Attached files

| file | filename |

|---|---|

| EX-21 - EX-21 - PENFORD CORP | d781083dex21.htm |

| EX-23 - EX-23 - PENFORD CORP | d781083dex23.htm |

| EX-31.1 - EX-31.1 - PENFORD CORP | d781083dex311.htm |

| EX-32 - EX-32 - PENFORD CORP | d781083dex32.htm |

| EX-24 - EX-24 - PENFORD CORP | d781083dex24.htm |

| EXCEL - IDEA: XBRL DOCUMENT - PENFORD CORP | Financial_Report.xls |

| EX-31.2 - EX-31.2 - PENFORD CORP | d781083dex312.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended August 31, 2014

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 0-11488

Penford Corporation

(Exact name of registrant as specified in its charter)

| Washington | 91-1221360 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 7094 S. Revere Parkway Centennial, Colorado |

80112-3932 | |

| (Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (303) 649-1900

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Stock, $1.00 par value | The NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for at least the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “accelerated filer” and “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one).

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the Registrant’s Common Stock held by non-affiliates of the Registrant as of February 28, 2014, the last business day of the Registrant’s second quarter of fiscal 2014, was approximately $160.1 million based upon the last sale price reported for such date on The NASDAQ Global Market. For purposes of making this calculation, Registrant has assumed that all the outstanding shares were held by non-affiliates, except for shares held by Registrant’s directors and officers and by each person who owns 10% or more of the outstanding Common Stock. However, this does not necessarily mean that there are not other persons who may be deemed to be affiliates of the Registrant.

The number of shares of the Registrant’s Common Stock outstanding as of November 11, 2014 was 12,788,527.

Documents Incorporated by Reference

The information required to be reported in Part III of this Annual Report on Form 10-K will be included in the Company’s definitive Proxy Statement relating to the 2015 Annual Meeting of Shareholders (to be incorporated herein by reference) or in an amendment to this Annual Report on Form 10-K.

Table of Contents

PENFORD CORPORATION

FISCAL YEAR 2014 FORM 10-K ANNUAL REPORT

1

Table of Contents

PART I

| Item 1: | Business |

Description of Business

Penford Corporation (which, together with its subsidiary companies, is referred to herein as “Penford” or the “Company”) is a developer, manufacturer and marketer of specialty natural-based ingredient systems for food and industrial applications, including fuel grade ethanol. Penford’s products provide convenient and cost-effective solutions derived from renewable sources. Sales of the Company’s products are generated using a combination of direct sales and distributor agreements. The Company’s strategically-located manufacturing facilities in the United States provide it with broad geographic coverage of its target markets. The Company has significant research and development capabilities, which are used in applying the complex chemistry of carbohydrate-based materials and in developing applications to address customer needs. In addition, the Company has specialty processing capabilities for a variety of modified starches.

Penford is a Washington corporation originally incorporated in September 1983. The Company commenced operations as a publicly-traded company on March 1, 1984.

In January 2012, the Company acquired, through purchase and capital lease, the net assets and operations of the business generally known as Carolina Starches, which manufactures and markets industrial potato starch based products and blends for the paper and packaging industries. The acquisition of this business has provided an important source of raw material to support continued growth in the Company’s Food Ingredients business and has broadened the Company’s portfolio of specialty modified industrial starches.

In March 2014, the Company acquired substantially all of the assets of Gum Technology, which distributes and blends gums and hydrocolloids for the food and beverage industries in North America and Asia. Gum Technology, an Arizona close corporation, specializes in developing and producing customized stabilizers to meet customers’ product formulation needs. This acquisition broadens the Company’s Food Ingredients portfolio of functional and specialty ingredient systems. See Note 17 to the Consolidated Financial Statements.

On October 14, 2014, the Company and Ingredion Incorporated (“Ingredion”) entered into an Agreement and Plan of Merger (the “Merger Agreement”) pursuant to which Ingredion will acquire the Company in an all-cash transaction valued at approximately $340.0 million. Upon closing of the merger, each outstanding share of the Company’s common stock will be converted into the right to receive $19.00 in cash. The merger is subject to certain closing conditions and covenants, and provides certain termination rights for the parties to the Merger Agreement. See Note 21 to the Consolidated Financial Statements.

Penford operates in two business segments, Industrial Ingredients and Food Ingredients. Each of the Company’s businesses utilizes the Company’s carbohydrate chemistry expertise to develop starch and gum-based ingredients for value-added applications that improve the quality and performance of customers’ products. Financial information about Penford’s segments and geographic areas is included in Note 18 to the Consolidated Financial Statements. Additional information on Penford’s two business segments follows:

| • | Industrial Ingredients, which in fiscal years 2014, 2013 and 2012 generated approximately 71%, 76% and 76%, respectively, of Penford’s revenue, is a supplier of chemically modified specialty starches to the paper and packaging industries. Industrial Ingredients also produces food grade corn starch for sale by the Company’s Food Ingredients business. Through a commitment to research and development, Industrial Ingredients develops customized product applications that help its customers realize improved manufacturing efficiencies and advancements in product performance. Industrial Ingredients has specialty processing capabilities for a variety of modified starches. Specialty products for industrial applications are designed to improve the strength and performance of customers’ products and efficiencies in the manufacture of coated and uncoated paper and paper packaging products. These starches are principally ethylated (chemically modified with ethylene oxide), oxidized (treated with sodium hypochlorite) and cationic (carrying a positive electrical charge). Ethylated and oxidized |

2

Table of Contents

| starches are used in coatings and as binders, providing strength and printability to fine white, magazine and catalog paper. Cationic and other liquid starches are generally used in the paper-forming process in paper production, providing strong bonding of paper fibers and other ingredients. |

| • | The Company’s Industrial Ingredients segment also produces and sells fuel grade ethanol from its facility in Cedar Rapids, Iowa. Ethanol production gives the Company the ability to select an additional output choice to capitalize on changing industry conditions and selling opportunities. Sales of ethanol in fiscal years 2014, 2013 and 2012 were 30%, 27% and 31%, respectively, of this segment’s reported revenue. |

| • | The Industrial Ingredients business produces certain by-products from its corn wet milling operations in Cedar Rapids, Iowa. These by-products include corn gluten feed and corn gluten meal, which are sold to various market participants for use in animal feed, and corn germ, which is sold to a producer of corn oil. Sales of by-products in fiscal years 2014, 2013 and 2012 were 20%, 23%, and 22%, respectively, of this segment’s reported revenue. |

| • | Food Ingredients, which in fiscal years 2014, 2013 and 2012 generated approximately 29%, 24% and 24%, respectively, of Penford’s revenue, is a developer and manufacturer of specialty starches, dextrins and gums to the food manufacturing and food service industries. This business’s expertise is in leveraging the inherent characteristics from potato, corn, tapioca, rice and gums to help improve its customers’ product performance. Food Ingredients’ specialty starches produced for food applications are used in coatings to provide crispness, improved taste and texture and increased product life for products such as french fries sold in restaurants. Food Ingredients starch products and gums are used to reduce fat levels, increase fiber content, modify texture and improve color and consistency in a variety of foods such as canned products, sauces, whole and processed meats, dry powdered mixes and bakery products. These products are also used as moisture binders and in companion pet products, such as dog treats and chews. |

Raw Materials

Corn: Penford’s North American corn wet milling plant is located in Cedar Rapids, Iowa, in the middle of the U.S. corn belt. Accordingly, the plant has truck-delivered corn available throughout the year from a number of suppliers at prices consistent with those available in the major U.S. grain markets.

Potato Starch: The Company’s facilities in Idaho Falls, Idaho; Richland, Washington; Plover, Wisconsin; Berwick, Pennsylvania and North Charleston, South Carolina use starch recovered as by-products from potato processors as the primary raw material to manufacture modified potato starches. The Company enters into contracts typically having durations of two to four years with potato processors in the United States and Canada to acquire potato-based raw materials.

Chemicals: The primary chemicals used in the manufacturing processes are readily available commodity chemicals. The prices for these chemicals are subject to price fluctuations due to market conditions.

Natural Gas: The primary energy source for most of Penford’s plants is natural gas. Penford contracts its natural gas supply with regional suppliers, generally under short-term supply agreements, and, at times, uses futures contracts to hedge the price of natural gas.

Gums: Many of the gums sold by the Company and used in its blends are derived from vegetable matter, such as beans, seaweed, cellulose or sap. The availability and cost of gums are dependent on climate conditions and the political environment in countries that supply the gums.

Corn, chemicals, natural gas and gums are not currently subject to availability constraints; however, demand for these items can significantly affect the prices. Penford’s current potato starch requirements constitute a material portion of the available North American supply. Penford estimates that it purchases approximately 70% of the recovered potato starch in North America. It is possible that, in the long term, continued growth in demand for potato starch-based ingredients and new product development could result in capacity constraints.

3

Table of Contents

Approximately 67% of the Company’s manufacturing costs consist of the costs of corn, potato starch, chemicals and natural gas. The remaining portion consists of the costs of labor, distribution, depreciation and maintenance of manufacturing plant and equipment and other utilities. The prices of raw materials may fluctuate, and increases in costs may affect Penford’s business adversely. To mitigate this risk, Penford hedges a portion of corn purchases, and, at times, natural gas purchases with futures and options contracts and enters into short-term supply agreements for other production requirements.

Research and Development

Penford’s research and development efforts cover a range of projects including technical service work focused on specific customer support projects, which require coordination with customers’ research efforts to develop innovative solutions to specific customer requirements. These projects are supplemented with longer-term, new product development and commercialization initiatives. Research and development expenses were $5.6 million, $5.9 million and $5.8 million for fiscal years 2014, 2013 and 2012, respectively.

Patents, Trademarks and Trade Names

Penford owns a number of patents, trademarks and trade names. The Company has approximately 28 current patents and pending patent applications, most of which are related to technologies in french fry coatings, coatings for the paper industry and animal nutrition. Penford’s issued patents expire at various times through 2033. The annual cost to maintain all of the Company’s patents is not significant. Most of Penford’s products are currently made with technology that is broadly available to companies that have the same level of scientific expertise and production capabilities as Penford.

Specialty starch ingredient brand names for industrial applications include, among others, Penford® gums, Pensize® binders, Penflex® sizing agent, Topcat® cationic additive and the Apollo® starch series. Product brand names and trademarks for food ingredient applications include PenFibe®, PenTech®, PenPure®, PenNovo®, PenBind®, PenCling® and PenPlus®. Gum products are sold under the GumPlete Coyote Brand® names.

Quarterly Fluctuations

Penford’s revenues and operating results vary from quarter to quarter for various reasons. For example, sales volumes of the Food Ingredients products used in food coatings are generally lower during Penford’s second fiscal quarter due to decreased consumption of some coated foods during the post-holiday season. In addition, the cost of natural gas in North America is generally higher in the winter months than the summer months.

Working Capital

The Company’s growth is funded through a combination of cash flows from operations and short- and long-term borrowings. For more information, see the “Liquidity and Capital Resources” section under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7 and the audited consolidated financial statements and the related notes included elsewhere in this Annual Report on Form 10-K.

Penford generally carries a one- to 45-day supply of materials required for production, depending on the lead time for specific items. Penford manufactures finished goods to customer orders or anticipated demand. The Company is therefore able to carry less than a 30-day supply of most products. Terms for trade receivables and trade payables are standard for the industry and region and generally do not exceed 30-45 day terms except for trade receivables for export sales.

Environmental Matters

Penford’s operations are governed by various federal, state and local environmental laws and regulations. These laws and regulations include the Clean Air Act, the Clean Water Act, the Resource Conservation and

4

Table of Contents

Recovery Act, the EPA Oil Pollution Control Act, the Occupational Safety and Health Administration’s hazardous materials regulations, the Toxic Substances Control Act, the Comprehensive Environmental Response Compensation and Liability Act and the Superfund Amendments and Reauthorization Act.

Permits are required by the various environmental agencies that regulate the Company’s operations. Penford believes that it has obtained all necessary material environmental permits required for its operations. Penford believes that its operations are in compliance with applicable environmental laws and regulations in all material aspects of its business. Penford estimates that annual compliance costs, excluding operational costs for emission control devices, wastewater treatment or disposal fees, are approximately $1.2 million.

Penford has adopted and implemented a comprehensive corporate-wide environmental management program. The program is managed and designed to structure the conduct of Penford’s business in a safe and fiscally responsible manner that protects and preserves the health and safety of employees, the communities surrounding the Company’s plants and the environment. The Company continuously monitors environmental legislation and regulations that may affect Penford’s operations.

During fiscal 2014, compliance with environmental regulations did not have a material impact on the Company’s operations. No unusual expenditures for environmental facilities and programs are anticipated in fiscal 2015.

Customers

Penford sells to a variety of customers and has several relatively large customers in each business segment. The Company’s sales of ethanol to its sole ethanol customer, Eco-Energy, Inc., represented approximately 22%, 21% and 24% of the Company’s net sales for fiscal years 2014, 2013 and 2012, respectively. Eco-Energy, Inc., a marketer and distributor of biofuels in the United States and Canada, is a customer of the Company’s Industrial Ingredients business.

Approximately 36%, 38% and 36% of the Company’s sales in fiscal 2014, 2013 and 2012, respectively, were made to customers who operate in the paper and packaging industries. Over the last few years, these industries suffered an economic downturn, which has resulted in the closure of a number of mills.

Competition

In its primary markets, Penford competes directly with approximately six other companies that manufacture specialty starches for the papermaking industry, approximately five other companies that manufacture specialty food ingredients and numerous producers of fuel grade ethanol. Penford also competes with a larger number of companies that provide synthetic and natural-based ingredients to industrial and food customers. Some of these competitors are larger companies, and have greater financial and technical resources than Penford. Application expertise, quality and service are the major competitive advantages for Penford.

Employees

As of August 31, 2014, Penford had 443 employees, of whom approximately 34% were members of a trade union. The collective bargaining agreement covering the Cedar Rapids-based manufacturing workforce expires in August 2015. The Company is currently engaged in labor contract negotiations with a new bargaining unit consisting of approximately 15 operating employees at its Richland, WA plant.

Sales and Distribution

Sales are generated using a combination of direct sales and distributor agreements. In many cases, Penford supports its sales efforts with technical and advisory assistance to customers. Penford generally ships its products upon receipt of purchase orders from its customers and, consequently, backlog is not significant.

5

Table of Contents

Since Penford’s customers are generally other manufacturers and processors, most of the Company’s products are distributed via rail or truck to customer facilities.

Export Sales

Export sales from Penford’s businesses in the United States accounted for approximately 8.0%, 8.0% and 7.6% of total sales in fiscal years 2014, 2013 and 2012, respectively. See Note 18 to the Consolidated Financial Statements for sales by country to which the product was shipped.

Available Information

Penford’s Internet address is www.penx.com. The Company makes available, free of charge through its Internet site, the Company’s annual reports on Form 10-K; quarterly reports on Form 10-Q; current reports on Form 8-K; Directors and Officers Forms 3, 4 and 5; and amendments to those reports, as soon as reasonably practicable after electronically filing such materials with, or furnishing them to, the Securities and Exchange Commission (“SEC”). The information found on Penford’s web site will not be considered to be part of this or any other report or other document filed with or furnished to the SEC. The SEC also maintains an Internet site, which contains reports, proxy and information statements and other information regarding issuers that file information electronically with the SEC. The SEC’s Internet address is www.sec.gov.

In addition, the Company makes available, through the Investor Center section of its Internet site, the Company’s Code of Business Conduct and Ethics and the written charters of its Board of Directors’ Audit, Governance and Executive Compensation and Development Committees.

Executive Officers of the Registrant

| Name |

Age | Title | ||||

| Thomas D. Malkoski |

58 | President and Chief Executive Officer | ||||

| Steven O. Cordier |

58 | Senior Vice President, Chief Financial Officer and Assistant Secretary | ||||

| Michael J. Friesema |

57 | Vice President – Corporate Development | ||||

| Timothy M. Kortemeyer |

48 | Vice President; President, Industrial Ingredients | ||||

| Christopher L. Lawlor |

64 | Vice President – Human Resources, General Counsel and Secretary | ||||

| John R. Randall |

70 | Vice President; President, Food Ingredients | ||||

Mr. Malkoski joined Penford Corporation as Chief Executive Officer and was appointed to the Board of Directors in January 2002. He was named President of Penford Corporation in January 2003. From 1997 to 2001, he served as President and Chief Executive Officer of Griffith Laboratories, North America, a formulator, manufacturer and marketer of ingredient systems to the food industry. Previously, he served in various senior management positions, including as Vice President/Managing Director of the Asia Pacific and South Pacific regions for Chiquita Brands International, an international marketer and distributor of bananas and other fresh produce. Mr. Malkoski began his career at the Procter and Gamble Company, a marketer of consumer brands, progressing through major product category management responsibilities. Mr. Malkoski holds a Masters of Business Administration degree from the University of Michigan.

Mr. Cordier is Penford’s Senior Vice President, Chief Financial Officer and Assistant Secretary. He joined Penford in July 2002 as Vice President and Chief Financial Officer and was promoted to Senior Vice President in November 2004. From September 2005 to April 2006, Mr. Cordier served as the interim Managing Director of Penford’s Australian and New Zealand operations. He came to Penford from Sensient Technologies Corporation, a manufacturer of specialty products for the food, beverage, pharmaceutical and technology industries, where he held a variety of senior financial management positions.

Mr. Friesema joined Penford in September 2010 as Director – Business Development and was promoted to Vice President – Corporate Development in August 2012. He came to Penford from Corn Products International, Inc. (now Ingredion), a manufacturer of starch and sweetener ingredients, where he most recently served as

6

Table of Contents

General Manager, Africa and Senior Director, Engineering, Asia-Africa Division. Prior to that, he was Chief Operating Officer and President – Food Ingredients for zuChem, Inc., a producer of unique sugars for use in the food, specialty and fine chemical markets.

Mr. Kortemeyer has served as Vice President of Penford Corporation since October 2005 and President, Industrial Ingredients since June 2006. He served as General Manager of the Industrial Ingredients business from August 2005 to June 2006. Mr. Kortemeyer joined Penford in 1999 and served as a Team Leader in the manufacturing operations of the Industrial Ingredients business until 2001. From 2001 until 2003, he was an Operations Manager and Quality Assurance Manager. From July 2003 to November 2004, Mr. Kortemeyer served as the business unit manager of the Company’s co-products business, and from November 2004 until August 2005, as the director of the Company’s specialty starches product lines, responsible for sales, marketing and business development.

Mr. Lawlor joined Penford in April 2005 as Vice President – Human Resources, General Counsel and Secretary. From 2002 to April 2005, Mr. Lawlor served as Vice President – Human Resources for Sensient Technologies Corporation, a manufacturer of specialty chemical and food products. From 2000 to 2002, he was Assistant General Counsel for Sensient. Mr. Lawlor was Vice President – Administration, General Counsel and Secretary for Kelley Company, Inc., a manufacturer of material handling and safety equipment from 1997 to 2000. Prior to joining Kelley Company, Mr. Lawlor was employed as an attorney at a manufacturer of paper and packaging products and in private practice with two national law firms.

Mr. Randall is Vice President of Penford Corporation and President, Food Ingredients. He joined Penford in February 2003 as Vice President and General Manager of Penford Food Ingredients and was promoted to President of the Food Ingredients division in June 2006. Prior to joining Penford, Mr. Randall was Vice President, Research & Development/Quality Assurance of Griffith Laboratories, USA, a specialty food ingredients business, from 1998 to 2003. From 1993 to 1998, Mr. Randall served in various research and development positions with KFC Corporation, a quick-service restaurant business, most recently as Vice President, New Product Development. Prior to 1993, Mr. Randall served in research and development leadership positions at Romanoff International, Inc., a manufacturer and marketer of gourmet specialty food products, and at Kraft/General Foods.

7

Table of Contents

| Item 1A: | Risk Factors |

Risk Factors Relating to Penford’s Business

The availability and cost of agricultural products Penford purchases are vulnerable to weather and other factors beyond its control. The Company’s ability to pass through cost increases for these products is limited by worldwide competition and other factors.

In fiscal 2014, approximately 50% of Penford’s manufacturing costs were the costs of corn, potato starch, gums and other agricultural raw materials. Weather conditions, plantings, government programs, policies and mandates and energy costs and global supply, among other things, have historically caused volatility in the supply and prices of these agricultural products. Due to local and/or international competition, the Company may not be able to pass through the increases in the cost of agricultural raw materials to its customers. To manage price volatility in the commodity markets, the Company may purchase inventory in advance or enter into exchange-traded futures contracts. Despite these hedging activities, the Company may not be successful in limiting its exposure to market fluctuations in the cost of agricultural raw materials. Increases in the cost of corn, potato starch and other agricultural raw materials due to weather conditions or other factors beyond Penford’s control and that cannot be passed through to customers will reduce Penford’s future profitability.

Increases in energy and chemical costs may reduce Penford’s profitability.

Energy and chemicals comprised approximately 8% and 9%, respectively, of the cost of manufacturing the Company’s products in fiscal 2014. Penford uses natural gas extensively in its Industrial Ingredients business to dry starch products, and, to a lesser extent, in the Food Ingredients business. The Company uses chemicals in all of the businesses to modify starch for specific product applications and customer requirements. The prices of these inputs to the manufacturing process fluctuate based on anticipated changes in supply and demand, weather and the prices of alternative fuels, including petroleum. The Company may use short-term purchase contracts or exchange-traded futures contracts to reduce the price volatility of natural gas; however, these strategies are not available for the chemicals the Company purchases. If the Company is unable to pass on increases in energy and chemical costs to its customers, margins and profitability would be adversely affected.

The loss of a major customer could have an adverse effect on Penford’s results of operations.

The Company’s sales of ethanol to its sole ethanol customer, Eco-Energy, Inc., represented approximately 22%, 21% and 24% of the Company’s net sales for fiscal years 2014, 2013 and 2012, respectively. Eco-Energy, Inc. is a marketer and distributor of biofuels in the United States and Canada. Sales to the Company’s top ten customers represented 55%, 56% and 60% of net sales for fiscal years 2014, 2013 and 2012, respectively. Generally, the Company does not have multi-year sales agreements with its customers. Many customers place orders on an as-needed basis and generally can change their suppliers without penalty. If Penford lost one or more of its major customers, or if one or more of its major customers significantly reduced its orders, sales, results of operations and cash flow would be adversely affected.

The Company is substantially dependent on its manufacturing facilities; any operational disruption could result in a reduction of the Company’s sales volumes and could cause it to incur substantial losses.

Penford’s revenues are, and will continue to be, derived from the sale of starch-based ingredients and ethanol that the Company manufactures at its facilities. The Company’s operations may be subject to significant interruption if any of its facilities experiences a major accident or is damaged by severe weather or other natural disasters, as occurred as a result of the flood of the Cedar River at the Company’s Cedar Rapids, Iowa facility in fiscal 2008. In addition, the Company’s operations may be subject to labor disruptions and unscheduled downtime, or other operational hazards inherent in the industry, such as equipment failures, fires, explosions, abnormal pressures, blowouts, pipeline ruptures, transportation accidents and natural disasters. Some of these operational hazards may cause personal injury or loss of life, severe damage to or destruction of property and equipment or

8

Table of Contents

environmental damage, and may result in suspension of operations and the imposition of civil or criminal penalties. The Company’s insurance may not be adequate to fully cover the potential operational hazards described above, or it may not be able to renew this insurance on commercially reasonable terms or at all.

The Company may experience an impairment charge related to its long-lived assets, which would decrease its earnings and net worth.

The Company reviews its long-lived assets for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Impairment is recognized when the fair values of long-lived assets are less than the carrying amount of the assets. The estimation of expected future net cash flows is inherently uncertain and involves significant judgment. These estimates rely, to a considerable extent, on assumptions regarding current and future economics, market conditions, availability of capital and forecasts of product sales and commodity and energy costs. If, in future periods, there are changes in the estimates or assumptions incorporated into the impairment review analysis, the changes could result in an adjustment to the carrying amount of the long-lived assets. There can be no assurance that management’s current projections of cash flows will be achieved or that an impairment charge will not be required in the future. An impairment charge could be material to the Company’s financial position and results of operations.

The agreements governing the Company’s debt contain various covenants that limit its ability to take certain actions and also require the Company to meet financial maintenance tests, and Penford’s failure to comply with any of the debt covenants could have a material adverse effect on the Company’s business, financial condition and results of operations.

The agreements governing Penford’s outstanding debt contain a number of significant covenants that, among other things, limit its ability to:

| • | incur additional debt or liens; |

| • | consolidate or merge with any person or transfer or sell all or substantially all of its assets; |

| • | make investments or acquisitions; |

| • | pay dividends or make certain other restricted payments; and |

| • | enter into transactions with affiliates. |

In addition, the Company’s revolving credit facility requires it to comply with specific financial ratios and tests, under which it is required to achieve specific financial and operating results. Events beyond the Company’s control may affect its ability to comply with these provisions. A breach of any of these covenants would result in a default under the Company’s revolving credit facility. In the event of any default that is not cured or waived, the Company’s lenders could elect to declare all amounts borrowed under the revolving credit facility, together with accrued interest thereon, due and payable. If any of the Company’s debt is accelerated, there is no assurance that the Company would have sufficient assets to repay that debt or that it would be able to refinance that debt on commercially reasonable terms or at all.

Changes in interest rates may affect Penford’s profitability.

As of August 31, 2014, approximately $76.0 million of its outstanding debt was subject to variable interest rates that move in direct relation to the LIBOR Index Rate or the prime rate in the United States, depending on the selection of borrowing options. Any significant changes in these interest rates would materially affect the Company’s profitability by increasing or decreasing its borrowing costs.

Unanticipated changes in tax rates or exposure to additional income tax liabilities could affect Penford’s profitability.

The Company is subject to income taxes in the federal and various state jurisdictions in the United States. The Company’s effective tax rates could be adversely affected by changes in the mix of earnings in tax

9

Table of Contents

jurisdictions with differing statutory tax rates, changes in the valuation of deferred tax assets and liabilities or changes in tax laws. The carrying value of deferred tax assets is dependent on the Company’s ability to generate future taxable income in the United States. The amount of income taxes paid is subject to interpretation of applicable tax laws in the jurisdictions in which the Company operates. Although the Company believes it has complied with all applicable income tax laws, there is no assurance that a tax authority will not have a different interpretation of the law or that any additional taxes imposed as a result of tax audits will not have an adverse effect on the Company’s results of operations and financial condition.

Pension expense and the funding of pension obligations are affected by factors outside the Company’s control, including the performance of plan assets, interest rates, actuarial data and experience and changes in laws and regulations.

The future funding obligations for the Company’s two U.S. defined benefit pension plans qualified with the Internal Revenue Service depend upon the level of benefits provided for by the plans, the future performance of assets set aside in trusts for these plans, the level of interest rates used to determine funding levels, actuarial data and experience and any changes in government laws and regulations. The pension plans hold a significant amount of equity and fixed income securities. When the values of these securities decline, pension expense can increase and materially affect the Company’s results. Decreases in interest rates that are not offset by contributions and asset returns could also increase the Company’s obligations under such plans. The Company is legally required to make contributions to the pension plans in the future, and those contributions could be material. The Company does not expect to make contributions to its pension plans during fiscal 2015.

The current capital and credit market conditions may adversely affect the Company’s access to capital, cost of capital and business operations.

The general economic and capital market conditions in the United States and other parts of the world continue to adversely affect access to capital and increase the cost of capital. If these conditions continue or become worse, the Company’s future cost of debt and equity capital and its access to capital markets could be adversely affected. An inability to obtain adequate financing from debt and equity sources could force the Company to self-fund strategic initiatives or even forgo some opportunities, potentially harming its financial position, results of operations and liquidity.

Economic conditions may impair the businesses of the Company’s customers and end user markets, which could adversely affect the Company’s business operations.

As a result of the continuing economic downturn and macro-economic challenges affecting the economy of the United States and other parts of the world, the businesses of some of the Company’s customers may not be successful in generating sufficient revenues. Customers may choose to delay or postpone purchases from the Company until the economy and their businesses strengthen. The Company’s Industrial Ingredients business is dependent upon end markets for paper and ethanol in North America. Paper markets have been under competitive pressure from substitutable electronic alternatives and may be further stressed by the continuing economic downturn. Ethanol markets have been under pressure from declining demand and volatile corn prices. Decisions by current or future customers to forego or defer purchases and/or customers’ inability to pay the Company for its products may adversely affect the Company’s earnings and cash flow.

The use and demand for ethanol and its supply may be affected by changes in federal and state legislation and regulation. Changes in legislation or regulation could cause the demand for ethanol to decline or its supply to increase, which could have a material adverse effect on the Company’s business.

Various federal and state laws, regulations and programs have affected the supply of ethanol and its use in fuel. Federal and state legislators and environmental regulators could adopt or modify laws, regulations or programs that could adversely affect the use and/or supply of ethanol. Of particular note, the Renewable Fuel

10

Table of Contents

Standard (“RFS”) currently requires an increasing amount of renewable fuels to be used in the United States. However, the United States Environmental Protection Agency (“EPA”) is currently considering various requests for waivers from compliance with the volume requirements of the RFS. If such waivers are granted, demand for the Company’s ethanol may decrease, and this may have a material effect on the Company’s results.

Penford depends on its senior management team; the loss of any member could adversely affect its operations.

Penford’s success depends on the management and leadership skills of its senior management team. The loss of any of these individuals, or the Company’s inability to attract, retain and maintain additional personnel, could affect the Company’s ability to fully implement its business strategy. There is no assurance that it will be able to retain its existing senior management personnel or attract additional qualified personnel when needed.

Penford is subject to stringent environmental and health and safety laws, which may require it to incur substantial compliance and remediation costs, thereby reducing profits.

Penford is subject to many federal, state and local environmental and health and safety laws and regulations, particularly with respect to the use, handling, treatment, storage, discharge and disposal of substances and hazardous wastes used or generated in its manufacturing processes. Compliance with these laws and regulations is a significant factor in the Company’s business. Penford has incurred and expects to continue to incur expenditures to comply with applicable environmental laws and regulations. The Company’s failure to comply with applicable environmental laws and regulations and permit requirements could result in civil or criminal fines, penalties or enforcement actions, including regulatory or judicial orders enjoining or curtailing operations or requiring corrective measures, installation of pollution control equipment or remedial actions.

The Company may be required to incur costs relating to the investigation or remediation of property, including property where it has disposed of its waste, and for addressing environmental conditions. Some environmental laws and regulations impose liability and responsibility on present and former owners, operators or users of facilities and sites for contamination at such facilities and sites without regard to causation or knowledge of contamination. Consequently, there is no assurance that existing or future circumstances, the development of new facts or the failure of third parties to address contamination at current or former facilities or properties will not require significant expenditures by the Company.

The Company expects to continue to be subject to increasingly stringent environmental and health and safety laws and regulations. It is difficult to predict the future interpretation and development of environmental and health and safety laws and regulations or their impact on the Company’s future earnings and operations. The Company anticipates that compliance will continue to require increased capital expenditures and operating costs. Any increase in these costs, or unanticipated liabilities arising, for example, out of discovery of previously unknown conditions or more aggressive enforcement actions, could adversely affect the Company’s results of operations, and there is no assurance that they will not have a material adverse effect on its business, financial condition and results of operations.

Penford’s unionized workforce could cause interruptions in the Company’s provision of services.

As of August 31, 2014, approximately 34% of the Company’s 443 employees were members of a trade union. In addition, the Company is currently engaged in contract negotiations with a new bargaining unit consisting of approximately 15 operating employees at its Richland, WA plant. Although the Company’s relations with the relevant unions are stable and the Company’s Cedar Rapids labor contract does not expire until August 2015, there is no assurance that the Company will not experience work disruptions or stoppages in the future, which could have a material adverse effect on its business and results of operations and adversely affect its relationships with its customers.

11

Table of Contents

The Company may fail to realize the benefits of the acquisition of substantially all the assets of Gum Technology, an Arizona close corporation.

As noted above, in March 2014, the Company acquired substantially all of the assets of Gum Technology, an Arizona close corporation, which distributes and blends gums and hydrocolloids for the food and beverage industries in North America and Asia, for approximately $9.9 million. Since the acquisition was recently completed, the Company has not yet determined whether it will be able to obtain all of the expected benefits from this acquisition. If not, the Company will suffer the loss of the expected benefits from this acquisition.

Risks Relating to the Proposed Merger with Ingredion

The merger is subject to various closing conditions, including governmental approvals, and other uncertainties and there can be no assurances as to whether and when it may be completed.

On October 14, 2014, the Company entered into the Merger Agreement with Ingredion and Prospect Sub, Inc. (“Merger Sub”), under which Merger Sub will merge with and into the Company, with the Company continuing as the surviving corporation and a wholly owned subsidiary of Ingredion. The consummation of the merger is subject to customary closing conditions. A number of the conditions are not within the Company’s control, and may prevent, delay or otherwise materially adversely affect the completion of the transaction. These conditions include, among other things, (a) receiving the required approval of the Company’s shareholders and (b) the expiration or termination of the applicable waiting period under the Hart-Scott-Rodino Act and any other foreign or U.S. laws that are designed or intended to prohibit, restrict or regulate actions having the purpose or effect of monopolization or restraint of trade or lessening of competition through merger or acquisition. It also is possible that a change, event, fact, effect or circumstance that could lead to a material adverse effect on Penford may occur, which may give Ingredion the ability to not complete the merger. The Company cannot predict with certainty whether and when any of the required closing conditions will be satisfied or if another uncertainty may arise. If the merger does not receive, or timely receive, the required regulatory approvals and clearances, or if another event occurs delaying or preventing the merger, such delay or failure to complete the merger may cause uncertainty or other negative consequences that may materially and adversely affect the Company’s sales, financial performance and operating results and the price per share for the Company’s common stock and perceived acquisition value.

If the Merger Agreement is terminated, the Company may, under certain circumstances, be obligated to pay a termination fee or a break-up fee to Ingredion.

If the merger is not completed, in certain circumstances, the Company would still be liable for significant transaction costs and could also be required to pay a termination fee of approximately $7.6 million. If the Merger Agreement is terminated, the expense reimbursement and the termination fee it may be required to pay, if any, under the Merger Agreement may require the Company to use available cash that would have otherwise been available for general corporate purposes. For these and other reasons, a failed merger could materially and adversely affect the Company’s business, operating results or financial condition, which in turn would materially and adversely affect the Company’s business and financial condition, the price per share of the Company’s common shares and the Company’s perceived acquisition value.

The Merger Agreement limits the Company’s ability to pursue alternative transactions to the proposed merger with Ingredion.

The Merger Agreement prohibits the Company and its directors, officers, representatives and agents, subject to narrow exceptions, from initiating, encouraging, soliciting or entering into discussions with any third party regarding alternative acquisition proposals. The prohibition limits the Company’s ability to pursue offers from other possible acquirers that may be superior to the pending merger. If the Company receives an unsolicited proposal from a third party that is superior and the Merger Agreement is terminated pursuant to its terms, the Company is contractually obligated to pay a termination fee of approximately $7.6 million to Ingredion. This termination fee makes it less likely that a third party will make an alternative acquisition proposal.

12

Table of Contents

While the merger is pending, the Company is subject to business uncertainties and contractual restrictions that could materially adversely affect its operations and the future of its business or result in a loss of employees.

The Merger Agreement includes restrictions on the conduct of the Company’s business prior to the completion of the merger, generally requiring the Company to conduct its business in the ordinary course and subjecting the Company to a variety of specified limitations absent Ingredion’s prior written consent. The Company may find that these and other contractual arrangements in the Merger Agreement may delay or prevent it from or limit its ability to respond effectively to competitive pressures, industry developments and future business opportunities that may arise during such period, even if the Company’s management thinks they may be advisable. The pendency of the merger may also divert management’s attention and the Company’s resources from ongoing business and operations. The Company’s employees, customers and suppliers may have uncertainties about the effects of the merger. In connection with the pending merger, it is possible that some customers, suppliers and other persons with whom the Company has a business relationship may delay or defer certain business decisions or might decide to seek to terminate, change or renegotiate their relationship with the Company as a result of the merger. Similarly, current and prospective employees may experience uncertainty about their future roles with the Company following completion of the merger, which may materially adversely affect the Company’s ability to attract and retain key employees. If any of these effects were to occur, it could materially and adversely impact the Company’s revenues, earnings, cash flows, other business results and financial condition, as well as the market price of the Company’s common shares and the Company’s perceived acquisition value, regardless of whether the merger is completed. In addition, whether or not the merger is completed, while it is pending, the Company will continue to incur costs, fees, expenses and charges related to the proposed merger, which may materially and adversely affect its business results and financial condition.

Failure to complete the merger could negatively impact the Company’s share price and its business and financial results.

There is no assurance that the merger or any other transaction will occur or that the conditions to the merger will be satisfied in a timely manner or at all. Further, there is no assurance that any event, change or other circumstances that could give rise to the termination of the Merger Agreement will not occur. Because the share price of the Company’s common stock after the announcement of the Merger Agreement may reflect an assumption that the merger will be completed, the share price of the Company’s common stock may drop, potentially significantly, if the merger is not completed. In addition, under circumstances defined in the Merger Agreement, if the merger is not completed, the Company may be required to pay a termination fee of up to approximately $7.6 million. Certain costs associated with the merger are already incurred or may be payable even if the merger is not completed. Further, a failed transaction may result in negative publicity and a negative impression of the Company in the investment community. Finally, any disruptions to the Company’s business resulting from the announcement and pendency of the merger and from intensifying competition from competitors, including any adverse changes in the Company’s relationships with its customers, vendors and employees or recruiting and retention efforts, could continue or accelerate in the event of a failed transaction. There can be no assurance that the Company’s business, these relationships or the Company’s financial condition will not be negatively impacted, as compared to prior to the announcement of the merger, if the merger is not consummated. If any of these effects were to occur, it could negatively impact the Company’s revenues, earnings, cash flows, other business results and financial condition, as well as the market price of the Company’s common stock and the Company’s perceived acquisition value.

Pending litigation against Penford and Company directors could result in an injunction preventing completion of the merger and significant litigation costs that could adversely affect the Company’s financial condition.

Since the announcement on October 15, 2014 of the signing of the Merger Agreement, the Company, as well as the members of its Board of Directors, have been named as defendants in one purported class action lawsuit filed on behalf of the Company’s shareholders challenging the proposed merger. The lawsuit generally alleges, among other things, that the members of the Company’s Board of Directors breached their fiduciary

13

Table of Contents

duties to Company shareholders by failing to take steps to maximize shareholder value or to engage in a fair sale process before approving the Merger Agreement, and that those breaches were aided and abetted by Ingredion and Merger Sub. The lawsuit seeks, among other things, injunctive relief to enjoin the defendants from completing the merger on the agreed-upon terms, rescission to the extent the merger terms have already been implemented, monetary relief and attorneys’ fees and costs. It is possible that other related lawsuits may subsequently be filed.

One of the conditions to the closing of the merger is that no injunction preventing the consummation of the merger and the other transactions contemplated by the Merger Agreement shall be in effect and that no rule, regulation, order or injunction shall have been enacted, entered, promulgated or enforced by any governmental entity that prohibits or makes illegal the consummation of the merger. Consequently, if the plaintiffs were to secure injunctive or other relief prohibiting, delaying, or otherwise adversely affecting the defendants’ ability to complete the merger, then such injunctive or other relief may prevent the merger from becoming effective within the expected time frame or at all. If completion of the merger is prevented or delayed, it could result in substantial costs to the Company and Ingredion. In addition, the Company and Ingredion are incurring and will continue incurring significant costs in connection with the lawsuit, including, for the Company, costs associated with the indemnification of its directors.

Risk Factors Relating to Penford’s Common Stock

Penford’s stock price has fluctuated significantly; the trading price of its common stock may fluctuate significantly in the future.

The trading price of the Company’s common stock has fluctuated significantly. In fiscal 2014, the stock price ranged from a low of $10.71 on June 24, 2014, to a high of $15.18 on October 15, 2013. The trading price of Penford’s common stock may fluctuate significantly in the future as a result of a number of factors, including:

| • | actual and anticipated variations in the Company’s operating results; |

| • | general economic and market conditions, including changes in demand for the Company’s products; |

| • | interest rates; |

| • | geopolitical conditions throughout the world; |

| • | perceptions of the strengths and weaknesses of the Company’s industries; |

| • | the Company’s ability to pay principal and interest on its debt when due; |

| • | developments in the Company’s relationships with its lenders, customers and/or suppliers; |

| • | the performance of the Company compared to its competitors; |

| • | announcements of alliances, mergers or other relationships by or between the Company’s competitors and/or its suppliers and customers; and |

| • | quarterly variations in the Company’s results of operations due to, among other things, seasonality in demand for products and fluctuations in the cost of raw materials. |

The stock markets in general have experienced broad fluctuations that have often been unrelated to the operating performance of particular companies. These broad market fluctuations may adversely affect the trading price of the Company’s common stock. Accordingly, Penford’s common stock may trade at prices significantly below an investor’s cost, and investors could lose all or part of their investment in the event that they choose to sell their shares.

Provisions of Washington law could discourage or prevent a potential takeover.

Washington law imposes restrictions on certain transactions between a corporation and certain significant shareholders. The Washington Business Corporation Act generally prohibits a “target corporation” from

14

Table of Contents

engaging in certain significant business transactions with an “acquiring person,” which is defined as a person or group of persons that beneficially owns 10% or more of the voting securities of the target corporation, for a period of five years after such acquisition, unless the transaction or acquisition of shares is approved by a majority of the members of the target corporation’s board of directors prior to the time of the acquisition. Such prohibited transactions include, among other things, (1) a merger or consolidation with, disposition of assets to, or issuance or redemption of stock to or from, the acquiring person; (2) a termination of 5% or more of the employees of the target corporation as a result of the acquiring person’s acquisition of 10% or more of the shares; and (3) allowing the acquiring person to receive any disproportionate benefit as a shareholder. After the five-year period, a “significant business transaction” may occur if it complies with “fair price” provisions specified in the statute. A corporation may not “opt out” of this statute.

| Item 1B: | Unresolved Staff Comments |

None.

15

Table of Contents

| Item 2: | Properties |

Penford’s facilities as of August 31, 2014 were as follows:

| Bldg. Area (Approx. Sq. Ft.) |

Land Area (Acres) |

Owned/ Leased |

Function of Facility | |||||||||

| Centennial, Colorado |

25,200 | — | Leased | Corporate headquarters and offices and research laboratories for the Food Ingredients segment | ||||||||

| Englewood, Colorado |

46,054 | — | Leased | |||||||||

| Cedar Rapids, Iowa |

759,000 | * | 29 | Owned | Manufacture of corn starch products and research laboratories for the Industrial Ingredients and Food Ingredients segments | |||||||

| Idaho Falls, Idaho |

30,000 | 4 | Owned | Manufacture of potato starch products for the Food Ingredients segment | ||||||||

| Richland, Washington (owned and leased) |

— | 4.4 | — | Manufacture of potato and tapioca starch products for the Food Ingredients segment | ||||||||

| Building 1 |

45,000 | — | Owned | |||||||||

| Building 2 |

9,600 | — | Leased | |||||||||

| Plover, Wisconsin (two facilities, one of which is located on leased land) |

||||||||||||

| Facility 1 |

45,000 | 9.5 | Owned | Manufacture of potato starch products for the Food Ingredients segment | ||||||||

| Facility 2 |

15,000 | 3.3 | Owned (leased land) |

Manufacture of potato starch products for the Food Ingredients segment | ||||||||

| Berwick, Pennsylvania |

31,200 | 2.1 | Leased | Manufacture of potato starch products for the Industrial Ingredients segment | ||||||||

| 20,000 | — | Leased | Office and warehouse | |||||||||

| North Charleston, South Carolina |

21,700 | 5.0 | Owned | Office and manufacture of potato starch products for the Industrial Ingredients segment | ||||||||

| Tucson, Arizona |

4,300 | — | Leased | Office and research laboratories for the Food Ingredients segment | ||||||||

| * | Approximately 119,150 square feet are subject to a long-term lease to the purchaser of the Company’s former dextrose business. |

Penford’s production facilities are strategically located near sources of raw materials. The Company believes that its facilities are maintained in good condition and that the capacities of its plants are sufficient to meet current production requirements. The Company invests in expansion, improvement and maintenance of property, plant and equipment as required.

| Item 3: | Legal Proceedings |

The Company regularly evaluates the status of claims and legal proceedings in which it is involved in order to assess whether a loss is probable or there is a reasonable possibility that a loss may have been incurred, and to determine if accruals are appropriate. The Company expenses legal costs as such costs are incurred.

16

Table of Contents

Pet Product Patent Litigation (T.F.H. Publications, Inc. v. Penford Products Co. et al)

In June 2011, the Company was notified that a complaint had been filed against a customer of a Company subsidiary, Penford Products Co., in the United States District Court for the District of New Jersey. The complaint alleged that certain pet products supplied by Penford Products to the customer infringed upon a patent owned by T.F.H. Publications, Inc. The customer tendered the defense of this lawsuit to Penford Products pursuant to the terms of its supply agreement with Penford Products. Penford Products thereafter commenced the defense of this litigation on behalf of the customer. In April 2012, the plaintiff filed an amended complaint alleging that certain additional products made by Penford Products for the same customer infringed upon two of the plaintiff’s patents. In November 2013, the plaintiff filed another amended complaint adding Penford Products as a defendant in the suit. The Plaintiff is seeking an injunction against infringement of its patents, as well as the recovery of an unspecified amount of damages.

The court held a claim construction hearing on August 7, 2013, and rendered an opinion dated April 30, 2014. The Company believes that the court’s opinion substantially supports its position that none of the products supplied by Penford Products infringes upon the patents in the suit. The Company has recently entered into settlement negotiations with the plaintiff, but there can be no assurance that these negotiations will be successfully completed. If the negotiations fail, the Company will continue to evaluate further steps in order to obtain the dismissal of the litigation. The Company cannot at this time determine the likelihood of any outcome or estimate any damages that might be awarded.

Estate of Brett D. Brown (Heather A. Brown as Administrator for the Estate of Brett D. Brown v. Penford Corporation and Penford Products Co)

In early October 2014, the Company was notified that a petition had been filed against it and its subsidiary company, Penford Products Co., in the Iowa District Court for Linn County by the Administrator for the Estate of Brett D. Brown alleging negligence by the Company in connection with the death of Brett D. Brown, a former employee of an electrical contractor for Penford Products, at the Company’s Cedar Rapids plant. The petition does not specify an amount of damages being sought. The Company expects to defend the matter and to deny all allegations of negligence or fault. Pursuant to an indemnification agreement, the Company has tendered the defense of this matter to Mr. Brown’s former employer, and, by virtue of the Company’s status as an additional insured, to the employer’s insurer. The Company cannot at this time determine the likelihood of any outcome or estimate any damages that might be awarded.

Merger Agreement Shareholder Litigation (David Pill, individually and on behalf of all others similarly situated v. Penford Corporation, Ingredion Incorporated, et al)

In early November 2014, the Company, its directors and others were served with a complaint purporting to institute a stockholder class action in the Superior Court of Washington, King County, in connection with the Agreement and Plan of Merger that the Company entered into with Ingredion Incorporated on October 14, 2014. The complaint alleges, among other things, breaches of fiduciary duties in connection with the proposed acquisition of the Company by Ingredion. The plaintiff seeks an injunction against the proposed transaction and unspecified damages. In addition to legal defenses, the Company believes that it has adequate insurance protection that is expected to provide coverage applicable to the defense of this matter.

Management is unable to provide additional information regarding any possible loss in connection with the foregoing claims and proceedings because (i) the Company currently believes that the claims are not adequately supported, and (ii) there are significant factual and/or legal issues to be resolved. With regard to these matters, management does not believe, based on currently available information, that the eventual outcomes will have a material adverse effect on the Company’s financial condition, results of operations or liquidity, although the outcomes could be material to the Company’s operating results for any particular period, depending, in part, upon the operating results for such period.

17

Table of Contents

NewPage Bankruptcy Preference Litigation (Pirinate Consulting v. Penford Products Co. and Carolina Starches, LLC)

In late August and early September 2013, two of the Company’s subsidiaries, Penford Products and Carolina Starches, LLC, were served with separate complaints filed by Pirinate Consulting Group, LLC, as Litigation Trustee, for the NP Creditor Litigation Trust, as successor in interest to the bankruptcy estate of NewPage Corporation, an industrial starch customer of each subsidiary, in the United States Bankruptcy Court for the District of Delaware. The complaint against Carolina Starches was settled in March 2014 in exchange for a payment of $10,000. The complaint against Penford Products was settled in October 2014 in exchange for a payment of $50,000.

Other Claims and Litigation

The Company is involved from time to time in various other claims and litigation arising in the normal course of business. In the judgment of management, which relies in part on information obtained from the Company’s outside legal counsel, the ultimate resolution of these other matters will not materially affect the consolidated financial position, results of operations or liquidity of the Company.

| Item 4: | Mine Safety Disclosures |

Not applicable.

18

Table of Contents

PART II

| Item 5: | Market for the Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities |

Market Information and Holders of Common Stock

Penford’s common stock, $1.00 par value, trades on The NASDAQ Global Market under the symbol “PENX.” On November 11, 2014, there were 326 shareholders of record. The high and low sales prices of Penford’s common stock during the last two fiscal years are set forth below.

| Fiscal 2014 | Fiscal 2013 | |||||||||||||||

| High | Low | High | Low | |||||||||||||

| Quarter Ended November 30 |

$ | 15.18 | $ | 11.18 | $ | 7.99 | $ | 6.50 | ||||||||

| Quarter Ended February 28 |

$ | 14.41 | $ | 10.93 | $ | 11.27 | $ | 7.25 | ||||||||

| Quarter Ended May 31 |

$ | 15.09 | $ | 11.18 | $ | 12.89 | $ | 9.35 | ||||||||

| Quarter Ended August 31 |

$ | 14.82 | $ | 10.71 | $ | 15.98 | $ | 11.04 | ||||||||

Dividends

Pursuant to the Company’s current revolving credit agreement, the Company may declare and pay dividends on its common stock in an amount not to exceed, in any consecutive four quarters, the lesser of $10 million or 50% of Free Cash Flow, as defined. As of August 31, 2014, the Company was not permitted to pay dividends. See Note 6 to the Consolidated Financial Statements.

Issuer Purchases of Equity Securities

None.

19

Table of Contents

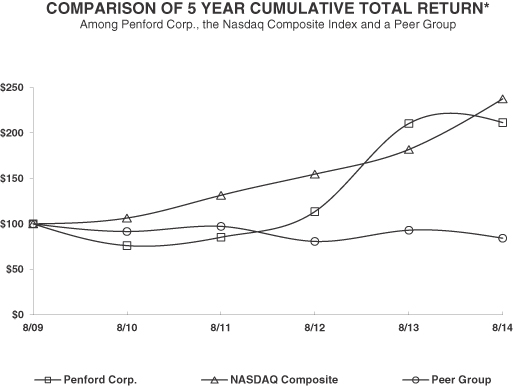

Performance Graph

The following graph compares the Company’s cumulative total shareholder return on its common stock for a five-year period (September 1, 2009 to August 31, 2014) with the cumulative total return of the Nasdaq Market Index and all companies traded on the Nasdaq Stock Market (“Nasdaq”) with a market capitalization of $100—$200 million, excluding financial institutions. The graph assumes that $100 was invested on September 1, 2009 in the Company’s common stock and in the stated indices. The comparison assumes that all dividends are reinvested. The Company’s performance as reflected in the graph is not indicative of the Company’s future performance.

| * | $100 invested on 8/31/09 in stock or index, including reinvestment of dividends. Fiscal year ended August 31. |

ASSUMES $100 INVESTED ON SEPTEMBER 1, 2009

ASSUMES DIVIDEND REINVESTED

FISCAL YEAR ENDED AUGUST 31, 2014

| 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | |||||||||||||||||||

| PENFORD CORPORATION |

$ | 100.00 | $ | 76.09 | $ | 85.40 | $ | 113.51 | $ | 210.40 | $ | 211.49 | ||||||||||||

| NASDAQ MARKET INDEX (U.S.) |

$ | 100.00 | $ | 106.46 | $ | 131.60 | $ | 154.71 | $ | 182.00 | $ | 237.54 | ||||||||||||

| NASDAQ MARKET CAP ($100-200M) |

$ | 100.00 | $ | 91.68 | $ | 97.27 | $ | 80.84 | $ | 93.08 | $ | 84.33 | ||||||||||||

Management does not believe there is either a published index or a group of companies whose overall business is sufficiently similar to the business of Penford to allow a meaningful benchmark against which the Company can be compared. The Company sells products based on specialty carbohydrate chemistry to several distinct markets, making overall comparisons to one of these markets misleading with respect to the Company as a whole. For these reasons, the Company has elected to use non-financial companies traded on Nasdaq with a similar market capitalization as a peer group.

20

Table of Contents

| Item 6: | Selected Financial Data |

The following table sets forth certain selected financial information for the five fiscal years as of and for the period ended August 31, 2014. This table should be read in conjunction with the Consolidated Financial Statements and the notes to these statements included in Item 8.

| Year Ended August 31, | ||||||||||||||||||||

| 2014 | 2013 | 2012 (3) | 2011 | 2010 (1) | ||||||||||||||||

| (Dollars in thousands, except share and per share data) | ||||||||||||||||||||

| Operating Data: |

||||||||||||||||||||

| Sales |

$ | 443,873 | $ | 467,250 | $ | 433,151 | $ | 373,763 | $ | 294,517 | ||||||||||

| Cost of sales |

$ | 389,566 | $ | 422,203 | $ | 389,241 | $ | 339,928 | $ | 271,063 | ||||||||||

| Gross margin percentage |

12.2 | % | 9.6 | % | 10.1 | % | 9.1 | % | 8.0 | % | ||||||||||

| Income (loss) from continuing operations |

$ | 7,753 | $ | 4,007 | $ | (9,566 | ) | $ | (5,117 | ) | $ | (9,629 | ) | |||||||

| Income (loss) from discontinued operations |

$ | — | $ | — | $ | — | $ | — | $ | 16,312 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

$ | 7,753 | $ | 4,007 | $ | (9,566 | ) | $ | (5,117 | ) | $ | 6,683 | ||||||||

| Diluted earnings (loss) per share from continuing operations |

$ | 0.60 | $ | 0.32 | $ | (0.78 | ) | $ | (0.42 | ) | $ | (0.84 | ) | |||||||

| Diluted earnings (loss) per share from discontinued operations |

$ | — | $ | — | $ | — | $ | — | $ | 1.41 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted earnings (loss) per share |

$ | 0.60 | $ | 0.32 | $ | (0.78 | ) | $ | (0.42 | ) | $ | 0.57 | ||||||||

| Dividends declared per common share |

$ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||

| Average common shares and equivalents – assuming dilution |

12,857,580 | 12,618,158 | 12,293,749 | 12,250,914 | 11,600,885 | |||||||||||||||

| Balance Sheet Data (as of August 31,): |

||||||||||||||||||||

| Total assets |

$ | 239,190 | $ | 224,618 | $ | 236,179 | $ | 212,414 | $ | 208,408 | ||||||||||

| Capital expenditures |

12,994 | 14,199 | 14,146 | 8,295 | 5,980 | |||||||||||||||

| Long-term debt |

76,665 | 72,739 | 84,004 | 23,802 | 21,038 | |||||||||||||||

| Total debt |

76,849 | 72,970 | 84,462 | 24,223 | 21,467 | |||||||||||||||

| Redeemable preferred stock, Series A (2) |

— | — | — | 38,982 | 34,104 | |||||||||||||||

| Shareholders’ equity |

92,133 | 82,893 | 68,850 | 85,465 | 83,572 | |||||||||||||||

| (1) | Income (loss) from continuing operations included (i) a pre-tax charge of approximately $1.0 million related to unamortized transaction fees associated with the Company’s prior credit facility when the Company refinanced its bank debt and (ii) a loss of approximately $1.6 million related to the termination of the Company’s interest rate swap agreements. Income (loss) from discontinued operations included the reclassification of $13.8 million of currency translation gains from other comprehensive income to earnings following the liquidation of most of the remaining net assets of the Australia/New Zealand Operations. |

| (2) | In fiscal 2010, the Company issued $40.0 million of Series A 15% cumulative non-voting, non-convertible preferred stock (“Series A Preferred Stock”) and 100,000 shares of Series B voting convertible preferred stock (“Series B Preferred Stock”) in a private placement to Zell Credit Opportunities Master Fund, L.P., an investment fund managed by Equity Group Investments, a private investment firm (the “Investor”). Proceeds from the preferred stock issuance of $40.0 million were used to repay bank debt. During fiscal 2012, the Company redeemed all of the Series A Preferred Stock with funds borrowed on the Company’s revolving line of credit. The amount redeemed was $40.0 million plus accrued dividends of $8.9 million. |

21

Table of Contents

| (3) | Income from continuing operations included (i) accelerated discount accretion of $5.5 million and (ii) amortization of issuance costs of $1.1 million, both related to the early redemption of the Series A Preferred Stock and recorded in other non-operating income (expense). The results of operations for Carolina Starches are included since the acquisition on January 11, 2012. |

22

Table of Contents

| Item 7: | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

This Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) should be read in conjunction with the Company’s Consolidated Financial Statements and the accompanying notes. The notes to the Consolidated Financial Statements referred to in this MD&A are included in Part II Item 8, “Financial Statements and Supplementary Data.”

Overview

Penford generates revenues, income and cash flows by developing, manufacturing and marketing specialty natural-based ingredient systems for food and industrial applications, including fuel grade ethanol. The Company develops and manufactures ingredients with starch as a base, providing value-added applications to its customers. Penford’s starch products are manufactured primarily from corn and potatoes and are used principally as binders and coatings in paper, packaging and food production and as an ingredient in fuel.

Penford manages its business in two segments: Industrial Ingredients and Food Ingredients. These segments are based on broad categories of end-market users. See Note 18 to the Consolidated Financial Statements for additional information regarding the Company’s business segment operations.

In January 2012, the Company acquired, through purchase and capital lease, the net assets and operations of the business generally known as Carolina Starches, which manufactures and markets industrial potato starch based products and blends for the paper and packaging industries. The acquisition of this business has provided an important source of raw material to support continued growth in the Company’s Food Ingredients business and has broadened the Company’s portfolio of specialty modified industrial starches.

In March 2014, the Company acquired substantially all of the assets of Gum Technology, an Arizona close corporation, which distributes and blends gums and hydrocolloids for the food and beverage industries in North America and Asia. Gum Technology specializes in developing and producing customized stabilizers to meet customers’ product formulation needs. This acquisition broadened the Company’s Food Ingredients portfolio of functional and specialty ingredient systems. See Note 17 to the Consolidated Financial Statements.