Attached files

| file | filename |

|---|---|

| 8-K - 8-K - FEDERAL HOME LOAN MORTGAGE CORP | d476285d8k.htm |

| EX-99.1 - EXHIBIT 99.1 - FEDERAL HOME LOAN MORTGAGE CORP | d476285dex991.htm |

| EX-99.2 - EXHIBIT 99.2 - FEDERAL HOME LOAN MORTGAGE CORP | d476285dex992.htm |

Fourth Quarter 2012

Financial Results

Supplement

February 28, 2013

Exhibit 99.3 |

2

Table of contents

Business Results

Credit Supplement

3 -

Quarterly Net Income and Comprehensive Income

20 -

National Home Prices

4 -

Full-Year Net Income and Comprehensive Income (Loss)

21 -

State-by-State Home Prices: June 2006 to December 2012

5 -

Comprehensive Income (Loss)

22 -

State-by-State Home Prices: December 2011 to December 2012

6 -

Treasury Draw Requests and Dividend Payments

23 -

Mortgage Market and Freddie Mac Serious Delinquency Rates

7 -

Total Equity (Deficit) and Senior Preferred Stock Activity

24 -

8 -

Total Other Comprehensive Income (Loss)

25 -

9 -

Loan Loss Reserves

26 -

10 -

Real Estate Owned

27 -

11 -

28 -

12 -

29 -

13 -

30 -

Multifamily Portfolio Composition

14 -

31 -

Multifamily New Business Volume by State

15 -

32 -

Multifamily Mortgage Portfolio UPB Concentration by State

16 -

33 -

Multifamily Mortgage Portfolio by Attribute

17 -

34 -

Multifamily Mortgage Portfolio by Attribute, Continued

18 -

Purchase Agreement Portfolio Limits

35 -

Multifamily Market and Freddie Mac Delinquency Rates

Loan Purpose of Single-Family Credit Guarantee Portfolio

Purchases

Credit Quality of Single-Family Credit Guarantee Portfolio Purchases

Single-Family Credit Guarantee Portfolio Characteristics

Single-Family 4Q 2012 Credit Losses and REO by Region and State

Single-Family Credit Profile by Book Year and Product Feature

Market Liquidity Provided

Single-Family Cumulative Foreclosure Transfer and Short Sale

Rates by Book Year

Single-Family Refinance Activity

Single-Family Loan Workouts

Repurchase Requests

Performance of Single-Family Modified Loans

Single-Family Loan Modifications

Administrative Expenses and Efficiency |

3

Quarterly net income and comprehensive income

Line

2:

(Provision)

benefit

for

credit

losses

shifted

from

provision expense for 3Q12 to a benefit for 4Q12. The

improvement is driven by a decrease in the volume of

newly delinquent single-family loans and the positive

impact of increased national home prices.

Line 5:

Net impairment of available-for-sale (AFS)

securities increased in 4Q12 mainly due to the

implementation of a third-party model to project cash flow

estimates on Freddie Mac’s single-family non-agency

mortgage-related securities, partially offset by

improvements in forecasted home prices over the

expected life of the company’s AFS securities.

Line 13:

Income tax benefit increased in 4Q12 primarily

due to the release of tax reserves as a result of the

favorable resolution of tax matters with the Internal

Revenue Service (IRS).

Line 15:

Total other comprehensive income decreased in

4Q12. The decrease mostly reflects that 3Q12 results

benefited from significant spread tightening on non-agency

AFS securities whereas non-agency spreads were

relatively flat in 4Q12.

($ Millions)

4Q 2012

vs

4Q 2011

3Q 2012

4Q 2012

3Q 2012

1

Net interest income

$4,683

$4,269

$4,456

$187

2

(Provision) benefit for credit losses

(2,578)

(610)

700

1,310

3

Net interest income after provision for credit

losses

2,105

3,659

5,156

1,497

Non-interest income (loss)

4

Derivative gains (losses)

(766)

(488)

(22)

466

5

Net impairment of available-for-sale securities

recognized in earnings

(595)

(267)

(1,239)

(972)

6

Other non-interest income

390

195

5

(190)

7

Non-interest income (loss)

(971)

(560)

(1,256)

(696)

Non-interest expense

8

Total administrative expenses

(380)

(401)

(422)

(21)

9

Real estate owned operations income (expense)

(80)

49

33

(16)

10

Other expenses

(93)

(121)

(199)

(78)

11

Non-interest expense

(553)

(473)

(588)

(115)

12

Income before income tax benefit

581

2,626

3,312

686

13

Income tax benefit

38

302

1,145

843

14

Net income

619

2,928

4,457

1,529

15

Total other comprehensive income,

net of taxes

887

2,702

1,271

(1,431)

16

Comprehensive income

$1,506

$5,630

$5,728

$98 |

4

Full-year net income and comprehensive income (loss)

Line 2:

Provision for credit losses improved in 2012

driven by a decrease in the volume of newly delinquent

single-family loans and the positive impact of increased

national home prices.

Line 4:

Derivative losses decreased in 2012 primarily due

to improvement in the fair value of the company’s net pay-

fixed swap portfolio as interest rates declined less in 2012

as compared to 2011.

Line 13:

Income tax benefit increased in 2012 primarily

due to the release of tax reserves as a result of the

favorable resolution of tax matters with the Internal

Revenue Service (IRS).

Line 15:

Total other comprehensive income increased in

2012 primarily driven by the favorable impact of spread

changes on certain of the company’s non-agency AFS

securities in 2012, partially offset by lower benefit from

interest rates as rates declined less in 2012 as compared

to 2011.

($ Millions)

2012

vs

2011

2012

2011

1

Net interest income

$18,397

$17,611

($786)

2

Provision for credit losses

(10,702)

(1,890)

8,812

3

Net interest income after provision for credit

losses

7,695

15,721

8,026

Non-interest income (loss)

4

Derivative gains (losses)

(9,752)

(2,448)

7,304

5

Net impairment of available-for-sale securities

recognized in earnings

(2,301)

(2,168)

133

6

Other non-interest income

1,175

533

(642)

7

Non-interest income (loss)

(10,878)

(4,083)

6,795

Non-interest expense

8

Total administrative expenses

(1,506)

(1,561)

(55)

9

Real estate owned operations expense

(585)

(59)

526

10

Other expenses

(392)

(573)

(181)

11

Non-interest expense

(2,483)

(2,193)

290

12

Income (loss) before income tax benefit

(5,666)

9,445

15,111

13

Income tax benefit

400

1,537

1,137

14

Net income (loss)

(5,266)

10,982

16,248

15

Total other comprehensive income,

net of taxes

4,036

5,057

1,021

16

Comprehensive income (loss)

($1,230)

$16,039

$17,269 |

5

Comprehensive income (loss)

1

Consists of the after-tax changes in: (a) the unrealized gains and losses on

available-for-sale securities; (b) the effective portion of derivatives previously

accounted for as cash flow hedges; and (c) defined benefit plans.

A

B

C = A + B

Net income (loss)

Comprehensive income (loss)

Total

other

comprehensive

income

(loss),

net

of

taxes

1 |

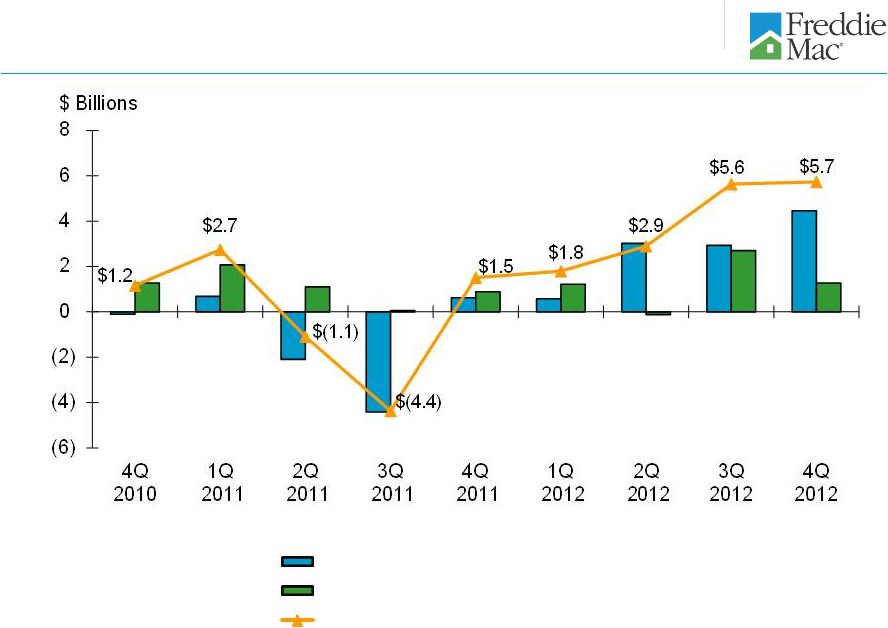

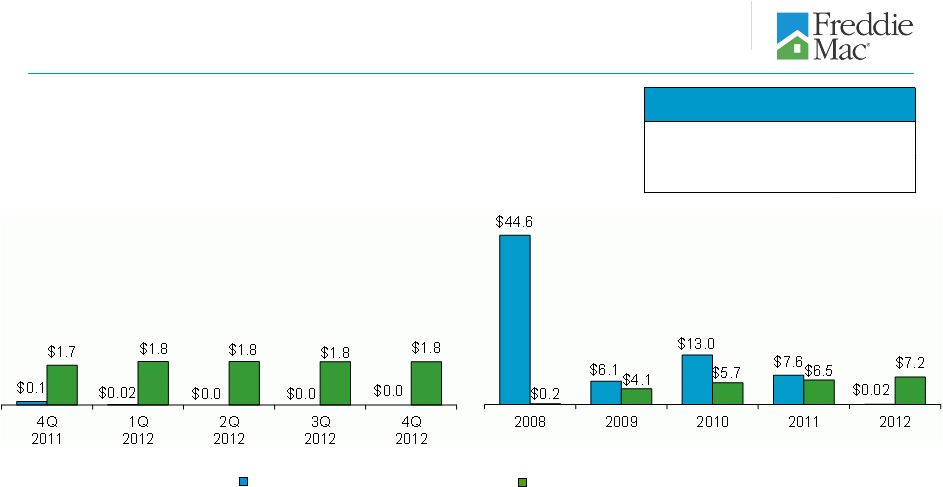

Dividend Payment to Treasury

Draw Request from Treasury

6

Treasury draw requests and dividend payments

1

Excludes the initial liquidation preference of Freddie Mac’s senior preferred

stock of $1.0 billion. 2

Quarterly

amounts

represent

the

draw

requested

based

on

Freddie

Mac’s

net

worth

deficit

for

the

quarters

presented.

Annual

amounts

represent

the

total

draws

requested

based

on Freddie Mac’s quarterly net deficits for the periods presented. Draw

requests are funded in the subsequent quarter (e.g., $19 million draw request for 1Q 2012 was funded in 2Q

2012).

3

Represents quarterly cash dividends paid by Freddie Mac to Treasury during the

periods presented. Through December 31, 2012, Treasury was entitled to receive cumulative

quarterly

cash

dividends

at

the

annual

rate

of

10%

per

year

on

the

liquidation

preference

of

the

senior

preferred

stock.

However,

the

fixed

dividend

rate

was

replaced

with

a

net

worth sweep dividend payment beginning in the first quarter of 2013. See the

company’s Annual Report on Form 10-K for the year ended December 31, 2012 for more information.

$ Billions

3

2

($ Billions)

Cumulative

Total

Treasury Draw Requests

$71.3

Dividend Payments

$23.8

1 |

7

Total equity (deficit) and Senior Preferred Stock activity

Senior Preferred Stock Funding Available to Freddie Mac as of January 1, 2013:

»

The amount of available funding remaining under the Purchase Agreement after 2012

is $140.5 billion. This amount will

be

reduced

by

any

future

draws.

This

reflects

the

remaining

funding

available

as

of

December

31,

2009

of

$149.3

billion less the company’s net worth at December 31, 2012 of $8.8

billion. The provisions of the Purchase Agreement whereby

Treasury’s funding commitment would increase as necessary to accommodate any cumulative reduction

in our net worth during 2010, 2011, and 2012 no longer apply.

1

Includes the initial liquidation preference of Freddie Mac’s senior preferred

stock of $1.0 billion. ($ Millions)

4Q 2011

1Q 2012

2Q 2012

3Q 2012

4Q 2012

1

Beginning balance -

Total equity (deficit) / GAAP net worth

($5,991)

($146)

($18)

$1,086

$4,907

2

Capital draw funded by Treasury

5,992

146

19

0

0

3

Net income

619

577

3,020

2,928

4,457

4

Total other comprehensive income (loss), net of taxes

887

1,212

(128)

2,702

1,271

5

Comprehensive income

1,506

1,789

2,892

5,630

5,728

6

Dividends paid to Treasury

(1,655)

(1,807)

(1,809)

(1,809)

(1,808)

7

Other

2

0

2

0

0

8

Ending balance -

Total equity (deficit) / GAAP net worth

($146)

($18)

$1,086

$4,907

$8,827

9

Requested capital draw

$146

$19

$0

$0

$0

10

Aggregate liquidation preference of the senior preferred stock

(including the current quarter's requested capital draw)

1

$72,317

$72,336

$72,336

$72,336

$72,336 |

8

Total

other

comprehensive

income

(loss)

1

1

Total other comprehensive income (loss) represents the

change in Total AOCI, net of taxes, on the company’s consolidated balance sheets. ($

Millions) 12/31/2012

12/31/2012

vs

vs

12/31/2011

9/30/2012

12/31/2012

9/30/2012

12/31/2011

Accumulated other comprehensive income (loss)

(AOCI), net of taxes, related to:

1

Total agency available-for-sale securities

$5,011

$4,212

$3,688

($524)

($1,323)

2

Total non-agency available-for-sale securities

(11,224)

(6,917)

(5,132)

1,785

6,092

3

Available-for-sale securities

(6,213)

(2,705)

(1,444)

1,261

4,769

4

Cash flow hedge relationships

(1,730)

(1,410)

(1,316)

94

414

5

Defined benefit plans

(52)

(94)

(178)

(84)

(126)

6

Total AOCI, net of taxes

($7,995)

($4,209)

($2,938)

$1,271

$5,057 |

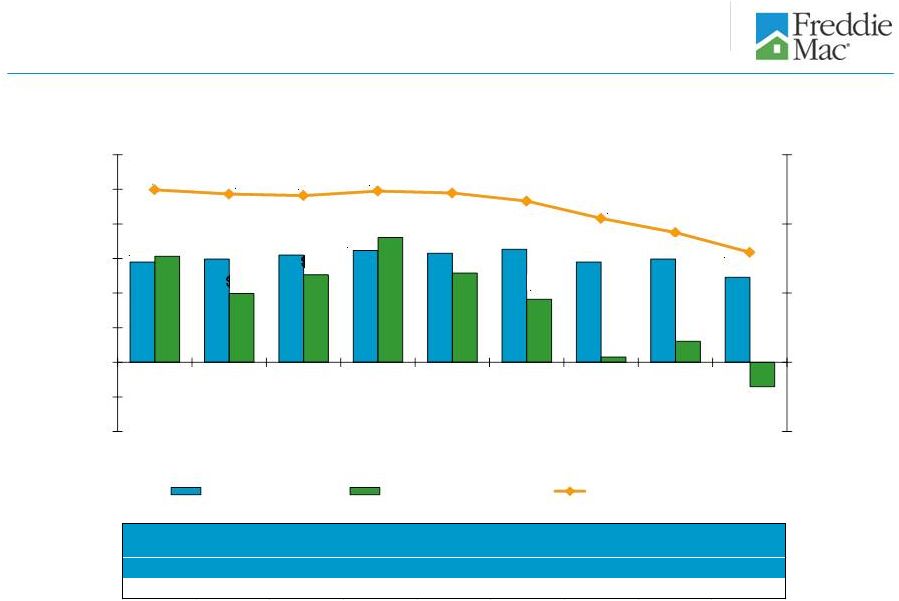

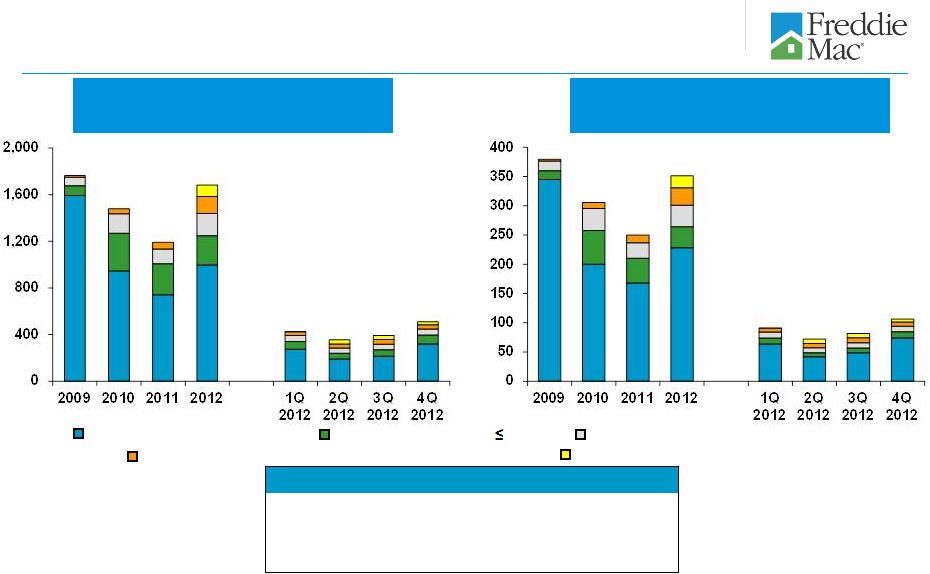

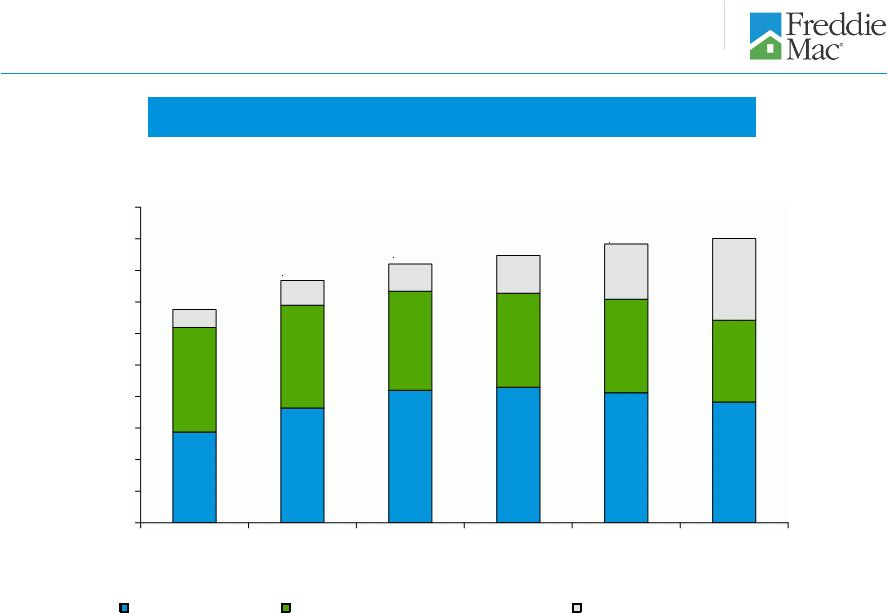

9

Loan loss reserves

1

1

1

Includes amounts related to certain loans purchased under financial guarantees and

reflected within other expenses on the company’s consolidated statements of comprehensive

income.

2

Consists of the allowance for loan losses and the reserve for guarantee losses.

3

Total mortgage portfolio, excluding non-Freddie Mac securities.

2

$2.9

$3.0

$3.1

$3.2

$3.2

$3.3

$2.9

$3.0

$2.5

$3.1

$2.0

$2.5

$3.6

$2.6

$1.8

$0.2

$0.6

($0.7)

$39.9

$39.3

$39.1

$39.7

$39.5

$38.3

$35.8

$33.8

$30.9

$5.0

$15.0

$25.0

$35.0

$45.0

($2.0)

($1.0)

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

4Q 2010

1Q 2011

2Q 2011

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012

4Q 2012

Period End Balances

$ Billions

$ Billions

Net Charge-offs

Provision (Benefit)

Loan Loss Reserves

4Q

2010

1Q

2011

2Q

2011

3Q

2011

4Q

2011

1Q

2012

2Q

2012

3Q

2012

4Q

2012

2.03%

2.02%

2.01%

2.06%

2.08%

2.03%

1.94%

1.86%

1.71%

Reserve as % of Total Mortgage Portfolio

3 |

10

Real

estate

owned

1

Property Inventory

2012 Activity

Geographic

Distribution

2

Based on Property Inventory

Historical Trend

Ending Property Inventory

1

Includes single-family and multifamily REO.

Multifamily ending property inventory was 20 properties as of December 31, 2011 and 6 properties as of December 31, 2012.

2

Region designation: West (AK, AZ, CA, GU, HI, ID, MT, NV, OR, UT, WA); Northeast

(CT, DE, DC, MA, ME, MD, NH, NJ, NY, PA, RI, VT, VA, WV); Southeast (AL, FL, GA, KY, MS,

NC, PR,

SC,

TN,

VI);

North

Central

(IL,

IN,

IA,

MI,

MN,

ND,

OH,

SD,

WI);

and

Southwest

(AR,

CO,

KS,

LA,

MO,

NE,

NM,

OK,

TX,

WY).

((Number of Properties)

In 2012, REO dispositions continued to exceed the volume of REO

acquisitions. We believe our single-family REO acquisition volume

in 2012 and 2011 was less than it otherwise would have been due in part to

the length of the single-family foreclosure timeline, particularly in

states where judicial foreclosures (those conducted under the supervision

of the court) are required. During 2012, our REO property inventory

declined most in the West region primarily due to increased disposition

activity and strengthening home prices in California. The North Central

region comprised 42 percent of our REO property inventory at December 31,

2012. We continue to have a significant number of properties in our

REO inventory that we are unable to list because they are occupied or in states

with a redemption period, particularly in Michigan, Minnesota and

Illinois. States with redemption periods require a period of time

after foreclosure during which the borrower may reclaim the property.

60,555

49,077

82,818

(94,296)

12/31/11

Inventory

Acquisitions

Dispositions

12/31/12

Inventory

5k

13k

21k

7k

13k

5k

11k

21k

5k

6k

-

5,000

10,000

15,000

20,000

25,000

Northeast

Southeast

North Central

Southwest

West

Number of

Properties

12/31/2011

12/31/2012

72k

65k

61k

60k

61k

59k

53k

51k

49k

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

4Q

2010

1Q

2011

2Q

2011

3Q

2011

4Q

2011

1Q

2012

2Q

2012

3Q

2012

4Q

2012

Number of

Properties |

11

Market liquidity provided

Number of Families Freddie Mac

Helped

to

Own

or

Rent

a

Home

1

In Thousands

Purchase

and

Issuance

Volume

2

(Single-Family and Multifamily)

$ Billions

1

For the periods presented, a borrower may be counted more than once if the company

purchased more than one loan (purchase or refinance mortgage) relating to the same

borrower.

2

Includes, on a settlement date basis, purchases of mortgages, issuance of other

guarantee commitments, and purchases of non-Freddie Mac mortgage-related securities.

Number

of

Families

Freddie

Mac

Helped

to

Own

or

Rent

a

Home

1

(In Thousands)

Refinance borrowers (includes HARP)

Purchase borrowers

Multifamily rental units

Freddie

Mac

Purchase

and

Issuance

Volume

2

Cumulative Totals

Since 2009

8,871

$1.8 Trillion

6,120

1,517

1,234 |

Relief

Refinance

–

LTV

>

100%

to

125%

(HARP)

12

Single-family

refinance

activity

1

Number of Borrowers

2, 3

In Thousands

$ Volume

3

In Billions

Non-Relief

Refinance

Relief

Refinance

–

LTV

80%

Relief

Refinance

–

LTV

>

80%

to

100%

(HARP)

$380

$306

$250

1,764

1,480

1,193

426

$91

4

4

356

$72

$351

$81

1,683

392

(In Thousands)

Number of Borrowers Freddie Mac Helped to Refinance²

Relief Refinance (Includes HARP)

Non-Relief Refinance

Freddie Mac Single-Family Refinance Volume

Cumulative Totals Since

2009

6,120

1,842

$1.3 Trillion

4,278

Relief

Refinance

–

LTV

>

125%

(HARP)

4

510

$106

1

Consists of all single-family refinance mortgage loans that we either purchased

or guaranteed during the period, including those associated with other guarantee commitments

and

Other

Guarantee

Transactions.

Prior

period

amounts

have

been

revised

to

conform

to

current

period

presentation.

2

Some

loans

have

multiple

borrowers,

but

the

company

has

counted

them

as

one

borrower

for

this

purpose.

For

the

periods

presented,

a

borrower

may

be

counted

more

than

once if the company purchased more than one refinance loan relating to the same

borrower. 3

The sum of the quarters may not equal the 2012 totals due to rounding.

4

The relief refinance mortgage initiative is Freddie Mac’s implementation of

the Home Affordable Refinance Program (HARP). Under the program, the company allows eligible

borrowers who have mortgages with high current LTV ratios to refinance their

mortgages without obtaining new mortgage insurance in excess of what was already in place.

HARP

is

targeted

at

borrowers

with

current

LTV

ratios

above

80%;

however,

Freddie

Mac’s

program

also

allows

borrowers

with

LTV

ratios

at

or

below

80%

to

participate.

4 |

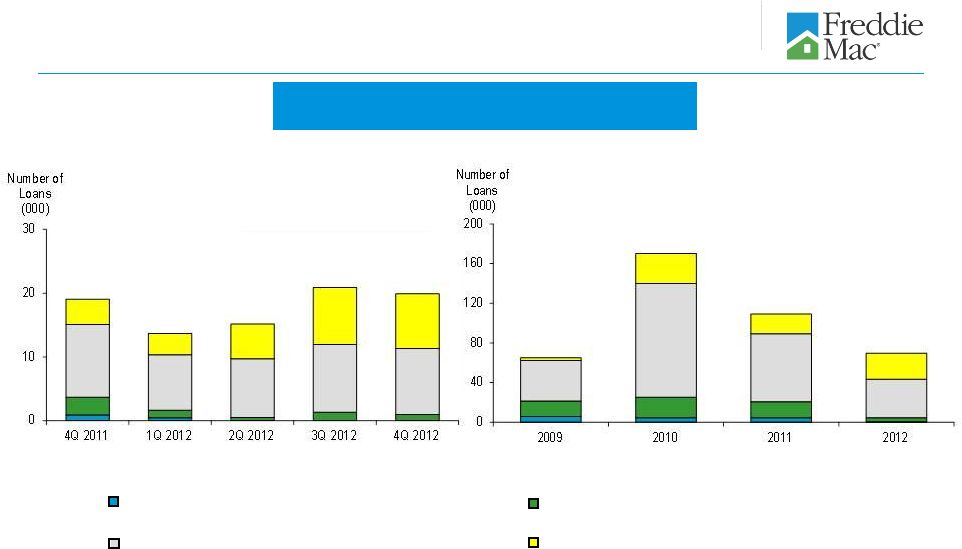

Repayment plans

13

Loan modifications

Forbearance agreements

Short sales and deed-in-lieu of foreclosure transactions

Single-family loan workouts

Home Retention Actions

1

Foreclosure Alternatives

1

44

40

41

1

These categories are not mutually exclusive and a borrower in one category may also

be included within another category in the same period. For the periods presented, borrowers

helped through home retention actions in each period may subsequently lose their

home through foreclosure or a short sale or deed-in-lieu transaction.

45

43

4Q 2011

1Q 2012

2Q 2012

3Q 2012

4Q 2012

Number of Loans

(000)

0

30

60

0

50

100

150

200

250

300

2009

2010

2011

2012

Number of Loans

(000)

133

275

208

169

Number of Families Avoiding Foreclosure

1

(In Thousands)

Families Retaining Homes

Cumulative Totals Since

2009

785

8 out of every 10 |

No change in terms

Term extension

Reduction of contractual interest rate, and in certain cases,

term extension

Rate reduction, term extension and principal forbearance

14

Single-family loan modifications

1

Includes

completed

loan

modifications

under

HAMP

and

under

the

company’s

other

modification

programs.

Excludes

those

loan

modification

activities

for

which

the

borrower

has

started the required process, but the modification has not been made permanent or

effective, such as loans in a modification trial period. 2

Principal forbearance is a change to a loan’s terms to designate a portion of

the principal as non-interest bearing and non-amortizing.

Single-family Loan Modifications

(HAMP and non-HAMP)

1

19

2

65

170

109

14

15

21

70

20 |

15

Quarterly Percentages of Modified Single-Family Loans

(HAMP and non-HAMP)

Performance of single-family modified loans

Of the loans modified in 4Q 2010, 63% were current and performing 24 to 26 months

post modification. Of the loans modified in 3Q 2012, 84% were current and

performing 3 to 5 months post modification. 1

Represents the percentage of loans that are current and performing (no payment is 30 days or more past due) or have been paid in full. Excludes loans in modification trial periods.

2

Loan

modifications

are

recognized

as

completed

in

the

quarterly

period

in

which

the

servicer

has

reported

the

modification

as

effective

and

the

agreement

has

been

accepted

by

the

company. For loans that have been remodified (e.g., where

a borrower has received a new modification after defaulting on the prior modification) the rates reflect the status of each

modification separately. For example, in the case of a remodified loan where the

borrower is performing, the previous modification would be presented as being in default in the

applicable period.

1

Time Since Modification

4Q 2010

1Q 2011

2Q 2011

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012

3 to 5 months

82%

83%

83%

81%

86%

85%

87%

84%

6 to 8 months

76%

77%

77%

79%

80%

80%

83%

N/A

9 to 11 months

72%

73%

76%

75%

75%

77%

N/A

N/A

12 to 14 months

68%

73%

73%

71%

73%

N/A

N/A

N/A

15 to 17 months

69%

70%

69%

69%

N/A

N/A

N/A

N/A

18 to 20 months

67%

67%

68%

N/A

N/A

N/A

N/A

N/A

21 to 23 months

64%

66%

N/A

N/A

N/A

N/A

N/A

N/A

24 to 26 months

63%

N/A

N/A

N/A

N/A

N/A

N/A

N/A

% Current and Performing

Quarter of Loan Modification Completion

2 |

16

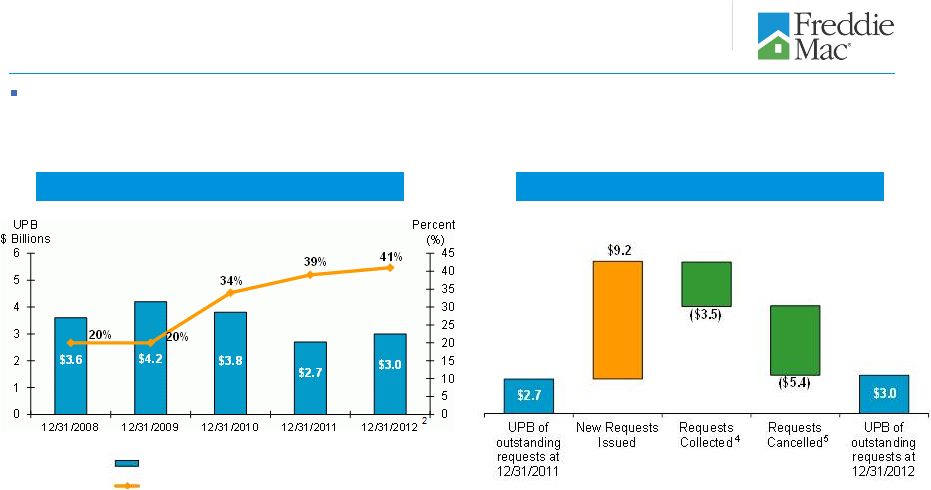

The UPB of outstanding repurchase requests issued to our single-family

seller/servicers based on breaches of representations and warranties

increased from $2.7 billion as of December 31, 2011 to $3.0 billion as of

December 31, 2012. 1

The amount the company expects to collect on outstanding requests is significantly

less than the unpaid principal balance (UPB) of the loans subject to repurchase requests primarily

because many of these requests are likely to be satisfied by reimbursement of the

company’s realized credit losses by seller/servicers, or rescinded in the course of the contractual appeals

process. Based on historical loss experience and the fact that many of these

loans are covered by credit enhancements (e.g., mortgage insurance), Freddie Mac expects the actual credit

losses experienced by the company should it fail to collect on these repurchase

requests to also be less than the UPB of the loans. 2

Approximately $1.2 billion of the total amount of repurchase requests outstanding

at December 31, 2012 were issued due to mortgage insurance rescission or mortgage insurance claim

denial.

3

Repurchase requests outstanding more than four months include repurchase requests

for which appeals were pending. 4

Requests collected are based on the UPB of the loans associated with the repurchase

request, which in many cases is more than the amount of payments received for reimbursement of

losses for requests associated with foreclosed mortgage loans, negotiated

settlements and other alternative remedies. 5

During

2012,

repurchase

requests

related

to

$5.4

billion

of

UPB

of

loans

were

cancelled,

primarily

as

a

result

of

the

servicer

providing

missing

documentation

or

a

successful

appeal

of

the

request. In addition, requests cancelled includes $30 million of other items

that affect the UPB of the loan while the repurchase request is outstanding, such as a change in UPB due to

payments made on the loan, as well as requests deemed uncollectible due to the

insolvency or other failure of the counterparty. Repurchase requests

Trend in Repurchase Requests Outstanding

2012 Repurchase Request Activity

$ Billions

1

Outstanding repurchase requests

Requests outstanding more than 4 months

3 |

17

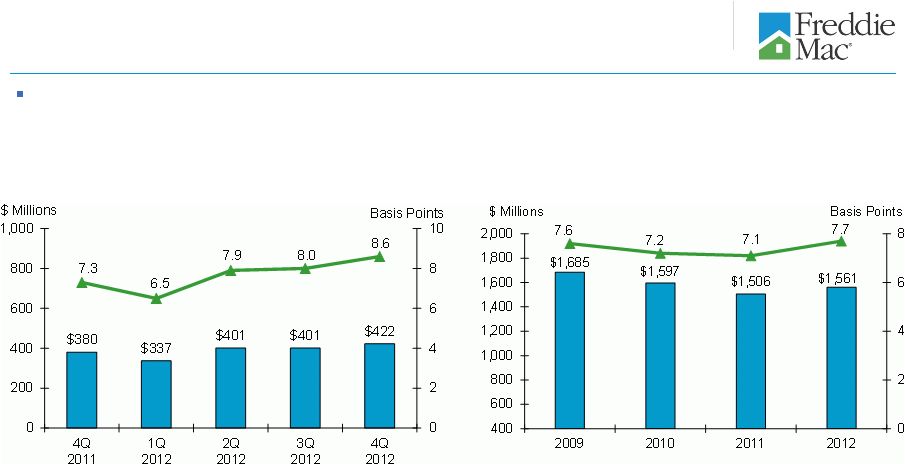

Administrative

expenses

and

efficiency

1

1

Administrative expenses, expressed as a percentage of the average total mortgage

portfolio. Basis points for the quarters are calculated on an annualized basis.

Administrative expenses increased during 2012 as a result of initiatives we are

pursuing under the Conservatorship Scorecard and other-FHFA mandated

strategic initiatives. |

$653

$618

$581

$568

$558

$729

$729

$729

$729

$650

$553

12/31/2011

3/31/2012

6/30/2012

9/30/2012

12/31/2012

12/31/2013

Mortgage-related investments portfolio ending balance

Mortgage-related investments portfolio limit

18

Purchase Agreement portfolio limits

Indebtedness

1, 3

($ Billions)

Mortgage Assets

1, 2

($ Billions)

Indebtedness limit

Total debt outstanding

4

4

4

$674

$629

$590

$570

$552

$972

$874.8

$874.8

$874.8

$874.8

$780

12/31/2011

3/31/2012

6/30/2012

9/30/2012

12/31/2012

1/1/2013

The company’s Purchase Agreement with Treasury limits the amount of mortgage assets the company

can own and indebtedness it can incur. Under the Purchase Agreement, mortgage assets and

indebtedness are calculated without giving effect to the January 1, 2010 change in the accounting guidance related to the transfer of financial assets and consolidation of

variable interest entities (VIEs). See the company’s Annual Report on

Form 10-K for the year ended December 31, 2012 for more information.

Represents the unpaid principal balance (UPB) of the company’s mortgage-related investments

portfolio. The company discloses its mortgage assets on this basis monthly in its Monthly

Volume Summary reports, which are available on its Web site and in Current Reports on Form 8-K

filed with the Securities and Exchange Commission (SEC). Represents the par value of the company’s unsecured short-term and long-term debt

securities issued to third parties to fund its business activities. The company discloses its

indebtedness on this basis monthly in its Monthly Volume Summary reports, which are available on its

Web site and in Current Reports on Form 8-K filed with the SEC.

Limit under the Purchase Agreement, as amended on August 17, 2012.

1

2

3

4 |

19

Credit

Supplement |

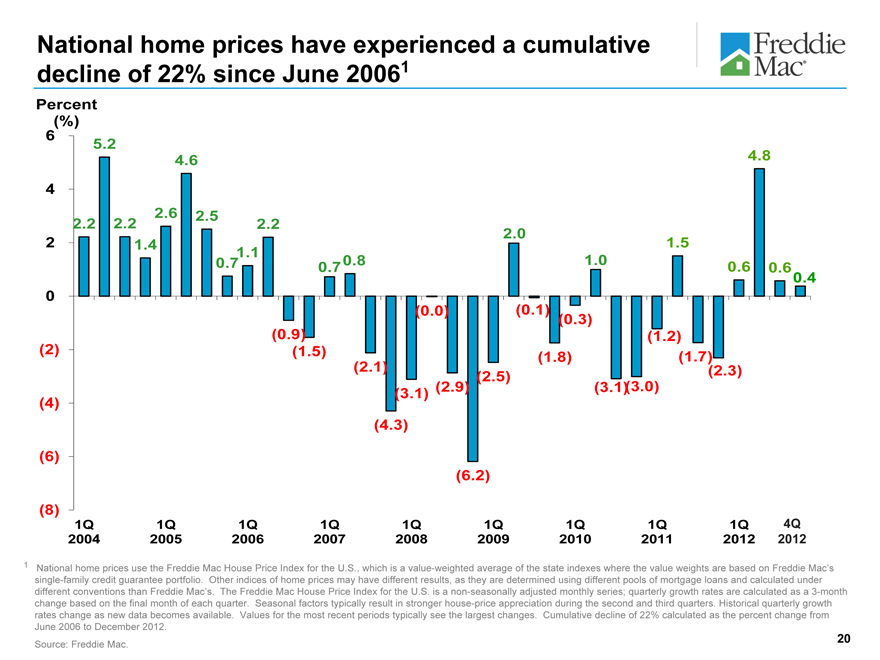

National home prices have experienced a cumulative decline of 22% since June 20061

Percent (%)

6 4 2 0 (2) (4) (6) (8)

5.2

4.6 4.8

2.6 2.5 .2 2.2 2.2

2.0

1.4 1.5

1.1

0.7 0.8 1.0

0.7 0.6 0.6

0.4

(0.0) (0.1)

(0.3)

(0.9) (1.2)

(1.5) (1.8) (1.7)

(2.1) (2.3)

(2.5)

(2.9) (3.1)(3.0)

(3.1)

(4.3)

(6.2)

1Q 1Q 1Q 1Q 1Q 1Q 1Q 1Q 1Q 4Q

2004 2005 2006 2007 2008 2009 2010 2011 2012 2012

1 National home prices use the Freddie Mac House Price Index for the U.S., which is a value-weighted average of the state indexes where the value weights are based on Freddie Mac’s single-family credit guarantee portfolio. Other indices of home prices may have different results, as they are determined using different pools of mortgage loans and calculated under different conventions than Freddie Mac’s. The Freddie Mac House Price Index for the U.S. is a non-seasonally adjusted monthly series; quarterly growth rates are calculated as a 3-month change based on the final month of each quarter. Seasonal factors typically result in stronger house-price appreciation during the second and third quarters. Historical quarterly growth rates change as new data becomes available. Values for the most recent periods typically see the largest changes. Cumulative decline of 22% calculated as the percent change from June 2006 to December 2012.

20

Source: Freddie Mac.

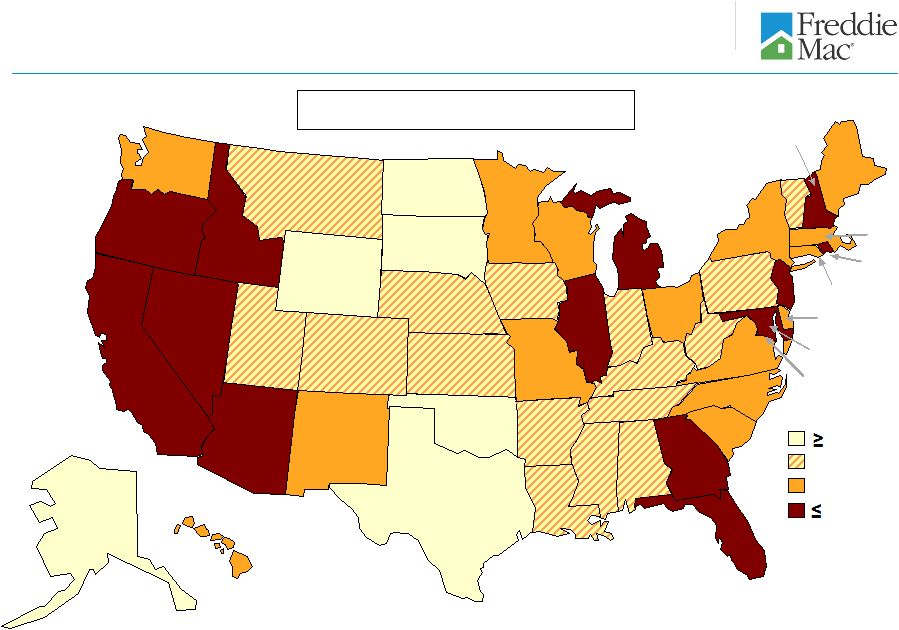

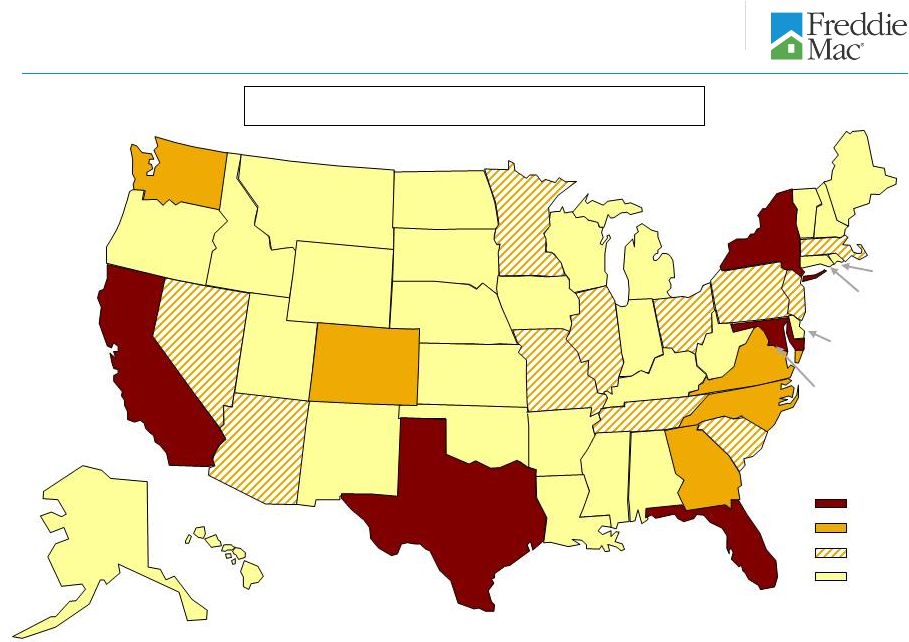

Home

Price Performance By State June

2006

to

December

2012

1

-11%

3%

0%

-12 to -1%

-23%

-22 to -13%

-7%

-37%

-38%

-3%

CT -22%

DC 10%

-18%

-41%

-29%

-17%

-2%

-23%

-29%

-11%

-4%

-4%

-1%

-18%

-27%

-15%

-29%

-22%

-15%

-12%

-4%

-13%

29%

-2%

-26%

-14%

-53%

-14%

-19%

3%

-24%

-11%

RI -30%

-14%

7%

-6%

7%

-10%

-18%

-7%

-22%

-20%

-4%

2%

-23%

WA

OR

CA

NV

ID

MT

WY

UT

AZ

NM

TX

LA

OK

KS

NE

SD

ND

MN

IA

MO

AR

MS

AL

GA

FL

TN

KY

IL

WI

MI

OH

PA

AK

HI

SC

NC

VA

NY

VT

NJ

ME

NH

MA

MD

DE

CO

WV

IN

United States -22%

1

The Freddie Mac House Price Index for the U.S. is a value-weighted average of

the state indexes where the value weights are based on Freddie Mac’s single-family credit

guarantee portfolio. Other indices of home prices may have different results,

as they are determined using different pools of mortgage loans and calculated under different

conventions.

The

Freddie

Mac

House

Price

Index

for

the

U.S.

is

a

non-seasonally

adjusted

monthly

series.

Source: Freddie Mac

21 |

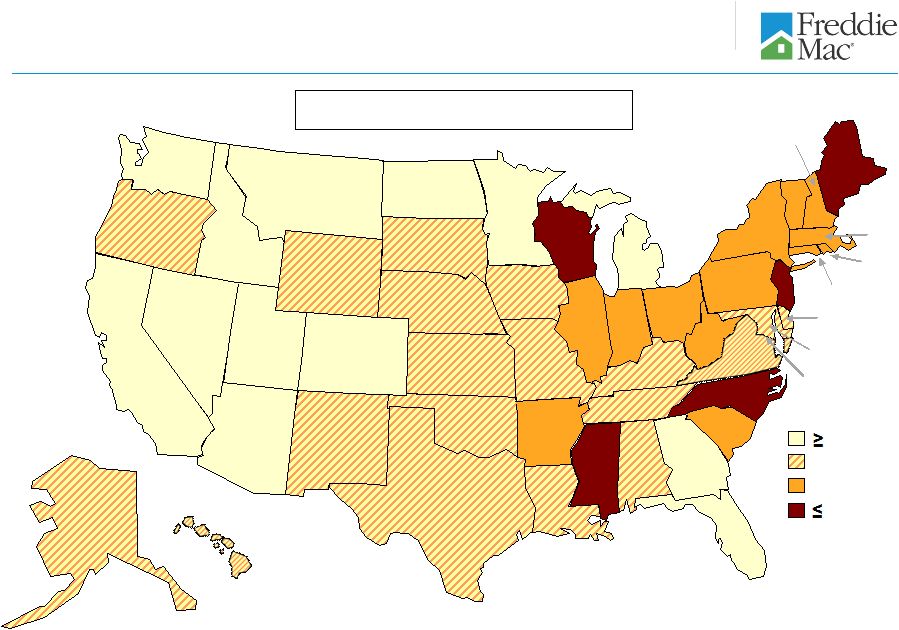

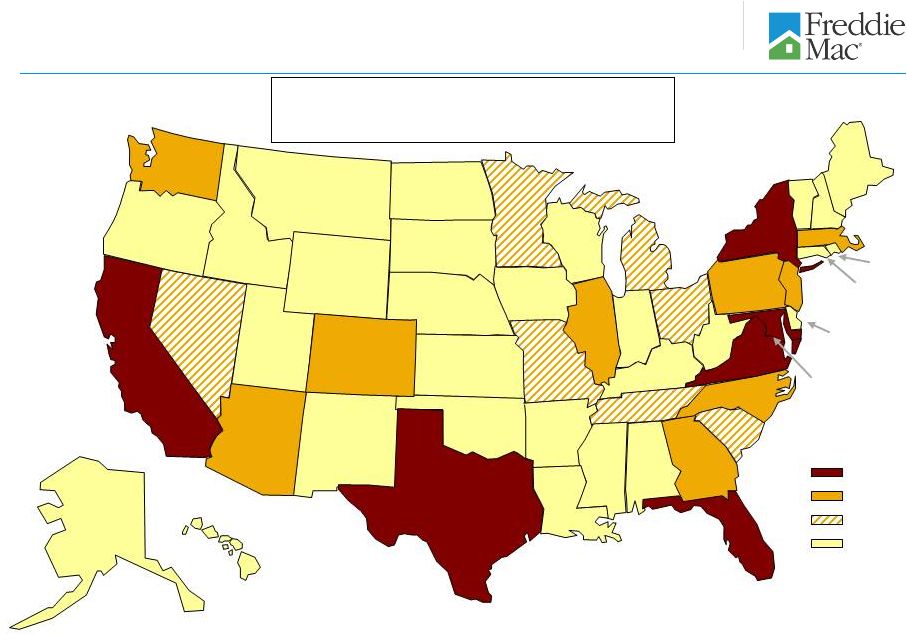

Home

Price Performance By State December

2011

to

December

2012

1

1

The Freddie Mac House Price Index for the U.S. is a value-weighted average of

the state indexes where the value weights are based on Freddie Mac’s single-family credit

guarantee portfolio. Other indices of home prices may have different results, as

they are determined using different pools of mortgage loans and calculated under different

conventions. The Freddie Mac House Price Index for the U.S. is a

non-seasonally adjusted monthly series.

Source: Freddie Mac

22

5%

6%

9%

3 to 8%

-1%

0 to 2%

1%

26%

13%

12%

CT 0%

DC 8%

4%

14%

9%

6%

3%

14%

1%

0%

4%

3%

5%

4%

-1%

16%

11%

6%

-1%

9%

-1%

11%

6%

-2%

3%

21%

0%

2%

3%

8%

1%

RI 1%

1%

6%

7%

6%

11%

6%

9%

-1%

2%

3%

2%

WA

OR

CA

NV

ID

AZ

MT

AK

HI

UT

NM

TX

OK

CO

WY

ND

SD

NE

KS

LA

AR

MO

IA

MN

WI

IL

MS

TN

KY

IN

OH

MI

AL

GA

FL

SC

NC

VA

WV

PA

ME

VT

MA

NH

MD

DE

NJ

United States 6%

0%

NY

2% |

23

1

Source: National Delinquency Survey from the Mortgage Bankers Association.

Categories represent first lien single-family loans. 2

See

“MD&A

–

RISK

MANAGEMENT

–

Credit

Risk

–

Mortgage

Credit

Risk

–

Single-Family

Mortgage

Credit

Risk

–

Credit

Performance

–

Delinquencies”

in

Freddie

Mac’s

Form

10-K

for the year ended December 31, 2012, for information about the company’s

reported delinquency rates. 1

1

1

Single-family Serious Delinquency Rates

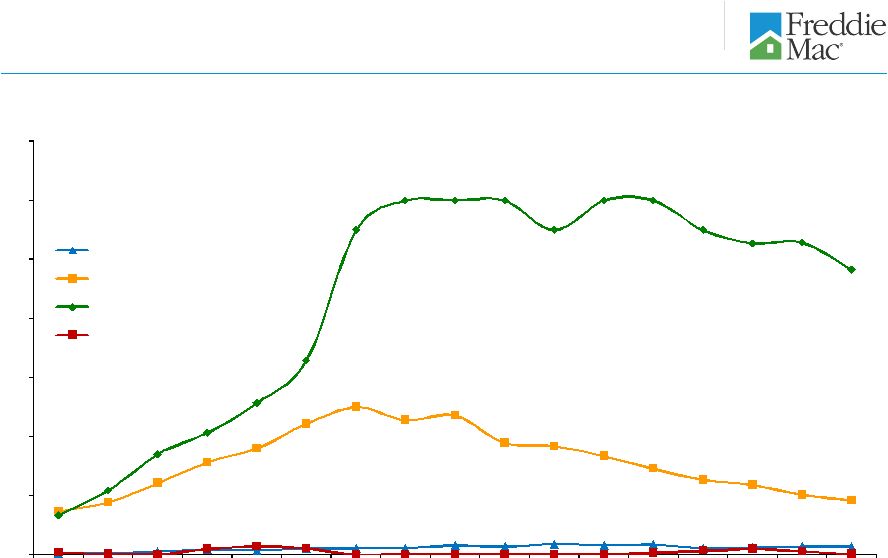

Mortgage market and Freddie Mac serious delinquency

rates

2

0

4

8

12

16

20

24

28

32

Dec-08

Mar-09

Jun-09

Sep-09

Dec-09

Mar-10

Jun-10

Sep-10

Dec-10

Mar-11

Jun-11

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

Total Mortgage Market

Prime

Subprime

Freddie Mac

21.70%

6.78%

4.34%

3.25% |

24

Loan purpose of single-family credit guarantee

portfolio purchases

1

The relief refinance mortgage initiative is Freddie Mac’s implementation of

the Home Affordable Refinance Program (HARP). Under the program, the company allows eligible

borrowers who have mortgages with high current LTV ratios to refinance their

mortgages without obtaining new mortgage insurance in excess of what was already in place. HARP is

targeted at borrowers with current LTV ratios above 80%; however, Freddie

Mac’s relief refinance initiative also allows borrowers with LTV ratios at or below 80% to participate.

2

Relief refinance mortgages with LTV ratios above 80% represented

approximately 20% of our total single-family credit guarantee portfolio

purchases in 2012, based on unpaid principal

balance. 1, 2

0

10

20

30

40

50

60

70

80

90

100

2005

2006

2007

2008

2009

2010

2011

2012

Percent

(%)

Purchase

Non-Relief Refinance

Relief Refinance (includes HARP)

82% |

25

Credit quality of single-family credit guarantee portfolio

purchases

2009

2010

2011

2012

Weighted Average Original LTV Ratio

1

Relief refinance (includes HARP)

80%

77%

77%

97%

All other

66%

67%

67%

68%

Total purchases

67%

70%

70%

76%

Weighted Average Credit Score

2

Relief refinance (includes HARP)

738

747

744

740

All other

757

758

759

762

Total purchases

756

755

755

756

2009

2010

2011

2012

Purchase of Relief Refinance Mortgages > 80% LTV (HARP loans)

3

$ Billions

$19.6

$47.9

$39.7

$86.9

% of single-family credit guarantee portfolio purchases

4%

12%

12%

20%

1

Original LTV ratios are calculated as the amount of the mortgage Freddie Mac

guarantees including the credit-enhanced portion, divided by the lesser of the appraised value of

the property at the time of mortgage origination or the mortgage borrower’s

purchase price. Second liens not owned or guaranteed by Freddie Mac are excluded from the LTV

ratio

calculation

because

we

generally

do

not

receive

data

about

them.

The

existence

of

a

second

lien

mortgage

reduces

the

borrower’s

equity

in

the

home

and, therefore, can

increase the risk of default.

2

Credit score data are based on FICO scores at the time of origination and may not

be indicative of the borrowers’ creditworthiness at December 31,

2012. FICO scores can range between approximately 300 to 850

points. 3

HARP

is

the

portion

of

the

company’s

relief

refinance

initiative

targeted

at

borrowers

with

current

LTV

ratios

above

80%.

HARP

was

expanded

in

October

2011

to

allow

eligible

borrowers

who

have

mortgages

with

current

LTV

ratios

above

125%

to

refinance

under

the

program. |

26

Single-family 4Q 2012 credit losses and REO

by region and state

1

Based on the unpaid principal balance (UPB) of the single-family credit

guarantee portfolio at December 31, 2012. 2

UPB amounts exclude Other Guarantee Transactions with ending balances of $553 million since these securities are backed by non-Freddie Mac issued securities for which loan

characteristic data was not available.

3

Based on the number of loans that are three monthly payments or more past due or in

the process of foreclosure. 4

Based

on

the

UPB

of

loans

at

the

time

of

REO

acquisition.

5

Consist of the aggregate amount of charge-offs, net of recoveries, and REO

operations expense for 4Q 2012. 6

Region designation: West (AK, AZ, CA, GU, HI, ID, MT, NV, OR, UT, WA); Northeast

(CT, DE, DC, MA, ME, MD, NH, NJ, NY, PA, RI, VT, VA, WV); Southeast (AL, FL, GA, KY, MS,

NC, PR, SC, TN, VI); North Central (IL, IN, IA, MI, MN, ND, OH, SD, WI); and

Southwest (AR, CO, KS, LA, MO, NE, NM, OK, TX, WY). ($ Billions)

% of Total

UPB

2

($ Millions)

% of Total

Serious

Delinquency

Rate

3

(%)

4Q 2012

Acquisitions

($ Millions)

REO

Inventory

($ Millions)

% of Total

Inventory

($ Millions)

% of Total

Region

6

1

West

$456

28%

$14,961

24%

2.79%

$667

$1,402

19%

$958

40%

2

Northeast

420

25

18,926

30

3.77%

283

944

12

219

9

3

North Central

293

18

8,402

14

2.52%

766

2,839

37

521

22

4

Southeast

277

17

16,703

27

4.97%

786

1,693

22

610

25

5

Southwest

192

12

3,270

5

1.69%

293

755

10

88

4

6

Total

$1,638

100%

$62,262

100%

3.25%

$2,795

$7,633

100%

$2,396

100%

State

7

California

$264

16%

$7,325

12%

2.34%

$340

$725

10%

$572

24%

8

Florida

95

6

11,968

19

9.87%

385

785

10

433

18

9

Illinois

83

5

4,095

7

4.08%

254

1,005

13

237

10

10

Ohio

46

3

1,244

2

2.73%

118

335

4

76

3

11

Michigan

47

3

916

1

1.88%

150

683

9

97

4

12

Arizona

40

2

1,170

2

2.45%

129

216

3

154

7

13

Nevada

17

1

1,782

3

8.14%

29

57

1

126

5

14

All other

1,046

64

33,762

54

2.77%

1,390

3,827

50

701

29

15

Total

$1,638

100%

$62,262

100%

3.25%

$2,795

$7,633

100%

$2,396

100%

Total Portfolio UPB

1

Credit Losses

5

REO Acquisitions & Balance

4

Seriously Delinquent Loans |

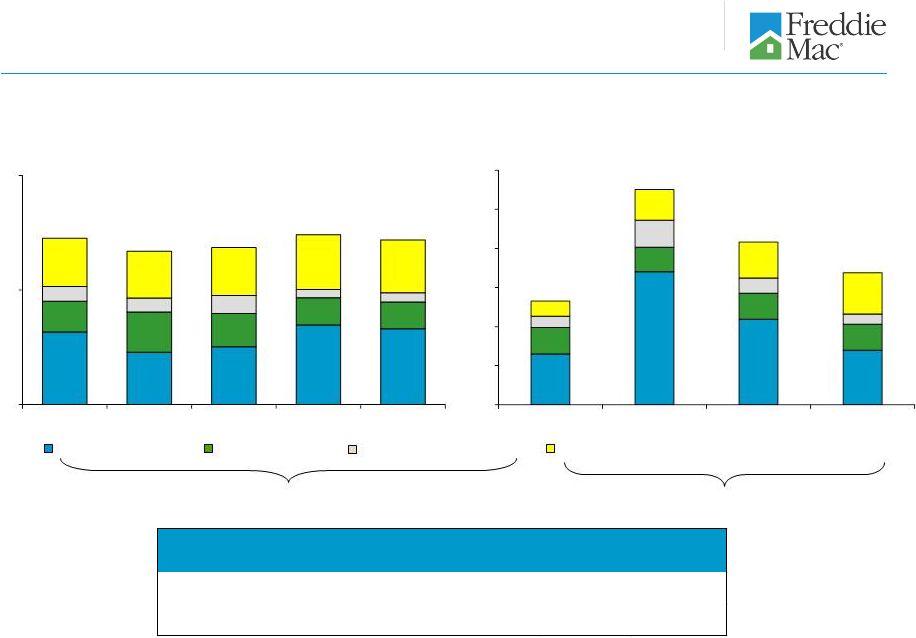

27

Single-family

credit

guarantee

portfolio

characteristics

1

1

Portfolio characteristics are based on the unpaid principal balance (UPB) of the

single-family credit guarantee portfolio. Approximately $1 billion in UPB for Other Guarantee Transactions is

included

in

total

UPB

and

percentage

seriously

delinquent

but

not

included

in

the

calculation

of

other

statistics

since

these

securities

are

backed

by

non-Freddie

Mac

issued

securities

for which

loan characteristic data was not available.

2

For

a

description

of

Alt-A,

see

the

“Glossary”

in

the

company’s

Annual

Report

on

Form

10-K

for

the

year

ended

December

31,

2012.

3

Beginning September 1, 2010, the company fully discontinued purchases of

interest-only loans. 4

Represents

the

FICO

score

of

the

borrower

at

loan

origination.

The

company

estimates

that

less

than

1%

of

loans

within

the

portfolio

are

missing

origination

FICO

scores

and

as

such

are

excluded.

5

Indicates year of loan origination. Calculated based on the loans remaining in the

portfolio as of December 31, 2012, rather than all loans originally guaranteed by the company and originated

in the respective year. Each Book Year category represents the percentage of

loans referenced in line 1 of the same vertical column. 6

Based on the number of loans that are three monthly payments or more past due or in

the process of foreclosure. Note: Individual categories are not mutually

exclusive, and therefore are not additive across columns. Option

FICO

FICO

Original

LTV

FICO < 620 &

Original

Attribute

Alt-A²

Interest-only

3

ARM

< 620

4

620 - 659

4

> 90%

LTV > 90%

4

1

UPB $ Billions

$1,638

$74

$50

$7

$51

$104

$219

$12

2

Percent of Total Portfolio

100%

5%

3%

0%

3%

6%

13%

1%

3

Average UPB per loan

$150,749

$154,561

$233,540

$205,933

$125,942

$132,676

$164,443

$131,181

4

Fixed Rate (% of total portfolio)

93%

64%

23%

0%

94%

93%

98%

97%

5

Owner Occupied

90%

82%

82%

76%

95%

94%

93%

97%

6

Original Loan-to-Value (OLTV)

74%

73%

74%

71%

80%

79%

105%

103%

7

OLTV > 90%

13%

4%

3%

2%

24%

21%

100%

100%

8

Current Loan-to-Value (CLTV)

75%

100%

110%

105%

89%

87%

104%

107%

9

CLTV > 90%

24%

59%

73%

64%

46%

42%

78%

76%

10

CLTV > 100%

15%

47%

60%

52%

33%

30%

47%

56%

11

CLTV > 110%

10%

37%

46%

40%

23%

21%

30%

38%

12

Average FICO Score

4

737

714

718

711

586

642

722

584

13

FICO < 620

4

3%

5%

3%

4%

100%

0%

6%

100%

Book Year

5

14

2012

22%

0%

0%

0%

9%

9%

36%

22%

15

2011

14%

0%

0%

0%

5%

6%

14%

8%

16

2010

15%

0%

1%

0%

5%

6%

14%

7%

17

2009

12%

0%

1%

0%

4%

5%

7%

4%

18

2008

6%

7%

10%

0%

7%

7%

4%

4%

19

2007

7%

30%

37%

2%

22%

18%

9%

22%

20

2006

5%

27%

28%

11%

12%

12%

3%

7%

21

2005

6%

20%

19%

58%

11%

12%

3%

5%

22

2004 and prior

13%

16%

4%

29%

25%

25%

10%

21%

23

% of Loans with Credit Enhancement

13%

13%

10%

16%

25%

22%

52%

65%

24

% Seriously Delinquent

6

3.25%

11.37%

16.27%

16.31%

12.21%

8.99%

4.83%

12.71%

Total Portfolio

as of

December 31, 2012 |

28

Single-family credit profile by book year and product

feature

1

1

Portfolio characteristics are based on the unpaid principal balance (UPB) of the

single-family credit guarantee portfolio. Approximately $1 billion in UPB for Other Guarantee Transactions

is

included

in

total

UPB

and

percentage

seriously

delinquent

but

not

included

in

the

calculation

of

other

statistics

since

these

securities

are

backed

by

non-Freddie

Mac

issued

securities

for which loan characteristic data was not available.

2

Indicates year of loan origination. Calculated based on the loans remaining in the

portfolio as of December 31, 2012, rather than all loans originally guaranteed by the company and

originated in the respective year.

3

Represents

the

average

of

the

borrowers’

FICO

scores

at

origination.

The

company

estimates

that

less

than

1%

of

loans

within

the

portfolio

are

missing

FICO

scores

and

as

such

are

excluded.

4

Beginning September 1, 2010, the company fully discontinued purchases of

interest-only loans. 5

States presented are those with the highest percentage of credit losses during the

three months ended December 31, 2012. 6

Attribute

2012

2011

2010

2009

2008

2007

2006

2005

2004 and

prior

1

UPB $ Billions

$1,638

$364

$226

$237

$205

$79

$119

$89

$101

$218

2

Original Loan-to-Value (OLTV)

74%

78%

72%

72%

70%

74%

77%

75%

73%

72%

3

OLTV > 90%

13%

22%

14%

12%

8%

10%

16%

9%

7%

10%

4

Current Loan-to-Value (CLTV)

75%

76%

67%

68%

69%

88%

107%

104%

89%

56%

5

CLTV > 100%

15%

13%

4%

4%

4%

28%

55%

50%

32%

6%

6

CLTV > 110%

10%

9%

2%

1%

1%

16%

42%

38%

22%

3%

7

Average FICO Score

3

737

755

753

751

750

719

700

705

712

715

8

FICO < 620

3

3%

1%

1%

1%

1%

5%

9%

7%

6%

6%

9

Adjustable-rate

7%

4%

7%

4%

1%

7%

11%

17%

19%

10%

10

Interest-only

4

3%

0%

0%

0%

0%

7%

16%

16%

10%

1%

11

Investor

5%

5%

5%

4%

3%

8%

7%

6%

5%

5%

12

Condo

8%

6%

6%

6%

7%

11%

12%

12%

11%

8%

Geography

5

13

California

16%

21%

17%

16%

13%

16%

16%

15%

15%

12%

14

Florida

6%

4%

3%

3%

4%

7%

11%

12%

11%

8%

15

Illinois

5%

5%

5%

5%

5%

5%

5%

5%

5%

5%

16

Michigan

3%

3%

2%

2%

2%

2%

2%

3%

3%

5%

17

Ohio

3%

3%

3%

3%

2%

2%

2%

2%

3%

4%

18

Arizona

2%

3%

2%

2%

2%

3%

3%

4%

4%

2%

19

Nevada

1%

1%

1%

1%

1%

2%

2%

2%

2%

1%

20

All other

64%

60%

67%

68%

71%

63%

59%

57%

57%

63%

21

% of Loans with Credit Enhancement

13%

13%

10%

8%

8%

26%

26%

15%

13%

12%

22

% Seriously Delinquent

6

3.25%

0.05%

0.26%

0.53%

0.88%

6.80%

12.37%

11.37%

7.20%

3.20%

Total Portfolio

as of

December 31, 2012

Book Year

2

Based on the number of loans that are three monthly payments or more past due or in the process of

foreclosure. |

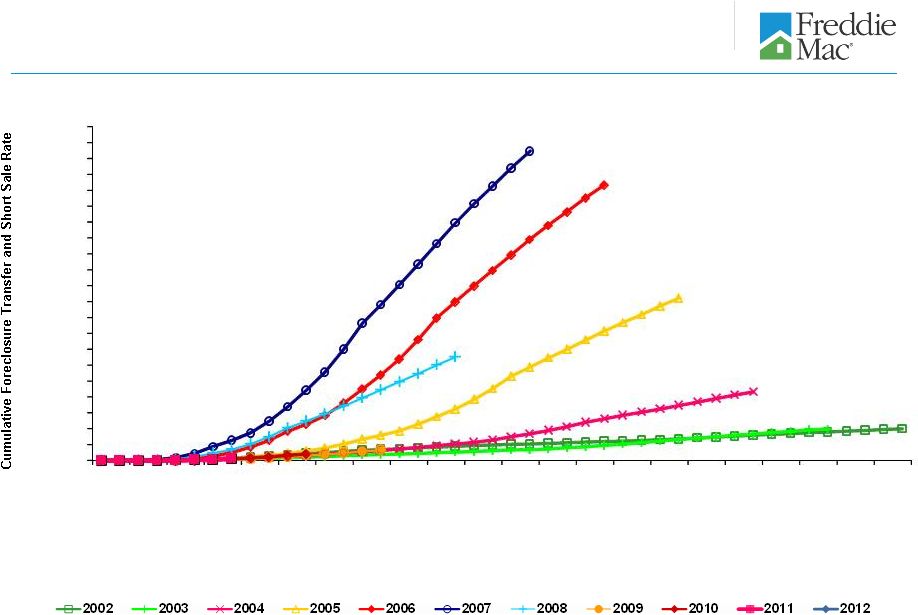

Single-family cumulative foreclosure transfer and

short sale rates

1

by book year

1

Rates are calculated for each year of origination as the number of loans that have

proceeded to foreclosure transfer or short sale and resulted in a credit loss, excluding any

subsequent

recoveries,

divided

by

the

number

of

loans

originated

in

that

year

that

were

acquired

in

the

company’s

single-family

credit

guarantee

portfolio.

Includes

Other

Guarantee

Transactions where loan characteristic data is available.

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.50%

6.50%

7.00%

7.50%

8.00%

8.50%

9.00%

9.50%

10.00%

10.50%

5.00%

6.00%

Yr1

Yr1

Yr2

Yr2

Yr3

Yr3

Yr4

Yr4

Yr5

Yr5

Yr6

Yr6

Yr7

Yr7

Yr8

Yr8

Yr9

Yr9

Yr10

Yr10

Yr11

Yr11

Q1

Q3

Q1

Q3

Q1

Q3

Q1

Q3

Q1

Q3

Q1

Q3

Q1

Q3

Q1

Q3

Q1

Q3

Q1

Q3

Q1

Q3

2007

2006

2005

2004

2002

2003

2008

2009

2010

2011

Quarter Post Origination

2012

29 |

30

Total Multifamily (MF) Portfolio

Multifamily portfolio composition

0

20

40

60

80

100

120

140

160

180

200

12/31/2007

12/31/2008

12/31/2009

12/31/2010

12/31/2011

12/31/2012

MF loan portfolio

MF investment securities portfolio

MF guarantee portfolio

UPB

$ Billions

$135

$154

$164

$169

$177

$180 |

Multifamily

2012

New

Business

Volume

by

State

1

(%)

31

1

Based on the unpaid principal balance (UPB) of the multifamily loan purchases and

issuance of other guarantee commitments. MF New Business Volume $28.8B

> 5%

> 3% -

5%

< 1%

> 1% -

3%

AK

0.0%

AR

0.2%

AZ

2.1%

CO

4.0%

HI

0.2%

IA

0.2%

ID

0.1%

IL

1.8%

IN

0.4%

KS

0.9%

LA

0.5%

MI

0.8%

MN

1.5%

MO

1.4%

MT

0.0%

ND

0.1%

NE

0.4%

NM

0.4%

NV

1.5%

OK

0.5%

OR

0.7%

SD

0.0%

UT

0.5%

VT

0.0%

WA

3.9%

WI

0.7%

WY

0.0%

AL

0.7%

CT

0.4%

DC

0.3%

DE

0.3%

FL

8.9%

GA

3.8%

KY

0.4%

MD

9.1%

ME

0.0%

MS

0.3%

NC

3.1%

NJ

1.5%

NY

7.4%

OH

1.9%

PA

1.8%

RI

0.1%

SC

1.1%

TN

1.8%

TX

13.9%

VA

4.4%

WV

0.2%

NH

0.0%

MA 2.6%

CA

13.2% |

Multifamily Mortgage Portfolio UPB Concentration by

State

1

CA

16.5%

32

1 Percentage based on the unpaid principal balance (UPB) of

unsecuritized mortgage loans, other guarantee commitments, and collateral underlying both Freddie Mac guaranteed

mortgage-related securities and related unguaranteed K Certificates.

2 Consists of the UPB of unsecuritized multifamily loans, other

guarantee commitments, and guaranteed Freddie Mac mortgage-related securities. Excludes the UPB associated with

unguaranteed K Certificates.

MF Mortgage Portfolio $127.4B

2

As of December 31, 2012

> 5%

> 2% -

5%

< 1%

> 1% -

2%

AL

0.9%

AK

0.0%

AR

0.3%

AZ

2.2%

CA

16.5%

CO

3.0%

CT

0.9%

DC

0.9%

DE

0.2%

FL

6.6%

GA

4.7%

HI

0.2%

IA

0.3%

ID

0.1%

IL

2.5%

IN

0.6%

KS

0.9%

KY

0.5%

LA

0.8%

MA 2.1%

MD

5.4%

ME

<0.1%

MI

1.0%

MN

1.3%

MO

1.2%

MS

0.4%

MT

<0.1%

NC

2.8%

ND

0.1%

NE

0.5%

NJ

2.5%

NM

0.3%

NV

1.3%

NY

8.4%

OH

1.9%

OK

0.5%

OR

0.7%

PA

2.4%

RI

0.2%

SC

1.0%

SD

0.1%

TN

1.5%

TX

12.5%

UT

0.5%

VA

5.2%

VT

0.0%

WA

3.3%

WI

0.6%

WV

0.1%

WY

<0.1%

NH

0.1% |

33

Multifamily

mortgage

portfolio

by

attribute

1

1

Based

on

the

unpaid

principal

balance

(UPB)

of

the

multifamily

mortgage

portfolio.

2

Based

on

the

UPB

of

mortgages

two

monthly

payments

or

more

past

due

or

in

the

process

of

foreclosure.

3

Based on either: (a) the year of acquisition, for loans recorded on the

company’s consolidated balance sheets; or (b) the year that the company issued its guarantee, for the

4

Presents

the

six

states

with

the

highest

UPB

at

December

31,

2012.

Year of Acquisition or Guarantee

3

1

2004 and prior

$12.4

0.40%

$10.4

0.26%

$9.2

0.35%

2

2005

7.2

0.20

6.7

0.56

6.5

0.17

3

2006

10.8

0.25

10.1

0.27

9.5

-

4

2007

19.8

0.74

19.3

0.96

17.8

0.86

5

2008

20.6

0.09

18.0

0.34

16.6

0.30

6

2009

13.8

-

12.8

-

12.2

-

7

2010

12.7

-

12.2

-

12.0

-

8

2011

18.8

-

17.4

-

17.0

-

9

2012

N/A

N/A

18.3

-

26.6

-

Total

$116.1

0.22%

$125.2

0.27%

$127.4

0.19%

Maturity Dates

10

2012

$3.0

1.35%

$1.6

1.57%

N/A

N/A

11

2013

5.6

-

3.5

-

$3.3

0.90%

12

2014

7.6

0.03

6.9

0.69

5.8

-

13

2015

11.0

0.17

10.3

0.19

9.8

0.53

14

2016

13.5

0.06

13.6

0.01

13.0

0.05

15

Beyond 2016

75.4

0.25

89.3

0.28

95.5

0.17

Total

$116.1

0.22%

$125.2

0.27%

$127.4

0.19%

Geography

4

16

California

$20.2

0.02%

$21.3

0.24%

$21.1

0.12%

17

Texas

14.0

0.46

15.5

0.46

15.9

0.13

18

New York

9.6

-

10.2

0.09

10.7

0.09

19

Florida

7.1

0.05

8.2

0.04

8.4

0.12

20

Maryland

5.7

-

6.5

-

6.9

-

21

Virginia

6.3

-

6.5

-

6.6

-

22

All other states

53.2

0.35

57.0

0.36

57.8

0.32

Total

$116.1

0.22%

$125.2

0.27%

$127.4

0.19%

UPB

($ Billions)

December 31, 2012

UPB

($ Billions)

Delinquency

Rate

2

(%)

September 30, 2012

Delinquency

Rate

2

(%)

December 31, 2011

Delinquency

Rate

2

(%)

UPB

($ Billions)

remaining loans in its multifamily mortgage portfolio.

|

34

Multifamily

mortgage

portfolio

by

attribute,

continued

1

1

Based on the

unpaid principal balance (UPB) of the multifamily mortgage portfolio.

2

Based on the UPB of mortgages two monthly payments or more past due or in the

process of foreclosure. 3

Current Loan Size

1

> $25M

$42.8

0.06%

$46.3

0.12%

$48.5

0.06%

2

> $5M & <= $25M

64.0

0.31

69.6

0.36

70.0

0.26

3

> $3M & <= $5M

5.7

0.35

5.9

0.35

5.7

0.22

4

> $750K & <= $3M

3.3

0.26

3.2

0.40

3.0

0.65

5

<= $750K

0.3

0.13

0.2

0.62

0.2

0.37

6

Total

$116.1

0.22%

$125.2

0.27%

$127.4

0.19%

Legal Structure

7

Unsecuritized Loans

$82.3

0.10%

$80.3

0.16%

$76.6

0.08%

8

Freddie Mac mortgage-related securities

24.2

0.64

35.4

0.49

41.4

0.41

9

Other guarantee commitments

9.6

0.18

9.5

0.40

9.4

0.13

10

Total

$116.1

0.22%

$125.2

0.27%

$127.4

0.19%

Credit Enhancement

11

Credit Enhanced

$31.6

0.52%

$42.7

0.45%

$47.8

0.36%

12

Non-Credit Enhanced

84.5

0.11

82.5

0.18

79.6

0.10

13

Total

$116.1

0.22%

$125.2

0.27%

$127.4

0.19%

Other

14

Original LTV > 80%

$6.4

2.34%

$6.2

2.75%

$5.8

2.31%

15

Original DSCR below 1.10

$2.8

2.58%

$2.7

3.18%

$2.3

2.97%

December 31, 2012

UPB

($ Billions)

Delinquency

Rate

2

(%)

September 30, 2012

Delinquency

Rate

2

(%)

December 31, 2011

Delinquency

Rate

2

(%)

UPB

($ Billions)

UPB

($ Billions)

DSCR –

Debt Service Coverage Ratio –

is an indicator of future credit performance for multifamily loans. DSCR estimates

a multifamily borrower’s ability to service its mortgage obligation

using the secured property’s cash flow, after deducting non-mortgage expenses from income. The higher the DSCR, the more likely a multifamily borrower will be able to

continue servicing its mortgage obligation.

3 |

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

3Q 2008

1Q 2009

3Q 2009

1Q 2010

3Q 2010

1Q 2011

3Q 2011

1Q 2012

3Q 2012

Freddie Mac (60+ day)

FDIC Insured Institutions (90+ day)

MF CMBS Market (60+ day)

ACLI Investment Bulletin (60+ day)

0.02%

Multifamily market and Freddie Mac delinquency rates

Percent

35

9.65%

1.84%

0.27%

1

See “MD&A – RISK MANAGEMENT – Credit Risk – Mortgage Credit Risk

– Multifamily Mortgage Credit Risk ” in Freddie Mac’s Form 10-K for the year ended December 31,

2012, for information about the company’s reported multifamily delinquency rate. The

multifamily delinquency rate at December 31, 2012 was 0.19%.

Source: Freddie Mac, FDIC Quarterly Banking Profile, TREPP (CMBS multifamily 60+

delinquency rate, excluding REOs), American Council of Life Insurers (ACLI).

Non-Freddie Mac data is not yet available for the fourth quarter of 2012.

1 |

36

Safe Harbor Statements

Freddie Mac obligations

Freddie Mac’s securities are obligations of Freddie Mac only. The securities,

including any interest or return of discount on the securities, are not

guaranteed by and are not debts or obligations of the United States or any federal agency or instrumentality other than Freddie

Mac.

No offer or solicitation of securities

This

presentation

includes

information

related

to,

or

referenced

in

the

offering

documentation

for,

certain

Freddie

Mac

securities,

including offering circulars and related supplements and agreements. Freddie Mac

securities may not be eligible for offer or sale in certain

jurisdictions

or

to

certain

persons.

This

information

is

provided

for

your

general

information

only,

is

current

only

as

of

its

specified

date and does not constitute an offer to sell or a solicitation of an offer to buy

securities. The information does not constitute a sufficient basis

for

making

a

decision

with

respect

to

the

purchase

or

sale

of

any

security.

All

information

regarding

or

relating

to

Freddie

Mac

securities

is

qualified

in

its

entirety

by

the

relevant

offering

circular

and

any

related

supplements.

Investors

should

review

the

relevant

offering circular and any related supplements before making a decision with respect

to the purchase or sale of any security. In addition, before purchasing any

security, please consult your legal and financial advisors for information about and analysis of the security, its

risks and its suitability as an investment in your particular circumstances.

Forward-looking statements

Freddie Mac's presentations may contain forward-looking statements, which may

include statements pertaining to the conservatorship, the company’s

current expectations and objectives for its efforts under the MHA Program, the servicing alignment initiative and other

programs to assist the U.S. residential mortgage market, future business plans,

liquidity, capital management, economic and market conditions and trends,

market share, the effect of legislative and regulatory developments, implementation of new accounting guidance,

credit

losses,

internal

control

remediation

efforts,

and

results

of

operations

and

financial

condition

on

a

GAAP,

Segment

Earnings

and

fair value basis. Forward-looking statements involve known and unknown

risks and uncertainties, some of which are beyond the company’s

control. Management’s expectations for the company’s future necessarily involve a number of assumptions, judgments and

estimates, and various factors, including changes in market conditions, liquidity,

mortgage-to-debt option-adjusted spread, credit outlook, actions

by FHFA, Treasury, the Federal Reserve, the SEC, HUD, other federal agencies, the Administration and Congress, and the

impacts of legislation or regulations and new or amended accounting guidance, could

cause actual results to differ materially from these expectations.

These assumptions, judgments, estimates and factors are discussed in the company’s Annual Report on Form 10-K for

the year ended December 31, 2012, which is available on the Investor Relations page

of the company’s Web site at www.FreddieMac.com/investors

and

the

SEC’s

Web

site

at

www.sec.gov.

The

company

undertakes

no

obligation

to

update

forward-

looking statements it makes to reflect events or circumstances after the date of

this presentation. |