Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - WCI Communities, Inc. | d765566d8k.htm |

| EX-99.1 - EARNINGS PRESS RELEASE ISSUED BY THE COMPANY ON AUGUST 5, 2014. - WCI Communities, Inc. | d765566dex991.htm |

WCI

Communities Second

Quarter

2014

-

Earnings

Conference

Call

August 5, 2014

Exhibit 99.2 |

2

2

Disclosure Statement

This presentation contains forward-looking statements. All statements that are

not statements of historical fact, including statements about the

Company’s beliefs and expectations, are forward-looking statements within the meaning of the federal securities laws, and

should be evaluated as such. Forward-looking statements include information

concerning the Company’s future goals, expected growth, market

conditions and outlook (including the estimates, forecasts, statements and projections relating to Florida or national

markets

prepared

by

John

Burns

Real

Estate

Consulting),

expected

liquidity

and

possible

or

assumed

future

results

of

operations,

including descriptions of its business plan and strategies. These

forward-looking statements may be identified by the use of such

forward-looking

terminology,

including

the

terms

“believe,”

“estimate,”

“project,”

“anticipate,”

“expect,”

“seek,”

“predict,”

“contemplate,”

“continue,”

“possible,”

“intend,”

“may,”

“might,”

“will,”

“could,”

“would,”

“should,”

“forecast,”

or “assume”

or, in each case, their negative,

or other variations or comparable terminology.

For more information concerning factors that could cause actual results to differ

materially from those contained in the forward-looking statements,

please

refer

to

“Risk

Factors”

in

Item

1A

of

Part

I

of

our

Annual

Report

on

Form

10-K

filed

by

the

Company

with

the

Securities and Exchange Commission on February 27, 2014 and subsequent filings by

the Company. The Company bases these forward-looking statements or

projections on its current expectations, plans and assumptions that it has made in light of its experience

in the industry, as well as its perceptions of historical trends, current

conditions, expected future developments and other factors it believes are

appropriate under the circumstances and at such time. As you read and consider this presentation, you should

understand that these statements are not guarantees of performance or results. The

forward-looking statements and projections are subject to and involve

risks, uncertainties and assumptions and you should not place undue reliance on these forward-looking

statements or projections. Although the Company believes that these

forward-looking statements and projections are based on reasonable

assumptions at the time they are made, you should be aware that many factors could affect the Company’s actual financial

results or results of operations and could cause actual results to differ

materially from those expressed in the forward-looking statements

and

projections.

The

Company

undertakes

no

obligation

to

update

or

revise

any

forward-looking

statements,

whether

as

a

result of new information, future events or otherwise. If the Company does update

one or more forward-looking statements, there should

be

no

inference

that

it

will

make

additional

updates

with

respect

to

those

or

other

forward-looking

statements.

In addition to the financial measures prepared in accordance with U.S. generally

accepted accounting principles (“GAAP”), this presentation

contains the non-GAAP financial measures EBITDA, Adjusted EBITDA and Adjusted gross margin from homes

delivered.

The reasons for the use of these measures, a reconciliation of these measures to

the most directly comparable GAAP measures and other information relating to

these measures are included below in the appendix to this presentation. |

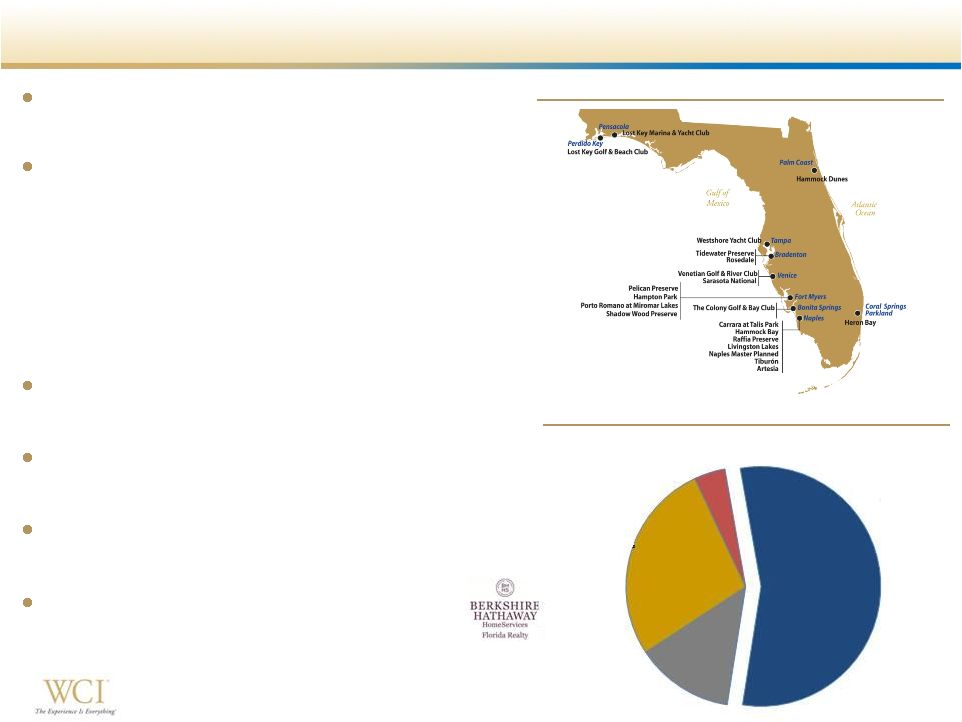

WCI

Communities at a Glance Lifestyle community developer and luxury

homebuilder throughout Florida

Target move-up, second-home and active

adult customers

–

High

average

selling

prices

-

$426k

on

2Q14

deliveries

–

High proportion of cash buyers -

55% in

2Q14; 59% year to date

•

Only 4% of buyers financed more than 80%

–

Low cancellation rate –

3.0% in 2Q14

Approximately 10,300 home sites owned

and controlled as of June 30, 2014

Conservative balance sheet -

$202 million

cash

Significant year-over-year Homebuilding

growth

Complementary and value-add Real

Estate Services & Amenities businesses

Geographic Footprint

Loan

to

Value

Percentage

–

2Q14

Deliveries

Buyer Profile with Low Reliance on Financing

Cash

55.2%

LTV 1

-64%

13.3%

LTV 65-80%

27.3%

LTV >80%

4.2%

3 |

Note:

Florida

as

referenced

to

John

Burns

Real

Estate

Consulting

and

in

the

charts

represents

a

compilation

of the major FL markets

(1)

US Census Bureau

(2)

John Burns Real Estate Consulting, July 2014

(3)

National

Association

of

Realtors

&

Florida

Realtors’

®

Florida

Housing

Market

statewide

data

reports

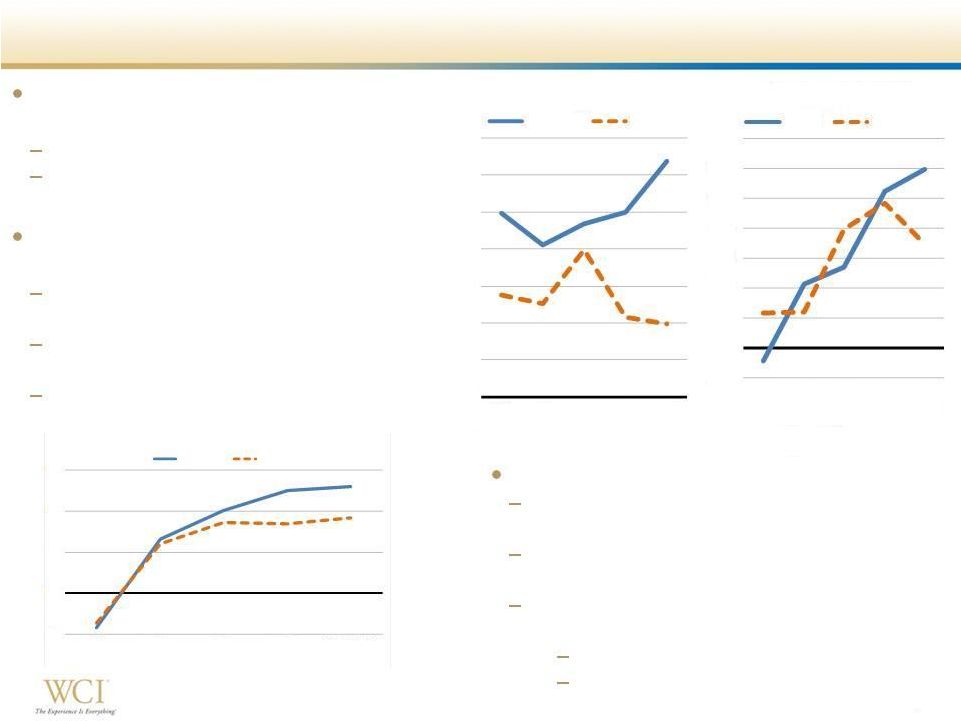

Compelling Florida Real Estate Market Opportunity

Florida building permits YTD 2014 -

2

nd

highest in the nation

(1)

2013 permits still ~70% off peak

LTM single family permit growth of

11.8%, compared to -0.8% nationally

(2)

Florida population growth -

3rd

highest growth state

(1)

Household growth rate three times the

national rate

(2)

Job growth rate 40% higher than the

national rate

(2)

Median new home price increase nearly

double the national rate

(2)

Florida resale market remains strong

(3)

2Q14 traditional single family and condo

transactions up 8.1% from 2Q13

National existing home sales down 4.6%

in 2Q14 vs. 2Q13

June 2014 median prices up compared to

June 2013

Single family median price up 5.2%

Condo median price up 8.5%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

2010

2011

2012

2013

May 2014

TTM

Household Growth -

YOY %

Change

Florida

National

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2010

2011

2012

2013

May

2014

TTM

Change

Florida

National

-1%

0%

1%

2%

3%

2010

2011

2012

2013

May 2014 TTM

Job Growth -

YOY % Change

Florida

National

Source: DataQuick(Metro, Attached & Detached Homes, Weighted

Averages), Census (National, SF only,*2014-05 is SA) , John Burns

R.E.

Consulting,

Pub:

Jul

-14.

Source: Moody's Analytics, John Burns R.E. Consulting, Pub: Jul-14

4

Source: BLS, John Burns R.E. Consulting - forecasts, *2014 - 05 for national is SA Median New Home Price -

YOY % |

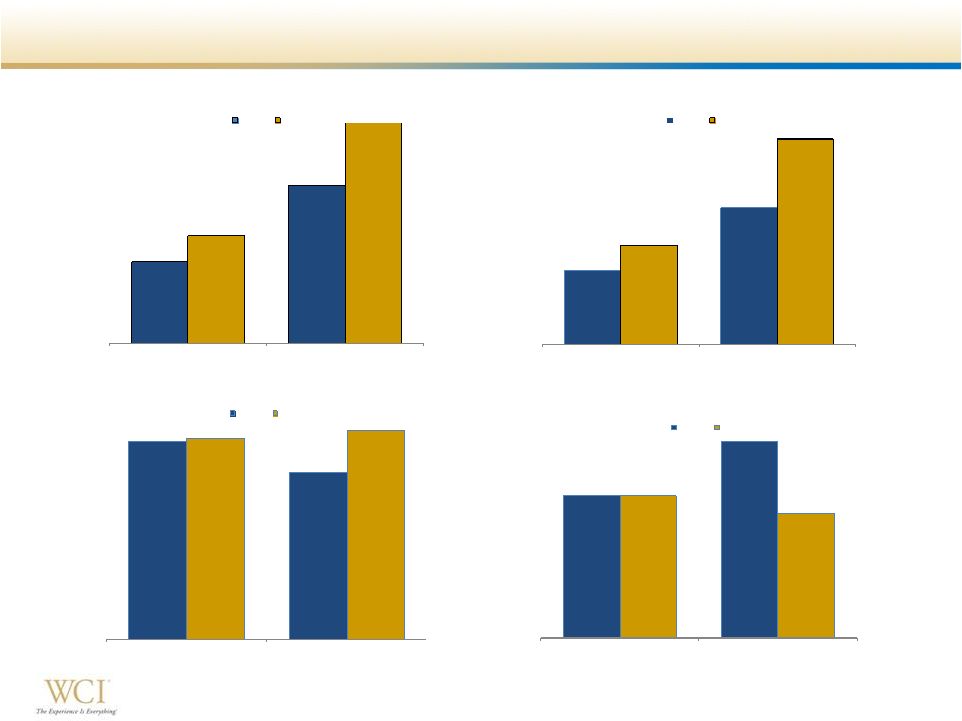

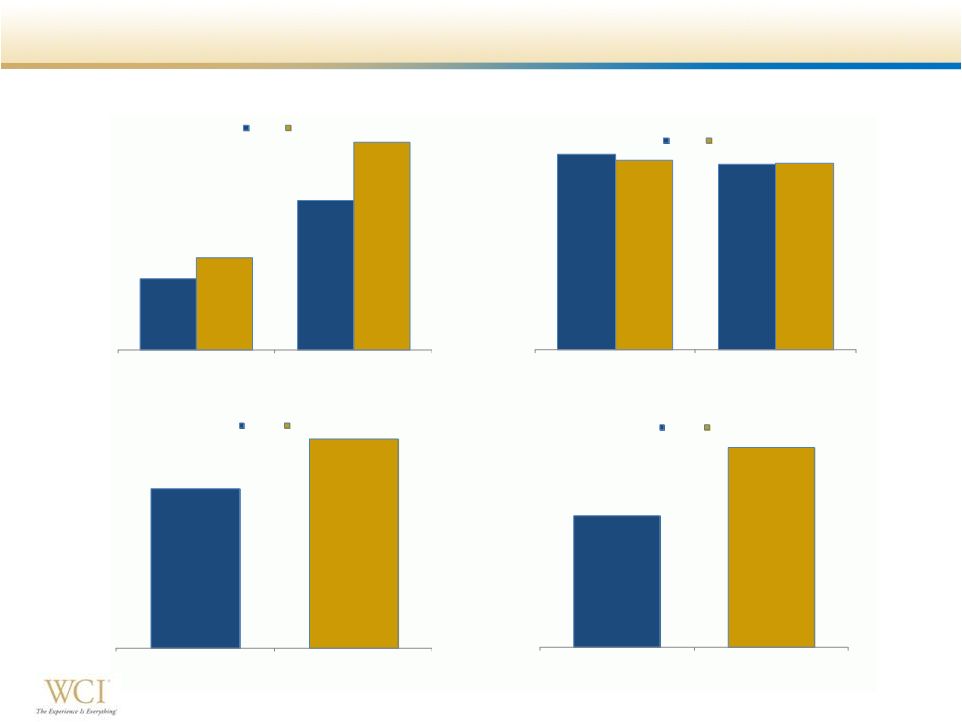

5

5

Continued New Order Growth ($ in thousands)

147

287

195

400

2Q

YTD

New Orders

2013

2014

+33%

+39%

3.1%

3.7%

3.1%

2.9%

2Q

YTD

New Orders

Incentives % of Base Price

2013

2014

-80 bps

$70,072

$128,936

$93,606

$194,749

2Q

YTD

Contract Value of New Orders

2013

2014

+34%

+51%

$477

$449

$480

$487

2Q

YTD

New Orders ASP

2013

2014

+1%

+9% |

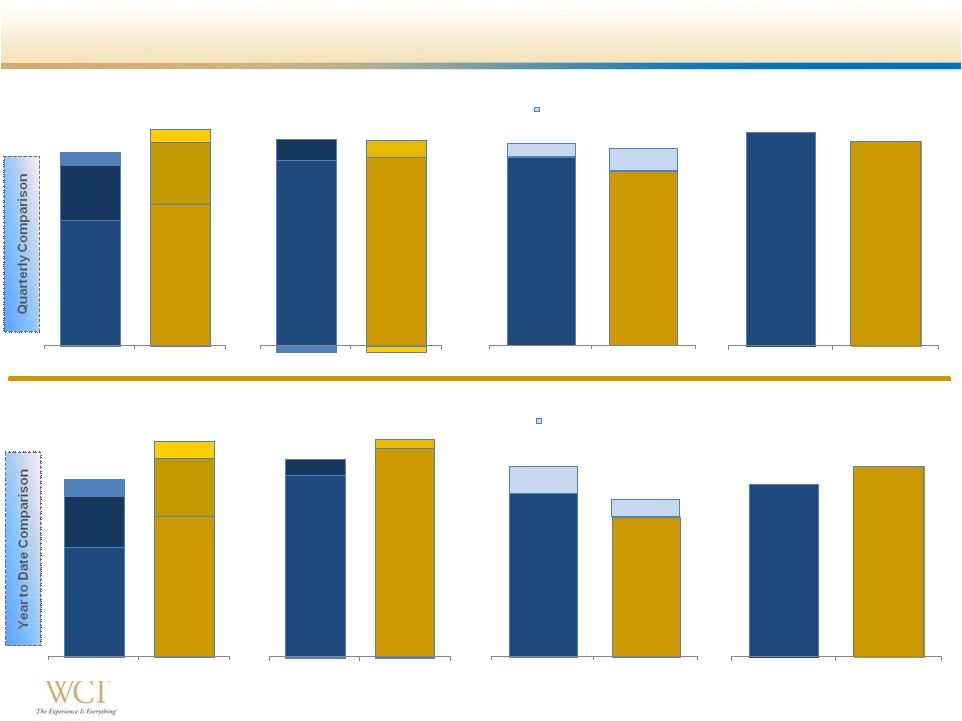

6

Continued Deliveries and Backlog Growth ($ in

thousands) 122

201

143

260

2Q

YTD

Deliveries

2013

2014

+17%

+29%

$441

$418

$426

$419

2Q

YTD

Average Selling Price per Delivered

Home

2013

2014

-3%

341

433

2Q13

2Q14

Backlog Units

2Q13

2Q14

+27%

$159,837

$229,983

2Q13

2Q14

Contract Value of Backlog

2Q13

2Q14

+44%

ASP -

$469

ASP -

$531

6 |

7

7

HB

$16.8

HB

$17.0

RES

$1.9

RES

$1.5

AM

$(0.6)

AM

$(0.5)

$18.1

$18.0

2Q13

2Q14

Gross Margin

($ in millions)

Executing on the Long Term Growth Strategy

(1)

Measured as a percentage of total homebuilding revenues

(2)

Measured as a percentage of total revenues

HB

$84.3

HB

$108.9

RES

$40.4

RES

$45.0

AM

$12.4

AM

$12.9

$137.1

$166.7

YTD 2013

YTD 2014

Revenues

($ in millions)

$14.4

$15.9

YTD 2013

YTD 2014

Adjusted EBITDA

(2)

($ in

millions)

10.5%

9.5%

$10.7

$10.2

2Q13

2Q14

Adjusted EBITDA

(2)

($ in

millions)

12.8%

11.0%

HB

$53.8

HB

$60.9

RES

$24.0

RES

$26.5

AM

$5.6

AM

$5.5

$83.3

$93.0

2Q13

2Q14

Revenues

($ in millions)

19.8%

17.7%

2.4%

1.5%

22.2%

19.3%

YTD 2013

YTD 2014

SG&A %

(1)

Non-Cash Incentive Comp

17.0%

16.1%

0.8%

1.4%

17.8%

17.5%

2Q13

2Q14

SG&A %

(1)

Non-Cash Incentive Comp

HB

$26.6

HB

$30.5

RES

$2.3

RES

$1.4

AM

$(0.2)

AM

$(0.0)

$28.7

$31.8

YTD 2013

YTD 2014

Gross Margin

($ in millions)

Note: Some totals may not foot due to rounding |

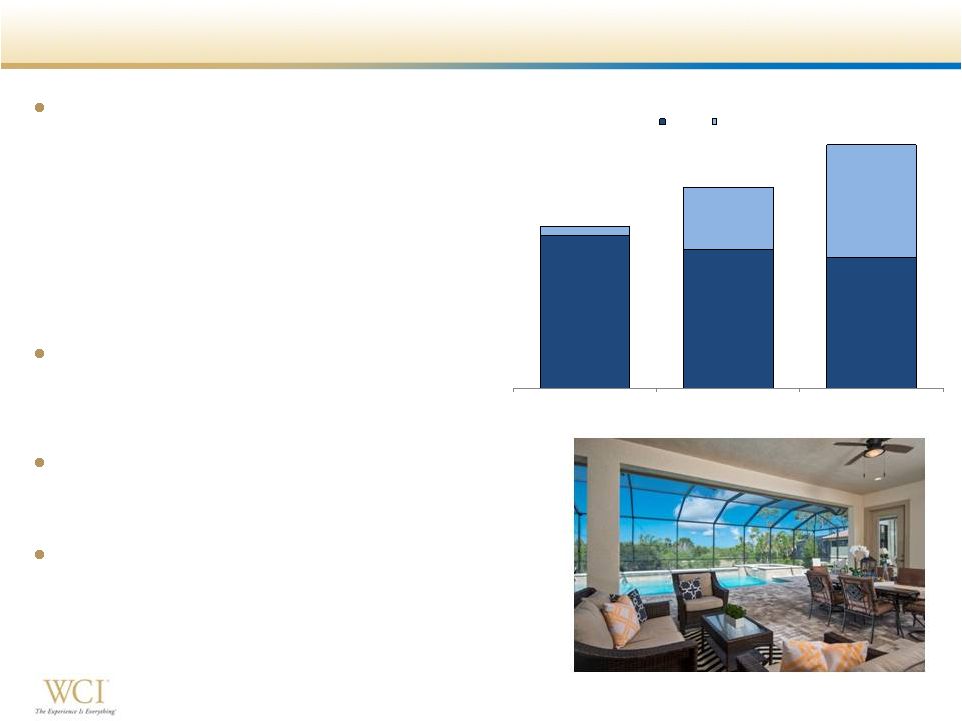

8

8

Land Acquisition -

Positioning for Future Growth

Closed on approximately 1,300 home

sites in the quarter for approximately $70

million

–

Master planned communities in Naples,

Fort Myers and Bradenton

–

Includes approximately 200 finished lots

and another 230 substantially developed

–

Represents eight potential incremental

neighborhoods

Contracted for property with a potential

additional 1,400 home sites

–

Inclusive of new master planned

communities in Fort Myers and Jacksonville

Actively pursuing additional land

acquisition opportunities throughout

Florida

Land portfolio now totals approximately

10,300 owned and controlled home sites

–

26% increase from the approximately 8,200

owned and controlled home sites in June

2013

6,483

5,872

5,564

379

2,635

4,770

6,862

8,507

10,334

4Q12

4Q13

2Q14

Owned and Controlled Home Sites

Legacy

New Acquisitions |

9

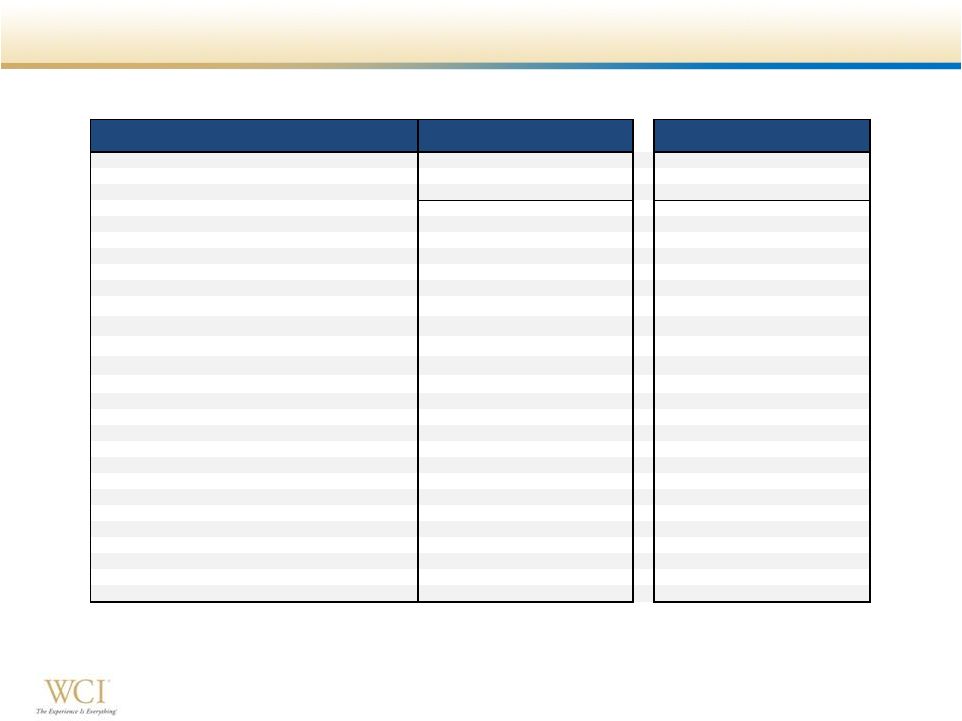

9

Selected Second Quarter & YTD Operating Results

(1)

Some variance percentage’s have been rounded to tie to second quarter 2014

Form 10-Q. $ in thousands, except per share amounts

2014

2013

Variance %

2014

2013

Variance %

Homebuilding revenues

60,918

$

53,761

$

13.2%

108,913

$

84,252

$

29.2%

Real estate services revenues

26,499

23,962

10.4%

44,962

40,391

11.4%

Amenities revenues

5,542

5,614

-1.8%

12,864

12,428

4.0%

Total revenues

92,959

83,337

11.6%

166,739

137,071

21.6%

Total gross margin

18,007

18,094

-0.5%

31,841

28,706

10.9%

Income tax (expense) benefit

(2,974)

-

NM

(4,634)

85

NM

Net income attributable to common shareholders

4,338

$

8,206

$

-47.1%

5,818

$

8,792

$

-33.8%

Earnings per share - diluted

0.17

$

0.45

$

-63.6%

0.22

$

0.49

$

-54.4%

Weighted average number of shares outstanding - diluted

26,278

18,084

45.3%

26,255

18,074

45.3%

SG&A expenses as a percent of Homebuilding revenues

17.5%

17.8%

-30 bps

19.3%

22.2%

-290 bps

Non-cash stock based compensation included in SG&A

1.4%

0.8%

+60 bps

1.5%

2.4%

-90 bps

Adjusted gross margin percentage

30.1%

33.3%

-320 bps

30.1%

33.5%

-340 bps

Adjusted EBITDA

10,235

$

10,687

$

-4.2%

15,893

$

14,404

$

10.3%

Homes delivered

143

122

17.2%

260

201

29.4%

Average selling price per home delivered

426

$

441

$

-3.4%

419

$

418

$

0.2%

New orders

195

147

32.7%

400

287

39.4%

Average selling price per new order

480

$

477

$

0.6%

487

$

449

$

8.5%

Backlog units

433

341

27.0%

Average selling price per backlog unit

531

$

469

$

13.2%

Three Months Ended June 30,

Six Months Ended June 30, |

10

10

Strong Balance Sheet with Ample Liquidity

Conservative balance sheet

Undrawn $75 million revolving

credit facility

Majority of land basis written down

in 2009

Issued additional $50 million of

principal amount Senior Notes due

2021

Sold CDD Bonds in April 2014

–

Proceeds of $22.7 million

–

Acquired from Sarasota National

community purchase in April 2013

(1)

Available liquidity includes the $75 million of borrowing capacity under a

four-year revolving credit facility and $8 million of borrowing capacity

available under a revolving credit facility with Stonegate Bank.

(2)

Net Debt represents total debt excluding premium less cash and cash equivalents;

capital represents net debt plus total equity.

$ in thousands

Cash & cash equivalents

201,542

$

213,352

$

Real estate inventories

384,662

280,293

Senior notes due 2021

250,000

200,000

Total equity

417,289

409,864

Total capitalization

667,289

609,864

Availabile liquidity

(1)

284,542

296,352

Debt to capitalization

37.5%

32.8%

Net debt to capital

(2)

10.4%

NM

(Cash + inventory) / debt

2.34

2.47

June 30, 2014

December 31, 2013 |

Key

Takeaways Fully integrated luxury homebuilder and

community developer

Complementary and strategic Amenities and

Real Estate Services businesses

Florida real estate market remains strong

Continued growth

–

Orders & deliveries

–

Revenues & Adjusted EBITDA

–

Neighborhood counts

Actively pursuing land acquisition opportunities

Leverage the scalable operating platform

Experienced and talented team

11

Focus on move-up, second-home and active

adult buyers |

12

Appendix

12 |

13

13

Reconciliation of Non-GAAP Financial Measures

Adjusted Gross Margin from Homes Delivered

Reconciliation of Non-GAAP Financial Measures

In addition to the results reported in accordance with U.S. generally accepted

accounting principles (“GAAP”), we have provided information in this

presentation relating to adjusted gross margin from homes delivered, EBITDA and

Adjusted EBITDA (as defined below). Adjusted Gross Margin from Homes

Delivered We calculate adjusted gross margin from homes delivered by

subtracting the gross margin from land and home sites, if any, from Homebuilding

gross

margin

to

arrive

at

gross

margin

from

homes

delivered.

Adjusted

gross

margin

from

homes

delivered

is

calculated

by

adding

asset

impairments, if any, and capitalized interest in cost of sales to gross margin from

homes delivered. Management uses adjusted gross margin from homes

delivered to evaluate operating performance in our Homebuilding segment and in making strategic decisions regarding sales price,

construction and development pace, product mix and other operating decisions.

We believe that adjusted gross margin from homes delivered is relevant and

useful to investors and other interested parties for evaluating our comparative operating performance from period to period and among

companies

within

the

homebuilding

industry

as

it

is

reflective

of

overall

profitability

during

any

given

reporting

period.

This

measure

is

considered

a

non-GAAP financial measure and should be considered in addition to, rather than

as a substitute for, the comparable GAAP financial measures when evaluating

our operating performance. Although other companies in the homebuilding industry report similar information, the methods used by such

companies

may

differ

from

our

methodology

and,

therefore,

may

not

be

comparable.

We

urge

investors

and

other

interested

parties

to

understand

the

methods

used

by

other

companies

in

the

homebuilding

industry

to

calculate

gross

margins

and

any

adjustments

to

such

amounts

before

comparing our measures to those of such other companies.

The table below reconciles adjusted gross margin from homes delivered to the most

directly comparable GAAP financial measure, Homebuilding gross margin, for

the periods presented herein. 2014

2013

2014

2013

($ in thousands)

Homebuilding gross margin

17,049

$

16,788

$

30,496

$

26,623

$

Less: gross margin (loss) from land and home sites

-

(34)

-

35

Gross

margin from homes delivered 17,049

16,822

30,496

26,588

Add: capitalized interest in cost of

sales 1,282

1,070

2,267

1,563

Adjusted gross margin from homes

delivered 18,331

$

17,892

$

32,763

$

28,151

$

Gross margin from homes delivered as a percentage

of revenues from homes delivered

28.0%

31.3%

28.0%

31.6%

Adjusted gross margin from homes delivered as a

percentage of revenues from homes delivered

30.1%

33.3%

30.1%

33.5%

Three Months Ended June 30,

Six Months Ended June 30, |

14

14

Reconciliation of Non-GAAP Financial Measures

EBITDA and Adjusted EBITDA (continued)

Adjusted

EBITDA

measures

performance

by

adjusting

net

income

(loss)

attributable

to

common

shareholders

of

WCI

Communities,

Inc.

to

exclude, if any, interest expense, capitalized interest in cost of sales, income

taxes, depreciation (‘‘EBITDA’’), preferred stock dividends, income

from discontinued operations, other income, stock-based and other non-cash

long-term incentive compensation expense, asset impairments and

expenses

related

to

early

repayment

of

debt.

We

believe

that

the

presentation

of

Adjusted

EBITDA

provides

useful

information

to

investors

and

other interested parties regarding our results of operations because it assists

those parties and us when analyzing and benchmarking the performance and

value of our business. We also believe that Adjusted EBITDA is useful as a measure of comparative operating performance

from

period

to

period

and

among

companies

in

the

homebuilding

industry

as

it

is

reflective

of

changes

in

pricing

decisions,

cost

controls

and

other

factors

that

affect

operating

performance,

and

it

removes

the

effect

of

our

capital

structure

(such

as

preferred

stock

dividends

and

interest

expense),

asset

base

(primarily

depreciation),

items

outside

of

our

control

(primarily

income

taxes)

and

the

volatility

related

to

the

timing

and

extent of non-operating activities (such as discontinued operations and asset

impairments). Accordingly, we believe that this measure is useful for

comparing

general

operating

performance

from

period

to

period.

Other

companies

may

define

Adjusted

EBITDA

differently

and,

as

a

result,

our

measure of Adjusted EBITDA may not be directly comparable to Adjusted EBITDA of

other companies. Although we use Adjusted EBITDA as a financial

measure

to

assess

the

performance

of

our

business,

the

use

of

Adjusted

EBITDA

is

limited

because

it

does

not

include

certain

material

costs,

such

as

interest

and

income

taxes,

necessary

to

operate

our

business.

Adjusted

EBITDA

and

EBITDA

should

be

considered

in

addition

to,

and

not

as

substitutes

for,

net

income

(loss)

in

accordance

with

GAAP

as

a

measure

of

performance.

Our

presentation

of

EBITDA

and

Adjusted

EBITDA should not be construed as an indication that our future results will be

unaffected by unusual or nonrecurring items. Our EBITDA-based

measures

have

limitations

as

analytical

tools

and,

therefore,

investors

and

other

interested

parties

should

not

consider

them

in

isolation

or

as

substitutes

for

analyses

of

our

results

as

reported

under

GAAP.

Some

such

limitations

are:

they do not reflect the impact of earnings or charges resulting from matters that

we consider not to be indicative of our ongoing operations; they are not

adjusted for all non-cash income or expense items that are reflected in our consolidated statements of cash flows;

they do not reflect the interest expense necessary to service our debt; and

Because

of

these

limitations,

our

EBITDA-based

measures

are

not

intended

to

be

alternatives

to

net

income

(loss),

indicators

of

our

operating

performance,

alternatives

to

any

other

measure

of

performance

in

conformity

with

GAAP

or

alternatives

to

cash

flow

provided

by

operating

activities as measures of liquidity. Investors and other interested parties

should therefore not place undue reliance on our EBITDA-based measures

or ratios calculated using those measures. Our GAAP-based measures can be found in our unaudited consolidated financial

statements in Item 1 of the Quarterly Report on Form 10-Q that we plan to file

with the Securities and Exchange Commission on or before August 8,

2014. other

companies

in

our

industry

may

calculate

these

measures

differently

than

we

do,

thereby

limiting

their

usefulness

as

comparative

measures. |

15

15

Reconciliation of Non-GAAP Financial Measures

EBITDA and Adjusted EBITDA

The table below reconciles EBITDA and Adjusted EBITDA to the most directly

comparable GAAP financial measure, net income attributable to

common

shareholders

of

WCI

Communities,

Inc.,

for

the

periods

presented

herein.

2014

2013

2014

2013

($ in thousands)

Net income attributable to common

shareholders of WCI Communities, Inc.

4,338

$

8,206

$

5,818

$

8,792

$

Interest expense

187

729

685

1,614

Capitalized interest in cost of

sales (1) 1,282

1,070

2,267

1,563

Income taxes (2)

2,974

-

4,634

(85)

Depreciation

644

545

1,232

1,008

EBITDA

9,425

10,550

14,636

12,892

Preferred stock dividend (3)

-

700

-

700

Other income,

net (4) (63)

(1,011)

(428)

(1,220)

Stock-based and other non-cash

long-term incentive compensation expense (5)

873

448

1,685

2,032

Adjusted EBITDA

10,235

$

10,687

$

15,893

$

14,404

$

Adjusted EBITDA margin

11.0%

12.8%

9.5%

10.5%

Three Months Ended June 30,

Six Months Ended June 30,

1)

Represents capitalized interest expensed in cost of sales on home deliveries and land and home site

sales. 2)

Represents the Company’s income taxes as reported in its unaudited consolidated

statements of operations.

3)

Represents a reduction in income available to common shareholders of WCI Communities, Inc. during the

three and six months ended June 30, 2013 pertaining to a payment of $0.7 million that we made

in April 2013 to purchase the one outstanding share of our Series B preferred stock. In accordance with Accounting Standards

Codification 260, Earnings Per Share, paragraph 10-S99-2, the difference between the

consideration transferred to our preferred stock shareholder and the corresponding book value

has been characterized as a preferred stock dividend in the Company’s unaudited consolidated statements of operations and deducted from

net income to arrive at net income attributable to common shareholders of WCI Communities, Inc. 4)

Represents the Company’s other income, net as reported in its unaudited consolidated statements

of operations.

5)

Represents expenses recorded in the Company’s unaudited consolidated statements of operations

related to its stock-based and other non-cash long-term incentive compensation

plans. |