Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - FAMILY DOLLAR STORES INC | d850571d8k.htm |

| EX-99.1 - EX-99.1 - FAMILY DOLLAR STORES INC | d850571dex991.htm |

Exhibit 99.2

|

|

Proposed Acquisition of

Family Dollar by Dollar Tree

January 12, 2015

1. DOLLAR TREE FAMILY DOLLAR

Additional Information About the Dollar General Tender Offer

Family Dollar has filed a solicitation/recommendation statement with respect to the tender offer with the SEC. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE

SOLICITATION/RECOMMENDATION STATEMENT WITH RESPECT TO THE TENDER OFFER AND OTHER RELEVANT DOCUMENTS THAT ARE FILED WITH THE SEC BECAUSE THEY CONTAIN IMPORTANT

INFORMATION ABOUT THE TENDER OFFER. You may obtain free copies of the solicitation/recommendation statement with respect to the tender offer and other documents filed with the SEC by Family Dollar through the website maintained by the SEC at http://www.sec.gov. Copies of the documents filed with the SEC by Family Dollar are available free of charge on Family Dollar’s internet website at www.FamilyDollar.com under the heading “Investor Relations” and then under the heading “SEC Filings” or by contacting Family Dollar’s Investor Relations Department at 704-708-2858.

Important Information for Investors and Stockholders

This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended. In connection with the proposed merger between Dollar Tree and Family Dollar, on October 28, 2014, the Securities and Exchange Commission (SEC) declared effective Dollar Tree’s registration statement on Form S-4 that included a definitive proxy statement of Family Dollar that also constitutes a prospectus of Dollar Tree. On October 28, 2014, Family Dollar commenced mailing the definitive proxy statement/prospectus to stockholders of Family Dollar. INVESTORS AND SECURITY HOLDERS OF FAMILY DOLLAR ARE URGED TO READ THE DEFINITIVE PROXY STATEMENT/PROSPECTUS (INCLUDING ALL AMENDMENTS AND SUPPLEMENTS THERETO) AND OTHER DOCUMENTS RELATING TO THE MERGER THAT ARE FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED MERGER. Investors and security holders are able to obtain free copies of the registration statement and the definitive proxy statement/prospectus (when available) and other documents filed with the SEC by Dollar Tree and Family Dollar through the website maintained by the SEC at http://www.sec.gov. Copies of the documents filed with the SEC by Dollar Tree are available free of charge on Dollar Tree’s internet website at www.DollarTree.com under the heading “Investor Relations” and then under the heading “Download Library” or by contacting Dollar Tree’s Investor Relations Department at 757-321-5284. Copies of the documents filed with the SEC by Family Dollar are available free of charge on Family Dollar’s internet website at www.FamilyDollar.com under the heading “Investor Relations” and then under the heading “SEC Filings” or by contacting Family Dollar’s Investor Relations Department at 704-708-2858.

Participants in the Solicitation For the Proposed Dollar Tree/Family Dollar Merger

Dollar Tree, Family Dollar, and their respective directors, executive officers and certain other members of management and employees may be deemed to be participants in the solicitation of proxies from the holders of Family Dollar common stock in respect of the proposed merger between Dollar Tree and Family Dollar. Information regarding the persons who may, under the rules of the SEC, be considered participants in the solicitation of proxies in favor of the proposed merger are set forth in the proxy statement/prospectus filed with the SEC. You can also find information about Dollar Tree’s and Family Dollar’s directors and executive officers in Dollar Tree’s definitive proxy statement filed with the SEC on May 12, 2014 and in Family Dollar’s Annual Report on Form 10-K for the fiscal year ended August 30, 2014, respectively. You can obtain free copies of these documents from Dollar Tree or Family Dollar using the contact information above.

Forward Looking Statements

Certain statements contained herein are “forward-looking statements” that are subject to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements and information about our current and future prospects and our operations and financial results are based on currently available information. Various risks, uncertainties and other factors could cause actual future results and financial performance to vary significantly from those anticipated in such statements. The forward looking statements contained herein include assumptions about our operations, such as cost controls and market conditions, and certain plans, activities or events which we expect will or may occur in the future and relate to, among other things, the business combination transaction involving Dollar Tree and Family Dollar, the unsolicited tender offer and proposals from Dollar General and any other alternative business combination transactions, the financing of the proposed transactions, the benefits, results, effects, timing and certainty of the proposed transactions, future financial and operating results, expectations concerning the antitrust review process for the proposed transactions and the combined company’s plans, objectives, expectations (financial or otherwise) and intentions.

Risks and uncertainties related to the proposed mergers include, among others: the risk that Family Dollar’s stockholders do not approve either merger; the risk that the merger agreement is terminated as a result of a competing proposal; the risk that regulatory approvals required for either merger are not obtained on the proposed terms and schedule or are obtained subject to conditions that are not anticipated; the risk that the other conditions to the closing of either merger are not satisfied; the risk that the financing required to fund either transaction is not obtained; potential adverse reactions or changes to business or employee relationships, including those resulting from the announcement or completion of either merger; uncertainties as to the timing of either merger; competitive responses to either proposed merger; response by activist stockholders to either merger; costs and difficulties related to the integration of Family Dollar’s business and operations with Dollar Tree’s or other potential business combination transaction counterparties’ business and operations; the inability to obtain, or delays in obtaining, the cost savings and synergies contemplated by either merger; uncertainty of the expected financial performance of the combined company following completion of either proposed transaction; the calculations of, and factors that may impact the calculations of, the acquisition price in connection with either proposed transaction and the allocation of such acquisition price to the net assets acquired in accordance with applicable accounting rules and methodologies; unexpected costs, charges or expenses resulting from either merger; litigation relating to either merger; the outcome of pending or potential litigation or governmental investigations; the inability to retain key personnel; and any changes in general economic and/or industry specific conditions. Consequently, all of the forward-looking statements made by Family Dollar, in this and in other documents or statements are qualified by factors, risks and uncertainties, including, but not limited to, those set forth under the headings titled “Cautionary Statement Regarding Forward-Looking Statements” and “Risk Factors” in Family Dollar’s Annual Report on Form 10-K for the fiscal year ended August 30, 2014, Family Dollar’s Quarterly Report on Form 10-Q for the quarter ended November 29, 2014, and other reports filed by Family Dollar with the SEC, which are available at the SEC’s website http://www.sec.gov.

Please read our “Risk Factors” and other cautionary statements contained in these filings. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Family Dollar undertakes no obligation to update or revise any forward-looking statements, even if experience or future changes make it clear that projected results expressed or implied in such statements will not be realized, except as may be required by law. As a result of these risks and others, actual results could vary significantly from those anticipated herein, and our financial condition and results of operations could be materially adversely affected.

FAMILY DOLLAR 2

Executive Summary

Transparency on FTC Feedback on DG Proposal: 3,500 to 4,000 Stores Presumptively Problematic

DG Has Offered to Divest Only 1,500 Stores

Transparency on FTC Feedback on DLTR Merger: 310 or Fewer Stores Presumptively Problematic

DLTR Has Committed to Divest as Many Stores as Necessary to Get FTC Approval

DLTR Jan. 9 Letter to FDO

“Dollar Tree is not willing to agree to any further adjournments.”

“[T]he existing transaction with Dollar Tree which is on terms that-- we believe-- could not be replicated at the present time.”

The Time is Right for Vote on Merger — Adjournment and Postponement Risks

DLTR Merger Will Deliver Substantial and Certain Value to FDO Stockholders

Challenging and Deteriorating Near-term Stand-alone Prospects

Delaware Court of Chancery Praised FDO Board and Sale Processes

FAMILY DOLLAR 3

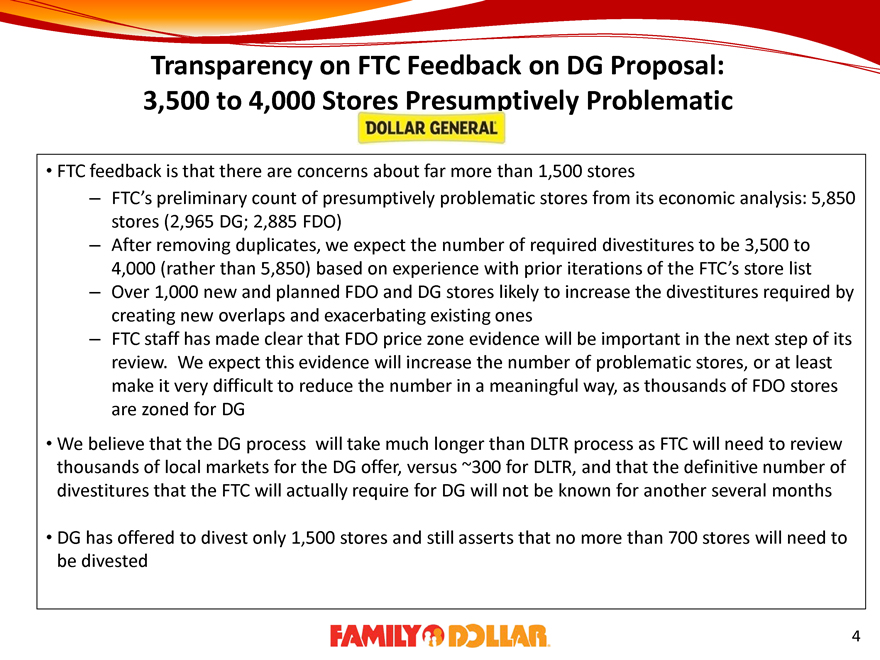

Transparency on FTC Feedback on DG Proposal:

3,500 to 4,000 Stores Presumptively Problematic

DOLLAR GENERAL

FTC feedback is that there are concerns about far more than 1,500 stores

– FTC’s preliminary count of presumptively problematic stores from its economic analysis: 5,850 stores (2,965 DG; 2,885 FDO)

– After removing duplicates, we expect the number of required divestitures to be 3,500 to 4,000 (rather than 5,850) based on experience with prior iterations of the FTC’s store list

– Over 1,000 new and planned FDO and DG stores likely to increase the divestitures required by creating new overlaps and exacerbating existing ones

– FTC staff has made clear that FDO price zone evidence will be important in the next step of its review. We expect this evidence will increase the number of problematic stores, or at least make it very difficult to reduce the number in a meaningful way, as thousands of FDO stores are zoned for DG

We believe that the DG process will take much longer than DLTR process as FTC will need to review thousands of local markets for the DG offer, versus ~300 for DLTR, and that the definitive number of divestitures that the FTC will actually require for DG will not be known for another several months

DG has offered to divest only 1,500 stores and still asserts that no more than 700 stores will need to be divested

FAMILY DOLLAR 4

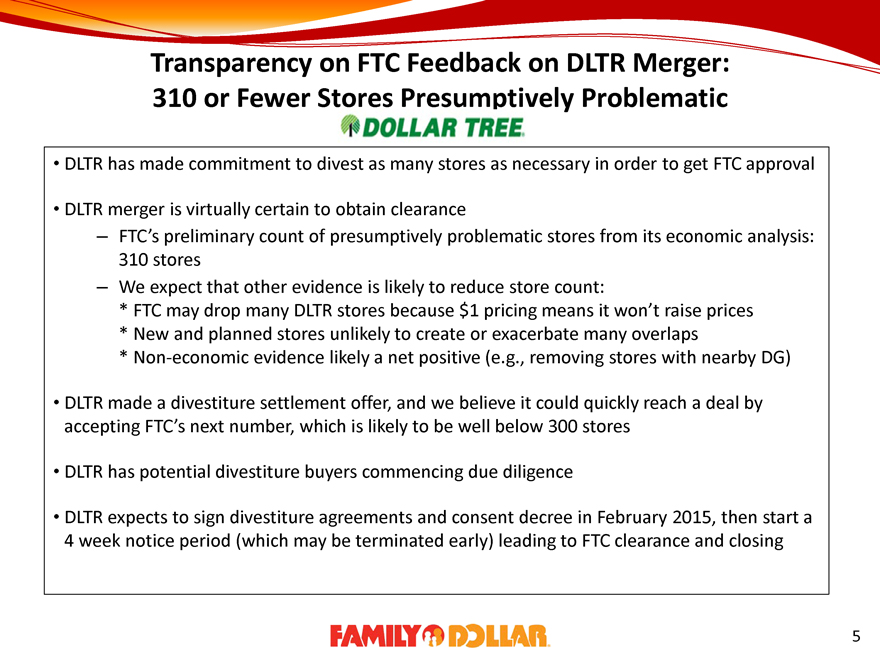

Transparency on FTC Feedback on DLTR Merger: 310 or Fewer Stores Presumptively Problematic

DOLLAR TREE

DLTR has made commitment to divest as many stores as necessary in order to get FTC approval

DLTR merger is virtually certain to obtain clearance

– FTC’s preliminary count of presumptively problematic stores from its economic analysis: 310 stores

– We expect that other evidence is likely to reduce store count:

* FTC may drop many DLTR stores because $1 pricing means it won’t raise prices

* New and planned stores unlikely to create or exacerbate many overlaps

* Non-economic evidence likely a net positive (e.g., removing stores with nearby DG)

DLTR made a divestiture settlement offer, and we believe it could quickly reach a deal by accepting FTC’s next number, which is likely to be well below 300 stores

DLTR has potential divestiture buyers commencing due diligence

DLTR expects to sign divestiture agreements and consent decree in February 2015, then start a 4 week notice period (which may be terminated early) leading to FTC clearance and closing

FAMILY DOLLAR 5

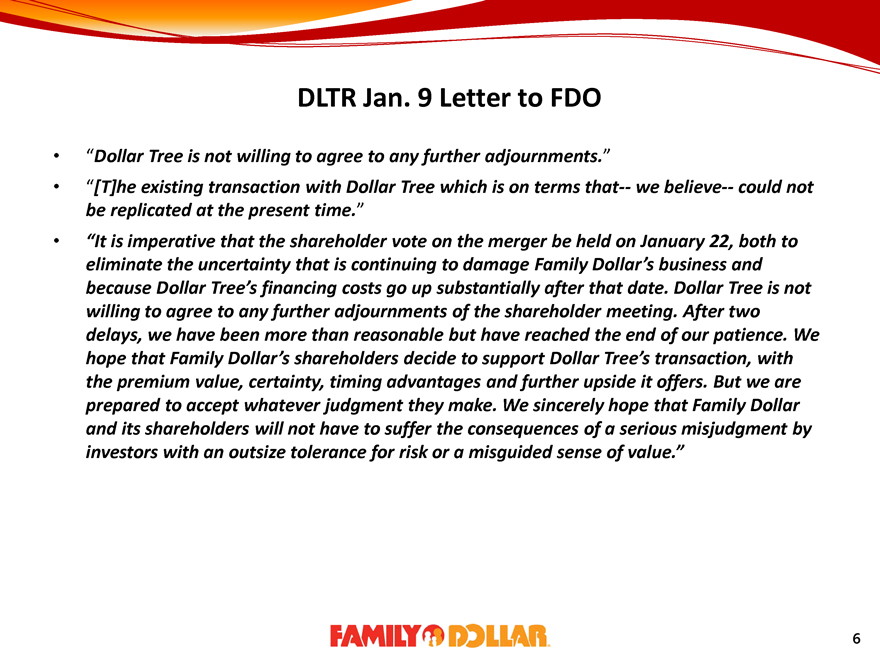

DLTR Jan. 9 Letter to FDO

“Dollar Tree is not willing to agree to any further adjournments.”

“ [T]he existing transaction with Dollar Tree which is on terms that-- we believe-- could not be replicated at the present time.”

“It is imperative that the shareholder vote on the merger be held on January 22, both to eliminate the uncertainty that is continuing to damage Family Dollar’s business and because Dollar Tree’s financing costs go up substantially after that date. Dollar Tree is not willing to agree to any further adjournments of the shareholder meeting. After two delays, we have been more than reasonable but have reached the end of our patience. We hope that Family Dollar’s shareholders decide to support Dollar Tree’s transaction, with the premium value, certainty, timing advantages and further upside it offers. But we are prepared to accept whatever judgment they make. We sincerely hope that Family Dollar and its shareholders will not have to suffer the consequences of a serious misjudgment by investors with an outsize tolerance for risk or a misguided sense of value.”

FAMILY DOLLAR 6

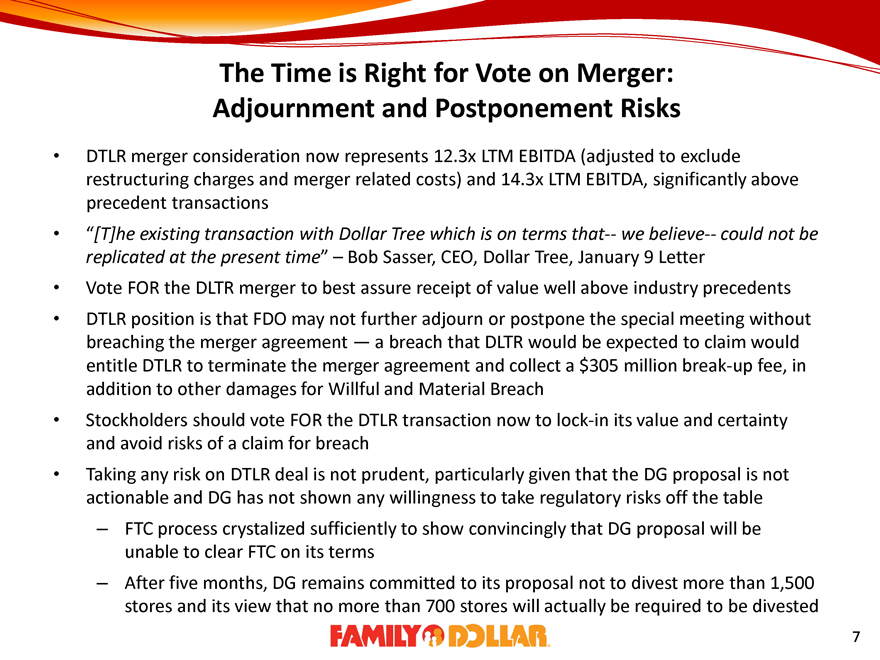

The Time is Right for Vote on Merger: Adjournment and Postponement Risks

DTLR merger consideration now represents 12.3x LTM EBITDA (adjusted to exclude restructuring charges and merger related costs) and 14.3x LTM EBITDA, significantly above precedent transactions

“[T]he existing transaction with Dollar Tree which is on terms that-- we believe-- could not be replicated at the present time” – Bob Sasser, CEO, Dollar Tree, January 9 Letter

Vote FOR the DLTR merger to best assure receipt of value well above industry precedents

DTLR position is that FDO may not further adjourn or postpone the special meeting without breaching the merger agreement — a breach that DLTR would be expected to claim would entitle DTLR to terminate the merger agreement and collect a $305 million break-up fee, in addition to other damages for Willful and Material Breach

Stockholders should vote FOR the DTLR transaction now to lock-in its value and certainty and avoid risks of a claim for breach

Taking any risk on DTLR deal is not prudent, particularly given that the DG proposal is not actionable and DG has not shown any willingness to take regulatory risks off the table

– FTC process crystalized sufficiently to show convincingly that DG proposal will be unable to clear FTC on its terms

– After five months, DG remains committed to its proposal not to divest more than 1,500 stores and its view that no more than 700 stores will actually be required to be divested

FAMILY DOLLAR 7

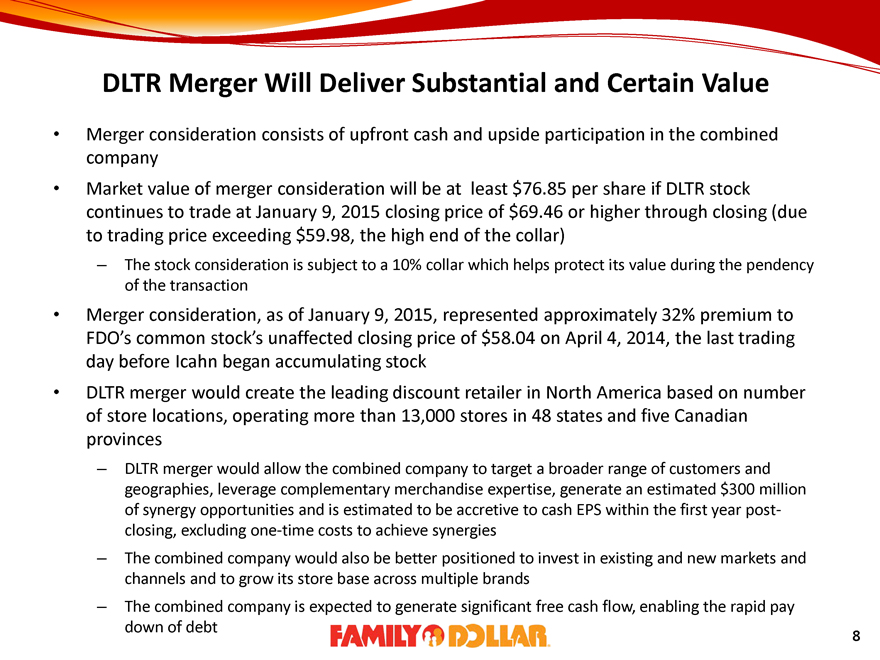

DLTR Merger Will Deliver Substantial and Certain Value

Merger consideration consists of upfront cash and upside participation in the combined company

Market value of merger consideration will be at least $76.85 per share if DLTR stock continues to trade at January 9, 2015 closing price of $69.46 or higher through closing (due to trading price exceeding $59.98, the high end of the collar)

– The stock consideration is subject to a 10% collar which helps protect its value during the pendency of the transaction

Merger consideration, as of January 9, 2015, represented approximately 32% premium to FDO’s common stock’s unaffected closing price of $58.04 on April 4, 2014, the last trading day before Icahn began accumulating stock

DLTR merger would create the leading discount retailer in North America based on number of store locations, operating more than 13,000 stores in 48 states and five Canadian provinces

– DLTR merger would allow the combined company to target a broader range of customers and geographies, leverage complementary merchandise expertise, generate an estimated $300 million of synergy opportunities and is estimated to be accretive to cash EPS within the first year post-closing, excluding one-time costs to achieve synergies

– The combined company would also be better positioned to invest in existing and new markets and channels and to grow its store base across multiple brands

– The combined company is expected to generate significant free cash flow, enabling the rapid pay down of debt

FAMILY DOLLAR 8

Challenging and Deteriorating Near-term Stand-alone Prospects

If DLTR merger agreement is not approved by FDO stockholders, there is a significant risk that FDO is left without a merger partner because of the very significant antitrust risks facing DG transaction on the terms proposed

Given current challenging market conditions, there are significant risks and uncertainties to FDO as a standalone company and to the value of its stockholders’ investment in FDO should the DLTR merger agreement not be adopted by FDO stockholders

As stated in our 1Q15 earnings release, FDO had a very challenging quarter and expects many of the headwinds faced in the fourth quarter of fiscal year 2014 to continue in fiscal year 2015, including ongoing topline challenges and pressure on gross margins

January 9, 2015 Letter from DLTR CEO to FDO highlights these concerns and concludes that the terms of the DLTR merger agreement “could not be replicated at the present time”

Recent analyst projections for share price of FDO, as standalone company, are $35-$50 (Barclays 1.9.15), $52 (Deutsche Bank 1.8.15) and $53 (Cannacord Genuity 1.8.15)

FAMILLY DOLLAR 9

Delaware Court Praised FDO’s Board and Sale Processes

“[DLTR] transaction that offers [stockholders] a significant premium for their shares and apparent deal certainty.”

FDO Board’s recommendation “reflects the reality that, for the company’s stockholders, a financially superior offer on paper does not equate to a financially superior transaction in the real world if there is a meaningful risk that the transaction will not close for antitrust reasons.”

“The record here demonstrates that the Board was properly motivated to maximize value for [FDO]’s stockholders.”

“The record fails to demonstrate that Levine, the only [FDO] executive on the Board, harbored any entrenchment motivation. To the contrary, the record shows that Levine had been planning his retirement since 2011 and had no desire to run a combined company after the transaction, but was advised to express a desire to do so as a negotiating tactic; that [DLTR] insisted that Levine stay on post-closing to help with integration of the companies; and that [DG] made the same request. Levine, moreover, personally held almost 9 million shares of [FDO] stock and thus, similar to [Ed] Garden [of Trian], had a significant economic incentive to pursue maximum value for his shares of [FDO].”

FAMILY DOLLAR 10

Delaware Court Praised FDO’s Board and Sale Processes (cont.)

“[T]he preliminary record shows that [FDO] had engaged in a number of discussions with [DG] dating back to early 2013 in an effort to explore a transaction between [FDO] and [DG]. Of particular note, in June 2014, after Icahn had surfaced and [DLTR] had made a proposal of $72 per share but not yet entered into an exclusivity arrangement with [FDO], the Board instructed Levine to encourage [DG] to re-engage in discussions in an effort to obtain a higher offer. Levine did so and directly solicited an offer from [DG]. When no offer was forthcoming from [DG], the Board continued its discussions with [DLTR], resulting in an offer of $74.50 per share. Only then did [FDO] commit to an exclusivity arrangement with [DLTR]. These actions do not suggest any favoritism of [DLTR] over [DG] based on an improper motivation. To the contrary, the record, albeit preliminary, demonstrates to me that the Board was motivated to maximize the value of [FDO].”

FAMILY DOLLAR 11