Attached files

| file | filename |

|---|---|

| EX-4.14 - EXHIBIT 4.14 - Axion Power International, Inc. | v391707_ex4-14.htm |

| EX-23.2 - EXHIBIT 23.2 - Axion Power International, Inc. | v391707_ex23-2.htm |

| EX-5.1 - EXHIBIT 5.1 - Axion Power International, Inc. | v391707_ex5-1.htm |

As filed with the Securities and Exchange Commission October 22, 2014 |

Registration Statement No. 333-197978 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 3 to

REGISTRATION STATEMENT

ON FORM S-1

UNDER

THE SECURITIES ACT OF 1933

AXION POWER INTERNATIONAL, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 3690 | 65-0774638 |

| (State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Identification Number) |

| incorporation or organization) | Classification Code Number) |

3601 Clover Lane

New Castle, Pennsylvania 16105

Telephone (724) 654-9300

(Address, including zip code, and telephone number, including

area code, of registrant’s principal executive offices)

David DiGiacinto

Chief Executive Officer

3601 Clover Lane

New Castle, Pennsylvania 16105

Telephone (724) 654-9300

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

with copies to:

| Jolie Kahn, Esq. | Steven M. Skolnick, Esq. |

| 1020 Riverview | Lowenstein Sandler LLP |

| Conshohocken, PA 19428 | 1251 Avenue of the Americas |

| New York, New York 10020 | |

| Telephone (215) 253-6645 | Telephone (212) 262-6700 |

Approximate Date of Commencement of Proposed Sale to the Public: As soon as practicable after the effective date hereof.

| If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x |

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “small reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o |

| Non-accelerated filer o | Smaller reporting company x |

| (Do not check if a smaller reporting company) |

CALCULATION OF REGISTRATION FEE

| Title

of each class of securities to be registered | Proposed

maximum aggregate offering price(1) | Amount of registration fee | ||||||

| Common stock, no par value (2)(3) | $ | 6,900,000 | $ | 1,932 | (7) | |||

| Warrants to purchase common stock(2) | — | (4) | — | (5) | ||||

| Shares of common stock underlying warrants (2)(3) | $ | — | $ | — | ||||

| Representative's warrants | — | — | (6) | |||||

| Shares of common stock underlying Representative's warrants (3) | $ | — | $ | — | ||||

| Total | $ | 6,900,000 | $ | 1,932 | ||||

| (1) | Estimated solely for the purpose of calculating the registration fee under Rule 457(o) of the Securities Act. Offering is now set at $6,900,000. |

| (2) | Includes shares of common stock and warrants to purchase shares of common stock which may be issued upon exercise of a 45-day option granted to the underwriter to cover over-allotments, if any. |

| (3) | Pursuant to Rule 416 under the Securities Act, the securities being registered hereunder include such indeterminate number of additional shares of common stock as may be issued after the date hereof as a result of stock splits, stock dividends or similar transactions. |

| (4) | The warrants to be issued to investors hereunder are included in the price of the common stock above. |

| (5) | No separate registration fee is required pursuant to Rule 457(g) promulgated under the Securities Act. |

| (6) | Assumes the underwriter’s over-allotment is fully exercised. |

| (7) | Paid with filing of the original Registration Statement on Form S-1, filed on August 8, 2014. |

THE REGISTRANT HEREBY AMENDS THIS REGISTRATION STATEMENT ON SUCH DATE OR DATES AS MAY BE NECESSARY TO DELAY ITS EFFECTIVE DATE UNTIL THE REGISTRANT SHALL FILE A FURTHER AMENDMENT WHICH SPECIFICALLY STATES THAT THIS REGISTRATION STATEMENT SHALL THEREAFTER BECOME EFFECTIVE IN ACCORDANCE WITH SECTION 8(a) OF THE SECURITIES ACT OF 1933 OR UNTIL THE REGISTRATION STATEMENT SHALL BECOME EFFECTIVE ON SUCH DATE AS THE COMMISSION, ACTING PURSUANT TO SECTION 8(a), MAY DETERMINE.

INFORMATION CONTAINED HEREIN IS SUBJECT TO COMPLETION OR AMENDMENT. A REGISTRATION STATEMENT RELATING TO THESE SECURITIES HAS BEEN FILED WITH THE SECURITIES AND EXCHANGE COMMISSION. THESE SECURITIES MAY NOT BE SOLD UNTIL THE REGISTRATION STATEMENT BECOMES EFFECTIVE. THIS PROSPECTUS IS NOT AN OFFER TO SELL AND IS NOT A SOLICITATION OF AN OFFER TO BUY IN ANY STATE IN WHICH AN OFFER, SOLICITATION OR SALE IS NOT PERMITTED.

SUBJECT TO COMPLETION, DATED October 22, 2014

PRELIMINARY PROSPECTUS

$6,000,000 of Shares and Warrants

We are offering $6,000,000 of shares of our common stock, $0.005 par value per share, together with warrants to purchase one share of our common stock for each share of common stock sold in this offering.

One share of common stock is being sold together with two warrants, a Series A warrant and a Series B warrant. Each Series A warrant is immediately exerciseable for one share of common stock at an expected exercise price of $3.25 per share and will expire 60 months after the issuance date, and each Series B warrant is immediately exerciseable at an expected exercise price of $3.25 per share and will expire 15 months after the issuance date.

Our common stock is currently traded on the OTCQB Marketplace, operated by OTC Markets Group, under the symbol “AXPW”. Our common stock and Series A warrants have been approved for listing, on The NASDAQ Capital Market under the symbols “AXPW” and “AXPWW”, respectively, subject to official notice of listing. Currently, no public market exists for our Series A warrants and we do not intend to apply for the listing of the Series B warrants on any securities exchange. The shares of common stock, the Series A warrants and the Series B warrants are immediately separable and will be issued separately, but will be purchased together in this offering. On September 24, 2014, the last reported sales price for our common stock was $3.76 per share on the OTCQB Marketplace. On July 7, 2014, our shareholders approved a reverse stock split of our common stock, in a ratio to be determined by our board of directors, of not less than 1-for-20 nor more than 1-for-50. All warrant, option, share and per share information in this prospectus gives retroactive effect for a 1-for-50 split with all numbers rounded up to the nearest whole share. Our stock split was effected and started trading giving effect to the reverse split on September 8, 2014.

INVESTING IN THE OFFERED SECURITIES INVOLVES RISKS, INCLUDING THOSE SET FORTH IN THE “RISK FACTORS” SECTION OF THIS PROSPECTUS BEGINNING ON PAGE 7. INVESTORS SHOULD ONLY CONSIDER AN INVESTMENT IN THESE SECURITIES IF THEY CAN AFFORD THE LOSS OF THEIR ENTIRE INVESTMENT.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR PASSED UPON THE ADEQUACY OR ACCURACY OF THIS PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

| Per Share (1) | Per

Series A Warrant (1) | Per

Series B Warrant (1) |

Total | |||||||||

| Public offering price | $ | $ | $ | $ | ||||||||

| Underwriting discounts and commissions (2) | $ | $ | $ | $ | ||||||||

| Proceeds, before expenses, to us | $ | $ | $ | $ | ||||||||

| (1) | One share of common stock is being sold together with a Series A warrant and a Series B warrant, with each warrant being exercisable for the purchase of one share of common stock. | |

| (2) | We have agreed to issue warrants to the underwriter and to reimburse the underwriter for certain expenses. See “Underwriting” on page 67 of this prospectus for a description of these arrangements. |

The underwriter expects to deliver our securities, against payment, on or about ______ __, 2014.

We have granted the underwriter a 45-day option to purchase up to an additional $900,000 of shares of common stock and/or additional Series A and Series B warrants to purchase shares of common stock from us at the offering price for each security, less underwriting discounts and commissions, to cover over-allotments, if any.

Sole Book Running Manager

Maxim Group LLC

The date of this prospectus is __________, 2014.

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus and any related free writing prospectus that we may provide to you in connection with this offering. We have not, and the underwriter has not, authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not, and the underwriter is not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

For investors outside the United States: neither we nor the underwriter have done anything that would permit this offering or possession or distribution of this prospectus or any free writing prospectus we may provide to you in connection with this offering in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus and any such free writing prospectus outside of the United States.

This summary highlights important information about this offering and our business. It does not include all information you should consider before investing in our common stock. Please review this prospectus in its entirety, including the risk factors and our financial statements and the related notes, before you decide to invest.

References in this prospectus to “we,” “us,” and “our” refer to Axion Power International, Inc. and its subsidiaries.

Our Company

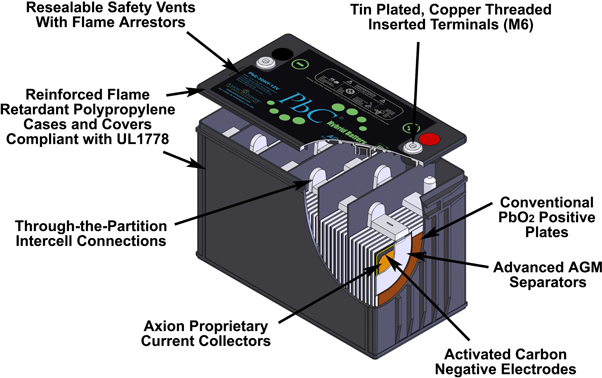

Axion Power Corporation, our wholly owned subsidiary, was formed in September 2003 to acquire and develop certain innovative battery technology. Since inception, Axion Power Corporation has been engaged in research and development of new technology for the production of our PbC (lead carbon) batteries.

In February 2006, we commenced operations at our Clover Lane facility in New Castle, PA. We have utilized this space to manufacture our PbC and specialty lead-acid battery products and to continue to produce and test prototypes which incorporate our developed technology. Through the third quarter of 2014, our Clover Lane plant has allowed us to manufacture batteries for sale under the Axion brand name; to manufacture for third parties under specific contract arrangements; or to manufacture prototypes for our own use and testing, or for testing by our customers. Our facility has been fully tested and found to be in compliance with emission standards established by new federal guidelines in accordance with the Clean Air Act–Title III. In November 2010, we expanded into our Green Ridge facility, which is less than ½ mile from our Clover Lane facility in New Castle, PA, to house offices, research & development, electrode manufacturing and warehousing.

Since inception, our operations have been primarily financed through the sale of equity and debt instruments to investors, with minimal revenue generated from our operations. We transitioned from a research and development based company to a commercial manufacturing company in the fourth quarter of 2012. We have determined that the most efficient use of our resources is to operate as a technology-based enterprise to promote and market our proprietary PbC technology and to streamline manufacturing efforts to focus on our total lead-activated carbon negative electrode. In the fourth quarter of 2014, we will take steps to evaluate and implement the staged phase out of the manufacturing of batteries and the redirection of our efforts toward carbon electrode manufacturing at our Greenridge Facility with some operations still taking place in our Clover Lane facility. We will also continue developing third party PbC battery suppliers, and selling energy storage systems. We believe that this streamlined effort with regard to our carbon negative electrode manufacturing will provide us with the best opportunity to commercialize our technology and thereby provide the potential to improve our financial condition, cash flow and market presence.

As further described below in “Our Business and Our Technology,” we have developed our PbC technology to commercial viability, and have commenced marketing and commercial sales in the United States and internationally. In addition to commercially marketing our PbC batteries as stand-alone products, we have also developed other products, including our Axion PowerCube which is a system, utilizing our PbC batteries, which can, among other things, provide power storage and backup power, and may be configured for different uses and different power levels.

Our Business and Our Technology

The cornerstone of our PbC technology is our proprietary PbC lead carbon battery, which substitutes an activated carbon negative electrode for the standard lead negative electrode in a lead-acid battery construct. All other components of the PbC battery (such as case, cover, separator material, positive plate, electrolyte and other components) are identical to those used in a conventional lead-acid battery. The PbC product is part battery with energy storage capabilities and part asymmetric hybrid supercapacitor with a fast recharge rate, charge acceptance and long cycle life. The construct design results in a relatively low cost device that can be manufactured in iterations that deliver maximum power, or deliver maximum energy, or provide a range of balances between the two. Our PbC battery can be used in applications that service the energy storage needs of several markets including transportation, renewable power, frequency regulation and backup power.

We have devoted more than ten years to research and development on our PbC technology. Our work has focused on developing our intellectual property, characterizing baseline performance, developing proprietary treatment processes for the activated carbon we use in our electrodes, developing proprietary designs, manufacturing techniques for electrode assemblies and fabricating a series of material and design evaluation prototypes that range from single cell to multi-cell batteries for use in energy storage devices and systems.

| 1 |

Our PbC technology is protected by thirteen issued U.S. patents and other proprietary features and structures, and we typically have a number of additional patent applications in process at any point in time. The resulting devices are technically sophisticated yet simple in design. The carbon negative electrode assemblies are fabricated from readily available raw materials using, for the most part, standard industrial processes and techniques. The PbC negative electrodes that are then assembled into PbC batteries can be used with the same case cover, positive plate, separators and electrolyte that are used in conventional lead-acid batteries. Our PbC batteries can be assembled with the same equipment and methodology commonly used for manufacturing conventional lead-acid batteries. PbC batteries use significantly less lead than standard lead-acid batteries with a comparable footprint. Moreover, the lead, plastics and acid employed, just like lead-acid batteries, can be routinely and profitably recycled at existing recycling facilities around the world. A 2007 United States EPA report indicated that in the United States lead-acid batteries are fully recycled 99.2% of the time.

We believe our advanced battery technologies are uniquely situated to answer the current challenges facing both the historic lead-acid battery industry and the challenges facing newer battery chemistries such as lithium-ion, nickel metal hydride, etc. While we further commercialize and continue to explore various potential applications for our PbC technology in the future, these two facilities in New Castle, Pennsylvania will continue to provide us with both an important research and development facility and a production plant in which to produce our lead-free activated carbon negative electrodes. We will also accelerate our development of strategic partners for energy storage manufacture.

In our current strategy, we will be moving away from specialty and contract manufacture of standard lead acid batteries. We will instead focus on our Green Ridge facility for the production of our finished lead-free carbon negative electrode. The facility also provides space for battery string testing and additional storage.

Our objective has consistently been to become an industry leader in the development, production and sourcing of components for cost competitive high performance energy storage systems. Effective as of the fourth quarter of 2014, we will be actively pursuing this strategy in the following core strategies:

| · | Platform technology business model. We are implementing a platform technology business model that will focus on developing and manufacturing carbon electrode assemblies that we can offer for sale to established battery manufacturers who want to use our PbC carbon electrode products in their batteries. | |

| · | Leverage relationships with battery manufacturers. Our business model is based on the premise that, as we continue forward, we can most effectively address the needs of the market by selling PbC negative electrode assemblies to established lead-acid battery manufacturers who want to add advanced battery technology to their existing product lines. We believe this business model should allow us to leverage the business abilities, manufacturing facilities and distribution networks of established manufacturers in order to reduce our time to market and increase our potential market penetration. | |

| · | Build a recognized brand. We believe strong brand name recognition is important in order to increase product awareness and to effectively penetrate the mass market. We intend to differentiate our brand by emphasizing our combination of high performance and low total cost of ownership per storage cycle. | |

| · | Targeted marketing strategy. Markets for motive power, utility grid connected power; renewable energy and standby power (UPS) are becoming increasingly attractive. We are actively pursuing the use of our lead carbon technology products in these markets. | |

| · | Maintain our technical advantage and reduce manufacturing costs. We intend to maintain our technical advantage by continuing to invest in research and development. Our research and development focus will now be working with prospective customers on the commercial application of our PbC technology to fit their unique requirements. |

Our commercial market applications focus is:

| · | Utility applications e.g. frequency regulation |

| · | Buffering, smoothing and micro grid for renewable energy sources (solar and wind) |

| · | Hybrid medium and heavy duty trucks |

| · | Residential and small community energy storage |

| · | Hybrid locomotives |

| · | Hybrid vehicles incorporating stop/start technology |

Recent Developments

The PowerCube is a highly mobile energy storage system that can be configured to deliver up to one megawatt of power for 24 minutes or 100 kilowatts of power for 4.6 hours. Our onsite PowerCube services the PJM frequency regulation market. PJM is a regional transmission organization that coordinates the movement of wholesale electricity to more than 60 million consumers in all or parts of 13 states and the District of Columbia. We provide this frequency regulation through our curtailment services provider (an entity which provides power services on demand to utilities) – Viridity Energy. We commission our onsite PowerCube in November 2011, and it continues to function on a daily basis and serve as a real world demonstration unit. Potential customers visit our project site and can observe the ”real time” screens that show our Cube responding to, and closely following, the PJM REG-D signal. This has been very helpful to us in explaining our technology and model and in providing a real world proof of application. In the first quarter of 2014, we installed batteries, racks, BMS, controller, wiring and miscellaneous equipment at the New Jersey location of our 500 kilowatt system being installed with our strategic partner. It is expected that this unit will participate daily in the PJM frequency regulation market in accordance with our model. Based upon our model and past PJM records –this 500 kilowatt installation will provide the owner with at least $9,000 per month (net after expense) in frequency regulation revenue, which is in addition to the storage and emergency back- up capability the PowerCube is expected to provide.

| 2 |

During the second quarter of 2014, this same customer delivered a purchase order to us for four additional 500 kilowatt PowerCube units designed to provide frequency regulation to PJM in a range covering 500 kilowatts up and 500 kilowatts down. This follow on order is further validation of their belief in our PbC product and our frequency regulation model. This purchase order is the next step in our planned partnership that is expected to include multiple – like sized – 500 kilowatt units in and out of New Jersey. In addition, our partnership is planning larger sized PowerCubes (1megawatt and beyond) in both New Jersey and in other states that have very competitive solar renewable energy credits and other incentives. In a separate initiative with potential new investors, we continue to pursue site selection for multi mega-watt systems that would service the frequency regulation market. Our 1.25 megawatt (or any multiple thereof) building block is an appropriate size for this market.

With regard to our development of smaller scale PowerCubes, in the first quarter of 2014, we sold, installed and subsequently fully commissioned a 10 kilowatt miniCube unit complete with a 12 kilowatt solar array. This unit was installed for a private individual in New Castle, PA and will provide us with additional information about our smaller applications that might be tied to solar and islanded or be grid tied. It will also provide data on the system’s use as an electric vehicle charging station. This is one of our offshore initiatives, so we are very interested in that charging station data. Currently the Owner is using that system to charge his all electric sports car and to net meter.

Our work with ePower Engine Systems, which is a third party entity which develops and markets auxiliary power systems for trucks, continues in accordance with our business plan. We continue to pursue the ePower series hybrid system that incorporates PbC batteries through 56 battery strings in Series 8 heavy duty 18 wheel trucks.

ePower recently purchased four trucks for conversion to their series hybrid system, and we have been issued a purchase order to provide 56 batteries per truck. The conversion of these trucks will allow ePower to continue its progress in improving fuel economy on a mile per gallon basis. Testing has shown that the system has the ability to reduce emissions of all types, which assists in compliance with the U.S. government’s regulatory initiatives in this area.

Effective as of July 1, 2014, Thomas Granville resigned as our Chief Executive Officer and Chairman of the Board due to certain unanticipated adverse health concerns. He will remain one of our directors and will also remain as an employee as Special Assistant to the CEO. Effective August 3, 2014, Mr. Granville resigned as a director and will transition to a consulting role with us.

Effective as of July 1, 2014, David DiGiacinto, who was appointed to our Board of Directors on February 1, 2014, was appointed as our Chief Executive Officer and Chairman of the Board. Also, effective on July 1, 2014, Charles Trego, who was our Chief Financial Officer from April 1, 2010 until August 2, 2013 and has been a Director since September 27, 2013, was appointed as our Interim Chief Financial Officer. Both Mr. DiGiacinto and Mr. Trego shall remain as Directors, although Mr. DiGiacinto and Mr. Trego have resigned from any Committee appointments.

On August 1, 2014, we entered into warrant exchange agreements with the holders of the senior warrants issued in conjunction with our May 7, 2013 senior convertible note financing. Pursuant to the warrant exchange agreements, the holders exchanged all of these warrants for shares of our common stock at a ratio of 1.7 shares (pre 1:50 reverse split) for each warrant exchanged, in a transaction exempt from registration under Section 3(a)(9) of the Securities Act of 1933, as amended. Warrants to purchase 345,623 shares of our common stock were exchanged for 587,558 shares of our common stock.

Pursuant to the warrant exchange agreements, the holders agreed to the following limitations on the resale of the shares:

| · | Through October 31, 2014, each holder may only sell, pledge, assign or otherwise transfer up to 10% of the number of shares issued to it. |

| · | From November 1, 2014 through January 31, 2015, each holder may sell, pledge, assign or otherwise transfer up to an additional 25% of the number of shares issued to it (up to an aggregate of 35% inclusive of the 10% set forth in the bullet point above). |

| · | Through January 31, 2015, each holder may not sell shares during any trading day in an amount, in the aggregate, exceeding 15% of the composite aggregate share trading volume of our common stock measured at the time of each sale of securities during such trading day as reported on Bloomberg. |

| · | However, each holder may sell shares in excess of those permitted under the bullet points above on any trading day on which the VWAP for our common stock for the preceding trading day is at least $9.50 or less than $1.00. |

The warrant exchange agreements contain customary covenants regarding maintenance by us of current reporting status under the Securities Exchange Act of 1934, as amended, and the rules and regulations promulgated thereunder. The warrant exchange agreements also reference our impending reverse stock split and contain provision for adjustment of share and share price adjustments pro rata with the amount of the reverse stock split.

Risk Factors

Investing in our common stock is a speculative proposition, and we encourage you to review our Risk Factors section commencing on p. 7 of this prospectus.

These risks include, but are not limited to, the following:

| · | our early stage of commercialization and our ability to achieve full commercialization of our product ahead of our competitors; |

| · | our ability to achieve market acceptance and to become profitable; |

| · | our ability to engage and retain key personnel, for which we do not carry key man insurance; and |

| · | the dilutive nature of this offering and the potential need to raise further capital in the future, which will have a further dilutive effect on our shareholders. |

| 3 |

Corporate Information

On December 31, 2003, Axion Power Corporation engaged in a reverse acquisition with Tamboril Cigar Company, a public shell company whereby Axion Power Corporation became a wholly owned subsidiary of Tamboril, which subsequently changed its name to Axion Power International, Inc.

Our principal executive office is located at 3601 Clover Lane, New Castle, PA 16105. Our telephone number is (724) 654-9300. Our website is www.axionpower.com. Our website and the information contained on, or that can be accessed through, our website will not be deemed to be incorporated by reference in, and are not considered part of, this prospectus. You should not rely on our website or any such information in making your decision whether to purchase our common stock.

We own various U.S. federal trademark registrations and applications, and unregistered trademarks and servicemarks, including PbCR, our corporate logo and PowerCubeTM. All other trademarks or trade names referred to in this prospectus are the property of their respective owners. Solely for convenience, the trademarks and trade names in this prospectus are referred to without the R and TM symbols, but such references should not be construed as any indicator that their respective owners will not assert, to the fullest extent under applicable law, their rights thereto. We do not intend the use or display of other companies’ trademarks and trade names to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

| 4 |

Summary of the Offering

| Securities offered: | $6,000,000 of shares of our common stock together with (i) a Series A warrant to purchase one share of our common stock at an expected exercise price of $3.25 per share and (ii) a Series B warrant to purchase one share of our common stock at an expected exercise price of $3.25 per share, for each share sold in the offering. The warrants will be immediately exercisable and the Series A warrants will expire 60 months after the issuance date and the Series B warrants will expire 15 months after the issuance date. | |

| Common stock outstanding before the offering (1): | 5,017,792 shares | |

| Common stock to be outstanding after the offering (1): | 6,863,946 shares | |

| Estimate of Proceeds: | $6,000,000 |

| Use of proceeds: | We intend to use a portion of the net proceeds from this offering for the following purposes: |

| Proceeds: | ||||

| Gross Proceeds | $ | 6,000,000 | ||

| Fees and Expenses | (825,000 | ) | ||

| Net Proceeds | $ | 5,175,000 | ||

| Uses: | ||||

| Operations | $ | 5,175,000 | ||

| Total Uses | $ | 5,175,000 | ||

| Risk Factors: | Investing in our securities involves substantial risks. You should carefully review and consider the “Risk Factors” section of this prospectus beginning on page 7 and the other information in this prospectus for a discussion of the factors you should consider before you decide to invest in this offering. | |

| Proposed Listing and Symbol: | NASDAQ Capital Markets under the symbol “AXPW” for our common stock and “AXPWW” for our Series A warrants. We do not intend to apply for listing for our Series B warrants on any securities exchange. | |

|

||

| Reverse Split: | All warrant, option, share and per share information in this prospectus gives retroactive effect for a 1-for-50 split. |

| 5 |

| (1) | Unless otherwise stated, all information contained in this prospectus reflects an assumed public offering price of $3.25 per share. The total number of shares of our common stock outstanding after this offering is based on 5,017,792 shares outstanding as of September 24, 2014 and excludes as of that date, the following: |

| · | 38,402 shares of common stock issuable upon exercise of the warrants issued in conjunction with the May 2013 subordinated convertible notes outstanding as of September 24, 2014, at a conversion price of $15.10 per share; |

| · | 60,606 shares of common stock issuable upon conversion of the Subordinated Convertible notes outstanding as of September 24, 2014, at an exercise price of $13.20 per share; |

| · | 913 shares of common stock issuable upon the exercise of warrants (other than the warrants issued in conjunction with the May 2013 senior convertible notes and the warrants issued in conjunction with the May 2013 subordinated convertible notes) outstanding as of September 24, 2014, at a weighted average exercise price of $100.00 per share; | |

| · | 54,541 shares of common stock issuable upon exercise of Placement Agent warrants outstanding as of September 24, 2014, at a conversion price of $15.10 per share; |

| · | 91,877 shares of common stock issuable upon the exercise of options outstanding as of September 24, 2014, at a weighted average exercise price of $57.50 per share; |

| · | 46,148 shares of common stock reserved for future grant or issuance as of September 24, 2014 under all of our 2004 Outside Directors Stock Option Plan and our 2010 Employees and Officers Stock Option Plan; |

| · | 1,846,154 shares of common stock issuable upon exercise of the warrants issued to the public in connection with this offering; and |

| · | 92,308 shares of common stock issuable upon exercise of the warrants to be received by the underwriter in connection with this offering. |

Except as otherwise indicated herein, all information in this prospectus assumes the underwriter does not sell any common stock or warrants contained in the over-allotment option and the warrants offered hereby are not exercised.

| 6 |

Investing in our common stock is very speculative and involves a high degree of risk. You should carefully consider all of the information in this report before making an investment decision. The following are among the risks we face related to our business, assets and operations. They are not the only risks we face. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may also arise. Any of these risks could materially and adversely affect our business, results of operations and financial condition, which in turn could materially and adversely affect the trading price of our common stock. You should not purchase our shares unless you can afford to lose your entire investment.

RISKS RELATED TO OUR FINANCIAL POSITION

We have a history of operating losses. We expect to incur operating losses in the future and we may never achieve or sustain profitability.

We have historically incurred substantial operating losses, including operating losses of $2.4 million and $4.4 million for the three and six months ended June, 2014, respectively, and $8.2 million and $8.6 million for the years ended December 31, 2013 and 2012, respectively. At June 30, 2014, we had an accumulated deficit of $105.1 million. These losses have had, and will continue to have, an adverse effect on our working capital, total assets, and stockholders’ equity. Because of the numerous risks and uncertainties associated with our business, including whether we will be able to develop future demand for our product in the form of purchase orders sufficient to sustain our business model, we are unable to predict when we will become profitable, and we may never become profitable. Even if we do achieve profitability, we may not be able to sustain or increase profitability on a quarterly or annual basis. Our inability to achieve and then sustain profitability would have a material adverse effect on our results of operations and business.

Our independent registered public accounting firm’s report for the fiscal year ended December 31, 2013 includes an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern.

Due to the uncertainty of our ability to meet our cash requirements to fund our current operations, working capital, and capital spending, in their report on our audited annual financial statements as of and for the year ended December 31, 2013, our independent auditors included an explanatory paragraph regarding concerns about our ability to continue as a going concern. Recurring losses from operations raise substantial doubt about our ability to continue as a going concern. If we are unable to continue as a going concern, we might have to liquidate our assets and the values we receive for our assets in liquidation or dissolution could be significantly lower than the values reflected in our financial statements. In addition, the inclusion of an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern and our lack of cash resources may materially adversely affect our share price and our ability to raise new capital or to enter into critical contractual relations with third parties.

We are in the early stages of commercialization and our products may never achieve significant commercial market acceptance.

Our success depends on our ability to develop and market products that are recognized as superior to those currently existing in the marketplace. Most of our potential customers currently use other products using different technology and may be reluctant to change those methods to a new technology. Market acceptance will depend on many factors, including our ability to convince potential customers that our PbC battery solution is an attractive alternative to existing products. We will need to demonstrate that our products provide reliable and cost-effective alternatives to existing products. Compared to most competing technologies, our technology is relatively new, and most potential customers have limited knowledge of, or experience with, our products. Prior to adopting our technology, potential customers may be required to devote significant time and effort to testing and validating our products. Many factors influence the perception of a new technology, including its use by leaders in the industry. If we are unable to continue to induce these leaders to adopt our technology, acceptance and adoption of our products could be slowed. In addition, if our products fail to gain significant acceptance in the marketplace and we are unable to expand our customer base, we may never generate sufficient revenue to achieve or sustain profitability.

We have an obligation to repay a $735,000 principal amount subordinated note by December 31, 2014, and if we do not satisfy this obligation, the noteholder has the right to demand payment in full or exercise remedies.

On June 30, 2014, we entered into an amended note with respect to that certain $735,000 principal amount subordinated note issued to Robert Averill on May 7, 2013. This amended note extends the maturity date to December 31, 2014. We secured the obligations under the amended note with a lien on our intellectual property assets. If we do not negotiate an extension or satisfy this note, Mr. Aveill can pursue remedies, including, asserting his lien on our intellectual property assets, which could have a material adverse affect on our ability to use our technology.

| 7 |

Our sales cycle is lengthy and variable, which makes it difficult for us to forecast revenue and other operating results.

The sales cycle for our products is lengthy, which makes it difficult for us to accurately forecast revenue in a given period, and may cause revenue and operating results to vary significantly from period to period. Some potential customers for our products typically need to commit significant time and resources to evaluate the technology used in our products and their decision to purchase our products may be further limited by budgetary constraints and numerous layers of internal review and approval, which are beyond our control. We spend substantial time and effort assisting potential customers in evaluating our products, including providing demonstrations and validation. Even after initial approval by appropriate decision makers, the negotiation and documentation processes for the actual adoption of our products can be lengthy. As a result of these factors, based on our experience to date, our sales cycle, the time from initial contact with a prospective customer to routine commercial utilization of our products, has varied and can sometimes be several months or longer, which has made it difficult for us to accurately project revenues and other operating results. In addition, the revenue generated from sales of our products may fluctuate from time to time due to market and general economic conditions. As a result, our financial results may fluctuate on a quarterly basis which may adversely affect the price of our common stock.

We will need to raise additional funds through debt or equity financings in the future to achieve our business objectives and to satisfy our cash obligations, which would dilute the ownership of our existing shareholders and possibly subordinate certain of their rights to the rights of new investors.

In addition to the funds raised in this offering, which we expect would cover our cash flow needs until December 31, 2015, we will need to raise additional funds through debt or equity financings in order to complete our ultimate business objectives, including funding working capital to support fulfillment of future orders for our products to pay-off our subordinated notes. We also may choose to raise additional funds in debt or equity financings if they are available to us on reasonable terms to increase our working capital, strengthen our financial position or to make acquisitions. Any sales of additional equity or convertible debt securities would result in dilution of the equity interests of our existing shareholders, which could be substantial. Additionally, if we issue shares of preferred stock or convertible debt to raise funds, the holders of those securities might be entitled to various preferential rights over the holders of our common stock, including repayment of their investment, and possibly additional amounts, before any payments could be made to holders of our common stock in connection with an acquisition of us. Such preferred shares, if authorized, might be granted rights and preferences that would be senior to, or otherwise adversely affect, the rights and the value of our common stock. Also, new investors may require that we and certain of our shareholders enter into voting arrangements that give them additional voting control or representation on our board of directors.

RISKS RELATED TO OUR BUSINESS OPERATIONS

We depend on key personnel, and our business may be severely disrupted if we lose the services of our senior management, employees, and consultants.

Our business is dependent upon the knowledge and experience of our key scientists, engineers, manufacturing staff and senior management. Given the competitive nature of our industry, there is the risk that one or more of our key scientists or engineers will resign their positions, which could have a disruptive impact on our operations. If any of our key scientists, engineers or senior management do not continue in their present positions, we may not be able to easily replace them and our business may be severely disrupted. We face competition for such personnel. If any of these individuals joins a competitor or forms a competing company, we could lose important know-how and experience and incur substantial expense to recruit and train suitable replacements. Our Compensation Committee remains committed to keeping our key team members in place as we move further into our commercialization stage of our PbC product. Currently, all of our key employees have employment contracts that include non-compete provisions.

| 8 |

We may be unable to manage our future growth effectively, which could make it difficult to execute our business strategy.

We commenced our formal commercial launch in the fourth quarter of 2012 and anticipate growth in our business operations. We expect to increase our number of employees further as our business grows. This future growth could create strain on our organizational, administrative and operational infrastructure, including laboratory operations, quality control, customer service and sales and marketing. Our ability to manage our growth properly will require us to continue to improve our operational, financial, and management controls, as well as our reporting systems and procedures. If our current infrastructure is unable to handle our growth, we may need to expand our infrastructure and staff and implement new decision making and reporting systems. The time and resources required to implement such expansion and systems could adversely affect our decision making and operations. Our expected future growth will impose significant added responsibilities on members of management, including the need to identify, recruit, maintain, and integrate additional employees. Our future financial performance and our ability to commercialize our products and to compete effectively will depend, in part, on our ability to manage this potential future growth effectively, without compromising quality and customer satisfaction.

Our operations expose us to litigation, tax, environmental and other legal compliance risks.

We are subject to a variety of litigation, tax, environmental, health and safety and other legal compliance risks. These risks include, among other things, possible liability relating to product liability matters, personal injuries, intellectual property rights, contract-related claims, government contracts, taxes, health and safety liabilities, environmental matters and compliance with U.S. and foreign laws, competition laws and laws governing improper business practices. We or one of our business units could be charged with wrongdoing as a result of such matters. If convicted or found liable, we could be subject to significant fines, penalties, repayments or other damages (in certain cases, treble damages). As a business with international reach, we are subject to complex laws and regulations in the U.S. and other countries in which we operate. Those laws and regulations may be interpreted in different ways. They may also change from time to time, as may related interpretations and other guidance. Changes in laws or regulations could result in higher expenses and payments, and uncertainty relating to laws or regulations may also affect how we conduct our operations and structure our investments and could limit our ability to enforce our rights.

In the area of taxes, changes in tax laws and regulations, as well as changes in related interpretations and other tax guidance could materially impact our tax receivables and liabilities and our deferred tax assets and tax liabilities. Additionally, in the ordinary course of business, we are subject to examinations by various authorities, including tax authorities. In addition to ongoing investigations, there could be additional investigations launched in the future by governmental authorities in various jurisdictions and existing investigations could be expanded. The global and diverse nature of our operations means that these risks will continue to exist and additional legal proceedings and contingencies will arise from time to time. Our results may be affected by the outcome of legal proceedings and other contingencies that cannot be predicted with certainty.

In the sourcing of our products throughout the world, we process, store, dispose of and otherwise use large amounts of hazardous materials, especially lead and acid. As a result, we are subject to extensive and changing environmental, health and safety laws and regulations governing, among other things: the generation, handling, storage, use, transportation and disposal of hazardous materials; remediation of polluted ground or water; emissions or discharges of hazardous materials into the ground, air or water; and the health and safety of our employees. Compliance with these laws and regulations results in ongoing costs. Failure to comply with these laws or regulations, or to obtain or comply with required environmental permits, could result in fines, criminal charges or other sanctions by regulators. Our ongoing compliance with environmental, health and safety laws, regulations and permits could require us to incur significant expenses, limit our ability to modify or expand our facilities or continue production and require us to install additional pollution control equipment and make other capital improvements. In addition, private parties, including current or former employees, could bring personal injury or other claims against us due to the presence of, or exposure to, hazardous substances used, stored or disposed of by us or contained in our products.

| 9 |

Changes in environmental and climate laws or regulations, including laws relating to greenhouse gas emissions, could lead to new or additional investment in production designs and could increase environmental compliance expenditures. Changes in climate change concerns, or in the regulation of such concerns, including greenhouse gas emissions, could subject us to additional costs and restrictions, including increased energy and raw materials costs. Additionally, we cannot assure you that we have been or at all times will be in compliance with environmental laws and regulations or that we will not be required to expend significant funds to comply with, or discharge liabilities arising under, environmental laws, regulations and permits, or that we will not be exposed to material environmental, health or safety litigation.

We are subject to stringent federal and state environmental and safety regulation, and we do not cover environmental impairment insurance, so we may suffer material adverse effects if any fines are ever imposed.

We use or generate certain hazardous substances in our research and manufacturing facilities. We are subject to varying regulations including OSHA and CERCLA and state equivalents. We do not carry environmental impairment insurance. We believe that all permits and licenses required for our current business activities are in place. Although we do not know of any material environmental, safety or health problems in our property or processes, there can be no assurance that problems will not develop in the future which could have a material adverse effect on our business, results of operation, or financial condition.

Our products contain hazardous materials including lead, and any discharge could lead to monetary damages and fines.

Lead is a toxic material that is an important raw material in our batteries. We also use, generate and discharge other toxic, volatile and hazardous chemicals and wastes in our research, development and manufacturing activities. We are required to comply with federal, state and local laws and regulations regarding pollution control and environmental protection. Under some statutes and regulations, a government agency, or other parties, may seek to recover response costs from operators of property where releases of hazardous substances have occurred or are ongoing, even if the operator was not responsible for such release or otherwise at fault. In addition, more stringent laws and regulations may be adopted in the future, and the costs of complying with those laws and regulations could be substantial. If we fail to control the use of, or inadequately restrict the discharge of, hazardous substances, we could be subject to significant monetary damages and fines, or be forced to suspend certain operations.

As we sell our products, we may become the subject of product liability claims, and we could face substantial fines which exceed our resources.

Due to the hazardous nature of many of the key materials used in the manufacturing of our batteries, the producers of such products may be exposed to a greater number of product liability claims, including possible environmental claims. We currently have domestic general liability insurance up to $1,000,000 per occurrence and $2,000,000 in the aggregate to protect us against the risk that in the future a product liability claim or product recall could materially and adversely affect our business operations. Inability to obtain sufficient insurance coverage at an acceptable cost or otherwise to protect against potential product liability claims could prevent or inhibit the commercialization of our product. We cannot assure you that as we continue distribution of our products that we will be able to obtain or maintain adequate coverage on acceptable terms, or that such insurance will provide adequate coverage against all potential claims. Even if we maintain adequate insurance, any successful claim could materially and adversely affect our reputation and prospects, and divert management’s time and attention. If we are sued for any injury allegedly caused by our future products our liability could exceed our total assets and our ability to pay such liability.

We have limited manufacturing experience with respect to our PbC technology, which may translate into cost overruns in manufacturing our products.

We have limited manufacturing experience with respect to production of our commercial PbC negative electrodes in quantities required to achieve our operational goals, and we may not be able to retain a qualified manufacturing staff or effectively manage the manufacturing of our proposed products when we are ready to do so. We began the commercial production of our energy storage devices in the fourth quarter of 2012. As production levels increase, we may experience cost overruns in manufacturing our PbC products, and we may not have sufficient capital in the future to successfully complete such tasks. In addition, we may not be able to manufacture our products because of industry conditions, general economic conditions, and/or competition from potential manufacturers and distributors. These inabilities could cause us to abandon our current business plan and may cause our operations to eventually fail.

| 10 |

We need to continue to improve the performance of our commercial PbC products to meet future requirements and competitive pressures.

We need to continue to improve various aspects of our PbC technology as we move forward with larger scale production and new applications of our products. Future developments and competition may reveal additional technical issues that are not currently recognized as obstacles. If we cannot continue to improve the performance of our products in a timely manner, we may be forced to redesign or delay large scale production or possibly abandon our product development efforts altogether.

We do not have any long-term supplier contracts.

We currently purchase the raw materials for our carbon electrodes and a variety of other components from third parties. We also intend to outsource manufacture of batteries using our carbon electrodes (which we will continue to manufacture in house). We do not have any long-term contracts with suppliers of raw materials and components, and our current suppliers may be unable to satisfy our future requirements on a timely basis. We have not yet secured an outsourced manufacturer for our batteries and we cannot assure that such a manufacturer will be able to satisfy our future requirements on a timely basis. Moreover, the price of purchased raw materials, components and assembled batteries could fluctuate significantly due to circumstances beyond our control. If our current suppliers and outsourced manufactures are unable to satisfy our long-term requirements on a timely basis, we may be required to seek alternative sources for necessary materials and components or redesign our proposed products to accommodate available substitutes.

We are a small player in an intensely competitive international market and may be unable to compete.

The lead-acid battery industry is large, intensely competitive and resistant to technological change. We may need to compete or enter into further strategic relationships with well-established companies that are much larger and have greater financial capital and other resources than we do. We may be unable to convince end users that products based on our PbC technology are superior to available alternatives. Moreover, if competitors introduce similar products, they may have a greater ability to withstand price competition and finance their marketing programs. There is no assurance that we will be able to compete effectively.

Our failure to introduce new products and product enhancements and broad market acceptance of new technologies introduced by our competitors could adversely affect our business.

Many new energy storage technologies have been introduced over the past several years. For certain important and growing international energy storage markets, lithium-based battery technologies have a large and growing market share. Our ability to achieve significant and sustained penetration of our key target markets will depend upon our success in developing or acquiring these and other technologies, either independently, through joint ventures or through acquisitions. If we fail to develop or acquire, and manufacture and sell, products that satisfy our customers’ demands, or we fail to respond effectively to new product announcements by our competitors by quickly introducing competitive products, then market acceptance of our products could be reduced and our business could be adversely affected. We cannot assure you that our products will remain competitive with products based on new technologies.

To the extent we enter into strategic relationships, we will be dependent upon our partners.

Some of our products are not intended for direct sale to end users and our business may require us to enter into strategic relationships with manufacturers of other power industry equipment that use batteries and other energy storage devices as important components of their finished products. The agreements governing any future strategic relationships may not provide us with control over the activities of any strategic relationship we negotiate and our future partners, if any, could retain the right to terminate the strategic relationship at their option. Our future partners will have significant discretion in determining the efforts and level of resources that they dedicate to our products and may be unwilling or unable to fulfill their obligations to us. In addition, our future partners may develop and commercialize, either alone or with others, products that are similar to or competitive with the products that we intend to produce.

| 11 |

RISKS RELATED TO OUR INTELLECTUAL PROPERTY

We may rely on licenses for our PbC technology, which may affect our continued operations with respect thereto.

As we develop our PbC technology, we may need to license additional technologies to optimize the performance of our products. We may not be able to license these technologies on commercially reasonable terms or at all. In addition, we may fail to successfully integrate any licensed technology into our proposed products. Our inability to obtain any necessary licenses could delay our product development and testing until alternative technologies can be identified, licensed and integrated. The inability to obtain any necessary third-party licenses could cause us to abandon a particular development path, which could seriously harm our business, financial position and results of our operations.

New technology may lead to our competitors developing superior products which would reduce demand for our products.

Research into the electrochemical applications for carbon nanotechnology and other storage technologies is proceeding at a rapid pace, and many private and public companies and research institutions are actively engaged in the development of new battery technologies based on carbon nanotubes, nanostructured carbon materials and other non-carbon materials. These new technologies may, if successfully developed, offer significant performance or price advantages when compared with our technologies. There is no assurance that our existing patents or our pending and proposed patent applications will offer meaningful protection if a competitor develops a novel product based on a new technology.

If we are unable to protect our proprietary technology and preserve our trade secrets, we will increase our vulnerability to competitors which could materially adversely impact our ability to remain in business.

Our ability to successfully commercialize our products will depend on our ability to protect those products and our technology with domestic and foreign patents. We will also need to continue to preserve our trade secrets. The issuance of a patent is not conclusive as to its validity or as to the enforceable scope of the claims of the patent. The patent positions of technology companies, including us, are uncertain and involve complex legal and factual issues.

We cannot assure you that our patents will prevent other companies from developing similar products or products which produce benefits substantially the same as our products, or that other companies will not be issued patents that may prevent the sale of our products or require us to pay significant licensing fees in order to market our products.

From time to time, we may need to obtain licenses to patents and other proprietary rights held by third parties in order to develop, manufacture and market our products. If we are unable to timely obtain these licenses on commercially reasonable terms, our ability to commercially exploit such products may be inhibited or prevented. Additionally, we cannot assure investors that any of our products or technology will be patentable or that any future patents we obtain will give us an exclusive position in the subject matter claimed by those patents. Furthermore, we cannot assure investors that our pending patent applications will result in issued patents, that patent protection will be secured for any particular technology, or that our issued patents will be valid or enforceable or provide us with meaningful protection.

If we are required to engage in expensive and lengthy litigation to enforce our intellectual property rights, the costs of such litigation could be material to our results of operations, financial condition and liquidity and, if we are unsuccessful, the results of such litigation could materially adversely impact our entire business.

Although we have entered into invention assignment agreements with our employees and with certain advisors, if those employees or advisors develop inventions or processes independently which may relate to products or technology under development by us, disputes may also arise about the ownership of those inventions or processes. Time-consuming and costly litigation could be necessary to enforce and determine the scope of our rights under these agreements.

| 12 |

We also rely on confidentiality agreements with our strategic partners, customers, suppliers, employees and consultants to protect our trade secrets and proprietary know-how. We may be required to commence litigation to enforce such agreements, and it is certainly possible that we will not have adequate remedies for breaches of our confidentiality agreements.

Other companies may claim that our technology infringes on their intellectual property or proprietary rights and commence legal proceedings against us which could be time-consuming and expensive and could result in our being prohibited from developing, marketing, selling or distributing our products.

Because of the complex and difficult legal and factual questions that relate to patent positions in our industry, we cannot assure you that our products or technology will not be found to infringe upon the intellectual property or proprietary rights of others. Third parties may claim that our products or technology infringe on their patents, copyrights, trademarks or other proprietary rights and demand that we cease development or marketing of those products or technology or pay license fees. We may not be able to avoid costly patent infringement litigation, which will divert the attention of management away from the development of new products and the operation of our business. We cannot assure investors that we would prevail in any such litigation. If we are found to have infringed on a third party’s intellectual property rights, we may be liable for money damages, encounter significant delays in bringing products to market or be precluded from manufacturing particular products or using particular technology.

Other parties may challenge certain of our foreign patent applications. If such parties are successful in opposing our foreign patent applications, we may not gain the protection afforded by those patent applications in particular jurisdictions and may face additional proceedings with respect to similar patents in other jurisdictions, as well as related patents. The loss of patent protection in one jurisdiction may influence our ability to maintain patent protection for the same technology in other jurisdictions.

RISKS RELATED TO THIS OFFERING

We may allocate net proceeds from this offering in ways which differ from our estimates based on our current plans and assumptions discussed in the section entitled “Use of Proceeds” and with which you may not agree.

The allocation of net proceeds of the offering set forth in the “Use of Proceeds” section below represents our estimates based upon our current plans and assumptions regarding industry and general economic conditions, our future revenues and expenditures. The amounts and timing of our actual expenditures will depend on numerous factors, including market conditions, cash generated by our operations, business developments and related rate of growth. We may find it necessary or advisable to use portions of the proceeds from this offering for other purposes. Circumstances that may give rise to a change in the use of proceeds and the alternate purposes for which the proceeds may be used are discussed in the section entitled “Use of Proceeds” below. You may not have an opportunity to evaluate the economic, financial or other information on which we base our decisions on how to use our proceeds. As a result, you and other stockholders may not agree with our decisions. See “Use of Proceeds” section for additional information.

Future sales by our stockholders may adversely affect our stock price and our ability to raise funds in new stock offerings.

Sales of our common stock by our stockholders and warrant or option holders following this offering could lower the market price of our common stock. Sales may also make it more difficult for us to sell equity securities or equity-related securities in the future at a time and price that our management deems acceptable or at all. Of the 5,017,792 shares of common stock outstanding as of September 24, 2014, all but approximately 247,297 of which are, or will be, freely tradable without restriction, unless held by our “affiliates.” Some of these shares may be resold under Rule 144 of the Securities Act of 1933, as amended (“Securities Act”). Additionally, the sale of shares underlying our outstanding warrants and options, including the warrants to be sold in this offering, could also lower the market price of our common stock.

| 13 |

You will experience immediate and substantial dilution as a result of this offering and may experience additional dilution in the future.

You will incur immediate and substantial dilution as a result of this offering. After giving effect to the sale by us of up to 1,846,154 shares of common stock and corresponding warrants offered in this offering at an assumed public offering price of $3.25 per share, and after deducting underwriter commissions and estimated offering expenses payable by us, investors in this offering can expect an immediate dilution of $1.68 per share, or 51.6%, at the public offering price, assuming no exercise of the warrants. In addition, in the past, we issued options and warrants to acquire shares of common stock and may need to do so in the future to support our operations. To the extent these options and/or warrants are ultimately exercised, you will sustain future dilution.

Holders of warrants will have no rights as common stockholders until such holders exercise their warrants and acquire our common stock.

Until holders of warrants acquire shares of our common stock upon exercise of the warrants, holders of warrants will have no rights with respect to the shares of our common stock underlying such warrants. Upon exercise of the warrants, the holders will be entitled to exercise the rights of a common stockholder only as to matters for which the record date occurs after the exercise date.

There is no public market for the warrants to purchase common stock in this offering.

There is no established public market for the Series A or Series B warrants and a market may not develop in this offering. In addition, we do not intend to apply to list the Series B warrants on any securities exchange. Without an active market, the liquidity of the warrants will be limited.

RISKS RELATED TO OUR COMMON STOCK

We have issued a large number of warrants and options, which if exercised would substantially increase the number of common shares outstanding.

On September 24, 2014, we had 5,017,792 shares of common stock outstanding, and (a) we had warrants outstanding that, if fully exercised, would generate proceeds of $1,494,767 and cause us to issue up to an additional 93,856 shares of common stock, and (b) we had options outstanding to purchase common stock that, if fully exercised, would generate proceeds of $5,690,504 and result in the issuance of an additional 138,025 shares of common stock, and (c) we have subordinated convertible notes convertible into our common stock that if fully converted would result in the issuance of 60,606 shares of common stock (not including interest).

As a key component of our growth strategy we have provided and intend to continue offering compensation packages to our management and employees that emphasize equity-based compensation and would thus cause further dilution.

Historically, we have not paid dividends on our common stock, and we do not anticipate paying any cash dividends in the foreseeable future.

We have never paid cash dividends on our common stock. We intend to retain our future earnings, if any, to fund operational and capital expenditure needs of our business, and we do not anticipate paying any cash dividends in the foreseeable future. Furthermore, future financing instruments may do the same. As a result, capital appreciation, if any, of our common stock will be the sole source of gain for our common stockholders in the foreseeable future.

Our stock price is speculative and there is a risk of litigation.

The trading price of our common stock has in the past and may in the future be subject to wide fluctuations in response to factors such as the following:

| • | revenue or results of operations in any quarter failing to meet the expectations, published or otherwise, of the investment community; | |

| • | reduced investor confidence in equity markets, due in part to corporate collapses in recent years; | |

| • | speculation in the press or analyst community; | |

| • | wide fluctuations in stock prices, particularly with respect to the stock prices for other technology companies; | |

| 14 |

| • | announcements of technological innovations by us or our competitors; | |

| • | new products or the acquisition of significant customers by us or our competitors; | |

| • | changes in interest rates; | |

| • | changes in investors’ beliefs as to the appropriate price-earnings ratios for us and our competitors; | |

| • | changes in recommendations or financial estimates by securities analysts who track our common stock or the stock of other battery companies; | |

| • | changes in management; | |

| • | sales of common stock by directors and executive officers; | |

| • | rumors or dissemination of false or misleading information, particularly through Internet chat rooms, instant messaging, and other rapid-dissemination methods; | |

| • | conditions and trends in the battery industry generally; | |

| • | the announcement of acquisitions or other significant transactions by us or our competitors; | |

| • | adoption of new accounting standards affecting our industry; | |

| • | general market conditions; | |

| • | domestic or international terrorism and other factors; and | |

| • | the other factors described in this section. |

Fluctuations in the price of our common stock may expose us to the risk of securities class action lawsuits. Although no such lawsuits are currently pending against us and we are not aware that any such lawsuit is threatened to be filed in the future, there is no assurance that we will not be sued based on fluctuations in the price of our common stock. Defending against such suits could result in substantial cost and divert management’s attention and resources. In addition, any settlement or adverse determination of such lawsuits could subject us to significant liability.

Future sales of our common stock could depress our stock price.

Sales of a large number of shares of our common stock, or the availability of a large number for sale, could materially adversely affect the per share market price of our common stock and could impair our ability to raise funds in addition offering of our debt or equity securities. In the event that we propose to register shares of common stock under the Securities Act for our own account, certain shareholders are entitled to receive notice of that registration to include their shares in the registration, subject to limitations described in the agreements granting these rights.

We have applied for listing of our common stock and the warrants issued in this offering on the NASDAQ Capital Market in connection with this offering. If we fail to comply with the continuing listing standards of The NASDAQ Capital Market, our securities could be delisted.

We expect that our common stock will be eligible to be quoted on the NASDAQ Capital Market. For our common stock to maintain listing on the NASDAQ Capital Market, we must maintain NASDAQ Capital Market continued listing requirements including but not limited to requirements to obtain shareholder approval of a transaction other than a public offering involving the sale or issuance equal to 20% or more of our common stock, our common stock could be delisted from the NASDAQ Capital Market. If our common stock were to be delisted from the NASDAQ Capital Market, our common stock could continue to trade on the over-the-counter bulletin board following any delisting from the NASDAQ Capital Market, or on the Pink Sheets, as the case may be. Any such delisting of our common stock could have an adverse effect on the market price of, and the efficiency of the trading market for, our common stock, not only in terms of the number of shares that can be bought and sold at a given price, but also through delays in the timing of transactions and less coverage of us by securities analysts, if any. Also, if in the future we were to determine that we need to seek additional equity capital, it could have an adverse effect on our ability to raise capital in the public or private equity markets.

| 15 |

Risks Associated with Our Reverse Stock Split

On September 8, 2014, we effected a one-for-50 reverse stock split. However, the reverse stock split may not result in a proportionate increase in the price of our common stock, in which case we may not be able to list our common stock and the warrants sold in this offering on The NASDAQ Capital Market, in which case this offering will not be completed.

We expect that the one-for-50 reverse stock split of our outstanding common stock will increase the market price of our common stock so that we will be able to meet the minimum bid price requirement of the listing rules of The NASDAQ Capital Market. However, the effect of a reverse stock split upon the market price of our common stock cannot be predicted with certainty, and the results of reverse stock splits by companies in similar circumstances have been varied. It is possible that the market price of our common stock following the reverse stock split will not increase sufficiently for us to be in compliance with the minimum bid price requirement. If we are unable meet the minimum bid price requirement, we may be unable to list our shares on The NASDAQ Capital Market, in which case this offering will not be completed.

Even if the reverse stock split achieves the requisite increase in the market price of our common stock, we cannot assure you that we will be able to continue to comply with the minimum bid price requirement of The NASDAQ Capital Market.

Even if the reverse stock split achieves the requisite increase in the market price of our common stock to be in compliance with the minimum bid price of The NASDAQ Capital Market, there can be no assurance that the market price of our common stock following the reverse stock split will remain at the level required for continuing compliance with that requirement. It is not uncommon for the market price of a company’s common stock to decline in the period following a reverse stock split. If the market price of our common stock declines following the effectuation of the reverse stock split, the percentage decline may be greater than would occur in the absence of a reverse stock split. In any event, other factors unrelated to the number of shares of our common stock outstanding, such as negative financial or operational results, could adversely affect the market price of our common stock and jeopardize our ability to meet or maintain The NASDAQ Capital Market’s minimum bid price requirement.