Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - PROVIDENT FINANCIAL SERVICES INC | d492705d8k.htm |

1

Exhibit 99.1 |

Certain statements

contained herein are "forward-looking statements" within the meaning of Section 27A of the Securities

Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward-looking

statements may be identified by reference to a future period or periods, or by the use of

forward-looking terminology, such as "may," "will," "believe,"

"expect,"

"estimate,"

"anticipate,"

"continue,"

or

similar

terms

or

variations

on

those

terms,

or

the

negative

of

those

terms. Forward-looking statements are subject to numerous risks and uncertainties,

including, but not limited to, those related to the economic environment, particularly in

the market areas in which Provident Financial Services, Inc. (the “Company”)

operates, competitive products and pricing, fiscal and monetary policies of the U.S. Government, changes in

government regulations affecting financial institutions, including regulatory fees and capital

requirements, changes in prevailing interest rates, acquisitions and the integration of

acquired businesses, credit risk management, asset-liability management, the

financial and securities markets and the availability of and costs associated with sources of liquidity.

The Company cautions readers not to place undue reliance on any such forward-looking

statements, which speak only as of the

date

made.

The

Company

also

advises

readers

that

the

factors

listed

above

could

affect

the

Company's

financial

performance and could cause the Company's actual results for future periods to differ materially

from any opinions or statements expressed with respect to future periods in any current

statements. The Company does not undertake and specifically declines any obligation to

publicly release the result of any revisions which may be made to any forward- looking

statements to reflect events or circumstances after the date of such statements or to reflect the occurrence of

anticipated or unanticipated events.

A detailed discussion of factors that could affect our results is included in our SEC filings,

including the “Risk Factors” section of our Annual Report on Form 10-K for

the year ended December 31, 2011 and our Quarterly Report on Form 10-Q filed November

9, 2012. 2

Forward Looking Statements

|

Superior

Markets Consistent Performance

Valuable Deposit Franchise

Proven Asset Generator

Capable Risk Manager

Shareholder Focused

3

Why PFS? |

New

Jersey’s oldest state chartered bank Over 75 branch offices

Wealth Management and Trust Administration Services

Well capitalized under current regulatory standards

Ten year history of quarterly cash dividends to stockholders

No TARP

No dilutive stock offerings

No bulk NPA sales or debt restructurings

4

Company Highlights |

5

Total Return |

6

Dividend History |

7

To date, requests for relief limited to 13 loans

totaling $4.9 million

Effective disaster contingency plan minimized

customer disruption

“At risk”

loans in designated flood zones in

Monmouth, Ocean, and Hudson counties represent

< 4% of the total loan portfolio

Strong sponsors, prudent underwriting, federal

flood insurance, private coverage, and business

interruption insurance are expected to minimize

loss exposure

Costs related to storm damage totaled $624,000 in

Q4 2012

Superstorm Sandy |

8

2012: A Record Setting Year

2012

Change vs. 2011

Total Assets

$7.3 B

$186 M

2.6%

Loans

$4.9 B

$251 M

5.4%

NIB

$864 M

$166 M

24.0%

Deposits

$5.4 B

$272 M

5.3% |

2012

Change vs. 2011

Net Int Inc

$217 M

$1 M

0.6%

Non Int Inc

$44 M

$11 M

34.0%

Net Revenue

$261 M

$12 M

5.0%

9

2012: A Record Setting Year

|

2012

Change vs. 2011

Net Income

$67 M

$10 M

5.3%

EPS

$1.18

$0.17

16.8%

ROAA

0.94%

0.11%

13.3%

ROAE

6.88%

0.79%

13.0%

ROATE

10.88%

1.07%

10.9%

10

2012: A Record Setting Year

|

11

4 Q 2011

1 Q 2012

2 Q 2012

3 Q 2012

4 Q 2012

1.91%

1.89%

1.81%

1.65%

1.53%

$135,351

$134,783

$129,141

$119,586

$111,463

NPAs

NPAs/Assets

Asset Quality 5 Quarter Trend

|

12

Asset Quality 5 Quarter Trend |

Q4 2012

Q3 2012

Q4 2011

ALL/Loans

1.43%

1.46%

1.60%

ALL/NPLs

71.07%

66.50%

60.67%

ALL/Ann. NCOs

4.50 yrs

3.14 yrs

3.53 yrs

13

ALL Coverage

|

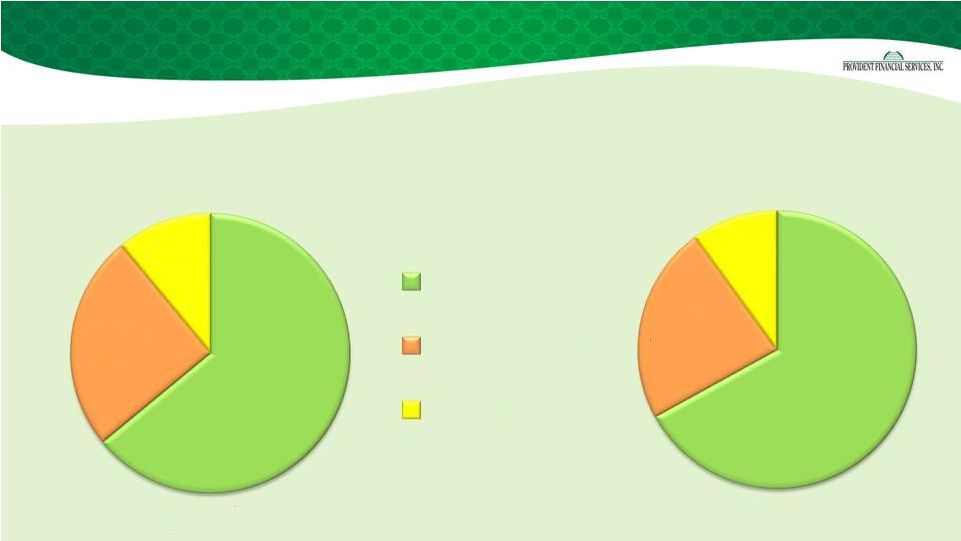

Asset

Composition $6.8 B

$7.3 B

64%

25%

11%

2009

67%

23%

10%

2012

Loans

Investments

Other

A Longer View: Structural Gains

14 |

Loan

Composition 15

A Longer View: Structural Gains

Commercial

$2.3B

53%

Consumer

$2.1B

47%

2009

Commercial

$3.1B

62%

Consumer

$1.8B

38%

2012 |

Direct vs.

Indirect Lending 16

A Longer View: Structural Gains

84.0%

11.0%

2.2%

1.8%

1.0%

2009

89.7%

8.4%

0.6%

0.8%

0.5%

2012

Direct

Purchased Residential

SNCs

Indirect Marine

Indirect Auto / Other |

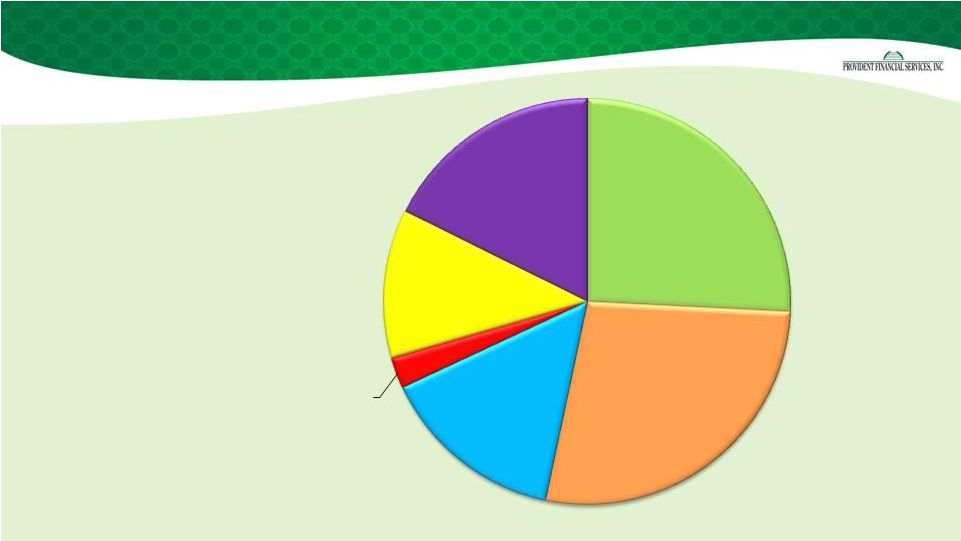

Total Loans:

$4.9 Billion Average Loan Yield: 4.58%

17

Loan Portfolio – 12/31/12

1-4 Res.

26%

CRE

27%

Multi-

family

15%

Constr.

2%

Consumer

12%

C&I

18% |

18

Two years average increase between 2010-2012

10.63%

Average

Increase

18.33%

Average

Increase

31.71%

Average

Increase

40.36%

Average

Increase

17.17%

Average

Increase

52.51%

Average

Increase

Loan Originations Trend |

19

Commercial Real Estate – 12/31/12

Multi-Family

35%

Retail

23%

Office

14%

Industrial

13%

Mixed Used

5%

Special Use

Property

4%

Hotel

3%

Land

1%

Residential

1%

Other

1% |

20

WAL AFS:

3.6 yrs

HTM:

4.3 yrs

Combined:

3.8 yrs

Municipal

Bonds

22%

Corporate

Notes -

Fixed

0%

Agency Notes -

Fixed

6%

Agency MBS -

Fixed

33%

Agency MBS -

ARMs

6%

Agency CMO -

Fixed

30%

Corporate

CMO -

Fixed

3%

Investment Portfolio – 12/31/12

|

Funding /

Earning Assets 21

A Longer View: Structural Gains

25%

16%

47%

8%

2009

Time Deposits

Borrowings

IB Core Deposits

NIB Deposits

15%

12%

55%

13%

2012 |

Non-Interest

Income/ Net Revenue: 2009 = $31.5M, 14.8%

2012 = $43.6M, 16.7%

22

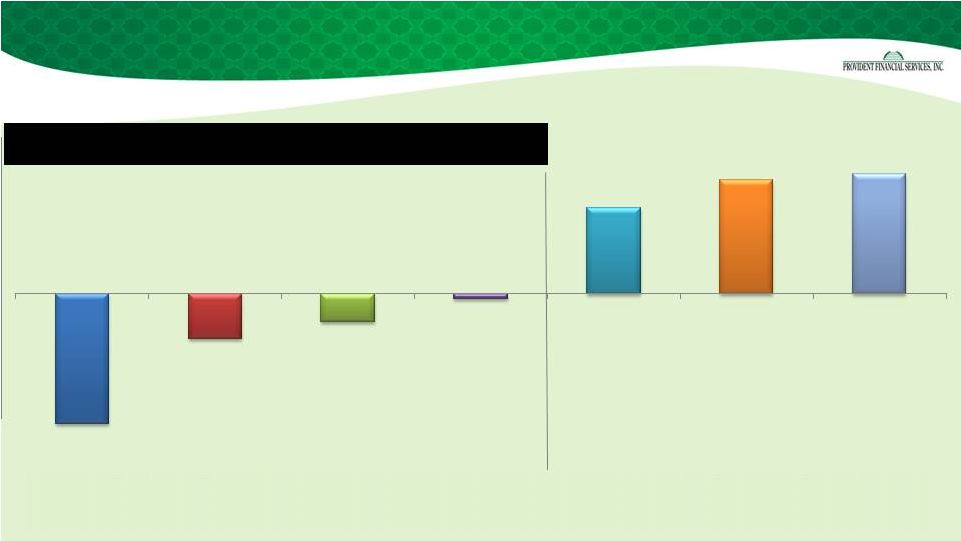

A Longer View: Structural Gains

-2.3%

-0.8%

-0.5%

-0.1%

1.5%

2.0%

2.1%

Deposit fees

($3.2M)

Equity fund income

($1.7M)

BOLI

($0.1M)

Other

$2.0M

Loan fees

$4.0M

Securities gains

$5.1M

Wealth fees &

Annuity Sales

$6.1M |

Capacity

Utilization 23

*Excludes impact of $152.5 million of Goodwill

impairment in 2009.

A Longer View: Structural Gains

2012

2009

Change

Revenue

$260,950

$212,469

$48,481

Eff.

Eff.

Non-Interest Expense*

Compensation & benefits

80,874

30.99%

68,735

32.35%

-1.36%

Net occupancy expense

20,487

7.85%

20,170

9.49%

-1.64%

Data processing expense

10,318

3.95%

9,325

4.39%

-0.43%

FDIC Insurance

5,095

1.95%

11,778

5.54%

-3.59%

Advertising & promo expense

4,139

1.59%

4,291

2.02%

-0.43%

Amortization of intangibles

2,466

0.95%

5,111

2.41%

-1.46%

Other operating expenses

25,449

9.75%

25,121

11.82%

-2.07%

148,828

57.03%

144,534

68.03%

-10.99%

|

24

*Excludes impact of $152.5 million of Goodwill impairment in 2009.

A Longer View: Structural Gains

2012

2009 NIM

3.38%

3.06%

Loans/Deposits

90.4%

89.5%

Net Revenues

$261M

$212M

Provision

$16M

$30M

Net Income*

$67M

$31M

|

25

Capital Ratios – 12/31/12

Provident

Consolidated

Bank

PFS

TCE

-

9.00%

Tier 1 Leverage

7.80%

8.93%

Tier 1 RBC

11.08%

12.68%

Total RBC

12.33%

13.93%

|

26

Capital flexibility

Recent additions to lending teams in Middle Market /

Consumer / Healthcare / CRE

Technology enhancements

Sandy stimulus

Accelerating economic recovery

Opportunities |

27

|