Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - 180 DEGREE CAPITAL CORP. /NY/ | v387225_8k.htm |

| EX-99.2 - EXHIBIT 99.2 - 180 DEGREE CAPITAL CORP. /NY/ | v387225_ex99-2.htm |

Fellow Shareholders:

Half way through 2014, we remain focused on our strategy of realize, invest, partner and return.

In the first six months of this year, we realized a gain on our Molecular Imprints investment upon its sale to Canon, and we realized a loss on our Kovio investment upon the disposition of its assets to a publicly traded Norwegian firm, Thin Film Electronics. Also, we continued to realize a gain on our public positions in Solazyme and Champions.

On April 18, 2014, Canon completed the acquisition of Molecular Imprints (MII) semiconductor lithography equipment business. We received $6.48 million at the close of the transaction, and we could receive an additional $625,000 from amounts held in escrow as well as up to $1.7 million upon the achievement of certain milestones. With the closing of the transaction, a new spin-out company was formed and retained the corporate name of Molecular Imprints, Inc. This company will continue development and commercialization of the technology for consumer and biomedical applications. We received shares in this new company. I like to think of it as having two bites at the apple.

It is worth noting that Harris & Harris Group was the only investor group to have a realized gain at the close of this transaction. This was a result of a strategic investment we were able to make during the first half of 2011 owing to the nature of our permanent capital. The other existing investors had little or no funds left to invest in MII because it took longer than their fund life to realize the acquisition from Canon. We were able to get a multiple on the dollars we invested in this last debt financing that translated into a return our investment for Harris & Harris Group.

I would like to contrast that with the realized loss of our investment in Kovio. Charles Harris, the founder of our firm, often said that the real distinguishing factor of a successful venture investor was that its companies reached their full potential, regardless of whether that potential turned out to be large or small. Even if a company realized a great exit, if its potential was not reached, we had not done our jobs. Alternatively, if a company’s potential turned out to be smaller, but where the right decisions were made to reach that potential, then our job was well done.

Kovio did not reach its potential. Kovio’s technology, originally from MIT, was a new way to print flexible, silicon electronics very cheaply. It was ahead of its time, but it was still an innovative and important technology. Devices enabled by its technology are now finding a commercial market and being launched by Thin Film Electronics. In our estimation the inability of Kovio to reach its potential was due to 1) traditional venture investor syndicates being in total disarray, 2) the investment taking too long for the fund life of the typical venture investor, 3) a hubris from top tier investors on the types of liquidity events they were willing to undertake and 4) us having too small an ownership, too little capital to affect a different outcome.

| 1 |

Kovio had a tier one group of venture investors. It was one of those investment syndicates that everyone brags about its association with. However, during its lifetime, many of the partners responsible for Kovio at these firms left or were dismissed from their funds. Multiple of the firms ceased investing or withdrew from venture investing entirely. There was no consistent leadership from these tier one investors making it difficult for Kovio’s management to lead in a consistent manner. Thus, the sale of the assets of the company to a microcap Norwegian publicly listed company that resulted in no proceeds to investors, not by the investors but by the debt provider was, in our opinion, mostly the result of the lack of investor leadership.

Kovio was a semiconductor company. It required a lot of capital and time to get to market. Harris & Harris Group had too small an ownership comparatively to try and affect a financing path chosen by the company without the support and backing of the other investors We wonder what the future of Kovio may have looked like if it had accessed the public markets for the growth capital it needed.

We are focusing more of our attention on finding better ways to realize returns in shorter periods of time with greater ownership and with less capital at risk, in ways that benefit our shareholders. We believe accessing the public markets sooner with high-quality companies will be one way to make sure these innovative companies realize their potential.

We believe the recent financing and listing of another MIT technology-based company, Enumeral is a step in that direction.

In 2009, we provided the seed capital to found Enumeral Biomedical based on a platform technology developed by J. Christopher Love, a professor in the Chemical Engineering department at MIT. Chris’s innovation was to leverage micro and nanofabrication techniques to create a simple device that enables its users to ask and answer questions in biology that were difficult or impossible to perform using existing methods. As we understood the technology more fully, we discovered that it held the potential to dramatically reduce the time and cost of discovering potential new therapeutic candidates as well as the potential to yield information that can help its users determine which candidates may be better and safer for the treatment of disease in humans.

The differentiated capabilities of this platform brought together an impressive founding management team at the very earliest stages and brought interest from large pharmaceutical companies. Enumeral signed proof-of-concept programs with multiple large pharmaceutical companies, and the company is now in negotiations on larger programs with these and other companies. Enumeral has also used its platform to discover antibody candidates for out-licensing, and these candidates have also generated interest from pharmaceutical companies. Of course, it is possible that such negotiations will not lead to signed engagements. That said, we are excited about this interest and the potential for the company in the future.

| 2 |

Enumeral has historically been funded primarily by Harris & Harris Group and high-net-worth individuals. As it set about raising a growth round of capital for the company now that it believed it had validation of the differentiated capabilities of the platform and interest from commercial partners, we thought that the public markets would be receptive to and excited by the company’s story and its potential. This interest was confirmed through the close of a $21.55 million round of financing simultaneous with a reverse merger of Enumeral into a publicly traded shell company. The surviving entity is Enumeral Biomedical Holdings, Inc., and is traded on the over the counter market under the symbol ENUM. Enumeral now has a strong balance sheet and we believe it is well positioned to be able to execute on its business and create value for its shareholders including Harris & Harris Group which owns approximately 15 percent of the outstanding shares of the publicly traded company.

We believe the public markets are an attractive source of capital and support for our portfolio companies that have demonstrated differentiation in technology and initial market interest. We hope that Enumeral is the first of many such financing events for our portfolio companies and we are spending a considerable amount of time and effort at Harris & Harris Group on working with our portfolio companies to be able to pursue such paths earlier in their respective financing and development cycles than may have historically occurred.

Additionally, one of the messages we heard loudly and clearly at our Meet the Portfolio Day in April of this year was that our shareholders are interested in gaining access to investment opportunities in our portfolio companies when available. Subject to compliance with federal and state securities laws, we are working actively to make it such that ownership in us confers opportunities that may otherwise not be available to our shareholders, such as making direct investments in our portfolio companies. We note that investments in private placements are typically limited to accredited investors, but there may be other investment opportunities that would be open to any investor. Our shareholders are a unique asset of Harris & Harris Group, and we appreciate your interest and support along these lines.

| 3 |

Turning to follow-on investments, three important financing events happened during the second quarter of 2014. D-Wave, HZO and PWA are important investments for us due to the potential for outsized investment returns if these companies execute on their business plans. In the latter two cases, this is directly tied to our increased ownership positions. During the second quarter, all three companies were able to raise their next round of capital at increased valuations and with impressive partners. We believe this is a strong demonstration of their progress and future potential value.

Additionally, we have continued to make new investments during the first half of 2014. During the second quarter of 2014, we announced an investment in a new company called UberSeq. We are the founding and only investor in the company. UberSeq is a translational genomics company that originated from Stanford University. The company is currently operating under “stealth,” which means we are not able to disclose details of its operating plan at this time. We look forward to sharing more details on the company with shareholders in future quarters as it emerges from its stealth state.

| 4 |

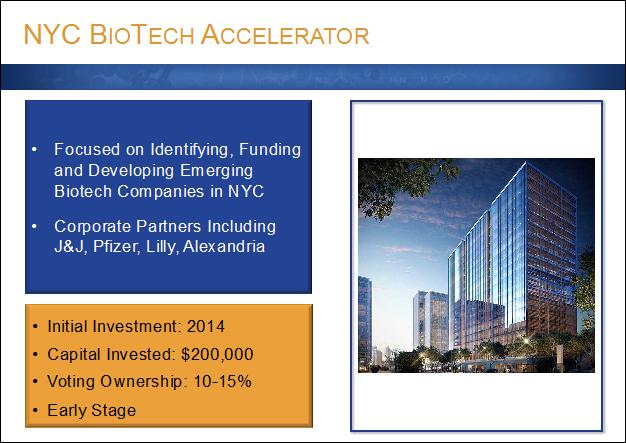

We also made a new investment in July of this year as one of the founding investors in the expansion of Accelerator Corporation, an investment vehicle for emerging biotechnology companies, into New York City. Those of you in New York may have read about it, as it has received a lot of press.

Accelerator is the result of collaboration between a consortium of top-tier venture capital and corporate investors, leading New York-based research institutions, scientific thought leaders, and executive managers who will identify, finance and manage the development of a select group of early stage biotechnology companies. Corporate participants in Accelerator's New York City operations include Johnson & Johnson Development Company, Pfizer Inc., and Eli Lily and Company.

The investment in Accelerator represents a new type of investment for Harris & Harris Group as it has not before participated in a co-investment vehicle that will develop a portfolio of biotechnology assets. Our interest is that Accelerator has brought together several components that are strategic and complementary to Harris & Harris Group’s BIOLOGY+ investment thesis including: 1) a built in syndicate of financial investors for high-risk biotechnology investments, 2) three corporate partners, that are also investors, that will help define critical markets as well as help design validation experiments, 3) a capital efficient investment model, 4) a complementary investment scope to H&H technology focus, and 5) an NYC life-science ecosystem anchor.

| 5 |

Accelerator brings together financial and corporate investors that aim to efficiently invest in clinical and late preclinical-stage assets that can be developed and exited on accelerated timelines. The involvement of three corporate partners (J&J, Eli Lilly and Pfizer) are critical and will help to ensure that the right experiments and data set will be pursued. This strategy should enable early license opportunities and financing options for the companies.

We also wanted to note that we have instituted some strategic personnel changes that begin to have an impact on expenses in the second half of 2014 and which will have a greater impact on expenses in 2015. During the second quarter of 2014, we had 12 full-time employees of Harris & Harris Group. By January 1, 2015, we plan to have 10 full-time employees. We expect this will have a positive impact on reducing our expenses.

In closing, we wanted to remind our shareholders and others of the blog posts on our website. These blog posts highlight some of our thoughts on areas of interest that are relevant to our business currently and into the future. We also have published a series of blogs under the concept of H&H at the Cutting Edge. These posts can be found on our website by clicking the BLOG menu option on our homepage or at http://www.hhvc.com/blog/.

We would like to thank you for your support of Harris & Harris Group. We believe the Harris & Harris Group of the future is going to look different than it has from the past decade. Some of these changes have been put in place over the past couple of years, but more are coming.

Douglas W. Jamison

| Chairman, Chief Executive Officer |

| and Managing Director |

August 19, 2014

This letter may contain statements of a forward-looking nature relating to future events. These forward-looking statements are subject to the inherent uncertainties in predicting future results and conditions. These statements reflect the Company's current beliefs, and a number of important factors could cause actual results to differ materially from those expressed in this letter. Please see the Company's Annual Report on Form 10-K for the fiscal year ended December 31, 2013, as well as subsequent filings, filed with the Securities and Exchange Commission for a more detailed discussion of the risks and uncertainties associated with the Company's business, including but not limited to, the risks and uncertainties associated with venture capital investing and other significant factors that could affect the Company's actual results. Except as otherwise required by Federal securities laws, the Company undertakes no obligation to update or revise these forward-looking statements to reflect new events or uncertainties. The reference to the website www.HHVC.com has been provided as a convenience, and the information contained on such website is not incorporated by reference into this letter.

| 6 |