Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Arlington Asset Investment Corp. | v344773_8k.htm |

Investor Presentation May 13, 2013

1 Information Related to Forward - Looking Statements This presentation contains “forward - looking statements” within the meaning of the Private Securities Litigation Reform Act of 19 95. These include statements regarding future results or expectations. Forward - looking statements can be identified by forward - look ing language, including words such as “believes,” “anticipates,” “views”, “expects,” “estimates,” “intends,” “may,” “plans,” “pro jec ts,” “potential,” “prospective,” “will” and similar expressions, or the negative of these words. Such forward - looking statements are based on facts and conditions as they exist at the time such statements are made. Forward - looking statements are also based on predictio ns as to future facts and conditions, the accurate prediction of which may be difficult and involve the assessment of events beyond ou r c ontrol. Forward - looking statements are further based on various operating and return assumptions. Caution must be exercised in relying o n forward - looking statements. Due to known and unknown risks, actual results may differ materially from expectations or projectio ns. You should carefully consider these risks when you make a decision concerning an investment in our common stock and senior notes, along with the following factors, among others, that may cause our actual results to differ materially from those described i n a ny forward - looking statements: availability of, and our ability to deploy, capital; our ability to grow our business through a strategy foc used on acquiring primarily private - label MBS and agency - backed MBS; yields on MBS; our ability to successfully implement our hedging strategy ; our ability to realize reflation on our assets; our ability to effectively migrate private - label MBS to agency - backed MBS; the credit performance of our private - label MBS; our ability to potentially realize a higher return on capital reallocated to agency - backed MBS; current conditions and further adverse developments in the residential mortgage market and the overall economy; job growth; home price stabilization; potential risk attributable to our mortgage - related portfolios; impacts of regulatory changes, including actions taken by the SEC, the U.S. Federal Reserve and the U.S. Treasury and changes affecting Fannie Mae and Freddie Mac; failure of sovereign or municipal entities to meet their debt obligations or a downgrade in the credit rating of such obligations; overall interest rate environment and changes in interest rates, interest rate spreads, the yield curve and prepayment rates; changes in anticipated earnings a nd returns; the amount and growth in our cash earnings and distributable income; growth in our book value per share; our ability to maintain adequate liquidity; our use of leverage and dependence on repurchase agreements and other short - term borrowings to finance our mortgage - r elated holdings; the loss of our exclusion from the definition of “investment company” under the Investment Company Act of 1940; our ab ility to forecast our tax attributes and protect and use our net operating loss carry - forwards and net capital loss carry - forwards to offset future taxable income and gains; changes in our strategies, asset allocation and operational policies; our ability and willingness t o m ake future dividends; competition for investment opportunities and qualified personnel; our ability to retain key personnel; effects of litigation and contractual claims; changes in, and our ability to remain in compliance with, law, regulations or governmental policies affecting our business; risk from strategic ventures or entry into new business areas; failure to maintain effective internal controls; and th e factors described in the sections entitled “Risk Factors” in our annual report on Form 10 - K for the year ended December 31, 2012 and our other public filings with the SEC. You should not place undue reliance on these forward - looking statements, which apply only as of th e date of this presentation. We undertake no obligation to update or revise any forward - looking statement, whether written or oral, relat ing to matters discussed in this presentation, except as may be required by applicable securities laws.

2 Consistent and attractive profitability - 1 Q 2013 Core Operating EPS of $ 1.04 (1) ; ROE on investable book value of 18% (1) - GAAP book value per share of $32.78 at March 31 , 2013 Tax - advantaged dividends – $3.50 per share annualized 1Q 2013 dividend rate (2)( 3 ) - 13% annualized dividend yield (17% adjusted annualized yield assuming a 23.8% individual Federal income tax rate on C - Corp dividends) (4) - $515 million of potential tax benefits; Arlington pays 2% cash tax rate Corporate structure permits complementary “Hybrid” portfolio and flexibility in allocation of capital - Agency MBS portfolio (5) – Prepayment protected, 30 - year fixed rate portfolio, mid - teens ROE $1.6 billion market value, $192 million capital (6) , low historical CPR, high hedge ratio - Private - label MBS portfolio (5) – Prime j umbo and Alt - A loans, no subprime or option ARMs $276 million market value, $237 million capital (6) , 8.5% cash yield at market value (7) Improving housing market enhances appreciation and elevates expected returns Potential growth in investable book value, cash earnings and distributable income - Potential EPS upside as private - label MBS gains are realized and reinvested - Cost efficiency opportunities and accretive capital offer enhanced returns (1) See Exhibit A for a reconciliation of Core Operating EPS to GAAP net income. (2) Based on closing class A common stock price of $28.01 on 5/10/13. (3) The annual dividend rate presented is calculated by annualizing the 1st quarter of 2013 dividend payment of $0.875. The Com pany maintains a variable dividend policy and the Board of Directors, in its sole discretion, approves the payment of dividends. Actual dividends in the future may differ materially f rom historical practice and from the annualized dividend rate presented. (4) The Company's dividends are eligible for the 23.8% federal income rate on qualified dividend income, whereas divi dends paid by a REIT are generally subject to tax at ordinary income rates (currently at a maximum federal rate of 43.4%). To provide the same after - tax return to a shareholder eli gible for the 23.8% rate on qualified dividend income and otherwise subject to the maximum rate on ordinary income, a REIT would be required to pay dividends providing a 17% yield. (5) As of 3/31/13. (6) Agency MBS allocated capital is composed of MBS and its related interest receivable, repo, its related interest and deriv ati ve instruments, and its related deposits and cash. Private - label MBS allocated capital is composed of MBS and repo and its related interest. (See “MBS Portfolio Composition – Capital Allocation ” slide) (7) Excluding non - cash accretion, based on ending market value. Consistent Tax Advantaged Returns Plus Potential Growth AI: Focus on residential mortgage - backed securities, $2.2 billion in assets, internally managed C - Corp structure, NYSE listed

3 Flexibility to allocate capital to best risk / return opportunities - No REIT asset or income test restrictions - No hedging constraints - Retention of capital from earnings above the dividend Internally managed with significant insider ownership - No incremental management fees associated with growth - Recurring expenses to investable capital down 50% Capital structure flexibility improves returns - 6.625% 10 - year unsecured notes enhance operating efficiency and reduce cost of capital - $25 million offering and $75 million at - the - market program $ 230 million of net operating loss carry - forwards - Applicable toward any form of taxable income; expiring 2027 – 2028; no annual limitation - AI pays 2% alternative minimum cash tax rate $285 million of capital loss carry - forwards expiring 2013 – 2014; applicable toward realized gains $ 159 million of deferred tax assets at March 31, 2013 equals $9.57 per share C - Corp Structure Provides Flexibility; Tax Benefits Enhance Returns

4 Complementary “Hybrid” MBS Portfolio Generates Consistent EPS Low and steady CPRs on agency MBS contribute to consistency High and stable CPRs on private - label MBS increase cash yields and spread income Improved cost efficiency and accretive capital enhance cash earnings Potential EPS upside as private - label MBS gains are realized and reinvested

5 MBS Portfolio Composition – Capital Allocation (1) (1) As of 3/31/13. (2) Agency MBS allocated capital is composed of MBS and its related interest receivable, repo, its related interest and derivative instruments, and its related deposits and cash. Private - label MBS allocated capital is composed of MBS and repo and its related interest. Agency MBS Private-label MBS MBS, at amortized cost $1,618 $229 MBS, at fair value $1,637 $276 Allocated capital (2) $192 $237 Capital Allocation ($ in millions)

6 Illustrative MBS Portfolio Returns (1) $ in millions. (2) Represents market value minus repo financing plus hedges , deposits and related net working capital. (3) Disclaimer: The numbers contained in the examples above are for illustrative purposes only and do not reflect Arlington Asset’s projections or forecasts. Any assumptions and estimates used may not be accurate and cannot be relied upon. Arlington Asset ’s ROE for any given period may differ materially from these examples. The foregoing is not an example of, and does not represe nt, expected returns from an investment in Arlington Asset’s common stock. (4) Based on 3/31/13 contract balances and estimated 2013 forward curve funding costs. (5) Excluding non - cash accretion, based on ending market value during the 1 st quarter of 2013. Market Value $1,637 Face Value $446 Repo Financing $1,168 Market Value $276 Capital Allocation (2) $192 Capital Allocation $237 Expected Yield (w/ 7 CPR) 2.9% Cash Yield (5) 7.2% Cash Repo Cost 0.4% Cash Repo Cost 2.1% 5 Yr. Hedge Cost (4) 0.6% Net Spread 1.9% Net Spread (5) 5.1% Target Leverage 7.5 x Target Leverage 0.25 x ROE 17.3% ROE (excluding appreciation) 8.5% Agency Portfolio Economics (3) Agency Portfolio Highlights (1) At 3 /31/13 Private - label Portfolio Highlights (1) At 3/31/13 Private - label Portfolio Economics (3)

7 MBS Portfolio Profile Attractive agency MBS portfolio spreads in current environment Expected yield of approximately 2.95% based on expected CPR of 7%, 109.10 fair value and 107.5 cost 100% selected for prepayment protections: 66% HARP, remainder primarily low balance loans 3 - month portfolio CPR of 8.64 %; May 2013 CPR of 7% - FN 4.0% universe has a 3 - month CPR of 30.0% with a 106.56 market price (1) - FN 4.50% universe has a 3 - month CPR of 33.7% with a 107.69 market price (1) Eurodollar futures provide hedge against increasing interest rates as economic and policy environments normalize - Quarterly contracts starting at mid - September 2013; $918 million average balance through September 2017 - Hedge period extends out four years – market rate of approximately 0.96% ( 1)(2) 10 - year Swap futures - $175 million notional (1 )(2) ( 1 ) Source : Bloomberg (2) As of 03/31/13. Private - Label MBS Portfolio Focus on Prime & Alt - A securities at deep discounts - No subprime, no option arms - Improving home prices and delinquencies, attractive yield, positive technicals - Attractive re - remic mezzanine structure Agency MBS Portfolio Private - Label MBS Portfolio Statistics Face Value $446M Weighted Average Cost/Mark 50% / 62% Purchase Discount $217M Average Loan Size $543,044 Coupon 4.17% Orig FICO 728 Orig LTV 70% WALA 81 Credit Enhancement 1.2% 60+ Delinquency 18% 3 month Severity 48 % 3 month CPR 18% as of 3/31/13

8 Private - label MBS Portfolio : Key Characteristics Jumbo Prime and Alt - A Loans - Higher home values and larger loan sizes - More prime borrowers with greater financial flexibility - Stronger demographics, higher incomes - More desirable / stable housing markets Top 5 Largest MSA’s (1) : - Los Angeles - Long Beach - Santa Ana, CA (17.5%) - San Francisco - Oakland - Fremont, CA (10.3%) - New York - Northern New Jersey - Long Island, NY - NJ - PA (7.8%) - Washington - Arlington - Alexandria, DC - VA - MD - WV (7.1%) - San Diego - Carlsbad - San Marcos, CA (5.1%) Los Angeles MSA (1) (1) Source: Bloomberg

9 U.S. Home Prices (1 ) Month - over - month, home prices increased nationally at a 19.5% seasonally adjusted annualized rate in March, the fastest growth since March 2005; excluding distressed sales, HPA was 28.0% CoreLogic reported that home prices increased 10.5% nationwide in March 2013 compared to March 2012, the biggest annual gain since March 2006…the recovery is accelerating and widespread Home prices increased in all of the 20 MSAs tracked by CoreLogic on a seasonally adjusted basis Housing supply remains limited and mortgage investor demand remains strong ( 1 ) Source : CoreLogic (2) Source: The Standard & Poor's Case – Shiller Home Price Indices -25% -20% -15% -10% -5% 0% 5% 10% 15% 20% Case - Shiller Composite 20 City Index (2) Year-over-Year % 11 of Arlington’s top 15 MSA concentrations experienced greater year - over - year home price appreciation than the national average

10 Asset selection and performance provides consistent spread income and opportunity for growth - 1Q 2013 Core Operating EPS of $ 1.04 (1) ; ROE on investable book value of 18 % (1) Tax - advantaged dividends – $3.50 per share annualized 1Q 2013 dividend rate (2)( 3 ) - 13% annualized dividend yield - 17% adjusted annualized yield assuming a 23.8% individual Federal income tax rate on C - Corp dividends (4) Potential growth in cash earnings and distributable income - Investment of offering proceeds - Accretion from proceeds of at - the - market program for 6.625% 10 - year notes - Upside from reinvestment of gains on appreciated private - label MBS Potential upside to investable book value - Private - label MBS appreciation At $0.75 price = $ 3.50 per AI share At $0.85 price = $ 6.17 per AI share - Tax Assets AMT prepaid taxes = $0.32 per AI share Net FIN 48 reserve = $0.43 per AI share ( 1 ) See Exhibit A for a reconciliation of Core Operating EPS to GAAP net income . ( 2 ) Based on closing class A common stock price of $ 28 . 01 on 5 / 10 / 13 . ( 3 ) The annual dividend rate presented is calculated by annualizing the 1 st quarter of 2013 dividend payment of $0.875. The Company maintains a variable dividend policy and the Board of Directors, in its sole discretion, approves the payment of dividends. Actual dividends in t he future may differ materially from historical practice and from the annualized dividend rate presented. ( 4) The Company's dividends are eligible for the 23.8% federal income rate on qualified dividend income, whereas dividends paid b y a REIT are generally subject to tax at ordinary income rates (currently at a maximum federal rate of 43.4%). To provide the same after - tax return to a shareholder eligible for the 23.8% rate on qualified dividend income and otherwise subject to the maximum rate on ordinary income, a REIT would be requir ed to pay dividends providing a 17% yield. Attractive Tax Advantaged Returns Plus Potential Growth AI: Focus on residential mortgage - backed securities, $2.2 billion in assets, internally managed C - Corp structure, NYSE listed

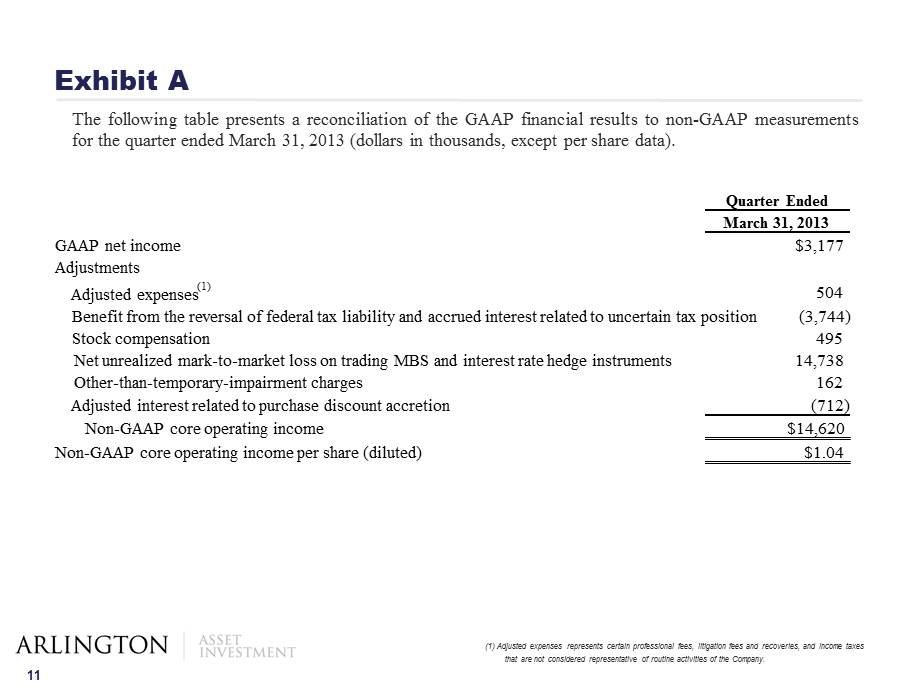

11 Exhibit A The following table presents a reconciliation of the GAAP financial results to non - GAAP measurements for the quarter ended March 31 , 2013 (dollars in thousands, except per share data) . ( 1) Adjusted expenses represents certain professional fees, litigation fees and recoveries, and income taxes that are not considered representative of routine activities of the Company. Quarter Ended March 31, 2013 GAAP net income $3,177 Adjustments Adjusted expenses (1) 504 Benefit from the reversal of federal tax liability and accrued interest related to uncertain tax position (3,744) Stock compensation 495 Net unrealized mark - to - market loss on trading MBS and interest rate hedge instruments 14,738 Other - than - temporary - impairment charges 162 Adjusted interest related to purchase discount accretion (712) Non - GAAP core operating income $14,620 Non - GAAP core operating income per share (diluted) $1.04