ) | (50.1 | ) | 348 | 85.7 | |||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Total |

$ | 4,915 | $ | 2,667 | $ | 2,571 | $ | 2,248 | 84.3 | $ | 96 | 3.7 | ||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Average debt outstanding |

$ | 108,461 | $ | 65,959 | $ | 52,949 | ||||||||||||||||||||||

| Effective interest rate |

4.9 | % | 5.2 | % | 5.6 | % | ||||||||||||||||||||||

Total interest costs on debt balances increased during 2014 compared to 2013 primarily due to the issuance of fixed and floating rate notes to finance the Wireless Transaction (see “Acquisitions and Divestitures”) resulting in an increase in average debt and a corresponding increase in interest expense, partially offset by a lower effective interest rate (see “Consolidated Financial Condition”). Capitalized interest costs were lower in 2014 primarily due to a decrease in wireless licenses that are currently under development, which was due to the deployment of AWS licenses for commercial service during 2014.

Total interest costs on debt balances increased during 2013 compared to 2012 primarily due to the issuance of $49.0 billion of fixed and floating rate notes to finance the Wireless Transaction (see “Acquisitions and Divestitures”) resulting in an increase in average debt as well as an incremental increase in interest expense of $0.7 billion, partially offset by a lower effective interest rate (see “Consolidated Financial Condition”). Capitalized interest costs were higher in 2013 primarily due to increases in wireless licenses that are currently under development.

Provision (Benefit) for Income Taxes

| (dollars in millions) | ||||||||||||||||||||||||||||

| Increase/(Decrease) | ||||||||||||||||||||||||||||

| Years Ended December 31, | 2014 | 2013 | 2012 | 2014 vs. 2013 | 2013 vs. 2012 | |||||||||||||||||||||||

| Provision (Benefit) for income taxes |

$ | 3,314 | $ | 5,730 | $ | (660) | $ | (2,416) | (42.2 | )% | $ | 6,390 | nm | |||||||||||||||

| Effective income tax rate |

21.7 | % | 19.6 | % | (6.7) | % | ||||||||||||||||||||||

nm – not meaningful

The effective income tax rate is calculated by dividing the provision for income taxes by income before the provision for income taxes. The effective income tax rate for 2014 was 21.7% compared to 19.6% for 2013. The increase in the effective income tax rate was primarily due to additional income taxes on the incremental income from the Wireless Transaction completed on February 21, 2014 and was partially offset by the utilization of certain tax credits in connection with the Omnitel Transaction in 2014 and the effective income tax rate impact of lower income before income taxes due to severance, pension and benefit charges recorded in 2014 compared to severance, pension and benefit credits recorded in 2013. The decrease in the provision for income taxes was primarily due to lower income before income taxes due to severance, pension and benefit charges recorded in 2014 compared to severance, pension and benefit credits recorded in 2013.

The effective income tax rate for 2013 was 19.6% compared to (6.7)% for 2012. The increase in the effective income tax rate and provision for income taxes was primarily due to higher income before income taxes as a result of severance, pension and benefit credits recorded during 2013 compared to lower income before income taxes as a result of severance, pension and benefit charges as well as early debt redemption costs recorded during 2012.

Our effective income tax rate differed significantly from the statutory federal income tax rate for 2013 and 2012 due to the inclusion of income attributable to Vodafone’s noncontrolling interest in the Verizon Wireless partnership for the full year within our income before the provision for income taxes. In 2013, we recorded a tax provision on income before the provision for income taxes and when we included the income attributable to Vodafone’s noncontrolling interest in the Verizon Wireless partnership in our income before the provision for income taxes it resulted in our effective income tax rate being 13.7 percentage points lower during 2013. In 2012, we recorded a tax benefit on income before the provision for income taxes, which resulted in a negative effective income tax rate. In this circumstance, including the income attributable to Vodafone’s noncontrolling interest in the Verizon Wireless partnership in our income before the provision for income taxes resulted in our negative effective tax rate being 300.3 percentage points higher during 2012.

A reconciliation of the statutory federal income tax rate to the effective income tax rate for each period is included in Note 13 to the consolidated financial statements.

Net Income Attributable to Noncontrolling Interests

| (dollars in millions) | ||||||||||||||||||||||||||||

| Increase/(Decrease) | ||||||||||||||||||||||||||||

| Years Ended December 31, | 2014 | 2013 | 2012 | 2014 vs. 2013 | 2013 vs. 2012 | |||||||||||||||||||||||

| Net income attributable to noncontrolling interests |

$ | 2,331 | $ | 12,050 | $ | 9,682 | $ (9,719 | ) | (80.7 | )% | $ | 2,368 | 24.5 | % | ||||||||||||||

The decrease in Net income attributable to noncontrolling interests during 2014 compared to 2013 was primarily due to the completion of the Wireless Transaction on February 21, 2014. As a result, our results reflect our 55% ownership interest of Verizon Wireless through the closing of the Wireless Transaction and reflect our full ownership of Verizon Wireless for the remainder of the year. The noncontrolling interests that remained after the completion of the Wireless Transaction primarily relate to wireless partnership entities.

The increase in Net income attributable to noncontrolling interests during 2013 compared to 2012 was due to higher earnings in our Verizon Wireless segment, which had a 45% noncontrolling partnership interest attributable to Vodafone as of December 31, 2013.

| Segment Results of Operations |

We have two reportable segments, Wireless and Wireline, which we operate and manage as strategic business units and organize by products and services. We measure and evaluate our reportable segments based on segment operating income. The use of segment operating income is consistent with the chief operating decision maker’s assessment of segment performance.

Segment earnings before interest, taxes, depreciation and amortization (Segment EBITDA), which is presented below, is a non-GAAP measure and does not purport to be an alternative to operating income as a measure of operating performance. Management believes that this measure is useful to investors and other users of our financial information in evaluating operating profitability on a more variable cost basis as it excludes the depreciation and amortization expenses related primarily to capital expenditures and acquisitions that occurred in prior years, as well as in evaluating operating performance in relation to our competitors. Segment EBITDA is calculated by adding back depreciation and amortization expense to segment operating income.

Wireless EBITDA margin is calculated by dividing Wireless EBITDA by total Wireless revenues. Wireless Segment EBITDA service margin, also presented below, is calculated by dividing Wireless Segment EBITDA by Wireless service revenues. Wireless Segment EBITDA service margin utilizes service revenues rather than total revenues. Service revenues primarily exclude equipment revenues in order to reflect the impact of providing service to the wireless customer base on an ongoing basis. Wireline EBITDA margin is calculated by dividing Wireline EBITDA by total Wireline revenues. You can find additional information about our segments in Note 14 to the consolidated financial statements.

| Wireless |

Our Wireless segment is primarily comprised of Cellco Partnership doing business as Verizon Wireless. Cellco Partnership was formed as a joint venture in April 2000 by the combination of the U.S. wireless operations and interests of Verizon and Vodafone. Prior to the completion of the Wireless Transaction, Verizon owned a controlling 55% interest in Verizon Wireless and Vodafone owned the remaining 45%. On February 21, 2014, the Wireless Transaction was completed and Verizon acquired 100% ownership of Verizon Wireless. Verizon Wireless provides wireless communications services across one of the most extensive wireless networks in the United States.

We provide these services and equipment sales to consumer, business and government customers in the United States on a postpaid and prepaid basis. Postpaid connections represent individual lines of service for which a customer is billed in advance a monthly access charge in return for a monthly network service allowance, and usage beyond the allowance is billed monthly in arrears. Our prepaid service enables individuals to obtain wireless services without a long-term contract or credit verification by paying for all services in advance.

All financial results included in the tables below reflect the consolidated results of Verizon Wireless.

Operating Revenues and Selected Operating Statistics

| (dollars in millions, except ARPA) | ||||||||||||||||||||||||||||

| Increase/(Decrease) | ||||||||||||||||||||||||||||

| Years Ended December 31, | 2014 | 2013 | 2012 | 2014 vs. 2013 | 2013 vs. 2012 | |||||||||||||||||||||||

| Retail service |

$ | 69,501 | $ | 66,334 | $ | 61,440 | $ | 3,167 | 4.8 | % | $ | 4,894 | 8.0 | % | ||||||||||||||

| Other service |

3,129 | 2,699 | 2,293 | 430 | 15.9 | 406 | 17.7 | |||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Service revenue |

72,630 | 69,033 | 63,733 | 3,597 | 5.2 | 5,300 | 8.3 | |||||||||||||||||||||

| Equipment |

10,959 | 8,111 | 8,023 | 2,848 | 35.1 | 88 | 1.1 | |||||||||||||||||||||

| Other |

4,057 | 3,879 | 4,112 | 178 | 4.6 | (233 | ) | (5.7 | ) | |||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Equipment and other |

15,016 | 11,990 | 12,135 | 3,026 | 25.2 | (145 | ) | (1.2 | ) | |||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Total Operating Revenues |

$ | 87,646 | $ | 81,023 | $ | 75,868 | $ | 6,623 | 8.2 | $ | 5,155 | 6.8 | ||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Connections (‘000):(1) |

||||||||||||||||||||||||||||

| Retail connections |

108,211 | 102,799 | 98,230 | 5,412 | 5.3 | 4,569 | 4.7 | |||||||||||||||||||||

| Retail postpaid connections |

102,079 | 96,752 | 92,530 | 5,327 | 5.5 | 4,222 | 4.6 | |||||||||||||||||||||

| Net additions in period (‘000):(2) |

||||||||||||||||||||||||||||

| Retail connections |

5,568 | 4,472 | 5,917 | 1,096 | 24.5 | (1,445 | ) | (24.4 | ) | |||||||||||||||||||

| Retail postpaid connections |

5,482 | 4,118 | 5,024 | 1,364 | 33.1 | (906 | ) | (18.0 | ) | |||||||||||||||||||

| Churn Rate: |

||||||||||||||||||||||||||||

| Retail connections |

1.33 | % | 1.27 | % | 1.19 | % | ||||||||||||||||||||||

| Retail postpaid connections |

1.04 | % | 0.97 | % | 0.91 | % | ||||||||||||||||||||||

| Account Statistics: |

||||||||||||||||||||||||||||

| Retail postpaid ARPA |

$ | 159.86 | $ | 153.93 | $ | 144.04 | $ | 5.93 | 3.9 | $ | 9.89 | 6.9 | ||||||||||||||||

| Retail postpaid accounts (‘000)(1) |

35,616 | 35,083 | 35,057 | 533 | 1.5 | 26 | 0.1 | |||||||||||||||||||||

| Retail postpaid connections per account(1) |

2.87 | 2.76 | 2.64 | 0.11 | 4.0 | 0.12 | 4.5 | |||||||||||||||||||||

| (1) | As of end of period |

| (2) | Excluding acquisitions and adjustments |

2014 Compared to 2013

Wireless’ total operating revenues increased by $6.6 billion, or 8.2%, during 2014 compared to 2013 primarily as a result of growth in service revenue and equipment revenue.

Accounts and Connections

Retail (non-wholesale) postpaid accounts primarily represent retail customers under contract with Verizon Wireless that are directly served and managed by Verizon Wireless and use its branded services. Accounts include More Everything plans and corporate accounts, as well as legacy single connection plans and family plans. A single account may include monthly wireless services for a variety of connected devices. Retail connections represent our retail customer device connections. Churn is the rate at which service to connections is terminated.

Retail connections under an account may include: smartphones, basic phones, tablets, LTE Internet (Installed) and other connected devices. Retail postpaid connection net additions increased during 2014 compared to 2013 primarily due to an increase in retail postpaid connection gross additions partially offset by an increase in our retail postpaid connection churn rate. Higher retail postpaid connection gross additions were driven by gross additions of tablets as well as 4G LTE smartphones. During 2014, our retail postpaid connection net additions included approximately 4.2 million tablets as compared to 1.4 million tablets in 2013.

Retail Postpaid Connections per Account

Retail postpaid connections per account is calculated by dividing the total number of retail postpaid connections by the number of retail postpaid accounts as of the end of the period. Retail postpaid connections per account increased 4.0% as of December 31, 2014 compared to December 31, 2013 primarily due to the increased penetration of tablets.

Service Revenue

Service revenue, which does not include recurring equipment installment billings related to Verizon Edge, increased by $3.6 billion, or 5.2%, during 2014 compared to 2013 primarily driven by higher retail postpaid service revenue, which increased largely as a result of an increase in retail postpaid connections as well as the continued increase in penetration of 4G LTE smartphones and tablets through our More Everything plans. The penetration of 4G LTE smartphones was driven by the activation of smartphones by new customers as well as existing customers migrating from basic phones and 3G smartphones to 4G LTE smartphones.

The increase in retail postpaid ARPA (the average revenue per account from retail postpaid accounts), which does not include recurring equipment installment billings related to Verizon Edge, during 2014 compared to 2013 was primarily driven by increases in smartphone penetration and retail postpaid connections per account. As of December 31, 2014, we experienced a 4.0% increase in retail postpaid connections per account compared to 2013, with smartphones representing 79% of our retail postpaid phone base as of December 31, 2014 compared to 70% as of December 31, 2013. The increased penetration in retail postpaid connections per account is primarily due to increases in Internet data devices, which represented 14.1% of our retail postpaid connection base as of December 31, 2014 compared to 10.7% as of December 31, 2013, primarily due to tablet activations. Additionally, during 2014, postpaid smartphone activations represented 92% of phones activated compared to 86% during 2013.

Other service revenue increased during 2014 compared to 2013 due to growth in wholesale connections.

Equipment and Other Revenue

Equipment and other revenue increased during 2014 compared to 2013 primarily due to an increase in equipment sales under both the traditional subsidy model and Verizon Edge.

2013 Compared to 2012

The increase in Wireless’ total operating revenues of $5.2 billion, or 6.8%, during 2013 compared to 2012 was primarily the result of growth in service revenue.

Accounts and Connections

Retail postpaid connection net additions decreased during 2013 compared to 2012 primarily due to an increase in our retail postpaid connection churn rate, partially offset by an increase in retail postpaid connection gross additions.

Retail Postpaid Connections per Account

Retail postpaid connections per account increased 4.5% as of December 31, 2013 compared to December 31, 2012 primarily due to the increased penetration of tablets and other Internet devices.

Service Revenue

Service revenue increased $5.3 billion, or 8.3%, during 2013 compared to 2012 primarily driven by higher retail postpaid service revenue, which increased largely as a result of an increase in retail postpaid connections as well as the continued increase in penetration of smartphones, tablets and other Internet devices through our Share Everything plans. The penetration of smartphones was driven by the activation of smartphones by new customers as well as existing customers migrating from basic phones to smartphones.

The increase in retail postpaid ARPA during 2013 compared to 2012 was primarily driven by increases in smartphone penetration and retail postpaid connections per account. As of December 31, 2013, we experienced a 4.5% increase in retail postpaid connections per account compared to 2012, with smartphones representing 70% of our retail postpaid phone base as of December 31, 2013 compared to 58% as of December 31, 2012. The increased penetration in retail postpaid connections per account is primarily due to increases in Internet data devices, which represented 10.7% of our retail postpaid connection base as of December 31, 2013 compared to 9.3% as of December 31, 2012, primarily due to activations of tablets and other Internet devices. Additionally, during 2013, postpaid smartphone activations represented 86% of phones activated compared to 77% during 2012.

Other service revenue increased during 2013 compared to 2012 due to growth in wholesale connections, partially offset by a decrease in revenue related to third party roaming.

Equipment and Other Revenue

Equipment and other revenue decreased during 2013 compared to 2012 as a decline in regulatory fees was partially offset by an increase in revenue related to upgrade fees.

Operating Expenses

| (dollars in millions) | ||||||||||||||||||||||||||||

| Increase/(Decrease) | ||||||||||||||||||||||||||||

| Years Ended December 31, | 2014 | 2013 | 2012 | 2014 vs. 2013 | 2013 vs. 2012 | |||||||||||||||||||||||

| Cost of services and sales |

$ | 28,825 | $ | 23,648 | $ | 24,490 | $ | 5,177 | 21.9 | % | $ | (842 | ) | (3.4 | )% | |||||||||||||

| Selling, general and administrative expense |

23,602 | 23,176 | 21,650 | 426 | 1.8 | 1,526 | 7.0 | |||||||||||||||||||||

| Depreciation and amortization expense |

8,459 | 8,202 | 7,960 | 257 | 3.1 | 242 | 3.0 | |||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Total Operating Expenses |

$ | 60,886 | $ | 55,026 | $ | 54,100 | $ | 5,860 | 10.6 | $ | 926 | 1.7 | ||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

Cost of Services and Sales

Cost of services and sales increased during 2014 compared to 2013 primarily due to an increase in cost of equipment sales of $5.3 billion as a result of an increase in the number of devices sold as well as an increase in the cost per unit. The increase in the number of devices sold was driven, in part, by the launch of new devices.

Cost of services and sales decreased during 2013 compared to 2012 primarily due to a decrease in cost of equipment sales of $0.4 billion, which was partially due to a decline in postpaid upgrades, decreased data roaming, a decline in cost of data services and a decrease in network connection costs due to the deployment of Ethernet backhaul facilities primarily targeted at sites upgrading to 4G LTE, partially offset by an increase in cost of network services.

Selling, General and Administrative Expense

Selling, general and administrative expense increased during 2014 compared to 2013 primarily due to a $0.2 billion increase in advertising expense and gains recorded in the first quarter of 2013 related to wireless license exchange agreements, partially offset by a decline in sales commission expense, which was driven by the adoption of Verizon Edge.

Selling, general and administrative expense increased during 2013 compared to 2012 primarily due to higher sales commission expense in our indirect channel. Indirect sales commission expense increased $1.1 billion during 2013 compared to 2012 primarily as a result of increases in indirect gross additions and upgrades, as well as the average commission per unit, as the mix of units continues to shift toward smartphones and more customers activate data services.

Depreciation and Amortization Expense

The increase in depreciation and amortization expense during 2014 compared to 2013, and 2013 compared to 2012, respectively, was primarily driven by an increase in net depreciable assets.

Segment Operating Income and EBITDA

| (dollars in millions) | ||||||||||||||||||||||||||||

| Increase/(Decrease) | ||||||||||||||||||||||||||||

| Years Ended December 31, | 2014 | 2013 | 2012 | 2014 vs. 2013 | 2013 vs. 2012 | |||||||||||||||||||||||

| Segment Operating Income |

$ | 26,760 | $ | 25,997 | $ | 21,768 | $ | 763 | 2.9 | % | $ | 4,229 | 19.4 | % | ||||||||||||||

| Add Depreciation and amortization expense |

8,459 | 8,202 | 7,960 | 257 | 3.1 | 242 | 3.0 | |||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Segment EBITDA |

$ | 35,219 | $ | 34,199 | $ | 29,728 | $ | 1,020 | 3.0 | $ | 4,471 | 15.0 | ||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Segment operating income margin |

30.5 | % | 32.1 | % | 28.7 | % | ||||||||||||||||||||||

| Segment EBITDA margin |

40.2 | % | 42.2 | % | 39.2 | % | ||||||||||||||||||||||

| Segment EBITDA service margin |

48.5 | % | 49.5 | % | 46.6 | % | ||||||||||||||||||||||

The changes in the table above during the periods presented were primarily a result of the factors described in connection with operating revenues and operating expenses.

Non-operational items excluded from Wireless’ Operating income were as follows:

| (dollars in millions) | ||||||||||||

| Years Ended December 31, | 2014 | 2013 | 2012 | |||||||||

| Gain on spectrum license transactions |

$ | (707 | ) | $ | (278 | ) | $ | – | ||||

| Severance, pension and benefit (credits) charges |

86 | (61 | ) | 37 | ||||||||

| Other costs |

109 | – | – | |||||||||

|

|

|

|||||||||||

| $ | (512 | ) | $ | (339 | ) | $ | 37 | |||||

|

|

|

|||||||||||

| Wireline |

Our Wireline segment provides voice, data and video communications products and enhanced services, including broadband video and data, corporate networking solutions, data center and cloud services, security and managed network services and local and long distance voice services. We provide these products and services to consumers in the United States, as well as to carriers, businesses and government customers both in the United States and around the world.

On July 1, 2014, our Wireline segment sold a non-strategic business (see “Acquisitions and Divestitures”). Accordingly, the historical Wireline results for these operations, which were not material to our consolidated financial statements or our segment results of operations, have been reclassified to Corporate, eliminations and other to reflect comparable segment operating results.

Operating Revenues and Selected Operating Statistics

| (dollars in millions) | ||||||||||||||||||||||||||||

| Increase/(Decrease) | ||||||||||||||||||||||||||||

| Years Ended December 31, | 2014 | 2013 | 2012 | 2014 vs. 2013 | 2013 vs. 2012 | |||||||||||||||||||||||

| Consumer retail |

$ | 15,583 | $ | 14,842 | $ | 14,145 | $ | 741 | 5.0 | % | $ | 697 | 4.9 | % | ||||||||||||||

| Small business |

2,464 | 2,541 | 2,601 | (77 | ) | (3.0 | ) | (60 | ) | (2.3 | ) | |||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Mass Markets |

18,047 | 17,383 | 16,746 | 664 | 3.8 | 637 | 3.8 | |||||||||||||||||||||

| Strategic services |

8,326 | 8,140 | 7,737 | 186 | 2.3 | 403 | 5.2 | |||||||||||||||||||||

| Core |

5,358 | 6,042 | 6,840 | (684 | ) | (11.3 | ) | (798 | ) | (11.7 | ) | |||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Global Enterprise |

13,684 | 14,182 | 14,577 | (498 | ) | (3.5 | ) | (395 | ) | (2.7 | ) | |||||||||||||||||

| Global Wholesale |

6,222 | 6,594 | 7,094 | (372 | ) | (5.6 | ) | (500 | ) | (7.0 | ) | |||||||||||||||||

| Other |

476 | 465 | 528 | 11 | 2.4 | (63 | ) | (11.9 | ) | |||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Total Operating Revenues |

$ | 38,429 | $ | 38,624 | $ | 38,945 | $ | (195 | ) | (0.5 | ) | $ | (321 | ) | (0.8 | ) | ||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||

| Connections (‘000):(1) |

||||||||||||||||||||||||||||

| Total voice connections |

19,795 | 21,085 | 22,503 | (1,290 | ) | (6.1 | ) | (1,418 | ) | (6.3 | ) | |||||||||||||||||

| Total Broadband connections |

9,205 | 9,015 | 8,795 | 190 | 2.1 | 220 | 2.5 | |||||||||||||||||||||

| FiOS Internet subscribers |

6,616 | 6,072 | 5,424 | 544 | 9.0 | 648 | 11.9 | |||||||||||||||||||||

| FiOS Video subscribers |

5,649 | 5,262 | 4,726 | 387 | 7.4 | 536 | 11.3 | |||||||||||||||||||||

| (1) | As of end of period |

Wireline’s revenues decreased $0.2 billion, or 0.5%, during 2014 compared to 2013 primarily driven by declines in Global Enterprise Core and Global Wholesale, partially offset by higher Consumer retail revenues driven by FiOS services and increased Strategic services revenues within Global Enterprise.

Mass Markets

Mass Markets operations provide broadband services (including high-speed Internet, FiOS Internet and FiOS Video services), local exchange (basic service and end-user access) and long distance (including regional toll) voice services to residential and small business subscribers.

2014 Compared to 2013

Mass Markets revenues increased $0.7 billion, or 3.8%, during 2014 compared to 2013 primarily due to the expansion of FiOS services (Voice, Internet and Video), including our FiOS Quantum offerings, as well as changes in our pricing strategies, partially offset by the continued decline of local exchange revenues. FiOS represented approximately 76% of Consumer retail revenue during 2014 compared to approximately 71% during 2013.

During 2014, we grew our subscriber base by 0.5 million FiOS Internet subscribers and by 0.4 million FiOS Video subscribers, while also improving penetration rates within our FiOS service areas. As of December 31, 2014, we achieved penetration rates of 41.1% and 35.8% for FiOS Internet and FiOS Video, respectively, compared to penetration rates of 39.5% and 35.0% for FiOS Internet and FiOS Video, respectively, at December 31, 2013.

The increase in Mass Markets revenues was partially offset by the decline of local exchange revenues primarily due to a 5.5% decline in Consumer retail voice connections resulting primarily from competition and technology substitution with wireless, competing VoIP, and cable telephony services. Total voice connections include traditional switched access lines in service as well as FiOS digital voice connections. There was also a decline in Small business retail voice connections, primarily reflecting competition and a continuing shift to both IP and high-speed circuits.

2013 Compared to 2012

Mass Markets revenues increased $0.6 billion, or 3.8%, during 2013 compared to 2012 primarily due to the expansion of FiOS services (Voice, Internet and Video) as well as changes in our pricing strategies, partially offset by the continued decline of local exchange revenues.