Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - ENCORE CAPITAL GROUP INC | d538431d8k.htm |

ENCORE CAPITAL GROUP, INC.

May 2013

JMP Securities 12th Annual Research Conference

Exhibit 99.1 |

PROPRIETARY

2

CAUTIONARY NOTE ABOUT FORWARD-LOOKING STATEMENTS

|

PROPRIETARY

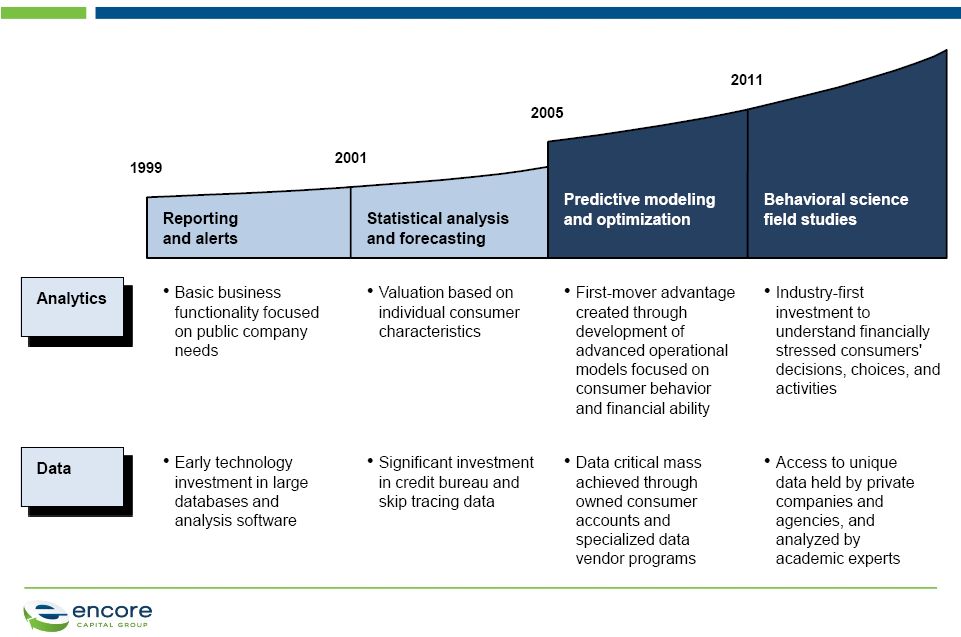

ENCORE IS A GROWING COMPANY WITH SOPHISTICATED

OPERATIONS AND DEEP CONSUMER EXPERTISE

3

1

in

7

American

consumers

have

accounts with us

3.1 million

consumers have

satisfied their obligations

$1.9

billion

in

estimated

remaining collections

27%

Adjusted

EBITDA

†

5-year

compound annual growth rate

2,800

employees worldwide

$987 million

collected in the last

twelve months

†

See endnote |

PROPRIETARY

ENCORE IS A LEADING PLAYER IN THE CONSUMER DEBT BUYING AND

RECOVERY INDUSTRY

Global Capabilities

Business Description

•

Purchase and collection of charged-off

unsecured consumer receivables (primarily

credit card)

•

Provision of tax lien transfers, and purchase of

tax lien certificates, through Propel subsidiary

•

Robust business model emphasizing

consumer intelligence and

operational

specialization

•

Invested ~$2.8 billion to acquire receivables

with a face value of ~$80

billion

•

Acquired ~49 million consumer accounts

since

inception

4 |

PROPRIETARY

OUR FIRST QUARTER RESULTS DEMONSTRATED STRONG

GROWTH

Q1 2013

Q1 2012

Increase/

(Decrease)

Collections

$270

$231

17%

Revenue

$144

$126

14%

Cost to collect

36.5%

38.4%

(190 bps)

Adjusted EBITDA†

$174

$144

21%

EPS*

$0.86

$0.70

23%

5

(in $M -

except CTC and EPS)

†

See endnote for a reconciliation to GAAP

* Excludes one-time deal costs

and non-cash convert interest

Adjusted EBITDA is a non-GAAP number. The Company considers Adjusted EBITDA to

be a meaningful indicator of operating performance and uses it as a measure

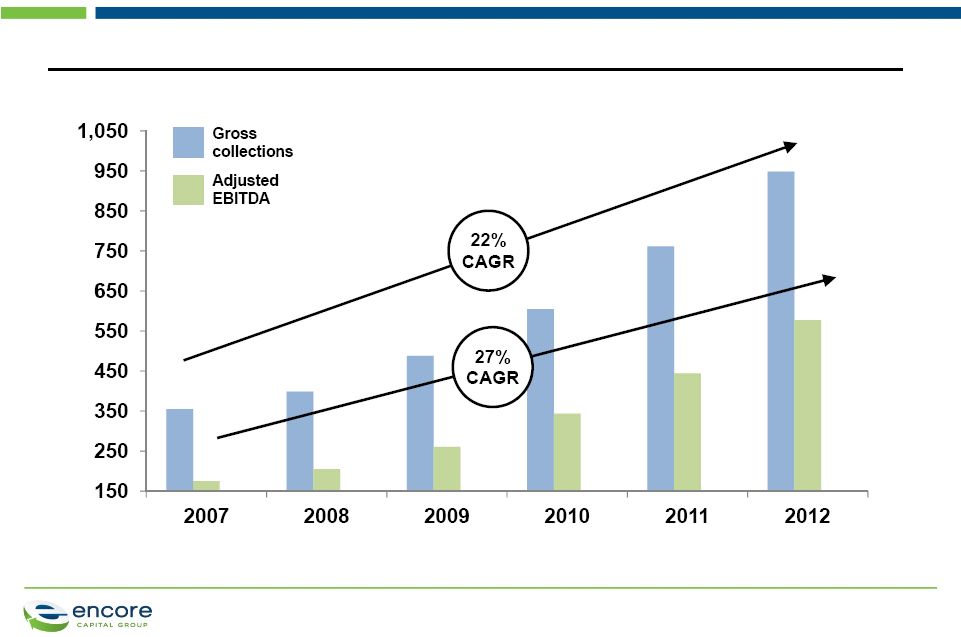

to assess the operating performance of the Company. See Reconciliation of Adjusted EBITDA to GAAP Net Income at the end of this presentation. |

PROPRIETARY

6

WHICH CONTINUES THE TREND WE’VE BEEN EXPERIENCING FOR THE

LAST SEVERAL YEARS

($M)

*

Adjusted EBITDA is a non-GAAP number. The Company considers Adjusted EBITDA to

be a meaningful indicator of operating performance and uses it as a measure

to assess the operating performance of the Company. See Reconciliation of Adjusted EBITDA to GAAP Net Income at the end of this presentation.

Adjusted EBITDA* and gross collections by year

PROPRIETARY |

PROPRIETARY

WE CONTINUE TO DRIVE DOWN OUR COST-TO-COLLECT DESPITE MAKING

SIGNIFICANT INVESTMENTS IN COMPLIANCE AND INTERNAL LEGAL

7

Overall cost to collect |

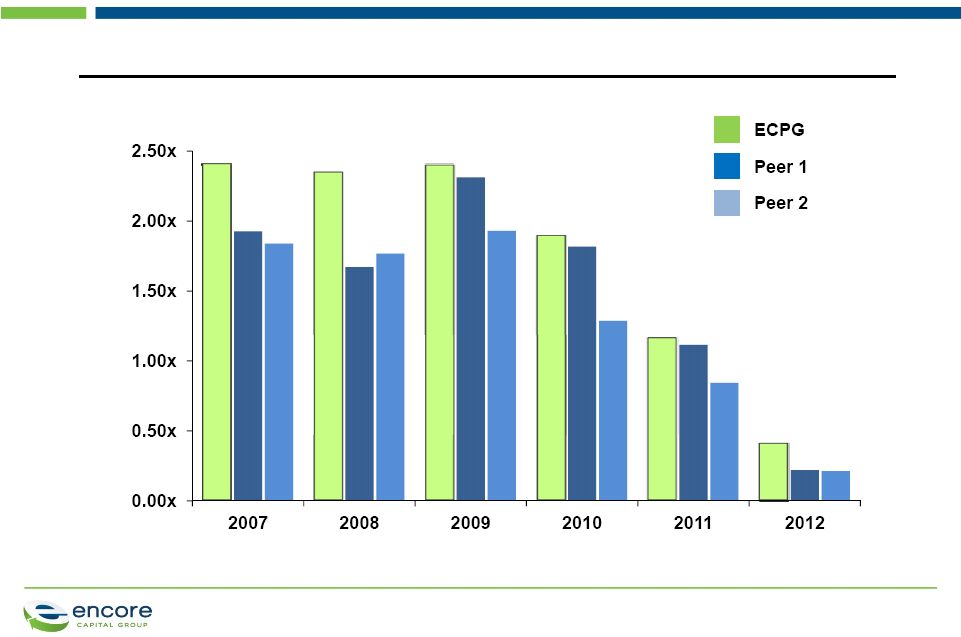

PROPRIETARY

OUR VALUATION AND OPERATING CAPABILITIES HAVE

ESTABLISHED ENCORE AS THE INDUSTRY LEADER

8

Cumulative actual collection multiples by vintage year, as of December 31, 2012

(Total collections / Purchase price)

Source: SEC filings –

For ECPG includes court costs recovered |

PROPRIETARY

ENCORE’S KEY

COMPETITIVE

ADVANTAGES

OUR SUCCESS IS DRIVEN BY OUR CORE COMPETENCIES

9

Portfolio

valuation

and

purchasing

Operational

modeling

International

operations

Account

Manager

expertise

Consumer

Credit

Research

Institute

Marketing

analytics

Legal

collections

COST

LEADERSHIP

PRINCIPLED

INTENT

ANALYTIC

STRENGTH

CONSUMER

INTELLIGENCE |

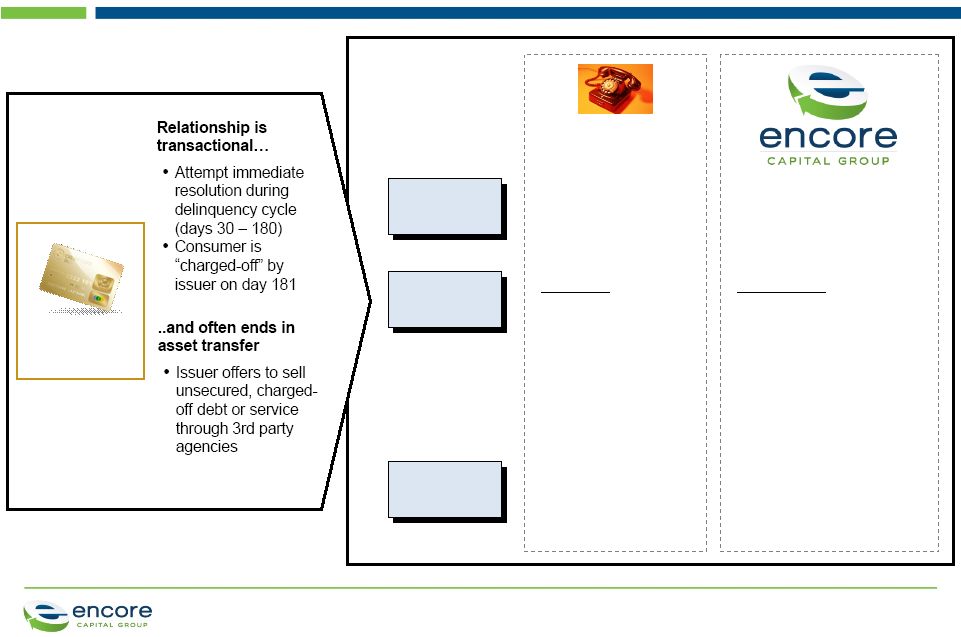

PROPRIETARY

ENCORE PROVIDES AN ESSENTIAL SERVICE AND ITS MODEL SHOULD

BECOME THE INDUSTRY STANDARD

10

Collection

time frame

Consumer

treatment

Outcome

Contingency

collection agency

•

Four-to-six month

collection cycle

Pressure

•

Artificial deadlines

•

Multiple collection

companies

•

Counterproductive

incentive structure

•

Consumer is

confused and

frustrated

•

Consumer has 84

months to recover

financially

Partnership

•

Create partnership

strategy and set goals

•

Tailor work strategies to

individual circumstances,

giving time for a

consumer to recover

•

Maximizes repayment

likelihood, creates

consistency, and

ensures fair treatment

Original

creditor |

PROPRIETARY

UNDERSTANDING FINANCIALLY STRESSED CONSUMER BEHAVIOR IS

AT THE HEART OF OUR COMPANY’S EVOLUTION

11 |

PROPRIETARY

Encore’s individual

underwriting approach

to portfolio valuation

accommodates our

specialized operational

strengths

Low willingness

Low ability

High willingness

High capability

High willingness

Moderate capability

High willingness

Low capability

Low willingness

High ability

Low willingness

Moderate ability

THIS IS CLEARLY SEEN IN OUR APPROACH TO ASSET VALUATION

12

The standard industry view

of a consumer debt portfolio

•

Strong partnership and

recovery opportunities

•

Payment plans and

opportunities to build

longer relationships

•

Enforce legal contract

through formal channels

•

Remind consumers

through legal messaging

•

Significant discounts and

many small payments

•

Hardship strategies

and warehousing |

PROPRIETARY

WE’VE SEEN A SIGNIFICANT INCREASE IN THE NUMBER OF

CONSUMERS WITH MULTIPLE OBLIGATIONS

13

Multiple obligations held within new portfolios, by purchase vintage

(% of unique consumers) |

PROPRIETARY

WE'RE BUILDING A PLATFORM THAT ENCOURAGES A DIFFERENT

KIND OF RELATIONSHIP WITH OUR CONSUMERS

14

Addressing

debt cycles

•

Acknowledging the limitations of our consumers’

household balance sheets

•

Living the Consumer Bill of Rights

Making focused

investments

•

Creating specialized work groups

•

Leveraging our industry-leading cost efficiency

•

Increasing direct control over consumer experience

Improving

consumer

experience

•

Using market-based surveys and tests to

understand consumer satisfaction

•

Partnering to develop new products and services

•

Pointing consumers to the best external references |

PROPRIETARY

AS WE LOOK TO THE FUTURE, WE ARE EXPLORING WAYS TO

LEVERAGE OUR CORE COMPETENCIES

15 |

PROPRIETARY

LAST YEAR, WE BEGAN TO DIVERSIFY THROUGH THE ACQUISITION

OF PROPEL

16

Leading provider of

debt management

and recovery

solutions for

consumers and

property owners

across a broad range

of asset classes

Property

Owners

Structured payment plans to

help residential and commercial

property owners settle tax

obligations and avoid

foreclosure

Consumer

Debt Holders

Robust collection plans to

maximize ability of consumers

to repay obligations and

ensure that consumers are

treated fairly

Financial

Institutions

Payment for

consumer debt

obligations

Local Tax

Authorities

Payment for residential

and commercial

property tax obligations |

PROPRIETARY

OUR PLAN WAS EXPAND IN OUR CORE MARKET AND INTO OTHER

STATES

17

Working to penetrate

the 80% of the Texas

market that has yet

to use a tax lien

transfer

Existing

market

Lobbying to introduce

legislation in other

states that will create

new markets

New

markets

Exploring alternative

tax lien models that

will allow us to

expand into new

markets

New

opportunities |

PROPRIETARY

WHICH HAS ALLOWED US TO GROW OUR PORTFOLIO WHILE

MAINTAINING AN EXCEPTIONALLY LOW RISK PROFILE

18

Propel portfolio size

($M)

•

$8,750 average balance

•

9-year term

•

6-year weighted average remaining term

•

13-15% typical interest rate

Portfolio characteristics

•

$230,000 average property value

•

3.84% average LTV at origination

•

0.4% foreclosure rate

•

Zero losses |

PROPRIETARY

Allows us to be

highly selective

in purchasing

opportunities for

the remainder

of the year

WE RECENTLY ANNOUNCED THE PENDING ACQUISITION OF ASSET

ACCEPTANCE CAPITAL CORP. (NASDAQ: AACC)

Largely satisfies

our 2013

purchasing

goals

Extends

Encore’s

Consumer Bill

of Rights and

best practices

to millions more

consumers

Able to leverage

best practices

across the two

platforms

19 |

PROPRIETARY

ONE OF THE BENEFITS OF THE TRANSACTION IS THAT WE HAD

FULL VISIBILITY TO HISTORICAL COLLECTIONS

20

Aggregated Portfolio: Actual and projected gross collections by month

($,Ms) |

PROPRIETARY

Acquisition

of

competitor’s

assets

Significant history

of acquiring assets

in the resale market

gave us an analytic

advantage when

conducting

operational due

diligence

Practice makes

perfect

Industry-leading

models used to

estimate individual

consumer willingness

and ability to pay

•

Enabled us to

identify and

acquire the most

valuable pools

Careful consumer

segmentation

ENCORE IS WELL POSITIONED TO PROVIDE A SOLUTION FOR

COMPETITORS WHO EXIT THE MARKET

21

Our operational

advantages generally

insulate us against

overpaying

•

Powerful operational

models and practices

•

Superior forecasting

methodology

Protection from the

“winner’s curse” |

PROPRIETARY

OUR CONFIDENCE IS TIED TO THE SUCCESSFUL COMPLETION OF

ONE OF THE INDUSTRY’S FEW DEALS OF THIS SIZE

22

$90M portfolio purchase in 2005, cumulative collections through 3/31/13

($M)

Initial

expectations:

$199M

Results to date:

$237M

Actual

collections

Estimated

collections |

PROPRIETARY

AND THE CONTINUED STRONG PERFORMANCE ON THE LARGE

PURCHASE COMPLETED LAST MAY

23

$100M+ portfolio purchase in 2012, cumulative collections through 3/31/13

($M)

Initial

expectations:

$59M

Results to date:

$77M

Actual

collections

Estimated

collections |

PROPRIETARY

WE ARE ALSO WELL WITHIN THE FINANCIAL COVENANTS OF OUR

CREDIT FACILITY

($M)

Covenant analysis

Cash flow leverage ratio

Debt

Trailing 4-quarter Adjusted EBITDA

†

Debt/Adjusted EBITDA (maximum 2.0x)

Minimum net worth

Excess room

Interest coverage ratio

EBIT/interest expense (minimum 2.0x)

Q1 2013

Pro forma

with AACC

811.9

1.03

153.0

24

†

See endnote

785.2

3.9

2012

706.0

577.4

1.22

133.0

5.7

Q1 2013

TTM

646.0

1.08

144.4

600.2

5.8 |

PROPRIETARY

ENCORE’S LONG-TERM PROSPECTS CONTINUE TO BE STRONG AND

ARE GAINING STRENGTH

•

Operating results continue to be strong and are exceeding

our internal projections

•

Tax lien expansion is part of a longer term diversification

strategy

•

Working collaboratively with legislators and policymakers to

shape the future of the collection industry, likely to be marked

by a significant reduction in competitors

•

Significant purchases in 2012 plus the closing of Asset

Acceptance in June are providing momentum

25 |

PROPRIETARY

ENDNOTE

26 |

PROPRIETARY

27

APPENDIX |

PROPRIETARY

RECONCILIATION OF ADJUSTED EBITDA

Reconciliation of Adjusted EBITDA to GAAP Net Income

(Unaudited, In Thousands)

Three Months Ended

Note:

The

periods

3/31/08

through

12/31/08

have

been

adjusted

to

reflect

the

retrospective

application

of

ASC

470-20.

All

periods

have

been

adjusted

to

show

discontinued

ACG

operations.

PROPRIETARY

28

3/31/08

6/30/08

9/30/08

12/31/08

3/31/09

6/30/09

9/30/09

12/31/09

3/31/10

6/30/10

9/30/10

12/31/10

GAAP net income, as reported

6,751

6,162

3,028

(2,095)

8,997

6,641

9,004

8,405

10,861

11,730

12,290

14,171

(Gain) loss from discontinued operations, net of tax

(422)

(89)

46

(483)

(457)

(365)

(410)

(901)

(687)

(684)

(315)

28

Interest expense

5,200

4,831

5,140

5,401

4,273

3,958

3,970

3,959

4,538

4,880

4,928

5,003

Contingent interest expense

-

-

-

-

-

-

-

-

-

-

-

-

Pay-off of future contingent interest

-

-

-

-

-

-

-

-

-

-

-

-

Provision for income taxes

4,227

4,161

2,429

(1,781)

5,670

3,936

5,676

4,078

6,080

6,356

6,474

9,057

Depreciation and amortization

438

482

396

391

410

402

443

516

522

591

650

789

Amount applied to principal on receivable portfolios

40,212

35,785

35,140

46,364

42,851

48,303

49,188

47,384

58,265

64,901

63,507

53,427

Stock-based compensation expense

1,094

1,228

860

382

1,080

994

1,261

1,049

1,761

1,446

1,549

1,254

Adjusted EBITDA

57,500

52,560

47,039

48,179

62,824

63,869

69,132

64,490

81,340

89,220

89,083

83,729

3/31/11

6/30/11

9/30/11

12/31/11

3/31/12

6/30/12

9/30/12

12/31/12

3/31/13

GAAP net income, as reported

13,679

14,775

15,310

17,134

11,406

16,596

21,308

20,167

19,448

(Gain) loss from discontinued operations, net of tax

(397)

(9)

(60)

101

6,702

2,392

-

-

-

Interest expense

5,593

5,369

5,175

4,979

5,515

6,497

7,012

6,540

6,854

Provision for income taxes

8,349

9,475

9,834

10,418

11,660

12,846

13,887

13,361

12,571

Depreciation and amortization

904

958

1,054

1,165

1,240

1,420

1,533

1,647

1,846

Amount applied to principal on receivable portfolios

85,709

83,939

73,187

69,462

104,603

101,813

105,283

90,895

129,487

Stock-based compensation expense

1,765

1,810

2,405

1,729

2,266

2,539

1,905

2,084

3,001

Acquisition related expense

-

-

-

-

489

3,774

-

-

1,276

Adjusted EBITDA

115,602

116,317

106,905

104,988

143,881

147,877

150,928

134,694

174,483

|

ENCORE CAPITAL GROUP, INC.

May 2013

JMP Securities 12th Annual Research Conference |