Attached files

| file | filename |

|---|---|

| EX-3.3 - EX-3.3 - TRINET GROUP, INC. | d572726dex33.htm |

| EX-23.2 - EX-23.2 - TRINET GROUP, INC. | d572726dex232.htm |

| EX-23.4 - EX-23.4 - TRINET GROUP, INC. | d572726dex234.htm |

| EX-23.3 - EX-23.3 - TRINET GROUP, INC. | d572726dex233.htm |

Table of Contents

As filed with the Securities and Exchange Commission on January 6, 2014

Registration No. 333-192465

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

TRINET GROUP, INC.

(Exact name of Registrant as specified in its charter)

| Delaware | 7389 | 95-3359658 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

1100 San Leandro Blvd., Suite 400

San Leandro, CA 94577

(510) 352-5000

(Address, including zip code and telephone number, including area code, of Registrant’s principal executive offices)

Burton M. Goldfield

Chief Executive Officer

TriNet Group, Inc.

1100 San Leandro Blvd., Suite 400

San Leandro, CA 94577

(510) 352-5000

(Name, address, including zip code and telephone number, including area code, of agent for service)

Copies to:

| Jodie M. Bourdet Craig D. Jacoby Andrew S. Williamson Cooley LLP 101 California Street, 5th Floor San Francisco, California 94111 (415) 693-2000 |

Gregory L. Hammond Chief Legal Officer TriNet Group, Inc. 1100 San Leandro Blvd., Suite 400 San Leandro, CA 94577 (510) 352-5000 |

Gordon K. Davidson Daniel J. Winnike Fenwick & West LLP 801 California Street Mountain View, CA 94041 (650) 988-8500 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | þ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion, dated January 6, 2014.

Prospectus

Shares

Common Stock

This is an initial public offering of shares of common stock of TriNet Group, Inc.

We are offering shares of our common stock. The selling stockholders identified in this prospectus are offering an additional shares. We will not receive any of the proceeds from the sale of the shares being sold by the selling stockholders.

Prior to this offering, there has been no public market for our common stock. It is currently estimated that the initial public offering price per share will be between $ and $ . We intend to list our common stock on the under the symbol “ .”

| Per Share | Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discount |

$ | $ | ||||||

| Proceeds, before expenses, to TriNet |

$ | $ | ||||||

| Proceeds, before expenses, to the selling stockholders |

$ | $ | ||||||

have granted the underwriters an option to purchase up to an additional shares at the initial public offering price, less the underwriting discount.

See “Risk Factors” beginning on page 14 to read about factors you should consider before buying shares of our common stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares against payment in New York, New York on , 2014.

| J.P. Morgan | Morgan Stanley | Deutsche Bank Securities | ||

| Jefferies | Stifel | William Blair | ||

Prospectus dated , 2014

Table of Contents

| Page | ||||

| 1 | ||||

| 8 | ||||

| 10 | ||||

| 14 | ||||

| 33 | ||||

| 35 | ||||

| 36 | ||||

| 37 | ||||

| 38 | ||||

| 40 | ||||

| 42 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

48 | |||

| 88 | ||||

| 103 | ||||

| 111 | ||||

| 129 | ||||

| 130 | ||||

| 133 | ||||

| 137 | ||||

| Material United States Federal Income Tax Consequences to Non-U.S. Holders of Our Common Stock |

139 | |||

| 142 | ||||

| 146 | ||||

| 146 | ||||

| 146 | ||||

| F-1 | ||||

Neither we, the selling stockholders nor the underwriters have authorized anyone to give any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared. Neither we, the selling stockholders nor the underwriters take responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, and only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date.

Through and including , 2014 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

Persons who come into possession of this prospectus and any applicable free writing prospectus we have prepared in jurisdictions outside the United States are required to inform themselves about and to observe any restrictions in this offering and the distribution of this prospectus and any such free writing prospectus applicable to that jurisdiction.

i

Table of Contents

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our common stock, you should read the entire prospectus carefully, including the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes included elsewhere in this prospectus. Unless the context suggests otherwise, references in this prospectus to “TriNet,” the “Company,” “we,” “us” and “our” refer to TriNet Group, Inc. and, where appropriate, its subsidiaries.

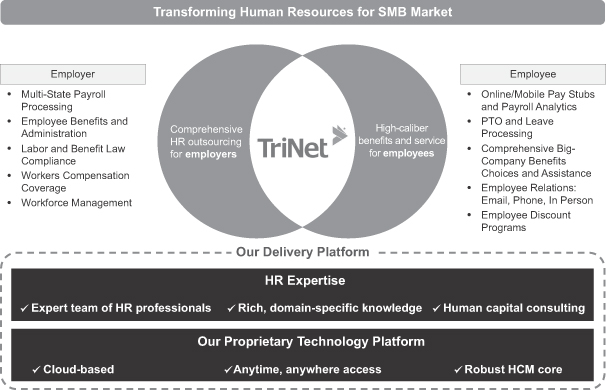

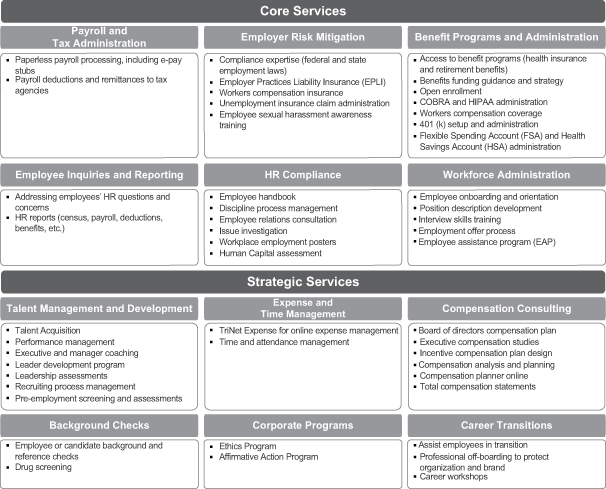

Company Overview

TriNet is a leading provider of a comprehensive human resources solution for small to medium-sized businesses, or SMBs. We enhance business productivity by enabling our clients to outsource their human resources, or HR, function to one strategic partner and allowing them to focus on operating and growing their core businesses. Our HR solution includes services such as payroll processing, human capital consulting, employment law compliance and employee benefits, including health insurance, retirement plans and workers compensation insurance. Our services are delivered by our expert team of HR professionals and enabled by our proprietary, cloud-based technology platform, which allows our clients and their employees to efficiently conduct their HR transactions anytime and anywhere. As of September 30, 2013, we served over 8,000 clients in 47 states, the District of Columbia and Canada and co-employed approximately 218,000 of our clients’ employees, which we refer to as worksite employees, or WSEs. In 2012, we processed over $10 billion in payroll and insurance premiums for our clients.

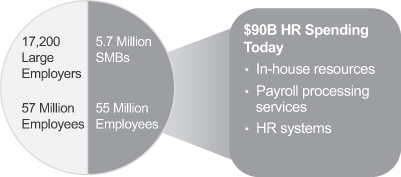

HR is a mission-critical function for businesses. Businesses of all sizes face increasing levels of complexity in managing HR processes, including regulatory pressures and escalating healthcare costs. These challenges are especially acute for SMBs, which typically lack the scale and capability to solve many of these issues on their own. In 2011, there were approximately 5.7 million employers with 500 or fewer employees. These SMBs employed approximately 55 million people in the United States, or 49% of all U.S. employees, and represented over 99% of all U.S. employers in 2011. We estimate that in 2013, SMBs will spend approximately $90 billion on in-house HR resources, payroll processing and other HR services. We believe that this in-house approach is more challenging for SMBs to manage, and is less effective and more costly as compared to our comprehensive, outsourced solution. Therefore, we believe that this presents a significant opportunity for us to continue to penetrate and expand our presence in the SMB market.

We offer our clients a bundled solution that enables them to outsource their HR function to a single provider. We believe that the combination of our HR professionals, full suite of services, vertical market orientation, broad geographic reach and powerful technology platform enables us to solve the HR challenges of our SMB clients. Our solution helps reduce the complexity, cost and risk of managing the HR function for our SMB clients while helping SMBs better retain their employees. In addition, our tailored approach allows us to serve a diverse range of industries with varying levels of HR requirements. For our clients’ employees, we provide access to high-caliber, big-company benefits, timely payroll processing and anytime and anywhere system access. We are also able to leverage our strong and diverse partner relationships to provide a broad and rich suite of services and benefits for our clients and their employees. We believe that this provides us with a highly referenceable customer base that allows us to further penetrate our target vertical markets.

Our proprietary, cloud-based technology platform and our team of HR professionals make HR transactions simple, seamless and efficient for employers and employees. Our platform is designed to function as the core system of record for all of our clients’ HR activities and allows our clients to enjoy 24/7, ubiquitous access. Our platform is also highly scalable, allowing us to efficiently add new clients and grow with our existing clients.

We sell our services primarily through our direct sales force, which we align around target vertical markets, including technology, life sciences, property management, professional services, banking and financial services,

1

Table of Contents

retail, manufacturing and hospitality services. The HR needs of our clients are influenced by the industry in which they operate. For example, wage and hour compliance and workers compensation are important components of our solution for clients in the food service industry, and retirement plans and specialized employee perquisites are significant components of the solution we provide to clients in the financial services industry. We believe that our vertical market expertise and tailored service offerings differentiate us in the market and allow us to compete more effectively. We acquire this expertise organically, by hiring individuals who are experienced in the markets that we target for our services. For example, we hire experienced sales persons and human capital consultants within the technology industry in order to build service teams that will understand the needs of our technology clients. Attracting employees with these skills in turn helps to increase the expertise and sophistication of our employees as they serve clients within a vertical industry. We also acquire vertical market expertise through our acquisitions. For example, we acquired significant expertise in blue- and gray-collar vertical markets such as property management and food services with our acquisition of SOI Holdings, Inc., and in the high-end financial services industry with our acquisition of Ambrose Employer Group, LLC. The industry-specific expertise we obtain through acquisitions allows us to better understand the needs of our clients and package the services we provide accordingly.

Our total revenues consist of professional service revenues and insurance service revenues. For 2012 and the nine months ended September 30, 2013, 15% and 17% of our total revenues, respectively, consisted of professional service revenues, and 85% and 83% of our total revenues, respectively, consisted of insurance service revenues. We earn professional service revenues by processing HR transactions, such as payroll and employment tax withholding, and providing labor and benefit law compliance services, on behalf of our clients. We earn insurance service revenues by providing risk-based, third-party plans to our clients, primarily employee health benefit plans and workers compensation insurance.

For professional service revenues, we recognize as revenues the fees we earn for processing HR transactions, which fees do not include the payroll that is paid to us by the client and paid out to WSEs or remitted as taxes. We recognize as insurance service revenues all insurance-related billings and administrative fees collected from clients and withheld from WSEs for risk-based insurance plans provided through third-party insurance carriers, primarily employee health insurance and workers compensation insurance. We in turn pay premiums to third-party insurance carriers for these insurance benefits, as well as reimburse them for claim payments within our insurance deductible layer. These premiums and reimbursements are classified as insurance costs on our statements of operations. To augment our financial information prepared in accordance with U.S. generally accepted accounting principles, or GAAP, we use internally a non-GAAP financial measure, Net Insurance Service Revenues, which consists of insurance service revenues less insurance costs. We also use a measure of total non-GAAP revenue, or Net Service Revenues, which is the sum of professional service revenues and Net Insurance Service Revenues. For 2012 and the nine months ended September 30, 2013, 55% and 66% of our Net Service Revenues, respectively, consisted of professional service revenues and 45% and 34% of our Net Service Revenues, respectively, consisted of Net Insurance Service Revenues.

We have grown our business organically and through strategic acquisitions. For 2010, 2011 and 2012, our total revenues were $906.2 million, $840.4 million and $1.0 billion, respectively, our Net Service Revenues were $192.5 million, $189.3 million and $269.0 million, respectively, and our net income (loss) was $(9.6 million), $15.5 million and $31.8 million, respectively. For the nine months ended September 30, 2012 and 2013, our total revenues were $696.9 million and $1.2 billion, respectively, our Net Service Revenues were $178.5 million and $296.0 million, respectively, and our net income was $23.0 million and $7.1 million, respectively. For 2010, 2011 and 2012, our Adjusted EBITDA was $29.8 million, $47.3 million and $95.4 million, respectively. For the nine months ended September 30, 2012 and 2013, our Adjusted EBITDA was $61.5 million and $92.3 million, respectively.

2

Table of Contents

Our Market Opportunity

We serve the HR needs of SMBs in the United States. The growing complexity of managing HR processes today presents a significant challenge for SMBs. Traditionally, SMBs have managed HR processes in-house through a range of separately delivered services rather than seeking a holistic and comprehensive solution, which we believe has further aggravated many of these challenges. We believe that a bundled HR solution better addresses these needs and allows SMBs to focus in-house resources on business operations instead of managing HR activities. As a result, we believe that this represents a significant opportunity for TriNet’s solution.

Large and Underpenetrated Market. SMBs employ a large percentage of the total employee base in the United States today. According to the U.S. Census Bureau, in 2011, approximately 55 million employees were employed by organizations with fewer than 500 employees, representing approximately 49% of U.S. employees. These SMBs comprised approximately 5.7 million business organizations, representing over 99% of U.S. employers in 2011. Though smaller, these companies have HR needs similar to their larger counterparts, including payroll, employee benefits and many other HR services for employees, and spend significant amounts on managing these processes. We estimate that in 2013 SMBs will spend approximately $90 billion in providing HR services, and that most of this spending will be on in-house resources. Based on data published by the National Association of Professional Employer Organizations, we estimate that in 2012 fewer than 5% of U.S. employees of businesses with fewer than 500 employees were part of a co-employment arrangement, in which all or some portion of the employer’s HR function was outsourced to a single third-party provider such as TriNet. We believe that our growth opportunity is primarily a function of our ability to increase our penetration of the SMB market.

HR Management Increasing in Complexity. The HR function is becoming increasingly complex. The scope of responsibilities and demands on HR departments continues to expand beyond the management of payroll and benefits as firms compete to attract, retain and motivate employees. In addition, external pressures continue to mount as firms must deal with the increased complexity of the laws and regulations that govern the provision and administration of HR services, including effectively managing multiple and disparate state and federal laws and regulations. As a recent example, the Patient Protection and Affordable Care Act, enacted in March 2010, imposes a staggered schedule of sweeping health care reforms, which began in 2010 and will continue through 2018, and which will put increased burdens on many employers.

Challenges Are Especially Acute for SMBs. SMBs typically confront an array of challenges as they seek to address increasingly complex HR requirements. These organizations frequently lack the dedicated and specialized personnel and systems that are necessary to provide complex HR solutions. According to The Bureau of National Affairs, Inc., in 2013, 39% of the smallest (fewer than 250 workers) organizations surveyed do not have an HR specialist on staff. Conversely, 90% of the largest (more than 2,500 workers) organizations surveyed have at least one employee devoted to just one or two areas of HR. Additionally, a large portion of HR-related spending by SMBs has traditionally been on a range of disparate products and services, where companies utilize a combination of third-party service and technology providers and in-house resources to administer the HR function. We believe that this approach of utilizing a combination of various third-party providers further complicates the delivery of HR services, dilutes the benefit that HR processes can have on an organization, and is typically more costly than a bundled solution. Lastly, SMBs typically cannot afford to invest in a comprehensive technology platform to manage their HR processes and often lack the scale required to negotiate favorable employee health benefit and workers compensation plan terms with insurance companies and other large employee benefits providers. As a result, we believe that SMBs will increasingly look to a bundled solution to help solve these issues.

Our Solution

We offer our clients a bundled solution that enables them to outsource their HR function to one strategic partner, so they can focus on operating and growing their core businesses. Our bundled solution, which includes services such as payroll processing, human capital consulting, employment law compliance and employee benefits, including health insurance, retirement plans and workers compensation insurance, holistically addresses

3

Table of Contents

the HR needs of both our clients and their employees. For each of our clients, we offer timely payroll processing and access to a team of HR professionals with specific knowledge of its industry to help reduce the complexity, cost and risk of managing the HR function, while helping them better retain their workforce. For employees, we provide access to high-caliber, big-company benefits and other services such as expert HR guidance and anytime, anywhere access to comprehensive HR information and services. We leverage our strong and diverse partner relationships to provide a broad and rich suite of services for our clients and their employees.

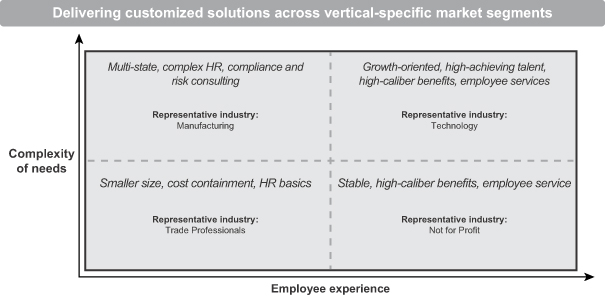

We serve a number of large vertical markets. Businesses in these vertical markets have HR requirements that vary across two primary dimensions: (1) the complexity of HR needs and (2) the importance of employee benefits and a high touch service experience. We believe that our ability to address our target vertical markets across these dimensions is a clear competitive differentiator.

Our vertical market expertise allows us to tailor our services for our target industries, which helps to further embed us within our clients and helps us to deliver meaningful business impact. Our solution is delivered by a team of HR professionals with expertise in our clients’ industries, enabled by our proprietary, cloud-based technology platform, which simplifies the day-to-day HR transactions of our clients and their employees. Our platform provides SMBs with the knowledge and features of large-business support and technology, as well as anywhere and any-device access to their HR systems. Our platform is also highly scalable, allowing our clients to efficiently add new employees and us to grow with our existing clients. Its seamless integration with partner systems allows single-sign-on functionality that enhances the employee and employer experience.

Our Competitive Advantages

We believe that we have the following key competitive advantages:

Comprehensive Suite of HR Capabilities. We are the strategic HR partner to our clients. Our innovative bundled solution, developed over our 25-year operating history, allows our clients to outsource their HR function

4

Table of Contents

to a single provider in an effective and cost-efficient manner. As the provider of a bundled solution, we deliver our services in a coordinated and comprehensive manner, which provides significant value to our clients by reducing the complexity of managing the HR function. The services that we provide are delivered through a combination of HR professionals and our proprietary, cloud-based technology platform. Each TriNet client is guided by a team of HR professionals with expertise in both complex and day-to-day HR questions and challenges, ensuring a high level of customer service and attention throughout the client’s organization. In addition to our HR services such as payroll processing and human capital consulting, we also offer our clients and their employees access to a broad range of big-company employee benefits plans, and our risk management tools allow us to significantly mitigate employer risk, such as compliance, legal and related risks, including workers compensation and employee practices liability insurance.

Deep Vertical Market Expertise. We focus on serving clients in specific industry vertical markets. We have developed deep expertise around the HR functions within our target industries, which enables us to provide our clients with a solution tailored to the industries in which they operate. Our direct sales force and go-to-market strategy is aligned with these vertical markets, which enhances our client value proposition and allows us to leverage our strong institutional knowledge to further expand our presence within these target industries. We believe that this verticalized approach allows us to target clients across a range of industries in which SMBs have varying levels of need for services based on the complexity of their HR environment and required employee experience.

Proprietary, Cloud-Based Technology Platform. Our proprietary, cloud-based technology platform enables our clients and their employees to conduct their HR transactions anytime and anywhere. Our platform offers online self-service tools for managing employee payroll, creating compensation reports, managing employee hiring and termination and managing health benefits. As a result of our long-standing partnerships and the significant investments that we have made in our platform, our technology and benefits services partners are able to integrate their systems with our platform, allowing employees to access a unified view of all of their pertinent HR information. In addition, our platform allows clients to leverage information about their workforce in real time to keep tactical HR demands under control. Our platform is also highly scalable, which allows our clients to efficiently add new employees.

Scale. We are able to leverage our national presence and large WSE base to provide a comprehensive and cost-effective solution to our clients. SMBs typically lack the scale required to negotiate favorable employee health benefit plan prices and other features with insurance companies and other large employee benefits providers. Leveraging the economies of scale arising from serving approximately 218,000 WSEs, we are able to make significant investments in our technology platform and are typically able to secure a broader range of benefits plans at rates and with features that are more competitive than those that an SMB would be able to procure on its own. In addition, our scale has allowed us to specialize our workforce by industry vertical markets and deliver more relevant services to our clients.

Strong Strategic Partnerships. We have developed strong relationships with our insurance and risk management partners, as well as other vendors and suppliers, which we believe enable us to provide a broader array of services to our clients and their employees more cost-effectively than if they attempted to purchase these offerings themselves. We have long-standing relationships with large health benefits insurers, such as Aetna, Blue Shield of California, Blue Cross and Blue Shield of Florida, Kaiser Permanente, MetLife and United Healthcare, as well as retirement plan providers, such as Transamerica Retirement Services and MassMutual. We believe that we are a valuable partner for our insurance and other service vendors, as we provide them with an attractive channel to the hard-to-reach SMB market through our large scale presence across the United States and Canada, and across a wide range of industry vertical markets.

5

Table of Contents

Our Growth Strategies

Our goal is to become the leading HR solutions provider to SMBs. Our strategies to achieve that goal include the following:

| • | Continue to Penetrate the SMB Market Using Our Vertical Market Approach. Our focus on serving clients in specific industry vertical markets has given us deep, substantive knowledge of the HR needs facing SMBs in those industries. This enables us to provide a bundled solution of services to each client that is tailored to its specific needs and better enables us to attract sales professionals with industry expertise. We intend to continue this focus on industry vertical markets. We also regularly assess additional and new industry vertical markets and intend to add them, either through acquisition or internal development, selectively based on what we believe the market opportunity is. |

| • | Expand Our Direct Sales Force. We believe that the SMB market remains significantly underpenetrated for a bundled HR solution such as ours. We intend to continue to invest in our direct sales force to enable us to identify and acquire new clients across our target vertical markets, in addition to expanding our sales force to target new vertical markets. |

| • | Grow With Our Clients by Enhancing the Breadth and Quality of Our Services. We intend to continue to expand the breadth and quality of our HR solution. We believe that this will allow us to continue to enhance the value proposition for our clients and to grow with them by providing additional high-quality service offerings. |

| • | Continue to Enhance Our Technology Platform. We intend to continue to invest in and improve our proprietary, cloud-based technology platform, including mobile applications, in order to provide our clients with enhanced features and functionality with which to conduct their HR transactions, manage employees and analyze employee benefits data. This may include acquiring or developing additional functionality or technology. |

| • | Continue to Grow Through Strategic Acquisitions. We have successfully completed numerous strategic acquisitions over the course of the past decade, which has allowed us to enhance and expand our presence in both existing and new target industries as well as expand our solution and technology platform. We intend to continue to pursue strategic acquisitions that will enable us to leverage our existing assets and offer our clients more comprehensive and attractive services. |

Risks Associated with Our Business

Our business is subject to numerous risks and uncertainties, including those highlighted in the section titled “Risk Factors” immediately following this prospectus summary. Some of these risks are:

| • | our success depends on growth in market acceptance of the HR outsourcing and related services we provide; |

| • | if we are unable to rapidly grow our sales force, we will not be able to grow our business at the rate that we anticipate, which could harm our business, results of operations and financial condition; |

| • | we are subject to client attrition; |

| • | our acquisition strategy creates risks for our business; |

| • | unexpected changes in workers compensation and health insurance claims by worksite employees could harm our business; |

| • | our quarterly results of operations may fluctuate as a result of numerous factors, many of which are outside of our control; |

6

Table of Contents

| • | our business is subject to numerous state and federal laws, and uncertainty as to the application of these laws, or adverse applications of these laws, as well as changes in applicable laws, could adversely affect our business; |

| • | if we are not recognized as an employer of worksite employees under federal and state regulations, we and our clients could be adversely impacted; |

| • | we and our clients could be adversely impacted by health care reform; |

| • | we may have additional tax liabilities, which could harm our business, operating results, financial condition and prospects; |

| • | our business and operations have experienced rapid growth in recent periods, and if we are unable to effectively manage this growth, our business and results of operations may suffer; |

| • | we may not be able to sustain our revenue growth rate or profitability in the future; |

| • | our industry is highly competitive, which may limit our ability to maintain or increase our market share or improve our results of operations; |

| • | adverse changes in our relationships with key vendors could impair the quality of our solution; |

| • | we depend on licenses to third-party software in order to provide our services; and |

| • | we have a substantial amount of indebtedness, which could adversely affect our financial condition and our operating flexibility. |

Corporate Information

We were incorporated in 1988 as TriNet Employer Group, Inc., a California corporation. We reincorporated as TriNet Group, Inc., a Delaware corporation, in 2000. Our principal executive offices are located at 1100 San Leandro Blvd., Suite 400, San Leandro, CA 94577 and our telephone number is (510) 352-5000. Our website address is www.trinet.com. Information contained on or accessible through our website is not a part of this prospectus and should not be relied upon in determining whether to make an investment decision.

TriNet, TriNet Group, SOI, Ambrose, Accord and ExpenseCloud and their associated logos and other trade names, trademarks or service marks of TriNet appearing in this prospectus are the property of TriNet. Trade names, trademarks and service marks of other companies appearing in this prospectus are the property of their respective holders.

Upon the completion of this offering, funds affiliated with General Atlantic will beneficially own approximately % of our outstanding common stock.

7

Table of Contents

| Common stock offered by TriNet |

shares |

| Common stock offered by the selling stockholders |

shares |

| Common stock to be outstanding after this offering |

shares |

| Option to purchase additional shares of common stock offered by |

shares |

| Use of proceeds |

We estimate that our net proceeds from this offering will be approximately $ million, based on an assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

| We intend to use the net proceeds to us from this offering to repay approximately $200 million of indebtedness outstanding under our credit facilities and for working capital and other general corporate purposes. We may also use a portion of the net proceeds from this offering for acquisitions of, or investments in, technologies, assets or businesses that complement our business, although we have no present commitments or agreements to enter into such acquisitions or investments. We will not receive any of the proceeds from the sale of shares to be offered by the selling stockholders. See “Use of Proceeds” for additional information. |

| Risk factors |

See “Risk Factors” beginning on page 14 and the other information included in this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

| Qualified Independent Underwriter |

Affiliates of J.P. Morgan Securities LLC, Morgan Stanley & Co. LLC and Deutsche Bank Securities Inc., underwriters in this offering, are lenders under our credit facilities and will receive more than 5% of the net proceeds of this offering in connection with our repayment of approximately $200 million of indebtedness under our credit facilities, as set forth under “Use of Proceeds.” Accordingly, this offering is being made in compliance with the requirements of Rule 5121 of the Financial Industry Regulatory Authority, Inc. In accordance with this rule, Jefferies LLC has assumed the responsibilities of acting as a qualified independent underwriter. In its role as qualified independent underwriter, Jefferies LLC has participated in due diligence and the preparation of this prospectus and the registration statement of which this prospectus is a part. Jefferies LLC will not receive any additional fees for serving as a qualified independent underwriter in connection with this offering. Affiliates of |

8

Table of Contents

| J.P. Morgan Securities LLC, Morgan Stanley & Co. LLC and Deutsche Bank Securities Inc. will not confirm sales of the shares to any account over which it exercises discretionary authority without the prior written approval of the customer. |

| Proposed symbol |

The number of shares of common stock to be outstanding after this offering is based on 26,449,910 shares of our common stock (including preferred stock on an as-converted basis) outstanding as of September 30, 2013, and excludes:

| • | 3,343,372 shares of common stock issuable upon the exercise of outstanding stock options as of September 30, 2013 pursuant to our 2000 Equity Incentive Plan, or our 2000 Plan, and our 2009 Equity Incentive Plan, or our 2009 Plan, at a weighted average exercise price of $2.85 per share; |

| • | 3,266 shares of common stock issuable upon the settlement of restricted stock units as of September 30, 2013 pursuant to our 2009 Plan; |

| • | shares of common stock issuable upon the exercise of outstanding stock options issued after September 30, 2013 pursuant to our 2009 Plan at a weighted average exercise price of $ ; |

| • | shares of common stock to be reserved for future issuance under our 2009 Plan, as amended in connection with this offering, as well as any automatic increases in the number of shares of common stock reserved for future issuance under this benefit plan; and |

| • | shares of common stock to be reserved for issuance under our 2013 Employee Stock Purchase Plan, or our ESPP, to be effective in connection with this offering, as well as any automatic increases in the number of shares of common stock reserved for future issuance under this benefit plan. |

In addition, unless we specifically state otherwise, all information in this prospectus assumes:

| • | that the two-for-one split of our common stock that occurred in July 2013 occurred as of the first date presented in this prospectus; |

| • | the conversion of all outstanding shares of our preferred stock into an aggregate of 19,032,854 shares of common stock immediately prior to the completion of this offering; |

| • | no exercise of options outstanding; |

| • | no exercise of the underwriters’ option to purchase up to an additional shares of common stock from ; and |

| • | the filing of our amended and restated certificate of incorporation in Delaware and the adoption of our amended and restated bylaws, each of which will occur immediately prior to the completion of this offering. |

9

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA

The following tables summarize our consolidated financial and other data. You should read this summary consolidated financial and other data together with the sections titled “Selected Consolidated Financial and Other Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” as well as our consolidated financial statements and related notes included elsewhere in this prospectus.

We have derived the consolidated statement of operations data for the years ended December 31, 2010, 2011 and 2012 from our audited consolidated financial statements that are included elsewhere in this prospectus. We have derived the unaudited consolidated statement of operations data for the nine months ended September 30, 2012 and 2013 and the unaudited consolidated balance sheet data as of September 30, 2013 from our unaudited consolidated financial statements that are included elsewhere in this prospectus. Our unaudited consolidated financial statements have been prepared on the same basis as our audited consolidated financial statements and, in the opinion of management, reflect all adjustments, which consist only of normal recurring adjustments, necessary for the fair statement of those unaudited consolidated financial statements. Our historical results are not necessarily indicative of the results that should be expected in the future, and our interim results are not necessarily indicative of the results that should be expected for the full year or any other period.

10

Table of Contents

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2010 | 2011 | 2012 | 2012 | 2013 | ||||||||||||||||

| (in thousands, except share and per share data) | ||||||||||||||||||||

| Consolidated Statement of Operations Data: |

||||||||||||||||||||

| Professional service revenues |

$ | 139,495 | $ | 113,279 | $ | 148,233 | $ | 94,892 | $ | 195,642 | ||||||||||

| Insurance service revenues |

766,695 | 727,111 | 870,828 | 601,967 | 959,246 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total revenues |

906,190 | 840,390 | 1,019,061 | 696,859 | 1,154,888 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Costs and operating expenses: |

||||||||||||||||||||

| Insurance costs |

713,653 | 651,094 | 750,025 | 518,386 | 858,862 | |||||||||||||||

| Cost of providing services (exclusive of depreciation and amortization of intangible assets)(1) |

72,073 | 59,388 | 63,563 | 44,944 | 74,042 | |||||||||||||||

| Sales and marketing(1) |

46,454 | 38,087 | 59,931 | 39,377 | 79,387 | |||||||||||||||

| General and administrative(1) |

28,366 | 31,421 | 37,879 | 24,147 | 39,821 | |||||||||||||||

| Systems development and programming costs(1) |

15,045 | 15,646 | 16,718 | 11,893 | 15,140 | |||||||||||||||

| Amortization of intangible assets |

17,960 | 12,388 | 17,441 | 7,853 | 35,926 | |||||||||||||||

| Depreciation |

12,042 | 9,201 | 11,676 | 9,100 | 8,908 | |||||||||||||||

| Restructuring |

5,922 | 2,358 | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total costs and operating expenses |

911,515 | 819,583 | 957,233 | 655,700 | 1,112,086 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating income (loss) |

(5,325 | ) | 20,807 | 61,828 | 41,159 | 42,802 | ||||||||||||||

| Other income (expense): |

||||||||||||||||||||

| Interest expense |

(4,444 | ) | (751 | ) | (9,709 | ) | (2,835 | ) | (32,091 | ) | ||||||||||

| Other, net |

67 | 127 | 57 | 22 | 309 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) before provision for (benefit from) income taxes |

(9,702 | ) | 20,183 | 52,176 | 38,346 | 11,020 | ||||||||||||||

| Provision for (benefit from) income taxes |

(100 | ) | 4,646 | 20,344 | 15,386 | 3,880 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

$ | (9,602 | ) | $ | 15,537 | $ | 31,832 | $ | 22,960 | $ | 7,140 | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) per share attributable to common stock: |

||||||||||||||||||||

| Basic |

$ | (2.58 | ) | $ | 0.68 | $ | 1.33 | $ | 0.97 | $ | 0.29 | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted |

$ | (2.58 | ) | $ | 0.65 | $ | 1.26 | $ | 0.92 | $ | 0.27 | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Weighted average common stock outstanding: |

||||||||||||||||||||

| Basic |

3,727,195 | 3,921,341 | 4,902,692 | 4,728,686 | 5,750,789 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted |

3,727,195 | 5,051,990 | 6,238,046 | 6,002,628 | 7,598,197 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Pro forma net income per share: |

||||||||||||||||||||

| Basic |

$ | $ | ||||||||||||||||||

|

|

|

|

|

|||||||||||||||||

| Diluted |

$ | $ | ||||||||||||||||||

|

|

|

|

|

|||||||||||||||||

| Pro forma weighted average shares of common stock outstanding: |

||||||||||||||||||||

| Basic |

||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||

| Diluted |

||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||

11

Table of Contents

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2010 | 2011 | 2012 | 2012 | 2013 | ||||||||||||||||

| Key Operating Metrics and Other Financial Data: |

||||||||||||||||||||

| Total WSEs(2) |

96,816 | 83,314 | 174,311 | 104,747 | 218,069 | |||||||||||||||

| Total Sales Representatives(3) |

114 | 80 | 224 | 149 | 301 | |||||||||||||||

| Net Insurance Service Revenues (in thousands)(4) |

$ | 53,042 | $ | 76,017 | $ | 120,803 | $ | 83,581 | $ | 100,384 | ||||||||||

| Net Service Revenues (in thousands)(5) |

$ | 192,537 | $ | 189,296 | $ | 269,036 | $ | 178,473 | $ | 296,026 | ||||||||||

| Adjusted EBITDA (in thousands)(6) |

$ | 29,797 | $ | 47,348 | $ | 95,362 | $ | 61,530 | $ | 92,305 | ||||||||||

| Adjusted Net Income (in thousands)(7) |

$ | 13,174 | $ | 28,788 | $ | 45,133 | $ | 29,695 | $ | 33,242 | ||||||||||

| (1) | Includes stock-based compensation expense as follows: |

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2010 | 2011 | 2012 | 2012 | 2013 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Cost of providing services (exclusive of depreciation and amortization of intangible assets) |

$ | 467 | $ | 438 | $ | 516 | $ | 382 | $ | 770 | ||||||||||

| Sales and marketing |

670 | 637 | 500 | 364 | 882 | |||||||||||||||

| General and administrative |

3,385 | 3,590 | 3,144 | 2,505 | 2,371 | |||||||||||||||

| Systems development and programming costs |

531 | 160 | 200 | 145 | 337 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total stock-based compensation expense |

$ | 5,053 | $ | 4,825 | $ | 4,360 | $ | 3,396 | $ | 4,360 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (2) | We define Total WSEs at the end of a given fiscal period as the total number of WSEs paid in the last calendar month of the fiscal period. For more information about Total WSEs, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Operating Metrics.” |

| (3) | We define Total Sales Representatives at the end of a given fiscal period as the total number of our direct sales force employees at that date. For more information about Total Sales Representatives, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Operating Metrics.” |

| (4) | Net Insurance Service Revenues is a non-GAAP financial measure that we calculate as insurance service revenues less insurance costs. For more information about Net Insurance Service Revenues and a reconciliation of Net Insurance Service Revenues to insurance service revenues, the most directly comparable financial measure calculated and presented in accordance with GAAP, see “Selected Consolidated Financial and Other Data—Non-GAAP Financial Results.” |

| (5) | Net Service Revenues is a non-GAAP financial measure that we calculate as the sum of professional service revenues and Net Insurance Service Revenues. For more information about Net Service Revenues and a reconciliation of Net Service Revenues to total revenues, the most directly comparable financial measure calculated and presented in accordance with GAAP, see “Selected Consolidated Financial and Other Data—Non-GAAP Financial Results.” |

| (6) | Adjusted EBITDA is a non-GAAP financial measure that we calculate as net income (loss) excluding the effects of our income tax provision (benefit), interest expense, depreciation, amortization of intangible assets, and stock-based compensation expense. For more information about Adjusted EBITDA and a reconciliation of Adjusted EBITDA to net income (loss), the most directly comparable financial measure calculated and presented in accordance with GAAP, see “Selected Consolidated Financial and Other Data—Non-GAAP Financial Results.” |

| (7) | Adjusted Net Income is a non-GAAP financial measure that we calculate as net income (loss), excluding the effects of stock-based compensation, amortization of intangible assets and the income tax effect of these pre-tax adjustments at our effective tax rate. For more information about Adjusted Net Income and a reconciliation of Adjusted Net Income to net income (loss), the most directly comparable financial measure calculated and presented in accordance with GAAP, see “Selected Consolidated Financial and Other Data—Non-GAAP Financial Results.” |

12

Table of Contents

| As of September 30, 2013 | ||||||||||

| Actual | Pro Forma(1) | Pro Forma As Adjusted(2)(3) | ||||||||

| (in thousands) | ||||||||||

| Consolidated Balance Sheet Data: |

||||||||||

| Cash and cash equivalents |

$ | 112,161 | $ | 112,161 | ||||||

| Working capital |

$ | 85,541 | $ | 85,541 | ||||||

| Total assets |

$ | 1,215,597 | $ | 1,215,597 | ||||||

| Notes payable and borrowings under capital leases |

$ | 820,610 | $ | 820,610 | ||||||

| Total liabilities |

$ | 1,448,163 | $ | 1,448,163 | ||||||

| Convertible preferred stock |

$ | 122,878 | — | |||||||

| Total stockholders’ equity (deficit) |

$ | (355,444 | ) | $ | (232,566 | ) | ||||

| (1) | The pro forma column reflects the conversion of all outstanding shares of our preferred stock into 19,032,854 shares of our common stock immediately prior to the completion of this offering. |

| (2) | The pro forma as adjusted column reflects the (i) conversion of all outstanding shares of our preferred stock into 19,032,854 shares of our common stock immediately prior to the closing of this offering, (ii) sale by us of shares of our common stock in this offering at an assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us, and (iii) the application of $200 million of the net proceeds of this offering to repay amounts outstanding under our credit facilities. |

| (3) | A $1.00 increase (decrease) in the assumed initial public offering price of $ per share would increase (decrease) the amount of cash and cash equivalents, working capital, total assets and total stockholders’ equity by approximately $ million, assuming the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions. Similarly, each increase (decrease) of 1,000,000 shares in the number of shares of our common stock offered by us would increase (decrease) the amount of cash and cash equivalents, working capital, total assets and total stockholders’ equity by approximately $ million, assuming that the assumed initial public offering price remains the same, and after deducting estimated underwriting discounts and commissions. The pro forma as adjusted information discussed above is illustrative only and will be adjusted based on the actual initial public offering price and the other terms of this offering determined at pricing. |

13

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the following risks and all of the other information contained in this prospectus, including our consolidated financial statements and related notes, before investing in our common stock. If any of the following risks materialize, our business, financial condition and results of operations could be materially and adversely affected. In that case, the trading price of our common stock could decline, and you may lose some or all of your investment.

Risks Related to Our Business and Industry

Our success depends on growth in market acceptance of the human resources outsourcing and related services we provide.

Our success depends on the willingness of SMBs to outsource their HR function to a third-party service provider. Based on data published by the National Association of Professional Employer Organizations, we estimate that in 2012 fewer than 5% of U.S. employees of businesses with fewer than 500 employees were part of a co-employment arrangement, in which all or some portion of the employer’s HR function was outsourced to a single third-party provider such as TriNet. We believe that our growth opportunity is primarily a function of our ability to penetrate the SMB market. Many companies have invested substantial personnel, infrastructure and financial resources in their own internal HR organizations and therefore may be reluctant to switch to our solution. Companies may not engage us for other reasons, including a desire to maintain control over all aspects of their HR activities, a belief that they manage their HR activities more effectively using their internal administrative organizations, perceptions about the expenses associated with our services, perceptions about whether our services comply with laws and regulations applicable to them or their businesses, or other considerations that may not always be evident. Additional concerns or considerations may also emerge in the future. We must address our potential clients’ concerns and explain the benefits of our approach in order to convince them to change the way that they manage their HR activities, particularly in parts of the United States where our company and solution are less well-known. If we are not successful in addressing potential clients’ concerns and convincing companies that our solution can fulfill their HR needs, then the market for our solution may not develop as we anticipate and our business may not grow.

If we are unable to rapidly grow our sales force, we will not be able to grow our business at the rate that we anticipate, which could harm our business, results of operations and financial condition.

In order to raise awareness of the benefits of our services and identify and acquire new clients, we must rapidly grow our direct sales force, which consists of regional sales representatives who focus on serving clients in specific industry vertical markets. Competition for skilled sales personnel is intense, and we cannot assure you that we will be successful in attracting, training and retaining qualified sales personnel, or that our newly hired sales personnel will function effectively, either individually or as a group. In addition, our newly hired sales personnel are typically not productive for up to a year following their hiring. This results in increased near-term costs to us relative to the sales contributions of these newly hired sales personnel. If we are unable to rapidly grow and effectively train our sales force, our revenues likely will not increase at the rate that we anticipate, which could harm our business, results of operations and financial condition.

We are subject to client attrition.

We regularly experience significant client attrition due to a variety of factors, including increases in administrative fees and insurance costs, disruption caused by the transition of WSEs we have gained through acquisition to our technology platform, client business failure, competition and clients determining to bring HR administration in-house. Our standard client service agreement can be cancelled by us or by the client without penalty with 30 days’ prior written notice. Clients who intend to cease doing business with us often elect to do so effective as of the beginning of a calendar year. As a result, in the first quarter of each year we experience our largest concentration of client attrition. In addition, we experience higher levels of client attrition in connection

14

Table of Contents

with renewals of the health insurance we provide for WSEs in the event that such renewals result in increased premiums that we pass on to our clients. If we were to experience client attrition in excess of our projected annual attrition rate of approximately 20% of our installed WSE base, as we did in 2010 and 2011, it could harm our business, results of operations and financial condition.

Our acquisition strategy creates risks for our business.

We have completed numerous acquisitions of other businesses, and we expect that we will continue to grow through acquisitions of other businesses, assets or technologies. We may fail to identify attractive acquisition candidates or we may be unable to reach acceptable terms for future acquisitions. If we are unable to complete acquisitions in the future, our ability to grow our business will be impaired.

We may pay for acquisitions by issuing additional shares of our common stock, which would dilute our stockholders, or by issuing debt, which could include terms that restrict our ability to operate our business or pursue other opportunities and subject us to meaningful debt service obligations. We may also use significant amounts of cash to complete acquisitions. To the extent that we complete acquisitions in the future, we likely will incur future depreciation and amortization expenses associated with the acquired assets. We may also record significant amounts of intangible assets, including goodwill, which could become impaired in the future. Acquisitions involve numerous other risks, including:

| • | difficulties integrating the operations, technologies, services and personnel of the acquired companies, including the migration of WSEs from an acquired company’s technology platform to ours; |

| • | challenges maintaining our internal standards, controls, procedures and policies; |

| • | diversion of management’s attention from other business concerns; |

| • | over-valuation by us of acquired companies; |

| • | litigation resulting from activities of the acquired company, including claims from terminated employees, customers, former stockholders and other third parties; |

| • | insufficient revenues to offset increased expenses associated with the acquisitions and unanticipated liabilities of the acquired companies; |

| • | insufficient indemnification or security from the selling parties for legal liabilities that we may assume in connection with our acquisitions; |

| • | entering markets in which we have no prior experience and may not succeed; |

| • | risks associated with foreign acquisitions, such as communication and integration problems resulting from geographic dispersion and language and cultural differences, compliance with foreign laws and regulations and general economic or political conditions in other countries or regions; |

| • | potential loss of key employees of the acquired companies; and |

| • | impairment of relationships with clients and employees of the acquired companies or our clients and employees as a result of the integration of acquired operations and new management personnel. |

If we fail to integrate newly acquired businesses effectively, we might not achieve the growth, service enhancement or operational efficiency objectives of the acquisitions, and our business, results of operations and financial condition could be harmed.

Unexpected changes in workers compensation and health insurance claims by worksite employees could harm our business.

Our insurance costs are impacted significantly by our WSEs’ health and workers compensation insurance claims experience. We establish reserves to provide for the estimated costs of reimbursing our workers

15

Table of Contents

compensation and health insurance carriers for paying claims within the deductible layer in accordance with their insurance policies. Estimating these reserves involves our consideration of a number of factors and requires significant judgment. If there is an unexpected increase in the severity or frequency of claims, such as due to our WSEs generating additional claims activity, or if we subsequently receive updated information indicating insurance claims were higher than previously estimated and reported, our insurance costs could be higher in that period or subsequent periods as we adjust our reserves accordingly. In addition, we may be unable to increase our pricing to offset increases in insurance costs on a timely basis. A number of factors affect claim activity levels, such as changes in general economic conditions, proposed and enacted regulatory changes and disease outbreaks.

Our quarterly results of operations may fluctuate as a result of numerous factors, many of which are outside of our control.

Our quarterly results of operations are likely to fluctuate, and our results in some quarters may be below the expectations of research analysts and our investors, which could cause the price of our common stock to decline. Some of our significant expenses, such as insurance costs for our WSEs, rent expense and debt expense, may require significant lead time to reduce. If we do not achieve our expected revenues targets, we may be unable to adjust our costs quickly enough to offset any revenues shortfall, which could harm our results of operations. Some of the important factors that may cause our revenues, results of operations and cash flows to fluctuate from quarter to quarter include:

| • | the number of our new clients initiating service and the number of WSEs employed by each new client; |

| • | our loss of existing clients; |

| • | reduction in the number of WSEs at existing clients; |

| • | the number and severity of health and workers compensation insurance claims by WSEs and the timing of claims information provided by our insurance carriers; |

| • | the timing of client payments and payment defaults by clients; |

| • | the amount and timing of our operating expenses and capital expenditures; |

| • | costs associated with our acquisitions of companies, assets and technologies; |

| • | expenses we incur for geographic and service expansion; |

| • | our regulatory compliance costs; |

| • | changes to our credit ratings by rating agencies; |

| • | changes in our effective tax rate; |

| • | extraordinary expenses such as litigation or other dispute-related settlement payments; and |

| • | the impact of new accounting pronouncements. |

Many of the above factors are discussed in more detail elsewhere in this “Risk Factors” section and in the sections titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business.” Many of these factors are outside our control, and the variability and unpredictability of these factors could cause us to fail to meet our expectations for revenues or results of operations for a given period. In addition, the occurrence of one or more of these factors might cause our results of operations to vary widely, which could lead to negative impacts on our margins, short-term liquidity or ability to retain or attract key personnel, and could cause other unanticipated issues. Accordingly, we believe that quarter-to-quarter comparisons of our revenues, results of operations and cash flows may not be meaningful and should not be relied upon as an indication of our future performance.

16

Table of Contents

Our business is subject to numerous state and federal laws, and uncertainty as to the application of these laws, or adverse applications of these laws, as well as changes in applicable laws, could adversely affect our business.

Our operations are governed by numerous federal, state and local laws relating to labor, tax, benefits, insurance and employment matters. We are a professional employer organization, and by entering into a co-employer relationship with WSEs, we assume certain obligations, responsibilities and potential legal risks of an employer under these laws. However, many of these laws (such as the Employee Retirement Income Security Act, or ERISA, and federal and state employment tax laws) do not specifically address the obligations and responsibilities of a provider of outsourced HR in a co-employer relationship, and the definition of employer under these laws is not uniform. In addition, many states have not addressed the co-employer relationship for purposes of compliance with applicable state laws governing the relationship between employers and employees and state insurance laws. There is even greater uncertainty on the federal level, such as the application of immigration reform to a co-employer relationship, and tax credits for small businesses that utilize a co-employer relationship.

We are not able to predict whether broader federal or state regulation governing the co-employer relationship will be implemented, or if it is, how it will affect us. Any adverse application or interpretation (in courts, agencies or otherwise) of new or existing federal or state laws to the co-employer relationship with our WSEs and clients could harm our business. If federal, state or local jurisdictions were to change their regulatory framework related to outsourced HR, or introduce new laws governing our industry that were materially different from existing laws, those changes could reduce or eliminate the need for some of our services, or could require that we make significant changes in our methods of doing business, which could increase our cost of doing business. Changes in regulations could also affect the extent and type of benefits employers can or must provide employees, the amount and type of taxes employers and employees are required to pay or the time within which employers must remit taxes to the applicable authority. These changes could substantially decrease our revenues and substantially increase our cost of doing business. If we fail to educate and assist our clients regarding new or revised legislation that impacts them, our reputation could be harmed.

Although some states do not explicitly regulate professional employer organizations, 42 states have passed laws that have licensing, certification or registration requirements applicable to professional employer organizations or recognize the professional employer organization model, and other states may implement such requirements in the future. Laws regulating professional employer organizations vary from state to state, but generally provide for oversight of the fiscal responsibility of professional employer organizations, and in some cases codify and clarify the co-employment relationship for processing unemployment claims, workers compensation and other purposes under state law. We may be required to spend significant time and resources to satisfy licensing requirements or other applicable regulations in some states, and we may not be able to satisfy these requirements or regulations in all states, which could prohibit us from doing business in such states. In addition, we cannot assure you that we will be able to renew our licenses in all states.

If we are not recognized as an employer of worksite employees under federal and state regulations, we and our clients could be adversely impacted.

In order for WSEs to receive the full benefit of our benefits offerings, it is important that we act and qualify as an employer of the WSEs under the Internal Revenue Code of 1986, or the Code, and ERISA. In addition, our status as an employer is important for purposes of ERISA preemption of state laws. The definition of employer under various laws is not uniform, and under both the Code and ERISA the term is defined in part by complex multi-factor tests under common law. We believe that we qualify as an employer of our WSEs in the United States under both the Code and ERISA, and we implement processes to protect and preserve this status. However, the U.S. Department of Labor has issued guidance that certain entities in the HR outsourcing industry do not qualify as common law employers of WSEs for ERISA purposes. If we were found not to be an employer under the Code, our WSEs may not receive the favorable tax treatment for any plans intended to qualify under Section 401 of the Code, including our 401(k) plans and cafeteria plans, which could have a material adverse effect on our business. If we were found not to be an employer for ERISA purposes, our plans would not comply with ERISA, and fines and penalties could be imposed. In addition, if we were found not to be an employer for

17

Table of Contents

ERISA purposes, we and our plans would not enjoy the full preemption of state laws provided by ERISA and could be subject to varying state laws and regulations, including laws governing multiple employer welfare arrangements, or MEWAs, as well as to claims based upon state laws.

We and our clients could be adversely impacted by health care reform.

The Patient Protection and Affordable Care Act and the Heath Care and Education Reconciliation Act of 2010, which we refer to collectively as the Act, entail sweeping health care reforms with staggered effective dates from 2010 through 2018, and many provisions of the Act require the issuance of additional guidance from the U.S. Departments of Labor and Health and Human Services, the Internal Revenue Service, or IRS, and U.S. states. Beginning in 2014, a number of key provisions of the Act take effect, including the establishment of state insurance exchanges, insurance market reforms, “pay or play” penalties on large employers and the imposition of excise taxes on the health insurance industry and reinsurance taxes on insurers and third-party administrators. Collectively, these items have the potential to significantly change the insurance marketplace for employers and how employers provide insurance to employees.

As a co-employer of our clients’ WSEs, we assume or share many of the employer-related responsibilities and legal risks and assist our clients in complying with many employment-related governmental regulations. Generally, the Act and subsequently issued guidance by the IRS and the U.S. Department of Health and Human Services have not addressed, or in some instances are unclear, as to their application in the co-employment relationship. For example, the Act provides for a small business tax credit for eligible companies offering health care coverage to employees. We believe that these tax credits are available to our clients that meet the qualification requirements; however, the Act and subsequently issued IRS guidance do not expressly address the issue of whether small business clients of a professional employer organization may still qualify as small business eligible for such tax credits. As a result of this uncertainty, we are not yet able to determine the impacts to our business, and to our clients, resulting from the Act. In future periods, the changes may result in increased costs to us and our clients and could affect our ability to attract and retain clients. Additionally, we may be limited or delayed in our ability to increase service fees to offset any associated potential increased costs resulting from compliance with the Act. Furthermore, the uncertainty surrounding the terms and application of the Act may delay or inhibit the decisions of potential clients to outsource their HR needs. Any of these developments could harm our business, results of operations and financial condition.

We may have additional tax liabilities, which could harm our business, operating results, financial condition and prospects.

Significant judgments and estimates are required in determining our provision for income taxes and other tax liabilities. Our provision for income taxes, results of operations and cash flows may be impacted if any of our tax positions are challenged and successfully disputed by the tax authorities. In determining the adequacy of our tax provision, we assess the likelihood of adverse outcomes that could result if our tax positions were challenged by the IRS and other tax authorities. The tax authorities in the United States regularly examine our income and other tax returns. For example, in connection with an IRS examination of prior federal income tax returns filed by Gevity, a company we acquired in 2009, we recently received a technical advice memorandum from the IRS taking the position that approximately $10.1 million of tax credits taken by Gevity, and an additional approximately $2.0 million taken by us after acquiring Gevity, should be reversed, which position we dispute. The ultimate outcome of these examinations and tax disputes cannot be predicted with certainty. Should the IRS or other tax authorities assess additional taxes as a result of examinations, we may be required to record charges to operations that could have a material impact on our results of operations, financial position or cash flows.

Our business and operations have experienced rapid growth in recent periods, and if we are unable to effectively manage this growth, our business and results of operations may suffer.

We have experienced rapid growth and have significantly expanded our operations in recent periods, which has placed a strain on our management, administrative, operational and financial infrastructure. Managing this growth requires us to further refine our operational, financial and management controls and reporting systems and procedures.

18

Table of Contents

Our ability to effectively manage any significant growth of our business will depend on a number of factors, including our ability to do the following:

| • | effectively recruit, integrate, train and motivate a large number of new employees, including our direct sales force, while retaining our existing employees, maintaining the beneficial aspects of our corporate culture and effectively executing our business plan; |

| • | satisfy our existing clients and identify and acquire new clients; |

| • | enhance the breadth and quality of our services; |

| • | continue to improve our operational, financial and management controls; and |

| • | make sound business decisions in light of the scrutiny associated with operating as a public company. |

These activities will require significant operating and capital expenditures and allocation of valuable management and employee resources, and we expect that our growth will continue to place significant demands on our management and on our operational and financial infrastructure.

Our future financial performance and our ability to execute on our business plan will depend, in part, on our ability to effectively manage any future growth. We cannot assure you that we will be able to do so in an efficient or timely manner, or at all. In particular, any failure to successfully implement systems enhancements and improvements will likely negatively impact our ability to manage our expected growth, ensure uninterrupted operation of key business systems and comply with the rules and regulations that are applicable to public companies. If we fail to manage our growth effectively, our costs and expenses may increase more than we expect them to, which in turn could harm our business, results of operations and financial condition.

We may not be able to sustain our revenue growth rate or profitability in the future.

While we have achieved profitability on an annual basis in each of the last two and four of the last five fiscal years, we expect our operating expenses to increase substantially in the near term, particularly as we make significant investments in our sales and marketing organization, expand our operations and infrastructure and enhance the breadth and quality of our services. If our revenues do not increase to offset these increases in our operating expenses, we may not be profitable in future periods.

Moreover, you should not consider our historical revenue growth to be indicative of our future performance. As we grow our business, our revenue growth rates may slow in future periods due to a number of reasons, which may include slowing demand for our services, increasing competition, a decrease in the growth of our overall market, our failure, for any reason, to continue to capitalize on growth opportunities, the maturation of our business or the decline in the number of SMBs in our target markets.

Our industry is highly competitive, which may limit our ability to maintain or increase our market share or improve our results of operations.