Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Blue Bird Corp | d849511d8k.htm |

Hennessy Capital Acquisition Corp.

Acquisition of Blue Bird Corporation

Investor Presentation

January 2015

Exhibit 99.1 |

2

Important Disclaimers

Use of Projections

The information in this presentation is highly confidential. The distribution of this presentation by

an authorized recipient to any other person is unauthorized. Any photocopying, disclosure,

reproduction or alteration of the contents of this presentation and any forwarding of a copy of this presentation or any portion of this presentation to any person is prohibited.

The recipient of this presentation shall keep this presentation and its contents confidential, shall

not use this presentation and its contents for any purpose other than as expressly authorized

by Hennessy Capital Acquisition Corp. (“HCAC”) and Blue Bird Corporation (“Blue Bird”) and shall be required to return or destroy all copies of this presentation or portions

thereof in its possession promptly following request for the return or destruction of such copies. By

accepting delivery of this presentation, the recipient is deemed to agree to the foregoing

confidentiality requirements. In this

presentation, certain of the above-mentioned projected information has been repeated (in each case, with an indication that the information is an estimate and is subject to the

qualifications presented herein), for purposes of providing comparisons with historical data. The

assumptions and estimates underlying the prospective financial information are inherently

uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from

those contained in the prospective financial information. Accordingly, there can be no assurance that

the prospective results are indicative of the future performance of Hennessy Capital or Blue

Bird or that actual results will not differ materially from those presented in the prospective financial information. Inclusion of the prospective financial information in this

presentation should not be regarded as a representation by any person that the results contained in

the prospective financial information will be achieved. Confidentiality

This presentation and the preliminary proxy statement referred to below contain financial forecasts

with respect to Blue Bird’s projected net revenues and Adjusted EBITDA for Blue Bird’s

fiscal 2015. Neither Hennessy Capital’s independent auditors, nor the independent registered public accounting firm of Blue Bird, audited, reviewed, compiled, or performed any

procedures with respect to the projections for the purpose of their inclusion in this presentation and

the preliminary proxy statement, and accordingly, neither of them expressed an opinion or

provided any other form of assurance with respect thereto for the purpose of this presentation or the preliminary proxy statement. PricewaterhouseCoopers LLP and KPMG

LLP did not audit, review, compile or perform any procedures with respect to that information and has

not expressed any opinion or any other form of assurance with respect thereto. These projections

should not be relied upon as being necessarily indicative of future results. Reference is made to pages 145-149 of the preliminary proxy statement for a full

description of the limitations associated with these forecasts. |

3

Important Disclaimers (continued)

Other companies may calculate Adjusted EBITDA and other non-GAAP measures differently, and

therefore our Adjusted EBITDA and other non-GAAP measures and that of Blue Bird may

not be directly comparable to similarly titled measures of other companies. This presentation includes “forward looking statements” within the meaning of

the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. Forward-looking

statements may be identified by the use of words such as "forecast," "intend,"

"seek," "target," “anticipate,” “believe,” “expect,” “estimate,” “plan,” “outlook,” and “project” and other similar

expressions that predict or indicate future events or trends or that are not statements of

historical matters. Such forward looking statements include projected financial information. Such forward

looking statements with respect to revenues, earnings, performance, strategies, prospects and

other aspects of the businesses of HCAC, Blue Bird and the combined company after completion of

the proposed business combination are based on current expectations that are subject to risks

and uncertainties. A number of factors could cause actual results or outcomes to differ materially

from those indicated by such forward looking statements. These factors include, but are not

limited to: (1) the failure of the parties to consummate the transactions contemplated by the definitive

purchase agreement relating to the proposed business combination (the “Purchase

Agreement”) including the occurrence of any event, change or other circumstances that could give rise to the

termination of the Purchase Agreement; (2) the outcome of any legal proceedings that may be

instituted against Blue Bird or HCAC arising from the announcement of the proposed business

combination and transactions contemplated thereby; (3) the inability to complete the

transactions contemplated by the proposed business combination due to the failure to obtain approval of the

stockholders of HCAC, or the failure to satisfy other conditions to closing in the Purchase

Agreement; (4) the inability to obtain or maintain the listing of the post-combination company’s common

stock on NASDAQ following the business combination; (5) the risk that the proposed business

combination disrupts current plans and operations as a result of the announcement and

consummation of the transactions described herein; (6) the inability to recognize the

anticipated benefits of the business combination, which may be affected by, among other things, competition,

and the ability of the combined business to grow and manage growth profitably; (7) costs related

to the business combination; (8) changes in applicable laws or regulations; (9) the possibility that

Blue Bird or HCAC may be adversely affected by other economic, business, and/or competitive

factors; and (10) other risks and uncertainties indicated from time to time in the proxy statement,

including those under “Risk Factors” therein, and other documents filed or to be filed

with the Securities and Exchange Commission (“SEC”) and delivered to HCAC's stockholders. You are cautioned

not to place undue reliance upon any forward-looking statements, which speak only as of the

date made. HCAC and Blue Bird undertake no commitment to update or revise the forward-looking

statements, whether as a result of new information, future events or otherwise. In most

instances, where third party sources are identified in this presentation, the information has been derived

by Blue Bird management from the source data.

Forward Looking Statements

Blue Bird believes that the use of these non-GAAP financial measures provides an additional

tool for investors to use in evaluating ongoing operating results and trends. Management

of Blue Bird does not consider these non-GAAP measures in isolation or as an alternative to

financial measures determined in accordance with GAAP. We have not reconciled the non-

GAAP forward looking information to their corresponding GAAP measures because we do not provide

guidance for the various reconciling items such as stock-based compensation,

provision for income taxes and depreciation and amortization, as certain items that impact these

measures are out of our control or cannot be reasonably predicted. You should review Blue

Bird’s audited financial statements, which are and will be presented in HCAC's proxy statement filings with the SEC, including the proxy statement to be delivered to HCAC’s

stockholders, and not rely on any single financial measure to evaluate Blue Bird’s

business. Use of Non-GAAP Financial Measures

This presentation includes non-GAAP financial measures, including Adjusted EBITDA, Adjusted

EBITDA Margin and Net Debt. Adjusted EBITDA involves certain adjustments to EBITDA, which

is calculated as earnings before interest, taxes, depreciation and amortization (“EBITDA” ). Adjusted EBITDA includes add-backs for Restructuring costs, Non-recurring

Management Incentive Compensation and other non-recurring expenses. Adjusted EBITDA

Margin is defined as Adjusted EBITDA divided by total revenues. Net Debt is defined as Total

Debt less Cash and Cash Equivalents. You can find the reconciliation of these measures to the

nearest comparable GAAP measures elsewhere in this presentation. Except as otherwise

noted, all references herein to full-year periods refer to Blue Bird’s fiscal year,

which ends on the Saturday closest to September 30. Blue Bird believes that these non-GAAP measures of financial results provide useful

information to management and investors regarding certain financial and business trends relating

to Blue Bird’s financial condition and results of operations. Blue Bird’s management

uses these non-GAAP measures to compare Blue Bird’s performance to that of prior periods for

trend analyses, for purposes of determining management incentive compensation, and for budgeting

and planning purposes. These measures are used in monthly financial reports prepared for

management and Blue Bird’s board of directors. |

4

Important Disclaimers (continued)

Additional Information

Important

Information

about

the

Warrant

Exchange

Offer

Participants in the Solicitation

The proposed business combination will be submitted to stockholders of HCAC for their consideration.

In connection with that approval, HCAC has filed with the SEC a preliminary proxy statement

containing information about the proposed transaction and the respective businesses of Blue Bird and HCAC. Stockholders are urged to read the preliminary proxy

statement and the definitive proxy statement when it becomes available because they will contain

important information. Stockholders will be able to obtain a free copy of the proxy

statement, as well as other filings containing information about HCAC, without charge, at the

SEC’s Internet site (www.sec.gov). Copies of the proxy statement can also be obtained,

without charge, by directing a request to Charles Lowrey, Executive Vice President & CFO, 700

Louisiana Street, Suite 900, Houston, Texas 77002. HCAC has commenced an exchange offer for HCAC’s outstanding warrants. This presentation is

neither an offer to exchange nor a solicitation of an offer to sell any securities. The

solicitation and the offer to exchange HCAC’s public warrants are being made solely pursuant to

an offer to exchange and related materials that HCAC has filed with the SEC on January 7, 2015,

as exhibits to the HCAC tender offer statement on Schedule TO. The Schedule TO (including an offer to exchange, a related letter of transmittal and other offer

documents) contains important information that should be read carefully and considered before any

decision is made with respect to the exchange offer. These materials are being sent free of

charge to holders of HCAC’s outstanding warrants. In addition, all of these materials (and all other materials filed by HCAC with the SEC) are available at no charge from

the SEC through its website at www.sec.gov. Security holders may also

obtain free copies of the documents filed with the SEC by HCAC by directing a request to: Morrow & Co., LLC,

HCAC’s information agent, at 470 West Avenue, 3rd Floor, Stamford, CT 06902, or by phone at (800)

662-5200 or email at hennessy.info@morrowco.com. Holders of HCAC’s

outstanding warrants are urged to read the exchange offer documents and the other relevant materials

(as they become available) before making any investment decision with respect to the exchange

offer because they contain important information about the exchange offer and the transaction. HCAC and its directors and executive officers and other persons may be deemed to be participants in

the solicitations of proxies from HCAC’s stockholders in respect of the proposed business

combination and the other matters set forth in the proxy statement. Information regarding HCAC’s directors and executive officers and a description of their direct and indirect

interests, by security holdings or otherwise, is contained in the Company’s preliminary proxy

statement for the Business Combination, which has been filed with the SEC.

|

5

Daniel J. Hennessy

Chairman and CEO, HCAC |

Hennessy Capital Acquisition Corp.

Hennessy Capital is a special purpose acquisition company

formed in Delaware on September 24, 2013 for the purpose of

effecting a merger, capital stock exchange, asset acquisition,

stock purchase, reorganization or similar business combination

Hennessy Capital’s securities are traded on NASDAQ under the

symbols HCAC, HCACU and HCACW and will convert to BLBD

and BLBDW after the closing of the Business Combination

Cash in trust account at HCAC at September 30, 2014 was $115

million

Hennessy Capital selected Blue Bird from a candidate list of over

125 companies and after interviews with representatives of 19

potential acquisition targets

6 |

7

HCAC View of Blue Bird

An iconic school bus brand

Engaged and committed leadership team with a proven

ability to drive productivity, growth and free cash flow

Substantial growth opportunities from both domestic

industry recovery and market share gains in existing and

new markets

Attractive valuation that is well positioned relative to

public market comparables

Strong support from a committed sponsor with

significant equity rollover |

8

Transaction

Overview

Consideration

HCAC will acquire all of the outstanding capital stock of School

Bus

Holdings Inc., the indirect parent company of Blue Bird Corporation

(“Blue Bird”

or the “Company”)

HCAC

stockholders,

including

the

founders,

will

collectively

own

57.6%

of

the

pro forma combined company

(1)

and an affiliate of Cerberus

Capital Management, L.P. will continue to own 42.4% of Blue Bird

equity

(1)

Entity

expected

to

be

listed

on

NASDAQ

post

business

combination

and

take

the

name of Blue Bird Corporation

12,125,000 outstanding HCAC Warrants will be exchanged for 1,212,500

shares of HCAC common stock as part of the transaction

Transaction anticipated to close promptly after the stockholders’

meeting scheduled for February 9

th

Transaction value of $469 million

7.0x FY2014 Adjusted EBITDA of $67 million

6.3x

to

6.5x

FY2015E

Adjusted

EBITDA

of

$72

to

$75

million

(2)

Transaction Overview

(1)

Assumes

no

redemption

of

cash

in

trust

account

and

does

not

include

shares

underlying

Convertible

Preferred

Stock

or

outstanding

warrants,

other

than

the

1,212,500

shares

mentioned

above

(2)

See

“Important

Disclaimers”

for

information

regarding

FY

2015

estimated

information |

9

Sources and Uses

Note: Assumes no redemption of cash in trust

$

%

HCAC Cash

115

$

41%

Convertible Preferred Stock

40

14%

Reinvestment of Existing Stockholders' Equity

115

41%

Cash from Blue Bird's Balance Sheet

10

4%

Total Sources

280

$

100%

$

%

Cash Purchase Price

140

$

50%

Reinvestment of Existing Stockholders' Equity

115

41%

Transaction Expenses

25

9%

Total Uses

280

$

100%

Sources

Uses

($ in millions) |

Cash on Balance

Sheet 53

$

Total Debt (incl. Capital Leases)

223

$

Convertible Preferred Stock

40

Market Equity Capitalization

271

Total Capitalization

534

$

Pro Forma Enterprise Value

481

Pro Forma Ent. Value / FY2015E Adj. EBITDA

6.4 - 6.7x

Net Debt / FY2014 Adj. EBITDA

2.5x

10

Pro Forma Capitalization

(1)

(1)

Debt and cash balances as of September 27, 2014, pro forma for closing of

transaction. Assumes no redemption of cash in trust (2)

Market Equity Capitalization based on pro forma share count including issuance of

1,212,500 shares pursuant to the Warrant Exchange Offer and Sponsor Warrant Exchange and $10.00 per share price;

excludes shares underlying all other public and placement warrants

(3)

See “Important Disclaimers”

for information regarding FY 2015 estimated information

(4)

Net debt is defined as total debt ($223 million) less cash and cash equivalents ($53

million), or $170 million (2)

(4)

(3)

($ in millions) |

11

Pro Forma Ownership

(1)

Assumes no redemption of cash in trust account; figures per proxy statement

(2)

Based on an assumed conversion price of $11.75 per share, which may be adjusted from

time to time (3)

Share count assumes the issuance of 575,000 shares of Hennessy Capital common stock

pursuant to the Public Warrant Exchange Offer; excludes shares underlying all other public warrants

(4)

Share count assumes the Issuance of 637,500 shares of Hennessy Capital common stock

pursuant to the Sponsor Warrant Exchange; excludes shares underlying all other placement warrants

(amounts in millions)

Assumes No Conversion

of Preferred Stock

(1)

Assumes Conversion

of Preferred Stock

(1)(2)

Common

Stock

%

Common

Stock

%

Cerberus Affiliate

11.5

42.4%

11.5

37.7%

HCAC Public Stockholders

(3)

12.1

44.6%

12.1

39.6%

HCAC Founders

(4)

3.5

13.0%

3.5

11.5%

PIPE Investment Investor

0.0

0.0%

3.4

11.2%

Total

27.1

100.0%

30.5

100.0% |

Directors

Management and Board Experience

Age

Years

Blue Bird

Chan Galbato

Chairman

Cerberus Operations and Advisory Co. (CEO), Invensys (President, Controls Division), The

Home Depot (President, Services Division), Armstrong Floor Products (CEO)

Board: YP Holdings (Chairman), DynCorp, Steward Health Care

51

5

Daniel Hennessy

Vice Chairman

Hennessy Capital (Chairman & CEO), Code Hennessy & Simmons (Founding

Partner) Board: Thermon Group (Chairman), Dura-Line (Chairman)

57

--

Phil Horlock

President & CEO

Ford Motor Company (CFO Asia Pacific & Africa; Chairman & CEO Ford Motor Land

Development; Controller, Corporate Finance; Controller, Global Sales &

Marketing) Board: LoJack Corporation

58

5

Gurminder Bedi

Director

Ford Motor Company (VP of North America Truck)

Board: Compuware (Chairman), KEMET, Actuant

67

--

Kevin Charlton

Director

Hennessy Capital (President & COO), River Hollow Partners (Managing Partner),

Macquarie Capital (Managing Director), Investcorp (Managing Director)

Board: Spirit Realty, FleetPride

48

--

Dennis Donovan

Director

Cerberus Operations and Advisory Co. (Vice Chairman), The Home Depot (EVP HR),

Raytheon (SVP HR), GE

65

6

Dev Kapadia

Director

Cerberus Capital Management (Managing Director), The Carlyle Group

Board: Tower International

43

8

James Marcotuli

Director

Cerberus Operations and Advisory Co. (Senior Operating Executive), North American Bus

Industries (CEO), Lockheed Martin

55

1

Alan Schumacher

Director

American National Can (CFO)

Board: Federal Accounting Standards Advisory Board, Bluelinx, Evertec, Quality

Distribution, Noranda Aluminum Holding Corporation

67

6

12

The New Blue Bird Board of Directors |

13

Phil Horlock

President and CEO

Blue Bird |

Blue

Bird Highlights & Agenda 14

Iconic and Fastest Growing School Bus Brand

Bus sales volume (units) up more than 40% since 2010

North American market share up from 23% in 2010 to an estimate of 30-31% in

2014 Undisputed Leader in Alternative Fuel-Powered Bus Sales

Sold approximately 6x more alternative-fuel buses than all competitors combined

since 2010 Proprietary and class-leading propane buses with proven lower

cost per mile than diesel buses

Downside Risk Mitigation

Break-even volume (based on Adj. EBITDA) of 315 units per month in 2014 compared

with 400 in 2010

Strong liquidity and cash flow

Significant Upside Potential

Early stages of school bus industry rebound following trough in 2011

Only ~360 customers have purchased propane to date from potential of ~10,000

Present and future products focus on affordable and exclusive differentiation

Proven track record in reducing costs and growing bus and parts sales

Central and South America and Middle East are new-market growth

opportunities Experienced and committed management team that delivers

results Highlights

Why

Blue Bird

What

We’ve Done

Where

We’re Going

Agenda |

15

Why

Blue Bird

What

We’ve Done

Where

We’re Going

Why Blue Bird |

Experienced Management Team

16

Years

Name

Position

Key Prior Experience

Auto

Industry

Blue

Bird

Phil Horlock

President & Chief Executive Officer

37

5

Phil Tighe

Chief Financial Officer

38

2

John Kwapis

Chief Operating Officer

29

5

Dale Wendell

Chief Commercial Officer

38

3

Mike McCurdy

VP HR & External Affairs

15

15

Paul Yousif

VP Legal Affairs & Treasurer

14

7

Dave Whelan

SVP Supply Chain & Quality

12

12

Dennis Whitaker

VP Engineering

35

35

John McKowen

VP Manufacturing

18

8

Bill Landreth

VP Service Parts

40

1

Jeff Terlep

VP Marketing & Product Planning

22

New

Dean Coulson

VP International & Commercial Bus

17

12

Jeff Carpenter

VP North American Sales

30

30

Trey Jenkins

VP Alternative Fuels

22

5 |

Strong Reputation

Blue Bird is an iconic brand with a track record of innovation

17

Blue Bird is the school bus brand

most likely to be recommended

(1)

Singularly focused on building the

world’s finest school bus

Purpose-built chassis designed

exclusively for safe transportation of

school children

Passionate about safety, quality,

durability and serviceability

Innovation that leads to unique-and-

affordable features

Key Blue Bird Industry Innovations

All Steel-Body School Bus (1937)

All American Forward Engine (1948)

Rear Engine Chassis (1978)

First CNG School Bus (1991)

First Propane School Bus (1992)

First All-Electric School Bus (1994)

Type C on Unique School Bus Chassis (2003)

First OEM-Manufactured Propane Bus (2007)

Ford/Roush CleanTech Propane Bus (2012)

OEM-installed telematics (2014)

(1)

Source: VSA Partners Research 3/22/2013 (study commissioned by Blue Bird)

|

Product-Focused Company

Focus on translating market wants into sustainable growth

18

Full Product Range

Type A Buses

(Unconsolidated)

Aftermarket

6% Net Sales

(2014)

Specialty Buses

7% Net Sales

(2014)

Expansive & innovative product

cycle plans

Proven product development

process

Leader in alternative fuels

Exclusive engine offerings

Differentiated product features

Research-driven product

enhancements

Extensive aftersales service and

support

Type C Buses

65% Net Sales

(2014)

Type D Buses

22% Net Sales

(2014)

“Build the Best Bus” |

Product Leadership

Blue Bird viewed as the leader in four of the five top attributes

19

(1)

Checkmarks/Corp. Logo indicate leadership in category

Ranked in Order of

Importance

(1)

Blue

Bird

Competitor A

Competitor B

#1

Safety

--

--

#2 Quality, Reliability &

Durability

--

--

#3 Operating Costs

--

--

#4 Acquisition Cost

--

--

#5 How the Bus Drives

--

--

Source: Freedonia Custom Research, Inc. 9/4/2013 (study commissioned by Blue

Bird) |

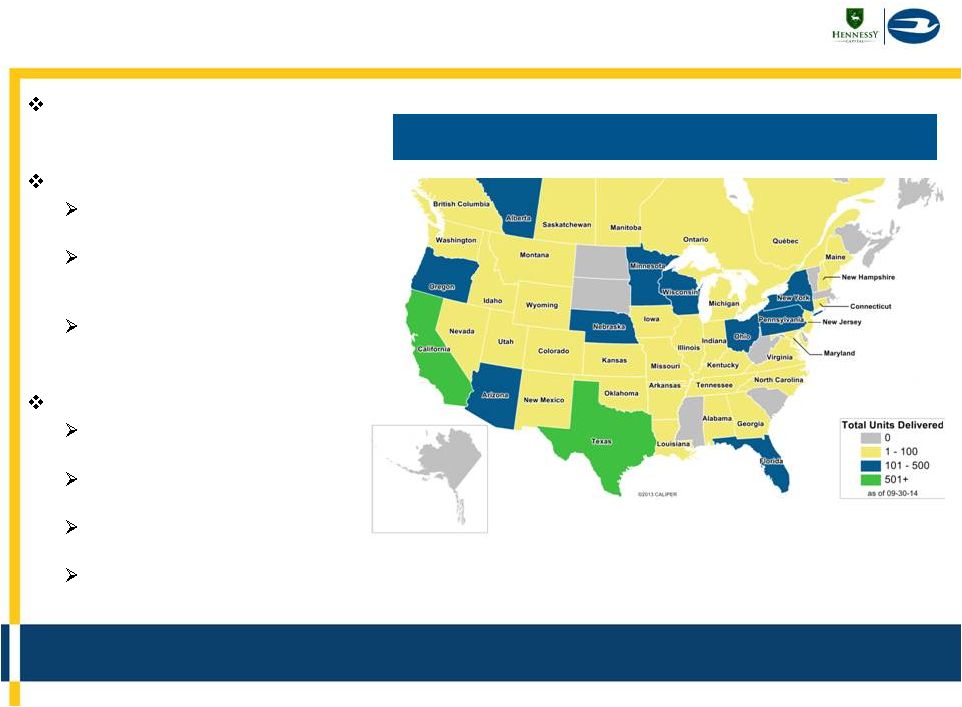

Strong Dealer Network

Customer base is diverse

20

Source: Blue Bird Management

Export

2%

~3,400

Contractors

21%

~10,000 School

Districts

67%

49 U.S. & Canadian

dealers address

~3,400 Contractors &

~10,000 Districts

Blue Bird

North American Dealer Network

GSA

5%

3 Nat’l Fleets

5%

Blue Bird

FY2014 Sales by Customer Type

Note: Many dealers have multiple locations

= Dealer Location

= Service Center |

Substantial production complexity

Stringent, industry-specific regulatory specifications

Unique customer requirements at both state and district

levels

~14,000 active production parts/bus

Average same-bus order less than 2 units

Labor-intensive production process with high employee

know-how

Significant capital and expertise required

Initial investment in facilities and tooling

Significant engineering to meet Federal and state

regulations

Development of an extensive distribution and service

channel with strong community ties

Conservative customers who demand proven products

Industry with High Barriers to Entry

Industry comprised of three material competitors since 2000

21 |

22

What We’ve Done

Why

Blue Bird

What

We’ve Done

Where

We’re Going |

Transformational Initiatives

Goal is sustained profitable growth

23

Reduced product cost and improved quality, cutting warranty claims by 39%

Operational

Commercial

2010

2009

2014

2013

2012

2011

Placed more than 85% of material purchases on long term contracts

Launched several leading and proprietary product features

Cut complexity by reducing body styles from 8 to 3

Increased productivity by reducing assembly plants from 2 to 1

Added 25% more capacity with 5-crew rolling shifts

Replaced 20% of dealer network

Institutionalized robust customer planning process with dealer body

Grew propane bus business with proprietary product offering

Started growing relationships with national fleets

Entered int’l business with Sigma bus for Bogota

Focused marketing on distinct product advantages

Formed JV with industry leader to design, produce and sell Type A bus

|

Propane Advantage

Blue Bird is the undisputed leader in propane bus sales

24

Blue Bird Propane Sales (units)

“With today's tight school budgets, using a

transportation fuel like propane autogas that saves

taxpayers' money, keeps the environment clean, and

keeps jobs within our national borders is a win-win

for everyone.”

-

William Schofield, Superintendent

Hall County Schools

Gainesville, GA

Blue Bird sold approximately ~6x more

alternative fuel buses than competitors

combined since 2010

Gained first mover advantage in propane

with introduction in 2007

Exclusive

relationships

with

both

Ford

and

Roush CleanTech

Adoption of propane-powered buses is

accelerating; run rate at about 20% of Blue

Bird's mix

Advantages are compelling

Lower fuel and maintenance costs

~$0.20 per mile less expensive than diesel

Better cold weather starting

Less greenhouse exhaust gases

Low cost fueling stations

Quieter and easy to drive

~1,900

Major fleet purchased

over 400 units from

bankrupt Atlantic

Express displacing

planned Blue Bird

propane purchases

430 unit

one-time

fleet order

2,033

1,476

524

426

356

FY2010

FY2011

FY2012

FY2013

FY2014

Cum. # of

Customers

Buying

Propane

118

146

193

281

359 |

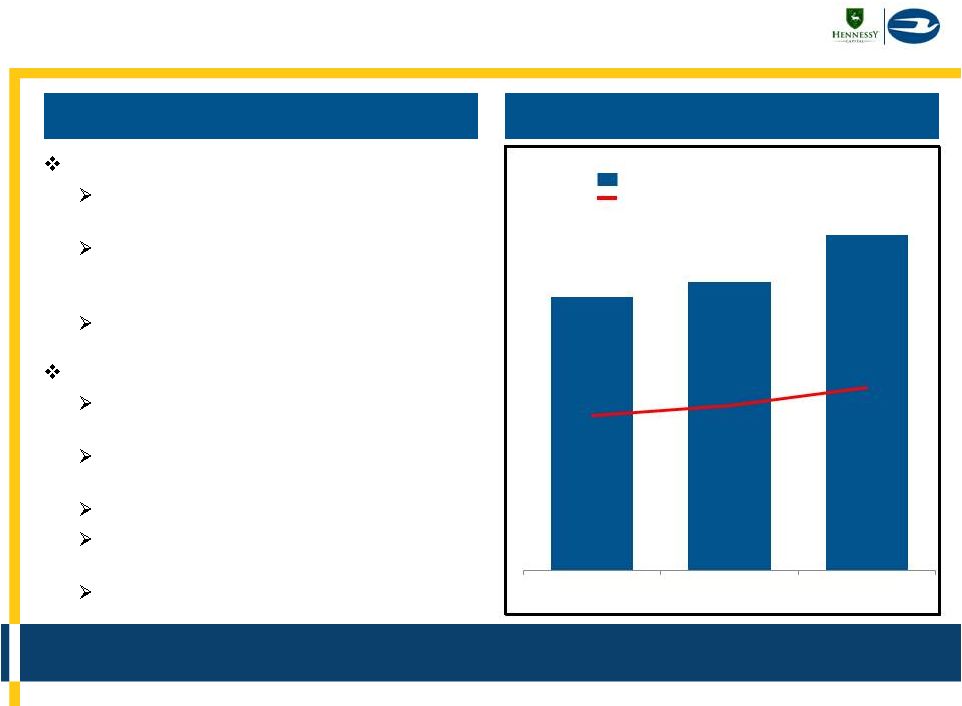

Strong Market Share and Profit Growth

Track record of winning and growing the business

Market Share

25

Actual

Actual

Estimate

Adj. EBITDA

Revenue

$566M

Revenue

$856M

Up 51%

($ in millions)

$14

$17

$50

$67

3%

3%

7%

8%

FY2011

FY2012

FY2013

FY2014

Adjusted EBITDA

% of Revenue

FY2011

FY2012

FY2013

FY2014

FY2010

23%

26%

27%

30%

30%-31% |

Why

Blue Bird

What

We’ve Done

Where

We’re Going

Where We’re Going

26 |

Future Growth & Profit Drivers

Build on track record of profitable growth

27

Industry Volume Upside

School Bus Market Recovery

New Markets & Products

International & Commercial Buses

Higher Operating Margins

Drive Productivity

Deliver Parts Growth

Market Share Growth

Increasing Propane Penetration

Continuous Product Enhancements

Dealer Network Improvements

Future

Growth &

Profitability

Long-Term Financial

Objective:

EBITDA 10%

of Sales |

Early

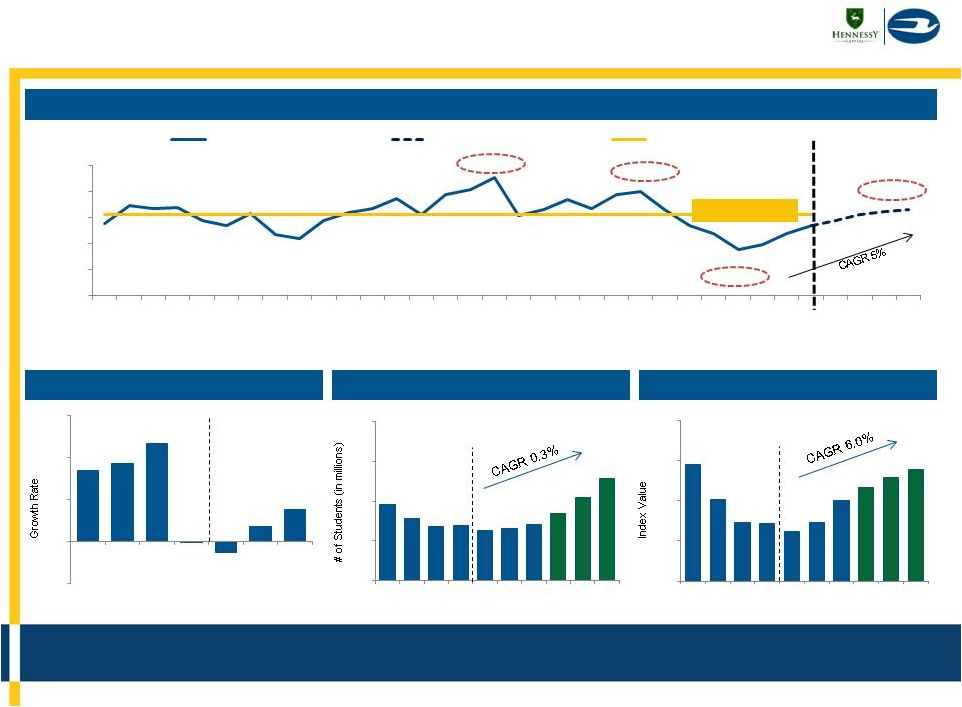

Stages of Industry Recovery Fundamentals support strong industry growth

28

U.S. Aggregate Housing Price Index

U.S. Total Student Enrollment

Source: National Center for Education Statistics

U.S. Property Tax Revenue Recovery

Type C/D School Bus Recovery

Source: U.S. Census Bureau

Source: CoreLogic House Price Index

Mean: 30,550

Source: Historical results are based on RL Polk vehicle registration data, and the

estimated 2014-2016 periods are based on Blue Bird management’s forecast model, which takes into account RL Polk vehicle

registration data, population of school age children forecasts from the National

Center for Education Statistics and bus ridership data collected and published by an industry magazine (School Transportation News)

37,641

34,882

23,822

31,600

15,000

20,000

25,000

30,000

35,000

40,000

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

Historical Registrations

Projected Registrations

Historical Avg. ('85-'14)

6.8%

7.4%

9.3%

0.0%

(1.0%)

1.4%

3.1%

(4.0%)

0.0%

4.0%

8.0%

12.0%

2007

2008

2009

2010

2011

2012

2013

55.2

55.0

54.8

54.9

54.8

54.8

54.9

55.1

55.3

55.6

54.0

54.6

55.3

55.9

56.5

2007

2008

2009

2010

2011

2012

2013

2014E

2015E

2016E

187.0

161.0

144.0

143.0

137.0

144.0

160.0

170.0

177.0

183.0

100.0

130.0

160.0

190.0

220.0

2007

2008

2009

2010

2011

2012

2013

2014E

2015E

2016E |

Propane competitiveness is increasing;

Lower diesel fuel costs potentially support higher bus sales

Fuel cost reductions have produced a greater

benefit for propane buses to date

The value proposition for propane buses relative

to diesel has improved considerably

Propane autogas pricing has decreased 47% over

the past year, while diesel has only decreased 20%

Lower propane prices could result in more

converts from diesel to propane

Oil price reductions may have a positive impact

on the school bus business

Fuel costs make up a large portion of school

transportation budgets

Lower fuel prices can translate into lower fuel

spending and budget favorability

Funds that were budgeted for fuel can potentially

be freed up for more school bus purchases

Some school districts enter longer term fuel

contracts that lock in prices over a period of time,

so these districts may not immediately benefit

from price reductions

29

Source

of

fuel

pricing:

www.eia.gov

January

2014

compared

to

January

2015

with

typical

propane

mark-up

over

terminal

price

of

$0.50

per

gallon

-20%

-47%

Diesel

Propane

2014

2015

2014

2015

Business Benefits from Lower Oil Prices

$1.90

$1.01

$3.89

$3.13 |

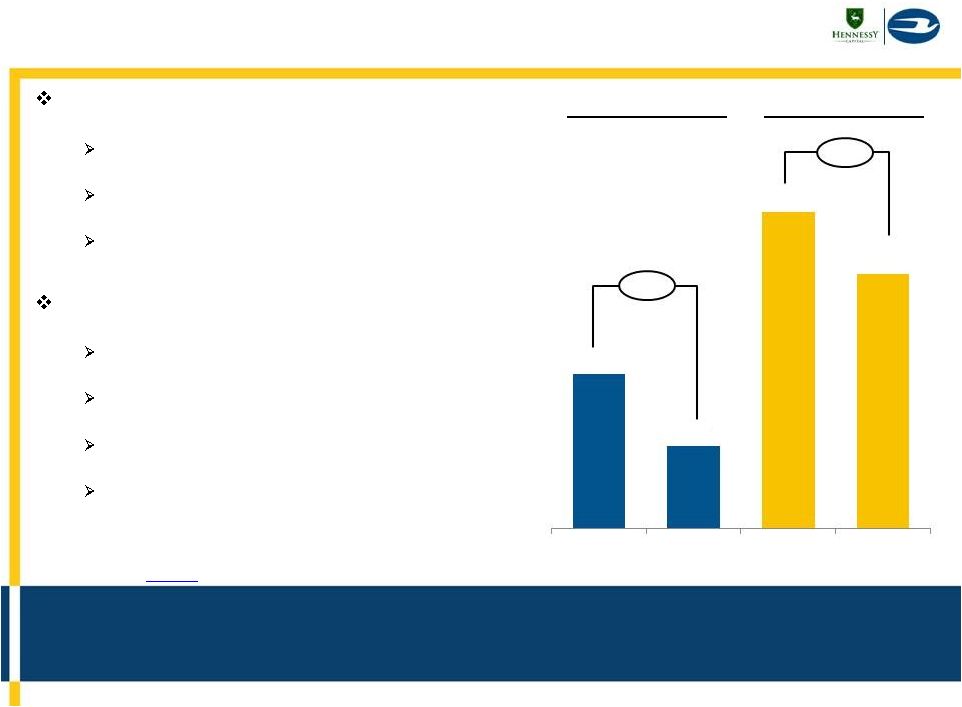

Share

Growth: Propane Opportunity Significant growth potential as many

districts test propane Propane is an effective conquest

tool that drives market share

growth

Early penetration of the market

Only ~360 of ~10,000

customers have tried propane

Customers that buy propane

buses are purchasing more

propane buses

Order sizes are growing as

existing customers come

back for more

Superior product offering

Exclusive contracts with Ford

and ROUSH CleanTech

Proven design with high

customer satisfaction

Only company offering an

extended-range fuel tank

Blue Bird is the undisputed

sales leader in this segment

30

Fewer than 4% of Customers Have Tried Propane |

Share

Growth: Product & Dealer Initiatives Focus on initiatives designed

to grow market share 31

Dealer network is strong and getting

stronger

Improve or replace underperforming

dealers

School bus focused dealerships

Using data to drive best practices

Enhanced marketing tools

Energized dealers will drive

increased sales penetration

Level of dealer engagement growing

New dealers that have replaced

underperforming dealers are

contributing to growth

Singular focus on buses

Purpose-built school bus chassis

Leading quality, reliability & durability

Outstanding warranty performance

Leadership in propane

Continue to enhance propane package

Leverage differentiators like exclusive

Ford/ROUSH relationship and industry’s

only extended-range propane fuel tank

Steady stream of new products and

industry-first innovations

OEM telematics pre-wiring through

exclusive partnership with Synovia

Industry-leading new E-Z windows

Proprietary powertrain offerings

Other differentiated products, features

and services in the pipeline

Dealer Network Improvements

Continuous Product Enhancements |

Margin Expansion: Productivity

Identified opportunities to continue enhancing margins

32

Lower Break-Even

Break-even volume (based on Adjusted

EBITDA) was 315 units per month in

2014; down from 400 units per month

in 2010

Continuous improvement

manufacturing mindset

Reduce overhead/unit

Increase labor productivity

Use and control of bulk materials

Reduce complexity

Highly skilled workforce with average

tenure of approximately 14 years

No significant capacity investments

required to support near-term growth

Note: Labor Productivity is Standard Hours per Bus divided by Actual Hours per

Bus 89%

96%

102%

106%

FY2011

FY2012

FY2013

FY2014

Labor Productivity |

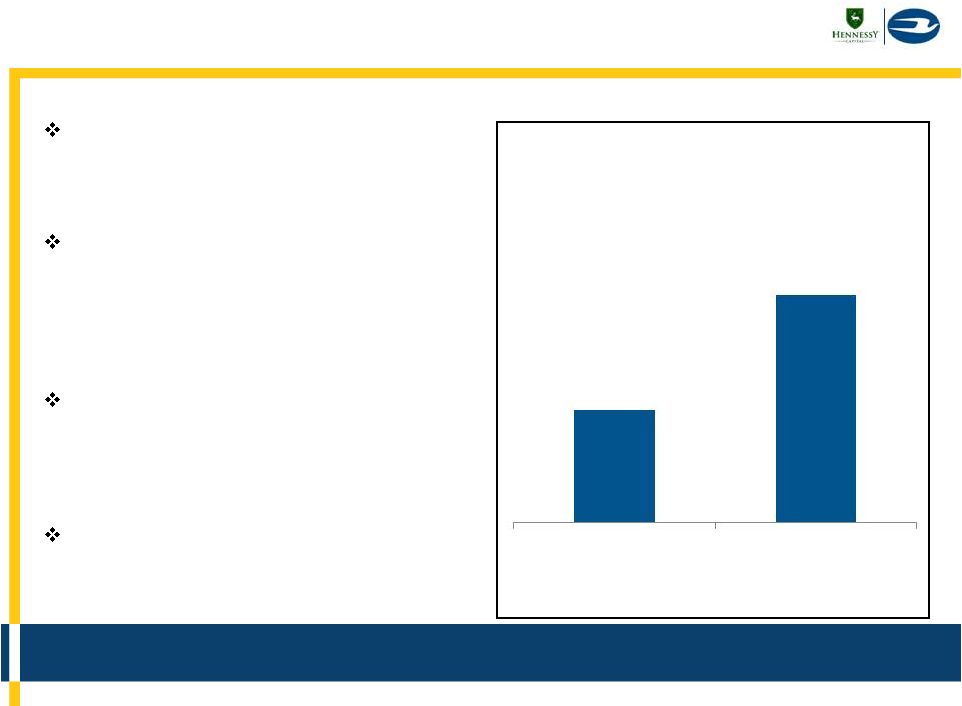

Margin Expansion: Growing Parts Business

Growth in Parts revenue will drive margin expansion

33

2014

Platform for growth

Installed base of ~180,000 buses in

North America

Blue Bird’s dealers maintain ~250

dealer-authorized service locations

across North America

New and experienced leadership

Focus of organic growth

Direct sales to dealer-authorized

service centers

Increased focus on best practices

deployment

Electronic parts catalog

Increased merchandising of high

volume parts

Direct marketing to end-customers

Parts Sales Outlook

Parts Sales Revenue & Gross Margin

Revenue

Gross Profit Margin

($ in millions)

$44

$46

$54

FY2012

FY2013

FY2014

35%

36%

37% |

New

Markets & Growth Beyond School Buses Will continually explore and pursue

new growth opportunities Continue to grow Sigma Bus sales in Colombia and

expand to other markets

Continue to be preferred vehicle choice for General

Services Administration (GSA)

Grow international Type C & D bus sales through

Bukkehave distributor

Expand commercial bus business in North America

Explore school bus sales opportunities in the Middle

East

Explore long-term service and vehicle refurbishment

contracts

34 |

35

Phil Tighe

CFO

Blue Bird |

Substantial Revenue Growth

Consistently driven volume and revenue growth

36

$566

$598

$777

$856

(1) Total does not sum precisely due to rounding

(1)

$80

$80

$84

Memo:

Revenue/Unit

$84

($ in thousands)

($ in millions)

$522

$554

$730

$802

$44

$44

$46

$54

6,525

6,882

8,654

9,604

FY2011

FY2012

FY2013

FY2014

Bus

Parts

Volume |

Impressive Profit Growth

EBITDA has grown at a faster rate than revenue

37

Note: Numbers have been rounded

9%

9%

12%

Memo:

GP Margin

13%

($ in millions)

$

$17

$50

$67

3%

3%

7%

8%

FY2011

FY2012

FY2013

FY2014

Adjusted EBITDA

% of Revenue

14 |

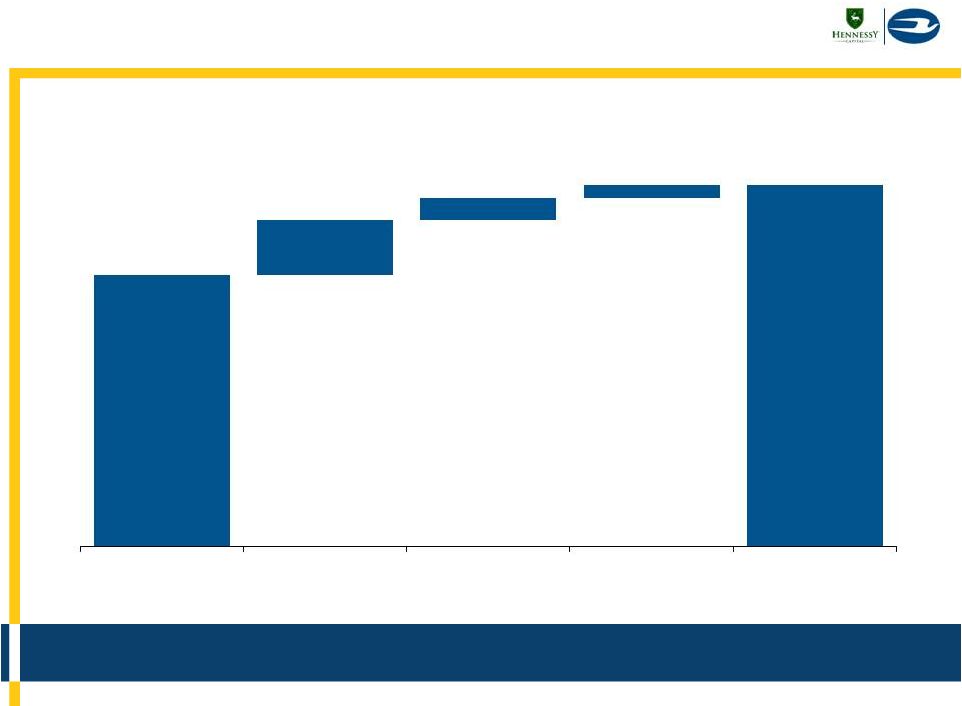

Profit Drivers: FY2012 to FY2014

Relentless focus on cost competitiveness

allows us to compete in all markets

38

Note: Total Adj. EBITDA walk does not sum precisely due to rounding

($ in millions)

$17

$67

$(1)

$21

$29

FY2012

Adj. EBITDA

Cost Reductions

Volume & Mix

Other

FY2014

Adj. EBITDA |

Profit Drivers: FY2013 to FY2014

Continuous improvements from cost reductions and mix

39

($ in millions)

$67

$3

$10

$4

$50

FY2013

Adj. EBITDA

Cost Reductions

Volume & Mix

Other

FY2014

Adj. EBITDA |

Substantial Free Cash Flow

Strong free cash flow enables optionality

40

(1)

FY2014 Free Cash Flow includes a $24.7 million special compensation payment related

to Blue Bird’s 2014 dividend recapitalization but is not pro forma for interest expense associated with new debt raised nor

future cash taxes

$5

$4

$5

Memo: Capex

$6

($ in millions)

(1)

$15

$12

$31

$32

FY2011

FY2012

FY2013

FY2014

Free Cash Flow

Source: Blue Bird Management

Notes: Free Cash Flow is defined as Cash from Continuing Operations less Capex.

|

School Bus Business is Highly Seasonal

Seasonality drives higher revenue and earnings in Second Half

R.L. Polk Unit

Registration Seasonality

Based on 3-Year Average

FY2012-FY2014

41

School districts typically purchase

buses for the start of the school

year, driving higher volumes in April

through September

Blue Bird’s quarterly financial

results are impacted by these

seasonal practices; the first fiscal

quarter is the most impacted and we

take planned shutdowns during this

period

Working capital is typically a

significant use of cash during the

first fiscal quarter and a significant

source of cash in the fourth fiscal

quarter

Blue Bird generally operates with

negative working capital

33%

67%

Oct -

Mar

(First Half)

Apr -

Sep

(Second Half) |

Flexible Capital Structure

42

Pro Forma Capital Structure (9/27/14)

Considerations

Undrawn Revolving Credit Facility

with $60 million of availability

supports working capital

seasonality

Convertible Preferred Stock

dividends are payable in stock or

cash, at the Company’s option

Pension plan has been frozen

since 2006

Pension liability of $40.9 million as

of September 27, 2014

$5.7 million projected 2015E pension

cash contribution

(1)

Reflects $12.1 million of unamortized discount

(2)

Net Debt is defined as Total Debt less Cash and Cash Equivalents

(3)

Liquidity is defined as Cash and Cash Equivalents plus $60 million of availability

under revolving credit facility less $5.3 million of outstanding letters of credit

(4)

Based on FY2014 Adj. EBITDA of $66.8 million

(5)

Reflects $17.0 million of pro forma net interest expense for full-year 2014

assuming approximately $222 million of debt at June 28, 2014 was outstanding as of September 29, 2013

($ in millions)

Cash and Cash Equivalents

$53.0

Revolving Credit Facility

$0.0

Term Loan Facility

(1)

222.9

Total Debt

$222.9

Net Debt

(2)

169.9

Memo:

Liquidity

(3)

$107.7

Convertible Preferred Stock

40.0

Capital Leases

0.2

Metrics based FY2014 Financials

(4)

Total Debt / Adj. EBITDA

3.3x

Net Debt / Adj. EBITDA

2.5x

Adj. EBITDA / PF Net Interest

(5)

3.9x |

43

Phil Horlock

President and CEO

Blue Bird |

Summary: Significant Momentum & Upside

Led by an Experienced and Committed

Management Team that Delivers Results

Iconic and Fastest Growing School Bus Brand

Undisputed Leader in Alternative Fuel-Powered Bus Sales

Downside Risk Mitigation

Significant Upside Potential

44 |

2015

Guidance EBITDA projected to grow 7-12% in FY2015

45

Revenue

$918–$940

Revenue

$856

(1)

Adj. EBITDA

($ in millions)

(1)

See

“Important

Disclaimers”

for

information

regarding

FY

2015

estimated

information

$67

$72 -

$75

FY2014

FY2015

Guidance

Up

7%-12%

Up

7%-10%

Range

Source: Blue Bird Management

Note:

Adjusted

EBITDA

excludes

public

company

costs,

stock

based

compensation,

amounts

payable

under

the

Blue

Bird

Phantom

Award

Plan,

and

transaction

expenses |

Our

Growth Objectives are Clear Deliver sustained growth and profitability

#1 in North American school bus market

share with highest customer loyalty

Differentiated and proprietary products and

features that customers want and value

Clear leader in affordable, alternative fuel-

powered school buses

Significant growth in parts sales

Significant and ongoing international

business

Growing presence in commercial bus

business

46 |

47

Appendix |

Public Company Valuation Benchmarks

FY 2014 EV / EBITDA

FY 2015 EV / EBITDA

Deal Multiple: 7.2x

Deal

Multiple

Range:

6.4

–

6.7x

Mean: 10.8x

Large Cap Branded Industrials

& Specialty Vehicles

Mean: 9.7x

Mean: 9.8x

Mean: 9.1x

Small Cap Branded Industrials

& Specialty Vehicles

Large Cap Branded Industrials

& Specialty Vehicles

Small Cap Branded Industrials

& Specialty Vehicles

24.3x

(1)

(1)

(1)

Deal Multiple calculated as Pro Forma Enterprise Value of $481 million (assuming

issuance of 1,212,500 shares pursuant to the Warrant Exchange Offer and Sponsor Warrant Exchange and no conversion of

Convertible Preferred Stock) divided by Adjusted EBITDA of $67 million for FY2014

and $72 to $75 million for FY2015E (2)

FY2014

multiples

for

Power

Solutions

International,

Inc.

are

not

included

in

mean

and

median

calculations

10.9x

12.8x

12.4x

7.1x

12.7x

9.6x

10.4x

9.7x

10.2x

11.9x

9.6x

8.3x

8.4x

10.0x

5.0x

10.0x

15.0x

8.3x

11.8x

11.5x

6.7x

12.3x

7.7x

10.2x

8.1x

8.7x

9.3x

7.6x

14.3x

7.5x

11.7x

5.9x

5.0x

10.0x

15.0x

Source: SEC Filings, Wall Street Research and First Call Consensus estimates. Blue

Bird company management Note: Multiples exclude Pension Liability from the

calculation of Enterprise Value; multiples have been calendarized to Blue Bird September fiscal year end. Quarterly consensus was used for comparable

companies wherever available

Note: Adj. EBITDA excludes public company costs, stock based compensation and

transaction expenses. Adjusted EBITDA for FY2014 includes add-backs for Restructuring costs, Non-recurring Management

Incentive Compensation and other non-recurring expenses

48 |

Detailed Comparable Company Benchmarks

49

($ in millions, except per share values)

Source: SEC Filings, Wall Street Research and First Call Consensus estimates

Note: N.M. represents negative multiples, EBITDA multiples greater than 35.0x, EBIT

multiples greater than 25.0x, P/E multiples greater than 65.0x and negative long-term growth rates

Note: Multiples have been calendarized to Blue Bird September fiscal year end.

Quarterly consensus was used for comparable companies wherever available

(1)

FY 2014 multiples for Power Solutions International, Inc. are not included in mean

and median calculations (1)

Stock Price

Market Value

Balance Sheet

Valuation Multiples

Large Cap Branded Industrials

Above

Below

Equity

Ent.

EV / Rev

EV / EBITDA

EV / EBIT

P/E

Price/

& Specialty Vehicles

1/2/15

Low

High

Value

Value

Cash

Debt

FY13

FY14

FY15

FY13

FY14

FY15

FY13

FY14

FY15

FY13

FY14

FY15

Book

Cummins Inc.

146.42

19%

9%

26,663

26,320

2,381

2,038

1.5x

1.4x

1.3x

12.4x

10.9x

8.3x

15.2x

13.3x

9.5x

18.8x

17.0x

14.0x

3.4x

Harley-Davidson, Inc.

65.79

21%

11%

14,193

18,949

688

5,444

3.6x

3.4x

3.2x

14.5x

12.8x

11.8x

16.5x

14.5x

13.5x

19.5x

16.8x

15.5x

4.3x

Allison Transmission Holdings, Inc.

33.85

29%

2%

6,170

8,560

208

2,597

4.5x

4.1x

4.0x

14.7x

12.4x

11.5x

23.5x

17.3x

15.9x

46.2x

27.9x

23.6x

4.6x

Oshkosh Corporation

48.31

22%

20%

3,807

4,388

314

895

0.6x

0.6x

0.7x

6.9x

7.1x

6.7x

8.5x

8.7x

8.5x

11.4x

12.3x

11.8x

1.9x

Generac Holdings Inc.

46.37

20%

26%

3,313

4,252

173

1,112

2.9x

3.0x

2.9x

11.6x

12.7x

12.3x

13.0x

14.1x

12.6x

11.6x

13.6x

13.9x

7.4x

Thor Industries Inc.

55.48

15%

14%

2,962

2,649

314

0

0.8x

0.7x

0.7x

10.4x

9.6x

7.7x

11.5x

10.6x

8.8x

18.5x

16.6x

14.3x

3.0x

The Manitowoc Company, Inc.

21.88

35%

35%

3,006

4,687

75

1,755

1.2x

1.2x

1.2x

10.0x

10.4x

10.2x

12.9x

13.4x

13.4x

18.7x

16.2x

15.9x

3.4x

Mean

2.2x

2.1x

2.0x

11.5x

10.8x

9.8x

14.4x

13.1x

11.7x

20.7x

17.2x

15.6x

4.0x

Median

1.5x

1.4x

1.3x

11.6x

10.9x

10.2x

13.0x

13.4x

12.6x

18.7x

16.6x

14.3x

3.4x

Stock Price

Market Value

Balance Sheet

Valuation Multiples

Small Cap Branded Industrials

Above

Below

Equity

Ent.

EV / Rev

EV / EBITDA

EV / EBIT

P/E

Price/

& Specialty Vehicles

1/2/15

Low

High

Value

Value

Cash

Debt

FY13

FY14

FY15

FY13

FY14

FY15

FY13

FY14

FY15

FY13

FY14

FY15

Book

Briggs & Stratton Corporation

20.27

18%

12%

920

1,083

62

226

0.6x

0.6x

0.6x

8.8x

9.7x

8.1x

15.7x

16.2x

10.6x

22.0x

19.9x

17.5x

1.5x

Federal Signal Corp.

15.34

33%

4%

974

1,014

29

69

1.2x

1.2x

1.1x

13.3x

10.2x

8.7x

16.3x

12.0x

10.1x

22.0x

15.8x

15.0x

2.6x

Astec Industries, Inc.

38.73

13%

16%

888

885

16

13

0.9x

0.9x

0.9x

9.5x

11.9x

9.3x

16.7x

17.6x

12.5x

24.6x

25.9x

18.6x

1.5x

New Flyer Industries Inc.

11.44

30%

5%

641

884

9

252

0.9x

0.6x

0.6x

14.2x

9.6x

7.6x

N.M.

14.9x

12.9x

37.8x

17.2x

15.8x

1.4x

Power Solutions International, Inc.

51.55

18%

42%

553

624

8

78

2.7x

2.0x

1.4x

N.M.

24.3x

14.3x

N.M.

N.M.

15.9x

63.0x

42.4x

23.6x

6.7x

Winnebago Industries, Inc.

21.90

8%

24%

590

562

28

0

0.7x

0.6x

0.6x

11.4x

8.3x

7.5x

12.6x

8.9x

8.0x

18.5x

13.1x

12.3x

3.0x

Douglas Dynamics, Inc.

21.34

51%

14%

476

616

4

144

4.1x

2.2x

2.2x

24.3x

8.4x

11.7x

N.M.

9.5x

12.6x

N.M.

13.6x

20.0x

2.8x

Manitex International, Inc.

12.60

33%

29%

174

224

5

55

0.9x

0.9x

0.6x

11.3x

10.0x

5.9x

14.2x

12.8x

7.7x

18.9x

18.1x

12.2x

1.9x

Mean

1.5x

1.0x

1.0x

13.3x

9.7x

9.1x

15.1x

13.1x

11.3x

29.5x

17.7x

16.9x

2.7x

Median

0.9x

0.9x

0.7x

11.4x

9.7x

8.4x

15.7x

12.8x

11.5x

22.0x

17.2x

16.6x

2.2x |

Detailed Comparable Company Benchmarks

50

($ in millions)

Source: SEC Filings, Wall Street Research and First Call Consensus estimates

Note: N.M. represents negative multiples, EBITDA multiples greater than 35.0x, EBIT

multiples greater than 25.0x, P/E multiples greater than 65.0x and negative long-term growth rates

Note: Financials have been calendarized to Blue Bird September fiscal year

end. Quarterly consensus was used for comparable companies wherever available

Revenue

Revenue Growth

Margin Analysis

Large Cap Branded Industrials

EBITDA

EBIT

Net Income

& Specialty Vehicles

FY13

FY14

FY15

FY13

FY14

FY15

FY13

FY14

FY15

FY14

FY15

FY13

FY14

FY15

Cummins Inc.

$17,005

$18,719

$20,503

(2%)

10.1%

9.5%

12.5%

12.9%

15.5%

10.6%

13.5%

8.3%

8.4%

9.3%

Harley-Davidson, Inc.

5,237

5,569

5,915

(6%)

6.3%

6.2%

25.0%

26.6%

27.2%

23.4%

23.7%

13.9%

15.2%

15.5%

Allison Transmission Holdings, Inc.

1,923

2,074

2,163

(10%)

7.9%

4.3%

30.3%

33.2%

34.5%

23.8%

24.9%

7.0%

10.7%

12.1%

Oshkosh Corporation

7,665

6,808

6,495

(4%)

(11.2%)

(4.6%)

8.3%

9.1%

10.1%

7.4%

8.0%

4.3%

4.5%

5.0%

Generac Holdings Inc.

1,452

1,433

1,457

23%

(1.3%)

1.7%

25.3%

23.4%

23.7%

21.0%

23.2%

19.6%

17.0%

16.3%

Thor Industries Inc.

3,280

3,647

4,021

19%

11.2%

10.2%

7.8%

7.6%

8.5%

6.9%

7.5%

4.9%

4.9%

5.1%

The Manitowoc Company, Inc.

4,061

3,938

4,027

4%

(3.0%)

2.3%

11.6%

11.4%

11.4%

8.9%

8.7%

4.0%

4.7%

4.7%

Mean

3%

2.9%

4.2%

17.3%

17.7%

18.7%

14.6%

15.7%

8.9%

9.3%

9.7%

Median

(2%)

6.3%

4.3%

12.5%

12.9%

15.5%

10.6%

13.5%

7.0%

8.4%

9.3%

Revenue

Revenue Growth

Margin Analysis

Small Cap Branded Industrials

EBITDA

EBIT

Net Income

& Specialty Vehicles

FY13

FY14

FY15

FY13

FY14

FY15

FY13

FY14

FY15

FY14

FY15

FY13

FY14

FY15

Briggs & Stratton Corporation

1,871

1,834

1,955

(5%)

(1.9%)

6.6%

6.6%

6.1%

6.9%

3.6%

5.2%

2.2%

2.5%

2.7%

Federal Signal Corp.

849

874

949

6%

2.9%

8.7%

9.0%

11.4%

12.3%

9.7%

10.5%

5.2%

7.1%

6.8%

Astec Industries, Inc.

937

960

1,026

0%

2.5%

6.9%

9.9%

7.7%

9.3%

5.2%

6.9%

3.9%

3.6%

4.6%

New Flyer Industries Inc.

1,020

1,406

1,514

18%

37.7%

7.7%

6.1%

6.6%

7.6%

4.2%

4.5%

1.7%

2.6%

2.7%

Power Solutions International, Inc.

229

306

449

13%

33.6%

47.1%

6.8%

8.4%

9.7%

7.2%

8.7%

3.8%

4.3%

5.2%

Winnebago Industries, Inc.

803

945

1,018

25%

17.7%

7.7%

6.1%

7.1%

7.3%

6.7%

6.9%

4.0%

4.8%

4.7%

Douglas Dynamics, Inc.

150

276

286

7%

84.9%

3.4%

16.9%

26.6%

18.5%

23.3%

17.1%

1.6%

12.7%

8.3%

Manitex International, Inc.

236

263

383

15%

11.2%

46.0%

8.4%

8.5%

9.8%

6.7%

7.6%

3.9%

3.7%

3.7%

Mean

10%

23.6%

16.8%

8.7%

10.3%

10.2%

8.3%

8.4%

3.3%

5.1%

4.9%

Median

10%

14.4%

7.7%

7.6%

8.1%

9.5%

6.7%

7.2%

3.8%

4.0%

4.7% |

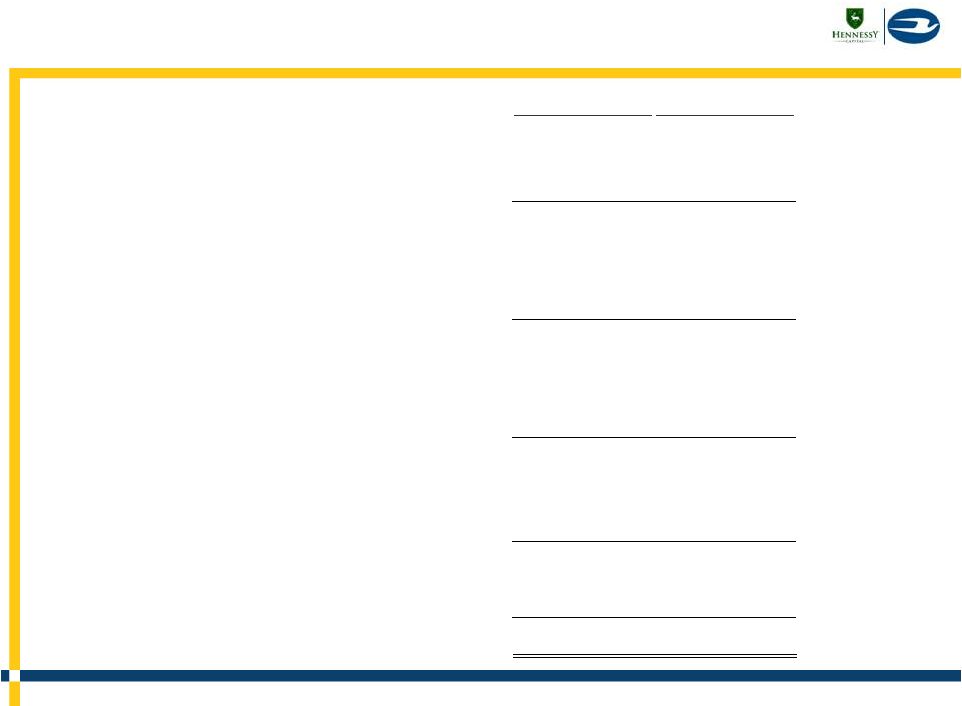

51

Blue Bird GAAP/Non-GAAP Reconciliation

(1)

Restructuring

costs

include

expenses

related

to

discontinued

operations

from

the

sale

of

a

business,

management

severance

costs,

a

write-off

of

leasing

software,

certain

plant

assets

and

a

write-down

on

a

note outstanding to a former related party for furniture and fixtures in Blue Bird's

Ohio facility (2)

In fiscal 2011, Blue Bird wrote-off $2.7 million of inventory purchased in

anticipation of orders from a foreign government that were never placed. In fiscal 2012, Blue Bird recorded a partial recovery of the

write-down as proceeds were received from sales of the inventory as scrap

(3)

Represents a payment made under Blue Bird's Phantom Award Plan to Phantom Plan

Participants in connection with Blue Bird's 2014 dividend recapitalization

(4)

Represents the add-back of an out-of-period vacation pay and holiday

bonus expense resulting from a change in policy to accrue throughout the year instead of expensing annually

(5)

Represents incentive compensation paid to officers in excess of a related accrual

(typically recorded at 100% target level) due to over-performance relative to budget. This adjustment excludes the amount of

the accrual above 200% of the target level

(6)

Represents a write-off due to an order for chassis with respect to which the

customer never took delivery of the chassis. The units that were not used or sold to other customers were written off

(7)

Represents costs incurred in redesigning Blue Bird's Type D bus in fiscal 2012. The

costs associated with this redesign related to prototypes, testing and services, engineering personnel, marketing and

consulting fees

(8)

Represents costs incurred in exploring the market potential for sales of school

buses in Asia. The costs related to this market test included sales and marketing expenses, travel, demonstration units and

professional services fees

(9)

Represents the allocated tax expense related to Blue Bird's non-consolidated

affiliate (10)

Represents expenses incurred by School Bus Holdings related to the Business

Combination (11)

Represents out-of-period cost of goods sold incurred by Blue Bird. See Note

1 to Blue Bird's audited consolidated financial statements in the proxy statement

($ in thousands)

Year Ended

Net Income to Adjusted EBITDA Reconciliation

October 1, 2011

September 29, 2012

September 28, 2013

September 27, 2014

Net income

(loss)

($5,224)

($2,998)

$54,208

$2,757

Loss (income) from discontinued operations, net of tax

1,625

328

159

(42)

Income from continuing operations

($3,599)

($2,670)

$54,367

$2,715

Interest expense

2,471

2,480

2,371

6,156

Interest income

(282)

(160)

(214)

(102)

Income tax expense (benefit)

(1,126)

429

(30,380)

10,076

Depreciation and amortization

12,855

13,194

11,808

9,898

Restructuring costs

(1)

1,382

1,946

258

—

Export inventory adjustment

(2)

2,721

(234)

—

—

Special compensation payment

(3)

—

—

—

24,679

Vacation pay adjustment

(4)

—

—

2,296

—

Management incentive compensation

(5)

—

—

5,638

3,271

Chassis write-off

(6)

—

—

1,196

—

Type D redesign

(7)

—

1,207

—

—

Asia market test

(8)

—

885

—

—

Tax expense, non-consolidated affiliate

(9)

—

—

2,836

365

Business combination

(10)

—

—

—

9,236

Out-of-period adjustment

(11)

—

—

—

407

Adjusted EBITDA

$14,422

$17,077

$50,176

$66,791

Adjusted EBITDA margin

2.5%

2.9%

6.5%

7.8% |

52

Blue Bird Income Statement

(1)

(2)

($ in thousands, except per share values)

Year Ended

September 29, 2012

September 28, 2013

September 27, 2014

Net sales

$598,330

$776,558

$855,735

Cost of goods sold

542,086

684,109

746,362

Gross profit

$56,244

$92,449

$109,373

Operating expenses

Selling, general and administrative expenses

57,418

65,332

91,445

Operating profit (loss)

($1,174)

$27,117

$17,928

Interest expense

(2,480)

(2,371)

(6,156)

Interest income

160

214

102

Other income (expense), net

9

96

72

Income (loss) before income taxes

($3,485)

$25,056

$11,946

Income tax (expense) benefit

(429)

30,380

(10,076)

Equity in net income (loss) of non-consolidated affiliates, net of tax

1,244

(1,069)

845

Income (loss) from continued operations

($2,670)

$54,367

$2,715

Income (loss) from discontinued operations, net of tax

(328)

(159)

42

Net income (loss)

($2,998)

$54,208

$2,757

Defined benefit pension plan (loss) gain

(3)

(7,804)

10,196

(4,150)

Comprehensive income (loss)

($10,802)

$64,404

($1,393)

Weighted average shares outstanding, basic and diluted

100

100

100

Basic and diluted income (loss) per share

Income (loss) from continuing operations

($26,695)

$543,672

$27,152

Income (loss) from discontinuing operations

(3,281)

(1,594)

425

(1)

This income tax benefit resulted primarily from a reduction in valuation reserves

established in prior periods. See Note 11 to Blue Bird’s audited consolidated financial statements in the proxy statement

(2)

Includes

$24.7

million

(approximately

$16.1

million

net

of

tax)

in

special

compensation

payments

related

to

Blue

Bird’s

2014

dividend

recapitalization

and

$9.3

million

(approximately

$7.4

million

net

of

tax)

of

expenses associated with the Business Combination

(3)

Net of tax of $0, $5,709 and $2,036 in 2012, 2013 and 2014 respectively

|

53

Blue Bird Balance Sheet

($ in thousands)

September 28, 2013

September 27, 2014

ASSETS

Cash and cash equivalents

$46,594

$61,137

Accounts receivables, net.

13,493

21,215

Inventories

62,603

71,300

Other current assets

3,125

4,353

Deferred tax asset

3,030

6,057

Total current assets

$128,845

$164,062

Property, plant and equipment, net

31,938

29,949

Goodwill

18,825

18,825

Intangible assets, net

64,103

62,240

Equity investment in affiliate

8,661

9,871

Deferred tax asset

8,001

4,073

Restricted cash

1,206

—

Other assets

1,406

2,912

Total assets

$262,985

$291,932

LIABILITIES AND STOCKHOLDERS’ EQUITY

Accounts payable

$72,960

$94,294

Accrued warranty costs - current portion

5,917

6,594

Accrued expenses

25,133

37,319

Deferred warranty income - current portion

3,767

4,117

Other current liabilities

3,020

5,668

Current portion of senior term debt.

2,979

11,750

Total current liabilities

$113,776

$159,742

Revolving senior credit facility

71

—

Long-term term debt

10,009

211,118

Accrued warranty costs

7,530

8,965

Deferred warranty income

6,976

7,886

Other liabilities

7,502

12,136

Accrued pension liability

37,703

40,881

Total long-term liabilities

$69,791

$280,986

Common stock

1

1

Additional paid-in capital

94,999

—

Retained (deficit) earnings

26,836

(102,229)

Accumulated other comprehensive loss

(42,418)

(46,568)

Total stockholder's (deficit) equity

$79,418

($148,796)

Total liabilities and stockholder's (deficit) equity

$262,985

$291,932 |

54

Blue Bird Statement of Cash Flows

Year Ended

September 29, 2012

September 28, 2013

September 27, 2014

Cash flows from operating activities

Net income

(loss)

($2,998)

$54,208

$2,757

(Income) loss from discontinued operations, net of

tax

328

159

(42)

Adjustments to reconcile net income (loss) to net cash provided by operating activities

Depreciation and

amortization

13,194

11,808

9,898

Amortization of debt

costs

210

128

1,301

Equity in net income of

affiliate

(1,244)

1,069

(845)

Impairment loss on fixed

assets

117

—

—

(Gain) loss on disposal of fixed

assets

285

36

(67)

Loss on sale of assets held for

sale

688

—

—

Deferred

taxes

375

(30,447)

2,874

Change in uncertain tax

position

—

—

6,390

Provision for bad

debt

193

21

(9)

Non-cash interest

expense

1,473

1,398

—

Amortization of deferred actuarial pension

losses

3,392

4,233

2,804

Changes in assets and

liabilities

Accounts

receivable

83

(4,178)

(7,713)

Inventories

(4,750)

(7,244)

(8,697)

Other

assets

159

1,315

(1,415)

Accounts

payable

10,059

6,889

18,080

Accrued expenses, pension and other

liabilities

(6,064)

(3,414)

12,096

Total

adjustments

$18,170

($18,386)

$34,697

Net cash provided by continuing

operations 15,500

35,981

37,412

Net cash used in discontinued

operations

(678)

(661)

(568)

Total cash provided by operating

activities $14,822

$35,320

$36,844

Cash flows from investing activities

Change in net investment in discounted

leases

863

563

778

Cash paid for fixed

assets

(3,659)

(4,945)

(5,535)

Proceeds from sale of

assets

2,077

—

102

Restricted

cash

—

—

1,206

Total cash used in investing

activities

($719)

($4,382)

($3,449)

Cash flows from financing activities

Borrowings under the senior credit

facility

10,868

63,743

2,862

Payments under the senior credit

facility

(10,938)

(63,672)

(2,933)

Borrowings under the senior term

loan

—

12,988

235,000

Repayments under the subordinated term

loans

(5,000)

(35,000)

(13,000)

Cash paid for capital

leases

(855)

(907)

(535)

Cash paid for debt

costs

(100)

(111)

(12,647)

Cash paid for

dividends

—

—

(226,821)

Change in advances collateralized by discounted

leases

(863)

(563)

(778)

Total cash used in financing

activities

($6,888)

($23,522)

($18,852)

Change in cash and cash

equivalents

7,215

7,416

14,543

Cash and cash equivalents at beginning of

period

31,963

39,178

46,594

Cash and cash equivalents at end of

year

$39,178

$46,594

$61,137

($ in thousands) |