Attached files

| file | filename |

|---|---|

| EX-99.1 - EX-99.1 - Mondelez International, Inc. | d488866dex991.htm |

| 8-K - FORM 8-K - Mondelez International, Inc. | d488866d8k.htm |

Exhibit 99.2

Mondelez International

CAGNY Conference

February 19, 2013 |

Forward-looking statements

2

This slide presentation contains a number of forward-looking statements. The words

“deliver,” “accelerating,” “leverage,” “drive,”

“expand,” “create,” “expect,” “opportunity,” “achievable,” and “increase”

and similar expressions are intended to identify our forward-looking statements. Examples of

our forward-looking statements include, but are not limited to, sustainable profitable

growth; H2 2013 growth; long runway for growth; Power Brands; innovation platforms; Hot Zone

penetration; Traditional Trade coverage; Next Wave markets; long-term growth target; Free

Cash Flow; use of capital; balance sheet; and ROIC. These forward-looking statements

involve risks and uncertainties, many of which are beyond our control, and important factors

that could cause actual results to differ materially from those in the forward-looking

statements include, but are not limited to, increased competition, pricing actions, continued

volatility in commodity costs, continued weak economic conditions, risks from operating

globally and tax law changes. For additional information on these and other factors that could

affect our forward-looking statements, see our risk factors, as they may be amended from

time to time, set forth in our filings with the SEC, including our most recently filed Annual

Report on Form 10-K and subsequent reports on Forms 10-Q and 8-K. We disclaim

and do not undertake any obligation to update or revise any forward-looking statement in

this slide presentation, except as required by applicable law or regulation. |

Irene

Rosenfeld Chairman & CEO |

Ingredients in place for sustainable,

profitable growth

4

Advantaged

Geographic

Footprint

Fast-

Growing

Categories

Favorite

Snacks

Brands

Strong

Routes-to-

Market

Proven

Innovation

Platforms

World-Class

Talent &

Capabilities |

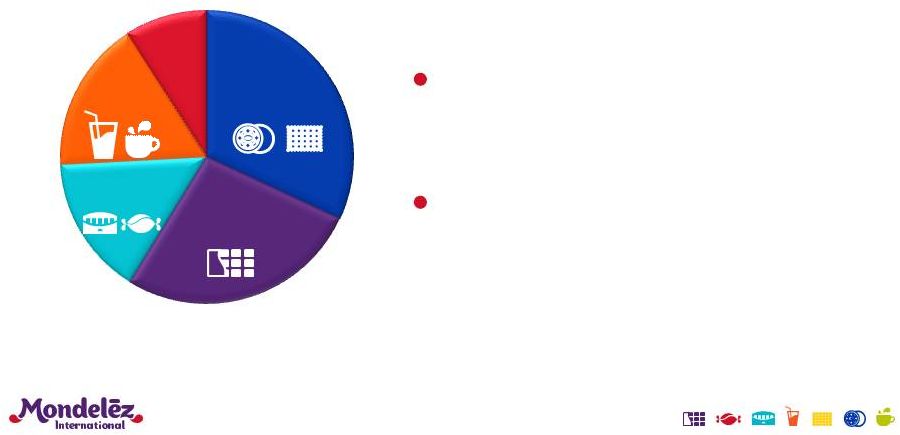

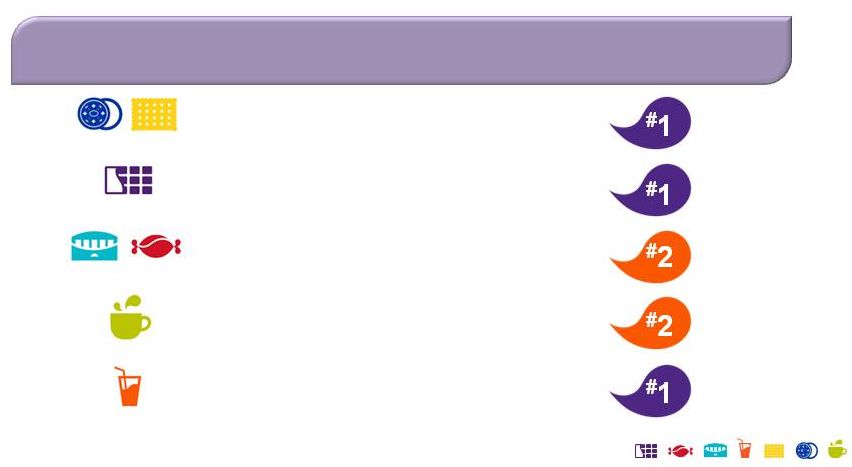

We are

a global snacks powerhouse… 5

$35 Billion

in 2012 Revenues

(1)

Biscuits includes salted/other snacks

Nearly 75% of revenues

in fast-growing snacks

categories

Beverages provide multi-

region scale, attractive growth

and strong margins

Biscuits

(1)

32%

Chocolate

27%

Gum & Candy

15%

Beverages

17%

Cheese &

Grocery

9% |

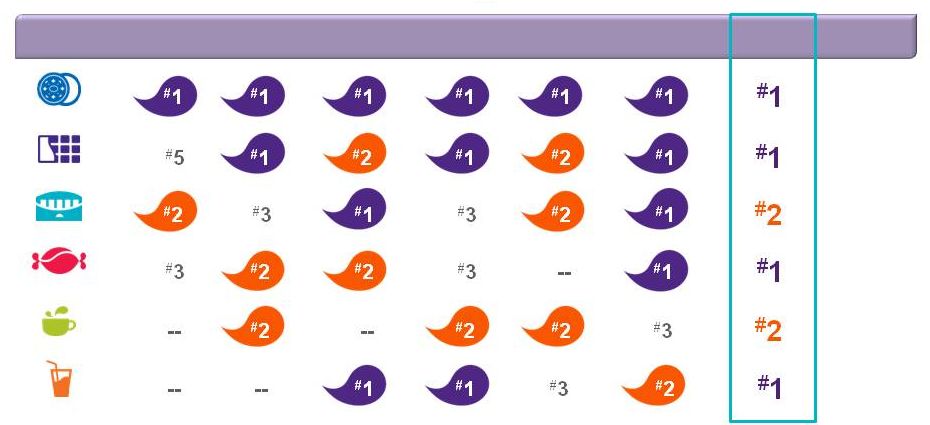

18%

…

and a leader in our categories

6

North

North

America

America

Europe

Europe

Global

Global

Market

Market

Share

Share

Latin

Latin

America

America

Asia

Asia

Pacific

Pacific

Eastern

Eastern

Europe

Europe

Middle East

Middle East

& Africa

& Africa

15%

30%

7%

11%

16%

Source: Euromonitor market share

Biscuits

Chocolate

Gum

Candy

Coffee

Powdered Beverages |

We

offer many of the world’s favorite brands |

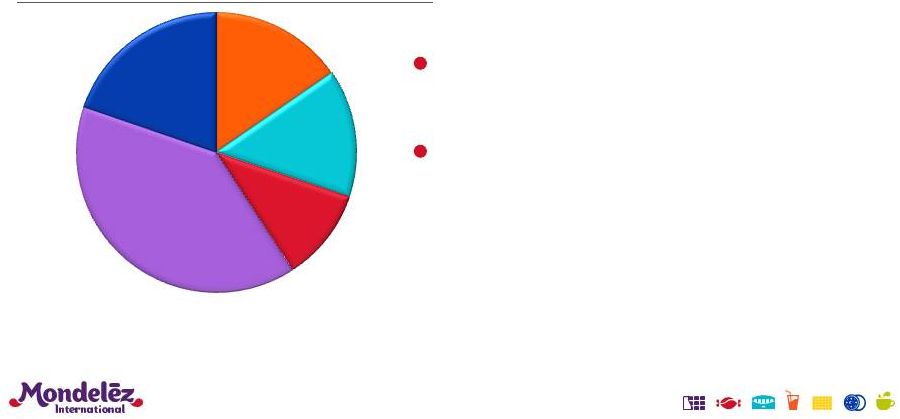

Advantaged geographic footprint

Large, growing developing

markets footprint

Strong positions in North

America and Europe

$35 Billion

in 2012 Revenues

8

Europe

39%

North

America

20%

Latin

America

15%

EEMEA

11%

Asia Pacific

15%

Based on 2013 Reporting Segments

*

*

In December 2012, we announced a reorganization of our management and reporting

structure following the Spin-Off of Kraft Foods Group. Beginning in

2013, our operations, management and operating segments will reflect: Asia Pacific;

Eastern Europe, Middle East & Africa (“EEMEA”); Europe; Latin America

and North America. Accordingly, we will begin reporting on our new

segment structure during the first quarter of 2013, including all historical periods we present. For

purposes of this presentation the above pie chart reflects this structure based on

our 2012 Net Revenues. |

Track

record of strong performance 9

O/H % of NR

(60) bps

Reinvest in

Growth

Power Brands +8%

Organic NR +4.4%

(1)

+50 bps

(2)

A&C % of NR

+60 bps

Focus on

Power Brands

Expand Gross

Margin

Leverage

Overheads

Note: All figures based on FY 2012 results.

1)

Reported net revenues decreased (2.2)% for FY 2012. See GAAP

to Non-GAAP reconciliation at the end of the presentation. 2)

Reflects Adjusted Gross Margin. Reported gross profit margin

increased 70 bps. See GAAP to Non-GAAP reconciliation at the

end of the presentation.

|

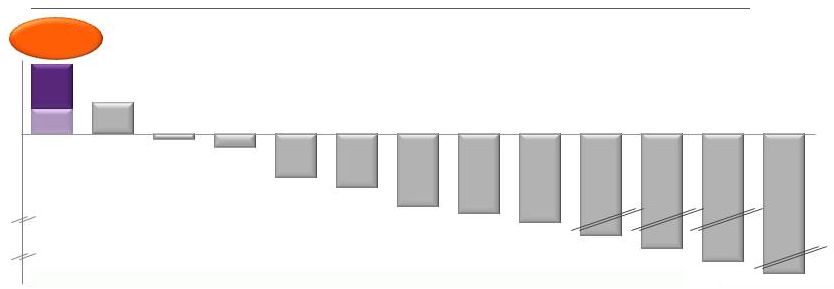

Led

the peer group in margin performance over the past two years

Basis

Points

Increase

in

Operating

Income

Margin

2010

to

2012

(1)

(3)

+110 bps

100

(100)

(400)

(2)

(200)

MDLZ

HSY

ULVR

NESN

HNZ

CL

BN

PG

CPB

GIS

PEP

K

KO

+70

+40

1)

Operating Income Margins exclude certain items as defined by the individual companies as sourced from

their respective company reports.

2)

Reflects Adjusted Operating Income Margin which excludes Integration Program costs, 2012-2014

Restructuring Program costs, Spin-Off Costs, Spin-Off-related pension adjustment,

operating income from divestitures and gains & losses from divestitures, net. Reported Operating Income Margin was 7.9% in FY 2010; 9.8% in 2011; and 10.4%

in FY 2012. See GAAP to Non-GAAP reconciliation at the end of this presentation. 3)

Through 1H 2012.

|

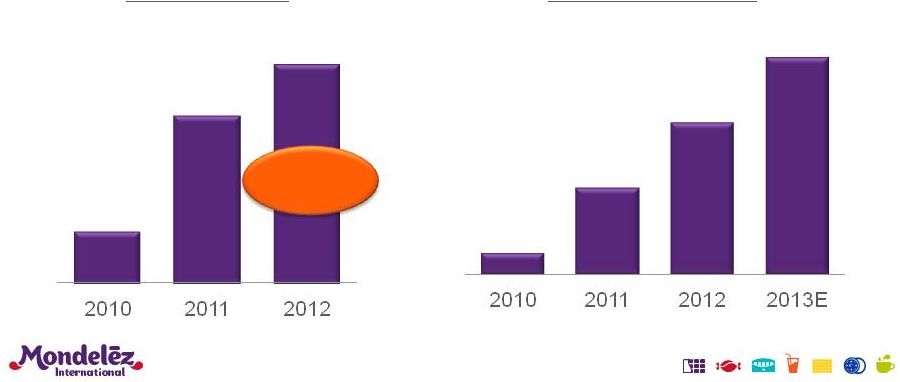

Successfully integrated Cadbury

11

($ in billions)

~$0.8

~$0.6

~$0.2

Cost Synergies

(Cumulative P&L Impact)

Revenue Synergies

~$0.1

~$0.4

~$0.7

~$1.0

~105% of

$750MM

Target |

Growth

accelerating in H2 2013 H2 2012

Growth tempered by:

Lower coffee pricing

Capacity constraints

Missteps in Brazil,

Russia and Canada

H1 2013

Lower coffee pricing

and capacity constraints

continue

Improvement in Brazil,

Russia and Canada

H2 2013

Cycle lower coffee

pricing

New capacity on-stream

12

FY 2013

Organic Revenue

growth at

low end of

5%-7% range |

Leverage fast-growing categories

Drive Power Brands and advantaged global

innovation platforms

Expand distribution

Capitalize on numerous white space opportunities

We have a long runway for growth

13 |

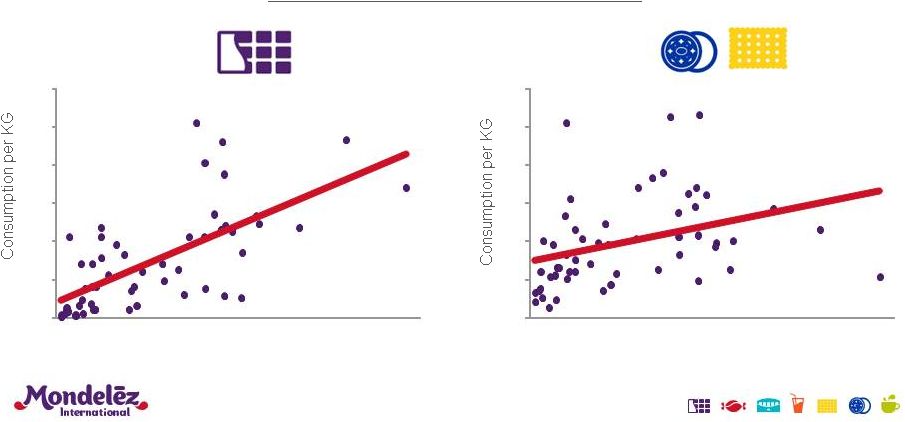

Powdered Beverages

Category growth remains robust…

14

Source: Euromonitor 2009-2011 actual and 2012 estimates

Category

MLDZ

Market Position

Global Category CAGR

(2009-2012)

+6%

+6%

+5%

+10%

+7%

Chocolate

Biscuits

Gum & Candy

Coffee |

…

driven by income growth in developing markets

15

GDP per Capita

GDP per Capita

Consumption vs. GDP per Capita

Source: Euromonitor 2011

Chocolate

Biscuits

0

2

4

6

8

10

12

$0

$20

$40

$60

$80

$100

0

2

4

6

8

10

12

$0

$20

$40

$60

$80

$100 |

Leverage Power Brands to drive top-tier growth

16

Capitalize on

Strengths in

Existing Markets

Seize White Space

Opportunities

Drive growth in Europe

Expanding into other developing

markets in 2013

$1B in revenues in developing markets,

up 20% in 2012

Leverage successful U.S. experience,

up 6% in 2012 |

Roll-out innovation platforms globally

17

2012

2013

Launch

Early 2012

UK

Ireland

Germany

France

Sweden

Norway

Belgium

Austria

Brazil

Argentina

Russia

S. Africa

Canada

Poland |

Increase Hot Zone penetration in Modern Trade

18

Hot

Zone

Presence

in

MDLZ Covered Outlets

2013E

Increase

’13E vs. ’11

% Outlets

Covered ’13E

1,800

+300

59%

6,200

+3,100

62%

56,700

+34,400

52% |

Significant opportunity to expand Traditional

Trade coverage

19

274,000

+18,000

32%

1,000,000

+298,000

14%

450,000

+348,000

20%

MDLZ Coverage of

Traditional Trade Outlets

2013E

Increase

’13E vs. ’11

% Outlets

Covered ’13E |

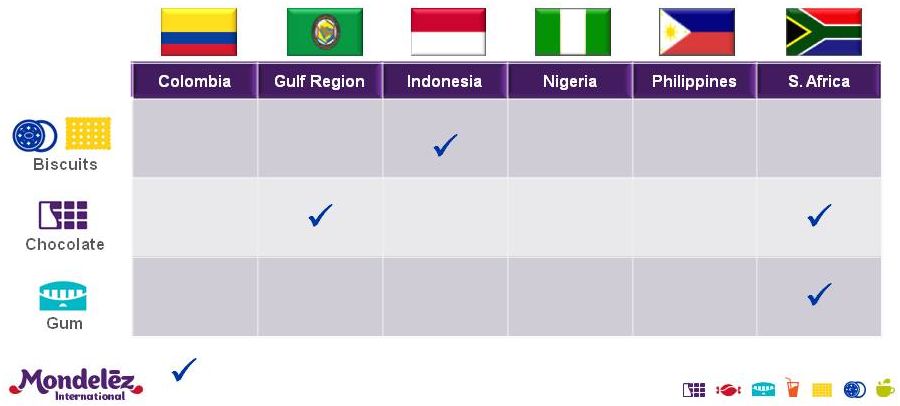

Initiated white space launches in India and China

20

Significant current market presence |

Significant white space opportunities in Next

Wave markets

21

Significant current market presence |

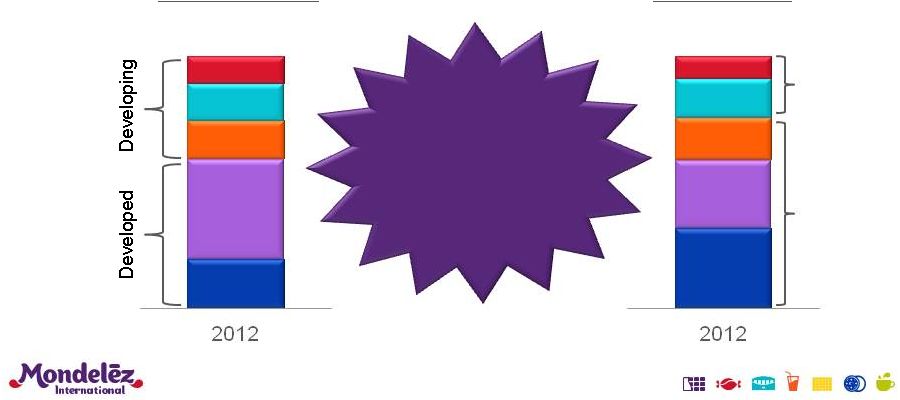

Long-term growth target is achievable

22

Double Digit

Growth

Low-to-Mid

Single Digit

Growth

$35B

EU

NA

LA

AP

EEMEA

By Geography

$35B

Low-to-Mid

Single Digit

Growth

Mid-to-High

Single Digit

Growth

Chocolate

Biscuits

Gum &

Candy

Beverages

Ch./Groc.

By Category

5% -

7%

Organic Growth |

Well-positioned for sustainable, profitable growth

23

Advantaged geographic footprint

Portfolio of iconic brands

Virtuous cycle in full swing

Long runway of future growth opportunities |

Dave

Brearton EVP and CFO |

Generating cash to fund growth and drive

solid returns

25

Delivering solid Free Cash Flow

Prioritizing uses of Free Cash Flow

Focusing on Return on Invested Capital |

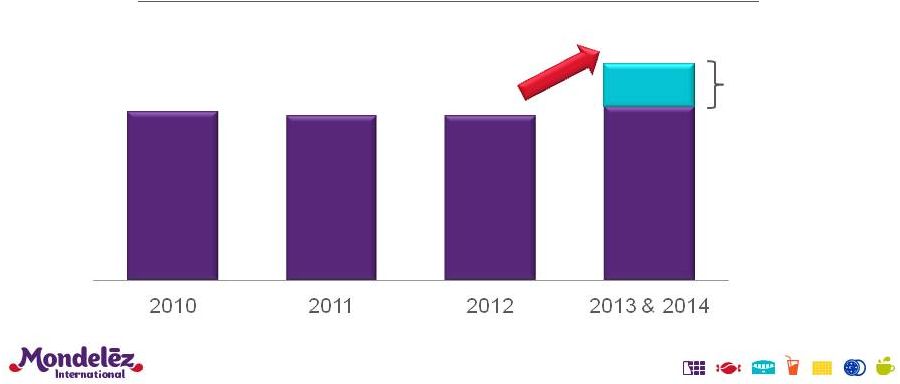

Expect

strong Free Cash Flow generation over next 2 years

26

Combined

2013 and 2014

Cash from Operating Activities

~ $8.0

Capital Expenditure

(excl. Restructuring Program)

~ 4.0

Free Cash Flow, Pre-Restructuring

~ 4.0

2012-2014 Restructuring Program,

cash impact

~ 1.0

Dividends @ $0.52 per share

~ 2.0

Cash Available for Deployment

~ $1.0 |

Priorities for use of Free Cash Flow

Disciplined Capital Deployment

27

Reinvest in the business to drive top-tier growth

Tack-on M&A, especially in Developing Markets

Return

of

capital

to

shareholders

–

dividends

and

share repurchases

Pay down debt to preserve balance sheet flexibility

2

1

3

4 |

Stepping-up capital investments to support growth

28

Capital

Expenditures

as

Percentage

of

Net

Revenue

5%+

3.9%

3.8%

3.8%

Long-Term

Rate

4%

-

5% |

Expanding capacity in developing markets

New Plants

Plant Expansions

Multi-Category

Multi-Category

Multi-Category

Multi-Category

Multi-Category

Biscuits

Gum

Biscuits

Gum

Biscuits

Biscuits

Chocolate

Chocolate

Chocolate

29 |

Returning capital to shareholders

30

Dividends

Modest dividend

increasing over time

Minimum payout ratio of

30% of net earnings

Share Repurchases

Later this year will seek

multi-year authorization

to offset dilution |

Preserve balance sheet flexibility

31

$19.4

~$17.5

Maintain investment-grade rating

with A2/P2 CP access

Use cash-on-hand to pay off

$1.8B of notes due 1H 2013

Possible further debt pay down to

build additional flexibility

Net Debt

~$15

Dec. 2012

Mid-2013 |

ROIC

improvement will be driven by earnings growth and disciplined capital

deployment 32

ROIC currently at 7%

–

Total invested capital of $47B at December 31, 2012

ROIC to improve 30-50 bps per annum

–

Double-digit EPS growth

–

Tight management of working capital and capex

–

Return of capital to shareholders |

Well-positioned for sustainable, profitable growth

33

Advantaged geographic footprint

Portfolio of iconic brands

Virtuous cycle in full swing

Long runway of future growth opportunities

Generate strong cash flow

•

•

•

•

• |

34 |

GAAP

to Non-GAAP Reconciliation 35

(1)

Includes

the

impacts

of

accounting

calendar

changes

and

the

53

rd

week

of

shipments

in

2011.

As

Restated

(GAAP)

Impact of

Divestitures

Impact of

Integration

Program

Impact of

Accounting

Calendar

Changes

(1)

Impact of

Currency

Organic

(Non-GAAP)

As

Restated

(GAAP)

Organic

(Non-GAAP)

2012

Mondelez International

35,015

$

(244)

$

-

$

-

$

1,576

$

36,347

$

(2.2)%

4.4%

2011

Mondelez International

35,810

$

(316)

$

1

$

(679)

$

-

$

34,816

$

Net Revenues to Organic Net Revenues

For the Twelve Months Ended December 31,

($ in millions, except percentages) (Unaudited)

% Change |

GAAP

to Non-GAAP Reconciliation 36

(1)

Includes

the

impacts

of

accounting

calendar

changes

and

the

53

rd

week

of

shipments

in

2011.

As Restated

(GAAP)

Impact of

Divestitures

Impact of

Integration

Program

Impact of

Accounting

Calendar

Changes

(1)

Impact of

Currency

Organic

(Non-GAAP)

As

Restated

(GAAP)

Organic

(Non-GAAP)

17,194

$

(157)

$

-

$

-

$

841

$

17,878

$

(0.9)%

6.2%

17,353

$

(176)

$

-

$

(349)

$

-

$

16,828

$

Net Revenues to Organic Net Revenues

For the Six Months Ended June 30,

($ in millions, except percentages) (Unaudited)

% Change

2012

2011

Mondelez International

Mondelez International |

GAAP

to Non-GAAP Reconciliation 37

(1)

costs

associated

with

the

acquisition.

For

the

twelve

months

ended

December

31,

2012,

$28

million

was

recorded

in

Cost

of

Sales

and

$112

million

was

recorded in Selling, General and Administrative expenses.

(2)

Spin-Off Costs represent non-recurring transaction and transition costs

associated with preparing the businesses for independent operations consisting primarily

of financial advisory fees, legal fees, accounting fees, tax services and

information systems infrastructure duplication, and financing and related costs to redistribute

to the pension adjustment defined as the estimated benefit plan expense based on

market conditions and benefit plan assumptions as of January 1, 2012,

associated with certain benefit plan obligations transferred to Kraft Foods Group

in the Spin-Off. (3)

Restructuring Program costs represent non-recurring restructuring and related

implementation costs reflecting primarily severance, asset disposals and other

manufacturing related non-recurring costs.

(4)

Reflects divestitures that occured in 2012.

Gross

Profit/Operating

Income

To

Adjusted

Gross

Profit/Operating

Income

For the Twelve Months Ended December 31,

($ in millions, except percentages) (Unaudited)

As

Restated

(GAAP)

Integration

Program

costs

(1)

Acquisition-

Related

costs

Spin-Off Costs

and Related

Adjustments

(2)

2012 - 2014

Restructuring

Program costs

(3)

Operating

Income from

Divested

Businesses

(4)

G/(L) on

Divestitures,

net

Adjusted

(Non-GAAP)

13,076

$

28

$

-

$

33

$

2

$

(71)

$

-

$

13,068

$

37.3%

37.6%

3,637

$

140

$

1

$

512

$

110

$

(58)

$

(107)

$

4,235

$

10.4%

12.2%

2012

Gross Profit

Gross Profit Margin

Operating Income

Operating Income Margin

Mondelez International

Integration

Program

costs

are

defined

as

the

costs

associated

with

combining

the

Mondelez

International

and

Cadbury

businesses,

and are separate from those

debt

and

secure

investment

grade

ratings

for

both

the

Kraft

Foods

Group

Business

and

the Mondelez

International

Business.

Spin-Off

related

adjustments refers |

GAAP

to Non-GAAP Reconciliation 38

As Restated

(GAAP)

Integration

Program

costs

(1)

Spin-Off Costs

and Related

Adjustments

(2)

Operating

Income from

Divested

Businesses

(3)

Adjusted

(Non-GAAP)

Mondelez International

Gross Profit

13,100

$

110

$

43

$

(83)

$

13,170

$

Gross Profit Margin

36.6%

37.1%

Operating Income

3,498

$

521

$

137

$

(59)

$

4,097

$

Operating Income Margin

9.8%

11.5%

(1)

Integration

Program

costs

are

defined

as

the

costs

associated

with

combining

the

Mondelez

International

and

Cadbury

businesses,

and

are separate from those costs associated with the acquisition. For the

twelve months ended December 31, 2011, $1 million was recorded in Revenue,

$109 million was recorded in Cost of Sales and $411 million was recorded in Selling, General and Administrative expenses.

(2)

Spin-Off Costs represent non-recurring transaction and transition costs

associated with preparing the businesses for independent operations

consisting primarily of financial advisory fees, legal fees, accounting fees, tax

services and information systems infrastructure duplication, and

financing

and

related

costs

to

redistribute

debt

and

secure

investment

grade

ratings

for

both

the

Kraft

Foods

Group

Business

and

the

Mondelez

International

Business.

Spin-Off

related

adjustments

refers

to

the

pension

adjustment

defined

as

the

estimated

benefit

plan

expense based on market conditions and benefit plan assumptions as of January 1,

2012, associated with certain benefit plan obligations transferred to Kraft

Foods Group in the Spin-Off. (3)

Reflects divestitures that occured in 2012.

Gross

Profit/Operating

Income

To

Adjusted

Gross

Profit/Operating

Income

For the Twelve Months Ended December 31,

($ in millions, except percentages) (Unaudited)

2011 |

39

GAAP to Non-GAAP Reconciliation

As Restated

(GAAP)

Integration

Program

costs

(1)

Spin-Off Costs

and Related

Adjustments

(2)

Operating

Income from

Divested

Businesses

(3)

Adjusted

(Non-GAAP)

Mondelez International

Gross Profit

11,872

$

49

$

99

$

(109)

$

11,911

$

Gross Profit Margin

37.7%

38.3%

Operating Income

2,496

$

646

$

364

$

(56)

$

3,450

$

Operating Income Margin

7.9%

11.1%

(1)

Integration

Program

costs

are

defined

as

the

costs

associated

with

combining

the

Mondelez

International

and

Cadbury

businesses,

and are separate from those costs associated with the acquisition. For the

twelve months ended December 31, 2010, $1 million was recorded in Revenue,

$48 million was recorded in Cost of Sales and $597 million was recorded in Selling, General and Administrative

expenses.

(2)

Spin-Off Costs represent non-recurring transaction and transition costs

associated with preparing the businesses for independent operations

consisting primarily of financial advisory fees, legal fees, accounting fees, tax

services and information systems infrastructure duplication, and

financing

and

related

costs

to

redistribute

debt

and

secure

investment

grade

ratings

for

both

the

Kraft

Foods

Group

Business

and

the

Mondelez

International

Business.

Spin-Off

related

adjustments

refers

to

the

pension

adjustment

defined

as

the

estimated

benefit

plan expense based on market conditions and benefit plan assumptions as of January

1, 2012, associated with certain benefit plan obligations transferred to

Kraft Foods Group in the Spin-Off. (3)

Reflects divestitures that occured in 2010 and 2012.

Gross

Profit/Operating

Income

To

Adjusted

Gross

Profit/Operating

Income

For the Twelve Months Ended December 31,

($ in millions, except percentages) (Unaudited)

2010 |

As

Reported

Integration

Program

Costs

(1)

Spin-Off

Costs

(2)

2012-2014

Restructuring

Program Costs

(3)

Acquisition-

Related Costs

Spin-Off

Pension

Adjustment

(2)

Spin-Off

Interest

Adjustment

(2)

Operating

Income from

Divested

Businesses

Gain on

Divestitures,

net

As

Adjusted

Net revenues

35,015

$

-

$

-

$

-

$

-

$

-

$

-

$

(244)

$

-

$

34,771

$

Cost of sales

21,939

(28)

-

(2)

-

(33)

-

(173)

-

21,703

Gross profit

13,076

28

-

2

-

(33)

-

(71)

-

13,068

Gross profit margin

37.3%

37.6%

Selling, general and administrative expenses

9,176

(112)

(444)

(7)

(1)

(35)

-

(13)

-

8,564

153

-

-

(101)

-

-

-

-

-

52

(107)

-

-

-

-

-

-

-

107

-

Amortization of intangibles

217

-

-

-

-

-

-

-

-

217

Operating income

3,637

140

444

110

1

68

-

(58)

(107)

4,235

Operating income margin

10.4%

12.2%

1,863

-

(609)

-

-

-

(161)

-

-

1,093

Earnings from continuing operations before income taxes

1,774

140

1,053

110

1

68

161

(58)

(107)

3,142

Provision for income taxes

207

6

347

40

-

26

60

(13)

(48)

625

Effective tax rate

11.7%

19.9%

Earnings from continuing operations

1,567

$

134

$

706

$

70

$

1

$

42

$

101

$

(45)

$

(59)

$

2,517

$

Noncontrolling interest

27

-

-

-

-

-

-

-

-

27

1,540

$

134

$

706

$

70

$

1

$

42

$

101

$

(45)

$

(59)

$

2,490

$

Per share data:

-

Continuing operations

0.86

$

0.08

$

0.39

$

0.04

$

-

$

0.02

$

0.06

$

(0.03)

$

(0.03)

$

1.39

$

Average shares outstanding:

Diluted

1,789

Condensed Consolidated Statements of Earnings

(Gains) / losses on divestitures, net

Interest and other expense, net

Reported to Adjusted

For the Twelve Months Ended December 31, 2012

(in millions of dollars, except per share data) (Unaudited)

Asset impairment and exit costs

40

GAAP to Non-GAAP Reconciliation

Net

earnings

attributable

to

Mondele

z

International

-

Diluted

earnings

per

share

attributable

to

Mondele

z

International:

-

(1)

(2)

Spin-Off Costs represent non-recurring transaction and transition costs

associated with preparing the businesses for independent operations consisting primarily of financial advisory fees, legal fees,

accounting fees, tax services and information systems infrastructure duplication,

and financing and related costs to redistribute debt and secure investment grade ratings for both the Kraft Foods Group

plan

assumptions

as

of

January

1,

2012,

associated

with

certain

benefit

plan

obligations

transferred

to

Kraft

Foods

Group

in

the

Spin-Off.

Integration

Program

costs

are

defined

as

the

costs

associated

with

combining

the

Mondele

z

International

and

Cadbury

businesses,

and

are

separate

from

those

costs

associated

with

the

acquisition.

ez

-

-

Restructuring

Program

costs

represent

non-recurring

restructuring

and

related

implementation

costs

reflecting

primarily

severance,

asset

disposals

and

other

manufacturing

related

non-recurring

costs.

(3)

Business

and

the

Mondel

International

Business.

Spin-Off

related

adjustments

refers

to

the

pension

adjustment

defined

as

the

estimated

benefit

plan

expense

based

on

market

conditions

and

benefit |

Net

earnings

attributable

to

Mondele

z

International

GAAP to Non-GAAP Reconciliation

41

-

As Reported

Integration

Program Costs

(1)

Spin-Off

Costs

(2)

Spin-Off

Pension

Adjustment

(2)

Spin-Off

Interest

Adjustment

(2)

Operating

Income from

Divested

Businesses

As Adjusted

Net revenues

35,810

$

1

$

-

$

-

$

-

$

(316)

$

35,495

$

Cost of sales

22,710

(109)

-

(43)

-

(233)

22,325

Gross profit

13,100

110

-

43

-

(83)

13,170

Gross profit margin

36.6%

37.1%

Selling, general and administrative expenses

9,382

(411)

(46)

(48)

-

(24)

8,853

(5)

-

-

-

-

-

(5)

-

-

-

-

-

-

-

Amortization of intangibles

225

-

-

-

-

-

225

Operating income

3,498

521

46

91

-

(59)

4,097

Operating income margin

9.8%

11.5%

1,618

-

-

-

(310)

-

1,308

Earnings from continuing operations before income taxes

1,880

521

46

91

310

(59)

2,789

Provision for income taxes

143

24

13

34

117

(14)

317

Effective tax rate

7.6%

11.4%

Earnings from continuing operations

1,737

$

497

$

33

$

57

$

193

$

(45)

$

2,472

$

Noncontrolling interest

20

-

-

-

-

-

20

1,717

$

497

$

33

$

57

$

193

$

(45)

$

2,452

$

Per share data:

Diluted

earnings

per

share

attributable

to

Mondele

z

International:

-

Continuing operations

0.97

$

0.28

$

0.02

$

0.03

$

0.11

$

(0.03)

$

1.38

$

Average shares outstanding:

Diluted

1,772

(1)

(2)

Spin-Off Costs represent non-recurring transaction and transition costs

associated with preparing the businesses for independent operations consisting primarily of financial advisory fees, legal fees,

accounting fees, tax services and information systems infrastructure duplication,

and financing and related costs to redistribute debt and secure investment grade ratings for both the Kraft Foods Group

plan

assumptions

as

of

January

1,

2012,

associated

with

certain

benefit

plan

obligations

transferred

to

Kraft

Foods

Group

in

the

Spin-Off.

Condensed Consolidated Statements of Earnings

(Gains) / losses on divestitures, net

Interest and other expense, net

Reported to Adjusted

For the Twelve Months Ended December 31, 2011

(in millions of dollars, except per share data) (Unaudited)

Asset impairment and exit costs

-

Integration

Program

costs

are

defined

as

the

costs

associated

with

combining

the

Mondele

z

International

and

Cadbury

businesses,

and

are

separate

from

those

costs

associated

with

the

acquisition.

Business

and

the

Mondele

z

International

Business.

Spin-Off

related

adjustments

refers

to

the

pension

adjustment

defined

as

the

estimated

benefit

plan

expense

based

on

market

conditions

and

benefit

-

- |