Attached files

| file | filename |

|---|---|

| 8-K - 8-K - DONEGAL GROUP INC | d641734d8k.htm |

Pursuing Effective

Business Strategy in

Regional Insurance Markets

Investor Meetings

December 2013

Exhibit 99.1 |

Forward-Looking Statements

The Company bases all statements made in this presentation that are not historic facts on its

current expectations. These statements are forward-looking in nature (as defined in

the Private Securities Litigation Reform Act of 1995) and involve a number of risks and

uncertainties. Actual results could vary materially. Factors that could cause actual

results to vary materially include: the Company’s ability to maintain profitable

operations, the adequacy of the loss and loss expense

reserves of the Company’s insurance subsidiaries, business and economic conditions in the

areas in which the Company operates, interest rates, competition from various insurance

and other financial businesses, terrorism, the availability and cost of reinsurance,

adverse and catastrophic weather events, legal and judicial developments, changes in

regulatory requirements, the Company’s ability to integrate and manage

successfully the companies it may acquire from time to time and other risks the Company

describes from time to time in the periodic reports it files with the Securities and

Exchange Commission. You should not place undue reliance on any such

forward-looking statements. The Company disclaims any obligation to update such

statements or to

announce publicly the results of any revisions that it may make to any forward-looking

statements to reflect the occurrence of anticipated or unanticipated events or

circumstances after the date of such statements.

Reconciliations of non-GAAP data are available on the Company’s website at

investors.donegalgroup.com

in the Company’s news releases regarding quarterly financial results.

2 |

Insurance Holding Company with Mutual

Affiliate

•

Structure provides stability for successful long-term business

strategy

•

Public company traded on NASDAQ (DGICA/DGICB)

–

Class A dividend yield of 3.25%

–

Class A shares have 1/10 vote; Class B shares have one vote

•

Regional property and casualty insurance group

–

22 Mid-Atlantic, Midwestern, New England and Southern states

–

Distribution force of approximately 2,500 independent agencies

–

$496 million in 2012 net written premiums, up 9.3% from 2011

($673 million in agency direct written premiums for insurance group*)

–

Completed ten M&A transactions since 1988

•

Rated A (Excellent) by A.M. Best (affirmed September 2013)

–

Debt-to-capital of approximately 18%

3

* Includes Donegal Mutual Insurance Company and Southern Mutual Insurance Company

|

Objective: Outperform Industry

Service, Profitability and Book Value Growth

4

Change in Net Written Premiums

DGI

CAGR:

10%

Index

CAGR:

2%

Donegal Group

SNL Small Cap U.S. Insurance Index (average)

GAAP Combined Ratio

DGI Avg: 97%

Index Avg: 103%

Change in Book Value

DGI CAGR: 7%

Index CAGR: N/A |

9mos

2013: Strong Growth and Operating EPS* of 58¢

vs. 53¢

in 9mos 2012

•

7.3% YTD increase in net written premiums

–

Driven by strong commercial lines growth

•

98.2% YTD statutory combined ratio

–

Q3 combined ratio of 96.0% is the lowest for any period in past five

years

–

Measurable progress from rate increases and underwriting

initiatives

–

Year-to-date weather losses and large fire losses below prior year

level –

minimal Q4 impact expected from November Midwest

storms

•

Book value per share at $14.95 vs. $15.63 at year-end 2012

–

Interest rate driven mark-to-market adjustments lowered book

value

5

Additional details are available on our website

(investors.donegalgroup.com)

* Reconciliations and definitions of non-GAAP data are available on the Investors area of

our website |

Achieve Book Value Growth

By Implementing

Plan

Drive revenues with opportunistic transactions and

organic growth

Focus on margin enhancements and investment

contributions |

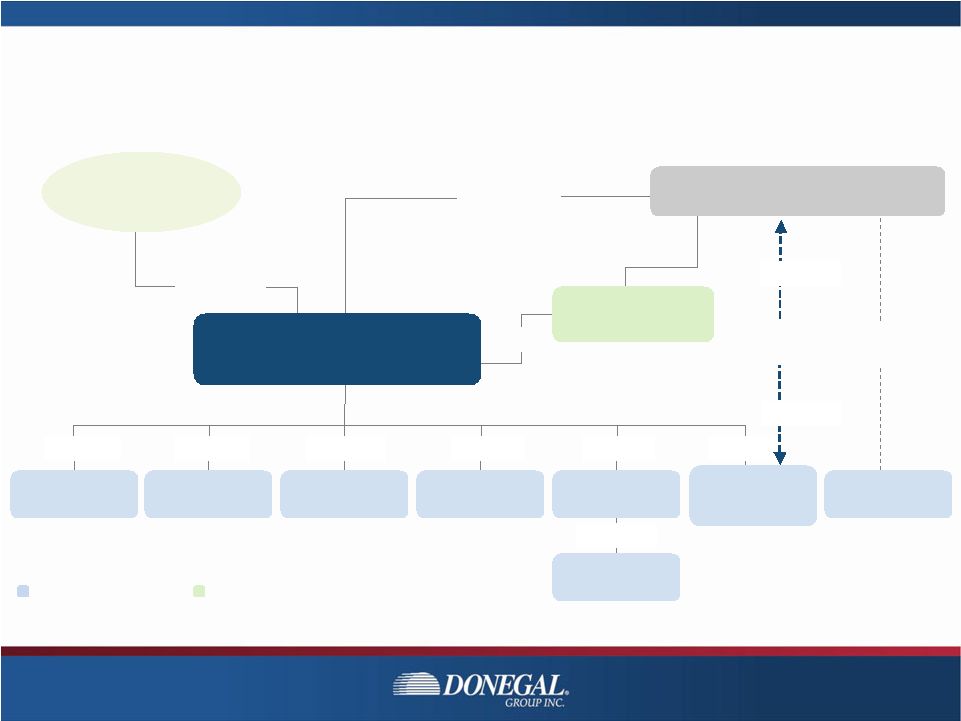

Atlantic

States Insurance

Company

(1)

Because

of

the

different

relative

voting

power

of

Class

A

common

stock

and

Class

B

common

stock,

public

stockholders

hold

approximately

34%

of

the

aggregate

voting

power

of

the

combined

classes,

and

Donegal

Mutual

holds

approximately

66%

of

the

aggregate

voting

power

of

the

combined

classes.

100%

54%

(1)

46%

(1)

100%

Reinsurance

48%

52%

= P&C Insurance Subsidiaries

= Thrift Holding Company /Federal Savings Bank

POOLING

AGREEMENT

100%

100%

100%

100%

100%

Donegal Group Inc.

Donegal Mutual

Insurance Company

Donegal Financial

Services Corporation

(Union Community Bank)

Opportunistic Ownership Structure Provides Flexibility and Capacity

Structure Provides Flexibility and Capacity

Public

Stockholders

Sheboygan Falls

Insurance Company

Michigan Insurance

Company

Southern Insurance

Company of Virginia

Le Mars

Insurance Company

The Peninsula

Insurance Company

Peninsula

Indemnity Company

Southern Mutual

Insurance Company

100%

7

80%

20% |

Acquisitions Have Made Meaningful

Contribution to Long-term Growth

8

January 2004

Acquired Le Mars and Peninsula

December 2010

Acquired Michigan

Implemented 25% Quota Share

December 2008

Acquired Sheboygan Falls

Implemented Pooling Change

$283

$302

$207

$307

$314

$365

$363

$392

$454

$496

Net Written Premiums

(dollars in millions) |

9

Acquisition Strategy Drives Geographic

Expansion

•

10 M&A transactions since

1988

–

Experienced consolidation team

•

Acquisition criteria:

–

Serving attractive

geography

–

Favorable regulatory,

legislative and judicial

environments

–

Similar personal/commercial

business mix

–

Premium volume

up to $100

million |

Example: Southern Mutual Insurance Co.

•

Affiliation with Donegal Mutual in 2009

•

Donegal Mutual surplus note investment of $2.5 million

•

$16.8 million in 2012 direct written premiums

•

100% quota share reinsurance with Donegal Mutual

–

SMIC cedes underwriting results to Donegal Mutual

–

Donegal Mutual includes business in pooling agreement with

Atlantic States (80% of SMIC business to Donegal Group)

•

Expanded market presence in Georgia and South Carolina

•

Serves as model for mutual-to-mutual affiliations

10 |

Example: Michigan Insurance Company

•

Attractive franchise

acquired in 2010

•

Potential for increased

premium contribution

•

Track record of profitability

•

Provided entry into new

state as part of Midwest

expansion strategy

–

Capable management

team

–

Quality agency distribution

system

–

Diversified mix of business

11

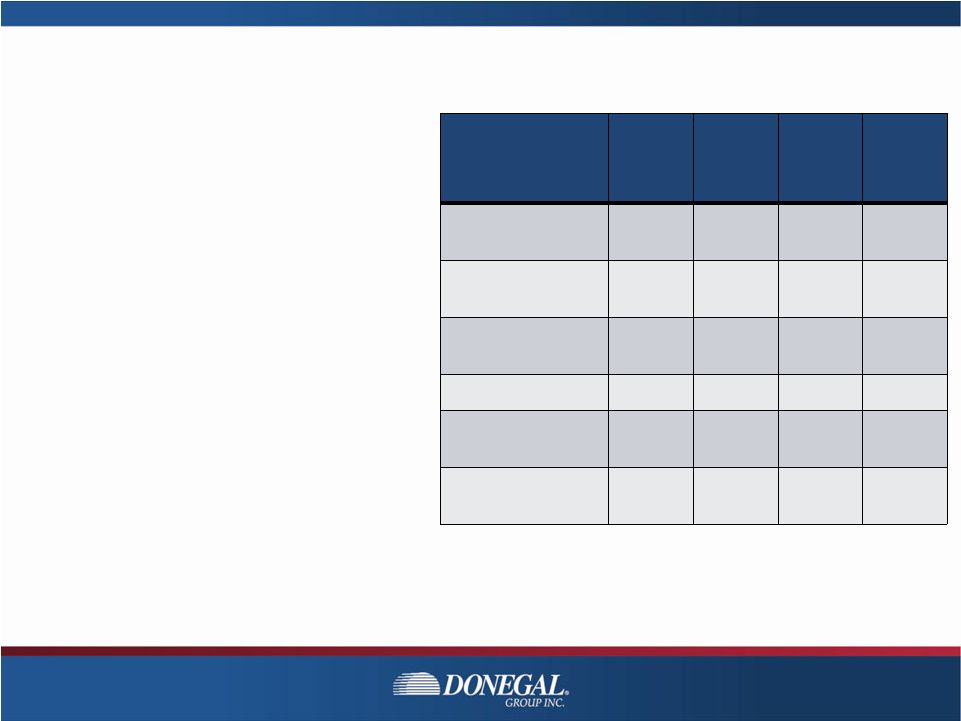

(Dollars in millions)

2010

(under

prior

owner)

2011

2012

2013

Direct written

premiums

$105

$108

$111

$115**

External quota

share

75%

50%

40%

30%

Ceded to Donegal

Mutual*

N/A

25%

25%

25%

Retained by MICO

25%

25%

35%

45%

Included in DGI

NPW

N/A

$46

$57

$68**

Statutory

combined ratio

97%

95%

94%

N/A

* Premiums ceded to Donegal Mutual are included in

pooling agreement with Atlantic States (80% to DGI)

** Projected based

on estimated 2013 growth rate |

Business Mix Offers Broad-based

Opportunities

•

Commercial lines = 41% of

NWP in 9mos 2013

–

Commercial lines renewal

premiums increases in 5-7%

range

–

Ongoing emphasis on new

business growth in all regions

•

Personal lines = 59% of

NWP in 9mos 2013

–

Rate increases in 3-8% range

–

Minimal exposure growth other

than MICO premiums retained

12

Net Written Premiums by Line of Business

(December 31, 2012) |

Organic Growth Centered on Relationships

with ~2,500 Independent Agencies

•

Ongoing objectives:

–

Achieve top three ranking within appointed agencies in lines of

business

we write

–

Leverage “regional”

advantages and maintain personal

relationships as agencies grow and consolidate

•

Continuing focus on commercial lines growth:

–

Emphasize expanded commercial lines products and capabilities

in current agencies

–

Appoint commercial lines focused agencies to expand

distribution in key geographies

–

Strengthen relationships with agencies appointed in recent years

13 |

Best-In-Class Technology and Agent Support

Personal Lines

•

Donegal offers state-of-the-art

quoting and underwriting

capabilities

Commercial Lines

•

Donegal offers web-based

underwriting system with

automated rating and

underwriting

14

Call

Call

Center

Center

Service

Service

Center

Center

ImageRight

ClaimCenter

Mobile App |

Achieve Book Value Growth

By Implementing

Plan

Drive revenues with opportunistic transactions and

organic growth

Focus on margin enhancements and investment

contributions |

Remain Focused on Underwriting to

Best Leverage Rate Increases

16

Donegal Insurance Group (SNL P&C Group)

SNL P&C Industry (Aggregate)

Personal Lines Loss Ratio

Commercial Lines Loss Ratio |

Focus

on Underwriting Profitability •

Sustain pricing discipline and conservative underwriting

•

Manage exposure to catastrophe/unusual weather events

–

Purchase reinsurance coverage in excess of a one-in-200 year

event

•

Link employee compensation directly to underwriting

performance

•

Focus on rate adequacy and pricing sophistication

•

Leverage centralized oversight of regional underwriting

•

Emphasize IT-based programs such as automated decision

trees and predictive modeling

17 |

Emphasize Growth in More Profitable

Commercial Lines

•

93.0% Q313 statutory

combined ratio

•

Introduce core Donegal

products in new regions

•

Growth focus on accounts

with premiums in $10,000 to

$75,000 range

•

Expand appetite within

classes and lines already

written

–

Add related classes

–

Appropriately use reinsurance

18 |

Focus

on Margin Improvement in Personal Lines

•

97.9% Q313 statutory

combined ratio

•

Acquired companies weighted

to personal lines

•

Focus on the preferred and

superior risk markets

•

Rate increases in virtually

every jurisdiction

•

New and renewal inspection

and renewal re-tiering

•

Seek geographic spread of risk

•

Balance portfolio (auto/home)

19 |

Employ Sophisticated Pricing and

Actuarial Tools

•

Predictive modeling tools

enhance our ability to

appropriately price our

products

–

Sophisticated predictive

modeling algorithms for

pricing/tiering risks

–

Territorial segmentation and

analysis of environmental

factors that affect loss

experience

–

Exploring tools that allow

consideration of vehicle-

specific data in pricing

•

External information

sources allow us to

develop price optimization

strategies

•

Formal schedule of regular

rate adequacy reviews for

all lines of business,

including GLM analysis on

claim costs and agency

performance

•

Currently evaluating usage-

based insurance tools

20 |

Maintain Reserve Adequacy to Support

Margin Expansion

21

•

Reserves at $251 million

at year-end 2012

–

Midpoint of actuarial range

–

Conservative reinsurance

program limits volatility

•

Emphasis on faster claims

settlements to reduce

longer-term exposures

•

Development YTD 2013 of

$9.6 million within normal

range

Values shown are selected reserves

Vertical bars represent actuarial ranges

Reserve Range at 12/31/2012

Low $228,720

High $275,282

Selected at midpoint

(dollars in thousands, net of reinsurance)

Established Reserves at Year-end |

Drive

Increased Efficiency with Automation •

Current infrastructure can

support premium growth

•

Premiums per employee rising

due to underwriting systems

•

Claims system allows more

rapid and efficient claims

handling

•

Mutual structure provides

opportunities for operational

and expense synergies

•

Statutory expense ratio of

29.6% for YTD 2013 vs. 29.3%

for 2012

22 |

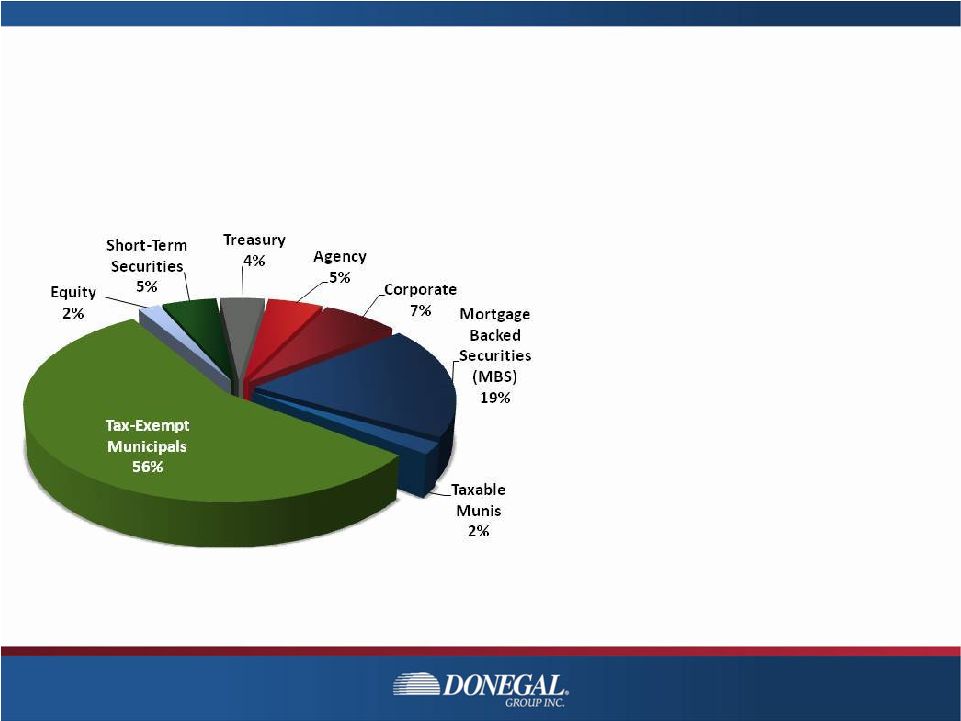

Maintain Conservative Investment Mix to

Minimize Risk

23

* Excluding investments in affiliates

$752 Million in Invested Assets*

(as of September 30, 2013)

•

89% of portfolio invested in

fixed maturities at

September 30, 2013

–

Effective duration = 5.3

years

–

Tax equivalent yield = 3.3%

•

Taking proactive steps to

reduce interest rate risk

•

Emphasis on quality

–

86% AA-rated or better

–

98% A-rated or better

•

Liquidity managed through

laddering |

Donegal Financial Services Corporation

Bank Investment = 5% of Invested Assets

•

DFSC owns 100% of Union Community Bank

–

Serves Lancaster County (location of Donegal headquarters)

•

Expanded to 13 branches via acquisition in May 2011

–

Added scale to banking operation

–

Enhanced value of historic bank investment

–

Increased potential for bottom-line contribution

•

DGI owns approximately 48% of DFSC

–

52% owned by Donegal Mutual

•

Union Community Bank is financially strong and profitable

24 |

Union

Community Bank is Financially Strong and Profitable

•

Results for first nine months of 2013:

–

$515

million in assets at September 30, 2013

–

$5.4 million in YTD net income

•

Excellent capital ratios at September 30, 2013:

25

Tier 1 capital to average total assets

15.73%

Tier 1 capital to risk-weighted assets

23.01%

Risk-based capital to risk-weighted assets

25.12% |

Achieve Book Value Growth

By Implementing

Plan

Drive revenues with opportunistic transactions and

organic growth

Focus on margin enhancements and investment

contributions |

Strong Capital + Solid Plan to Drive Results

•

Rated A (Excellent) by

A.M.

Best

–

Debt-to-capital of

approximately 18%

–

Premium-to-surplus of

approximately 1.5-to-1

•

Dividend yield of 3.25% for

Class A shares

•

New authorization for

repurchase of up to

500,000 shares of Class A

common stock

27 |

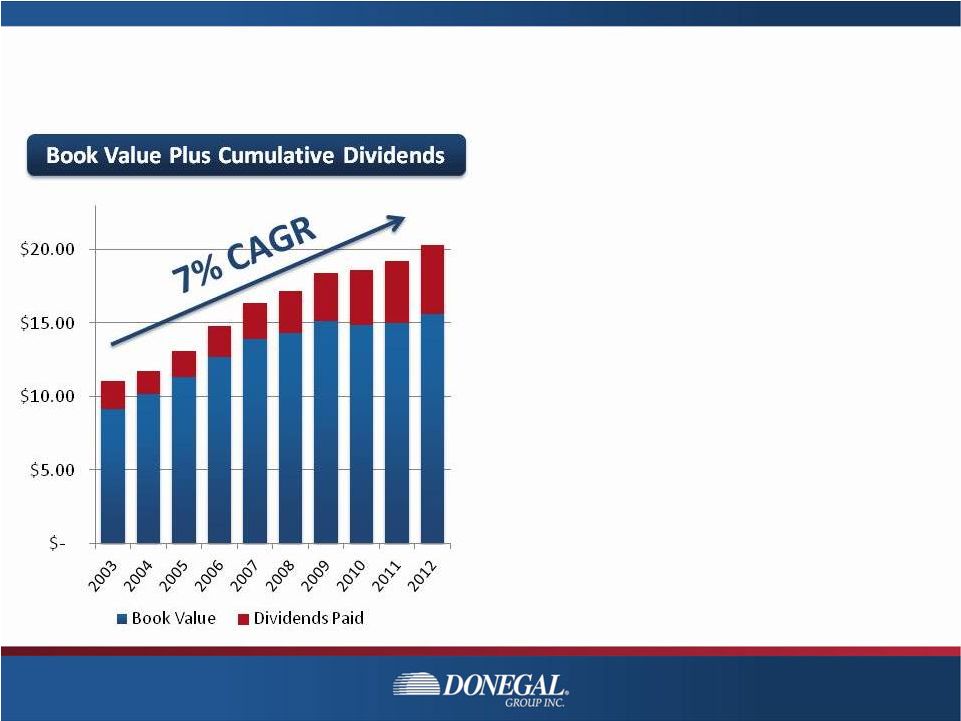

Structure Provides Stability to Pursue

Successful Long-Term Business Strategy

•

Regional property casualty insurance company

–

Insurance holding company with mutual affiliate

•

Objective to outperform industry in service, profitability

and book value growth

•

Drive revenues with opportunistic transactions and organic

growth

–

10% CAGR in net written premiums since 2002

•

Focus on margin enhancements and investment

contributions

28 |

Supplemental Information |

History of Contributing Transactions

Company

Le Mars

Peninsula

Sheboygan

Southern

Mutual

Michigan

Year Acquired

2004

2004

2008

2009

2010

Company Type

Mutual

Stock

Mutual

Mutual

Stock

Primary Product Line

Personal

Niche

Personal

Personal

Pers./Comm.

Geographic Focus

Midwest

Mid-Atlantic

Wisconsin

Georgia/

South

Carolina

Michigan

Transaction Type

Demutualization

Purchase

Demutualization

Affiliation

Purchase

Net Premiums Acquired

$20 million

$34 million

$8 million

$11 million

$27 million*

Acquisition Price

$4 million

$24 million

$4 million

N/A

$42 million

Avg. Growth Rate**

4%

3%

13%

N/A

N/A

Avg. Combined Ratio**

93%

93%

106%

106%

95%

30

* Michigan's direct premiums written were $105 million in 2010

** Since acquisition |

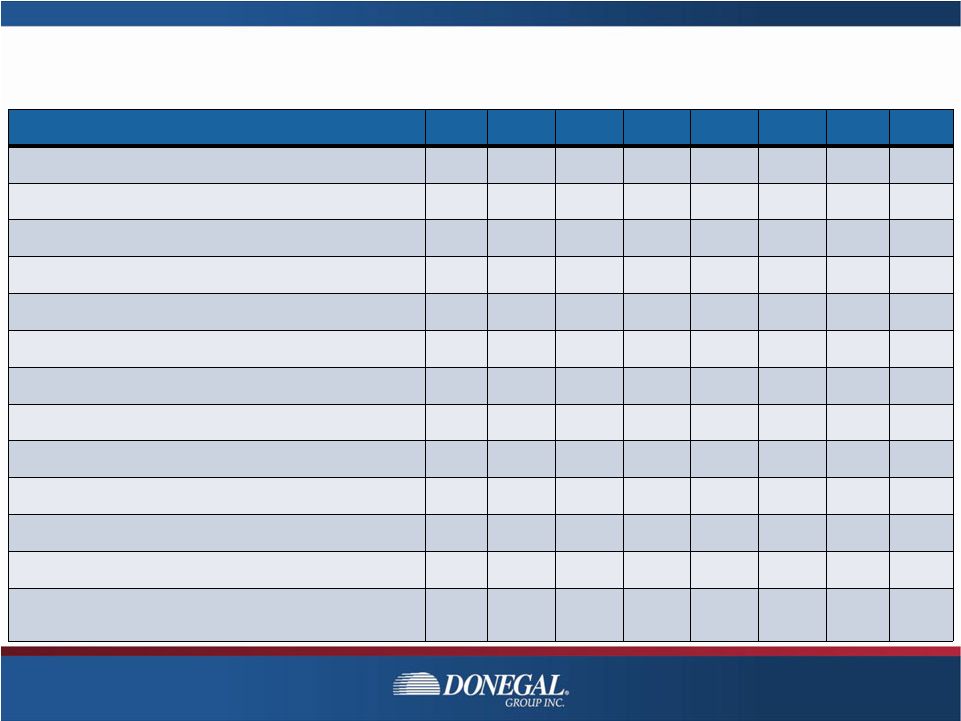

Net

Premiums Written by Line of Business (in millions)

Q3 13

Q2 13

Q1 13

Q4 12

Q3 12

Q2 12

Q1 12

Q4 11

Personal lines:

Automobile

$50.9

$50.2

$48.6

$45.6

$51.4

$50.2

$48.0

$44.6

Homeowners

29.8

29.1

21.9

22.3

27.6

27.0

20.2

22.3

Other

4.2

4.3

3.4

4.0

4.2

4.2

3.7

3.8

Total personal lines

84.8

83.6

73.8

71.9

83.1

81.4

71.9

70.7

Commercial lines:

Automobile

14.0

15.7

15.5

12.0

12.5

14.0

12.9

10.6

Workers’

compensation

18.3

19.7

23.2

14.3

16.1

16.3

18.6

11.0

Commercial multi-peril

18.0

20.0

19.7

14.7

15.9

17.4

16.4

13.4

Other

1.4

1.6

0.3

1.8

1.7

2.0

1.5

2.0

Total commercial lines

51.8

57.0

58.6

42.8

46.2

49.7

49.4

37.0

Total net premiums written

$136.6

$140.6

$132.5

$114.7

$129.3

$131.1

$121.3

$107.7

31 |

Combined Ratio Analyses

(percents)

Q3 13

Q2 13

Q1 13

Q4 12

Q3 12

Q2 12

Q1 12

Q4 11

Stat Combined Ratios:

Personal lines

97.9

100.2

98.1

108.9

101.3

108.4

101.6

116.7

Commercial lines

93.0

101.4

98.4

88.5

91.4

95.1

88.8

105.5

Total lines

96.0

100.6

98.0

101.2

97.6

103.5

96.9

112.8

GAAP Combined Ratios (total lines):

Loss ratio (non-weather)

57.8

63.1

64.1

68.2

58.6

63.8

62.3

71.6

Loss ratio (weather-related)

7.2

7.4

4.5

3.9

9.3

9.6

4.5

10.6

Expense ratio

32.3

32.3

30.7

29.3

31.4

31.9

32.4

30.5

Dividend ratio

0.3

0.3

0.4

0.3

0.3

0.1

0.2

0.5

Combined ratio

97.6

103.1

99.7

101.7

99.6

105.4

99.4

113.2

GAAP Supplemental Ratios:

Fire losses greater than $50,000

2.4

4.4

6.5

5.5

5.5

5.9

2.9

6.0

Development (savings) on prior year loss reserves

2.4

3.7

1.5

1.6

2.4

1.9

0.4

2.2

32 |

For Further

Information: Jeffrey D. Miller

Senior Vice President and Chief Financial Officer

Phone: (717) 426-1931

E-mail: investors@donegalgroup.com

Website: investors.donegalgroup.com

Pursuing Effective

Business Strategy in

Regional Insurance Markets |