Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - AutoWeb, Inc. | abtl8k_july312014.htm |

| EX-99.1 - PRESS RELEASE DATED JULY 31, 2014 - AutoWeb, Inc. | ex99-1.htm |

Exhibit 99.2

AUTOBYTEL INC

Moderator: Jeffrey Coats

July 31, 2014

5:00 p.m. ET

|

Operator:

|

Good day, ladies and gentlemen, and welcome to the Autobytel Announces 2014 Second Quarter Financial Results Conference Call. At this time, all participants are in a listen-only mode.

|

Later, we will conduct a question and answer session, and instructions will follow at that time. If anyone should require assistance during this conference, you may press star then zero on your touchtone telephone to reach an operator. As a reminder, this conference call may be recorded.

I would now like to introduce your host for today's conference, Laurie Berman, Investor Relations of Autobytel. Please go ahead.

|

Laurie Berman:

|

Thank you, Charlotte, and hello, everyone. Welcome to Autobytel’s 2014 Second Quarter Earnings Conference Call. Presenting today are Jeff Coats, President and Chief Executive Officer, and Curt DeWalt, Senior Vice President and Chief Financial Officer.

|

|

Laurie Berman:

|

Before I introduce Jeff, I need to remind you that during today’s call, including the question-and-answer session, any projections and forward-looking statements made regarding future events or Autobytel’s future financial performance are covered by the Safe Harbor statements contained in today’s press release, the slides accompanying this presentation, and the company’s public filings with the SEC. Actual events may differ materially from those forward-looking statements.

|

Specifically, please refer to the company’s Form 10-Q for the period ended June 30th, 2014, which was filed prior to this call, as well as other filings made from time to time by Autobytel with the SEC. These filings identify factors that could cause results to differ materially from those forward-looking statements.

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 2

There are slides included with today’s presentation to help illustrate some of the points being made and discussed during the call. The slides can be accessed by clicking on the link in today’s press release or by visiting Autobytel’s website at www.autobytel.com. When there, go to “Investor Relations” and then click on “Events & Presentations.”

Please also note that, during this call and/or in the accompanying slides, management will be discussing EBITDA, adjusted EBITDA and adjusted EBITDA per diluted share, which are non-GAAP financial measures, as defined by SEC Regulation G. Reconciliations of these non-GAAP financial measures to most directly comparable GAAP measures are included in today’s press release and in the slides which are posted on the company’s website.

|

|

And with that, I’ll now the turn the call over to Jeff.

|

|

Jeff Coats:

|

Thank you, Laurie. Good afternoon, everyone.

|

As you can see by the numbers we reported this afternoon, our second quarter was very positive, with 46% year-over-year revenue growth, near 40% gross margins, and a strong bottom-line performance that exceeded our expectations.

|

|

During the quarter we completed the integration of AutoUSA, which was acquired from AutoNation in January of this year, removing more than $4.5 million, or 75%, of AutoUSA’s costs. At the same time, we continued to further strengthen our core leads business. Total lead volume grew 43% over last year, driven by strong wholesale demand and internally-generated lead supply, as well as the AutoUSA acquisition.

|

|

|

We are highly committed to consistently delivering serious in-market car buyers to our dealer and manufacturer customers. Our focus on providing these customers with the highest quality and highest converting leads possible is key to our current and future success.

|

|

|

After Curt’s financial review of the quarter, I will update you on our continuing progress.

|

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 3

|

Curt DeWalt:

|

Thank you, Jeff.

|

|

|

On Slide 4, you can see total revenues, inclusive of AutoUSA, increased to $25.9 million for the second quarter of 2014, up from $17.8 million last year. Total revenues were just shy of our Q2 guidance, related in part to an OEM lead program we assumed through AutoUSA, whose terms were changed by the manufacturer during the second quarter. Revenues were also impacted by a decision we made to cut back on lead purchases from a large AutoUSA supplier, whose lead quality had fallen, no longer meeting our standards. This decision to pull back on the lead purchases did, however, have a positive effect on gross margins and our sales conversions rates, as a result of increased delivery of our high margin, high quality internally-generated leads. Jeff will provide additional details a bit later.

|

|

|

Revenues from automotive leads and services grew 52% over last year’s second quarter. Retail revenue sales rose 81%, and wholesale channel sales increased 29%. The retail channel benefited from our acquisitions of AutoUSA and Advanced Mobile, as well as from strong internally-generated lead supply. The retail channel also benefited from continued increases in our average selling price. The wholesale channel benefitted from strong demand across nearly all programs, as well as a lead program that began in mid-2013 with a major OEM using Autobytel as the primary supplier.

|

|

|

Advertising revenues were $764,000 for the second quarter of 2014; up approximately $100,000, or 13%, on a sequential basis, as we continued to optimize the Jumpstart relationship, which we've previously discussed.

|

|

|

Moving now to Slide 5, you’ll see that we delivered approximately 1.6 million automotive leads during the 2014 second quarter; a 43% increase over last year’s second quarter. 63% of the leads were delivered to the wholesale channel customers and 37% to retail channel customers. I’d also like to point out that we’ve began focusing on expanding our used car lead business, and you can see the benefit we derived in the current second quarter.

|

We delivered approximately 113,000 specialty finance leads during the 2014 second quarter; up from 84,000 in the corresponding period a year ago. The

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 4

increase in volume reflects continuing efforts to ease supply constraints that we’ve discussed in prior quarters. Specialty finance lead revenue grew more than 20% for the second quarter of 2014, to $1.9 million versus $1.6 million last year.

|

|

On Slide 6, you’ll note a 48% improvement in gross profit, which grew to $10.3 million for the 2014 second quarter, from $7.0 million last year. Gross margin was 39.8% of total revenues for the 2014 second quarter; up from 39.1% of total revenues one year ago. The improvement was due to the delivery of a higher percentage of internally-generated leads being delivered to AutoUSA customers, while also using Autobytel’s buying power to improve AutoUSA’s lead pricing from outside suppliers. As we’ve discussed in the past, historical AutoUSA gross margin was in the 25% to 27% range, temporarily reducing Autobytel’s overall margin. So we are extremely pleased with the quick progress we have been making in this area. We expect gross margins to remain in the 37% to 40% range.

|

Total operating expenses were $8.9 million, or 34.2% of total revenues, for the 2014 second quarter, compared with $6.4 million, or 36.0% of total revenues, for the same quarter last year. The majority of the dollar increase is related to sales and marketing expenses associated with our acquisitions of AutoUSA and Advanced Mobile, as well as sales activities related to SaleMove, all of which are paying off nicely. We also had $116,000 of additional acquisition-related costs.

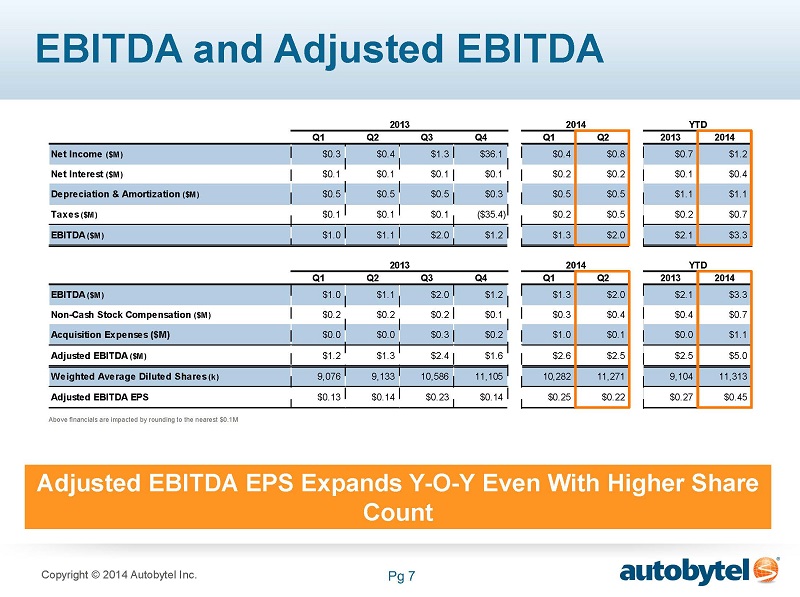

You’ll see on Slide 7, non-cash stock-based compensation totaled $368,000, compared with $188,000 for the 2013 second quarter. The increase resulted from additional grants, as well as higher share price this year versus last year and the related Black-Scholes values used for expensing. Depreciation and amortization was $548,000, versus $523,000 last year.

Net income grew to $801,000, or $0.08 per diluted share, from $386,000, or $0.04 per diluted share, for last year’s second quarter. Note there were approximately 23% more diluted weighted average shares outstanding during the second quarter of 2014, compared with last year. This change in diluted shares outstanding reflects an increase in the price of Autobytel’s common

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 5

stock, as well as the company’s Cyber Ventures acquisition-related warrants being included in the diluted share calculation as a result of the share price increase. Diluted share calculation also is influenced quarter-to-quarter by the interplay between net income and interest expense on acquisition-related convertible debt.

As you’re aware, we now have a higher effective tax rate provision for book purposes than we’ve had in the past. This is the result of the valuation allowance reversal on the deferred tax assets. However, this increase will not impact cash due to the utilization of our NOL tax credits.

We’re also including non-GAAP financial information to help investors better understand Autobytel’s financial performance, given the higher tax rate provision and recent acquisitions. So, on Slide 7, you can see that adjusted EBITDA, which adds back acquisition expenses and stock-based compensation, was $2.5 million, or $0.22 per diluted share, up from $1.3 million, or $0.14 per diluted share, one year ago.

Cash and cash equivalents balance grew to $20.5 million at June 30, 2014, up from $18.9 million at the end of 2013, and $19.3 million at the end of the first quarter. Cash provided by operations for the 2014 second quarter was $1.9 million, compared with $1.3 million in the prior year quarter. For the six-month period, cash provided by operations was $2.8 million, versus $918,000 for the same period last year.

Detailed year-to-date financial information can be found – is available on the press release we issued earlier today and in our Form 10-Q for the second quarter filed prior to this call.

|

|

Now, I’ll turn the call back to Jeff.

|

|

Jeff Coats:

|

Thanks, Curt.

|

As I mentioned earlier, the integration of AutoUSA was completed in the second quarter. As noted on Slide 8, we have effectively retired the AutoUSA brand and have removed more than $4.5 million, or 75%, of AutoUSA’s $6 million of operating expense, greatly surpassing our original 30% target. We

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 6

have also expanded our gross margin from AutoUSA’s dealers much faster than anticipated, by delivering a higher proportion of internally-generated leads to them, while also improving AutoUSA’s lead pricing from outside suppliers by bringing Autobytel’s buying power to the table.

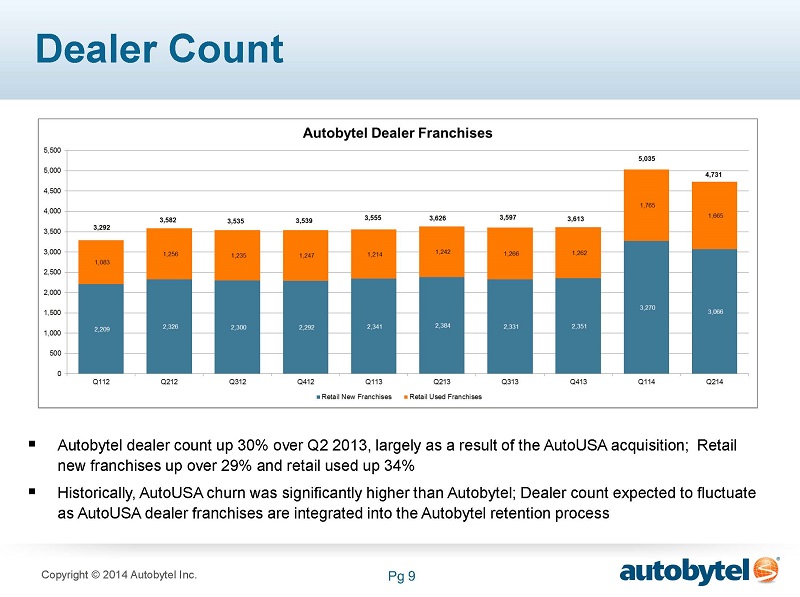

Dealer count, which can be seen on Slide 9, stood at approximately 4,700 franchises at the end of June, down, as we expected, from just over 5,000 at the end of the first quarter. To reiterate something we’ve been saying since we announced the acquisition, our business plan anticipated a decline in AutoUSA dealer count, and accordingly, retail revenue, for several quarters before bottoming out and growing again. We’ve been working to implement our successful dealer retention and rewind procedures to reverse AutoUSA’s historically higher dealer churn. The most important facet of our discussions with AutoUSA dealers revolves around our unwavering commitment to lead quality, so we have been educating them about our sales conversion rates based on actual vehicle registration data as validated by IHS Automotive; formerly R.L. Polk. We do expect to retain and rewind more of these dealers in the coming months.

|

|

As Curt explained earlier, our revenues during the quarter were also affected by changes to an OEM program that we assumed through the acquisition of AutoUSA. In Q2 we were informed that the business rules and pricing of this program would change. The original program was relatively low margin for AutoUSA as all leads were acquired from affiliates. The new program, for which Autobytel is still one of the largest suppliers, is producing better margins for us since almost all of the leads are generated internally. So, while the new program resulted in a bit of a step-back in our revenue profile, and had an $800,000 impact on revenues for the last two months of the second quarter, we believe our margin profile will improve going forward, keeping with our commitment to achieving long-term profitable growth. We anticipate the impact of the new program will continue at least through the remainder of this year. I’d also note that the impact will be slightly more pronounced for the third quarter as we will see a full quarter effect from the program changes. It is also important to note that we do expect this program to grow over time.

|

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 7

|

|

When we re-prioritized Autobytel’s focus on our leads business in 2009, we made a quality commitment and pledge to our dealers and manufacturers. A pledge that we take very seriously and that is at the heart of why customers purchase leads from us. Through a host of initiatives, we reenergized our company and created a core leads business that we believe truly sets us apart. As you can see on Slide 10, we have grown the number of leads Autobytel generates internally, from 3% at the beginning of 2009, to a highpoint in the 70-75% range just prior to our acquisition of AutoUSA, and are already back up to the mid-60s post acquisition. As a result, we have significantly improved the sales conversion rates of our leads, while also expanding gross margins, as you can also see on Slide 10. The leads we internally generate obviously carry a lower cost than those we purchase from outside sources.

|

|

|

Given our focus on delivering high quality, high converting leads, we do intentionally cut back on lead purchases from suppliers from time to time, when their leads do not meet our quality standards ... because it’s what our customers expect of us, and it’s the right thing to do. Our success is built on the quality and sales conversion rates of our leads, so when necessary, we will forgo short-term revenue to maintain our marketplace stature and credibility. Our main focus is on the long-term profitable growth of our business and our ability to provide significant value to all of our customers, which we believe will translate ultimately to enhanced shareholder value.

|

As Curt noted earlier, during the second quarter, we took action to reduce lead volume from one of AutoUSA’s largest lead suppliers that did not match up to our quality standards. Based on numerous dealer complaints, and supported by data we received from IHS Automotive, leads from this supplier were converting to sales at 5%, which is much lower than our outside supplier average, as you can see on Slide 9. We also have an ongoing relationship with this supplier and while these results were surprising to us, we have shared our IHS data with the supplier and are working with them to help them improve the quality of their leads so that we can continue and expand our relationship with them. While we knew our decision to reduce lead flow from this supplier would impact our second quarter revenues by almost $400,000, we believe the long-term outcome will be positive both in terms of customer retention and improved profitability, given the higher margin our internally-

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 8

generated leads produce and the higher-quality leads that we expect to receive from this supplier and other suppliers on an ongoing basis. We expect only a modest impact on the third quarter revenue, since we're already making good progress to replace this volume with outside suppliers and based on our ability to generate more leads internally.

To summarize, we are extremely pleased with the acquisition of AutoUSA. It has provided us with a substantially larger retail footprint, helping reinforce our ongoing mission of improving the retail automotive experience for both dealers and consumers. As previously disclosed, we went into the acquisition knowing that we would have some work to do with AutoUSA’s higher dealer churn and historically lower margins. We are making good progress, especially related to margin improvement, and expect to see meaningful dealer churn improvements in 2015. And even though we are now working through the challenges related to the OEM and supplier issues we assumed through the acquisition, we are gratified that we were able to purchase this profitable revenue and incremental relationships at what we believe was a very reasonable price. With a better understanding of AutoUSA’s revenue profile, we reduced operating expenses to more appropriate levels to better match this profile. The net result of our actions is that AutoUSA’s business is now smaller, but much leaner and more profitable. We have added hundreds of incremental dealers to our network, gained new dealer products, significantly enhanced our competitive position and created a more solid platform from which we can continue to grow.

|

|

As noted above, lead volume grew 43% for the quarter, compared with last year. We believe our success in this area relates to the high sales conversion rates we deliver to our customers. As you can also see on Slide 11, and as validated by IHS Automotive, the leads we generate from Autobytel.com currently convert to sales, on average, at a rate of approximately 22%, and all leads internally-generated by Autobytel currently convert to sales, on average, at a rate of approximately 16%.

|

We believe that our higher conversion rates can help generate higher ROIs for dealers. For example, as shown on Slide 12, if a dealer purchases 100 leads at $22 per lead from Autobytel and sells just 8 vehicles as a result of those leads,

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 9

the dealer’s cost per sale would equate to $275. This compares favorably to the $299 to $399, which is the cost-per-sale equivalent from some of our competitors. Remember, the example we’ve used assumes only an 8% conversion rate, which is significantly lower than our average conversion rates of 16 to 22% for a lead delivered by Autobytel. The higher the conversion rate, the greater the price disparity becomes. Additionally, we have heard anecdotally from dealers that they generate a higher gross on vehicles sold as a result of Autobytel leads than they do from some other suppliers.

Along with bolstering the quality and volume of the leads we deliver, we are continuing to provide high quality products to our customers, aimed at helping them sell more vehicles. Our dealer products are also helping us move beyond the solely lead-supplier relationship, to become a more important strategic partner that delivers in-market buyers directly to dealers. I’ll briefly highlight a few.

|

|

Autobytel Mobile, which is shown on Slide 15, continues to be well accepted in the marketplace. It goes without saying that texting has become a part of everyday life; however, most dealers, OEMs and large dealer groups do not currently have the ability to enable text communications with consumers in a centralized, regulatory compliant environment. Autobytel Mobile’s TextShield is being recognized as the solution through which they can create new sales opportunities through text messaging.

|

|

|

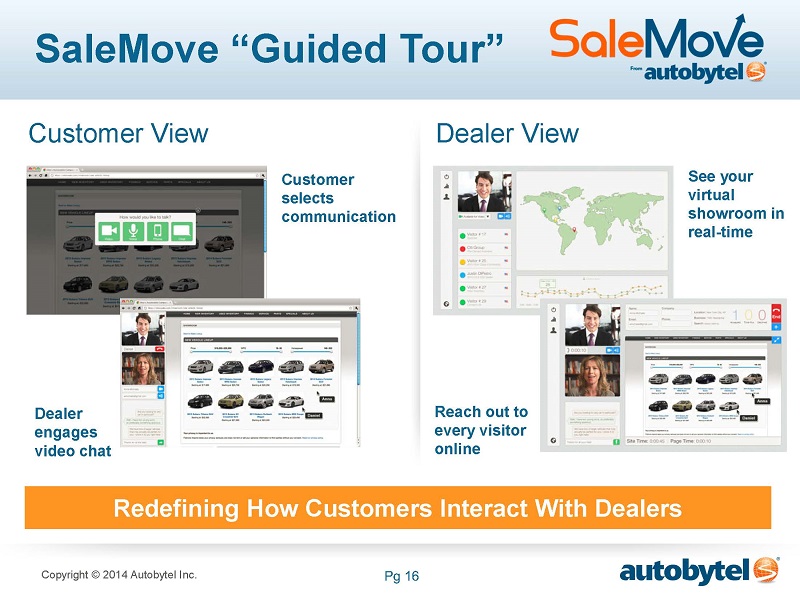

Another value-add product is SaleMove, as shown on Slide 16. Autobytel is the exclusive provider of SaleMove’s suite of tools to the automotive industry ... tools that improve the online car shopping experience. Whether through live video, audio, text-based chat or phone, SaleMove allows dealers to interact with consumers in the manner they most prefer. As I’ve mentioned previously, SaleMove turns the dealer’s website into what we think of as a virtual showroom. Because the average consumer now physically visits only 1.9 automotive dealerships, on average, before buying a car, down from the historical 3 to 5 visits, and because online shopping is continuing to become more popular, it is imperative that a dealer’s website, or virtual showroom, be fully functional and fully attended. SaleMove provides dealers with the ability to leverage those trends and opportunities.

|

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 10

One additional new product offering, which resulted from a reseller relationship we assumed with the AutoUSA acquisition, is Payment Pro, as shown on Slide 17. Payment Pro is an innovative dealer website tool that displays real online payments for a dealer’s inventory. This process does not require the consumer’s social security number or birth date, but combines the consumer’s credit, the vehicle and the dealer finance programs to show the consumer prequalified custom payments. Payment Pro is fully integrated to the dealer mobile website and allows dealers to bring more of the vehicle purchase process online.

I’d also like to say a few words about our finance leads business. During the second quarter, we began turning the corner on what had been a challenging marketplace due to supply constraints. We delivered 34% more finance leads in the 2014 second quarter than in the prior year, generating a 20% increase in finance lead revenue. With supply constraints beginning to ease, we think this business provides more opportunity for us.

I’d also like to briefly update you on AutoWeb, the company in which we made a strategic investment late last year. AutoWeb, whose new platform enables specialized targeting to high-intent online car shoppers, while also allowing advertisers to optimize their campaigns efficiently, is gaining traction for its product. Our relationship with them continues to bear fruit and is generating meaningful revenue for Autobytel. We plan to talk more about this relationship in the coming quarters.

The automotive market remains solid and continues to provide Autobytel with growth opportunities. As you can see on Slide 19, the July retail seasonally adjusted annual run rate is expected to be approximately 13.8 million units, up from 13.3 million in June, and 13.2 million one year ago. Retail U.S. light vehicle sales are expected to grow 9% in July, compared with the prior year.

Based upon current business trends and an ongoing healthy automotive market, we expect 2014 third quarter revenue growth in the range of 22% to 26%, compared with the 2013 third quarter. We also expect 2014 third quarter adjusted EBITDA per diluted share will be in the range of $0.22 to $0.25 cents per share, based upon 11.3 million diluted average weighted

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 11

shares outstanding. It is also our intention to provide longer-term trends and targets later this year.

Our ongoing business initiatives are summarized on Slide 20. We plan to continue on the current path by focusing on the things that have fueled our growth and profitability over the past several years, while also identifying outside opportunities to further solidify our business and accelerate our revenue generation capabilities. It does bear repeating also, however, that we currently have no plans for raising additional capital.

As you can tell, we remain upbeat about our business, about our industry and about our opportunity, and are looking forward to continued growth and profitability.

Operator, we will now take questions.

|

Operator:

|

So, ladies and gentlemen, if you have a question at this time, please press the star then the number 1 key on your touchtone telephone. And if your question has been answered or you wish to remove yourself from the queue, you may press the pound key.

|

Once again, if you have a question at this time, please press the star then the number 1 key on your touchtone telephone.

|

|

Our first question comes from the line of Eric Martinuzzi from Lake Street Capital. Your line is open.

|

|

Eric Martinuzzi:

|

Just trying to size the exposure from the two issues that you raised regarding AutoUSA. On the one side, you’ve got the change in the OEM relationship, and then on the other you’ve got one of the large lead suppliers. When you acquired AutoUSA, I recall you guys saying you expected it to contribute, I think it was, $22 to $24 million in 2014. Based on these two issues, what would the correct number be, kind of an annualized basis?

|

|

Jeff Coats:

|

Actually, Eric, the way we characterized this is we said that AutoUSA was on a run rate of around $25 million in revenue for 2014, before there would be

|

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 12

20% to 25% elimination through the intercompany based on the fact that we were their second largest supplier of leads prior to the acquisition.

|

|

So, it’s not quite as you just characterized. The OEM program is obviously going to bring that revenue profile down a few million dollars. The third quarter will be a little larger than the second quarter impact. The fourth quarter impact should be less, because it’s generally a slower quarter. We do expect that program to grow. We knew there would be changes made to the program, but the magnitude of the changes were unexpected, is the way that turned out.

|

|

Eric Martinuzzi:

|

And then on the third party supplier, or the (inaudible) …

|

|

Jeff Coats:

|

The third party supplier issue was completely unexpected. We began hearing it from the marketplace in an increasing crescendo of complaints from dealers. Once we were able to run some of the data through our IHS relationship we saw it was very clear that their quality standards had fallen pretty dramatically. We immediately took action with that – curtailed those purchases. Our reputation for quality is the most important to us in terms of keeping, growing and getting new dealers on our program.

|

|

|

I think the third quarter impact will be much less than the second quarter impact. We’ve already begun making significant progress in that area. We are working with that supplier to improve their quality so we can turn their volume back up.

|

|

|

We’re working with other outside suppliers to increase our volume, and we are increasing our internal lead generation on that. So, it’ll be a much, much smaller impact.

|

|

Eric Martinuzzi:

|

Okay, and then just one more on the OEM side. The agreement that you inherited with the AutoUSA acquisition – do you have any similar agreements in your own internal base of OEM accounts, where it sounds like this unilateral ability to change the terms caught you off guard with this OEM. Are there any other contracts that have terms like that?

|

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 13

|

Jeff Coats:

|

I would not expect to see another program change its business rules as dramatically as we saw in this particular instance. We do think it is unique. It was a somewhat unique program anyway in that some of the prices in the program were higher than the normal market. And that manufacturer made some internal changes and that resulted in the program changes. So, we would not anticipate anything like this with any of our other manufacturer programs, at all.

|

|

Eric Martinuzzi:

|

Thank you.

|

|

Operator:

|

Thank you. And as a reminder, ladies and gentlemen, if you have a question at this time, please press the star then the number 1 key on your touchtone telephone. Once again, if you have a question at this time, please press the star, then the number 1 key on your touchtone telephone.

|

|

|

Our next question will be coming from the line of John Blackledge from Cowen and Company.

|

|

John Blackledge:

|

Great, thanks. Just a couple of questions on the third quarter revenue guide. Could you talk about your expectations for retail revenue growth versus the wholesale revenue growth on the advertising side?

|

|

|

And then if you could just talk about the dealer churn rate in the second quarter – expectations, maybe in the back half of the year, and I think you mentioned you expected to improve in 2015. Maybe talk us through that. Thank you.

|

|

Jeff Coats:

|

With regards to churn; churn has – our core churn, as I have – we have talked about with many of you, has historically been in the 3% to 3¼% range. The dealer churn that we inherited along with the AutoUSA acquisition was running above 7% – closer to 8%, actually – so we’ve been trying to get our arms around that. We’ve begun making progress on that. From an overall standpoint, churn is still above 5%. It’s probably pretty close to 6%, from an overall standpoint, given what’s happened with that.

|

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 14

|

|

It’s a function, candidly, of getting more of our high quality leads into those dealers. It’s also a function of sitting down and having conversations with them.

|

|

|

I think there’s been a lot of noise in the marketplace the last few months with TrueCar going public – a lot of other things taking place – that’s really kind of, I think, created a lot of noise. There have been a lot of comments made out of some of the larger dealer groups with regards to third party leads, I think all of which have created some confusion in the marketplace.

|

|

|

So, we believe this is all short term. We believe that this is nothing unusual. We’ve seen spikes in churn in the past, just related to market conditions, and we’ve been able to successfully get our arms around it and reduce it, because it really comes down to helping the dealers understand exactly how many cars they’re selling from the leads that we provide to them.

|

|

|

With regards to the revenue growth, there will be a higher growth in retail revenue in the second half of the year than there will be in wholesale revenue, in part based upon this step-back in the wholesale program we were talking about earlier.

|

|

John Blackledge:

|

That's great. Thank you.

|

|

Jeff Coats:

|

Thank you.

|

|

Operator:

|

Thank you. And as a reminder, ladies and gentlemen, if you have a question at this time, please press the star then the number 1 key on your touchtone telephone. Once again, if you have question at this time, please press the star then the number 1 key on your touchtone telephone.

|

|

|

Our next question will be coming from the line of Eric Martinuzzi from Lake Street Capital. Your line is open.

|

|

Eric Martinuzzi:

|

Thanks for taking a follow-up here. Just curious on Slide 12 – this is the one where you talk about the cost per lead of the Autobytel lead and the conversion rate. The example you had given was you sell 8

|

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 15

vehicles and the dealer’s cost per sale would equate to $275. I’m just wondering why, you know to me, it seems pretty obvious that that makes sense. You get a positive return on ad spend. You know, dealers should be beating a path to your door, and yet there’s still this big gap. You know, is there – is it an issue of they have a monthly budget; they exhaust the monthly budget; they revisit this plan once a year; twice a year and don't come back? Because if – I would think, if that’s the case, they would be increasing their spend with you just to the point where there would be a parity with some of the other options in the market.

|

Jeff Coats:

|

I would – I agree with your characterization. The – I think the – as we've discussed, Eric, the lead business in the automotive industry developed a bad reputation during the go-go days. There were just way too many bad quality leads, and for a long time dealers got really jaded with really poor quality, so leads developed a really bad reputation.

|

|

|

As you know – as many people know – we’re the only ones in the marketplace out there talking about quality. We’re the only ones that talk about our own close rates. We are pushing to rehabilitate the image of leads and remind dealers. And there are a lot of trainers out in the marketplace, dealer consultants and other people, who recognize that buying leads with good close rates are in fact the best return on investment for a dealer in terms of turning up their ability to sell more cars during the month at any time. I mean they can call us and increase the volume at almost any time during the month, during the year. So it’s a combination of getting that message out there again and then delivering to it, making sure that we’re sending them the best quality leads that we can either generate ourselves internally or buy from others in the market.

|

|

|

That’s why we cut back on that supplier in the second quarter. Believe me. That was not an easy decision to make in terms of knowing it was going to have a negative impact on our revenue, but it was the absolute right decision to make, because if we fall off of the quality metrics that we’re pursuing then we are no better than some of the other players in the market and won’t have a leg to stand on.

|

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 16

So, we believe we’ve actually taken the absolute right action and that it will bear a lot of fruit for us. It’s very important for the dealers to know that they can count on us to deliver quality every month, month after month. We've been doing that now for over a couple of years. We have a lot of dealers on the program that constantly increase with us. So, we will rewind these dealers that are churning off. We do believe this is a short term anomaly. We just have to get our arms around what’s going on with the AutoUSA dealers, educate them on this, and we are confident we will be able to do that at the end of the day.

|

|

And the numbers are pretty obvious. Even at what we would consider to be a very low 8% close rate, it’s very attractive, particularly used versus – used with a $399 for a used car pay-per-lead. So we believe that we have a very compelling product in the marketplace which we will continue to promote.

|

|

Eric Martinuzzi:

|

And I think you have talked in the past about getting value for that premium lead that you know in prior – I've seen in prior years, you’ve used a $20 per lead example, and now you’re using a $22 per lead example.

|

|

|

Have you seen continued success in being able to push through price increases?

|

|

Jeff Coats:

|

We are making progress on doing that. We are continuing to push up our ASP. I think, while it’s definitely not a popular topic with dealers to talk about increasing lead prices, people understand that when you are spending more and producing a higher quality product that gets them a much better return on their investment, it’s reasonable to pay something closer to a market price. So, as we have talked about, I do believe it’ll take us some time to push that up over time, but we are, and we are successfully.

|

|

Eric Martinuzzi:

|

Okay. Was there any – back to the AutoUSA acquisition –was there any earn-out or holdback? Like, a lot of times, there’s a 12-month look-back after the deal closes. Was there anything in that agreement?

|

|

Jeff Coats:

|

No. It was – they have some warrants tied to the stock, and there is a convertible note for $1 million, but, I mean, you know we only paid

|

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 17

$11 million for those assets. We paid what we think of as a very good price for the revenue that we absolutely are retaining, which is extremely profitable and is giving us those hundreds of additional dealers to market our products to. So, even at a revenue profile that is lower than where it ended 2013 and lower than the run rate that it entered 2014, it’s still, what I would personally consider, a great deal for us.

|

Eric Martinuzzi:

|

Okay, and I’m going to take the liberty of asking a couple of more questions. It doesn’t sound like there’s a long queue.

|

|

|

The long term trend that you talked about potentially that at some point you would address, I’m not sure ... You know, to me, it’s no time like the present, but you’re talking about long term trends and targets later this year. Is there – is it going to be the next earnings call? Is there going to be an analyst day? What are you waiting for?

|

|

Jeff Coats:

|

Perhaps the next earnings call. We’re looking on putting something together. I know only focusing on guidance one quarter in advance is absolutely a two-edged sword. We have heard our shareholders and our analysts loud and clear that they’d like to see a little more longer-term clarity on how we see the market and the business, and so we are working to be able to provide that for 2015 and forward.

|

|

Eric Martinuzzi:

|

Okay, so stay tuned for October.

|

|

|

All right, and then just back to AutoWeb. You spent a little bit of time on it, but where is that showing in your P&L presently, and how does it move the needle going forward?

|

|

Jeff Coats:

|

It’s primarily in lead revenue today based upon the way some of the revenue is generated. There is also a portion of it in other revenue related to advertising revenue we receive from them. They will both scale over. The majority of the current revenue that we receive them from is up in lead revenue. The proportions will change over time, and we will start talking about it on a broken-out basis, but we think it’s too early, and they would certainly prefer that we not disclose a lot of details too early.

|

AUTOBYTEL INC

Moderator: Jeffrey Coats

7-31-14/5:00 p.m. ET

Confirmation # 73076662

Page 18

|

Eric Martinuzzi:

|

And that current – that ownership stake today is 16%. Is that correct?

|

|

Jeff Coats:

|

Yes. That ownership stake is 16%. We paid $2.5 million for 10%. We also received an incremental 6% for contributing the brand name that we owned – autoWeb.com. We also have an option for an additional 10% at the original $2.5 million price, and that option, I believe, is good through the end of September, 2015. So, we beneficially own 26% – the way we would think about it.

|

|

Eric Martinuzzi:

|

Okay. I’ll take the rest of my questions offline. Thanks.

|

|

Jeff Coats:

|

Thank you.

|

|

Operator:

|

Thank you, and at this time, I’m not showing any further questions. I would now like to turn the call back over to Jeff Coats for any closing remarks.

|

|

Jeff Coats:

|

We’d like to thank you all for joining us today. I know the message was not all sunshine and roses, but we are very bullish about our business. We are, in fact, very happy about the AutoUSA acquisition. We are working through some issues, as we’ve noted today, but we are retaining extremely profitable revenue from that acquisition, and we do believe strongly that it will add significantly to shareholder value and customer satisfaction as we go forward.

|

|

|

I also look forward to seeing many of you at the Canaccord Conference in Boston in a couple of weeks. So, thank you all.

|

|

Operator:

|

Ladies and gentlemen, thank you for participating in today’s conference. This does conclude the program, and you may all disconnect. Everyone, have a great day.

|

|

|

END

|