Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SEACOAST BANKING CORP OF FLORIDA | v351325_8k.htm |

| EX-99.1 - EXHIBIT 99.1 - SEACOAST BANKING CORP OF FLORIDA | v351325_ex99-1.htm |

| EX-99.2 - EXHIBIT 99.2 - SEACOAST BANKING CORP OF FLORIDA | v351325_ex99-2.htm |

Second Quarter 2013 July 29, 2013

2 Cautionary Notice Regarding Forward - Looking Statements This press release contains “forward - looking statements” within the meaning of Section 27 A of the Securities Act of 1933 and Section 21 E of the Securities Exchange Act of 1934 , including, without limitation, statements about future financial and operating results, ability to realized deferred tax assets, cost savings, enhanced revenues, economic and seasonal conditions in our markets, and improvements to reported earnings that may be realized from cost controls and for integration of banks that we have acquired, as well as statements with respect to Seacoast’s objectives, expectations and intentions and other statements that are not historical facts . Actual results may differ from those set forth in the forward - looking statements . Forward - looking statements include statements with respect to our beliefs, plans, objectives, goals, expectations, anticipations, estimates and intentions, and involve known and unknown risks, uncertainties and other factors, which may be beyond our control, and which may cause the actual results, performance or achievements of Seacoast to be materially different from future results, performance or achievements expressed or implied by such forward - looking statements . You should not expect us to update any forward - looking statements . You can identify these forward - looking statements through our use of words such as “may,” “will,” “anticipate,” “assume,” “should,” “support”, “indicate,” “would,” “believe,” “contemplate,” “expect,” “estimate,” “continue,” “further”, “point to,” “project,” “could,” “intend” or other similar words and expressions of the future . These forward - looking statements may not be realized due to a variety of factors, including, without limitation : the effects of future economic and market conditions, including seasonality ; governmental monetary and fiscal policies, as well as legislative, tax and regulatory changes ; changes in accounting policies, rules and practices ; the risks of changes in interest rates on the level and composition of deposits, loan demand, liquidity and the values of loan collateral, securities, and interest sensitive assets and liabilities ; interest rate risks, sensitivities and the shape of the yield curve ; the effects of competition from other commercial banks, thrifts, mortgage banking firms, consumer finance companies, credit unions, securities brokerage firms, insurance companies, money market and other mutual funds and other financial institutions operating in our market areas and elsewhere, including institutions operating regionally, nationally and internationally, together with such competitors offering banking products and services by mail, telephone, computer and the Internet ; and the failure of assumptions underlying the establishment of reserves for possible loan losses . The risks of mergers and acquisitions, include, without limitation : unexpected transaction costs, including the costs of integrating operations ; the risks that the businesses will not be integrated successfully or that such integration may be more difficult, time - consuming or costly than expected ; the potential failure to fully or timely realize expected revenues and revenue synergies, including as the result of revenues following the merger being lower than expected ; the risk of deposit and customer attrition ; any changes in deposit mix ; unexpected operating and other costs, which may differ or change from expectations ; the risks of customer and employee loss and business disruption, including, without limitation, as the result of difficulties in maintaining relationships with employees ; increased competitive pressures and solicitations of customers by competitors ; as well as the difficulties and risks inherent with entering new markets . All written or oral forward - looking statements attributable to us are expressly qualified in their entirety by this cautionary notice, including, without limitation, those risks and uncertainties described in our annual report on Form 10 - K for the year ended December 31 , 2012 under “Special Cautionary Notice Regarding Forward - Looking Statements” and “Risk Factors”, and otherwise in our SEC reports and filings . Such reports are available upon request from the Company, or from the Securities and Exchange Commission, including through the SEC’s Internet website at http : //www . sec . gov .

3 Generating Momentum – Highlights, YTD 2013 Building Shareholder Value • Net income for the first six months of 2013 totaled $5.0 million, $6.4 million higher than the prior year’s result. • Net loan outstandings increased $39.8 million from December 2012 (6.5% on an annualized basis) • Noninterest income excluding security gains for the first six months of 2013 up 20.8%, the result of better performance in deposit interchange and service charges, mortgage banking fees, and wealth management revenue . • Total revenues excluding security gains increased $1.6 million to $44.4 million year to date. • Performance restoration plan results in noninterest expense reduction of 10.4% or $4.4 million when compared to the first six months of 2012. Growing Our Franchise • Customer demand deposits increased $75 million or 19%, year over year. • Originated $305 million in loans over the first six months, up 45% over the prior year • Added seasoned commercial acquisition teams in key markets, four commercial focused offices opened, with one additional office to open in late 2013. • Rebranded digital offerings, launched tablet platform, and enhanced ATM capabilities. Reducing our Risk Posture • Net charge - offs of $3.5 million for the first six months, compared to $9.7 million one year prior. • Nonperforming loans declined by $15.2 million, or 31% when compared to the second quarter of 2012. • Accruing restructured loans reduced by $25.2 million, or 46% when compared to the second quarter of 2012 • Nonperforming assets to total assets of 1.98%

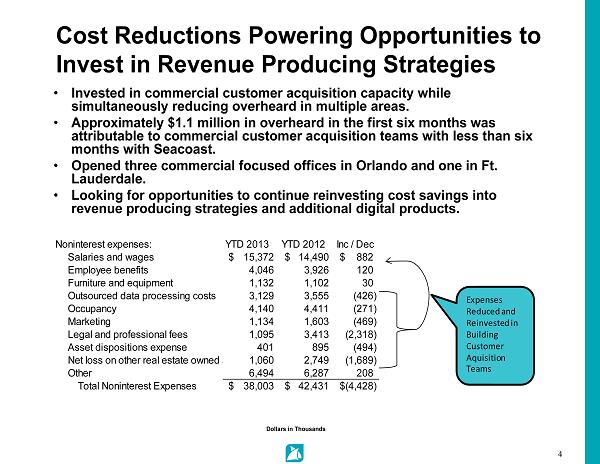

4 Cost Reductions Powering Opportunities to Invest in Revenue Producing Strategies • Invested in commercial customer acquisition capacity while simultaneously reducing overheard in multiple areas. • Approximately $1.1 million in overheard in the first six months was attributable to commercial customer acquisition teams with less than six months with Seacoast. • Opened three commercial focused offices in Orlando and one in Ft. Lauderdale. • Looking for opportunities to continue reinvesting cost savings into revenue producing strategies and additional digital products. Noninterest expenses: YTD 2013 YTD 2012 Inc / Dec Salaries and wages 15,372$ 14,490$ 882$ Employee benefits 4,046 3,926 120 Furniture and equipment 1,132 1,102 30 Outsourced data processing costs 3,129 3,555 (426) Occupancy 4,140 4,411 (271) Marketing 1,134 1,603 (469) Legal and professional fees 1,095 3,413 (2,318) Asset dispositions expense 401 895 (494) Net loss on other real estate owned and repossessed assets1,060 2,749 (1,689) Other 6,494 6,287 208 Total Noninterest Expenses 38,003$ 42,431$ (4,428)$ Expenses Reduced and Reinvested in Building Customer Aquisition Teams Dollars in Thousands

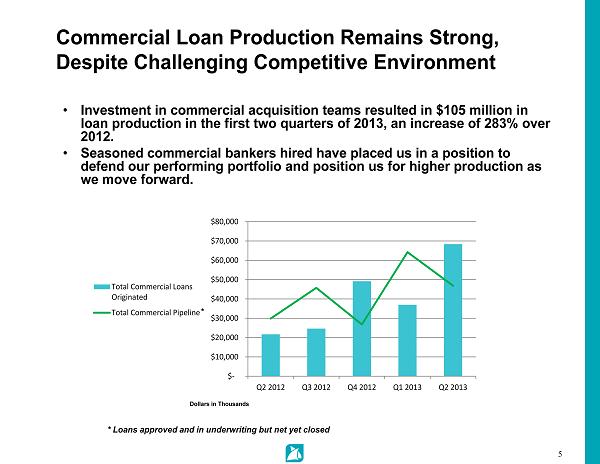

5 Commercial Loan Production Remains Strong, Despite Challenging Competitive Environment • Investment in commercial acquisition teams resulted in $105 million in loan production in the first two quarters of 2013, an increase of 283% over 2012. • Seasoned commercial bankers hired have placed us in a position to defend our performing portfolio and position us for higher production as we move forward. * * Loans approved and in underwriting but net yet closed Dollars in Thousands $ - $10,000 $20,000 $30,000 $40,000 $50,000 $60,000 $70,000 $80,000 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Total Commercial Loans Originated Total Commercial Pipeline

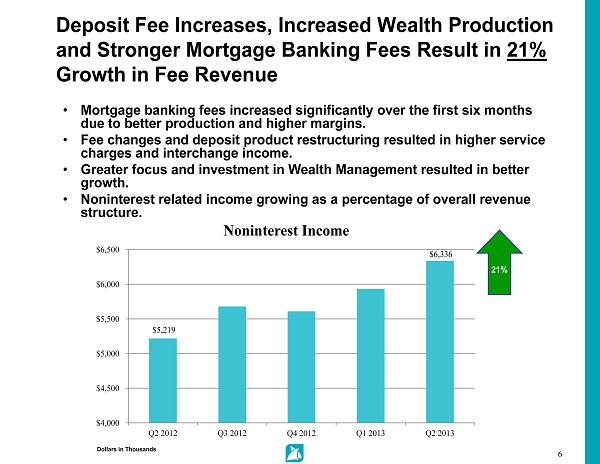

6 Deposit Fee Increases, Increased Wealth Production and Stronger Mortgage Banking Fees Result in 21% Growth in Fee Revenue $5,219 $6,336 $4,000 $4,500 $5,000 $5,500 $6,000 $6,500 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Noninterest Income • Mortgage banking fees increased significantly over the first six months due to better production and higher margins. • Fee changes and deposit product restructuring resulted in higher service charges and interchange income. • Greater focus and investment in Wealth Management resulted in better growth. • Noninterest related income growing as a percentage of overall revenue structure. 21% Dollars in Thousands

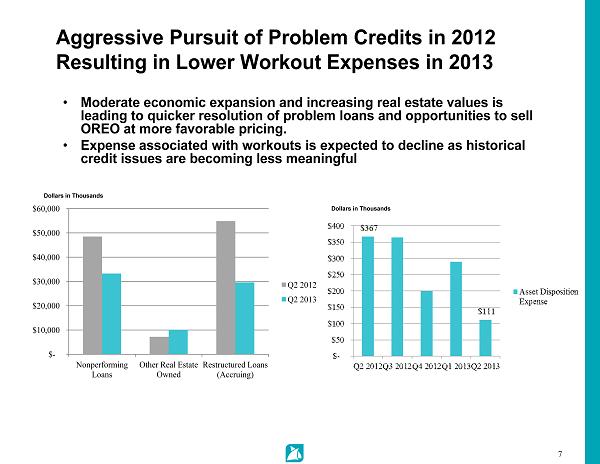

7 Aggressive Pursuit of Problem Credits in 2012 Resulting in Lower Workout Expenses in 2013 • Moderate economic expansion and increasing real estate values is leading to quicker resolution of problem loans and opportunities to sell OREO at more favorable pricing. • Expense associated with workouts is expected to decline as historical credit issues are becoming less meaningful Dollars in Thousands Dollars in Thousands $ - $10,000 $20,000 $30,000 $40,000 $50,000 $60,000 Nonperforming Loans Other Real Estate Owned Restructured Loans (Accruing) Q2 2012 Q2 2013

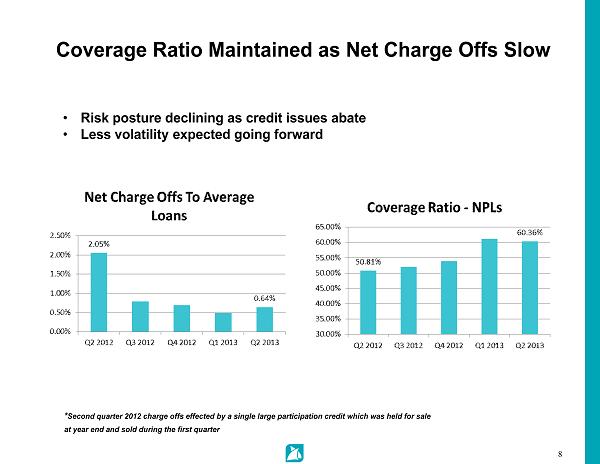

8 Coverage Ratio Maintained as Net Charge Offs Slow • Risk posture declining as credit issues abate • Less volatility expected going forward * Second quarter 2012 charge offs effected by a single large participation credit which was held for sale at year end and sold during the first quarter

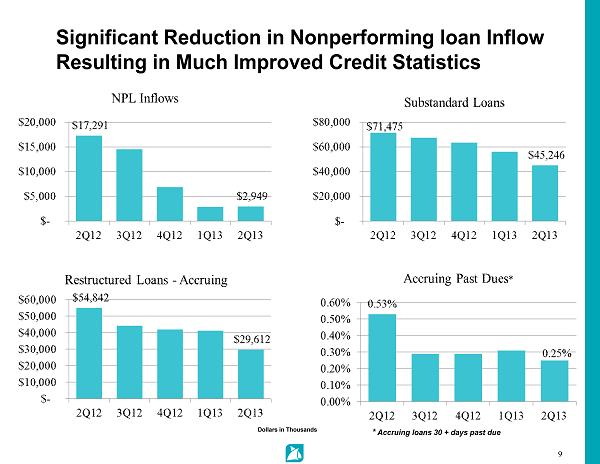

9 Significant Reduction in Nonperforming loan Inflow Resulting in Much Improved Credit Statistics Dollars in Thousands * Accruing loans 30 + days past due

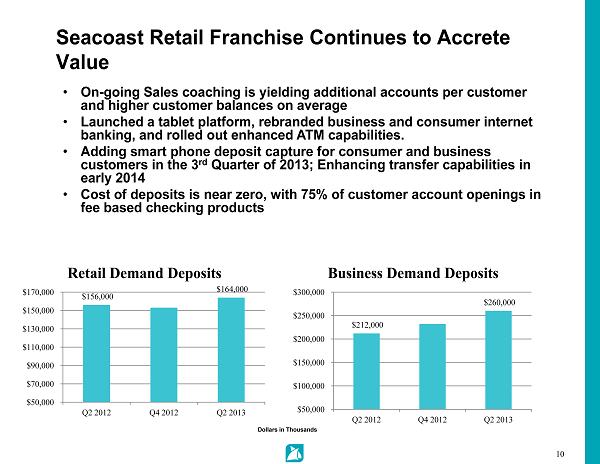

10 Seacoast Retail Franchise Continues to Accrete Value • On - going Sales coaching is yielding additional accounts per customer and higher customer balances on average • Launched a tablet platform, rebranded business and consumer internet banking, and rolled out enhanced ATM capabilities. • Adding smart phone deposit capture for consumer and business customers in the 3 rd Quarter of 2013; Enhancing transfer capabilities in early 2014 • Cost of deposits is near zero, with 75% of customer account openings in fee based checking products Dollars in Thousands $156,000 $164,000 $50,000 $70,000 $90,000 $110,000 $130,000 $150,000 $170,000 Q2 2012 Q4 2012 Q2 2013 Retail Demand Deposits $212,000 $260,000 $50,000 $100,000 $150,000 $200,000 $250,000 $300,000 Q2 2012 Q4 2012 Q2 2013 Business Demand Deposits

11 2013 - 2014 Priorities Building Shareholder Value • Continue expense control posture, maximize revenue opportunities and position the bank for stronger earnings in 2014 • Continue reducing risk posture, positioning for an exit of the formal agreement and DTA recovery • Position for offensive strategic opportunities and higher ROE in 2014 Growing Our Franchise • Enhance value proposition with innovative digital product offerings and enhanced customer interactions • Examine branch network for opportunities for reinvestment and enhancements to increase customer experience • Continue refining our commercial and business banking strategy; develop out branding and presence in Orlando, Boca Raton and Ft. Lauderdale • Look for opportunities to expand our presence into the deeper markets of Orlando and South Florida.

12