Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CAESARS HOLDINGS, INC. | d602303d8k.htm |

Exhibit 99.1

Offering Memorandum Excerpts

FORWARD LOOKING STATEMENTS

This offering memorandum contains “forward-looking statements” intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995. These statements can be identified by the fact that they do not relate strictly to historical or current facts. We have based these forward-looking statements on our current expectations about future events. Further, statements that include words such as “may,” “will,” “project,” “might,” “expect,” “believe,” “anticipate,” “intend,” “could,” “would,” “estimate,” “continue,” or “pursue,” or the negative of these words or other words or expressions of similar meaning may identify forward-looking statements. These forward-looking statements are found at various places throughout this offering memorandum. These forward-looking statements, including, without limitation, those relating to future actions, new projects, strategies, future performance, the outcome of contingencies such as legal proceedings, and future financial results, wherever they occur in this offering memorandum, are necessarily estimates reflecting the best judgment of our management and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by the forward-looking statements. These forward-looking statements should, therefore, be considered in light of various important factors set forth above and in this offering memorandum.

In addition to the risk factors set forth above, important factors that could cause actual results to differ materially from estimates or projections contained in the forward-looking statements include without limitation:

| • | the impact of our substantial indebtedness and the restrictions in our debt agreements; |

| • | our dependence on Caesars Entertainment Corporation (“Caesars Entertainment”) and Caesars Entertainment Operating Company, Inc. for services pursuant to the Shared Services Agreement (as defined below), access to intellectual property rights, the Total Rewards loyalty program, its customer database and other services, rights and information; |

| • | our ability to use Caesars Entertainment’s customer-tracking, customer loyalty and yield-management programs to continue to increase customer loyalty and same-store or hotel sales; |

| • | our dependence on Caesars Entertainment’s management and the managers of our properties; |

| • | the effects of competition, including locations of competitors, growth of online gaming, competition for new licenses and operating and market competition; |

| • | reductions in consumer discretionary spending due to economic downturns or other factors; |

| • | continued growth in consumer demand for non-gaming replacing demand for gambling; |

| • | construction factors related to Project Linq, including delays, increased costs of labor and materials, availability of labor and materials, zoning issues, environmental restrictions, soil and water conditions, weather and other hazards, site access matters and building permit issues; |

| • | our ability to realize any or all of our projected increases to Adjusted EBITDA that we attribute to the completion of Project Linq; |

| • | our ability to renew our agreement to host the World Series of Poker’s Main Event; |

| • | our ability to retain our resident performers on acceptable terms; |

| • | uncertainty in the completion of projects neighboring our properties that are expected to be beneficial to our properties; |

| • | our ability to realize any or all of our projected cost savings; |

| • | changes in the extensive governmental regulations to which we are subject, and changes in laws, including increased tax rates, smoking bans, gaming regulations or accounting standards, third-party relations and approvals, and decisions, disciplines and fines of courts, regulators and governmental bodies; |

1

| • | any impairments to goodwill, indefinite-lived intangible assets, or long-lived assets that we may incur; |

| • | acts of war or terrorist incidents, severe weather conditions, uprisings or natural disasters, including losses therefrom, including losses in revenues and damage to property, and the impact of severe weather conditions on our ability to attract customers to certain of our facilities, such as the amount of losses and disruption to our business as a result of Hurricane Sandy in late October 2012; |

| • | fluctuations in energy prices; |

| • | work stoppages and other labor problems; |

| • | the impact, if any, of unfunded pension benefits under multi-employer pension plans; |

| • | our ability to recover on credit extended to our customers; |

| • | the potential difficulties in employee retention and recruitment as a result of our substantial indebtedness, the ongoing downturn in the gaming industry, or any other factor; |

| • | differences in our interests and those of our Sponsors (as defined below); |

| • | damage caused to our brands due to the unauthorized use of our brand names by third parties; |

| • | the failure of Caesars Entertainment to protect the trademarks that are licensed to us; |

| • | litigation outcomes and judicial and governmental body actions, including gaming legislative action, referenda, regulatory disciplinary actions, and fines and taxation; |

| • | our ability to access additional capital on acceptable terms or at all; |

| • | abnormal gaming holds (“gaming hold” is the amount of money that is retained by the casino from wagers by customers); |

| • | our exposure to environmental liability, including as a result of unknown environmental contamination; |

| • | our ability to recoup costs of capital investments through higher revenues; |

| • | access to insurance on reasonable terms for our assets; |

| • | the effects of compromises to our information systems or unauthorized access to confidential information or our customers’ personal information; |

| • | the effects of deterioration in the success of third parties adjacent to our business; and |

| • | the other factors set forth under “Risk Factors.” |

You are cautioned to not place undue reliance on these forward-looking statements, which speak only as of the date of this offering memorandum. We undertake no obligation to publicly update or release any revisions to these forward-looking statements to reflect events or circumstances after the date of this offering memorandum or to reflect the occurrence of unanticipated events, except as required by law.

2

The following summary contains information about the Issuers, Caesars Entertainment and the Notes. It does not contain all of the information that may be important to you in making a decision to participate in the offering. For a more complete understanding of the Issuers, Caesars Entertainment and the Notes, we urge you to read this offering memorandum carefully, including the sections entitled “Risk Factors,” “Forward Looking Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business.” Unless otherwise noted or indicated by the context, the terms “Caesars,” “Caesars Entertainment” and “CEC” refer to Caesars Entertainment Corporation, and “Caesars Entertainment Resort Properties,” “CERP,” “we,” “us” and “our” refer to the Issuers and their respective consolidated subsidiaries on a combined basis.

As of June 30, 2013, our parent, Caesars Entertainment Corporation, owned, operated or managed 52 casinos through its subsidiaries (including the Casino Resort Properties (as defined below)). In connection with the financing of the acquisition (the “Acquisition”) of Caesars Entertainment by funds affiliated with and controlled by the Sponsors (as defined below), six casinos were spun or transferred out of Caesars Entertainment Operating Company, Inc. (“CEOC”), a direct subsidiary of Caesars Entertainment, to subsidiaries of Caesars Entertainment that are organized side-by-side with CEOC (the “Casino Resort Borrowers”).

The Issuers and their subsidiaries collectively own the Casino Resort Properties, as well as Octavius Tower and Project Linq. Management of Caesars Entertainment manages all of the properties of the Issuers and those held by Caesars Entertainment’s other subsidiaries as one company, but the Issuers will not be entitled to receive any direct contribution or proceeds from the operations of Caesars Entertainment’s other subsidiaries. Neither Caesars Entertainment nor CEOC will guarantee the Notes.

Our Business

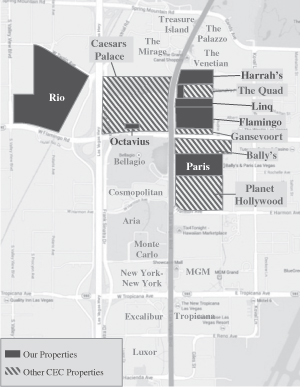

We own, through various subsidiaries, six of the 52 casino properties that are owned, operated or managed by subsidiaries of Caesars Entertainment. Our casino properties operate under the well-known Harrah’s, Rio, Paris and Flamingo brands and include four leading casino resort properties located in the heart of the attractive Las Vegas market in Las Vegas, Nevada, a leading casino resort property in Laughlin, Nevada and another in Atlantic City, New Jersey (collectively, the “Casino Resort Properties”):

| • | Paris Las Vegas: a 2,916-room hotel, a casino featuring 1,021 slot machines and 94 table games, 9 restaurants and 5 bars and clubs, and 117,000 square feet of meeting space; |

| • | Harrah’s Las Vegas: a 2,526-room hotel, a casino featuring 1,313 slot machines and 105 table games, 21 restaurants and bars, and 30,000 square feet of meeting space; |

| • | Flamingo Las Vegas: a 3,460-room hotel, a casino featuring 1,213 slot machines and 124 table games, 15 restaurants and bars, and 80,000 square feet of meeting space; |

| • | Rio All-Suite Hotel and Casino: a 2,522-room all-suite hotel, a casino featuring 1,086 slot machines and 171 table games, 21 restaurants and bars, and 160,000 square feet of meeting space; |

| • | Harrah’s Laughlin: located on the banks of the Colorado river in Laughlin, Nevada, including a 1,505-room hotel, a casino featuring 921 slot machines and 36 table games, 10 restaurants and bars, and 10,000 square feet of meeting space; and |

| • | Harrah’s Atlantic City: located in Atlantic City, New Jersey, including a 2,590-room hotel, a casino featuring 2,306 slot machine and 179 table games, 15 restaurants and bars, and 22,000 square feet of meeting space. |

3

Our properties also include three other assets in Las Vegas that are being contributed to us in connection with the refinancing of the existing debt of the Casino Resort Borrowers:

| • | Project Linq: an open-air dining, entertainment and retail development on the east side of the Las Vegas Strip, the entrance of which will directly face Caesars Palace Las Vegas. Project Linq will feature over 25 new retail, dining and entertainment offerings and is scheduled to open in phases beginning in late 2013. The property will also feature the world’s tallest observation wheel named the “High Roller,” which will be 550 feet tall and is expected to open in the second quarter of 2014; |

| • | Octavius Tower at Caesars Palace Las Vegas: a 23-story premium hotel tower on the Flamingo Avenue side of Caesars Palace Las Vegas, featuring 662 guest rooms, 60 suites and six luxury villas (the “Octavius Tower”). The Octavius Tower is operated by Desert Palace, Inc. (“Caesars Palace”) under a long-term operating lease and we receive a fixed $35 million annual payment under the terms of the lease; and |

| • | Quad Strip-Front Lease: a long-term operating lease (“Quad Strip-Front Lease”) with a subsidiary of CEOC relating to prime Las Vegas Strip parcels which are owned by one of our subsidiaries. We will receive a fixed $15 million annual payment under the terms of the lease beginning when the premises are ready to be open to the public. |

As of June 30, 2013, our facilities had an aggregate of 588,900 square feet of gaming space, 15,519 hotel rooms, 7,860 slots, 709 gaming tables, 419,000 square feet of meeting space and 96 restaurants and bars.

Pursuant to our shared services agreement with CEOC (the “Shared Services Agreement”), we have access to Caesars Entertainment’s leading brand portfolio and management expertise and expect to benefit from its corporate scale, which we anticipate will provide a competitive advantage in the operation of our properties. We also benefit from management agreements that we have entered into with management company subsidiaries of Caesars Entertainment. Under these agreements, the management companies manage the Casino Resort Properties. Caesars Entertainment is the world’s most diversified casino-entertainment provider and the most geographically diverse U.S. casino entertainment company. We also participate in Caesars Entertainment’s industry-leading customer loyalty program, Total Rewards, which has over 44 million members, including approximately 8.7 million active players. We use the Total Rewards system to market promotions and to generate customer play within our properties. For more information regarding the Shared Services Agreement and management agreements, see “Certain Relationships and Related Party Transactions.”

Caesars Entertainment revolutionized the approach the gaming industry takes with respect to marketing by introducing the Total Rewards loyalty program in 1997. Continual improvements have been made throughout the years enabling the system to remain the most effective in the industry and enabling Caesars Entertainment to grow and sustain revenues more efficiently than its largest competitors and generate cross-market play, which is defined as play by a guest in one of Caesars Entertainment’s properties outside its home market, which is where the guest signed up for Total Rewards. To support the Total Rewards loyalty program, Caesars Entertainment created the Winner’s Information Network, or WINet, the industry’s first sophisticated nationwide customer database. In combination, these systems supported the first technology-based customer relationship management strategy implemented in the gaming industry and have enabled Caesars Entertainment’s management teams to enhance overall operating results at its properties.

For the twelve months ended June 30, 2013, we derived approximately 50% of our gross revenues from gaming sources and approximately 50% from other sources, such as sales of lodging, food, beverages and entertainment. In future periods, we expect to derive additional revenue from non-gaming sources such as Project Linq and the High Roller observation wheel. For the twelve months ended June 30, 2013, we generated net revenues of $1,982.3 million, net income of $39.6 million and Property EBITDA of $537.8 million. For that same period, we generated LTM Adjusted EBITDA—Pro Forma of $599.0 million. See “Summary Historical Combined Financial Information and Other Data of Caesars Entertainment Resort Properties” for definitions of Property EBITDA and LTM Adjusted EBITDA—Pro Forma and reconciliations of these non-GAAP measures to net income.

4

Our Business and Properties

Set forth below is certain information as of June 30, 2013 concerning our casino properties, each of which is more fully described following the table below.

| Gaming Sq. Footage |

Hotel Rooms | Slots | Gaming Tables | Meeting Space Sq. Footage |

Restaurant & Bars |

|||||||||||||||||||

| Paris Las Vegas |

95,300 | 2,916 | 1,021 | 94 | 117,000 | 14 | ||||||||||||||||||

| Harrah’s Las Vegas |

93,000 | 2,526 | 1,313 | 105 | 30,000 | 21 | ||||||||||||||||||

| Flamingo Las Vegas |

72,300 | 3,460 | 1,213 | 124 | 80,000 | 15 | ||||||||||||||||||

| Rio Las Vegas |

117,300 | 2,522 | 1,086 | 171 | 160,000 | 21 | ||||||||||||||||||

| Harrah’s Laughlin |

56,000 | 1,505 | 921 | 36 | 10,000 | 10 | ||||||||||||||||||

| Harrah’s Atlantic City |

155,000 | 2,590 | 2,306 | 179 | 22,000 | 15 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total |

588,900 | 15,519 | 7,860 | 709 | 419,000 | 96 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Las Vegas Properties

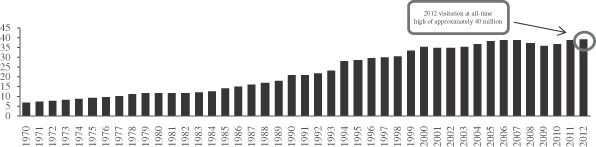

The Las Vegas market has shown signs of recovery since the visitation and spend declines in 2008 and 2009. Las Vegas visitation reached an all-time high of approximately 40 million people in 2012, and Las Vegas Strip gaming revenues for the twelve months ended June 30, 2013 were 13.3% higher than in 2009. Additionally, recent trends have reflected a growth in customer demand for non-gaming offerings. According to the Las Vegas Convention and Visitors Authority (“LVCVA”), 47% of Las Vegas visitors in 2012 indicated that their primary reason to visit was for vacation or pleasure as opposed to solely for gambling as the main attraction, up from 39% of visitors in 2008.

We believe that our portfolio of assets is well positioned to capitalize on these trends. In 2012, approximately 70% of our revenue was derived from properties located in Las Vegas and approximately 50% of our revenue was generated from non-gaming offerings. These amounts do not include expected revenue from Project Linq, which is scheduled to open in phases beginning in late 2013, the High Roller observation wheel, which is expected to open in the second quarter of 2014, or the Quad Strip-Front Lease, which will begin generating lease payments in late 2013.

Our Las Vegas properties are all strategically located in the heart of Las Vegas, with three properties (Paris, Flamingo and Harrah’s Las Vegas) located at the center of the Las Vegas Strip near or adjacent to the Project Linq development. In addition, Caesars Entertainment plans to invest approximately $195 million in the Gansevoort Las Vegas hotel (which we will not own), which is expected to open in the first quarter of 2014. The Gansevoort Las Vegas hotel will have 188 luxury hotel rooms and a new 65,000 square foot nightclub/poolclub located on the roof of the property. Our nearby Las Vegas Strip properties should benefit from the investments in, and the visitation to, these new developments. Further, all of our Las Vegas properties benefit from their prime location in the attractive Las Vegas market and from their close proximity to other casino properties owned by Caesars Entertainment, with which they share certain services and costs.

5

Paris Las Vegas is a French-themed resort, casino and entertainment facility that opened in September 1999. Strategically located in the center of the strip on Las Vegas Boulevard, the property features 14 bars and restaurants, spa services, 117,000 square feet of conference and meeting space, and distinctive entertainment offerings, currently including Jersey Boys, American Idol winner Taylor Hicks, Anthony Cools and Napoleon’s Dueling Pianos. Paris Las Vegas is home to the popular Gordon Ramsay Steak restaurant, which opened in the second quarter of 2012. The property has also recently refreshed its slot machines with new games. Paris Las Vegas also offers shopping at Le Boulevard and shares the Paris-Bally’s Promenade with Bally’s Las Vegas.

Paris Las Vegas is our most premium product offering with strong VIP play and group business. Recent initiatives continue to focus on growing high-end Asian customer visitation. Paris Las Vegas is currently being featured as a stop location for Asian VIP customers and is the only property in Las Vegas to offer a rolling chip program, similar to that offered in Macau. Rolling chips are identifiable chips that are used to track VIP wagering volume (turnover) for purposes of calculating incentives. To date these initiatives have been successful as Paris Las Vegas has experienced significant year-over-year growth in its VVIP segment of 34% in the second quarter of 2013 as compared to the second quarter of 2012 (“VVIP” is defined as guests with a theoretical daily loss between $1,000 and $74,999) and has seen strong growth in Property EBITDA for the six months ended June 30, 2013 as compared to the prior year, which was also driven in part by the implementation of resort fees and ongoing cost saving initiatives. For the twelve months ended June 30, 2013, Paris Las Vegas had approximately 73% cash room nights, 55% VIP play (defined as guests with a theoretical daily loss greater than $400) and 59% non-gaming revenue.

Harrah’s Las Vegas opened in 1973 and is located on the Las Vegas Strip, in close proximity to the Project Linq development and the Gansevoort Las Vegas hotel that is expected to open in 2014. The property features a Mardi Gras / Carnival theme with 21 restaurants and bars, a range of specialty retail shopping, spa services and

6

30,000 square feet of meeting space. The property is also home to the Carnaval Court, an open-air venue on the strip that features live music and events. Popular restaurants include the recently opened Ruth’s Chris Steak House and Toby Keith’s I Love This Bar & Grill. The property recently implemented a slot merchandising concept to better organize games by amount and type. Entertainment offerings currently include Million Dollar Quartet, which opened in February 2013, The Improv, Mac King’s Comedy and Defending the Caveman.

Harrah’s Las Vegas is one of our mid-level product offerings and benefits from strong customer loyalty cultivated since our opening. This dedicated customer base drives a high mix of casino gaming customers at the property. Harrah’s Las Vegas is located close to Project Linq and is well positioned to benefit from increased visitation to the area. The property will be accessible to Project Linq via a guest walk path from the Carnaval Court outdoor plaza, which will help guide incremental customers to the property’s entertainment and casino gaming offerings. For the twelve months ended June 30, 2013, Harrah’s Las Vegas had approximately 67% cash room nights, 43% VIP play and 49% non-gaming revenue.

Flamingo Las Vegas opened in December 1946, is located in the heart of the Las Vegas Strip and is the longest operating resort on the Strip. Its architectural theme is reminiscent of the Art Deco and Streamline Modern style of Miami and South Beach and features a garden courtyard that houses a wildlife habitat with live flamingos. The resort is home to the popular Margaritaville restaurant, bar and casino and the Center Cut Steakhouse. The Flamingo also features several entertainment offerings, currently including Donny & Marie and Legends in Concert, which recently celebrated its 30th anniversary, George Wallace, Vinny Favorito and X Burlesque, and 80,000 square feet of meeting space. The Flamingo also has a variety of activities for guests, including a large beach club and pool area that appeals to summer travelers, retail shopping and spa services. The property underwent a recent renovation of approximately 2,200 hotel rooms in 2011.

The Flamingo is one of our mid-level product offerings with a long brand history in Las Vegas that we believe has mass appeal due to its prime location and amenities. The large garden courtyard and pool area attract hotel customers and drive visitation to the property. The Flamingo is ideally situated to benefit from increased visitation driven by Project Linq, located directly to its north, and the Gansevoort Las Vegas hotel, which will be located directly to its south. In addition, the Flamingo, including the planned expansion of the main casino and the Margaritaville restaurant and casino, will have direct access to Project Linq. The Flamingo has seen strong growth in Property EBITDA for the six months ended June 30, 2013 as compared to the prior year, driven in part by the implementation of resort fees and ongoing cost saving initiatives (which were partially offset by construction disruptions at the Quad Resort & Casino). For the twelve months ended June 30, 2013, the Flamingo had approximately 80% cash room nights, 34% VIP play and 56% non-gaming revenue.

Rio Las Vegas opened in January 1990 and is located just off of the Las Vegas Strip. It was the first all-suite resort in the Las Vegas area and features a Brazilian theme inspired by the city of Rio de Janeiro. The resort offers 21 restaurants and bars, including the popular Village Seafood Buffet. The Rio is home to the World Series of Poker, an annual poker event that attracted over 75,000 entrants in 2013 over the seven weeks of the event. Rio Las Vegas also offers spa and salon services, the VooDoo Rooftop Nightclub, a large pool area, and 160,000 square feet of meeting space. The property also includes Masquerade village, which includes over 60,000 square feet of food and beverage and retail space. Rio Las Vegas features an array of shows currently including Penn & Teller, Chippendales, MJ Live, Eddie Griffin and The Rat Pack is Back.

The Rio is one of our mid-level product offerings with strong appeal to locals as compared to other casino resorts in the area and also a strong group / conference business given its substantial meeting facilities, with 160,000 square feet of meeting space. The property has recently opened several new restaurant offerings to appeal to the local Asian customer base, including KJ Dim Sum & Seafood and Pho Da Nang Vietnamese Kitchen. For the twelve months ended June 30, 2013, the Rio had approximately 68% cash room nights, 49% VIP play and 57% non-gaming revenue.

7

Project Linq is an open-air dining, entertainment and retail development located at the heart of the Las Vegas Strip and is scheduled to open in phases beginning in late 2013, with the High Roller observation wheel scheduled to open in the second quarter of 2014. Project Linq has been designed to be a destination attraction with more than 250,000 square feet of gross leasable retail and dining space and the High Roller observation wheel, which will be the world’s tallest observation wheel at 550 feet. The property is meant to be the first central “Party District” in Las Vegas, and is currently expected to include 4 bars, 12 food and beverage offerings, 7 retail outlets and an entertainment venue, with 7 additional spaces currently in negotiations. We intend to own and operate 5 spaces (which is approximately 15% of the leasable space), and 76% of the remaining space is currently subject to executed leases, with the rest of the remaining space currently in negotiations. We estimate annual base rent will produce approximately $17.1 million in gross rent revenues and $14.3 million in Adjusted EBITDA annually. These projections do not include potential rent based on the performance of our tenants’ businesses, which is included in the lease terms, or Adjusted EBITDA that will be attributable to the 5 spaces we will own and operate, including Guy’s American Kitchen and Bar and Starbucks. Other popular offerings will include: Brooklyn Bowl, Yard House, Tilted Kilt, Foto Bar, Ghirardelli and Sprinkles Cupcakes. The location will take advantage of the significant foot traffic and visitation to the Las Vegas Strip and should provide increased visitation to our nearby Strip properties by attracting visitors to the area. Project Linq is planned to appeal to the region’s growing Generation X and Generation Y clientele (ages 21 to 46) whose market share is estimated to grow in the future.

The property will be anchored on the east side by the High Roller observation wheel, which will offer breathtaking views of the famous Las Vegas Strip. Expected to open in the second quarter of 2014, the High Roller will be the tallest observation wheel in the world with 28 capsules that will feature dynamic audio and video entertainment and accommodate up to 40 passengers each.

Octavius Tower, which opened in January 2012, is the newest of Caesars Palace Las Vegas’s six hotel towers and is located on the Flamingo Avenue side of Caesars Palace Las Vegas. The 23-story high-end luxury hotel complex features 662 guest rooms, 60 suites and six luxury villas. The property offers patrons a unique luxurious resort experience with large rooms with custom furniture and technological upgrades, direct access to the Garden of the Gods pool oasis and gardens, which consists of eight pools, and a private entrance and separate hotel lobby for VIPs. The high-end luxury tower is positioned to cater to VIP customers and to target ultra high-end Asian guests. The Octavius Tower benefits from a long-term lease agreement with Caesars Palace, which has the right to operate the tower for a 15-year term. We receive a fixed $35 million annual payment, paid monthly, under the terms of the lease.

Quad Strip-Front Lease is a long-term operating lease with a subsidiary of CEOC relating to prime Las Vegas Strip parcels which are owned by one of our subsidiaries. We will receive a fixed $15 million annual payment under the terms of the lease beginning when the premises are ready to be open to the public.

Harrah’s Laughlin, which opened in August 1988, is a Mexican-themed integrated hotel and casino located along the banks of the Colorado River in Laughlin, Nevada. Harrah’s Laughlin features a festive Southwestern atmosphere and Nevada-style casino gambling 24 hours a day. It has 10 restaurants and bars, with several other entertainment offerings, including the Fiesta Showroom and a 3,000-seat Amphitheater. Harrah’s Laughlin owns a hotel guest beach, two pools, salon and day spa, boutique and gift shop. It has 10,000 square feet of conference and meeting space and is the second largest hotel and casino located in Laughlin, Nevada. The hotel and casino is located near four golf courses and features personal watercraft and water taxi access. Entertainment offerings currently include Dirk Arthur Wild Magic, Frank Marino’s Divas and Defending the Caveman. Harrah’s Laughlin focuses on underserved gaming markets and is accessible by planes chartered by CEOC that transport passengers to and from regional cities. Harrah’s Laughlin is a leading property in its market with a 26% market share and better gaming metrics as compared to its competition. Harrah’s Laughlin’s win per unit per day (including slots and table games) was $338 versus $124 for competitors for the twelve months ended June 30, 2013, which represents a $214 premium.

8

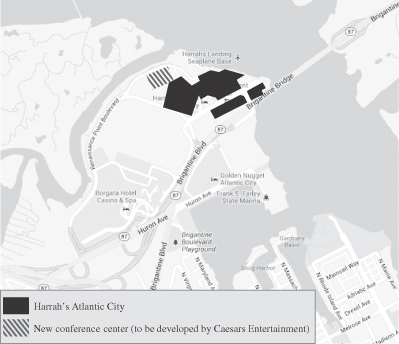

Harrah’s Atlantic City, which opened in November 1980, is an integrated hotel and resort located in the marina district of Atlantic City, New Jersey. Caesars Entertainment has invested significantly in Harrah’s Atlantic City, with over $500 million invested for a new hotel tower and new food and beverage offerings. The hotel tower was completed in 2008, adding 960 rooms, which currently makes Harrah’s Atlantic City the second largest property in Atlantic City by number of rooms. We believe the property has the number two market share based on gross gaming revenue for the twelve months ended June 30, 2013. Harrah’s Atlantic City features 15 restaurants and bars, with several new offerings including Sammy D’s, Bill’s Bar and Burger, Atlantic City Grill, Luke Palladino and Dos Caminos. The property also has a dedicated concert venue and several other amenities including the Elizabeth Arden Red Door Spa. In addition, Harrah’s Atlantic City includes an indoor domed pool area with a 33,000 square foot pool and a 14,000 square foot sundeck, both available for use year round. Harrah’s Atlantic City also has 22,000 square feet of conference and meeting space. We anticipate that this property will benefit from increased visitation as a result of Caesars Entertainment’s planned investment in a new 125,000 square foot conference center directly adjacent to the property, which will be owned by Caesars Entertainment’s other subsidiaries and not us. The $125 million conference center, which has recently begun construction, will be partially funded with $45 million of Casino Reinvestment Development Authority (“CRDA”) capital and will also take advantage of $24 million of Economic Redevelopment and Growth Grant (“ERG Grant”), and will not require any funding by us. The conference center will allow for multiple configurations, including as many as 56 individual rooms or two large ballrooms, and include state-of-the-art technology and audio-visual capabilities.

Our Competitive Strengths

We attribute our operating success and the historical strong performance of our properties to the following key strengths that differentiate us from our competition:

Las Vegas concentration and irreplaceable center-strip location. Our Las Vegas properties are located on or near the Las Vegas Strip in the heart of the attractive Las Vegas market, and approximately 70% of our 2012 revenue was generated in the Las Vegas market. We expect our Las Vegas assets will provide approximately 80% of our estimated EBITDA in the near-term. The Las Vegas market is one of most visited

9

casino resort destinations in the world and attracted a record level of approximately 40 million people in 2012. Additionally, Las Vegas Strip year-to-date revenue growth, as of June 30, 2013, has outperformed several other U.S. major metro markets. We believe we are well positioned to continue to benefit from our significant exposure to the strong Las Vegas market.

Strong non-gaming presence to capitalize on trends in Las Vegas. LVCVA reports have shown that Las Vegas visitors have become more interested in the non-gaming offerings in Las Vegas, with 47% indicating that their primary purpose for visiting was vacation or pleasure as opposed to solely for gambling, up from 39% in 2008. We currently have a strong presence in non-gaming offerings, with approximately 50% of our revenue in 2012 generated from non-gaming sources. Additionally, the new Project Linq development will feature a mid-range distinctive mix of lifestyle dining, retail and entertainment offerings to appeal to the region’s growing Generation X and Generation Y clientele (ages 21 to 46) whose market share is estimated to grow in the future.

Close proximity to new large developments in Las Vegas, driving increased visitation to our properties. Our Las Vegas properties are located near or adjacent to new large developments in Las Vegas: Project Linq (which we own) and the Gansevoort Las Vegas hotel, both of which we believe will drive increased visitation to our gaming and non-gaming assets, due to increased foot traffic and the presence of additional visitors in the vicinity of our properties. Over $500 million is being invested in Project Linq, which is scheduled to open in phases beginning in late 2013. Additionally, a newly redeveloped luxury boutique hotel, the Gansevoort Las Vegas, is currently undergoing refurbishment at the North-East corner of East Flamingo Road and Las Vegas Boulevard and is expected to open in 2014. Caesars Entertainment plans to invest approximately $195 million in the Gansevoort Las Vegas hotel, which will feature 188 luxury hotel rooms and 65,000 square foot indoor/outdoor beach club/nightclub.

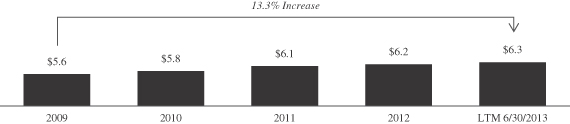

Well positioned for continued recovery in Las Vegas. Between 1970 and 2007, Las Vegas overall visitation grew at a 5% compound annual growth rate. Despite declines in 2008 and 2009 due to a broad macroeconomic slowdown, overall visitation continued to increase from 2009 through 2012. By 2012, total visitation to Las Vegas returned to all-time highs of approximately 40 million people. Las Vegas hotel average daily rate (“ADR”) has also showed signs of improvement, but still remains significantly below the peak in 2007. Las Vegas Strip gaming revenues for the twelve months ended June 30, 2013 were 13.3% higher than in 2009, but still remains approximately $540 million below peak levels. We believe we are well positioned to benefit if the recovery in Las Vegas continues as approximately 70% of our 2012 revenue was generated in the Las Vegas market.

Access to leading casino brands, a global network of casinos, a leading innovator in the gaming industry and the Total Rewards loyalty program. Caesars Entertainment is the world’s most diversified casino-entertainment provider and the most geographically diverse U.S. casino entertainment company. Caesars Entertainment currently owns, operates or manages 52 casinos (including the Casino Resort Properties) that bear many of the most recognized brand names in the gaming industry. Pursuant to the Shared Services Agreement, we have access to and utilize Caesars Entertainment’s scale and market leading position, in combination with its proprietary marketing technology and customer loyalty programs, to foster revenue growth and encourage repeat business. The close proximity of our properties in Las Vegas and Atlantic City to other casino properties of, and operated by, Caesars Entertainment allows us to leverage the Caesars brands to attract customers to our casinos and resorts. Caesars Entertainment also has a proven record of innovation, including revolutionizing our industry’s approach to marketing with the introduction of the Total Rewards loyalty program in 1997, which is currently accepted at 38 casinos in North America. We have access to the Total Rewards loyalty program, which is considered to be one of the leading loyalty rewards programs in the casino entertainment industry. For example, for the twelve months ended June 30, 2013, Caesars Entertainment had a 15% and 21% fair share premium in its destination and regional markets, respectively versus competitors. The Total Rewards loyalty program rewards customers for their brand loyalty and incentivizes them to seek out Caesars Entertainment’s brands and is connected to the Total Rewards Marketplace, comprised of 392 online retailers and over 2,000

10

stores as of June 30, 2013. Total Rewards has been successful in driving cross property play at our properties, with cross property play of approximately 47% related to our properties in 2012. Total Rewards has also been successful in improving win per position. We also benefit from the Total Rewards loyalty program through its marketing and technological capabilities in combination with Caesars Entertainment’s nationwide casino network. We believe that the Total Rewards loyalty program, along with other marketing tools, provide us with a significant competitive advantage that enables us to efficiently market our products to a large and recurring customer base.

Well-known, large entertainment facilities generating significant revenue and free cash flow. We own large scale casinos that bear some of the most highly recognized brand names in the gaming industry, including Harrah’s, Rio, Paris and Flamingo. These brands have a strong identity and enjoy widespread customer recognition. We also own two large non-gaming properties, the Octavius Tower and Project Linq. We believe the location of our casino and non-gaming properties offer distinct advantages. Our Las Vegas properties are located on or near the Las Vegas Strip and several sit among a contiguous strip of casinos owned by Caesars Entertainment. In addition, Harrah’s Atlantic City is located in Atlantic City’s marina district and Harrah’s Laughlin benefits from Caesars Entertainment’s charter flight program. We believe our properties’ prime locations, adjoining facilities and accessibility enables them to attract a significant customer base and continue to capture growth in market share. All of our casinos have been operating for over 10 years and have a successful track record of generating strong stable revenue and free cash flow.

Experienced and highly motivated management team with proven track record. We benefit from the management team, led by Caesars Entertainment’s CEO, Gary W. Loveman, that has built Caesars Entertainment into an industry leader by geographically diversifying its operations and introducing technology-based tools to loyalty programs. A former associate professor at the Harvard University Graduate School of Business Administration, Mr. Loveman joined us as Chief Operating Officer in 1998 and drew on his extensive background in retail marketing and service-management to enhance Total Rewards. Mr. Loveman has been named “Best CEO” in the gaming and lodging industry by Institutional Investor magazine four times. In addition, Caesars’ senior management operations team has an average of 27 years of industry experience. Other senior management team members possess significant experience in government and a variety of consumer industries.

Our Business Strategy

Continue to invest in new non-gaming offerings in Las Vegas to drive visitation and profitability. Trends in Las Vegas have shown that non-gaming offerings are becoming increasingly important to visitors and that Las Vegas is attracting a younger demographic. We expect this trend to continue and have been investing in new food and beverage offerings as well as other non-gaming amenities to drive increased visitation and profitability. New restaurants include Gordon Ramsay Steak at Paris, Ruth’s Chris Steak House at Harrah’s Las Vegas and expansion of the Margaritaville restaurant at Flamingo. New entertainment offerings include the Project Linq open-air dining, entertainment and retail development and the new show Million Dollar Quartet at Harrah’s Las Vegas. We derived approximately 50% of our gross revenues from gaming sources and approximately 50% from other sources, such as sales of lodging, food, beverages and entertainment, for the twelve months ended June 30, 2013.

Capitalize on the revitalization of the east side of the Las Vegas Strip. We are focused on strategically investing in our casino properties located on the east side of the Las Vegas Strip. These investments are focused on improving both gaming and non-gaming offerings, including upgrading our hotel rooms, casinos, public areas and general amenities. Over $500 million is being invested in Project Linq, a new open-air dining, entertainment and retail development, and Caesars Entertainment plans to invest approximately $195 million in the Gansevoort Las Vegas hotel, which, when it opens in 2014, will be a luxury boutique hotel with new entertainment and dining options. All of these investments should drive increased foot traffic and significant visitation to our properties.

11

Maximize our core business profitability by capitalizing on recovery in Las Vegas. While Las Vegas has shown signs of recovery, ADR is currently 33%, or $42, below the peak in 2007, revenue per available room remains approximately 25% below the peak in 2007 and gross gaming revenue is 29%, or $227 million, below the peak in 2007 of $784 million, at our Las Vegas Strip properties (Paris, Flamingo and Harrah’s Las Vegas). This is in part due to an overall general decline in the gaming market and in part due to increased capacity from new casinos. Our businesses have inherently low variable costs such that positive change in revenues should drive relatively large improvements in Property EBITDA. An increase in ADR would drive nearly a dollar for dollar improvement in Property EBITDA. For example, based on our cash room nights in 2012 of 2.3 million, we estimate that a $20 increase or $41.92 increase (which would bring ADR back to the peak in 2007 of $126.48) in ADR on an annual basis would equate to an improvement to annual Property EBITDA of approximately $46 million or $96 million, respectively. We also estimate that a $150 million increase or $227 million increase (which would bring gross gaming revenue back to the peak in 2007 of $784 million) in gross gaming revenue on an annual basis would equate to an improvement to annual Property EBITDA of approximately $98 million or $148 million, respectively. Additionally, resort fees were introduced in March 2013 at our four Las Vegas properties and are already driving incremental Property EBITDA. Resort fees range from $18 to $20 per night and provide hotel customers with access to select property amenities including fitness centers and internet access. Since the inception of the program, we believe that we have generated approximately $5 million incremental Property EBITDA with little impact to occupancy at our Las Vegas properties (which have increased from 95.5% in 2007 to 96.6% in 2012). We believe this favorable impact will increase as the program ramps to full effect and more hotel guests fall into the guidelines of the program.

Capitalize on relationship with Caesars Entertainment. Our access to the industry-leading Total Rewards loyalty program, which included over 44 million members as of June 30, 2013, improves the ability of our businesses to cross market and cross promote with Caesars Entertainment’s database and many of its casinos. This relationship allows us to utilize Caesars Entertainment’s sophisticated customer database and technology systems to efficiently and effectively manage our existing customer relationships. We leverage Caesars Entertainment’s superior marketing and technology innovation and capabilities to generate gaming revenue growth, attract additional customers and generate loyalty. In addition, we believe that through the Total Rewards loyalty program we are uniquely able to market to customers who wish to patronize a casino in their local market wherein they can accumulate rewards points redeemable in other destination markets, such as Las Vegas and Atlantic City.

Leverage Caesars Entertainment’s unique scale and proprietary loyalty programs to drive outperformance versus our competitors. We plan to continue to aggressively leverage Caesars Entertainment’s distribution platform and superior marketing and technological capabilities to generate same store gaming revenue growth and cross-market play. The Total Rewards system includes over 44 million program members. Through this system, Caesars Entertainment promotes cross-market play and targets our efforts and marketing expenditures on areas and customer segments that generate the highest return. This system, coupled with Caesars Entertainment’s vast footprint in the U.S., enables us to profitably stimulate substantial cross-market play. As part of Caesars Entertainment, we offer a unique value proposition to loyal players whereby they get the best service and product in their local market, and as a reward for their loyalty, they receive especially attentive and customized services when they visit our properties in Las Vegas and Atlantic City. This distribution strategy is unique to Caesars Entertainment and an important source of our competitive advantage. Caesars Entertainment’s extensive historical knowledge and refined decision modeling procedures enable us to distribute best practices to ensure our marketing expenditures are being used to their utmost efficiency. Given Caesars Entertainment’s historical investments in information technology and broad geographic footprint, we believe we have a competitive advantage in stimulating customer demand.

Continue to enhance the efficiency of our operations. We believe that Caesars Entertainment will continue to dedicate significant efforts towards optimizing its business and cost structure. Over the last several

12

years, the Caesars Entertainment management team has instituted operational concepts, such as LEAN operations, Kaizen and dynamic volume-based scheduling, with the intention to ensure Caesars Entertainment operates at consistently high efficiency rates. Additionally, Caesars Entertainment has consolidated activities, advanced its targeted marketing efforts and achieved procurement efficiencies. Moreover, Caesars Entertainment has achieved these cost savings while showing improved customer satisfaction levels since 2009. We initiated a cost-saving program in late 2010 that was designed to take advantage of the Caesars Entertainment’s nationwide scale. This initiative has now been fully implemented and we continue to realize cost savings. We estimate that Caesars Entertainment’s cost-savings programs realized approximately $70.3 million in incremental cost savings at our properties for the twelve months ended June 30, 2013 as compared to the twelve months ended June 30, 2012, with approximately $43 million of annualized savings yet to be realized from our properties as of June 30, 2013. Recently Caesars Entertainment embarked on an initiative to reduce corporate expenses by an additional $45 million and has identified savings that will meet or exceed that target. Our contractual share of these potential expense reductions is approximately $13.5 million.

Continued focus on differentiated customer service as a competitive advantage. Caesars Entertainment concentrates intensely on measuring and continuously improving customer service. Customer service surveys are collected weekly from guests, allowing us to pinpoint customer feedback on over 35 attributes/functional areas. Each customer service department is required to develop and implement plans to improve its individual service scores. Management bonuses, as well as individual performance evaluations, are partially dependent on achieving measured improvement on year over year customer service scores.

Leverage Caesars Entertainment’s scale to optimize our cost structure. Caesars Entertainment’s global scale provides us with significant purchasing power and provides a larger fixed cost base with which to optimize our cost structure. Caesars Entertainment’s approximate $2.1 billion of enterprise-wide supplier spend provides us with unsurpassed scale and the associated negotiating power with our suppliers, allowing us to achieve optimal terms and providing us with significant cost savings. Integration with Caesars Entertainment’s corporate services enables us to eliminate unnecessary expenses and improve efficiencies. Caesars Entertainment provides us with functional expertise in areas such as labor efficiency, food and beverage procurement and retailing to ensure that best practices are utilized throughout our business. We also benefit from shared work groups in the areas of procurement, internal audit, planning and analysis, advertising and collections. Local competitors without Caesars Entertainment’s scale would require property specific teams for these types of necessary functions. We also benefit from Caesars Entertainment’s national marketing initiatives under the Harrah’s brand name, which is the brand deployed on three of our properties. Rather than develop our own brand identity, we benefit from the nationally-recognized Harrah’s brand, and we effectively share the costs of branding and marketing Harrah’s with all other properties. We believe that without the benefit of affiliation with the Caesars Entertainment’s brands, our marketing and branding costs would be substantially higher.

The Sponsors

Apollo

Founded in 1990, Apollo is a leading global alternative asset manager with offices in New York, Los Angeles, London, Frankfurt, Luxembourg, Singapore, Hong Kong and Mumbai. As of June 30, 2013, Apollo had assets under management of approximately $113.1 billion in its private equity, capital markets and real estate businesses.

TPG

TPG is a leading global private investment firm founded in 1992 with $55.3 billion of capital under management and offices in San Francisco, Beijing, Fort Worth, Hong Kong, London, Luxembourg, Melbourne, Moscow, Mumbai, New York, Paris, Shanghai, Singapore and Tokyo. TPG has extensive experience with global public and private investments executed through leveraged buyouts, recapitalizations, spinouts, growth investments, joint ventures and restructurings.

13

Recent Developments

Estimated Impact of Completion of Project Linq

We expect that the completion of Project Linq will have a significant positive impact on our results of operations. The following discusses the estimated impact of the completion of Project Linq. These estimates assume the project is open or fully implemented and operated at a steady state, which may not occur until 12 to 24 months after the High Roller observation wheel commences operations.

End of Construction Disruption

Based upon our review of the trends and results of operations at other properties owned by Caesars Entertainment, we believe Project Linq construction has negatively impacted performance at the Casino Resort Properties since construction began in 2011, specifically at Harrah’s Las Vegas and Flamingo. We estimate the Adjusted EBITDA impact of this disruption for the twelve months ended June 30, 2013 was between $8 million and $11 million.

Operation of High Roller Observation Wheel

Based on the performance of other comparable attractions and visitation to Las Vegas, we estimate that ridership on the High Roller observation wheel will range between 3 million and 4 million passengers annually. We plan to dynamically yield pricing for tickets to ride the observation wheel and estimate that spend per passenger will likely range between $16.50 and $21.50 on average. Our estimates for the ridership on the High Roller observation wheel and the range of spend per customer are based on a third-party consultant report regarding the performance of similar attractions from 2010, prior to the time we initiated construction, as updated based upon estimates by members of management and the Project Linq design team. The High Roller observation wheel’s operations will consist mainly of fixed costs. We project margins of approximately 60% to 70%, which would yield Adjusted EBITDA from the High Roller observation wheel between $30 million to $60 million annually.

Estimated Additional Income from Project Linq

We estimate annual base rent from Project Linq will result in approximately $14.3 million of Adjusted EBITDA annually. This estimate does not include potential rent based on the performance of Project Linq’s tenants’ businesses, which is included in the lease terms. Our estimates of the performance of the tenants’ businesses are based on third-party consultant reports relating to the average sales per square foot of retail space from 2010, prior to the time we initiated construction, as updated based upon estimates by members of management. In addition, we project to generate incremental Adjusted EBITDA from the five spaces that we will own and operate. We project that the estimated potential annual rental income from Project Linq based on the performance of the tenants’ businesses and Adjusted EBITDA from the five spaces we will own and operate would collectively result in approximately $9 million to $14 million of Adjusted EBITDA annually.

Increase in Gaming Revenue

Prior to the commencement of the Project Linq construction in 2011, a pedestrian circulation analysis was performed that indicated this corridor saw more than 20 million pedestrians annually walk by its primary entranceway. We estimate that our properties should capture approximately 4% to 5% of this pedestrian traffic as

14

incremental gaming trips, at an average spend per patron of $10 to $15. Incremental gaming revenue at our Las Vegas properties is projected to have a 65% flowthrough to Adjusted EBITDA, implying a $5 million to $10 million increase in annual Adjusted EBITDA to our Casino Resort Properties from Project Linq. Additionally, we expect improved occupancy and spend at both our hotel and restaurant and bar offerings as a result of increased traffic to the area.

This “Estimated Impact of Completion of Project Linq” section and other parts of this offering memorandum contain forward-looking statements, including, without limitation, statements relating to our future actions, new projects, strategies, future performance and future financial results, and are necessarily estimates reflecting the best judgment of our management and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by such forward-looking statements. Investors should also recognize that the reliability of any forecasted financial data diminishes the farther in the future that the data is forecast. In light of the foregoing, investors are urged to put the information in context and not to place undue reliance on it. See “Forward Looking Statements” and “Risk Factors,” including “Risk Factors—Risks Related to Our Business—We may not realize any or all of our projected increases to Adjusted EBITDA, including projected increases that are attributable to the completion of Project Linq.” You are cautioned to not place undue reliance on these forward-looking statements, which represent our estimates and speak only as of the date of this offering memorandum. Prospective financial information is necessarily speculative in nature and it can be expected that some or all of the assumptions of the information described above may not materialize or will vary significantly from actual results. We undertake no obligation to update publicly any forward-looking statement for any reason after the date of this document to conform these statements to actual results or to changes to our expectations.

Formation of Caesars Entertainment Resort Properties Holdco, LLC, Caesars Entertainment Resort Properties, LLC and Caesars Entertainment Resort Properties Finance, Inc.

On August 9, 2013, (i) Caesars Entertainment Resort Properties Holdco, LLC (f/k/a Caesars NJ/NV Holdco, LLC) (“CERP Holdco”) was formed as a wholly owned subsidiary of Caesars Entertainment and a sister subsidiary of CEOC, (ii) Caesars Entertainment Resort Properties, LLC (f/k/a Caesars NJ/NV Newco, LLC) (“CERP LLC”) was formed and became a direct subsidiary of CERP Holdco and (iii) Caesars Entertainment Resort Properties Finance, Inc. (f/k/a Caesars NJ/NV Finance, Inc.) (“CERP Finance”) was formed and became a direct subsidiary of CERP LLC. CERP LLC and CERP Finance were formed to act as co-issuers in this offering and CERP Holdco was formed as an intermediate holding company. Following the Post-Closing Restructuring Transaction (as defined below), CERP LLC will be the parent company of each of the Issuers.

Transactions

Transfer of Octavius/Linq

Caesars Entertainment, through CEOC and its subsidiaries, indirectly owns Octavius/Linq Holding Co., LLC (“Octavius/Linq Holdings”) and its subsidiaries, Caesars Linq, LLC and Caesars Octavius, LLC, which own the Octavius Tower and Project Linq. On or prior to the closing date of this offering, Octavius/Linq Holding Co., LLC will form an intermediate holding company, Octavius/Linq Intermediate Holding, LLC, for the purposes of owning its existing subsidiaries named above. On the closing date of this offering, Caesars Entertainment will contribute all of the membership interests of Octavius/Linq Intermediate Holding, LLC to Rio Properties, LLC (the “Octavius/Linq Transfer”). Following the Octavius/Linq Transfer, Rio Properties, LLC, an Issuer, will own Octavius/Linq Intermediate Holdings, LLC and its subsidiaries, each of which will be a Subsidiary Guarantor.

As part of the Transactions, Octavius/Linq Holdings, which is an indirect subsidiary of CEOC that is not subject to restrictions imposed by covenants governing CEOC’s debt facilities, will transfer Octavius/Linq Intermediate Holding, LLC to Caesars Entertainment Corporation, which will then contribute Octavius/Linq

15

Intermediate Holding, LLC to Rio Properties, LLC. The Transactions will provide direct and indirect value and benefits to CEOC and its subsidiaries, including the transfer to CEOC of $69 million in aggregate principal amount (approximately $59 million aggregate market value) of one or more series of outstanding notes of CEOC (and that will be retired by CEOC), $81 million in cash and the repayment of $450 million in debt associated with these assets. Some or all of the $81 million in cash consideration may be substituted with additional outstanding notes of CEOC. In addition, by facilitating the refinancing of the CMBS Financing (as defined below), the Transactions will (a) preserve for CEOC and its subsidiaries the substantial payments made under our shared services arrangements; and (b) allow the Casino Resort Properties to continue in the Caesars corporate family, which has significant value to CEOC and its 46 owned properties, given, among other things, the prominent positions of the Casino Resort Properties on the Las Vegas Strip, the integrated operations of our casinos and the Casino Resort Properties’ participation in the Total Rewards program. We have been advised that CEOC intends to obtain an opinion of an independent financial advisor that, based upon and subject to the assumptions and other matters set forth in such opinion, it will receive reasonably equivalent value in the transfer.

Refinancing Transactions

On September 17, 2013, the Casino Resort Borrowers launched an offer to repurchase for cash (the “CMBS Repurchase”) (i) 100% of the aggregate principal amount of mortgage loans under the CMBS Financing (as defined below) at a price of $0.99 per $1.00 of principal plus accrued and unpaid interest and (ii) 100% of the aggregate principal amount of mezzanine loans under the CMBS Financing at a price of $0.90 per $1.00 of principal plus accrued and unpaid interest. The consummation of the CMBS Repurchase is conditioned upon the acceptance by lenders holding at least 65% of the outstanding aggregate principal amount of the mortgage loans and 85% of the outstanding aggregate principal amount of the mezzanine loans. The lenders under the CMBS Financing have ten business days to respond to the offer to participate in the CMBS Repurchase. As of September 17, 2013, lenders holding approximately 63% of the outstanding aggregate principal amount of mortgage loans and approximately 84% of the outstanding aggregate principal amount of mezzanine loans have accepted the offer to participate in the CMBS Repurchase.

On the closing date of this offering, we intend to (i) retire 100% of the aggregate principal amount of loans outstanding under the mortgage and mezzanine loan agreements entered into by the Casino Resort Borrowers to finance the Acquisition (the “CMBS Financing”), (ii) repay in full all amounts then outstanding under the senior secured credit facility entered into by Octavius/Linq Holding Co., LLC (the “Octavius/Linq Credit Facility”), (iii) enter into (a) a $3,000 million senior secured term loan facility, the net cash proceeds of which will be used to finance in part the repurchase of the loans under CMBS Financing and the repayment of the Octavius/Linq Credit Facility, and (b) a senior secured revolving credit facility providing a revolving line of credit of up to $269.5 million (together, the “Senior Secured Credit Facilities”) and (iv) issue $500.0 million of the First Lien Notes and $1,350.0 million of the Second Lien Notes, the net cash proceeds of which will be used to finance in part the repurchase of the loans under the CMBS Financing and the repayment of the Octavius/Linq Credit Facility ((i), (ii), (iii) and (iv) are collectively referred to as the “Refinancing Transactions”). The Refinancing Transactions and any other related transactions are subject to regulatory approval and market and other conditions, and may not occur as described or at all.

After June 30, 2013, we repurchased approximately $49.8 million principal amount of the mezzanine loans that were outstanding under the CMBS Financing. As used in this offering memorandum, the term “Transactions” refers collectively to the Octavius/Linq Transfer, the repurchase of approximately $49.8 million principal amount of the mezzanine loans that were outstanding under the CMBS Financing after June 30, 2013, the CMBS Repurchase and the Refinancing Transactions.

16

Restructuring Transactions

Pre-Closing Restructuring Transaction

On or prior to the closing date of this offering, we intend to enter into a series of transactions that are intended to simplify our existing organizational structure (the “Pre-Closing Restructuring Transaction”). In connection with the Pre-Closing Restructuring Transaction, certain subsidiaries of Paris Las Vegas Holding, LLC, Harrah’s Las Vegas, LLC, Flamingo Las Vegas Holding, LLC, Rio Properties, LLC and Harrah’s Laughlin, LLC will be merged out of existence and, in addition, certain unoccupied parcels of land not owned by the Casino Resort Borrowers will be transferred to subsidiaries of Caesars Entertainment. Additionally, as discussed above, as part of the Transactions, on or prior to the closing date of this offering, we will consummate the Octavius/Linq Transfer.

Post-Closing Restructuring Transaction

If we receive all required regulatory approvals, which may not occur for several months, we intend to reorganize our structure through a series of transactions that will result in all of the Issuers being direct subsidiaries of CERP LLC. In connection with this reorganization, Harrah’s Atlantic City Holding, Inc., Paris Las Vegas Holding, LLC and Flamingo Las Vegas Holding, LLC will be merged into CERP LLC. Some of the Issuers’ subsidiaries will also be merged out of existence in connection with these transactions. See “Organizational Structure.”

In addition, upon or following the closing of this offering, we intend to subdivide and transfer a portion of the real property next to Harrah’s Atlantic City to an indirect subsidiary of Caesars Entertainment (“Conference Newco”). The transfer of such real property and any corresponding release of security therein is contemplated by the terms of the CMBS Financing. Caesars Entertainment plans to build the new conference center on such real property. Harrah’s Atlantic City will provide services to the convention center pursuant to a new management agreement.

The transactions described in the preceding two paragraphs are referred to as the “Post-Closing Restructuring Transaction.”

17

Organizational Structure

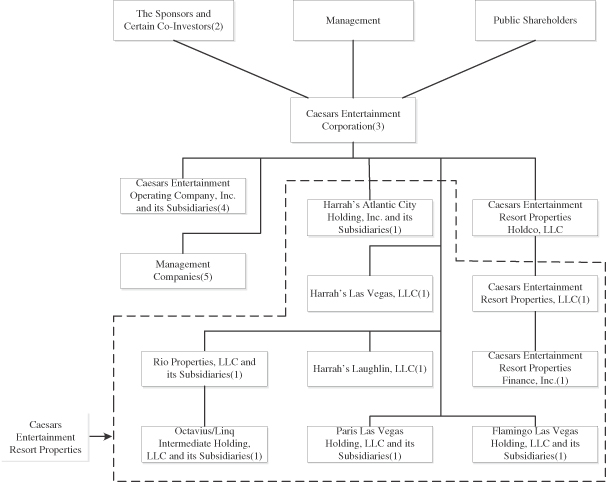

Structure Before Post-Closing Restructuring Transaction

The diagram below is a summary of our organizational structure after giving effect to the Pre-Closing Restructuring Transaction, the Transactions, including the Octavius/Linq Transfer, and prior to the Post-Closing Restructuring Transaction.

| (1) | After giving effect to the Transactions, each Issuer’s indebtedness will include $500.0 million of First Lien Notes, $1,350.0 million of Second Lien Notes and $3,000.0 million of indebtedness outstanding under the Senior Secured Credit Facilities (with $269.5 million of unutilized capacity under the revolving credit facility portion of the Senior Secured Credit Facilities). In connection with the Post-Closing Restructuring Transaction, Harrah’s Atlantic City Holding, Inc., Paris Las Vegas Holding, LLC and Flamingo Las Vegas Holding, LLC will be merged out of existence. Some of the Issuers’ subsidiaries will also be merged out of existence in connection with the Post-Closing Restructuring Transaction. Each of the wholly owned domestic subsidiaries of the Issuers will guarantee the Issuers’ obligations under the First Lien Notes, the Second Lien Notes and the Senior Secured Credit Facilities and pledge its assets to secure the First Lien Notes, the Second Lien Notes and the Senior Secured Credit Facilities; provided, however, that the equity interests of the Issuers’ subsidiaries that have been pledged to secure the Issuers’ and the Subsidiary |

18

| Guarantors’ obligations under the Senior Secured Credit Facilities will, upon our filing of a registration statement with the SEC under the terms of the registration rights agreement, be released from the collateral securing the First Lien Notes and the Second Lien Notes to the extent it would require separate financial statements under Regulation S-X of the Securities Act. See “Description of First Lien Notes—Security for the Notes,” “Description of Second Lien Notes—Security for the Notes” and “Registration Rights; Additional Interest.” |

| (2) | Shares held by funds affiliated with and controlled by the Sponsors and their co-investors, representing approximately 69.4% of Caesars Entertainment’s outstanding common stock as of June 30, 2013, are subject to the irrevocable proxy that gives Hamlet Holdings LLC (“Hamlet Holdings”), the members of which are comprised of individuals affiliated with the Sponsors, sole voting and sole dispositive power with respect to such shares. |

| (3) | Caesars Entertainment currently guarantees all of the debt securities of CEOC and CEOC’s senior secured credit facilities. Caesars Entertainment will not guarantee, or pledge its assets as security for, the First Lien Notes, the Second Lien Notes or the Senior Secured Credit Facilities. Not all subsidiaries of Caesars Entertainment are depicted. |

| (4) | CEOC and its subsidiaries will not guarantee, or pledge their assets as security for, the First Lien Notes, the Second Lien Notes, the Senior Secured Credit Facilities or any other indebtedness of the Issuers and are not liable for any obligations thereunder. |

| (5) | Our casino properties are managed by management companies that are subsidiaries of Caesars Entertainment. The management companies will not guarantee, or pledge their assets as security for, the First Lien Notes, the Second Lien Notes, the Senior Secured Credit Facilities or any other indebtedness of the Issuers and are not liable for any obligations thereunder. |

19

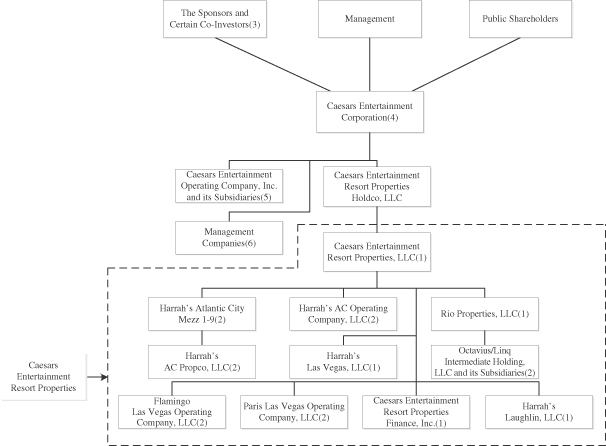

Structure After Post-Closing Restructuring Transaction

The diagram below is a summary of our organizational structure following the Post-Closing Restructuring Transaction.

| (1) | After giving effect to the Transactions, each Issuer’s indebtedness will include $500.0 million of First Lien Notes, $1,350.0 million of Second Lien Notes and $3,000.0 million of indebtedness outstanding under Senior Secured Credit Facilities (with $269.5 million of unutilized capacity under the revolving credit facility portion of the Senior Secured Credit Facilities). |

| (2) | Each of the wholly owned domestic subsidiaries of CERP LLC (other than the other Issuers) will guarantee the Issuers’ obligations under the First Lien Notes, the Second Lien Notes and the Senior Secured Credit Facilities and pledge its assets to secure the First Lien Notes, the Second Lien Notes and the Senior Secured Credit Facilities; provided, however, that the equity interests of the Issuers’ subsidiaries that have been pledged to secure the Issuers’ and the Subsidiary Guarantors’ obligations under the Senior Secured Credit Facilities will, upon our filing of a registration statement with the SEC under the terms of the registration rights agreement, be released from the collateral securing the First Lien Notes and the Second Lien Notes to the extent it would require separate financial statements under Regulation S-X of the Securities Act. See “Description of First Lien Notes—Security for the Notes,” “Description of Second Lien Notes—Security for the Notes” and “Registration Rights; Additional Interest.” |

| (3) | Shares held by funds affiliated with and controlled by the Sponsors and their co-investors, representing approximately 69.4% of Caesars Entertainment’s outstanding common stock as of June 30, 2013, are subject |

20

| to the irrevocable proxy that gives Hamlet Holdings the members of which are comprised of individuals affiliated with the Sponsors, sole voting and sole dispositive power with respect to such shares. |

| (4) | Caesars Entertainment currently guarantees all of the debt securities of CEOC and CEOC’s senior secured credit facilities. Caesars Entertainment will not guarantee, or pledge its assets as security for, the First Lien Notes, the Second Lien Notes or the Senior Secured Credit Facilities. Not all subsidiaries of Caesars Entertainment are depicted. |

| (5) | CEOC and its subsidiaries will not guarantee, or pledge their assets as security for, the First Lien Notes, the Second Lien Notes, the Senior Secured Credit Facilities or any other indebtedness of the Issuers and are not liable for any obligations thereunder. |

| (6) | Our casino properties are managed by management companies that are subsidiaries of Caesars Entertainment. The management companies will not guarantee, or pledge their assets as security for, the First Lien Notes, the Second Lien Notes, the Senior Secured Credit Facilities or any other indebtedness of the Issuers and are not liable for any obligations thereunder. |

Additional Information

Our principal executive offices are located at One Caesars Palace Drive, Las Vegas, NV 89109 and our telephone number is (702) 407-6000. The address of Caesars Entertainment’s internet site is http://www.caesars.com. This internet address is provided for informational purposes only and is not intended to be a hyperlink. Accordingly, no information at this internet address is included or incorporated by reference herein.

21

Summary Historical Combined Financial Information and Other Data

of Caesars Entertainment Resort Properties

The following table presents the unaudited historical combined financial statements of Caesars Entertainment Resort Properties for the years ended December 31, 2011 and 2012, for the six month periods ended June 30, 2012 and 2013 and for the twelve months ended June 30, 2013.

The following tables and related footnotes contain forward-looking statements, including, without limitation, statements relating to our future actions, new projects, strategies, future performance and future financial results, and are necessarily estimates reflecting the best judgment of our management and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by such forward-looking statements. These forward-looking statements should, therefore, be considered in light of various important factors set forth in the sections entitled “Forward Looking Statements” and “Risk Factors.” You are cautioned to not place undue reliance on these forward-looking statements, which speak only as of the date of this offering memorandum.

22

| (in millions, except ratios) |

Year ended December 31, 2011(1) |

Year ended December 31, 2012(1) |

Six months ended June 30, 2012(1) |

Six months ended June 30, 2013(1) |

Twelve months ended June 30, 2013(1) |

|||||||||||||||

| Income Statement Data |

||||||||||||||||||||

| Revenues |

||||||||||||||||||||

| Casino |

$ | 1,229.0 | $ | 1,192.7 | $ | 612.9 | $ | 581.5 | $ | 1,161.3 | ||||||||||

| Food and beverage |

501.2 | 505.5 | 259.2 | 253.7 | 500.0 | |||||||||||||||

| Rooms |

453.4 | 446.0 | 230.8 | 228.0 | 443.2 | |||||||||||||||

| Other |

200.2 | 210.2 | 104.0 | 111.7 | 217.9 | |||||||||||||||

| Less: casino promotional allowances |

(363.0 | ) | (351.5 | ) | (177.6 | ) | (166.2 | ) | (340.1 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net revenues |

2,020.8 | 2,002.9 | 1,029.3 | 1,008.7 | 1,982.3 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating Expenses |

||||||||||||||||||||

| Direct |

||||||||||||||||||||

| Casino |

638.0 | 623.0 | 317.7 | 283.8 | 589.1 | |||||||||||||||

| Food and beverage |

243.6 | 248.2 | 126.3 | 121.0 | 242.9 | |||||||||||||||

| Rooms |

115.8 | 121.1 | 63.1 | 62.9 | 120.9 | |||||||||||||||

| Property, general, administrative and other |

524.4 | 494.3 | 250.5 | 247.8 | 491.6 | |||||||||||||||

| Depreciation and amortization |

162.7 | 192.8 | 97.9 | 81.7 | 176.6 | |||||||||||||||

| Write-downs, reserves, and project opening costs, net of recoveries |

7.2 | 21.5 | 5.9 | 18.7 | 34.3 | |||||||||||||||

| Intangible and tangible asset impairment charges |

— | 3.0 | — | 24.4 | 27.4 | |||||||||||||||

| Loss/(income) on interests in non-consolidated affiliates |

1.0 | (1.4 | ) | (0.5 | ) | (2.7 | ) | (3.6 | ) | |||||||||||

| Corporate expense |

85.0 | 80.3 | 40.4 | 25.2 | 65.1 | |||||||||||||||

| Acquisition and integration costs |

0.2 | — | — | — | — | |||||||||||||||

| Amortization of intangible assets |

59.6 | 59.0 | 29.5 | 29.5 | 59.0 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total operating expenses |

1,837.5 | 1,841.8 | 930.8 | 892.3 | 1,803.3 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income from operations |

183.3 | 161.1 | 98.5 | 116.4 | 179.0 | |||||||||||||||

| Interest expense, net of interest capitalized |

(218.6 | ) | (231.8 | ) | (119.8 | ) | (108.4 | ) | (220.4 | ) | ||||||||||

| Gain on early extinguishments of debt |

47.5 | 135.0 | 78.5 | 39.0 | 95.5 | |||||||||||||||

| Other income, including interest income |

1.3 | 1.0 | 0.6 | 0.1 | 0.5 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before income taxes |

13.5 | 65.3 | 57.8 | 47.1 | 54.6 | |||||||||||||||

| Provision for income taxes |

(4.3 | ) | (21.9 | ) | (20.0 | ) | (13.1 | ) | (15.0 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 9.2 | $ | 43.4 | $ | 37.8 | $ | 34.0 | $ | 39.6 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Other Financial Data |

||||||||||||||||||||

| Capital expenditures, net of changes in construction payables |

$ | 126.7 | $ | 246.7 | $ | 97.5 | $ | 148.8 | $ | 298.0 | ||||||||||

| Property EBITDA(2) |

499.0 | 516.3 | 271.7 | 293.2 | 537.8 | |||||||||||||||

| Ratio of earnings to fixed charges |

— | 1.2 | x | 1.4 | x | 1.4 | x | 1.2 | x | |||||||||||

| Net first lien secured debt to LTM Adjusted EBITDA—Pro Forma(3)(4) |

|

5.7 | x | |||||||||||||||||

| Net debt to LTM Adjusted EBITDA—ProForma(3)(4) |

|

8.0 | x | |||||||||||||||||

| Estimated range of net first lien secured debt to Projected Run-Rate LTM Adjusted EBITDA—Pro Forma(3)(4) |

|

5.0x – 5.3 | x | |||||||||||||||||

| Estimated range of net debt to Projected Run-Rate LTM Adjusted EBITDA—Pro Forma(3)(4) |

|

7.0x –7.5 | x | |||||||||||||||||

| LTM Adjusted EBITDA—Pro Forma(4) |

|

$ | 599.0 | |||||||||||||||||