Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Bristow Group Inc | d864207d8k.htm |

February 6, 2015

Third quarter FY15 earnings presentation

Bristow Group Inc.

Exhibit 99.1 |

2

Third quarter FY15 earnings call agenda

Introduction

CEO remarks and safety review

Operational highlights

Current and future financial performance

Closing remarks

Questions and answers

Linda McNeill, Director Investor Relations

Jonathan Baliff, President and CEO

Jeremy Akel, SVP and COO

John Briscoe, SVP and CFO

Jonathan Baliff, President and CEO |

3

Forward-looking statements

This

presentation

may

contain

“forward-looking

statements”

within

the

meaning

of

the

Private

Securities

Litigation

Reform

Act

of

1995.

Forward-looking

statements

include

statements

about

our

future

business,

operations,

capital

expenditures,

fleet

composition,

capabilities

and

results; modeling

information,

earnings

and

adjusted

earnings

growth

guidance,

expected

contract

revenue,

expected

operating

margins,

cash

flow

stability and

other

financial

projections;

future

dividends,

share

repurchases

and

other

uses

of

excess

cash;

plans,

strategies

and

objectives

of

our

management,

including

our

plans

and

strategies

to

grow

earnings

and

our

business,

our

general

strategy

going

forward,

our

business

model

and

our

operational

excellence

initiative;

expected

actions

by

us

and

by

third

parties,

including

our

customers,

competitors

and

regulators;

impact

of

grounding

and

the

effects

thereof;

the

valuation

of

our

company

and

its

valuation

relative

to

relevant

financial

indices;

assumptions

underlying

or

relating

to

any

of

the

foregoing,

including

assumptions

regarding

factors

impacting

our

business,

financial

results

and

industry

including

oil

prices;

expected

impact

of

our

investment

in

Eastern

Airways

and

our

acquisition

of

an

interest

in

Airnorth;

aircraft

delivery

dates

and

other

matters.

Our

forward-looking

statements

reflect

our

views

and

assumptions

on

the

date

of

this

presentation

regarding

future

events

and

operating

performance.

They

involve

known

and

unknown

risks,

uncertainties

and

other

factors,

many

of

which

may

be

beyond

our

control,

that

may

cause

actual

results

to

differ

materially

from

any

future

results,

performance

or

achievements

expressed

or

implied

by

the

forward-looking

statements.

These

risks,

uncertainties

and

other

factors

include

fluctuations

in

the

demand

for

our

services;

fluctuations

in

worldwide

prices

of

and

supply

and

demand

for

natural

gas

and

oil;

fluctuations

in

levels

of

natural

gas

and

oil

exploration,

development

and

production

activities;

the

impact

of

competition;

actions

by

customers;

the

risk

of

reductions

in

spending

on

aircraft

services

by

governmental

agencies;

changes

in

tax

and

other

laws

and

regulations;

changes

in

foreign

exchange

rates

and

controls;

risks

associated

with

international

operations;

operating

risks

inherent

in

our

business,

including

the

possibility

of

declining

safety

performance;

general

economic

conditions

including

the

capital

and

credit

markets;

our

ability

to

obtain

financing;

the

possibility

that

we

may

lack

sufficient

liquidity

to

continue

to

repurchase

shares

or

pay

a

quarterly

dividend;

the

risk

of

grounding

of

segments

of

our

fleet

for

extended

periods

of

time

or

indefinitely;

our

ability

to

re-deploy

our

aircraft

to

regions

with

greater

demand;

our

ability

to

acquire

additional

aircraft

and

dispose

of

older

aircraft

through

sales

into

the

aftermarket;

the

possibility

that

we

or

our

suppliers

will

be

unable

to

deliver

new

aircraft

on

time

or

on

budget;

the

possibility

that

we

do

not

achieve

the

anticipated

benefit

of

our

fleet

investment

program;

availability

of

employees;

political

instability,

war

or

acts

of

terrorism

in

any

of

the

countries

where

we

operate;

and

those

discussed

under

the

captions

“Risk

Factors”

and

“Management’s

Discussion

and

Analysis

of

Financial

Condition

and

Results

of

Operations”

in

our

Annual

Report

on

Form

10-K

for

the

fiscal

year

ended

March

31,

2014

and

our

Quarterly

Report

on

Form

10-Q

for

the

quarter

ended

December

31,

2014.

We

do

not

undertake

any

obligation,

other

than

as

required

by

law,

to

update

or

revise

any

forward-looking

statements,

whether

as

a

result

of

new

information,

future

events

or

otherwise. |

CEO

remarks and safety review Jonathan Baliff, President and CEO

|

5

Operational safety review

1)

AAR includes consolidated commercial operations only

2)

TRIR includes consolidated commercial operations, corporate and Bristow Academy

employees Total

Recordable

Injury

Rate

2

(TRIR)

per

200,000 man hours (cumulative)

Commercial Air Accident Rate

1

(AAR) per 100,000

flight hours (fiscal year) |

6

HeliOffshore: Safety through collaboration

•

Interest is very strong.

Since its launch in October 2014,

enrollment has grown to more than 20 members, with an

additional 50 in process

•

Global engagement is underway.

Membership interest from

all regions of the world

•

HeliOffshore is producing real results.

Airbus Helicopters

recently issued the industry’s first standardized EC225 Flight

Crew Operating Manual

•

Sharing is the norm.

Member operators are now routinely

exchanging safety events, best practices and lessons learned

under the HeliOffshore umbrella |

7

Q3 FY15 highlights

Adjusted EPS and adjusted EBITDAR amounts exclude gains and losses on dispositions

of assets and any special items during the period. See reconciliation of these items to GAAP measures in the

appendix hereto and in our earnings release for the quarter ended December 31,

2014 Bristow Value Added (BVA) is calculated by taking gross cash flow less

the product of gross operating assets times a capital charge of 10.5%. Example calculation can be found in the appendix hereto.

Please see our earnings release and slide 24 for more information regarding earnings

guidance range *

**

***

•

Continued operating revenue growth, up 15.2% over Q3 FY14

•

Adjusted EBITDAR increased year-over-year, but adjusted EPS is down due

primarily to unfavorable changes in foreign exchange rates

•

Q3 FY15 BVA** is up $7.6 million year-over-year and down $6.4 million

sequentially, with gross cash flow returns growing due to growth and excellent

capital management •

Strong operating cash flow, up 18.3% over YTD Q3 FY14

•

EPS

guidance

for

the

full

year

FY15

is

being

lowered

to

$4.05

-

$4.45

from

$4.70

-

$5.20***

•

Q3 operating revenue of $430.3M (15.2% increase from Q3 FY14, 2.3% decrease

from Q2 FY15) •

Q3 GAAP EPS loss of $0.03 (105.9% decrease from Q3 FY14, 104.1% decrease from Q2

FY15) •

Q3 adjusted EPS* of $0.70 (17.6% decrease from Q3 FY14, 19.5% decrease from Q2

FY15) •

Q3 adjusted EBITDAR* of $109.1M (8.3% increase from Q3 FY14, 2.7% decrease from Q2

FY15) |

8

Bristow market perspectives

Overall oil

price

perspective

•

Clients are only at the start of a three phase response in this downturn:

retrenching, recalibration, and (eventually) renewal

•

The strength of the U.S. dollar has impacted Bristow’s current financial

results more than the oil price decline

•

Bristow believes this is not just a supply-oriented decline, but is driven by

weaker global economic growth, especially in China and Europe

•

Because it's supply and demand driven, we believe the current price decline

will last (with a significant volatility) between 12 and 24 months

•

Continued focus on safety with best practice collaboration through

HeliOffshore continuing and expanding

•

Although production-oriented services (like aviation) are doing better than

many in energy services, short-term available capacity is

increasing •

Bristow and clients are proactively working together to find efficiencies and

ways to reduce costs, without compromising physical or financial

safety

•

Bristow is also working with our OEM and lessor partners during this

downturn to find cost and capital efficiencies

Offshore

aviation

market

perspective |

9

Operational highlights

Jeremy Akel, SVP and COO |

10

•

Europe contributed 46% of Bristow operating revenue

and 47% of adjusted EBITDAR* in Q3 FY15

•

Operating revenue increased 22.3% to $193.8M in

Q3 FY15 from $158.5M in Q3 FY14 with the net

addition of eleven LACE, the addition of Eastern

Airways and an overall increase in activity over the

comparable quarter

•

Adjusted EBITDAR increased 15% to $64.2M in Q3

FY15 from $56.0M in Q3 FY14 with adjusted

EBITDAR margin of 33.1% in Q3 FY15 vs. 35.3% in

Q3 FY14

Outlook:

Higher demand for newer technology aircraft in the

Southern North Sea from CAP 1145 implementation

has resulted in one LACE contracted for up to five

years

Minor reduction in Norway activity

Clients are increasingly focused on efficiency over

flexibility with no projects canceled to date

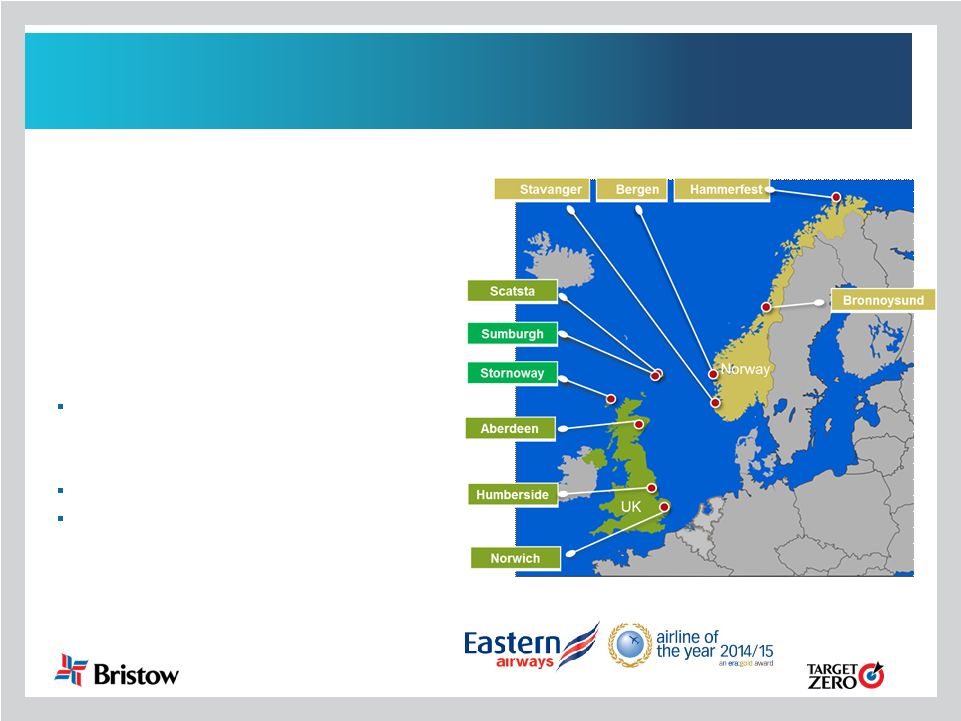

Europe (EBU)

* Operating revenue and adjusted EBITDAR percentages exclude corporate and

other FY15 adjusted EBITDAR margin expected to

remain ~ low thirties |

11

UK SAR update

•

From the start of the GAP SAR contract on June 1, 2013 through December 31, 2014,

we have conducted 519 missions and rescued and/or assisted 520 people

•

Sumburgh and Stornoway bases generated $11.9M of operating revenue in Q3 FY15 and

$76.1M since the beginning of the contract

•

Completed construction of the first two UK SAR bases in Inverness and Humberside;

non-revenue pre-operational activities have commenced

Outlook:

Humberside and Inverness on track for contract start April 2015

Five additional bases are on track for Q2-Q4 FY16 start up

Seven bases

expected to be

operational by

end FY16 |

12

West Africa (WASBU)

•

West Africa (Nigeria) contributed 19% of Bristow

operating revenue and 20% of adjusted EBITDAR* in

Q3 FY15

•

Operating revenue increased to $80.5M in Q3 FY15

from $79.4M in Q3 FY14 due to increased activity

levels and improved contract terms

•

Adjusted EBITDAR increased to $27.9M in Q3 FY15

from $26.6M in Q3 FY14 and adjusted EBITDAR

margin increased to 34.6% in Q3 FY15 vs. 33.5% in

Q3 FY14 due to increased revenue and

implementation of new cost control measures

Outlook:

Uncertainty around national elections is hindering

sector investment

Despite clients seeking efficiencies, no projects

have been canceled to date

Expansion into point-to-point transportation

services is on track to start in Q4 FY15

FY15 adjusted EBITDAR margin expected to

remain ~ low thirties

* Operating revenue and adjusted EBITDAR percentages exclude corporate and

other |

13

•

North America contributed 15% of Bristow operating

revenue and 18% of adjusted EBITDAR* in Q3 FY15

•

Operating revenue increased to $62.4M in Q3 FY15

from $54.9M in Q3 FY14 primarily due to an

increase in the number of medium and large aircraft

on contract

•

Adjusted EBITDAR increased to $24.9M in

Q3 FY15 vs. $18.2M in Q3 FY14 while adjusted

EBITDAR margin increased to 40.0% from 33.1% in

Q3 FY14, driven by a change in the contracted fleet

mix and improved utilization

Outlook:

Additional aircraft mobilized to GoM to meet

client demand

GoM market and fleet utilization remain robust

Despite current global market environment we

are not delaying facility improvements

North America (NABU)

* Operating revenue and adjusted EBITDAR percentages exclude corporate and

other FY15 adjusted EBITDAR margin increased

from low-to-mid thirties to ~ mid-to-high

thirties |

14

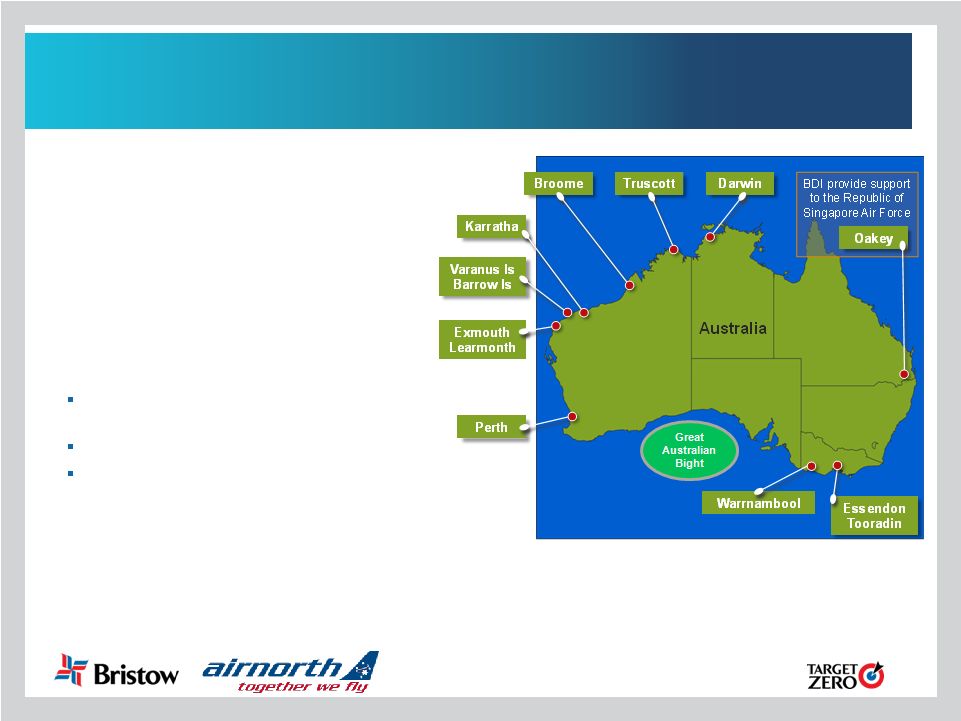

Australia (AUSBU)

•

Australia contributed 12% of Bristow operating

revenue and 10% of adjusted EBITDAR* in

Q3 FY15

•

Operating revenue increased by 51.5% to $52.4M

in Q3 FY15 from $34.6M in Q3 FY14

•

Adjusted EBITDAR increased 157.1% to $13.3M

in Q3 FY15 from $5.2M in Q3 FY14 and adjusted

EBITDAR margin increased to 25.4% in Q3 FY15

from 15.0% in Q3 FY14 due to the ramp up of the

INPEX contract

Outlook:

Several client exploration projects being

delayed

Larger client projects are still moving forward

Continue to retire old aircraft creating

operational efficiencies

* Operating revenue and adjusted EBITDAR percentages exclude corporate and

other FY15 adjusted EBITDAR margin expected to

remain ~ low twenties |

15

Bristow has acquired Airnorth, Northern Australia’s

largest regional airline

•

Bristow acquired an 85% interest in the privately

owned Airnorth

•

Airnorth is an Australian regional fixed-wing

operator with a balanced portfolio of charter and

scheduled flights servicing oil and gas and mining

clients from its Darwin hub

•

Airnorth is a codeshare partner with Qantas

•

Bristow’s investment is A$30M ($24M USD) with a

possible A$17M ($13.5M USD)

earn out over

~ three years and includes:

13 fixed-wing aircraft to meet demand for fixed

wing/rotor wing tenders from oil and gas clients

Current CEO will retain the remaining 15%,

subject to a Bristow call option

Financial results from Airnorth will be

consolidated within Bristow’s AUSBU |

16

Airnorth provides scale, stability and positive

financial impact for Bristow

This

investment

solidifies

Bristow’s

ability

to

offer

point-to-point

transportation

services

in

four

of

its

five

business

units

leveraging

an

integrated

rotary

and

fixed

wing

services

model

•

Bristow Helicopters and Airnorth are

culturally aligned

with shared core values of

safety, quality and service

•

Together, Bristow Helicopters and Airnorth

are

positioned

to

facilitate

and

expand

passengers’

transport experience from home to

offshore bases, a market niche underserved by

major airlines

•

Exclusive Darwin hub provides access to

key markets

in which Bristow can introduce

integrated fixed and rotary wing logistics to

existing and potential clients

•

Financially attractive investment

with

expected immediately accretive EBITDAR,

BVA and EPS

See

10-Q

Note

11

“Subsequent

Event”

for

more

information

Combined BRS and Airnorth locations

BRS locations

Airnorth locations

Airnorth regular passenger transport route

Airnorth charter route

Planned LNG plant

Operational LNG plant

Domestic gas plant |

17

•

Other International contributed 8% of Bristow operating

revenue and 5% of adjusted EBITDAR* in Q3 FY15

•

Operating revenue increased to $32.6M in Q3 FY15 vs.

$30.8M in Q3 FY14 due to addition of a contract in

Tanzania and increased activity in Trinidad

•

Adjusted EBITDAR decreased to $6.8M in Q3 FY15 vs.

$10.2M in Q3 FY14 and adjusted EBITDAR margin

decreased to 20.7% in Q3 FY15 from 33.2% in Q3 FY14

primarily as the result of foreign currency exchange rate

changes

* Operating revenue and adjusted EBITDAR percentages exclude corporate and

other Consolidated in OIBU

Unconsolidated Affiliate

Other International (OIBU)

Outlook:

Despite headwinds from current price environment, several opportunities

continue in Africa, Russia and southeast Asia

BU restructuring to simplify business and reduce operating costs

Currently evaluating opportunities in point-to-point transportation

services FY15 adjusted EBITDAR margin expected to ~ mid thirties

|

18

Líder update

* Reconciliation of adjusted EBITDAR, leverage and BVA provided in the

appendix Líder adjusted EBITDAR*

•

CY14 adjusted EBITDAR was flat year-over-year

despite unfavorable changes in foreign currency

rates

•

Absolute BVA contribution to Bristow from Líder

was $5.1M* in Q3 FY15 (December 31, 2014)

•

Adjusted debt to TTM adjusted EBITDAR

increased to 2.9x as of December 31, 2014 from

2.8x as of December 31, 2013

Outlook:

Petrobras medium aircraft tender

closed on January 22

Petrobras large aircraft tender

closed on January 29

Despite its current situation, lower

lifting costs position Petrobras to

grow over the long term benefiting

the industry |

Current and future financial

performance

John Briscoe, SVP and CFO |

20

$0.85

$0.70

$0.43

$0.30

$0.28

Q3 FY14

Operations

Corporate and Other

FX Changes

Q3 FY15

Financial highlights:

Adjusted EPS and adjusted EBITDAR summary year-over-year

Q3 FY14 to Q3 FY15 adjusted EPS bridge

$100.7

$109.1

$36.5

$15.7

$12.4

Q3 FY14

Operations

Corporate and Other

FX Changes

Q3 FY15

Q3 FY14 to Q3 FY15 adjusted EBITDAR bridge (in millions)

Note: Adjusted EPS and adjusted EBITDAR amounts exclude gains and losses on

dispositions of assets and any special items during the period. See reconciliation of these items

to GAAP in our earnings release for the quarter ended December 31, 2014.

|

21

LACE and LACE rate continue to increase led by new

technology aircraft and improved utilization/terms

FY15 average LACE guidance range changed to 165-170 and average LACE rate

guidance

range

changed

to

$9.00

-

$9.50

million

* See appendix hereto for more information on LACE and LACE

rate. Consolidated commercial aircraft, LACE and LACE rate exclude Bristow Academy, affiliate aircraft, fixed

wing aircraft, aircraft held for sale, aircraft construction in progress and

reimbursable revenue. |

22

Bristow Value Added (BVA) drives improving Gross Cash

Flow (GCF) performance

•

Q3 FY15 absolute BVA is positive $19.7M, a $7.6M or 63% increase from Q3

FY14 •

Year-over-year change in BVA is driven by:

Solid revenue growth

Margin improvement

Capital efficiency efforts

•

EBU and NABU generated key improvements year-over-year

Note: BVA is computed by subtracting a capital charge (10.5%) for the use of gross

invested capital from after tax operating cash flow. GCF Return % is based

on trailing twelve months after tax operating cash flows (Gross Cash Flow) over average quarterly gross invested capital (Gross Operating Assets).

Refer to the appendix for additional details. |

23

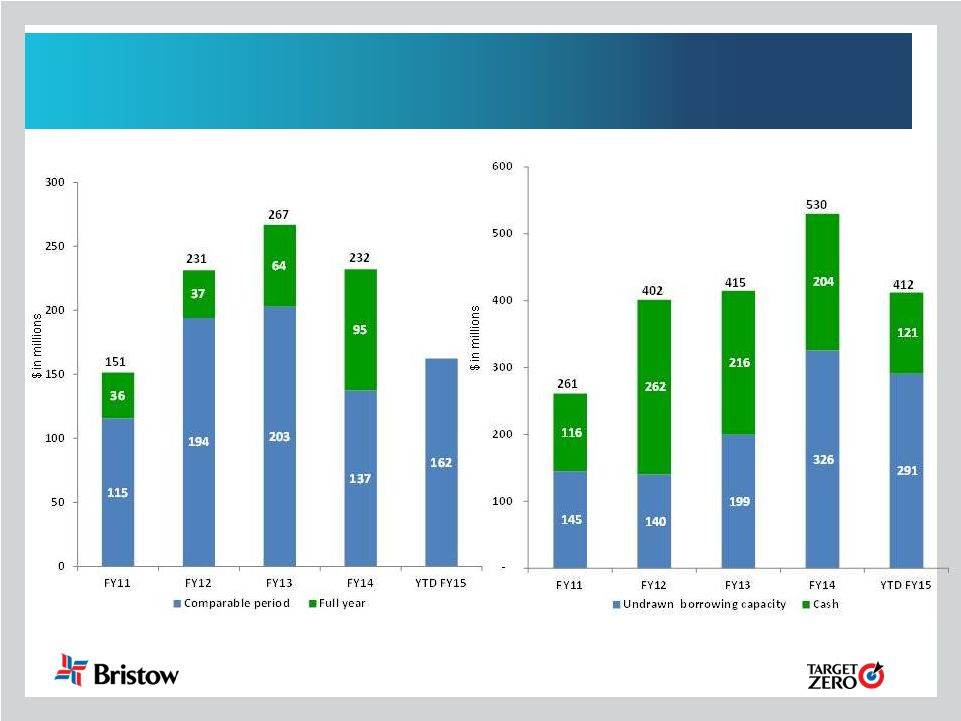

Our progress on BVA yields stronger operating cash flow

for growth, dividends and share repurchases

Net

cash

provided

by

operating

activities

1

Total liquidity

2

1)

See 10-Q for more information on cash flow provided by operating

activities. 2)

At period end |

24

FY15 guidance updated . . .

•

FY15

adjusted

EPS

guidance

range

is

reduced

to

$4.05

-

$4.45,

excluding special items and aircraft sales. FY15 guidance

includes:

*Assuming

FY15

revenue

earned

in

same

regions

and

same

mix

as

in

FY14.

Highlighted figures have changed since the last earnings release.

Average LACE (Large AirCraft

Equivalent)

~165-170

Interest expense

~ $28 - $32M

Average LACE Rate

~ $9.00 - $9.50M

Rent expense (aircraft only)

~$140 - $145M

G & A expense (all inclusive)

~ $245 - $250M

Tax rate*

~ 20 - 23%

Depreciation expense

~ $100 - $105M

Adj. EPS guidance

$4.05 - $4.45

FY15 guidance as of December 31, 2014 |

25

. . . as we continue to invest for Bristow’s future

•

Our Q3 FY15 financial performance is similar to our last quarter:

excellent BVA and operating cash flow, with adjusted EPS lower than

expectations

•

Declines in recent oil prices with a strengthening dollar are negatively

impacting our business in the short term

•

The FY16 perspective and beyond remains positive given new

production-oriented contracts and UK SAR

•

We continue to work with clients to identify cost effective logistics

solutions, with our recent Airnorth acquisition as a prime example

•

We expect improving BVA, cash flow, and EPS performance, with a

commitment to cost control, future prudent investment, and a

balanced shareholder return, including doubling of our annual

dividend every three to five years |

Appendix |

27

Organizational chart -

as of December 31, 2014

Business Unit

(% of FY15 operating revenue)

Corporate

Region

( # of aircraft / # of locations)

Joint Venture

(# of aircraft)

Key

Operated Aircraft

Bristow owned and/or operated 369

aircraft as of December 31, 2014

Affiliated Aircraft

Bristow affiliates and joint

ventures operated 131 aircraft

as of December 31, 2014

* Includes corporate and other |

28

Aircraft fleet –

medium and large

as of December 31, 2014

Next Generation Aircraft

Medium capacity 12-15 passengers

Large capacity 16-25 passengers

Mature Aircraft

Fair

market

value

of

our

owned

fleet

is

~$1.9

billion

and

leased

fleet

is

~$1.6

billion

Aircraft

Type

No. of PAX

Engine

Consl

Unconsl

Total

Ordered

Large Helicopters

AS332 L Super Puma

18

Twin Turbine

17

-

17

-

AW189

16

Twin Turbine

2

-

2

15

EC175

16

Twin Turbine

-

-

-

5

EC225

19

Twin Turbine

26

-

26

1

Mil Mi 8

20

Twin Turbine

7

-

7

-

Sikorsky S-61

25

Twin Turbine

2

-

2

-

Sikorsky S-92

19

Twin Turbine

69

9

78

6

123

9

132

27

LACE

111

Medium Helicopters

AW139

12

Twin Turbine

22

2

24

3

Bell 212

12

Twin Turbine

-

14

14

-

Bell 412

13

Twin Turbine

22

19

41

-

EC155

13

Twin Turbine

1

-

1

-

Sikorsky S-76A/A++

12

Twin Turbine

-

5

5

-

Sikorsky S-76C/C++

12

Twin Turbine

51

34

85

-

Sikorsky S-76D

12

Twin Turbine

3

-

3

7

99

74

173

10

LACE

47

|

29

Aircraft fleet –

small, training and fixed

as of December 31, 2014 (continued)

Mature Aircraft

Small capacity 4-7 passengers

Training capacity 2-6 passengers

* LACE does not include held for sale, training helicopters and fixed wing

Next Generation Aircraft

Aircraft

Type

No. of PAX

Engine

Consl

Unconsl

Total

Ordered

Small Helicopters

AW109

6

Twin Turbine

-

1

1

AS 350BB

4

Turbine

-

2

2

Bell 206B

4

Turbine

1

2

3

-

Bell 206 L Series

6

Turbine

5

6

11

-

Bell 407

6

Turbine

32

-

32

-

BK-117

7

Twin Turbine

2

-

2

-

EC135

6

Twin Turbine

-

3

3

-

40

14

54

-

LACE

10

Training Helicopters

AW109

6

Twin Turbine

2

-

2

-

AS 355

5

Twin turbine

2

-

2

-

Bell 206B

4

Turbine

12

-

12

-

Robinson R22

2

Piston

8

-

8

-

Robinson R44

4

Piston

7

-

7

-

Sikorsky 300CB/CBi

2

Piston

42

-

42

-

Fixed Wing

1

-

1

-

74

-

74

-

Fixed Wing

33

34

67

-

Total

369

131

500

37

TOTAL LACE (Large Aircraft Equivalent)*

168 |

30

Small

Medium

Large

Total

Leased LACE

Total LACE

% Leased

EBU

-

3

37

40

39

70

55%

WASBU

-

1

1

2

2

20

8%

NABU

1

13

5

19

12

34

35%

AUSBU

2

2

7

11

9

24

36%

OIBU

-

-

-

-

-

22

-

Total

3

19

50

72

60

168

36%

Operating lease strategy: lowering the cost and amount of

capital needed to grow

•

Of the 115 aircraft currently leased in our fleet, 72 are commercial (60 LACE), 30

are training and 13 fixed wing

•

60 LACE aircraft represent approximately 36% of our commercial fleet

•

Our

goal

is

for

commercial

fleet

operating

leases

to

account

for

approximately

30-35% of our LACE

Leased aircraft as of December 31, 2014

* The percentage of LACE leased is calculated by taking the total LACE for leased

aircraft divided by the total LACE for all aircraft we operate, including both owned and leased aircraft.

See

10-Q

Note

5

“Commitments

and

Contingencies”

for

more

information

provided

on

operating

leases.

* |

31

Consolidated fleet changes and aircraft sales for Q3 FY15

See

10-Q

Note

5

“Commitments

and

Contingencies”

for

more

information

provided

on

operating

leases.

# of aircraft

sold

Cash

received*

Q1 FY15

4

4.7

$

Q2 FY15

7

8.2

$

Q3 FY15

4

2.5

$

Total

15

15.4

$

* Amounts stated in millions

Small

Medium

Large

Training

Fixed wing

Total

EBU

-

3

37

-

13

53

WASBU

-

1

1

-

-

2

NABU

1

13

5

-

-

19

AUSBU

2

2

7

-

-

11

OIBU

-

-

-

-

-

-

Academy

-

-

-

30

-

30

Total

3

19

50

30

13

115

Leased aircraft in consolidated fleet

Q1 FY15

Q2 FY15

Q3 FY15

Fleet Count Beginning

363

363

363

Delivered

Large

6

2

4

Medium

3

-

2

Total Delivered

9

2

6

Removed

Sales

(4)

(7)

(4)

Other*

(5)

5

4

Total Removed

(9)

(2)

-

363

363

369

* Includes writeoffs, lease returns and commencements

Fleet changes

Small

Medium

Large

Training

Total

EBU

-

-

8

-

8

WASBU

-

2

2

-

4

NABU

-

-

-

-

-

AUSBU

-

-

2

-

2

OIBU

-

3

-

-

3

Academy

-

-

-

1

1

Total

-

5

12

1

18

Held for sale aircraft in consolidated fleet |

32

Operating revenue, LACE and LACE rate by BU

4

1)

$ in millions

2)

LACE rate is annualized

3)

$ in millions per LACE

4)

Excludes Bristow Academy and Eastern Airways

YTD op revenue

1

LACE

LACE Rate

2,3

EBU

$487

70

$9.33

WASBU

241

20

16.04

NABU

176

34

7.00

AUSBU

146

24

8.29

OIBU

104

22

6.44

Total

$1,176

168

$9.33

Operating Revenue, LACE, and LACE Rate by BU

as of December 31, 2014 |

33

Historical LACE by BU

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

EBU

45

45

45

42

42

43

48

46

44

46

46

45

WASBU

23

23

24

25

24

24

21

22

23

22

22

22

NABU

39

36

36

36

39

35

34

29

30

29

30

30

AUSBU

20

20

22

22

20

23

24

20

19

20

20

19

OIBU

36

34

34

35

33

33

33

38

39

38

38

34

Consolidated

163

158

161

160

157

158

159

154

154

154

155

149

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

EBU

47

45

51

55

57

59

59

56

61

67

70

WASBU

22

22

20

21

21

21

22

23

23

23

20

NABU

30

31

39

37

37

33

34

34

33

32

34

AUSBU

18

17

17

19

19

19

20

22

23

22

24

OIBU

32

28

27

27

27

28

28

24

25

23

22

Consolidated

147

142

154

158

161

160

162

158

163

166

168

LACE

FY11

FY12

FY10

FY13

FY14

FY15 |

34

Historical LACE rate by BU

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

EBU

$8.36

$8.28

$8.40

$8.76

$8.20

$8.50

$7.90

$8.40

$9.80

$9.60

$9.63

$10.09

WASBU

9.08

8.81

8.66

8.34

9.70

9.40

10.70

9.90

9.10

10.30

11.17

11.46

NABU

5.05

5.44

5.26

5.23

5.40

6.10

6.00

6.60

5.80

6.30

5.89

5.79

AUSBU

5.38

5.56

5.59

5.67

6.80

6.00

6.00

7.50

8.60

7.10

6.96

7.78

OIBU

3.66

4.09

4.06

3.78

3.90

4.10

4.40

3.90

3.50

3.70

3.78

4.22

Consolidated

$6.31

$6.52

$6.49

$6.45

$6.70

$6.90

$6.90

$7.10

$7.30

$7.40

$7.43

$7.89

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

EBU

$10.60

$11.03

$9.74

$9.13

$9.63

$9.95

$10.30

$10.84

$10.60

$9.78

$9.33

WASBU

12.35

12.24

13.71

13.28

14.26

14.62

14.17

13.99

14.21

14.23

16.04

NABU

7.05

7.11

5.84

6.12

6.34

7.13

6.75

6.84

7.02

7.04

7.00

AUSBU

8.48

9.29

9.55

8.58

8.04

7.74

7.21

6.76

8.27

8.72

8.29

OIBU

4.22

4.62

4.76

4.94

4.97

4.73

4.58

5.57

5.80

6.20

6.44

Consolidated

$8.55

$8.95

$8.49

$8.35

$8.78

$9.07

$8.97

$9.34

$9.55

$9.43

$9.33

LACE Rate

1,2

FY10

FY11

FY12

FY13

FY14

FY15

1)

$ in millions

2)

LACE rate is annualized |

35

Order and options book as of December 31, 2014

1)

Five

large

aircraft

on

order

and

seven

large

aircraft

on

option

are

subject

to

the

successful

development

and

certification

of

the

aircraft

2)

SAR configured

#

Helicopter

Class

Delivery Date

2

Large

June-16

3

Medium

June-16

3

Large

September-16

2

Medium

September-16

4

Large

December-16

1

Medium

December-16

2

Large

March-17

1

Medium

March-17

2

Large

June-17

1

Medium

June-17

3

Large

September-17

1

Medium

September-17

4

Large

December-17

3

Medium

December-17

1

Large

March-18

2

Medium

March-18

1

Large

June-18

1

Large

September-18

1

Large

December-18

1

Large

March-19

39

OPTIONS BOOK

#

Helicopter

Class

Delivery Date

Location

Contracted

3

Medium

March-15

IBU

3 of 3

3

Medium

June-15

WASBU

2

Large

September-15

EBU

2

1

Large

September-15

NABU

1 of 1

4

Medium

September-15

WASBU

2

Large

December-15

AUSBU

2

1 of 2

2

Large

December-15

EBU

2

Large

December-15

EBU

2

1

Large

March-16

EBU

1

Large

June-16

EBU

1

Large

June-16

NABU

1

Large

September-16

NABU

2

Large

December-16

NABU

1

Large

March-17

NABU

26

5 of 26

ORDER BOOK

1 |

36

Order and options book as of December 31, 2014 (continued)

#

Helicopter

Class

Delivery Date

Location

Contracted

5

Large

March-15

EBU

5 of 5

2

Large

June-15

EBU

2 of 2

2

Large

June-15

EBU

2 of 2

2

Large

September-15

EBU

2 of 2

2

Large

December-15

EBU

2 of 2

13

13 of 13

The aircraft that are indicated in grey italic will be leased upon delivery.

UK SAR CONFIGURED ORDER BOOK |

37

Total net asset FMV with and without leased aircraft FMV

NOTE: The gray shaded area represents the range of FMV with and without the impact

of leased aircraft (upper range includes leased aircraft and related NPV of lease payments; lower

range excludes FMV of leased aircraft as well as the NPV of lease

payments). The

reconciliation

for

net

asset

FMV

per

share

(

)

and

net

asset

FMV

per

share

implied

by

our

UK

SAR

aircraft

(

)

is

provided

on

the

following

pages.

shaded area |

38

Net asset FMV reconciliation as of December 31, 2014

(in millions)

Including leases

Excluding leases

(+) FMV of aircraft

$1,944

$1,944

(+) FMV of leased aircraft

1,564

-

(+) NBV of PPE without aircraft

576

576

(+) Working capital

259

259

(-) LT debt

(804)

(804)

(-) Leased imputed debt

(650)

-

(-) Pension liability

(62)

(62)

Net asset FMV

$2,828

$1,913

# of common shares

35.1

35.1

Net asset FMV per share

$80.62

$54.55

December 31, 2014 |

39

UK SAR net asset FMV reconciliation

UK SAR contribution

(in millions)

December 31, 2014

FY16 - FY17

Implied

(+) FMV of aircraft

$1,944

$79

$2,023

(+) FMV of leased aircraft

1,564

172

1,737

(+) NBV of PPE without

aircraft 576

113

689

(+) Working

capital 259

174

433

(-) LT

debt (804)

(88)

(892)

(-) Leased

imputed debt (650)

(95)

(744)

(-) Pension

liability (62)

-

(62)

Net

asset FMV $2,828

$355

$3,183

# of common shares

35.1

35.1

35.1

Net asset FMV per

share $80.62

$10.13

$90.75 |

40

Adjusted EBITDAR margin* trend

*

Adjusted

EBITDAR

excludes

special

items

and

asset

dispositions

and

margin

is

calculated

by

taking

adjusted

EBITDAR

divided

by

operating

revenue

Q1

Q2

Q3

Q4

Full Year

Q1

Q2

Q3

Q4

Full Year

EBU

33.0%

31.4%

30.7%

36.1%

32.9%

32.2%

34.6%

39.5%

38.3%

36.2%

WASBU

29.5%

35.5%

37.2%

36.6%

35.0%

31.9%

26.5%

35.0%

31.8%

31.5%

NABU

14.3%

20.6%

14.8%

19.4%

17.3%

23.2%

20.7%

29.1%

29.5%

25.7%

AUSBU

20.2%

14.4%

23.5%

35.6%

24.3%

27.0%

28.0%

27.3%

26.0%

27.1%

OIBU

48.1%

19.1%

47.8%

42.9%

39.5%

36.2%

44.2%

55.7%

51.6%

46.6%

Consolidated

23.4%

24.0%

27.6%

31.2%

26.6%

26.3%

26.1%

31.5%

29.4%

28.3%

Q1

Q2

Q3

Q4

Full Year

Q1

Q2

Q3

EBU

30.3%

35.3%

35.3%

37.3%

34.7%

34.1%

33.7%

33.1%

WASBU

31.3%

30.4%

33.5%

33.2%

32.1%

25.6%

31.1%

34.6%

NABU

29.2%

31.0%

33.1%

35.4%

32.1%

39.7%

32.4%

40.0%

AUSBU

17.7%

21.0%

15.0%

24.0%

19.6%

23.7%

22.6%

25.4%

OIBU

67.4%

39.3%

33.2%

53.3%

47.7%

41.4%

18.5%

20.7%

Consolidated

28.5%

28.7%

27.0%

30.4%

28.6%

29.2%

25.4%

25.3%

FY13

FY14

FY12

FY15 |

41

Adjusted EBITDAR* reconciliation

* Adjusted EBITDAR excludes special items and asset dispositions

($ in millions)

Q1

Q2

Q3

Q4

FY12

Q1

Q2

Q3

Q4

FY13

Net income

$21

$3

$26

$15

$65

$24

$30

$37

$40

$132

Income tax expense

$7

-$2

$7

$2

$14

$6

$8

$8

$13

$35

Interest expense

$9

$9

$10

$10

$38

$9

$9

$15

$10

$42

Gain on disposal of assets

-$1

$2

$3

$29

$32

$5

$1

-$7

-$7

-$8

Depreciation and amortization

$23

$25

$23

$25

$96

$21

$23

$25

$27

$96

Special items

$0

$25

$0

$3

$28

$2

-$2

$15

$2

$16

Adjusted EBITDA Subtotal

$58

$62

$69

$84

$273

$68

$70

$92

$85

$314

Rental expense

$9

$9

$13

$15

$46

$16

$15

$18

$18

$67

Adjusted EBITDAR

$67

$71

$82

$99

$319

$84

$85

$109

$103

$381

($ in millions)

Q1

Q2

Q3

Q4

FY14

Q1

Q2

Q3

Net income

$27

$110

$19

$32

$188

$45

$28

$0

Income tax expense

$8

$41

$3

$6

$57

$12

$6

$1

Interest expense

$20

$9

$7

$8

$45

$7

$8

$7

Gain on disposal of assets

$2

$3

-$4

$0

$1

-$1

$0

$26

Depreciation and amortization

$23

$24

$24

$26

$96

$25

$28

$24

Special items

$0

-$102

$24

$20

-$59

$6

$7

$5

Adjusted EBITDA Subtotal

$79

$85

$72

$92

$328

$95

$77

$63

Rental expense

$23

$23

$28

$31

$106

$33

$35

$46

Adjusted EBITDAR

$102

$109

$101

$123

$434

$128

$112

$109

Fiscal year ended,

3/31/2012

3/31/2013

3/31/2014

3/31/2015

Fiscal year ended, |

42

Bristow Value Added (BVA)

Sample calculation for Q3 FY15 and Q3 FY14

Bristow Value Added = Gross Cash Flow –

(Gross Operating Assets X Capital Charge)

BVA = GCF –

(GOA x 10.5%**)

Bristow Value Added calculation for Q3 FY15

$19.7 = $118.1* –

($3,751* x 2.625%**)

Bristow Value Added calculation for Q3 FY14

$12.1 = $100.8* –

($3,378* x 2.625%**)

* Reconciliation for these items follows right after this

slide ** Quarterly capital charge of 2.625% is based on annual

capital charge of 10.5% |

43

Bristow gross cash flow reconciliation

(in millions)

Gross cash flow reconciliation

Q3 FY14

Q3 FY15

Net income

19

(1)

Depreciation and amortization

24

24

Interest expense

7

7

Interest income

(0)

(0)

Rent

28

46

Other income/expense-net

1

1

Gain/loss on asset sale

(4)

26

Special items

4

7

Tax effect from special items

(4)

(7)

Earnings (losses) from unconsolidated affiliates, net

16

1

Non-controlling interests

0

1

Gross cash flow before Líder

$91

$106

Gross cash flow - Líder proportional

10

12

Gross cash flow after Líder

$101

$118 |

44

Bristow adjusted gross operating assets reconciliation

(in millions)

Adjusted gross operating assets reconciliation

Q3 FY14

Q3 FY15

Total assets

3,277

3,180

Accumulated depreciation

530

495

Capitalized operating leases

419

660

Cash and cash equivalents

(323)

(121)

Investment in unconsolidated entities

(255)

(257)

Goodwill

(30)

(54)

Intangibles

(2)

(16)

Assets held for sale: net

(22)

(26)

Assets held for sale: gross

48

110

Adj. for gains & losses on assets sales

(5)

28

Accounts payable

(60)

(90)

Accrued maintenance and repairs

(17)

(19)

Other accrued taxes

(8)

(8)

Accrued wages, benefits and related taxes

(67)

(77)

Other accrued liabilities

(145)

(110)

Income taxes payable

(20)

(8)

Deferred revenue

(23)

(29)

ST deferred taxes

(2)

(13)

LT deferred taxes

(146)

(163)

Adjusted gross operating assets before Líder

$3,150

3,482

Adjusted gross operating assets -

Líder proportional

228

269

Adjusted gross operating assets after Líder

$3,378

3,751 |

45

Líder Bristow Value Added (BVA)

Sample calculation for Q3 FY15 and Q3 FY14

Bristow Value Added = Gross Cash Flow –

(Gross Operating Assets X Capital Charge)

BVA = GCF –

(GOA x 10.5%** )

Bristow Value Added calculation for Q3 FY15

$5.1 = $12.2* –

($269* x 2.625%**)

Bristow Value Added calculation for Q3 FY14

$4.2 = $10.2* –

($228* x 2.625%**)

* Reconciliation for these items follows right after this

slide ** Quarterly capital charge of 2.625% is based on annual

capital charge of 10.5% |

46

Líder gross cash flow reconciliation

($ in millions)

Gross cash flow reconciliation

Q3 FY13

Q3 FY15

Net income (loss)

7.1

$

(6.5)

$

Depreciation and amortization

3.6

3.5

Rent

6.5

7.4

Interest expense

3.7

4.4

Interest income

(1.2)

(1.4)

FX (gains) losses

6.4

15.7

Other income/expense-net

(1.2)

(0.2)

Special Adjustment- remove Lider tax per income stmt.

1.1

5.2

Earnings (losses) from unconsolidated affiliates, net

0.2

-

Non-controlling Interests

(0.4)

0.6

Gross cash flow

25.7

28.8

Special item outside of Líder - add Bristow tax calc.

(1.9)

0.3

Gross cash flow

23.9

29.1

Líder proportional consolidation - GCF

10.0

$

12.2

$ |

47

Líder adjusted gross operating assets reconciliation

($ in millions)

Adjusted gross operating assets reconciliation

Q3 FY14

Q3 FY15

Total assets

589

$

611

$

Cash and cash equivalents

(100)

(67)

Accumulated depreciation

75

80

Capitalized operating leases

129

148

Investments & escrow deposits

(33)

(46)

Intangibles

(5)

(5)

Intangibles, amortization

4

4

Other, non operating assets

(19)

(19)

Adj. for gains & losses on assets sales

-

-

Accounts payable

(26)

(29)

Other payables

(1)

(0)

Other accrued taxes

-

(6)

Accrued wages, benefits and related taxes

(25)

(20)

Income taxes payable

(5)

(5)

Deferred revenue

(11)

(5)

LT deferred taxes

(34)

-

Adjusted gross operating assets

537

643

Líder proportional consolidation GOA

225

$

269

$

|

48

Líder's adjusted EBITDAR* reconciliation

* Adjusted EBITDAR excludes special items and asset dispositions

($ in millions)

Q4 CY13

Q1 CY14

Q2 CY14

Q3 CY14

Q4 CY14

Gross revenue

119.3

121.2

113.7

116.4

100.9

(-) Revenue deductions

(7.6)

(5.9)

(7.3)

(7.7)

(6.1)

Net operating revenue

111.3

115.3

106.4

108.7

94.8

(-) Cost of products and services

(87.0)

(90.8)

(79.5)

(82.0)

(72.1)

Gross profit

24.6

24.5

26.9

26.6

22.7

(-) Selling and administrative expenses

(9.6)

(7.0)

(7.5)

(8.8)

(9.0)

(+) Equity income of associates

(0.0)

0.5

0.8

(0.6)

(0.2)

(+) Other operating income/expenses

0.7

0.2

0.2

0.2

11.7

Operating result

15.7

18.3

20.4

17.5

25.2

(+) Depreciation and amortization

3.5

3.4

3.5

3.5

3.3

EBITDA

19.2

21.6

23.9

21.0

28.5

Leasing costs

7.3

7.4

7.3

7.4

6.8

Adjusted EBITDAR

26.4

29.1

31.2

28.4

35.3

|

49

GAAP reconciliation

1)

See information about special items in 10-Q or earnings release for Q3

FY15 2)

These amounts are presented after applying the appropriate tax effect to each item

and dividing by the weighted average shares outstanding during the related period to calculate the earnings

per share impact

2014

2013

2014

2013

Adjusted operating income

$43,564

$49,056

$161,303

$165,293

Gain (loss) on disposal of assets

(26,331)

3,982

(25,594)

(803)

Special

items

1

(8,317)

(23,536)

(17,537)

(24,934)

Operating income

$8,916

$29,502

$118,172

$139,556

Adjusted EBITDAR

$109,056

$100,677

$347,494

$310,968

Gain (loss) on disposal of assets

(26,331)

3,982

(25,594)

(803)

Special items

1

(5,086)

(23,536)

(16,207)

78,990

Depreciation and amortization

(23,625)

(23,655)

(77,164)

(70,332)

Rent expense

(46,282)

(28,255)

(114,839)

(74,630)

Interest expense

(7,094)

(7,253)

(22,415)

(36,701)

Provision for income taxes

(567)

(2,946)

(18,376)

(51,682)

Net income

$71

$19,014

$72,899

$155,810

Adjusted net income

$24,719

$31,331

$102,159

$113,891

Gain

(loss)

on

disposal

of

assets

2

(21,033)

3,146

(20,441)

(634)

Special

items

1,2

(4,654)

(15,550)

(12,495)

43,162

Net income (loss) attributable to Bristow Group

($968)

$18,927

$69,223

$156,419

Adjusted diluted earnings per share

$0.70

$0.85

$2.87

$3.11

Gain

(loss)

on

disposal

of

assets

2

(0.60)

0.09

(0.57)

(0.02)

Special

items

1,2

(0.13)

(0.42)

(0.35)

1.18

Diluted earnings (loss) per share

($0.03)

$0.51

$1.94

$4.28

Three months ended

December 31,

Nine months ended

December 31,

(In thousands, except per share amounts) |

50

Bristow leverage reconciliation

*Adjusted EBITDAR excludes gains and losses on dispositions of assets

Debt

Investment

Capital

Leverage

(a)

(b)

(c) = (a) + (b)

(a) / (c)

(in millions)

As of December 31, 2014

818.2

$

1,694.2

$

2,512.4

$

32.6%

Adjust for:

Unfunded Pension Liability

62.1

62.1

NPV of Lease Obligations

649.7

649.7

Letters of credit

2.5

2.5

Adjusted

1,532.5

$

(d)

1,694.2

$

3,226.7

$

47.5%

Calculation of debt to adjusted EBITDAR multiple

TTM Adjusted EBITDAR*:

FY 2015

470.2

$

(e)

= (d) / (e)

3.26:1 |

51

Líder leverage reconciliation

(in millions)

Dec-13

Dec-14

Total book debt

279

$

310

$

NPV of leases

69

46

Total adjusted debt

348

356

TTM adjusted EBITDAR

123

$

124

$

Adjusted debt / TTM adj. EBITDAR

2.8x

2.9x |

52

Bristow Group Inc. (NYSE: BRS)

2103 City West Blvd., 4

th

Floor

Houston, Texas 77042

t

713.267.7600

f

713.267.7620

bristowgroup.com

Contact us |