Attached files

| file | filename |

|---|---|

| EX-31.1 - CERTIFICATION OF THE CHIEF EXECUTIVE OFFICER OF METROSPACES, INC. PURSUANT TO SECTION 302 OF THE SARBANES-OXLEY ACT OF 2002 - METROSPACES, INC. | mspc10k041014ex311.htm |

| EXCEL - IDEA: XBRL DOCUMENT - METROSPACES, INC. | Financial_Report.xls |

| EX-10.16 - METROSPACES, INC. | mspc10k041041ex1016.htm |

| EX-32.1 - CERTIFICATION OF THE PRINCIPAL FINANCIAL AND ACCOUNTING OFFICER OF METROSPACES, INC. PURSUANT TO SECTION 906 OF THE SARBANES OXLEY ACT OF 2002 - METROSPACES, INC. | mspc10k041014ex321.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(MARK ONE)

[x] Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2013

[ ] Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from ________ to ________

Commission file number: 333-186559

| METROSPACES, INC. |

| (Exact name of registrant as specified in its charter) |

| Delaware | 90-0817201 |

| (State or other jurisdiction of incorporation or organization) | (IRS Employee Identification No.) |

| 888 Brickell Key Dr., Unit 1102, Miami, FL | 33131 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (305) 600-0407

Securities Registered pursuant to Section 12(b) of the Exchange Act:

| Title of each class | Name of each exchange on which registered |

| None | None |

Securities Registered pursuant to Section 12(g) of the Exchange Act:

| Common Stock, Par Value $0.000001 per share |

| (Title of class) |

Indicate by check mark if the registrant is a

well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No[x]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [x]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [ ] No [x]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [x]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b2 of the Exchange Act.

| [ ] | Large accelerated filer | [ ] | Accelerated filer | |

| [ ] | Non-accelerated filer | [x] | Smaller reporting company | |

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes [ ] No [x]

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant was approximately $27,000,000 on June 26, 2013, the last day of the second quarter on which the Common Stock traded. Until the quarter beginning September 1, 2013, trading in our common stock, which was the only common equity held by non-affiliates, was sporadic and the amounts of shares traded were very small. We do not believe that the aggregate market value set forth in the previous sentence reflects the value thereof on June 30, 2013, or at any time thereafter.

APPLICABLE ONLY TO REGISTRANTS INVOLVED

IN BANKRUPTCY

PROCEEDINGS DURING THE PRECEDING FIVE YEARS:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes [ ] No [ ]

(APPLICABLE ONLY TO CORPORATE REGISTRANTS)

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. None.

The number of shares outstanding of the registrant’s common stock as of April 10, 2014, was 2,565,233,149.

(DOCUMENTS INCORPORATED BY REFERENCE)

None

METROSPACES, INC.

FORM 10-K

| Page | ||||

| PART I | ||||

| ITEM 1. BUSINESS | 1 | |||

| ITEM 1A. RISK FACTORS | 10 | |||

| ITEM 1B. UNRESOLVED STAFF COMMENTS | 10 | |||

| ITEM 2. PROPERTIES | 10 | |||

| ITEM 3. LEGAL PROCEEDINGS | 10 | |||

| ITEM 4. (REMOVED AND RESERVED) | 10 | |||

| PART II | ||||

| ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 12 | |||

| ITEM 6. SELECTED FINANCIAL DATA | 12 | |||

| ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 12 | |||

| ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 17 | |||

| ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 18 | |||

| ITEM 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 29 | |||

| ITEM 9A. CONTROLS AND PROCEDURES | 29 | |||

| ITEM 9B. OTHER INFORMATION | 29 | |||

| PART III | ||||

| ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | 30 | |||

| ITEM 11. EXECUTIVE COMPENSATION | 34 | |||

| ITEM 12. SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 35 | |||

| ITEM 13. CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 35 | |||

| ITEM 14. PRINCIPAL ACCOUNTING FEES AND SERVICES | 36 | |||

| PART IV | ||||

| ITEM 15. EXHIBITS, FINANCIAL STATEMENT SCHEDULES | 37 | |||

| SIGNATURES | 38 | |||

PART I

This annual report on Form 10-K contains forward-looking statements that are based on current expectations, estimates, forecasts and projections about the Company, us, our future performance, our beliefs and our Management’s assumptions. In addition, other written or oral statements that constitute forward-looking statements may be made by us or on our behalf. Words such as “expects,” “anticipates,” “targets,” “goals,” “projects,” “intends,” “plans,” “believes,” “seeks,” “estimates,” variations of such words and similar expressions are intended to identify such forward-looking statements. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict or assess. Therefore, actual outcomes and results may differ materially from what is expressed or forecast in such forward-looking statements. Except as required under the federal securities laws and the rules and regulations of the SEC, we do not have any intention or obligation to update publicly any forward-looking statements after the filing of this Form 10-K, whether as a result of new information, future events, changes in assumptions or otherwise.

Unless the context otherwise requires, throughout this Annual Report on Form 10-K the words “Company,” “we,” “us” and “our” refer to Metrospaces, Inc.

ITEM 1. BUSINESS

General

We acquire land and design, build, develop and resell condominiums on it, principally in urban areas in Latin America, alone or together with investors; we are also acquiring condominiums that are under construction for resale, but do not intend to conduct business in this manner after these condominiums have been sold. We sell condominiums at different prices, depending principally on their location, size and level of options and amenities to customers who are able to make substantial payments upon signing purchase agreements and at agreed time as construction progresses. Our current projects are located in Buenos Aires, Argentina, and Caracas, Venezuela. One of these projects is nearing completion (see “Business – Projects – Argentina – Chacabuco Project” on page 4), one is in the construction stage (see “Business – Projects – Venezuela – Las Narnajas 320 Project” on page 5) and one is in the planning stage (see “Business – Projects – Venezuela – Las Narnajas 450 Project” on page 7). We are considering projects in Peru and Colombia, but have taken no measures to implement them. We will market directly with our own sales force by personal contact, through real estate brokers and agents and internet websites. We will also manage these condominiums for customers who wish to lease them on a long- or short-term basis. For more detailed information about our business and operations, see “Business” on page 3. The Company’s operating subsidiary, Urban Spaces, Inc., a Nevada corporation (“Urban Spaces”), which the Company acquired on August 13, 2012, commenced operations on April 3, 2012. The Company is a development-stage company.

The address of the Company is 888 Brickell Key Drive, Unit 1102, Miami, FL 33131 and its telephone number is (305) 600-0407.

Our consolidated financial statements include only the period commencing with the inception of our operating subsidiary, Urban Spaces, on April 3, 2012, include the financial statements of Urban Spaces and its subsidiaries and do not include any historical financial data of the Company, which was incorporated on December 10, 2007, and which never conducted any business. Accordingly, these financial statements are those of Urban Spaces, which was the accounting acquirer in the merger which is discussed under the caption “History – The Merger,” on page 2.

Our common stock is quoted on the OTC Markets Inc. OTCQB tier under the symbol “MSPC.”

History

Prior to the Merger

The Company was incorporated in Delaware on December 10, 2007, under the corporate name “Strata Capital Corporation” for the purpose of acquiring Cyberoad.com Corporation, a Florida corporation (“Cyberoad”).

Cyberoad was formed as a Florida corporation in 1988, under the name Sunshine Equities Corp. In 1998, it changed its corporate name to LAL Ventures Corp and again, in 1999, it changed its corporate name to Cyberoad.com Corporation. In 1999, Cyberoad was an internet technology and software development company that developed, marketed and licensed complete computer software systems along with related technical and marketing support to operators of internet sports book and casino websites.

In 2006, Cyberoad was placed into receivership by the Circuit Court of the Eleventh Judicial Circuit in and for Miami-Dade County, Florida, pursuant to Florida Statutes, Chapter 607. In June 2007, the Court appointed a receiver in these proceedings. The receiver elected Mark Renschler as Cyberoad’s sole officer and director. In October 2007, the receivership was terminated.

On December 18, 2007, the Company acquired Cyberoad, which had no material assets, through conversion under Delaware law. Conversion is a procedure available under the corporate laws of the States of Delaware and Florida whereby a corporation may change its corporate domicile. No consideration was paid in connection with this conversion. On January 22, 2008, the Company amended its Certificate of Incorporation to increase its authorized capital stock to 5,000,000,000 shares of common stock, par value $0.000001 per share “(“Common Stock”), and 10,000,000 shares of preferred stock, par value $0.000001 per share, issuable in series, all of which was designated as Series A Preferred Stock (“Series A Preferred Stock”).

The Merger

On August 10, 2012, the Company, Strata Acquisition, Inc., a Nevada corporation (“Acquisition”), and Urban Spaces entered into a Plan and Agreement of Merger (the “Merger Agreement”),under which Acquisition was merged with and into Urban Spaces, with the results described in the next paragraph. When the Merger Agreement was signed, the Company was a shell company, with no operations and substantially no assets. The merger contemplated by the Merger Agreement is referred to as the “Merger.”

On August 13, 2012, the closing under the Merger Agreement took place and on October 5, 2012, Urban Spaces and Acquisition filed articles of merger with the Secretary of State of the State of Nevada, pursuant to which Acquisition was merged with and into Urban Spaces, with Urban Spaces being the surviving corporation and the wholly owned subsidiary of the Company. As a result of the Merger, the Company ceased to be a shell company. In connection with the Merger, the Company issued 2,000,000,000 shares of Common Stock to Oscar Brito, the sole holder of the common stock of Urban Spaces, who thereby became the Company’s controlling stockholder. Upon the closing of the Merger, Richard Astrom resigned as the Company’s sole director and president and Oscar Brito became the Company’s sole director and president.

Also in connection with the Merger:

| • | On August 13, 2012, the Company completed a private placement with 9 investors (the “Private Placement”) of 335,200,000 shares of Common Stock for proceeds of $36,396 in cash and payment for services valued at $3,604 under Securities Purchase Agreements. The price paid by each investor was 0.0001193317 per share. The Company also entered into Registration Rights Agreements with these investors, pursuant to which the Company filed a registration statement with the United States Securities and Exchange Commission (the “Commission”) under the Securities Act of 1933 (the “Securities Act”) relating to these shares on February 11, 2013, which was declared effective on May 15, 2013. | |

| • | Richard S. Astrom, the Company’s president and sole director, entered into an Exchange Agreement with the Company, under which 10,000,000 shares of Series A Preferred Stock owned by him and $170,146 of the Company’s indebtedness to him were exchanged for the proceeds of the Private Placement and a secured promissory note of the Company payable to him in the principal amount of $260,000 and bearing interest at the rate of 0.24% per annum. The promissory note was due August 13, 2013, is subject to acceleration in the event of certain events of default, contains certain restrictive covenants and is secured by a pledge of all of the shares of common stock of Urban Spaces. For information concerning this promissory note and the pledge, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Overview – Pledge of the Shares of the Company’s Operating Subsidiary,” on page 12, “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Overview – Pledge of Membership Interests in Urban Properties LLC” on page 13, and “Directors, Executive Officers and Corporate Governance – Related Party Transactions – Exchange Transaction” on page 31. |

| • | On October 31, 2012, the Company filed a certificate of amendment to its certificate of incorporation with the Secretary of State of the State of Delaware changing its corporate name from “Strata Capital Corporation.” to “Metrospaces, Inc.” | |

| • | Immediately prior to the Merger and the Private Placement, 33,334 shares of Common Stock were surrendered and canceled in satisfaction of a condition precedent set forth in the Merger Agreement, reducing the number of shares of Common Stock outstanding to 33,149. |

As a result of the Merger, we conduct the business described above under the caption “General” and below under the caption “Business” on page 3.

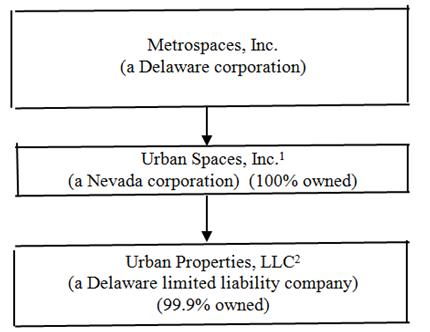

The Company’s corporate structure is as follows:

| 1. | All of the shares of Urban Spaces have been pledged to secure indebtedness of the Company. For further information respecting this indebtedness and this pledge, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Overview – Pledge of the Shares of the Company’s Operating Subsidiary,” on page 12. | |

| 2. | All of the interests of Urban Properties, LLC owned by Urban Spaces have been pledged to secure its indebtedness. For further information respecting this indebtedness and this pledge, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Overview – Pledge of Membership Interests in Urban Properties LLC,” on page 13. |

Business

Introduction

The Company is the parent of Urban Spaces. The Company has no material assets other than all of the outstanding shares of Urban Spaces. The Company has no plans to conduct any business activities other than obtaining or guaranteeing financing for the business conducted by Urban Spaces or assisting Urban Spaces and its local subsidiaries in obtaining such financing.

Through Urban Spaces and its subsidiaries, we acquire and develop land in urban areas primarily for the construction of condominiums on such land, principally in Latin American markets, and offer them at different prices and with varying levels of options and amenities to customers who are able to make substantial payments upon signing purchase agreements and at agreed times as construction progresses. For the foreseeable future, we do not expect our projects to exceed 25 units or to cost more than $5,000,000. Typically, a project will comprise several one- and two-bedroom units with areas from approximately 700 to 1,450 square feet and a few penthouse or luxury units of 3,200 or more square feet.

We do not provide financing to our customers and our target customer base will comprise persons who are able either to self-finance their purchases from us or obtain such financing. The source of substantially all of our revenue will be sales of these condominiums, although we may also obtain additional revenue from managing units that our customers acquire for rental. We do not have sufficient information as to the number of customers who will use these services and we have not yet determined the basis for our compensation for rendering these services; we believe that the aggregate amount that we receive for these services will not be material.

We state the purchase price for each condominium in U.S. dollars and purchasers will be required to make payments to us in that currency or in the local currency equivalent thereof on the date that the payment is made. Our intention in so doing is to reduce the effects on us of adverse currency fluctuations and devaluations, which are a risk if prices are denominated in local currency. On the other hand, we will not benefit from any strengthening of the U.S. dollar against the relevant local currency.

We may construct our projects alone or with joint venture partners. If we construct a project on a joint-venture basis, the joint venture partner will usually provide the land on which we will construct a building in exchange for an interest in the joint venture in the range of 15%-25%, depending principally upon the value of the land and the relative bargaining strength of the parties, and we will usually have responsibility for and management control over all other aspects of the project. Although we have less than a majority interest in the projects described below, it is not our intention to invest in the future in projects over which we will not have a majority interest and have management control.

We market directly with our own commissioned sales force, by personal contact by our officers, which will not involve additional compensation to them, through real estate brokers and agents and internet websites and manage these condominiums for customers who wish to lease them on a long- or short-term basis.

We are presently involved in projects in Argentina and Venezuela, which are at the stages described below. We are also considering projects in Colombia and Peru.

Projects

We have investments in the following projects:

Argentina

The Chacabuco Project

Chacabuco 1353 Caba Trust, an Argentinian trust (the “Trust”), is constructing a 26-unit condominium project at Chacabuco 1353, in Buenos Aires, Argentina. Estudio Peru, a Buenos Aires architectural firm that is not affiliated with the Company and its affiliates, designed and is acting as project manager for this project. Construction began in April 2010 and we have been advised that estimated cost of the project is $1,350,000. The building is approximately 95% complete. The construction was expected to be completed and the units delivered by the end of 2012, but has been delayed on several occasions owing to depleted inventories of building materials, transportation strikes that caused their late delivery, work stoppages due to governmental inspections and various other causes; in addition, work was stopped for about 6 weeks when the contractor for the project ceased performing due to labor problems and was replaced. The project is now scheduled to be completed by June 30, 2014.

GBS Capital Partners Inc., a Panamanian corporation (“GBS”), agreed to purchase substantially similar 9 loft-type efficiency units in this project specifically identified by apartment number, each having an area of 495 square feet, and advanced full payment for them to the Trust. GBS assigned its rights to receive these units to Urban Properties, LLC (“UPLLC”). In the instrument of assignment, UPLLC agreed to pay GBS $750,000 in consideration of its assignment and UPLLC. This amount was originally to be paid in installments of $400,000 and $350,000, due on April 15, 2013, and April 15, 2014, respectively. The dates for these payments were first extended to October 15, 2013, and October 15, 2014, respectively, because of delays in completion of this project. Due to further delays, they have been extended further to dates which are presently indeterminable, because they are based on the actual completion date; they are unlikely to fall before October 15, 2014, and October 15, 2015, respectively. Upon completion of the project, the Trust will deed these 9 loft-type units directly to UPLLC without action on the part of GBS. For further information concerning this assignment, including the circumstances and terms of the extension of the dates for payment of the two installments of said $750,000, see “Directors, Executive Officers and Corporate Governance – Related Party Transactions – GBS” on page 32.

The lot on which the building is being constructed is located in the San Telmo area of Buenos Aires, which is an area of that city popular with tourists and has a combination of upscale shops, restaurants, fine homes and condominiums, many of which are leased by their owners to tourists on a short-term basis. There are in San Telmo a number of projects similar to this project that have been completed or are in progress. The lot has an area of approximately 4,850 square feet, the 26 units have a total area of 12,900 square feet and the common areas in the project have an area of approximately 4,850 square feet. The structure has 7 floors. It common areas comprise parking, halls and stairways, a swimming pool, a social area with barbecues and a laundry room. The apartments include flooring, air conditioning and heating, a kitchen area with refrigerator, stove and cabinets and wireless internet service.

UPLLC has entered into contracts for the sale of 4 of the 9 units for a total of $360,000 and has received payments of approximately $80,000 under these contracts. When UPLLC has been deeded the remaining 5 units, it will initially offer them for sale at prices ranging from $94,000 to $96,000, depending principally on the floor on which they are located. Although our general target market for these units is as described above, we believe that some will be acquired by investors who will furnish them and re-lease them to tourists. To the extent that they are acquired by such investors, we will assist them in re-renting them.

We believe that we will receive approximately $825,000 from the sale of these units, which is $75,000 more than the $750,000 that we have invested, before deducting sales commissions (which will range from nothing, if we sell a unit through personal contact to 1% if we sell it through a broker), real property transfer taxes (1.5 to 2.5% of the sales price) and monthly costs, including maintenance fees and utilities, of approximately $150. However, until these units are sold, no assurance can be given as to the price that will be paid for a unit (which could be less than the price at which we initially plan to offer it for sale), the sales commissions that will be paid, the exact amount of transfer tax that will be paid or the monthly costs that will have accrued between the time that we receive a unit and the time of its sale. Accordingly, we cannot predict the profit or loss that will result from such sale.

For further information respecting GBS, the interest of our president in GBS, the acquisition by GBS of its right to these units and the terms of the payment of the $750,000 owed by UPLLC to GBS, see “Directors, Executive Officers and Corporate Governance – Related Party Transactions – GBS” on page 32.

Venezuela

The Los Naranjos 320 Project

This project (the “Las Naranjos 320 Project”), which we promote and manage, is located at Los Naranjos de Las Mercedes, Lot 320, in Caracas Venezuela. The project manager is Guillermo Mendez, a civil engineer, with offices in Caracas who has overseen the construction of over 100,000 square feet. The lot on which the project is located is in a neighborhood populated by upper middle-class families, mainly comprising. Individually gated homes. A number of lots in this community are being purchased with a view to demolishing the existing structures and building condominiums.

The building will have 9 units on 4 floors, as follows: (i) one 1-bedroom unit, with an area of 720 square feet, (ii) six 2-bedroom units, with areas between 890 and 1,290 square feet, (iii) two 3-bedroom penthouse units, with areas of 1,450 and 2,150 square feet. The total area of these 9 units is approximately 11,800 square feet and the project has approximately 7,500 square feet of common areas, including a lobby, hallways and staircases, parking and a roof-top social area.

The lot on which the project is located has an area of 6,460 square feet and is owned by Promotora Alon-Bell, C.A., a Venezuelan corporation (“Alon-Bell”), all of whose outstanding shares are held by GBS Real Estate Fund I, LLC, a Florida limited liability company (“GBS Fund”), which was formed in March 2013 solely for the purpose of obtaining financing for and developing this project. GBS is the managing member. GBS Fund acquired these shares and we acquired an interest in GBS Fund as follows:

| • | On February 10, 2012, Oscar Brito entered into a contract with the holders of all of the outstanding shares of Alon-Bell (the “Alon-Bell Contact”), which holds legal title to the land, for the acquisition of these shares for the purchase price in local currency that was equivalent to $520,000. These holders are unrelated to the Company and its affiliates. | |

| • | Mr. Brito personally paid $150,000 to these stockholders in installments over the next several months. | |

| • | On April 20, 2012, Mr. Brito assigned his interest under the contract to UPLLC in exchange for a promissory note payable to him in the principal amount of $150,000. This promissory note is due on April 20, 2015, and will accrue interest at the rate of 11% per annum. | |

| • | GBS Fund raised $420,000 from investors, of which $370,000 was used to pay these stockholders the balance due under the contract and $50,000 was used to defray architectural fees, demolition and construction permits and other preliminary expenses. UPLLC entered into a subscription agreement with GBS Fund to acquire for $150,000 membership interests in GBS Fund, which is one of these investors, for $150,000, representing an interest of 26.31% therein. | |

| • | On December 3, 2012, UPLLC satisfied its obligation under its subscription agreement with GBS Fund by assigning its rights under the Alon-Bell Contract to GBS Fund in lieu of the payment of cash and received in exchange the aforesaid membership interests. | |

| • | The shares of Alon-Bell were registered in the name of GBS Fund on December 16, 2012. |

GBS Fund was formed on February 14, 2012, for the sole purpose of acquiring the shares of Alon-Bell, obtaining funds for the development of this project and constructing and selling units in the project upon its completion. It has and the Company has been advised that it does not intend to have other operations. The persons from whom GBS Fund acquired the Alon-Bell shares are unrelated to it, GBS Fund or Mr. Brito and his affiliates.

Although we expected to qualify GBS Fund to do business in Venezuela in order that it could act as the developer of this project, this process was delayed because of the slowdown in the provision of government services because of continuing political unrest in Venezuela. As a result, we decided not to liquidate Alon-Bell and are now using it as the developer of the project. In connection with this decision, GBS Fund, Propietaria Alimentos Globalia C.A. (“PAGCA”), which is the obligor under a bank loan to finance this project to which we are not a signatory in the principal amount of $1,000,000, to be drawn down as the project reaches prescribed benchmarks, of which $400,000 has been received, and Alon-Bell entered into a joint venture agreement. Under this agreement, PAGCA owns the property on which the project is to be built, and will receive 20% of gross sales of units. Alon-Bell, will act as the promoter and builder and will receive 15% of gross sales, GBS Fund will receive the remaining 65% of gross sales, which will be divided such that we receive 26% of gross sales and GBS Fund will retain the rest, subject to change in the event of future equity investments.

We may make further investments in, and provide management, promotional and other services to, GBS Fund; as a result our interest in GBS Fund could increase.

The total cost of this project is expected to be approximately $1,900,000. As indicated above, as of December 31, 2013, approximately $900,000 had been invested in this project, approximately $520,000 of which was spent for the shares of Alon-Bell, which owns the land on which the project will be constructed, and the remainder for the expenses described above. We have presold the 1,450-square-foot penthouse unit for $400,000 and the remaining cost of the project is being financed by the above mentioned bank loan.

Construction on this project began in August 2013 and we expect that it will be completed by February 2014. However, for the reasons set forth under the caption “Delays in the Las Naranjas 320 Project and the Las Naranjas 450 Project Due to Political and Other Conditions in Venezuela,” below, this project may not be completed by that date.

As indicated above, one of the penthouse units has been presold. Other units are expected to be sold as the project progresses. The total list price for all of the units is expected to be approximately $3,500,000, but no assurance can be given that it will be possible to sell them at prices that will aggregate this amount.

Las Naranjos 450 Project

This project (the “Los Naranjos 450 Project”), which we promote and manage, is in its planning stage. The project manager is Guillermo Mendez, who is the project manager of the Las Naranjos 320 Project. The project is located at Los Naranjos de Las Mercedes, Lot 450, in Caracas, Venezuela, in the same neighborhood and a few blocks away from the Las Naranjos 320 Project. This land, which is valued at $700,000 and has an area of approximately 7,500 square feet, is owned by LM 1109, C.A., an unrelated entity (“LM1109”). The sole stockholder of LM1109, Carlos Artiles, a Venezuelan architect, will serve as project manager without additional compensation and we expect to enter into an agreement with Sr. Artiles under which we will receive 70% of the shares in LM1109 in consideration of our investing in and obtaining funding for the project as described below. It is expected that permits will be obtained by June 2014 and that construction will begin as soon as possible thereafter. However, because there have been delays in finishing the architecture for the project and for the reasons set forth below under the caption “Delays in the Las Naranjas 320 Project and the Las Naranjas 450 Project Due to Political and Other Conditions in Venezuela,” we can give no assurance that these permits will be obtained when expected, when construction will commence and when the project will be completed.

This project will have 9 units, from 1 to 3 bedrooms having areas from 915 to 2,150 square feet; the number of units or each size has not been determined. The total area of these 9 units will be approximately 11,800 square feet and the project will have approximately 8,600 square feet of common areas, including a lobby, hallways and staircases, parking and social areas.

The total list price for all of the units is expected to be approximately $4,500,000, but no assurance can be given that it will be possible to sell them at prices that will aggregate this amount.

The total cost of this project, exclusive of land, is expected to be approximately $1,300,000, which is expected to be financed approximately as follows:

| • | Preconstruction and precompletion sales of $300,000. We intend to pre-sell one or a few units as soon as possible after we have obtained construction permits and others as necessary during construction to provide funds. | |

| • | A loan or loans of $500,000 from one or more local lenders, on terms to be negotiated. We have not yet identified a lender, but expect to complete a loan by the end of the second quarter of 2013. | |

| • | Further cash investments of $500,000 in the Venezuelan entity, which we will make from time to time as construction proceeds. These funds will be provided from amounts that we will raise to meet our capital needs. For further information as to our capital needs and our prospects for satisfying them, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources” on page 14. We can give no assurance as to when or whether we will be able to obtain the amounts that we plan to invest in this project. |

Delays in the Las Naranjas 320 Project and the Las Naranjas 450 Project Due to Political and Other Conditions in Venezuela

The death of Hugo Chavez, President of Venezuela, in March 2013, the ensuing political campaign for the election of his successor and recent civil unrest and political demonstrations have affected businesses generally in Venezuela because they have resulted in delays in governmental administrative processes and have materially slowed the conduct of business. Another result is that we have encountered delays in procuring construction materials. Accordingly, we may not complete the Los Naranjas 320 and Las Naranjas 450 Projects on schedule. We expect the civil unrest and political demonstrations to continue indefinitely.

Marketing and Sales

Our potential customers are highly liquid persons or persons who have the ability to borrow, such that, in either case, they will be able to make a substantial payment to us when they sign a contract for the purchase of a unit, make progress payments at prescribed points specified in the contract and make the final payment due upon delivery of the unit. We plan to market through brokers, by personal contact by members of our management and through websites. We do not plan to have a permanent sales staff or, except when brokers hold “open houses,” to have sales personnel located at our projects.

Legally, the process of creating and selling condominiums in Latin American countries is similar to that in the United States. Condominium units and common areas in a building and the land on which it is situated are created by a legal instrument pursuant to a statute. This instrument will also provide for the governance of the property, typically, by a board of directors appointed by the entity that constructs the project until it is sold or nearly sold and thereafter elected by the owners of the units. This board of directors will adopt rules and regulations to which the owners of units and the use of common areas are subject.

When a customer decides to purchase a condominium, he will enter into a contract of purchase and sale, the contents of which will vary in accordance with the unit and project of which it is a part and the applicable provisions of law respecting condominiums and real property generally under the laws of the country in which it is constructed. This agreement will describe the unit to be purchased; the price for the unit; the specifications for the unit and the options and amenities to be included with it; the initial, progress and final payments and, in the case of progress payments, the times at or the milestones upon the occurrence of which they are to be made; the delivery date for the unit and the reasons, such as labor disruptions and unforeseeable events, for which it may be deferred without liability; the warranties, if any, that will be given to the purchaser with respect to the property that he is purchasing, which may be additional to those given to the purchaser in the deed for the property and to those mandated by law; an escalator clause for labor and material costs, where lawful; the rights of the parties to terminate the contract and the remedies of the parties; and other matters that the parties deem desirable or are customary. When the construction of the unit and the property is completed, we will deliver a deed to the customer upon the completion of the payment of the purchase price.

Project Management

We will develop each project through an entity established for that purpose. Rather than have an internal project management staff, once we have acquired the land on which a project will be constructed (either directly or through a joint venture partner), we will retain the services of a local engineer, architect or other person with expertise in overseeing construction projects, who will manage the project and who will receive as compensation a nominal salary and approximately 8% to 10% of the profits of the project. Through him, the local entity will enter into contracts for the construction of the building and its adjacent areas and landscaping; hire labor, to the extent not provided under construction contracts; purchase materials, to the extent not purchased under construction contracts; retain the services of local real estate brokers and arrange for advertising; and contract for other goods and services required to complete the project. He will be responsible for assuring that the project is completed on time, in accordance with its specifications and within its prescribed cost.

Construction Materials

We believe that the materials required for construction of our products will for the most part be readily available in local markets and that, in most cases, they will be locally produced. At present, we believe that it will be possible to acquire imported materials to the extent necessary, at higher cost than local materials. Nevertheless, it is possible that the supply of such materials may be disrupted, as has occurred in Venezuela due to political unrest (see “Delays in the Las Naranjas 320 Project and the Las Naranjas 450 Project Due to Political and Other Conditions in Venezuela,” above, or that their cost may rise. We intend to provide in each contract for the purchase of a unit for escalation in its price in the event that the cost of materials increases above a prescribed level during the period from the signing of a contract of purchase for a unit to its delivery in countries, including Argentina, where such a provision is legally permissible. In countries, including Venezuela, where such a provision is not legally permissible, we will estimate increases in such costs over such period and take this estimate into account in establishing the contract price for the unit, but we can give no assurance that we will be able to make such estimate accurately or be aware of all existing or future factors that might affect such costs. Our failure accurately to make such estimate could adversely our profit on the unit or could even result in a loss.

Labor

We believe that labor for construction of our products will be readily available. Labor disruptions as a result of strikes or political demonstrations occur more often in Latin America than in the United States and are occurring with increasing frequency in Venezuela (see “Delays in the Las Naranjas 320 Project and the Las Naranjas 450 Project Due to Political and Other Conditions in Venezuela,” on page 7). We intend to provide in each contract for the purchase of a unit for escalation in its price in the event that labor costs increase above a prescribed level during the period from the signing of a contract of purchase for a unit to its delivery in countries, including Argentina, where such a provision is legally permissible. In countries such as Venezuela, where such a provision is not legally permissible, we will estimate increases in labor costs over such period and take this estimate into account in establishing the contract price for the unit, but we can give no assurance that we will be able to make such estimate accurately or be aware of all existing or future factors that might affect such costs. Our failure accurately to make such estimate could adversely our profit on the unit or could even result in a loss.

Warranty

The laws of Argentina and Venezuela impose liability for defective construction of a building on the person or entity that built it and the architect or engineer that designed it; the seller is liable on if it also had acted in one of those capacities. Accordingly, since we plan to enter into construction contracts with third parties for the buildings that will contain the condominiums that we will sell, we will not be liable to our customers for construction defects in those countries. We will have the opportunity to inspect buildings before we accept them and to require the builder to repair defects. Nevertheless, we will absorb the costs of repairing minor defects, such as uneven plastering, poorly hung doors and improperly aligned cabinets, that escape our preacceptance inspection. We do not expect these costs to be material.

In the event that we construct buildings in jurisdictions in which such liability is imposed on sellers of real property, we plan to limit our liability contractually and will consider the possible cost of such imposition of liability in setting prices for our condominiums.

Latin American countries impose statutory warranties of title on sellers of real property; we do not believe that we will have liabilities thereunder.

Competition

We compete primarily in the luxury condominium segment of the condominium industry on the basis of location, price, quality, reputation, design, amenities, and our customers’ overall sales and homeownership experiences. The condominium industry in the markets in which we operate or intend to conduct operations is fragmented and highly competitive. We do not believe that any of our competitors in these areas has as much as 5% of the number or value of the condominiums constructed in these markets. In each of these markets, there are numerous builders of condominiums with which we will compete and our market share is expected to be less than 1% of the units built or the value of the units sold. We will also compete with sales of existing housing inventory, and any provider of housing units, for sale or for rent, including apartment operators and businesses that convert apartments into condominiums, may be considered a competitor.

Seasonality

In countries that lie near the Equator, such as Venezuela, where temperatures are nearly constant, we do not expect that our construction operations or sales will be materially impacted by seasonality. In countries where there are greater changes of temperature during a year, we expect that both our construction activities and sales will occur at a slower place during the colder portions of the year than they will during the warmer portions.

Regulation

Our operations are subject to regulations imposed and enforced by various governmental authorities. These regulations may be complex and include building codes, land zoning and similar restrictions, health and safety regulations, labor practices, marketing and sales practices, environmental regulations and various other laws, rules, and regulations. Collectively, these regulations have a significant impact on the site selection and development of our properties, our designs and construction techniques, our relationships with customers, employees, and suppliers/subcontractors, and other aspects of our business. The applicable governing authorities frequently have broad discretion in administering these regulations, including inspections of condominiums prior to their delivery to customers.

In the United States, our only operations will be obtaining financing for our foreign projects. As such, we will be subject to state and federal securities laws if we issue securities in connection with such financing. We are also required by Section 15(d) of the Exchange Act to file periodic reports with the SEC, including an annual report containing audited financial statements. We will also be required to file Federal and State tax returns. The costs associated with these matters and the amount of time expended by management in connection therewith may be material.

In the foreign counties where we have projects, our most significant regulatory burden is obtaining construction permits. Generally, construction permits (including requisite environmental permissions) are routinely granted in 90 to 120 days, provided that sufficiently detailed plans and other documents necessary to support the issuance of the permit are submitted. However, permitting processes have moved substantially more slowly in Venezuela (see “Delays in the Las Naranjas 320 Project and the Las Naranjas 450 Project Due to Political and Other Conditions in Venezuela” on page 7). While the cost of obtaining these permits is not expected to be material, there is a material amount of management time involved in obtaining them. Environmental laws are not as fully developed in these countries as they are in the United States and we do not expect to expend material amounts in connection with complying with them or to experience delays as a result of them. We will also be required to file tax returns in these countries, but do not expect to incur material costs in connection with doing so.

In addition to existing regulations, more stringent requirements could be imposed in the future, thereby increasing the cost of compliance and potentially adversely affecting our profitability.

Employees

We have 1 employee, namely, the Company’s president. While we intend to hire other employees, we intend, as indicated above under “Project Management,” to manage our projects through independent project managers and not to hire an internal sales staff. A project manager will typically receive a fee of approximately 7% of construction costs, including the costs of materials and labor.

ITEM 1A. RISK FACTORS

We are a smaller reporting company as defined by Rule 12b-2 of the Exchange Act and are not required to provide information under this item.

ITEM 1B. UNRESOLVED STAFF COMMENTS

As we are not an accelerated filer or a large accelerated filer, as defined in Rule 12b-2 of the Exchange Act, or a well-known seasoned issuer, as defined in Rule 405 promulgated under the Securities Act, we are not required to provide information under this item.

ITEM 2. PROPERTIES

We have offices at 888 Brickell Key Drive, Unit 1102, Miami, FL 33131. We do not have a lease and we do not pay rent for the leased space. Except as described above under the caption “Business – Projects” we do not own, lease or have an interest in any properties.

ITEM 3. LEGAL PROCEEDINGS

We are not a party to any pending legal proceedings nor are any of our property the subject of any pending legal proceedings.

ITEM 4. (REMOVED AND RESERVED).

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock is quoted on the OTCQB tier maintained by OTC Markets Inc. under the symbol “MSPC.”

The following table reflects the high and low closing bid information for our common stock for each fiscal quarter during the fiscal years ended December 31, 2013 and 2012. The bid information was obtained from the OTC Markets, Inc. and reflects prices between dealers, without retail mark-up, markdown or commission, and may not represent actual transactions.

| Quarter Ended | Closing Bid High | Closing Bid Low | ||||||

| Fiscal Year 2013* | ||||||||

| December 31, 2013 | $ | 0.003 | $ | 0.004 | ||||

| September 30, 2013 | $ | 0.08 | $ | 0.021 | ||||

| June 30, 2013 | $ | 0.10 | $ | 0.08 | ||||

| March 31, 2013 | $ | ---- | $ | ---- | ||||

| Fiscal Year 2012 | ||||||||

| December 31, 2012 | $ | 0.08 | $ | 0.10 | ||||

| September 30, 2012 | $ | 0.08 | $ | 0.12 | ||||

| June 30, 2012 | $ | 0.10 | $ | 0.12 | ||||

| April 30, 2012 | $ | 0.12 | $ | 0.12 | ||||

Until the quarter beginning September 1, 2013, following the consummation of the Merger and the effectiveness of a registration statement filed under the Securities Act respecting 335,200,000 shares of common stock held by certain of our stockholders, trading in our common stock was sporadic and the amounts of shares traded were very small. We do not believe that the information provided in the table above for periods prior to that quarter reflect the value or the prospects of the Company as it now exists.

As of December 31, 2013, there were 64 holders of record of our common stock.

We have never declared or paid cash dividends on our capital stock. We currently intend to retain all available funds and any future earnings for use in the operation and expansion of our business and do not anticipate paying any cash dividends in the foreseeable future.

Recent Sales of Unregistered Securities.

Following the consummation of the Merger on October 5, 2012, the Registrant issued 2,000,000,000 shares of Common Stock to the former holder of the common stock of Urban Spaces as merger consideration under the Merger Agreement. On August 10, 2012, the Registrant entered into Securities Purchase Agreements with 9 separate investors, who are the selling stockholders under this Registration Statement, pursuant to which the Registrant issued collectively 335,200,000 shares of the Common Stock at the price of $0.0001193315 per share for an aggregate purchase price of $40,000.

The shares of Common Stock issued in the above transactions were exempt from registration under Section 4(2) of the Securities Act as sales by an issuer not involving a public offering and under Regulation D promulgated under the Securities Act. These shares of Common Stock were not registered under the Securities Act, or the securities laws of any state, and were offered and sold in reliance on the exemption from registration afforded by Section 4(2) and Regulation D (Rule 506) under the Securities Act and corresponding provisions of state securities laws, which exempts transactions by an issuer not involving any public offering. Such securities were subsequently registered under a registration statement filed with the Commission on February 11, 2013, and declared effective on May 15, 2013. In addition, on February 19, 2014, the Company issued 230,000,000 shares of Common Stock to investors who were not affiliates upon conversion of $107,640 of the principal amount of a convertible promissory note dated as of February 19, 2014, pursuant to the exemption from registration afforded by Rule 144 promulgated under the Securities Act. For further information about this Convertible Promissory Note, see “Directors, Executive Officers and Corporate Governance – Related Party Transactions – Exchange Transaction – Promissory Note,” on page 31.

ITEM 6. SELECTED FINANCIAL DATA

We are a smaller reporting company as defined by Rule 12b-2 of the Exchange Act and are not required to provide information under this item.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

The financial data discussed below are derived from the audited consolidated financial statements of the Company as at December 31, 2013, which were prepared and presented in accordance with generally accepted United States accounting principles. These financial data are only a summary and should be read in conjunction with the financial statements and related notes contained elsewhere herein, which more fully present our financial condition and operations as at that date. We do not believe that the results set forth in these consolidated financial statements are necessarily indicative of our future performance. This section and other parts of this report contain forward-looking statements that involve risks and uncertainties. Our actual results may differ significantly from the results discussed in the forward-looking statements.

Overview

The Company is a development stage company and there is substantial doubt about our ability to continue as a going concern because we will need a substantial amount of additional capital to continue our operations. No assurance can be given that any additional capital can be obtained or, if obtained, will be adequate to meet our needs. If adequate capital cannot be obtained on a timely basis and on satisfactory terms, our operations would be materially negatively impacted or we could be forced to terminate operating. In addition, the following matters may affect our ability to continue as a going concern:

Pledge of the Shares of the Company’s Operating Subsidiary.

The Company has pledged the shares of its operating subsidiary, Urban Spaces, for the payment of a promissory note in the principal amount of $260,000, which is due in full on February 19, 2015. The Company is presently unable to repay this promissory note and, unless it is able to develop sufficient revenues and/or obtain sufficient financing, it will be unable to repay the promissory note when due. In that event, the lender could foreclose on and sell the shares of Urban Spaces, through which we conduct all of our operations, in order to satisfy, as a whole or in part, the indebtedness outstanding under this promissory note, with the result that the Company would be left with no operations and the stockholders would lose all, or substantially all, of their investment. For further information on this convertible promissory note, the circumstances under which it was issued, the prior promissory note which was exchanged for it and the pledge, see “Directors, Executive Officers and Corporate Governance–Exchange Transaction–Promissory Note–Pledge Agreement” on page 31.

Pledge of Membership Interests in UPLLC.

As discussed more fully in “Business – Projects – Argentina – The Chacabuco Project” on page 4 and “Directors, Executive Officers, Promoters and Control Persons – Related Party Transactions – GBS” on page 32, was assigned the right to receive 9 condominium units from GBS in exchange for the agreement of UPLLC to pay $750,000 to GBS. We hold 99.9% of the membership interests in UPLLC through Urban Spaces. Urban Spaces pledged these membership interests to GBS as security for the payment of this indebtedness. If we were unable to repay these amounts, GBS could foreclose on these membership interests, as a result of which, we would lose our entire interest in UPLLC and in such assets as it then held, including any of the condominium units that were then unsold and any cash and other assets that UPLLC then held. The loss as a result of such foreclosure could be substantial. As more fully discussed under the caption “Directors, Executive Officers, Promoters and Control Persons – Related Party Transactions – GBS” on page 32, the Company’s president and sole director, who is also the president and sole director of its subsidiary, Urban Spaces, and the managing member of its subsidiary, UPLLC, is the holder of one-third of the shares of GBS and will therefore share in any profits arising from its assignment to UPLLC of the right to receive these units.

Urban Spaces owns, directly or indirectly, substantially all of our assets and UPLLC owns a substantial portion of our assets. In the event that lenders were to foreclose on the shares of Urban Spaces and/or the membership units in UPLLC, the effect would be immediate and adverse; in the former case, it is unlikely that we could continue to operate.

RESULTS OF OPERATIONS

FISCAL YEAR ENDED DECEMBER 31, 2013 COMPARED TO

FISCAL YEAR ENDED DECEMBER 31, 2012

Revenues

Revenues for the full year ended December 31, 2013 (“FY 2013”) were $0.00 compared to $0.00 for the partial year beginning April 3, 2012, when the Company commenced business, and ending December 31, 2012 (“FY 2012”).

Operating Expenses

Operating expenses for FY 2013 were $42,811, compared to operating expenses of $21,891 for FY 2012. Operating expenses increased for FY 2013 over FY 2012, primarily due to increased audit costs, administrative expenses and the costs of being a public company. The sole component of our operating expenses during both FY 2013 and FY 2012 was general and administrative expenses. Of these expenses, $15,000 was for salary in FY 2013 and in FY 2012, $11,250 was for salary.

Income (Loss) from Operations

We had an operating loss of $98,306 for FY 2013, as compared to an operating loss of $73,277 for FY 2012. The loss was higher for FY 2013, as compared to FY 2012, for the reason that operating expenses were higher for FY 2013, as stated above.

Net Income (Loss) Applicable To Common Stock

Net loss from operations applicable to common stock for FY 2013, was $98,306, compared to net loss from operations of $73,277 for FY 2012, for the reason that operating expenses were higher for FY 2013, as stated above.

LIQUIDITY AND CAPITAL RESOURCES

At December 31, 2013, and December 31, 2012, respectively, we had total assets of $848,173, of which $3,179 was cash, and $815,984, only a minimal amount of which was liquid. At those dates, we had stockholder deficits of $429,583 and $$331,277, respectively.

All assets are recorded at historical cost. Management reviews on an annual basis the book value, along with the prospective dismantlement, restoration, and abandonment costs and estimate residual value for the assets, in comparison to the carrying values on the financial statements.

Net Cash (Used in) Provided By Operating Activities

During FY 2013, cash used in operating activities was $19,770, compared to $5,141 during FY 2012.

Net Cash Used in Investing Activities

We did not utilize any cash in investing activities of continuing operations during the FY 2013 or FY 2012.

Net Cash (Used in) Provided by Financing Activities

During FY 2013, we received loans of $22,949, of which $12,949 was a loan from our chief executive officer, and in FY 2012, we received a loan of $5,141 from our chief executive officer.

At December 31, 2013, we had a stockholders’ deficit of $429,583. The report of our independent registered public accounting firm on our audited financial statements at December 31, 2013, contains a paragraph regarding doubt as to our ability to continue as a going concern. We do not have sufficient working capital to pay our operating costs for the next 12 months and we will require additional funds to pay our legal, accounting and other fees associated with our company and its filing obligations under federal securities laws, as well as to pay our other accounts payable generated in the ordinary course of our business.

The Company believes that it will require approximately $2,000,000 million to fund its operations for the next 12 months. The Company plans to fund its activities, including those of Urban Spaces, during the balance of 2014 and beyond through the sale of debt or equity securities, preconstruction sales of condominiums and/or deposits on condominium units sold after construction of a project commences but before these units are delivered. The ability of the Company to obtain funding from pension funds in Argentina has been restricted by the recent nationalization of the largest Argentine pension funds. The Company believes that it will be able to obtain funding for its projects from other private lenders, but can give no assurance that it will be successful in so doing or that such financing, if available, will be on acceptable terms.

In Latin American countries, the proceeds of these preconstruction sales and deposits are not held in escrow pending closing, but may be used freely. Most commonly, the Company will make a preconstruction sale of one or a few penthouse or luxury condominiums in a project at a discount of 15%-25% from their list price. This discount approximates the rate of interest that the Company would pay for borrowed money in these countries. Such preconstruction sales and deposits are respectively expected to provide approximately 10% to 25% of a project’s costs. We believe that we will receive approximately $650,000 from preconstruction sales and deposits from the Las Naranjas 320 Project and the Las Naranjas 450 Project over the next 12 months.

We believe that we will receive approximately $850,000 from the sale of the 9 condominium units which we are acquiring in the Chacabuco Project, which is $100,000 more than the $750,000 that we have invested. However, until these units are sold, no assurance can be given as to what amount we will receive from such sale and accordingly, the profit or loss that will result from such sale.

On August 13, 2012, the Company issued a promissory note payable to Richard S. Astrom in the principal amount of $260,000. This promissory note was due on August 13, 2013, bears interest at the rate of 0.24% per annum and is secured by a Pledge Agreement, dated as of August 13, 2012, between the Company and Mr. Astrom, under which the Company pledged the shares of Urban Spaces to Mr. Astrom. The maturity of the promissory note was extended to April 14, 2014, on August 12, 2013, and on February 19, 2014, the promissory note was exchanged for a convertible promissory note due February 19, 2015. Because of conversions of the principal amount of the convertible promissory note into shares of Common Stock, the principal amount has been reduced to $152,360. Further information respecting these matters is set forth under the caption “Directors, Executive Officers, Promoters and Control Persons – Related Party Transactions – Exchange Agreement” on page 31.

On April 13, 2012, UPLLC entered into an agreement with GBS under which GBS assigned to UPLLC the right to receive 9 condominium units being constructed in Buenos Aires and UPLLC agreed to pay $750,000 to GBS for these units. The obligation of UPLLC to pay GBS is secured by a Pledge Agreement, dated April 13, 2012, between Urban Spaces and GBS, under which Urban Spaces pledged its membership interests in UPLLC to GBS. Installments of $350,000 and $400,000 were due under this agreement on April 15, 2013, and April 15, 2014, respectively. Because the units were not timely delivered, the parties agreed that these dates would be extended to October 15, 2013, and 2014, respectively and that the new dates would be further extended by the number of days after May 30, 2013, that elapse until delivery. As of the date of this report, the units have not been delivered and the date on which these payments will be due is not ascertainable; if the units were delivered on May 30, 2014, for example, these payments would be due on October 15, 2014, and 2015, respectively. Further information respecting these matters is set forth under the caption “Directors, Executive Officers, Promoters and Control Persons – Related Party Transactions – GBS” on page 32.

While the Company is not in default under the above mentioned convertible promissory note or pledge agreement, it does not presently have funds available to pay the $152,360 outstanding under this note when due; likewise, while UPLLC is not in default under its obligation to pay $750,000 to GBS and Urban Spaces is not in default under the pledge agreement that it entered into with GBS, Urban Spaces does not presently have funds available to pay GBS when required to do so. The amount of the funds required for the Company to pay the promissory note to Mr. Astrom and for UPLLC to pay its obligation to GBS is included in the $2,000,000 that the Company will require to fund its operations for the next 12 months. The Company plans to obtain such funds through the sale of debt or equity securities and from any profits that it receives from the Chacabuco project, rather than from preconstruction sales of condominiums and/or deposits on condominium units sold after construction of its other projects commence but before these units are delivered. In the event that we are unable to pay Mr. Astrom or GBS when required to do so, we intend to ask for further extensions of due dates, but Mr. Astrom is not obligated to do so and GBS is obligated to do so only if and to the extent that the 9 units comprising the Chacabuco project continue to be undelivered. Further, the Company has no information as to whether or on what terms any such extension would be granted.

We can give no assurance that any of the funding described above will be available on acceptable terms, or available at all. If we are unable to raise funds in sufficient amount, when required or on acceptable terms, we may have to significantly reduce, or discontinue, our operations. To the extent that we raise additional funds by issuing equity securities or securities that are convertible into the Company’s equity securities, its stockholders may experience significant dilution.

Off-Balance Sheet Arrangements

None.

Risks and Uncertainties

We operate in an industry that is subject to rapid and sometimes unpredictable change. Our operations will be subject to significant risk and uncertainties, including financial, operational and other risks, including the risk of business failure. Further, as noted in this report, in order to develop its business, the Company will require substantial capital resources.

Critical Accounting Policies and Estimates

Use of Estimates

The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period.

Making estimates requires management to exercise significant judgment. It is at least reasonably possible that the estimate of the effect of a condition, situation or set of circumstances that existed at the date of the financial statements, which management considered in formulating its estimate, could change in the near term due to one or more future confirming events. Accordingly, the actual results could differ significantly from estimates.

Real Property

Real property is stated at cost less accumulated depreciation. Depreciation is provided for on a straight-line basis over the useful lives of the assets. Expenditures for additions and improvements are capitalized; repairs and maintenance are expensed as incurred.

Investments in non-consolidated subsidiaries

Investments in non-consolidated entities are accounted for using the equity method or cost basis depending upon the level of ownership and/or the Company's ability to exercise significant influence over the operating and financial policies of the investee. When the equity method is used, investments are recorded at original cost and adjusted periodically to recognize the Company's proportionate share of the investees' net income or losses after the date of investment. When net losses from an investment accounted for under the equity method exceed its carrying amount, the investment balance is reduced to zero and additional losses are not provided for. The Company resumes accounting for the investment under the equity method if the entity subsequently reports net income and the Company's share of that net income exceeds the share of net losses not recognized during the period the equity method was suspended. Investments are written down only when there is clear evidence that a decline in value that is other than temporary has occurred.

Impairment of Long Lived Assets

Long-lived assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset group may not be recoverable. If events or changes in circumstances indicate that the carrying amount of an asset group may not be recoverable, the Company compares the carrying amount of the asset group to future undiscounted net cash flows, excluding interest costs, expected to be generated by the asset group and their ultimate disposition. If the sum of the undiscounted cash flows is less than the carrying value, the impairment to be recognized is measured by the amount by which the carrying amount of the asset group exceeds the fair value of the asset group. Assets to be disposed of are reported at the lower of the carrying amount or fair value, less costs to sell.

JOBS Act

Section 102(b)(1) of the JOBS Act provides that, as an emerging growth company, the Company (A) need not present more than 2 years of audited financial statements in order for the Company’s registration statement with respect to an initial public offering of the Company’s common equity securities to be effective, and in any other registration statement that the Company files with the SEC, the Company need not present selected financial data prescribed by the Commission in its regulations for any period prior to the earliest audited period presented in connection with the Company’s initial public offering; and (B) may not be required to comply with any new or revised financial accounting standard until such date that a company that is not an issuer (as defined under section 2(a) of Sarbanes-Oxley is required to comply with such new or revised accounting standard, if such standard applies to companies that are not issuers. The term “issuer” generally means any person who issues or proposes to issue any security, the securities of which are registered under section 12 of the Exchange Act or that is required to file reports under section 15(d) of the Exchange Act, or that files or has filed a registration statement that has not yet become effective under the Securities Act and that it has not withdrawn.

While the Company is permitted to opt out of these provisions of the JOBS Act, it has not done so and do not intend to do so. As a result, our financial statements may not be comparable to companies that that elect to opt out of these provisions.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK.

We are a smaller reporting company as defined by Rule 12b-2 of the Exchange Act and are not required to provide information under this item.

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA.

| PAGE(S) | ||||

| Report of Independent Registered Public Accounting Firm | 19 | |||

| Balance Sheets as of December 31, 2013 and December 31, 2012 | 20 | |||

| Statements of Operations for the Year Ended December 31, 2013 and the periods from Inception to December 31, 2013 and 2012 | 21 | |||

| Statements of Cash Flows for the Year Ended December 31, 2013 and the periods from Inception to December 31, 2013 and 2012 | 22 | |||

| Statement of Changes in Stockholders’ Deficiency from Inception to December 31, 2013 | 23 | |||

| Notes to Financial Statements | 24-28 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

|

Paritz |

& Company, P.A |

15 Warren Street, Suite 25 Hackensack, New Jersey 07601 (201) 342-7753 Fax: (201) 342-7598 E-Mail: PARITZ@paritz.com |

| Certified Public Accountants | |||

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors

Metrospaces, Inc.

We have audited the accompanying consolidated balance sheet of Metrospaces, Inc.as of December 31, 2013 and 2012 and the related consolidated statements of operations, changes in stockholders’ deficiency and cash flows for the year ended December 31, 2013, the period April 3, 2012 (Inception) to December 31, 2012, and the period April 3, 2012 (Inception) to December 31, 2013. These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 3 to the financial statements, the Company has not generated any revenues since inception and has minimal cash on hand to meet its working capital and capital expenditure needs. In addition, the company had a stockholders’ deficiency of $429,583 as of December 31, 2013. These factors, among others, raise substantial doubt about the Company’s ability to continue as a going concern. The financial statements do not include any adjustments that might be necessary if the Company is unable to continue as a going concern.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Metrospaces, Inc. as of December 31, 2013 and 2012, and the results of its operations and cash flows for the year ended December 31, 2013, the period April 3, 2012 (Inception) to December 31, 2012, and the period April 3, 2012 (Inception) to December 31, 2013 in conformity with accepted accounting principles generally accepted in the United States of America.

/S/Paritz & Company, P.A.

Hackensack, New Jersey

April 15, 2014

METROSPACES, INC.

(A DEVELOPMENT STAGE COMPANY)

BALANCE SHEETS

AS AT DECEMBER 31, 2013 AND 2012

| 2013 | 2012 | |||||||

| ASSETS | ||||||||

| Advance payment for Real property | 665,984 | 665,984 | ||||||

| Investment in non-consolidated subsidiary | 150,000 | 150,000 | ||||||

| Cash | 3,179 | — | ||||||

| Prepaid expenses | 29,010 | — | ||||||

| Total assets | $ | 848,173 | $ | 815,984 | ||||

| LIABILITIES AND STOCKHOLDERS' DEFICIT | ||||||||

| Liabilities | ||||||||

| Long term debt related party, net of imputed interest of $23,808 and $45,005 | 742,852 | 704,995 | ||||||

| Notes payable -related parties | 426,090 | 413,141 | ||||||

| Note payable | 10,000 | |||||||

| Accrued expenses | 39,750 | 16,750 | ||||||

| Accrued interest - related party | 30,013 | 12,375 | ||||||

| Sales deposit | 29,051 | |||||||

| Total liabilities | 1,277,756 | 1,147,261 | ||||||

| STOCKHOLDERS' DEFICIENCY | ||||||||

| Preferred stock, $0.000001 par value, 2,000,000 shares authorized, no shares issued and outstanding | — | — | ||||||

| Common stock, $0.000001 par value, 5,000,000,000 shares authorized, 2,335,233,149 shares issued and outstanding | 2,335 | 2,335 | ||||||

| Additional paid in capital | 39,665 | 39,665 | ||||||

| Deficit accumulated during development stage | (471,583 | ) | (373,277 | ) | ||||

| TOTAL STOCKHOLDERS' DEFICIENCY | (429,583 | ) | (331,277 | ) | ||||

| TOTAL LIABILITIES AND STOCKHOLDERS' DEFICIENCY | 848,173 | 815,984 | ||||||

| The accompanying notes are an integral part of these financial statements | ||||||||

METROSPACES, INC.

(A DEVELOPMENT STAGE COMPANY)

STATEMENTS OF OPERATIONS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

| Year ended December 31, 2013 | From Inception (April 3, 2012) to December 31, 2012 | From Inception (April 3, 2012) to December 30, 2013 | ||||||||||

| OPERATING EXPENSES: | ||||||||||||

| General and administrative expenses | 42,811 | 21,891 | 64,702 | |||||||||

| Total operating expenses | 42,811 | 21,891 | 64,702 | |||||||||

| Interest expense - related parties | 55,495 | 51,386 | 106,881 | |||||||||

| NET LOSS | (98,306 | ) | (73,277 | ) | (171,583 | ) | ||||||

| BASIC AND DILUTED LOSS PER COMMON SHARE | $ | (0.00 | ) | $ | (0.00 | ) | ||||||

| WEIGHTED AVERAGE SHARES OUTSTANDING | 2,335,233,149 | 2,335,233,149 | ||||||||||

| The accompanying notes are an integral part of these financial statements | ||||||||||||

METROSPACES, INC.

(A

DEVELOPMENT STAGE COMPANY)