Attached files

| file | filename |

|---|---|

| 8-K - 8-K - LyondellBasell Industries N.V. | d716306d8k.htm |

| EX-99.1 - EX-99.1 - LyondellBasell Industries N.V. | d716306dex991.htm |

Jim

Gallogly, Chief Executive Officer Karyn Ovelmen, Chief Financial

Officer Sergey Vasnetsov, SVP –

Strategic Planning and Transactions

Doug Pike, VP –

Investor Relations

First-Quarter 2014 Earnings

Exhibit 99.2 |

lyondellbasell.com

Cautionary Statement

2

The

statements

in

this

presentation

relating

to

matters

that

are

not

historical

facts

are

forward-looking

statements.

These

forward-looking statements are based upon assumptions of management which are

believed to be reasonable at the time made and are subject to significant

risks and uncertainties. Actual results could differ materially based on factors including, but not

limited to, the business cyclicality of the chemical, polymers and refining

industries; the availability, cost and price volatility of raw materials and

utilities, particularly the cost of oil, natural gas, and associated natural gas liquids; competitive product and

pricing pressures; labor conditions; our ability to attract and retain key

personnel; operating interruptions (including leaks, explosions, fires,

weather-related incidents, mechanical failure, unscheduled downtime, supplier disruptions, labor shortages,

strikes, work stoppages or other labor difficulties, transportation interruptions,

spills and releases and other environmental risks);

the

supply/demand

balances

for

our

and

our

joint

ventures’

products,

and

the

related

effects

of

industry

production

capacities and operating rates; our ability to achieve expected cost savings and

other synergies; our ability to successfully execute projects and growth

strategies; legal and environmental proceedings; tax rulings, consequences or proceedings;

technological developments, and our ability to develop new products and process

technologies; potential governmental regulatory actions; political unrest

and terrorist acts; risks and uncertainties posed by international operations, including foreign

currency fluctuations; and our ability to comply with debt covenants and service

our debt. Additional factors that could cause results

to

differ

materially

from

those

described

in

the

forward-looking

statements

can

be

found

in

the

“Risk

Factors”

section

of

our Form 10-K for the year ended December 31, 2013, which can be found at

www.lyondellbasell.com on the Investor Relations page and on the Securities

and Exchange Commission’s website at www.sec.gov.

The illustrative results or returns of growth projects are not in any way intended

to be, nor should they be taken as, indicators or guarantees of performance.

The assumptions on which they are based are not projections and do not necessarily represent the

Company’s expectations and future performance. You should not rely on

illustrated results or returns or these assumptions as being indicative of

our future results or returns. This presentation contains time sensitive

information that is accurate only as of the date hereof. Information contained in this

presentation is unaudited and is subject to change. We undertake no

obligation to update the information presented herein except as required by

law. |

lyondellbasell.com

Information Related to Financial Measures

3

We have included EBITDA in this presentation, which is a non-GAAP measure, as

we believe that EBITDA

is

a

measure

commonly

used

by

investors.

However,

EBITDA,

as

presented

herein,

may

not

be

comparable to a similarly titled measure reported by other companies due to

differences in the way the measure is calculated.

We calculate EBITDA as income from continuing operations plus interest

expense (net), provision for (benefit from) income taxes, and depreciation &

amortization. EBITDA should not be considered an alternative to profit or

operating profit for any period as an indicator of our performance, or as an

alternative to operating cash flows as a measure of our liquidity. See Table 8 of

our accompanying earnings release for reconciliations of EBITDA to net

income. While

we

also

believe

that

free

cash

flow

(FCF)

and

book

capital

are

measures

commonly

used

by

investors,

free

cash

flow

and

book

capital,

as

presented

herein,

may

not

be

comparable

to

similarly

titled

measures reported by other companies due to differences in the way the measures are

calculated. For purposes of this presentation, free cash flow means net cash

provided by operating activities minus capital

expenditures

and

book

capital

means

total

debt

plus

stockholders’

equity

plus

minority

interests. |

lyondellbasell.com

Highlights

4

EBITDA

LTM EBITDA -

$6,394 million LTM

EPS

–

$6.93

per

share

($ in millions)

Income

from

Continuing

Operations

($ in millions, except per share data)

1Q'14

4Q'13

1Q'13

EBITDA

$1,668

$1,543

$1,585

Income from Continuing Operations

$943

$1,177

$906

Diluted Earnings ($ / share) from Continuing Operations

$1.72

$2.11

$1.56

500

1,000

1,500

$2,000

1Q'13

2Q'13

3Q'13

4Q'13

1Q'14

300

600

900

1,200

1Q'13

2Q'13

3Q'13

4Q'13

1Q'14 |

lyondellbasell.com

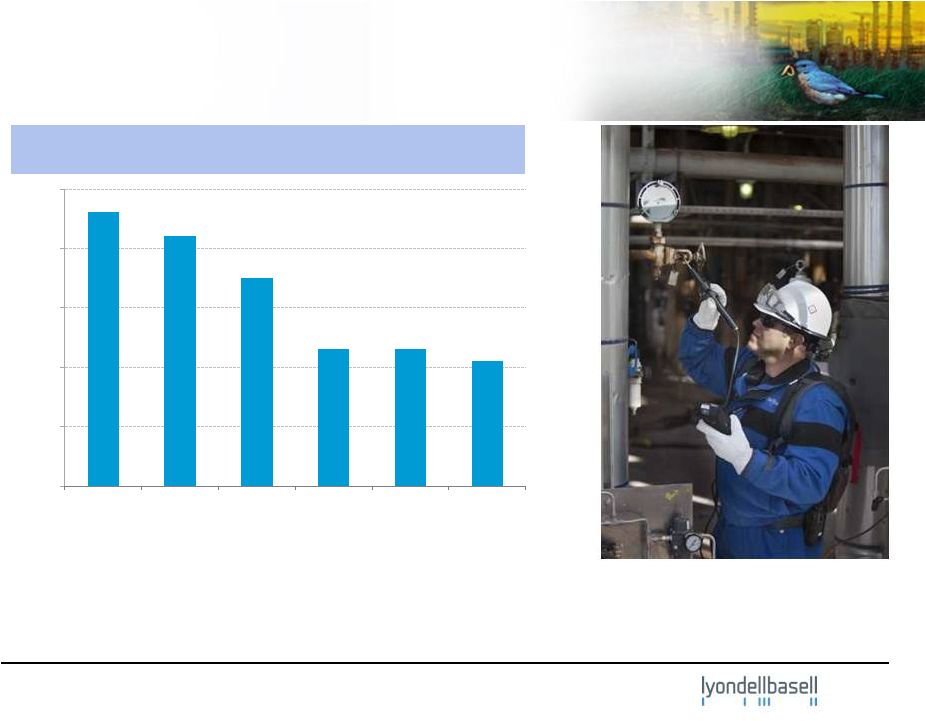

LyondellBasell Safety Performance

5

1) Includes employees and contractors.

Safety -

Injuries per 200,000 Hours Worked

(1)

0.0

0.1

0.2

0.3

0.4

0.5

2009

2010

2011

2012

2013

Q1' 2014 |

lyondellbasell.com

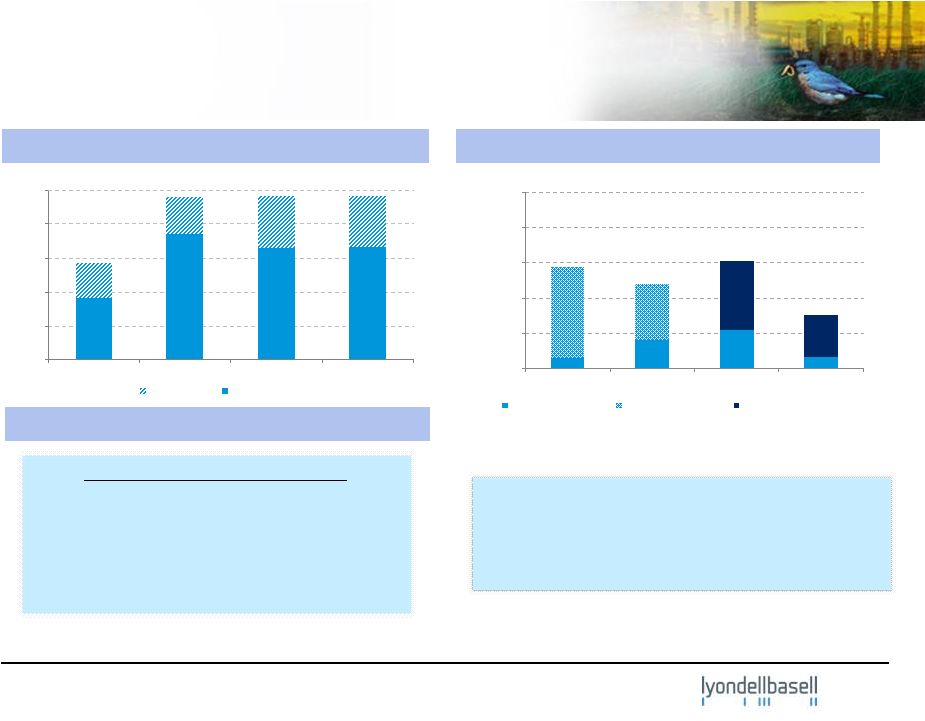

First Quarter 2014 and Last Twelve Months (LTM)

Segment EBITDA

6

($ in millions)

($ in millions)

200

400

600

800

$1000

Olefins &

Polyolefins -

Americas

Olefins &

Polyolefins -

EAI

Intermediates

& Derivatives

Refining

Technology

750

1,500

2,250

3,000

$3,750

Olefins &

Polyolefins -

Americas

Olefins &

Polyolefins -

EAI

Intermediates

& Derivatives

Refining

Technology

LTM March 2014 EBITDA

First Quarter 2014 EBITDA

Q1’14 EBITDA

$1,668 million

Q1’14 Operating Income

$1,340 million

LTM March 2014 EBITDA

$6,394 million

LTM March 2014 Operating Income

$5,175 million |

lyondellbasell.com

Cash Flow

7

1) Beginning and ending cash balances include cash and short-term securities; 2)

Includes accounts receivable, inventories and accounts payable; 3) Includes capital and maintenance turnaround spending.

($ in millions)

Q1 2014

LTM March 2014

(3)

(2)

(1)

(2)

(1)

(3)

(1)

(1)

~ $4.4 billion in dividends and share repurchases in the LTM March 2014

$4,450

$4,379

0

4,000

6,000

$8,000

Jan 2014

Balance

CF from

Operations

excl.

Working

Capital

Working

Capital

Changes

Dividends &

Share

Repurchases

Net Debt

Borrowings

Other

Mar 2014

Ending

Balance

2,000

Beginning

Capex

$2,879

$4,379

0

2,000

6,000

$8,000

Apr 2013

Beginning

Balance

CF from

Operations

excl.

Working

Capital

Working

Capital

Changes

Capex

Dividends &

Share

Repurchases

Net Debt

Borrowings

Other

Ending

Balance

4,000

Mar 2014 |

lyondellbasell.com

Sustained Cash Generation:

Share Repurchases & Dividends

8

1,000

2,000

3,000

4,000

$5,000

2011

2012

2013

Q1' 2014

Interim Dividends

Special Dividends

Share Repurchases

Cash From Operations

Dividends & Share Repurchases

($ in millions)

($ in millions)

~ 15 million shares repurchased during

Q1’2014 and ~ 42 million shares

repurchased as of March 31, 2014

1,000

2,000

3,000

4,000

$5,000

2011

2012

2013

LTM March

2014

Capex

Free Cash Flow

Key Statistics

1) Cash balances include cash and short-term securities.

Snapshot at March 31, 2014

LTM FCF: $3.3 billion

LTM Capex: $1.5 billion

Cash

(1)

: $4.4 billion

Total Debt/LTM EBITDA: 1.1x

Total Debt/Book Capital: 37% |

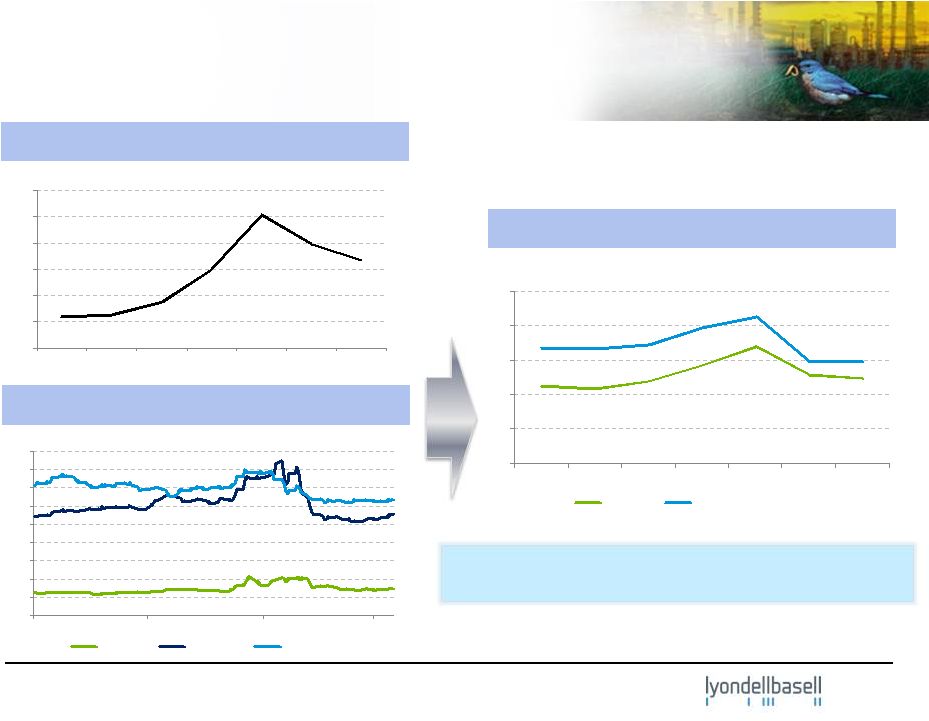

lyondellbasell.com

0

5

10

15

20

25

Oct'13

Nov'13

Dec'13

Jan'14

Feb'14

Mar'14

Apr'14

Ethane

Industry Wt. Avg

(cents/lb)

9

Cold U.S. Weather Created First-Quarter

Pressure

Henry Hub Natural Gas Prices

U.S. Cost of Ethylene Production

U.S. NGL Prices

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Oct'13

Nov'13

Dec'13

Jan'14

Feb'14

Mar'14

Apr'14

($/MMBTU)

0

20

40

60

80

100

120

140

160

180

10/1/2013

12/1/2013

2/1/2014

4/1/2014

Ethane

Propane

Butane

(cents/gal)

Source: Third party consultants’

data.

The beginning of spring has provided relief |

lyondellbasell.com

(20)

0

20

40

60

Ethane Margin

Naphtha Margin

HDPE Margin

Ethylene/HDPE Chain

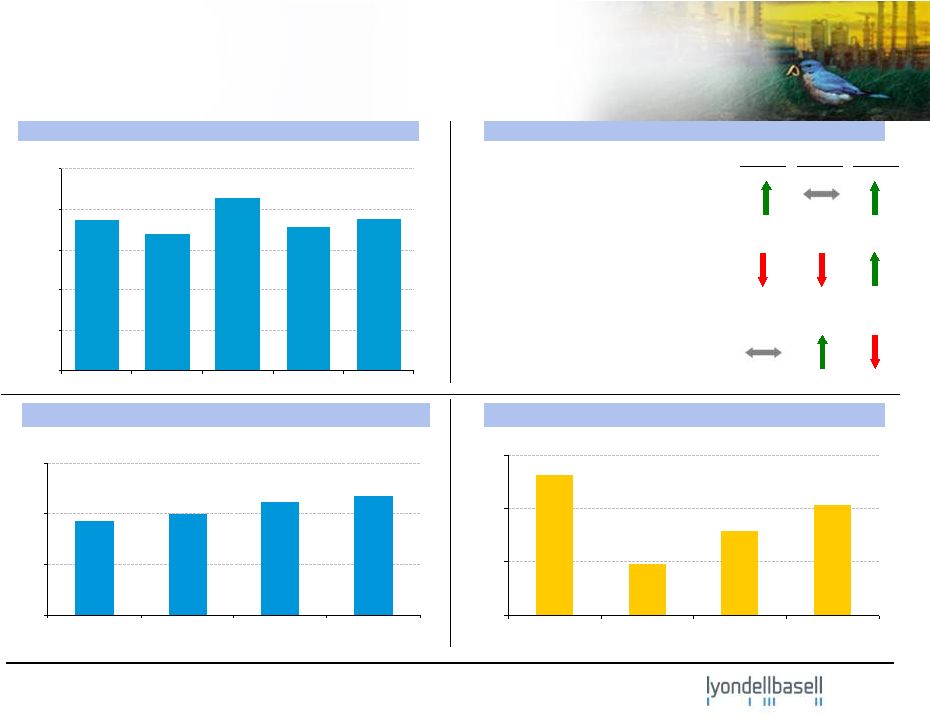

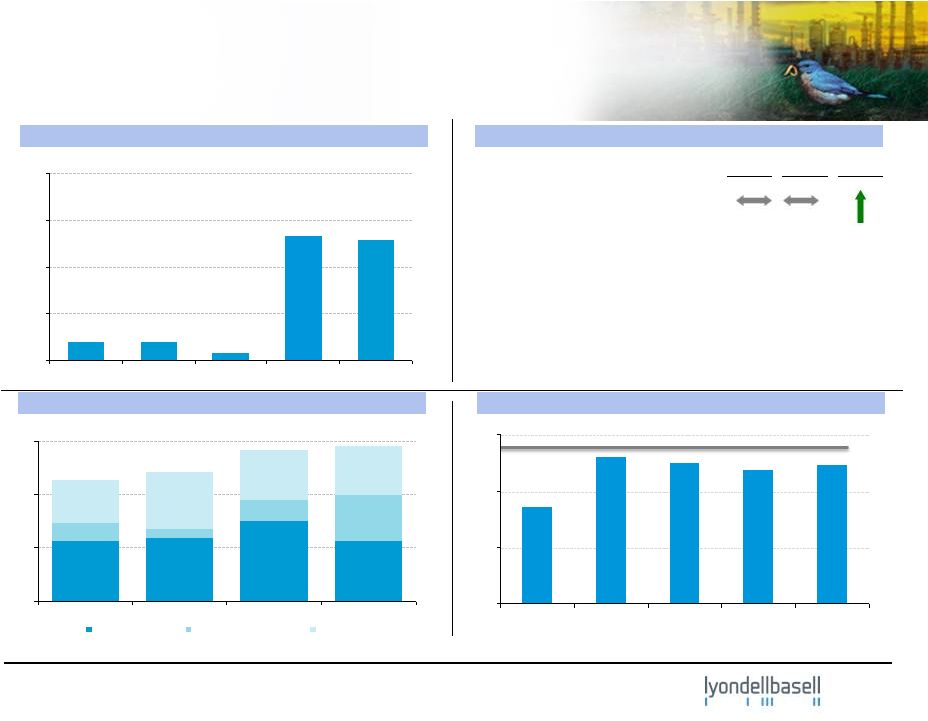

Olefins & Polyolefins –

Americas

Highlights and Business Drivers –

1Q’14

10

U.S. Olefins

•

Impacts from maintenance and NGL

price volatility

•

Inventory build ahead of La Porte

turnaround

•

Metathesis unit adding to margin

Polyethylene

•

Price up ~ 3¢/lb

•

Volumes flat

Polypropylene (includes Catalloy)

•

Spread flat

•

Volumes down ~ 4%

Ethylene Chain Margins

(1)

EBITDA

Performance vs. 4Q’13

Polypropylene Margins

(1)

EBITDA

Margin

Volume

($ in millions)

1) Source: Quarterly average industry data from third party consultants; 2) The

direction of the arrows reflects our underlying business metrics. 200

400

600

800

$1000

1Q'13

2Q'13

3Q'13

4Q'13

1Q'14

0.0

1.5

3.0

4.5

6.0

1Q'13

4Q'13

1Q'14

Apr'14

(2)

1Q’13

4Q’13

1Q’14

Apr’14

(cents / lb)

(cents / lb) |

lyondellbasell.com

Olefins & Polyolefins –

Europe, Asia, International

Highlights and Business Drivers –

1Q’14

11

100

200

300

$400

1Q'13

2Q'13

3Q'13

4Q'13

1Q'14

(10)

5

20

35

50

1Q'13

4Q'13

1Q'14

Apr'14

HDPE Margin

Naphtha Margin

Ethylene/HDPE Chain

EU Olefins

•

Margin expansion –

increased

cracking of advantaged feedstocks

•

Operating rate ~ 93%

Polyethylene

•

Volumes up ~ 8%

Polypropylene (includes Catalloy)

•

Volumes flat

•

Margins modestly up

JV equity income

European Ethylene Chain Margins

(1)

EBITDA

Performance vs. 4Q’13

European Polypropylene Margins

(1)

EBITDA

Margin

Volume

(cents / lb)

(cents / lb)

1) Source: Quarterly average data from third party

consultants; 2) The direction of the arrows reflects our underlying business metrics.

(6)

(4)

(2)

0

2

1Q'13

4Q'13

1Q'14

Apr'14

($ in millions)

(2) |

lyondellbasell.com

Intermediates & Derivatives

Highlights and Business Drivers –

1Q’14

12

EBITDA

Propylene Oxide and Derivatives

•

Higher deicer sales

Intermediates

•

Higher methanol volumes and

margins

•

Lower styrene and EG margins

Oxyfuels

EBITDA

Margin

Volume

Performance vs. 4Q’13

($ in millions)

EU MTBE Raw Material Margins (per Platts)

(1)

(cents / gallon)

P-Glycol Raw Material Margins (per Chemdata)

(1)

1) Data represents quarterly average; 2) The direction of the

arrows reflects our underlying business metrics. 100

200

300

400

$500

1Q'13

2Q'13

3Q'13

4Q'13

1Q'14

0

40

80

120

1Q'13

4Q'13

1Q'14

Apr'14

0

20

40

60

1Q13

4Q13

1Q14

2Q14 E

(2)

(cents / lb)

•

Increased raw material margins

•

Shipping delays impacted volumes |

lyondellbasell.com

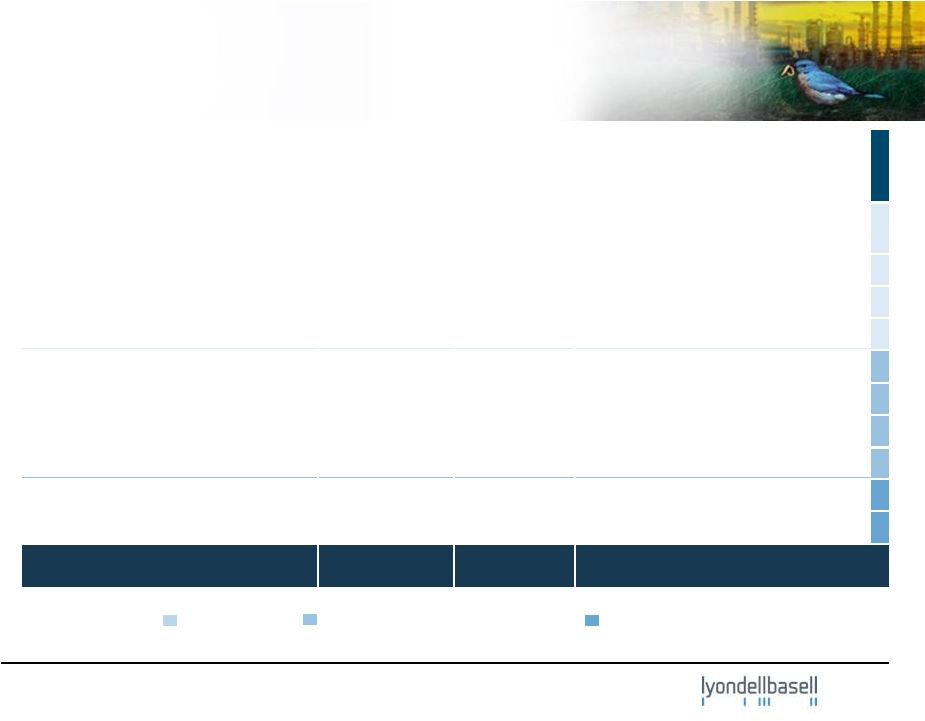

Refining Highlights and Business Drivers –

1Q’14

13

0

100

200

300

1Q'13

2Q'13

3Q'13

4Q'13

1Q'14

Houston Refinery

•

Crude throughput: 247 MBPD

•

Maya 2-1-1: $28.26 per bbl

•

Coker outage

•

Increased costs of natural gas and

RINs

EBITDA

Performance vs. 4Q’13

EBITDA

Margin

Volume

($ in millions)

1) Light Louisiana Sweet (LLS) is the referenced light crude. Data represents

quarterly average; 2) The direction of the arrows reflects our underlying business metrics.

50

100

150

$200

1Q'13

2Q'13

3Q'13

4Q'13

1Q'14

Refining Spreads (per Platts)

(1)

Refining Throughput

(2)

($ / bbl)

(MBPD)

0

10

20

30

1Q'13

4Q'13

1Q'14

Apr'14

Lt-Hvy

Lt-Gasoline

Lt-ULSD

Capacity = 268 MBPD |

lyondellbasell.com

Projects Annual Potential Values &

Completion Timelines

14

200

400

600

800

1,000

$1,200

BD

Expansion

Methanol

Restart

PE

Debottleneck

La Porte

Expansion

Channelview

Expansion

Corpus

Christi

Expansion

Q2

Q4

Q1

Q1

Q3

Q4

Annual Potential Value

(1)

($ Million/ yr)

1) Annual potential values are based on FY 2013 industry benchmark margins.

Completed |

Methanol Restart

15

Last Review

Now

lyondellbasell.com |

Channelview Ethylene Expansion

16

Last Review

Now

lyondellbasell.com |

La

Porte Ethylene Expansion 17

Last Review

Now

lyondellbasell.com |

lyondellbasell.com

Projects Completed and Active

18

(1)

Costs are based on recent company estimates and potential pre-tax values are

based on FY 2013 industry benchmark margins. Project

Cost

($Million)

Start-up

Potential Pre-Tax Earnings

($ Million/year)

Increase Ethane Capability and

Midwest Debottlenecks

~$50

2012

$150 - $180

EU Butadiene Expansion

~$100

Mid 2013

$40 - $50

Methanol Restart

~$180

Late 2013

$250 - $260

PE Debottleneck

~$20

Early 2014

$10 - $20

La Porte Expansion

~$510

Mid 2014

$300 - $350

Channelview Expansion

~$200

Early 2015

$90 - $110

Corpus Christi Expansion

~$600

Late 2015

$300 - $350

PP Compounding Growth

~ $40

2013 - 2016

$70 - $90

New PE line

~ $400

Mid 2017

$50 - $100

PO/TBA Joint Venture

MOU

2018

$70 - $90

Total

~ $2,100

~ $1,300 - $1,600

Complete

In Construction/Permit Obtained

In Development |

lyondellbasell.com

First Quarter Summary and Outlook

19

–

La Porte turnaround started in late

Q1’2014, estimate ~ 80 days

–

O&P –

EAI is expected to benefit from

advantaged feedstocks cracking in

the summer months

–

Intermediates and Derivatives is

expected to benefit from increased

oxyfuels margins

–

April 2014 Maya 2-1-1 crack spread

relatively unchanged from Q1

average

–

Growth projects progressing rapidly

First-Quarter Summary

Near-Term Outlook

–

Impact on O&P –

Americas from

maintenance, NGL volatility, and

weather related delays

–

Europe olefins and polyolefins

improvement from seasonal

recovery of volumes and margins;

continued profitability in

differentiated products

–

Steady Intermediates and

Derivatives results

–

Houston refinery impacted by coker

maintenance

–

Received permit for Corpus Christi

ethylene expansion |