Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CU Bancorp | d500755d8k.htm |

Investor Presentation

Investor Presentation

Raymond James & Associates

Presentation to Financial Advisors

March 12, 2013

St. Petersburg, FL

Exhibit 99.1 |

Forward-Looking Statements

Forward-Looking Statements

2

This presentation contains certain forward-looking information

about CU Bancorp and California United Bank (collectively the

“Company”) that is intended to be covered by the safe harbor

for “forward-looking statements” provided by the Private Securities

Litigation Reform Act of 1995. All statements other than statements of

historical fact are forward-looking statements. Such statements

involve inherent risks and uncertainties, many of which are difficult

to predict and are generally beyond the control of the Company.

There are a number of important factors that could cause actual results

to differ materially from those expressed in, implied or

projected by, such forward-looking statements. Risks and

uncertainties include but are not limited to lower than expected revenues;

credit quality deterioration which could cause an increase in the

allowance for loan losses and a reduction in net earnings; increased

competitive pressure among depository institutions; a change in the

interest rate environment which reduces interest margins;

asset/liability repricing risks and liquidity risks; general economic

conditions, either nationally or in the market areas in which the

Company does or anticipates doing business are less favorable than

expected; environmental conditions, including natural disasters,

may disrupt our business, impede our operations, negatively impact the

values of collateral security for the Company’s loans or impair

the ability of our borrowers to support their debt obligations; the

economic and regulatory effects of the continuing war on terrorism

and other events of war; legislative or regulatory requirements or

changes adversely affecting the Company’s business; and changes in

the securities markets. If any of these risks or uncertainties

materializes or if any of the assumptions underlying such forward-looking

statements proves to be incorrect, the Company’s results could

differ materially from those expressed in, implied or projected by such

forward-looking statements. The Company assumes no obligation to

update such forward-looking statements. For a more complete

discussion of risks and uncertainties, read the Bank’s annual

report on Form 10-K, quarterly reports on Form 10-Q and other reports

filed by the Bank with the FDIC and by CU Bancorp with the SEC. The

documents filed with the FDIC and the SEC may be obtained at

California United Bank’s website at www.cunb.com. These documents may also be obtained free of charge from CU Bancorp by

directing a request to CU Bancorp, 15821 Ventura Boulevard, Suite 100,

Encino, California 91436, Attention: Investor Relations.

Telephone 818 257-7700. |

Corporate Overview

Corporate Overview

California United Bank is a premier community-based

California United Bank is a premier community-based

commercial bank servicing the Metropolitan Los Angeles,

commercial bank servicing the Metropolitan Los Angeles,

Orange County and Ventura County markets

Orange County and Ventura County markets

Established by local business owners and entrepreneurs in 2005

Eight full-service offices in Los Angeles, San Fernando Valley, Conejo

Valley,

Santa

Clarita

Valley,

Simi

Valley,

South

Bay,

and

Orange

County

(Anaheim and Irvine/Newport Beach)

Servicing businesses, non-profit organizations, entrepreneurs,

professionals, and high-net worth individuals

Total assets of $1.25 billion

California

United

Bank

grew

total

assets

at

a

43%

CAGR

and

total

deposits

at a 51% CAGR since inception in 2005 through December 31, 2012

3 |

Investment Highlights

Investment Highlights

Emerging business banking franchise reaching an inflection

point in profitability

Attractive low-cost core deposit base

Non-interest bearing deposits comprise 50% of total deposits at 12/31/12

Cost of deposits was 17 bps in Q4 2012

Demonstrated ability to grow both organically and through

acquisitions

Experienced management team with an established track

record of delivering results

Recent acquisition of Premier Commercial Bank (PCB)

provides near-term catalyst for earnings growth

Growing awareness in local markets and the investment

community

Surpassed $1 billion in total assets in July 2012

Transferred listing to Nasdaq Capital Market in October 2012

4 |

Strategic Geographic Locations

Strategic Geographic Locations

Encino (2005) –

Headquarters

Los Angeles (2006)

Santa Clarita Valley (2007)

South Bay (2009) –

Converted to a

branch in 2010

Orange County (2010) –

Loan

Production Office

Simi Valley (2010) –

Acquired from

California Oaks State Bank

Thousand Oaks (2010) –

Acquired from

California Oaks State Bank

Anaheim (2012) –

Acquired from

Premier Commercial Bank

Irvine/Newport Beach (2012) –

Acquired from Premier Commercial Bank

5

CUNB Branch

CUNB LPO

Former COSB

Branch

Former PCB

Branch

California

California

United Bank has a

United Bank has a

footprint that spans the most

footprint that spans the most

attractive markets in Southern

attractive markets in Southern

California:

California:

|

Why

We Are Different Why We Are Different

CUNB has been engaged in the successful practice of business

banking since its inception

Strong growth combined with stellar asset quality

We have the ability to do larger, more complex financings than

similar sized banks

Formula lines of credit

Asset-based lending

Executive team has extensive experience building high performing

banks

Demonstrated ability to identify, acquire and successfully integrate banks

Proven ability to attract top bankers

Multiple experienced banking teams added from competitors since 2010

Local advisory boards guide the Bank in its respective business

communities

6 |

Our

Customers Our Customers

Our customer base reflects the diversity

Our customer base reflects the diversity

of industries in Southern California

of industries in Southern California

Majority of customers participate in the manufacturing,

distribution and services industries

Typical customer has between $10 million and $60 million in

annual sales (excluding SBA borrowers)

Typical loan commitment ranges between $1 million and $5

million (excluding SBA loans)

Majority of new customers come from larger banks

Most new business generation results from warm leads provided

by referral sources

7 |

Dedicated to the Community

Dedicated to the Community

CUNB employees are involved in

their local communities

Strong cultural value demonstrates

that supporting the community is

also good business

CUNB supports over 75 charities

throughout Southern California

financially and with volunteer hours

Utilize local advisory boards to help

guide the Bank in its respective

markets

“Outstanding”

CRA Rating

8 |

Experienced Management

Experienced Management

9

*Formerly EVP at Premier Commercial Bank, N.A.

Name

Title

Functional

Banking Exp

CUB Tenure

David Rainer

President

Chief Executive Officer

32 years

7 years

Anne Williams

EVP

Chief Operating Officer & Chief

Credit Officer

32 years

7 years

Karen

Schoenbaum

EVP

Chief Financial Officer

19 years

3 years

Anita Wolman

EVP

General Counsel

35 years

7 years

Sam Kunianski

EVP

Executive Manager –

Commercial

and Private Banking

28 years

6 years

William Sloan

EVP

Executive Manager –

Real Estate and

Santa Clarita Regional Manager

28 years

7 years

Stephen Pihl

EVP

Executive Manager –

SBA and

Orange County Regional Manager

25 years

New addition* |

A

History of Success A History of Success

10

The Management Team at California United Bank has three decades of banking

experience

in

the

Southern

California

Market.

The

same

Executive

Team

that

created success at the banks below are now in charge at California United Bank.

Wells Fargo/Security Pacific –

1980s

California United Bank (1992 –

1997)

Grew to $1 billion in assets

Sold to Bank of Hawaii in 1997

Santa Monica Bank

Sold to U.S. Bancorp in 2000

U.S. Bank (2001 –

2004)

California United Bank (Current)

Opened in 2005

Acquired Cal Oaks State Bank December 31, 2010

Merged with Premier Commercial Bancorp July 31, 2012

$1.25 billion in total assets at December 31, 2012 |

Our Growth Strategy

Our Growth Strategy

11

Organic

Organic

Acquisitions

Acquisitions

De novo regional offices with strong local leadership

Hire “in market”

talent

Offer sophisticated products/solutions

Expertise in C&I and Commercial Real Estate lending

Relationship-based business

Distinguish by service

New SBA lending expertise provided by PCB

California Oaks State Bank (12/31/10)

Premier Commercial Bank (7/31/12) |

Q4

2012 Highlights Q4 2012 Highlights

12

Core earnings

*

of $3.9 million

+146% YoY

Strong balance sheet growth

+8% loan growth (linked quarter)

+3% non-interest bearing deposit growth (linked quarter)

High quality deposit base

50% non-interest bearing

17 bps cost of deposits

NIM and efficiency ratio improve

NIM increases 30 bps to 3.87%

Efficiency ratio improves to 72%

Continued pristine credit quality

No charge-offs in Q4

*

Core earnings reconciliation to net income provided in Appendix |

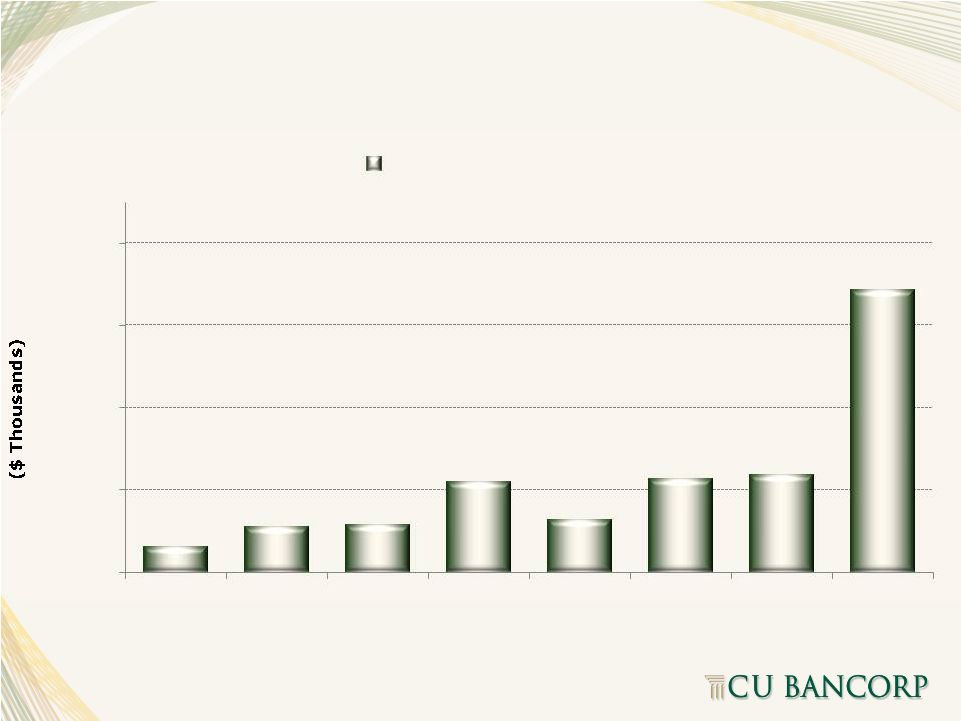

Increasing Earnings Power

Increasing Earnings Power

*

Core earnings reconciliation to net income provided in Appendix

13

$803

$1,046

$1,076

$1,596

$1,134

$1,627

$1,683

$3,929

$500

$1,500

$2,500

$3,500

$4,500

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

Core Earnings* |

Improving Operating Leverage

Improving Operating Leverage

14

3Q12 operating expenses excludes $2.5 million in merger-related

expenses $6

$7

$8

$9

$10

$11

$12

$13

$14

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

Revenue

Operating Expenses |

Impact of PCB Merger

Impact of PCB Merger

15

*

Core earnings reconciliation to net income provided in Appendix

$1,596

$3,929

$500

$1,500

$2,500

$3,500

$4,500

4Q11

4Q12

Core Earnings*

83%

72%

50%

60%

70%

80%

90%

100%

4Q11

4Q12

Efficiency Ratio

0.15%

0.50%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

4Q11

4Q12

ROAA

1.52%

5.14%

0.00%

2.00%

4.00%

6.00%

4Q11

4Q12

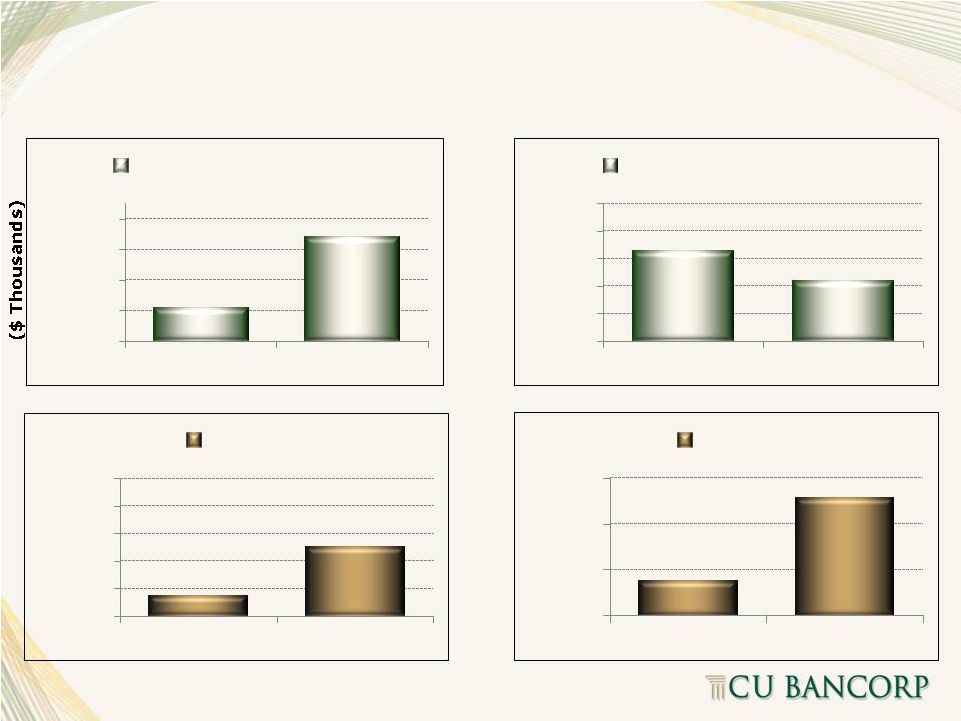

ROAE |

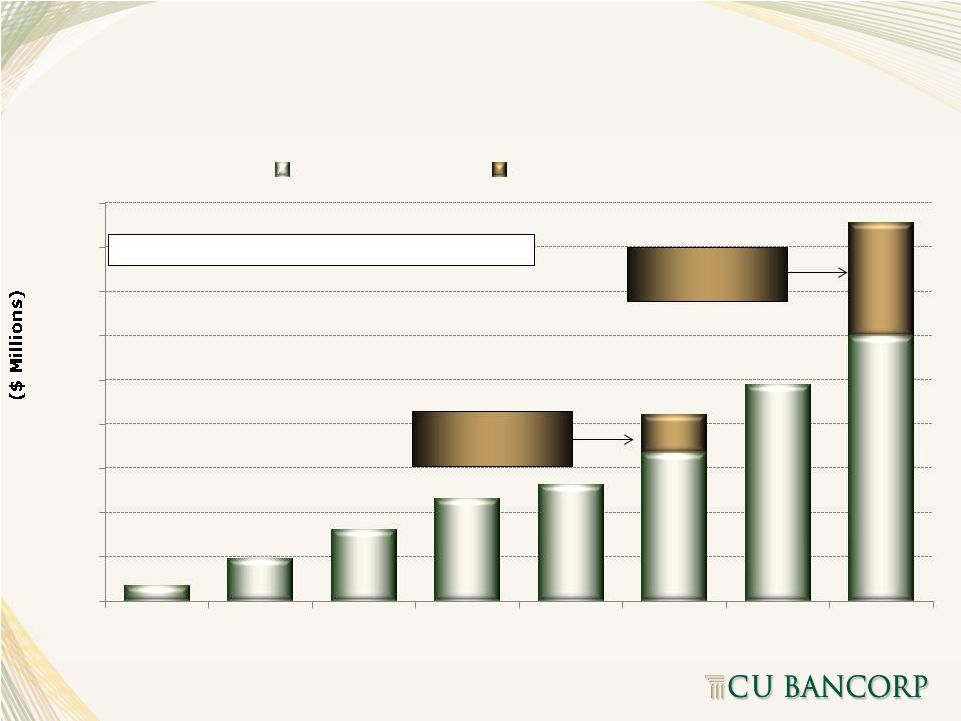

Consistent Asset Growth

Consistent Asset Growth

16

*Represents the assets acquired from Premier

Commercial Bancorp on July 31, 2012 $102

$178

$260

$379

$457

$638

$800

$853

$118

$397*

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

2005

2006

2007

2008

2009

2010

2011

2012

$1,250

PCB

acquisition

$756

COSB

acquisition

CUB Organic

Acquisitions |

Loan Growth

Loan Growth

17

Q4 2012 Loan Growth = $60MM or 8%

$35

$96

$162

$232

$263

$334

$489

$600

$87

$255

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2005

2006

2007

2008

2009

2010

2011

2012

CUB Organic

Acquisitions

$855

PCB

acquisition

$421

COSB

acquisition |

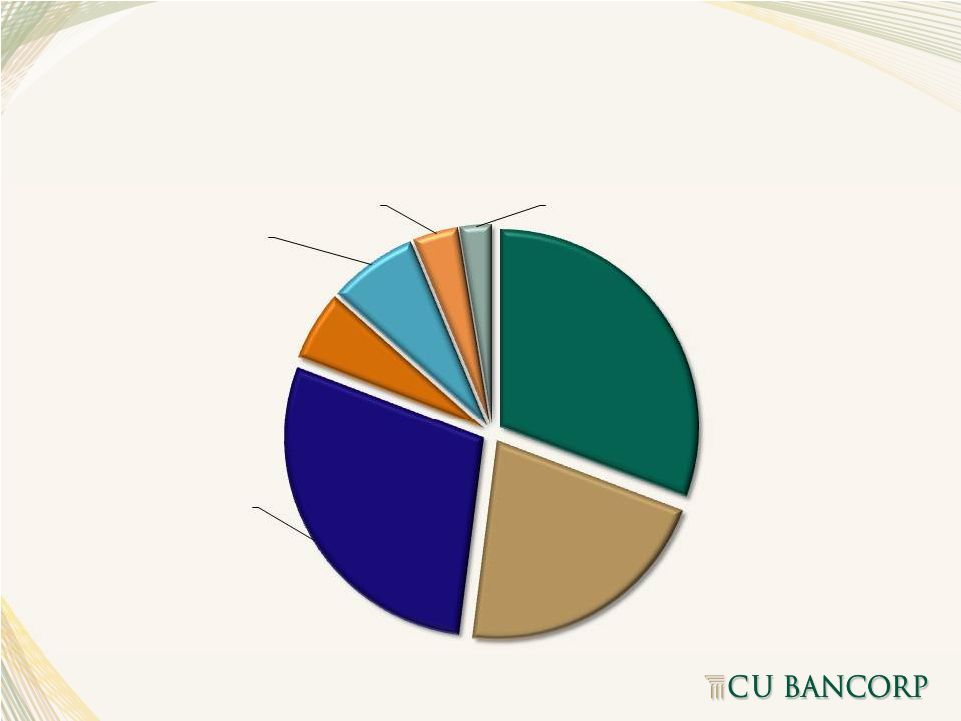

Loan Portfolio Composition

Loan Portfolio Composition

(December 31, 2012)

(December 31, 2012)

18

C&I

31%

Owner-

Occupied CRE

21%

Non-Owner

Occupied CRE

29%

Construction

6%

1-4 Family

7%

Multi-Family

4%

Other

2% |

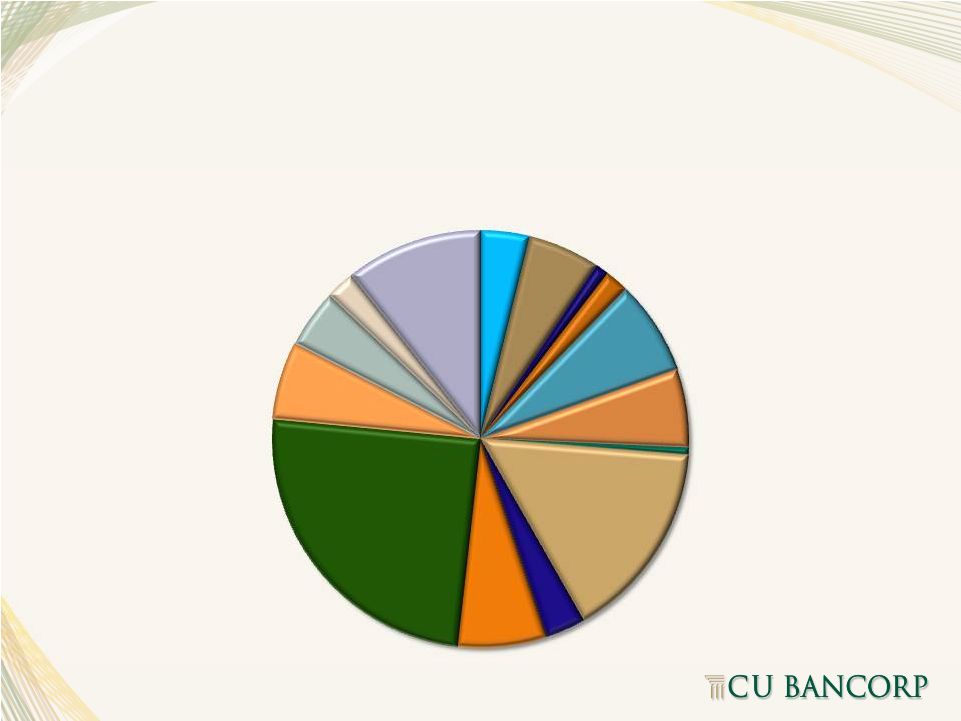

Loans by Industry

Loans by Industry

(C&I and Owner-Occupied)

(C&I and Owner-Occupied)

(December 31, 2012)

(December 31, 2012)

19

Admin Mgmt

4%

Construction

6%

Education

1%

Entertainment

2%

Finance

7%

Healthcare

6%

Information

1%

Manufacturing

15%

Other Services

3%

Professional Svces

7%

Real Estate

25%

Restaurant/Lodging

6%

Retail

4%

Transportation

2%

Wholesale

11% |

NPAs/Total Assets

NPAs/Total Assets

20

Peer Group includes public banks or bank holding companies in

California with total assets between $1.0-$1.5 billion 0.00%

1.12%

1.42%

1.19%

1.05%

0.98%

1.07%

1.09%

2.55%

4.44%

3.31%

3.18%

3.27%

2.91%

2.62%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

2008

2009

2010

2011

1Q12

2Q12

3Q12

4Q12

CUNB

Peer Group Avg.

5.26% |

NCOs/Avg. Loans

NCOs/Avg. Loans

21

Peer Group includes public banks or bank holding companies in California

with total assets between $1.0-$1.5 billion 0.00%

0.80%

0.49%

0.08%

1.01%

1.98%

1.51%

0.88%

0.90%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

2008

2009

2010

2011

2012

CUNB

Peer Group Avg.

-0.04%

-0.50% |

$60

$116

$191

$246

$346

$545

$691

$800

$113

$278

$0

$200

$400

$600

$800

$1,000

$1,200

2005

2006

2007

2008

2009

2010

2011

2012

CUB Organic

Acquisitions

$1,078

PCB

acquisition

$658

COSB

acquisition

Q4 2012 Non-Interest Bearing Growth = $18MM

Strong Deposit Growth

Strong Deposit Growth

22 |

Deposit Composition

Deposit Composition

(December 31, 2012)

(December 31, 2012)

23

Non-Int.

Bearing

Demand

50.4%

Interest

Bearing

Transaction

10.5%

MM and

Savings

31.6%

CDs

7.5% |

Transaction

Transaction

Accounts

Accounts

and

and

Cost

Cost

of

of

Funds

Funds

24

Peer Group includes public banks or bank holding companies in California

with total assets between $1.0-$1.5 billion 26.8

28.4

31.1

36.9

38.4

40.3

47.8

51.4

46.2

53.5

64.5

67.5

57.6

60.9

2.00

1.31

0.87

0.64

0.47

0.47

0.33

1.59

0.70

0.45

0.19

0.12

0.24

0.24

0.0

0.5

1.0

1.5

2.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2008Y

2009Y

2010Y

2011Y

Q2 2012

Q3 2012

Q4 2012

Peer

Average

(Transaction

Accounts)

CUNB (Transaction Accounts)

Peer

Average

(Cost

of

Funds)

CUNB (Cost of Funds) |

CU

CU

Bancorp

Bancorp

Capital

Capital

Ratios

Ratios

25

Tier 1 Leverage Capital Ratio (%)

Total Risk Based Capital Ratio (%)

Peer Group includes public banks or bank holding companies in California

with total assets between $1.0-$1.5 billion (peer group data as of December 31, 2012)

9.13%

11.65%

5.00%

0%

2%

4%

6%

8%

10%

12%

14%

CUNB

Peer Group

Avg.

FDIC Well

Capitalized

12.35%

16.04%

10.00%

0%

5%

10%

15%

20%

CUNB

Peer Group

Avg.

FDIC Well

Capitalized |

Merger Overview

Merger Overview

26

Creates one of Los Angeles/Orange County’s largest independent

commercial banking franchises focused exclusively in the market

Partnered two of Southern California’s strongest commercial

banks; strengthening the franchise for long-term earnings

growth and value creation

The critical mass of a larger institution will enable the bank to

expand available services and penetrate additional markets

The transaction will be beneficial for stakeholders in both

organizations: creating value for shareholders, employees,

customers, and the Southern California communities

Southern California’s

Preeminent Business Bank |

Merger of Two Attractive Franchises

Merger of Two Attractive Franchises

27

Low Cost Deposits

C&I Lending Expertise

Attractive Locations

Strong Credit Quality

Experienced Management Team

SBA Expertise

Real Estate Lending Expertise

Attractive Orange County Market

Strong Credit Quality

Experienced Management Team |

An

Abundance of Synergies An Abundance of Synergies

28

Combined breadth of products and services will

increase business development capabilities

throughout footprint

PCB’s award-winning SBA lending platform will be

leveraged throughout CUB’s markets

Improving PCB’s deposit mix and reducing funding

costs

Elimination of redundancies will provide meaningful

cost savings and enhance efficiencies

Greater scale will enable better absorption of

increasing regulatory compliance costs |

Shifting from Growth

Shifting from Growth

to High Performance

to High Performance

29

Capture synergies from PCB merger

Expand non-interest income through

increased SBA loan production and sales

Continue attracting high performing bankers

Further penetrate existing footprint

Enhance efficiencies as we continue to scale |

Contact Information

Contact Information

30

For more information, please contact:

Karen Schoenbaum, CFO

(818) 257-7700

kschoenbaum@cunb.com |

Appendix

Appendix

31

Reconciliation of Core Earnings to Net Income (Loss)

4Q12

3Q12

2Q12

1Q12

4Q11

3Q11

2Q11

1Q11

Net Income (Loss)

1,628

(932)

525

506

306

601

312

248

Add back: Provision for income tax expense (benefit)

1,166

(453)

502

450

181

454

242

270

Add back: Provision for loan losses

867

521

380

-

781

-

467

194

Subtract: Gain on sale of securities, net

-

-

-

-

-

6

69

144

Subtract: Other-than-temporary impairment losses, net

(65)

(30)

(30)

(30)

(130)

(19)

(70)

(45)

Add back: Merger related expenses

203

2,517

190

148

198

8

24

190

Core Earnings

3,929

1,683

1,627

1,134

1,596

1,076

1,046

803 |