Attached files

| file | filename |

|---|---|

| 8-K - 8-K - PRIVATEBANCORP, INC | pvtb063020148-ker.htm |

Exhibit 99.1

For further information:

Media Contact:

Amy Yuhn

312-564-1378

ayuhn@theprivatebank.com

Investor Relations Contact:

Jeanette O'Loughlin

312-564-6076

joloughlin@theprivatebank.com

PrivateBancorp Reports Second Quarter 2014 Earnings

Earnings per share of $0.52 for second quarter 2014, up 41 percent from second quarter 2013

and 18 percent from first quarter 2014

CHICAGO, July 17, 2014 - PrivateBancorp, Inc. (NASDAQ: PVTB) today reported net income of $40.8 million, or $0.52 per diluted share, for the second quarter 2014, compared to $28.9 million, or $0.37 per diluted share, for the second quarter 2013 and $34.5 million, or $0.44 per diluted share, for the first quarter 2014. For the six months ended June 30, 2014, the Company had net income of $75.3 million, or $0.96 per diluted share, compared to $56.2 million, or $0.72 per diluted share, for the six months ended June 30, 2013.

“Our second quarter results reflect the benefit of our consistent focus on developing client relationships as higher net interest income and strong fee income led to net income of $40.8 million, a 41 percent increase over last year,” said Larry D. Richman, President and CEO, PrivateBancorp, Inc. “Total loans increased 10 percent year-over-year, with about $365 million in fundings to new clients in the second quarter. Operating profit was up 21 percent from a year ago on higher revenue driven by loan growth and lower credit costs.

“With a strong first half of the year behind us, I am pleased with our success in adding new clients and expanding our relationships with existing clients,” Richman continued. “Client sentiment continues to improve, and I like how we are positioned for the rest of the year to do more with commercial middle market companies as they grow their own businesses.”

Second Quarter 2014 Highlights

• | Return on average common equity improved to 11.9 percent and return on average assets improved to 1.14 percent for the second quarter 2014. |

• | Operating profit increased to $67.9 million, up 21 percent from the second quarter 2013 and 13 percent from the first quarter 2014. Higher revenues from continued growth in earning assets and increased fee revenue drove the improvement in the efficiency ratio to 52.6 percent for the second quarter 2014, from 57.9 percent for the second quarter 2013 and 55.8 percent for the first quarter 2014. |

• | Total loans increased to $11.1 billion, up 10 percent from a year ago and 2 percent from March 31, 2014, primarily driven by growth in commercial and industrial loans. Average loans grew $932.6 million from the second quarter 2013 and $335.7 million from the first quarter 2014. |

1

• | Total deposits grew to $12.2 billion, compared to $11.3 billion as of June 30, 2013, and $11.9 billion as of March 31, 2014. Noninterest-bearing demand deposits increased $283.7 million during the quarter. |

• | Net interest margin was 3.21 percent, compared to 3.22 percent for the second quarter 2013 and 3.23 percent for the first quarter 2014. |

• | Provision for loan and covered loan losses was $327,000, as a $2.0 million provision for loan losses was offset by $1.7 million of covered loan recoveries recorded during the second quarter 2014. |

Operating Performance

Net interest income was $112.4 million in the second quarter 2014, an increase of 8 percent compared to the second quarter 2013, and up 3 percent compared to the first quarter 2014. Compared to the previous periods, interest income benefited from higher average loans as loan yields continued to decline. Average loans increased 9 percent from the second quarter 2013 and 3 percent from the first quarter 2014. Interest expense declined to $16.6 million from $17.9 million for the second quarter 2013, largely reflecting the prepayment of a subordinated debt facility in the fourth quarter 2013, while a $385.7 million increase in average noninterest-bearing demand deposits was also beneficial. Net interest margin was 3.21 percent in the second quarter 2014, compared to 3.23 percent in the first quarter 2014 and 3.22 percent in the second quarter 2013. Larger-than-average interest recoveries in the first quarter 2014 contributed three basis points to net interest margin. On a sequential basis, net interest margin benefited from higher loan fees; however, the competitive environment continued to pressure loan pricing.

Noninterest income was $30.3 million in the second quarter 2014, up $1.3 million compared to the second quarter 2013 and $4.0 million compared to the first quarter 2014, primarily due to higher syndication fees. Syndication fees were $5.4 million, up $2.3 million compared to the second quarter 2013 and $2.1 million compared to the first quarter 2014, driven by strong loan activity during the current quarter. Mortgage banking revenue was $2.6 million compared to $3.2 million for the second quarter 2013 and $1.6 million for the first quarter 2014, reflecting industry-wide mortgage origination trends.

Capital markets revenue of $5.0 million, down from $6.0 million for the second quarter 2013, increased from $4.1 million for the first quarter 2014. Excluding the impact of the credit valuation adjustment, capital markets revenue increased $1.1 million on a sequential basis, primarily related to a higher level of foreign exchange-related transactions. Treasury management fees were $6.7 million in the second quarter 2014, up 8 percent from the second quarter 2013, largely due to additional client relationships, and were relatively unchanged from the first quarter 2014.

Asset management revenue was $4.4 million in the second quarter 2014, compared to $4.8 million for the second quarter 2013 and $4.3 million for the first quarter 2014. The prior-year period included fees generated by the investment management subsidiary sold at year-end. Assets under management and administration were $6.4 billion as of June 30, 2014, compared to $5.4 billion a year ago and $6.0 billion at March 31, 2014.

Expenses

Noninterest expense of $75.5 million was $1.8 million lower than the second quarter 2013 and down slightly compared to the first quarter 2014.

Salary and employee benefits expense was relatively unchanged compared to the first quarter 2014, as first quarter's seasonally higher payroll taxes and benefits were offset by a full quarter's impact of annual salary adjustments, additional performance-based incentive compensation, and higher revenue-based compensation. Compared to the second quarter 2013, salary and employee benefits expense increased 11 percent due to the impact of annual salary adjustments during the first quarter, additional staff, and increased incentive compensation based on improved performance.

2

Marketing expense was up $1.2 million compared to the first quarter 2014, primarily driven by the launch of an advertising campaign in the second quarter. Net foreclosed property expense decreased 50 percent compared to the second quarter 2013, primarily reflecting reduced inventory of foreclosed property (OREO). While expected to trend lower going forward, compared to the first quarter 2014, net foreclosed property expense was relatively unchanged at $2.8 million.

Other expenses declined $4.0 million from the second quarter 2013 and $2.3 million from the first quarter 2014. The second quarter 2013 included one-time charges of $3.0 million related to restructuring costs and a charge on repurchased loans. During the second quarter 2014, other expense benefited from a change in unfunded commitments, as certain nonperforming assets with related commitments were reduced.

Credit Quality

Nonperforming assets were 0.66 percent of total assets at June 30, 2014, down from 1.33 percent at June 30, 2013, and 0.82 percent at March 31, 2014. At June 30, 2014, nonperforming loans were $76.6 million, down $45.2 million from June 30, 2013, and $17.2 million from March 31, 2014. OREO of $19.8 million at June 30, 2014, declined $37.3 million from June 30, 2013, and $3.7 million from March 31, 2014.

The allowance for loan losses as a percentage of total loans was 1.32 percent at June 30, 2014, compared to 1.34 percent at March 31, 2014. The provision for loan losses was $2.0 million for the second quarter 2014 compared to $3.4 million for the first quarter 2014. Charge-off levels remained low and provision expense benefited from the release of specific reserves previously established for problem credits resolved in the second quarter 2014. Specific reserves declined $4.3 million from the first quarter 2014. General allocated reserves increased on a sequential basis, reflecting loan growth and changes in the composition of the loan portfolio.

Credit quality results exclude covered assets acquired through an FDIC-assisted transaction that are subject to a loss sharing agreement.

Balance Sheet

Total assets were $14.6 billion at June 30, 2014, up compared to $13.5 billion at June 30, 2013, and $14.3 billion at March 31, 2014. Total loans of $11.1 billion grew $1.0 billion, or 10 percent, from June 30, 2013, and $212.0 million, or 2 percent, from the previous quarter end. Excluded from total loans at June 30, 2014, were $80.7 million of loans held-for-sale, composed of $60.4 million in commercial credits funded in the second quarter that are expected to be syndicated and mortgage loans to be sold in the third quarter. At June 30, 2014, total commercial loans comprised 68 percent of total loans, up from 66 percent a year ago, and total commercial real estate and construction loans comprised 26 percent of total loans, down slightly from 27 percent at June 30, 2013. The Company's investment securities portfolio was $2.6 billion at June 30, 2014, up 2 percent from June 30, 2013, and consistent with March 31, 2014.

Total liabilities were $13.2 billion at June 30, 2014, up compared to $12.2 billion at June 30, 2013, and $13.0 billion compared to March 31, 2014. Total deposits were $12.2 billion at June 30, 2014, an increase of $927.9 million, or 8 percent, from June 30, 2013, and $350.0 million, or 3 percent, from March 31, 2014. Noninterest bearing demand deposits comprised 28 percent of total deposits at June 30, 2014, up from 24 percent at June 30, 2013, and 26 percent at March 31, 2014. At June 30, 2014, the loan-to-deposit ratio was 91 percent, compared to 89 percent as of June 30, 2013, and 92 percent as of March 31, 2014.

Capital

As of June 30, 2014, the total risk-based capital ratio was 13.41 percent, the Tier 1 risk-based capital ratio was 11.24 percent, and the leverage ratio was 10.63 percent. The Tier 1 common capital ratio was 9.42 percent (excluding the effect of the final Basel III capital rules that go into effect January 2015) and the tangible common equity ratio was 8.94 percent at the end of the second quarter 2014.

3

Quarterly Conference Call and Webcast Presentation

PrivateBancorp will host a conference call Thursday, July 17, 2014, at 10 a.m. CDT. The call may be accessed by telephone at (888) 782-9127 (U.S. and Canada) or (706) 634-5643 (International) and entering passcode #57714115. A live webcast of the call can be accessed on the Company website at: investor.theprivatebank.com or by visiting the Investor Relations tab under the About Us section. A rebroadcast will be available beginning approximately two hours after the call until midnight July 30, 2014, by calling (855) 859-2056 (U.S. and Canada) or (404) 537-3406 (International) and entering passcode #57714115.

About PrivateBancorp, Inc.

PrivateBancorp, Inc., through its subsidiaries, delivers customized business and personal financial services to middle-market companies, as well as business owners, executives, entrepreneurs and families in all of the markets and communities we serve. As of June 30, 2014, the Company had 33 offices in 10 states and $14.6 billion in assets. The Company’s website is www.theprivatebank.com.

Forward-Looking Statements

Statements made in this press release that are not historical facts may constitute forward-looking statements within the meaning of federal securities laws. Our ability to predict results or the actual effects of future plans, strategies or events is inherently uncertain. Factors which could cause actual results to differ from those reflected in forward-looking statements include:

• | continued uncertainty regarding U.S. and global economic outlook that may impact market conditions or prolong weakness in demand for certain banking products and services; |

• | unanticipated developments in pending or prospective loan transactions or greater than expected paydowns or payoffs of existing loans; |

• | unanticipated changes in interest rates; |

• | competitive pressures in the financial services industry that may affect the pricing of the Company’s loan and deposit products as well as its services; |

• | unforeseen credit quality problems or changing economic conditions that could result in charge-offs greater than we have anticipated in our allowance for loan losses or changes in value of our investments; |

• | lack of sufficient or cost-effective sources of liquidity or funding as and when needed; |

• | loss of key personnel or an inability to recruit and retain appropriate talent; |

• | greater than anticipated impact on costs, revenues and offered products and services associated with the implementation of other regulatory changes; or |

• | failures or disruptions to our data processing or other information or operational systems, including the potential impact of disruptions or breaches at our third party service providers. |

These factors should be considered in evaluating forward-looking statements and undue reliance should not be placed on our forward-looking statements. Readers should also consider the risks, assumptions and uncertainties set forth in the "Risk Factors" section of our Annual Report on Form 10-K for the year ended December 31, 2013, and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section of our Quarterly Report on Form 10-Q for the quarter ended March 31, 2014, as well as those set forth in our subsequent periodic and current reports filed with the SEC. Forward-looking statements speak only as of the date they are made and we assume no obligation to update any of these statements in light of new information, future events or otherwise unless required under the federal securities laws.

4

Non-U.S. GAAP Financial Measures

This press release contains both financial measures based on accounting principles generally accepted in the United States (U.S. GAAP) and non-U.S. GAAP based financial measures. We believe that presenting these non-U.S. GAAP financial measures will provide information useful to investors in understanding our underlying operational performance, our business, and performance trends and facilitates comparisons with the performance of others in the banking industry. If non-U.S. GAAP financial measures are used, the comparable U.S. GAAP financial measure, as well as the reconciliation to the comparable U.S. GAAP financial measure, can be found in this press release. These disclosures should not be viewed as a substitute for operating results determined in accordance with U.S. GAAP, nor are they necessarily comparable to non-U.S. GAAP performance measures that may be presented by other companies.

Editor's Note: Financial highlights attached. Full financial supplement available on the Company's website at investor.theprivatebank.com.

5

Consolidated Income Statements | |||||||||||||||

(Amounts in thousands, except per share data) | |||||||||||||||

(Unaudited) | |||||||||||||||

Quarter Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2014 | 2013 | 2014 | 2013 | ||||||||||||

Interest Income | |||||||||||||||

Loans, including fees | $ | 113,696 | $ | 107,407 | $ | 223,895 | $ | 214,194 | |||||||

Federal funds sold and interest-bearing deposits in banks | 139 | 112 | 281 | 320 | |||||||||||

Securities: | |||||||||||||||

Taxable | 13,625 | 12,519 | 26,880 | 25,341 | |||||||||||

Exempt from Federal income taxes | 1,432 | 1,532 | 2,961 | 3,034 | |||||||||||

Other interest income | 59 | 62 | 92 | 152 | |||||||||||

Total interest income | 128,951 | 121,632 | 254,109 | 243,041 | |||||||||||

Interest Expense | |||||||||||||||

Interest-bearing demand deposits | 842 | 1,034 | 1,784 | 2,149 | |||||||||||

Savings deposits and money market accounts | 4,087 | 3,887 | 8,061 | 8,286 | |||||||||||

Time and brokered time deposits | 5,034 | 4,956 | 9,840 | 10,085 | |||||||||||

Short-term and secured borrowings | 141 | 410 | 337 | 528 | |||||||||||

Long-term debt | 6,496 | 7,613 | 12,984 | 15,221 | |||||||||||

Total interest expense | 16,600 | 17,900 | 33,006 | 36,269 | |||||||||||

Net interest income | 112,351 | 103,732 | 221,103 | 206,772 | |||||||||||

Provision for loan and covered loan losses | 327 | 8,843 | 4,034 | 19,200 | |||||||||||

Net interest income after provision for loan and covered loan losses | 112,024 | 94,889 | 217,069 | 187,572 | |||||||||||

Non-interest Income | |||||||||||||||

Asset management | 4,440 | 4,800 | 8,787 | 9,194 | |||||||||||

Mortgage banking | 2,626 | 3,198 | 4,258 | 7,368 | |||||||||||

Capital markets products | 5,006 | 6,048 | 9,089 | 11,087 | |||||||||||

Treasury management | 6,676 | 6,209 | 13,275 | 12,133 | |||||||||||

Loan, letter of credit and commitment fees | 4,806 | 4,282 | 9,440 | 8,359 | |||||||||||

Syndication fees | 5,440 | 3,140 | 8,753 | 6,972 | |||||||||||

Deposit service charges and fees and other income | 1,069 | 1,196 | 2,366 | 3,587 | |||||||||||

Net securities gains | 196 | 136 | 527 | 777 | |||||||||||

Total non-interest income | 30,259 | 29,009 | 56,495 | 59,477 | |||||||||||

Non-interest Expense | |||||||||||||||

Salaries and employee benefits | 44,405 | 39,854 | 89,025 | 82,994 | |||||||||||

Net occupancy expense | 7,728 | 7,387 | 15,504 | 14,921 | |||||||||||

Technology and related costs | 3,205 | 3,476 | 6,488 | 6,940 | |||||||||||

Marketing | 3,589 | 3,695 | 6,002 | 6,012 | |||||||||||

Professional services | 2,905 | 1,782 | 5,664 | 3,681 | |||||||||||

Outsourced servicing costs | 1,850 | 1,964 | 3,314 | 3,598 | |||||||||||

Net foreclosed property expenses | 2,771 | 5,555 | 5,594 | 12,198 | |||||||||||

Postage, telephone, and delivery | 927 | 981 | 1,752 | 1,824 | |||||||||||

Insurance | 3,016 | 2,804 | 5,919 | 5,343 | |||||||||||

Loan and collection expense | 1,573 | 2,280 | 2,629 | 5,057 | |||||||||||

Other expenses | 3,496 | 7,477 | 9,324 | 13,650 | |||||||||||

Total non-interest expense | 75,465 | 77,255 | 151,215 | 156,218 | |||||||||||

Income before income taxes | 66,818 | 46,643 | 122,349 | 90,831 | |||||||||||

Income tax provision | 25,994 | 17,728 | 47,020 | 34,646 | |||||||||||

Net income available to common stockholders | $ | 40,824 | $ | 28,915 | $ | 75,329 | $ | 56,185 | |||||||

Per Common Share Data | |||||||||||||||

Basic earnings per share | $ | 0.52 | $ | 0.37 | $ | 0.97 | $ | 0.72 | |||||||

Diluted earnings per share | $ | 0.52 | $ | 0.37 | $ | 0.96 | $ | 0.72 | |||||||

Cash dividends declared | $ | 0.01 | $ | 0.01 | $ | 0.02 | $ | 0.02 | |||||||

Weighted-average common shares outstanding | 77,062 | 76,415 | 76,869 | 76,280 | |||||||||||

Weighted-average diluted common shares outstanding | 77,806 | 76,581 | 77,612 | 76,393 | |||||||||||

6

Consolidated Income Statements | |||||||||||||||||||

(Amounts in thousands, except per share data) | |||||||||||||||||||

(Unaudited) | |||||||||||||||||||

2Q14 | 1Q14 | 4Q13 | 3Q13 | 2Q13 | |||||||||||||||

Interest Income | |||||||||||||||||||

Loans, including fees | $ | 113,696 | $ | 110,199 | $ | 110,723 | $ | 108,912 | $ | 107,407 | |||||||||

Federal funds sold and interest-bearing deposits in banks | 139 | 142 | 221 | 111 | 112 | ||||||||||||||

Securities: | |||||||||||||||||||

Taxable | 13,625 | 13,255 | 13,038 | 12,931 | 12,519 | ||||||||||||||

Exempt from Federal income taxes | 1,432 | 1,529 | 1,604 | 1,562 | 1,532 | ||||||||||||||

Other interest income | 59 | 33 | 34 | 61 | 62 | ||||||||||||||

Total interest income | 128,951 | 125,158 | 125,620 | 123,577 | 121,632 | ||||||||||||||

Interest Expense | |||||||||||||||||||

Interest-bearing demand deposits | 842 | 942 | 1,021 | 1,032 | 1,034 | ||||||||||||||

Savings deposits and money market accounts | 4,087 | 3,974 | 4,169 | 3,895 | 3,887 | ||||||||||||||

Time and brokered time deposits | 5,034 | 4,806 | 5,062 | 5,014 | 4,956 | ||||||||||||||

Short-term and secured borrowings | 141 | 196 | 161 | 161 | 410 | ||||||||||||||

Long-term debt | 6,496 | 6,488 | 6,751 | 7,640 | 7,613 | ||||||||||||||

Total interest expense | 16,600 | 16,406 | 17,164 | 17,742 | 17,900 | ||||||||||||||

Net interest income | 112,351 | 108,752 | 108,456 | 105,835 | 103,732 | ||||||||||||||

Provision for loan and covered loan losses | 327 | 3,707 | 4,476 | 8,120 | 8,843 | ||||||||||||||

Net interest income after provision for loan and covered loan losses | 112,024 | 105,045 | 103,980 | 97,715 | 94,889 | ||||||||||||||

Non-interest Income | |||||||||||||||||||

Asset management | 4,440 | 4,347 | 4,613 | 4,570 | 4,800 | ||||||||||||||

Mortgage banking | 2,626 | 1,632 | 1,858 | 2,946 | 3,198 | ||||||||||||||

Capital markets products | 5,006 | 4,083 | 5,720 | 3,921 | 6,048 | ||||||||||||||

Treasury management | 6,676 | 6,599 | 6,321 | 6,214 | 6,209 | ||||||||||||||

Loan, letter of credit and commitment fees | 4,806 | 4,634 | 4,474 | 4,384 | 4,282 | ||||||||||||||

Syndication fees | 5,440 | 3,313 | 2,153 | 4,322 | 3,140 | ||||||||||||||

Deposit service charges and fees and other income | 1,069 | 1,297 | 1,322 | 1,298 | 1,196 | ||||||||||||||

Net securities gains | 196 | 331 | 279 | 118 | 136 | ||||||||||||||

Total non-interest income | 30,259 | 26,236 | 26,740 | 27,773 | 29,009 | ||||||||||||||

Non-interest Expense | |||||||||||||||||||

Salaries and employee benefits | 44,405 | 44,620 | 42,575 | 41,360 | 39,854 | ||||||||||||||

Net occupancy expense | 7,728 | 7,776 | 7,548 | 7,558 | 7,387 | ||||||||||||||

Technology and related costs | 3,205 | 3,283 | 3,443 | 3,343 | 3,476 | ||||||||||||||

Marketing | 3,589 | 2,413 | 3,592 | 2,986 | 3,695 | ||||||||||||||

Professional services | 2,905 | 2,759 | 2,393 | 2,465 | 1,782 | ||||||||||||||

Outsourced servicing costs | 1,850 | 1,464 | 1,612 | 1,607 | 1,964 | ||||||||||||||

Net foreclosed property expenses | 2,771 | 2,823 | 3,600 | 4,396 | 5,555 | ||||||||||||||

Postage, telephone, and delivery | 927 | 825 | 845 | 852 | 981 | ||||||||||||||

Insurance | 3,016 | 2,903 | 2,934 | 2,590 | 2,804 | ||||||||||||||

Loan and collection expense | 1,573 | 1,056 | 2,351 | 1,345 | 2,280 | ||||||||||||||

Other expenses | 3,496 | 5,828 | 4,934 | 2,767 | 7,477 | ||||||||||||||

Total non-interest expense | 75,465 | 75,750 | 75,827 | 71,269 | 77,255 | ||||||||||||||

Income before income taxes | 66,818 | 55,531 | 54,893 | 54,219 | 46,643 | ||||||||||||||

Income tax provision | 25,994 | 21,026 | 21,187 | 21,161 | 17,728 | ||||||||||||||

Net income available to common stockholders | $ | 40,824 | $ | 34,505 | $ | 33,706 | $ | 33,058 | $ | 28,915 | |||||||||

Per Common Share Data | |||||||||||||||||||

Basic earnings per share | $ | 0.52 | $ | 0.44 | $ | 0.43 | $ | 0.42 | $ | 0.37 | |||||||||

Diluted earnings per share | $ | 0.52 | $ | 0.44 | $ | 0.43 | $ | 0.42 | $ | 0.37 | |||||||||

Cash dividends declared | $ | 0.01 | $ | 0.01 | $ | 0.01 | $ | 0.01 | $ | 0.01 | |||||||||

Weighted-average common shares outstanding | 77,062 | 76,675 | 76,533 | 76,494 | 76,415 | ||||||||||||||

Weighted-average diluted common shares outstanding | 77,806 | 77,417 | 76,967 | 76,819 | 76,581 | ||||||||||||||

7

Consolidated Balance Sheets | |||||||||||||||||||

(Dollars in thousands) | |||||||||||||||||||

6/30/14 | 3/31/14 | 12/31/13 | 9/30/13 | 6/30/13 | |||||||||||||||

(Unaudited) | (Unaudited) | (Audited) | (Unaudited) | (Unaudited) | |||||||||||||||

Assets | |||||||||||||||||||

Cash and due from banks | $ | 247,048 | $ | 233,685 | $ | 133,518 | $ | 247,460 | $ | 150,683 | |||||||||

Federal funds sold and interest-bearing deposits in banks | 160,349 | 117,446 | 306,544 | 180,608 | 147,699 | ||||||||||||||

Loans held-for-sale | 80,724 | 26,262 | 26,816 | 27,644 | 34,803 | ||||||||||||||

Securities available-for-sale, at fair value | 1,527,747 | 1,577,406 | 1,602,476 | 1,611,022 | 1,580,179 | ||||||||||||||

Securities held-to-maturity, at amortized cost | 1,066,216 | 1,023,214 | 921,436 | 931,342 | 955,688 | ||||||||||||||

Federal Home Loan Bank ("FHLB") stock | 28,666 | 30,005 | 30,005 | 34,063 | 34,063 | ||||||||||||||

Loans – excluding covered assets, net of unearned fees | 11,136,942 | 10,924,985 | 10,644,021 | 10,409,443 | 10,094,636 | ||||||||||||||

Allowance for loan losses | (146,491 | ) | (146,768 | ) | (143,109 | ) | (145,513 | ) | (148,183 | ) | |||||||||

Loans, net of allowance for loan losses and unearned fees | 10,990,451 | 10,778,217 | 10,500,912 | 10,263,930 | 9,946,453 | ||||||||||||||

Covered assets | 81,047 | 94,349 | 112,746 | 140,083 | 158,326 | ||||||||||||||

Allowance for covered loan losses | (14,375 | ) | (16,571 | ) | (16,511 | ) | (21,653 | ) | (24,995 | ) | |||||||||

Covered assets, net of allowance for covered loan losses | 66,672 | 77,778 | 96,235 | 118,430 | 133,331 | ||||||||||||||

Other real estate owned, excluding covered assets | 19,823 | 23,565 | 28,548 | 35,310 | 57,134 | ||||||||||||||

Premises, furniture, and equipment, net | 40,088 | 39,556 | 39,704 | 36,445 | 37,025 | ||||||||||||||

Accrued interest receivable | 36,568 | 39,273 | 37,004 | 35,758 | 38,325 | ||||||||||||||

Investment in bank owned life insurance | 54,500 | 54,184 | 53,865 | 53,539 | 53,216 | ||||||||||||||

Goodwill | 94,041 | 94,041 | 94,041 | 94,484 | 94,496 | ||||||||||||||

Other intangible assets | 7,381 | 8,136 | 8,892 | 10,486 | 11,266 | ||||||||||||||

Derivative assets | 47,012 | 44,528 | 48,422 | 57,771 | 57,361 | ||||||||||||||

Other assets | 135,118 | 137,486 | 157,328 | 130,848 | 144,771 | ||||||||||||||

Total assets | $ | 14,602,404 | $ | 14,304,782 | $ | 14,085,746 | $ | 13,869,140 | $ | 13,476,493 | |||||||||

Liabilities | |||||||||||||||||||

Demand deposits: | |||||||||||||||||||

Noninterest-bearing | $ | 3,387,424 | $ | 3,103,736 | $ | 3,172,676 | $ | 3,106,986 | $ | 2,736,868 | |||||||||

Interest-bearing | 1,230,681 | 1,466,095 | 1,470,856 | 1,183,471 | 1,234,134 | ||||||||||||||

Savings deposits and money market accounts | 5,033,247 | 4,786,398 | 4,799,561 | 4,778,057 | 4,654,930 | ||||||||||||||

Time deposits | 1,299,616 | 1,320,466 | 1,336,522 | 1,333,232 | 1,355,522 | ||||||||||||||

Brokered time deposits | 1,285,233 | 1,209,466 | 1,234,026 | 1,430,810 | 1,326,878 | ||||||||||||||

Total deposits | 12,236,201 | 11,886,161 | 12,013,641 | 11,832,556 | 11,308,332 | ||||||||||||||

Short-term and secured borrowings | 235,319 | 333,400 | 8,400 | 131,400 | 308,700 | ||||||||||||||

Long-term debt | 626,793 | 627,793 | 627,793 | 499,793 | 499,793 | ||||||||||||||

Accrued interest payable | 6,282 | 6,251 | 6,326 | 6,042 | 5,963 | ||||||||||||||

Derivative liabilities | 35,402 | 40,522 | 48,890 | 55,933 | 62,014 | ||||||||||||||

Other liabilities | 64,586 | 67,409 | 78,792 | 69,728 | 58,651 | ||||||||||||||

Total liabilities | 13,204,583 | 12,961,536 | 12,783,842 | 12,595,452 | 12,243,453 | ||||||||||||||

Equity | |||||||||||||||||||

Common stock: | |||||||||||||||||||

Voting | 75,526 | 75,428 | 75,240 | 75,240 | 75,238 | ||||||||||||||

Nonvoting | 1,585 | 1,585 | 1,585 | 1,585 | 1,585 | ||||||||||||||

Treasury stock | (945 | ) | (1,697 | ) | (6,415 | ) | (7,303 | ) | (9,001 | ) | |||||||||

Additional paid-in capital | 1,024,869 | 1,021,436 | 1,022,023 | 1,019,143 | 1,016,615 | ||||||||||||||

Retained earnings | 273,380 | 233,347 | 199,627 | 166,700 | 134,423 | ||||||||||||||

Accumulated other comprehensive income, net of tax | 23,406 | 13,147 | 9,844 | 18,323 | 14,180 | ||||||||||||||

Total equity | 1,397,821 | 1,343,246 | 1,301,904 | 1,273,688 | 1,233,040 | ||||||||||||||

Total liabilities and equity | $ | 14,602,404 | $ | 14,304,782 | $ | 14,085,746 | $ | 13,869,140 | $ | 13,476,493 | |||||||||

Note: Certain reclassifications have been made to prior period amounts to conform to the current period presentation.

8

Selected Financial Data | ||||||||||||||||||||

(Amounts in thousands, except per share data) | ||||||||||||||||||||

(Unaudited) | ||||||||||||||||||||

2Q14 | 1Q14 | 4Q13 | 3Q13 | 2Q13 | ||||||||||||||||

Selected Statement of Income Data: | ||||||||||||||||||||

Net interest income | $ | 112,351 | $ | 108,752 | $ | 108,456 | $ | 105,835 | $ | 103,732 | ||||||||||

Net revenue (1)(2) | $ | 143,354 | $ | 135,788 | $ | 136,036 | $ | 134,426 | $ | 133,546 | ||||||||||

Operating profit (1)(2) | $ | 67,889 | $ | 60,038 | $ | 60,209 | $ | 63,157 | $ | 56,291 | ||||||||||

Provision for loan and covered loan losses | $ | 327 | $ | 3,707 | $ | 4,476 | $ | 8,120 | $ | 8,843 | ||||||||||

Income before income taxes | $ | 66,818 | $ | 55,531 | $ | 54,893 | $ | 54,219 | $ | 46,643 | ||||||||||

Net income available to common stockholders | $ | 40,824 | $ | 34,505 | $ | 33,706 | $ | 33,058 | $ | 28,915 | ||||||||||

Per Common Share Data: | ||||||||||||||||||||

Basic earnings per share | $ | 0.52 | $ | 0.44 | $ | 0.43 | $ | 0.42 | $ | 0.37 | ||||||||||

Diluted earnings per share | $ | 0.52 | $ | 0.44 | $ | 0.43 | $ | 0.42 | $ | 0.37 | ||||||||||

Dividends declared | $ | 0.01 | $ | 0.01 | $ | 0.01 | $ | 0.01 | $ | 0.01 | ||||||||||

Book value (period end) (1) | $ | 17.90 | $ | 17.21 | $ | 16.75 | $ | 16.40 | $ | 15.88 | ||||||||||

Tangible book value (period end) (1)(2) | $ | 16.61 | $ | 15.90 | $ | 15.43 | $ | 15.05 | $ | 14.52 | ||||||||||

Market value (period end) | $ | 29.06 | $ | 30.51 | $ | 28.93 | $ | 21.40 | $ | 21.22 | ||||||||||

Book value multiple (period end) | 1.62 | x | 1.77 | x | 1.73 | x | 1.31 | x | 1.34 | x | ||||||||||

Share Data: | ||||||||||||||||||||

Weighted-average common shares outstanding | 77,062 | 76,675 | 76,533 | 76,494 | 76,415 | |||||||||||||||

Weighted-average diluted common shares outstanding | 77,806 | 77,417 | 76,967 | 76,819 | 76,581 | |||||||||||||||

Common shares issued (period end) | 78,101 | 78,108 | 77,982 | 77,993 | 78,015 | |||||||||||||||

Common shares outstanding (period end) | 78,069 | 78,049 | 77,708 | 77,680 | 77,630 | |||||||||||||||

Performance Ratio: | ||||||||||||||||||||

Return on average common equity | 11.88 | % | 10.48 | % | 10.28 | % | 10.43 | % | 9.28 | % | ||||||||||

Return on average assets | 1.14 | % | 1.00 | % | 0.96 | % | 0.96 | % | 0.86 | % | ||||||||||

Return on average tangible common equity (1)(2) | 12.97 | % | 11.50 | % | 11.33 | % | 11.55 | % | 10.30 | % | ||||||||||

Net interest margin (1)(2) | 3.21 | % | 3.23 | % | 3.18 | % | 3.18 | % | 3.22 | % | ||||||||||

Fee revenue as a percent of total revenue (1) | 21.11 | % | 19.24 | % | 19.61 | % | 20.72 | % | 21.77 | % | ||||||||||

Non-interest income to average assets | 0.84 | % | 0.76 | % | 0.76 | % | 0.81 | % | 0.87 | % | ||||||||||

Non-interest expense to average assets | 2.10 | % | 2.19 | % | 2.16 | % | 2.07 | % | 2.31 | % | ||||||||||

Net overhead ratio (1) | 1.26 | % | 1.43 | % | 1.40 | % | 1.26 | % | 1.44 | % | ||||||||||

Efficiency ratio (1)(2) | 52.64 | % | 55.79 | % | 55.74 | % | 53.02 | % | 57.85 | % | ||||||||||

Balance Sheet Ratios: | ||||||||||||||||||||

Loans to deposits (period end) (3) | 91.02 | % | 91.91 | % | 88.60 | % | 87.97 | % | 89.27 | % | ||||||||||

Average interest-earning assets to average interest-bearing liabilities | 143.72 | % | 143.43 | % | 144.87 | % | 140.72 | % | 139.76 | % | ||||||||||

Capital Ratios (period end): | ||||||||||||||||||||

Total risk-based capital (1) | 13.41 | % | 13.39 | % | 13.30 | % | 13.48 | % | 13.70 | % | ||||||||||

Tier 1 risk-based capital (1) | 11.24 | % | 11.19 | % | 11.08 | % | 11.05 | % | 11.04 | % | ||||||||||

Tier 1 leverage ratio (1) | 10.63 | % | 10.60 | % | 10.37 | % | 10.32 | % | 10.25 | % | ||||||||||

Tier 1 common equity to risk-weighted assets (1)(2)(4) | 9.42 | % | 9.33 | % | 9.19 | % | 9.11 | % | 9.05 | % | ||||||||||

Tangible common equity to tangible assets (1)(2) | 8.94 | % | 8.74 | % | 8.57 | % | 8.49 | % | 8.43 | % | ||||||||||

Total equity to total assets | 9.57 | % | 9.39 | % | 9.24 | % | 9.18 | % | 9.15 | % | ||||||||||

(1) | Refer to Glossary of Terms for definition. |

(2) | This is a non-U.S. GAAP financial measure. Refer to "Non-U.S. GAAP Financial Measures" for a reconciliation from non-U.S. GAAP to U.S. GAAP. |

(3) | Excludes covered assets. Refer to Glossary of Terms for definition. |

(4) | For purposes of our presentation, we calculate this ratio under currently effective requirements and without giving effect to the final Basel III capital rules adopted and issued by the Federal Reserve Board in July 2013, which are effective January 1, 2014 with compliance required January 1, 2015. |

9

Selected Financial Data (continued) | |||||||||||||||||||

(Dollars in thousands) | |||||||||||||||||||

(Unaudited) | |||||||||||||||||||

2Q14 | 1Q14 | 4Q13 | 3Q13 | 2Q13 | |||||||||||||||

Additional Selected Information: | |||||||||||||||||||

(Increase) decrease credit valuation adjustment on capital markets derivatives (1) | $ | (250 | ) | $ | (66 | ) | $ | 619 | $ | (521 | ) | $ | 1,882 | ||||||

Salaries and employee benefits: | |||||||||||||||||||

Salaries and wages | $ | 25,671 | $ | 24,973 | $ | 23,971 | $ | 23,639 | $ | 23,397 | |||||||||

Share-based costs | 3,892 | 3,685 | 3,316 | 3,261 | 3,236 | ||||||||||||||

Incentive compensation and commissions | 10,493 | 8,244 | 11,711 | 10,753 | 9,240 | ||||||||||||||

Payroll taxes, insurance and retirement costs | 4,349 | 7,718 | 3,577 | 3,707 | 3,981 | ||||||||||||||

Total salaries and employee benefits | $ | 44,405 | $ | 44,620 | $ | 42,575 | $ | 41,360 | $ | 39,854 | |||||||||

(Release) provision for unfunded commitments | $ | (339 | ) | $ | 496 | $ | 1,019 | $ | (1,346 | ) | $ | 467 | |||||||

Assets under management and administration (AUMA) (1) | $ | 6,361,560 | $ | 6,036,381 | $ | 5,731,980 | $ | 5,570,614 | $ | 5,427,498 | |||||||||

Custody assets included in AUMA | $ | 2,928,116 | $ | 2,663,502 | $ | 2,506,291 | $ | 2,427,093 | $ | 2,351,163 | |||||||||

Basic and Diluted Earnings per Common Share | |||||||||||||||||||

(Amounts in thousands, except per share data) | |||||||||||||||||||

2Q14 | 1Q14 | 4Q13 | 3Q13 | 2Q13 | |||||||||||||||

Basic earnings per common share | |||||||||||||||||||

Net income | $ | 40,824 | $ | 34,505 | $ | 33,706 | $ | 33,058 | $ | 28,915 | |||||||||

Net income allocated to participating stockholders (2) | (519 | ) | (613 | ) | (664 | ) | (655 | ) | (576 | ) | |||||||||

Net income allocated to common stockholders | $ | 40,305 | $ | 33,892 | $ | 33,042 | $ | 32,403 | $ | 28,339 | |||||||||

Weighted-average common shares outstanding | 77,062 | 76,675 | 76,533 | 76,494 | 76,415 | ||||||||||||||

Basic earnings per common share | $ | 0.52 | $ | 0.44 | $ | 0.43 | $ | 0.42 | $ | 0.37 | |||||||||

Diluted earnings per common share | |||||||||||||||||||

Diluted earnings applicable to common stockholders (3) | $ | 40,308 | $ | 33,897 | $ | 33,046 | $ | 32,406 | $ | 28,340 | |||||||||

Weighted-average diluted common shares outstanding: | |||||||||||||||||||

Weighted-average common shares outstanding | 77,062 | 76,675 | 76,533 | 76,494 | 76,415 | ||||||||||||||

Dilutive effect of stock awards | 744 | 742 | 434 | 325 | 166 | ||||||||||||||

Weighted-average diluted common shares outstanding | $ | 77,806 | $ | 77,417 | $ | 76,967 | $ | 76,819 | $ | 76,581 | |||||||||

Diluted earnings per common share | $ | 0.52 | $ | 0.44 | $ | 0.43 | $ | 0.42 | $ | 0.37 | |||||||||

(1) | Refer to Glossary of Terms for definition. |

(2) | Participating stockholders are those that hold certain share-based payment awards that contain nonforfeitable rights to dividends or dividend equivalents. Such shares or units are considered participating securities (i.e., the Company’s deferred stock units and certain restricted stock units and nonvested restricted stock awards). |

(3) | Earnings allocated to common stockholders for basic and diluted earnings per share may differ under the two-class method as a result of adding common stock equivalents for options to dilutive shares outstanding, which alters the ratio used to allocate earnings to common stockholders and participating securities for the purposes of calculating diluted earnings per share. |

10

Loan Composition (excluding covered assets (1)) | ||||||||||||||||||||||||||||||||||

(Dollars in thousands) | ||||||||||||||||||||||||||||||||||

6/30/14 | % of Total | 3/31/14 | % of Total | 12/31/13 | % of Total | 9/30/13 | % of Total | 6/30/13 | % of Total | |||||||||||||||||||||||||

(Unaudited) | (Unaudited) | (Audited) | (Unaudited) | (Unaudited) | ||||||||||||||||||||||||||||||

Commercial and industrial | $ | 5,871,425 | 53 | % | $ | 5,652,008 | 52 | % | $ | 5,457,574 | 51 | % | $ | 5,384,222 | 52 | % | $ | 5,019,494 | 50 | % | ||||||||||||||

Commercial - owner-occupied CRE | 1,699,861 | 15 | % | 1,744,940 | 16 | % | 1,674,260 | 16 | % | 1,604,470 | 15 | % | 1,641,973 | 16 | % | |||||||||||||||||||

Total commercial | 7,571,286 | 68 | % | 7,396,948 | 68 | % | 7,131,834 | 67 | % | 6,988,692 | 67 | % | 6,661,467 | 66 | % | |||||||||||||||||||

Commercial real estate | 1,985,273 | 18 | % | 1,974,534 | 18 | % | 1,987,307 | 19 | % | 1,914,725 | 18 | % | 1,981,541 | 20 | % | |||||||||||||||||||

Commercial real estate - multi-family | 533,854 | 5 | % | 524,872 | 5 | % | 513,194 | 5 | % | 573,371 | 6 | % | 520,160 | 5 | % | |||||||||||||||||||

Total commercial real estate | 2,519,127 | 23 | % | 2,499,406 | 23 | % | 2,500,501 | 24 | % | 2,488,096 | 24 | % | 2,501,701 | 25 | % | |||||||||||||||||||

Construction | 360,313 | 3 | % | 335,476 | 3 | % | 293,387 | 3 | % | 237,440 | 3 | % | 211,976 | 2 | % | |||||||||||||||||||

Residential real estate | 337,329 | 3 | % | 337,832 | 3 | % | 341,868 | 3 | % | 346,619 | 3 | % | 347,629 | 3 | % | |||||||||||||||||||

Home equity | 144,081 | 1 | % | 147,574 | 1 | % | 149,732 | 1 | % | 148,058 | 1 | % | 159,958 | 2 | % | |||||||||||||||||||

Personal | 204,806 | 2 | % | 207,749 | 2 | % | 226,699 | 2 | % | 200,538 | 2 | % | 211,905 | 2 | % | |||||||||||||||||||

Total loans | $ | 11,136,942 | 100 | % | $ | 10,924,985 | 100 | % | $ | 10,644,021 | 100 | % | $ | 10,409,443 | 100 | % | $ | 10,094,636 | 100 | % | ||||||||||||||

(1) | Refer to Glossary of Terms for definition. |

11

Commercial Loans Composition by Industry Segment (excluding covered assets (1)) | ||||||||||||||||||||

(Dollars in thousands) | ||||||||||||||||||||

(Unaudited) | ||||||||||||||||||||

(Classified pursuant to the North American Industrial Classification System standard industry descriptions and represents our client's primary business activity) | ||||||||||||||||||||

June 30, 2014 | March 31, 2014 | December 31, 2013 | ||||||||||||||||||

Amount | % of Total | Amount | % of Total | Amount | % of Total | |||||||||||||||

Manufacturing | $ | 1,712,112 | 23 | % | $ | 1,693,837 | 23 | % | $ | 1,583,679 | 22 | % | ||||||||

Healthcare | 1,740,045 | 23 | % | 1,733,221 | 23 | % | 1,653,596 | 23 | % | |||||||||||

Wholesale trade | 702,216 | 9 | % | 680,930 | 9 | % | 695,049 | 10 | % | |||||||||||

Finance and insurance | 690,722 | 9 | % | 619,757 | 8 | % | 643,119 | 9 | % | |||||||||||

Real estate, rental and leasing | 491,788 | 6 | % | 461,619 | 6 | % | 444,210 | 6 | % | |||||||||||

Professional, scientific and technical services | 492,476 | 7 | % | 462,657 | 7 | % | 454,373 | 7 | % | |||||||||||

Administrative, support, waste management and remediation services | 465,097 | 6 | % | 433,379 | 6 | % | 449,777 | 6 | % | |||||||||||

Architecture, engineering and construction | 271,055 | 4 | % | 258,868 | 3 | % | 249,444 | 4 | % | |||||||||||

Retail | 240,950 | 3 | % | 263,924 | 4 | % | 223,541 | 3 | % | |||||||||||

All other (2) | 764,825 | 10 | % | 788,756 | 11 | % | 735,046 | 10 | % | |||||||||||

Total commercial (3) | $ | 7,571,286 | 100 | % | $ | 7,396,948 | 100 | % | $ | 7,131,834 | 100 | % | ||||||||

Commercial Real Estate and Construction Loan Portfolio by Collateral Type | ||||||||||||||||||||

(Unaudited) | ||||||||||||||||||||

June 30, 2014 | March 31, 2014 | December 31, 2013 | ||||||||||||||||||

Amount | % of Total | Amount | % of Total | Amount | % of Total | |||||||||||||||

Commercial Real Estate Portfolio | ||||||||||||||||||||

Land | $ | 171,588 | 7 | % | $ | 205,705 | 8 | % | $ | 216,176 | 9 | % | ||||||||

Residential 1-4 family | 90,634 | 4 | % | 99,917 | 4 | % | 103,568 | 4 | % | |||||||||||

Multi-family | 533,854 | 21 | % | 524,872 | 21 | % | 513,194 | 20 | % | |||||||||||

Industrial/warehouse | 278,681 | 11 | % | 275,065 | 11 | % | 271,230 | 11 | % | |||||||||||

Office | 476,380 | 19 | % | 461,379 | 18 | % | 470,790 | 19 | % | |||||||||||

Retail | 539,602 | 21 | % | 494,728 | 20 | % | 490,955 | 19 | % | |||||||||||

Healthcare | 143,466 | 6 | % | 150,528 | 6 | % | 167,226 | 7 | % | |||||||||||

Mixed use/other | 284,922 | 11 | % | 287,212 | 12 | % | 267,362 | 11 | % | |||||||||||

Total commercial real estate | $ | 2,519,127 | 100 | % | $ | 2,499,406 | 100 | % | $ | 2,500,501 | 100 | % | ||||||||

Construction Portfolio | ||||||||||||||||||||

Residential 1-4 family | $ | 24,541 | 7 | % | $ | 22,880 | 7 | % | $ | 20,960 | 7 | % | ||||||||

Multi-family | 83,797 | 23 | % | 88,075 | 26 | % | 58,131 | 20 | % | |||||||||||

Industrial/warehouse | 26,210 | 7 | % | 20,054 | 6 | % | 29,343 | 10 | % | |||||||||||

Office | 14,531 | 4 | % | 23,375 | 7 | % | 20,596 | 7 | % | |||||||||||

Retail | 88,376 | 25 | % | 89,397 | 27 | % | 83,640 | 28 | % | |||||||||||

Healthcare | 78,226 | 22 | % | 60,234 | 18 | % | 43,506 | 15 | % | |||||||||||

Mixed use/other | 44,632 | 12 | % | 31,461 | 9 | % | 37,211 | 13 | % | |||||||||||

Total construction | $ | 360,313 | 100 | % | $ | 335,476 | 100 | % | $ | 293,387 | 100 | % | ||||||||

(1) | Refer to Glossary of Terms for definition. |

(2) | All other consists of numerous smaller balances across a variety of industries with no category greater than 3%. |

(3) | Includes owner-occupied commercial real estate of $1.7 billion at June 30, 2014, March 31, 2014 and December 31, 2013, respectively. |

12

Asset Quality (excluding covered assets (1)) | |||||||||||||||||||

(Dollars in thousands) | |||||||||||||||||||

(Unaudited) | |||||||||||||||||||

2Q14 | 1Q14 | 4Q13 | 3Q13 | 2Q13 | |||||||||||||||

Credit Quality Key Ratios | |||||||||||||||||||

Net charge-offs (recoveries) (annualized) to average loans | 0.08 | % | -0.01 | % | 0.28 | % | 0.40 | % | 0.56 | % | |||||||||

Nonperforming loans to total loans | 0.69 | % | 0.86 | % | 0.89 | % | 1.09 | % | 1.20 | % | |||||||||

Nonperforming loans to total assets | 0.52 | % | 0.66 | % | 0.67 | % | 0.82 | % | 0.90 | % | |||||||||

Nonperforming assets to total assets | 0.66 | % | 0.82 | % | 0.87 | % | 1.07 | % | 1.33 | % | |||||||||

Allowance for loan losses to: | |||||||||||||||||||

Total loans | 1.32 | % | 1.34 | % | 1.34 | % | 1.40 | % | 1.47 | % | |||||||||

Nonperforming loans | 191 | % | 156 | % | 152 | % | 128 | % | 122 | % | |||||||||

Nonperforming assets | |||||||||||||||||||

Loans past due 90 days and accruing | $ | — | $ | — | $ | — | $ | — | $ | — | |||||||||

Nonaccrual loans | 76,589 | 93,827 | 94,238 | 113,286 | 121,759 | ||||||||||||||

OREO | 19,823 | 23,565 | 28,548 | 35,310 | 57,134 | ||||||||||||||

Total nonperforming assets | $ | 96,412 | $ | 117,392 | $ | 122,786 | $ | 148,596 | $ | 178,893 | |||||||||

Restructured loans accruing interest | $ | 32,982 | $ | 26,462 | $ | 20,176 | $ | 32,343 | $ | 48,281 | |||||||||

Loans past due and still accruing | |||||||||||||||||||

30-59 days | $ | 3,566 | $ | 4,296 | $ | 7,854 | $ | 3,602 | $ | 7,750 | |||||||||

60-89 days | $ | 117 | $ | 8,792 | $ | 1,016 | $ | 3,000 | $ | 3,016 | |||||||||

Total loans past due and still accruing | $ | 3,683 | $ | 13,088 | $ | 8,870 | $ | 6,602 | $ | 10,766 | |||||||||

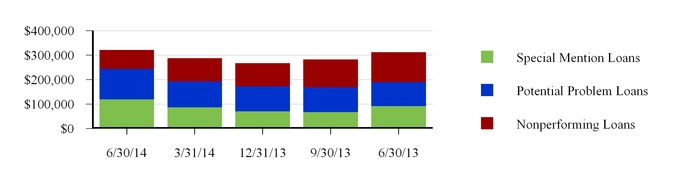

Special mention loans | $ | 119,878 | $ | 87,329 | $ | 71,257 | $ | 67,518 | $ | 92,880 | |||||||||

Potential problem loans | $ | 125,033 | $ | 106,474 | $ | 101,772 | $ | 101,324 | $ | 97,196 | |||||||||

Nonperforming Loans Rollforward | |||||||||||||||||||

Beginning balance | $ | 93,827 | $ | 94,238 | $ | 113,286 | $ | 121,759 | $ | 128,657 | |||||||||

Additions: | |||||||||||||||||||

New nonaccrual loans | 16,327 | 14,882 | 20,082 | 25,642 | 26,190 | ||||||||||||||

Reductions: | |||||||||||||||||||

Return to performing status | — | (119 | ) | (370 | ) | — | (2,288 | ) | |||||||||||

Paydowns and payoffs, net of advances | (19,936 | ) | (3,326 | ) | (16,464 | ) | (12,205 | ) | (246 | ) | |||||||||

Net sales | (7,875 | ) | (6,327 | ) | (4,438 | ) | (1,119 | ) | (12,601 | ) | |||||||||

Transfer to OREO | (1,111 | ) | (689 | ) | (6,642 | ) | (1,036 | ) | (3,366 | ) | |||||||||

Transfer to loans held for sale | — | — | — | (7,359 | ) | — | |||||||||||||

Charge-offs | (4,643 | ) | (4,832 | ) | (11,216 | ) | (12,396 | ) | (14,587 | ) | |||||||||

Total reductions | (33,565 | ) | (15,293 | ) | (39,130 | ) | (34,115 | ) | (33,088 | ) | |||||||||

Balance at end of period | $ | 76,589 | $ | 93,827 | $ | 94,238 | $ | 113,286 | $ | 121,759 | |||||||||

OREO Rollforward | |||||||||||||||||||

Beginning balance | $ | 23,565 | $ | 28,548 | $ | 35,310 | $ | 57,134 | $ | 73,857 | |||||||||

New foreclosed properties | 1,111 | 689 | 6,642 | 1,036 | 3,366 | ||||||||||||||

Valuation adjustments | (2,252 | ) | (1,463 | ) | (3,138 | ) | (5,734 | ) | (6,128 | ) | |||||||||

Disposals: | |||||||||||||||||||

Sales proceeds | (2,539 | ) | (3,892 | ) | (10,273 | ) | (18,902 | ) | (14,677 | ) | |||||||||

Net (loss) gains on sale | (62 | ) | (317 | ) | 7 | 1,776 | 716 | ||||||||||||

Balance at end of period | $ | 19,823 | $ | 23,565 | $ | 28,548 | $ | 35,310 | $ | 57,134 | |||||||||

(1) | Refer to Glossary of Terms for definition. |

13

Asset Quality (excluding covered assets (1)) | |||||||||||||||||||||||||||

(Dollars in thousands) | |||||||||||||||||||||||||||

(Unaudited) | |||||||||||||||||||||||||||

Credit Quality Indicators | |||||||||||||||||||||||||||

Special Mention Loans | % of Portfolio Loan Type | Potential Problem Loans | % of Portfolio Loan Type | Non-Performing Loans | % of Portfolio Loan Type | Total Loans | |||||||||||||||||||||

June 30, 2014 | |||||||||||||||||||||||||||

Commercial | $ | 114,165 | 1.5 | % | $ | 114,443 | 1.5 | % | $ | 34,522 | 0.5 | % | $ | 7,571,286 | |||||||||||||

Commercial real estate | 773 | * | 1,924 | 0.1 | % | 21,953 | 0.9 | % | 2,519,127 | ||||||||||||||||||

Construction | — | — | % | — | — | % | — | — | % | 360,313 | |||||||||||||||||

Residential real estate | 2,778 | 0.8 | % | 6,661 | 2.0 | % | 9,337 | 2.8 | % | 337,329 | |||||||||||||||||

Home equity | 1,939 | 1.3 | % | 1,990 | 1.4 | % | 10,197 | 7.1 | % | 144,081 | |||||||||||||||||

Personal | 223 | 0.1 | % | 15 | * | 580 | 0.3 | % | 204,806 | ||||||||||||||||||

Total | $ | 119,878 | 1.1 | % | $ | 125,033 | 1.1 | % | $ | 76,589 | 0.7 | % | $ | 11,136,942 | |||||||||||||

March 31, 2014 | |||||||||||||||||||||||||||

Commercial | $ | 79,362 | 1.1 | % | $ | 92,962 | 1.3 | % | $ | 31,074 | 0.4 | % | $ | 7,396,948 | |||||||||||||

Commercial real estate | 1,004 | * | 4,677 | 0.2 | % | 40,928 | 1.6 | % | 2,499,406 | ||||||||||||||||||

Construction | — | — | % | — | — | % | — | — | % | 335,476 | |||||||||||||||||

Residential real estate | 4,000 | 1.2 | % | 6,613 | 2.0 | % | 9,354 | 2.8 | % | 337,832 | |||||||||||||||||

Home equity | 2,774 | 1.9 | % | 2,171 | 1.5 | % | 11,846 | 8.0 | % | 147,574 | |||||||||||||||||

Personal | 189 | 0.1 | % | 51 | * | 625 | 0.3 | % | 207,749 | ||||||||||||||||||

Total | $ | 87,329 | 0.8 | % | $ | 106,474 | 1.0 | % | $ | 93,827 | 0.9 | % | $ | 10,924,985 | |||||||||||||

* | Less than 0.1%. |

Nonaccrual loans | |||||||||||||||||||

2Q14 | 1Q14 | 4Q13 | 3Q13 | 2Q13 | |||||||||||||||

Nonaccrual loans | |||||||||||||||||||

Commercial | $ | 34,522 | $ | 31,074 | $ | 24,779 | $ | 26,881 | $ | 47,782 | |||||||||

Commercial real estate | 21,953 | 40,928 | 46,953 | 62,954 | 45,759 | ||||||||||||||

Residential real estate | 9,337 | 9,354 | 9,976 | 11,237 | 12,812 | ||||||||||||||

Personal and home equity | 10,777 | 12,471 | 12,530 | 12,214 | 15,406 | ||||||||||||||

Total | $ | 76,589 | $ | 93,827 | $ | 94,238 | $ | 113,286 | $ | 121,759 | |||||||||

Nonaccrual loans as a percent of total loan type: | |||||||||||||||||||

Commercial | 0.5 | % | 0.4 | % | 0.4 | % | 0.4 | % | 0.7 | % | |||||||||

Commercial real estate | 0.9 | % | 1.6 | % | 1.9 | % | 2.5 | % | 1.8 | % | |||||||||

Residential real estate | 2.8 | % | 2.8 | % | 2.9 | % | 3.2 | % | 3.7 | % | |||||||||

Personal and home equity | 3.1 | % | 3.5 | % | 3.3 | % | 3.5 | % | 4.1 | % | |||||||||

Total | 0.7 | % | 0.9 | % | 0.9 | % | 1.1 | % | 1.2 | % | |||||||||

(1) | Refer to Glossary of Terms for definition. |

14

Nonaccrual Loan Stratification (excluding covered assets (1)) | |||||||||||||||||||||||

(Dollars in thousands) | |||||||||||||||||||||||

(Unaudited) | |||||||||||||||||||||||

$10.0 Million or More | $5.0 to $9.9 Million | $3.0 to $4.9 Million | $1.5 to $2.9 Million | Under $1.5 Million | Total | ||||||||||||||||||

June 30, 2014 | |||||||||||||||||||||||

Amount: | |||||||||||||||||||||||

Commercial | $ | 12,113 | $ | 8,004 | $ | 3,059 | $ | 4,023 | $ | 7,323 | $ | 34,522 | |||||||||||

Commercial real estate | — | 5,562 | — | 4,564 | 11,827 | 21,953 | |||||||||||||||||

Residential real estate | — | — | 4,438 | — | 4,899 | 9,337 | |||||||||||||||||

Personal and home equity | — | — | — | — | 10,777 | 10,777 | |||||||||||||||||

Total | $ | 12,113 | $ | 13,566 | $ | 7,497 | $ | 8,587 | $ | 34,826 | $ | 76,589 | |||||||||||

Number of borrowers: | |||||||||||||||||||||||

Commercial | 1 | 1 | 1 | 2 | 22 | 27 | |||||||||||||||||

Commercial real estate | — | 1 | — | 2 | 24 | 27 | |||||||||||||||||

Residential real estate | — | — | 1 | — | 28 | 29 | |||||||||||||||||

Personal and home equity | — | — | — | — | 51 | 51 | |||||||||||||||||

Total | 1 | 2 | 2 | 4 | 125 | 134 | |||||||||||||||||

March 31, 2014 | |||||||||||||||||||||||

Amount: | |||||||||||||||||||||||

Commercial | $ | — | $ | 16,289 | $ | — | $ | 6,585 | $ | 8,200 | $ | 31,074 | |||||||||||

Commercial real estate | — | 14,325 | 7,693 | 2,563 | 16,347 | 40,928 | |||||||||||||||||

Residential real estate | — | — | 3,438 | — | 5,916 | 9,354 | |||||||||||||||||

Personal and home equity | — | — | — | — | 12,471 | 12,471 | |||||||||||||||||

Total | $ | — | $ | 30,614 | $ | 11,131 | $ | 9,148 | $ | 42,934 | $ | 93,827 | |||||||||||

Number of borrowers: | |||||||||||||||||||||||

Commercial | — | 2 | — | 3 | 25 | 30 | |||||||||||||||||

Commercial real estate | — | 2 | 2 | 1 | 28 | 33 | |||||||||||||||||

Residential real estate | — | — | 1 | — | 28 | 29 | |||||||||||||||||

Personal and home equity | — | — | — | — | 51 | 51 | |||||||||||||||||

Total | — | 4 | 3 | 4 | 132 | 143 | |||||||||||||||||

(1) | Refer to Glossary of Terms for definition. |

15

Foreclosed Real Estate (OREO), excluding covered assets (1) | |||||||||||||||||||||||||||||

(Dollars in thousands) | |||||||||||||||||||||||||||||

(Unaudited) | |||||||||||||||||||||||||||||

OREO Properties by Type | |||||||||||||||||||||||||||||

June 30, 2014 | March 31, 2014 | December 31, 2013 | |||||||||||||||||||||||||||

Number of Properties | Amount | % of Total | Number of Properties | Amount | % of Total | Number of Properties | Amount | % of Total | |||||||||||||||||||||

Single-family homes | 12 | $ | 2,053 | 10 | % | 11 | $ | 1,733 | 7 | % | 12 | $ | 3,405 | 12 | % | ||||||||||||||

Land parcels | 138 | 10,111 | 52 | % | 140 | 10,746 | 46 | % | 142 | 12,710 | 44 | % | |||||||||||||||||

Multi-family | 2 | 423 | 2 | % | 1 | 124 | 1 | % | 1 | 175 | 1 | % | |||||||||||||||||

Office/industrial | 11 | 6,365 | 32 | % | 15 | 10,005 | 42 | % | 20 | 11,301 | 40 | % | |||||||||||||||||

Retail | 1 | 871 | 4 | % | 1 | 957 | 4 | % | 1 | 957 | 3 | % | |||||||||||||||||

Total | 164 | $ | 19,823 | 100 | % | 168 | $ | 23,565 | 100 | % | 176 | $ | 28,548 | 100 | % | ||||||||||||||

(1) | Refer to Glossary of Terms for definition. |

16

Allowance for Loan Losses (excluding covered assets (1)) | |||||||||||||||||||

(Dollars in thousands) | |||||||||||||||||||

(Unaudited) | |||||||||||||||||||

2Q14 | 1Q14 | 4Q13 | 3Q13 | 2Q13 | |||||||||||||||

Change in allowance for loan losses: | |||||||||||||||||||

Balance at beginning of period | $ | 146,768 | $ | 143,109 | $ | 145,513 | $ | 148,183 | $ | 153,992 | |||||||||

Loans charged-off: | |||||||||||||||||||

Commercial | (2,142 | ) | (1,487 | ) | (1,536 | ) | (7,285 | ) | (2,372 | ) | |||||||||

Commercial real estate | (2,082 | ) | (2,582 | ) | (7,297 | ) | (1,706 | ) | (8,725 | ) | |||||||||

Construction | — | — | — | — | — | ||||||||||||||

Residential real estate | (180 | ) | (235 | ) | (1,887 | ) | (395 | ) | (783 | ) | |||||||||

Home equity | (268 | ) | (447 | ) | (591 | ) | (2,146 | ) | (334 | ) | |||||||||

Personal | (13 | ) | (130 | ) | (51 | ) | (893 | ) | (2,776 | ) | |||||||||

Total charge-offs | (4,685 | ) | (4,881 | ) | (11,362 | ) | (12,425 | ) | (14,990 | ) | |||||||||

Recoveries on loans previously charged-off: | |||||||||||||||||||

Commercial | 813 | 3,662 | 2,898 | 1,301 | 459 | ||||||||||||||

Commercial real estate | 1,360 | 688 | 302 | 366 | 141 | ||||||||||||||

Construction | 9 | 7 | 7 | 7 | 25 | ||||||||||||||

Residential real estate | 135 | 300 | 4 | 7 | 2 | ||||||||||||||

Home equity | 60 | 28 | 80 | 135 | 199 | ||||||||||||||

Personal | 20 | 406 | 757 | 142 | 46 | ||||||||||||||

Total recoveries | 2,397 | 5,091 | 4,048 | 1,958 | 872 | ||||||||||||||

Net (charge-offs) recoveries | (2,288 | ) | 210 | (7,314 | ) | (10,467 | ) | (14,118 | ) | ||||||||||

Provisions charged to operating expenses | 2,011 | 3,449 | 4,910 | 7,797 | 8,309 | ||||||||||||||

Balance at end of period | $ | 146,491 | $ | 146,768 | $ | 143,109 | $ | 145,513 | $ | 148,183 | |||||||||

Allocation of allowance for loan losses: | |||||||||||||||||||

General allocated reserve: | |||||||||||||||||||

Commercial | $ | 85,213 | $ | 81,402 | $ | 75,873 | $ | 74,734 | $ | 64,868 | |||||||||

Commercial real estate | 28,420 | 28,096 | 29,826 | 30,843 | 36,820 | ||||||||||||||

Construction | 3,621 | 3,547 | 3,338 | 3,314 | 2,626 | ||||||||||||||

Residential real estate | 4,650 | 4,780 | 5,143 | 4,254 | 4,945 | ||||||||||||||

Home equity | 3,300 | 3,226 | 3,262 | 2,952 | 3,070 | ||||||||||||||

Personal | 2,800 | 2,950 | 3,290 | 2,718 | 3,130 | ||||||||||||||

Total allocated | 128,004 | 124,001 | 120,732 | 118,815 | 115,459 | ||||||||||||||

Specific reserve | 18,487 | 22,767 | 22,377 | 26,698 | 32,724 | ||||||||||||||

Total | $ | 146,491 | $ | 146,768 | $ | 143,109 | $ | 145,513 | $ | 148,183 | |||||||||

Allocation of reserve by a percent of total allowance for loan losses: | |||||||||||||||||||

General allocated reserve: | |||||||||||||||||||

Commercial | 59 | % | 56 | % | 53 | % | 52 | % | 44 | % | |||||||||

Commercial real estate | 19 | % | 19 | % | 21 | % | 21 | % | 25 | % | |||||||||

Construction | 2 | % | 2 | % | 2 | % | 2 | % | 2 | % | |||||||||

Residential real estate | 3 | % | 3 | % | 4 | % | 3 | % | 3 | % | |||||||||

Home equity | 2 | % | 2 | % | 2 | % | 2 | % | 2 | % | |||||||||

Personal | 2 | % | 2 | % | 2 | % | 2 | % | 2 | % | |||||||||

Total allocated | 87 | % | 84 | % | 84 | % | 82 | % | 78 | % | |||||||||

Specific reserve | 13 | % | 16 | % | 16 | % | 18 | % | 22 | % | |||||||||

Total | 100 | % | 100 | % | 100 | % | 100 | % | 100 | % | |||||||||

Allowance for loan losses to: | |||||||||||||||||||

Total loans | 1.32 | % | 1.34 | % | 1.34 | % | 1.40 | % | 1.47 | % | |||||||||

Nonperforming loans | 191 | % | 156 | % | 152 | % | 128 | % | 122 | % | |||||||||

(1) | Refer to Glossary of Terms for definition. |

17

Deposits | ||||||||||||||||||||||||||||||||||

(Dollars in thousands) | ||||||||||||||||||||||||||||||||||

6/30/14 | % of Total | 3/31/14 | % of Total | 12/31/13 | % of Total | 9/30/13 | % of Total | 6/30/13 | % of Total | |||||||||||||||||||||||||

(Unaudited) | (Unaudited) | (Audited) | (Unaudited) | (Unaudited) | ||||||||||||||||||||||||||||||

Noninterest-bearing deposits | $ | 3,387,424 | 28 | % | $ | 3,103,736 | 26 | % | $ | 3,172,676 | 26 | % | $ | 3,106,986 | 26 | % | $ | 2,736,868 | 24 | % | ||||||||||||||

Interest-bearing demand deposits | 1,230,681 | 10 | % | 1,466,095 | 12 | % | 1,470,856 | 12 | % | 1,183,471 | 10 | % | 1,234,134 | 11 | % | |||||||||||||||||||

Savings deposits | 281,099 | 2 | % | 288,686 | 3 | % | 284,482 | 2 | % | 260,822 | 2 | % | 245,133 | 2 | % | |||||||||||||||||||

Money market accounts | 4,752,148 | 39 | % | 4,497,712 | 38 | % | 4,515,079 | 38 | % | 4,517,235 | 38 | % | 4,409,797 | 39 | % | |||||||||||||||||||

Time deposits | 1,299,616 | 11 | % | 1,320,466 | 11 | % | 1,336,522 | 11 | % | 1,333,232 | 11 | % | 1,355,522 | 12 | % | |||||||||||||||||||

Brokered time deposits: | ||||||||||||||||||||||||||||||||||

Client other | 113,104 | * | 111,601 | 1 | % | 114,249 | 1 | % | 127,214 | 1 | % | 136,082 | 1 | % | ||||||||||||||||||||

Non-client traditional | 604,688 | 5 | % | 458,344 | 4 | % | 408,365 | 3 | % | 548,429 | 5 | % | 445,666 | 4 | % | |||||||||||||||||||

Client CDARS(1) | 554,575 | 5 | % | 639,521 | 5 | % | 711,412 | 7 | % | 755,167 | 7 | % | 695,130 | 6 | % | |||||||||||||||||||

Non-client CDARS(1) | 12,866 | * | — | — | % | — | — | % | — | — | % | 50,000 | 1 | % | ||||||||||||||||||||

Total brokered time deposits | 1,285,233 | 10 | % | 1,209,466 | 10 | % | 1,234,026 | 11 | % | 1,430,810 | 13 | % | 1,326,878 | 12 | % | |||||||||||||||||||

Total deposits | $ | 12,236,201 | 100 | % | $ | 11,886,161 | 100 | % | $ | 12,013,641 | 100 | % | $ | 11,832,556 | 100 | % | $ | 11,308,332 | 100 | % | ||||||||||||||

Client deposits(1) | $ | 11,618,647 | 95 | % | $ | 11,427,817 | 96 | % | $ | 11,605,276 | 97 | % | $ | 11,284,127 | 95 | % | $ | 10,812,666 | 95 | % | ||||||||||||||

Note: Certain reclassifications have been made to prior period amounts to conform to the current period presentation.

(1) | Refer to Glossary of Terms for definition. |

* | Less than 1%. |

18

Net Interest Margin | ||||||||||||||||||||||||||||||||||

(Dollars in thousands) | ||||||||||||||||||||||||||||||||||

(Unaudited) | ||||||||||||||||||||||||||||||||||

Quarters Ended | ||||||||||||||||||||||||||||||||||

June 30, 2014 | March 31, 2014 | June 30, 2013 | ||||||||||||||||||||||||||||||||

Average Balance | Interest (1) | Yield/ Rate | Average Balance | Interest (1) | Yield/ Rate | Average Balance | Interest (1) | Yield/ Rate | ||||||||||||||||||||||||||

Assets: | ||||||||||||||||||||||||||||||||||

Federal funds sold and interest-bearing deposits in banks | $ | 225,135 | $ | 139 | 0.24 | % | $ | 233,311 | $ | 142 | 0.24 | % | $ | 181,823 | $ | 112 | 0.24 | % | ||||||||||||||||

Securities: | ||||||||||||||||||||||||||||||||||

Taxable | 2,291,837 | 13,625 | 2.38 | % | 2,237,628 | 13,255 | 2.37 | % | 2,149,465 | 12,519 | 2.33 | % | ||||||||||||||||||||||

Tax-exempt (2) | 268,765 | 2,176 | 3.24 | % | 265,551 | 2,329 | 3.51 | % | 239,851 | 2,337 | 3.90 | % | ||||||||||||||||||||||

Total securities | 2,560,602 | 15,801 | 2.47 | % | 2,503,179 | 15,584 | 2.49 | % | 2,389,316 | 14,856 | 2.49 | % | ||||||||||||||||||||||

FHLB stock | 28,916 | 59 | 0.81 | % | 30,005 | 33 | 0.44 | % | 34,270 | 62 | 0.72 | % | ||||||||||||||||||||||

Loans, excluding covered assets: | ||||||||||||||||||||||||||||||||||

Commercial | 7,485,211 | 81,366 | 4.30 | % | 7,186,657 | 78,215 | 4.35 | % | 6,635,679 | 74,150 | 4.42 | % | ||||||||||||||||||||||

Commercial real estate | 2,470,926 | 22,132 | 3.54 | % | 2,487,677 | 22,009 | 3.54 | % | 2,502,503 | 23,920 | 3.78 | % | ||||||||||||||||||||||

Construction | 378,189 | 3,612 | 3.78 | % | 315,136 | 3,077 | 3.91 | % | 194,958 | 2,051 | 4.16 | % | ||||||||||||||||||||||

Residential | 348,267 | 3,221 | 3.70 | % | 350,388 | 3,357 | 3.83 | % | 395,196 | 3,633 | 3.68 | % | ||||||||||||||||||||||

Personal and home equity | 355,262 | 2,747 | 3.10 | % | 362,335 | 2,753 | 3.08 | % | 376,955 | 3,031 | 3.22 | % | ||||||||||||||||||||||

Total loans, excluding covered assets (3) | 11,037,855 | 113,078 | 4.06 | % | 10,702,193 | 109,411 | 4.09 | % | 10,105,291 | 106,785 | 4.18 | % | ||||||||||||||||||||||

Covered assets (4) | 84,246 | 618 | 2.91 | % | 95,842 | 788 | 3.30 | % | 148,242 | 621 | 1.66 | % | ||||||||||||||||||||||

Total interest-earning assets (2) | 13,936,754 | $ | 129,695 | 3.69 | % | 13,564,530 | $ | 125,958 | 3.72 | % | 12,858,942 | $ | 122,436 | 3.77 | % | |||||||||||||||||||

Cash and due from banks | 148,143 | 146,746 | 143,973 | |||||||||||||||||||||||||||||||

Allowance for loan and covered loan losses | (164,694 | ) | (164,933 | ) | (181,235 | ) | ||||||||||||||||||||||||||||

Other assets | 486,593 | 483,870 | 588,082 | |||||||||||||||||||||||||||||||

Total assets | $ | 14,406,796 | $ | 14,030,213 | $ | 13,409,762 | ||||||||||||||||||||||||||||

Liabilities and Equity: | ||||||||||||||||||||||||||||||||||

Interest-bearing demand deposits | $ | 1,199,553 | $ | 842 | 0.28 | % | $ | 1,293,652 | $ | 942 | 0.30 | % | $ | 1,250,305 | $ | 1,034 | 0.33 | % | ||||||||||||||||

Savings deposits | 285,501 | 194 | 0.27 | % | 284,703 | 196 | 0.28 | % | 246,928 | 126 | 0.21 | % | ||||||||||||||||||||||

Money market accounts | 4,947,609 | 3,893 | 0.32 | % | 4,660,158 | 3,778 | 0.33 | % | 4,383,915 | 3,760 | 0.34 | % | ||||||||||||||||||||||

Time and brokered time deposits | 2,591,585 | 5,034 | 0.78 | % | 2,547,508 | 4,806 | 0.77 | % | 2,647,015 | 4,956 | 0.75 | % | ||||||||||||||||||||||

Total interest-bearing deposits | 9,024,248 | 9,963 | 0.44 | % | 8,786,021 | 9,722 | 0.45 | % | 8,528,163 | 9,876 | 0.46 | % | ||||||||||||||||||||||

Short-term and secured borrowings | 45,363 | 141 | 1.23 | % | 43,289 | 196 | 1.81 | % | 173,089 | 410 | 0.94 | % | ||||||||||||||||||||||

Long-term debt | 627,716 | 6,496 | 4.13 | % | 627,793 | 6,488 | 4.13 | % | 499,793 | 7,613 | 6.08 | % | ||||||||||||||||||||||

Total interest-bearing liabilities | 9,697,327 | 16,600 | 0.69 | % | 9,457,103 | 16,406 | 0.70 | % | 9,201,045 | 17,899 | 0.78 | % | ||||||||||||||||||||||

Noninterest-bearing demand deposits | 3,202,460 | 3,101,219 | 2,816,783 | |||||||||||||||||||||||||||||||

Other liabilities | 128,428 | 136,478 | 141,793 | |||||||||||||||||||||||||||||||

Equity | 1,378,581 | 1,335,413 | 1,250,141 | |||||||||||||||||||||||||||||||

Total liabilities and equity | $ | 14,406,796 | $ | 14,030,213 | $ | 13,409,762 | ||||||||||||||||||||||||||||

Net interest spread (2) | 3.00 | % | 3.02 | % | 2.99 | % | ||||||||||||||||||||||||||||

Contribution of noninterest-bearing sources of funds | 0.21 | % | 0.21 | % | 0.23 | % | ||||||||||||||||||||||||||||

Net interest income/margin (2) | 113,095 | 3.21 | % | 109,552 | 3.23 | % | 104,537 | 3.22 | % | |||||||||||||||||||||||||

Less: tax equivalent adjustment | 744 | 800 | 805 | |||||||||||||||||||||||||||||||

Net interest income, as reported | $ | 112,351 | $ | 108,752 | $ | 103,732 | ||||||||||||||||||||||||||||

(1) | Interest income included $6.6 million, $6.2 million, and $6.3 million in loan fees for the quarter ended June 30, 2014, March 31, 2014 and June 30, 2013, respectively. |

(2) | Interest income and yields are presented on a tax-equivalent basis, assuming a federal income tax rate of 35%. This is a non-U.S. GAAP measure. |

(3) | Average loans on a nonaccrual basis for the recognition of interest income totaled $86.7 million, $93.0 million, and $125.3 million for the quarter ended June 30, 2014, March 31, 2014, and June 30, 2013, respectively, and are included in loans for purposes of this analysis. Interest foregone on nonperforming loans was estimated to be approximately $836,000, $870,000 and $1.2 million for the quarter ended June 30, 2014, March 31, 2014, and June 30, 2013, respectively, based on the average loan portfolio yield for the corresponding period. |

(4) | Covered interest-earning assets consist of loans acquired through an FDIC-assisted transaction that are subject to a loss share agreement and the related indemnification asset. |

(5) | Refer to Glossary of Terms for definition. |

19

Net Interest Margin | |||||||||||||||||||||

(Dollars in thousands) | |||||||||||||||||||||

(Unaudited) | |||||||||||||||||||||

Six Months Ended June 30, | |||||||||||||||||||||

2014 | 2013 | ||||||||||||||||||||

Average Balance | Interest (1) | Yield / Rate | Average Balance | Interest (1) | Yield / Rate | ||||||||||||||||

Assets: | |||||||||||||||||||||

Federal funds sold and interest-bearing deposits in banks | $ | 229,200 | $ | 281 | 0.24 | % | $ | 258,444 | $ | 320 | 0.25 | % | |||||||||

Securities: | |||||||||||||||||||||

Taxable | 2,264,882 | 26,880 | 2.37 | % | 2,128,004 | 25,341 | 2.38 | % | |||||||||||||

Tax-exempt (2) | 267,167 | 4,505 | 3.37 | % | 230,240 | 4,623 | 4.02 | % | |||||||||||||

Total securities | 2,532,049 | 31,385 | 2.48 | % | 2,358,244 | 29,964 | 2.54 | % | |||||||||||||

FHLB stock | 29,457 | 92 | 0.62 | % | 36,189 | 152 | 0.83 | % | |||||||||||||

Loans, excluding covered assets: | |||||||||||||||||||||

Commercial | 7,336,579 | 159,581 | 4.33 | % | 6,582,441 | 145,406 | 4.39 | % | |||||||||||||

Commercial real estate | 2,479,255 | 44,141 | 3.54 | % | 2,576,407 | 49,312 | 3.81 | % | |||||||||||||

Construction | 346,880 | 6,689 | 3.84 | % | 191,604 | 4,004 | 4.16 | % | |||||||||||||

Residential | 349,426 | 6,579 | 3.77 | % | 400,805 | 7,395 | 3.69 | % | |||||||||||||

Personal and home equity | 358,784 | 5,500 | 3.09 | % | 383,155 | 6,237 | 3.28 | % | |||||||||||||

Total loans, excluding covered assets (3) | 10,870,924 | 222,490 | 4.07 | % | 10,134,412 | 212,354 | 4.17 | % | |||||||||||||

Covered assets (4) | 90,012 | 1,405 | 3.12 | % | 155,004 | 1,839 | 2.37 | % | |||||||||||||

Total interest-earning assets (2) | 13,751,642 | $ | 255,653 | 3.70 | % | 12,942,293 | $ | 244,629 | 3.76 | % | |||||||||||

Cash and due from banks | 147,448 | 143,443 | |||||||||||||||||||

Allowance for loan and covered loan losses | (164,813 | ) | (185,043 | ) | |||||||||||||||||

Other assets | 485,268 | 612,269 | |||||||||||||||||||

Total assets | $ | 14,219,545 | $ | 13,512,962 | |||||||||||||||||

Liabilities and Equity: | |||||||||||||||||||||

Interest-bearing demand deposits | $ | 1,246,343 | $ | 1,784 | 0.29 | % | $ | 1,257,482 | $ | 2,149 | 0.34 | % | |||||||||

Savings deposits | 285,104 | 391 | 0.28 | % | 260,543 | 291 | 0.23 | % | |||||||||||||

Money market accounts | 4,804,677 | 7,670 | 0.32 | % | 4,474,835 | 7,995 | 0.36 | % | |||||||||||||

Time and brokered time deposits | 2,569,668 | 9,840 | 0.77 | % | 2,587,113 | 10,084 | 0.79 | % | |||||||||||||

Total interest-bearing deposits | 8,905,792 | 19,685 | 0.45 | % | 8,579,973 | 20,519 | 0.48 | % | |||||||||||||

Short-term and secured borrowings | 44,332 | 337 | 1.51 | % | 133,219 | 528 | 0.79 | % | |||||||||||||

Long-term debt | 627,754 | 12,984 | 4.13 | % | 499,793 | 15,221 | 6.08 | % | |||||||||||||

Total interest-bearing liabilities | 9,577,878 | $ | 33,006 | 0.69 | % | 9,212,985 | $ | 36,268 | 0.79 | % | |||||||||||

Noninterest-bearing demand deposits | 3,152,119 | 2,910,375 | |||||||||||||||||||

Other liabilities | 132,432 | 150,654 | |||||||||||||||||||

Equity | 1,357,116 | 1,238,948 | |||||||||||||||||||

Total liabilities and equity | $ | 14,219,545 | $ | 13,512,962 | |||||||||||||||||

Net interest spread (2)(5) | 3.01 | % | 2.97 | % | |||||||||||||||||

Contribution of noninterest-bearing sources of funds | 0.21 | % | 0.23 | % | |||||||||||||||||

Net interest income/margin (2)(5) | 222,647 | 3.22 | % | 208,361 | 3.20 | % | |||||||||||||||

Less: tax-equivalent adjustment | 1,544 | 1,589 | |||||||||||||||||||

Net interest income, as reported | $ | 221,103 | $ | 206,772 | |||||||||||||||||

(1) | Interest income included $12.7 million and $11.5 million in loan fees for the six months ended June 30, 2014 and 2013, respectively. |

(2) | Interest income and yields are presented on a tax-equivalent basis, assuming a federal income tax rate of 35%. This is a non-U.S. GAAP measure. |

(3) | Average loans on a nonaccrual basis for the recognition of interest income totaled $89.3 million and $131.5 million for the six months ended June 30, 2014 and 2013, respectively, and are included in loans for purposes of this analysis. Interest foregone on nonperforming loans was estimated to be approximately $1.7 million and $2.6 million for the six months ended June 30, 2014 and 2013, respectively, based on the average loan portfolio yield for the corresponding period. |

(4) | Covered interest-earning assets consist of loans acquired through an FDIC-assisted transaction that are subject to a loss share agreement and the related indemnification asset. |

(5) | Refer to Glossary of Terms for definition. |

20

NON-U.S. GAAP FINANCIAL MEASURES

This press release contains both U.S. GAAP and non-U.S. GAAP based financial measures. These non-U.S. GAAP financial measures include net interest income, net interest margin, net revenue, operating profit, and efficiency ratio all on a fully taxable-equivalent basis, return on average tangible common equity, Tier 1 common equity to risk-weighted assets, tangible common equity to risk-weighted assets, tangible common equity to tangible assets, and tangible book value. We believe that presenting these non-U.S. GAAP financial measures will provide information useful to investors in understanding our underlying operational performance, our business, and performance trends and facilitates comparisons with the performance of others in the banking industry.

We use net interest income on a taxable-equivalent basis in calculating various performance measures by increasing the interest income earned on tax-exempt assets to make it fully equivalent to interest income earned on taxable investments assuming a 35% tax rate. Management believes this measure to be the preferred industry measurement of net interest income as it enhances comparability to net interest income arising from taxable and tax-exempt sources, and accordingly believes that providing this measure may be useful for peer comparison purposes.

In addition to capital ratios defined by banking regulators, we also consider various measures when evaluating capital utilization and adequacy, including return on average tangible common equity, Tier 1 common equity to risk-weighted assets, tangible common equity to risk-weighted assets, tangible common equity to tangible assets, and tangible book value. These calculations are intended to complement the capital ratios defined by banking regulators for both absolute and comparative purposes. All of these measures exclude the ending balances of goodwill and other intangibles while certain of these ratios exclude preferred capital components. Because U.S. GAAP does not include capital ratio measures, we believe there are no comparable U.S. GAAP financial measures to these ratios. We believe these non-U.S. GAAP financial measures are relevant because they provide information that is helpful in assessing the level of capital available to withstand unexpected market conditions. Additionally, presentation of these measures allows readers to compare certain aspects of our capitalization to other companies. However, because there are no standardized definitions for these ratios, our calculations may not be comparable with other companies, and this may affect the usefulness of these measures to investors. Calculations of the Tier 1 common equity to risk-weighted assets ratio contained herein exclude the effect of the final Basel III capital rules adopted and issued by the Federal Reserve Board in July 2013, which are effective January 1, 2014 with compliance required January 1, 2015.

Non-U.S. GAAP financial measures have inherent limitations, are not required to be uniformly applied, and are not audited. Although these non-U.S. GAAP financial measures are frequently used by stakeholders in the evaluation of a company, they have limitations as analytical tools, and should not be considered in isolation or as a substitute for analyses of results as reported under U.S. GAAP. As a result, we encourage readers to consider our Consolidated Financial Statements in their entirety and not to rely on any single financial measure.

21

Non-U.S. GAAP Financial Measures

(Amounts in thousands)

(Unaudited)

The following table reconciles non-U.S. GAAP financial measures to U.S. GAAP.

Quarters Ended | |||||||||||||||||||

2014 | 2013 | ||||||||||||||||||

June 30 | March 31 | December 31 | September 30 | June 30 | |||||||||||||||

Taxable-equivalent net interest income | |||||||||||||||||||

U.S. GAAP net interest income | $ | 112,351 | $ | 108,752 | $ | 108,456 | $ | 105,835 | $ | 103,732 | |||||||||

Taxable-equivalent adjustment | 744 | 800 | 840 | 818 | 805 | ||||||||||||||

Taxable-equivalent net interest income (a) | $ | 113,095 | $ | 109,552 | $ | 109,296 | $ | 106,653 | $ | 104,537 | |||||||||

Average Earning Assets (b) | $ | 13,936,754 | $ | 13,564,530 | $ | 13,472,632 | $ | 13,154,557 | $ | 12,858,942 | |||||||||

Net Interest Margin ((a) annualized) / (b) | 3.21 | % | 3.23 | % | 3.18 | % | 3.18 | % | 3.22 | % | |||||||||

Net Revenue | |||||||||||||||||||

Taxable-equivalent net interest income | $ | 113,095 | $ | 109,552 | $ | 109,296 | $ | 106,653 | $ | 104,537 | |||||||||

U.S. GAAP non-interest income | 30,259 | 26,236 | 26,740 | 27,773 | 29,009 | ||||||||||||||

Net revenue (c) | $ | 143,354 | $ | 135,788 | $ | 136,036 | $ | 134,426 | $ | 133,546 | |||||||||

Operating Profit | |||||||||||||||||||

U.S. GAAP income before income taxes | $ | 66,818 | $ | 55,531 | $ | 54,893 | $ | 54,219 | $ | 46,643 | |||||||||

Provision for loan and covered loan losses | 327 | 3,707 | 4,476 | 8,120 | 8,843 | ||||||||||||||

Taxable-equivalent adjustment | 744 | 800 | 840 | 818 | 805 | ||||||||||||||

Operating profit | $ | 67,889 | $ | 60,038 | $ | 60,209 | $ | 63,157 | $ | 56,291 | |||||||||

Efficiency Ratio | |||||||||||||||||||

U.S. GAAP non-interest expense (d) | $ | 75,465 | $ | 75,750 | $ | 75,827 | $ | 71,269 | $ | 77,255 | |||||||||

Net revenue | $ | 143,354 | $ | 135,788 | $ | 136,036 | $ | 134,426 | $ | 133,546 | |||||||||

Efficiency ratio (d) / (c) | 52.64 | % | 55.79 | % | 55.74 | % | 53.02 | % | 57.85 | % | |||||||||

Adjusted Net Income | |||||||||||||||||||

U.S. GAAP net income available to common stockholders | $ | 40,824 | $ | 34,505 | $ | 33,706 | $ | 33,058 | $ | 28,915 | |||||||||

Amortization of intangibles, net of tax | 458 | 458 | 471 | 472 | 473 | ||||||||||||||

Adjusted net income (e) | $ | 41,282 | $ | 34,963 | $ | 34,177 | $ | 33,530 | $ | 29,388 | |||||||||

Average Tangible Common Equity | |||||||||||||||||||

U.S. GAAP average total equity | $ | 1,378,581 | $ | 1,335,413 | $ | 1,300,893 | $ | 1,257,541 | $ | 1,250,141 | |||||||||

Less: average goodwill | 94,041 | 94,041 | 94,477 | 94,494 | 94,506 | ||||||||||||||

Less: average other intangibles | 7,749 | 8,506 | 10,074 | 10,865 | 11,644 | ||||||||||||||

Average tangible common equity (f) | $ | 1,276,791 | $ | 1,232,866 | $ | 1,196,342 | $ | 1,152,182 | $ | 1,143,991 | |||||||||

Return on average tangible common equity ((e) annualized) / (f) | 12.97 | % | 11.50 | % | 11.33 | % | 11.55 | % | 10.3 | % | |||||||||

22

Non-U.S. GAAP Financial Measures (continued)

(Amounts in thousands)

(Unaudited)

Six Months Ended June 30, | |||||||

2014 | 2013 | ||||||

Taxable-equivalent net interest income | |||||||