Attached files

| file | filename |

|---|---|

| EX-99.1 - EX-99.1 - Equity Commonwealth | a15-4714_1ex99d1.htm |

| 8-K - 8-K - Equity Commonwealth | a15-4714_18k.htm |

Exhibit 99.2

|

|

Fourth Quarter 2014 Corporate Headquarters Investor Relations Two North Riverside Plaza Sarah Byrnes Suite 600 (312) 646-2801 Chicago, IL 60606 ir@eqcre.com (312) 646-2800 www.eqcre.com Supplemental Operating and Financial Data |

|

|

Corporate Information Company Profile and Investor Information 3 Financial Information Key Financial Data 4 Condensed Consolidated Balance Sheets 5 Additional Balance Sheet Information 6 Condensed Consolidated Statements of Operations 7 Additional Income Statement Information 8 Calculation of Same Property Net Operating Income (NOI) and Same Property Cash Basis NOI 9 Calculation of EBITDA and Adjusted EBITDA 10 Calculation of Fund from Operations (FFO) and Normalized FFO 11 Debt Summary 12 Debt Maturity Schedule 13 Leverage Ratios, Coverage Ratios and Public Debt Covenants 14 Capital Expenditures Summary 15 Acquisitions and Dispositions Information Since January 1, 2014 16 Portfolio Information Portfolio Summary by Property Location 17 Same Property Results of Operations by Location 18 Top 30 Properties by Annualized Rental Revenue 19 Leasing Summary 20 Leasing Summary by Property Location 21 Occupancy and Leasing Analysis by Property Location 22 Tenants Representing 1% or More of Total Annualized Rental Revenue 23 Portfolio Lease Expiration Schedule 24 Property Detail 25 Additional Support Condensed Consolidated Statements of Operations - Discontinued Operations 28 Summary of Equity Investments 29 Definitions 30 Forward-Looking Statements TABLE OF CONTENTS Some of the statements contained in this presentation constitute forward-looking statements within the meaning of the federal securities laws. Any forward-looking statements contained in this presentation are intended to be made pursuant to the safe harbor provisions of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. Forward-looking statements relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. In particular, statements pertaining to our capital resources, portfolio performance and results of operations contain forward-looking statements. Likewise, all of our statements regarding anticipated growth in our funds from operations and anticipated market conditions are forward-looking statements. In some cases, you can identify forward-looking statements by the use of forward-looking terminology such as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” or “potential” or the negative of these words and phrases or similar words or phrases which are predictions of or indicate future events or trends and which do not relate solely to historical matters. You can also identify forward-looking statements by discussions of strategy, plans or intentions. The forward-looking statements contained in this presentation reflect our current views about future events and are subject to numerous known and unknown risks, uncertainties, assumptions and changes in circumstances that may cause our actual results to differ significantly from those expressed in any forward-looking statement. We do not guarantee that the transactions and events described will happen as described (or that they will happen at all). We disclaim any obligation to publicly update or revise any forward-looking statement to reflect changes in underlying assumptions or factors, of new information, data or methods, future events or other changes. For a further discussion of these and other factors that could cause our future results to differ materially from any forward-looking statements, see the sections entitled “Risk Factors” in our most recent Annual Report on Form 10-K and Quarterly Reports on Form 10-Q. 2 |

2

|

|

No. of Sq. % Q4 2014 Cash Basis Properties Ft. Leased Revenues NOI (1) CBD Properties 40 21,892 84.7% 64.1% 60.4% Suburban Properties 116 21,027 87.0% 35.9% 39.6% Total 156 42,919 85.8% 100.0% 100.0% Senior Unsecured Debt Ratings NYSE Trading Symbols Moody's -- Baa3 Common Stock -- EQC Standard & Poor's -- BBB- Preferred Stock Series D -- EQC-PD Preferred Stock Series E -- EQC-PE 5.75% Senior Notes due 2042 -- EQCO Sam Zell (Chairman) David A. Helfand Kenneth Shea James S. Corl Peter Linneman Gerald A. Spector Martin L. Edelman James L. Lozier, Jr. James A. Star Edward A. Glickman Mary Jane Robertson David A. Helfand David S. Weinberg President and Chief Executive Officer Executive Vice President and Chief Operating Officer Adam S. Markman Orrin S. Shifrin Executive Vice President, Executive Vice President, General Chief Financial Officer and Treasurer Counsel and Secretary Bank of America / Merrill Lynch RBC Capital Markets JMP Securities James Feldman Rich Moore Mitch Germain (646) 855-5808 (440) 715-2646 (212) 906-3546 james.feldman@baml.com rich.moore@rbccm.com mgermain@jmpsecurities.com Citigroup Stifel Nicolaus Green Street Advisors Michael Bilerman John Guinee John Bejjani (212) 816-1383 (443) 224-1307 (949) 640-8780 michael.bilerman@citi.com jwguinee@stifel.com jbejjani@greenst.com Citigroup Credit Suisse J.P.Morgan Thomas Cook John Giordano Mark Streeter (212) 723-1112 (212) 538-4935 (212) 834-5086 thomas.n.cook@citigroup.com john.giordano@credit-suisse.com mark.streeter@jpmorgan.com Wells Fargo Securities Thierry Perrein (704) 715-8455 thierry.perrein@wellsfargo.com Moody's Investors Service Standard & Poor's Lori Marks Jaime Gitler (212) 553-1098 (212) 438-5049 lori.marks@moodys.com jaime.gitler@standardandpoors.com (1) (2) Debt Research Coverage (2) Rating Agencies (2) Non-GAAP financial measure which is defined in the "Definitions" section of this document. Please refer to the calculation in this document which reconciles the differences between the non- GAAP financial measure and the most directly comparable GAAP financial measure. Any opinions, estimates or forecasts regarding EQC's performance made by these analysts or agencies do not represent opinions, forecasts or predictions of EQC or its management. EQC does not by its reference to the analysts and agencies above imply its endorsement of or concurrence with any information, conclusions or recommendations provided by any of these analysts or agencies. COMPANY PROFILE AND INVESTOR INFORMATION Equity Commonwealth (NYSE: EQC) is an internally managed and self-advised real estate investment trust (REIT). EQC is one of the largest commercial office REITs in the United States, with a portfolio of over 42 million square feet located in 30 states, DC and Australia. Board of Trustees Senior Management Equity Research Coverage (2) 3 |

3

|

|

12/31/2014 9/30/2014 6/30/2014 3/31/2014 12/31/2013 OPERATING INFORMATION Percent leased 85.8% 85.9% 86.7% 86.5% 87.0% Total revenues 212,808 $ 216,595 $ 215,194 $ 217,260 $ 214,028 $ NOI (1) 118,650 117,203 122,493 115,529 114,568 Cash Basis NOI (1) 116,947 114,571 124,435 111,292 110,439 Adjusted EBITDA (1) 107,248 99,626 125,736 116,116 126,332 NOI margin (2) 55.8% 54.1% 56.9% 53.2% 53.5% Net (loss) income (158,561) 156,740 5,385 20,448 (5,301) Net (loss) income attributable to EQC common shareholders (165,542) 149,759 (17,802) 9,297 (16,452) Normalized FFO attributable to EQC common shareholders(1) 68,733 57,306 81,317 60,967 72,370 Common distributions paid - - - 29,597 29,596 SHARES OUTSTANDING AND PER SHARE DATA Shares Outstanding at End of Period Common stock outstanding -- basic (includes unvested restricted shares) 129,607 128,894 128,860 118,414 118,387 Restricted share units (3) - - - - - Preferred stock outstanding (4) 15,915 15,915 15,917 26,180 26,180 Weighted Average Shares Outstanding - EPS & FFO Weighted Average Common shares outstanding -- basic 129,398 128,880 123,812 118,400 118,387 Weighted Average Common shares outstanding -- diluted (4) 129,398 131,243 123,812 118,400 118,387 Weighted Average Shares Outstanding - Normalized FFO Weighted Average Common shares outstanding -- basic and diluted (4) 129,398 128,880 123,812 118,400 118,387 Per Share Data Net (loss) income attributable to EQC common shareholders - basic (1.28) $ 1.16 $ (0.14) $ 0.08 $ (0.14) $ Net (loss) income attributable to EQC common shareholders - diluted (4) (1.28) 1.16 (0.14) 0.08 (0.14) Normalized FFO attributable to EQC common shareholders - diluted (4) 0.53 0.44 0.66 0.51 0.61 Common distributions paid - - - 0.25 0.25 BALANCE SHEET Total assets 5,761,639 $ 6,170,796 $ 6,593,360 $ 6,600,714 $ 6,646,434 $ Total liabilities 2,442,056 2,681,793 3,222,472 3,241,644 3,282,848 MARKET CAPITALIZATION Total debt (book value) (5) 2,207,665 $ 2,442,942 $ 2,986,604 $ 3,009,627 $ 3,025,428 $ Plus: Market value of preferred shares (at end of period) 398,570 400,571 403,997 657,820 551,142 Plus: Market value of common shares (at end of period) 3,327,012 3,313,853 3,391,593 3,114,281 2,759,599 Total market capitalization 5,933,247 $ 6,157,366 $ 6,782,194 $ 6,781,728 $ 6,336,169 $ RATIOS Total debt (5) / total market capitalization 37.2% 39.7% 44.0% 44.4% 47.7% Net debt (6) / annualized adjusted EBITDA 4.3x 4.6x 5.1x 6.1x 5.5x Adjusted EBITDA / interest expense 3.3x 2.8x 3.3x 3.0x 3.3x (1) (2) (3) (4) (5) (6) Net debt is calculated as total debt minus cash and cash equivalents. Total debt includes mortgage debt related to properties classified as held for sale totaling $19,688 and $20,018 as of March 31, 2014, and December 31, 2013, respectively, and net unamortized premiums and discounts for all periods presented. Total debt excludes the debt of our unconsolidated equity investees. Non-GAAP financial measure which is defined in the "Definitions" section of this document. Please refer to the calculation in this document which reconciles the differences between the non-GAAP financial measure and the most directly comparable GAAP financial measure. KEY FINANCIAL DATA (dollar and share amounts in thousands, except per share data) As of and for the Three Months Ended As of December 31, 2014, we had 4,915 series D preferred shares outstanding that were convertible into 2,363 of our common shares, which for GAAP earnings per common share and FFO per common share, were dilutive for the three months ended September 30, 2014 and anti-dilutive for all other periods presented. The series D preferred shares outstanding were anti-dilutive for all periods presented with respect to Normalized FFO per common share. NOI margin is defined as NOI as a percentage of total revenues. As of December 31, 2014, we had granted 1,266 restricted share untis ("RSU"s). None were granted as of the other periods presented. The RSUs contain both service and market-based vesting components. None of the RSUs have vested and the market-based vesting component is currently "out of the money." As a result of these factors, the RSUs are excluded from basic and diluted GAAP EPS, FFO per common share and Normalized FFO per common share. 4 |

4

|

|

December 31, December 31, 2014 2013 ASSETS Real estate properties: Land 714,238 $ 699,135 $ Buildings and improvements 5,014,205 4,838,030 5,728,443 5,537,165 Accumulated depreciation (1,030,445) (895,059) 4,697,998 4,642,106 Properties held for sale - 573,531 Acquired real estate leases, net 198,287 255,812 Equity investments - 517,991 Cash and cash equivalents 379,058 222,449 Restricted cash 17,715 22,101 Rents receivable, net of allowance for doubtful accounts of $6,565 and $7,885, respectively 248,101 223,769 Other assets, net 220,480 188,675 Total assets 5,761,639 $ 6,646,434 $ LIABILITIES AND SHAREHOLDERS' EQUITY Revolving credit facility - $ 235,000 $ Senior unsecured debt, net 1,598,416 1,855,900 Mortgage notes payable, net 609,249 914,510 Liabilities related to properties held for sale - 28,734 Accounts payable and accrued expenses 162,204 165,855 Assumed real estate lease obligations, net 26,784 33,935 Rent collected in advance 31,359 27,553 Security deposits 14,044 11,976 Due to related persons - 9,385 Total liabilities 2,442,056 $ 3,282,848 $ Shareholders' equity: Preferred shares of beneficial interest, $0.01 par value: 50,000,000 shares authorized; Series D preferred shares; 6 1/2% cumulative convertible; 119,266 $ 368,270 $ Series E preferred shares; 7 1/4% cumulative redeemable on or after May 15, 2016; 11,000,000 shares issued and outstanding, aggregate liquidation preference $275,000 265,391 265,391 Common shares of beneficial interest, $0.01 par value: 350,000,000 shares authorized; 129,607,279 and 118,386,918 shares issued and outstanding, respectively (including 710,182 and 130,914 unvested restricted shares) 1,296 1,184 Additional paid in capital 4,487,133 4,213,474 Cumulative net income 2,233,852 2,209,840 Cumulative other comprehensive loss (53,216) (38,331) Cumulative common distributions (3,111,868) (3,082,271) Cumulative preferred distributions (622,271) (573,971) Total shareholders' equity 3,319,583 $ 3,363,586 $ Total liabilities and shareholders' equity 5,761,639 $ 6,646,434 $ (amounts in thousands, except share data) CONDENSED CONSOLIDATED BALANCE SHEETS 4,915,497 and 15,180,000 shares issued and outstanding, respectively, aggregate liquidation preference of $122,887 and $379,500, respectively 5 |

5

|

|

December 31, December 31, 2014 2013 Additional Balance Sheet Information Straight-line rents receivable, net of allowance for doubtful accounts 220,855 $ 199,587 $ Tenant accounts receivable, net of allowance for doubtful accounts 16,837 9,794 Other 10,409 14,388 Rents receivable, net of allowance for doubtful accounts 248,101 $ 223,769 $ Capitalized lease incentives 15,191 $ 15,259 $ Deferred financing fees 16,861 24,530 Deferred leasing costs 126,252 100,768 Other 62,176 48,118 Other assets, net 220,480 $ 188,675 $ Accounts payable 7,749 $ 16,011 $ Accrued interest 25,007 26,882 Accrued taxes 57,237 62,611 Other accrued liabilities (1) 72,211 60,351 Accounts payable and accrued expenses 162,204 $ 165,855 $ (1) Other accrued liabilities inclues $1.2 million payable to REIT Management and Research Inc. (RMR), EQC's former external advisor, as of December 31, 2014. RMR was a related person as of December 31, 2013, and such amounts were included in Due to related persons as of that date. RMR ceased to be a related person after certain of EQC's former officers, who were also officers of RMR, resigned. 6 |

6

|

|

1 2 3 4 December 31, December 31, 2014 2013 2014 2013 Revenues Rental income (1) 173,036 $ 171,041 $ 691,699 $ 763,262 $ Tenant reimbursements and other income 39,772 42,987 170,158 189,767 Total revenues 212,808 $ 214,028 $ 861,857 $ 953,029 $ Expenses Operating expenses 94,158 $ 99,460 $ 387,982 $ 410,045 $ Depreciation and amortization 58,839 51,908 227,532 234,402 General and administrative 16,760 17,050 113,155 80,504 Loss on asset impairment 167,145 - 185,067 124,253 Acquisition related costs - (19) 5 318 Total expenses 336,902 $ 168,399 $ 913,741 $ 849,522 $ Operating (loss) income (124,094) $ 45,629 $ (51,884) $ 103,507 $ Interest and other income 490 $ 298 $ 1,561 $ 1,229 $ Interest expense (including net amortization of debt discounts, premiums and deferred financing fees of $151, $(256), $(549), and $9, respectively) (32,151) (38,559) (143,230) (173,011) (Loss) gain on early extinguishment of debt (1,790) (25) 4,909 (60,052) (Loss) gain on sale of equity investments (160) - 171,561 66,293 Gain on issuance of shares by an equity investee - - 17,020 - (Loss) income from continuing operations before income tax expense and equity in earnings of investees (157,705) 7,343 (63) (62,034) Income tax expense (1,025) (107) (3,191) (2,634) Equity in earnings of investees - 10,841 24,460 25,754 (Loss) income from continuing operations (158,730) 18,077 21,206 (38,914) Discontinued operations: Income from discontinued operations (1) 169 4,661 8,389 6,393 Loss on asset impairment from discontinued operations - (1,507) (2,238) (102,869) Loss on early extinguishment of debt from discontinued operations - (1,011) (3,345) (1,011) Net loss on sale of properties from discontinued operations - (25,521) - (22,162) (Loss) income before gain on sale of properties (158,561) (5,301) 24,012 (158,563) Gain on sale of properties - - - 1,596 Net (loss) income (158,561) $ (5,301) $ 24,012 $ (156,967) $ Net income attributable to noncontrolling interest in consolidated subsidiary - - - (20,093) Net (loss) income attributable to Equity Commonwealth (158,561) $ (5,301) $ 24,012 $ (177,060) $ Preferred distributions (6,981) $ (11,151) $ (32,095) $ (44,604) $ Distribution on conversion of preferred shares - - (16,205) - Net loss attributable to EQC common shareholders (165,542) $ (16,452) $ (24,288) $ (221,664) $ (1) CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (amounts in thousands, except per share data) For the Three Months Ended For the Year Ended We report rental income on a straight line basis over the terms of the respective leases; rental income and income from discontinued operations include non-cash straight line rent adjustments. Rental income and income from discontinued operations also include non-cash amortization of intangible lease assets and liabilities. 7 |

7

|

|

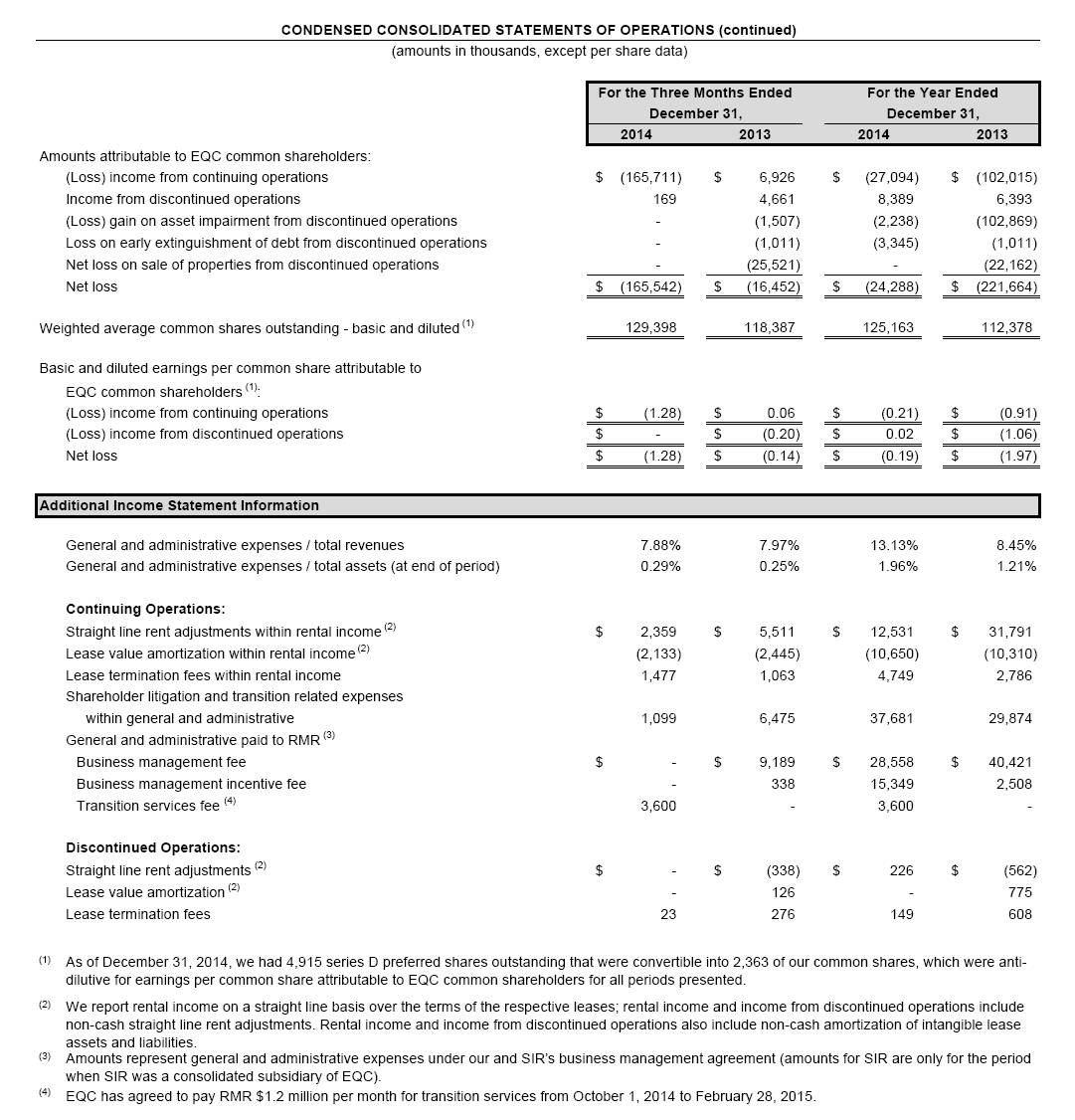

December 31, December 31, 2014 2013 2014 2013 Amounts attributable to EQC common shareholders: (Loss) income from continuing operations (165,711) $ 6,926 $ (27,094) $ (102,015) $ Income from discontinued operations 169 4,661 8,389 6,393 (Loss) gain on asset impairment from discontinued operations - (1,507) (2,238) (102,869) Loss on early extinguishment of debt from discontinued operations - (1,011) (3,345) (1,011) Net loss on sale of properties from discontinued operations - (25,521) - (22,162) Net loss (165,542) $ (16,452) $ (24,288) $ (221,664) $ Weighted average common shares outstanding - basic and diluted (1) 129,398 118,387 125,163 112,378 Basic and diluted earnings per common share attributable to EQC common shareholders (1): (Loss) income from continuing operations (1.28) $ 0.06 $ (0.21) $ (0.91) $ (Loss) income from discontinued operations - $ (0.20) $ 0.02 $ (1.06) $ Net loss (1.28) $ (0.14) $ (0.19) $ (1.97) $ Additional Income Statement Information General and administrative expenses / total revenues 7.88% 7.97% 13.13% 8.45% General and administrative expenses / total assets (at end of period) 0.29% 0.25% 1.96% 1.21% Continuing Operations: Straight line rent adjustments within rental income (2) 2,359 $ 5,511 $ 12,531 $ 31,791 $ Lease value amortization within rental income (2) (2,133) (2,445) (10,650) (10,310) Lease termination fees within rental income 1,477 1,063 4,749 2,786 Shareholder litigation and transition related expenses within general and administrative 1,099 6,475 37,681 29,874 General and administrative paid to RMR (3) Business management fee - $ 9,189 $ 28,558 $ 40,421 $ Business management incentive fee - 338 15,349 2,508 Transition services fee (4) 3,600 - 3,600 - Discontinued Operations: Straight line rent adjustments (2) - $ (338) $ 226 $ (562) $ Lease value amortization (2) - 126 - 775 Lease termination fees 23 276 149 608 (1) (2) (3) (4) EQC has agreed to pay RMR $1.2 million per month for transition services from October 1, 2014 to February 28, 2015. Amounts represent general and administrative expenses under our and SIR's business management agreement (amounts for SIR are only for the period when SIR was a consolidated subsidiary of EQC). We report rental income on a straight line basis over the terms of the respective leases; rental income and income from discontinued operations include non-cash straight line rent adjustments. Rental income and income from discontinued operations also include non-cash amortization of intangible lease assets and liabilities. CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (continued) (amounts in thousands, except per share data) For the Three Months Ended For the Year Ended As of December 31, 2014, we had 4,915 series D preferred shares outstanding that were convertible into 2,363 of our common shares, which were antidilutive for earnings per common share attributable to EQC common shareholders for all periods presented. 8 |

8

|

|

December 31, December 31, 2014 2013 2014 2013 Calculation of Same Property NOI and Same Property Cash Basis NOI (1), (2): Rental income 173,036 $ 171,041 $ 691,699 $ 763,262 $ Tenant reimbursements and other income 39,772 42,987 170,158 189,767 Operating expenses (94,158) (99,460) (387,982) (410,045) NOI 118,650 114,568 473,875 542,984 Straight line rent adjustments (2,359) (5,511) (12,531) (31,791) Lease value amortization 2,133 2,445 10,650 10,310 Lease termination fees (1,477) (1,063) (4,749) (2,786) Cash Basis NOI 116,947 $ 110,439 $ 467,245 $ 518,717 $ Cash Basis NOI from non-same properties 11 1 (266) (68,470) Same Property Cash Basis NOI 116,958 $ 110,440 $ 466,979 $ 450,247 $ Non-cash rental and termination income from same properties 1,704 4,129 6,629 19,064 Same Property NOI 118,662 $ 114,569 $ 473,608 $ 469,311 $ Reconciliation of Same Property NOI to GAAP Operating (Loss) Income Same Property NOI 118,662 $ 114,569 $ 473,608 $ 469,311 $ Non-cash rental and termination income from same properties (1,704) (4,129) (6,629) (19,064) Same Property Cash Basis NOI 116,958 $ 110,440 $ 466,979 $ 450,247 $ Cash Basis NOI from non-same properties (11) (1) 266 68,470 Cash Basis NOI 116,947 $ 110,439 $ 467,245 $ 518,717 $ Straight line rent adjustments 2,359 5,511 12,531 31,791 Lease value amortization (2,133) (2,445) (10,650) (10,310) Lease termination fees 1,477 1,063 4,749 2,786 NOI 118,650 114,568 473,875 542,984 Depreciation and amortization (58,839) (51,908) (227,532) (234,402) General and administrative (16,760) (17,050) (113,155) (80,504) Loss on asset impairment (167,145) - (185,067) (124,253) Acquisition related costs - 19 (5) (318) Operating (Loss) Income (124,094) 45,629 (51,884) 103,507 (1) (2) 2014 results include income from the settlement of litigation with a former tenant of $2.7 million and $8.8 million for the three months and year ended December 31, 2014, respectively. Properties classified as discontinued operations are excluded. Quarter-to-date same property results include properties continuously owned from October 1, 2013 through December 31, 2014. Year-to-date same property results include properties continuously owned from January 1, 2013 through December 31, 2014. Amounts related to the settlement of outstanding assets and liabilities of previously-disposed properties that are reflected in our consolidated results are excluded from same property results. For the Year Ended CALCULATION OF SAME PROPERTY NET OPERATING INCOME (NOI) AND SAME PROPERTY CASH BASIS NOI (amounts in thousands) For the Three Months Ended |

9

|

|

December 31, December 31, 2014 2013 2014 2013 Net (loss) income (158,561) $ (5,301) $ 24,012 $ (156,967) $ Plus: Interest expense from continuing operations 32,151 38,559 143,230 173,011 Interest expense from discontinued operations - 416 608 1,742 Income tax expense 1,025 107 3,191 2,634 Depreciation and amortization from continuing operations 58,839 51,908 227,532 234,402 Depreciation and amortization from discontinued operations - 825 - 12,550 EBITDA from equity investees - 15,908 36,103 38,460 Less: Equity in earnings of investees - (10,841) (24,460) (25,754) EBITDA (1) (66,546) $ 91,581 $ 410,216 $ 280,078 $ Plus: Loss on asset impairment from continuing operations 167,145 - 185,067 124,253 Loss on asset impairment from discontinued operations - 1,507 2,238 102,869 Acquisition related costs from continuing operations - (19) 5 318 Loss (gain) on early extinguishment of debt from continuing operations 1,790 25 (4,909) 60,052 Loss on early extinguishment of debt from discontinued operations - 1,011 3,345 1,011 Shareholder litigation and transition costs 1,099 6,475 37,681 29,874 Transition services fee (2) 3,600 - 3,600 - Adjusted EBITDA from equity investees, net of EBITDA - 231 64 (902) Less: Gain on sale of properties - - - (1,596) Net loss on sale of properties from discontinued operations - 25,521 - 22,162 Loss (gain) on sale of equity investments 160 - (171,561) (66,293) Gain on issuance of shares by an equity investee - - (17,020) - Adjusted EBITDA (1) 107,248 $ 126,332 $ 448,726 $ 551,826 $ (1) (2) For the Year Ended CALCULATION OF EBITDA AND ADJUSTED EBITDA (amounts in thousands) For the Three Months Ended 2014 EBITDA and Adjusted EBITDA include income from the settlement of litigation with a former tenant of $2.7 million and $8.8 million for the three months and year ended December 31, 2014, respectively. EQC has agreed to pay RMR $1.2 million per month for transition services from October 1, 2014 to February 28, 2015. 10 |

10

|

|

December 31, December 31, 2014 2013 2014 2013 Calculation of FFO Net (loss) income attributable to Equity Commonwealth (158,561) $ (5,301) $ 24,012 $ (177,060) $ Plus: Depreciation and amortization from continuing operations 58,839 51,908 227,532 234,402 Depreciation and amortization from discontinued operations - 825 - 12,550 Loss on asset impairment from continuing operations 167,145 - 185,067 124,253 Loss on asset impairment from discontinued operations - 1,507 2,238 102,869 FFO from equity investees - 14,568 33,007 33,564 Net income attributable to noncontrolling interest - - - 20,093 Less: FFO attributable to noncontrolling interest - - - (26,270) Gain on sale of properties - - - (1,596) Net loss on sale of properties from discontinued operations - 25,521 - 22,162 Equity in earnings of investees - (10,841) (24,460) (25,754) FFO attributable to Equity Commonwealth 67,423 78,187 447,396 319,213 Less: Preferred distributions (6,981) (11,151) (32,095) (44,604) FFO attributable to EQC Common Shareholders (1) 60,442 $ 67,036 $ 415,301 $ 274,609 $ Calculation of Normalized FFO FFO attributable to EQC common shareholders 60,442 $ 67,036 $ 415,301 $ 274,609 $ Recurring adjustments: Lease value amortization from continuing operations 2,133 2,445 10,650 10,310 Lease value amortization from discontinued operations - (126) - (775) Straight line rent from continuing operations (2,359) (5,511) (12,531) (31,791) Straight line rent from discontinued operations - 338 (226) 562 Loss (gain) on early extinguishment of debt from continuing operations 1,790 25 (4,909) 60,052 Loss on early extinguishment of debt from discontinued operations - 1,011 3,345 1,011 Minimum cash rent from direct financing lease (2) 2,032 2,032 8,128 8,125 Loss (gain) on sale of equity investments 160 - (171,561) (66,293) Gain on issuance of shares by an equity investee - - (17,020) - Interest earned from direct financing lease (164) (251) (787) (1,128) Normalized FFO from equity investees, net of FFO - (1,085) (3,353) (2,530) Normalized FFO from noncontrolling interest, net of FFO - - - 1,987 Other items which affect comparability: Shareholder litigation and transition related expenses 1,099 6,475 37,681 29,874 Transition services fee (4) 3,600 - 3,600 - Acquisition related costs from continuing operations - (19) 5 318 Normalized FFO attributable to EQC Common Shareholders (1) 68,733 $ 72,370 $ 268,323 $ 284,331 $ Weighted average common shares outstanding -- basic & diluted (3) 129,398 118,387 125,163 112,378 FFO attributable to EQC common shareholders per share -- basic & diluted (3) 0.47 $ 0.57 $ 3.32 $ 2.44 $ Normalized FFO attributable to EQC common shareholders per share -- basic & diluted (3) 0.53 $ 0.61 $ 2.14 $ 2.53 $ (1) (2) (3) (4) EQC has agreed to pay RMR $1.2 million per month for transition services from October 1, 2014 to February 28, 2015. For the Year Ended (amounts in thousands, except per share data) For the Three Months Ended CALCULATION OF FUNDS FROM OPERATIONS (FFO) AND NORMALIZED FFO As of December 31, 2014, we had 4,915 series D preferred shares outstanding that were convertible into 2,363 of our common shares, which were anti-dilutive for FFO and Normalized FFO per common share for all periods presented. Contractual cash payments (including management fees) from one tenant at Arizona Center for 2014 were $8,128 and will decrease to approximately $515 beginning in 2016. Our calculation of Normalized FFO reflects the cash payments received from this tenant. The terms of this tenant's lease require us to classify the lease as a direct financing (or capital) lease. As such, the revenue recognized on a GAAP basis within our condensed consolidated statements of operations was $172 and $257 for the quarters ended December 31, 2014 and 2013, respectively and $817 and $1,154 years ended December 31, 2014 and 2013, respectively. This direct financing lease has an expiration date in 2045. 2014 FFO attributable to EQC Common Shareholders and Normalized FFO attributable to EQC Common Shareholders include income from the settlement of litigation with a former tenant of $2.7 million and $8.8 million for the three months and year ended December 31, 2014, respectively. 11 |

11

|

|

Interest Principal Maturity Due at Years to Rate Balance Date Maturity Maturity Unsecured Debt: Unsecured Floating Rate Debt: Revolving credit facility (LIBOR + 150 bps) (1) 1.669% - $ 10/19/2015 - $ 0.8 Term loan (LIBOR + 185 bps) (2) 2.019% 400,000 12/15/2016 400,000 2.0 Total / weighted average unsecured floating rate debt 2.019% 400,000 $ 400,000 $ 2.0 Unsecured Fixed Rate Debt: 5.75% Senior Unsecured Notes due 2015 5.750% 138,773 $ 11/1/2015 138,773 $ 0.8 6.25% Senior Unsecured Notes due 2016 6.250% 139,104 8/15/2016 139,104 1.6 6.25% Senior Unsecured Notes due 2017 6.250% 250,000 6/15/2017 250,000 2.5 6.65% Senior Unsecured Notes due 2018 6.650% 250,000 1/15/2018 250,000 3.0 5.875% Senior Unsecured Notes due 2020 5.875% 250,000 9/15/2020 250,000 5.7 5.75% Senior Unsecured Notes due 2042 5.750% 175,000 8/1/2042 175,000 27.6 Total / weighted average unsecured fixed rate debt 6.125% 1,202,877 $ 1,202,877 $ 6.6 Secured Fixed Rate Debt: 111 Monument Circle 5.235% 116,000 $ 3/1/2016 116,000 $ 1.2 225 Water Street (3) 6.030% 40,059 5/11/2016 38,994 1.4 111 East Wacker Drive 6.290% 142,666 7/11/2016 139,478 1.5 2501 20th Place South 7.360% 10,267 8/1/2016 9,333 1.6 Parkshore Plaza 5.670% 41,275 5/1/2017 41,275 2.3 1735 Market Street (4) 5.660% 171,498 12/2/2019 160,710 4.9 206 East 9th Street 5.690% 27,965 1/5/2021 24,836 6.0 1320 Main Street 5.300% 38,979 6/1/2021 34,113 6.4 33 Stiles Lane 6.750% 3,132 3/1/2022 - 7.2 97 Newberry Road 5.710% 6,819 3/1/2026 - 11.2 Total / weighted average secured fixed rate debt 5.767% 598,660 $ 564,739 $ 3.0 Total / weighted average 5.281% 2,201,537 $ (5) 2,167,616 $ 4.8 $1.15 Billion Credit Agreement, Effective January 29, 2015 (1) (2) (3) (4) (5) Represents amounts outstanding on EQC's term loan as of December 31, 2014. The interest rate presented is as of December 31, 2014, and equals LIBOR plus 1.85%. The spread over LIBOR varies depending upon EQC's credit rating. Total debt outstanding as of December 31, 2014, including net unamortized premiums and discounts, was $2,207,665. Represents amounts outstanding on EQC's $750,000 revolving credit facility as of December 31, 2014. The interest rate presented is as of December 31, 2014, and equals LIBOR plus 1.5%. We also pay a 35 basis point facility fee annually. The spread over LIBOR and the facility fee vary depending upon EQC's credit rating. Interest is payable at a rate equal to LIBOR plus 2.625% but has been fixed by a cash flow hedge, which sets the rate at approximately 5.66% until December 1, 2016. On October 10, 2014, we were notified by the lender that our decision to cease making loan servicing payments on the mortgage loan secured by 225 Water Street created an event of default effective July 11, 2014, and the lender has exercised its option to accelerate the maturity of the unpaid balance of $40,059. Since July 11, 2014, we have accrued interest on this loan at 10.03% to include the 4% of default interest. DEBT SUMMARY (dollars in thousands) As of December 31, 2014 On January 29, 2015, we entered into a new credit agreement, pursuant to which the lenders agreed to provide (i) a $750.0 million unsecured revolving credit facility, (ii) a $200.0 million 5-year term loan facility and (iii) a $200.0 million 7-year term loan facility. The new agreement replaces our prior credit agreement and our prior term loan agreement. The revolving credit facility has a scheduled maturity date of January 28, 2019 with two six-month extension options subject to certain conditions and the payment of an extension fee. The 5-year term loan and the 7-year term loan have scheduled maturity dates of January 28, 2020 and January 28, 2022, respectively. We used the proceeds of borrowings under the credit agreement to repay all amounts outstanding and due under the previous term loan agreement. 12 |

12

|

|

Unsecured Unsecured Secured Weighted Floating Fixed Fixed Rate Average Year Rate Debt Rate Debt Debt Total Interest Rate (1) - $ 138,773 $ 7,200 $ 145,973 $ 5.8% 400,000 (2) 139,104 309,604 (3) 848,708 4.1% - 250,000 45,592 295,592 6.2% - 250,000 4,614 254,614 6.6% - - 165,422 165,422 5.7% - 250,000 2,523 252,523 5.9% - - 60,470 60,470 5.5% - - 799 799 5.9% - - 702 702 5.7% - - 743 743 5.7% - 175,000 991 175,991 5.7% Total 400,000 $ 1,202,877 $ 598,660 $ 2,201,537 $ (4) 5.3% Percent 18.2% 54.6% 27.2% 100.0% (1) (2) (3) (4) Scheduled Principal Payments During Period (dollars in thousands) DEBT MATURITY SCHEDULE 2015 2016 2017 2018 2019 2020 2021 Total debt outstanding as of December 31, 2014, including net unamortized premiums and discounts, was $2,207,665. 2022 Thereafter Based on current contractual interest rates excluding an additional 4% of default interest incurred on the mortgage loan secured by 225 Water Street. Represents amounts outstanding on EQC's term loan as of December 31, 2014. The interest rate presented is as of December 31, 2014, and equals LIBOR plus 1.85%. The spread over LIBOR varies depending upon EQC's credit rating. 2023 On October 10, 2014, we were notified by the lender that our decision to cease making loan servicing payments on the mortgage loan secured by 225 Water Street created an event of default effective July 11, 2014, and the lender has exercised its option to accelerate the maturity of the unpaid balance of $40,059. Since July 11, 2014, we have accrued interest on this loan at 10.030% to include the 4% of default interest. 2024 13 |

13

|

|

12/31/2014 9/30/2014 6/30/2014 3/31/2014 12/31/2013 Leverage Ratios Total debt (1) / total assets 38.3% 39.6% 45.3% 45.6% 45.5% Total debt (1) / total market capitalization 37.2% 39.7% 44.0% 44.4% 47.7% Total debt (1) + preferred stock / total market capitalization 43.9% 46.2% 50.0% 54.1% 56.4% Total debt (1) / annualized adjusted EBITDA 5.1x 6.1x 5.9x 6.5x 6.0x Total debt (1) + preferred stock / annualized adjusted EBITDA 6.1x 7.1x 6.7x 7.9x 7.1x Net debt (2) / enterprise value (3) 32.9% 33.2% 40.3% 42.9% 45.8% Net debt (2) + preferred stock / enterprise value (3) 40.1% 40.4% 46.6% 52.8% 54.9% Net debt (2) / annualized adjusted EBITDA 4.3x 4.6x 5.1x 6.1x 5.5x Net debt (2) + preferred stock / annualized adjusted EBITDA 5.2x 5.6x 5.9x 7.5x 6.6x Secured debt / total assets 10.6% 10.0% 13.6% 13.9% 14.1% Variable rate debt / total debt (1) 18.1% 20.5% 24.6% 24.4% 24.3% Variable rate debt / total assets 6.9% 8.1% 11.1% 11.1% 11.1% Coverage Ratios Adjusted EBITDA (4) / interest expense 3.3x 2.8x 3.3x 3.0x 3.3x Adjusted EBITDA (4) / interest expense + preferred distributions 2.7x 2.4x 2.8x 2.4x 2.5x Public Debt Covenants Debt / adjusted total assets (5) (maximum 60%) 31.0% 33.4% 38.9% 38.8% 38.9% Secured debt / adjusted total assets (5) (maximum 40%) 8.6% 8.5% 11.6% 11.8% 12.0% Consolidated income available for debt service (6) / debt service (minimum 1.5x) 3.8x 3.4x 3.1x 3.2x 3.3x Total unencumbered assets (5) / unsecured debt (minimum 150% / 200%) 385.8% 348.7% 302.8% 304.4% 303.9% (1) (2) (3) (4) (5) (6) Adjusted total assets and total unencumbered assets includes original cost of real estate assets calculated in accordance with GAAP and excludes depreciation and amortization, accounts receivable, other intangible assets and impairment write downs, if any. Consolidated income available for debt service is earnings from operations excluding interest expense, depreciation and amortization, taxes, loss on asset impairment and gains and losses on acquisitions and sales of assets and early extinguishment of debt, determined together with debt service on a pro forma basis for the four consecutive fiscal quarters most recently ended. LEVERAGE RATIOS, COVERAGE RATIOS AND PUBLIC DEBT COVENANTS As of and for the Three Months Ended Total debt includes net unamortized premiums and discounts and mortgage debt related to properties classified as held for sale totaling $19,688 and $20,018 as of March 31, 2104, and December 31, 2013, respectively. Total debt excludes the debt of our unconsolidated equity investees. Non-GAAP financial measure which is defined in the "Definitions" section of this document. Please refer to the calculation in this document which reconciles the differences between the non-GAAP financial measure and the most directly comparable GAAP financial measure. (dollars in thousands) Net debt is calculated as total debt minus cash and cash equivalents. Enterprise value is calculated as total market capitalization minus cash and cash equivalents. 14 |

14

|

|

12/31/2014 9/30/2014 6/30/2014 3/31/2014 12/31/2013 Tenant improvements 15,989 $ 10,719 $ 11,687 $ 19,843 $ 30,563 $ Leasing costs 10,517 15,838 5,661 5,075 11,810 Building improvements 8,206 5,897 4,659 4,244 8,137 Development, redevelopment and other activities 1,544 2,273 2,804 3,743 8,796 Total capital expenditures 36,256 $ 34,727 $ 24,811 $ 32,905 $ 59,306 $ Average square feet during period (1) 42,919 42,919 44,309 45,698 48,650 Building improvements per average total sq. ft. during period 0.19 $ 0.14 $ 0.11 $ 0.09 $ 0.17 $ (1) Average square feet during each period includes properties held for sale at the end of each period. As of December 31, 2014, EQC did not have any properties classified as held for sale. For the Three Months Ended CAPITAL EXPENDITURES SUMMARY (dollars and square feet in thousands, except per square foot data) 15 |

15

|

|

Acquisitions: Dispositions: Annualized Date No. of Property Square % Net Book Rental Mortgage Sold Property City State Bldgs Location Feet Leased (1) Value (2) Revenue (1) Debt (3) 1. 6/27/2014 11201 N. Tatum Boulevard Phoenix AZ 1 Suburban 109,961 36.8% 9,339 $ 767 $ - $ 2. 6/27/2014 Dominguez Technology Center Carson CA 5 Suburban 402,000 100.0% 39,678 5,906 - 3. 6/27/2014 Madrone Business Park Morgan Hill CA 3 Suburban 308,665 70.0% 37,161 4,807 11,226 4. 6/27/2014 8555 Aero Drive San Diego CA 1 Suburban 48,561 65.6% 2,587 562 - 5. 6/27/2014 Fountainview Business Park San Diego CA 3 Suburban 89,976 81.6% 7,571 1,514 - 6. 6/27/2014 400 Princeton Boulevard Adairsville GA 1 Suburban 292,000 100.0% 8,068 876 - 7. 6/27/2014 Corporate Square Atlanta GA 5 Suburban 246,225 84.9% 11,585 3,359 - 8. 6/27/2014 1000 Holcomb Woods Parkway Roswell GA 8 Suburban 244,379 70.4% 10,411 1,952 - 9. 6/27/2014 500 4th Street & Roma Albuquerque NM 2 CBD 229,123 67.8% 15,114 2,722 - 10. 6/27/2014 Stephenson Center Columbia SC 3 Suburban 104,300 75.7% 4,681 1,233 - 11. 6/27/2014 Synergy Business Park Columbia SC 4 Suburban 311,382 71.0% 17,750 3,392 - 12. 6/27/2014 6060 Primacy Parkway Memphis TN 1 Suburban 130,574 56.4% 6,164 1,273 - 13. 6/27/2014 Stafford Commerce Center Stafford VA 4 Suburban 149,023 25.4% 16,107 960 4,331 14. 6/27/2014 Stafford Commerce Park Stafford VA 2 Suburban 117,929 34.7% 13,332 1,041 4,203 43 2,784,098 73.4% 199,548 $ 30,364 $ 19,760 $ (1) Percent leased and annualized rental revenue is as of March 31, 2014. (2) Represents the carrying value of real estate properties, after depreciation and amortization, purchase price allocations and impairment write downs, if any. (3) In connection with the mortgage debt repayments, EQC paid $2,270 of yield maintenance for Madrone, CA and $547 in defeasance costs for Stafford, VA. ACQUISITIONS AND DISPOSITIONS INFORMATION SINCE JANUARY 1, 2014 (dollars in thousands) There were no acquisitions during the period. On June 27, 2014, EQC sold its interest in 14 properties (43 buildings) for an aggregate gross sales price of $215,900, excluding mortgage debt repayments and closing costs. 16 |

16

|

|

CBD Suburban Properties Properties Total Number of properties 40 116 156 Percent of total 25.6% 74.4% 100.0% Total square feet 21,892 21,027 42,919 Percent of total 51.0% 49.0% 100.0% Leased square feet 18,552 18,288 36,840 Percent leased (2) 84.7% 87.0% 85.8% Total revenues 136,499 $ 76,475 $ 212,974 $ Percent of total 64.1% 35.9% 100.0% NOI (3), (4) 72,482 $ 46,334 $ 118,816 $ Percent of total 61.0% 39.0% 100.0% Cash Basis NOI (3), (4) 70,681 $ 46,431 $ 117,112 $ Percent of total 60.4% 39.6% 100.0% (1) (2) (3) (4) 2014 Suburban NOI and Cash Basis NOI include income from the settlement of litigation with a former tenant of $2.7 million and $8.8 million for the three months and year ended December 31, 2014, respectively. As of and for the Three Months Ended December 31, 2014 SAME PROPERTY SUMMARY BY PROPERTY LOCATION (1) (square feet and dollars in thousands) Includes properties continuously owned from October 1, 2013 through December 31, 2014, and excludes amounts related to the settlement of outstanding assets and liabilities of previously-disposed properties that are reflected in our consolidated results. Non-GAAP financial measure which is defined in the "Definitions" section of this document. Please refer to the calculation in this document which reconciles the differences between the non-GAAP financial measure and the most directly comparable GAAP financial measure. Percent leased includes (i) space being fitted out for occupancy pursuant to existing leases and (ii) space which is leased but is not occupied or is being offered for sublease by tenants. 17 |

17

|

|

2014 (1) 2013 (1) Change 2014 (1) 2013 (1) Change Total Properties 156 156 156 156 Square Feet (2) 42,919 42,915 42,919 42,915 % Leased 85.8% 87.0% (1.1%) 85.8% 87.0% (1.1%) Revenues Cash rental income 171,332 $ 166,908 $ 685,084 $ 667,165 $ Straight line adjustment 2,360 5,512 12,531 26,088 Above/below market rent amortization (2,133) (2,446) (10,651) (9,811) Early termination income 1,477 1,063 4,749 2,787 Rental income 173,036 171,037 691,713 686,229 Tenant reimbursements 38,896 41,872 164,947 170,867 Other income 876 1,131 5,138 5,310 Total revenues 212,808 214,040 (0.6%) 861,798 862,406 (0.1%) Total revenues excluding non-cash rental and termination income 211,104 209,911 0.6% 855,169 843,342 1.4% Operating expenses 94,146 99,471 (5.4%) 388,190 393,095 (1.2%) NOI (3) 118,662 114,569 3.6% 473,608 469,311 0.9% NOI margin 55.8% 53.5% 55.0% 54.4% Cash Basis NOI (3) 116,958 $ 110,440 $ 5.9% 466,979 $ 450,247 $ 3.7% Cash Basis NOI margin 55.4% 52.6% 54.6% 53.4% CBD Properties 40 40 40 40 Square Feet (2) 21,892 21,890 21,892 21,890 % Leased 84.7% 85.7% (1.0%) 84.7% 85.7% (1.0%) Revenues Cash rental income 108,470 $ 106,889 $ 430,958 $ 428,238 $ Straight line adjustment 2,161 3,366 10,219 15,286 Above/below market rent amortization (1,604) (1,890) (8,801) (7,290) Termination income 1,244 956 4,050 1,711 Rental income 110,271 109,321 436,426 437,945 Tenant reimbursements 25,344 28,533 108,460 114,972 Other income 778 937 4,090 4,450 Total revenues 136,393 138,791 (1.7%) 548,976 557,367 (1.5%) Total revenues excluding non-cash rental and termination income 134,592 136,359 (1.3%) 543,508 547,660 (0.8%) Operating expenses 64,009 67,552 (5.2%) 260,061 264,718 (1.8%) NOI 72,384 71,239 1.6% 288,915 292,649 (1.3%) NOI margin 53.1% 51.3% 52.6% 52.5% CBD Cash Basis NOI 70,583 $ 68,807 $ 2.6% 283,447 $ 282,942 $ 0.2% Cash Basis NOI margin 52.4% 50.5% 52.2% 51.7% Suburban Properties 116 116 116 116 Square Feet (2) 21,027 21,025 21,027 21,025 % Leased 87.0% 88.3% (1.3%) 87.0% 88.3% (1.3%) Revenues Cash rental income 62,862 $ 60,019 $ 254,126 $ 238,927 $ Straight line adjustment 199 2,146 2,312 10,802 Above/below market rent amortization (529) (556) (1,850) (2,521) Termination income 233 107 699 1,076 Rental income 62,765 61,716 255,287 248,284 Tenant reimbursements 13,552 13,339 56,487 55,895 Other income 98 194 1,048 860 Total revenues 76,415 75,249 1.5% 312,822 305,039 2.6% Total revenues excluding non-cash rental and termination income 76,512 73,552 4.0% 311,661 295,682 5.4% Operating expenses 30,137 31,919 (5.6%) 128,129 128,377 (0.2%) NOI (3) 46,278 43,330 6.8% 184,693 176,662 4.5% NOI margin 60.6% 57.6% 59.0% 57.9% Suburban Cash Basis NOI (3) 46,375 $ 41,633 $ 11.4% 183,532 $ 167,305 $ 9.7% Cash Basis NOI margin 60.6% 56.6% 58.9% 56.6% (1) (2) Total square footage changed due to remeasurement. (3) 2014 Suburban NOI and Cash Basis NOI include income from the settlement of litigation with a former tenant of $2.7 million and $8.8 million for the three months and year ended December 31, 2014, respectively. SAME PROPERTY RESULTS OF OPERATIONS BY PROPERTY LOCATION (dollars and square feet in thousands) As of and for the Three Months Ended December 31, As of and for the Year Ended December 31, Quarter-to-date results include properties continuously owned from October 1, 2013 through December 31, 2014. Year-to-date results include properties continuously owned from January 1, 2013 through December 31, 2014. Amounts related to the settlement of outstanding assets and liabilities of previously-disposed properties that are reflected in our consolidated results are excluded. |

18

|

|

Weighted Average Year Annualized Built or No. of Property Square Leased Rental Undepreciated Net Book Date Substantially Property City State Buildings Location Feet Occupancy Revenue (2) Book Value (3) Value (4) Acquired Renovated (5) 1. Illinois Center Chicago IL 2 CBD 2,090,162 72.7% 45,982 $ 333,635 $ 310,502 $ 5/11/2011;1/9/2012 2001 2. 600 West Chicago Avenue Chicago IL 2 CBD 1,511,849 90.9% 45,529 354,937 327,581 8/10/2011 2001 3. 1735 Market Street Philadelphia PA 1 CBD 1,290,678 91.8% 36,754 297,904 186,994 6/30/1998 1990 4. 1500 Market Street Philadelphia PA 1 CBD 1,773,967 79.5% 34,522 282,247 213,271 10/10/2002 1974 5. 111 Monument Circle Indianapolis IN 2 CBD 1,063,885 80.1% 23,824 172,769 164,032 10/22/2012 1990 6. 111 River Street Hoboken NJ 1 CBD 566,215 95.7% 22,965 134,801 116,595 8/11/2009 2002 7. 185 Asylum Street Hartford CT 1 CBD 868,395 98.6% 21,607 78,098 73,851 3/30/2012 2010 8. 1225 Seventeenth Street Denver CO 1 CBD 672,465 92.7% 20,401 145,106 127,650 6/24/2009 1982 9. 701 Poydras Street New Orleans LA 1 CBD 1,256,971 95.6% 20,013 97,611 90,359 8/29/2011 2010 10. 333 108th Avenue NE Bellevue WA 1 CBD 416,503 100.0% 17,590 152,543 134,114 11/12/2009 2008 11. 1600 Market Street Philadelphia PA 1 CBD 825,968 84.9% 17,583 131,728 80,220 3/30/1998 1983 12. 6600 North Military Trail Boca Raton FL 3 Suburban 639,830 100.0% 17,086 145,690 132,711 1/11/2011 2008 13. North Point Office Complex Cleveland OH 2 CBD 873,335 79.3% 16,028 121,944 103,095 2/12/2008 1988 14. 8750 Bryn Mawr Avenue Chicago IL 2 Suburban 631,518 92.4% 15,656 90,824 81,687 10/28/2010 2005 15. 310-320 Pitt Street Sydney Australia 1 CBD 313,865 100.0% 14,661 137,587 128,478 12/21/2010 1989 16. Arizona Center (6) Phoenix AZ 4 CBD 1,070,724 94.0% 13,837 97,876 90,906 3/4/2011 1992 17. Foster Plaza Pittsburgh PA 8 Suburban 727,365 90.0% 13,125 73,280 56,615 9/16/2005 1993 18. 101-115 W. Washington Street Indianapolis IN 1 CBD 634,058 92.1% 11,883 89,120 68,245 5/10/2005 1977 19. 100 East Wisconsin Avenue Milwaukee WI 1 CBD 435,067 94.7% 11,843 81,878 72,815 8/11/2010 1989 20. Research Park Austin TX 4 Suburban 1,110,007 98.0% 11,507 90,585 63,737 10/7/1998 1976 21. 111 Market Place Baltimore MD 1 CBD 540,854 96.9% 11,177 76,043 54,112 1/28/2003 1990 22. East Eisenhower Parkway Ann Arbor MI 2 Suburban 410,464 92.8% 10,311 55,045 49,517 6/15/2010 2006 23. Bridgepoint Parkway Austin TX 5 Suburban 440,007 93.4% 10,270 88,067 53,238 12/5/1997 1995 24. 420 20th Street North Birmingham AL 1 CBD 514,893 77.9% 9,718 55,702 50,978 7/29/2011 2006 25. 111 East Kilbourn Avenue Milwaukee WI 1 CBD 373,669 95.9% 9,309 55,069 46,150 6/12/2008 1988 26. 109 Brookline Avenue Boston MA 1 CBD 285,556 94.3% 9,047 45,057 27,812 9/28/1995 1915 27. Inverness Center Birmingham AL 4 Suburban 475,882 89.7% 8,798 51,699 46,485 12/9/2010 1981 28. Woodcliff Drive Fairport NY 6 Suburban 516,760 79.8% 8,417 48,047 44,396 3/14/2006 1995 29. 5073, 5075, & 5085 S. Syracuse Street Denver CO 1 Suburban 248,493 100.0% 8,035 63,610 56,739 4/16/2010 2007 30. 1320 Main Street Columbia SC 1 CBD 334,075 91.2% 7,733 55,117 52,109 9/18/2012 2004 Subtotal (30 properties) 63 22,913,480 89.0% 525,211 3,703,619 3,104,994 All other properties (126 properties) 199 20,005,355 82.2% 259,979 2,024,824 1,593,004 Total (156 properties) 262 42,918,835 85.8% 785,190 $ 5,728,443 $ 4,697,998 $ Q4 2014 Q4 2014 Cash Basis % of Cash NOI (7) % of NOI NOI (7) Basis NOI Subtotal (30 properties) 80,178 $ 67.5% 77,542 $ 66.2% All other properties (126 properties) 38,638 32.5% 39,570 33.8% Total (156 properties) 118,816 $ 100.0% 117,112 $ 100.0% (1) Excludes SIR properties and properties classified as discontinued operations for the period ended December 31, 2014. (2) (3) Represents the carrying value of real estate properties, after purchase price allocations, impairment write downs and currency adjustments, if any. (4) Represents the carrying value of real estate properties, after depreciation and amortization, purchase price allocations, impairment write downs and currency adjustments, if any. (5) Weighted based on square feet. (6) (7) Non-GAAP financial measure which is defined in the "Definitions" section of this document. Please refer to the calculation in this document which reconciles the differences between the non-GAAP financial measure and the most directly comparable GAAP financial measure. Contractual cash payments (including management fees) from one tenant at Arizona Center for 2014 were $8,128 and will decrease to approximately $515 beginning in 2016. Our calculation of Normalized FFO reflects the cash payments received from this tenant. The terms of this tenant's lease require us to classify the lease as a direct financing (or capital) lease. As such, the revenue recognized on a GAAP basis within our condensed consolidated statements of operations was $172 and $257 for the quarters ended December 31, 2014 and 2013, respectively and $817 and $1,154 years ended December 31, 2014 and 2013, respectively. This direct financing lease has an expiration date in 2045. Annualized rental revenue is annualized contractual rents from our tenants pursuant to existing leases as of December 31, 2014, plus straight line rent adjustments and estimated recurring expense reimbursements; includes some triple net lease rents and excludes lease value amortization. TOP 30 PROPERTIES BY ANNUALIZED RENTAL REVENUE As of December 31, 2014 (1) (sorted by annualized rental revenue, dollars in thousands) 19 |

19

|

|

12/31/2014 9/30/2014 6/30/2014 3/31/2014 12/31/2013 Properties 156 156 156 156 156 Total square feet (2) 42,919 42,919 42,920 42,913 42,915 Percentage leased (3) 85.8% 85.9% 86.7% 86.5% 87.0% Renewal Leases Square feet 1,173 792 1,204 459 1,215 Lease term (years) 4.5 12.4 6.0 5.5 7.2 Percent change in cash rent (4) 1.6% (2.8%) (2.2%) (3.9%) (3.1%) Percent change in GAAP rent (4) 8.8% 0.4% 3.7% (1.2%) 1.9% Total TI & LC per square foot (5) 10.17 $ 37.39 $ 9.37 $ 10.98 $ 15.06 $ Total TI & LC per sq. ft. per year of lease term (5) 2.28 $ 3.02 $ 1.56 $ 2.00 $ 2.09 $ New Leases Square feet 275 317 358 214 255 Lease term (years) 6.4 7.0 5.9 8.1 6.1 Percent change in cash rent (4) (2.9%) (2.9%) (8.9%) 6.2% 2.9% Percent change in GAAP rent (4) 1.3% (1.6%) (3.6%) 12.7% 9.7% Total TI & LC per square foot (5) 35.16 $ 13.83 $ 29.89 $ 27.78 $ 22.74 $ Total TI & LC per sq. ft. per year of lease term (5) 5.48 $ 1.98 $ 5.07 $ 3.43 $ 3.73 $ Total Leases Square feet 1,448 1,109 1,562 673 1,470 Lease term (years) 4.8 10.8 6.0 6.3 7.0 Percent change in cash rent (4) 1.2% (2.8%) (3.7%) (0.7%) (2.1%) Percent change in GAAP rent (4) 8.1% 0.1% 2.0% 3.3% 3.2% Total TI & LC per square foot (5) 14.92 $ 30.66 $ 14.07 $ 16.32 $ 16.39 $ Total TI & LC per sq. ft. per year of lease term (5) 3.08 $ 2.84 $ 2.36 $ 2.45 $ 2.38 $ (1) (2) (3) (4) (5) LEASING SUMMARY (dollars and square feet in thousands, except per square foot data) Excludes SIR's properties and properties classified as discontinued operations for the period ended December 31, 2014. Sq. ft. measurements are subject to modest changes when space is re-measured or re-configured for tenants. Percent leased includes (i) space being fitted out for occupancy pursuant to existing leases and (ii) space which is leased but is not occupied or is being offered for sublease by tenants. Percent change in GAAP and cash rent is a comparison of current rent (including tenant expense reimbursements, if any, and excluding any initial period free rent), to the rent (including tenant expense reimbursements, if any) last received for the same space during EQC's ownership on a GAAP and cash basis, respectively. Beginning in Q4 2014, new leasing in suites vacant longer than 2 years were excluded from the calculation. Includes commitments made for leasing expenditures and concessions, such as tenant improvements and leasing commissions. The above leasing summary is based on leases executed during the periods indicated. As of and for the Three Months Ended (1) 20 |

20

|

|

CBD Properties Suburban Properties Total Properties 40 116 156 Total square feet (2) 21,892 21,027 42,919 Percentage leased (3) 84.7% 87.0% 85.8% Renewal Leases Square feet 553 620 1,173 Lease term (years) 2.8 5.9 4.5 Percentage change in cash rent (4) 9.9% (5.6%) 1.6% Percentage change in GAAP rent (4) 17.0% 1.5% 8.8% Total TI & LC per square foot (5) 8.61 $ 11.57 $ 10.17 $ Total TI & LC per sq. ft. per year of lease term (5) 3.05 $ 1.95 $ 2.28 $ New Leases Square feet 133 142 275 Lease term (years) 7.2 5.6 6.4 Percentage change in cash rent (4) (8.2%) 1.4% (2.9%) Percentage change in GAAP rent (4) (4.4%) 5.8% 1.3% Total TI & LC per square foot (5) 46.19 $ 24.89 $ 35.16 $ Total TI & LC per sq. ft. per year of lease term (5) 6.38 $ 4.41 $ 5.48 $ Total Leases Square feet 686 763 1,448 Lease term (years) 3.7 5.9 4.8 Percentage change in cash rent (4) 8.4% (5.0%) 1.2% Percentage change in GAAP rent (4) 15.2% 1.9% 8.1% Total TI & LC per square foot (5) 15.87 $ 14.05 $ 14.92 $ Total TI & LC per sq. ft. per year of lease term (5) 4.32 $ 2.39 $ 3.08 $ (1) (2) (3) (4) (5) The above leasing summary is based on leases executed during the periods indicated. As of and for the Three Months Ended (1) LEASING SUMMARY BY PROPERTY LOCATION (dollars and square feet in thousands, except per square foot data) Percent leased includes (i) space being fitted out for occupancy pursuant to existing leases and (ii) space which is leased but is not occupied or is being offered for sublease by tenants. Square feet measurements are subject to modest changes when space is re-measured or re-configured for tenants. Excludes SIR's properties and properties classified as discontinued operations for the period ended December 31, 2014. Percent change in GAAP and cash rent is a comparison of current rent (including tenant expense reimbursements, if any, and excluding any initial period free rent), to the rent (including tenant expense reimbursements, if any) last received for the same space during EQC's ownership on a GAAP and cash basis, respectively. Beginning in Q4 2014, new leasing in suites vacant longer than 2 years were excluded from the calculation. Includes commitments made for leasing expenditures and concessions, such as tenant improvements and leasing commissions. December 31, 2014 21 |

21

|

|

Total Sq. Ft. As of 12/31/2014 Renewals New Total CBD Properties 21,892 553 133 686 Suburban Properties 21,027 620 142 763 Total 42,919 1,173 275 1,448 Renewals Total % Leased (1) Expired and New Acquisitions Total % Leased (1) CBD Properties 18,508 84.5% (642) 686 - 18,552 84.7% Suburban Properties 18,369 87.4% (843) 763 - 18,288 87.0% Total 36,877 85.9% (1,485) 1,448 - 36,840 85.8% (1) OCCUPANCY AND LEASING ANALYSIS BY PROPERTY LOCATION (square feet in thousands) Property Location Three Months Ended December 31, 2014 Leases Executed During Property Location Square Footage Leased Percent leased includes (i) space being fitted out for occupancy pursuant to existing leases and (ii) space which is leased but is not occupied or is being offered for sublease by tenants. September 30, 2014 December 31, 2014 22 |

22

|

|

% of Weighted Average Square % of Total Annualized Rental Remaining Feet (1) Sq. Ft. (1) Revenue (2) Lease Term 1. Office Depot, Inc. 651 1.5% 2.2% 8.7 2. Expedia, Inc. 398 0.9% 2.2% 3.8 3. John Wiley & Sons, Inc. 386 0.9% 2.0% 18.2 4. Telstra Corporation Limited 311 0.7% 1.9% 5.4 5. PNC Financial Services Group 587 1.4% 1.9% 6.1 6. U.S. Government 463 1.1% 1.6% 5.2 7. Royal Dutch Shell plc 700 1.6% 1.4% 11.3 8. J.P. Morgan Chase & Co. 388 0.9% 1.4% 9.4 9. Flextronics International Ltd. 1,051 2.4% 1.4% 5.0 10. United Healthcare Services Inc. 479 1.1% 1.3% 7.9 11. The Bank of New York Mellon Corp. 395 0.9% 1.3% 2.9 12. Carmike Cinemas, Inc. 417 1.0% 1.2% 1.7 13. Bankers Life and Casualty Company 349 0.8% 1.2% 5.8 14. Jones Day 343 0.8% 1.2% 11.5 15. Wells Fargo & Co 350 0.8% 1.2% 3.5 16. Level 3 Communications, Inc. 219 0.5% 1.1% 5.3 17. Towers Watson & Co. 348 0.8% 1.1% 4.4 18. Ballard Spahr LLP 218 0.5% 1.1% 15.1 19. RE/MAX Holdings, Inc. 248 0.6% 1.0% 13.3 Total 8,301 19.2% 27.7% 7.3 (1) (2) Annualized rental revenue is annualized contractual rents from our tenants pursuant to existing leases as of December 31, 2014, plus straight line rent adjustments and estimated recurring expense reimbursements; includes some triple net lease rents and excludes lease value amortization. Square footage is pursuant to existing leases as of December 31, 2014 and includes (i) space being fitted out for occupancy and (ii) space which is leased but is not occupied or is being offered for sublease. TENANTS REPRESENTING 1% OR MORE OF TOTAL ANNUALIZED RENTAL REVENUE (square feet in thousands) Tenant As of December 31, 2014 |

23

|

|

CBD Properties Cumulative % Number of Cumulative % Annualized % of Annualized of Annualized Tenants Sq. Ft. % of Sq. Ft. of Sq. Ft. Rental Revenue Rental Revenue Rental Revenue Year Expiring Expiring (1) Expiring Expiring Expiring (2) Expiring Expiring 2015 228 1,794 9.7% 9.7% 52,455 10.7% 10.7% 2016 140 1,393 7.5% 17.2% 41,744 8.5% 19.2% 2017 148 1,707 9.2% 26.4% 44,904 9.1% 28.3% 2018 132 2,603 14.0% 40.4% 66,286 13.5% 41.8% 2019 96 1,442 7.8% 48.2% 39,407 8.0% 49.8% 2020 64 2,115 11.4% 59.6% 60,743 12.4% 62.2% 2021 42 1,247 6.7% 66.3% 31,637 6.4% 68.6% 2022 37 1,038 5.6% 71.9% 22,919 4.7% 73.3% 2023 39 1,211 6.5% 78.4% 31,424 6.4% 79.7% 2024 25 744 4.0% 82.4% 22,016 4.5% 84.2% Thereafter 41 3,259 17.6% 100.0% 77,740 15.8% 100.0% Total 992 18,552 100.0% 491,275 $ 100.0% Weighted average remaining lease term (in years) 6.5 6.4 Suburban Properties Cumulative % Number of Cumulative % Annualized % of Annualized of Annualized Tenants Sq. Ft. % of Sq. Ft. of Sq. Ft. Rental Revenue Rental Revenue Rental Revenue Year Expiring Expiring (1) Expiring Expiring Expiring (2) Expiring Expiring 2015 183 2,307 12.6% 12.6% 34,904 11.9% 11.9% 2016 165 3,195 17.5% 30.1% 42,035 14.3% 26.2% 2017 131 1,984 10.8% 40.9% 36,856 12.5% 38.7% 2018 98 1,583 8.7% 49.6% 24,972 8.5% 47.2% 2019 81 2,309 12.6% 62.2% 31,995 10.9% 58.1% 2020 59 1,714 9.4% 71.6% 21,967 7.5% 65.6% 2021 41 1,082 5.9% 77.5% 18,955 6.4% 72.0% 2022 23 928 5.1% 82.6% 17,609 6.0% 78.0% 2023 24 1,594 8.7% 91.3% 36,403 12.4% 90.4% 2024 13 534 2.9% 94.2% 6,320 2.2% 92.5% Thereafter 15 1,057 5.8% 100.0% 21,899 7.5% 100.0% Total 833 18,288 100.0% 293,915 $ 100.0% Weighted average remaining lease term (in years) 4.6 5.0 Total Properties Cumulative % Number of Cumulative % Annualized % of Annualized of Annualized Tenants Sq. Ft. % of Sq. Ft. of Sq. Ft. Rental Revenue Rental Revenue Rental Revenue Year Expiring Expiring (1) Expiring Expiring Expiring (2) Expiring Expiring 2015 411 4,101 11.1% 11.1% 88,674 11.3% 11.3% 2016 305 4,588 12.5% 23.6% 83,616 10.6% 21.9% 2017 279 3,691 10.0% 33.6% 80,566 10.3% 32.2% 2018 230 4,187 11.4% 45.0% 91,443 11.6% 43.8% 2019 177 3,751 10.2% 55.2% 70,949 9.0% 52.9% 2020 123 3,829 10.4% 65.6% 82,362 10.5% 63.4% 2021 83 2,329 6.3% 71.9% 51,120 6.5% 69.9% 2022 60 1,966 5.3% 77.2% 39,661 5.1% 74.9% 2023 63 2,804 7.6% 84.8% 68,063 8.7% 83.6% 2024 38 1,278 3.5% 88.3% 28,008 3.6% 87.2% Thereafter 56 4,316 11.7% 100.0% 100,728 12.8% 100.0% Total 1,825 36,840 100.0% 785,190 $ 100.0% Weighted average remaining lease term (in years) 5.6 5.9 (1) (2) Annualized rental revenue is annualized contractual rents from our tenants pursuant to existing leases as of 12/31/2014, plus straight line rent adjustments and estimated recurring expense reimbursements; includes some triple net lease rents and excludes lease value amortization. PORTFOLIO LEASE EXPIRATION SCHEDULE As of December 31, 2014 (dollars and sq. ft. in thousands) Square feet is pursuant to existing leases as of December 31, 2014 and includes (i) space being fitted out for occupancy and (ii) space which is leased but is not occupied or is being offered for sublease. 24 |

24

|

|

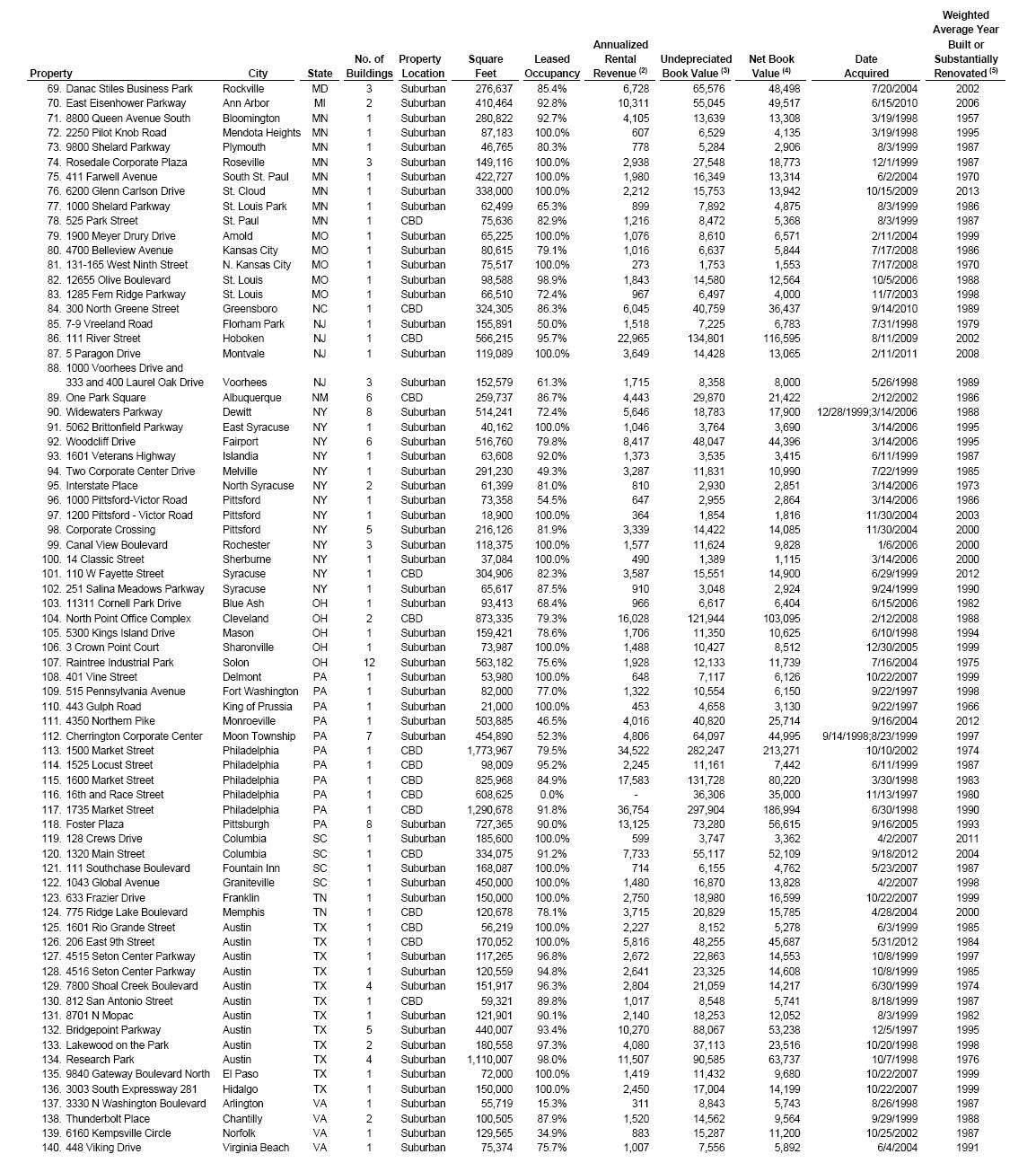

Weighted Average Year Annualized Built or No. of Property Square Leased Rental Undepreciated Net Book Date Substantially Property City State Buildings Location Feet Occupancy Revenue (2) Book Value (3) Value (4) Acquired Renovated (5) 1. 2501 20th Place South Birmingham AL 1 CBD 125,722 98.6% 2,947 $ 24,115 $ 19,962 $ 12/27/2006 2001 2. 420 20th Street North Birmingham AL 1 CBD 514,893 77.9% 9,718 55,702 50,978 7/29/2011 2006 3. Inverness Center Birmingham AL 4 Suburban 475,882 89.7% 8,798 51,699 46,485 12/9/2010 1981 4. 785 Schilinger Road South Mobile AL 1 Suburban 72,000 100.0% 1,388 11,269 9,522 10/22/2007 1998 5. Arizona Center (6) Phoenix AZ 4 CBD 1,070,724 94.0% 13,837 97,876 90,906 3/4/2011 1992 6. 4 South 84th Avenue Tolleson AZ 1 Suburban 236,007 100.0% 1,515 11,382 8,743 12/19/2003 1989 7. One South Church Avenue Tucson AZ 1 CBD 240,811 66.1% 3,673 33,380 24,251 2/27/2002 1986 8. Parkshore Plaza Folsom CA 4 Suburban 269,281 98.0% 5,820 46,629 42,847 6/16/2011 1999 9. Leased Land Gonzalez CA 7 Suburban - 100.0% 3,181 31,825 29,549 8/31/2010 - 10. Sky Park Centre San Diego CA 2 Suburban 63,485 100.0% 1,364 9,786 6,757 6/24/2002 1986 11. Sorrento Valley Business Park San Diego CA 4 Suburban 105,003 100.0% 2,039 17,575 10,624 12/31/1996 1984 12. 1921 E. Alton Avenue Santa Ana CA 1 Suburban 67,846 84.7% 1,683 11,522 8,614 11/10/2003 2000 13. 9110 East Nichols Avenue Centennial CO 1 Suburban 143,958 96.2% 2,397 20,286 14,547 11/2/2001 1984 14. 7450 Campus Drive Colorado Springs CO 1 Suburban 77,411 100.0% 1,814 9,481 8,519 4/30/2010 1996 15. 1225 Seventeenth Street Denver CO 1 CBD 672,465 92.7% 20,401 145,106 127,650 6/24/2009 1982 16. 5073, 5075, & 5085 S. Syracuse Street Denver CO 1 Suburban 248,493 100.0% 8,035 63,610 56,739 4/16/2010 2007 17. 1601 Dry Creek Drive Longmont CO 1 Suburban 552,865 97.0% 6,661 32,355 24,189 10/26/2004 1982 18. 129 Worthington Ridge Road Berlin CT 1 Suburban 227,500 100.0% 781 5,252 4,538 10/24/2006 1968 19. 97 Newberry Road East Windsor CT 1 Suburban 289,386 100.0% 1,761 15,350 12,795 10/24/2006 1989 20. 185 Asylum Street Hartford CT 1 CBD 868,395 98.6% 21,607 78,098 73,851 3/30/2012 2010 21. 599 Research Parkway Meriden CT 1 Suburban 48,249 100.0% 823 8,092 6,154 7/24/2003 1982 22. 33 Stiles Lane North Haven CT 1 Suburban 175,301 100.0% 1,119 9,793 7,844 10/24/2006 2002 23. 181 Marsh Hill Road Orange CT 1 Suburban 162,036 100.0% 1,199 10,794 9,135 10/24/2006 2006 24. 101 Barnes Road Wallingford CT 1 Suburban 45,755 90.5% 951 1,423 1,384 12/22/1998 1988 25. 15 Sterling Drive Wallingford CT 1 Suburban 173,015 72.5% 1,324 4,805 4,689 10/24/2006 1978 26. 35 Thorpe Avenue Wallingford CT 1 Suburban 79,862 85.1% 1,065 6,502 6,317 6/1/1998 1986 27. 50 Barnes Industrial Road North Wallingford CT 1 Suburban 154,255 100.0% 1,342 11,404 8,947 10/24/2006 1976 28. 5-9 Barnes Industrial Road Wallingford CT 1 Suburban 38,006 99.3% 430 3,510 2,963 10/24/2006 1980 29. 860 North Main Street Wallingford CT 1 Suburban 31,165 99.5% 451 3,850 2,931 10/24/2006 1982 30. One Barnes Industrial Road SouthWallingford CT 1 Suburban 30,170 100.0% 351 2,366 1,900 10/24/2006 1977 31. Village Lane Wallingford CT 2 Suburban 58,185 100.0% 708 4,016 3,907 10/24/2006 1977 32. 100 Northfield Drive Windsor CT 1 Suburban 116,986 97.4% 1,843 13,286 9,052 8/29/2003 1988 33. 1250 H Street, NW Washington DC 1 CBD 187,684 74.7% 5,481 65,025 40,956 6/23/1998 1992 34. Georgetown-Green and Harris Buildings Washington DC 2 CBD 240,475 100.0% 6,073 60,023 55,226 9/3/2009 2006 35. 802 Delaware Avenue Wilmington DE 1 CBD 240,780 100.0% 3,549 43,464 21,500 7/23/1998 1986 36. 6600 North Military Trail Boca Raton FL 3 Suburban 639,830 100.0% 17,086 145,690 132,711 1/11/2011 2008 37. 225 Water Street Jacksonville FL 1 CBD 318,997 44.7% 2,650 20,012 19,674 11/24/2008 1985 38. 9040 Roswell Road Atlanta GA 1 Suburban 178,941 79.2% 2,425 23,221 17,796 8/24/2004 1985 39. Executive Park Atlanta GA 9 Suburban 427,443 67.9% 4,973 43,431 29,484 7/16/2004;7/26/2007 1972 40. The Exchange Atlanta GA 2 Suburban 187,632 79.3% 2,279 17,880 13,504 9/9/2004;9/2/2005 1995 41. 3920 Arkwright Road Macon GA 1 Suburban 196,156 79.5% 2,739 20,494 15,669 4/28/2006 1988 42. 1775 West Oak Commons Court Marietta GA 1 Suburban 79,854 100.0% 1,180 8,304 6,846 9/5/2007 1998 43. 633 Ahua Street Honolulu HI 1 Suburban 120,803 89.2% 1,769 16,397 13,000 12/5/2003 2006 44. 625 Crane Street Aurora IL 1 Suburban 103,683 100.0% 408 1,611 1,555 4/2/2007 1977 45. 905 Meridian Lake Drive Aurora IL 1 Suburban 74,652 100.0% 2,157 12,309 9,700 5/1/2007 1999 46. 1200 Lakeside Drive Bannockburn IL 1 Suburban 260,084 74.6% 4,680 65,037 52,073 12/29/2005 1999 47. 600 West Chicago Avenue Chicago IL 2 CBD 1,511,849 90.9% 45,529 354,937 327,581 8/10/2011 2001 48. 8750 Bryn Mawr Avenue Chicago IL 2 Suburban 631,518 92.4% 15,656 90,824 81,687 10/28/2010 2005 49. Illinois Center Chicago IL 2 CBD 2,090,162 72.7% 45,982 333,635 310,502 5/11/2011;1/9/2012 2001 50. 1717 Deerfield Road Deerfield IL 1 Suburban 141,186 69.5% 2,288 8,499 8,286 12/14/2005 1986 51. 1955 West Field Court Lake Forest IL 1 Suburban 59,130 100.0% 1,176 11,925 8,900 12/14/2005 2001 52. 11350 North Meridian Street Carmel IN 1 Suburban 72,264 78.4% 707 2,721 2,596 6/15/2006 1982 53. 101-115 W. Washington Street Indianapolis IN 1 CBD 634,058 92.1% 11,883 89,120 68,245 5/10/2005 1977 54. 111 Monument Circle Indianapolis IN 2 CBD 1,063,885 80.1% 23,824 172,769 164,032 10/22/2012 1990 55. 5015 S. Water Circle Wichita KS 1 Suburban 113,524 100.0% 581 5,874 5,143 4/2/2007 1995 56. 701 Poydras Street New Orleans LA 1 CBD 1,256,971 95.6% 20,013 97,611 90,359 8/29/2011 2010 57. 109 Brookline Avenue Boston MA 1 CBD 285,556 94.3% 9,047 45,057 27,812 9/28/1995 1915 58. Adams Place Braintree/Quincy MA 2 Suburban 230,259 76.2% 3,774 19,775 18,922 4/3/1998 2006 59. Cabot Business Park Mansfield MA 2 Suburban 252,755 48.8% 1,834 14,728 14,172 8/1/2003 1980 60. Cabot Business Park Land Mansfield MA - Suburban - 100.0% - 1,033 1,033 8/1/2003 - 61. 2300 Crown Colony Drive Quincy MA 1 Suburban 45,974 95.5% 1,002 7,144 4,725 2/24/2004 1999 62. Myles Standish Industrial Park Taunton MA 2 Suburban 74,800 100.0% 1,091 7,878 7,743 8/29/2007 1988 63. 340 Thompson Road Webster MA 1 Suburban 25,000 100.0% 191 3,188 1,918 5/15/1997 1995 64. 100 South Charles Street Baltimore MD 1 CBD 159,616 86.0% 2,792 16,361 9,491 11/18/1997 1988 65. 111 Market Place Baltimore MD 1 CBD 540,854 96.9% 11,177 76,043 54,112 1/28/2003 1990 66. 25 S. Charles Street Baltimore MD 1 CBD 343,815 93.9% 6,405 38,503 27,345 7/16/2004 1972 67. 820 W. Diamond Gaithersburg MD 1 Suburban 134,933 82.1% 2,670 33,372 23,142 3/31/1997 1995 68. 6710 Oxon Hill Oxon Hill MD 1 Suburban 118,336 60.3% 1,461 17,532 10,500 3/31/1997 1992 PROPERTY DETAIL As of December 31, 2014 (1) (sorted by geographic location, dollars in thousands) 25 |

25

|

|

Weighted Average Year Annualized Built or No. of Property Square Leased Rental Undepreciated Net Book Date Substantially Property City State Buildings Location Feet Occupancy Revenue (2) Book Value (3) Value (4) Acquired Renovated (5) 69. Danac Stiles Business Park Rockville MD 3 Suburban 276,637 85.4% 6,728 65,576 48,498 7/20/2004 2002 70. East Eisenhower Parkway Ann Arbor MI 2 Suburban 410,464 92.8% 10,311 55,045 49,517 6/15/2010 2006 71. 8800 Queen Avenue South Bloomington MN 1 Suburban 280,822 92.7% 4,105 13,639 13,308 3/19/1998 1957 72. 2250 Pilot Knob Road Mendota Heights MN 1 Suburban 87,183 100.0% 607 6,529 4,135 3/19/1998 1995 73. 9800 Shelard Parkway Plymouth MN 1 Suburban 46,765 80.3% 778 5,284 2,906 8/3/1999 1987 74. Rosedale Corporate Plaza Roseville MN 3 Suburban 149,116 100.0% 2,938 27,548 18,773 12/1/1999 1987 75. 411 Farwell Avenue South St. Paul MN 1 Suburban 422,727 100.0% 1,980 16,349 13,314 6/2/2004 1970 76. 6200 Glenn Carlson Drive St. Cloud MN 1 Suburban 338,000 100.0% 2,212 15,753 13,942 10/15/2009 2013 77. 1000 Shelard Parkway St. Louis Park MN 1 Suburban 62,499 65.3% 899 7,892 4,875 8/3/1999 1986 78. 525 Park Street St. Paul MN 1 CBD 75,636 82.9% 1,216 8,472 5,368 8/3/1999 1987 79. 1900 Meyer Drury Drive Arnold MO 1 Suburban 65,225 100.0% 1,076 8,610 6,571 2/11/2004 1999 80. 4700 Belleview Avenue Kansas City MO 1 Suburban 80,615 79.1% 1,016 6,637 5,844 7/17/2008 1986 81. 131-165 West Ninth Street N. Kansas City MO 1 Suburban 75,517 100.0% 273 1,753 1,553 7/17/2008 1970 82. 12655 Olive Boulevard St. Louis MO 1 Suburban 98,588 98.9% 1,843 14,580 12,564 10/5/2006 1988 83. 1285 Fern Ridge Parkway St. Louis MO 1 Suburban 66,510 72.4% 967 6,497 4,000 11/7/2003 1998 84. 300 North Greene Street Greensboro NC 1 CBD 324,305 86.3% 6,045 40,759 36,437 9/14/2010 1989 85. 7-9 Vreeland Road Florham Park NJ 1 Suburban 155,891 50.0% 1,518 7,225 6,783 7/31/1998 1979 86. 111 River Street Hoboken NJ 1 CBD 566,215 95.7% 22,965 134,801 116,595 8/11/2009 2002 87. 5 Paragon Drive Montvale NJ 1 Suburban 119,089 100.0% 3,649 14,428 13,065 2/11/2011 2008 88. 1000 Voorhees Drive and 333 and 400 Laurel Oak Drive Voorhees NJ 3 Suburban 152,579 61.3% 1,715 8,358 8,000 5/26/1998 1989 89. One Park Square Albuquerque NM 6 CBD 259,737 86.7% 4,443 29,870 21,422 2/12/2002 1986 90. Widewaters Parkway Dewitt NY 8 Suburban 514,241 72.4% 5,646 18,783 17,900 12/28/1999;3/14/2006 1988 91. 5062 Brittonfield Parkway East Syracuse NY 1 Suburban 40,162 100.0% 1,046 3,764 3,690 3/14/2006 1995 92. Woodcliff Drive Fairport NY 6 Suburban 516,760 79.8% 8,417 48,047 44,396 3/14/2006 1995 93. 1601 Veterans Highway Islandia NY 1 Suburban 63,608 92.0% 1,373 3,535 3,415 6/11/1999 1987 94. Two Corporate Center Drive Melville NY 1 Suburban 291,230 49.3% 3,287 11,831 10,990 7/22/1999 1985 95. Interstate Place North Syracuse NY 2 Suburban 61,399 81.0% 810 2,930 2,851 3/14/2006 1973 96. 1000 Pittsford-Victor Road Pittsford NY 1 Suburban 73,358 54.5% 647 2,955 2,864 3/14/2006 1986 97. 1200 Pittsford - Victor Road Pittsford NY 1 Suburban 18,900 100.0% 364 1,854 1,816 11/30/2004 2003 98. Corporate Crossing Pittsford NY 5 Suburban 216,126 81.9% 3,339 14,422 14,085 11/30/2004 2000 99. Canal View Boulevard Rochester NY 3 Suburban 118,375 100.0% 1,577 11,624 9,828 1/6/2006 2000 100. 14 Classic Street Sherburne NY 1 Suburban 37,084 100.0% 490 1,389 1,115 3/14/2006 2000 101. 110 W Fayette Street Syracuse NY 1 CBD 304,906 82.3% 3,587 15,551 14,900 6/29/1999 2012 102. 251 Salina Meadows Parkway Syracuse NY 1 Suburban 65,617 87.5% 910 3,048 2,924 9/24/1999 1990 103. 11311 Cornell Park Drive Blue Ash OH 1 Suburban 93,413 68.4% 966 6,617 6,404 6/15/2006 1982 104. North Point Office Complex Cleveland OH 2 CBD 873,335 79.3% 16,028 121,944 103,095 2/12/2008 1988 105. 5300 Kings Island Drive Mason OH 1 Suburban 159,421 78.6% 1,706 11,350 10,625 6/10/1998 1994 106. 3 Crown Point Court Sharonville OH 1 Suburban 73,987 100.0% 1,488 10,427 8,512 12/30/2005 1999 107. Raintree Industrial Park Solon OH 12 Suburban 563,182 75.6% 1,928 12,133 11,739 7/16/2004 1975 108. 401 Vine Street Delmont PA 1 Suburban 53,980 100.0% 648 7,117 6,126 10/22/2007 1999 109. 515 Pennsylvania Avenue Fort Washington PA 1 Suburban 82,000 77.0% 1,322 10,554 6,150 9/22/1997 1998 110. 443 Gulph Road King of Prussia PA 1 Suburban 21,000 100.0% 453 4,658 3,130 9/22/1997 1966 111. 4350 Northern Pike Monroeville PA 1 Suburban 503,885 46.5% 4,016 40,820 25,714 9/16/2004 2012 112. Cherrington Corporate Center Moon Township PA 7 Suburban 454,890 52.3% 4,806 64,097 44,995 9/14/1998;8/23/1999 1997 113. 1500 Market Street Philadelphia PA 1 CBD 1,773,967 79.5% 34,522 282,247 213,271 10/10/2002 1974 114. 1525 Locust Street Philadelphia PA 1 CBD 98,009 95.2% 2,245 11,161 7,442 6/11/1999 1987 115. 1600 Market Street Philadelphia PA 1 CBD 825,968 84.9% 17,583 131,728 80,220 3/30/1998 1983 116. 16th and Race Street Philadelphia PA 1 CBD 608,625 0.0% - 36,306 35,000 11/13/1997 1980 117. 1735 Market Street Philadelphia PA 1 CBD 1,290,678 91.8% 36,754 297,904 186,994 6/30/1998 1990 118. Foster Plaza Pittsburgh PA 8 Suburban 727,365 90.0% 13,125 73,280 56,615 9/16/2005 1993 119. 128 Crews Drive Columbia SC 1 Suburban 185,600 100.0% 599 3,747 3,362 4/2/2007 2011 120. 1320 Main Street Columbia SC 1 CBD 334,075 91.2% 7,733 55,117 52,109 9/18/2012 2004 121. 111 Southchase Boulevard Fountain Inn SC 1 Suburban 168,087 100.0% 714 6,155 4,762 5/23/2007 1987 122. 1043 Global Avenue Graniteville SC 1 Suburban 450,000 100.0% 1,480 16,870 13,828 4/2/2007 1998 123. 633 Frazier Drive Franklin TN 1 Suburban 150,000 100.0% 2,750 18,980 16,599 10/22/2007 1999 124. 775 Ridge Lake Boulevard Memphis TN 1 CBD 120,678 78.1% 3,715 20,829 15,785 4/28/2004 2000 125. 1601 Rio Grande Street Austin TX 1 CBD 56,219 100.0% 2,227 8,152 5,278 6/3/1999 1985 126. 206 East 9th Street Austin TX 1 CBD 170,052 100.0% 5,816 48,255 45,687 5/31/2012 1984 127. 4515 Seton Center Parkway Austin TX 1 Suburban 117,265 96.8% 2,672 22,863 14,553 10/8/1999 1997 128. 4516 Seton Center Parkway Austin TX 1 Suburban 120,559 94.8% 2,641 23,325 14,608 10/8/1999 1985 129. 7800 Shoal Creek Boulevard Austin TX 4 Suburban 151,917 96.3% 2,804 21,059 14,217 6/30/1999 1974 130. 812 San Antonio Street Austin TX 1 CBD 59,321 89.8% 1,017 8,548 5,741 8/18/1999 1987 131. 8701 N Mopac Austin TX 1 Suburban 121,901 90.1% 2,140 18,253 12,052 8/3/1999 1982 132. Bridgepoint Parkway Austin TX 5 Suburban 440,007 93.4% 10,270 88,067 53,238 12/5/1997 1995 133. Lakewood on the Park Austin TX 2 Suburban 180,558 97.3% 4,080 37,113 23,516 10/20/1998 1998 134. Research Park Austin TX 4 Suburban 1,110,007 98.0% 11,507 90,585 63,737 10/7/1998 1976 135. 9840 Gateway Boulevard North El Paso TX 1 Suburban 72,000 100.0% 1,419 11,432 9,680 10/22/2007 1999 136. 3003 South Expressway 281 Hidalgo TX 1 Suburban 150,000 100.0% 2,450 17,004 14,199 10/22/2007 1999 137. 3330 N Washington Boulevard Arlington VA 1 Suburban 55,719 15.3% 311 8,843 5,743 8/26/1998 1987 138. Thunderbolt Place Chantilly VA 2 Suburban 100,505 87.9% 1,520 14,562 9,564 9/29/1999 1988 139. 6160 Kempsville Circle Norfolk VA 1 Suburban 129,565 34.9% 883 15,287 11,200 10/25/2002 1987 140. 448 Viking Drive Virginia Beach VA 1 Suburban 75,374 75.7% 1,007 7,556 5,892 6/4/2004 1991 26 |

26

|

|

Weighted Average Year Annualized Built or No. of Property Square Leased Rental Undepreciated Net Book Date Substantially Property City State Buildings Location Feet Occupancy Revenue (2) Book Value (3) Value (4) Acquired Renovated (5) 141. 333 108th Avenue NE Bellevue WA 1 CBD 416,503 100.0% 17,590 152,543 134,114 11/12/2009 2008 142. 600 108th Avenue NE Bellevue WA 1 CBD 243,520 85.7% 5,394 45,711 35,592 7/16/2004 2012 143. 1331 North Center Parkway Kennewick WA 1 Suburban 53,980 100.0% 909 9,187 7,864 10/22/2007 1999 144. 100 East Wisconsin Avenue Milwaukee WI 1 CBD 435,067 94.7% 11,843 81,878 72,815 8/11/2010 1989 145. 111 East Kilbourn Avenue Milwaukee WI 1 CBD 373,669 95.9% 9,309 55,069 46,150 6/12/2008 1988 146. 7 Modal Crescent Canning Vale Australia 1 Suburban 164,160 100.0% 1,462 13,226 12,772 10/7/2010 2001 147. 71-93 Whiteside Road Clayton Australia 1 Suburban 303,488 100.0% 1,914 15,209 14,460 10/7/2010 1965 148. 9-13 Titanium Court Crestmead Australia 1 Suburban 69,664 46.8% 309 5,078 4,797 10/7/2010 2005 149. 16 Rodborough Road Frenchs Forest Australia 1 Suburban 90,525 100.0% 2,135 14,467 13,608 10/7/2010 1987 150. 22 Rodborough Road Frenchs Forest Australia 1 Suburban 43,427 100.0% 1,043 6,828 6,369 10/7/2010 1997 151. 127-161 Cherry Lane Laverton North Australia 1 Suburban 278,570 100.0% 1,427 8,249 7,787 10/7/2010 1965 152. 310-314 Invermay Road Mowbray Australia 1 Suburban 47,480 100.0% 238 47 - 10/7/2010 1970 153. 253-293 George Town Road Rocherlea Australia 1 Suburban 143,914 100.0% 1,011 117 - 10/7/2010 1970 154. 310-320 Pitt Street Sydney Australia 1 CBD 313,865 100.0% 14,661 137,587 128,478 12/21/2010 1989 155. 44-46 Mandarin Street Villawood Australia 1 Suburban 226,718 82.7% 1,702 13,457 12,643 10/7/2010 1980 156. 19 Leadership Way Wangara Australia 1 Suburban 76,714 100.0% 563 5,941 5,694 10/7/2010 2000 262 42,918,835 85.8% 785,190 $ 5,728,443 $ 4,697,998 $ (1) Excludes SIR properties and properties classified as discontinued operations for the period ended December 31, 2014. (2) (3) Represents the carrying value of real estate properties, after purchase price allocations, impairment writedowns and currency adjustments, if any. (4) Represents the carrying value of real estate properties, after depreciation and amortization, purchase price allocations, impairment writedowns and currency adjustments, if any. (5) Weighted based on square feet. (6) Annualized rental revenue is annualized contractual rents from our tenants pursuant to existing leases as of December 31, 2014, plus straight line rent adjustments and estimated recurring expense reimbursements; includes some triple net lease rents and excludes lease value amortization. Contractual cash payments (including management fees) from one tenant at Arizona Center for 2014 were $8,128 and will decrease to approximately $515 beginning in 2016. Our calculation of Normalized FFO reflects the cash payments received from this tenant. The terms of this tenant's lease require us to classify the lease as a direct financing (or capital) lease. As such, the revenue recognized on a GAAP basis within our condensed consolidated statements of operations was $172 and $257 for the quarters ended December 31, 2014 and 2013, respectively and $817 and $1,154 years ended December 31, 2014 and 2013, respectively. This direct financing lease has an expiration date in 2045. 27 |