Attached files

| file | filename |

|---|---|

| 8-K - 8-K - MARKWEST ENERGY PARTNERS L P | a14-6934_18k.htm |

| EX-99.1 - EX-99.1 - MARKWEST ENERGY PARTNERS L P | a14-6934_1ex99d1.htm |

Exhibit 99.2

|

|

FOURTH QUARTER 2013 CONFERENCE CALL PRESENTATION FEBRUARY 27, 2014 |

|

|

Forward-Looking Statements This presentation contains forward-looking statements and information. These forward-looking statements, which in many instances can be identified by words like “could,” “may,” “will,” “should,” “expects,” “plans,” “project,” “anticipates,” “believes,” “planned,” “proposed,” “potential,” and other comparable words, regarding future or contemplated results, performance, transactions, or events, are based on MarkWest Energy Partners, L.P. (“MarkWest” and the “Partnership”) current information, expectations and beliefs, concerning future developments and their potential effects on MarkWest. Although MarkWest believes that the expectations reflected in the forward-looking statements are reasonable, it can give no assurance that such expectations will prove to be correct, and actual results, performance, distributions, events or transactions could vary significantly from those expressed or implied in such statements and are subject to a number of uncertainties and risks. Among the factors that could cause results to differ materially are those risks discussed in the periodic reports filed with the SEC, including MarkWest’s Annual Report on Form 10-K for the year ended December 31, 2013. You are urged to carefully review and consider the cautionary statements and other disclosures, including those under the heading “Risk Factors,” made in those documents. If any of the uncertainties or risks develop into actual events or occurrences, or if underlying assumptions prove incorrect, it could cause actual results to vary significantly from those expressed in the presentation, and MarkWest’s business, financial condition, or results of operations could be materially adversely affected. Key uncertainties and risks that may directly affect MarkWest’s performance, future growth, results of operations, and financial condition, include, but are not limited to: Fluctuations and volatility of natural gas, NGL products, and oil prices; A reduction in natural gas or refinery off-gas production which MarkWest gathers, transports, processes, and/or fractionates; A reduction in the demand for the products MarkWest produces and sells; Financial credit risks / failure of customers to satisfy payment or other obligations under MarkWest’s contracts; Effects of MarkWest’s debt and other financial obligations, access to capital, or its future financial or operational flexibility or liquidity; Construction, procurement, and regulatory risks in our development projects; Hurricanes, fires, and other natural and accidental events impacting MarkWest’s operations, and adequate insurance coverage; Terrorist attacks directed at MarkWest facilities or related facilities; Changes in and impacts of laws and regulations affecting MarkWest operations and risk management strategy; and Failure to integrate recent or future acquisitions. 2 |

|

|

Non-GAAP Measures Distributable Cash Flow, Adjusted EBITDA, and Net Operating Margin are not measures of performance calculated in accordance with GAAP, and should not be considered separately from or as a substitute for net income, income from operations, or cash flow as reflected in our financial statements. The GAAP measure most directly comparable to Distributable Cash Flow and Adjusted EBITDA is net income (loss). The GAAP measure most directly comparable to Net Operating Margin is income (loss) from operations. In general, we define DCF as net income (loss) adjusted for (i) depreciation, amortization, impairment, and other non-cash expense; (ii) amortization of deferred financing costs and discount; (iii) loss on redemption of debt net of current tax benefit; (iv) non-cash (earnings) loss from unconsolidated affiliates; (v) distributions from (contributions to) unconsolidated affiliates (net of affiliate growth capital expenditures); (vi) non-cash compensation expense; (vii) non-cash derivative activity; (viii) losses (gains) on the disposal of property, plant, and equipment (PP&E) and unconsolidated affiliates; (ix) provision for deferred income taxes; (x) cash adjustments for non-controlling interest in consolidated subsidiaries; (xi) revenue deferral adjustment; (xii) losses (gains) relating to other miscellaneous non-cash amounts affecting net income for the period; and (xiii) maintenance capital expenditures, net of joint venture partner contributions. We define Adjusted EBITDA as net income (loss) adjusted for (i) depreciation, amortization, impairment, and other non-cash expense; (ii) interest expense; (iii) amortization of deferred financing costs; (iv) loss on redemption of debt; (v) losses (gains) on the disposal of PP&E and unconsolidated affiliates; (vi) non-cash derivative activity; (vii) non-cash compensation expense; (viii) provision for income taxes; (ix) adjustments for cash flow from unconsolidated affiliates; (x) adjustment related to non-guarantor, consolidated subsidiaries; and (xi) losses (gains) relating to other miscellaneous non-cash amounts affecting net income for the period. We generally define Operating Income before Items Not Allocated to Segments as (i) revenue, excluding derivative gains and losses and adjusted for certain revenue deferral adjustments less; (ii) purchased product costs, excluding derivative gains and losses less; (iii) facility expenses, adjusted for certain non-cash items not allocated to segments and certain interest payments allocable to the segments less; ( iv) the portion allocable to non-controlling interests. Distributable Cash Flow is a financial performance measure used by management as a key component in the determination of cash distributions paid to unitholders. We believe distributable cash flow is an important financial measure for unitholders as an indicator of cash return on investment and to evaluate whether the Partnership is generating sufficient cash flow to support quarterly distributions. In addition, distributable cash flow is commonly used by the investment community because the market value of publicly traded partnerships is based, in part, on distributable cash flow and cash distributions paid to unitholders. Adjusted EBITDA is a financial performance measure used by management, industry analysts, investors, lenders, and rating agencies to assess the financial performance and operating results of the Partnership’s ongoing business operations. Additionally, we believe Adjusted EBITDA provides useful information to investors for trending, analyzing, and benchmarking our operating results from period to period as compared to other companies that may have different financing and capital structures. Net Operating Margin is a financial performance measure used by management and investors to evaluate the underlying baseline operating performance of our contractual arrangements. Management also uses Net Operating Margin to evaluate the Partnership’s financial performance for purposes of planning and forecasting. Please see the Appendix for reconciliations of Distributable Cash Flow, Adjusted EBITDA, and Net Operating Margin to the most directly comparable GAAP measure. 3 |

|

|

Fourth Quarter 2013: Financial Summary 4 Record total volume for fourth quarter and full year 2013 Total system volume of 3.2 Bcf/d for fourth quarter, an increase of 8% from the prior quarter. Total volume increased over 30% for full year 2013 vs. 2012 Marcellus total volume grew by 22% compared to prior quarter. Volume increased over 135% for full year 2013 vs. 2012 Utica total volume grew by 27% compared to prior quarter DCF for fourth quarter and full year 2013 DCF for fourth quarter was $127.2 million, an increase of 8% from the prior year quarter DCF for full year 2013 was a record $483.4 million, an increase of 17% from the full year 2012 Full year 2013 DCF was reduced by $27 million due to operational impacts during the second half of 2013. As of January 2014, all of these constraints have been resolved Increased fourth quarter distribution to 86 cents per common unit |

|

|

Fourth Quarter 2013: Operational Summary 5 19 major projects under development, which will increase our total processing capacity in the region to nearly 5 billion cubic feet per day and total fractionation capacity to over 400,000 barrels per day Completed eight new major projects Five processing facilities totaling 1 Bcf/d of new processing capacity in the Marcellus and Utica Shales Two fractionation facilities: 60,000 Bbl/d propane plus Hopedale fractionation facility to support producers in the Marcellus and Utica Shales 38,000 Bbl/d De-ethanization facility at Majorsville complex in the Marcellus Shale 200 MMcf/d Buffalo Creek processing plant in Granite Wash Announced three new major projects Executed amendments to agreements with Antero Resources for 200 MMcf/d of additional processing to be constructed at the Seneca processing facility in the Utica Shale 40,000 Bbl/d de-ethanization facility at Mobley complex in the Marcellus Shale Condensate stabilization solution in the Utica Shale |

|

|

Southwest Segment Overview Southwest continued to deliver strong financial results in Granite Wash, Haynesville Shale, Woodford Shale and Gulf Coast Total volumes increased 2% compared to the prior year quarter and declined 3% compared to prior quarter primarily due to planned Gulf Coast turnaround Processing capacity operated at approximately 86% utilization during the fourth quarter Commenced operations of 200 MMcf/d Buffalo Creek in Granite Wash to support Chesapeake Energy In early planning stages for additional plant in East Texas to support Haynesville rich-gas development ~20% Forecasted Increase from FY2013 to FY2014 2014 Avg. 6 |

|

|

Marcellus Segment Overview 7 MarkWest continues to achieve record volumes and operating income at five major complexes Continue to execute growth strategy and announced one new major project Segment operating income was $89.5m, an increase from the prior quarter of 10% Total volumes increased 22% from the prior quarter and over 135% for the full year 2013 versus full year 2012 Houston fractionation facility operated at full utilization Completed second 38,000 Bbl/d Marcellus De-ethanizer at Majorsville complex Constructed approximately 200 miles of gas and liquids pipeline in 2013 ~75% Forecasted Increase from FY2013 to FY2014 2014 Avg. |

|

|

Marcellus Segment Overview 8 Five complexes in Marcellus with over 2.2 Bcf/d of total processing capacity Added 600 MMcf/d of processing capacity during the quarter – new 200 MMcf/d plants at Majorsville, Mobley & Sherwood Total utilization of processing capacity was 63% during the fourth quarter 2013 Complex Capacity (MMcf/d) 4Q13 Avg. Volume (MMcf/d) Utilization (%) Houston 355 333 94 Majorsville 670 414 62 Mobley 520 248 48 Sherwood 600 325 54 Keystone 90 82 91 Total 2,235 1,402 63 |

|

|

9 MWE Gathering Area MWE NGL Pipelines MWE Marcellus Counties MWE Plants MWE Purity Ethane Pipeline MWE NGL/Purity Ethane Pipelines Under Construction Brooke Doddridge Marshall Ohio Ritchie Tyler Wetzel Allegheny Beaver Butler Greene Washington KEYSTONE COMPLEX MOBLEY COMPLEX SHERWOOD COMPLEX MarkWest’s Marcellus Producers Sunoco Mariner Pipeline ATEX Express Pipeline TEPPCO Product Pipeline HOUSTON COMPLEX MAJORSVILLE COMPLEX |

|

|

MarkWest Utica EMG’s Producers 10 MWE NGL Pipelines MWE Gathering Area MWE Purity Ethane Pipeline MWE NGL/Purity Ethane Pipelines Under Construction MWE Utica Counties MWE Plants CADIZ & SENECA COMPLEXES Belmont Guernsey Harrison Monroe Noble |

|

|

Utica Segment Overview 11 MarkWest Utica EMG continues to develop its full-service leading position in Ohio Total volumes increased by 27% compared to prior quarter Processing capacity operated at 43% utilization for the fourth quarter 2013. Over 50% of the capacity was brought into service during the quarter Recently announced two new major projects, including an additional processing plant at the Seneca complex and a condensate stabilization facility Constructed over 200 miles of gas and liquids pipeline in 2013 ~530% Forecasted Increase from FY2013 to FY2014 2014 Avg. |

|

|

Utica Condensate Solutions MarkWest and EMG will construct a condensate stabilization facility with associated logistics and storage terminal capabilities in Harrison County, Ohio The facility will provide condensate handling and stabilization services, and we are in active discussions with numerous Utica producers The facility will have initial stabilization capacity of 23,000 Bbl/d and is expected to be in service by the third quarter of 2014 Stabilizers will remove butanes and lighter NGLs from produced condensate in order to yield a higher value pentanes plus product 12 Hopedale Belmont Guernsey Harrison Monroe Noble Ohio |

|

|

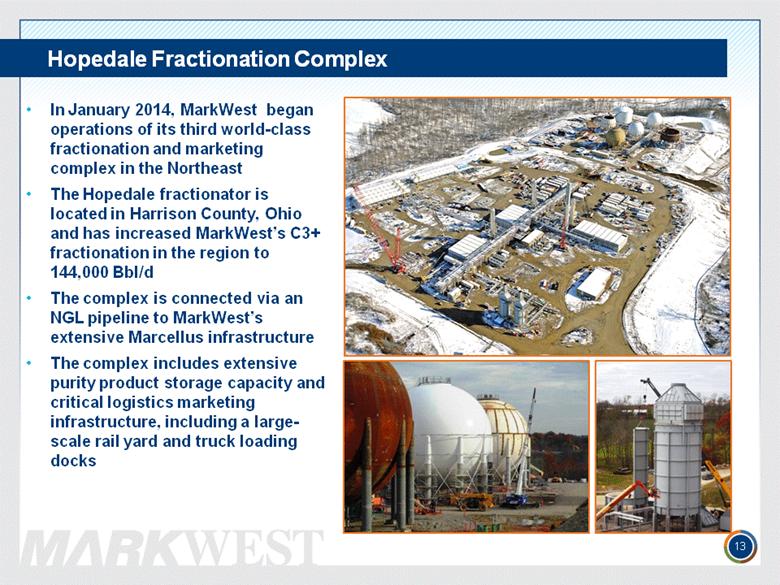

Hopedale Fractionation Complex In January 2014, MarkWest began operations of its third world-class fractionation and marketing complex in the Northeast The Hopedale fractionator is located in Harrison County, Ohio and has increased MarkWest’s C3+ fractionation in the region to 144,000 Bbl/d The complex is connected via an NGL pipeline to MarkWest’s extensive Marcellus infrastructure The complex includes extensive purity product storage capacity and critical logistics marketing infrastructure, including a large-scale rail yard and truck loading docks 13 |

|

|

MWE Complexes ATEX Express Pipeline MWE Purity Ethane Pipeline MWE NGL Pipelines MWE NGL/Purity Ethane Pipelines Under Construction UMTP Pipeline Sunoco Mariner Pipeline Virginia Michigan West Virginia Pennsylvania Gathering & Processing NGL Transportation & Marketing MWE Gathering Systems NGL Gathering & Fractionation Rich-Gas Areas Fully integrated NGL transportation, fractionation and logistics solutions in the Marcellus and Utica Shales Growing to over 400 MBbl/d of total C2+ fractionation capacity Integrated natural gas gathering systems 7 major processing complexes with current capacity of 2.8 Bcf/d. Growing to over 5 Bcf/d Access to all major NGL takeaway pipeline projects in the Northeast Access to Gulf Coast NGL markets through a proposed joint venture with Kinder Morgan TEPPCO Product Pipeline Gulf Coast Mobley Sherwood Keystone Seneca Lake Erie Mariner East Mariner West Utica Marcellus Texas Pipeline (UMTP) Marcellus & Utica: Full-Service Capabilities Houston Hopedale Cadiz Condensate JV 14 Ohio |

|

|

Total Volume Growth 15 Base case total volumes are forecasted to increase over 50% from 2013 42% 62% 52% |

|

|

MWE NGL Pipelines Barbour Brooke Doddridge Hancock Harrison Marion Marshall Monongalia Ohio Pleasants Preston Ritchie Taylor Tyler Wetzel Wood Belmont Carroll Columbiana Coshocton Guernsey Harrison Holmes Mahoning Medina Monroe Morgan Muskingum Noble Portage Stark Summit Trumbull Tuscarawas Washington Wayne Allegheny Armstrong Beaver Butler Clarion Crawford Fayette Greene Lawrence Mercer Venango Washington Westmoreland West Virginia Ohio MWE Utica Counties MWE Marcellus Counties MWE Plants ATEX Express Pipeline TEPPCO Product Pipeline Jefferson Marcellus & Utica: 23 Major Projects Complete Mariner Projects Rich Utica Rich Marcellus MWE Gathering Area 16 MWE Purity Ethane Pipeline 19 Major projects under construction HOUSTON COMPLEX Houston I – III – 355 MMcf/d – Complete Houston IV – 200 MMcf/d – 1Q15 C3+ Fractionation – 60,000 Bbl/d – Complete De-ethanization – 38,000 Bbl/d – Complete HOPEDALE FRACTIONATOR C3+ Fractionation – 60,000 Bbl/d – Complete MAJORSVILLE COMPLEX Majorsville I – III, V – 670 MMcf/d – Complete Majorsville IV – 200 MMcf/d – 2Q14 Majorsville VI – 200 MMcf/d – 2016 De-ethanization I – 38,000 Bbl/d – Complete De-ethanization II – 38,000 Bbl/d – TBD MOBLEY COMPLEX Mobley I – III – 520 MMcf/d – Complete Mobley IV – 200 MMcf/d – 4Q14 De-ethanization – 40,000 Bbl/d – 3Q15 SHERWOOD COMPLEX Sherwood I – III – 600 MMcf/d – Complete Sherwood IV – 200 MMcf/d – 3Q14 Sherwood V – 200 MMcf/d – 4Q14 De-ethanization – 38,000 Bbl/d – TBD MWE NGL/Purity Ethane Pipelines Under Construction UTICA CONDENSATE JV Stabilization Facility – 23,000 Bbl/d – 3Q14 CADIZ COMPLEX Cadiz I & Refrig – 185 MMcf/d – Complete Cadiz II – 200 MMcf/d – 3Q14 De-ethanization – 40,000 Bbl/d – 2Q14 SENECA COMPLEX Seneca I – II – 400 MMcf/d – Complete Seneca III – 200 MMcf/d – 2Q14 Seneca IV – 200 MMcf/d – 1Q15 De-ethanization – 38,000 Bbl/d – TBD KEYSTONE COMPLEX Bluestone I & Sarsen I – 90 MMcf/d – Complete Bluestone II – 120 MMcf/d – 2Q14 Bluestone III – 200 MMcf/d – TBD De-ethanization – 10,000 Bbl/d – 2Q14 C3+ Fractionation – 10,000 Bbl/d –2Q14 |

|

|

Liquidity 17 MarkWest preserves a strong balance sheet to fund growth As of today, we have $1 billion of liquidity to support our capital investment program As of December 31, 2013, our total Debt to Capital was 39%, interest coverage was 4.5 times and our leverage ratio was 4.5 times Maintain flexible financing options Funding of base capital requirements using a combination of long-term debt and equity $1.2 billion dollar revolving credit facility to support short-term funding needs Ability to maintain consistent access to the equity markets through our continuous equity program Enhancing financial flexibility through partnerships and joint ventures MarkWest has $1 billion of liquidity |

|

|

Increasing Fee-Based Income Note: Forecast Assumes Crude Oil ($/bbl) range of $97.26 to $89.47 and Natural Gas ($/mmbtu) range of $5.03 to $4.32 2014 fee-based net operating margin is forecasted to exceed 70% 18 Increase of ~3x since 2008 Over 70% 25% 39% 38% 38% 53% 61% |

|

|

Distributable Cash Flow: Sensitivity Table 19 MarkWest estimates the effect on DCF resulting from changes in volume forecast and NGL prices The Partnership has become less sensitive to changes in commodity prices as fee-based income has increased significantly (1) The composition is based on the Partnership’s projected barrel of approximately: Ethane: 35%, Propane: 35%, Iso-Butane: 6%, Normal Butane: 12%, Natural Gasoline: 12%. (2) Composite NGL prices is based on the Partnership’s average price. (3 Volume Forecast is increased/decreased by 10% in the Marcellus and Utica segments for the High and Low Cases. Volume Forecast (3) Composite NGL $/Gal (1) (2) Low Case Base Case High Case $1.05 $610 $662 $720 $1.00 $601 $652 $709 $0.95 $591 $642 $698 $0.90 $583 $633 $690 $0.85 $574 $624 $681 MarkWest is more sensitive to changes in volumes than changes in commodity prices |

|

|

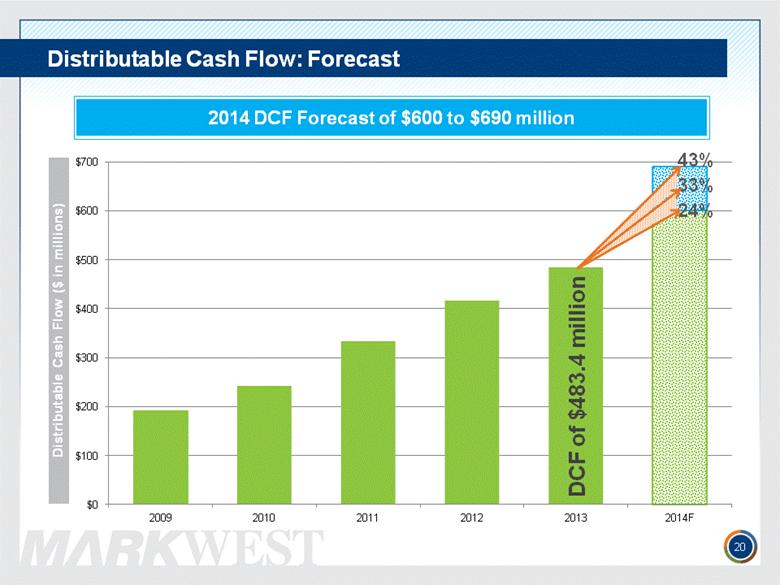

Distributable Cash Flow: Forecast 24% 33% 43% DCF of $483.4 million 2014 DCF Forecast of $600 to $690 million 20 |

|

|

2014 Capital Forecast 21 Utica 26% Southwest 7% Marcellus 67% 2014 Capital Forecast of $1.8 to $2.3 billion |

|

|

APPENDIX |

|

|

Reconciliation of DCF and Distribution Coverage 23 Year Ended Year Ended ($ in millions) 12/31/2012 12/31/2013 Net Income $ 217.0 $ 40.4 Depreciation, amortization, impairment, and other non-cash operating 237.6 365.7 expenses Loss (gain) on sale and or disposal of assets, net of tax benefit 6.3 (30.7) Loss on redemption of debt, net of tax benefit - 36.2 Amortization of deferred financing costs and discount 5.6 6.7 Non-cash earnings from unconsolidated affiliates (2.3) (1.4) Distributions from unconsolidated affiliates 8.4 6.4 Non-cash compensation expense 8.2 7.8 Non-cash derivative activity (102.1) 15.6 Provision for income tax –deferred 40.7 23.9 Cash adjustment for non-controlling interest of consolidated subsidiaries 2.3 6.1 Revenue deferral adjustment 7.4 7.2 Other 3.3 17.5 Maintenance capital expenditures, net of joint venture partner contributions (15.3) (18.0) Distributable cash flow (DCF) $ 417.1 $ 483.4 Total distributions declared for the period 370.3 490.6 Distribution coverage ratio (DCF / Total distributions declared) 1.13x 0.99x |

|

|

Reconciliation of Adjusted EBITDA 24 Includes derivative activity related to interest expense, amortization of deferred financing costs and discount, and excludes interest expense related to the Steam Methane Reformer. Year Ended Year Ended Year Ended ($ in millions) 12/31/2011 12/31/2012 12/31/2013 Net income $ 104.8 $ 217.0 $ 40.4 Non-cash compensation expense 3.4 8.2 7.8 Non-cash derivative activity (0.3) (102.1) 15.6 Interest expense (1) 109.9 117.1 150.1 Depreciation, amortization, impairments, 188.8 237.6 365.7 and other non-cash operating expenses Loss (gain) on sale and disposal of assets 8.8 6.2 (33.8) Loss on redemption of debt 79.0 - 38.5 Provision for income tax 13.7 38.3 12.7 Adjustment for cash flow from 4.2 6.1 4.9 unconsolidated affiliate Other 3.0 0.1 4.1 Adjusted EBITDA $ 515.3 $ 528.5 $ 606.0 (1) Includes derivative activity related to interest expense, amortization of deferred financing costs and discount, and excludes interest expense related to the Steam Methane Reformer. |

|

|

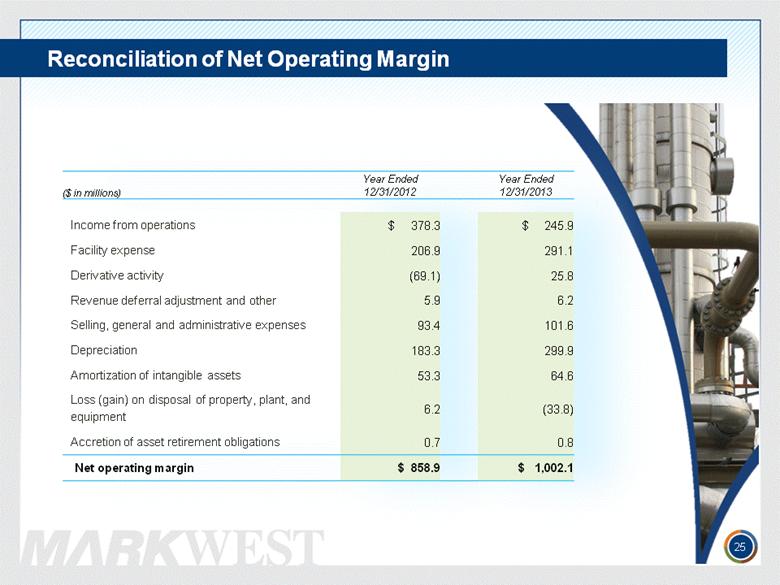

Reconciliation of Net Operating Margin 25 Year Ended Year Ended ($ in millions) 12/31/2012 12/31/2013 Income from operations $ 378.3 $ 245.9 Facility expense 206.9 291.1 Derivative activity (69.1) 25.8 Revenue deferral adjustment and other 5.9 6.2 Selling, general and administrative expenses 93.4 101.6 Depreciation 183.3 299.9 Amortization of intangible assets 53.3 64.6 Loss (gain) on disposal of property, plant, and 6.2 (33.8) equipment Accretion of asset retirement obligations 0.7 0.8 Net operating margin $ 858.9 $ 1,002.1 |

|

|

1515 Arapahoe Street Tower 1, Suite 1600 Denver, Colorado 80202 Phone: 303-925-9200 Investor Relations: 866-858-0482 Email: investorrelations@markwest.com Website: www.markwest.com |