Attached files

| file | filename |

|---|---|

| 8-K - 8-K - HERITAGE FINANCIAL CORP /WA/ | d868412d8k.htm |

Investor

Presentation February 2015

Brian Vance

Chief Executive Officer

Jeff Deuel

President and Chief Operating Officer

Don Hinson

Executive Vice President and Chief Financial Officer

Bryan McDonald

Executive Vice President and Chief Lending Officer

Exhibit 99.1 |

Forward-Looking Statements

2

This presentation contains forward-looking statements that are subject to risks and

uncertainties, including, but not limited to: The expected revenues, cost savings,

synergies and other benefits from the Washington Banking merger and our other merger

and acquisition activities might not be realized within the anticipated time frames or at all, and costs or difficulties

relating to integration matters, including but not limited to, customer and employee retention

might be greater than expected;

The credit and concentration risks of lending activities;

Changes in general economic conditions, either nationally or in our market areas;

Competitive market pricing factors and interest rate risks;

Market interest rate volatility;

Balance sheet (for example, loans) concentrations;

Fluctuations in demand for loans and other financial services in our market areas;

Changes in legislative or regulatory requirements or the results of regulatory

examinations; The ability to recruit and retain key management and staff;

Risks associated with our ability to implement our expansion strategy and merger

integration; Stability of funding sources and continued availability of

borrowings; Adverse changes in the securities markets;

The inability of key third-party providers to perform their obligations to us;

Changes

in

accounting

policies

and

practices

and

the

use

of

estimates

in

determining

fair

value

of

certain

of

our

assets,

which

estimates

may

prove

to

be

incorrect

and

result

in

significant

declines

in

valuation;

and

These and other risks as may be detailed from time to time in our filings with the Securities

and Exchange Commission. The Company cautions readers not to place undue reliance on any

forward-looking statements. Moreover, you should treat these statements as speaking

only as of the date they are made and based only on information then actually known to the Company. The

Company does not undertake and specifically disclaims any obligation to revise any

forward-looking statements to reflect the occurrence of anticipated or

unanticipated events or circumstances after the date of such statements. These risks could cause our

actual results for 2014 and beyond to differ materially from those expressed in any

forward-looking statements by, or on behalf of, us, and could negatively affect the

Company’s operating and stock price performance. |

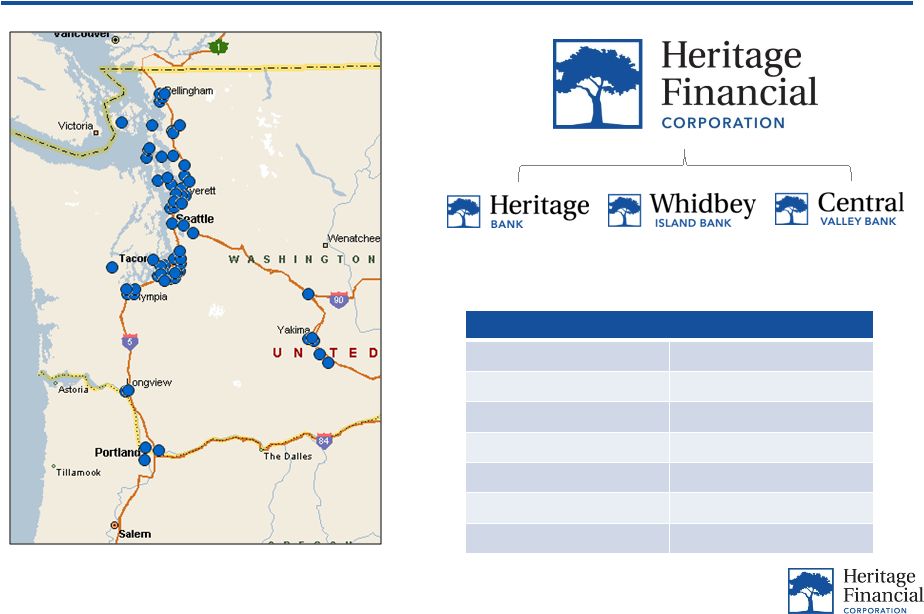

Overview

3

Overview

NASDAQ Symbol

HFWA

Market Capitalization

$481.7 million

Institutional Ownership

75.3%

Total Assets

$3.5 billion

Headquarters

Olympia, WA

# of Branches

66

Year Established

1927

Note: Financial information as of 12/31/2014 and market information as of 2/2/2015

Three banks, one charter |

Transformational Merger with WBCO in 2014

4

Merger of Heritage Financial Corporation and Washington Banking Company

combined two quality community banks to create a $3.5+ billion franchise

Logical geographic fit

Created significant operational scale and efficiencies

Effective use of capital with improved returns on tangible common equity

Positioned to expand in metro markets

Completed merger on May 1, 2014

Completed system conversion onto Heritage’s core system on October 5, 2014

Achieving targeted merger related cost savings –

full benefit expected to be

recognized in early 2015 |

Rank

Total

WA -

HQ

Institution (State)

Number of

Branches

Deposits in

Market

Market

Share

1

Bank of America Corp. (NC)

189

25,422,347

$

+3.6%

20.68%

2

Wells Fargo & Co. (CA)

159

14,569,387

$

+7.5%

11.85%

3

U.S. Bancorp (MN)

189

12,940,872

$

+0.8%

10.53%

4

JPMorgan Chase & Co. (NY)

211

12,235,289

$

+10.0%

9.95%

5

KeyCorp (OH)

162

8,935,023

$

+4.4%

7.27%

6

Umpqua Holdings Corp. (OR)

110

5,101,869

$

+13.7%

4.15%

7

1

Washington Federal Inc. (WA)

82

4,916,698

$

-2.5%

4.00%

8

2

Banner Corp. (WA)

99

4,029,793

$

+7.7%

3.28%

9

3

Columbia Banking System Inc. (WA)

78

3,655,191

$

+3.2%

2.97%

10

4

W.T.B. Financial Corp. (WA)

27

3,192,886

$

+4.3%

2.60%

11

Mitsubishi UFJ Finl Grp Inc.

43

3,098,038

$

+0.6%

2.52%

12

5

Heritage Financial Corp. (WA)

65

2,853,726

$

+1.2%

2.32%

13

6

HomeStreet Inc. (WA)

29

1,905,969

$

+9.9%

1.55%

14

7

Yakima FS&LA (WA)

10

1,367,785

$

-2.4%

1.11%

15

8

Peoples Bancorp (WA)

23

1,179,743

$

+5.4%

0.96%

16

9

Cashmere Valley Bank (WA)

11

1,148,312

$

+4.9%

0.93%

17

Opus Bank (CA)

24

1,070,464

$

+10.6%

0.87%

18

East West Bancorp Inc. (CA)

4

1,008,752

$

+9.1%

0.82%

19

10

Olympic Bancorp Inc. (WA)

20

846,053

$

+4.8%

0.69%

20

Zions Bancorp. (UT)

1

727,672

$

+1.0%

0.59%

21

11

Skagit Bancorp Inc. (WA)

11

686,204

$

+2.9%

0.56%

22

12

Riverview Bancorp Inc. (WA)

14

618,304

$

+4.5%

0.50%

23

13

First FS&LA of Port Angeles (WA)

10

602,816

$

+0.7%

0.49%

24

14

Timberland Bancorp Inc. (WA)

22

598,670

$

+0.4%

0.49%

25

15

Pacific Financial Corp. (WA)

16

585,507

$

+4.9%

0.48%

Total For Institutions In Market

1,826

$ 122,930,458

+4.4%

Out of 88 Institutions

Washington - Top 25

Deposit

Growth

(1-Year)

Deposit Market Share

5

Source: SNL Financial, deposit market share data as of 6/30/2014

Note: All dollars in thousands

HFWA

ranked

5

th

for

deposit

market

share in Washington among banks

headquartered in the state |

Strong and

Diverse Economic Landscape 6

Headquartered in Western Washington

Major Operations in Western Washington

Thriving local economy with job growth in technology

and aerospace sectors

Seattle

economy

ranks

11

th

largest

in

the

country

by

GDP, which increased 4.1% since 2013

Seattle’s population grew 5.2% from 2010 to 2014

Washington

per

capita

income

in

2013

ranked

13

th

in

the United States at $47,031, 6.3% higher than the

national average

Nine Fortune 500 companies headquartered in

Washington, including Amazon, Costco, Microsoft and

Starbucks

Significant increase in new construction coupled with

improving economic conditions have led to an

improving real estate market

Number of Seattle building permits increased

by 20% year-to-date*

Number of Washington building permits

increased 7% overall year-to-date*

Seattle home prices increased 6% in

September 2014 versus September 2013

Note: Information for Seattle MSA, where available

Source:

U.S.

Department

of

Commerce,

Federal

Reserve

Bank

of

St.

Louis,

Office

of

Financial

Management,

U.S. Census Bureau, City of Seattle, Puget Sound Economic Forecaster, National Association of

Home Builders, S&P Case-Shiller

*Information as of 10/31/2014

Fort Lewis

McChord Air Force Base |

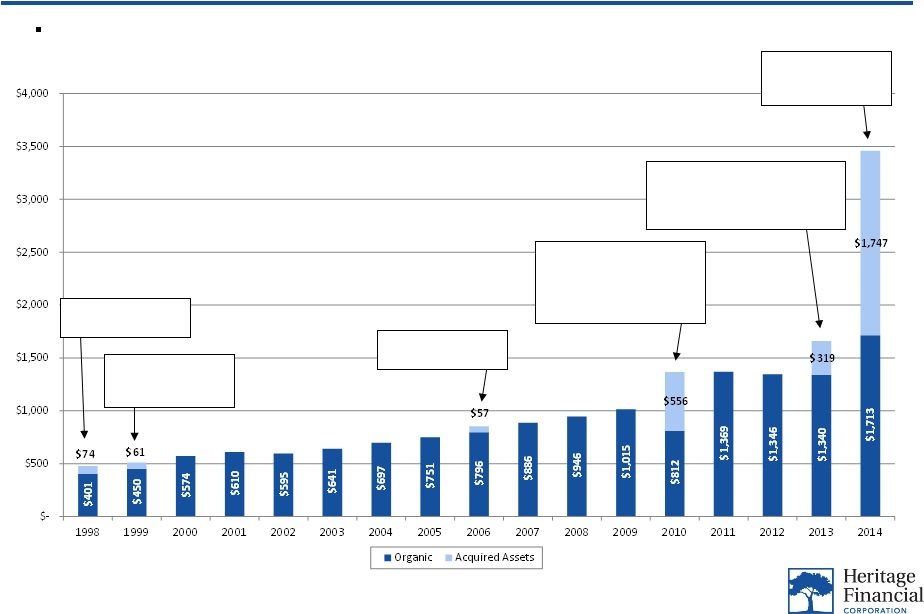

Historical

Growth – Organic and Acquisitive

7

Source: Company financials, as of 12/31/2014

Note: All dollars in millions

Acquired North Pacific

Bancorporation

Acquired Washington

Independent

Bancshares Inc.

Acquired Western

Washington Bancorp

Completed 2 FDIC deals -

Pierce Commercial Bank and

Cowlitz Bank acquiring $211M

and $345M in deposits,

respectively

Acquired Valley Community

Bancshares, Inc. with $254M in

assets and Northwest Commercial

Bank with $65M in assets

Merger with

Washington Banking

Company

In addition to organic growth, HFWA has completed 6 whole bank mergers and 2 FDIC-assisted

transactions since 1998 |

Financial

Update – Q4 2014

8

Source: Company financials, as of 12/31/2014

Net income of $7.3 million, or $0.24 diluted earnings per share

Return on average assets of 0.83% and return on average tangible

common equity of 8.85%

Net interest margin of 4.74%, which increased by 42 basis points

from prior quarter. Excluding the impact from accretion on

purchased loans, the net interest margin was 3.86% which increased by 3 basis points from

prior quarter Gross loans held for investment increased to $2.125 billion vs. $2.064

billion in prior quarter, or annualized growth of 11.8% Total deposits of $2.9 billion,

which includes noninterest bearing deposits of 24.4% and non-maturity deposits of 81.9% of the total

deposit balance, respectively

Total noninterest bearing demand deposits increased to $709.7 billion vs. $694.4 billion in

prior quarter, or annualized growth of 8.8% Total assets of $4.6 million per FTE

employee vs. $4.4 million from prior quarter Nonperforming noncovered assets decreased

by 38.5%, to $9.7 million at December 31, 2014 vs. $15.8 million in prior quarter

Tangible book value per share of $10.73 vs. $10.62 from prior quarter, an increase of $0.11

per share Dividends per share of $0.25, including a regular dividend of $0.09 and

special dividend of $0.16 |

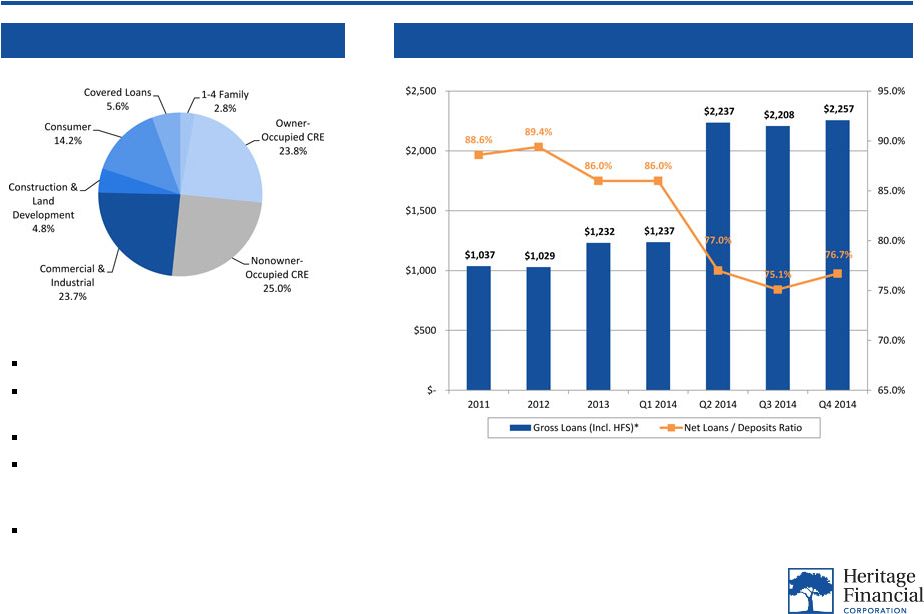

Loan

Portfolio 9

Loan Portfolio Trends

Loan Portfolio Mix -

% of Total*

Source: Company financials, as of 12/31/2014

Note: All dollars in millions

*Includes non-covered and covered loans

**Excludes impact from incremental accretion on purchased loans

Total CRE of 48.8% of total loans

Total C&I and owner-occupied CRE of 47.5% of total

loans

Core yield on loans of 5.03% in Q4 2014**

Total loans of $2.3 billion, including $126.2 million

of covered loans remaining in loan portfolio from

FDIC-assisted acquisitions

$244.9 million of loan originations in Q4 2014 |

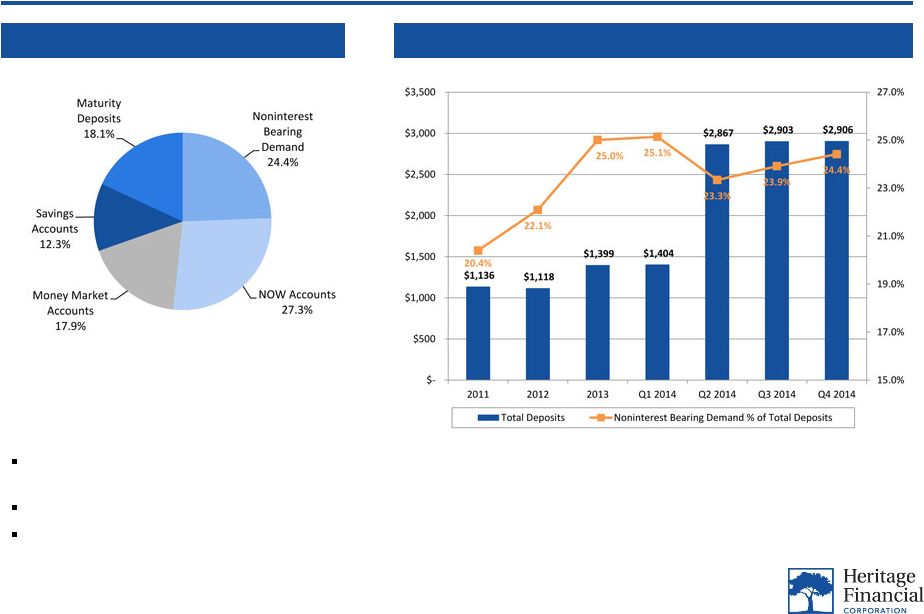

Deposit

Profile 10

Deposit Trends

Deposit Mix -

% of Total

Source: Company financials, as of 12/31/2014

Note: All dollars in millions

Noninterest bearing demand of 24.4% of total

deposits

Non-maturity deposits of 81.9% of total deposits

Cost of total deposits of 0.20% in Q4 2014 |

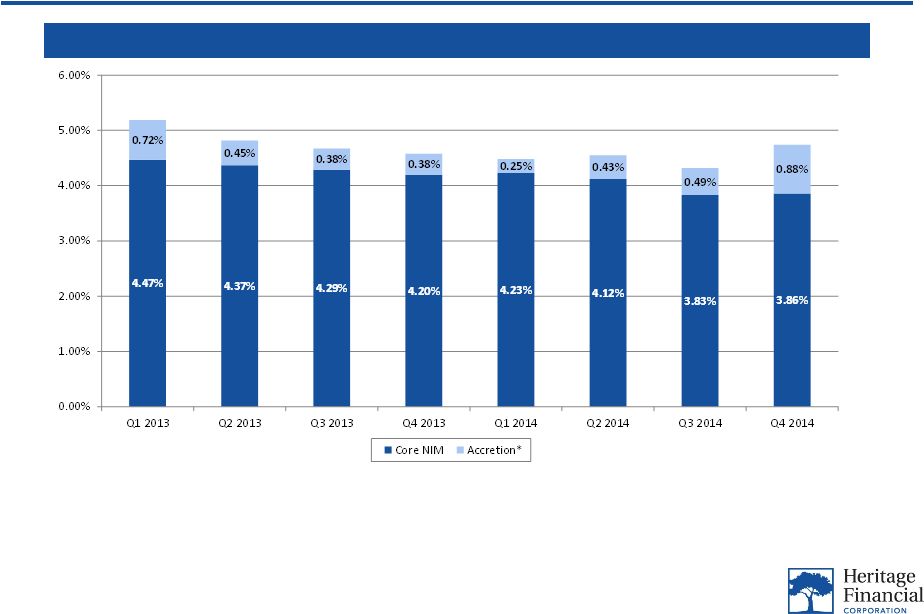

Net Interest

Margin Trends 11

Net Interest Margin (Core vs. Accretion)*

Source: Company financials, as of 12/31/2014

*Impact on net interest margin from incremental accretion on purchased loans

5.19%

4.82%

4.67%

4.58%

4.48%

4.55%

4.32%

4.74% |

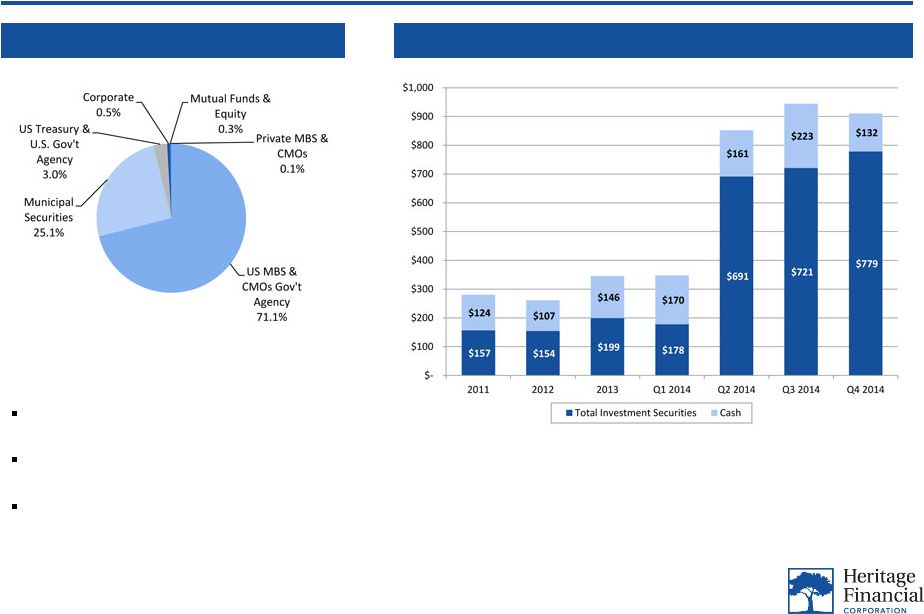

Cash and

Investment Securities Portfolio 12

Cash and Investment Securities

Investment Portfolio Mix

Source: Company financials, as of 12/31/2014

Note: All dollars in millions

Total cash and investment securities of $910 million, or

26.3% of total assets

Average yield on taxable investment securities of

1.94% in Q4 2014

Average yield on non-taxable investment securities of

1.98% in Q4 2014 |

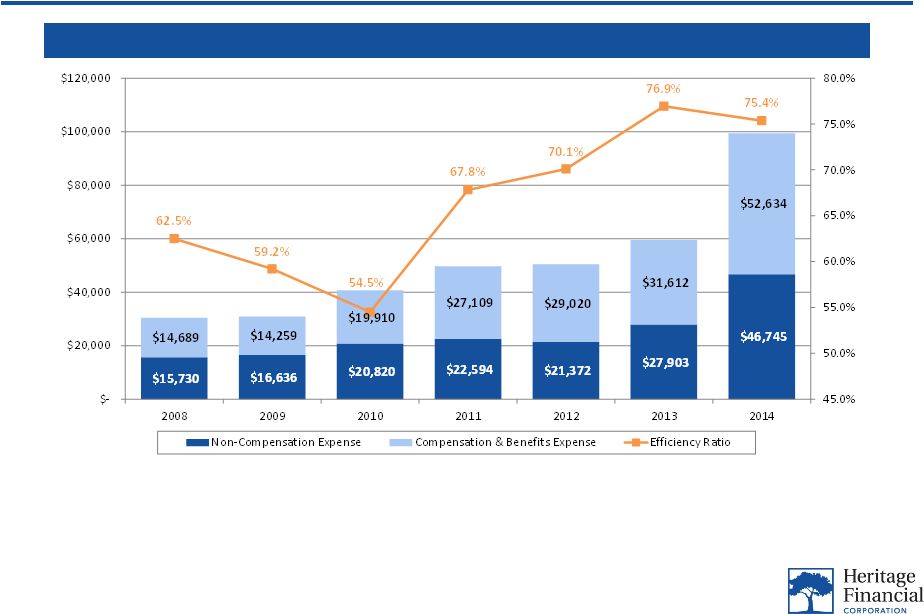

Non-Interest Expense

13

Source: Company financials, as of 12/31/2014

Note: All dollars in thousands

Non-Interest Expense Detail and Efficiency Ratio |

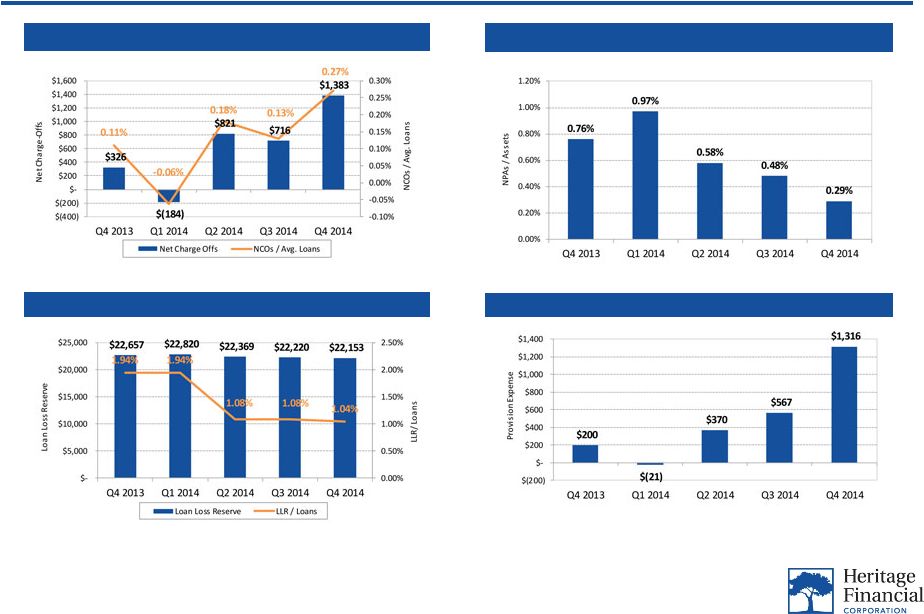

Credit Quality

Trends 14

Source: Company financials, as of 12/31/2014

Note: All dollars in thousands

Note: Excludes purchased covered loans

Loan Loss Reserve and LLR/Loans

Net Charge

Offs and NCOs/Avg. Loans

Provision Expense

NPAs / Assets |

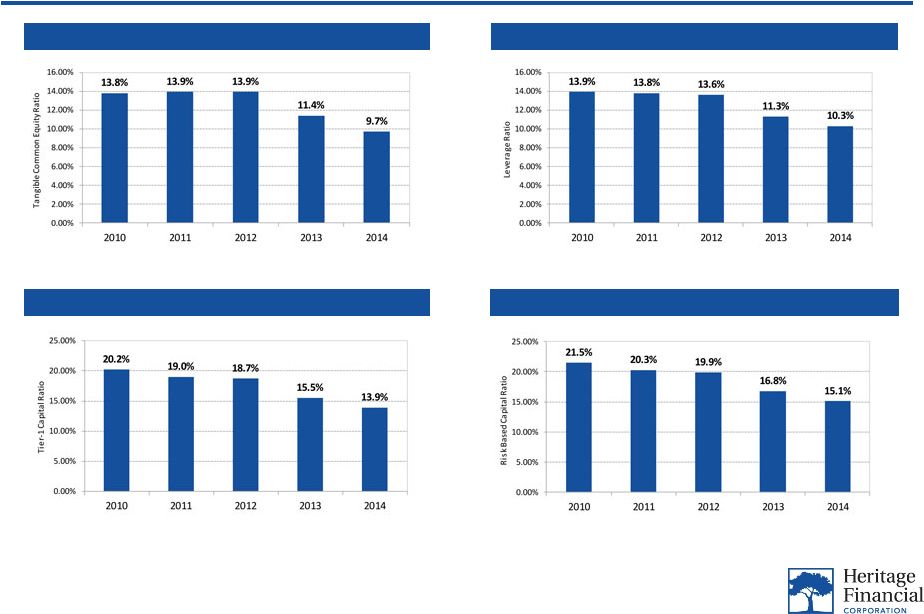

Capital Ratio

Trends 15

Source: Company financials, as of 12/31/2014

Tier -

1 Capital Ratio

Tangible Common Equity Ratio

Risk Based Capital Ratio

Leverage Ratio |

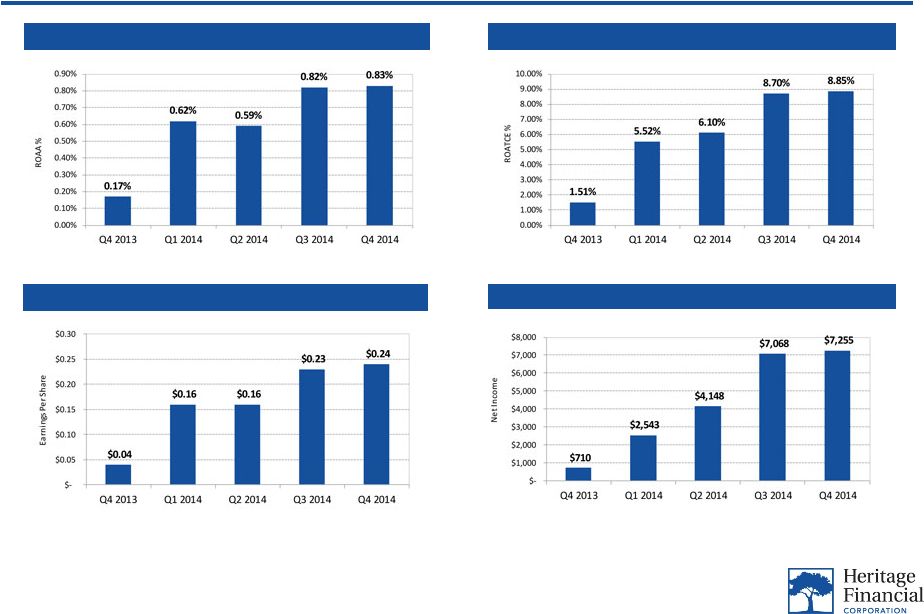

Profitability

Trends 16

Source: Company financials, as of 12/31/2014

Note: All dollars in thousands, except per share

Earnings Per Share

ROAA

ROATCE

Net Income |

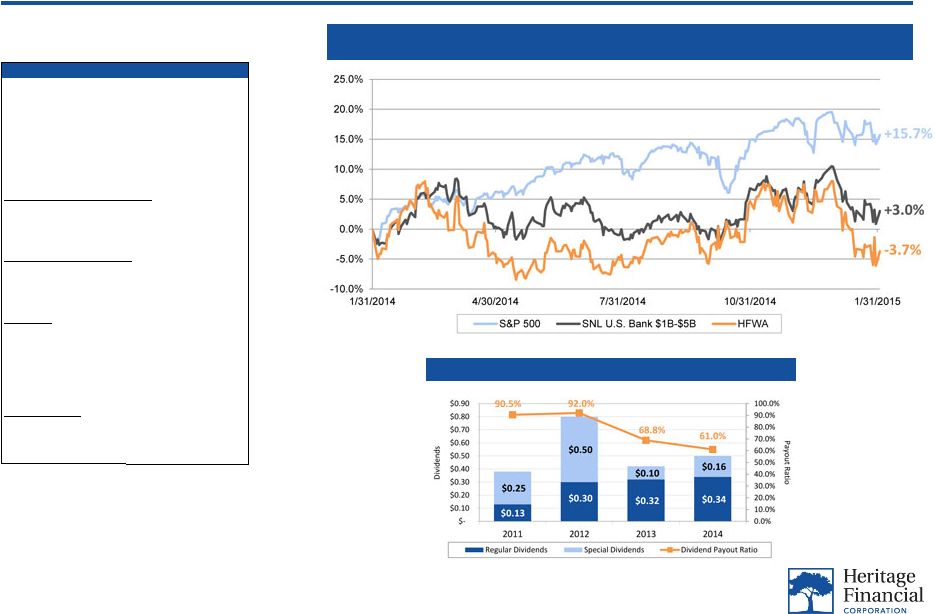

Total

Shareholder Return 17

Total Return* –

Last Twelve Months

Source: SNL Financial, as of 2/2/2015

Note: SNL U.S. Bank $1B-$5B index includes banks nationwide with total assets of

$1.0 billion to $5.0 billion

*Total return includes stock price appreciation and reinvested dividends

**Average Street EPS estimates, per FactSet Research Systems, Inc.

***Dividends based on date declared

Ticker

HFWA

Exchange

NASDAQ

Stock Price

15.92

$

Market Cap. ($MM)

481.7

$

Dividend Yield (Regular Div. Only)

2.51%

Average Daily Volume (3 Mo.)

Avg. Daily Volume (Shares)

71,611

Avg. Daily Volume ($000s)

1,140

$

52-Week High / Low Price

52-Week High (3/05/2014)

18.39

$

52-Week Low (5/16/2014)

15.19

$

Per Share

Tg. Book Value Per Share

10.73

$

EPS -

2015E**

1.24

$

EPS -

2016E**

1.31

$

Number of Research Analysts

4

Valuation Ratios

Price / Tg. Book Value

148.4%

Price / 2015E EPS**

12.8x

Price / 2016E EPS**

12.2x

Dividends Per Share*** |

HFWA

Investment Thesis 18

Western Washington geographic footprint with vibrant economy and

attractive long-term demographics

Continued focus on growth trends and capital management

Grow organically and continue to evaluate M&A opportunities

Return

capital

to

shareholders

via

dividends

and

stock

buybacks,

as

appropriate

Benefits of merger with Washington Banking Company expected to be

reflected in HFWA’s 2015 results

Attractive valuation |

19

Appendix

***

***

****

**** |

Historical

Financial Highlights 20

Source: Company financials, as of 12/31/2014

Note: All dollars in thousands

Note: All credit quality information excludes covered loans

Last 5 Quarters

Q4 2013

Q1 2014

Q2 2014

Q3 2014

Q4 2014

Balance Sheet

Total Assets

1,659,038

$

1,662,473

$

3,391,579

$

3,451,320

$

3,459,916

$

Asset Growth (Anlzd. vs. Prior Period)

-3.7%

0.8%

416.0%

7.0%

1.0%

Gross Loans (Incl. HFS)

1,231,920

$

1,237,037

$

2,236,572

$

2,207,524

$

2,256,659

$

Loan Growth (Anlzd. vs. Prior Period)

-1.6%

1.7%

323.2%

-5.2%

8.9%

Total Deposits

1,399,189

$

1,404,214

$

2,866,542

$

2,903,069

$

2,906,331

$

Deposit Growth (Anlzd. vs. Prior Period)

-7.5%

1.4%

416.6%

5.1%

0.4%

Net Loans / Deposits Ratio

86.0%

86.0%

77.0%

75.1%

76.7%

Cash and Securities / Total Assets

20.8%

20.9%

25.1%

27.4%

26.3%

Noninterest Bearing Deposits (% of Total)

25.0%

25.1%

23.3%

23.7%

24.4%

Non-CDs (% of Total)

77.9%

78.8%

78.3%

80.1%

81.9%

Capital Adequacy

Tangible Common Equity

184,782

$

185,593

$

319,476

$

321,179

$

324,588

$

Tangible Common Equity Ratio

11.3%

11.5%

9.8%

9.7%

9.7%

Leverage Ratio

11.3%

11.5%

12.6%

10.3%

10.3%

Risk Based Capital Ratio

16.8%

16.6%

15.7%

15.9%

15.1%

Credit Quality Ratios

NPAs / Total Assets

0.76%

0.97%

0.58%

0.48%

0.29%

NCOs / Avg. Loans

0.11%

-0.06%

0.18%

0.13%

0.27%

Loan Loss Reserves / Gross Loans

1.94%

1.94%

1.08%

1.08%

1.04%

Income Statement and Performance Ratios

Net Interest Income

17,646

$

16,741

$

28,596

$

33,307

$

36,780

$

Net Income

710

$

2,543

$

4,148

$

7,068

$

7,255

$

ROAA

0.17%

0.62%

0.59%

0.82%

0.83%

Net Interest Margin

4.58%

4.48%

4.55%

4.32%

4.74%

Noninterest Expense / Avg. Assets

4.38%

3.63%

3.85%

3.27%

3.36%

Assets Per Employee

4,448

$

4,644

$

4,192

$

4,352

$

4,626

$

Efficiency Ratio

92.2%

77.6%

80.9%

73.1%

71.9% |

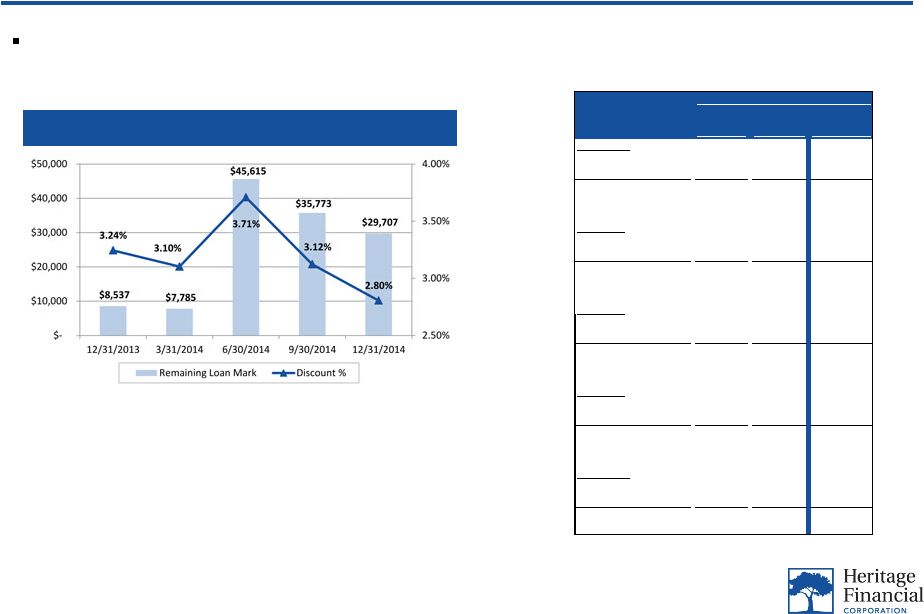

Discounts on

Acquired Loans 21

Total Discount on Acquired Loans

$29.7 million remaining loan discount on acquired loans, including covered and non-covered

portfolios Source: Company information, as of 12/31/2014

Note: All dollars in thousands

Covered

Non-

Covered

Total

12/31/2013

Loan Balance

64,788

$

198,384

$

263,172

$

Remaining Loan Mark

1,034

$

7,503

$

8,537

$

Recorded Investment

63,754

$

190,881

$

254,635

$

Discount %

1.60%

3.78%

3.24%

3/31/2014

Loan Balance

62,450

$

188,461

$

250,911

$

Remaining Loan Mark

976

$

6,809

$

7,785

$

Recorded Investment

61,474

$

181,652

$

243,126

$

Discount %

1.56%

3.61%

3.10%

6/30/2014

Loan Balance

174,187

$

1,055,584

$

1,229,771

$

Remaining Loan Mark

14,519

$

31,096

$

45,615

$

Recorded Investment

159,668

$

1,024,488

$

1,184,156

$

Discount %

8.34%

2.95%

3.71%

9/30/2014

Loan Balance

149,673

$

995,910

$

1,145,583

$

Remaining Loan Mark

10,840

$

24,933

$

35,773

$

Recorded Investment

138,833

$

970,977

$

1,109,810

$

Discount %

7.24%

2.50%

3.12%

12/31/2014

Loan Balance

131,882

$

927,231

$

1,059,113

$

Remaining Loan Mark

5,682

$

24,025

$

29,707

$

Recorded Investment

126,200

$

903,206

$

1,029,406

$

Discount %

4.31%

2.59%

2.80%

Total Acquired Loans |