Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - PUBLIC SERVICE ENTERPRISE GROUP INC | d765207d8k.htm |

| EX-99 - EX-99 - PUBLIC SERVICE ENTERPRISE GROUP INC | d765207dex99.htm |

Public Service Enterprise Group

PSEG Earnings Conference Call

2

nd

Quarter 2014

July 30, 2014

EXHIBIT 99.1 |

1

Forward-Looking Statement

Certain of the matters discussed in this report about our and our subsidiaries'

future performance, including, without limitation, future revenues, earnings, strategies, prospects, consequences

and all other statements that are not purely historical constitute

“forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking

statements are subject to risks and uncertainties, which could cause actual

results to differ materially from those anticipated. Such statements are based on management's beliefs as well as

assumptions made by and information currently available to management. When

used herein, the words “anticipate,” “intend,” “estimate,” “believe,” “expect,” “plan,” “should,” “hypothetical,”

“potential,” “forecast,” “project,” variations of

such words and similar expressions are intended to identify forward-looking statements. Factors that may cause actual results to differ are often

presented with the forward-looking statements themselves. Other factors

that could cause actual results to differ materially from those contemplated in any forward-looking statements made by

us herein are discussed in filings we make with the United States Securities

and Exchange Commission (SEC), including our Annual Report on Form 10-K and subsequent reports on Form 10-Q

and Form 8-K and available on our website: http://www.pseg.com. These

factors include, but are not limited to: •

adverse changes in the demand for or the price of the capacity and energy that

we sell into wholesale electricity markets, •

adverse changes in energy industry law, policies and regulation, including

market structures and a potential shift away from competitive markets toward subsidized market

mechanisms, transmission planning and cost allocation rules, including rules

regarding how transmission is planned and who is permitted to build transmission in the future, and

reliability standards,

•

any inability of our transmission and distribution businesses to obtain

adequate and timely rate relief and regulatory approvals from federal and state regulators,

•

changes in federal and state environmental regulations and enforcement that

could increase our costs or limit our operations, •

changes in nuclear regulation and/or general developments in the nuclear power

industry, including various impacts from any accidents or incidents experienced at our facilities or

by others in the industry, that could limit operations of our nuclear

generating units, •

actions or activities at one of our nuclear units located on a multi-unit

site that might adversely affect our ability to continue to operate that unit or other units located at the same site,

•

any inability to manage our energy obligations, available supply and risks,

adverse outcomes of any legal, regulatory or other proceeding,

settlement, investigation or claim applicable to us and/or the energy industry,

•

any deterioration in our credit quality or the credit quality of our

counterparties, •

availability of capital and credit at commercially reasonable terms and

conditions and our ability to meet cash needs, •

changes in the cost of, or interruption in the supply of, fuel and other

commodities necessary to the operation of our generating units, •

delays in receipt of necessary permits and approvals for our

construction and development activities, •

delays or unforeseen cost escalations in our construction and development

activities, •

any inability to achieve, or continue to sustain, our expected levels of

operating performance, •

any equipment failures, accidents, severe weather events or other incidents

that impact our ability to provide safe and reliable service to our customers, and any inability to obtain

sufficient insurance coverage or recover proceeds of insurance with respect to

such events, •

acts of terrorism, cybersecurity attacks or intrusions that could adversely

impact our businesses, •

increases in competition in energy supply markets as well as competition for

certain transmission projects, •

any inability to realize anticipated tax benefits or retain tax credits,

•

challenges associated with recruitment and/or retention of a qualified

workforce, •

adverse performance of our decommissioning and defined benefit plan trust fund

investments and changes in funding requirements, •

changes in technology, such as distributed generation and micro grids, and

greater reliance on these technologies, and •

changes in customer behaviors, including increases in energy efficiency,

net-metering and demand response. All of the forward-looking

statements made in this report are qualified by these cautionary statements and we cannot assure you that the results or developments anticipated by management

will be realized or even if realized, will have the expected consequences to,

or effects on, us or our business prospects, financial condition or results of operations. Readers are cautioned not

to place undue reliance on these forward-looking statements in making any

investment decision. Forward-looking statements made in this report apply only as of the date of this report. While

we may elect to update forward-looking statements from time to time, we

specifically disclaim any obligation to do so, even if internal estimates change, unless otherwise required by applicable

securities laws.

The forward-looking statements contained in this report are intended to

qualify for the safe harbor provisions of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the

Securities Exchange Act of 1934, as amended. |

2

GAAP Disclaimer

PSEG presents Operating Earnings in addition to its Net Income reported in

accordance with accounting principles generally accepted in the United

States (GAAP). Operating Earnings is a non-GAAP financial measure that

differs from Net Income because it excludes gains or losses associated with

Nuclear Decommissioning Trust (NDT), Mark-to-Market (MTM)

accounting, and other material one-time items. PSEG presents

Operating Earnings because management believes that it is appropriate for

investors to

consider results excluding these items in addition to the results reported in

accordance with GAAP. PSEG believes that the non-GAAP financial

measure of Operating Earnings provides a consistent and comparable

measure of performance of its businesses to help shareholders understand

performance trends. This information is not

intended to be viewed as an

alternative to GAAP information. The last slide in this presentation includes

a list of items excluded from Net Income to reconcile to Operating Earnings,

with a reference to that slide included on each of the slides where the

non- GAAP information appears.

These

materials

and

other

financial

releases

can

be

found

on

the

pseg.com

website

under the investor tab, or at http://investor.pseg.com/

|

PSEG

2014 Q2 Review

Ralph Izzo

Chairman, President and Chief Executive Officer |

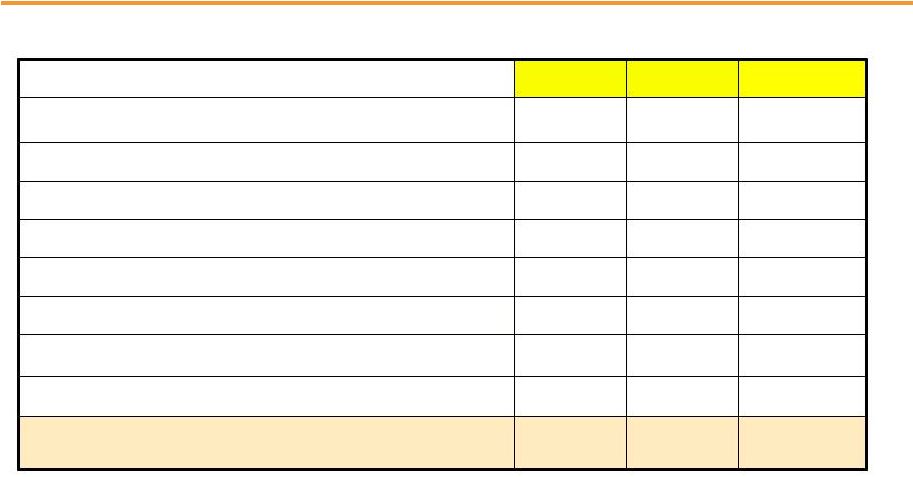

4

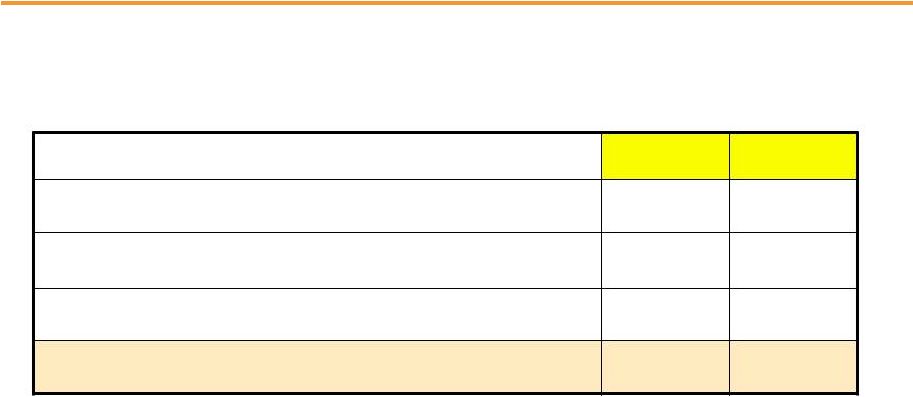

Q2 Earnings Summary

$ millions (except EPS)

2014

2013

Operating Earnings

$ 245

$ 243

Reconciling Items, Net of Tax

(33)

90

Net Income

$ 212

$ 333

EPS from Operating Earnings*

$ 0.49

$ 0.48

Quarter ended June 30

* See Slide A for Items excluded from Net Income to reconcile to Operating Earnings.

|

5

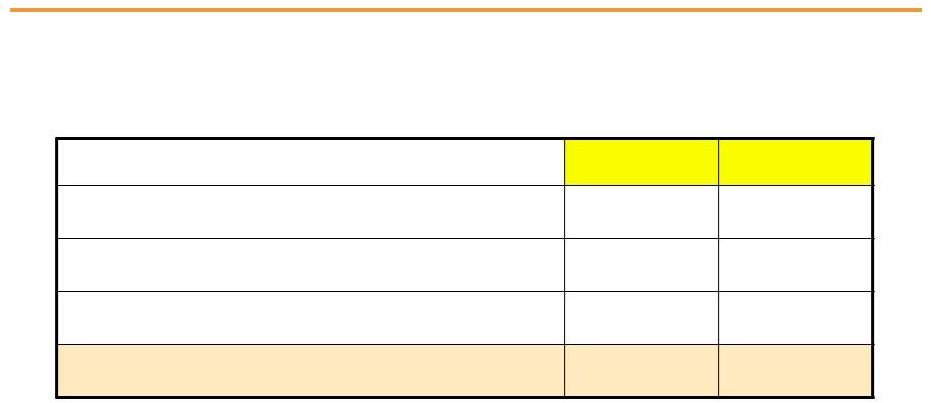

First Half 2014 Earnings Summary

Six months ended June

30 $

millions (except EPS) Operating Earnings

Reconciling Items, Net of Tax

Net Income

EPS from Operating Earnings*

2014

2013

$ 760

(162)

$ 598

$ 1.50

$ 676

(23)

$ 653

$ 1.33

* See Slide A for Items excluded from Net Income to reconcile to Operating Earnings. |

6

PSEG

–

Q2

2014

Highlights

Earnings on Track

Operating earnings of $0.49 vs. $0.48 per share in Q2 2013

Increased earnings contribution from PSE&G’s investment in

Transmission Expect 2014 Operating Earnings to be at the upper end of

the $2.55

to

$2.75

per

share

guidance

range

–

assuming

normal

weather

and

plant

operations

for the balance of the year

Operating Review

PSEG Power output down 5% vs. Q2 2013 from Linden and Salem 2 outages,

partially offset by improvement in coal generation

PSE&G placed the 230 kV North Central Reliability transmission project in

service Power’s fleet fully restored from storm outages

PSEG Disciplined Capital Investment

BPU approved $1.22 billion investment in PSE&G’s Energy Strong

infrastructure program PJM

deferred

a

final

decision

on

its

recommended

solution,

to

be

built

by

PSE&G,

for

the

Artificial Island project via FERC 1000 competitive bidding process

Market Developments

Recent EPA actions on 316(b) and GHGs |

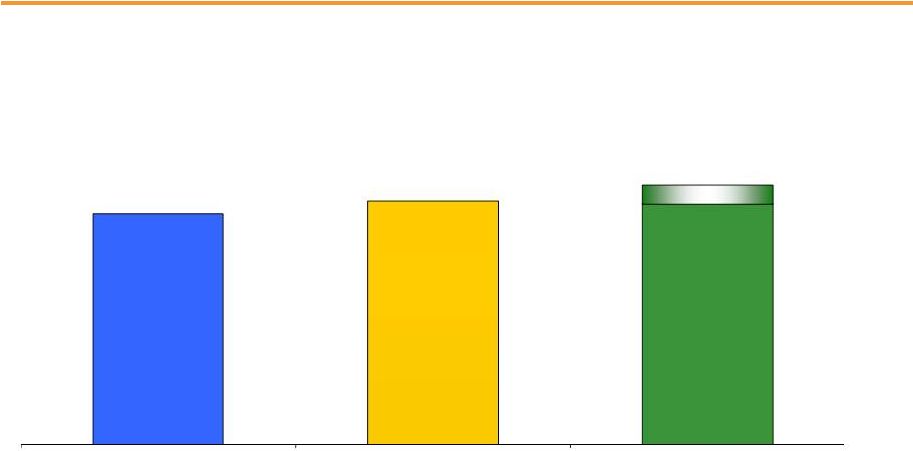

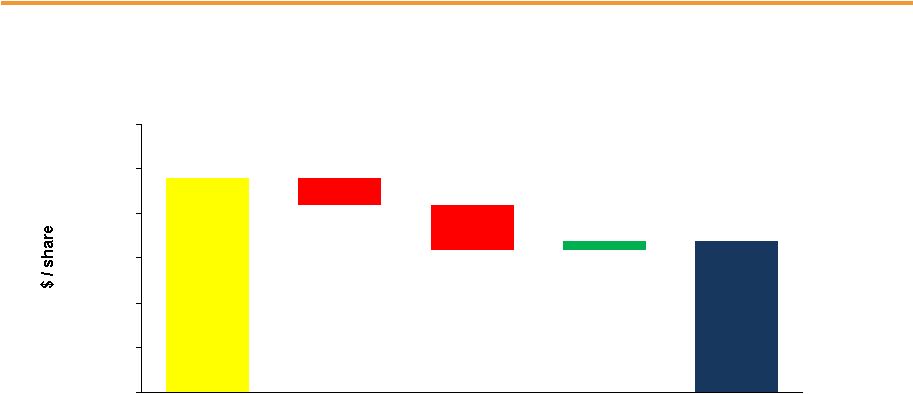

7

$2.55 -

$2.75E

PSEG –

2014 Earnings Guidance at the Upper End of Range

$2.44

$2.58

2014 guidance reflects increased level of investment,

pension savings and assumes normal weather and unit operations for rest of

year 2012 Operating Earnings*

2013 Operating Earnings*

2014 Operating Earnings Guidance

* See Slide A for Items excluded from Net Income to reconcile to Operating Earnings. E =

Estimate. |

PSEG

2014 Q2 Operating Company Review

Caroline Dorsa

EVP and Chief Financial Officer |

9

Q2 Operating Earnings by Subsidiary

Operating Earnings

Earnings per Share

$ millions (except EPS)

2014

2013

2014

2013

PSE&G

$ 151

$ 121

$ 0.30

$ 0.24

PSEG Power

87

120

0.17

0.24

PSEG Enterprise/Other

7

2

0.02

-

Operating Earnings*

$ 245

$ 243

$ 0.49

$ 0.48

Quarter ended June 30

* See Slide A for Items excluded from Net Income to reconcile to Operating Earnings. |

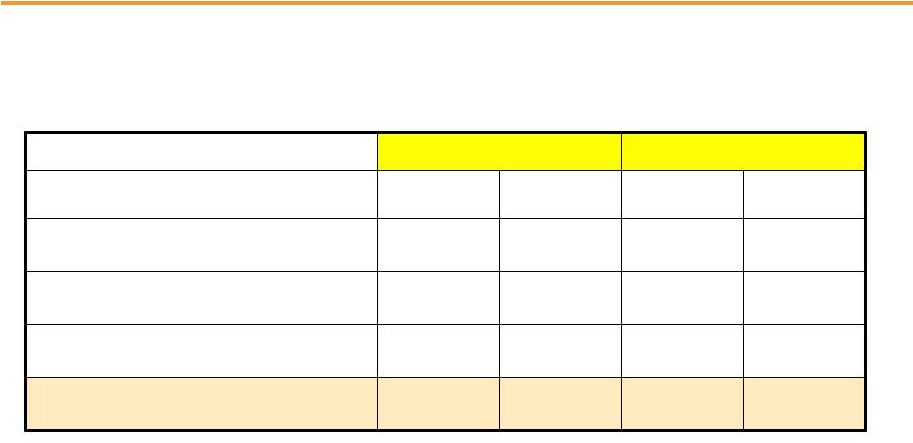

10

$0.48

0.06

0.02

$0.49

(0.07)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

PSEG EPS Reconciliation –

Q2 2014 versus Q2 2013

Q2 2014

Operating

Earnings*

Q2 2013

Operating

Earnings*

PSEG Power

PSE&G

Enterprise/

Other

Capacity 0.04

Re-Contracting & Market

Pricing (0.04)

Lower Volume (0.03)

O&M (0.04)

D&A (0.01)

Taxes & Other 0.01

Transmission

Net Earnings 0.03

Gas Volume &

Other Revenue 0.01

Weather (0.01)

O&M 0.02

Lower Interest

Expense 0.01

PSEG

Long Island

and Other

* See Slide A for Items excluded from Net Income to reconcile to Operating Earnings. |

11

First Half Operating Earnings by Subsidiary

Operating Earnings

Earnings per Share

$ millions (except EPS)

2014

2013

2014

2013

PSE&G

$ 365

$ 300

$ 0.72

$ 0.59

PSEG Power

380

374

0.75

0.74

PSEG Enterprise/Other

15

2

0.03

-

Operating Earnings*

$ 760

$ 676

$ 1.50

$ 1.33

Six months ended June 30

•See Slide A for Items excluded from Net Income to reconcile to Operating

Earnings. |

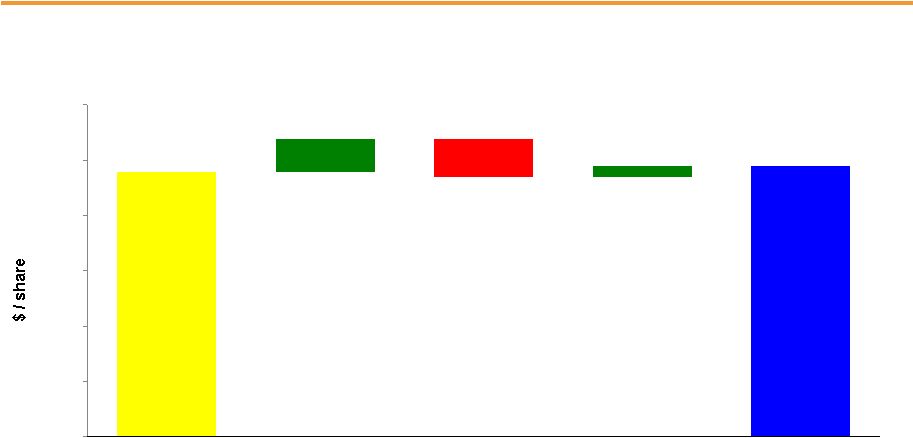

12

$1.50

0.03

0.01

0.13

$1.33

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

PSEG EPS Reconciliation –

First Half 2014 versus First Half 2013

YTD 2014

Operating

Earnings*

YTD 2013

Operating

Earnings*

Capacity 0.15

Re-Contracting

& Market Pricing

(0.04)

Lower Volume (0.01)

O&M (0.08)

D&A (0.01)

PSEG Power

Transmission

Net Earnings 0.06

Gas Volume,

Demand & Other

Revenue 0.03

Distribution

O&M 0.02

Lower Interest

Expense 0.01

Taxes & Other 0.01

PSE&G

Enterprise/

Other

PSEG Long

Island and

Other

* See Slide A for Items excluded from Net Income to reconcile to Operating Earnings.

|

PSE&G

2014 Q2 Review |

14

PSE&G –

Q2 EPS Summary

$ millions (except EPS)

Q2 2014

Q2 2013

Variance

Operating Revenues

$ 1,435

$ 1,423

$ 12

Operating Expenses

565

580

(15)

362

369

(7)

217

207

10

-

14

(14)

Total Operating Expenses

1,144

1,170

(26)

Operating Earnings/Net Income

$ 151

$ 121

$ 30

EPS from Operating Earnings/Net Income

$ 0.30

$ 0.24

$ 0.06

Energy Costs

Operation & Maintenance

Depreciation & Amortization

Taxes Other than Income Taxes |

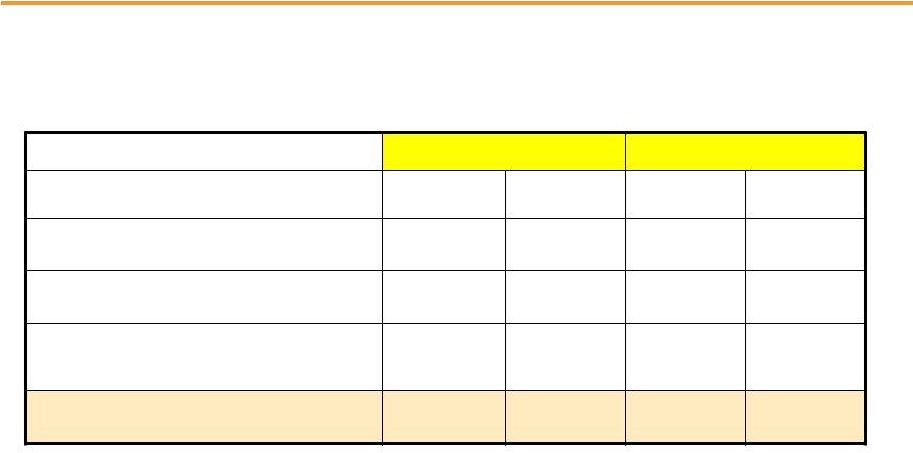

15

PSE&G EPS Reconciliation –

Q2 2014

versus Q2 2013

Q2 2013

Operating

Earnings*

Q2 2014

Operating

Earnings*

* Operating Earnings is equal to Net Income.

$0.24

0.03

0.03

$0.30

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

Transmission

Net Earnings 0.03

Gas Volume &

Other Revenue 0.01

Weather (0.01)

O&M 0.02

Lower Interest

Expense 0.01 |

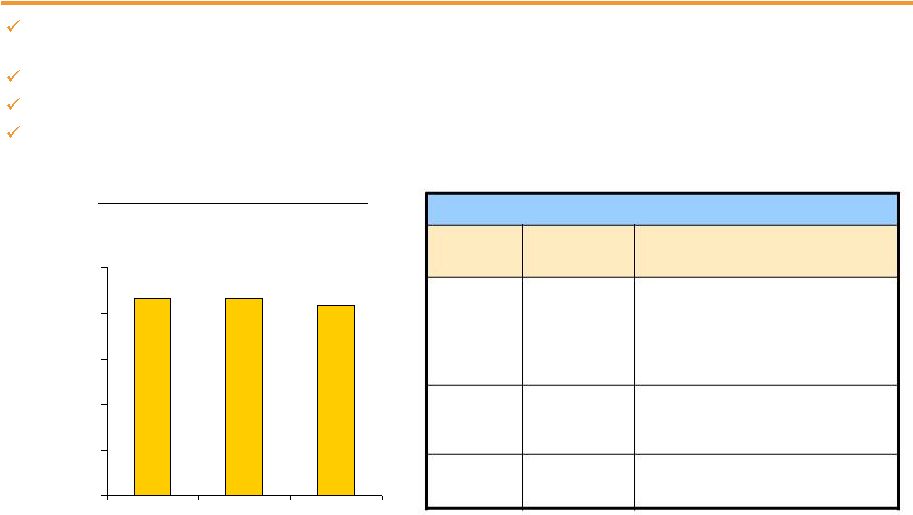

16

PSE&G –

Monthly Summer Weather Data

84

579

2,771

83

1,242

3,330

170

794

3,054

0

400

800

1,200

1,600

2,000

2,400

2,800

3,200

3,600

4,000

April

May

June

2014

2013

Normal

2014 vs. 2013 vs. Normal

PSE&G Monthly Temperature Humidity Index (THI)

-26% Q2 2014 vs. Q2 2013

-15% Q2 2014 vs. Normal |

17

PSE&G –

Q2 2014 Operating Highlights

Operations

PSE&G received final NJBPU approval to invest $1.22 billion in the Energy

Strong program PJM

deferred

a

final

decision

on

its

recommended

solution,

to

be

built

by

PSE&G,

for

the

Artificial Island project via FERC 1000 competitive bidding process

Construction

of

major

transmission

lines

progressing

on

schedule

and

on

budget

PSE&G residential gas customers to benefit from a proposed rate reduction this

October, estimated to save the average customer $100 per year

PSE&G plans to invest over $2.2 billion in its T&D system in 2014

PSE&G’s 2014-2018 Capital Spending increased to $11.3 billion

with recently approved Energy Strong PSE&G earned its authorized return

in the quarter PSE&G issued $250 million, 1.8% secured medium-term

notes due June 2019 and $250 million, 4% secured medium-term notes due

June 2044 S&P revised PSE&G’s credit rating outlook from Stable

to Positive Financial

Q2 2014 weather was milder than Q2 2013: Heating degree days were 3% below

normal, and cooling load was 15% below normal

Economy slowly improving, weather normalized electric sales up 1.6% YTD;

residential demand up 0.5% and commercial sector up 1.3% in Q2

Gas deliveries (weather normal), up 7.5% in Q2 and up 4.4% for the YTD, continue to

benefit from decline in supply costs

Regulatory and Market

Environment |

PSEG

Power 2014 Q2 Review |

19

PSEG Power –

Q2 EPS Summary

$ millions (except EPS)

Q2 2014

Q2 2013

Variance

Operating Revenues

$ 986

$ 1,193

$ (207)

Operating Earnings

87

120

(33)

Reconciling Items, Net of Tax**

(33)

90

(123)

Net Income

$ 54

$ 210

$ (156)

EPS from Operating Earnings*

$ 0.17

$ 0.24

$ (0.07)

* See Slide A for Items excluded from Net Income to reconcile to Operating Earnings.

** Includes the financial impact from Mark-to-Market positions with forward delivery

months. |

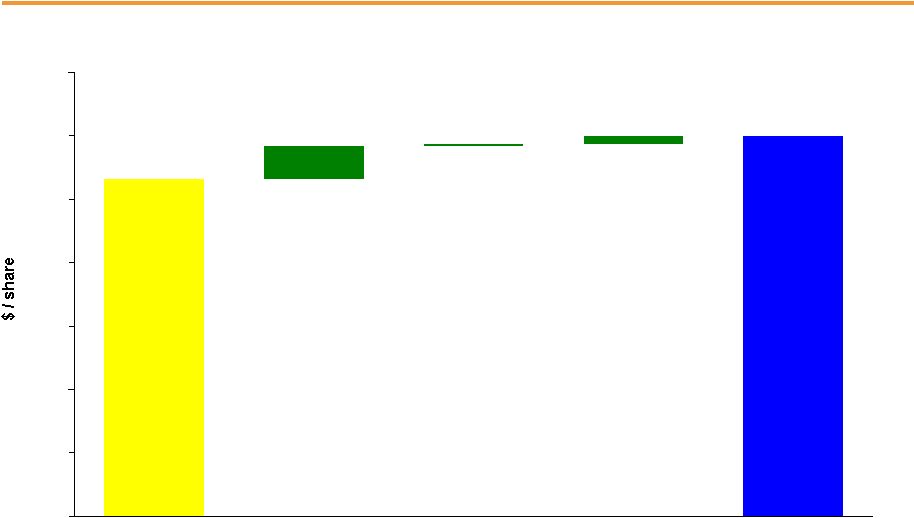

20

$0.24

0.01

$0.17

(0.03)

(0.05)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

Capacity 0.04

Lower Volume (0.03)

Re-Contracting &

Market Pricing

(0.04)

PSEG Power EPS Reconciliation –

Q2 2014 versus Q2 2013

Q2 2014

Operating

Earnings*

Q2 2013

Operating

Earnings*

O&M (0.04)

D&A (0.01)

Taxes

and

Other

* See Slide A for Items excluded from Net Income to reconcile to Operating Earnings.

|

21

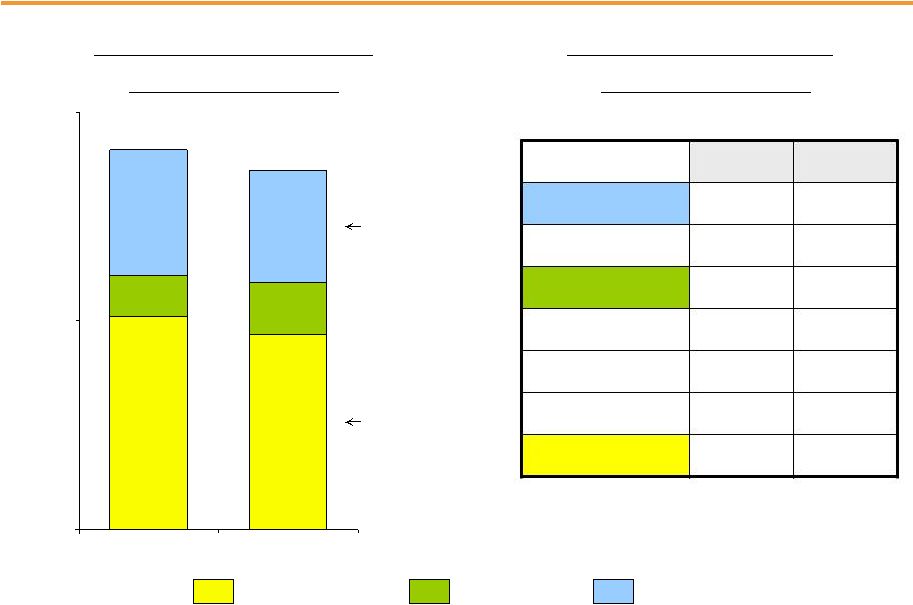

PSEG Power –

Q2 2014 Generation Measures

7,147

6,538

4,187

3,788

1,724

1,384

0

7,000

14,000

2013

2014

Quarter ended June 30

Total Nuclear

Total Coal*

Oil & Natural Gas

Generation by Fuel (GWh)**

12,050

Quarter ended June 30

2013

2014

Combined

Cycle

PJM and NY

57%

49%

Coal*

NJ (Coal/Gas)

8%

14%

PA

70%

80%

CT

3%

4%

Nuclear

88%

81%

12,718

Fleet Capacity Factors (%)

54%

of

Output

31%

of

Output

* Includes figures for Pumped Storage; also includes Natural Gas fuel switching

intervals. ** Excludes Solar and Kalaeloa. |

22

PSEG Power –

YTD 2014 Generation Measures

15,284

14,588

7,764

3,590

4,266

8,001

0

10,000

20,000

30,000

2013

2014

Six Months ended June 30

Total Nuclear

Total Coal*

Oil & Natural Gas

26,875

26,618

Six Months ended June 30

2013

2014

Combined Cycle

PJM and NY

55%

48%

Coal*

NJ (Coal/Gas)

13%

17%

PA

78%

81%

CT

19%

38%

Nuclear

94%

90%

29%

of

Output

55%

of

Output

Generation by Fuel (GWh)**

Fleet Capacity Factors (%)

* Includes figures for Pumped Storage; also includes Natural Gas fuel switching

intervals. ** Excludes Solar and Kalaeloa. |

23

PSEG Power –

Fuel Costs

Quarter ended June 30

($ millions)

2013

2014

Coal

$30

$40

Oil & Gas

160

119

Total Fossil

190

159

Nuclear

52

47

Total Fuel Cost

$242

$206

Total Generation

(GWh)

12,718

12,050

$ / MWh

19.03

17.10

PSEG Power –

Fuel Costs

YTD June 30

($ millions)

2013

2014

Coal

$96

$127

Oil & Gas

338

484

Total Fossil

434

611

Nuclear

110

109

Total Fuel Cost

$544

$720

Total Generation

(GWh)

26,875

26,618

$ / MWh

20.24

27.05 |

24

PSEG Power –

Gross Margin Performance

$0

$10

$20

$30

$40

$50

2012

2013

2014

$42

$43

Quarter ended June 30

Weather-driven volatility pushed natural gas and power prices to multi-year

highs; Q2 spot prices in PJM peaked in April

Decline in average hedge prices

Capacity prices reset on June 1 to ~$166/MW-day and remain stable for the next

three capacity years Fuel

flexibility

and

access

to

lower

cost

Marcellus

gas

continue

to

benefit

margin

Q2 2014 Regional Performance

Region

Gross

Margin ($M)

2014 Performance

PJM

$468

Higher capacity pricing for most of

the quarter offset lower hedge prices.

Output hurt by outages at Linden

and Salem 2.

New

England

$18

Higher volume offset lower priced

hedges.

New York

$18

Higher volume offset lower pricing.

PSEG Power Gross Margin ($/MWh)

$43 |

25

Hedging Update…

Contracted Energy*

* Hedge

percentages

and

prices

as

of

June

30,

2014.

Revenues

of

full

requirement

load

deals

based

on

contract

price,

including

renewable

energy

credits,

ancillary,

and

transmission

components

but

excluding

capacity.

Hedges

include

positions

with

MTM

accounting

treatment

and

options.

Jul-Dec

2014

2015

2016

Volume TWh

17

36

36

Base Load

% Hedged

100%

100%

45-50%

(Nuclear and Base Load Coal)

Price $/MWh

$50

$50

$51

Volume TWh

13

21

19

Intermediate Coal, Combined

% Hedged

35-40%

5-10%

0%

Cycle, Peaking

Price $/MWh

$50

$50

$51

Volume TWh

30

55-57

55-57

Total

% Hedged

70-75%

65-70%

30-35%

Price $/MWh

$50

$50

$51 |

26

PSEG Power –

Q2 2014 Operating Highlights

Q2 output down 5% due to Linden and Salem 2 outages

Advance gas path uprates (~63MW) completed at Linden

Output of NJ coal units was 10% coal, 90% gas fueled in Q2; 45% coal, 55% gas for

the YTD Operations

Financial

Regulatory and Market

Environment

Capacity pricing for the 2014/2015 capacity year reset to $166 MW/day on June

1 Access to Marcellus gas benefited off-system sales and reduced the

fleet’s cost of gas FERC and PJM reviewing implications of circuit

court ruling on use of DR in capacity auctions Power recorded a charge of $25

million in Q1 2014 related to potential liability associated with the

discovery of bidding errors in the PJM energy market. Power identified additional

errors in Q2 2014, as well as differences between the quantity of energy

offered into the market and the amount for which it was compensated

in

the

capacity

market.

Power

has

corrected

these

errors.

This

matter

remains

under

review

with the FERC,

PJM and its Independent Market Monitor. We are unable to estimate the

ultimate impact or predict any resulting penalties or other costs associated

with the matter at this time. Power’s total debt as a percentage of

capital at June 30 was 32% S&P revised PSEG Power’s credit rating

outlook from Stable to Positive |

PSEG |

28

PSEG Financial Highlights

Maintaining

2014

operating

earnings

guidance

of

$2.55

-

$2.75

per

share,

expecting results at upper end of the range

Focused on maintaining operating efficiency and customer reliability

PSE&G expected to grow at double-digit rate in 2014 and provide over 50% of

operating earnings PSE&G expanded capital program of $11.3 billion over

2014-2018 is expected to further support double digit rate base

growth PSEG capital program now projected at $13.1 billion over the

2014-2018 period PSE&G has begun construction of Energy Strong

infrastructure projects and continues to build out its Transmission plan

on-time and on-budget Financial position remains strong

Positive cash from Power and increasing cash flow from PSE&G supports

sustainable dividend growth and funds capital spending program without the

need to issue equity PSEG’s debt as a percentage of capital was 42% at

June 30 Standard & Poor’s revised the credit rating outlooks of

PSEG, PSE&G and PSEG Power from Stable to Positive in May

Long history of returning cash to the shareholder through the common dividend,

with opportunity for consistent and sustainable dividend growth

|

29

PSEG 2014 Operating Earnings Guidance -

By Subsidiary

$ millions (except EPS)

2014E

2013

2012

PSE&G

$705 –

$745

$612

$528

PSEG Power

$550 –

$610

$710

$663

PSEG Enterprise/Other

$35 –

$40

$(13)

$45

Operating Earnings*

$1,290 –

$1,395

$1,309

$1,236

Earnings per Share

$2.55 –

$2.75

$2.58

$2.44

* See Slide A for Items excluded from Net Income to reconcile to Operating Earnings. E =

Estimate. |

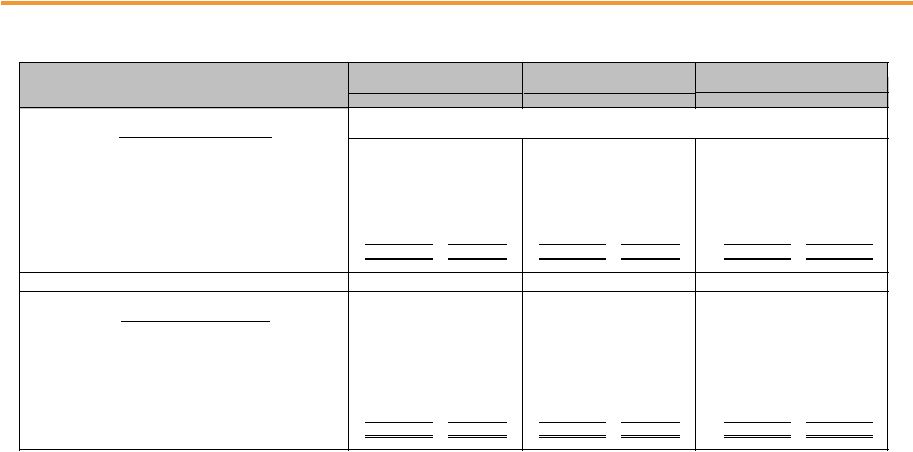

Expiration

Total

Available

Company

Facility

Date

Facility

Usage

Liquidity

($Millions)

PSE&G

5-year Credit Facility

Mar-18

$600

1

$13

$587

5-Year Credit Facility (Power)

Apr-19

$1,600

$114

$1,486

5-Year Credit Facility (Power)

Mar-18

$1,000

2

$0

$1,000

5-Year Bilateral (Power)

Sep-15

$100

$100

$0

5-year Credit Facility (PSEG)

Apr-19

$500

$8

$492

5-year Credit Facility (PSEG)

Mar-18

$500

3

$0

$500

Total

$4,300

$4,065

1 PSE&G Facility to be reduced by $29M on April 15, 2016

$278

2 Power Facility to be reduced by $48M on April 15, 2016

PSE&G ST Investment

$224

3 PSEG Facility to be reduced by $23M on April 15, 2016

Total Liquidity Available

$4,567

Total Parent / Power Liquidity

$3,756

PSEG /

Power

PSEG Money Pool ST Investment

PSEG Liquidity as of June 30, 2014

30

$235 |

A

Items Excluded from Net Income to Reconcile to Operating Earnings

Please see Slide 2 for an explanation of PSEG’s use of Operating Earnings as a

non-GAAP financial measure and how it differs from Net Income.

2014

2013

2014

2013

2013

2012

Earnings Impact ($ Millions)

Operating Earnings

245

$

243

$

760

$

676

$

1,309

$

1,236

$

Gain (Loss) on Nuclear Decommissioning Trust (NDT)

Fund Related Activity (PSEG Power)

14

8

23

17

40

52

Gain (Loss) on Mark-to-Market (MTM)

(a)

(PSEG Power)

(42)

80

(174)

(25)

(74)

(10)

Lease Related Activity (PSEG Enterprise/Other)

-

-

-

-

-

36

Storm O&M, net of insurance recoveries (PSEG Power)

(5)

2

(11)

(15)

(32)

(39)

Net Income

212

$

333

$

598

$

653

$

1,243

$

1,275

$

Fully Diluted Average Shares Outstanding (in Millions)

508

507

508

507

508

507

Per Share Impact (Diluted)

Operating Earnings

0.49

$

0.48

$

1.50

$

1.33

$

2.58

$

2.44

$

Gain (Loss) on NDT Fund Related Activity (PSEG Power)

0.02

0.02

0.04

0.04

0.08

0.10

Gain (Loss) on MTM

(a)

(PSEG Power)

(0.08)

0.16

(0.34)

(0.05)

(0.14)

(0.02)

Lease Related Activity (PSEG Enterprise/Other)

-

-

-

-

-

0.07

Storm O&M, net of insurance recoveries (PSEG Power)

(0.01)

-

(0.02)

(0.03)

(0.07)

(0.08)

Net Income

0.42

$

0.66

$

1.18

$

1.29

$

2.45

$

2.51

$

(a) Includes the financial impact from positions with forward delivery

months. June 30,

June 30,

December 31,

(Unaudited)

PUBLIC SERVICE ENTERPRISE GROUP INCORPORATED

Reconciling Items, net of tax

Three Months Ended

Six Months Ended

Year Ended |