Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - HERITAGE FINANCIAL CORP /WA/ | d534195d8k.htm |

Q2

2013

Investor

Presentation

Brian L. Vance

CEO & President

Exhibit 99.1

Heritage

Financial

Corporation |

Forward

Looking Statement 2

This presentation contains forward-looking statements that are subject to

risks and uncertainties, including, but not limited to: The credit and

concentration risks of lending activities; Changes in general economic

conditions, either nationally or in our market areas; Competitive market

pricing factors and interest rate risks; Market interest rate

volatility; Balance sheet (for example, loans) concentrations;

Fluctuations in demand for loans and other financial services in our market

areas; Changes in legislative or regulatory requirements or the results

of regulatory examinations; The ability to recruit and retain key

management and staff; Risks associated with our ability to implement our

expansion strategy and merger integration; Stability of funding sources

and continued availability of borrowings; Adverse changes in the

securities markets; The inability of key third-party providers to

perform their obligations to us; Changes in accounting policies and

practices and the use of estimates in determining fair value of certain of our

assets, which estimates may prove to be incorrect and result in significant

declines in valuation; and These and other risks as may be detailed from

time to time in our filings with the Securities and Exchange

Commission.

The Company cautions readers not to place undue reliance on any

forward-looking statements. Moreover, you should treat these

statements as speaking only as of the date they are made and based only on information then actually known to the

Company. The Company does not undertake and specifically disclaims any

obligation to revise any forward-looking statements to

reflect

the

occurrence

of

anticipated

or

unanticipated

events

or

circumstances

after

the

date

of

such

statements.

These

risks could cause our actual results for 2013 and beyond to differ materially

from those expressed in any forward-looking statements by, or on

behalf of, us, and could negatively affect the Company’s operating and stock price performance. |

Overview

•

Company Information

•

Financial Performance

•

Strategic Initiatives

3 |

Company

Information 4 |

Our

Market Area |

2013

Announcements 6

•

January 9, 2013 –

Completed Merger with Northwest Commercial Bank

•

Results in an Auburn location, consolidation of Lakewood branches and $65

million in total assets. Completed systems conversion March 9,

2013. •

March 11, 2013 –

Announced Definitive Agreement to Acquire Valley Community

Bancshares, Inc.

•

9 branches in Pierce & King Counties and $234 million in total

assets •

Transaction is anticipated to close in Q3 2013 with conversion in October

2013

•

April 8, 2013 –

Heritage to Consolidate Bank Subsidiary

•

Central Valley Bank has been a wholly-owned subsidiary of Heritage

Financial Corporation for 14 years

•

Central Valley Bank will merge into Heritage Bank to gain efficiencies and as

a result of the President’s planned retirement in 2014

•

Merger anticipated to be completed in Q2 2013 with conversion in

October

2013 |

Valley

Bank Transaction Overview Transaction Value:

Approximately $44.2 million (including cash out of stock options)

Offer Price Per Share:

$39.00

Consideration Mix:

50% of Valley shares exchanged for $19.50 cash

50% of Valley shares exchanged for 1.3611 HFWA shares

Stock Option Treatment:

In-the-money stock options cashed out (approximately $232

thousand) Board Representation:

One Valley Board member will join the Board of HFWA

Exchange Ratio:

Fixed exchange ratio

Collars:

A 20% collar above and below HFWA’s stock price of $14.33

Walk-away Provision:

If HFWA’s stock price drops below $11.46 HFWA has the option to fill with

cash or stock or walk-away

Termination Fee:

$1.76 million

Required Approvals:

Customary regulatory approvals and Valley shareholder approval

Expected Closing:

Q3 2013

7

Source: Company documents and SNL Financial. |

Valley

Bank Transaction Overview Purchase Accounting Adjustments

(pre-tax): •

Estimated credit mark of 2.0% or ~$279 thousand

•

Estimated $1.5 million mark-up on real estate and other assets

•

Estimated core deposit intangible equaling 1.0% of Valley’s core deposits

(1)

Other Financial Impacts:

•

Estimated cost savings of between 45% and 50%

–

Phased-in 50% in 2013 and 100% in 2014

–

Assumes consolidation of four branches

•

Estimated after-tax deal related expenses of $2.0 million

8

(1)

Core deposits represent total deposits less total certificates

of deposit. |

Valley

Bank Transaction Overview 9

•

Valley Bank has a history of strong and stable profitability with an average

ROAA of 0.97% over the past 5 years

•

Strong

asset

quality

has

been

maintained

throughout

the

economic

recession

•

Attractive low-cost funding mix (total cost of funds was 0.17% as of

12/31/2012) Overview:

Headquarters:

Year Established (BHC / Bank):

Number of Branches:

FTE:

Assets / FTE ($000s):

Puyallup, WA

1998 / 1972

9*

67

$3,615

Balance Sheet & Capital

Assets ($000s):

Deposits ($000s):

Gross Loans:

Loans / Deposits:

Securities / Assets:

TCE / TA:

Tier 1 Leverage Ratio:

$242,220

$212,501

$125,085

58.9%

25.9%

11.7%

11.2%

Profitability

ROAA:

ROAE:

Net Interest Margin:

Cost of Interest-Bearing Deposits:

Efficiency Ratio:

0.78%

6.57%

3.68%

0.25%

69.82%

Asset Quality

NPAs / Assets:

NPAs / (Loans + OREO):

Reserves / Loans:

Reserves / NPAs:

NCOs / Avg. Loans:

1.00%

1.93%

1.78%

91.94%

0.04%

Note: Consolidated Valley Community Bancshares, Inc. financials not publicly

available. *1 location is a drive-up facility only

FTE = Full-time employees

Source: SNL Financial & Valley Bank call report data as of and for the year

ended 12/31/2012. |

Valley

Bank Transaction Overview 10

•

Valley has maintained strong asset quality throughout the economic downturn,

despite being located in a region that was not immune to the

recession Valley Net Charge-Off History

Cumulative net charge-offs since

2008 total $1.1 million |

Valley

Bank Transaction Overview 11

Earnings Accretion & Return

(1)

:

2014 EPS Accretion:

2015 EPS Accretion:

IRR:

Tangible Book Value Earnback Period:

> 19%

> 24%

> 16%

<4.5 years, using incremental earnings

(2)

<1.5 years, on static basis

(3)

Capital Ratios (as of 03/31/13):

TCE / TA:

Leverage Ratio:

Tier 1 Ratio:

Total Risk-Based Capital Ratio:

13.0%

13.3%

17.8%

19.1%

12.2%

11.6%

20.1%

21.4%

11.7%

11.7%

16.4%

17.7%

Pro Forma

(1)

Based on internal earnings estimates

(2)

Incremental tangible book value earnback represents the number of years

to eliminate tangible book value dilution at closing utilizing just the incremental earnings

realized through the merger (it ignores HFWA stand alone earnings)

(3)

Static tangible book value earnback represents the number of years to eliminate

tangible book value dilution at closing utilizing combined pro forma earnings |

Benefits of the Central Valley Bank Merger

12

•

Leadership transition

•

Operational efficiencies

•

Improved financial performance

•

Regulatory risks reduced

•

Improved shareholder value through

improved efficiencies |

Financial Performance

13 |

Balance

Sheet 14 |

Total

Loan Portfolio 15

Financial data as of March 31, 2013 |

Loan

Trends Net Loan Balance

16

2009

2010

2011

2012

Q1 2013

CAGR

Originated

Loans

$746.1

$720.0

$815.6

$855.4

$869.2

3.89%

Purchased

Covered

Loans

-

$128.7

$105.4

$84.0

$81.4

n/a

Purchased

Non-Covered

Loans

-

$131.0

$83.5

$59.0

$104.9

n/a

Total

$746.1

$979.8

$1,004.5

$998.4

$1,055.5

9.06%

Dollars in millions |

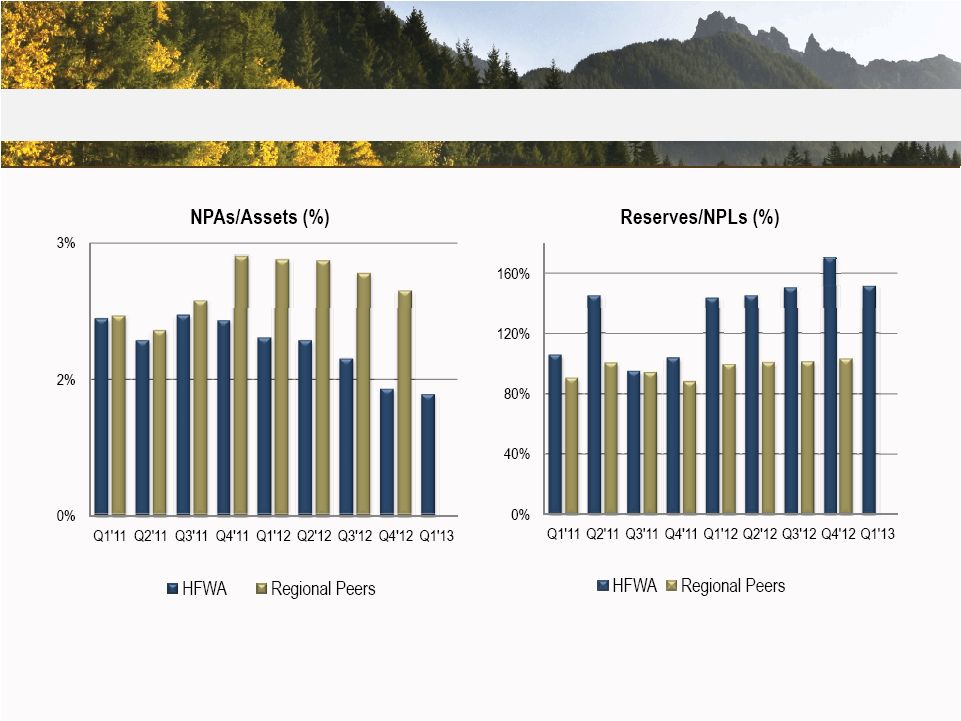

Credit

Quality 17

* HFWA ratios relate to originated loan portfolios only. Regional Peer data not

available for Q1’13 Regional

Peer

Group

(10):

Ticker

Symbols

–

BANR,

CACB,

COLB,

FFNW,

HOME,

NRIM,

PCBK,

RVSB,

TSBK,

WBCO

Source: SNL Financial |

Deposit

Base 18

Financial data as of and for the quarter ending March 31, 2013.

|

Deposit

Growth 19 |

Equity

20

*After the anticipated acquisition of Valley Bank Tangible Common

Equity/Tangible Assets is estimated to be 11.7% |

Earnings

21

*Includes after-tax gain of $7.7 million for FDIC-assisted bank

acquisitions. |

Diluted

Earnings Per Share 22

*Includes $0.69 earnings per share related to the after-tax gain on

FDIC-assisted acquisitions. |

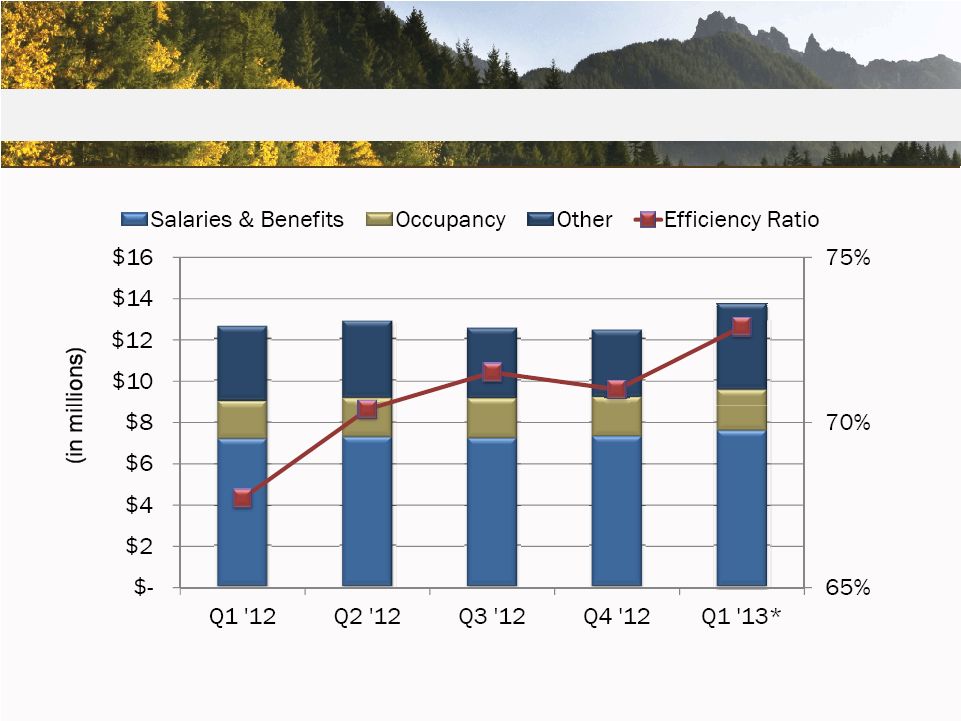

Operating Expenses

23

*Includes Northwest Commercial Bank acquisition expenses of $665,000

and the proposed Valley Bank acquisition expenses of $148,000

|

24

Strategic Initiatives

24 |

2013

Strategic Initiatives •

Acquisitions

•

Enhance Pacific Northwest footprint

•

Balance Sheet Growth

•

2013 projected originated loan growth of 3-5%

•

Maintain loan to deposit ratio 85-90%

•

Efficiency Improvements

•

A disciplined approach to managing expenses

•

Merge Central Valley Bank into Heritage Bank

•

Core System Conversion

25 |

2013

Strategic Initiatives •

Branching

•

De Novo branch -

East Vancouver, WA

•

Re-locating branches –

Tumwater and Kent, WA

•

Valley Bank branch consolidation

•

Wealth Management

•

Continue growth focus on Trust, Brokerage, Advisory

Management Services

•

Grow Assets under Management

26 |

Strategic Efficiency Initiatives

•

Emphasis on improving:

•

Assets per employee (ApE)

•

Deposits per branch (DpB)

•

Loan commitments per lender

•

Efficiency Ratio

27 |

Strategic Capital Management

•

Cash Dividends

•

Continued focus on

•

Regular dividends in the 35% to 40% payout range

•

Special dividend as appropriate but dependent on acquisition

activities

•

Stock buybacks on an opportunistic basis

28

2011

2012

2013

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Quarterly

Dividend

$0.03

$0.05

$0.05

$0.06

$0.08

$0.08

$0.08

$0.08

$0.08

Special

Dividend

-

-

$0.25

-

$0.20

-

$0.30

-

- |

Capital

Return 29

Total

Capital

Returned*

Since

Q1

2011

(%

of

Tg.

Common

Equity

in

Q1

2011)

Source: SNL Financial, as of 12/31/2012 unless noted otherwise

*Total capital returned includes all cash dividends and stock buybacks since Q1

2011 HFWA has returned

more capital to

shareholders than

most peers since Q1

2011 based on

beginning balance of

tangible common

equity

14.0%

5.1%

8.2%

12.7%

7.3%

9.7%

8.1%

9.4%

6.9%

9.9%

6.6%

12.1%

8.2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

HFWA

BMRC

COLB

CVBF

FIBK

GBCI

PCBK

PACW

TCBK

UMPQ

WBCO

WAFD

Median |

Capital

Return 30

Source: SNL Financial, as of 12/31/2012 unless noted otherwise

*Total capital returned includes all cash dividends and stock buybacks since Q1

2011 HFWA has

returned more

capital to

shareholders

than

accumulated net

income since Q1

2011

Total Capital Returned* / Net Income (Since Q1 2011)

138.7%

22.1%

54.7%

52.6%

39.0%

80.0%

74.4%

40.9%

37.0%

59.2%

34.9%

81.8%

52.6%

0%

20%

40%

60%

80%

100%

120%

140%

160%

HFWA

BMRC

COLB

CVBF

FIBK

GBCI

PCBK

PACW

TCBK

UMPQ

WBCOWAFD

Median |

Capital

Return 31

Source: SNL Financial, as of 12/31/2012

*Total capital returned includes all cash dividends and stock buybacks since Q1

2011 HFWA has returned capital through both dividends and stock

buybacks 68.3% through dividends and 31.7% through buybacks

vs. peer median 93.3% through dividends and 6.7% through buybacks

More advantageous for shareholders from a tax perspective for stock buybacks

vs. dividends None of the selected companies had a buyback program in

place without a dividend program as well Mix of Capital Returned* (Since Q1 2011)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

HFWA

BMRC

COLB

CVBF

FIBK

GBCI

PCBK

PACW

TCBK

UMPQ

WBCO

WAFD

Median

Buyback

Dividends |

32

Conclusion

32 |

Investment Value

•

Strong financial foundation performance

trends

•

Positioned to take advantage of the right

opportunities

•

Continued focus on building long-term

franchise value

•

Disciplined approach to acquisitions

33 |

Thank

You Questions? |