Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - DIGITAL REALTY TRUST, INC. | d681377d8k.htm |

| EX-99.1 - EX-99.1 - DIGITAL REALTY TRUST, INC. | d681377dex991.htm |

Exhibit 99.2

Supplemental Operating and Financial Data

FOURTH QUARTER: DECEMBER 31, 2013

This Supplemental Operating and Financial Data package is not an offer to sell or solicitation to buy securities of Digital Realty Trust, Inc.

Any offers to sell or solicitations to buy securities of Digital Realty Trust, Inc. shall be made only by means of a prospectus approved for that purpose.

| Table of Contents |

|

Financial Supplement | ||

|

Fourth Quarter 2013 |

| PAGE | ||||

| Overview | ||||

| Corporate Information |

3 | |||

| Ownership Structure |

5 | |||

| Key Quarterly Financial Data |

6 | |||

| Consolidated Statements of Operations | ||||

| 2014 Guidance |

7 | |||

| Consolidated Quarterly Statements of Operations |

8 | |||

| Funds From Operations |

9 | |||

| Adjusted Funds From Operations |

10 | |||

| Balance Sheet | ||||

| Consolidated Balance Sheets |

11 | |||

| Components of Net Asset Value |

12 | |||

| Consolidated Debt Analysis and Global Revolving Credit Facility |

13 | |||

| Debt Maturities |

14 | |||

| Debt Analysis & Covenant Compliance |

15 | |||

| Internal Growth | ||||

| Same-Store Operating Trend Summary |

16 | |||

| Summary of Leasing Activity - Signed |

17 | |||

| Summary of Leasing Activity - Commenced |

18 | |||

| Lease Expirations and Lease Distribution |

19 | |||

| Lease Expirations - By Product Type |

20 | |||

| Top 20 Tenants by Annualized Rent |

21 | |||

| Portfolio Summary |

22 | |||

| Portfolio Overview by Product Type |

23 | |||

| Turn-Key Flex & Colocation Product Overview by Market |

24 | |||

| Occupancy Analysis |

25 | |||

| External Growth | ||||

| Development Lifecycle - Committed Active Development |

30 | |||

| Development Lifecycle - In Service |

31 | |||

| Construction in Projects in Progress - Total Investments |

32 | |||

| Historical Capital Expenditures Incurred and Paid |

33 | |||

| Development Lifecycle - Held for Development |

34 | |||

| Acquisitions |

35 | |||

| Unconsolidated Joint Ventures |

36 | |||

| External Growth Pipeline |

37 | |||

| Definitions | ||||

| Reconciliation of Earnings Before Interest, Taxes, Depreciation, and Amortization and Financial Ratios |

41 | |||

| Management Statements on Non-GAAP Supplemental Measures |

42 | |||

Page 2

| Corporate Information |

|

Financial Supplement | ||

|

Fourth Quarter 2013 |

Corporate Profile

Digital Realty Trust, Inc. owns, acquires, develops and manages technology-related real estate. The Company is focused on providing data center solutions for domestic and international tenants across a variety of industry verticals ranging from financial services, cloud and information technology services, to manufacturing, energy, healthcare, and consumer products. As of December 31, 2013, the Company’s 131 properties, including 12 properties held as investments in unconsolidated joint ventures, contain applications and operations critical to the day-to-day operations of technology industry and corporate enterprise data center tenants. Digital Realty’s portfolio is comprised of approximately 21.4 million square feet, excluding approximately 1.8 million square feet of space under active development and 1.3 million square feet of space held for future development, located throughout North America, Europe, Asia and Australia. For additional information, please visit the Company’s website at www.digitalrealty.com.

Corporate Headquarters

Four Embarcadero Center, Suite 3200

San Francisco, California 94111

Telephone: (415) 738-6500

Facsimile: (415) 738-6501

Website: www.digitalrealty.com

Senior Management

Michael F. Foust: Chief Executive Officer

A. William Stein: Chief Financial Officer and Chief Investment Officer

Scott E. Peterson: Chief Acquisitions Officer

Jim Smith: Chief Technology Officer

David J. Caron: Senior Vice President, Portfolio Management

Matthew Miszewski: Senior Vice President, Sales

Investor Relations

To request an Investor Relations package or to be added to our e-mail distribution list, please visit our website:

www.digitalrealty.com (Proceed to Information Request in the Investor Relations section)

Analyst Coverage

| Baird | Bank of America Merrill Lynch |

Barclays Capital | Canaccord Genuity | Cantor Fitzgerald | Citigroup | |||||

| Dave Rodgers | Stephen Douglas | Ross Smotrich | Greg Miller | David Toti | Michael Bilerman | |||||

| (216) 737-7341 | (646) 855-2615 | (212) 526-2306 | (212) 389-8128 | (212) 915-1219 | (212) 816-1383 | |||||

| Jeffery Spector | Charles Croson | Eric Z. Chu | Evan Smith | Emmanuel Korchman | ||||||

| (646) 855-1363 | (212) 526-7164 | (212) 389-8129 | (212) 915-1220 | (212) 816-1382 | ||||||

| Deutsche Bank | Evercore | Green Street | ISI | Jefferies | JMP Securities | |||||

| Vincent Chao | Johnathan Schildkraut | Michael Knott | Steve Sakwa | Omotayo Okusanya | Mitch Germain | |||||

| (212) 250-6799 | (212) 497-0864 | (949) 640-8780 | (212) 446-9462 | (212) 336-7076 | (212) 906-3546 | |||||

| Jeremy Metz | Robert Gutman | John Bejjani | George Auerbach | David Shamis | Peter Lunenburg | |||||

| (212) 250-4667 | (212) 497-0877 | (949) 640-8780 | (212) 446-9459 | (212) 284-1796 | (212) 906-3537 | |||||

| KeyBanc Capital | Macquarie | MLV & Co. | Morgan Stanley | Raymond James | RBC Capital Markets | |||||

| Jordan Sadler | Kevin Smithen | Jonathan M. Petersen | Vance Edelson | Paul D. Puryear | Jonathan Atkin | |||||

| (917) 368-2280 | (212) 231-0695 | (646) 556-9185 | (212) 761-0078 | (727) 567-2253 | (415) 633-8589 | |||||

| Austin Wurschmidt | Ryan Meliker | Landon Park | William A. Crow | Michael Carroll | ||||||

| (917) 368-2311 | (212) 542-5872 | (212) 761-6368 | (727) 567-2594 | (440) 715-2649 | ||||||

| Stifel Nicolaus | UBS | |||||||||

| Todd Weller | Ross Nussbaum | |||||||||

| (443) 224-1305 | (212) 713-2484 | |||||||||

| Ben Lowe | Gabriel Hilmoe | |||||||||

| (443) 224-1264 | (212) 713-3876 | |||||||||

This Supplemental Operating and Financial Data package supplements the information provided in our quarterly and annual reports filed with the Securities and Exchange Commission. Additional information about us and our properties is also available on our website www.digitalrealty.com.

Page 3

| Corporate Information (Continued) |

|

Financial Supplement | ||

|

Fourth Quarter 2013 |

Stock Listing Information

The stock of Digital Realty Trust, Inc. is traded primarily on the New York Stock Exchange under the following symbols:

| Common Stock: | DLR | |||

| Series E Preferred Stock: | DLRPRE | |||

| Series F Preferred Stock: | DLRPRF | |||

| Series G Preferred Stock: | DLRPRG |

Note that symbols may vary by stock quote provider.

Credit Ratings

| Standard & Poors | ||||

| Corporate Credit Rating: | BBB | (Negative Watch) | ||

| Preferred Stock: | BB+ |

| Moody’s | ||||

| Issuer Rating: | Baa2 | (Stable Outlook) | ||

| Preferred Stock: | Baa3 |

| Fitch | ||||

| Issuer Default Rating: | BBB | (Stable Outlook) | ||

| Preferred Stock: | BB+ |

These credit ratings may not reflect the potential impact of risks relating to the structure or trading of the Company’s securities and are provided solely for informational purposes. Credit ratings are not recommendations to buy, sell or hold any security, and may be revised or withdrawn at any time by the issuing organization at its sole discretion. The Company does not undertake any obligation to maintain the ratings or to advise of any change in ratings. Each agency’s rating should be evaluated independently of any other agency’s rating. An explanation of the significance of the ratings may be obtained from each of the rating agencies.

Common Stock Price Performance

The following summarizes recent activity of Digital Realty’s common stock (DLR):

| 31-Dec-13 | 30-Sep-13 | 30-Jun-13 | 31-Mar-13 | 31-Dec-12 | ||||||||||||||||

| High Price (1) |

$ | 58.35 | $ | 65.43 | $ | 74.00 | $ | 72.92 | $ | 70.16 | ||||||||||

| Low Price (1) |

$ | 43.04 | $ | 50.98 | $ | 56.02 | $ | 62.75 | $ | 59.25 | ||||||||||

| Closing Price, end of quarter (1) |

$ | 49.12 | $ | 53.10 | $ | 61.00 | $ | 66.91 | $ | 67.89 | ||||||||||

| Average daily trading volume (1) |

1,814,127 | 1,571,339 | 1,680,636 | 1,420,527 | 1,389,261 | |||||||||||||||

| Indicated dividend per common share (2) |

$ | 3.12 | $ | 3.12 | $ | 3.12 | $ | 3.12 | $ | 2.92 | ||||||||||

| Closing annual dividend yield, end of quarter |

6.4 | % | 5.9 | % | 5.1 | % | 4.7 | % | 4.3 | % | ||||||||||

| Shares and units outstanding, end of quarter (3) |

131,422,371 | 131,421,001 | 131,418,758 | 131,410,505 | 127,992,183 | |||||||||||||||

| Closing market value of shares and units outstanding (4) |

$ | 6,455,467 | $ | 6,978,455 | $ | 8,016,544 | $ | 8,792,677 | $ | 8,689,389 | ||||||||||

| (1) | New York Stock Exchange trades only. |

| (2) | On an annualized basis. |

| (3) | As of December 31, 2013, the total number of shares and units includes 128,455,350 shares of common stock, 1,491,814 common units held by third parties and 1,475,207 common units, vested and unvested long-term incentive units and vested class C units held by officers and directors, and excludes all unexercised common stock options and all shares potentially issuable upon exchange of our 5.50% exchangeable senior debentures due 2029 or upon conversion of our series E, series F and series G cumulative redeemable preferred stock upon certain change of control transactions. |

| (4) | Dollars in thousands as of the end of the quarter. |

This Supplemental Operating and Financial Data package supplements the information provided in our quarterly and annual reports filed with the Securities and Exchange Commission. Additional information about us and our properties is also available on our website www.digitalrealty.com.

Page 4

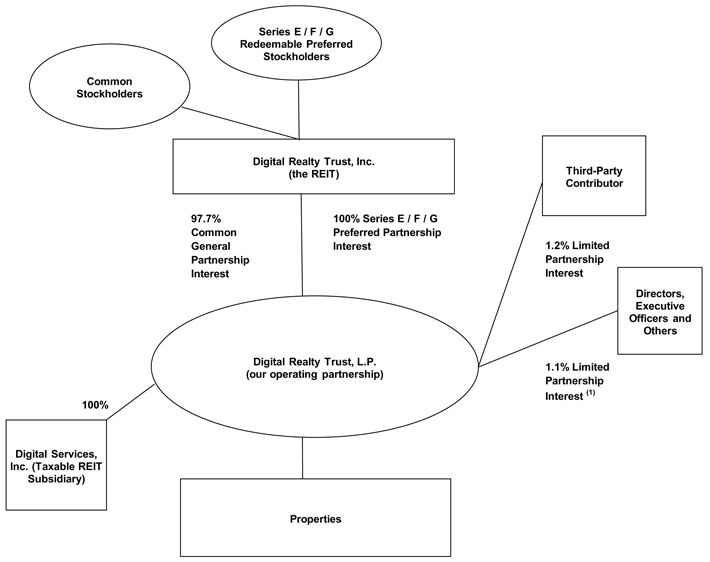

| Ownership Structure |

|

Financial Supplement | ||

| As of December 31, 2013 |

Fourth Quarter 2013 |

| Partner |

# of Units (2) | % Ownership | ||||||

| Digital Realty Trust, Inc. |

128,455,350 | 97.7 | % | |||||

| Cambay Tele.com, LLC (3) |

1,491,814 | 1.2 | % | |||||

| Directors, Executive Officers and Others |

1,475,207 | 1.1 | % | |||||

|

|

|

|

|

|||||

| Total |

131,422,371 | 100.0 | % | |||||

| (1) | Reflects limited partnership interests held by our officers and directors in the form of common units, vested and unvested long-term incentive units and vested class C units and excludes all unexercised common stock options. |

| (2) | The total number of units includes 128,455,350 general partnership common units, 1,491,814 common units held by third parties and 1,475,207 common units, vested and unvested long-term incentive units and vested class C units held by officers and directors, and excludes all unexercised common stock options and all shares potentially issuable upon exchange of our 5.50% exchangeable senior debentures due 2029 or upon conversion of our series E, series F and series G cumulative redeemable preferred stock upon certain change of control transactions. |

| (3) | This third-party contributor received the common units (along with cash and our operating partnership’s assumption of debt) in exchange for their interests in 200 Paul Avenue, 1100 Space Park Drive, the eXchange colocation business and other specified assets and liabilities. Includes 403,913 common units held by the members of Cambay Tele.com, LLC. |

Page 5

| Key Quarterly Financial Data |

|

Financial Supplement | ||

|

Unaudited and dollars in thousands, except per share data |

Fourth Quarter 2013 |

| 31-Dec-13 | 30-Sep-13 | 30-Jun-13 | 31-Mar-13 | 31-Dec-12 | ||||||||||||||||

| Shares and Units at End of Quarter |

||||||||||||||||||||

| Common shares outstanding |

128,455,350 | 128,438,970 | 128,421,888 | 128,413,791 | 125,140,783 | |||||||||||||||

| Common units outstanding |

2,967,021 | 2,982,031 | 2,996,870 | 2,996,714 | 2,851,400 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Shares and Partnership Units |

131,422,371 | 131,421,001 | 131,418,758 | 131,410,505 | 127,992,183 | |||||||||||||||

| Enterprise Value |

||||||||||||||||||||

| Market value of common equity (1) |

$ | 6,455,467 | $ | 6,978,455 | $ | 8,016,544 | $ | 8,792,677 | $ | 8,689,389 | ||||||||||

| Liquidation value of preferred equity |

720,000 | 720,000 | 720,000 | 470,000 | 593,413 | |||||||||||||||

| Total debt at balance sheet carrying value |

4,961,892 | 4,780,397 | 4,698,248 | 4,682,124 | 4,278,565 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Enterprise Value |

$ | 12,137,359 | $ | 12,478,852 | $ | 13,434,792 | $ | 13,944,801 | $ | 13,561,367 | ||||||||||

| Total debt / total enterprise value |

40.9 | % | 38.3 | % | 35.0 | % | 33.6 | % | 31.5 | % | ||||||||||

| Selected Balance Sheet Data |

||||||||||||||||||||

| Investments in real estate (before depreciation) |

$ | 9,950,082 | $ | 9,576,467 | $ | 9,335,886 | $ | 9,011,433 | $ | 8,809,153 | ||||||||||

| Total Assets |

9,685,745 | 9,426,041 | 9,184,859 | 8,971,492 | 8,819,214 | |||||||||||||||

| Total Liabilities |

6,039,233 | 5,745,472 | 5,601,589 | 5,589,544 | 5,320,830 | |||||||||||||||

| Selected Operating Data |

||||||||||||||||||||

| Total operating revenues |

$ | 380,931 | $ | 379,456 | $ | 363,502 | $ | 358,370 | $ | 349,736 | ||||||||||

| Total operating expenses |

282,876 | 294,279 | 263,508 | 259,784 | 255,098 | |||||||||||||||

| Interest expense |

45,996 | 47,742 | 47,583 | 48,078 | 40,350 | |||||||||||||||

| Net income |

55,667 | 153,480 | 59,621 | 51,681 | 55,895 | |||||||||||||||

| Net income available to common stockholders |

42,977 | 138,872 | 47,077 | 42,657 | 44,815 | |||||||||||||||

| Financial Ratios |

||||||||||||||||||||

| EBITDA (2) |

$ | 215,884 | $ | 308,868 | $ | 211,238 | $ | 203,561 | $ | 192,893 | ||||||||||

| Adjusted EBITDA (3) |

228,019 | 217,577 | 223,782 | 212,585 | 203,973 | |||||||||||||||

| Net Debt to Adjusted EBITDA (4) |

5.4x | 5.4x | 5.2x | 5.5x | 5.2x | |||||||||||||||

| GAAP interest expense |

45,996 | 47,742 | 47,583 | 48,078 | 40,350 | |||||||||||||||

| Fixed charges (5) |

68,207 | 69,498 | 69,372 | 65,371 | 61,701 | |||||||||||||||

| Interest coverage ratio (6) |

4.3x | 4.0x | 4.1x | 4.0x | 4.2x | |||||||||||||||

| Fixed charge coverage ratio (7) |

3.3x | 3.1x | 3.2x | 3.3x | 3.3x | |||||||||||||||

| Profitability Measures |

||||||||||||||||||||

| Net income per common share - basic |

$ | 0.33 | $ | 1.08 | $ | 0.37 | $ | 0.34 | $ | 0.36 | ||||||||||

| Net income per common share - diluted |

$ | 0.33 | $ | 1.06 | $ | 0.37 | $ | 0.34 | $ | 0.36 | ||||||||||

| Funds from operations (FFO) / diluted share and unit (8) |

$ | 1.26 | $ | 1.10 | $ | 1.22 | $ | 1.16 | $ | 1.16 | ||||||||||

| Core funds from operations (CFFO) / diluted share and unit (8) |

$ | 1.26 | $ | 1.16 | $ | 1.19 | $ | 1.18 | $ | 1.19 | ||||||||||

| Adj. funds from operations (AFFO) / diluted share and unit (9) |

$ | 0.94 | $ | 0.92 | $ | 0.95 | $ | 0.92 | $ | 0.88 | ||||||||||

| Dividends per share and common unit |

$ | 0.78 | $ | 0.78 | $ | 0.78 | $ | 0.78 | $ | 0.73 | ||||||||||

| Diluted FFO payout ratio (10) |

61.7 | % | 71.0 | % | 64.1 | % | 67.5 | % | 63.0 | % | ||||||||||

| Diluted CFFO payout ratio (11) |

61.7 | % | 67.0 | % | 65.7 | % | 66.3 | % | 61.4 | % | ||||||||||

| Diluted AFFO payout ratio (9) (12) |

83.1 | % | 85.2 | % | 82.1 | % | 85.2 | % | 82.6 | % | ||||||||||

| Portfolio Statistics |

||||||||||||||||||||

| Buildings (13) |

187 | 188 | 187 | 178 | 171 | |||||||||||||||

| Properties (13) |

131 | 130 | 129 | 127 | 122 | |||||||||||||||

| Net rentable square feet, excluding development space (13) |

21,399,551 | 21,033,398 | 20,948,042 | 20,606,509 | 19,889,396 | |||||||||||||||

| Occupancy at end of quarter (14) |

92.6 | % | 93.0 | % | 93.1 | % | 94.0 | % | 94.4 | % | ||||||||||

| Occupied square footage |

19,821,269 | 19,563,183 | 19,490,315 | 19,362,123 | 18,769,656 | |||||||||||||||

| Space under active development (15) |

1,759,681 | 1,532,902 | 1,282,612 | 1,389,795 | 1,372,006 | |||||||||||||||

| Space held for development (16) |

1,331,685 | 2,127,025 | 2,276,858 | 2,087,801 | 2,014,354 | |||||||||||||||

| Weighted average remaining lease term (years) (17) |

7.0 | 6.9 | 7.1 | 6.9 | 6.9 | |||||||||||||||

| Same-store occupancy at end of quarter (14) (18) |

91.2 | % | 91.8 | % | 91.8 | % | 92.6 | % | 93.3 | % | ||||||||||

| (1) | The market value of common equity is based on the closing stock price at the end of the quarter and assumes 100% redemption of the limited partnership units in our operating partnership, including common units and vested and unvested long-term incentive units (including vested class C units), for shares of our common stock. Excludes shares issuable with respect to stock options that have been granted but have not yet been exercised, and also excludes all shares potentially issuable upon exchange of our 5.50% exchangeable senior debentures due 2029 or upon conversion of our series E, series F and series G cumulative redeemable preferred stock upon certain change of control transactions. |

| (2) | EBITDA is calculated as earnings before interest, taxes, depreciation & amortization. For a discussion of EBITDA, see page 42. For a reconciliation of net income available to common stockholders to EBITDA, see page 41. |

| (3) | Adjusted EBITDA is adjusted for straight-line rent expense adjustment attributable to prior periods, gain on contribution of properties to unconsolidated joint venture, preferred dividends and non-controlling interests. For a discussion of Adjusted EBITDA, see page 42. For a reconciliation of net income available to common stockholders to Adjusted EBITDA, see page 41. |

| (4) | Calculated as total debt at balance sheet carrying value less unrestricted cash and cash equivalents, divided by the product of Adjusted EBITDA multiplied by four. |

| (5) | Fixed charges consist of GAAP interest expense, capitalized interest, scheduled debt principal payments and preferred dividends. |

| (6) | Interest coverage ratio is Adjusted EBITDA divided by GAAP interest expense plus capitalized interest. |

| (7) | Fixed charge coverage ratio is Adjusted EBITDA divided by fixed charges. |

| (8) | For a definition and discussion of FFO and CFFO, see page 42. For a reconciliation of net income available to common stockholders to FFO, see page 9. |

| (9) | All periods presented include internal leasing commissions, the amounts of which have historically been included in capitalized leasing commissions and were previously excluded from recurring capital expenditures. For a definition and discussion of AFFO, see page 42. For a reconciliation of FFO to AFFO, see page 10. |

| (10) | Diluted FFO payout ratio is dividends declared per common share and unit divided by diluted FFO per share and unit. |

| (11) | Diluted CFFO payout ratio is dividends declared per common share and unit divided by diluted CFFO per share and unit. |

| (12) | Diluted AFFO payout ratio is dividends declared per common share and unit divided by diluted AFFO per share and unit. |

| (13) | Includes properties held as investments in unconsolidated joint ventures. |

| (14) | Occupancy and same-store occupancy exclude space under active development and space held for development. For some of our properties, we calculate occupancy based on factors in addition to contractually leased square feet, including available power, required support space and common area. |

| (15) | Space under active development includes current Base Building and Data Centers projects in progress. See page 30. |

| (16) | Space held for development includes space held for future Data Center development, and excludes space under active development. See page 34. |

| (17) | Weighted average remaining lease term excludes renewal options and is weighted by net rentable square feet. |

| (18) | Same-store properties were acquired before December 31, 2011. |

Page 6

| 2014 Guidance |

|

Financial Supplement | ||

|

Fourth Quarter 2013 |

| As of October 29, 2013 | As of January 6, 2014 | As of February 25, 2014 | ||||||||||

| Internal Growth |

||||||||||||

| Rental rates on renewal leases |

||||||||||||

| Cash basis |

Roughly flat | Roughly flat | Roughly flat | |||||||||

| GAAP basis |

Modestly Positive | Modestly Positive | Modestly Positive | |||||||||

| Operating margin |

25 - 75 bps < historical run-rate | 25 - 75 bps < historical run-rate | 25 - 75 bps < historical run-rate | |||||||||

| Incremental revenue from speculative leasing (1) |

N/A | $20 - $30 million | $20 - $30 million | |||||||||

| Overhead load |

75 - 85 bps on total assets | 75 - 85 bps on total assets | 75 - 85 bps on total assets | |||||||||

| External Growth |

||||||||||||

| Acquisitions |

||||||||||||

| Dollar volume |

$0 - $400 million | $0 - $400 million | $0 - $400 million | |||||||||

| Cap Rate |

7.5% - 8.5 | % | 7.5% - 8.5 | % | 7.5% - 8.5 | % | ||||||

| Joint ventures |

||||||||||||

| Dollar volume |

$0 - $400 million | $0 - $400 million | $0 - $400 million | |||||||||

| Cap rate |

6.75% - 7.25 | % | 6.75% - 7.25 | % | 6.75% - 7.25 | % | ||||||

| Development |

||||||||||||

| Capex |

$600 - $800 million | $600 - $800 million | $600 - $800 million | |||||||||

| Average stabilized yields |

10% - 12 | % | 10% - 12 | % | 10% - 12 | % | ||||||

| Enhancements and other non-recurring capex (2) |

N/A | $85 - $90 million | $85 - $90 million | |||||||||

| Recurring capex + capitalized leasing costs (3) |

$75 - $80 million | $75 - $80 million | $75 - $80 million | |||||||||

| Balance Sheet |

||||||||||||

| Preferred equity |

||||||||||||

| Dollar amount |

$100 - $250 million | $100 - $250 million | $100 - $250 million | |||||||||

| Pricing |

7.5% - 8.0 | % | 8.0% - 8.5 | % | 8.0% - 8.5 | % | ||||||

| Timing |

Late 2013 or early 2014 | Early 2014 | Early 2014 | |||||||||

| Long-term debt |

||||||||||||

| Dollar amount |

$700 - $900 million | $700 - $900 million | $700 - $900 million | |||||||||

| Pricing |

4.75% - 5.25 | % | 4.75% - 5.50 | % | 4.75% - 5.50 | % | ||||||

| Timing |

Late 2013 or early 2014 | Early 2014 | Early 2014 | |||||||||

| Core Funds From Operations / share |

Mid-single digit growth | $4.75 - $4.90 | $4.75 - $4.90 | |||||||||

| (1) | Incremental revenue from speculative leasing represents revenue expected to be recognized in the current year from leases that have not yet been signed. |

| (2) | Other non-recurring CapEx represents costs incurred to enhance the capacity or marketability of operating properties, such as network fiber initiatives, the build-out of an additional sub-station or installation of a new security system, in addition to major remediation costs on recently-acquired properties, whether or not contemplated in the original acquisition underwriting. Other non-recurring CapEx also includes infrequent and major component replacements. |

| (3) | Recurring CapEx represents non-incremental improvements required to maintain current revenues, including second-generation tenant improvements and leasing commissions. Capitalized leasing costs include capitalized leasing compensation as well as capitalized internal leasing commissions, as disclosed in the AFFO reconciliation on page 10. |

Page 7

| Consolidated Quarterly Statements of Operations |

|

Financial Supplement | ||

|

Unaudited and in thousands, except share and per share data |

Fourth Quarter 2013 |

| Three Months Ended | Twelve Months Ended | |||||||||||||||||||||||||||

| 31-Dec-13 | 30-Sep-13 | 30-Jun-13 | 31-Mar-13 | 31-Dec-12 | 31-Dec-13 | 31-Dec-12 | ||||||||||||||||||||||

| Rental revenues |

$ | 296,987 | $ | 290,712 | $ | 285,953 | $ | 281,399 | $ | 272,906 | $ | 1,155,051 | $ | 990,715 | ||||||||||||||

| Tenant reimbursements - Utilities |

55,319 | 59,936 | 54,397 | 51,245 | 50,085 | 220,897 | 185,520 | |||||||||||||||||||||

| Tenant reimbursements - Other |

27,310 | 28,123 | 22,284 | 24,672 | 25,062 | 102,389 | 86,789 | |||||||||||||||||||||

| Fee income |

1,315 | 671 | 728 | 806 | 1,525 | 3,520 | 8,428 | |||||||||||||||||||||

| Other |

— | 14 | 140 | 248 | 158 | 402 | 7,615 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total Operating Revenues |

$ | 380,931 | $ | 379,456 | $ | 363,502 | $ | 358,370 | $ | 349,736 | $ | 1,482,259 | $ | 1,279,067 | ||||||||||||||

| Utilities |

$ | 58,773 | $ | 65,055 | $ | 57,142 | $ | 53,972 | $ | 53,040 | $ | 234,942 | $ | 194,880 | ||||||||||||||

| Rental property operating |

27,545 | 28,460 | 26,911 | 29,180 | 25,044 | 112,096 | 94,791 | |||||||||||||||||||||

| Repairs & maintenance |

27,109 | 24,788 | 22,283 | 23,628 | 28,011 | 97,808 | 90,505 | |||||||||||||||||||||

| Non-cash straight-line rent expense adjustment |

— | 9,988 | — | — | — | 9,988 | — | |||||||||||||||||||||

| Property taxes |

23,831 | 26,074 | 19,374 | 21,042 | 19,682 | 90,321 | 69,475 | |||||||||||||||||||||

| Insurance |

2,156 | 2,144 | 2,238 | 2,205 | 2,647 | 8,743 | 9,600 | |||||||||||||||||||||

| Construction management |

35 | 51 | 294 | 384 | 184 | 764 | 1,596 | |||||||||||||||||||||

| Depreciation & amortization |

126,776 | 121,198 | 115,867 | 111,623 | 107,718 | 475,464 | 382,553 | |||||||||||||||||||||

| General & administrative |

15,536 | 16,275 | 17,891 | 15,951 | 13,441 | 65,653 | 57,209 | |||||||||||||||||||||

| Transactions |

1,108 | 243 | 1,491 | 1,763 | 5,331 | 4,605 | 11,120 | |||||||||||||||||||||

| Other |

7 | 3 | 17 | 36 | — | 63 | 1,260 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total Operating Expenses |

$ | 282,876 | $ | 294,279 | $ | 263,508 | $ | 259,784 | $ | 255,098 | $ | 1,100,447 | $ | 912,989 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Operating Income |

$ | 98,055 | $ | 85,177 | $ | 99,994 | $ | 98,586 | $ | 94,638 | $ | 381,812 | $ | 366,078 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Equity in earnings of unconsolidated joint ventures |

$ | 2,957 | $ | 2,174 | $ | 2,330 | $ | 2,335 | $ | 1,733 | $ | 9,796 | $ | 8,135 | ||||||||||||||

| Gain on insurance settlement |

— | — | 5,597 | — | — | 5,597 | — | |||||||||||||||||||||

| Gain on contribution of properties to unconsol. JV |

555 | 115,054 | — | — | — | 115,609 | — | |||||||||||||||||||||

| Interest and other income |

231 | (127 | ) | (6 | ) | 41 | (116 | ) | 139 | 1,892 | ||||||||||||||||||

| Interest expense |

(45,996 | ) | (47,742 | ) | (47,583 | ) | (48,078 | ) | (40,350 | ) | (189,399 | ) | (157,108 | ) | ||||||||||||||

| Tax benefit (expense) |

473 | (352 | ) | (210 | ) | (1,203 | ) | (10 | ) | (1,292 | ) | (2,647 | ) | |||||||||||||||

| Loss from early extinguishment of debt |

(608 | ) | (704 | ) | (501 | ) | — | — | (1,813 | ) | (303 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net Income |

$ | 55,667 | $ | 153,480 | $ | 59,621 | $ | 51,681 | $ | 55,895 | $ | 320,449 | $ | 216,047 | ||||||||||||||

| Net income attributable to noncontrolling interests |

(964 | ) | (2,882 | ) | (1,145 | ) | (970 | ) | (1,329 | ) | (5,961 | ) | (5,713 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net Income Attributable to Digital Realty Trust, Inc. |

$ | 54,703 | $ | 150,598 | $ | 58,476 | $ | 50,711 | $ | 54,566 | $ | 314,488 | $ | 210,334 | ||||||||||||||

| Preferred stock dividends |

(11,726 | ) | (11,726 | ) | (11,399 | ) | (8,054 | ) | (9,751 | ) | (42,905 | ) | (38,672 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net Income Available to Common Stockholders |

$ | 42,977 | $ | 138,872 | $ | 47,077 | $ | 42,657 | $ | 44,815 | $ | 271,583 | $ | 171,662 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Weighted-average shares outstanding - basic |

128,444,744 | 128,427,444 | 128,419,745 | 126,445,285 | 123,824,957 | 127,941,134 | 115,717,667 | |||||||||||||||||||||

| Weighted-average shares outstanding - diluted |

128,641,470 | 135,301,765 | 128,623,076 | 126,738,339 | 124,145,590 | 128,127,641 | 116,006,577 | |||||||||||||||||||||

| Weighted-average fully diluted shares and units |

137,890,892 | 137,851,514 | 131,177,283 | 129,181,095 | 127,835,847 | 137,769,299 | 131,467,271 | |||||||||||||||||||||

| Net income per share - basic |

$ | 0.33 | $ | 1.08 | $ | 0.37 | $ | 0.34 | $ | 0.36 | $ | 2.12 | $ | 1.48 | ||||||||||||||

| Net income per share - diluted |

$ | 0.33 | $ | 1.06 | $ | 0.37 | $ | 0.34 | $ | 0.36 | $ | 2.12 | $ | 1.48 | ||||||||||||||

Page 8

| Funds From Operations and Core Funds From Operations |

|

Financial Supplement | ||

|

Unaudited and in thousands, except per share data |

Fourth Quarter 2013 |

| Three Months Ended | Twelve Months Ended | |||||||||||||||||||||||||||

| Reconciliation of Net Income to Funds From Operations (FFO) |

31-Dec-13 | 30-Sep-13 | 30-Jun-13 | 31-Mar-13 | 31-Dec-12 | 31-Dec-13 | 31-Dec-12 | |||||||||||||||||||||

| Net Income Available to Common Stockholders |

$ | 42,977 | $ | 138,872 | $ | 47,077 | $ | 42,657 | $ | 44,815 | $ | 271,583 | $ | 171,662 | ||||||||||||||

| Adjustments: |

||||||||||||||||||||||||||||

| Noncontrolling interests in operating partnership |

849 | 2,757 | 936 | 824 | 1,336 | 5,366 | 6,157 | |||||||||||||||||||||

| Real estate related depreciation & amortization (1) |

125,671 | 120,006 | 114,913 | 110,690 | 106,797 | 471,281 | 378,970 | |||||||||||||||||||||

| Unconsolidated JV real estate related depreciation & amortization |

1,387 | 788 | 797 | 833 | 727 | 3,805 | 3,208 | |||||||||||||||||||||

| Gain on contribution of properties to unconsolidated joint venture |

(555 | ) | (115,054 | ) | — | — | — | (115,609 | ) | — | ||||||||||||||||||

| Gain on sale of assets held in unconsolidated joint venture |

— | — | — | — | — | — | (2,325 | ) | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Funds From Operations |

$ | 170,329 | $ | 147,369 | $ | 163,723 | $ | 155,004 | $ | 153,675 | $ | 636,426 | $ | 557,672 | ||||||||||||||

| Add: Series C convertible preferred dividends |

— | — | — | — | — | — | 1,402 | |||||||||||||||||||||

| Add: Series D convertible preferred dividends |

— | — | — | — | 1,697 | — | 8,212 | |||||||||||||||||||||

| Add: 5.50% exchangeable senior debentures interest expense |

4,050 | 4,050 | 4,050 | 4,050 | 4,050 | 16,200 | 16,200 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Funds From Operations - diluted |

$ | 174,379 | $ | 151,419 | $ | 167,773 | $ | 159,054 | $ | 159,422 | $ | 652,626 | $ | 583,486 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Weighted-average shares and units outstanding - basic |

130,982 | 130,977 | 130,974 | 128,888 | 127,515 | 130,463 | 119,861 | |||||||||||||||||||||

| Weighted-average shares and units outstanding - diluted (2) |

137,891 | 137,851 | 137,787 | 137,680 | 137,510 | 137,771 | 131,467 | |||||||||||||||||||||

| Funds From Operations per share - basic |

$ | 1.30 | $ | 1.13 | $ | 1.25 | $ | 1.20 | $ | 1.21 | $ | 4.88 | $ | 4.65 | ||||||||||||||

| Funds From Operations per share - diluted (2) |

$ | 1.26 | $ | 1.10 | $ | 1.22 | $ | 1.16 | $ | 1.16 | $ | 4.74 | $ | 4.44 | ||||||||||||||

| Reconciliation of FFO to CFFO | Three Months Ended | Twelve Months Ended | ||||||||||||||||||||||||||

| 31-Dec-13 | 30-Sep-13 | 30-Jun-13 | 31-Mar-13 | 31-Dec-12 | 31-Dec-13 | 31-Dec-12 | ||||||||||||||||||||||

| Funds From Operations - diluted |

$ | 174,379 | $ | 151,419 | $ | 167,773 | $ | 159,054 | $ | 159,422 | $ | 652,626 | $ | 583,486 | ||||||||||||||

| Termination fees and other non-core revenues (3) |

— | (14 | ) | (140 | ) | (248 | ) | (158 | ) | (402 | ) | (9,034 | ) | |||||||||||||||

| Gain on insurance settlement |

— | — | (5,597 | ) | — | — | (5,597 | ) | — | |||||||||||||||||||

| Significant transaction expenses |

1,108 | 243 | 1,491 | 1,763 | 5,331 | 4,605 | 11,120 | |||||||||||||||||||||

| Loss from early extinguishment of debt |

608 | 704 | 501 | — | — | 1,813 | 303 | |||||||||||||||||||||

| Straight-line rent expense adjustment attributable to prior periods (4) |

— | 9,155 | — | — | — | 7,489 | — | |||||||||||||||||||||

| Change in fair value of contingent consideration (5) |

(1,749 | ) | (943 | ) | (370 | ) | 1,300 | (1,051 | ) | (1,762 | ) | (1,051 | ) | |||||||||||||||

| Other non-core expense adjustments (6) |

7 | 3 | 17 | 36 | — | 63 | 1,260 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Core Funds From Operations - diluted |

$ | 174,353 | $ | 160,567 | $ | 163,675 | $ | 161,905 | $ | 163,544 | $ | 658,835 | $ | 586,084 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Weighted-average shares and units outstanding - diluted (2) |

137,891 | 137,851 | 137,787 | 137,680 | 137,510 | 137,771 | 131,467 | |||||||||||||||||||||

| Core Funds From Operations per share - diluted (2) |

$ | 1.26 | $ | 1.16 | $ | 1.19 | $ | 1.18 | $ | 1.19 | $ | 4.78 | $ | 4.46 | ||||||||||||||

| Three Months Ended | Twelve Months Ended | |||||||||||||||||||||||||||||

| (1) | Real Estate Related Depreciation & Amortization | 31-Dec-13 | 30-Sep-13 | 30-Jun-13 | 31-Mar-13 | 31-Dec-12 | 31-Dec-13 | 31-Dec-12 | ||||||||||||||||||||||

| Depreciation & amortization per income statement |

$ | 126,776 | $ | 121,198 | $ | 115,867 | $ | 111,623 | $ | 107,718 | $ | 475,464 | $ | 382,553 | ||||||||||||||||

| Non-real estate depreciation |

(1,105 | ) | (1,192 | ) | (954 | ) | (933 | ) | (921 | ) | (4,183 | ) | (3,583 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Real Estate Related Depreciation & Amortization |

$ | 125,671 | $ | 120,006 | $ | 114,913 | $ | 110,690 | $ | 106,797 | $ | 471,281 | $ | 378,970 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| (2) | At December 31, 2013, we had 0 series D convertible preferred shares outstanding, as a result of the conversion of all remaining shares on February 26, 2013, which translates into 471 common shares on a weighted average basis for the year ended December 31, 2013. At December 31, 2012, we had 4,937 series D convertible preferred shares outstanding that were convertible into 3,143 common shares on a weighted average basis for the three months ended December 31, 2012. At December 31, 2012, we had 0 series C convertible preferred shares (as a result of the conversion of all remaining shares on April 17, 2012) and 4,937 series D convertible preferred shares outstanding that were convertible into 814 common shares and 4,017 common shares on a weighted average basis for the year ended December 31, 2012, respectively. For the three months ended December 31, 2013, September 30, 2013 and December 31, 2012, we have excluded the effect of dilutive series E, series F and series G preferred stock, as applicable, that may be converted upon the occurrence of specified change in control transactions as described in the articles supplementary governing the series E, series F and series G preferred stock, as applicable, which we consider highly improbable; if included, the dilutive effect for the three months ended December 31, 2013, September 30, 2013 and December 31, 2012 would be 15,372, 12,734 and 7,116 shares, respectively. For the year ended December 31, 2013 and December 31, 2012, we have excluded the effect of dilutive series E, series F and series G preferred stock, as applicable, that may be converted upon the occurrence of specified change in control transactions as described in the articles supplementary governing the series E, series F and series G preferred stock, as applicable, which we consider highly improbable; if included, the dilutive effect for the year ended December 31, 2013 and December 31, 2012 would be 12,358 and 5,428 shares, respectively. In addition, we had a balance of $266,400 of 5.50% exchangeable senior debentures due 2029 that were exchangeable for 6,712, 6,684 and 6,531 common shares on a weighted average basis for the three months ended December 31, 2013, September 30, 2013 and December 31, 2012, respectively, and were exchangeable for 6,650 and 6,486 common shares on a weighted average basis for the year ended December 31, 2013 and December 31, 2012, respectively. See below for calculations of diluted FFO available to common stockholders and unitholders and weighted average common stock and units outstanding. |

| (3) | Includes one-time fees, proceeds and certain other adjustments that are not core to our business. |

| (4) | Impact for the three months ended December 31, 2012 and the year ended December 31, 2012 would have resulted in additional expense of $833 and $3,333, respectively. CFFO per share and unit, as adjusted, would have been $1.18 and $4.43 for the above periods, respectively. |

| (5) | Relates to earn-out contingency in connection with the Sentrum Portfolio acquisition. |

| (6) | Includes reversal of accruals and certain other adjustments that are not core to our business. |

Page 9

| Adjusted Funds From Operations (AFFO) |

|

Financial Supplement | ||

|

Unaudited and in thousands, except per share data |

Fourth Quarter 2013 |

| Three Months Ended | Twelve Months Ended | |||||||||||||||||||||||||||

| Reconciliation of FFO to AFFO | 31-Dec-13 | 30-Sep-13 | 30-Jun-13 | 31-Mar-13 | 31-Dec-12 | 31-Dec-13 | 31-Dec-12 | |||||||||||||||||||||

| FFO available to common stockholders and unitholders |

$ | 170,329 | $ | 147,369 | $ | 163,723 | $ | 155,004 | $ | 153,675 | $ | 636,425 | $ | 557,672 | ||||||||||||||

| Adjustments: |

||||||||||||||||||||||||||||

| Non-real estate depreciation |

$ | 1,105 | $ | 1,192 | $ | 954 | $ | 933 | $ | 921 | $ | 4,184 | $ | 3,583 | ||||||||||||||

| Amortization of deferred financing costs |

2,925 | 2,831 | 2,471 | 2,431 | 2,359 | 10,658 | 8,700 | |||||||||||||||||||||

| Amortization of debt discount/premium |

338 | 418 | 418 | 605 | 340 | 1,779 | 1,097 | |||||||||||||||||||||

| Non-cash compensation |

2,183 | 2,877 | (5) | 3,580 | 2,888 | 2,709 | 11,528 | 12,632 | ||||||||||||||||||||

| Loss from early extinguishment of debt |

608 | 704 | 501 | — | — | 1,813 | 303 | |||||||||||||||||||||

| Straight-line rents |

(21,858 | ) | (19,661 | ) | (19,892 | ) | (21,169 | ) | (20,004 | ) | (82,580 | ) | (75,776 | ) | ||||||||||||||

| Non-cash straight-line rent expense adjustment |

— | 9,988 | — | — | — | 9,988 | — | |||||||||||||||||||||

| Above- and below-market rent amortization |

(2,887 | ) | (2,746 | ) | (3,041 | ) | (3,045 | ) | (2,819 | ) | (11,719 | ) | (10,262 | ) | ||||||||||||||

| Change in fair value of contingent consideration (1) |

(1,749 | ) | (943 | ) | (370 | ) | 1,300 | (1,051 | ) | (1,762 | ) | (1,051 | ) | |||||||||||||||

| Capitalized leasing compensation |

(4,214 | ) | (4,924 | ) | (4,786 | ) | (5,053 | ) (6) | (4,008 | ) | (18,977 | ) | (15,102 | ) | ||||||||||||||

| Recurring capital expenditures (2) |

(17,025 | ) | (12,895 | ) | (13,429 | ) | (9,860 | ) | (14,432 | ) | (53,209 | ) | (41,430 | ) | ||||||||||||||

| Capitalized internal leasing commissions |

(4,435 | ) | (2,077 | ) | (3,331 | ) | (2,025 | ) | (1,877 | ) | (11,868 | ) | (7,301 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| AFFO available to common stockholders and unitholders (3) |

$ | 125,320 | $ | 122,133 | $ | 126,798 | $ | 122,009 | $ | 115,813 | $ | 496,260 | $ | 433,065 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Weighted-average shares and units outstanding - basic |

130,982 | 130,977 | 130,974 | 128,888 | 127,515 | 130,463 | 119,861 | |||||||||||||||||||||

| Weighted-average shares and units outstanding - diluted (4) |

137,891 | 137,851 | 137,787 | 137,680 | 137,510 | 137,771 | 131,467 | |||||||||||||||||||||

| AFFO available to common stockholders and unitholders - basic |

125,320 | 122,133 | 126,798 | 122,009 | 115,813 | 496,260 | 433,065 | |||||||||||||||||||||

| Add: Convertible preferred dividends and Interest and amortization of debt issuance costs on 2029 Debentures |

4,050 | 4,050 | 4,050 | 4,050 | 5,747 | 16,200 | 25,814 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| AFFO available to common stockholders and unitholders - diluted |

129,370 | 126,183 | 130,848 | 126,059 | 121,560 | 512,460 | 458,879 | |||||||||||||||||||||

| AFFO per share - diluted (3) |

$ | 0.94 | $ | 0.92 | $ | 0.95 | $ | 0.92 | $ | 0.88 | $ | 3.72 | $ | 3.49 | ||||||||||||||

| Dividends per share and common unit |

$ | 0.78 | $ | 0.78 | $ | 0.78 | $ | 0.78 | $ | 0.73 | $ | 3.12 | $ | 2.92 | ||||||||||||||

| Diluted AFFO Payout Ratio |

83.1 | % | 85.2 | % | 82.1 | % | 85.2 | % | 82.6 | % | 83.9 | % | 83.7 | % | ||||||||||||||

| Three Months Ended | Twelve Months Ended | |||||||||||||||||||||||||||

| Share Count Detail | 31-Dec-13 | 30-Sep-13 | 30-Jun-13 | 31-Mar-13 | 31-Dec-12 | 31-Dec-13 | 31-Dec-12 | |||||||||||||||||||||

| Weighted Average Common Stock and Units Outstanding |

130,982 | 130,977 | 130,974 | 128,888 | 127,515 | 130,463 | 119,861 | |||||||||||||||||||||

| Add: Effect of dilutive securities (excl. series C & D convert. preferred stock & 5.50% debentures) |

197 | 190 | 203 | 293 | 321 | 187 | 289 | |||||||||||||||||||||

| Add: Effect of dilutive series C convertible preferred stock |

— | — | — | — | — | — | 814 | |||||||||||||||||||||

| Add: Effect of dilutive series D convertible preferred stock |

— | — | — | 1,909 | 3,143 | 471 | 4,017 | |||||||||||||||||||||

| Add: Effect of dilutive 5.50% exchangeable senior debentures |

6,712 | 6,684 | 6,610 | 6,590 | 6,531 | 6,650 | 6,486 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Weighted Avg. Common Stock and Units Out. - diluted |

137,891 | 137,851 | 137,787 | 137,680 | 137,510 | 137,771 | 131,467 | |||||||||||||||||||||

| (1) | Relates to earn-out contingency in connection with the Sentrum Portfolio acquisition. |

| (2) | For a definition of recurring capital expenditures, see page 33. |

| (3) | For a definition and discussion of AFFO, see page 42. For a reconciliation of net income available to common stockholders to FFO, see page 9. |

| (4) | At December 31, 2013, we had 0 series D convertible preferred shares outstanding, as a result of the conversion of all remaining shares on February 26, 2013, which translates into 471 common shares on a weighted average basis for the year ended December 31, 2013. At December 31, 2012, we had 4,937 series D convertible preferred shares outstanding that were convertible into 3,143 common shares on a weighted average basis for the three months ended December 31, 2012. At December 31, 2012, we had 0 series C convertible preferred shares (as a result of the conversion of all remaining shares on April 17, 2012) and 4,937 series D convertible preferred shares outstanding that were convertible into 814 common shares and 4,017 common shares on a weighted average basis for the year ended December 31, 2012, respectively. For the three months ended December 31, 2013, September 30, 2013 and December 31, 2012, we have excluded the effect of dilutive series E, series F and series G preferred stock, as applicable, that may be converted upon the occurrence of specified change in control transactions as described in the articles supplementary governing the series E, series F and series G preferred stock, as applicable, which we consider highly improbable; if included, the dilutive effect for the three months ended December 31, 2013, September 30, 2013 and December 31, 2012 would be 15,372, 12,734 and 7,116 shares, respectively. For the year ended December 31, 2013 and December 31, 2012, we have excluded the effect of dilutive series E, series F and series G preferred stock, as applicable, that may be converted upon the occurrence of specified change in control transactions as described in the articles supplementary governing the series E, series F and series G preferred stock, as applicable, which we consider highly improbable; if included, the dilutive effect for the year ended December 31, 2013 and December 31, 2012 would be 12,358 and 5,428 shares, respectively. In addition, we had a balance of $266,400 of 5.50% exchangeable senior debentures due 2029 that were exchangeable for 6,712, 6,684 and 6,531 common shares on a weighted average basis for the three months ended December 31, 2013, September 30, 2013 and December 31, 2012, respectively, and were exchangeable for 6,650 and 6,486 common shares on a weighted average basis for the year ended December 31, 2013 and December 31, 2012, respectively. See below for calculations of diluted FFO available to common stockholders and unitholders and weighted average common stock and units outstanding. |

| (5) | Corrects overstated amount in previously reported non-cash compensation. |

| (6) | Corrects understated amount in previously reported capitalized leasing compensation. |

Page 10

| Consolidated Balance Sheets |

|

Financial Supplement | ||

|

Dollars in thousands, except per share data |

Fourth Quarter 2013 |

| Unaudited | ||||||||||||||||||||

| 31-Dec-13 | 30-Sep-13 | 30-Jun-13 | 31-Mar-13 | 31-Dec-12 | ||||||||||||||||

| Assets |

||||||||||||||||||||

| Investments in real estate: |

||||||||||||||||||||

| Land |

$ | 693,791 | $ | 684,644 | $ | 690,356 | $ | 679,803 | $ | 661,058 | ||||||||||

| Acquired ground leases |

14,618 | 14,355 | 13,216 | 13,137 | 13,658 | |||||||||||||||

| Buildings and improvements |

8,680,677 | 8,357,786 | 8,125,636 | 7,826,501 | 7,662,973 | |||||||||||||||

| Tenant improvements |

490,492 | 466,616 | 432,631 | 419,062 | 404,830 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Investments in Real Estate |

$ | 9,879,578 | $ | 9,523,401 | $ | 9,261,839 | $ | 8,938,503 | $ | 8,742,519 | ||||||||||

| Accumulated depreciation & amortization |

(1,565,996 | ) | (1,459,055 | ) | (1,377,375 | ) | (1,288,440 | ) | (1,206,017 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net Investments in Properties |

$ | 8,313,582 | $ | 8,064,346 | $ | 7,884,464 | $ | 7,650,063 | $ | 7,536,502 | ||||||||||

| Land held for sale |

— | 11,015 | — | — | — | |||||||||||||||

| Investment in unconsolidated joint ventures |

70,504 | 53,066 | 74,047 | 72,930 | 66,634 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net Investments in Real Estate |

$ | 8,384,086 | $ | 8,128,427 | $ | 7,958,511 | $ | 7,722,993 | $ | 7,603,136 | ||||||||||

| Cash and cash equivalents |

$ | 56,808 | $ | 55,118 | $ | 24,260 | $ | 42,130 | $ | 56,281 | ||||||||||

| Accounts and other receivables (1) |

181,163 | 191,715 | 159,847 | 177,951 | 168,286 | |||||||||||||||

| Deferred rent |

393,504 | 369,979 | 360,588 | 340,753 | 321,715 | |||||||||||||||

| Acquired above market leases, net |

52,264 | 54,446 | 56,310 | 59,079 | 65,055 | |||||||||||||||

| Acquired in place lease value and deferred leasing costs, net |

489,456 | 484,445 | 492,884 | 494,384 | 495,205 | |||||||||||||||

| Deferred financing costs, net |

36,475 | 39,132 | 31,881 | 33,393 | 30,621 | |||||||||||||||

| Restricted cash |

40,362 | 42,457 | 38,977 | 43,929 | 44,050 | |||||||||||||||

| Other assets |

51,627 | 60,322 | 61,601 | 56,880 | 34,865 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Assets |

$ | 9,685,745 | $ | 9,426,041 | $ | 9,184,859 | $ | 8,971,492 | $ | 8,819,214 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Liabilities and Equity |

||||||||||||||||||||

| Global revolving credit facility |

$ | 724,668 | $ | 498,082 | $ | 610,328 | $ | 546,649 | $ | 723,729 | ||||||||||

| Unsecured term loan |

1,020,984 | 950,205 | 741,178 | 747,830 | 757,839 | |||||||||||||||

| Unsecured senior notes, net of discount |

2,364,232 | 2,382,059 | 2,342,990 | 2,341,972 | 1,738,221 | |||||||||||||||

| Exchangeable senior debentures |

266,400 | 266,400 | 266,400 | 266,400 | 266,400 | |||||||||||||||

| Mortgage loans, net of premiums |

585,608 | 683,651 | 737,352 | 779,273 | 792,376 | |||||||||||||||

| Accounts payable and other accrued liabilities |

662,687 | 652,720 | 617,766 | 613,537 | 646,427 | |||||||||||||||

| Accrued dividends and distributions |

102,509 | — | — | — | 93,434 | |||||||||||||||

| Acquired below market leases, net |

130,269 | 133,625 | 137,297 | 141,257 | 148,233 | |||||||||||||||

| Security deposits and prepaid rents |

181,876 | 178,730 | 148,278 | 152,626 | 154,171 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Liabilities |

$ | 6,039,233 | $ | 5,745,472 | $ | 5,601,589 | $ | 5,589,544 | $ | 5,320,830 | ||||||||||

| Equity |

||||||||||||||||||||

| Preferred Stock: $0.01 par value per share, 70,000,000 shares authorized: |

||||||||||||||||||||

| Series D Cumulative Convertible Preferred Stock (2) |

— | — | — | — | $ | 119,348 | ||||||||||||||

| Series E Cumulative Redeemable Preferred Stock (3) |

277,172 | 277,172 | 277,172 | 277,172 | 277,172 | |||||||||||||||

| Series F Cumulative Redeemable Preferred Stock (4) |

176,191 | 176,191 | 176,191 | 176,191 | 176,191 | |||||||||||||||

| Series G Cumulative Redeemable Preferred Stock (5) |

241,468 | 241,511 | 241,565 | — | — | |||||||||||||||

| Common Stock: $0.01 par value per share (6) |

1,279 | 1,279 | 1,279 | 1,279 | 1,247 | |||||||||||||||

| Additional paid-in capital |

3,688,937 | 3,685,668 | 3,681,618 | 3,677,070 | 3,562,642 | |||||||||||||||

| Dividends in excess of earnings |

(785,222 | ) | (728,012 | ) | (766,704 | ) | (713,612 | ) | (656,104 | ) | ||||||||||

| Accumulated other comprehensive income, net |

10,691 | (10,327 | ) | (64,010 | ) | (72,473 | ) | (12,191 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Stockholders’ Equity |

$ | 3,610,516 | $ | 3,643,482 | $ | 3,547,111 | $ | 3,345,627 | $ | 3,468,305 | ||||||||||

| Noncontrolling Interests |

||||||||||||||||||||

| Noncontrolling interest in operating partnership |

$ | 29,027 | $ | 30,264 | $ | 28,935 | $ | 30,186 | $ | 24,135 | ||||||||||

| Noncontrolling interest in consolidated joint ventures |

6,969 | 6,823 | 7,224 | 6,135 | 5,944 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Noncontrolling Interests |

$ | 35,996 | $ | 37,087 | $ | 36,159 | $ | 36,321 | $ | 30,079 | ||||||||||

| Total Equity |

$ | 3,646,512 | $ | 3,680,569 | $ | 3,583,270 | $ | 3,381,948 | $ | 3,498,384 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Liabilities and Equity |

$ | 9,685,745 | $ | 9,426,041 | $ | 9,184,859 | $ | 8,971,492 | $ | 8,819,214 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (1) | Net of allowance for doubtful accounts of $5,576 and $3,609 as of December 31, 2013 and December 31, 2012, respectively. |

| (2) | Series D Cumulative Convertible Preferred Stock, 5.500%, $0 and $123,413 liquidation preference, respectively ($25.00 per share), 0 and 4,936,505 shares issued and outstanding as of December 31, 2013 and December 31, 2012, respectively. |

| (3) | Series E Cumulative Redeemable Preferred Stock, 7.000%, $287,500 and $287,500 liquidation preference, respectively ($25.00 per share), 11,500,000 and 11,500,000 shares issued and outstanding as of December 31, 2013 and December 31, 2012, respectively. |

| (4) | Series F Cumulative Redeemable Preferred Stock, 6.625%, $182,500 and $182,500 liquidation preference, respectively ($25.00 per share), 7,300,000 and 7,300,000 shares issued and outstanding as of December 31, 2013 and December 31, 2012, respectively. |

| (5) | Series G Cumulative Redeemable Preferred Stock, 5.875%, $250,000 and $0 liquidation preference, respectively ($25.00 per share), 10,000,000 and 0 shares issued and outstanding as of December 31, 2013 and December 31, 2012, respectively. |

| (6) | Common Stock: $0.01 par value per share, 215,000,000 shares authorized, 128,455,350 and 125,140,783 shares issued and outstanding as of December 31, 2013 and December 31, 2012, respectively. |

Page 11

| Components of NAV (1) |

|

Financial Supplement | ||

|

In Thousands |

Fourth Quarter 2013 |

Consolidated Properties Cash Net Operating Income (NOI) (2), Annualized (8)

| Internet Gateway (3) |

$ | 169,766 | ||

| Turn-Key Flex (3) |

424,416 | |||

| Powered Base Building (3) |

169,766 | |||

| Colo & Non-tech (3) |

84,883 | |||

| less: Partner’s share of consolidated JV’s |

(497 | ) | ||

| 4Q13 acquisitions, annualized adjustment |

3,067 | |||

| 4Q13 & FY14 backlog Cash NOI (stabilized) (4) |

49,258 | |||

|

|

|

|||

| Total Consolidated Cash NOI, Annualized |

$ | 900,659 | ||

|

|

|

|||

| Digital Realty’s Pro Rata Share of Unconsolidated Joint Venture Cash NOI |

||||

| Turn-Key Flex |

$ | 12,832 | ||

| PBB |

6,349 | |||

|

|

|

|||

| Total Unconsolidated Cash NOI, Annualized |

$ | 19,181 | ||

|

|

|

|||

| Other Income |

||||

| Development and Management Fees (net), Annualized |

$ | 5,120 | ||

|

|

|

|||

| Other Assets |

||||

| Pre-stabilized inventory, at cost |

$ | 465,293 | ||

| Land held for development |

106,327 | |||

| Development CIP (5) |

876,803 | |||

| less: CIP associated with FY14 Backlog NOI |

(141,805 | ) | ||

| Cash and cash equivalents |

56,808 | |||

| Restricted cash |

40,362 | |||

| Accounts and other receivables, net |

181,163 | |||

| Other assets |

51,627 | |||

| less: Partner’s share of consolidated JV assets |

(2,400 | ) | ||

|

|

|

|||

| Total Other Assets |

$ | 1,634,178 | ||

|

|

|

|||

| Liabilities |

||||

| Global revolving credit facility |

$ | 724,668 | ||

| Unsecured term loan |

1,020,984 | |||

| Unsecured senior notes |

2,364,232 | |||

| add: Unamortized discounts |

15,048 | |||

| Mortgage loans, net of premiums |

585,608 | |||

| Accounts payable and other accrued liabilities (6) |

662,687 | |||

| Accrued dividends and distributions |

102,509 | |||

| Security deposits and prepaid rents |

181,876 | |||

| FY14 backlog NOI cost to complete (7) |

160,111 | |||

| Preferred stock, at liquidation value |

720,000 | |||

| Digital Realty’s share of unconsolidated JV debt |

113,477 | |||

|

|

|

|||

| Total Liabilities |

$ | 6,651,200 | ||

|

|

|

|||

| Diluted Shares and Units Outstanding |

138,323 | |||

|

|

|

|||

| (1) | Includes Digital Realty’s share of backlog leasing at unconsolidated joint venture properties. |

| (2) | For a definition and discussion of NOI and Cash NOI, see page 42. |

| (3) | Reflects annualized 4Q13 Cash NOI of $855M less $6M of run-rate adjustments related to the reversal of a bonus accrual which is not expected to recur. NOI is allocated 20% to PBB, 50% to TKF, 20% to Internet Gateway, and 10% to Colo/Non-tech. Actual Cash NOI allocable to each product or property type may be different. |

| (4) | Estimated Cash NOI related to signed leasing expected to commence in FY14. Includes DLR’s share of signed leasing at unconsolidated JV properties. |

| (5) | See page 32 for further details on the breakdown of the CIP balance. |

| (6) | Includes net deferred tax liability of approximately $146.6 million. |

| (7) | Includes Digital Realty’s share of cost to complete at unconsolidated joint venture properties. |

| (8) | Annualized Cash NOI is calculated by multiplying results for the most recent quarter by four. Annualized results may not be indicative of any four-quarter period and do not take into account scheduled lease expirations, among other things. Annualized data is presented for illustrative purposes only. |

Page 12

| Consolidated Debt Analysis |

|

Financial Supplement | ||

|

Unaudited, in thousands |

Fourth Quarter 2013 |

| Figures as of December 31, 2013 |

||||||||||||||||||

| Maturity Date |

Principal Balance | % of Total Debt | Interest Rate | Interest Rate Including swaps |

||||||||||||||

| Global Revolving Credit Facility (1) |

||||||||||||||||||

| Global revolving credit facility |

November 3, 2018 |

$ | 724,668 | |||||||||||||||

|

|

|

|||||||||||||||||

| Total Global Revolving Credit Facility |

$ | 724,668 | 15 | % | 1.60 | % | ||||||||||||

| Unsecured Term Loan (1) |

||||||||||||||||||

| Unhedged variable rate portion of term loan |

April 16, 2018 |

$ | 460,040 | |||||||||||||||

| Hedged variable rate portion of term loan |

April 16, 2018 |

560,944 | ||||||||||||||||

|

|

|

|||||||||||||||||

| Total Unsecured Term Loan |

$ | 1,020,984 | 20 | % | 1.67 | % | 2.00 | % | ||||||||||

| Prudential Unsecured Senior Notes |

||||||||||||||||||

| Series C |

January 6, 2016 |

$ | 25,000 | 9.68 | % | |||||||||||||

| Series D |

January 20, 2015 |

50,000 | 4.57 | % | ||||||||||||||

| Series E |

January 20, 2017 |

50,000 | 5.73 | % | ||||||||||||||

| Series F |

February 3, 2015 |

17,000 | 4.50 | % | ||||||||||||||

|

|

|

|

|

|||||||||||||||

| Total Prudential Unsecured Senior Notes |

$ | 142,000 | 3 | % | ||||||||||||||

| Senior Notes |

||||||||||||||||||

| 4.50% notes due 2015 |

July 15, 2015 |

$ | 375,000 | 4.50 | % | |||||||||||||

| 5.875% notes due 2020 |

February 1, 2020 |

500,000 | 5.88 | % | ||||||||||||||

| 5.25% notes due 2021 |

March 15, 2021 |

400,000 | 5.25 | % | ||||||||||||||

| 3.625% notes due 2022 |

October 1, 2022 |

300,000 | 3.63 | % | ||||||||||||||

| 4.25% notes due 2025 |

January 17, 2025 |

662,280 | 4.25 | % | ||||||||||||||

| Unamortized discounts |

(15,048 | ) | ||||||||||||||||

|

|

|

|

|

|||||||||||||||

| Total Senior Notes |

$ | 2,222,232 | 45 | % | ||||||||||||||

|

|

|

|

|

|||||||||||||||

| Total Unsecured Senior Notes |

$ | 2,364,232 | 48 | % | ||||||||||||||

|

|

|

|

|

|||||||||||||||

| Exchangeable Senior Debentures |

||||||||||||||||||

| 5.50% exchangeable senior debentures due 2029 |

April 15, 2029 |

$ | 266,400 | 5.50 | % | |||||||||||||

| Unamortized discount |

— | |||||||||||||||||

|

|

|

|

|

|||||||||||||||

| Total Exchangeable Senior Debentures |

$ | 266,400 | 5 | % | ||||||||||||||

| Mortgage Loans |

||||||||||||||||||

| Cressex 1 |

October 16, 2014 |

$ | 28,583 | 5.68 | % | |||||||||||||

| Manchester Technopark |

October 16, 2014 |

8,695 | 5.68 | % | ||||||||||||||

| Secured Term Debt |

November 11, 2014 |

132,966 | 5.65 | % | ||||||||||||||

| 200 Paul Avenue |

October 8, 2015 |

70,713 | 5.74 | % | ||||||||||||||

| 8025 North Interstate 35 |

March 6, 2016 |

6,314 | 4.09 | % | ||||||||||||||

| 600 West Seventh Street |

March 15, 2016 |

49,548 | 5.80 | % | ||||||||||||||

| 34551 Ardenwood Boulevard |

November 11, 2016 |

52,152 | 5.95 | % | ||||||||||||||

| 2334 Lundy Place |

November 11, 2016 |

37,930 | 5.96 | % | ||||||||||||||

| 1100 Space Park Drive |

December 11, 2016 |

52,115 | 5.89 | % | ||||||||||||||

| 2045 & 2055 LaFayette Street |

February 6, 2017 |

63,623 | 5.93 | % | ||||||||||||||

| 150 South First Street |

February 6, 2017 |

50,097 | 6.30 | % | ||||||||||||||

| 731 East Trade Street |

July 1, 2020 |

4,186 | 8.22 | % | ||||||||||||||

| 636 Pierce Street |

April 15, 2023 |

26,327 | 5.27 | % | ||||||||||||||

| Unamortized net premiums |

2,359 | |||||||||||||||||

|

|

|

|

|

|||||||||||||||

| Total Mortgage Loans |

$ | 585,608 | 12 | % | ||||||||||||||

|

|

|

|

|

|||||||||||||||

| Debt Summary |

||||||||||||||||||

| Total unhedged variable rate debt |

$ | 1,184,708 | 24 | % | ||||||||||||||

| Total fixed rate / hedged variable rate debt |

3,777,184 | 76 | % | |||||||||||||||

|

|

|

|

|

|||||||||||||||

| Total Consolidated Debt |

$ | 4,961,892 | 100 | % | 3.92 | % | ||||||||||||

|

|

|

|

|

|||||||||||||||

Global Revolving Credit Facility Detail as of December 31, 2013

(in thousands)

| Maximum Available | Existing Capacity (2) | Currently Drawn | ||||||||||

| Global Revolving Credit Facility |

$ | 2,000,000 | $ | 1,254,763 | $ | 724,668 | ||||||

| (1) | Maturity dates assume that all extensions will be exercised. |

| (2) | Net of letters of credit issued of $20.6 million. |

Page 13

| Debt Maturities |

|

Financial Supplement | ||

|

Unaudited, in thousands |

Fourth Quarter 2013 |

| Figures as of December 31, 2013 | ||||||||||||||||||||||||||||||||

| Interest Rate | 2014 | 2015 | 2016 | 2017 | 2018 | Thereafter | Total | |||||||||||||||||||||||||

| Global Revolving Credit Facility (1) |

||||||||||||||||||||||||||||||||

| Global revolving credit facility |

— | — | — | — | $ | 724,668 | — | $ | 724,668 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total Global Revolving Credit Facility |

1.60 | % | — | — | — | — | $ | 724,668 | — | $ | 724,668 | |||||||||||||||||||||

| Unsecured Term Loan (1) |

||||||||||||||||||||||||||||||||

| Unhedged variable rate portion of term loan |

— | — | — | — | $ | 460,040 | — | $ | 460,040 | |||||||||||||||||||||||

| Hedged variable rate portion of term loan |

— | — | — | — | 560,944 | — | 560,944 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total Unsecured Term Loan |

2.00 | % | — | — | — | — | $ | 1,020,984 | — | $ | 1,020,984 | |||||||||||||||||||||

| Senior Notes |

||||||||||||||||||||||||||||||||

| 4.25% notes due 2025 |

4.25 | % | — | — | — | — | — | $ | 662,280 | $ | 662,280 | |||||||||||||||||||||

| 5.875% notes due 2020 |

5.88 | % | — | — | — | — | — | 500,000 | 500,000 | |||||||||||||||||||||||

| 5.25% notes due 2021 |

5.25 | % | — | — | — | — | — | 400,000 | 400,000 | |||||||||||||||||||||||

| 4.50% notes due 2015 |

4.50 | % | — | 375,000 | — | — | — | — | 375,000 | |||||||||||||||||||||||

| 3.625% notes due 2022 |

3.63 | % | — | — | — | — | — | 300,000 | 300,000 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total Senior Notes |

4.75 | % | — | $ | 375,000 | — | — | — | $ | 1,862,280 | $ | 2,237,280 | ||||||||||||||||||||

| Exchangeable Senior Debentures |

||||||||||||||||||||||||||||||||

| 5.50% exchangeable senior debentures due 2029 (2) |

5.50 | % | $ | 266,400 | — | — | — | — | — | $ | 266,400 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total Exchangeable Senior Debentures |

5.50 | % | $ | 266,400 | — | — | — | — | — | $ | 266,400 | |||||||||||||||||||||

| Prudential Unsecured Senior Notes |

||||||||||||||||||||||||||||||||

| Series C |

9.68 | % | — | — | $ | 25,000 | — | — | — | $ | 25,000 | |||||||||||||||||||||

| Series D |

4.57 | % | — | 50,000 | — | — | — | — | 50,000 | |||||||||||||||||||||||

| Series E |

5.73 | % | — | — | — | 50,000 | — | — | 50,000 | |||||||||||||||||||||||

| Series F |

4.50 | % | — | 17,000 | — | — | — | — | 17,000 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total Prudential Unsecured Senior Notes |

5.87 | % | — | $ | 67,000 | $ | 25,000 | $ | 50,000 | — | — | $ | 142,000 | |||||||||||||||||||

| Mortgage Loans |

||||||||||||||||||||||||||||||||

| Secured Term Debt (4) |

5.65 | % | $ | 132,966 | — | — | — | — | — | $ | 132,966 | |||||||||||||||||||||

| 200 Paul Avenue |

5.74 | % | 2,048 | 68,665 | — | — | — | — | 70,713 | |||||||||||||||||||||||

| 2045 & 2055 LaFayette Street |

5.93 | % | 1,060 | 1,125 | 1,195 | 60,243 | — | — | 63,623 | |||||||||||||||||||||||

| 34551 Ardenwood Boulevard |

5.95 | % | 812 | 862 | 50,478 | — | — | — | 52,152 | |||||||||||||||||||||||

| 1100 Space Park Drive |

5.89 | % | 821 | 871 | 50,423 | — | — | — | 52,115 | |||||||||||||||||||||||

| 150 South First Street |

6.30 | % | 781 | 832 | 878 | 47,606 | — | — | 50,097 | |||||||||||||||||||||||

| 600 West Seventh Street |

5.80 | % | 1,723 | 1,825 | 46,000 | — | — | — | 49,548 | |||||||||||||||||||||||

| 2334 Lundy Place |

5.96 | % | 590 | 627 | 36,713 | — | — | — | 37,930 | |||||||||||||||||||||||

| Cressex 1 |

5.68 | % | 28,583 | — | — | — | — | — | 28,583 | |||||||||||||||||||||||

| 636 Pierce Street |

5.27 | % | 1,778 | 1,940 | 2,043 | 2,155 | 2,454 | 15,957 | 26,327 | |||||||||||||||||||||||

| Manchester Technopark |

5.68 | % | 8,695 | — | — | — | — | — | 8,695 | |||||||||||||||||||||||

| 8025 North Interstate 35 |

4.09 | % | 257 | 268 | 5,789 | — | — | — | 6,314 | |||||||||||||||||||||||

| 731 East Trade Street |

8.22 | % | 350 | 416 | 504 | 546 | 593 | 1,777 | 4,186 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total Mortgage Loans |

5.81 | % | $ | 180,464 | $ | 77,431 | $ | 194,023 | $ | 110,550 | $ | 3,047 | $ | 17,734 | $ | 583,249 | ||||||||||||||||

| Total unhedged variable rate debt |

— | — | — | — | $ | 1,184,708 | — | $ | 1,184,708 | |||||||||||||||||||||||

| Total fixed rate / hedged variable rate debt |

446,864 | 519,431 | 219,023 | 160,550 | 563,991 | 1,880,014 | 3,789,873 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total Debt |

3.92 | % | $ | 446,864 | $ | 519,431 | $ | 219,023 | $ | 160,550 | $ | 1,748,699 | $ | 1,880,014 | $ | 4,974,581 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

Summary

| Weighted Average Term to Initial Maturity (2) | 4.9 Years | |

| Weighted Average Maturity (assuming exercise of extension options) (3) | 5.2 Years | |

| (1) | Assumes all extensions will be exercised. |

| (2) | Assumes maturity of 5.50% exchangeable senior debentures due 2029 at first redemption date in April 2014. |

| (3) | Assumes exercise of extension options and maturity of 5.50% exchangeable senior debentures due 2029 at first redemption date in April 2014. |

| (4) | This amount represents six mortgage loans secured by our interests in 36 NE 2nd Street, 3300 East Birch Street, 100 & 200 Quannapowitt Parkway, 300 Boulevard East, 4849 Alpha Road, and 11830 Webb Chapel Road. Each of these loans is cross-collateralized by the six properties. |

| Note: | Total excludes $2,359 of loan premiums, net and ($4,672), ($5,779), ($377), ($693), and ($3,527) of debt discount on 4.25% unsecured senior notes due 2025, 5.875% unsecured senior notes due 2020, 4.50% unsecured senior notes due 2015, 5.25% unsecured senior notes due 2021, and 3.625% unsecured senior notes due 2022, respectively. |

Page 14

| Debt Analysis & Covenant Compliance |

|

Financial Supplement | ||

| Unaudited | Fourth Quarter 2013 |

| As of December 31, 2013 | ||||||||||||||||

| 4.50% Notes due 2015 5.875% Notes due 2020 5.25% Notes due 2021 |

3.625% Notes due 2022 4.250% Notes due 2025 |

Global Revolving Credit Facility | ||||||||||||||

| Required | Actual | Actual | Required | Actual | ||||||||||||

| Debt Covenant Ratios (1) |

||||||||||||||||

| Total outstanding debt / total assets (2) |

Less than 60% | 44 | % | 41 | % | Less than 60% (3) | 37 | % | ||||||||

| Secured debt / total assets (4) |

Less than 40% | 5 | % | 5 | % | Less than 40% | 5 | % | ||||||||

| Total unencumbered assets / unsecured debt |

Greater than 150% | 233 | % | 251 | % | N/A | N/A | |||||||||

| Consolidated EBITDA / interest expense (5) |

Greater than 1.50x | 4.0x | 4.0x | N/A | N/A | |||||||||||

| Fixed charge coverage |

N/A | N/A | Greater than 1.50x | 3.3x | ||||||||||||

| Unsecured debt / total unencumbered asset value (6) |

N/A | N/A | Less than 60% | 41 | % | |||||||||||

| Unencumbered assets debt service coverage ratio |

N/A | N/A | Greater than 1.50x | 4.9x | ||||||||||||

| (1) | For a definition of the terms used in the table above and related footnotes, please refer to: the Indenture dated January 28, 2010, which governs the 5.875% Notes due 2020; the Indenture dated July 8, 2010, which governs the 4.50% Notes due 2015; the Indenture and Supplemental Indenture No. 1 dated March 8, 2011, which governs the 5.25% Notes due 2021; the Indenture and Supplemental Indenture No. 1 dated September 24, 2012, which governs the 3.625% Notes due 2022; the Indenture dated January 18, 2013, which governs the 4.250% Notes due 2025; and the Global Senior Credit Agreement dated as of August 15, 2013, which are filed as exhibits to our reports filed with the Securities and Exchange Commission. |

| (2) | This ratio is referred to as the Leverage Ratio, defined as Consolidated Debt / Total Asset Value, under the Global Revolving Credit Facility. Under the 4.50% Notes due 2015, 5.875% Notes due 2020, and 5.25% Notes due 2021, Total Assets is calculated using Consolidated EBITDA capped at 9.0%. Under the 3.625% Notes due 2022 and 4.250% Notes due 2025, Total Assets is calculated using Consolidated EBITDA capped at 8.25%. Under the Global Revolving Credit Facility, Total Asset Value is calculated using Adjusted Net Operating Income capped at 8.00% for Data Center Assets and 7.50% for Other Assets. |

| (3) | The Company has the right to maintain a Leverage Ratio of greater than 60.0% but less than or equal to 65.0% for up to four consecutive fiscal quarters during the term of the Facility following an acquisition of one or more Assets for a purchase price and other consideration in an amount not less than 5% of Total Asset Value. |

| (4) | This ratio is referred to as the Secured Debt Leverage Ratio, defined as Secured Debt / Total Asset Value, under the Global Revolving Credit Facility. |

| (5) | Calculated as current quarter annualized Consolidated EBITDA to current quarter annualized Interest Expense (including capitalized interest and debt discounts). |