Attached files

| file | filename |

|---|---|

| 8-K - 8-K - GRAY TELEVISION INC | d611898d8k.htm |

| EX-99.2 - EX-99.2 - GRAY TELEVISION INC | d611898dex992.htm |

Exhibit 99.1

Historical Financial Data as of June 30, 2013

Select Other Data as of September 2013

NYSE: GTN

Investor Presentation |

2

Gray Television, Inc.

Agenda

Company Overview

Gray Television is a Dominant Mid-Market TV Platform with Significant

Upside Industry Overview

Strong Industry Fundamentals and Growing Revenue Streams

Financial Overview

Strong Momentum in the Core Business with Record Political and Retransmission

Growth |

3

Gray Television, Inc.

Highly Experienced Senior Management

Focused on maximizing potential of existing portfolio, while prudently pursuing

strategic growth opportunities Name

Years at

Gray TV

Years in

Industry

Background and Notable Achievements

Hilton H Howell, Jr.

Director, Vice Chairman,

President & CEO

20

20

CEO since 2008, Vice Chairman since 2002 and director since 1993

Served as President and CEO of Atlantic American Corporation since 1995

Served as EVP and General Counsel of Delta Life Insurance Company and Delta Fire

& Casualty Insurance Company since 1991

James C. Ryan

SVP & CFO

15

28

CFO since 1998 and additionally serves as SVP of Finance

Served as SVP since 2002 and as VP from 1998 to 2002

Served

as

the

CFO

of

Busse

Broadcasting

Corporation

from

1987

to

1998

Kevin P. Latek

SVP –

Business Affairs

2

16

Joined Gray in 2012, after spending 15 years representing television broadcasters

in FCC regulatory and transactional matters with law firm Dow Lohnes

Member of the CBS Affiliate Association; former member of, and previously counsel

to, Fox Affiliate Board of Governors

Nick Waller

SVP –

Mid-Atlantic &

South

13

13

Joined Gray in 2000, after spending 20 years with Datasouth Computer Corporation,

first as CFO and eventually as President

Director of the Florida Association of Broadcasters

Bob Smith

SVP –

Midwest & West

27

27

Started as an account executive at Gray TV in Eau Claire, Wisconsin in 1986

Serves

as

SVP

since

July

2013

and

served

in

various

roles

from

1986

–

2013

at

Gray

TV

Has served on the Boards of Directors of the Wisconsin Broadcaster Association,

among others Jason Effinger

SVP –

Media &

Technology

12

22

Joined Gray TV in 2001 as a station manager

Serves

as

SVP

since

July

2013

and

served

as

Regional

VP

prior

to

that

Serves as Vice Chair of the Nebraska Broadcasters Association

|

Company Overview |

5

Gray Television, Inc.

A Leading Television Broadcaster in Diverse Mid Markets with Dominant Market

Positions #1 or #2 market share in 29 out of 31 markets

Improving Advertising Market and Diversification of Revenue Mix

Strategic Acquisition and Duopoly Opportunities

Large Political Upside in Election Years with Presence in Key States

Strong Growth in Net Retransmission Revenue and Increasing Leverage With

Networks Successful New Media Initiatives and Spectrum Upside

Robust Free Cash Flow Generation Over a Two Year Cycle

Experienced Management Team With Healthy Track Record of Equity Value

Creation Key Investment Highlights |

6

Gray Television, Inc.

Other

Gray Television is a Dominant Mid-Market

TV Platform

Primary Channels by Affiliate: 46

1

2012 Revenue by Affiliate: $405 mm

(1)

Certain additional channels are affiliated with more than one network

simultaneously. As a result, Gray has 42 additional channels with 49 affiliations

88 total channels of programming spread

across 31 attractive markets

46 channels affiliated with a “Big 4”

network

and

42

additional

channels

1

Reaches 6.2% of U.S. TV households,

significantly below FCC cap

#1 news rating in 23 markets and leading

franchises

#1 channel in 22 markets

Strong market and network diversification

17 collegiate markets and 8 state capitals

provide stability

Dominance in political revenue through

presence in key states

22

48%

11

24%

8

17%

5

11%

2%

2%

15%

42%

Gray Television, Inc.

39% |

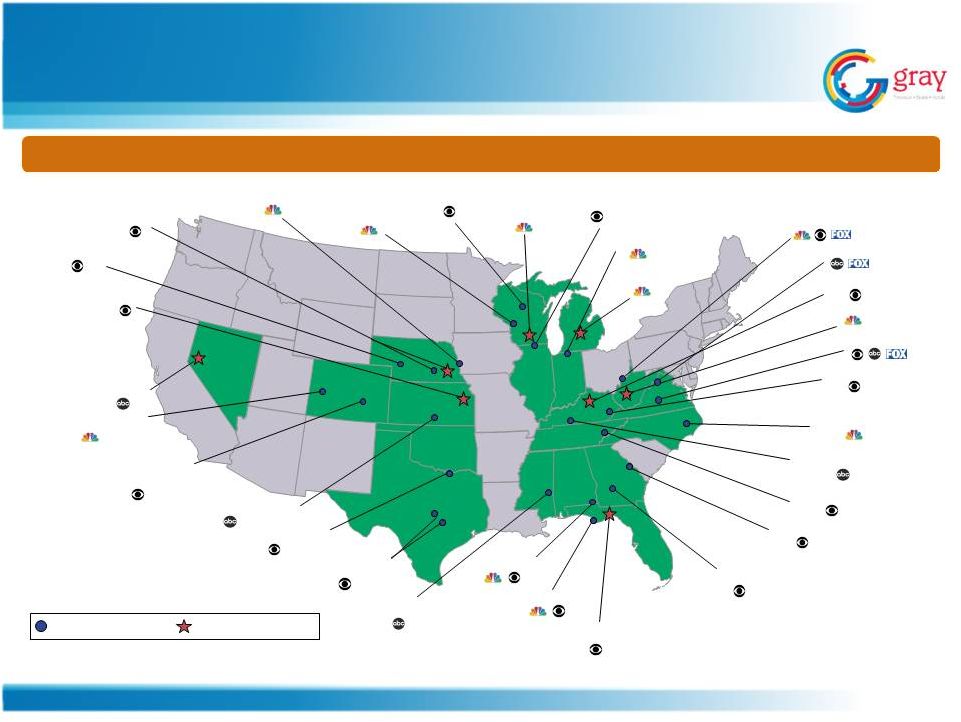

Gray

Has a Diverse and National Footprint Reno, NV

Lincoln

-

Hastings

-

Kearney, NE

Topeka, KS

Omaha, NE

La Crosse -

Eau Claire, WI

Madison, WI

Rockford, IL

Lansing, MI

Parkersburg, WV

Harrisonburg, VA

Lexington, KY

Hazard, KY

Greenville

-

New

Bern

-

Washington, NC

Bowling Green, KY

Knoxville, TN

Augusta, GA

Tallahassee, FL -

Thomasville, GA

Panama City, FL

Dothan, AL

Meridian, MS

Waco-Temple -

Bryan, TX

Sherman, TX -

Ada, OK

Wichita -

Hutchinson, KS

Colorado Springs -

Pueblo, CO

Charlottesville, VA

Grand Junction, CO

Wausau -

Rhinelander, WI

Charleston-Huntington, WV

South Bend, IN

Albany, GA

31 markets reaching approximately 6.2% of US TV households

North Platte, NE

State Capital in DMA

Gray TV Station

7

Gray Television, Inc. |

Key

Recent Developments and Strategic Initiatives

Appointed new management structure in July 2013, with significant industry

experience, to increase focus on:

Strategic growth: Kevin Latek

Station operations and performance: Nick Waller and Bob Smith

Digital media strategy: Jason Effinger

Launched “Big Four”

affiliated channels on the Syncbak Internet Platform on September 4, 2013

Constructed and launched seven entirely new television stations since September

2012 Back office services agreement with Excalibur with anticipated closing

of October 31, 2013 Acquisition of KSNB (MyTV) from Colins Broadcasting

Corporation on February 25, 2013 Launched new and modern looking logo and

website in September 2013, emphasizing Gray TV’s focus on local market

dominance 8

Gray Television, Inc. |

The

Importance of Being #1 Dominate local and political revenue with

highly-rated news platforms

Greater purchasing power and leverage

with MVPDs, networks and programmers

Partner

of

choice

–

duopoly

opportunities

Deliver high margins

Maximize free cash flow

Attract and retain high quality talent

Long

History

of

Being

#1

in

the

Market

1

Dominant

News

Franchises

Drive Traffic

Price

Leadership

Network and

News

Ratings

Reinvest

in

Business

Reinvest

in

Business

CBS National Ranking

1

1

2

1

1

1

1

(1)

Number of Gray stations ranked #1

NBC National Ranking

3

4

4

4

4

4

3

ABC National Ranking

2

2

3

2

2

2

2

4

4

4

4

3

3

4

'05/'06

'06/'07

'07/'08

'08/'09

'09/'10

'10/'11

'11/'12

8

7

5

5

8

7

7

'05/'06

'06/'07

'07/'08

'08/'09

'09/'10

'10/'11

'11/'12

11

12

12

12

12

12

11

'05/'06

'06/'07

'07/'08

'08/'09

'09/'10

'10/'11

'11/'12

Gray Television, Inc.

9 |

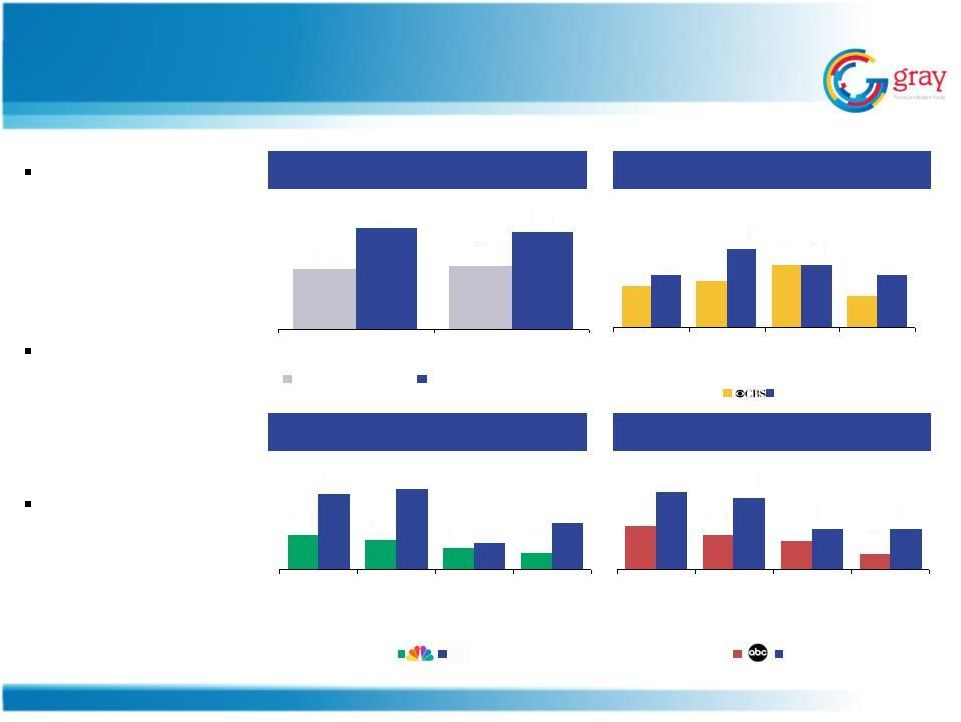

National Average vs. Gray

November ’12 Household Share

Gray’s Stations Dominate Local News

and Information

NBC vs. Gray

November ’12 Household Share

ABC vs. Gray

November ’12 Household Share

CBS vs. Gray

November ’12 Household Share

Gray’s Early Evening

newscasts

outperform the

national average by

71%

Gray’s late local

news outperforms

the national average

by 53%

Better than national

average for all major

affiliate news

programs

8

9

12

6

10

15

12

10

The Early

Show

Network

News

Prime

(Mon-Sun)

The Late

Show

Gray

13

11

8

6

28

30

10

17

The Today

Show

Network

News

Prime

(Mon–Sun)

The

Tonight

Show

14

11

9

5

25

23

13

13

Good

Morning

America

Network

News

Prime

(Mon-Sun)

Nightline /

Jimmy

Kimmel

Gray

14

15

24

23

Early Evening News

Late News

NSI National Average

Gray Average of All Stations

10

Gray Television, Inc.

Gray |

Stable

Markets

–

Concentration

on

DMAs

61-208

With Focus on State Capitals / Collegiate Presence

Note: Shading indicates DMA includes state capital. Enrollment in

thousands. Gray stations cover 8 state capitals and

17 university towns, representing

enrollment of approximately 474,000

students

Why university towns and state capitals?

Better demographics

More stable economies

Affinity between station and university

sports teams

Approximate

Approximate

Market

College(s)

Enrollment

Market

College(s)

Enrollment

Waco, TX

62

Lincoln, NE

24

Topeka, KS

53

Bowling Green, KY

21

Lansing, MI

49

Charlottesville, VA

21

Tallahassee, FL

44

Harrisonburg, VA

20

Madison, WI

43

Reno,

NV

18

Knoxville, TN

30

Charleston-Huntington, WV

14

Lexington, KY

29

South Bend,

IN

12

Greenville, NC

28

Colorado Springs, CO

4

Parkersburg, WV

2

11

Gray Television, Inc. |

Operational Strategy Focused on

Market Leadership and Growth

Maintain and grow our market

leadership position

Continue to prudently invest in

local content and news,

syndicated programs, top talent

and community relationships

Seek new media opportunities –

currently operates web, mobile

and desktop applications in all

of our markets

Monetize digital spectrum

through growth in spectrum

channels

Pursue selective strategic

transactions

Drive free cash flow generation

Core Advertising Growth

Political Revenue

Retransmission Revenue

Internet and Socialization

Accretive Partnerships

Monetize Spectrum

Maintain

Leadership

and Grow

Free

Cash

Flow

12

Gray Television, Inc. |

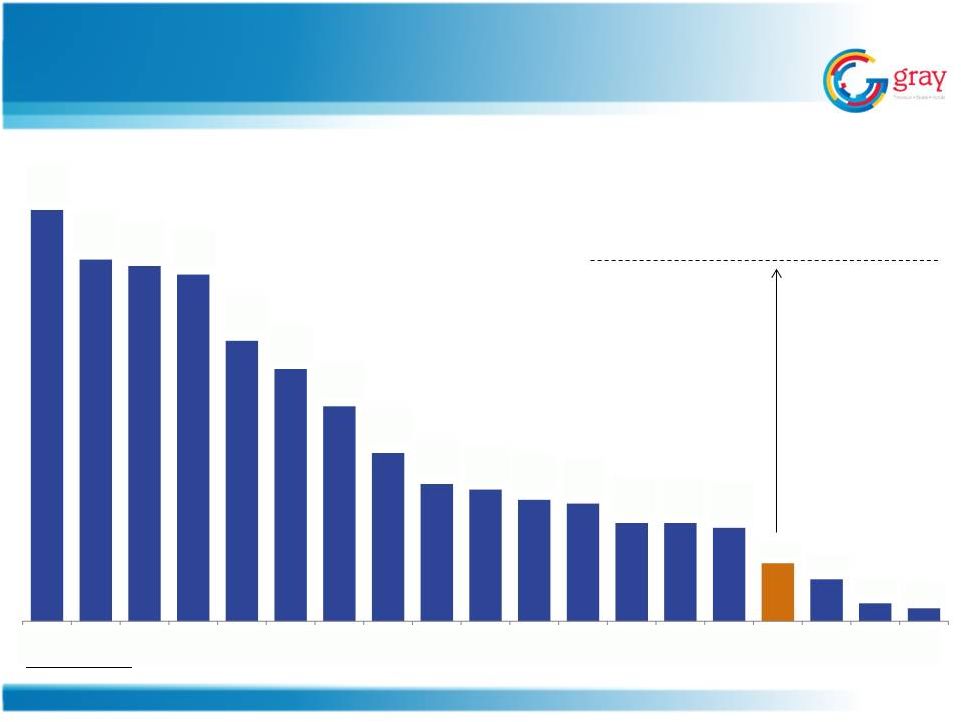

Gray

TV has Significant Opportunity to Grow Source: Company filings, BIA Investing

in Television 2013 and SNL Kagan FCC U.S. TV Household Cap of 39%

44%

39%

38%

37%

30%

27%

23%

18%

15%

14%

13%

13%

11%

11%

10%

6%

4%

2%

1%

Tribune

Sinclair

CBS

FOX

Gannett

NBC

ABC

Hearst

Media

General

Nexstar

EW

Scripps

Raycom

Cox

LIN TV

Meredith

Gray

Journal

Quincy

Hoak

13

Gray Television, Inc. |

Strategic Acquisitions and Duopoly Opportunities

Industry continues to consolidate rapidly

Gray TV’s strategic transactions should

not be impacted by proposed regulatory

thresholds

Gray TV is focused on prudently

increasing its scale through accretive

acquisitions and partnerships

In discussions with several partners

across our markets for duopoly, JSA /

SSA opportunities

Increase in scale adds to operating

leverage and negotiation power

Growth in free cash flow generation

Illustrative Stock Price Accretion

Source: Company filings

Potential for Equity Value Creation Through Accretive Acquisitions /

Duopolies Blended Buyer’s Multiple

Acquisitions /

Duopolies

0.0%

5.0%

10.0%

15.0%

8.0x

7.5x

7.0x

14

Gray Television, Inc. |

Revenue Mix Continues to Diversify

2008 Net Revenue Mix: $327 mm

2012 Net Revenue Mix: $405 mm

Growth in Net Revenue, driven by core revenue, political, retransmission and

internet Revenue mix continues to diversify from traditional ad-based

sources to new media ad-based –

Internet, and subscriber driven –

Retransmission

Lowers overall revenue volatility

Local

57%

National

21%

Political

15%

Internet

4%

Retransmission

1%

Other

3%

Local

47%

National

14%

Political

21%

Internet

6%

Retransmission

8%

Other

3%

15

Gray Television, Inc. |

All Secondary

Channels & Other

All Secondary Channels

& Other

Diversification Across Networks and Markets

46

Big

4

Affiliates:

22 CBS

11 NBC

8 ABC

5 FOX

42

Additional

Channels

(2)

with

49

Affiliations:

8 CW

17 MyNetwork TV

7 ME TV

5 Antenna TV

3 This TV Network

1 Live Well Network

8 Local News/Weather

88

channels

of

programming:

Current Station Mix

2012

1

BCF:

Top

10

Markets

2012

1

BCF

by

Affiliate:

$192.5

mm

3

(1)

LTM 2012 –

Last 12 months ended December 31, 2012.

(2)

Certain additional channels are affiliated with more than one network simultaneously. As a result, Gray

has 42 additional channels with 49 affiliations. (3) Excludes corporate

expenses. 2012

1

Revenue: Top 10 Markets

2012

1

Revenue by Affiliate: $405 mm

Charleston /

Huntington, WV

10%

Omaha, NE

7%

Madison, WI

7%

Reno, NV

6%

Lexington, KY

5%

Eau Claire, WI

5%

Tallahassee, FL

5%

Greenville, NC

5%

Lansing, MI

5%

Wausau, WI

5%

Other

43%

Lexington, KY

5%

Omaha, NE

6%

Waco -

Bryan, TX

5%

Madison, WI

5%

Reno, NV

5%

Tallahassee, FL

4%

Lansing, MI

4%

Other

50%

Charleston /

Huntington, WV

8%

South Bend, IN

4%

Eau Claire, WI

3%

45%

36%

14%

3%

2%

42%

39%

15%

2%

2%

16

Gray Television, Inc. |

Gray

is the Leading Beneficiary of Political Revenue with Large Upside

$86

Million

in

2012

–

New

Record

2011 Odd Year Record $13.5 million

Gray operates in key battleground states

#1 stations can capture over 50% of the political budget for a

market

Supreme Court decision to remove limits on corporate and union

spending on political campaigns helps drive political revenue for

Gray

Revenue from issue-based political advertising expected to

further drive growth

Local news is a key medium for political advertisers to connect

with potential voters

2012 Political as % of Total Net Revenue

Gray TV Political Commentary

Gray TV Political Revenue

Strong

Presence

in

Key

Election

States

1

$86

($ in millions)

Note: Based on as reported financials per Company filings

CAGRs

’08-’12:

16%

’06-’10: 7%

Source: Politico, Electoral-vote.com and University of Virginia Center for

Politics (1) Represents key swing states for presidential, senate and

gubernatorial elections 21.2%

15.1%

13.8%

10.4%

9.6%

Gray TV

Media

General

Lin TV

Nexstar

Sinclair

$58

$48

$53

$43

2006PF

2008

2010

2012

2004PF

GTN Overlap with Key Elections

New

Record

New

Record

17

Gray Television, Inc. |

18

Gray Television, Inc.

Automotive Ad Spending on TV Continues to

Grow and Still Below Peak Levels

Gray TV continues to benefit from the growth in auto ad spending

Auto for the first half of 2013 is up ~10%

In 2012, ~18% of Gray TV’s total broadcast advertising revenue was derived

from automotive customers TV auto ad spending growth of $0.4 billion or 16%

from 2011 to 2012 but still below peak TV Ad Spending in the Automotive

Sector ($ in billions)

SAAR of U.S. Light Vehicle Sales

(in millions)

Source: TVB and U.S. Bureau of Economic Analysis (2009A-2012A); National

Automobile Dealers Association (2013E) $3.7

$2.9

$1.7

$2.7

$2.7

$3.1

2007A

2008A

2009A

2010A

2011A

2012A

16.1

13.2

10.4

11.6

12.7

14.4

15.4

2007A

2008A

2009A

2010A

2011A

2012A

2013E |

Strong Growth in Retransmission Revenue

Over 50% of MVPD subscriber base

renewed at year-end 2011 at

significant increases

Approximately 2 million subs

re-pricing in two deals in Q4 2013

Remaining 4.5 million subs re-pricing

between 12/31/14 and 3/31/15

Anticipate significant price increase

in each case

Gray TV Retransmission Revenue

% of Total

Revenue 0.4%

0.5% 0.8% 0.9%

5.8%

5.4% 6.6% 8.3%

($ in millions)

Long

Term

Affiliate

Contracts

with

“Big

4”

Networks

17

# of

Channels

Renewal

Date

3

12-31-14

12-31-16

10

# of

Channels

Renewal

Date

1

12-31-15

1-1-16

8

# of

Channels

Renewal

Date

12-31-13

5

# of

Channels

Renewal

Date

6-30-14

2

8-31-18

22

11

19

Gray Television, Inc.

$1.0

$1.6

$2.4

$3.0

$15.6

$18.8

$20.2

$33.8

2005

2006

2007

2008

2009

2010

2011

2012 |

20

Gray Television, Inc.

Operate web and mobile

applications in all markets

Focused on local content: news,

weather, sports

Demonstrated strong growth in page

views: ‘05 to ’12: +746%

(30.6% CAGR)

All sites already converted to

responsive design

Launched live video streaming in all

markets in September 2013 through

Syncbak

Owns Moms Everyday digital

vertical; deployed in each Gray TV

market and continues to expand to

other markets

Successful Digital Media Initiatives

% of Total

Revenue 2.4%

2.3% 3.1% 3.6%

4.2% 3.9% 6.5% 6.0%

Gray TV Digital Media Revenue

($ in millions)

$6.4

$7.6

$9.5

$11.9

$11.4

$13.4

$20.1

25.0

2005

2006

2007

2008

2009

2010

2011

2012 |

21

Gray Television, Inc.

Significant Potential Upside from the Monetization of Spectrum

Unlocking the Value of Spectrum

42

additional

channels

of

programming

(including

49

affiliations

1

)

with

key

networks

including CW, MyNetwork TV, MeTv and Antenna TV

$14.9 million in 2012 Revenue

$8.2

million

in

BCF

2

–

55%

Margin

Opportunity

to

monetize

digital

spectrum

through

more

efficient

use

of

spectrum

Converting spectrum to a Content Delivery Network via Broadcast Overlay

Technology Leasing it to wireless carriers

Limited to no near-term interference from potential broadcast spectrum auction

and regulatory rulings

(1)

Certain additional channels are affiliated with more than one network

simultaneously. As a result, Gray has 42 additional channels with 49 affiliations

(2)

Excludes corporate expenses |

Industry Overview |

23

Gray Television, Inc.

Television Continues to be the #1 Choice for

Critical Mass Reach Among Advertisers

Source: TVB Media Comparison Study 2012

Program

Broadcast

Cable

Rank

Stations

TV

Total

1-25

24

1

25

26-50

24

1

25

51-75

24

1

25

76-100

24

1

25

Total

96

4

100

TV is the Most Influential Local Media

96 of the Top 100 Rated Programs are

Broadcast Programs (P18-49)

88%

73%

59%

36%

28%

25%

12%

Television

Internet

Radio

Newspaper

Mobile Phone

Magazines

Tablet

Primary

Source

of

News

Broadcast

TV

52.2%

Cable News

Networks

20.6%

Internet

22.7%

Newspapers

0.6%

Radio

3.9%

Most

Influential

of

All

Media

Television

52.1%

Newspapers

10.5%

Radio

3.8%

Magazines

8.9%

Internet

11.4%

Mobile

0.5%

Outdoor

0.5%

Other

12.3%

Source

of

Local

Weather,

Traffic

and

Sports

Broadcast TV

49.7%

Internet

17.1%

Radio

6.5%

Public TV

6.7%

Cable News

Networks

3.6%

Newspapers

2.4%

Mobile / Other

14.0%

Note: Based on 2013 season NTI Live + Same Day estimates. Ranked by average

audience % (ratings); in the event of a tie, impressions (000's) are used as a tiebreaker.

Ad-Supported Subscription television only. Programming under 5 minutes excluded

Source: TVB

TV Reaches More People than Any Other

Medium |

Strong Growth on Other Key Revenue Streams

Industry-wide

Political

Spend

on

Local

TV

1

(1) Based on Local Broadcast TV political advertising only (excludes Local Cable

TV) Source: Magna Global and SNL Kagan

Strong Growth in Retransmission Revenue

Changing Composition of Television Revenue

Ad Revenue

Gross Retrans Revenue

Online Revenue

Other Revenue

($ in billions)

CAGR

19%

14%

Gross Retrans

Net Retrans

Record level of political in 2012 and estimates for

2014 and 2016 project continued growth

TV broadcasting captures 35% of viewers but

only 7% of Retransmission Fees

$1.5

$1.7

$2.1

$2.8

$3.2

$3.7

2006A

2008A

2010A

2012A

2014E

2016E

($ in billions)

Net Retransmission Revenue as % of Gross Retransmission Revenue:

92%

79%

75%

71%

68%

68%

67%

67%

$1.8

$2.4

$3.0

$3.6

$4.3

$4.9

$5.5

$6.1

$1.6

$1.9

$2.3

$2.6

$2.9

$3.3

$3.7

$4.0

2011A

2012E

2013E

2014E

2015E

2016E

2017E

2018E

96%

1%

2%

1%

2006A

85%

9%

5%

2012A

77%

16%

6%

2016E

24

Gray Television, Inc. |

25

Gray Television, Inc.

Significant Asset Value and Transaction

Synergies for Television Broadcasters

Source: Company filings, SNL Kagan and Wall Street research

Average Blended Seller EBITDA Multiple of ~9.3x

10.0x

10.1x

8.3x

10.0x

8.3x

10.0x

10.1x

10.4x

6.2x

7.8x

12.4x

7.9x

8.9x

7.9x

9.2x

10.5x

10.2x

8.5x

9.7x

Sinclair /

Four Points

(9/2011)

Scripps /

McGraw-Hill

(10/2011)

Sinclair /

Freedom

(11/2011)

LIN /

New Vision

(9/2012)

Nexstar /

Newport

(7/2012)

Sinclair /

Newport

(7/2012)

Cox Media /

Newport

(7/2012)

Journal /

Landmark

(9/2012)

Sinclair /

Cox

(2/2013)

Sinclair /

Barrington

(2/2013)

Sinclair /

Fisher

(4/2013)

Nexstar /

CCA

(4/2013)

Sinclair /

Titan

(4/2013)

Media

General /

Young

(6/2013)

Gannett /

Belo

(6/2013)

Tribune /

Local TV

(7/2013)

Sinclair /

Allbritton

(7/2013)

Nexstar /

Citadel &

Stainless

(9/2013)

Sinclair /

New Age

(9/2013)

Stage 1: “Low hanging fruit”

Stage 2: “Merger of smaller equals”

Stage 3: “Merger of larger equals”

Stage 4: “Station Swaps”

TV broadcasting M&A activity has ramped up considerably

Sizeable individual transactions in 2013 at attractive valuations

Significant transaction synergies

M&A

Consolidation

Stages |

Financial Overview |

27

Gray Television, Inc.

(1)

Operating Cash Flow as defined in Senior Credit Facility

(2)

Net of proceeds from asset sales or dispositions and insurance proceeds

Historical

Financial

Overview

–

Continued

Growth

Net Revenue

Operating Cash Flow

1

Capital Expenditures

2

% Margin

32% 36% 26% 39%

32%

43% % of Rev

8% 5%

7% 5%

7% 6%

YOY Growth

($ in millions)

($ in millions)

($ in millions)

)

$307

$327

$270

$346

$307

$405

2007

2008

2009

2010

2011

2012

$99

$119

$71

$136

$97

$174

2007

2008

2009

2010

2011

2012

$25

$16

$18

$19

$21

$23

2007

2008

2009

2010

2011

2012

(12%)

6%

14%

17%

6%

(17%)

2YOY Growth

32%

28%

(11%) |

28

Gray Television, Inc.

% of OCF

8%

42%

N/M

37%

19%

54%

FCF/Share²

$0.17

$1.04

N/M

$0.92

$0.32

$1.64

$8

$50

($15)

$50

$18

$94

2007

2008

2009

2010

2011

2012

Free Cash Flow

1

($ and shares in millions)

Record Free Cash Flow in 2012

(1) Free Cash Flow defined as Operating Cash Flow less cash interest, cash taxes

and capital expenditures (2) Based on weighted average basic shares

outstanding Record free cash flow of $94

million in 2012

2012 OCF conversion rate into

FCF: 54%

Equity value creation through

strong free cash flow generation

Significant NOLs expected to

shield cash taxes in the near-term

Trades at a discount to peers on

a free cash flow basis with

significant potential upside |

29

Gray Television, Inc.

Net Debt

$770

$794

$828

$832

$824

$812

Net Debt +

Preferred

$870

$913

$881

$872

$824

$812

L8QA OCF

$109

$95

$104

$117

$136

$139

7.1x

8.4x

8.0x

7.1x

6.1x

5.8x

8.0x

9.6x

8.5x

7.5x

6.1x

5.8x

2008

2009

2010

2011

2012

6/30/2013

Net Debt / OCF

Net Debt + Preferred / OCF

De-levered by over $100 million (~3.8x) between December 2009 and June

2013 Consistently reduced weighted average cost of debt

Gray now generates significant free cash flow in both political and

non-political years ($ in millions)

Financial Leverage at Five Year Low

(1) Leverage shown on a two year blended basis to account for biennial shifts in

political revenues Net Financial Leverage

1

|

30

Gray Television, Inc.

Prudent Cost Management and Increasing Margins

Increasing Operating Cash Flow Margins

Gray TV continues to grow

operating margins through

identified operational

efficiencies

As of December 31, 2012,

reduced total number of

employees by 367, or 15%,

since December 31, 2007

Decreased operating costs by

converting to digital

1.23% TV Expense CAGR from

2007 –

2012

36%

39%

43%

2008

2010

2012 |

31

Gray Television, Inc.

$43

$51

YTD 2011

YTD 2013

($5)

$13

YTD 2011

YTD 2013

YTD 6/30/2013 Operating Performance Update

Strength in revenue driven by automotive and

retransmission, etc.

Local revenue +3% vs. 2012 and +6% vs. 2011

National Revenue +4% vs. 2012 and +8% vs. 2011

OCF +28% from 2010 to 2012 and +18% from

YTD 2011 to YTD 2013

Net Revenue

YTD 2013 Highlights

Operating Cash Flow

($ in millions)

($ in millions)

($ in millions)

Free Cash Flow

(1) YTD signifies year to date June 30th

$146

$163

YTD 2011

YTD 2013 |

32

32

Gray Television, Inc.

Capitalization Overview

Current and Pro Forma Capitalization

($ in Millions)

Actual

Pro Forma

1

6/30/2013

6/30/2013

Cash and Cash Equivalents

$23.4

$23.4

$40MM Revolver due 2017

$0.0

$0.0

Term Loan B due 2019 (L+350

2

/ 1.0% LIBOR Floor)

535.0

159.0

Total First Lien Debt

$535.0

$159.0

7.500% Senior Unsecured Notes due 2020

300.0

675.0

Total Debt

$835.0

$834.0

Net Debt

$811.6

$810.6

Market Capitalization

3

$484.1

$484.1

Total Capitalization

$1,319.1

$1,318.1

6/30/2013 L8QA OCF

4

$139.5

$139.5

6/30/2013 LTM OCF

5

$158.9

$158.9

Total First Lien Debt, Net Cash / L8QA OCF

3.7x

1.0x

Total Debt, Net Cash / L8QA OCF

5.8x

5.8x

Total First Lien Debt, Net Cash / LTM OCF

3.2x

0.9x

Total Debt, Net Cash / LTM OCF

5.1x

5.1x

(1)

Pro forma for October 2013 $375 million add-on to the 7.500% Senior

Notes (2)

Step down from L+375 at 6/30/13A due to paydown of Term Loan B

(3)

Based on 10/11/2013 GTN share price of $8.33 and 58.1 million shares outstanding

(combines GTN and GTN.A) (4)

OCF as defined in the existing Credit Agreement for the last eight quarters on an

annualized basis (5)

OCF as defined in the existing Credit Agreement for the last twelve months

|

33

Gray Television, Inc.

SAFE-HARBOR

Certain statements in this presentation constitute “forward-looking

statements”

within the meaning of and subject to the protections the

Private Securities Litigation Reform Act of 1995 and other federal and

state securities laws. Such forward-looking statements involve known and

unknown risks, uncertainties and other factors which may cause the actual

results, performance or achievements of the Company to be materially

different from any future results, performance or achievements expressed

or implied by such “forward-looking statements.”

See

the

Company’s

website

www.gray.tv

for

reconciliations

of

GAAP

to

non-

GAAP data. Reconciliations of broadcast cash flow, broadcast cash flow

less cash corporate expenses and free cash flow to GAAP data is

included in the financial

reports

section

of

the

www.gray.tv

website. |